UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

OR

SECURITIES EXCHANGE ACT OF 1934

Commission file number 000-18516

(Exact name of registrant as specified in its charter)

|

|

|

|

|

(State or other jurisdiction of incorporation or organization)

|

|

(I.R.S. Employer Identification Number)

|

Address of principal executive offices

(302 ) 453 – 6900

Registrant’s telephone number, including area code

|

Securities registered pursuant to Section 12(b) of the Act:

|

||

|

Title of each class

|

Trading Symbol (s)

|

Name of each exchange on which registered

|

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

□

|

Yes

|

☑

|

|

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

□

|

Yes

|

☑

|

|

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

☑

|

|

□

|

No

|

|

Indicate by check mark whether the registrant has submitted electronically every Interactive Data file required to be submitted pursuant to Rule 405 of

Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

|

☑

|

|

□

|

No

|

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an

emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12(b)-2 of the Exchange Act.

|

Large Accelerated Filer □

|

Accelerated Filer □

|

|

Smaller Reporting Company

|

|

Emerging Growth Company

|

|||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or

revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. □

Indicate by check mark whether the registrant has filed a report on and

attestation to its management’s assessment of the effectiveness of its internal control over financial report under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its

audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the

filing reflect the correction of an error to previously issued financial statements. □

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by

any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b) ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

The aggregate market value of the Class A Non-Voting Common Stock and Class B

Common Stock held by non-affiliates of the registrant at June 30, 2023 was $426,719,824 and $14,196,292 ,

respectively. The aggregate market value of Class A Non-Voting Common Stock was computed by reference to the closing price of such class as reported on the Nasdaq Global Select Market on June 30, 2023, which trade date was June 30, 2023. The

aggregate market value of Class B Common Stock was computed by reference to the last reported trade of such class as reported on the OTC Bulletin Board as of June 30, 2023, which trade date was May 11, 2023.

As of March 12, 2024, 9,406,786 shares of Class A

Non-Voting Common Stock and 881,452 shares of Class B

Common Stock were outstanding.

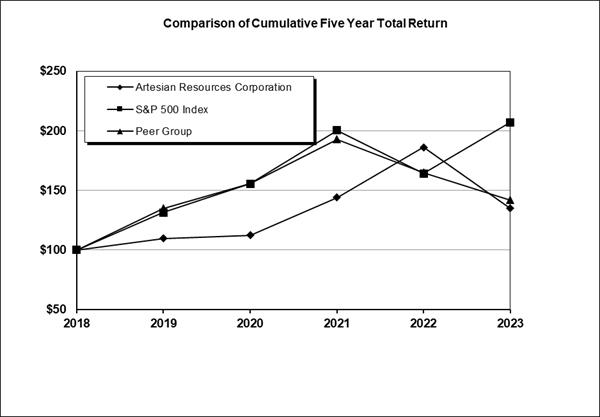

ARTESIAN RESOURCES CORPORATION

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statements in this Annual Report on Form 10-K which express our “belief,” “anticipation” or “expectation,” as well as other statements which are not

historical fact, are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act and the Private Securities Litigation Reform Act of

1995 and involve risks and uncertainties that could cause actual results to differ materially from those projected. Words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “projects”, “forecasts”, “may”, “should”,

variations of such words and similar expressions are intended to identify such forward-looking statements. They include, but are not limited to, the statements below:

|

-

|

general economic, employment and business conditions;

|

|

-

|

material costs and availability;

|

|

-

|

consumer and producer price inflation;

|

|

-

|

the impact of recent acquisitions on our ability to expand and foster relationships;

|

|

-

|

strategic plans for goals, priorities, growth and expansion;

|

|

-

|

expectations for our water and wastewater subsidiaries and non-utility subsidiaries;

|

|

-

|

customer base growth opportunities in Delaware and Cecil County, Maryland;

|

|

-

|

our belief regarding our capacity to provide water services for the foreseeable future to our customers;

|

|

-

|

our belief relating to our compliance and the cost to achieve compliance with relevant governmental regulations;

|

|

-

|

our expectation of the timing of decisions by regulatory authorities;

|

|

-

|

the impact of weather and climate change on our operations;

|

|

-

|

the execution of our strategic initiatives;

|

|

-

|

our expectation regarding the timing for construction on new projects;

|

|

-

|

the adoption of recent accounting pronouncements from time to time;

|

|

-

|

contract operations opportunities;

|

|

-

|

legal proceedings;

|

|

-

|

our properties;

|

|

-

|

deferred tax assets;

|

|

-

|

the adequacy of our available sources of financing;

|

|

-

|

the expected recovery of expenses related to our long-term debt;

|

|

-

|

our expectation to be in compliance with financial covenants in our debt instruments;

|

|

-

|

our ability to refinance our debt as it comes due;

|

|

-

|

our ability to adjust our debt level, interest rate, maturity schedule and structure;

|

|

-

|

the timing and terms of renewals of our lines of credit;

|

|

-

|

changes in interest rates;

|

|

-

|

plans to increase our wastewater treatment operations, engineering services and other revenue streams less affected by weather;

|

|

-

|

expected future contributions to our postretirement benefit plan;

|

|

-

|

anticipated growth in our non-utility subsidiaries;

|

|

-

|

anticipated investments in certain of our facilities and systems and the sources of funding for such investments;

|

|

-

|

sufficiency of internally generated funds and credit facilities to provide working capital and our liquidity needs; and

|

|

-

|

the specific and overall impacts of global pandemics on our financial condition and results of operations.

|

Certain factors, as discussed under Item 1A - Risk Factors, that could cause results to differ materially from those in the forward-looking statements

include, but are not limited to:

|

-

|

changes in weather and climate;

|

|

-

|

changes in our contractual obligations;

|

|

-

|

ability to sufficiently control certain operating expenses which are necessary to provide public utility services;

|

|

-

|

changes in government policies;

|

|

-

|

timely availability of materials and supplies for essential infrastructure projects and operations;

|

|

-

|

the timing and results of our rate requests;

|

|

-

|

failure to receive regulatory approvals;

|

|

-

|

cyber-attacks;

|

|

-

|

changes in economic and market conditions generally;

|

|

-

|

effectiveness of internal control over financial reporting;

|

|

-

|

unexpected events, restrictions and policies related to a public health crisis; and

|

|

-

|

other matters discussed elsewhere in this Annual Report on Form 10-K.

|

While the Company may elect to update forward-looking statements, we specifically disclaim any obligation to do so, except as may be required under

applicable securities laws, and you should not rely on any forward-looking statement as a representation of the Company’s views as of any date subsequent to the date of the filing of this Annual Report on Form 10-K.

General Information

Artesian Resources Corporation, or Artesian Resources, is a Delaware corporation incorporated in 1927, that is the holding company of eight wholly-owned

subsidiaries offering water, wastewater and other services in Delaware, Maryland and Pennsylvania. The Company’s principal executive offices are located at 664 Churchmans Road, Newark, Delaware 19702. Our principal subsidiary, Artesian Water Company,

Inc., is the oldest and largest investor-owned public water utility on the Delmarva Peninsula and has been providing superior water service since 1905. We distribute and sell water, including water for public and private fire protection, to

residential, commercial, industrial, municipal and utility customers in the states of Delaware, Maryland and Pennsylvania. We provide wastewater services to customers in Delaware. In addition, we provide contract water and wastewater operations, and

water, sewer and internal Service Line Protection Plans. Our Class A Non-Voting Common Stock is listed on the Nasdaq Global Select Market and trades under the symbol “ARTNA.” Our Class B Common Stock trades on the Nasdaq’s OTC Bulletin Board under

the symbol “ARTNB.”

Artesian Resources is the holding company of five regulated public utilities: Artesian Water Company, Inc., or Artesian Water, Artesian Water Pennsylvania,

Inc., or Artesian Water Pennsylvania, Artesian Water Maryland, Inc., or Artesian Water Maryland, Artesian Wastewater Management, Inc., or Artesian Wastewater, and Artesian Wastewater Maryland, Inc., or Artesian Wastewater Maryland; and three

non-utility subsidiaries: Artesian Utility Development, Inc., or Artesian Utility, Artesian Development Corporation, or Artesian Development, and Artesian Storm Water Services, Inc., or Artesian Storm Water. Effective January 14, 2022, Artesian

Wastewater is the holding company of Tidewater Environmental Services, Inc. dba Artesian Wastewater, or TESI, a regulated public utility. The terms “we,” “our,” “Artesian,” and the “Company” as used herein refer to Artesian Resources and its

subsidiaries. The business activity conducted by each of our subsidiaries is discussed below under separate headings.

Our Market

Our current market area is the Delmarva Peninsula. Our largest service area is in the State of Delaware. Substantial portions of Delaware, particularly

outside of northern New Castle County, are not served by a public water or wastewater system and represent potential opportunities for Artesian Water and Artesian

Wastewater to obtain new exclusive franchised service areas. We continue to focus resources on developing and serving existing service territories and obtaining new territories throughout Delaware.

We hold Certificates of Public Convenience and Necessity, or CPCNs, for approximately 308 square miles of exclusive water service territory, most of which is

in Delaware with some territory being in Maryland and Pennsylvania. Our largest connected regional water system, consisting of approximately 141 square miles and 79,300 metered customers, is located in northern New Castle County and portions of

southern New Castle County, Delaware. We hold CPCNs for approximately 59 square miles of wastewater service territory located in Sussex County, Delaware, of which approximately 23 square miles was added in January 2022 upon the closing of the

acquisition of TESI. A significant portion of our exclusive service territory is in Sussex County, Delaware and remains undeveloped, and if and when development occurs and there is population growth in these areas, we anticipate we will increase our

customer base by providing water and/or wastewater service to the newly developed areas and new customers.

Subsidiaries

Artesian Water

Artesian Water, our principal subsidiary, distributes and sells water to residential, commercial, industrial, governmental, municipal and utility customers

throughout the State of Delaware. In addition, Artesian Water provides services to other water utilities, including operations and billing functions, and has contract operation agreements with private, municipal and state water providers. Artesian

Water also provides water for public and private fire protection to customers in our service territories. Artesian Water produced approximately 81% of our 2023 consolidated operating revenues. In May 2022, Artesian Water completed its purchase of substantially all of the water operating assets from the Town of Clayton, or Clayton, a Delaware municipality located in Kent County, Delaware. This purchase agreement is

discussed further in the “Strategic Direction and Recent Developments” section.

We derive about 90% of our self-supplied groundwater from wells that pump groundwater from aquifers and other formations located in the Atlantic Coastal

Plain. The remaining 10% of our groundwater supply comes from wells in the Piedmont Province. We use a variety of treatment methods, including aeration, pH adjustment, chlorination, fluoridation, ultra violet oxidation, arsenic removal, nitrate

removal, radium removal, iron removal, and carbon adsorption to meet federal, state and local water quality standards. Additionally, a corrosion inhibitor is added to our self-supplied groundwater and to supply from interconnections. We have 62

different water treatment facilities in our Delaware systems. All water supplies that we purchase from neighboring utilities are potable.

To supplement our groundwater supply, we purchase treated surface water through

interconnections only in the northern service area of our New Castle County, Delaware system. The treated surface water is blended with our groundwater supply for distribution to our customers. Nearly 95% of the overall 8.7 billion gallons of water

we distributed in all of our Delaware systems during 2023 came

from our groundwater wells, while the remaining 5% came from interconnections with other utilities and municipalities. In Delaware in 2023, we pumped an average of 23.1 million gallons per day, or mgd, from our groundwater wells and obtained an

average of approximately 0.8 mgd from interconnections. Our peak water supply capacity currently is approximately 57.7 mgd. We believe that we have in place sufficient capacity to provide water service for the foreseeable future to all existing and

new customers in all of our service territories.

Most of our New Castle County, Delaware water system is interconnected. In the remainder of the State of Delaware, we have several satellite systems that

have not yet been connected by transmission and distribution facilities. We intend to join these systems into larger integrated regional systems through the construction of a transmission and distribution network as development continues and our

expansion efforts provide us with contiguous exclusive service territories.

In Delaware, we have 24 interconnections with three neighboring water utilities

and seven municipalities that provide us with the ability to purchase or sell water. An interconnection agreement with Chester Water Authority, which is effective from January 1, 2022 through December 31, 2026, includes automatic five-year renewal

terms, unless terminated by either party, and has a “take or pay” clause which required us to purchase water on a step-down schedule through July 5, 2022 and now requires us to purchase a minimum of 0.5 mgd. Artesian’s capital investments in

self-sufficiency of water supply facilitated a reduction in the minimum amount of water required to be purchased under the current contract compared to previous contracted requirements. The reduced purchased water minimum requirement has lowered

purchased water utility operating costs.

As of December 31, 2023, we were serving customers through approximately 1,470 miles of transmission and distribution mains. Mains range in diameter from

two inches to twenty-four inches, and most of the mains are made of ductile iron or cast iron.

We have 36 storage tanks in Delaware, most of which are elevated, providing total system storage of approximately 45.0 million gallons. We have developed and

are using an Aquifer Storage and Recovery, or ASR, system in New Castle County, Delaware. Our ASR system provides approximately 130.0 million gallons of storage capacity, which can be withdrawn at an average rate of approximately 1.0 mgd. At some

locations, we rely on hydro-pneumatic tanks to maintain adequate system pressures. Where possible, we combine our smaller satellite systems with systems having elevated storage facilities.

Artesian Water Maryland

Artesian Water Maryland began operations in August 2007. Artesian Water

Maryland distributes and sells water to residential, commercial, industrial and municipal customers in Cecil County, Maryland. Artesian Water Maryland owns and operates 10 public water systems.

The majority of the 0.1 billion gallons of water we distributed in all of our

Maryland systems during 2023 came from our groundwater wells,

while a portion came from treated surface water. We have ten separate water treatment facilities in our Maryland systems. We have one surface water treatment facility located in Cecil County, Maryland, with the current ability to treat up to 1.0

mgd from an intake in the Susquehanna River that is permitted a withdrawal of a maximum of 5.0 mgd and a daily average of 3.5 mgd. Our total peak water supply capacity in Cecil County, Maryland currently is approximately 2.0 mgd. We have 9 storage

tanks capable of storing approximately 2.5 million gallons. We believe that we have in place sufficient capacity to provide water service for the foreseeable future to all existing and new customers in all of our service territories.

In Maryland, we have one interconnection with the Artesian Water system in

Delaware, one interconnection with a neighboring utility, and four interconnections with municipalities. These interconnections are capable of providing over 3.0 mgd of water to our Maryland systems.

Artesian Water Pennsylvania

Artesian Water Pennsylvania began operations in 2002. It provides water

service to a residential community in Chester County, Pennsylvania.

Artesian Wastewater

Artesian Wastewater began providing wastewater services in Sussex County, Delaware in July 2005. Artesian Wastewater is a regulated entity that owns

wastewater collection and treatment infrastructure and provides wastewater services to customers in Delaware as a regulated public wastewater service company.

Artesian Wastewater owns and operates three wastewater treatment facilities, which, combined, are permitted to treat and/or dispose of approximately 2.3

mgd. Artesian Wastewater and Sussex County, a political subdivision of Delaware, provide reciprocal services to address the need of each for additional wastewater treatment and disposal capacity in certain service areas within Sussex County. Artesian

Wastewater also owns and operates a disposal facility that includes a 90-million gallon storage lagoon and spray irrigation to agricultural land. This facility provides treated process wastewater disposal services for an industrial customer at a rate

up to 1.5 mgd. We began operating this facility in June 2021.

TESI

In January 2022, Artesian Wastewater acquired Tidewater Environmental Services, Inc. Artesian Wastewater operates as the parent holding company of Tidewater

Environmental Services, Inc. dba Artesian Wastewater, or TESI. TESI was incorporated in 2004 and is a regulated entity that owns wastewater collection and treatment infrastructure and provides wastewater services to customers in Sussex County,

Delaware as a regulated public wastewater service company. Artesian Wastewater purchased all of the stock of TESI from Middlesex Water Company, or Middlesex, for $6.4 million in cash and other consideration, including forgiveness of a $2.1 million

note due from Middlesex. This acquisition more than doubled the number of wastewater customers served by Artesian’s Delaware wastewater subsidiaries in Sussex County, Delaware and included all residents within the Town of Milton, Delaware.

TESI owns and operates seven wastewater treatment facilities, which, combined, are permitted to treat and/or dispose of approximately 713,000 gallons per

day.

Artesian Wastewater Maryland

Artesian Wastewater Maryland was incorporated on June 3, 2008 and is

authorized and able to provide regulated wastewater services to customers in the State of Maryland. It is currently not providing these services.

Artesian Utility

Artesian Utility was formed in 1996 and designs and builds water and wastewater infrastructure and provides contract water and wastewater operation services

on the Delmarva Peninsula to private, municipal and governmental institutions. Artesian Utility also evaluates land parcels, provides recommendations to developers on the size of water or wastewater facilities and the type of technology that should be

used for treatment at such facilities and operates water and wastewater facilities in Delaware for municipal and governmental agencies. Artesian Utility also contracts with developers and government agencies for design and construction of wastewater

infrastructure throughout the Delmarva Peninsula.

Artesian Utility currently operates wastewater treatment facilities for the Town of Middletown, in southern New Castle County, Delaware, or Middletown, under

a 20-year contract that expires in July 2039. Artesian Utility currently operates three wastewater treatment systems with a combined capacity of up to approximately 3.8 mgd. The wastewater treatment facilities in Middletown provide reclaimed

wastewater for use in spray irrigation on public and agricultural lands in the area.

Artesian Utility also offers three protection plans to customers, the Water Service Line Protection Plan, or WSLP Plan, the Sewer Service Line Protection

Plan, or SSLP Plan, and the Internal Service Line Protection Plan, or ISLP Plan (collectively, SLP Plans). The WSLP Plan covers all parts, material and labor required to repair or replace participating customers' leaking water service lines up to an

annual limit. The SSLP Plan covers all parts, material and labor required to repair or replace participating customers' leaking or clogged sewer lines up to an annual limit. The ISLP Plan enhances available coverage to include water and wastewater

lines within customers' residences up to an annual limit.

Artesian Development

Artesian Development is a real estate holding company that owns properties, including land approved for office buildings, a water treatment plant and

wastewater facility, as well as property for current operations, including an office facility in Sussex County, Delaware. The office facility consists of approximately 10,000 square feet of office space along with approximately 7,000 square feet of

warehouse space.

Artesian Storm Water

Artesian Storm Water, incorporated in 2017, was formed to provide design, installation, maintenance and repair services related to existing or proposed

storm water management systems in Delaware and the surrounding areas. In May 2023, the Board of Directors of Artesian Storm Water unanimously approved its dissolution. Also, in May 2023, the Board of Directors of Artesian Resources Corporation, the

sole shareholder of Artesian Storm Water, unanimously approved the dissolution of Artesian Storm Water. The Company filed a Certificate of Dissolution with the Delaware Secretary of State, which became effective on June 20, 2023.

Government Regulations

Overview

The Company is subject to federal, state and local laws and regulations in all of the jurisdictions in which it operates.

These regulations include state commission orders, environmental protection, securities and exchange activities, including financial reporting and internal

controls processes, data protection and privacy, tax compliance, health and safety, labor and employment practices, and other general business activities.

State Regulatory Commission Matters

Our water and wastewater utility operations are subject to regulation by their respective state regulatory commissions, which have broad administrative power

and authority to regulate rates charged for service, determine franchise areas and conditions of service, approve acquisitions, authorize the issuance of securities and the incurrence of indebtedness, and other matters. The profitability of our

utility operations is influenced, to a great extent, by the timeliness and adequacy of regulatory relief we are granted by the respective regulatory commissions or authorities in the states in which we operate. See Notes to Consolidated Financial

Statements – Note 13 – Regulatory Proceedings for a full description of recent regulatory proceedings.

Service Territory Expansion

In Delaware, a CPCN grants a water or wastewater company the exclusive right to serve all existing and new customers within a designated area. The Delaware

Public Service Commission, or DEPSC, has the authority to issue and revoke these CPCNs. In this Form 10-K, we may refer to CPCNs as "franchises" or "service territories."

For a water company, the DEPSC may grant a CPCN under circumstances where there has been a determination that the water in the proposed service area does not

meet the regulations governing drinking water standards of the Delaware Division of Public Health, or DPH, for human consumption or where the supply is insufficient to meet the projected demand. For a wastewater company, the DEPSC has jurisdiction

over non-governmental wastewater utilities having fifty or more customers in the aggregate. A CPCN for water and wastewater utilities shall be granted by the DEPSC to applicants in possession of one of the following:

|

-

|

a signed service agreement with the developer of a proposed subdivision or development, which subdivision or development has been duly approved by

the respective county government;

|

|

-

|

a petition requesting such service signed by a majority of the landowners of the proposed territory to be served; or

|

|

-

|

a duly certified copy of a resolution from the governing body of a county or municipality requesting the applicant to provide service to the

proposed territory to be served.

|

A water or wastewater utility that has a CPCN must obtain the approval of the DEPSC to abandon a service territory. Once a CPCN is granted to a water or

wastewater utility, it may not be suspended or terminated unless the DEPSC determines in accordance with its rules and regulations that good cause exists for any such suspension or termination. Although we have been granted an exclusive franchise for

each of our existing water and wastewater systems in Delaware, our ability to expand service areas can be affected by the DEPSC awarding franchises to other regulated water or wastewater utilities with whom we compete for such franchises.

In Maryland, the Company must obtain approval from the appropriate local government authority for the ability to serve a particular area and also ensure that

the acquired area is in the county’s master water and sewer plan. The authority to exercise a franchise must then be obtained from the Maryland Public Service Commission, or MDPSC. Utilities that seek to develop a franchise by constructing new

facilities must obtain appropriate approvals from the Maryland Department of the Environment, or MDE, the local government and the MDPSC. The utility must also obtain approval for soil and erosion plans and easement agreements from appropriate

parties.

Environmental Regulation

The United States Environmental Protection Agency, or the EPA, the Delaware Department of Natural Resources and Environmental Control, or DNREC, and DPH,

regulate the water quality of our treatment and distribution systems in Delaware, as do the EPA and the MDE, with respect to our operations in Maryland. The Chester Water Authority, which supplies water to Artesian Water through an interconnection in

northern New Castle County, and Artesian Water Pennsylvania, which also supplies water to Artesian Water, are regulated by the Pennsylvania Department of Environmental Protection, or PADEP, as well as the EPA. We believe that we are in material

compliance with all current federal, state and local water quality standards, including regulations under the federal Safe Drinking Water Act. However, if new water quality regulations are too costly, or if we fail to comply with such regulations, it

could have a material adverse effect on our financial condition, results of operations and planned capital investments.

The water industry is capital intensive, with one of the highest levels of capital investment in plant and equipment per dollar of revenue among all

utilities. Increasingly stringent drinking water regulations adopted to meet the requirements of the Safe Drinking Water Act have required the water industry to invest in more advanced treatment systems and processes, which require a heightened level

of expertise. We have made significant enhancements to existing facilities to effectively treat and remove compounds as required by government agencies, such as ultra violet oxidation treatment, ceramic membrane filtration and carbon filtration. We

are currently in full compliance with the requirements of the Safe Drinking Water Act. Even though our water utility was founded in 1905, the majority of our investment in infrastructure occurred in the last 40 years.

As required by the Safe Drinking Water Act, the EPA has established maximum contaminant levels for various substances found in drinking water to ensure that

the water is safe for human consumption. These limits are known as Maximum Contaminant Levels and Maximum Residual Disinfection Levels. The EPA also regulates how often public water systems monitor their water for contaminants and report the

monitoring results to the individual state agencies or the EPA. Generally, the larger the population served by a water system, the more frequent the monitoring and reporting requirements. The Safe Drinking Water Act applies to all 50 states. The EPA

has recently proposed regulatory actions addressing per- and polyfluoroalkyl substances, or PFAS, including rules to confront PFAS contamination nationwide, with potentially significant implications. The EPA issued a proposal to designate two of the

most widely used PFAS as hazardous substances. The EPA has also declared drinking water health advisory levels for PFAS.

The Lead and Copper Rule, or LCR, is a United States federal regulation that limits the concentration of lead and

copper allowed in public drinking water at the consumer's tap, in addition to limiting the permissible amount of pipe corrosion occurring due to the water itself. The EPA first issued the rule in 1991 pursuant to the Safe Drinking Water Act. The EPA

promulgated the regulations following studies that concluded that copper and lead adversely affect an individual’s physical and mental health. The LCR therefore sought to limit the levels of these metals in water by improving water treatment centers,

determining copper and lead levels for customers who use lead plumbing parts, and eliminating the water source as a source of lead and copper. If the lead and copper levels exceed the "action levels," water suppliers are required to educate their

consumers on how to reduce exposure to lead. The EPA published a revision to the LCR in 2021, with a compliance deadline of October 2024 for developing an inventory of lead service lines within a utility’s water system. These revised requirements

provide greater and more effective protection of public health by reducing exposure to lead and copper in drinking water. Implementation of the revised rule will identify locations of lead, improve the reliability of lead tap sampling results,

strengthen corrosion control treatment requirements, expand consumer awareness and improve risk communication. In addition, implementation of the revised rule will accelerate lead service line replacements by implementing timelines and strengthening

replacement requirements. We are fully compliant with the current LCR and on schedule to be in compliance with the revised LCR ahead of the October 2024 compliance date.

The DPH has set maximum contaminant levels for certain substances that are more restrictive than the maximum contaminant levels set by the EPA. The DPH is

the EPA's agent for enforcing the Safe Drinking Water Act in Delaware and, in that capacity, monitors the activities of Artesian Water and reviews the results of water quality tests performed by Artesian Water for adherence to applicable regulations.

Artesian Water is also subject to other laws regulating substances and contaminants in water, including rules for volatile organic compounds and the Total Coliform Rule.

A normal by-product of our iron removal treatment facilities is a solid consisting of the iron removed from untreated groundwater plus residue from chemicals

used in the treatment process. The solids produced at our facilities are either disposed directly into approved wastewater facilities or removed from our facilities by a licensed third-party vendor. A normal by-product of our carbon adsorption

filtration process is exhausted carbon media, which is disposed of by the contractor providing the media replacement. Management believes that the costs of compliance with existing federal, state and local laws and regulations regulating the discharge

of materials into the environment, or otherwise relating to the protection of the environment, has had no material adverse effect upon the business and affairs of the Company, but there is no assurance that such compliance costs will continue to not

have a material effect in the future.

Under Delaware state laws and regulations, we are required to file applications

with DNREC for water allocation permits for each of our operating wells pumping greater than 50,000 gallons per day. For any wells in the Delaware River Basin, we must also file allocation permits with the Delaware River Basin Commission, or

DRBC. We have 142 operating and 62 observation and monitoring wells in our Delaware systems. At December 31, 2023, we had allocation permits for 116 wells and 25 wells that

did not require a permit.

Our access to aquifers within our service territory is not exclusive. Water

allocation permits control the amount of water that can be drawn from water resources and are granted with specific restrictions on water level draw down limits, annual, monthly and daily pumpage limits, and well field allocation pumpage limits. We

are also subject to water allocation regulations that control the amount of water that we can draw from water sources. As a result, if new or more restrictive water allocation regulations are imposed, they could have an adverse effect on our

ability to supply the demands of our customers, and in turn, our water supply revenues and results of operations. Our ability to supply the demands of our customers historically has not been affected by private usage of the aquifers by landowners or

the limits imposed by the State of Delaware. Because of the extensive regulatory requirements relating to the withdrawal of any significant amounts of water from the aquifers, we believe that third-party usage of the aquifers within our service

territory will not interfere with our ability to meet the present and future demands of our customers.

The MDE ensures that water quality and quantity at all public water systems in Maryland meet the needs of the public and are in compliance with federal and

state regulations. The MDE also ensures that public drinking water systems provide safe and adequate water to all current and future users in Maryland and that appropriate usage, planning, and conservation policies are implemented for Maryland’s water

resources. The MDE oversees the development of Source Water Assessments for water supplies and issues water appropriation permits for public drinking water systems. In order to appropriate water for municipal, commercial, industrial or other

non-domestic uses, a Water Appropriation Permit must be obtained. Issuance of the permit involves evaluating the needs of the user and the potential impact of the withdrawal on neighboring users and the water source in order to maximize beneficial use

of the water. Permits for large appropriations often involve conducting pump tests to measure adequacy of an aquifer and safe yield of a well, or reviewing stream flow records to determine the adequacy of a surface water source. Regulations require

all new community water systems to have sufficient technical, managerial and financial capacity to provide safe drinking water to their consumers prior to being issued a construction permit. Also, capacity management guidance contains capacity limiting factors that can include source capacity, treatment capacity and appropriation permit quantity. The quantity of water withdrawn from the Port Deposit surface water

intake is allocated by the Susquehanna River Basin Commission, or SRBC, and the MDE. We have 14 operating wells and one surface water in-take in our Maryland systems.

The PADEP administers and oversees departmental programs involving surface and groundwater quantity and quality

planning and water conservation in Pennsylvania. The office also coordinates policies, procedures, and regulations which influence public water supply withdrawals and quality. The DRBC administers and oversees programs involving water quality

protection, water supply allocation, water conservation initiatives and watershed planning, regulatory review and permitting, and drought management in Pennsylvania. We have one operating well in Pennsylvania within the DRBC’s jurisdiction. This well

is treated by a water treatment plant located in Delaware.

The Clean Water Act has established the foundation for wastewater discharge control in the United States. The Clean Water Act established a control program

for ensuring that communities have clean water by regulating the release of contaminants into waterways. Permits that limit the amounts of pollutants discharged are required for all wastewater dischargers under the National Pollutant Discharge

Elimination System, or the NPDES, permit program. In accordance with the NPDES permit program, the implementing states set maximum discharge limits for wastewater effluents and overflows from wastewater collection systems. Discharges that exceed the

limits specified under the NPDES permit program can lead to the imposition of penalties. The Clean Water Act also requires that wastewater treatment plant discharges meet a minimum of secondary treatment. The secondary treatment process can remove

90% to 99% of the organic matter in wastewater. Our removal efficiency is generally 96% to 98%.

Under Delaware state laws and regulations, we are required to hold a permit from DNREC for the construction, operation, maintenance or repair of any on-site

wastewater treatment and disposal systems with daily design flow rates of 2,500 gallons or greater. A classification on the facility is performed in accordance with Regulations Licensing Operators of Wastewater Facilities. The class of operator

required for the facility is determined by the Board of Certification for Licensed Wastewater Operations in accordance with Regulations Licensing Operators of Wastewater Facilities. We work to ensure that we operate environmentally friendly wastewater

systems that meet federal, state and local laws.

Additional General Information

Seasonality

Substantially all of our water customers are metered, which allows us to measure and bill for our customers’ water consumption. Demand for water during the

warmer months is generally greater than during cooler months primarily due to additional customer requirements for water in connection with cooling systems, swimming pools, irrigation systems and other outside water use. Throughout the year, and

particularly during typically warmer months, demand for water will vary with temperature and rainfall. In the event that temperatures during the typically warmer months are cooler than expected, or there is more rainfall than expected, the demand for

water may decrease and our revenues may be adversely affected.

Competition

Our business in our franchised service areas is substantially free from direct competition with other public utilities, municipalities and other entities.

However, our ability to provide additional water and wastewater services is subject to competition from other public utilities, municipalities and other entities. Even though our regulated subsidiaries have been granted an exclusive franchise for each

of our existing community water and wastewater systems, our ability to expand service areas can be affected by the DEPSC, the MDPSC or the Pennsylvania Public Utility Commission, or PAPUC, awarding franchises to other regulated water or wastewater

utilities with whom we compete for such franchises.

Suppliers and Independent Contractors

We are dependent upon the ability of our suppliers and independent contractors to meet performance specifications, quality standards and delivery schedules

at our anticipated costs. While we maintain an extensive qualification and performance review system to control risk associated with such reliance on third parties, failure of suppliers or independent contractors to meet commitments could adversely

affect construction and maintenance schedules. We are also dependent on the availability of electricity and purchased water at affordable prices. Our electric costs and purchased water costs are at a fixed price under contract.

Employees and Human Capital Resources

As of December 31, 2023, we employed 251 full-time employees. Of these

employees, 59 were officers and managers; 119 were employed as operations personnel, including engineers, technicians, draftsman, maintenance and repair persons, meter readers and utility personnel; and 38 were employed in accounting, budgeting,

information systems, human resources, customer relations and public relations. The remaining 35 employees were administrative personnel. The Company has no collective bargaining agreements with any of its employees, and its work force is not union

organized or union represented. We believe that our relations with our employees are good. Through ongoing employee development, competitive compensation and benefits, and a focus on health, safety and employee wellbeing, we strive to help

our employees in all aspects of their lives.

We believe the Company’s success depends on its ability to attract, develop and retain key personnel. We provide our employees with resources that

contribute to their professional development, including technical training and performance reviews. A core principle of our company is to promote from within and offer advancement opportunities at all levels of employment, which helps us retain

talented employees. We believe our management team has the experience, talent and dedication necessary to effectively execute our business goals and growth strategy. We recognize that the skills, experience, diversity, industry knowledge and

dedication of our employees significantly benefit our operations and performance.

We set pay ranges based on market data. When considering compensation, we

consider factors such as an employee’s role, experience, and his or her performance. We regularly review our compensation practices, both in terms of our overall workforce and individual employees, to ensure our compensation is fair and

equitable.

Health and safety in the workplace for our employees is one of the Company’s core values. Hazards in the workplace are proactively identified and actions

are taken to maintain workplace safety. We sponsor a wellness program designed to enhance physical, financial, and mental wellbeing for all our employees. Throughout the year, we encourage healthy behaviors through regular communications, educational

sessions and other incentives.

We use outside consultants and independent contractors on an as needed basis for various services. We rely on our independent contractors to manage their

respective employee relations so that the services they are contractually obligated to perform for us satisfy our requirements. Management believes that through our own employees, coupled with the services provided by our independent contractors and

outside consultants, we have sufficient human capital to continue to operate our business successfully.

Available Information

We are a Delaware corporation with our principal executive offices located at 664 Churchmans Road, Newark, Delaware, 19702. Our telephone number is (302)

453-6900 and our website address is www.artesianwater.com. We make available free of charge through our website our Code of Ethics, Annual Reports on Form

10-K, Quarterly Reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports, our Corporate Governance Guidelines, and our Board Committee Charters as soon as reasonably practicable after such material is electronically filed

with or furnished to the Securities and Exchange Commission, or the SEC. We include our website address in this Annual Report on Form 10-K only as an inactive textual reference and do not intend it to be an active link to our website. Information

contained on our website shall not be deemed incorporated into, or to be a part of, this report.

We are exposed to a variety of risks and uncertainties. Most are general risks and uncertainties applicable to all water and wastewater utility companies.

We describe below some of the specific known risk factors that could negatively affect our business, financial condition or results of operations. If one or more of these risks or uncertainties occur, actual results may vary materially from our

projections.

Risks Related to Our Operations

We are dependent upon the ability of our suppliers and independent contractors to meet performance specifications, quality standards and delivery

schedules at our anticipated costs.

While we maintain an extensive qualification and performance review system to control risk associated with such reliance on third parties, failure of

suppliers or independent contractors to meet commitments could adversely affect construction and maintenance schedules and our results of operations and financial condition. We have been affected and could continue to be affected by supplier delays

and increased costs, due to the impacts of inflation, which are outside of our control and could affect our results of operations. We are also dependent on the availability of electricity and purchased water at affordable prices. While our

electricity costs and purchased water costs are at fixed prices under contracts, after the expiration of these contracts, we may be required to pay higher electricity costs and purchased water costs.

We are subject to risks associated with the collection, treatment and disposal of wastewater.

Wastewater collection, treatment and disposal involve various unique risks. If collection or treatment systems fail, overflow, or do not operate properly,

untreated wastewater or other contaminants could spill onto nearby properties or into nearby streams and rivers, causing damage to persons or property, injury to wildlife and economic damages, which may not be recoverable in fees. This risk is most

acute during periods of substantial rainfall or flooding, which are common causes of sewer overflow and system failure. Liabilities resulting from such damages and injuries could materially and adversely affect our business, results of operations and

financial condition.

Aging infrastructure may lead to service disruptions, property damage and increased capital expenditures and operation and management costs, all of which

could negatively impact our financial results.

We have risks associated with aging infrastructure, including water and sewer mains, pumping stations and water and wastewater treatment facilities.

Additionally, the nature of information available on buried and newly acquired assets may be limited, which may challenge our ability to conduct efficient asset management and maintenance practices. Assets that have aged beyond their expected useful

lives may experience a higher rate of failure. Failure of aging infrastructure could result in increased capital expenditures and operation and management costs. In addition, failure of aging infrastructure may result in property damage, and in safety,

environmental and public health impacts. To the extent that any increased costs or expenditures are not fully recovered in rates, our results of operations, liquidity and cash flows could be negatively impacted.

Potential terrorist attacks or sabotage may disrupt our operations and adversely affect our business, operating results and financial condition.

We are subject to possible sabotage of our water and wastewater systems, including vandalism causing an interruption in water supply and a reduction in water

quality, and terrorism causing contamination of the water supply and a reduction in water quality. We have security measures in place at our facilities to reduce the possibility of occurrences of sabotage, vandalism, or terrorism and to secure our

water and wastewater systems. These security measures address water collection, pretreatment, treatment, distribution, storage, wastewater disposal, electronic or automated systems, and the use, handling, delivery, and storage of all chemicals. We

also have programs in place to ensure employee awareness of potential threats. We have and will continue to bear any increase in costs, most of which have been recoverable under state regulatory policies, for security precautions to protect our

facilities, operations and supplies. While the costs of increases in security, including capital expenditures, may be significant, we expect these costs to continue to be recoverable in water and wastewater rates. Despite our security measures, we

may not be in a position to control the outcome of terrorist events, sabotage or other attacks on our water systems, should they occur.

We depend on the availability of capital for expansion, construction and maintenance. Weaknesses in capital and credit markets or increased interest rates

may limit our access to capital.

Our ability to continue our expansion efforts and fund our utility construction and maintenance program depends on the availability of adequate capital.

There is no guarantee that we will be able to obtain sufficient capital in the future on favorable terms and conditions, such as changes in market conditions and events beyond our control, most recently increases to interest rates, for expansion,

construction and maintenance. In the event our lines of credit are not extended or we are unable to refinance our first mortgage bonds when due and the borrowings are called for payment, we will have to seek alternative financing sources, although

there can be no assurance that these alternative financing sources will be available on terms acceptable to us. In the event we are unable to obtain sufficient capital, our expansion efforts could be curtailed, which may affect our growth and may

affect our future results of operations.

We may be adversely affected by global climate change or by regulatory, legal or market responses to such change.

The issue of climate variability is receiving increasing attention nationally and worldwide. Climate change is an intrinsically complex global phenomenon

with inherent residual risks across its physical and regulatory dimensions that cannot be mitigated given their wide-ranging, interdependent and largely unpredictable potential scope, nature, timing or duration. Some climate researchers believe that

there will be worsening of weather volatility in the future associated with climate variability, which presents several potential challenges to water and wastewater utilities. Severe weather, climate variability patterns and natural or other events

may cause weather volatility in the future and may impact water usage and related revenue, or may require additional expenditures, all of which may not be fully recoverable in rates or otherwise.

We may experience substantial negative impacts to our business if an unexpectedly severe weather event or natural disaster damages our facilities and/or

operations or those of our suppliers or independent contractors in our service areas, or from the unintended consequences of regulatory changes that directly or indirectly impose substantial restrictions on our activities or adaptation requirements.

Potential climate variability challenges include the following: increased frequency and duration of droughts, increased precipitation and flooding, increased frequency and severity of storms and other weather events, potential degradation of water

quality, unexpected changes in temperature, increases in ocean levels, disruptions in water or wastewater services to our customers, decreases in available water supply, extreme changes in water usage patterns, increases in expenditures to repair any

damages, increases in costs to reduce risks associated with significant weather events or natural disasters, and increases in costs to improve the reliability of our water and wastewater systems and facilities. Due to the uncertainty of weather

volatility related to climate variability, we cannot predict its potential impact on our financial condition, results of operations, cash flows and liquidity. Although some or all potential expenditures and costs with respect to our regulated

businesses could be recovered through rates we charge to our customers, there can be no assurance that the applicable regulatory authority would authorize recovery of such costs, in whole or in part, for any of these impacts.

Furthermore, federal, state and local authorities and legislative bodies have issued, implemented or proposed regulations, penalties, standards and/or

guidance intended to restrict, moderate or promote activities consistent with resource conservation, Greenhouse Gas, or GHG, emission reduction, environmental protection or other climate-related objectives. Compliance with those directed at or

otherwise affecting our business or our suppliers’ (or their suppliers’) operations, or services, could lead to increased environmental compliance expenditures, increased energy and raw materials costs and new and/or additional investment in designs

and technologies. We continually assess our compliance status and management of environmental matters to ensure our operations are in compliance with all applicable environmental laws and regulations. It is reasonably possible that costs incurred

related to the various physical and regulatory risks from climate change may affect our future results of operations, financial condition, cash flows or liquidity. While we have health and safety protocols in place, we can provide no assurance that we

or our suppliers or independent contractors can successfully operate in areas experiencing a significant weather event or natural disaster, and we or they may be more significantly impacted and take longer, and incur higher costs, to resume operations

in an affected location, depending on the nature of the event or other circumstances. Although some or all potential expenditures and costs with respect to our regulated businesses could be recovered through rates we charge to our customers, there can

be no assurance that the applicable regulatory authority would authorize recovery of such costs, in whole or in part, for any of these impacts.

Though we have not as of the date of this report identified or experienced any particular material impact, whether singular or in combination, to our

consolidated financial statements from climate change or the associated regulatory, physical, and other risks discussed above, we cannot provide any assurance that we have or can successfully prepare for, or are or will be able to reduce or manage any

of them to the extent they may arise. In addition, the SEC has proposed extensive climate-related disclosure rules, which, if adopted, would likely result in increased compliance costs and capital expenditures.

Risks Related to Governmental Laws and Regulations

We rely on governmental approvals in the States of Delaware and Maryland and the Commonwealth of Pennsylvania, as well as approvals from the Delaware

River Basin Commission and Susquehanna River Basin Commission for applicable water allocation, water appropriation and water capacity permits. In addition, we rely on governmental approvals in the State of Delaware for applicable wastewater

collection, treatment and disposal permits for the operation of our wastewater facilities.

Our water and wastewater services are governed by various federal and state governmental agencies. Pursuant to these regulations, we are required to obtain

various permits for any additional systems and current systems to assist in our operations. If any of those permit approvals are not received timely or at all, we may risk the loss of economic opportunity and our ability to create additional systems

for the effective operation of our water business in Delaware, Maryland and Pennsylvania or our wastewater business in Delaware. We can provide no assurances that we will receive all necessary permits to add systems or continue to operate facilities

of our water or wastewater business.

Our operating revenue is primarily from water sales. The rates that we charge our customers are subject to the regulations of the public service

commissions in the states in which we operate. If a public service commission disapproves or is unable to timely approve our requests for rate increases or approves rate increases that are inadequate to cover our investments, deferred regulatory

assets or increased costs, our profitability may suffer.

We file rate increase requests, from time to time, to recover our investments in utility plant, deferred regulatory assets and expenses, see Notes to Consolidated Financial Statements - Note 13 – Regulatory Proceedings. Once a rate increase petition is filed with a public service commission, the ensuing

administrative and hearing process may be lengthy and costly. We can provide no assurances that any future rate increase request will be approved by the DEPSC, MDPSC or PAPUC, and if approved, we cannot guarantee that these rate increases will be

granted in a timely manner and/or will be sufficient in amount to cover the investments, deferred regulatory assets and expenses for which we initially sought the rate increase. To the extent we are able to pass through such costs to customers and a

state public service commission subsequently determines that such costs should not have been paid by customers, we may be required to refund such costs, with interest, to customers. Any such costs not recovered through rates, or any such refund, could

adversely affect our results of operations, financial position or cash flows.

Our water and wastewater operations are subject to extensive federal and state laws and regulations. In addition, our operating costs and capital

expenditures could be significantly increased if new or stricter regulatory standards are imposed by federal or state environmental agencies.

We are subject to various federal, state, and local laws and regulations relating to environmental protection, including the discharge, treatment, storage,

disposal and remediation of hazardous substances and wastes. Our water and wastewater services are governed by various federal and state environmental protection and health and safety laws and regulations, including, among others, the federal Safe

Drinking Water Act, the Clean Water Act, the LCR and other federal and state laws. These federal and state regulations are issued by the EPA and state environmental regulatory agencies. Pursuant to these laws and regulations, we are required to

obtain various water allocation permits and environmental permits for our operations. The water allocation permits control the amount of water that can be drawn from water resources. New or stricter water allocation regulations can adversely affect

our ability to meet the demands of our customers. While we have budgeted for future capital and operating expenditures to maintain compliance with these laws and our permits, it is possible that new or stricter standards would be imposed that will

raise our operating costs and capital expenditures. Thus, we can provide no assurances that our costs of complying with, or discharging liability under, current and future environmental and health and safety laws will not adversely affect our

business, results of operations or financial condition.

Risks Related to Our Financial Statements and Operating Results

Our business is subject to seasonal fluctuations, which could affect demand for our water service and our revenues.

Demand for water during warmer months is generally greater than during cooler months primarily due to additional customer requirements in irrigation systems,

swimming pools, cooling systems and other outside water use. In the event that temperatures during typically warmer months are cooler than normal, or rainfall is more than normal, the demand for our water may decrease and adversely affect our

revenues.

Drought conditions and government-imposed water use restrictions may impact our ability to serve our current and future customers, and may impact our

customers’ use of our water, which may adversely affect our financial condition and results of operations.

We believe that we have in place sufficient capacity to provide water service for the foreseeable future to all existing and new customers in all of our

service territories. However, severe drought conditions could interfere with our sources of water supply and could adversely affect our ability to supply water in sufficient quantities to our existing and future customers. This may adversely affect

our revenues and earnings. Moreover, governmental restrictions on water usage during drought conditions may result in a decreased demand for water, which may adversely affect our revenue and earnings.

General economic conditions may materially and adversely affect our financial condition and results of operations.

The effects of adverse U.S. economic conditions may lead to a number of impacts on our business that may materially and adversely affect our financial

condition and results of operations. Such impacts may include a reduction in discretionary and recreational water use by our residential water customers, particularly during the summer months; a decline in usage by industrial and commercial customers

as a result of decreased business activity and commerce in our customers’ businesses; an increased incidence of customers’ inability to pay their bills, bankruptcy or delay in paying their bills which may lead to higher bad debt expense and reduced

cash flow; and a lower natural customer growth rate may result as compared to what had been experienced before due to a decline in new housing starts or a decline in the number of active customers due to housing vacancies or abandonments.

We could be adversely impacted by inflation.

We have been affected and could continue to be affected by increased costs for items such as, among others, materials for capital expenditures, fuel, and

treatment chemicals, due to the impacts of inflation. If inflation increases significantly, we may seek to increase our rates charged to customers. We can provide no assurances that any future rate increase request will be approved by the applicable

regulatory authority, and if approved, we cannot guarantee that any rate increase will be granted in a timely manner and/or will be sufficient in amount to cover costs for which we initially sought the rate increase. The impact of inflation could

adversely affect our results of operations, financial position or cash flows.

We may be required to record impairments of goodwill, or otherwise change the fair value of certain assets, in the future that could have a material

adverse effect on our financial condition and results of operations.

The Company records goodwill when the purchase price of a business combination exceeds the estimated fair value of net identified tangible and intangible

assets acquired as of the date of an acquisition. The Company’s goodwill is associated with the January 2022 acquisition of Tidewater Environmental Services, Inc. Goodwill is not amortized, but is evaluated for impairment at least annually, or more

frequently, if impairment indicators are present that would more likely than not reduce the fair value of a reporting unit below its carrying amount. We may be required to recognize in the future an impairment of goodwill due to market conditions, or

other factors related to our performance or the performance of an acquired business, or other circumstances that may impact the fair value of assets acquired. Recognition of impairments of goodwill and changes in fair value of certain of our assets

would result in a charge to income in the period in which the impairment or change occurred, which may negatively affect our financial condition, results of operations and total capitalization.

Risks Related to Our Business Strategy

We face competition from other water and wastewater utilities for the acquisition of new exclusive service territories.

We face competition from other water and wastewater utilities as we pursue the right to exclusively serve new territories in Delaware and Maryland. We

address this competition by entering into agreements with landowners, developers or municipalities and, under current law, then applying to the DEPSC or the MDPSC for a CPCN. If we are unable to enter into agreements with landowners, developers or

municipalities and secure CPCNs for the right to exclusively serve new territories in Delaware or Maryland, our ability to expand may be significantly impeded.

Any future acquisitions we undertake or other actions to further grow our water and wastewater business may involve risks.

An element of our growth strategy is the acquisition and integration of water and wastewater systems in order to broaden our current service areas and move

into new ones. It is our intent, when practical, to integrate any organizations we acquire with our existing operations. The negotiation of potential acquisitions as well as the integration of acquired organizations could require us to incur

significant costs and cause diversion of our management’s time and resources. We may not be successful in the future in identifying organizations that meet our acquisition criteria. The failure to identify such organizations may limit the rate of our

growth. In addition, future acquisitions or expansion of our service areas by us could result in:

|

-

|

Dilutive issuance of our equity securities;

|

|

-

|

Incurrence of debt and contingent liabilities;

|

|

-

|

Difficulties in integrating the operations and personnel of the acquired organization;

|

|

-

|

Diversion of our management’s attention from ongoing business concerns;

|

|

-

|

Failure to have effective internal control over financial reporting;

|

|

-

|

Overload of human capital resources; and

|

|

-

|

Other acquisition-related expense.

|

Some or all of these items could have a material adverse effect on our business and our ability to finance our business and comply with regulatory

requirements. The organizations we acquire in the future may not achieve sales and profitability that would justify our investment.

We also may experience risks relating to the challenges and costs of closing a transaction and the risk that an announced transaction may not close.

Completion of certain acquisition transactions are conditioned upon, among other things, the receipt of approvals, including from certain state public utilities commissions. The timeliness and outcome of those state public utilities commissions could

hinder future acquisitions and any failure to complete a pending transaction would prevent us from realizing the anticipated benefits. We would also remain liable for significant transaction costs, including legal and accounting fees, whether or not

the transaction is completed.

Risks Related to Legal Uncertainty

Contamination of our water supply or wastewater operational malfunctions may

result in disruption in our services and could lead to litigation that may adversely affect our business, operating results and financial condition.

Our water supplies are subject to contamination from naturally-occurring compounds as well as pollution resulting from man-made sources. Even though we

monitor the quality of our water on an ongoing basis, any possible contamination could interrupt the use of our water supply until we are able to substitute it from an uncontaminated water source. Additionally, treating the contaminated water source

could involve significant costs and could adversely affect our business. We could also be held liable for consequences arising out of human or environmental exposure to hazardous substances, if found, in our water supply. If wastewater collection or

treatment systems fail, overflow, or do not operate properly, untreated wastewater or other contaminants could spill onto nearby properties or into nearby streams and rivers, causing damage to persons or property, injury to wildlife and economic

damages for which we could be held liable. Any such occurrence could adversely affect our business, results of operations and financial condition.

We are subject to various laws and regulations that could expose us to governmental investigations or actions by other third parties.

We are subject to various federal and state laws and regulations, including environmental laws and regulations, violations of which can involve civil or

criminal sanctions.

Our Company from time to time could be parties to or our operations targets of, lawsuits, claims, investigations and proceedings, including system failure,

injury, contract, environmental, health and safety and employment matters, which are handled and defended in the ordinary course of business. The results of any future litigation or settlement of such lawsuits and claims are inherently unpredictable,

but such outcomes could also materially and adversely affect our business, financial position and results of operations.

Risk Related to Cybersecurity and Technology

We are dependent on the continuous and reliable operation of our information technology systems that require, potentially costly, maintenance and could

become subject to cyberattacks disrupting our operations.

We rely on our information technology systems to manage operation of our business. Specifically, our business relies on the following technology systems,

among others: customer information system, financial reporting system, asset tracking system, remote monitoring system for some of our treatment, storage and pumping facilities, human resources management system, inventory management system, and

accounts receivable collection management system. Such systems require periodic modifications, upgrades or replacement that subject us to inherent costs and risks, including substantial capital expenditures, additional administration and operating

expenses, and other risks and costs of delays in transitioning to new systems or of integrating new systems into our current systems. Our computer and communications systems and operations could be damaged or interrupted by natural disasters, power

loss, telecommunications failures or acts of war or terrorism, sabotage, theft or similar events or disruptions. A loss of these systems or major problems with the operation of these systems could affect our operations and have a material adverse

effect on our business and results of operations.

To date, there have been no risks identified from cybersecurity threats or previous cybersecurity incidents that have materially affected or are reasonably

likely to materially affect the company. Despite our efforts, a cyberattack, if it occurred, could cause water or wastewater system operational complications, disrupt

service to our customers, compromise important data or systems or result in an unintended release of customer or other confidential information. Possible impacts associated with a cyberattack could also include remediation costs related to lost,

stolen, or compromised data, repairs to information technology and data processing systems, increased cyber security protection costs, adverse effects on our compliance with regulatory and environmental laws and regulations, including standards for

water and wastewater utility providers, and litigation. We feel we have adequate cybersecurity insurance coverage to mitigate the cost of any such cyberattack; however, a possible cyberattack could affect our operations and have a material adverse

effect on our business and results of operations. We have implemented, and will continue to internally monitor and manage, business processes to support our cybersecurity program. For additional information concerning the Company’s cybersecurity

program, see Item 1C - Cybersecurity.

Risk Associated with Management

Turnover in our management team could have an adverse impact on our business or the financial market’s perception of our ability to continue to grow.

Our success depends significantly on the continued contribution of our management team both individually and collectively. The loss of the services of any

member of our management team or the inability to hire and retain experienced management personnel could harm our operating results. In addition, turnover in our management team could adversely affect the financial market’s perception of our ability

to continue to grow.

Risks Related to Our Common Stock