UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

OR

For the fiscal year ended December 31 , 2022

OR

OR

Date of event requiring this shell company report

For the transition period from ________________ to ________________

Commission file number: 001-35129

(Exact name of Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Chief Legal Officer

Arcos Dorados Holdings Inc.

Telephone: +598 2626-3000

Fax: +598 2626-3018

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close of the period covered by the annual report.

Class A shares: 130,594,545

Class B shares: 80,000,000

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes o No x

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

x | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Emerging growth company | ||||||||||||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

x | International Financial Reporting Standards as issued by the International Accounting Standards Board | o | Other | o | |||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No x

ARCOS DORADOS HOLDINGS INC.

TABLE OF CONTENTS

| Page | |||||

i

ii

iii

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

All references to “U.S. dollars,” “dollars,” “U.S.$” or “$” are to the U.S. dollar. All references to “Argentine pesos” or “ARS$” are to the Argentine peso. All references to “Brazilian reais” or “R$” are to the Brazilian real. All references to “Mexican pesos” or “Ps.” are to the Mexican peso. All references to “Chilean pesos” or “CLPs.” are to the Chilean peso. All references to “Venezuelan bolívares” or “Bs.” are to the Venezuelan bolívar, the legal currency of Venezuela. See “Item 3. Key Information—A. Selected Financial Data—Exchange Rates and Exchange Controls” for information regarding exchange rates for the Argentine, Brazilian, Mexican and Chilean currencies.

Definitions

In this annual report, unless the context otherwise requires, all references to “Arcos Dorados,” the “Company,” “we,” “our,” “ours,” “us” or similar terms refer to Arcos Dorados Holdings Inc., together with its subsidiaries. All references to “systemwide” refer only to the system of McDonald’s-branded restaurants operated by us or our sub-franchisees in 20 countries and territories in Latin America and the Caribbean, including Argentina, Aruba, Brazil, Chile, Colombia, Costa Rica, Curaçao, Ecuador, French Guiana, Guadeloupe, Martinique, Mexico, Panama, Peru, Puerto Rico, Trinidad and Tobago, Uruguay, the U.S. Virgin Islands of St. Croix and St. Thomas, and Venezuela, which we refer to as the “Territories,” and do not refer to the system of McDonald’s-branded restaurants operated by McDonald’s Corporation, its affiliates or its franchisees (other than us).

We own our McDonald’s franchise rights pursuant to a Master Franchise Agreement for all of the Territories, except Brazil, which we refer to as the “MFA,” and a separate, but substantially identical, Master Franchise Agreement for Brazil, which we refer to as the “Brazilian MFA.” We refer to the MFA and the Brazilian MFA, as amended or otherwise modified to date, collectively as the “MFAs.” We commenced operations on August 3, 2007, as a result of our purchase of McDonald’s operations and real estate in the Territories (except for Trinidad and Tobago), which we refer to collectively as the “McDonald’s LatAm” business, and the acquisition of McDonald’s franchise rights pursuant to the MFAs, which together with the purchase of the McDonald’s LatAm business, we refer to as the “Acquisition.”

Financial Statements

We prepare our financial statements in accordance with accounting principles and standards generally accepted in the United States, or U.S. GAAP, and elect to report in U.S. dollars.

The financial information contained in this annual report includes our consolidated financial statements at December 31, 2022 and 2021 and for the years ended December 31, 2022, 2021 and 2020, which have been audited by Pistrelli, Henry Martin y Asociados S.R.L., member Firm of Ernst & Young Global, as stated in their report included elsewhere in this annual report.

Our fiscal year ends on December 31. References in this annual report to a fiscal year, such as “fiscal year 2022,” relate to our fiscal year ended on December 31 of that calendar year.

Operating Data

Effective October 1, 2021, the Company made certain changes in its internal management structure in order to gain operational agility. As a result, the Company also reorganized its operations from four geographic divisions to three geographic divisions, as follows: (i) Brazil, (ii) the North Latin American division, or “NOLAD,” consisting of Costa Rica, Mexico, Panama, Puerto Rico, Martinique, Guadeloupe, French Guiana and the U.S. Virgin Islands of St. Croix and St. Thomas, and (iii) the South Latin American division, or “SLAD,” consisting of Argentina, Chile, Ecuador, Peru, Uruguay, Colombia, Venezuela, Trinidad and Tobago, Aruba and Curaçao. For more information see “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Segment Presentation.”

We operate McDonald’s-branded restaurants under two different operating formats: those directly operated by us, or “Company-operated” restaurants, and those operated by sub-franchisees, or “franchised” restaurants. All references to “restaurants” are to our freestanding, food court, in-store and mall store restaurants and do not refer to our McCafé locations or Dessert Centers. Systemwide data represents measures for both our Company-operated restaurants and our franchised restaurants.

iv

We are the majority stakeholder in two joint ventures with third parties that collectively own 16 restaurants in Argentina and Chile. We consider these restaurants to be Company-operated restaurants. We also have granted developmental licenses to 7 restaurants. Developmental licensees own or lease the land and buildings on which their restaurants are located and pay a franchise fee to us in addition to the continuing franchise fee due to McDonald’s. We consider these restaurants to be franchised restaurants. Additionally, in November 2021, a joint venture was formed with a Mexican sub-franchisee in which the Company is a minority stakeholder. We consider these restaurants to be franchised restaurants. The Company’s joint ventures in Argentina, Chile and Mexico operate as a joint venture under the traditional definition used within the McDonald’s system for such business arrangements. For purposes of this annual report, a joint venture is an entity that operates certain restaurants in the Company’s territory in which the Company is a stakeholder together with a third party. This third party is always a sub-franchisee of the Company. Although in most joint ventures the Company exercises control or significant influence over the entity’s operating and financial policies, the third party is responsible for the day-to-day operation of the entity’s restaurants. Restaurants operated by entities in which the Company has a majority stake are considered to be Company-operated; whereas, entities in which the Company holds a minority stake are considered to be franchised.

Market Share and Other Information

Market data and certain industry forecast data used in this annual report were obtained from internal reports and studies, where appropriate, as well as estimates, market research, publicly available information (including information available from the United States Securities and Exchange Commission, or the “SEC,” website) and industry publications, including the United Nations Economic Commission for Latin America and the Caribbean and the CIA World Factbook. Industry publications generally state that the information they include has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Similarly, internal reports and studies, estimates and market research, which we believe to be reliable and accurately extracted by us for use in this annual report, have not been independently verified. However, we believe such data is accurate and agree that we are responsible for the accurate extraction of such information from such sources and its correct reproduction in this annual report.

Basis of Consolidation

The accompanying consolidated financial statements have been prepared on the accrual basis of accounting and include the accounts of the Company and its subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

Rounding

We have made rounding adjustments to some of the figures included in this annual report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

v

FORWARD-LOOKING STATEMENTS

This annual report contains statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Many of the forward-looking statements contained in this annual report can be identified by the use of forward-looking words such as “aim,” “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate” and “potential,” among others.

Forward-looking statements appear in a number of places in this annual report and include, but are not limited to, statements regarding our intent, belief or current expectations. Forward-looking statements are based on our management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to various factors, including, but not limited to, those identified in “Item 3. Key Information—D. Risk Factors” in this annual report. These risks and uncertainties include factors relating to:

•general economic, political, social, demographic and business conditions in Latin America and the Caribbean;

•fluctuations in inflation, interest rates and exchange rates in Latin America and the Caribbean;

•our ability to implement our growth strategy;

•the success of operating initiatives, including advertising and promotional efforts and new product and concept development by us and our competitors;

•our ability to compete and conduct our business in the future;

•unforeseen events, such as disruptions, natural disasters, adverse weather conditions, war, such as the Russia-Ukraine war, pandemics and other catastrophic events;

•changes in consumer tastes and preferences, including changes resulting from concerns over nutritional or safety aspects of beef, poultry, french fries or other foods or the effects of pandemics or food-borne illnesses, such as COVID-19, bovine spongiform encephalopathy disease and avian influenza or “bird flu,” climate change, and changes in spending patterns and demographic trends, such as the extent to which consumers eat meals away from home;

•the availability, location and lease terms for restaurant development;

•our sub-franchisees, including their business and financial viability and the timely payment of our sub-franchisees’ obligations due to us and to McDonald’s;

•our ability to comply with the requirements of the MFAs, including McDonald’s standards;

•our decision to own and operate restaurants or to operate under franchise agreements;

•the availability of qualified restaurant personnel for us and for our sub-franchisees, and the ability to retain such personnel;

•changes in commodity costs, labor, supply, fuel, utilities, distribution and other operating costs;

•changes in labor laws;

•our ability, if necessary, to secure alternative distribution of supplies of food, equipment and other products to our restaurants at competitive rates and in adequate amounts, and the potential financial impact of any interruptions in such distribution;

•material changes in government regulation;

•material changes in tax legislation;

•climate change manifesting as physical or transition risks;

vi

•climate-related conditions, regulations, targets and weather events;

•changes in our liquidity or the availability of lines of credit and other sources of financing;

•other factors that may affect our financial condition, liquidity and results of operations; and

•other risk factors discussed under “Item 3. Key Information—D. Risk Factors.”

Forward-looking statements speak only as of the date they are made, and we do not undertake any obligation to update them in light of new information or future developments or to release publicly any revisions to these statements in order to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

ENFORCEMENT OF JUDGMENTS

We are incorporated under the laws of the British Virgin Islands with limited liability. We are incorporated in the British Virgin Islands because of certain benefits associated with being a British Virgin Islands company, such as political and economic stability, an effective judicial system, a favorable tax system, the absence of exchange control or currency restrictions, and the availability of professional and support services. However, the British Virgin Islands has a less developed body of securities laws as compared to the United States and provides protections for investors to a significantly lesser extent. In addition, British Virgin Islands companies may not have standing to sue before the federal courts of the United States.

A majority of our directors and officers, as well as certain of the experts named herein, reside outside of the United States. A substantial portion of our assets and several of such directors, officers and experts are located principally in Argentina, Brazil and Uruguay. As a result, it may not be possible for investors to effect service of process outside Argentina, Brazil and Uruguay upon such directors or officers, or to enforce against us or such parties in courts outside Argentina, Brazil and Uruguay judgments predicated solely upon the civil liability provisions of the federal securities laws of the United States or other non-Argentine, Brazilian or Uruguayan regulations, as applicable. In addition, local counsel to the Company have advised that there is doubt as to whether the courts of Argentina, Brazil or Uruguay would enforce in all respects, to the same extent and in as timely a manner as a U.S. court or non-Argentine, Brazilian or Uruguayan court, an original action predicated solely upon the civil liability provisions of the U.S. federal securities laws or other non-Argentine, Brazilian or Uruguayan regulations, as applicable; and that the enforceability in Argentine, Brazilian or Uruguayan courts of judgments of U.S. courts or non-Argentine, Brazilian or Uruguayan courts predicated upon the civil liability provisions of the U.S. federal securities laws or other non-Argentine, Brazilian or Uruguayan regulations, as applicable, will be subject to compliance with certain requirements under Argentine, Brazilian or Uruguayan law, including the condition that any such judgment does not violate Argentine, Brazilian or Uruguayan public policy.

We have been advised by Maples and Calder, our counsel as to British Virgin Islands law, that the United States and the British Virgin Islands do not have a treaty providing for reciprocal recognition and enforcement of judgments of courts of the United States in civil and commercial matters and that a final judgment for the payment of money rendered by any general or state court in the United States based on civil liability, whether or not predicated solely upon the U.S. federal securities laws, would not be automatically enforceable in the British Virgin Islands. We have been advised by Maples and Calder that a final and conclusive judgment obtained in U.S. federal or state courts under which a sum of money is payable (i.e., not being a sum claimed by a revenue authority for taxes or other charges of a similar nature by a governmental authority, or in respect of a fine or penalty or multiple or punitive damages) may be the subject of an action on a debt in the court of the British Virgin Islands under British Virgin Islands common law.

vii

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

A. Directors and Senior Management

Not applicable.

B. Advisers

Not applicable.

C. Auditors

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

A. Offer Statistics

Not applicable.

B. Method and Expected Timetable

Not applicable.

1

ITEM 3. KEY INFORMATION

A. Selected Financial Data

The selected balance sheet data as of December 31, 2022 and 2021 and the income statement data for the years ended December 31, 2022, 2021 and 2020 of Arcos Dorados Holdings Inc. are derived from the consolidated financial statements included elsewhere in this annual report, which have been audited by Pistrelli, Henry Martin y Asociados S.R.L., member firm of Ernst & Young Global.

Effective October 1, 2021, the Company made certain changes in its internal management structure in order to gain operational agility. As a result, the Company also reorganized its operations from four geographic divisions to three geographic divisions, as follows: (i) Brazil (ii) NOLAD, which now consists of Costa Rica, Mexico, Panama, Puerto Rico, Martinique, Guadeloupe, French Guiana and the U.S. Virgin Islands of St. Croix and St. Thomas and (iii) SLAD, which now consists of Argentina, Chile, Ecuador, Peru, Uruguay, Colombia, Venezuela, Trinidad and Tobago, Aruba and Curaçao. In accordance with ASC 280 Segment Reporting, the Company began providing information with the revised structure of geographic divisions in the annual period ended December 31, 2021 and has restated its comparative segment information as of and for the years ended December 31, 2020 and 2019 based on the structure prevailing since October 1, 2021.

We were incorporated on December 9, 2010 as a direct, wholly-owned subsidiary of Arcos Dorados Limited, the prior holding company for the Arcos Dorados business. On December 13, 2010, Arcos Dorados Limited effected a downstream merger into and with us, with us as the surviving entity. The merger was accounted for as a reorganization of entities under common control in a manner similar to a pooling of interest and the consolidated financial statements reflect the historical consolidated operations of Arcos Dorados Limited as if the reorganization structure had existed since Arcos Dorados Limited was incorporated in July 2006. We did not commence operations until the Acquisition on August 3, 2007.

We prepare our financial statements in accordance with accounting principles and standards generally accepted in the United States, or U.S. GAAP, and elect to report in U.S. dollars. This financial information should be read in conjunction with “Presentation of Financial and Other Information,” “Item 5. Operating and Financial Review and Prospects” and our consolidated financial statements, including the notes thereto, included elsewhere in this annual report.

2

For the Years Ended December 31, | |||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||

(in thousands of U.S. dollars, except for per share data) | |||||||||||||||||||||||||||||||||||

| Income (Loss) Statement Data: | |||||||||||||||||||||||||||||||||||

| Sales by Company-operated restaurants | $ | 3,457,491 | $ | 2,543,907 | $ | 1,894,618 | |||||||||||||||||||||||||||||

| Revenues from franchised restaurants | 161,411 | 116,034 | 89,601 | ||||||||||||||||||||||||||||||||

| Total revenues | 3,618,902 | 2,659,941 | 1,984,219 | ||||||||||||||||||||||||||||||||

| Company-operated restaurant expenses: | |||||||||||||||||||||||||||||||||||

| Food and paper | (1,227,293) | (899,077) | (677,087) | ||||||||||||||||||||||||||||||||

| Payroll and employee benefits | (668,764) | (482,608) | (413,074) | ||||||||||||||||||||||||||||||||

| Occupancy and other operating expenses | (967,690) | (772,169) | (624,154) | ||||||||||||||||||||||||||||||||

| Royalty fees | (194,522) | (131,401) | (110,957) | ||||||||||||||||||||||||||||||||

| Franchised restaurants—occupancy expenses | (68,028) | (50,627) | (43,512) | ||||||||||||||||||||||||||||||||

| General and administrative expenses | (239,263) | (210,909) | (171,382) | ||||||||||||||||||||||||||||||||

| Other operating income (expenses), net | 11,080 | 26,369 | (10,807) | ||||||||||||||||||||||||||||||||

| Total operating costs and expenses | (3,354,480) | (2,520,422) | (2,050,973) | ||||||||||||||||||||||||||||||||

| Operating income (loss) | 264,422 | 139,519 | (66,754) | ||||||||||||||||||||||||||||||||

| Net interest expense and other financing results | (43,750) | (49,546) | (33,392) | ||||||||||||||||||||||||||||||||

| Loss from derivative instruments | (10,490) | (5,183) | (2,297) | ||||||||||||||||||||||||||||||||

| Foreign currency exchange results | 16,501 | (9,189) | (31,707) | ||||||||||||||||||||||||||||||||

| Other non-operating (expenses) income, net | (287) | 2,185 | 2,296 | ||||||||||||||||||||||||||||||||

| Income (loss) before income taxes | 226,396 | 77,786 | (131,854) | ||||||||||||||||||||||||||||||||

| Income tax expense | (85,476) | (31,933) | (17,532) | ||||||||||||||||||||||||||||||||

| Net income (loss) | 140,920 | 45,853 | (149,386) | ||||||||||||||||||||||||||||||||

| Less: Net income attributable to non-controlling interests | (577) | (367) | (65) | ||||||||||||||||||||||||||||||||

| Net income (loss) attributable to Arcos Dorados Holdings Inc. | $ | 140,343 | $ | 45,486 | $ | (149,451) | |||||||||||||||||||||||||||||

| Earnings per share: | |||||||||||||||||||||||||||||||||||

| Basic net income (loss) per common share attributable to Arcos Dorados | $ | 0.67 | $ | 0.22 | $ | (0.72) | |||||||||||||||||||||||||||||

| Diluted net income (loss) per common share attributable to Arcos Dorados | $ | 0.67 | $ | 0.22 | $ | (0.72) | |||||||||||||||||||||||||||||

3

As of December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(in thousands of U.S. dollars, except for share data) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance Sheet Data: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash and cash equivalent | $ | 266,937 | $ | 278,830 | $ | 165,989 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total current assets | 684,363 | 540,116 | 415,531 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Property and equipment, net | 856,085 | 743,533 | 796,532 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total non-current assets | 1,952,267 | 1,821,141 | 1,878,423 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total assets | 2,636,630 | 2,361,257 | 2,293,954 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts payable | 353,468 | 269,215 | 209,535 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Short-term debt and current portion of long-term debt | 19,351 | 4,741 | 3,129 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total current liabilities | 759,412 | 617,863 | 503,471 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Long-term debt, excluding current portion | 711,671 | 739,217 | 773,445 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total non-current liabilities | 1,552,791 | 1,522,232 | 1,592,467 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total liabilities | 2,312,203 | 2,140,095 | 2,095,938 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total common stock | 522,308 | 521,284 | 519,518 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total equity | 324,427 | 221,162 | 198,016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total liabilities and equity | 2,636,630 | 2,361,257 | 2,293,954 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares outstanding | 210,594,545 | 210,478,322 | 207,265,773 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

4

For the Years Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(in thousands of U.S. dollars, except percentages) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other Data: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Revenues | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Brazil | $ | 1,429,105 | $ | 1,002,781 | $ | 862,748 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NOLAD | 920,189 | 780,866 | 584,646 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SLAD | 1,269,608 | 876,294 | 536,825 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | 3,618,902 | $ | 2,659,941 | $ | 1,984,219 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Income (Loss) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Brazil | $ | 186,862 | $ | 117,887 | $ | 16,121 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NOLAD | 61,832 | 48,785 | 30 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SLAD | 107,520 | 48,614 | (28,842) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate and others and purchase price allocation | (91,792) | (75,767) | (54,063) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | 264,422 | $ | 139,519 | $ | (66,754) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Margin(1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Brazil | 13.1 | % | 11.8 | % | 1.9 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NOLAD | 6.7 | 6.2 | 0.0 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SLAD | 8.5 | 5.5 | (5.4) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | 7.3 | % | 5.2 | % | (3.4) | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Adjusted EBITDA(2) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Brazil | $ | 242,346 | $ | 175,603 | $ | 76,155 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NOLAD | 95,290 | 85,323 | 41,496 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SLAD | 134,253 | 77,573 | 830 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate and others | (85,325) | (66,741) | (50,370) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | 386,564 | $ | 271,758 | $ | 68,111 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Adjusted EBITDA Margin(3) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Brazil | 17.0 | % | 17.5 | % | 8.8 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NOLAD | 10.4 | 10.9 | 7.1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SLAD | 10.6 | 8.9 | 0.2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | 10.7 | % | 10.2 | % | 3.4 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other Financial Data: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Working capital(4) | (75,049) | (77,747) | (87,940) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital expenditures(5) | 221,915 | 115,077 | 90,144 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash Dividends declared per common share | $ | 0.15 | $ | — | $ | 0.05 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock Dividends declared per every 70 common shares | — | 1.00 | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stock Dividends declared per every 75 common shares | — | — | 1.00 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

5

As of December 31, | ||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | ||||||||||||||||||||||||

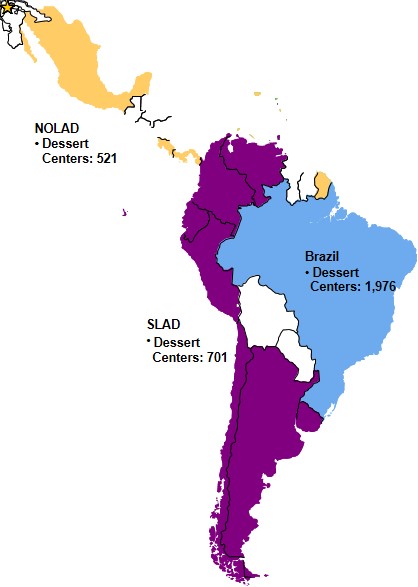

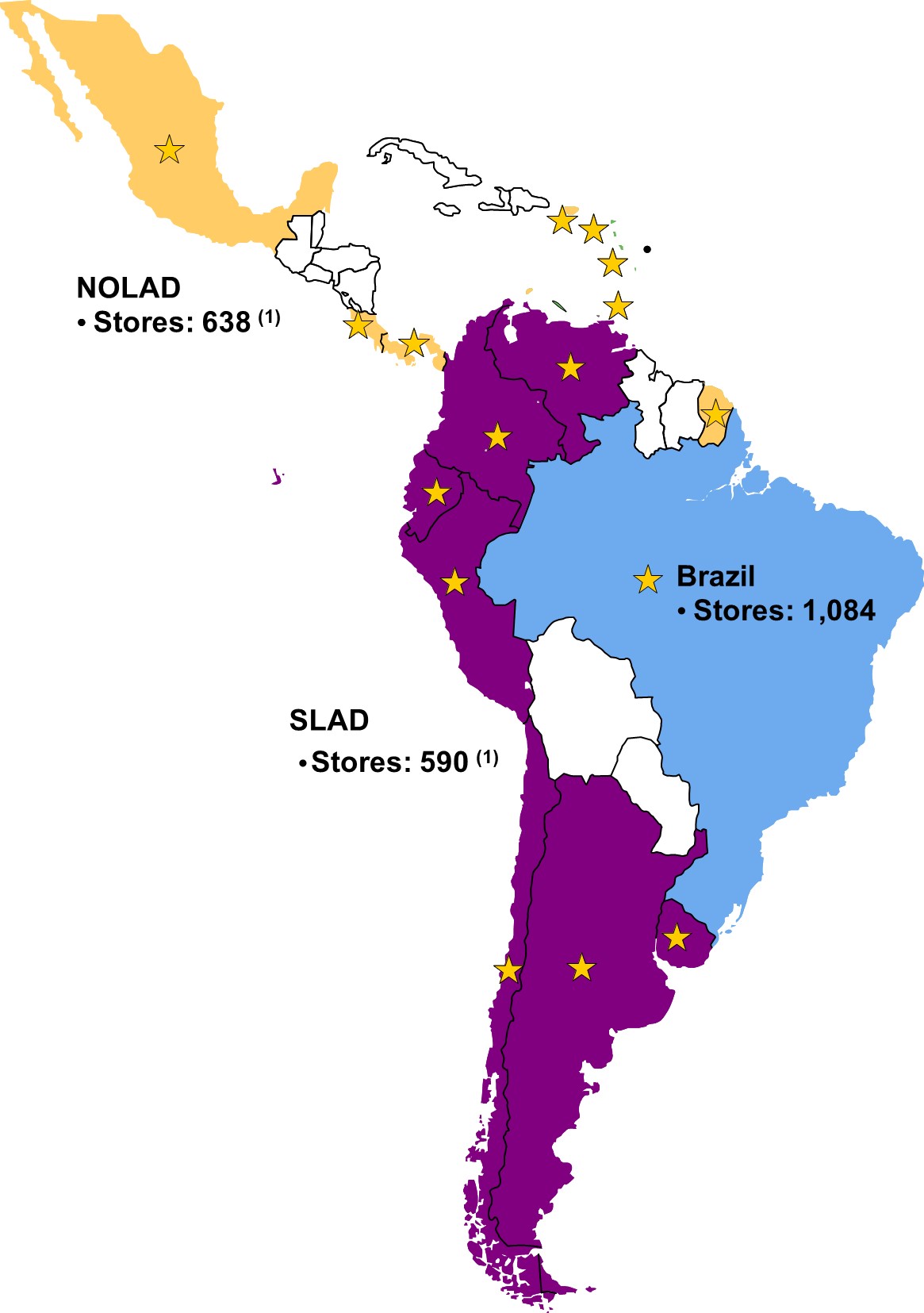

| Number of systemwide restaurants(6) | 2,312 | 2,261 | 2,236 | |||||||||||||||||||||||

| Brazil | 1,084 | 1,051 | 1,020 | |||||||||||||||||||||||

| NOLAD | 638 | 625 | 629 | |||||||||||||||||||||||

| SLAD | 590 | 585 | 587 | |||||||||||||||||||||||

| Number of Company-operated restaurants | 1,633 | 1,579 | 1,576 | |||||||||||||||||||||||

| Brazil | 656 | 631 | 610 | |||||||||||||||||||||||

| NOLAD | 473 | 453 | 475 | |||||||||||||||||||||||

| SLAD | 504 | 495 | 491 | |||||||||||||||||||||||

| Number of franchised restaurants | 679 | 682 | 660 | |||||||||||||||||||||||

| Brazil | 428 | 420 | 410 | |||||||||||||||||||||||

| NOLAD | 165 | 172 | 154 | |||||||||||||||||||||||

| SLAD | 86 | 90 | 96 | |||||||||||||||||||||||

(1)Operating margin is operating income (loss) divided by total revenues, expressed as a percentage.

(2)Adjusted EBITDA is a measure of our performance that is reviewed by our management. Adjusted EBITDA does not have a standardized meaning and, accordingly, our definition of Adjusted EBITDA may not be comparable to Adjusted EBITDA as used by other companies. Total Adjusted EBITDA is a non-GAAP measure. For our definition of Adjusted EBITDA, see “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Key Business Measures.”

(3)Adjusted EBITDA margin is Adjusted EBITDA divided by total revenues, expressed as a percentage.

(4)Working capital equals current assets minus current liabilities.

(5)Includes property and equipment expenditures and purchase of restaurant businesses paid at the acquisition date.

(6)Includes both traditional restaurants and satellite non-traditional restaurants. We define non-traditional satellite restaurants as those points of distribution that have one or more of the following characteristics: (i) depend on another of our restaurants, (ii) offer a limited menu of products, (iii) have approximately 30% of the size of our average restaurants (other than McCafe or other satellites), (iv) generate approximately 50% of the gross sales of our average restaurants (other than McCafe or other satellites), or (v) are located inside a Wal-Mart.

6

Presented below is the reconciliation between net income and Adjusted EBITDA on a consolidated basis:

Consolidated Adjusted EBITDA Reconciliation | For the Years Ended December 31, | ||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||

(in thousands of U.S. dollars) | |||||||||||||||||||||||||||||||||||

| Net income (loss) attributable to Arcos Dorados Holdings Inc. | $ | 140,343 | $ | 45,486 | $ | (149,451) | |||||||||||||||||||||||||||||

| Plus (Less): | |||||||||||||||||||||||||||||||||||

| Net interest expense and other financing results | 43,750 | 49,546 | 33,392 | ||||||||||||||||||||||||||||||||

| Loss from derivative instruments | 10,490 | 5,183 | 2,297 | ||||||||||||||||||||||||||||||||

| Foreign currency exchange results | (16,501) | 9,189 | 31,707 | ||||||||||||||||||||||||||||||||

| Other non-operating expenses (income), net | 287 | (2,185) | (2,296) | ||||||||||||||||||||||||||||||||

| Income tax expense | 85,476 | 31,933 | 17,532 | ||||||||||||||||||||||||||||||||

| Net income attributable to non-controlling interests | 577 | 367 | 65 | ||||||||||||||||||||||||||||||||

| Operating income (loss) | 264,422 | 139,519 | (66,754) | ||||||||||||||||||||||||||||||||

| Plus (Less): | |||||||||||||||||||||||||||||||||||

| Items excluded from computation that affect operating income: | |||||||||||||||||||||||||||||||||||

| Depreciation and amortization | 119,777 | 120,394 | 126,853 | ||||||||||||||||||||||||||||||||

| Gains from sale, insurance recovery and contribution in equity method investments of property and equipment | (1,949) | (4,876) | (4,210) | ||||||||||||||||||||||||||||||||

| Write-offs of property and equipment | 3,143 | 3,094 | 4,501 | ||||||||||||||||||||||||||||||||

| Impairment of long-lived assets | 1,171 | 1,573 | 6,636 | ||||||||||||||||||||||||||||||||

| Impairment of goodwill | — | — | 1,085 | ||||||||||||||||||||||||||||||||

| Reorganization and optimization plan | — | 12,054 | — | ||||||||||||||||||||||||||||||||

| Adjusted EBITDA | 386,564 | 271,758 | 68,111 | ||||||||||||||||||||||||||||||||

Exchange Rates and Exchange Controls

In 2022, 71.1% of our total revenues were derived from our restaurants in Brazil, Argentina, Mexico and Chile. While we elect to report figures in U.S. dollars, our revenues are conducted in the local currency of the territories in which we operate, and as such may be affected by changes in the local exchange rate to the U.S. dollar. The exchange rates discussed in this section have been obtained from each country’s central bank. However, in most cases, for consolidation purposes, we use a foreign currency to U.S. dollar exchange rate provided by Bloomberg that differs slightly from that reported by the aforementioned central banks.

Brazil

Exchange Rates

The Brazilian real depreciated 29% against the U.S. dollar in 2020, depreciated 7.4% in 2021, appreciated 5.3% in 2022 and appreciated 4.1% in the first quarter of 2023. As of April 26, 2023, the exchange rate for the purchase of U.S. dollars was R$5.05 per U.S. dollar.

Exchange Controls

Brazilian Resolution 3,568 establishes that, without prejudice to the duty of identifying customers, operations of foreign currency purchase or sale up to $3,000 or its equivalent in other currencies are not required to submit documentation relating to legal transactions underlying these foreign exchange operations. According to Resolution 3,568, the Central Bank of Brazil may define simplified forms to record operations of foreign currency purchases and sales of up to $3,000 or its equivalent in other currencies.

7

The Brazilian Monetary Council may issue further regulations in relation to foreign exchange transactions, as well as on payments and transfers of Brazilian currency between Brazilian residents and non-residents (such transfers being commonly known as the international transfer of reais), including those made through so-called non-resident accounts.

Brazilian law also imposes a tax on foreign exchange transactions, or “IOF/Exchange,” on the conversion of reais into foreign currency and on the conversion of foreign currency into reais. As of October 7, 2014, the general IOF/Exchange rate applicable to almost all foreign currency exchange transactions was increased from zero to 0.38%, although other rates may apply in particular operations, such as the below transactions which are currently not taxed:

•inflow related to transactions carried out in the Brazilian financial and capital markets, including investments in our common shares by investors which register their investment under Resolution No. 4,373;

•outflow related to the return of the investment mentioned under the first bulleted item above; and

•outflow related to the payment of dividends and interest on shareholders’ equity in connection with the investment mentioned under the first bulleted item above.

Notwithstanding these rates of the IOF/Exchange, in force as of the date hereof, the Minister of Finance is legally entitled to increase the rate of the IOF/Exchange to a maximum of 25% of the amount of the currency exchange transaction, but only on a prospective basis.

Although the Central Bank of Brazil has intervened occasionally to control movements in the foreign exchange rates, the exchange market may continue to be volatile as a result of capital movements or other factors, and, therefore, the Brazilian real may substantially decline or appreciate in value in relation to the U.S. dollar in the future.

Brazilian law further provides that whenever there is a significant imbalance in Brazil’s balance of payments or reasons to foresee such a significant imbalance, the Brazilian government may, and has done so in the past, impose temporary restrictions on the remittance of funds to foreign investors of the proceeds of their investments in Brazil. The likelihood that the Brazilian government would impose such restricting measures may be affected by the extent of Brazil’s foreign currency reserves, the availability of foreign currency in the foreign exchange markets on the date a payment is due, the size of Brazil’s debt service burden relative to the economy as a whole and other factors. We cannot assure you that the Central Bank of Brazil will not modify its policies or that the Brazilian government will not institute restrictions or delays on cross-border remittances in respect of securities issued in the international capital markets.

Argentina

Exchange Rates

The Argentine peso depreciated 40.5% against the U.S. dollar in 2020, depreciated 22.1% in 2021, depreciated 72.4% in 2022 and depreciated 18.0% in the first quarter of 2023. As of April 26, 2023, the exchange rate for the purchase of U.S. dollars was ARS$221.55 per U.S. dollar.

Exchange Controls

Since 2019, Argentina has had currency controls in place that tightened restrictions on capital flows, exchange controls, the official U.S. dollar exchange rate and transfers that substantially limit the ability of companies to retain foreign currency or make payments abroad.

By means of Decree No. 609/2019, as amended, the Argentine government reinstated foreign exchange controls and authorized the Central Bank of Argentina to (a) regulate access to the foreign exchange market (Mercado Libre de Cambios or “MLC”) for the purchase of foreign currency and outward remittances; and (b) set forth regulations to avoid practices and transactions aimed to circumvent the measures adopted through the decree. As a consequence of these exchange controls, the spread between the official exchange rate and other exchange rates implicitly resulting from certain capital market operations usually effected to obtain U.S. dollars has broadened significantly, reaching a value of approximately 101.5% above the official exchange rate as of April 26, 2023.

At present, foreign exchange regulations have been (i) extended indefinitely, and (ii) consolidated in a single set of regulations, Communication “A” 7490, as subsequently amended and supplemented from time to time by the Central Bank of Argentina’s communications (jointly, the “Argentine FX Regulations”). Below is a description of the main exchange control measures implemented through the aforementioned regulations:

8

Specific provisions for inward remittances

Obligation to repatriate and settle in Argentine pesos the proceeds from exports of services

Section 2.2 of the Argentine FX Regulations imposes the obligation on exporters to repatriate, and exchange into Argentine pesos through the MLC, the proceeds from services rendered to non-residents within 5 business days following payment thereof.

Sale of non-financial non-produced assets

Pursuant to section 2.3 of the Argentine FX Regulations, the proceeds in foreign currency of the sale to non-residents of non-financial non-produced assets must be repatriated and settled in Argentine pesos in the MLC within 5 business days following either the perception of funds in the country or abroad, or their accreditation in foreign accounts.

External financial indebtedness

Pursuant to section 2.4 of the Argentine FX Regulations, the new regulations have reinstated the requirement to repatriate, and exchange into Argentine pesos through the MLC, the proceeds of new financial indebtedness disbursed as of September 1, 2019, as a condition for accessing the MLC to make debt principal and service payments thereunder. The reporting of debt under the reporting regime established by Communication “A” 6401 (as amended and restated from time to time, the “External Assets and Liabilities Reporting Regime”) is also a condition to access the MLC to repay external financial indebtedness.

Specific Provisions Regarding Access to the MLC

Payment of principal under intercompany foreign financial indebtedness

Access to the MLC for payments of principal under intercompany foreign financial indebtedness is subject to the Central Bank of Argentina’s prior approval until December 31, 2023. This provision has been previously extended on several occasions.

Payment of imports of goods

Pursuant to Argentine FX Regulations, accessing the MLC to pay for imports of goods requires Central Bank of Argentina’s prior approval until December 31, 2023.

In order to clear customs, all imported goods are subject to the Argentina Imports System (Sistema de Importaciones de la República Argentina or “SIRA”), which replaced the Import Monitoring System (Sistema Integral de Monitoreo de Importaciones or “SIMI”) and the Prior Import Sworn Statement (Declaración Jurada de Importacion or “DJAI”). Access to the MLC to pay for imports of goods may only be granted to transactions associated with a declaration submitted through the SIRA. Also, the SIRA created an obligation for importers to file certain information with the Argentine Tax Authority (Administración Federal de Ingresos Públicos or “AFIP”).

A licensing regime is also in place, which requires importers of non-automatic import licenses to provide information about the product they intend to import (e.g., FOB value, type and quantity, commercial brand, model, country of origin and of shipping). Access to the MLC is only provided after 180 days from the product’s date of dispatch.

Though there are some exceptions to the aforementioned access to the MLC for the payment of imports of goods, they do not apply to the operations of our Company.

Payment of services provided by non-residents

Pursuant to section 3.2 of the Argentine FX Regulations, residents may access the MLC for payment of services rendered by non-residents (except for intercompany services), as long as it is verified that the operation has been declared, if applicable, in the last overdue presentation of the External Assets and Liabilities Reporting. Access to the MLC for payment of intercompany imports of services is subject to prior approval by the Central Bank of Argentina.

9

As of January 3, 2022, if new financial indebtedness is settled through the MLC and such indebtedness is (x) entered into with a third party, (y) has an average life of not less than 2 years, and (y) has no principal maturities until at least 3 months from settlement, then access to the MLC will be granted to repay intercompany services upon maturity and for services rendered at least 180 calendar days prior to requiring access to the MLC or for services arising from a contract executed 180 calendar days prior to requiring access. Access to the MLC for the prepayment of debts for services requires prior authorization by the Central Bank of Argentina.

Other Specific Provisions

Additional requirements on outflows through the MLC

As a general rule, and in addition to any rules regarding the specific purpose for access, certain general requirements must be met by a local company to access the MLC for the purchase of foreign currency or its transfer abroad (i.e., payments of imports and other purchases of goods abroad; payment of services rendered by non-residents; remittances of profits and dividends; payment of principal and interest on external indebtedness; payments of interest on debts for the import of goods and services, among others), without the need for prior approval by the Central Bank of Argentina. These include the following:

(i) during the 90 days preceding the date of such access, the local company must not have:

(a) sold securities in Argentina in exchange for foreign currency;

(b) transferred securities issued by resident issuers to a foreign depositary;

(c) exchanged securities issued by resident issuers for foreign assets;

(d) purchased with pesos in Argentina securities issued by non-resident issuers.

(e) as of July 22, 2022, (x) acquired Argentine depositary certificates representing shares issued by non-resident companies, (y) acquired corporate debt securities (i.e., securities issued by private-sector issuers, as opposed to public-sector issuances) issued outside Argentina, or (z) delivered Argentine pesos or any other local assets (other than foreign currency funds deposited in Argentine banks) to any person, receiving in exchange thereof, whether prior to or after such delivery, and whether directly or indirectly through a related, controlled or controlling entity, foreign assets, crypto assets or securities deposited abroad; and

(ii) on the date of such access, the local company must:

(a) not have any available foreign liquid assets or Argentine depositary certificates representing shares issued by non-resident companies for an aggregate amount exceeding U.S.$100,000, Communication “A” 7030 of the Central Bank of Argentina contains a non-exhaustive list of assets that qualify as “foreign liquid assets” for purposes thereof, which include foreign currency bills and coins, gold bars, sight deposits with foreign banks and, generally, any investment that allows for immediate availability of foreign currency (e.g., foreign bonds and securities, investment accounts with foreign investment managers, crypto-assets, cash held with payment service providers, etc.);

(b) deposit all its local holdings of foreign currency in accounts held with local financial institutions;

(c) undertake to settle through the MLC within 5 business days from the date of receipt of any funds originating from abroad as a result of the repayment of loans, the release of term-deposits or the sale of any type of asset, to the extent the asset was originally acquired, the deposit made or the loan granted, as applicable, after May 28, 2020;

(d) during the 90 days following such access to the MLC, undertake to not sell securities issued by residents in Argentina for foreign currency, transfer such securities to foreign depositaries, exchange such securities for other foreign assets, or purchase foreign securities with pesos in Argentina; and

Furthermore, in order to access the MLC without obtaining prior approval from the Central Bank of Argentina, the local company has to file several affidavits. In connection with this matter, the affidavit shall meet certain requirements established in Section 3.16.3 of the Argentine FX Regulations.

10

Payment of principal under intercompany foreign financial indebtedness, and payment of dividends

Access to the MLC for payments of principal under intercompany foreign financial indebtedness is subject to the Central Bank of Argentina’s prior approval until December 31, 2023. This provision has been previously extended on several occasions.

Foreign Exchange Criminal Regime

Foreign exchange regulations are characterized as “public policy” rules in Argentina. Failure to comply with such provisions could result in penalties pursuant to the Foreign Exchange Criminal Law No. 19,359.

Notwithstanding the above mentioned measures adopted by the current administration, the Central Bank of Argentina and the federal government may impose additional exchange controls in the future that may further impact our ability to transfer funds abroad and may prevent or delay payments that our Argentine subsidiaries are required to make outside Argentina.

Mexico

Exchange Rates

The Mexican peso depreciated 5.2% against the U.S. dollar in 2020, depreciated 3.1% in 2021, appreciated 5.0% in 2022 and appreciated 7.5% in the first quarter of 2023. As of April 26, 2023, the free-market exchange rate for the purchase of U.S. dollars was Ps.18.15 per U.S. dollar.

Exchange Controls

For the last few years, the Mexican government has maintained a policy of non-intervention in the foreign exchange markets, other than conducting periodic auctions for the purchase of U.S. dollars, and has not had in effect any exchange controls (although these controls have existed and have been in effect in the past). We cannot assure you that the Mexican government will maintain its current policies with regard to the Mexican peso or that the Mexican peso will not further depreciate or appreciate significantly in the future.

Chile

Exchange Rates

The Chilean peso appreciated 5.6% against the U.S. dollar in 2020, depreciated 19.9% in 2021, appreciated 0.1% in 2022 and appreciated 6.5% in the first quarter of 2023. As of April 26, 2023, the free-market exchange rate for the purchase of U.S. dollars was CLPs.805.6 per U.S. dollar.

Exchange Controls

For the last few years, the Chilean government has maintained a policy of non-intervention in the foreign exchange markets, other than conducting periodic auctions for the purchase of U.S. dollars, and has not had in effect any exchange controls (although these controls have existed and have been in effect in the past). We cannot assure you that the Chilean government will maintain its current policies with regard to the Chilean peso or that the Chilean peso will not further depreciate or appreciate significantly in the future.

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

11

D. Risk Factors

Our business, financial condition and results of operations could be materially and adversely affected if any of the risks described below occur. As a result, the market price of our class A shares could decline, and you could lose all or part of your investment. This annual report also contains forward-looking statements that involve risks and uncertainties. See “Forward-Looking Statements.” Our actual results could differ materially and adversely from those anticipated in these forward-looking statements as a result of certain factors, including the risks facing our company or investments in Latin America and the Caribbean described below and elsewhere in this annual report.

Summary of Risk Factors

An investment in our Company is subject to a number of risks, including risks related to our business, results of operations and Financial Conditions, risks related to our liquidity and indebtedness and risks related to our industry. The following summarizes some, but not all, of these risks. Please carefully consider all of the information discussed in “Item 3. Key Information—D. Risk Factors” in this annual report for a more thorough description of these and other risks.

Risks Related to Our Business and Operations

•Our rights to operate and franchise McDonald’s-branded restaurants are dependent on the MFAs, the expiration of which would adversely affect our business, results of operations, financial condition and prospects.

•Our business depends on our relationship with McDonald’s and changes in this relationship may adversely affect our business, results of operations and financial condition.

•McDonald’s has the right to acquire control of all or portions of our business upon the occurrence of certain events and, in the case of a material breach of the MFAs, may terminate such MFA or acquire our non-public shares or our interests in one or more Territories at 80% of their fair market value.

•Our business activity and results of operations may be negatively affected by unforeseen events, such as disruptions, natural disasters, adverse weather conditions, war, such as the Russia-Ukraine war, pandemics, such as the COVID-19 pandemic, or other catastrophic events.

•The failure to successfully manage our future growth may adversely affect our results of operations.

•From time to time, we depend on oral agreements with third-party suppliers and distributors for the provision of products and services that are necessary for our operations.

•Supply chain interruptions may increase our costs and reduce revenues.

•Our financial condition and results of operations depend, to a certain extent, on the financial condition of our sub-franchisees and their ability to fulfill their obligations under their franchise agreements.

•We do not have full operational control over the businesses of our sub-franchisees.

•Ownership and leasing of a broad portfolio of real estate exposes us to potential losses and liabilities.

•The success of our business is dependent on the effectiveness of our marketing strategy.

•The inability to attract and retain qualified personnel may affect our growth and results of operations.

•The resignation, termination, permanent incapacity or death of our Executive Chairman could adversely affect our business, results of operations, financial condition and prospects.

•Labor shortages or increased labor costs could harm our results of operations.

•A failure by McDonald’s to protect its intellectual property rights, including its brand image, could harm our results of operations.

Risks Related to Our Results of Operations and Financial Condition

•We may use non-committed lines of credit to partially finance our working capital needs.

•Covenants and events of default in the agreements governing our outstanding indebtedness could limit our ability to undertake certain types of transactions and adversely affect our liquidity.

•Fluctuation in market interest rates could affect our ability to refinance our indebtedness or results of operations.

•Inflation and government measures to curb inflation may adversely affect the economies in the countries where we operate, our business and results of operations.

•Exchange rate fluctuations against the U.S. dollar in the countries in which we operate have negatively affected, and could continue to negatively affect, our results of operations.

•Price controls and other similar regulations in certain countries have affected, and may in the future affect, our results of operations.

•We are subject to significant foreign currency exchange controls, currency devaluation and cross-border money transfer controls and restrictions in certain countries in which we operate, which could affect our ability to move our cash flow and pay dividends out from those countries.

12

Risks Related to Government Regulation

•If we fail to comply with, or if we become subject to, more onerous government regulations, our business could be adversely affected.

•We could be subject to expropriation or nationalization of our assets and government interference with our business in certain countries in which we operate.

•Non-compliance with anti-terrorism and anti-corruption regulations could harm our reputation and have an adverse effect on our business, results of operations and financial condition.

•Any tax increase or change in tax legislation may adversely affect our results of operations.

•Tax, customs or other inspections and investigations in any of the jurisdictions in which we operate may negatively affect our business and results of operations.

•Litigation and other pressure tactics could expose our business to financial and reputational risk.

•Information technology system failures or interruptions or breaches of our network security may interrupt our operations, exposing us to increased operating costs, fraud, data protection incidents and litigation.

•Our insurance may not be sufficient to cover certain losses.

•Our cash balance may not be covered by government-backed deposit insurance programs in the event of a default or failure of any bank with which we maintain a commercial relationship, which may have a material adverse effect on our business, financial condition results of operations and cash flows

Risks Related to Our Industry

•The food services industry is intensely competitive and we may not be able to continue to compete successfully.

•Increases in commodity prices, logistic or other operating costs could harm our operating results.

•Demand for our products may decrease due to changes in consumer preferences or other factors.

•Our investments to enhance the customer experience, including through technology, may not generate the expected returns.

•Food safety and food- or beverage-borne illnesses may have an adverse effect on our business and results of operations.

•Restrictions on promotions and advertisements directed at families with children and regulations regarding the nutritional content of children’s meals may harm McDonald’s brand image and our results of operations.

•We are subject to increasingly strict data protection laws, which could increase our costs, damage our reputation and adversely affect our business.

•Environmental laws and regulations may affect our business.

•Our business is subject to an increasing focus on environmental, social, and governance (“ESG”) matters.

•We may be adversely affected by legal actions with respect to our business.

•Unfavorable publicity or a failure to respond effectively to adverse publicity, particularly on social media platforms, could harm our reputation and adversely impact our business and financial performance.

Risks Related to Our Business and Operations in Latin America and the Caribbean

•Our business is subject to the risks generally associated with international business operations.

•Developments and the perception of risk in other countries, especially emerging market countries, as well as the increasingly complex political and social environment in Latin America and the Caribbean have in the past and could in the future lead to social protests and riots, which may adversely affect our business, operations, sales, results, financial conditions and prospects.

•Changes in governmental policies in the Territories could adversely affect our business, results of operations, financial condition and prospects.

•Latin America has experienced, and may continue to experience, adverse economic conditions that have impacted, and may continue to impact, our business, financial condition and results of operations.

13

Risks Related to Our Class A Shares

•Mr. Woods Staton, our Executive Chairman, controls all matters submitted to a shareholder vote, which will limit your ability to influence corporate activities and may adversely affect the market price of our class A shares.

•Sales of substantial amounts of our class A shares in the public market, or the perception that these sales may occur, could cause the market price of our class A shares to decline.

•As a foreign private issuer, we are permitted to, and we will, rely on exemptions from certain NYSE corporate governance standards applicable to U.S. issuers, including the requirement that a majority of an issuer’s directors consist of independent directors. This may afford less protection to holders of our class A shares.

Risks Related to Investing in a British Virgin Islands Company

•We are a British Virgin Islands company and it may be difficult for you to obtain or enforce judgments against us or our executive officers and directors in the United States.

•You may have more difficulty protecting your interests than you would as a shareholder of a U.S. corporation.

•You may not be able to participate in future equity offerings, and you may not receive any value for rights that we may grant.

Risks Related to Our Business and Operations

Our rights to operate and franchise McDonald’s-branded restaurants are dependent on the MFAs, the expiration of which would adversely affect our business, results of operations, financial condition and prospects.

Our rights to operate and franchise McDonald’s-branded restaurants in the Territories, and therefore our ability to conduct our business, derive exclusively from the rights granted to us by McDonald’s in two MFAs through August 2, 2027. As a result, our ability to continue operating in our current capacity is dependent on the renewal of our contractual relationship with McDonald’s.

McDonald’s has the right, in its reasonable business judgment based on our satisfaction of certain criteria set forth in the MFAs, to grant us an option to extend the term of the MFAs with respect to all Territories for an additional period of 10 years after the expiration in 2027 of the initial term of the MFAs upon such terms as McDonald’s may determine. Pursuant to the MFAs, McDonald’s will determine whether to grant us the option to renew between August 2020 and August 2024. If McDonald’s grants us the option to renew and we elect to exercise the option, then we and McDonald’s will amend the MFAs to reflect the terms of such renewal option, as appropriate. We cannot assure you that McDonald’s will grant us an option to extend the term of the MFAs or that the terms of any renewal option will be acceptable to us, will be similar to those contained in the MFAs or will not be less favorable to us than those contained in the MFAs.

If McDonald’s elects not to grant us the renewal option or we elect not to exercise the renewal option, we will have a three-year period in which to solicit offers for our business, which offers would be subject to McDonald’s approval. Upon the expiration of the MFAs, McDonald’s has the option to acquire all of our non-public shares and all of the equity interests of our wholly owned subsidiary Arcos Dourados Comercio de Alimentos S.A., the master franchisee of McDonald’s for Brazil, at their fair market value.

In the event McDonald’s does not exercise its option to acquire LatAm, LLC and Arcos Dourados Comercio de Alimentos S.A., the MFAs would expire and we would be required to cease operating McDonald’s-branded restaurants, identifying our business with McDonald’s and using any of McDonald’s intellectual property. Although we would retain our real estate and infrastructure, the MFAs prohibit us from engaging in certain competitive businesses, including Burger King, Subway, KFC or any other quick-service restaurant (“QSR”), business, or duplicating the McDonald’s system at another restaurant or business during the two-year period following the expiration of the MFAs. As the McDonald’s brand and our relationship with McDonald’s are among our primary competitive strengths, the expiration of the MFAs for any of the reasons described above would materially and adversely affect our business, results of operations, financial condition and prospects.

Our business depends on our relationship with McDonald’s and changes in this relationship may adversely affect our business, results of operations and financial condition.

Our rights to operate and franchise McDonald’s-branded restaurants in the Territories, and therefore our ability to conduct our business, derive exclusively from the rights granted to us by McDonald’s in the MFAs. As a result, our revenues are dependent on the continued existence of our contractual relationship with McDonald’s.

14

Pursuant to the MFAs, McDonald’s has the ability to exercise substantial influence over the conduct of our business. For example, under the MFAs, we are not permitted to operate any other QSR chains, we must comply with McDonald’s high quality standards, we must own and operate at least 50% of all McDonald’s-branded restaurants in each of the Territories, we must maintain certain guarantees in favor of McDonald’s, including a standby letter of credit (or other similar financial guarantee acceptable to McDonald’s) in an amount of $80.0 million, to secure our payment obligations under the MFAs and related credit documents, we cannot incur debt above certain financial ratios, we cannot transfer the equity interests of our subsidiaries, any significant portion of their assets or certain of the real estate properties that we own without McDonald’s consent, and McDonald’s has the right to approve the appointment of our chief executive officer and chief operating officer. In addition, the MFAs require us to reinvest a significant amount of money, including through reimaging our existing restaurants, opening new restaurants and advertising, which McDonald’s has the right to approve.

However, McDonald’s does not have an obligation to fund our operations. Furthermore, McDonald’s does not guarantee any of our financial obligations, including trade payables or outstanding indebtedness, and has no obligation to do so.

In addition to using our cash flow from operations, we may need to incur additional indebtedness in order to finance future commitments, which could adversely affect our financial condition. Moreover, we may not be able to obtain this additional indebtedness on favorable terms, or at all. Failure to comply with our future commitments could constitute a material breach of the MFAs and may lead to a termination by McDonald’s of the MFAs.

If the terms of the MFAs excessively restrict our ability to operate our business or if we are unable to satisfy our restaurant opening and reinvestment commitments under the MFAs, our business, results of operations and financial condition would be materially and adversely affected.

McDonald’s has the right to acquire control of all or portions of our business upon the occurrence of certain events and, in the case of a material breach of the MFAs, may terminate such MFA or acquire our non-public shares or our interests in one or more Territories at 80% of their fair market value.

Pursuant to the MFAs, McDonald’s has the right to acquire all of our non-public shares or our interests in one or more Territories upon the occurrence of certain events, including the death or permanent incapacity of our controlling shareholder or a material breach of the MFAs. In the event McDonald’s were to exercise its right to acquire all of our non-public shares, McDonald’s would become our controlling shareholder.

McDonald’s also has the option to acquire all, but not less than all, of our non-public shares at 100% of their fair market value during the twelve-month period following the earlier of: (i) the eighteen-month anniversary of the death or permanent incapacity of Mr. Woods Staton, our Executive Chairman and controlling shareholder, and (ii) the receipt by McDonald’s of notice from Mr. Woods Staton’s beneficiaries that such beneficiaries have elected to have such twelve-month period commence as of a date specified in such notice, which date shall be after the receipt of such notice.

If there is a material breach of the MFA, McDonald’s has the option to acquire all, but not less than all, of our non-public shares. In addition, if there is a material breach that relates to one or more Territories in which, at the time of the material breach determination, there are at least 100 franchised restaurants in operation, McDonald’s also has the right, in McDonald´s sole discretion, to acquire (i) all of our interests in our subsidiaries in all Territories or (ii) all of our interests in our subsidiaries in the Territory or Territories identified by McDonald’s as being affected by such material breach or to which such material breach may be attributable. By contrast, if the initial material breach of the MFAs affects or is attributable to any of the Territories in which, at the time of the material breach determination, there are less than 100 franchised restaurants in operation, McDonald’s only has the right to acquire the equity interests of any of our subsidiaries in the Territory or Territories being affected by such material breach or to which such material breach may be attributable. For example, since, as of the date of this annual report, we have more than 100 franchised restaurants in Mexico, if there is a material breach with respect to our business in Mexico identified by McDonald’s as being affected by such material breach or to which such material breach may be attributable, McDonald’s would have the right to acquire our entire business throughout Latin America and the Caribbean or just our Mexican operations, whereas upon a similar breach relating to our Ecuadorian business, which, as of the date of this annual report, has less than 100 franchised restaurants in operation, McDonald’s would only have the right to acquire our business in Ecuador.

If there is a material breach under an MFA, McDonald’s has the right to terminate such MFA, in whole or, in McDonald’s sole discretion, with respect to any one or more Territories identified by McDonald’s as being affected by such material breach or to which such material breach may be, directly or indirectly attributable. Any such termination would have a material adverse effect on our business, results of operations and financial condition.

15

McDonald’s was granted a perfected security interest in the equity interests of LatAm, LLC, Arcos Dourados Comercio de Alimentos S.A. and certain of their subsidiaries to protect this right. In the event this right is exercised as a result of a material breach of the MFAs, the amount to be paid by McDonald’s would be equal to 80% of the fair market value of the acquired equity interests. If McDonald’s exercises its right to acquire our interests in one or more Territories as a result of a material breach, our business, results of operations and financial condition would be materially and adversely affected. See “Item 10. Additional Information—C. Material Contracts—The MFAs—Termination” for more details about fair market value calculation.

Our business activity and results of operations may be negatively affected by unforeseen events, such as disruptions, natural disasters, adverse weather conditions, war, such as the Russia-Ukraine war, pandemics, such as the COVID-19 pandemic, or other catastrophic events.

Unforeseen events beyond our control, including war, terrorist activities, political and social unrest, natural disasters (or expectations about them), adverse weather conditions and pandemics, such as the COVID-19 pandemic, could disrupt our operations and results of operations and those of our sub-franchisees, suppliers or customers, have a negative effect on consumer spending or result in political or economic instability. These events could reduce demand for our products or make it difficult to ensure the regular supply of products through our distribution chain. For instance, the Russia-Ukraine war and related sanctions has adversely impacted the macroeconomic environment, heightened volatile economic conditions and resulted in heightened inflationary pressures, including heightened food inflation levels, increased costs of commodity prices, including energy prices, and exacerbated supply chain disruptions, which we expect may continue to affect consumer behavior and demand, geopolitical tensions and may continue to impact our business and financial results. Additionally, adverse weather conditions, including climate change, which has become more pronounced in recent years, may also increase the frequency and severity of weather-related events and natural disasters or affect customer behavior or preferences. Furthermore, incidents of pandemics could reduce sales in our restaurants. Recurrent events in our region related to Dengue, Yellow Fever, Zika and COVID-19 viruses, among others, have resulted in heightened health concerns in the region, which could reduce the visits to our restaurants if these cases are not controlled.

Moreover, although the global economy has largely recovered from the COVID-19 pandemic, certain adverse effects of the pandemic that adversely impacted our business and results of operations in the past may affect us in the future. As a result of the COVID-19 pandemic, governments at the local, state and/or federal level in all countries in which we operate implemented measures intended to stem the spread of the virus. In order to comply with these government measures, some of our markets closed all restaurants for a period of time, particularly from March through the middle of April 2020. Additionally, in order to mitigate the impact on our business, results of operations, financial condition and outlook during 2020 and part of 2021, we implemented several cash preservation measures including, but not limited to, reducing costs and expenses, limiting capital expenditures and renegotiating terms and conditions with lessors and other suppliers of goods and services. Furthermore, McDonald’s granted us a deferral of all royalty payments due, related to sales from March to July 2020 and we agreed with McDonald’s to reduce the advertising and promotion spending requirement from 5% to 4% of our gross sales for the full year 2020. McDonald’s also granted us limited waivers of the MFAs’ requirement to maintain a minimum fixed charge coverage ratio equal to or greater than 1.50 and a maximum leverage ratio of 4.25 from June 30, 2020 through and including December 31, 2021. Finally, in December 2020, we agreed with McDonald’s to withdraw the previously-approved 2020-2022 growth and investment plan and instead implement a plan for 2021 only. We have since paid all deferred royalties due, resumed spending 5% of our gross sales on advertising and promotion, resumed compliance with the fixed charge coverage ratio and the maximum leverage ratio and reached an agreement with McDonald’s on a new growth and investment plan. For more information on the McDonald’s MFA requirements, see “Item 10. Additional Information—C. Material Contracts—The MFAs.”