UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark One) | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number 001-38735

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||

| (Address of principal executive offices, zip code) | ||||||||

( | ||||||||

| (Registrant’s telephone number, including area code) | ||||||||

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Sec.232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ☐ Yes x No

The aggregate market value of the Common Stock held by non-affiliates of the registrant (excluding outstanding shares beneficially owned by directors, executive officers, and other affiliates) on June 30, 2023, was approximately $1.3 billion based on the closing price of the Company’s common stock as reported that date on the New York Stock Exchange of $164.36 per share. Such assumptions should not be deemed to be conclusive for any other purpose.

Number of shares of the registrant’s Common Stock, $0.01 par value, outstanding as of February 19, 2024: 12,994,558

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates certain information by reference from the registrant’s definitive proxy statement for the 2024 annual meeting of stockholders (the “Proxy Statement”), which will be filed no later than 120 days after the close of the registrant’s fiscal year ended December 31, 2023.

| TABLE OF CONTENTS | ||||||||

3

4

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report includes statements of our expectations, intentions, plans and beliefs that constitute “forward-looking statements.” These statements, which involve risks and uncertainties, relate to analyses and other information that are based on forecasts of future results and estimates of amounts not yet determinable and may also relate to our future prospects, developments and business strategies. We have used the words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “should” and similar terms and phrases, including references to assumptions, in this report to identify forward-looking statements, but these terms and phrases are not the exclusive means of identifying such statements. These forward-looking statements are made based on expectations and beliefs concerning future events affecting us and are subject to uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond our control, that could cause our actual results to differ materially from those expressed in or implied by these forward-looking statements.

The following factors are among those that may cause actual results to differ materially from our forward-looking statements:

•the financial performance of the company;

•our liquidity, results of operations and financial condition;

•our ability to generate sufficient cash or obtain financing to fund our business operations;

•depressed levels or declines in coal prices;

•railroad, barge, truck, port and other transportation availability, performance and costs;

•changes in domestic or international environmental laws and regulations, and court decisions, including those directly affecting our coal mining and production and those affecting our customers’ coal usage, including potential climate change initiatives;

•steel and coke producers switching to alternative energy sources such as natural gas, renewables and coal from basins where we do not operate;

•our ability to obtain or renew surety bonds on acceptable terms or maintain our current bonding status;

•worldwide market demand for coal and steel, including demand for U.S. coal exports, and competition in coal markets;

•attracting and retaining key personnel and other employee workforce factors, such as labor relations;

•our ability to execute our share repurchase program;

•our ability to self-insure certain of our black lung obligations without a significant increase in required collateral;

•our ability to meet collateral requirements and fund employee benefit obligations;

•inflationary pressures on supplies and labor and significant or rapid increases in commodity prices;

•disruptions in delivery or changes in pricing from third-party vendors of key equipment and materials that are necessary for our operations, such as diesel fuel, steel products, explosives, tires and purchased coal;

•our ability to consummate financing or refinancing transactions, and other services, and the form and degree of these services available to us, which may be significantly limited by the lending, investment and similar policies of financial institutions and insurance companies regarding carbon energy producers and the environmental impacts of coal combustion;

•failures in performance, or non-performance, of services by third-party contractors, including contract mining and reclamation contractors;

•disruption in third-party coal supplies;

•cybersecurity attacks or failures, threats to physical security, extreme weather conditions or other natural disasters;

•the imposition or continuation of barriers to trade, such as tariffs;

•increased volatility and uncertainty regarding worldwide markets, seaborne transportation and our customers as a result of developments in and around Ukraine and the Middle East;

•changes in, renewal or acquisition of, terms of and performance of customers under coal supply arrangements and the refusal by our customers to receive coal under agreed-upon contract terms;

•reductions or increases in customer coal inventories and the timing of those changes;

•our production capabilities and costs;

•our ability to obtain, maintain or renew any necessary permits or rights;

•inherent risks of coal mining, including those that are beyond our control;

•changes in, interpretations of, or implementations of domestic or international tax or other laws and regulations, including the Inflation Reduction Act of 2022 and its related regulations;

•our relationships with, and other conditions affecting, our customers, including the inability to collect payments from our customers if their creditworthiness declines;

•our indebtedness as we may incur it from time to time;

•reclamation and mine closure obligations; and

•our assumptions concerning economically recoverable coal reserve estimates.

5

The list of factors identified above is not exhaustive. We caution readers not to place undue reliance on any forward looking statements, which are based on information currently available to us and speak only as of the dates on which they are made. When considering these forward-looking statements, you should keep in mind the cautionary statements in this report. We do not undertake any responsibility to publicly revise these forward-looking statements to take into account events or circumstances that occur after the date of this report. Additionally, except as expressly required by federal securities laws, we do not undertake any responsibility to update you on the occurrence of any unanticipated events, which may cause actual results to differ from those expressed or implied by the forward-looking statements contained in this report.

6

Part I

Item 1. Business

Unless otherwise indicated or the context otherwise requires, references in this “Item 1. Business” section to “the combined company,” “we,” “us” and other similar terms refer to Alpha Metallurgical Resources, Inc. and its consolidated subsidiaries (previously Contura Energy, Inc. and its consolidated subsidiaries). Disclosures in this “Item 1. Business” section should be read in conjunction with “Item 1A. Risk Factors” for further discussion of factors impacting our business. Effective February 1, 2021, we changed our corporate name from Contura Energy, Inc. to Alpha Metallurgical Resources, Inc. to more accurately reflect our strategic focus on the production of metallurgical coal. Following the effectiveness of our name change, our ticker symbol on the New York Stock Exchange changed from “CTRA” to “AMR” effective on February 4, 2021.

Our Company

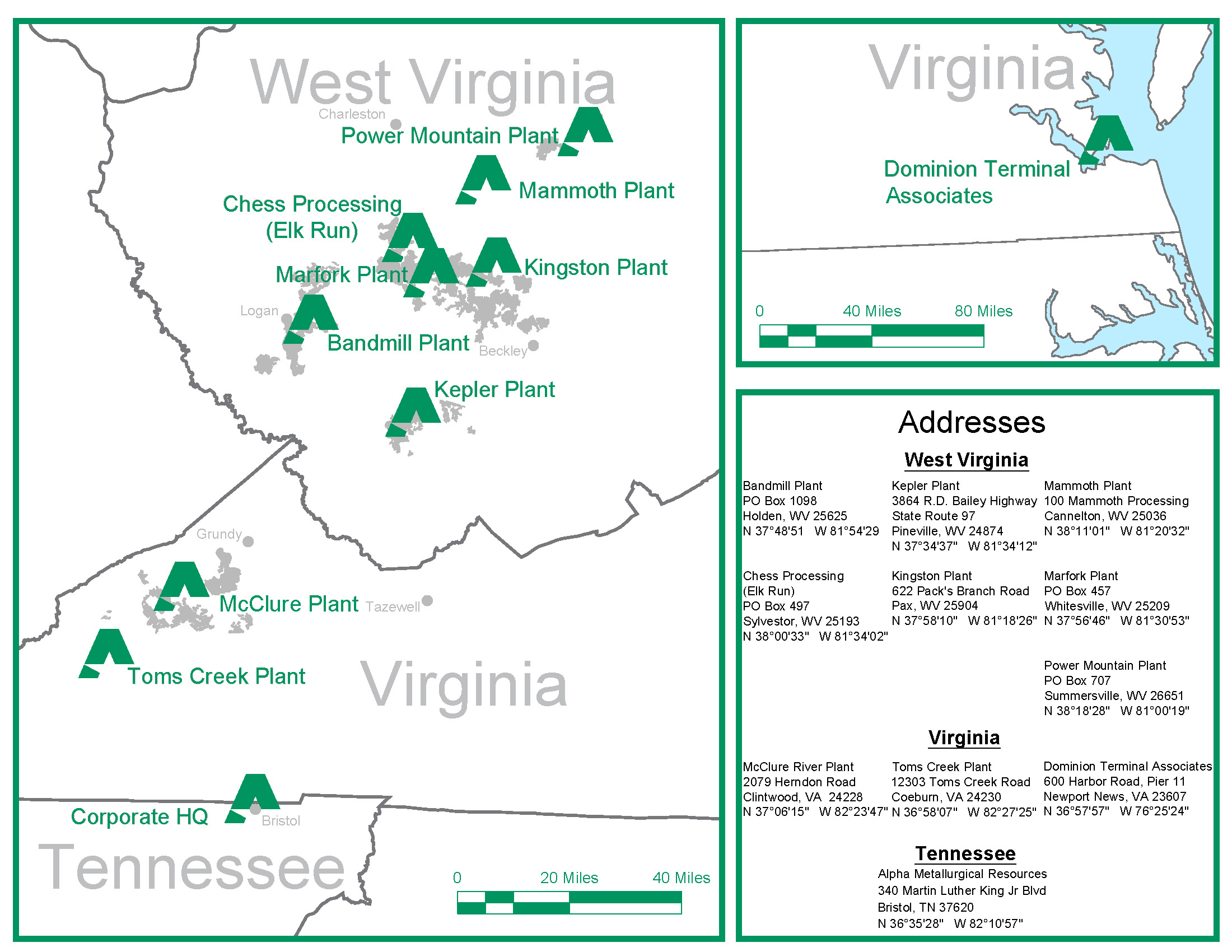

We are a Tennessee-based mining company with operations in Virginia and West Virginia. With customers across the globe, high-quality reserves and significant port capacity, we reliably supply metallurgical coal products to the steel industry. We operate highly productive, cost-competitive coal mines across the CAPP coal basin. Our portfolio of mining operations consists of 15 underground mines, seven surface mines and nine coal preparation plants. We own a 65.0% interest in Dominion Terminal Associates (“DTA”), a coal export terminal in Newport News, Virginia. DTA provides us with the ability to fulfill a broad range of customer coal quality requirements through coal blending, while also providing storage capacity and transportation flexibility.

We predominantly produce metallurgical (“met”) coal, which is shipped to domestic and international steel and coke producers. Although our strategic focus is on the production of met coal, we also produce thermal coal as byproduct and it is primarily sold to large utilities and industrial customers both in the United States and across the world. Refer to Notes 22 and 23 to the Consolidated Financial Statements for geographical information about our coal sales and additional segment information.

We have a substantial reserve base of 316.0 million tons of proven and probable reserves as of December 31, 2023. Our reserve base consists of 303.0 million tons of proven and probable metallurgical reserves, and 12.9 million tons of proven and probable thermal reserves.

Through our operations across the CAPP coal basin in Virginia and West Virginia, we are able to source coal from multiple mines to meet the needs of a long-standing global customer base, many of which have been served by us or our predecessors for decades. We are continuously evaluating opportunities to strategically cultivate current relationships to drive new business in our target growth markets. In addition, our experienced management team regularly analyzes potential acquisitions, joint ventures and other opportunities that would be accretive and synergistic to our existing asset portfolio.

Other Business Developments

During 2023, development was completed and production began at our Rolling Thunder and Checkmate Powellton mines within our Power Mountain and Elk Run mining complexes, respectively, which produce High-Vol. B quality met coal from the Powellton coal seam.

In August 2023, we completed our transition to a pure-play metallurgical producer with the closure of Slabcamp, which was our last remaining thermal mine.

Our History

We were formed in 2016 to acquire and operate certain of Alpha Natural Resources, Inc.’s former core coal operations, as part of the Alpha Natural Resources, Inc. Plan of Reorganization. We entered into various settlement agreements with the Debtors, their bankruptcy successor, and third parties as part of the Debtors’ bankruptcy reorganization process. We assumed acquisition-related obligations through those settlement agreements, which became effective on July 26, 2016, the effective date of the Debtors’ Plan of Reorganization. As of December 31, 2023, we did not have any remaining acquisition-related obligations. Refer to Note 14 to the Consolidated Financial Statements for further information on our acquisition-related obligations.

On December 8, 2017, we closed a transaction with Blackjewel to sell our Western Mines located in the PRB, Wyoming, along with related coal reserves, equipment, infrastructure and other real properties. On October 4, 2019, we closed on the ESM Transaction in connection with Blackjewel’s subsequent bankruptcy filing. On May 29, 2020, certain of our subsidiaries

7

(Contura Coal West, LLC and Contura Wyoming Land, LLC), one of which held the mining permits for the Western Mines, were merged with certain subsidiaries of ESM to become wholly-owned subsidiaries of ESM and to complete the permit transfer process in connection with the ESM Transaction.

On November 9, 2018, we merged with Alpha Natural Resources Holdings, Inc. and ANR, Inc. Upon the consummation of the transactions contemplated by a definitive merger agreement (the “Merger Agreement”), our common stock began trading on the New York Stock Exchange under the ticker “CTRA.” Previously, our shares traded on the OTC market under the ticker “CNTE.”

On December 10, 2020, we closed on a transaction with Iron Senergy Holdings, LLC, to sell our thermal coal mining operations located in Pennsylvania consisting primarily of our Cumberland mining complex and related property (our former NAPP operations). This transaction accelerated our strategic exit from thermal coal production to shift our focus to met coal production.

Effective February 1, 2021, we changed our corporate name from Contura Energy, Inc. to Alpha Metallurgical Resources, Inc. to more accurately reflect our strategic focus on the production of met coal. Following the effectiveness of our name change, our ticker symbol on the New York Stock Exchange changed from “CTRA” to “AMR” effective on February 4, 2021.

Our Mining Operations and Properties

The following table provides a summary of information regarding our active mining complexes as of December 31, 2023 (see also “Item 2. Properties” for further information):

(Amounts in thousands, except for mine data) | Tons Sold (4) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mining Complex | Location | Acquired | Mines (1) | Equipment (2) | Rail (3) | 2023 | 2022 | 2021 | Carrying Value (5) | Reserves (6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aracoma | WV | 2018 | 3 | CM | CSX | 2,607 | 2,643 | 2,221 | $ | 174,652 | 41,276 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Kepler | WV | 2018 | 1 | CM | CSX/NS | 1,958 | 1,897 | 1,571 | $ | 235,203 | 41,190 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Kingston | WV | 2018 | 4 | CM/S/H | CSX | 2,254 | 1,935 | 2,348 | $ | 34,208 | 38,657 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Marfork | WV | 2018 | 6 | CM/S/H | CSX | 4,345 | 4,106 | 4,032 | $ | 322,733 | 97,653 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| McClure/Toms Creek | VA | 2016 | 5 | CM/S/H | CSX/NS | 4,071 | 3,703 | 4,033 | $ | 114,530 | 68,747 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Power Mountain | WV | 2016 | 2 | CM | NS | 718 | 832 | 837 | $ | 70,594 | — | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Elk Run | WV | 2018 | 1 | CM | CSX | — | — | — | $ | 35,535 | 28,434 | |||||||||||||||||||||||||||||||||||||||||||||||||||

(1) Number of active mines as of December 31, 2023.

(2) Equipment: S = Shovel/Excavator/Loader/Trucks; CM = Continuous Miner; H = Highwall Miner

(3) CSX = CSX Transportation; NS = Norfolk Southern Railway Company

(4) Tons of coal purchased from third parties and not processed are not included.

(5) Net book value of property, plant and equipment and owned and leased mineral rights as of December 31, 2023.

(6) Proven and probable reserves as of December 31, 2023. Refer to Item 2. Properties for further information. Feasibility/Pre-feasibility study not considered cost beneficial for Power Mountain complex.

Aracoma – Aracoma is a mining complex located in Logan, Mingo, and Boone counties, West Virginia. The complex has three active underground mines which produce primarily High-Vol. B quality met coal from the Upper Chilton, Upper Cedar Grove, and No. 2 Gas coal seams. Mine lives range from 5 to 16 years. Coal is processed at the Bandmill Preparation Plant and loaded onto CSX rail for delivery to customers.

Kepler – Kepler is a mining complex located in Wyoming, McDowell, and Raleigh counties, West Virginia. The complex has one active underground mine (with an estimated life of 15 years) which produces primarily Low-Vol. quality met coal from the Pocahontas No. 3 coal seam. Coal is processed at the Kepler Preparation Plant and either loaded onto NS rail or trucked to the Feats Loadout and loaded onto the CSX rail for delivery to customers.

Kingston – Kingston is a mining complex located in Fayette and Raleigh counties, West Virginia. The complex has one active underground mine, which produces primarily Mid-Vol. quality met coal from the Douglas coal seam. The complex also has three active surface mines which produced High-Vol. A quality met coal as well as some thermal quality coal as a by-product of mining from multiple coal seams. Mine lives range from 2 to 11 years. Coal from the underground mine is processed at the Kingston Preparation Plant and trucked to the Pax Loadout to be loaded onto CSX rail for delivery to customers. Coal from the

8

surface mines may be processed through the Kingston Preparation Plant, trucked to and processed through the Mammoth Plant, or trucked directly to the Pax Loadout or Marmet Dock for delivery to customers.

Marfork – Marfork is a mining complex located in Raleigh, Boone, Kanawha, and Fayette counties, West Virginia. The complex has three active underground mines which produce High-Vol. A quality met coal from the Eagle coal seam and one active underground mine that produces mid-vol quality met coal from the Glen Alum Tunnel seam. The complex also has two active surface mines which produce High-Vol. A quality met coal as well as some thermal quality coal as a by-product of mining from multiple coal seams. Mine lives range from 2 to 17 years. Coal from the underground mines is processed at the Marfork Preparation Plant and loaded onto the CSX rail for delivery to customers. Coal from the surface mines may be processed through the Marfork Preparation Plant or trucked directly to the Pax Loadout or the Marmet Dock for delivery to customers.

McClure/Toms Creek – McClure/Toms Creek is a mining complex located in Dickenson, Buchanan, Russell, and Wise counties, Virginia. The complex has three active underground mines which produce High-Vol. A and Mid-Vol. quality met coal from the Upper Banner, Lower Banner, and Jawbone coal seams. The complex also has two active surface mines which produce primarily High-Vol. A quality met coal as well as some thermal quality coal as a by-product of mining from multiple coal seams. Mine lives range from 2 to 27 years. Coal is processed at either the McClure Preparation Plant or the Toms Creek Preparation Plant and loaded on the CSX or NS rail, respectively for delivery to customers.

Power Mountain – Power Mountain is a mining complex located in Nicholas County, West Virginia. The complex has one active underground mine (with an estimated life of 3 years) which produces High-Vol. B quality met coal from the Eagle coal seam. Coal is processed at the Power Mountain Preparation Plant and loaded onto NS rail for delivery to customers. In addition, during 2023 development was completed and production began at a second underground mine (with an estimated life of 15 years) which produces High-Vol. B quality met coal from the Powellton coal seam. Coal from the mine is currently trucked to and processed through the Mammoth Preparation Plant. Following the expected development of a haul road in 2024, coal is expected to be trucked to and processed through the Power Mountain Preparation Plant.

Elk Run – Elk Run is a mining complex located in Boone County, West Virginia. During 2023, development was completed and production began at an underground mine (with an estimated life of 22 years) which produces High-Vol. B quality met coal from the Powellton coal seam. Coal from the mine is processed at the Chess Processing Plant and loaded onto CSX rail for delivery to customers.

Equipment

Our plant and equipment, including underground and surface equipment, are of varying age, in good operational condition, and are regularly maintained and serviced by a dedicated maintenance workforce and third-party suppliers, including scheduled preventive maintenance.

Preparation Plants, Loadouts, and Docks

The following is a summary of information regarding our active preparation plants as of December 31, 2023:

| Preparation Plant | Year Constructed/Upgraded | Processing Capacity (Tons per hour) | Utilization % | Power Source | ||||||||||||||||||||||

| Bandmill | 2010 | 1,200 | 66% | American Electric Power | ||||||||||||||||||||||

| Kepler | 1967 | 900 | 54% | American Electric Power | ||||||||||||||||||||||

| Kingston | 1974/2001 | 700 | 73% | American Electric Power | ||||||||||||||||||||||

| Marfork | 1994/2019 | 2,400 | 70% | American Electric Power | ||||||||||||||||||||||

| McClure | 1979/2019 | 1,100 | 53% | American Electric Power | ||||||||||||||||||||||

| Toms Creek | 1980/2004 | 1,100 | 43% | American Electric Power | ||||||||||||||||||||||

| Power Mountain | 1985/2010 | 1,200 | 26% | American Electric Power | ||||||||||||||||||||||

Chess Processing (1) | 1980/1998 | 2,200 | N/A | American Electric Power | ||||||||||||||||||||||

| Mammoth | 1950/2008 | 1,200 | 18% | American Electric Power | ||||||||||||||||||||||

(1) Plant refurbished in 2023. Produced tons received during the fourth quarter of 2023 but not processed until the first quarter of 2024.

The following is a summary of information regarding our active loadouts and docks as of December 31, 2023:

9

| Loadout/Dock | Year Constructed | Loading Capacity (Tons per hour) | ||||||||||||

| Pax Loadout | 2006 | 3,500 | ||||||||||||

| Feats Loadout | 1975 | 3,500 | ||||||||||||

| Marmet Dock | 1986 | 1,600 | ||||||||||||

Export Terminal

The following is a summary of information regarding DTA (in which we own a 65% interest) as of December 31, 2023:

Export Terminal | Year Constructed | Loading Capacity (Tons per hour) | Storage Capacity (Net tons) | |||||||||||||||||

| DTA | 1984 | Up to 6,500 | 1.7 million | |||||||||||||||||

Coal Mining Techniques

We use four different mining techniques to extract coal from the ground: room-and-pillar mining, truck-and-shovel mining and truck and front-end loader mining, contour mining, and highwall mining. We do not use mountaintop removal mining and currently have no plans to do so in the future.

Room-and-Pillar Mining

Certain of our mines in CAPP use room-and-pillar mining methods. In this type of mining, main airways and transportation entries are developed and maintained while remote-controlled continuous miners extract coal from the seam, leaving pillars to support the roof. Shuttle cars or battery coal haulers are used to transport coal from the continuous miner to the conveyor belt for transport to the surface. This method is more flexible than longwall mining and often used to mine smaller coal blocks or thinner seams of coal. Ultimate seam recovery of in-place reserves is less than that achieved with longwall mining. All of this production is also processed in preparation plants to remove rock and impurities before it becomes saleable clean coal.

Truck-and-Shovel Mining and Truck and Front-End Loader Mining

We utilize truck/shovel and truck/front-end loader mining methods at some of our CAPP surface mines. These methods are similar and involve using large, electric or hydraulic-powered shovels or diesel-powered front-end loaders to remove earth and rock (overburden) covering a coal seam which is later used to refill the excavated coal pits after the coal is removed. The loading equipment places the coal into trucks for transportation to a preparation plant or loadout area. Ultimate seam recovery of in-place reserves on average exceeds 90%. Depending on geology and market destination, surface-mined coal may need to be processed in a preparation plant before sale. In the case of some metallurgical grade coals, as much as 80% of surface mined coal may need to be processed in a preparation plant to enhance the sales value of the coal. Productivity depends on overburden and coal thickness (strip ratio), equipment utilized and geologic factors.

Contour Mining

We use contour mining at certain of our CAPP surface mines, which limits the overburden removal from above a coal seam or series of coal seams. In contour mining, surface mining machinery follows the contours of a coal seam or seams around a ridge, excavating the overburden and recovering the coal seam or seams as a “contour bench” around the ridge is created. This contour bench is then backfilled and graded in accordance with an approved reclamation plan. Highwall mining methods are used in connection with some contour mining operations. Depending on geology and market destination, coal mined by contour mining may need to be processed in preparation plants to remove rock and impurities before it becomes a saleable clean coal.

Highwall Mining

We utilize highwall mining methods at certain of our CAPP surface mines. A highwall mining system consists of a remotely controlled continuous miner, which extracts coal and conveys it via augers or belt conveyors to the surface. The cut is typically a rectangular, horizontal opening in the highwall (the unexcavated face of exposed overburden and coal in a surface mine) 9-feet or 11-feet wide and reaching depths of up to 1,000 feet. Multiple parallel openings are driven into the highwall, separated by narrow pillars that extend the full depth of the hole. All of the coal mined at our highwall mining operations is processed in preparation plants to remove rock and impurities before it becomes saleable clean coal.

10

Financial Information About Reportable Segments and Geographic Areas

Refer to “Item 7. Management’s Discussion and Analysis of Financial Condition—Results of Operations” and Notes 22 and 23 to the Consolidated Financial Statements for financial information about our reportable segment and geographic areas.

Marketing, Sales and Customer Contracts

We market coal produced at our operations and purchase and resell coal mined by others. We have coal supply commitments with a wide range of steel and coke manufacturers, industrial customers, and electric utilities. Our marketing efforts are centered on meeting customer needs and requirements. By offering coal of various grades, we are able to provide the specific qualities relevant to our customers and to serve a global customer base. Through this global platform, our coals are shipped to customers on five continents. Our broad customer and product base allows us to adjust to changing market conditions. Many of our larger customers are well-established steel manufacturers and public utilities.

Our coal volumes include coal produced and processed by us, our “captive coal,” as well as coal purchased from third-party producers to blend with our produced coal in order to meet customer specifications. These volumes are processed by us, meaning that we washed, crushed or blended the coal at one of our preparation plants or loading facilities prior to resale. Our coal volumes within our Met segment operations also include met coal volumes purchased from domestic third-party producers and sold into international markets.

Our export shipments serviced customers in 25 and 26 countries during the years ended December 31, 2023 and 2022, respectively. Asia was our largest export market for the years ended December 31, 2023 and 2022, with coal sales to Asia accounting for approximately 46% and 53%, respectively of export coal revenues and 34% and 43%, respectively, of coal revenues. All of our sales are conducted in U.S. dollars. Refer to Note 22 to the Consolidated Financial Statements for additional export coal revenue information.

Met coal accounted for approximately 95% of our coal revenues for each of the years ended December 31, 2023 and 2022. Our met coal sales are typically made with customers with whom we have a long-term relationship. Domestic met customers typically enter into one-year agreements with a fixed price for the entire contract year. Any longer-term agreement would generally have a renegotiation of price each subsequent contract year. Export sales are generally made on an annual, quarterly, or spot cargo basis. Annual and quarterly agreements typically have market-indexed pricing that changes with the market monthly. Any export agreement with a term greater than one year would generally have a renegotiation of pricing terms for each subsequent contract year. Volume for future years is generally contingent on both parties agreeing to a pricing mechanism to cover the contract year.

Thermal coal accounted for approximately 5% of our coal revenues for each of the years ended December 31, 2023 and 2022. We sometimes enter into long-term contracts with our thermal coal customers. Terms of these agreements may address coal quality requirements, quantity parameters, flexibility and adjustment mechanisms, permitted sources of supply, treatment of environmental constraints, options to extend, force majeure, suspension, termination and assignment issues, the allocation between the parties of the cost of complying with future governmental regulations and many other matters.

Generally, our long-term thermal coal agreements contain committed volumes and fixed prices for a period or a certain number of periods pursuant to which thermal coal will be delivered under these agreements. After a fixed price period elapses, the long-term agreement may provide for a price negotiation/determination period prior to the commencement of the pending unpriced contract period. The price negotiations generally consider either then current market prices and/or relevant market indices. Provisions of this sort increase the difficulty of predicting the exact prices a coal supplier will receive for its coal during the course of the long-term agreement. During the years ended December 31, 2023 and 2022, approximately 21% and 54%, respectively, of our thermal coal sales volume were delivered pursuant to long-term contracts.

Distribution and Transportation

Coal consumed domestically is usually sold at the mine and transportation costs are normally borne by the purchaser. Export coal is usually sold at the loading port, with purchasers responsible for further transportation.

For our export sales, we negotiate transportation agreements with various providers, including railroads, trucks, barge lines, and terminal facilities to transport shipments to the relevant loading port. We coordinate with customers, mining facilities and transportation providers to establish shipping schedules that meet each customer’s needs. Our captive coal is loaded from our preparation plants, loadout facilities, and in certain cases directly from our mines. The coal we purchase is loaded in some cases directly from mines and preparation plants operated by third parties or from an export terminal. Virtually all of our coal is transported from the mine to our preparation plants by truck or belt conveyor systems. It is transported from preparation plants

11

and loading facilities to the customer by means of railroads, trucks, barge lines, and lake-going and ocean-going vessels from terminal facilities. We depend upon rail, barge, trucking and other systems to deliver coal to markets. In the years ended December 31, 2023 and 2022, our produced coal was transported from the mines and to the customer primarily by rail, with the main rail carriers being CSX Transportation and Norfolk Southern Railway Company. Rail shipments constituted approximately 89% and 84% of total shipments of coal volume from our mines during the years ended December 31, 2023 and 2022, respectively. The balance was shipped from our preparation plants, loadout facilities or mines via truck or barge. Our export sales are primarily shipped to DTA and Pier 6 (Lambert’s Point) shipping ports in the Hampton Roads area of Virginia. We may ship limited export quantities through other U.S. ports when warranted by logistics and economics.

Procurement

Principal goods and services used in our business include mining equipment, replacement parts and materials such as explosives, diesel fuel, tires, conveyance structure, ventilation supplies, lubricants, steel, magnetite and other raw materials, maintenance and repair services, electricity, and roof control and support items. We rely substantially on third-party suppliers to provide mining materials and equipment. Although there continues to be consolidation, which has resulted in a limited number of suppliers for certain types of equipment and supplies, we believe that adequate substitute suppliers are available.

In the first quarter of 2023, we completed a series of transactions to acquire a number of coal trucks and related equipment and facilities to secure trucking services for our operations. In December 2022, we purchased substantially all of the assets of a mining equipment component manufacturing and rebuild business to help secure the supply of certain underground mining equipment parts needed for our operations.

We incur substantial expenses each year to procure goods and services in support of our respective business activities in addition to capital expenditures. We use suppliers for a significant portion of our equipment rebuilds and repairs, as well as construction and reclamation activities.

We have a centralized sourcing group, which sets sourcing policy and strategy focusing primarily on major supplier contract negotiation and administration, including but not limited to the purchase of major capital goods in support of the mining operations. We promote competition between suppliers and seek to develop relationships with suppliers that focus on lowering our costs while improving quality and service. We seek suppliers who identify and concentrate on implementing continuous improvement opportunities within their area of expertise.

Competition

The coal industry is highly competitive, both in the U.S. and internationally. In the met coal market, of the approximately 72.4 million tons produced in the U.S. in 2023, we produced approximately 14.8 million tons, or 20%. A significant portion of U.S. met coal production is shipped internationally, where it competes directly with international sources of production. Approximately 71% of our met coal tons sold were shipped internationally in 2023.

In the thermal market, of the approximately 502.0 million tons produced in the U.S. in 2023, we produced approximately 1.9 million tons, or less than 1%. Only a small portion of overall U.S. thermal production is shipped internationally, but there is strong competition in the domestic market. Approximately 66% of our thermal coal tons sold were shipped internationally in 2023. We compete for U.S. sales with numerous coal producers in the Appalachian region and the Illinois basin, and in some cases with western coal producers.

Demand for met coal and the prices that we are able to obtain for it depend to a large extent on the demand and price for steel in the U.S. and internationally. This demand is influenced by factors beyond our control, including overall economic activity and the availability and relative cost of substitute materials. In the export met coal market, we compete with producers from Australia and Canada and with other international producers on many of the same factors as in the U.S. market. Competition in the export market is also affected by fluctuations in relative foreign exchange rates and costs of inland and ocean transportation, among other factors.

Demand for thermal coal and the prices that we are able to obtain for it are closely linked to coal consumption patterns of the domestic electric generation industry. These coal consumption patterns are influenced by many factors beyond our control, including the demand for electricity, which is significantly dependent upon summer and winter temperatures, and commercial and industrial outputs in the U.S., environmental and other government regulations, technological developments and the location, availability, quality and price of competing sources of power. These competing sources include natural gas, nuclear, fuel oil and increasingly, renewable sources such as solar and wind power. Demand for thermal coal and the prices that we are able to obtain for it are affected by each of the above factors.

12

Human Capital Resources

As of December 31, 2023, we had approximately 4,160 employees, all of which were full-time employees, with 74% of our total workforce being hourly workers. Our employees were almost entirely located in the United States, with three employees located outside the United States. Approximately 97% of our total workforce was union-free as of December 31, 2023. Certain of our subsidiaries have wage agreements with the UMWA representing roughly 3% of our workforce. Certain of our subsidiaries have wage agreements with the UMWA that are subject to termination by either the employer or the UMWA, without cause, on July 31, 2025 and one on February 28, 2026. We strive to maintain positive working relationships with organized labor. Relations with our employees are important to our success, and we believe that we have good relations with our workforce.

As of December 31, 2023, we had approximately 3,900 employees working at our mining operations across Central Appalachia in Virginia and West Virginia, while the remainder of our personnel were employed at our headquarters in Bristol, Tennessee, in Julian, West Virginia, or at other administrative offices throughout the region. As of December 31, 2023, approximately 37% of our total workforce had at least ten years of service with our Company, while approximately 25% had fifteen or more years of service with our Company.

Employee Compensation and Benefits

We require a skilled workforce with mining experience and proficiency as well as qualified managers and supervisors to run our business. In addition, we depend on the experience and industry knowledge of our officers and other key employees to design and execute our business plans. We, along with the mining industry generally, face a shortage of skilled and experienced employees. Therefore, we offer employees competitive compensation and benefits to attract and retain a skilled and qualified workforce. We offer our employees competitive fixed base pay; a bonus incentive program for administrative positions tied to company safety, environmental stewardship, and financial performance; an operations bonus incentive program tied to site-specific safety, environmental stewardship and production goals; retention programs; paid time-off including holidays; a comprehensive benefits package that includes medical, dental, and vision coverage; disability and life insurance coverages; and a 401(k) retirement savings program with an employer match. All employees have access to our Employee Assistance Program (“EAP”) at no cost, which gives them and their family access to licensed professionals for help with mental health, stress, addiction, grievances, relationship issues, childcare and eldercare services, legal and personal finance services and other work/life balance matters. To help retain key employees in certain positions, our long-term incentive program awards cash or equity grants with time-based and performance-based vesting conditions. Certain key employees are also eligible to participate in our non-qualified deferred compensation plan.

Employee Training and Development

At Alpha, we strive to maintain a positive culture where employees can contribute their best work, take pride in doing the right thing, and work to improve and strengthen the organization. To have a successful operation, we endeavor to establish and maintain relationships with and among our employees that are built upon mutual respect, trust, and appreciation.

Due to the industry shortage of skilled and experienced employees, we have an extensive in-house apprentice miner training program. Selected participants are given robust safety and mining training over a six-month period in order to obtain their required miner’s certification. We frequently provide training opportunities for operations employees to obtain certifications for Emergency Medical Technician (“EMT”), Mechanical Engineering Technology (“MET”), foreman and supervisory certifications, and electrical certifications in addition to providing apprentice miner training and supervisor training programs.

In addition to various training programs that we require employees in certain skilled positions to complete, all of our employees are provided with employee handbooks and are expected to follow policies and procedures concerning employment matters at Alpha and our affiliates including, but not limited to: anti-harassment, workplace violence, code of business ethics, drug and alcohol policies, safety policies and vehicle policies.

Employee Safety, Health, and Welfare

Safety is one of our core values and is the foundation for how we manage every aspect of our business. Our employees are empowered with the skills, training, resources, and responsibility to perform their jobs in a safe manner and are accountable for their own safety as well as the safety of their co-workers. Every employee has a voice in the safety process at each of our mines

13

and other operating sites. Our behavior-based safety process empowers employees to engage in the elimination of at-risk behaviors in the workplace and in incident prevention and continuous improvement. In recognition of the interdependence between safety and operations, our “Safe Production” process promotes the effective utilization of procedures, developing safety action plans at each operating group and sharing of best practices, safety alerts and lessons learned across the entire organization.

Safety leadership and training programs are based upon the concepts of situational awareness and observation, changing behaviors and, most importantly, employee involvement. The core elements of our safety training include identification of critical behaviors and the frequency of those behaviors, employee feedback, and removal of barriers for continuous improvement. All employees are empowered to champion the safety process and are challenged to identify hazards and initiate prompt corrective actions. All levels of the organization are expected to be proactive and commit to continuous improvement and implementation of new safety processes that promote a safe and healthy work environment.

In 2023, we achieved an overall Non-fatal days lost (“NFDL”) safety incident rate that was 41% better than the U.S. industry average NFDL safety incident rate per 200,000 hours worked. The industry rate is based on available data for the first three quarters of 2023 and the Alpha rate reflects full year 2023.

Alpha’s mine operations routinely collaborate with academic institutions as well as federal and state agencies to facilitate testing of new concepts and technologies and to utilize them whenever possible to provide the best safety and protection for our employees.

We also believe in taking precautions to avoid incidents and prevent them from occurring. Our Incident Response Plan and Mine Emergency Response Drills have been developed and widely disseminated to appropriate operations and corporate personnel to build the framework for a prompt and coordinated response in the event an incident occurs. Alpha’s award winning mine rescue teams undergo highly specialized training and compete in regional and national mine rescue events to test their skills in first aid, firefighting, mine ventilation, and critical decision-making.

As posted on our Company website, several of our mine operations have been recognized on numerous occasions for outstanding performance and have received several awards in the areas of safety and mine rescue. In 2023, Alpha mine rescue teams won two overall grand champion awards along with several other first-place awards in both overall competition honors and technical category titles.

Refer to Exhibit 95 Mine Safety Disclosure included in this Annual Report on Form 10-K for additional mine safety information.

Legal Proceedings

We could become party to legal proceedings from time to time. These proceedings, as well as governmental examinations, could involve various business units and a variety of claims, including, but not limited to, contract disputes, personal injury claims, property damage claims (including those resulting from blasting, subsidence, trucking and flooding), environmental and safety issues, and employment matters. While some legal matters may specify the damages claimed by the plaintiffs, many seek an unquantified amount of damages. Even when the amount of damages claimed against us or our subsidiaries is stated, (i) the claimed amount may be exaggerated or unsupported; (ii) the claim may be based on a novel legal theory or involve a large number of parties; (iii) there may be uncertainty as to the likelihood of a class being certified or the ultimate size of the class; (iv) there may be uncertainty as to the outcome of pending appeals or motions; and/or (v) there may be significant factual issues to be resolved. As a result, if such legal matters arise in the future, we may be unable to estimate a range of possible loss for matters that have not yet progressed sufficiently through discovery and development of important factual information and legal issues. We record accruals based on an estimate of the ultimate outcome of these matters, but these estimates can be difficult to determine and involve significant judgment. For additional information about the Company’s legal proceedings, refer to Note 21, part (d), to the Consolidated Financial Statements, which is incorporated herein by reference.

14

ENVIRONMENTAL AND OTHER REGULATORY MATTERS

Federal, state and local authorities regulate the U.S. coal mining industry and the industries it serves with respect to matters such as employee health and safety, permitting and licensing requirements, air quality standards, water quality, plant and wildlife protection, the reclamation of mining properties after mining has been completed, the discharge of materials into the environment, surface subsidence from underground mining, and the effects of mining on groundwater quality and availability. These laws and regulations, which are extensive, subject to change, and have tended to become stricter over time, have had, and will continue to have, a significant effect on our production costs and our competitive position relative to certain other sources of electricity generation. Future legislation, regulations or orders, as well as future interpretations and more rigorous enforcement of existing laws, regulations or orders, may require substantial increases in equipment and operating costs to us and delays, interruptions, or a termination of operations, the likelihood or extent of which we cannot predict. In particular, the U.S. Securities and Exchange Commission (“SEC”) continues to work to finalize regulations it proposed in March 2022 intended to standardize climate-related disclosures. We intend to continue to comply with regulatory requirements as they evolve by timely implementing necessary modifications to facilities or operating procedures. Future legislation, regulations, orders or regional or international arrangements, agreements or treaties, as well as efforts by private organizations, including those relating to global climate change, may continue to cause coal to become more heavily regulated.

We endeavor to conduct our mining operations in compliance with all applicable federal, state, and local laws and regulations. We have certain procedures in place that are designed to enable us to comply with these laws and regulations. However, due to the complexity and interpretation of these laws and regulations, we cannot guarantee that we have been or will be at all times in complete compliance, and violations are likely to occur from time to time. None of the violations or the monetary penalties assessed upon us have been material. Future liability under or compliance with environmental and safety requirements could, however, have a material adverse effect on our operations or competitive position. Under some circumstances, substantial fines and penalties, including revocation, denial or suspension of mining permits, may be imposed under the laws described below.

Monetary sanctions, expensive compliance measures and, in severe circumstances, criminal sanctions may be imposed for failure to comply with these laws.

As of December 31, 2023, we had accrued $205.4 million for reclamation liabilities and mine closures, including $38.9 million of current liabilities.

Mining Permits and Approvals

Numerous governmental permits or approvals are required for mining operations pursuant to certain federal, state and local laws applicable to our operations. When we apply for these permits and approvals, we may be required to prepare and present data to federal, state or local authorities pertaining to the effect or impact that any proposed production or processing of coal may have upon the environment and measures we will take to minimize and mitigate those impacts. The requirements imposed by any of these authorities may be costly and time consuming and may delay commencement or continuation of mining operations.

In order to obtain mining permits and approvals from federal and state regulatory authorities, mine operators, including us, must submit a reclamation plan for restoring, upon the completion of mining operations, the mined property to its prior or better condition, productive use or other permitted condition. Typically, we submit the necessary permit applications several months, or even years, before we plan to begin mining a new area. Mining permits generally are approved months or even years after a completed application is submitted. Therefore, we cannot be assured that we will obtain future mining permits in a timely manner.

Permitting requirements also require, under certain circumstances, that we obtain surface owner consent if the surface estate has been severed from the mineral estate. This requires us to negotiate with third parties for surface rights that overlie coal we control or intend to control. These negotiations can be costly and time-consuming, lasting years in some instances, which can create additional delays in the permitting process. If we cannot successfully negotiate for surface rights, we could be denied a permit to mine coal we already control.

On October 4, 2019, the WV Bankruptcy Court entered an order approving the sale by Blackjewel of the Western Assets to ESM. The ESM Transaction occurred on October 18, 2019. We were the former owner of the Western Assets, having sold them to Blackjewel in December 2017 (the “2017 Blackjewel Sale”). As the mine permit transfer process relating to our sale of the Western Assets to Blackjewel had not been completed prior to Blackjewel’s and certain of its affiliates’ filing petitions for relief under chapter 11 of title 11 of the U.S. Code (the “Bankruptcy Code”), we remained the permitholder in good standing for both

15

mines. In connection with ESM’s acquisition of the Western Assets from Blackjewel, on October 18, 2019, we and ESM finalized an agreement that provided, among other items, for the eventual transfer of the Western Asset permits from us to ESM and replacement by ESM of our surety bonds associated with these properties. In furtherance of certain objectives contemplated under that agreement, we and ESM agreed to the merger of two of our now-former subsidiaries, i.e., Contura Coal West, LLC (“CCW”), which held and still holds the Western Asset permits, and Contura Wyoming Land, LLC (“CWL”), with certain entities formed by ESM for purposes of acquiring CCW and CWL. The ESM entities involved in the mergers were ESM Coal West SPV, LLC (“First Merging Entity”) and ESM Wyoming Land SPV, LLC (“Second Merging Entity”). The mergers were consummated effective May 29, 2020, with the First Merging Entity merging with and into CCW, with CCW as the surviving entity (the “First Surviving Entity”), and the Second Merging Entity merging with and into CWL, with CWL as the surviving entity (the “Second Surviving Entity”). Upon the mergers becoming effective, each of the First Surviving Entity and the Second Surviving Entity became wholly-owned subsidiaries of ESM. As such, the Western Asset permits are still held by the same entity, Contura Coal West, LLC, but said entity is no longer a subsidiary of ours, and we no longer have surety bonds associated with these permits and properties.

Surface Mining Control and Reclamation Act

SMCRA, which is administered by the Office of Surface Mining Reclamation and Enforcement (“OSM”), establishes mining, environmental protection, reclamation, and closure standards for all aspects of surface mining as well as many aspects of underground mining that effect surface expressions. Mine operators must obtain SMCRA permits and permit renewals from the OSM or from the applicable state agency if the state agency has obtained primary control of administration and enforcement of the SMCRA program, or primacy. A state agency may obtain primacy if OSM concludes that the state regulatory agency’s mining regulatory program is no less stringent than the federal mining program under SMCRA. States where we have active mining operations have achieved primacy and issue permits in lieu of OSM. OSM maintains oversight of how the states administer their programs.

SMCRA permit provisions include a complex set of requirements which include: coal prospecting; mine plan development; topsoil or growth medium removal, storage and replacement; selective handling of overburden materials; mine pit backfilling and grading; protection of the hydrologic balance, including outside the permit area; subsidence control for underground mines; surface drainage control; mine drainage and mine discharge control and treatment; and re-vegetation and reclamation.

The mining permit application process is initiated by collecting baseline data to adequately characterize the pre-mine environmental condition of the permit area. This work includes, but is not limited to, surveys of cultural and historical resources, soils, vegetation, wildlife, assessment of surface and ground water hydrology, climatology, and wetlands. In conducting this work, we collect geologic data to define and model the soil and rock structures associated with the coal that we will mine. We develop mining and reclamation plans by utilizing this geologic data and incorporating elements of the environmental data. The mining and reclamation plan incorporates the provisions of SMCRA, the state programs, and the complementary environmental programs that affect coal mining. Also included in the permit application are documents defining ownership and agreements pertaining to coal, minerals, oil and gas, water rights, rights of way and surface land, and documents required of the OSM’s Applicant Violator System (“AVS”), including the mining and compliance history of officers, directors and principal owners of the entity.

Regulations under SMCRA and its state analogues provide that a mining permit or modification can, under certain circumstances, be delayed, refused or revoked if we or any entity that owns or controls us or is under common ownership or control with us have unabated permit violations or have been the subject of permit or reclamation bond revocation or suspension. These regulations define certain relationships, such as owning over 50% of stock in an entity or having the authority to determine the manner in which the entity conducts mining operations, as constituting ownership and control. Certain other relationships are presumed to constitute ownership or control, including being an officer or director of an entity or owning between 10% and 50% of the mining operator. This presumption, in some cases, can be rebutted where the person or entity can demonstrate that it in fact does not or did not have authority directly or indirectly to determine the manner in which the relevant coal mining operation is conducted. Thus, past or ongoing violations of federal and state mining laws by us or by coal mining operations owned or controlled by our significant stockholders, directors or officers or certain other third-party affiliates could provide a basis to revoke existing permits and to deny the issuance of additional permits or modifications or amendments of existing permits. This is known as being “permit-blocked.” In recent years, the permitting required for coal mining has been the subject of increasingly stringent regulatory and administrative requirements and extensive litigation by environmental groups.

Once a permit application is prepared and submitted to the regulatory agency, it goes through a completeness review and technical review. Public notice of the proposed permit is given, which also provides for a comment period before a permit can be issued. Some SMCRA mine permits take over a year to prepare, depending on the size and complexity of the mine and may

16

take months or even years to be issued. Regulatory authorities have considerable discretion in the timing of the permit issuance and the public and other agencies have rights to comment on and otherwise engage in the permitting process, including through intervention in the courts.

The Abandoned Mine Land Fund, which is part of SMCRA, requires a fee on all coal produced. The proceeds are used to reclaim mine lands closed or abandoned prior to SMCRA’s adoption in 1977. The current fee, which is effective through September 30, 2034, is $0.224 per ton on surface-mined coal and $0.096 per ton on deep-mined coal. For each of the years ended December 31, 2023 and 2022, we recorded $2.0 million of expense related to these fees.

While SMCRA is a comprehensive statute, SMCRA does not supersede the need for compliance with other major environmental statutes, including the Endangered Species Act; Clean Air Act; Clean Water Act; Resource Conservation and Recovery Act (“RCRA”) and Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA” or “Superfund”).

Surety Bonds

Federal and state laws require us to obtain surety bonds or other approved forms of security to cover the costs of certain long-term obligations, including mine closure or reclamation costs under SMCRA, federal and state workers’ compensation costs, coal leases and other miscellaneous obligations. As of December 31, 2023 and 2022, our posted third-party surety bond amount in all states where we operate was approximately $177.1 million and $165.6 million, respectively, which was used to primarily secure the performance of our reclamation and lease obligations.

Posting of a bond or other security with respect to the performance of reclamation obligations is a condition to the issuance of a permit under SMCRA. Under the terms of agreements we and Alpha Natural Resources, Inc. entered into in connection with the Alpha Natural Resources, Inc. Restructuring, we and Alpha Natural Resources, Inc. were required to replace Alpha Natural Resources, Inc.’s self-bonds with surety bonds, collateralized bonds, or other financial assurance mechanisms, over time and under applicable regulations. Self-bonding may not be available to us as a means to comply with our reclamation bonding obligations for the foreseeable future. In August 2016, OSM announced its decision to pursue a rulemaking to evaluate self-bonding for coal mines, including eligibility standards. OSM has not yet issued a proposed rule to address this issue.

Clean Air Act

The Clean Air Act and comparable state laws that regulate air emissions affect coal mining operations both directly and indirectly. Direct impacts on coal mining and processing operations include Clean Air Act permitting requirements and emission control requirements relating to particulate matter (“PM”), which may include controlling fugitive dust. The Clean Air Act indirectly affects coal mining operations by extensively regulating air emissions of particulate matter, sulfur dioxide, nitrogen oxides, mercury and other compounds emitted by coal-fired electricity generating plants or the use of met coal in connection with steelmaking operations. In recent years, Congress has considered legislation that would require increased reductions in emissions of sulfur dioxide, nitrogen oxide, and mercury. The general effect of emission regulations on coal-fired power plants could be to reduce demand for coal.

In addition to the greenhouse gas (“GHG”) issues discussed below, the air emissions programs that may materially and adversely affect our operations, financial results, liquidity, and demand for coal, directly or indirectly, include, but are not limited to, the following:

•Acid Rain. Title IV of the Clean Air Act requires reductions of sulfur dioxide emissions by electric utilities. Affected electricity generators have sought to meet these requirements by, among other compliance methods, switching to lower sulfur fuels, installing pollution control devices, reducing electricity generating levels or purchasing or trading sulfur dioxide emission allowances. We cannot accurately predict the effect of these provisions of the Clean Air Act on us in future years.

•NAAQS for Criteria Pollutants. The Clean Air Act requires the EPA to set standards, referred to as National Ambient Air Quality Standards (“NAAQS”), for six common air pollutants, including nitrogen oxide, sulfur dioxide, particulate matter, and ozone. Areas that are not in compliance (referred to as “non- attainment areas”) with these standards must take steps to reduce emissions levels. Over the past several years, the EPA has revised its NAAQS for nitrogen oxide, sulfur dioxide, particulate matter and ozone, in each case making the standards more stringent. As a result, some states will be required to amend their existing individual state implementation plans (“SIPs”) to achieve compliance with the new air quality standards. Other states will be required to develop new plans for areas that were previously in “attainment,” but do not meet the revised standards. On December 7, 2020, the EPA announced the agency’s final

17

decision to retain the existing National Ambient Air Quality Standards for particulate matter set by the Obama-Biden Administrations without changes. However, on January 6, 2023, the EPA proposed to revise the primary (health-based) annual standard for PM2.5, from its current level of 12.0 parts per billion (ppb or µg/m3) to within the range of 9.0 to 10.0 µg/m3. The EPA also proposed revisions to some other provisions of the PM NAAQS, including revisions to the air quality index and monitoring requirements, but did not propose to change other key aspects of the standard: (i) the secondary (welfare-based) annual PM2.5 standard; (ii) the primary and secondary 24-hour PM2.5 standards and (iii) the primary and secondary 24-hour PM10 standards. On February 7, 2024, the EPA revised the primary (health-based) annual standard for PM2.5, from its current level of 12.0 µg/m3 to 9.0 µg/m3. The EPA retained the 24-hour standard and the current primary 24-hour standard for PM10, which provides protection against coarse particles. The EPA is not changing the secondary (welfare-based) standards for fine particles and coarse particles at this time.

In October 2015, the EPA finalized the NAAQS for ozone pollution and reduced the limit to 70 ppb from the previous 75 ppb standard. The EPA made the majority of area designations related to this rule on November 16, 2017 and June 4, 2018 and finalized designations for the remaining regions of the country on July 25, 2018. Under the revised NAAQS for ozone in particular, significant additional emissions control expenditures may be required at coal-fired power plants. The final rules and new standards may impose additional emissions control requirements on our customers in the electric generation, steelmaking, and coke industries. Although coal mining and processing operations may emit certain criteria pollutants, we operate in material compliance with our permits. However, our operations could be affected if the attainment status of the areas in which we operate changes in the future.

A suit by industry in the D.C. Circuit challenged the EPA’s 2015 Ozone NAAQS (Murray Energy Corp. v. EPA), which resulted in the court upholding the rule with the exception of the secondary NAAQS standards addressing protection of animals, crops and vegetation, which were sent back to the EPA for further consideration. On December 23, 2020, the EPA announced its decision to retain, without changes, the 2015 ozone National Ambient Air Quality Standards set by the Obama-Biden Administration.

•NOx SIP Call. The NOx SIP Call program was established by the EPA in October of 1998 to reduce the transport of nitrogen oxide and ozone on prevailing winds from the Midwest and South to states in the Northeast, which said they could not meet federal air quality standards because of migrating pollution. The program is designed to reduce nitrogen oxide emissions by one million tons per year in 22 eastern states and the District of Columbia. As a result of the program, many power plants have been or will be required to install additional emission control measures, such as selective catalytic reduction devices. Installation of additional emission control measures will make it more costly to operate coal-fired power plants, potentially making coal a less attractive fuel. On February 26, 2019, the EPA published a final rule amending the NOx SIP Call regulations to allow states to establish alternative monitoring and reporting requirements for certain sources.

On March 15, 2023, the EPA issued its Good Neighbor Plan rules (the “Good Neighbor Plan”), which secure significant reductions in cross-state air pollution of ozone-forming emissions of nitrogen oxides (NOx) from power plants and industrial facilities. The Good Neighbor Plan is intended to reduce seasonal ozone-forming emissions of NOx from power plants and industrial facilities in 23 states. Industry groups and the State of Ohio have filed lawsuits challenging the Good Neighbor Plan. Due to court orders staying implementation of certain aspect of the Good Neighbor Plan, the EPA is implementing the Good Neighbor Plan only in certain states. As of September 21, 2023, the Good Neighbor Plan's “Group 3” ozone-season NOx control program for power plants is being implemented in the following states: Illinois, Indiana, Maryland, Michigan, New Jersey, New York, Ohio, Pennsylvania, Virginia, and Wisconsin. Due to the court orders, the EPA is not currently implementing the Good Neighbor Plan “Group 3” ozone-season NOx control program for power plants in the following states: Alabama, Arkansas, Kentucky, Louisiana, Minnesota, Mississippi, Missouri, Nevada, Oklahoma, Texas, Utah, and West Virginia. On December 20, 2023, the United States Supreme Court agreed to hear oral argument in four consolidated cases challenging the Good Neighbor Plan. The Court has scheduled oral argument for the cases in its February 2024 term and directed the parties to address, among other issues, whether the emissions controls imposed by the Good Neighbor Plan are reasonable regardless of the number of states subject to the Good Neighbor Plan.

•Cross-State Air Pollution Rule. In June 2011, the EPA finalized the CSAPR, which required 28 states in the Midwest and the eastern seaboard of the U.S. to reduce power plant emissions that cross state lines and contribute to ozone and/or fine particle pollution in other states. Nitrogen oxide and sulfur dioxide emission reductions were scheduled to commence in 2012, with further reductions effective in 2014. However, implementation of CSAPR’s requirements were delayed due to litigation. In October 2014, the EPA issued an interim final rule reconciling the CSAPR with the Court’s order, which called for Phase 1 implementation in 2015 and Phase 2 implementation in 2017.

18

In September 2016, the EPA finalized an update to the CSAPR ozone season program by issuing the Final CSAPR Update rule. The Final CSAPR Update rule is the subject of a pending legal challenge in the D.C. Circuit by five states. In September 2019, the D.C. Circuit concluded that the rule was valid in certain respects but that it failed to ensure that pollution from upwind states would not prevent downwind states from meeting air quality standards in a timely manner. The court directed the EPA to revise the rule to address this failure. For states to meet their requirements under the Final CSAPR Update rule, a number of coal-fired electric generating units will likely need to be retired, rather than retrofitted with the necessary emission control technologies, reducing demand for thermal coal. On October 15, 2020, the EPA proposed the Revised CSAPR Update rule in order to fully address 21 states’ outstanding interstate pollution transport obligations for the 2008 ozone National Ambient Air Quality Standards. The EPA finalized the Revised CSAPR Update rule on April 30, 2021. The EPA estimated that the Revised CSAPR Update rule will reduce NOX emissions from power plants in 12 states in the eastern United States by 17,000 tons in 2021 compared to projections without the rule, yielding public health and climate benefits that are valued, on average, at up to $2.8 billion each year from 2021 to 2040. An industry group challenged the Revised CSAPR Update rule in the U.S. Court of Appeals for the District of Columbia. On March 3, 2023, the Court rejected this challenge.

•Mercury and Hazardous Air Pollutants. In February 2012, the EPA formally adopted a rule to regulate emissions of mercury and other metals, fine particulates, and acid gases such as hydrogen chloride from coal- and oil-fired power plants, referred to as “MATS.” In March 2013, the EPA finalized reconsideration of the MATS rule as it pertains to new power plants, principally adjusting emissions limits for new coal-fired units to levels considered attainable by existing control technologies. In subsequent litigation, the U.S. Supreme Court struck down the MATS rule based on the EPA’s failure to take costs into consideration. The D.C. Circuit allowed the current rule to stay in place until the EPA issued a new finding. In April 2016, the EPA issued a final finding that it is appropriate and necessary to set standards for emissions of air toxics from coal- and oil-fired power plants. However, in April 2017, the EPA indicated in a court filing that it may reconsider this finding, and on April 27, 2017, the D.C. Circuit stayed the litigation. In August 2018, the EPA stated that it plans on sending a draft proposal to the White House questioning the EPA’s earlier finding and intends to reevaluate the MATS rule itself.

On December 27, 2018, the EPA issued a proposed revised Supplemental Cost Finding for MATS, as well as the Clean Air Act required “risk and technology review.” After taking account of both the cost to coal- and oil-fired power plants of complying with the MATS rule and the benefits attributable to regulating hazardous air pollutant (“HAP”) emissions from these power plants, the EPA proposed to determine that it is not “appropriate and necessary” to regulate HAP emissions from power plants under Section 112 of the Clean Air Act. The emission standards and other requirements of the MATS rule, first promulgated in 2012, would remain in place, however, since the EPA did not propose to remove coal- and oil-fired power plants from the list of sources that are regulated under Section 112 of the Act.

On April 15, 2020, the EPA established a new subcategory in the MATS for electric utility steam generating units (“EGU’s”) that burn eastern bituminous coal refuse (“EBCR”). Coal refuse includes low-quality coal mixed with rock, clay and other material. The EPA is also establishing emission standards from these facilities. The new subcategory and emission standards will affect six existing EGUs that burn EBCR.

On May 22, 2020, the EPA published the completed reconsideration of the appropriate and necessary finding for the MATS. The EPA concluded that it is not “appropriate and necessary” to regulate electric utility steam generating units under Section 112 of the Clean Air Act. The EPA is also taking final action on the residual risk and technology review that is required by the CAA Section 112. The EPA states, “emissions of HAP have been reduced such that residual risk is at acceptable levels, that there are no developments in HAP emissions controls to achieve further cost-effective reductions beyond the current standard, and, therefore, no changes to the MATS rule are warranted.”

On February 15, 2023, however, the EPA revoked its 2020 finding that it was not appropriate and necessary to regulate coal- and oil-fired power plants under Section 112 of the Clean Air Act, which regulates HAP emissions. The EPA reviewed the 2020 finding and stated that it considered updated information on both (i) the public health burden associated with HAP emissions from coal- and oil-fired power plants; and (ii) the costs associated with reducing those emissions under the MATS rule. On April 3, 2023, the EPA issued a proposed rule that the EPA said would strengthen and update the MATS for power plants to reflect recent developments in control technologies and the performance of these plants.

Apart from MATS, several states have enacted or proposed regulations requiring reductions in mercury emissions from coal-fired power plants, and federal legislation to reduce mercury emissions from power plants has been proposed. Regulation of mercury emissions by the EPA (and in particular, the reconsideration by the current EPA of

19

any rulemaking relating to the MATS rule during the prior presidential administration), states, Congress, or pursuant to an international treaty may further decrease the demand for coal. Like CSAPR, MATS and other similar future regulations could accelerate the retirement of a significant number of coal-fired power plants, in addition to the significant number of plants and units that have already been retired as a result of environmental and regulatory requirements and uncertainties adversely impacting coal-fired generation. Such retirements would likely adversely impact our business.