UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(MARK ONE)

FOR THE FISCAL YEAR ENDED

OR

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (

Securities registered pursuant to Section 12(b) of the Act:

Title Of Each Class |

| Trading Symbol |

| Name of Each Exchange On Which Registered |

The | ||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ◻ Yes ⌧

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ◻ Yes ⌧

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. ⌧

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ⌧

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “ accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ◻ | Accelerated filer ◻ | Smaller reporting company | |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant has filed a report on and attestation to its mangagement’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. The aggregate market value was $

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. There were

DOCUMENTS INCORPORATED BY REFERENCE.

None

FORM 10-K INDEX

2

PART I

ITEM 1. BUSINESS

GENERAL

AmeriServ Financial, Inc. (the Company) is a bank holding company organized under the Pennsylvania Business Corporation Law. The Company became a holding company upon acquiring all of the outstanding shares of AmeriServ Financial Bank (the Bank) in January 1983. The Company’s other wholly owned subsidiary is AmeriServ Trust and Financial Services Company (the Trust Company) which was formed in October 1992. When used in this report, the “Company” may refer, depending on the context, to AmeriServ Financial, Inc. individually or AmeriServ Financial, Inc. and its direct and indirect subsidiaries.

The Company’s principal activities consist of owning and operating its two wholly owned subsidiary entities. At December 31, 2023, the Company had, on a consolidated basis, total assets, deposits, and shareholders’ equity of $1.4 billion, $1.2 billion, and $102.3 million, respectively. The Company and its subsidiaries derive substantially all of their income from banking, bank related services, and trust and wealth management related services. The Company functions primarily as a coordinating and servicing unit for its subsidiary entities in general management, accounting and taxes, loan review, internal audit, investment accounting, marketing and risk management.

As a bank holding company, the Company is subject to supervision and regular examination by the Federal Reserve Bank of Philadelphia and the Pennsylvania Department of Banking and Securities (PDB). The Company is also under the jurisdiction of the Securities and Exchange Commission (SEC) for matters relating to registered offerings and sales of its securities under the Securities Act of 1933, as amended, and the disclosure and regulatory requirements of the Securities Exchange Act of 1934, as amended. The Company’s common stock is listed on The NASDAQ Stock Market under the trading symbol “ASRV,” and the Company is subject to the NASDAQ rules applicable to listed companies.

AMERISERV FINANCIAL BANK

The Bank is a state bank chartered under the Pennsylvania Banking Code of 1965, as amended (Banking Code). Through 17 branch locations in Allegheny, Cambria, Centre, Somerset, and Westmoreland counties, Pennsylvania and Washington county, Maryland, the Bank conducts a general banking business. It is a full-service bank offering (i) retail banking services, such as demand, savings and time deposits, checking accounts, money market accounts, secured and unsecured consumer loans, mortgage loans, safe deposit boxes, holiday club accounts, and money orders; and (ii) lending, depository and related financial services to commercial, industrial, financial, and governmental customers, such as commercial real estate mortgage loans (CRE), short and medium-term loans, revolving credit arrangements, lines of credit, inventory and accounts receivable financing, real estate construction loans, business savings accounts, time deposits, wire transfers, night depository, and lock box services. The Bank also operates 18 automated bank teller machines (ATMs) through its 24-hour banking network that is linked with NYCE, a regional ATM network, and CIRRUS, a national ATM network. West Chester Capital Advisors (WCCA), a SEC-registered investment advisor, is a subsidiary of the Bank. The Company also operates loan production offices (LPOs) in Altoona and Wilkins Township in Pennsylvania.

We believe that the loss of one depositor or a related group of depositors would not have a materially adverse effect on the Bank’s business. The Bank’s business is not seasonal, nor does it have any risks attendant to foreign sources. A significant majority of the Bank’s customer base is located within a 250-mile radius of Johnstown, Pennsylvania, the Bank’s headquarters.

3

The Bank is subject to supervision and regular examination by the Federal Reserve Bank of Philadelphia and the PDB. Various federal and state laws and regulations govern many aspects of its banking operations. The following is a summary of key data (dollars in thousands) and ratios of the Bank at December 31, 2023:

Headquarters |

| Johnstown, PA |

| |

Total Assets | $ | 1,378,660 | ||

Total Investment Securities (net of allowance for credit losses) |

| 222,213 | ||

Total Loans and Loans Held for Sale (net of unearned income) |

| 1,038,401 | ||

Total Deposits |

| 1,162,066 | ||

Total Net Loss |

| (250) | ||

Asset Leverage Ratio |

| 8.78 | % | |

Return on Average Assets |

| (0.02) | ||

Return on Average Equity |

| (0.22) | ||

Total Full-time Equivalent Employees |

| 236 | ||

RISK MANAGEMENT OVERVIEW

Risk identification and management are essential elements for the successful management of the Company. In the normal course of business, the Company is subject to various types of risk, which includes credit, interest rate and market, liquidity, operational, legal/compliance, strategic/reputational and security risk. The Company seeks to identify, manage and monitor these risks with policies, procedures, and various levels of oversight from the Company’s Board of Directors (the Board) and management. The Company has a Management Enterprise Risk Committee with Board of Director representation to help manage and monitor the Company’s risk position, which is reported formally to the Board, at a minimum, on a semi-annual basis.

Interest rate risk is the sensitivity of net interest income and the market value of financial instruments to the magnitude, direction, and frequency of changes in interest rates. Interest rate risk results from various repricing frequencies and the maturity structure of assets and liabilities. The Company uses its asset/liability management policy to monitor and manage interest rate risk.

Liquidity risk represents the inability to generate cash or otherwise obtain funds at reasonable rates to satisfy commitments to borrowers, as well as the obligations to depositors, debtholders and the funding of operating costs. The Company uses its asset/liability management policy and contingency funding plan to monitor and manage liquidity risk.

Credit risk represents the possibility that a customer may not perform in accordance with contractual terms resulting in an economic loss to the organization. Credit risk results from extending credit to customers, purchasing securities, and entering into certain off-balance sheet loan funding commitments. The Company’s primary credit risk occurs in the loan portfolio with limited credit risk within the investment portfolio due to holdings of corporate and municipal securities. The Company uses its credit policy and disciplined approach to evaluating the adequacy of the allowance for credit losses (the ACL) to monitor and manage credit risk. The Company’s investment policy and hedging policy seeks to limit the amount of credit risk that may be assumed in the investment portfolio and through hedging activities.

A significant portion of the Company's loan portfolio consists of commercial real estate loans, including owner occupied properties, non-owner-occupied properties, and other commercial properties. These types of loans are generally viewed as having more risk of default than residential real estate loans and depend on cash flows from the owner’s business or the property’s tenants to service the debt. The borrower’s cash flows may be affected significantly by general economic conditions, a downturn in the local economy or in occupancy rates in the market where the property is located, any of which could increase the likelihood of default. Commercial real estate loans also typically have larger loan balances, and, therefore, the deterioration of one or a few of these loans could cause a significant increase in the percentage of the Company's non-performing loans. An increase in non-performing loans could result in a loss of earnings from these loans, an increase in the provision for credit losses for loans, and an increase in charge-offs, all of which could have a material adverse effect on the Company's business, financial condition, and results of operations.

The banking regulatory agencies have recently expressed concerns about weaknesses in the current commercial real estate market. Banking regulators generally give commercial real estate lending greater scrutiny and may require banks with higher levels of commercial real estate loans to implement enhanced risk management practices, including stricter underwriting, internal controls, risk management policies, more granular reporting, and portfolio stress testing, as well as possibly higher levels of allowances for credit losses and capital levels as a result of commercial real estate lending

4

growth and exposures. If the Company's banking regulators determine that our commercial real estate lending activities are particularly risky and are subject to such heightened scrutiny, the Company may incur significant additional costs or be required to restrict certain of our commercial real estate lending activities. Furthermore, failures in the Company's risk management policies, procedures and controls could adversely affect our ability to manage this portfolio going forward and could result in an increased rate of delinquencies in, and increased losses from, this portfolio, which could have a material adverse effect on the Company's business, financial condition, and results of operations.

The following summarizes and describes the Company’s various loan categories and the underwriting standards applied to each:

Commercial Loans

This category includes credit extensions to commercial and industrial borrowers. Business assets, including accounts receivable, inventory and/or equipment, typically secure these credits. The commercial loan segment includes commercial loans secured by owner occupied real estate. In appropriate instances, extensions of credit in this category are subject to collateral advance formulas. Balance sheet strength and profitability are considered when analyzing these credits, with special attention given to historical, current and prospective sources of cash flow, and the ability of the customer to sustain cash flow at acceptable levels. The Bank’s policy permits flexibility in determining acceptable debt service coverage ratios. Personal guarantees are frequently required; however, as the financial strength of the borrower increases, the Bank’s ability to obtain personal guarantees decreases. In addition to economic risk, this category is impacted by the strength of the borrower’s management, industry risk and portfolio concentration risk each of which are also monitored and considered during the underwriting process.

Commercial Loans Secured by Non-Owner Occupied Real Estate

This category includes various types of loans, including acquisition and construction of investment property. Maximum term, minimum cash flow coverage, leasing requirements, maximum amortization and maximum loan to value ratios are controlled by the Bank’s credit policy and follow industry guidelines and norms, and regulatory limitations. Personal guarantees are frequently required on CRE loans especially if there is a speculative component to the credit. In addition to economic risk, this category is subject to geographic and portfolio concentration risk, each of which are monitored and considered in underwriting.

The Company utilizes a robust and diligent risk management framework to monitor the non-owner occupied commercial real estate segment of the portfolio. This analysis considers more forward looking credit metrics such as stress test results and underwriting trend data, coupled with risk tolerance and concentration guidelines. The process is intended to allow identification of emerging risk, in part, to determine any future change to lending policy, underwriting practices or broader lending strategy prior to any indication of performance deterioration.

The commercial real estate loan segment includes the non-owner occupied commercial real estate loan classes of retail, multi-family, and other. At December 31, 2023, the Bank’s non-owner occupied commercial real estate loan concentration stood at 375% of total regulatory capital. It should be noted that this ratio increased from 350% at December 31, 2022 due to growth in non-owner occupied commercial real estate loan balances as well as a slight decrease in total regulatory capital between years. Further, non-owner occupied commercial real estate loans represented 49.3% and 45.5% of total loans as of December 31, 2023 and 2022, respectively.

5

The following table presents our non-owner occupied commercial real estate loan portfolio by property type.

DECEMBER 31, 2023 | ||||||||||||

COMMERCIAL | COMMERCIAL | |||||||||||

REAL ESTATE | REAL ESTATE | OTHER COMMERCIAL | ||||||||||

(NON-OWNER OCCUPIED) - | (NON-OWNER OCCUPIED) - | REAL ESTATE | ||||||||||

| RETAIL |

| MULTI-FAMILY |

| (NON-OWNER OCCUPIED) |

| TOTAL | |||||

(IN THOUSANDS) | ||||||||||||

1-4 unit residential | $ | — | $ | — | $ | 27,038 | $ | 27,038 | ||||

Multi-family |

| — |

| 92,037 |

| — |

| 92,037 | ||||

Mixed use - apartments & retail/office | — | 17,971 | — | 17,971 | ||||||||

Retail strip plaza | 45,691 | — | — | 45,691 | ||||||||

Mall | 3,995 | — | — | 3,995 | ||||||||

Major shopping center with anchor tenants | 29,471 | — | — | 29,471 | ||||||||

Commercial office - urban | — | — | 13,734 | 13,734 | ||||||||

Commercial office - suburban | — | — | 9,404 | 9,404 | ||||||||

Mixed use - retail/office | — | — | 34,144 | 34,144 | ||||||||

Hotel/motel |

| — |

| — |

| 43,546 |

| 43,546 | ||||

Retail/service shops |

| 82,804 |

| — |

| — |

| 82,804 | ||||

Personal care/hospital/medical office |

| — |

| — |

| 20,291 |

| 20,291 | ||||

Manufacturing/warehouse |

| — |

| — |

| 85,981 |

| 85,981 | ||||

Other |

| — |

| — |

| 68 |

| 68 | ||||

Land acquisition and development |

| — |

| — |

| 6,080 |

| 6,080 | ||||

Total | $ | 161,961 | $ | 110,008 | $ | 240,286 | $ | 512,255 | ||||

Residential Mortgages

This category includes mortgages that are secured by residential property. Underwriting of loans within this category is pursuant to Freddie Mac/Fannie Mae underwriting guidelines, with the exception of Community Loan Program loans, which have specialized internal loan program standards. The major risk in this category is that a significant downward economic trend would increase unemployment and cause payment default. The Bank does not engage, and has never engaged, in subprime residential mortgage lending.

Secondary Market Activities

The residential lending department of the Bank continues to originate one-to-four family mortgage loans for customers, some of which are sold to outside investors in the secondary market and some of which are retained for the Bank’s portfolio. Mortgages sold in the secondary market are sold to investors on a “flow” basis; mortgages are priced and delivered on a “best efforts” pricing basis, with servicing released to the investor. As previously stated above, Fannie Mae/Freddie Mac guidelines are used in underwriting all mortgages with the exception of a limited amount of Community Reinvestment Act (CRA) loans and internal special programs. Mortgages with longer terms, such as 30-year, FHA, and VA loans, are usually sold. The remaining production of the department includes construction, adjustable rate mortgages, and quality non-salable loans. These loans are usually kept in the Bank’s portfolio.

Consumer Loans

This category includes consumer installment loans and revolving credit plans. A meaningful portion of this portfolio consists of home equity loans secured by residential real estate. Underwriting is pursuant to industry norms and guidelines. The major risk in this category is a significant economic downturn.

INVESTMENTS

The strategic focus of the investment securities portfolio is managed for liquidity and earnings in a prudent manner that is consistent with proper bank asset/liability management and current banking practices. The objectives of portfolio management include consideration of proper liquidity levels, interest rate and market valuation sensitivity, and profitability. The investment portfolio of the Company and its subsidiaries are proactively managed, including in accordance with federal and state laws and regulations and in accordance with generally accepted accounting principles (GAAP). All holdings must meet standards documented in its investment policy, unless otherwise approved by the Company’s CEO or the Asset/Liability Management Committee.

6

The investment portfolio is primarily made up of AAA rated agency mortgage-backed securities, high quality corporate securities, taxable municipal securities, and agency securities. Management strives to maintain a portfolio duration that is less than 60 months.

Investment securities classified as held to maturity are carried at amortized cost while investment securities classified as available for sale are reported at fair market value with unrealized aggregate appreciation/depreciation excluded from income and credited/charged to accumulated other comprehensive income (loss) within shareholders’ equity on a net of tax basis. The Company measures current expected credit losses on debt securities in accordance with ASU 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. See Note 1 within the Notes to Consolidated Financial Statements for information regarding the Company’s calculation of the allowance for credit losses on both the held to maturity and available for sale investment securities portfolios.

The following table sets forth the weighted average yield for each type of investment security and range of maturity as of December 31, 2023. Yields are not presented on a tax-equivalent basis, but are based upon the cost basis and are weighted for the scheduled maturity.

Investment securities available for sale:

AT DECEMBER 31, 2023 | |||||||||||||||

TOTAL | |||||||||||||||

|

|

|

| U.S. AGENCY | INVESTMENT | ||||||||||

MORTGAGE- | SECURITIES | ||||||||||||||

CORPORATE | BACKED | AVAILABLE | |||||||||||||

U. S. AGENCY | MUNICIPAL | BONDS | SECURITIES | FOR SALE | |||||||||||

Within 1 year | 5.20 | % |

| 2.71 | % |

| 5.16 | % |

| — | % | 4.48 | % | ||

After 1 year but within 5 years | 2.69 |

| 3.01 |

| 5.95 |

| 2.83 | 5.41 | |||||||

After 5 years but within 10 years | 1.67 |

| 2.41 |

| 7.18 |

| 2.81 | 5.50 | |||||||

Over 10 years | 2.69 |

| — |

| 4.31 |

| 3.09 | 3.09 | |||||||

Total | 2.22 |

| 2.71 |

| 6.40 |

| 3.07 | 4.13 | |||||||

Investment securities held to maturity:

AT DECEMBER 31, 2023 | |||||||||||||||

TOTAL | |||||||||||||||

|

|

|

| U.S. AGENCY | INVESTMENT | ||||||||||

CORPORATE | MORTGAGE- | SECURITIES | |||||||||||||

BONDS AND | BACKED | HELD TO | |||||||||||||

U. S. AGENCY | MUNICIPAL | OTHER | SECURITIES | MATURITY | |||||||||||

Within 1 year | — | % |

| 3.58 | % |

| 1.16 | % |

| 2.82 | % | 2.59 | % | ||

After 1 year but within 5 years | — |

| 3.37 |

| 4.21 |

| — | 3.48 | |||||||

After 5 years but within 10 years | 2.01 |

| 2.84 |

| 7.36 |

| 3.86 | 2.91 | |||||||

Over 10 years | — |

| 2.82 |

| 7.44 |

| 3.87 | 3.96 | |||||||

Total | 2.01 |

| 3.08 |

| 4.58 |

| 3.83 | 3.43 | |||||||

DEPOSITS

The Bank believes it has a stable core deposit base made up of traditional commercial bank products that exhibit modest fluctuation during the year, other than jumbo certificates of deposit and certain municipal deposits, which demonstrate some seasonality. The Company also utilizes certain Trust Company specialty deposits related to the ERECT funds as a funding source, which serve as an alternative to wholesale borrowings and can exhibit some limited degree of volatility. The Company does not use brokered deposits as a funding source.

7

The following table sets forth the average balance of the Company’s deposits and average rates paid thereon for the past two calendar years:

| 2023 |

| 2022 |

| |||||||

(IN THOUSANDS, EXCEPT PERCENTAGES) | |||||||||||

Demand: |

|

| |||||||||

Non-interest bearing | $ | 191,580 |

| — | % | $ | 215,196 |

| — | % | |

Interest bearing |

| 225,713 |

| 1.80 |

| 227,838 |

| 0.53 | |||

Savings |

| 127,539 |

| 0.10 |

| 137,845 |

| 0.10 | |||

Money market |

| 302,964 |

| 2.46 |

| 289,674 |

| 0.69 | |||

Time deposits (1) |

| 306,044 |

| 3.06 |

| 285,760 |

| 1.08 | |||

Total deposits | $ | 1,153,840 |

| 2.18 | % | $ | 1,156,313 |

| 0.68 | % | |

| (1) | Time deposits include certificates of deposit (CDs) and individual retirement accounts (IRAs). |

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against loss. The Bank is an FDIC-insured institution, therefore, deposits are insured up to the standard insurance amount of $250,000 per depositor. As of December 31, 2023 and 2022, the estimated amount of uninsured deposits was $384.5 million and $316.5 million, respectively. The estimate of uninsured deposits was done at a single account level and does not take into account total customer balances in the Bank. It should be noted that approximately 50% of these uninsured deposits relate to public funds from municipalities, government entities, and school districts which by law are required to be collateralized with investment securities or FHLB letters of credit to protect these depositor funds.

The maturities on CDs with balances that exceed the FDIC insurance limit of $250,000 as of December 31, 2023, are as follows:

| (IN THOUSANDS) | ||

MATURING IN: |

|

| |

Three months or less | $ | 27,194 | |

Over three through six months |

| 13,655 | |

Over six through twelve months |

| 36,248 | |

Over twelve months |

| 4,734 | |

Total | $ | 81,831 | |

AMERISERV TRUST AND FINANCIAL SERVICES COMPANY

AmeriServ Trust and Financial Services Company is a trust company organized under Pennsylvania law in October 1992. Its staff of approximately 44 professionals administers assets valued at approximately $2.5 billion that are not recognized on the Company’s balance sheet at December 31, 2023. The Trust Company focuses on wealth management. Wealth management includes personal trust products and services such as personal investment portfolio management, estate planning and administration, custodial services and pre-need trusts. Also, institutional trust products and services such as 401(k) plans, defined benefit and defined contribution employee benefit plans, and individual retirement accounts are included in this segment. This segment also includes financial services, which provide the sale of mutual funds, annuities, and insurance products. The wealth management business also includes the union collective investment funds, the ERECT funds, which are designed to use union pension dollars in construction projects that utilize union labor. At December 31, 2023, the Trust Company had total assets of $6.4 million and total shareholders’ equity of $6.1 million. In 2023, the Trust Company contributed earnings to the Company as its gross revenue amounted to $10.4 million and the net income contribution was $1.1 million. The Trust Company is subject to regulation and supervision by the Federal Reserve Bank of Philadelphia and the PDB.

MONETARY POLICIES

Commercial banks are affected by policies of various regulatory authorities including the Board of Governors of the Federal Reserve System (the Federal Reserve). An important function of the Federal Reserve is to regulate the national supply of bank credit. Among the instruments of monetary policy used by the Federal Reserve are: open market operations in U.S. Government securities, changes in the federal funds rate and discount rate on member bank borrowings, and changes in reserve requirements on bank deposits. These means are used in varying combinations to influence overall growth of bank loans, investments, and deposits, and may also affect interest rate charges on loans or

8

interest paid for deposits. The monetary policies of the Federal Reserve have had a significant effect on the operating results of commercial banks in the past and are expected to continue to do so in the future.

COMPETITION

Our subsidiaries face strong competition from other commercial banks, savings banks, credit unions, savings and loan associations, and other financial or investment service institutions for business in the communities they serve. Several of these institutions are affiliated with major banking and financial institutions which are substantially larger and have greater financial resources than the Bank and the Trust Company. As the financial services industry continues to consolidate, the scope of potential competition affecting our subsidiaries will also increase. Brokerage houses, consumer finance companies, insurance companies, financial technology firms, and pension trusts are important competitors for various types of financial services. Personal and corporate trust investment counseling services are offered by insurance companies, other firms, and individuals. In addition, some of these competitors, such as credit unions, are subject to a lesser degree of regulation or taxation than that imposed on us.

MARKET AREA & ECONOMY

After a year of the most aggressive Fed tightening in four decades in 2022, most economists, including the Federal Reserve staff, expected a recession when 2023 began. The recession never happened, making resilience the economic word of 2023. In early March, two regional banks failed in quick succession, followed by a third a few weeks later, rocking the financial markets. After weeks of stalemate, Congressional leaders eventually agreed to suspend the debt ceiling in late May, but ratings agencies viewed the systemic dysfunction as worthy of a credit downgrade that further rocked markets. Recession fears subsided over the summer when consumer services spending soared. In the third quarter of 2023, gross domestic product (GDP) grew 4.9% annualized, the fastest since mid-2021, further quelling recession fears. Inflation subsided at an accelerating pace all year. Fed rhetoric was still hawkish at the September Federal Open Market Committee (FOMC) meeting, but the FOMC stopped hiking in July. At the December FOMC meeting, a dovish pivot by Chair Powell suggested the focus for 2024 will shift to deciding when to end quantitative tightening and start to cut fed funds. The S&P 500 rose 23.8% in 2023. The 10-year U.S. Treasury yield started and ended the year at 3.87%. There was plenty of movement in the interim. GDP far exceeded expectations in 2023, thanks to consumer and government spending. The 2023 budget was more stimulative than expected, and a surge in late filings for 2021 Employer Tax Credits further lifted demand. A resilient labor market allowed consumers to maintain elevated spending. GDP growth and falling inflation are the key ingredients to a soft landing. The pace of nonfarm payrolls growth slowed through 2023 but remained solid through the end of the year, even with the United Auto Workers strike in October. The labor market has become more balanced, with job openings falling and wage growth moderating. The Fed’s 25 basis point hike in July could very well be the last for this cycle. History suggests the longer the Fed pauses, the larger the chance the next move is in the other direction. December FOMC minutes indicate Fed officials are already discussing rate cuts, but with no urgency.

Johnstown, Pennsylvania, where the Company is headquartered, continues to have a cost of living that is lower than the national average. Johnstown is home to The University of Pittsburgh at Johnstown, Pennsylvania Highlands Community College and Conemaugh Health System. The high-tech defense industry is the main non-health care staple of the Johnstown economy, with the region fulfilling many federal government contracts, punctuated by one of the premier defense trade shows in the U.S., the annual Showcase for Commerce. The city also hosts annual events such as the Flood City Music Festival that draws several thousand visitors. The Johnstown, PA MSA unemployment rate decreased from a 5.1% average in 2022 to a 4.4% average in 2023. The Johnstown, PA MSA continues to have one of the highest jobless rates among the 18 metropolitan statistical areas across the state. Slow economic conditions, coupled with a declining population trend, creates a growth challenge moving forward.

Economic conditions are stronger in the State College market and have demonstrated the same improvement experienced in the national economy. The community is a college town, dominated economically and demographically by the presence of the University Park campus of the Pennsylvania State University. “Happy Valley” is another often-used term to refer to the State College area, including the borough and the townships of College, Harris, Patton, and Ferguson. The unemployment rate for the State College MSA decreased from a 3.2% average in 2022 to a 2.9% average in 2023 and remains one of the lowest of all regions in the Commonwealth. A large percentage of the population in State College falls into the 18 to 34-year-old age group, while potential customers in the Cambria/Somerset markets tend to be over 50 years of age.

9

Hagerstown in Washington County, Maryland offers a rare combination of business advantages providing a major crossroads location that is convenient to the entire East Coast at the intersection of I-81 and I-70. It has a workforce of over 400,000 with strengths in manufacturing and technology. It also offers an affordable cost of doing business and living, all within an hour of the Washington, D.C./Baltimore regions. There are also plenty of facilities and land slated for industrial/commercial development. Hagerstown has become a choice location for manufacturers, financial services, and distribution companies. The Hagerstown, MD-Martinsburg, WV MSA unemployment rate decreased from a 3.4% average in 2022 to a 2.8% average in 2023.

The Company also has loan production offices in Wilkins Township in Allegheny County and Altoona in Blair County, Pennsylvania. Wilkins Township in Allegheny County, Pennsylvania is located 15 miles east of the city of Pittsburgh. While the city is historically known for its steel industry, today its economy is largely based on healthcare, education, technology and financial services. The city of Pittsburgh is home to many colleges, universities and research facilities, the most well-known of which are Carnegie Mellon University, Duquesne University and the University of Pittsburgh. Pittsburgh is rich in art and culture. Pittsburgh museums and cultural sites include the Andy Warhol Museum, the Carnegie Museum of Art, the Frick Art & Historical Center, and Pittsburgh Center for the Arts among numerous others. Pittsburgh is also the home of the Pirates, Steelers and Penguins. The unemployment rate for the Pittsburgh MSA decreased from a 4.3% average in 2022 to a 3.7% average in 2023.

Altoona is the business center of Blair County, Pennsylvania with a strong retail, government and manufacturing base. The top field of employment in Altoona and the metro area is healthcare. Its location along I-99 draws from a large trade area over a wide geographic area that extends to State College and Johnstown. It serves as the headquarters for Sheetz Corporation, which ranks on Forbes’ list of the top privately owned companies. In addition to being located adjacent to I-99 and a major highway system, Altoona also has easy access to rail and air transportation. The average unemployment rate in the Altoona MSA decreased from 4.1% in 2022 to 3.5% in 2023.

HUMAN CAPITAL RESOURCES

The Company’s long-term growth and success depends on its ability to attract, develop and retain a high-performing and diverse workforce. The Company strives to provide a work environment that promotes collaboration, productivity, and employee engagement, which in turn drives both employee and customer success, as well as benefits the communities in which the Company does business.

The Company’s executive team and the Compensation/Human Resources Committee of the Board of Directors oversee the strategic management of the Company’s human capital resources, and the Company’s Human Resources Department manages the day-to-day of those resources.

Employee profile

The Company employed 323 people as of December 31, 2023 in full- and part-time positions. Approximately 149 non-supervisory employees of the Company are represented by the United Steelworkers AFL-CIO-CLC, Local Union 2635-06. The Company is under a four-year labor contract with the United Steelworkers Local, which expires on October 15, 2025. The contract calls for annual wage increases of 2% during the life of the contract. The Company has not experienced a work stoppage since 1979. Unionization in financial institutions remains exceptionally low with less than 0.25% of banks nationwide being covered by a collective bargaining agreement. This unique unionization situation creates both challenges and opportunities for the Company. The key goals of organized labor are to provide their members with strong wages and benefits, stable jobs, and safe and respectable workplaces. As a result of these key union goals, the Company’s salaries and benefit costs are higher than its non-union peers as we offer good wages and strong benefits which include affordable health care and strong retirement benefits with the majority of current union employees participating in a defined benefit pension plan. The Company has consistently viewed its positive union relationships as a potential source of additional revenue. Examples of success in these efforts include the previously mentioned ERECT Fund where the wealth management group is trustee for this $243 million fund whose purpose is to invest in commercial construction projects with the requirement that they utilize union labor. The Bank has also been a preferred mortgage and consumer loan provider for the Pennsylvania State Education Association for almost 10 years which provides us with the opportunity to expand our lending in these products throughout Pennsylvania. Since inception of the partnership, the Bank has funded over $315 million in mortgage and consumer loans to unionized teachers and their family members.

10

Competitive Compensation

As part of the Company’s compensation philosophy, market competitive programs are maintained for employees to attract and retain top talent. In addition to competitive base wages, additional programs include health and welfare benefits, a 401(k) Plan, flexible spending accounts, paid time off, family leave, and employee assistance programs. Some employees participate in a defined benefit pension plan. In addition, the Company promotes health and wellness by encouraging work-life balance and, where appropriate, offering flexible work schedules. The Company has also adopted a hybrid remote work policy for certain positions.

Talent and Promoting Diversity

A core tenet of the Company’s talent philosophy is to both develop talent from within and supplement with external hires. Whenever possible, the Company seeks to fill positions by promotion and transfer from within the organization. The Company’s talent acquisition team uses internal and external resources to recruit highly skilled and talented candidates; employee referrals are also encouraged.

The Company is dedicated to recruitment and career development practices that support its employees and promotes diversity in its workforce at all levels of the Company. The Company is committed to having a workforce that reflects the communities in which it serves. The Company strives to promote inclusion through defined Company values and behaviors. With the support from the Board of Directors, the Company continues to explore additional diversity, equity, inclusion, and belonging efforts through multiple approaches to inclusion: candidates, employees, and the marketplace. The Company is focused on sourcing and hiring with fair and equitable approaches, creating an environment where all employees can develop and thrive.

INDUSTRY REGULATION

The banking and trust industry, and the operation of bank holding companies, is highly regulated by federal and state law, and by numerous regulations adopted by the federal and state banking agencies. Bank regulation affects all aspects of conducting business as a bank, including such major items as minimum capital requirements, limits on types and amounts of investments, loans and other assets, as well as borrowings and other liabilities, and numerous restrictions or requirements on the loan terms and other products made available to customers, particularly consumers. Federal deposit insurance from the Federal Deposit Insurance Corporation (FDIC) is required for all banks in the United States, and maintaining FDIC insurance requires observation of the various rules of the FDIC, as well as payment of deposit insurance premiums. New branches, or acquisitions or mergers, are required to be pre-approved by the responsible agency, which in the case of the Company and the Bank is the Federal Reserve and the PDB. The Bank provides detailed financial information to its regulators, including a quarterly call report that is filed pursuant to detailed prescribed instructions to ensure that all U.S. banks report the same way. The U.S. banking laws and regulations are frequently updated and amended, especially in response to crises in the financial industry, such as the global financial crisis of 2008, which resulted in the Dodd-Frank Wall Street Reform and Consumer Protection Act enacted in 2010 (the Dodd-Frank Act), a statute affecting many facets of the financial industry. The Economic Growth, Regulatory Relief, and Consumer Protection Act was enacted into law in 2018 and was designed to ease certain restrictions imposed by the Dodd-Frank Act.

While it is impractical to discuss all laws and regulations that regularly affect the business of the Company and its subsidiaries, set forth below is an overview of some of the major provisions and statutes that apply.

CAPITAL REQUIREMENTS

One of the most significant regulatory requirements for banking institutions is minimum capital, imposed as a ratio of capital to assets. The Federal Deposit Insurance Act, as amended (FDIA), identifies five capital categories for insured depository institutions: well capitalized, adequately capitalized, undercapitalized, significantly undercapitalized and critically undercapitalized. It requires U.S. federal bank regulatory agencies to implement systems for prompt corrective action for insured depository institutions that do not meet minimum capital requirements based on these categories. Both federal and state banking regulation impose progressively more restrictive constraints on operations, management and capital distributions, depending on the category in which an institution is classified. Unless a bank is well capitalized, it is subject to restrictions on its ability to utilize brokered deposits and on other aspects of its operations. Generally, a bank is prohibited from paying any dividend or making any capital distribution or paying any management fee to its holding company if the bank would thereafter be undercapitalized.

11

Minimum Capital | Well |

| |||

| Plus Buffer |

| Capitalized |

| |

Common equity tier 1 capital ratio |

| 7.00 | % | 6.50 | % |

Tier 1 capital ratio |

| 8.50 | % | 8.00 | % |

Total capital ratio |

| 10.50 | % | 10.00 | % |

DIVIDEND RESTRICTIONS

The primary source of cash to pay dividends, if any, to the Company’s shareholders and to meet the Company’s obligations is dividends paid to the Company by the Bank and the Trust Company. Dividend payments by the Bank to the Company are subject to the laws of the Commonwealth of Pennsylvania, the Banking Code, the FDIA and the regulation of the PDB and the Federal Reserve. Under the Banking Act and the FDIA, a bank may not pay any dividends if, after paying such dividends, it would be undercapitalized under applicable capital requirements. In addition to these explicit limitations, the federal regulatory agencies are authorized to prohibit a banking subsidiary or bank holding company from engaging in unsafe or unsound banking practices. Depending upon the circumstances, the agencies could take the position that paying a dividend would constitute an unsafe or unsound banking practice.

It is the policy of the Federal Reserve that bank holding companies should generally pay cash dividends on common stock only out of income available from the immediately preceding year and only if prospective earnings retention is consistent with the organization’s expected future needs and financial condition. The policy provides that bank holding companies should not maintain a level of cash dividend that undermines the bank holding company’s ability to serve as a source of strength to its banking subsidiary. A bank holding company may not pay dividends when it is insolvent.

For more information regarding quarterly cash dividends, see Part II, Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities below.

PRIVACY PROVISIONS

Federal banking regulators adopted rules that limit the ability of banks and other financial institutions to disclose non-public information about customers to non-affiliated third parties. These limitations require disclosure of privacy policies to consumers and, in some circumstances, allow consumers to prevent disclosure of certain personal information to non-affiliated third parties. The privacy provisions affect how consumer information is transmitted through diversified financial companies and conveyed to outside vendors. The Company believes it is in compliance with the various provisions.

USA PATRIOT ACT

A major focus of governmental policy on financial institutions has been aimed at combating money laundering and terrorist financing. The USA Patriot Act substantially broadened the scope of United States anti-money laundering laws and regulations by imposing significant new compliance and due diligence obligations, creating new crimes and penalties and expanding the extra-territorial jurisdiction of the United States. The United States Treasury Department has issued and, in some cases, proposed a number of regulations that apply various requirements of the USA Patriot Act to financial institutions. These regulations impose obligations on financial institutions to maintain appropriate policies, procedures and controls to detect, prevent and report money laundering and terrorist financing and to verify the identity of their customers. Failure of a financial institution to maintain and implement adequate programs to combat money laundering and terrorist financing, or to comply with all of the relevant laws or regulations, could have serious legal and reputational consequences for the Company.

Community Reinvestment Act

All FDIC-insured institutions have a responsibility under the Community Reinvestment Act (CRA) and related regulations to help meet the credit needs of their communities, including low- and moderate-income neighborhoods. In connection with its examination of a state-chartered bank, the federal bank regulators are required to assess an institution’s record of compliance with the CRA. On October 24, 2023, the FDIC, the Federal Reserve Board, and the Office of the Comptroller of the Currency issued a final rule to strengthen and modernize the CRA regulations. Under the final rule, the asset size thresholds were updated to account for changes in the banking industry as follows: (a) “small banks” with assets less than $600 million (from less than $376 million), (b) “intermediate banks” with assets between $600 million and $2 billion (from between $376 million and $1.503 billion), and (c) “large banks” with assets greater than or equal to $2 billion (from $1.503 billion), each as adjusted for inflation subsequently. The assets as of December

12

31st in both of the prior two calendar years will be used to determine the appropriate size threshold. The agencies will evaluate large banks under four performance tests: the Retail Lending Test, the Retail Services and Products Test, the Community Development Financing Test, and the Community Development Services Test. For intermediate banks, the two performance tests will be: Retail Lending Test and the existing CD test, which is the default but banks can opt-in to the CD Financing Test. The rule also exempts small and intermediate banks from new data collection requirements that apply to banks with assets of at least $2 billion and limits certain data collection and reporting requirements to large banks with assets greater than $10 billion. The applicability date for the majority of the provisions in the CRA regulations is January 1, 2026, and additional requirements will be applicable on January 1, 2027.

FDIC Insurance of Certain Accounts and Regulation by the FDIC

The Bank is an FDIC insured financial institution whereby the FDIC provides deposit insurance for a certain maximum dollar amount per customer. The Bank, as is true for all FDIC insured banks, is subject to deposit insurance assessments as determined by the FDIC.

Under the FDIC’s risk-based deposit premium assessment system, the assessment rates for an insured depository institution (IDI) are determined by an assessment rate calculator, which is based on a number of elements that measure the risk each institution poses to the Deposit Insurance Fund (DIF). As a result of the Dodd-Frank Act, the calculated assessment rate is applied to average consolidated assets less the average tangible equity of the IDI during the assessment period to determine the dollar amount of the quarterly assessment. Under the current system, premiums are assessed quarterly and could increase if, for example, criticized loans and leases and/or other higher risk assets increase or balance sheet liquidity decreases. In addition, the FDIC can impose special assessments in certain instances. Deposit insurance assessments fund the DIF.

On October 18, 2022, the FDIC adopted a final rule that increased initial base deposit insurance assessment rates by 2 basis points, beginning with the first quarterly assessment period of 2023. Due to the decline in the DIF reserve ratio below the statutory minimum of 1.35% as of June 30, 2020, caused by extraordinary growth in insured deposits during the first and second quarters of 2020, the FDIC established a Restoration Plan in September 2020 to restore the DIF reserve ratio to meet or exceed the statutory minimum of 1.35% within eight years. This 2020 plan did not include an increase in the deposit insurance assessment rate. On June 21, 2022, however, the FDIC adopted an Amended Restoration Plan and notice of proposed rulemaking to increase the deposit insurance assessment rates as it was otherwise at risk of not reaching the statutory minimum by the statutory deadline of September 30, 2028. The proposed rule was adopted as final without change.

Also, in the final rule adopted on October 18, 2022, the FDIC incorporated Accounting Standards Update (ASU) 2022-02, Financial Instruments - Credit Losses (Topic 326) Troubled Debt Restructurings and Vintage Disclosures in the risk-based deposit insurance assessment system applicable to all large and highly complex IDIs. In March 2022, the FASB issued ASU 2022-02, which eliminates accounting guidance for troubled debt restructurings (TDRs) and introduces new disclosures and enhances existing disclosures concerning certain loan refinancings and restructurings when a borrower is experiencing financial difficulty. The FDIC final rule amends the assessment regulations to include a new term, “modifications to borrowers experiencing financial difficulty,” in two financial measures—the underperforming assets ratio and the higher-risk assets ratio – used to determine deposit insurance assessments for large and highly complex IDIs. This final rule was effective January 1, 2023, and applicable to the first quarterly assessment period of 2023.

On November 16, 2023, the FDIC adopted a final rule on special assessment to recover the losses to the DIF from the protection of uninsured depositors following the closures of Silicon Valley Bank, Santa Clara, CA, and Signature Bank, New York, NY during March 2023. The assessment base for the special assessment is equal to an IDI’s estimated uninsured deposits, reported for the quarter that ended December 31, 2022, adjusted to exclude the first $5 billion in estimated uninsured deposits from the IDI, or for IDIs that are part of a holding company with one or more subsidiary IDIs, at the banking organization level. The FDIC will collect the special assessment at an annual rate of approximately 13.4 basis points, over eight quarterly assessment periods. The FDIC retains the ability to cease collection early, extend the special assessment collection period, and impose a final shortfall special assessment to collect the difference between actual losses and the amounts collected after the receiverships for Silicon Valley Bank and Signature Bank terminate. The final rule will be effective April 1, 2024, with the first collection for the special assessment reflected on the invoice for the first quarterly assessment period of 2024 with a payment date of June 28, 2024.

13

AVAILABLE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the SEC. These filings are available to the public on the internet at the SEC’s website at http://www.sec.gov.

Our internet address is http://www.ameriserv.com. We make available, free of charge on http://www.ameriserv.com, our annual, quarterly and current reports, and amendments to those reports, as soon as reasonably practical after we electronically file such material with, or furnish it to, the SEC.

ITEM 1A. RISK FACTORS

Not applicable.

ITEM 1B. UNRESOLVED STAFF COMMENTS

The Company has no unresolved staff comments from the SEC for the reporting periods presented.

ITEM 1C. CYBERSECURITY

The Company maintains comprehensive and continually evolving processes for assessing, identifying, and managing material risks from cybersecurity threats, including any potential unauthorized occurrence on, or conducted through, the Company’s information systems that may result in adverse effects on the confidentiality, integrity, or availability of such systems or any information residing on such systems. The processes relating to cybersecurity threats are integrated into the Company’s overall risk management processes, which are overseen by the Board of Directors.

Risk Management and Strategy

The Company’s Enterprise Risk Management Policy assists the Board of Directors and management in clarifying their tolerance for identifying those credit, market, liquidity, operational, legal, compliance, strategic, reputation and security (information and physical) risks that have the potential to cause material financial harm to the institution, as well as describing a methodology for determining the proper level of controls to manage and mitigate those risks. Cybersecurity is a critical component of risk management, given the increasing reliance on technology and the increasing cybersecurity threat landscape. The Information Security Program is built on the Federal Financial Institutions Examination Council (FFIEC) IT Handbooks, National Institute of Standards and Technology (NIST) Cybersecurity Framework, the Center for Internet Security (CIS) Cybersecurity Controls (CSC), and industry best practice. The Information Security Program utilizes a defense in depth strategy that leverages multiple security measures to protect Company assets and information.

The Board of Directors is responsible for overseeing management’s development and execution of the Company’s risk management process. Risk management is administered by a senior management team called the Management Enterprise Risk Committee (MERC). Periodic risk assessments are performed to identify technical and physical risks to information systems. These risk assessments identify internal and external threats that could cause a cybersecurity incident, assessing the likelihood of potential impact of those threats, and assessing the measures and controls in place to manage the risks. As per FFIEC guidance, a Change Management Policy and Committee are in place to manage changes to technology and systems. Information Security is a member of this Committee to evaluate changes for information security impact.

The Company leverages internal and external auditors to periodically review information technology and information security policy, processes, and controls to ensure they meet regulatory compliance and operate effectively. Independent penetration testing is performed annually.

The Company maintains an Incident Response Plan and a Crisis Communication Plan that provide documented guidelines for handling potential threats and taking appropriate measures including timely notification of cybersecurity threats and incidents to senior management and the Board of Directors when appropriate. The Incident Response Plan is managed by the Chief Information Security Officer (CISO) and is reviewed and tested at least annually. The Crisis Communication Plan, managed by the Director of Marketing and Alternative Delivery, is reviewed and tested at least annually.

14

The Company uses third-party vendors to assist in monitoring, detecting, and managing cyber threats, including managed security service monitoring, penetration testing and vulnerability assessment. The Management Enterprise Risk Committee has established risk management guidelines for third-party vendors. Through the Vendor Management Committee, the Company conducts due diligence reviews of third-party vendors before contracts or agreements for provision of services are signed and conducts ongoing due diligence and oversight procedures with the frequency of the procedures determined based on a risk assessment of the services provided. Generally, the Company’s agreements with service providers include requirements related to cybersecurity and data privacy. All such agreements are reviewed periodically. The Company cannot guarantee, however, that such agreements, due diligence, and oversight procedures will prevent a cybersecurity incident from impacting information systems. Moreover, as a result of applicable laws and regulations or applicable contractual provisions, the Company may be held responsible for cybersecurity incidents attributed to its service providers in relation to any data that the Company shares with such providers.

Notwithstanding our efforts at cybersecurity, no system of prevention is impenetrable, and we cannot guarantee that we will be successful in preventing or mitigating a cybersecurity incident that could have a material adverse effect on us. To date, the Company has not detected any material cybersecurity incident to our own systems. However, during the second quarter of 2023, a prominent third-party vendor experienced a cybersecurity incident due to a previously unknown (i.e., zero-day) vulnerability in a popular file sharing software the vendor used called MOVEit Transfer. For further information regarding this incident, please see our Quarterly Report on Form 10-Q for the quarter ended June 30, 2023 filed on August 10, 2023 and our Quarterly Report on Form 10-Q for the quarter ended September 30, 2023 filed on November 9, 2023. Future cybersecurity incidents could, however, materially affect our business strategy, results of operations, or financial condition.

Governance

The Company’s information technology resources are managed by the Information Technology Department, which is responsible for the first line of defense – identifying, assessing, and managing material risks from cybersecurity threats. The Information Technology Department is managed by the Chief Information Officer (CIO), who reports to the Company’s President and CEO. The present CIO has been employed by the Company in the information technology area for two and a half years and was previously the CISO at the Company for two years. The present CIO has over thirty-five years of IT experience, twelve of that in banking. The CIO holds a current Certified Information Systems Security Professional (CISSP) designation.

The Chief Information Security Officer (CISO) whose responsibilities constitute the second line of defense provides the vision, leadership, and strategies necessary to protect the information security of the Company. The CISO manages policy, procedure, and process to ensure the execution of the Company’s Information Security and Business Continuity/ Disaster Recovery (BC/DR) Programs. The CISO reports directly to the Chief Risk Officer to provide segregation between the first and second line of defense. The Information Security Department, among other duties, supervises internal employee training relating to cybersecurity risks, conducts access reviews relating to the Company’s information systems, and monitors implemented security measures.

The Company has established a Management Technology Committee and a Board Technology Committee. These Committees provide oversight and governance of information technology and the Information Security Program and meet quarterly. The Board Technology Committee’s responsibilities include: (1) monitoring the strategic deployment and usage of Information Technology throughout the Company using reports and presentations from management; (2) oversight of cybersecurity preparedness through information security reports, discussion of internal events and discussion of cybersecurity topics pertinent to the Company and the industry; (3) oversight of activities in support of the Company’s business continuity/disaster recovery program to ensure optimal corporate resiliency in the unlikely event of a disaster; and (4) providing broad strategic guidance on the technology direction of the Company by, among other things, overseeing the development of the AmeriServ Strategic Technology Plan.

ITEM 2. PROPERTIES

The principal offices of the Company and the Bank occupy the five-story AmeriServ Financial building at the corner of Main and Franklin Streets in Johnstown plus eleven floors of the building adjacent thereto. The Company occupies the main office and its subsidiary entities have 14 locations which are owned. Seven additional locations are leased with terms expiring from April 30, 2025 to June 30, 2033.

15

ITEM 3. LEGAL PROCEEDINGS

The Company is subject to various types of lawsuits and claims arising in the ordinary course of business. In the opinion of management, after review and consultation with counsel, there are no material legal proceedings currently pending to which the Company or any of its subsidiaries is a party or of which any of their property is the subject. As discussed further in the Non-Interest Expense section of Item 7, Management’s Discussion and Analysis of Consolidated Financial Position and Results of Operations, during 2023, the Company incurred certain non-interest expenses due to increased legal and professional fees resulting from the activities of an activist investor and a proxy contest relating to the Company’s 2023 annual meeting of shareholders, some of which expenses involved lawsuits brought by the activist investor in connection with the Company’s 2023 annual meeting of shareholders.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

16

PART II

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

COMMON STOCK

As of March 20, 2024, the Company had 2,489 shareholders of record for its common stock. The Company’s common stock is traded on The NASDAQ Stock Market under the symbol “ASRV.” The following table sets forth the actual high and low closing prices and the cash dividends declared per share for the periods indicated:

CASH | |||||||||

PRICES | DIVIDENDS | ||||||||

| HIGH |

| LOW |

| DECLARED | ||||

Year ended December 31, 2023: |

|

|

| ||||||

First Quarter | $ | 4.09 | $ | 3.05 | $ | 0.030 | |||

Second Quarter |

| 3.28 |

| 2.46 |

| 0.030 | |||

Third Quarter |

| 3.33 |

| 2.41 |

| 0.030 | |||

Fourth Quarter |

| 3.28 |

| 2.51 |

| 0.030 | |||

Year ended December 31, 2022: |

|

|

|

|

|

| |||

First Quarter | $ | 4.50 | $ | 3.85 | $ | 0.025 | |||

Second Quarter |

| 4.08 |

| 3.92 |

| 0.030 | |||

Third Quarter |

| 4.03 |

| 3.80 |

| 0.030 | |||

Fourth Quarter |

| 4.10 |

| 3.70 |

| 0.030 | |||

The declaration of cash dividends on the Company’s common stock is at the discretion of the Board, and any decision to declare a dividend is based on a number of factors, including, but not limited to, earnings, prospects, financial condition, regulatory capital levels, applicable covenants under any credit agreements and other contractual restrictions, Pennsylvania law, federal and Pennsylvania bank regulatory law, and other factors deemed relevant. Additionally, the Company does not currently have a common stock repurchase program authorized.

ITEM 6. [RESERVED]

17

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF CONSOLIDATED FINANCIAL CONDITION AND RESULTS OF OPERATIONS (MD&A)

The following discussion and analysis of financial condition and results of operations of the Company should be read in conjunction with the consolidated financial statements of the Company including the related notes thereto, included elsewhere herein.

SELECTED FIVE-YEAR CONSOLIDATED FINANCIAL DATA

AT OR FOR THE YEAR ENDED DECEMBER 31, | ||||||||||||||||

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 | |||||||

(DOLLARS IN THOUSANDS, EXCEPT PER SHARE DATA AND RATIOS) | ||||||||||||||||

SUMMARY OF INCOME STATEMENT DATA: |

|

|

|

|

|

|

|

|

|

| ||||||

Total interest income | $ | 60,860 | $ | 49,058 | $ | 46,669 | $ | 46,882 | $ | 49,767 | ||||||

Total interest expense |

| 24,840 |

| 8,495 |

| 7,586 |

| 10,515 |

| 14,325 | ||||||

Net interest income |

| 36,020 |

| 40,563 |

| 39,083 |

| 36,367 |

| 35,442 | ||||||

Provision for credit losses |

| 7,429 |

| 50 |

| 1,100 |

| 2,375 |

| 800 | ||||||

Net interest income after provision for credit losses |

| 28,591 |

| 40,513 |

| 37,983 |

| 33,992 |

| 34,642 | ||||||

Total non-interest income |

| 16,389 |

| 16,692 |

| 17,761 |

| 16,275 |

| 14,773 | ||||||

Total non-interest expense |

| 49,368 |

| 48,004 |

| 46,970 |

| 44,455 |

| 41,815 | ||||||

Income (loss) before income taxes |

| (4,388) |

| 9,201 |

| 8,774 |

| 5,812 |

| 7,600 | ||||||

Provision (benefit) for income taxes |

| (1,042) |

| 1,753 |

| 1,702 |

| 1,214 |

| 1,572 | ||||||

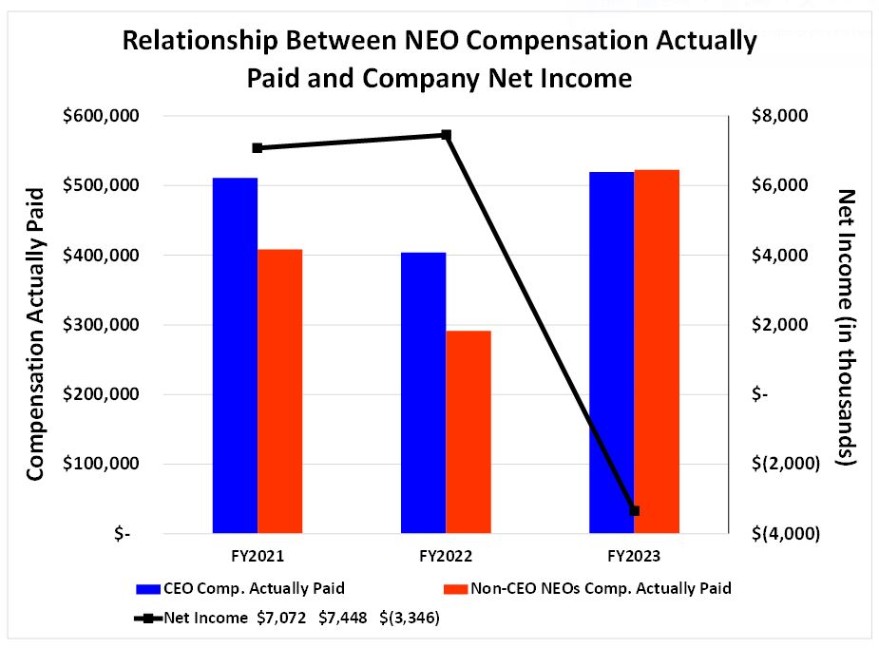

Net income (loss) | $ | (3,346) | $ | 7,448 | $ | 7,072 | $ | 4,598 | $ | 6,028 | ||||||

PER COMMON SHARE DATA: |

|

|

|

|

|

|

|

|

|

| ||||||

Basic earnings per share | $ | (0.20) | $ | 0.44 | $ | 0.41 | $ | 0.27 | $ | 0.35 | ||||||

Diluted earnings per share |

| (0.20) |

| 0.43 |

| 0.41 |

| 0.27 |

| 0.35 | ||||||

Cash dividends declared |

| 0.120 |

| 0.115 |

| 0.100 |

| 0.100 |

| 0.095 | ||||||

Book value at period end |

| 5.96 |

| 6.20 |

| 6.82 |

| 6.12 |

| 5.78 | ||||||

BALANCE SHEET AND OTHER DATA: |

|

|

|

|

|

|

|

|

|

| ||||||

Total assets | $ | 1,389,638 | $ | 1,363,874 | $ | 1,335,560 | $ | 1,282,733 | $ | 1,171,184 | ||||||

Loans and loans held for sale, net of unearned income |

| 1,038,401 |

| 990,825 |

| 986,037 |

| 978,345 |

| 887,574 | ||||||

Allowance for credit losses - loans |

| 15,053 |

| 10,743 |

| 12,398 |

| 11,345 |

| 9,279 | ||||||

Investment securities, net of allowance for credit losses: | ||||||||||||||||

Available for sale |

| 165,711 |

| 179,508 |

| 163,171 |

| 144,165 |

| 141,749 | ||||||

Held to maturity |

| 63,979 |

| 61,878 |

| 53,751 |

| 44,222 |

| 39,936 | ||||||

Deposits |

| 1,158,360 |

| 1,108,537 |

| 1,139,378 |

| 1,054,920 |

| 960,513 | ||||||

Total borrowed funds |

| 115,556 |

| 138,373 |

| 72,837 |

| 114,080 |

| 100,574 | ||||||

Shareholders’ equity |

| 102,277 |

| 106,178 |

| 116,549 |

| 104,399 |

| 98,614 | ||||||

Full-time equivalent employees |

| 307 |

| 315 |

| 304 |

| 299 |

| 309 | ||||||

SELECTED FINANCIAL RATIOS: |

|

|

|

|

|

|

|

|

|

| ||||||

Return on average assets |

| (0.25) | % |

| 0.55 | % |

| 0.52 | % |

| 0.37 | % |

| 0.51 | % | |

Return on average total equity |

| (3.23) |

| 6.83 |

| 6.48 |

| 4.52 |

| 6.02 | ||||||

Loans and loans held for sale, net of unearned income, as a percent of deposits, at period end |

| 89.64 |

| 89.38 |

| 86.54 |

| 92.74 |

| 92.41 | ||||||

Common stock cash dividends as a percent of net income (loss) |

| (61.48) |

| 26.41 |

| 24.14 |

| 37.09 |

| 27.36 | ||||||

Interest rate spread |

| 2.47 |

| 3.11 |

| 3.01 |

| 3.01 |

| 3.05 | ||||||

Net interest margin |

| 2.86 |

| 3.27 |

| 3.15 |

| 3.19 |

| 3.29 | ||||||

Allowance for credit losses - loans as a percentage of loans, net of unearned income, at period end |

| 1.45 |

| 1.08 |

| 1.26 |

| 1.16 |

| 1.05 | ||||||

Non-performing assets as a percentage of loans and other real estate owned, at period end |

| 1.19 |

| 0.52 |

| 0.34 |

| 0.34 |

| 0.26 | ||||||

Net charge-offs as a percentage of average loans |

| 0.35 |

| 0.17 |

| — |

| 0.03 |

| 0.02 | ||||||

18

RESULTS OF OPERATIONS FOR THE YEARS ENDED DECEMBER 31, 2023, 2022, AND 2021

PERFORMANCE OVERVIEW. The following table summarizes some of the Company’s key profitability performance indicators for each of the past three years.

| YEAR ENDED DECEMBER 31, |

| ||||||||

| 2023 |

| 2022 |

| 2021 |

| ||||

(IN THOUSANDS, EXCEPT |

| |||||||||

PER SHARE DATA AND RATIOS) | ||||||||||

Net income (loss) | $ | (3,346) | $ | 7,448 | $ | 7,072 | ||||

Diluted earnings per share |

| (0.20) |

| 0.43 |

| 0.41 | ||||

Return on average assets |

| (0.25) | % |

| 0.55 | % |

| 0.52 | % | |

Return on average equity |

| (3.23) |

| 6.83 |

| 6.48 | ||||

The Company reported a net loss of $3,346,000, or $0.20 per diluted common share, in 2023. This compares to net income of $7,448,000, or $0.43 per diluted common share, for 2022. The net loss was caused primarily by an increased provision for credit losses related to certain commercial real estate loans as well as management’s decision to execute an investment portfolio repositioning strategy. Specifically, Rite Aid, a national tenant in several commercial real estate properties financed by the Bank, declared bankruptcy in the fourth quarter of 2023 resulting in increased credit costs and charge-offs related to these loans. Total non-interest income was lower for the full year of 2023 when compared to last year primarily due to the recognition of a loss on the sale of investment securities in December of 2023. The Company believes that recognizing this loss on the investment securities positions the Company for improved interest earnings from the investment securities portfolio in 2024. Total non-interest expense is higher for the full year of 2023 compared to 2022, due to additional legal and professional services costs caused by litigation and responses to the actions of an activist investor. Overall, the Company’s 2023 net loss reflects the significantly higher provision for credit losses, decreased levels of both net interest income and non-interest income and increased total non-interest expense. Despite the net loss recognized for 2023, the Company continued to see several encouraging new business development results during the year which included a $47.6 million, or 4.8%, increase in total loans and the fourth consecutive quarter of growth in wealth management revenues. Additionally, the Company continued to maintain strong capital ratios that exceed the regulatory defined well capitalized status.

The Company reported net income of $7.4 million, or $0.43 per diluted common share, in 2022. This represented a 4.9% increase in earnings per share from the full year of 2021 when net income totaled $7.1 million, or $0.41 per diluted common share. The improved earnings performance for the 2022 year reflected the full benefit of several important strategic actions that the Company executed in 2021, the successful management of our asset quality throughout the pandemic, and effective balance sheet management. Overall, the increase in net interest income, along with a reduced loan loss provision, more than offset a lower level of non-interest income and higher non-interest expense resulting in an improved earnings performance in 2022.

The Company reported net income of $7.1 million, or $0.41 per diluted common share, for 2021. This represented a 51.9% increase in earnings per share from 2020 when net income totaled $4.6 million, or $0.27 per diluted common share. During 2021, earnings demonstrated meaningful improvement as the Company realized the benefit of several important strategic actions that were executed during the year. Overall, increased net interest income, a growing level of non-interest income, and a reduced loan loss provision more than offset a higher level of non-interest expense resulting in an improved earnings performance.

NET INTEREST INCOME AND MARGIN. The Company’s net interest income represents the amount by which interest income on earning assets exceeds interest paid on interest bearing liabilities. Net interest income is a primary source of the Company’s earnings; it is affected by interest rate fluctuations as well as changes in the amount

19

and mix of earning assets and interest bearing liabilities. The following table summarizes the Company’s net interest income performance for each of the past three years:

| YEAR ENDED DECEMBER 31, |

| ||||||||

| 2023 |

| 2022 |

| 2021 |

| ||||

(IN THOUSANDS, EXCEPT RATIOS) |

| |||||||||

Interest income | $ | 60,860 | $ | 49,058 | $ | 46,669 | ||||

Interest expense |

| 24,840 |

| 8,495 |

| 7,586 | ||||

Net interest income |

| 36,020 |

| 40,563 |

| 39,083 | ||||

Net interest margin |

| 2.86 | % |

| 3.27 | % |

| 3.15 | % | |

2023 NET INTEREST PERFORMANCE OVERVIEW. The Company’s net interest income for the full year of 2023 decreased by $4.5 million, or 11.2%, when compared to the full year of 2022. The Company’s net interest margin was 2.86% for the full year of 2023 representing a 41-basis point decline from the full year of 2022. The decrease in net interest income reflects total interest expense increasing to a higher level than the increase in total interest income. The Company continues to benefit from increased yields on total loans and investment securities due to a higher U.S. Treasury yield curve and the Federal Reserve’s action to tighten monetary policy in their effort to tame decades high inflation. But, similar to what is occurring across the banking industry, increased national interest rates have caused total deposit and borrowing costs to increase to a higher degree, resulting in net interest margin compression and lower net interest income.

Overall, in 2023, the average balance of total interest earning assets was modestly higher than the full year of 2022 average, totaling $1.3 billion. Specifically, total loans averaged $997.2 million in 2023 which is $19.7 million, or 2.0%, higher than the 2022 full year average. Short-term investments averaged $3.9 million in 2023 which is $19.3 million, or 83.0%, lower than the 2022 full year average. Total investment securities averaged $262.2 million in 2023 which is $16.9 million, or 6.9%, higher than the 2022 full year average. Given only a slight increase in the balance of total interest earning assets from the prior year, total interest income increased by $11.8 million, or 24.1%, between years due primarily to an improvement in the yield on earning assets, which increased from 3.95% to 4.84%.