UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

OR

Date of the event requiring this shell company report _________________

Commission file number:

(Exact name of Registrant as specified in its charter) |

Not Applicable |

(Translation of Registrant’s name into English) |

(Jurisdiction of incorporation or organization) |

(Address of principal executive offices) |

Telephone: +1 ( E-mail: |

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Trading symbol(s) | Name of each exchange on which |

*Not for trading, but only in connection with the listing on the NYSE American

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None |

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock as of the close of the period covered by this report.

| par value $0.003 per share, as of December 31, 2022 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

| Accelerated filer ☐ |

| |

|

|

|

| Emerging Growth Company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued |

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes

|

| |

6 | ||

6 | ||

6 | ||

30 | ||

52 | ||

52 | ||

69 | ||

80 | ||

81 | ||

82 | ||

82 | ||

91 | ||

92 | ||

|

| |

|

| |

95 | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 95 | |

95 | ||

96 | ||

96 | ||

96 | ||

96 | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 96 | |

96 | ||

96 | ||

96 | ||

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 96 | |

| ||

| ||

97 | ||

97 | ||

98 |

2

CONVENTIONS THAT APPLY IN THIS ANNUAL REPORT ON FORM 20-F

Except where the context requires otherwise and for purposes of this annual report only:

| ● | “ADSs” refers to our American depositary shares, each of which represents two Class A Ordinary Shares, and “ADRs” refers to the American depositary receipts that evidence our ADSs. |

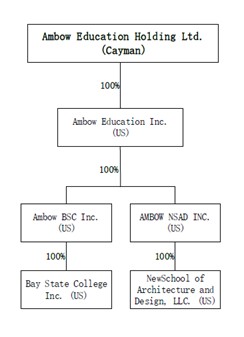

| ● | “Ambow” refers to Ambow Education Holding Ltd., a Cayman Island company; “we”, “us”, “our company”, “the company”, “the Group”, “our” or similar terms refer to Ambow Education Holding Ltd., its consolidated subsidiaries unless the context otherwise indicate. |

| ● | “China” or “PRC” refers to the People’s Republic of China, excluding, for the purpose of this annual report, Hong Kong, Macau and Taiwan. |

| ● | “IPO” refers to the initial public offering of our ADSs. |

| ● | “RMB” or “Renminbi” refers to the legal currency of China. |

| ● | “Sale of Ambow China” refers to the sale of all of the equity interests in Ambow Education Ltd., Ambow Education Management Ltd. and Ambow Education Group Ltd. (collectively, the “Ambow China”) to Clover Wealth Limited (the “Purchaser”) in consideration of the Purchaser paying US$12.0 million to Ambow, as contemplated by and pursuant to the terms and conditions of a share purchase agreement dated November 23, 2022 entered into by and between Ambow and the Purchaser. The Sale of Ambow China was consummated on December 31, 2022. |

| ● | “U.S. GAAP” refers to the Generally Accepted Accounting Principles in the United States. |

| ● | “VIEs” refers to our variable interest entities, which are certain domestic PRC companies in which we do not have direct or controlling equity interests but through contractual arrangements (“VIE Agreements”) whose historical financial results have been consolidated in our financial statements in accordance with U.S. GAAP, including Shanghai Ambow Education Information Consulting Co., Ltd (“Ambow Shanghai”), Ambow Rongye Education and Technology Co., Ltd. (“Ambow Rongye”), Ambow Sihua Intelligent Technology Co., Ltd. (“Ambow Sihua”), Beijing Ambow Zhixin Education and Technology Co., Ltd. (“Ambow Zhixin”), Beijing OOOK Education and Technology Co., Ltd. (“Beijing OOOK”), Beijing Ambow Shida Education Technology Co., Ltd. (“Ambow Shida”), Beijing Le’an Operational Management Co., Ltd. (“Beijing Le’an”), Beijing JFR Education & Technology Co., Ltd. (“Beijing JFR”), Jinan LYZX Business Management Co., Ltd. (“Jinan LYZX”) and subsidiaries and schools they hold respectively, each a PRC company; and IValley Co., Ltd. (“IValley”), a Taiwanese company, and subsidiaries it hold respectively. |

| ● | “$”, “US$” or “U.S. dollars” refers to the legal currency of the United States. |

3

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F includes forward-looking statements that relate to future events or our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to differ materially from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Words such as, but not limited to, “believe”, “expect”, “anticipate”, “estimate”, “intend”, “plan”, “likely”, “will”, “would”, “could”, and similar expressions or phrases identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and future events and financial trends that we believe may affect our financial condition, results of operation, business strategy and financial needs. Forward-looking statements include, but are not limited to, statements about:

| ● | Anticipated trends and challenges in our business and the markets in which we operate; |

| ● | Our ability to anticipate market needs or develop new or enhanced services and products to meet those needs; |

| ● | Our ability to compete in our industry and innovation by our competitors; |

| ● | Our ability to protect our confidential information and intellectual property rights; |

| ● | Risks associated with opening new learning centers and other strategic plans; |

| ● | Our need to obtain additional funding and our ability to obtain funding in the future on acceptable terms; |

| ● | The impact on our business and results of operations arising from the defects in our real properties; |

| ● | Our ability to create and maintain our positive brand awareness and brand loyalty; |

| ● | Our ability to manage growth; |

| ● | Risks associated with school closures and reduced enrollment due to the COVID-19 pandemic. |

All forward-looking statements involve risks, assumptions and uncertainties. You should not rely upon forward-looking statements as predictors of future events. The occurrence of the events described, and the achievement of the expected results, depend on many events, some or all of which are not predictable or within our control. Actual results may differ materially from expected results. See the information under “Item 3.D Key Information—Risk Factors” and elsewhere in this annual report for a more complete discussion of these risks, assumptions and uncertainties and for other risks and uncertainties. These risks, assumptions and uncertainties are not necessarily all of the important factors that could cause actual results to differ materially from those expressed in any of our forward-looking statements. Other unknown or unpredictable factors also could harm our results. We undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise. In light of these risks, uncertainties and assumptions, the forward-looking events discussed in this annual report might not occur.

4

Summary of Risks

An investment in our securities involves a high degree of risk. The occurrence of one or more of the events or circumstances described in the section titled “Risk Factors,” alone or in combination with other events or circumstances, may materially adversely affect our business, financial condition and operating results. In that event, the trading price of our securities could decline, and you could lose all or part of your investment. Such risks include, but are not limited to:

| ● | If we are not able to continue to attract students to enroll in our programs, our net revenues may decline and we may not be able to maintain profitability. |

| ● | We face significant competition in each major program we offer and each geographic market in which we operate, and if we fail to compete effectively, we may lose our market share and our profitability may be adversely affected. |

| ● | NYSE may delist our securities from trading on its exchange, which could limit investors’ ability to make transactions in our securities and subject us to additional trading restrictions. |

| ● | We may not be able to successfully integrate businesses that we acquire, which may cause us to lose anticipated benefits from such acquisitions and to incur significant additional expenses. |

| ● | We face risks related to natural disasters or other extraordinary events and public health epidemics, such as the global coronavirus outbreak experienced, in the locations in which we, our students, faculty, and employees live, work, which could have a material adverse effect on our business and results of operations. |

| ● | If we are not able to continually enhance our online programs, services and products and adapt them to rapid technological changes and student needs, we may lose market share and our business could be adversely affected. |

| ● | Our ADSs or Ordinary Shares may be delisted under the Holding Foreign Companies Accountable Act (“HFCA Act”) if the PCAOB is unable to adequately inspect audit documentation located in China. The delisting of our ADSs or Ordinary Shares, or the threat of their being delisted, may materially and adversely affect the value of your investment. Additionally, the inability of the PCAOB to conduct adequate inspections deprives our investors with the benefits of such inspections. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which was enacted on December 29, 2022 under the Consolidated Appropriations Act 2023, amends the HFCA Act and requires the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. |

| ● | If we fail to comply with the extensive U.S. regulatory requirements related to operating a U.S. higher education institution, we could face significant monetary liabilities, fines and penalties, including loss of access to federal student loans and grants for our students. |

| ● | Our failure to demonstrate financial responsibility or administrative capability may result in the loss of eligibility to participate in Title IV programs. |

| ● | The ongoing regulatory effort aimed at for-profit post-secondary institutions of higher education could lead to additional legislation or other governmental action that may negatively affect the industry. |

| ● | Insiders have substantial control over us, which could adversely affect the market price of our ADSs. |

5

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. | [Reserved] |

B. | Capitalization and Indebtedness |

Not applicable.

C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

D. | Risk Factors |

6

RISKS RELATED TO OUR BUSINESS AND INDUSTRY

If we are not able to continue to attract students to enroll in our programs, our net revenues may decline and we may not be able to maintain profitability.

The success of our business largely depends on the number of students who are enrolled in our programs and the amount of fees that our students are willing to pay for our courses. Therefore, our ability to continue to attract students to enroll in our programs without significantly decreasing course fees is critical to the continued success and growth of our business. This will depend on several factors, including our ability to develop new programs and enhance existing programs to respond to changes in market trends and student demands, expanding our geographic reach, managing our growth while maintaining the consistency of our teaching quality, effectively marketing our programs to a broader base of prospective students, developing and licensing additional high-quality educational content and responding to competitive pressures. It also depends on macroeconomic factors like unemployment and the resulting lower confidence in job prospects, and many of the regulatory risks discussed as below. Our enrollment in future years will be affected by legislative uncertainty, regulatory activity, and macroeconomic conditions. It is likely that legislative, regulatory, and economic uncertainties will continue for the foreseeable future, and thus it is difficult to assess our long-term growth prospects. If we are unable to continue to attract students to enroll in our programs without significantly decreasing course fees, our net revenues may decline and we may not be able to achieve profitability, either of which could result in a material adverse effect on our business, results of operations and financial condition.

If we are not able to continue to attract and retain qualified education professionals, we may not be able to maintain consistent teaching quality throughout our school and our brand, business and results of operations may be materially and adversely affected.

Our education professionals are critical to maintaining the quality of our services, software products and programs, and maintaining our brand and reputation, as they interact with our students on a regular basis. We must continue to attract qualified education professionals who have a strong command of the subject areas to be taught and who meet our qualifications. We may not be able to hire and retain enough qualified education professionals to keep pace with our anticipated growth or at acceptable costs while maintaining consistent teaching quality across many different schools and programs in different geographic locations. Shortages of qualified education professionals, or decreases in the quality of our instruction, whether actual or perceived in one or more of our markets, or an increase in hiring costs, may have a material and adverse effect on our business and our reputation. Further, our inability to retain our education professionals may hurt our existing brands and those brands we are trying to develop, and retaining qualified teachers at additional costs may have a material adverse effect on our business and results of operations.

Our business depends on the strength of our brands in the marketplace. We may not be able to retain existing students or attract new students if we cannot continue to use, protect and enhance our brands successfully in the marketplace.

Our operational and financial performance and the successful growth of our business are highly dependent on market awareness of our “Ambow” brand and the regional brands that we have acquired. We believe that maintaining and enhancing the “Ambow” brand is critical to maintaining and enhancing our competitive advantage and growing our business. In order to retain existing students and attract new students, we plan to continue to make expenditures to create and maintain our positive brand awareness and create brand loyalty. The diverse set of services and products that we offer to college students places significant demands on us to maintain the consistency and quality of our services and products to ensure that our brands do not suffer from any actual or perceived decrease in the quality of our services and products. As we continue to grow in size, expand our services and products and extend our geographical reach, maintaining the quality and consistency of our services and products may be more difficult. Any negative publicity about our services, products, or schools, regardless of its veracity, could harm our brand image and have a material adverse effect on our business and results of operations.

7

We face significant competition in each major program we offer and each geographic market in which we operate, and if we fail to compete effectively, we may lose our market share and our profitability may be adversely affected.

Competition could result in loss of market share and revenues, lower profit margins and limit our future growth.

We face competition from many different companies that focus on one area of our business and are able to devote all of their resources to that business line, and these companies may be able to more quickly adapt to changing technology, student preferences and market conditions in these markets than we can. These companies may, therefore, have a competitive advantage over us with respect to these business areas.

Post-secondary education in the United States is highly competitive. Our U.S. colleges, Bay State College Inc. (“Bay State College”) and NewSchool of Architecture and Design, LLC (“NewSchool”), compete with traditional public and private two-year and four-year colleges, other for-profit schools, and alternatives to higher education. Some of our competitors in both the public and private sectors have substantially greater financial and other resources than we do. These competitors may be able to devote greater resources than we can to the development, promotion and sale of their services and products, and respond more quickly than we can to changes in student needs, testing materials, admissions standards, market needs or new technologies. Some of our competitors, both public and private, may offer programs similar to ours at a lower tuition level as a result of government subsidies, government and foundation grants, tax-deductible contributions, and other financial sources not available to proprietary institutions, or by providing fewer student services or larger class sizes. While we believe that our U.S. colleges provide valuable education to their students, we may not always accurately predict the drivers of a student’s or potential students’ decisions to choose among the range of educational and other options available to them. Our student enrollment may decrease due to intense competition, and we may be required to reduce course fees or increase spending in response to competition in order to retain or attract students or pursue new market opportunities. As a result, our net revenues and profitability may decrease. We cannot assure you that we will be able to compete successfully against current or future competitors. If we are unable to maintain our competitive position or otherwise respond to competitive pressures effectively, we may lose our market share and our profitability may be materially adversely affected.

We may not be able to successfully integrate businesses that we acquire, which may cause us to lose anticipated benefits from such acquisitions and to incur significant additional expenses.

It is challenging to integrate the business operations, infrastructure and management philosophies of acquired schools and companies. The benefits of our past and future acquisitions depend in significant part on our ability to integrate technology, operations and personnel. The integration of acquired schools and companies is a complex, time-consuming and expensive process that, without proper planning and implementation, could significantly disrupt our business and operations. The main challenges involved in integrating acquired entities include the following:

| ● | Ensuring and demonstrating to our students that the acquisitions will not result in adverse changes in service standards or business focus; |

| ● | Consolidating and rationalizing corporate IT and administrative infrastructures; |

| ● | Retaining qualified education professionals for our acquired entities; |

| ● | Consolidating service and product offerings; |

| ● | Coordinating and rationalizing research and development activities to enhance the introduction of new products and technologies with reduced costs; |

| ● | Preserving strategic, marketing or other important relationships of the acquired entity and resolving potential conflicts that may arise with our key relationships; and |

| ● | Minimizing the diversion of senior management attention from day-to-day operations. |

8

We may not successfully integrate our operations and the operations of entities we acquire in a timely manner, or at all, and we may not realize the anticipated benefits or synergies of the acquisitions to the extent or in the timeframe anticipated, which would have a material adverse effect on our results of operations.

Our results of operations may fluctuate, which makes our financial results difficult to forecast, and could cause our results to fall short of expectations.

Our results of operations may fluctuate as a result of a number of factors, many of which are outside of our control. Our net revenues from continuing operations decreased from RMB 120.2 million in 2020 to RMB 113.5 million in 2021, and further decreased to RMB 102.4 million (US$ 14.8 million) in 2022. Comparing our results of operations on a period-to-period basis may not be meaningful, and you should not rely on our past results as an indication of our future performance. Our quarterly and annual net revenues and costs and expenses as a percentage of net revenues may be significantly different from our historical or projected rates. Our quarterly and annual net revenues and gross margins may fluctuate due to a number of factors, including:

| ● | The increase of costs associated with our strategic expansion plans; |

| ● | The revenue and gross margin profiles of our acquisitions in a given period; |

| ● | Our ability to successfully integrate our acquisitions and the timing of our post-integration activities; |

| ● | Our ability to reduce our costs as a percentage of our net revenues; |

| ● | Increased competition; and |

| ● | Our ability to manage our financial resources, including administration of bank loans and bank accounts. |

As a result of these and other factors, we may not sustain our past growth rates in future periods, and we may not sustain profitability on a quarterly or annual basis in the future.

We face risks related to natural disasters or other extraordinary events and public health epidemics, such as the global coronavirus outbreak experienced, in the locations in which we, our students, faculty, and employees live and work, which could have a material adverse effect on our business and results of operations.

Our business could be severely disrupted and materially adversely affected by natural disasters, inclement weather, or the outbreak of health epidemics in the locations in which we, our students, faculty, and employees live, work, and attend classes. From the beginning of 2020, the global spread of a novel coronavirus pandemic, also known as COVID-19, had a significant effect on our business. The pandemic continues to be fluid and uncertain, making it difficult to forecast the final impact it could have on our future operations. The COVID-19 pandemic may adversely affect our business operations and operating results for future years, including but not limited to negative impact on the Group’s revenues, delayed or impaired collection of tuition and fees, etc. Any future natural disasters or health epidemics could also severely disrupt our business operations and have a material adverse effect on our business and results of operations.

9

Our business depends on the continuing efforts of our senior management team and other key personnel and our business may be harmed if we lose their services.

Our future success depends heavily upon the continuing services of the members of our senior management team and, in particular, upon our retaining the services of our founder, Chairman, Chief Executive Officer and acting Chief Financial Officer, Dr. Jin Huang. If one or more of our senior executives or other key personnel are unable or unwilling to continue in their present positions, we may not be able to replace them easily or at all, and as a result our business may be disrupted and our financial condition and results of operations may be materially and adversely affected. In addition, if any member of our senior management team or any of our other key personnel joins a competitor or forms a competing company, we may lose teachers, students, key professionals and staff members. Competition for experienced management personnel in the private education sector is intense, the pool of qualified candidates is very limited, and we may not be able to retain the services of our senior executives or key personnel, or attract and retain high-quality senior executives or key personnel in the future, which could have a material adverse effect on our business and results of operations.

If we are not able to continually enhance our online programs, services and products and adapt them to rapid technological changes and student needs, we may lose market share and our business could be adversely affected.

Our online programs, services and products are vital to the success of our business. The market for such programs, services and products is characterized by rapid technological changes and innovation, as well as unpredictable product life cycles and user preferences. We must quickly modify our online programs, services and products to adapt to changing student needs and preferences, technological advances and evolving Internet practices. Ongoing enhancement of our online offerings and related technologies may entail significant expense and technical risk. We may use new technologies ineffectively or fail to adapt our online services or products and related technologies on a timely and cost-effective basis. If our improvements to our online offerings and the related technology are delayed, if they result in systems interruptions or are not aligned with market expectations or preferences, we may lose market share and our business could be materially adversely affected.

Failure to adequately and promptly respond to industry changes in curriculum, testing materials and standards could cause our services and products to be less attractive to our students.

Our success depends in part on our ability to continually update and expand the content, curriculum and test preparation materials of our academic programs, develop new programs and our teaching methods in a cost-effective manner, and meet students’ needs in a timely manner. Any inability to track and respond to industry changes in a timely and cost-effective manner would make our services and products less attractive to students, which may materially and adversely affect our reputation and ability to continue to attract students without a significant decrease in course fees.

If we are unable to obtain new loans, at all or on terms that are acceptable to us, our growth pace will be impacted.

We may seek to obtain additional bank loans in the future. We cannot assure you that we will be able to obtain new loans or credit facilities, at all or on terms that are acceptable to us. Our ability to obtain financing may be affected by our financial position and leverage, our credit rating and investor perception of the education industry, as well as by prevailing economic conditions and the cost of financing in general. In addition, factors beyond our control, such as recent global market and economic conditions and the tightening of credit markets may result in a diminished availability of financing and increased volatility in credit and equity markets, which may materially adversely affect our ability to secure financing at reasonable costs or at all. If we were unable to obtain financing in the future on terms acceptable to us, our business operations and our growth plans would be materially harmed.

10

Our business is subject to seasonal fluctuations, which may cause our operating results to fluctuate from quarter to quarter.

We have experienced, and expect to continue to experience, seasonal fluctuations in our revenues and results of operations, primarily due to seasonal changes in service days and student enrollment. Historically, the number of days on which our students attend our courses is lower in the first and third quarters due to school closures for the celebration of the winter break and summer break. Because our colleges recognize revenues based on the number of service days in the quarters, we expect our revenues in the first and third quarters would be lower than the second and fourth quarters. Our costs and expenses, however, do not necessarily correspond with changes in our student enrollment, service days or net revenues. We make investments in marketing and promotion, teacher recruitment and training, and product development throughout the year. We expect quarterly fluctuations in our revenues and results of operations to continue. As the revenues grow in colleges, these seasonal fluctuations may become more pronounced.

We may not be able to adequately protect our intellectual property, which could cause us to be less competitive.

Our brand, copyrights, patents, trade secrets, trade names and other intellectual property rights are important to our success. Unauthorized use of any of our intellectual property may adversely affect our business and reputation. We rely on a combination of copyright, trademark and trade secrets laws and confidentiality agreements with our employees, consultants and others, including our partner schools, to protect our intellectual property rights. Nevertheless, it may be possible for third parties to obtain and use our intellectual property without authorization. Moreover, litigation may be necessary in the future to enforce our intellectual property rights. Future litigation could result in substantial costs and diversion of our management’s attention and resources and could disrupt our business. If we are unable to enforce our intellectual property rights, it could have a material adverse effect on our financial condition and results of operations. Failure to adequately protect our intellectual property could materially adversely affect our competitive position, our ability to attract students and our results of operations.

We may be exposed to infringement and misappropriation claims by third parties, which, if successful, could cause us to pay significant damage awards.

Third parties may initiate litigation against us alleging infringement upon their intellectual property rights.

In the event of a future successful claim of infringement or misappropriation and our failure or inability to develop non-infringing technology or license the infringed or misappropriated or similar technology on a timely basis, our business could be harmed. In addition, even if we are able to license the infringed or misappropriated or similar technology, license fees could be substantial and may adversely affect our results of operations.

Unexpected network interruptions, security breaches or computer virus attacks and system failures could have a material adverse effect on our business, financial condition and results of operations.

Any failure to maintain satisfactory performance, reliability, security or availability of our network infrastructure may cause significant damage to our reputation and our ability to attract and maintain students. Major risks involving our network structure include:

| ● | Breakdowns or system failures resulting in a prolonged shutdown of our servers, including failures attributable to power shutdowns, or attempts to gain unauthorized access to our systems, which may cause loss or corruption of data, including customer data, or malfunctions of software or hardware; |

| ● | Disruption or failure in the national backbone network, which would make it impossible for visitors and students to log on to our websites; |

| ● | Damage from fire, flood, power loss and telecommunications failures; and |

| ● | Any infection by or spread of computer viruses. |

11

Any network interruption or inadequacy that causes interruptions in the availability of our websites or deterioration in the quality of access to our websites could reduce customer satisfaction and result in a reduction in the number of students using our services. If sustained or repeated, these performance issues could reduce the attractiveness of our online and offline programs. In addition, we may be subject to a security breach caused by a computer hacker, which could involve attempts to gain unauthorized access to our systems or personal information stored in our systems, or to cause intentional malfunctions or loss or corruption of data, software, hardware or another computer equipment. A user who circumvents our security measures could misappropriate proprietary information or cause interruptions or malfunctions in our operations. As a result, we may be required to expend significant resources to protect against the threat of these security breaches or to alleviate problems caused by these breaches.

Furthermore, increases in the volume of traffic on our websites could also strain the capacity of our existing computer systems, which could lead to slower response times or system failures. This would cause a disruption or suspension in our online course programs, which would hurt our brand and reputation, and thus negatively affect our net revenue growth. We may need to incur additional costs to upgrade our computer systems in order to accommodate increased demand if we anticipate that our systems cannot handle higher volumes of traffic in the future; or to protect against system errors, failures or disruptions, or to repair or otherwise mitigate problems.

Our legal right to lease certain properties could be challenged by property owners or other third parties, which may cause interruptions to business operations of the affected schools, tutoring centers, training offices and career enhancement centers and adversely affect our financial results.

We lease the premises used for the operation of our college campuses. As a result, we are dependent on the property rights of these properties held by their owners to enable us to use the premises. We cannot assure you that all lessors of our leased business premises have the relevant land use right certificates or building ownership certificates of the premises they lease to us or otherwise have the right to lease the premises to us.

We are not aware of any actions, claims or investigations being contemplated by the relevant governmental entities with respect to the defects in our leased real properties. However, if we are unable to use the existing properties, enter new leases or renew our current leases in a timely basis and on terms favorable to us, our business, results of operations and financial condition could be materially adversely affected. No impairment loss was made against the operating lease right-of-use assets in 2021 and 2022 from the continuing operations.

We may need to record a significant charge to earnings if our goodwill or intangible assets arising from acquisitions become impaired, which would adversely affect our net income.

In accordance with U.S. GAAP, we account for our acquisitions using the acquisition method of accounting, and such acquisitions have resulted in significant goodwill and intangible assets. These assets may become impaired in the future, which could have a material adverse effect on our results of operations following such acquisitions. We are required under U.S. GAAP to review our amortizable intangible assets for impairment when events or changes in circumstances indicate the carrying value may not be recoverable. Goodwill is required to be tested for impairment annually, or more frequently, if facts and circumstances warrant a review. Factors that may be considered a change in circumstances indicating that the carrying value of our amortizable intangible assets may not be recoverable include a decline in stock price and market capitalization and slower or declining growth rates in our industry. During 2022, we recognized RMB 4.5 million on impairment loss of intangible assets. In the future, we may be required to record a significant charge to earnings in our financial statements during the period in which any impairment of our goodwill or amortizable intangible assets is determined, which could have a material adverse effect on our results of operations.

12

Our grant of employee share options, restricted shares or other share-based compensation and any future grants could have an adverse effect on our net income.

We adopted an equity incentive plan in 2010, the 2010 Equity Incentive Plan, which was amended and restated in November 2018, the Amended and Restated 2010 Plan (the “Amended 2010 Plan”). We have granted options and restricted shares under these plans to our employees and consultants. U.S. GAAP prescribes how we account for share-based compensation, which may have an adverse or negative impact on our results of operations. U.S. GAAP requires us to recognize share-based compensation as compensation expense in the statement of operations based on the fair value of equity awards on the date of the grant, with the compensation expense recognized over the period in which the recipient is required to provide service in exchange for the equity award. These statements also require us to adopt a fair value-based method for measuring the compensation expense related to share-based compensation. During the year ended December 31, 2022, we recorded share-based compensation expenses of RMB 7.5 million (US$ 1.1 million) for the restricted stock and the unrecognized share-based compensation expenses amounted to nil as of December 31, 2022. The expenses associated with share-based compensation may reduce the attractiveness of issuing share options or restricted shares under our equity incentive plan. However, if we do not grant share options or restricted shares, or reduce the number of share options or restricted shares that we grant, we may not be able to attract and retain key personnel. If we grant more share options or restricted shares to attract and retain key personnel, the expenses associated with share-based compensation may adversely affect our results of operation.

Changes to accounting standards or taxation rules or practices or greater than anticipated tax liabilities may adversely affect our reported results of operations or how we conduct our business.

A change in accounting standards or taxation rules or practices can have a significant effect on our reported results and may even affect our reporting of transactions completed before the change is effective. New accounting standards or taxation rules, such as FASB Interpretation No. 48 “Accounting for Uncertainty in Income Taxes”, or FIN 48 (now codified as ASC 740), and various interpretations of accounting standards or taxation practices have been adopted and may be adopted in the future. These accounting standard and tax regulation changes, future changes and the uncertainties surrounding current practices and implementation procedures may adversely affect our reported financial results or the way we conduct our business. The determination of our provision for income tax and other tax liabilities requires significant judgment and, in the ordinary course of our business, there are many transactions and calculations where the ultimate tax determination is uncertain. Although we believe our estimates are reasonable, the ultimate decisions by the relevant tax authorities may differ from the amounts recorded in our financial statements and may materially affect our financial results in the period or periods for which such determination is made. Moreover, we may lose the tax benefits we are currently receiving or we may be forced to disgorge prior tax benefits we have enjoyed and pay additional taxes and possibly penalties for prior tax years, any of which would harm our results of operations.

13

RISKS RELATED TO REGULATIONS OF OUR U.S. BUSINESS

If we fail to comply with the extensive U.S. regulatory requirements related to operating a U.S. higher education institution, we could face significant monetary liabilities, fines and penalties, including loss of access to federal student loans and grants for our students.

As a provider of higher education in the United States, we are subject to extensive regulation on both the federal and state levels. These regulatory requirements cover virtually all phases and aspects of our U.S. postsecondary operations, including educational program offerings, facilities, civil rights, safety, public health, privacy, instructional and administrative staff, administrative procedures, marketing and recruiting, financial operations, payment of refunds to students who withdraw, acquisitions or openings of new schools or programs, addition of new educational programs, and changes in our corporate structure and ownership. In particular, the Higher Education Act and related regulations subject our U.S. colleges that participate in the various Title IV programs to significant regulatory scrutiny.

The Higher Education Act mandates specific regulatory responsibilities for each of the following components of the higher education regulatory triad: (1) the federal government through the Department of Education; (2) the accrediting agencies recognized by the Secretary of Education; and (3) state education regulatory bodies. In addition, other federal agencies such as the Consumer Financial Protection Bureau and Federal Trade Commission, and various state agencies and state attorneys general enforce consumer protection laws applicable to post-secondary educational institutions.

The regulations, standards, and policies of these regulatory agencies frequently change, and changes in, or new interpretations of, applicable laws, regulations, standards, or policies could have a material adverse effect on our accreditation, authorization to operate in various states, permissible activities, receipt of funds under Title IV programs, or costs of doing business.

Title IV requirements are enforced by the Department of Education and, in some instances, by private plaintiffs. If we are found not to be in compliance with these laws, regulations, standards, or policies, we could lose our access to Title IV program funds, which would have a material adverse effect on our U.S. college operations. Findings of noncompliance also could result in our being required to pay monetary damages, or being subjected to fines, penalties, injunctions, restrictions on our access to Title IV program funds, or other censure that could have a material adverse effect on our business.

On January 19, 2023, Bay State College was informed its accreditation is considered to be withdrawn by The New England Commission of Higher Education ("NECHE"). For detail please refer to "Risks related to regulations of our U.S. Business - Our failure to demonstrate financial responsibility or administrative capability may result in the loss of eligibility to participate in Title IV programs".

The ongoing regulatory effort aimed at for-profit post-secondary institutions of higher education could lead to additional legislation or other governmental action that may negatively affect the industry.

The proprietary post-secondary education sector has at times experienced scrutiny from federal legislators, agencies, and state legislators and attorneys general. An adverse disposition of these existing inquiries, administrative actions, or claims, or the initiation of other inquiries, administrative actions, or claims, could, directly or indirectly, have a material adverse effect on our business, financial condition, result of operations, and cash flows and result in significant restrictions on us and our ability to operate.

On January 19, 2023, Bay State College was informed its accreditation is considered to be withdrawn by The New England Commission of Higher Education ("NECHE"). For detail please refer to "Risks related to regulations of our U.S. Business - Our failure to demonstrate financial responsibility or administrative capability may result in the loss of eligibility to participate in Title IV programs".

14

If we fail to maintain our institutional accreditation or if our institutional accrediting body loses recognition by the Department of Education, we would lose our ability to participate in Title IV programs.

The loss of institutional accreditation by any of our U.S. colleges would render any of our U.S. colleges ineligible to participate in Title IV programs and would have a material adverse effect on our business, financial condition, results of operations, and cash flows and result in the imposition of significant restrictions on us and our ability to operate. In addition, an adverse action by our institutional accreditors other than loss of accreditation, such as issuance of a warning, could have a material adverse effect on our business.

If we fail to obtain recertification by the Department of Education when required, we would lose our ability to participate in Title IV programs.

Each institution participating in Title IV programs must enter into a Program Participation Agreement with the Department of Education. Under the agreement, the institution agrees to follow the Department of Education’s rules and regulations governing Title IV programs. An institution generally must seek recertification from the Department of Education at least every six years and possibly more frequently depending on various factors, such as whether it is provisionally certified. The Department of Education may also review an institution’s continued eligibility and certification to participate in Title IV programs, or scope of eligibility and certification, in the event the institution undergoes a change in ownership resulting in a change of control or expands its activities in certain ways, such as the addition of certain types of new programs, or, in certain cases, changes to the academic credentials that it offers. In certain circumstances, the Department of Education must provisionally certify an institution. The Department of Education may withdraw our certification if it determines that we are not fulfilling material requirements for continued participation in Title IV programs. If the Department of Education does not renew, or withdraws our certification to participate in Title IV programs, our students would no longer be able to receive Title IV program funds. Alternatively, the Department of Education could (1) renew the certifications for an institution, but restrict or delay receipt of Title IV funds, limit the number of students to whom an institution could disburse such funds, or place other restrictions on that institution, or (2) delay recertification after an institution’s PPA expires, in which case the institution’s certification would continue on a month-to-month basis, any of which would have a material adverse effect on our business, financial condition, results of operations, and cash flows.

On October 13, 2020, the Department of Education and Bay State College executed a Provisional Program Participation Agreement, approving Bay State College’s continued participation in Title IV programs with full certification through September 30, 2023. On January 16, 2022, the Department of Education and NewSchool executed a Program Participation Agreement, approving NewSchool’s continued participation in Title IV programs with full certification through December 31, 2024. Furthermore, the Department of Education has approved the change of ownership control for Bay State College and NewSchool.

Student loan defaults could result in the loss of eligibility to participate in Title IV programs.

In general, under the Higher Education Act, an educational institution may lose its eligibility to participate in some or all Title IV programs if, for three consecutive federal fiscal years, 30% or more of its students who were required to begin repaying their student loans in the relevant federal fiscal year default on their payment by the end of the second federal fiscal year following that fiscal year. Institutions with a cohort default rate equal to or greater than 15% for any of the three most recent fiscal years for which data are available are subject to a 30-day delayed disbursement period for first-year, first-time borrowers.

If we lose eligibility to participate in Title IV programs because of high student loan default rates, it would have a material adverse effect on our business, financial condition, results of operations, and cash flows and result in the imposition of significant restrictions on us and our ability to operate. The latest default rate for Bay State College published by the Department of Education is 4.7% for the fiscal year of 2022 and 3.6% for NewSchool for the fiscal year of 2022, respectively.

15

Our U.S. colleges could lose their eligibility to participate in federal student financial aid programs or be provisionally certified with respect to such participation if the percentage of our revenues derived from those programs were too high.

A proprietary institution may lose its eligibility to participate in the federal Title IV student financial aid program if it derives more than 90% of its revenues, on a cash basis, from Title IV programs for two consecutive fiscal years. A proprietary institution of higher education that violates the 90/10 Rule for any fiscal year will be placed on provisional status for up to two fiscal years. Using the formula specified in the Higher Education Act, Bay State College and NewSchool derived approximately 56% and 55% of their cash-basis revenues from these programs in the year of 2021, respectively. Percentages of Bay State College and NewSchool for the year of 2022 are in process of audits as of the date of this report, which we estimate will be in compliance with the 90/10 Rule. If any of our U.S. colleges lose eligibility to participate in Title IV programs because they are unable to comply with 90/10 Rule, it could have a material adverse effect on our business, financial condition, results of operations, and cash flows and result in the imposition of significant restrictions on us and our ability to operate.

Our failure to demonstrate financial responsibility or administrative capability may result in the loss of eligibility to participate in Title IV programs.

All U.S. colleges are subject to meeting financial and administrative standards. These standards are assessed through annual compliance audits, periodic renewal of institutional PPAs, periodic program reviews and ad hoc events which may lead the Department of Education to evaluate an institution’s financial responsibility or administrative capability. The administrative capability criteria require, among other things, that our institution (1) has an adequate number of qualified personnel to administer Title IV programs, (2) has adequate procedures for disbursing and safeguarding Title IV funds and for maintaining records, (3) submits all required reports and consolidated financial statements in a timely manner, and (4) does not have significant problems that affect the institution’s ability to administer Title IV programs.

A financial responsibility test is required for continued participation by an institution’s students in U.S. federal financial assistance programs. The test is based upon a composite score of three ratios: an equity ratio that measures the institution’s capital resources; a primary reserve ratio that measures an institution’s ability to fund its operations from current resources; and a net income ratio that measures an institution’s ability to operate profitably. A minimum score of 1.5 is necessary to meet the financial standards. Institutions with scores of less than 1.5 but greater than or equal to 1.0 are considered financially responsible, but require additional oversight. These schools are subject to heightened cash monitoring and other participation requirements. An institution with a score of less than 1.0 is considered not financially responsible. However, a school with a score of less than 1.0 may continue to participate in the Title IV programs under provisional certification. In addition, this lower score typically requires that the school be subject to heightened cash monitoring requirements and post a letter of credit (equal to a minimum of 10% of the Title IV aid it received in the institution’s most recent fiscal year). For the fiscal year of 2020, the composited scores of Bay State College was 1.8. NewSchool was first subject to a composite score calculation for the year ending December 31, 2021 since being acquired by the Group. The audits to calculate the composited scores of Bay State College and NewSchool for the fiscal year of 2021 are in process as of the date of this report. We estimate both Bay State College and NewSchool would meet the required minimum of 1.5.

If the Department of Education determines, in its judgment, that Bay State College and NewSchool have failed to demonstrate either financial responsibility or administrative capability, we could be subject to sanctions, including, among other things, a requirement to post a letter of credit, fines, suspension or termination of our eligibility to participate in Title IV programs or repayment of funds received under Title IV programs, any of which could have a material adverse effect on our business, financial condition, results of operation and cash flows and result in the imposition of significant restrictions on us and our ability to operate. The Department of Education has considerable discretion under the regulations to impose the foregoing sanctions and, in some cases, such sanctions could be imposed without advance notice or any prior right of review or appeal.

16

On January 19, 2023, The New England Commission of Higher Education (“NECHE”) informed Bay State College of its intention to withdraw Bay State College’s accreditation as of August 31, 2023. The determination was based on NECHE’s opinion that the College could not come into compliance with Institutional Resources (Accreditation Standard 7) within three years. The decision has no bearing on the quality of the Bay State College’s educational program or outcomes. On March 20, 2023, the appeal panel of NECHE affirmed NECHE’s decision to withdraw Bay State College’s accreditation. Without NECHE accreditation, Bay State College will not be able to disburse Title IV funding to its students for classes after August 2023, and will not be able to disburse VA funding to its students for classes after Spring semester ends. We anticipated the annualized impact to the topline will be approximately US$ 6.0 million with no negative impact on our bottom line. Our plan is to keep its nursing teaching staff and teaching equipment, and to partner with hospitals in creating training institutions that provide pre-service education for nursing staff.

Our failure to comply with the Borrower Defense to Repayment Regulations could result in sanctions and other liability.

Under the Higher Education Act, The Department of Education is authorized to specify in regulations, which acts or omissions of an institution of higher education a borrower may assert as a defense to repayment of a Direct Loan made under the Direct Loan Program. On July 1, 2020, new Defense to Repayment regulations went into effect that include a higher threshold for establishing misrepresentation, provides for a statute of limitation for claims submission, narrows the current triggers allowed for letter of credit requirements, and eliminates provisions for group discharges. The new regulations are effective with claims on loans disbursed on or after July 1, 2020.

Management is unable to predict how regulations will be revised, the result of any other current or future rulemakings, or the impact of such rulemakings on our business. The outcome of any legal proceeding instituted by a private party or governmental authority, facts asserted in pending or future lawsuits, and/or the outcome of any future governmental inquiry, lawsuit, or enforcement action could serve as the basis for claims by students or The Department of Education under the Defense to Repayment regulations, the posting of substantial letters of credit, or the termination of eligibility of our institutions to participate in the Title IV program based on The Department of Education’s institutional capability assessment, any of which could, individually or in the aggregate, have a material adverse effect on our business, financial condition, results of operations, and cash flows.

Our business operations could be harmed if we experience a disruption in our ability to process student loans under the Federal Direct Loan Program.

Any processing disruptions by the Department of Education may affect our students’ ability to obtain student loans on a timely basis. If we experience a disruption in our ability to process student loans through the Federal Direct Loan Program, either because of administrative challenges on our part or the inability of the Department of Education to process the volume of direct loans on a timely basis, our business, financial condition, results of operations, and cash flows related to our U.S. colleges could be adversely and materially affected.

Our business operations could be harmed if Congress makes changes to the availability of Title IV funds.

We collected approximately 41.3% and 31.2% of the consolidated net revenues in our revenue from receipt by Bay State College and NewSchool of Title IV financial aid program funds in the year of 2022, respectively, principally from federal student loans under the Federal Direct Loan Program. Changes in the availability of these funds or a reduction in the amount of funds disbursed may have a material adverse effect on our enrollment, financial condition, results of operations, and cash flows. Action by the U.S. Congress to revise the laws governing the federal student financial aid programs or reduce funding for those programs could reduce our student enrollment and/or increase costs of operation. Political and budgetary concerns significantly affect Title IV programs. Any action by the U.S. Congress that significantly reduces Title IV program funding or the ability of our U.S. colleges or students to participate in Title IV programs could have a material adverse effect on our business, financial condition, results of operations, and cash flows.

17

RISKS RELATED TO OWNERSHIP OF OUR ADSS

We have disposed of our China business and currently do not conduct any business activities in China, which could negatively impact the price of our ADSs.

On May 14, 2021, the PRC State Council promulgated the 2021 Implementing Rules for the Law for Promoting Private Education, which became effective on September 1, 2021. The 2021 Implementing Rules prohibit foreign-invested enterprises established in China and social organizations whose actual controllers are foreign parties from controlling private schools that provide compulsory education by means of mergers, acquisitions, contractual arrangements, etc. To comply with the 2021 Implementing Rules, on November 23, 2022, we entered a share purchase agreement to dispose all of our equity interest in Ambow China for a cash consideration of US$ 12.0 million (the “Sale of Ambow China”). The Sale of Ambow China was completed on December 31, 2022. After the Sale of Ambow China, we have sold all our assets and operations in China and have ceased control of all the VIEs. This is a material shift of our business and may adversely affect the market price of our ordinary shares and ADSs

We cannot assure you that the ADSs will not be delisted from the NYSE American, which could negatively impact the price of the ADSs and our ability to access the capital markets.

We cannot give you any assurance that a broader or more active public trading market for the ADSs will develop on the NYSE American or be sustained, or that current trading levels in ADSs will be sustained. In addition, if we fail to meet the criteria set forth in SEC regulations, by law, various requirements would be imposed on broker-dealers who sell our securities to persons other than established customers and accredited investors. Consequently, such regulations may deter broker-dealers from recommending or selling the ADSs, which may further affect the liquidity of the ADSs.

The listing standards of the NYSE American provide that a company, in order to qualify for continued listing, must maintain a minimum share price of $1.00 and satisfy standards relative to minimum shareholders’ equity, minimum market value of publicly held shares and various additional requirements. If we fail to comply with all listing standards applicable to issuers listed on the NYSE American, the ADSs may be delisted. If the ADSs are delisted, it could reduce the price of the ADSs and the levels of liquidity available to our shareholders. In addition, the delisting of the ADSs could materially and adversely affect our access to the capital markets and any limitation on liquidity or reduction in the price of the ADSs could materially and adversely affect our ability to raise capital. Delisting from the NYSE American could also result in other negative consequences, including the potential loss of confidence by suppliers, customers and employees, the loss of institutional investor interest and fewer business development opportunities.

The market price of our ordinary shares and the ADSs could be subject to volatility.

The market price of our ordinary shares and the ADSs is likely to be highly volatile and subject to wide fluctuations in response to factors such as:

| ● | variations in our actual and perceived operating results; |

| ● | announcements of new products or services by us or our competitors; |

| ● | technological breakthroughs by us or our competitors; |

| ● | news regarding gains or losses of customers or partners by us or our competitors; |

| ● | news regarding gains or losses of key personnel by us or our competitors; |

| ● | announcements of competitive developments, acquisitions or strategic alliances in our industry by us or our competitors; |

| ● | changes in earnings estimates or buy/sell recommendations by financial analysts; |

| ● | potential litigation; |

18

| ● | general market conditions or other developments affecting us or our industry; and |

| ● | the operating and stock price performance of other companies, other industries and other events or factors beyond our control. |

In addition, the securities markets have from time to time experienced significant price and volume fluctuations that are not related to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of the ordinary shares and the ADSs.

Insiders have substantial control over us, which could adversely affect the market price of our ADSs.

Under our Sixth Amended and Restated Memorandum and Articles of Association, our ordinary shares are divided into Class A Ordinary Shares and Class C Ordinary Shares. Holders of Class A Ordinary Shares are entitled to one vote per share, while holders of Class C Ordinary Shares are entitled to ten votes per share. Shareholdings of our executive officers and directors, and their respective affiliates, give them the power to control any actions that require shareholder approval under Cayman Islands law, our Sixth Amended and Restated Memorandum and Articles of Association, including the election and removal of any member of our board of directors, mergers, consolidations and other business combinations, changes to our Sixth Amended and Restated Memorandum and Articles of Association, the number of shares available for issuance under share incentive plans and the issuance of significant amounts of our ordinary shares in private placements. Our executive officers and directors and their respective affiliates have sufficient voting rights to determine the outcome of all matters requiring shareholder approval.

As a result of our executive officers and directors and their respective affiliates’ ownership of a majority of our ordinary shares, their voting power may cause transactions to occur that might not be beneficial to you as a holder of ADSs and may prevent transactions that would be beneficial to you. For example, their voting power may prevent a transaction involving a change of control of us, including transactions in which you as a holder of our ADSs might otherwise receive a premium for your securities over the then-current market price. Similarly, our executive officers and directors and their respective affiliates may approve a merger or consolidation of our company which may result in you receiving a stake (either in the form of shares, debt obligations or other securities) in the surviving or new consolidated company which may not operate our current business model and dissenters’ rights may not be available to you in such an event. This concentration of ownership could also adversely affect the market price of our ADSs or lessen any premium over market price that an acquirer might otherwise pay.

We may need additional capital, and the sale of additional ADSs or other equity securities would result in additional dilution to our shareholders.

We believe that our current cash and cash equivalents and anticipated cash flow from operations will be sufficient to meet our anticipated cash needs for more than the next twelve months. We may, however, require additional cash resources due to changed business conditions or other future developments. If our resources are insufficient to satisfy our cash requirements, we may seek to sell additional equity or debt securities or obtain a credit facility. To consummate these transactions, we may issue additional shares in these acquisitions that will dilute our shareholders. The sale of additional equity securities could result in additional dilution to our shareholders. The incurrence of indebtedness would result in increased debt service obligations and could result in operating and financing covenants that would restrict our operations or our ability to pay dividends. Our ability to raise additional funds in the future is subject to a variety of uncertainties, including:

| ● | Our future financial condition, results of operations and cash flows; |

| ● | General market conditions for capital raising activities; and |

| ● | Economic, political and other conditions in China and elsewhere. |

We cannot assure you that if we need additional cash financing it will be available in amounts or on terms acceptable to us, or at all.

19

Anti-takeover provisions in our Sixth Amended and Restated Memorandum and Articles of Association may discourage, delay or prevent a change in control.

Some provisions of our Sixth Amended and Restated Memorandum and Articles of Association may discourage, delay or prevent a change in control of our company or management that shareholders may consider favorable, including, among other things, the following:

| ● | Provisions that authorize our board of directors to issue preferred shares in one or more series and to designate the price, rights, preferences, privileges and restrictions of such preferred shares without any further vote or action by our shareholders; and |

| ● | Provisions that restrict the ability of our shareholders to call meetings and to propose special matters for consideration at shareholder meetings. |

You may be subject to limitations on transfer of your ADSs.

Your ADSs are transferable on the books of the depositary. However, the depositary may close its transfer books at any time or from time to time when it deems expedient in connection with the performance of its duties. In addition, the depositary may refuse to deliver, transfer or register transfers of ADSs generally when our books or the books of the depositary are closed, or at any time if we or the depositary deem it advisable to do so because of any requirement of law or of any government or governmental body, or under any provision of the deposit agreement, or for any other reason.

Before the Sale of Ambow China, all of our PRC corporate entities, including Beijing Ambow Shengying Education and Technology Co., Ltd. (“Ambow Shengying”), Beijing BoheLe Science and Technology Co., Ltd. (“BoheLe”) and OOOK (Beijing) Education and Technology Co., Ltd. (“OOOK WFOE”), our VIEs and their subsidiaries, maintained corporate records and filings with industry and commerce administration authorities where such PRC entities are registered. Information contained in such corporate records and filings includes, among others, business address, registered capital, business scope, articles of association, equity interest holders, legal representative, changes to the above information, annual financial reports, matters relating to termination or dissolution, information relating to penalties imposed, and annual inspection records.

There have been regulations promulgated by various government authorities in PRC that govern the public access to corporate records and filings. Pursuant to the Company Law and Regulations of the People’s Republic of China on the Registration Administration of Companies, the company registration authority shall record the registered items of companies in a company recording book for the consultation and reproduction purposes of the public. The general public may apply to the company registration authority for inspection of the registered items of companies. Under the Measures for Accessing Corporate Records and Filings promulgated on December 16, 1996 by the State Administration for Industry and Commerce (“SAIC”), or the SAIC Measures, a wide range of basic corporate records, except for such restricted information as business results and financial reports, can be inspected by the public without restrictions. Under these SAIC Measures, a company’s restricted information can only be inspected by authorized government officers and officials from judicial authorities or lawyers involved in pending litigation relating to such company and with court-issued proof of such litigation. In practice, local industry and commerce administration authorities in different cities have adopted various regional regulations, which impose more stringent restrictions than the SAIC Measures by expanding the scope of restricted information that the public cannot freely access. Many local industry and commerce administration authorities only allow unrestricted public access to such basic corporate information as name, legal representative, registered capital and business scope of a company. Under these local regulations, access to the other corporate records and filings (many of which are not restricted information under the SAIC Measures) is only granted to authorized government officers and officials from judicial authorities or lawyers involved in pending litigation relating to such company and with court-issued proof of such litigation.

20

However, neither the SAIC nor the local industry and commerce administration authorities have strictly implemented the restrictions under either the SAIC Measures or the various regional regulations before early 2012. As a result, before early 2012, the public was able to access all or most corporate records and filings of these listed companies’ PRC affiliates maintained with the industry and commerce administration authorities. Such records and filings were reported to have formed important components of research reports on certain China-based, U.S.-listed companies, which were claimed to have uncovered wrongdoings and fraud committed by these companies.

It was reported that, since the first half of 2012, local industry and commerce administration authorities in a number of cities had started strictly implementing the above restrictions and had significantly curtailed public access to corporate records and filings. There have also been reports that only the limited scope of basic corporate records and filings are still accessible by the public, and much of the previously publicly accessible information, such as financial reports and changes to equity interests, now can only be accessed by the parties specified in, and in strict accordance with the restrictions under, the various regional regulations. Individuals other than the parties specified in the various regional regulations may get access to the corporate records and filings including, but not limited to, financial reports, shareholder changes and assets transfers with the permission of the PRC subject companies with reference letters issued by the companies. Such reported limitation on the public access to corporate records and filings and the resulting concerns over the loss of, or limit in, an otherwise available source of information to verify and evaluate the soundness of China-based U.S.-listed companies’ business operations in China may have a significant adverse effect on the overall investor confidence in such companies’ reported results or other disclosures, including those of our company, and may cause the trading price of our ADSs to decline.

Our ADSs or Ordinary Shares may be delisted under the Holding Foreign Companies Accountable Act (“HFCA Act”) if the PCAOB is unable to adequately inspect audit documentation located in China. The delisting of our ADSs or Ordinary Shares, or the threat of their being delisted, may materially and adversely affect the value of your investment. Additionally, the inability of the PCAOB to conduct adequate inspections deprives our investors from the benefits of such inspections. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which was enacted on December 29, 2022 under the Consolidated Appropriations Act 2023, amends the HFCA Act and requires the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three.

The Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted on December 18, 2020. The HFCA Act states if the SEC determines that a company has filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit such ordinary shares from being traded on a national securities exchange or in the over-the-counter trading market in the U.S.