UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

SECURITIES EXCHANGE ACT OF 1934

OR

EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2022

OR

EXCHANGE ACT OF 1934

OR

EXCHANGE ACT OF 1934

Date of event requiring this shell company report ______________

For the transition period from ________ to _______

Commission file number 1-14014

|

|

|

(Exact name of registrant as specified in its

charter)

|

|

|

|

(Jurisdiction of incorporation or organization)

|

|

Of our subsidiary

|

|

|

|

|

|

|

|

|

|

(Address of principal executive offices)

|

|

|

|

Chief Financial Officer

|

|

Credicorp Ltd

|

|

|

|

|

|

|

|

|

|

Phone (+

|

|

Facsimile (+

|

|

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

|

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class

|

Trading Symbol(s)

|

Name of each exchange on which registered

|

||

|

|

|

|

Securities registered or to be registered pursuant to Section 12(g) of the Act. None

Securities for which there is a reporting obligation pursuant to Section 15(d) of

the Act. None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the

period covered by the annual report.

Common Shares, par value $5.00 per share 94,382,317

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports

pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted

pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or

an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act

|

|

☒

|

Accelerated filer

|

☐

|

|

|

Non-accelerated filer

|

☐

|

Emerging Growth Company

|

|

If an emerging growth company that prepares its financial statements in

accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its

Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal

control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the

financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a

recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate by check mark which basis of accounting the registrant has used to prepare the financial

statements included in this filing:

|

U.S. GAAP ☐

|

|

Other ☐

|

|

by the International Accounting Standards Board ☒

|

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the

registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the

Exchange Act).

Yes ☐ No ☒

| 2 | ||||

|

10

|

||||

|

12

|

||||

|

14

|

||||

|

14

|

||||

|

14

|

||||

|

14

|

||||

|

14

|

||||

|

17

|

||||

|

17

|

||||

|

17

|

||||

|

52

|

||||

|

52

|

||||

|

60

|

||||

|

60

|

||||

|

75

|

||||

|

75

|

||||

|

97

|

||||

|

100

|

||||

|

105

|

||||

|

107

|

||||

|

113

|

||||

|

116

|

||||

|

116

|

||||

|

120

|

||||

|

124

|

||||

|

128

|

||||

|

129

|

||||

|

129

|

||||

|

133

|

||||

|

168

|

||||

|

168

|

||||

|

172

|

||||

|

175

|

||||

|

188

|

||||

|

190

|

||||

|

190

|

||||

|

191

|

||||

|

191

|

||||

|

191

|

||||

|

191

|

||||

|

203

|

||||

|

222

|

||||

|

232

|

||||

|

242

|

||||

|

259

|

||||

|

269

|

||||

|

269

|

||||

|

273

|

||||

|

274

|

||||

|

274

|

||||

2

|

285

|

|||

|

287

|

|||

|

293

|

|||

|

294

|

|||

|

295

|

|||

|

295

|

|||

|

295

|

|||

|

299

|

|||

|

300

|

|||

|

300

|

|||

|

306

|

|||

|

307

|

|||

|

307

|

|||

|

307

|

|||

|

307

|

|||

|

309

|

|||

|

309

|

|||

|

310

|

|||

|

310

|

|||

|

310

|

|||

|

310

|

|||

|

314

|

|||

|

314

|

|||

|

315

|

|||

|

326

|

|||

|

326

|

|||

|

327

|

|||

|

327

|

|||

|

327

|

|||

|

328

|

|||

|

330

|

|||

|

332

|

|||

|

333

|

|||

|

334

|

|||

|

340

|

|||

|

343

|

|||

|

358

|

|||

|

359

|

|||

|

359

|

|||

|

360

|

|||

|

360

|

|||

|

360

|

|||

|

360

|

|||

|

360

|

|||

|

360

|

|||

|

360

|

|||

|

360

|

|||

|

361

|

|||

|

365

|

|||

|

365

|

|||

|

366

|

|||

3

|

366

|

|||

|

369

|

|||

|

370

|

|||

|

370

|

|||

|

370

|

|||

|

371

|

|||

|

377

|

|||

|

381

|

|||

|

381

|

|||

|

381

|

|||

|

381

|

|||

|

381

|

|||

|

381

|

|||

|

382

|

|||

ABBREVIATIONS

|

Abbreviations

|

Meaning

|

|

|

AFP

|

Administradora de Fondo de Pensiones or Private Pension Funds Administrators

|

|

|

ALCO

|

Asset and Liabilities Committee

|

|

|

ALM

|

Asset and Liabilities Management

|

|

|

AML

|

Anti-Money Laundering

|

|

|

AMV

|

Autorregulador del Mercado de Valores de Colombia or Colombia’s Stock Market Self-regulator

|

|

|

ANPDP

|

Autoridad Nacional de Protección de Datos Personales del Perú or National Authority

for the Protection of Personal Data of Peru

|

|

|

APS

|

Autoridad de Fiscalización y Control de Pensiones y Seguros de Bolivia or Supervision and Control Authority for Pensions and

Insurance of Bolivia

|

|

|

ARRC

|

Alternative Reference Rates Committee

|

|

|

ASB

|

Atlantic Security Bank, currently ASB Bank Corp.

|

|

|

ASBANC

|

Asociación de Bancos del Perú or Association of Banks of Peru

|

|

|

ASFI

|

Autoridad Supervisora del Sistema Financiero or Financial System Supervisory Authority – Bolivia

|

|

|

ASHC

|

Atlantic Security Holding Corporation

|

|

|

ASOMIF

|

Asociación de Instituciones de Microfinanzas del Peru or Association of Microfinance Institutions of Peru

|

|

|

ATM

|

Automated Teller Machine (cash machine)

|

|

|

Bancompartir

|

Banco Compartir S.A., now Mibanco Colombia

|

|

|

BCB

|

Banco Central de Bolivia or Bolivian Central Bank

|

|

|

BCCh

|

Banco Central de Chile or Central Bank of Chile

|

|

|

BCM

|

Business Continuity Management

|

|

|

BCP Bolivia

|

Banco de Crédito de Bolivia S.A.

|

|

|

BCP Consolidated

|

BCP Consolidated includes BCP Stand-alone, Mibanco and Solución Empresa Administradora Hipotecaria

|

|

|

BCP Miami

|

Banco de Crédito del Perú, Miami Agency

|

|

|

BCP Panama

|

Banco de Crédito del Perú, Panama Branch

|

|

|

BCP Stand-alone

|

Banco de Crédito del Perú including BCP Panama (Panama Branch) and BCP Miami (Miami Agency), but excluding subsidiaries

|

|

|

BCRP

|

Banco Central de Reserva del Perú or Peruvian Central Bank

|

|

|

BLMIS

|

Bernard L. Madoff Investment Securities LLC.

|

|

|

BOB

|

Bolivianos – Bolivian Currency

|

|

|

Bps

|

Basis Points

|

|

|

BVL

|

Bolsa de Valores de Lima or Lima Stock Exchange

|

|

|

CAS

|

Contrato Administrativo de Servicios or Administrative Contracting of Services

|

|

|

CCSI

|

Credicorp Capital Securities Inc.

|

|

|

CEO

|

Chief Executive Officer

|

|

CET1

|

Common Equity Tier I

|

|

|

CGU

|

Cash-Generating Unit

|

|

|

CID

|

Corporate and International Division

|

|

|

CIMA

|

Cayman Islands Monetary Authority

|

|

|

CINO

|

Chief Innovation Officer

|

|

|

CLP

|

Chilean Peso – Chilean Currency

|

|

|

CMF

|

Comisión para el Mercado Financiero or Financial Markets Commission of Chile

|

|

|

CODM

|

Chief Operating Decision Maker

|

|

|

CoE

|

Center Of Excellence

|

|

|

COFIDE

|

Corporación Financiera de Desarrollo S.A. or Peruvian Government-Owned Development Bank

|

|

|

CONFIEP

|

Confederación Nacional de Instituciones Empresariales Privadas or National Confederation of Private Business Institutions in Peru

|

|

|

COO

|

Chief Operating Officer

|

|

|

Consolidated Supervision of Financial and Mixed Conglomerates Regulation

|

SBS Resolution No. 11823-2010, Reglamento para la Supervisión Consolidada de los Conglomerados Financieros y Mixtos

|

|

|

COOPACS

|

Cooperativa de Ahorro y Créditos de Peru or Savings and Loans Associations of Peru

|

|

|

COP

|

Colombian Peso – Colombian Currency

|

|

|

COSO

|

Committee of Sponsoring Organizations of the Treadway Commission

|

|

|

CPS

|

Comisión de Protección Social or Social Protection Committee of Peru

|

|

|

CSF

|

Cybersecurity Framework

|

|

|

Credicorp Capital

|

Credicorp Capital Ltd., formerly Credicorp Investments Ltd.

|

|

|

Credicorp Capital Bolsa

|

Credicorp Capital Sociedad Agente de Bolsa S.A., formerly Credibolsa SAB S.A.

|

|

|

Credicorp Capital Chile

|

Credicorp Capital Chile S.A., operating subsidiary of Credicorp Capital Holding Chile

|

|

|

Credicorp Capital Colombia

|

Credicorp Capital Colombia S.A., formerly Correval S.A.

|

|

|

Credicorp Capital Fondos

|

Credicorp Capital Sociedad Administradora de Fondos S.A., formerly Credifondo SAFI S.A.

|

|

|

Credicorp Capital Holding Chile

|

Credicorp Capital Holding Chile S.A., holding subsidiary of Credicorp Capital Ltd.

|

|

|

Credicorp Capital Holding Colombia

|

Credicorp Capital Holding Colombia S.A.S., holding subsidiary of Credicorp Capital Ltd.

|

|

|

Credicorp Holding Colombia

|

Credicorp Holding Colombia S.A.S., holding subsidiary of Credicorp Ltd., which holds Credicorp Capital Colombia S.A.S. and Mibanco – Banco de la Microempresa de Colombia S.A.

|

|

|

Credicorp Capital Holding Peru

|

Credicorp Capital Holding Peru S.A., holding subsidiary of Credicorp Capital Ltd.

|

|

|

Credicorp Capital Peru

|

Credicorp Capital Peru S.A.A., operating subsidiary of Credicorp Capital Holding Peru, and formerly BCP Capital S.A.A.

|

|

|

Credicorp Capital Servicios Financieros

|

Credicorp Capital Servicios Financieros S.A., formerly BCP Capital Financial Services S.A.

|

|

|

Credicorp Capital Titulizadora

|

Credicorp Capital Sociedad Titulizadora S.A., formerly Credititulos S.A.

|

|

CRS

|

Common Reporting Standards

|

|

|

CTF

|

Counter-Terrorism Financing

|

|

|

Culqi

|

Compañia Incubadora de Soluciones Moviles S.A.

|

|

|

DANE

|

Departamento Administrativo Nacional de Estadísticas or Colombian National Statistics Bureau

|

|

|

D&S

|

Disability and Survivorship

|

|

|

Deposit Insurance Fund

|

Fondo de Seguro de Depósitos or Deposit Insurance Fund of Peru

|

|

|

DIAN

|

Dirección de Impuestos y Aduanas Nacionales de Colombia or Taxes and National Customs Authority of Colombia

|

|

|

DTA

|

Deferred Tax Assets

|

|

|

Edpymes

|

Empresas de Crédito or Small and Micro Firm Development Institution, formerly Empresas de

Desarrollo de Pequeña y Microempresa (Legislative Decree No. 1531)

|

|

|

Edyficar

|

Empresa Financiera Edyficar S.A. – Perú

|

|

|

EIR

|

Effective Interest Rate

|

|

|

Encumbra

|

Empresa Financiera Edyficar S.A.S. – Colombia

|

|

|

EPS

|

Entidad Prestadora de Salud or Health Care Facility

|

|

|

ENPS

|

Employee Net Promoter Score

|

|

|

ES Act

|

Economic Substance Act 2018 (as amended) of Bermuda

|

|

|

EY

|

Ernst & Young LLP

|

|

|

FAE

|

Fondo de Apoyo Empresarial del Perú or Business Support Fund of Peru

|

|

|

FAE-Mype

|

Fondo de Apoyo Empresarial a la Mype del Perú or SME Business Support Fund of Peru

|

|

|

FATCA

|

Foreign Account Tax Compliance Act

|

|

|

FCA

|

Financial Conduct Authority – United Kingdom

|

|

|

FED

|

Board of Governors of the U.S. Federal Reserve System

|

|

|

FFIEC

|

Federal Financial Institutions Examination Council

|

|

|

FIBA

|

Financial and International Business Association, formerly Florida International Bankers Association

|

|

|

FINRA

|

Financial Industry Regulatory Authority – US

|

|

|

Fintech

|

Financial Technology

|

|

|

FMV

|

Fair market value

|

|

|

Fondemi

|

Fondo de Desarrollo de la Microempresa del Perú or SMEs Development Fund of Peru

|

|

|

GAAP

|

Generally Accepted Accounting Principles

|

|

|

GDP

|

Gross Domestic Product

|

|

|

Grupo Pacífico

|

Pacífico Compañía de Seguros y Reaseguros S.A. and consolidated subsidiaries

|

|

|

IASB

|

International Accounting Standards Board

|

|

|

IBA

|

ICE Benchmark Administration Limited

|

|

|

IBNR

|

Incurred but not reported

|

|

|

ICBSA

|

Inversiones Credicorp Bolivia S.A.

|

|

INDECOPI

|

Instituto Nacional de Defensa de la Competencia y de la Protección de la Propiedad Intelectual del Perú or National Institute

for the Defense of Competition and the Protection of Intellectual Property

|

|

|

IFRS

|

International Financial Reporting Standards

|

|

|

IGA

|

Intergovernmental Agreements

|

|

|

IIA

|

Institute of Internal Auditors

|

|

|

IMF

|

International Monetary Fund

|

|

|

IMO

|

Innovation Management Office

|

|

|

INE

|

National Statistics Institute of Chile

|

|

|

INEI

|

Instituto Nacional de Estadística e Informática or Peruvian National institute of Statistic and Informatics

|

|

|

IPO

|

Initial Public Offering

|

|

|

IRS

|

Internal Revenue Service

|

|

|

ISACA

|

Information Systems Audit and Control Association

|

|

|

IT

|

Information Technology

|

|

|

IUs

|

Innovation Units

|

|

|

KRI

|

Key Risk Indicators

|

|

|

LCR

|

Liquidity Coverage Ratio

|

|

|

LGD

|

Loss Given Default

|

|

|

LIBOR

|

London Interbank Offered Rate

|

|

|

LoB

|

Lines of Business

|

|

|

LTV

|

Loan to Value

|

|

|

MEF

|

Ministry of Economy and Finance of Peru

|

|

|

Merger Control Law

|

Law No. 31112, Ley que establece el control previo de operaciones de concentración empresarial

|

|

|

Mibanco

|

Mibanco, Banco de la Microempresa S.A.

|

|

|

Mibanco Colombia

|

Mibanco, Banco de la Microempresa de Colombia S.A.

|

|

|

MMD

|

Middle-Market Banking Division

|

|

|

Mype

|

Micro y Pequeña Empresa or Micro and Small Enterprise

|

|

|

NIM

|

Net Interest Margin

|

|

|

NIST

|

National Institute of Standards and Technology

|

|

|

NPS

|

Net Promoter Score

|

|

|

NYSE

|

New York Stock Exchange

|

|

|

OECD

|

Organization for Economic Cooperation and Development

|

|

|

P&C

|

Property and Casualty

|

|

|

Pacífico Seguros

|

Pacífico Compañía de Seguros y Reaseguros S.A.

|

|

|

PEN

|

Peruvian Sol (S/) – Peruvian Currency

|

|

|

Peruvian Banking and Insurance Law

|

Law No. 26702, Ley General del Sistema Financiero y del Sistema de Seguros y Orgánica de la Superintendencia de Banca y Seguros

|

|

|

PPS

|

Peruvian Private Pension System

|

|

|

RBG

|

Retail Banking Group

|

|

|

ROAA

|

Return on Average Assets

|

|

ROAE

|

Return on Average Equity

|

|

|

ROE

|

Return on equity

|

|

|

RWAs

|

Risk-Weighted Asset

|

|

|

S&P

|

Standard and Poor’s

|

|

|

SBP

|

Superintendencia de Bancos de Panamá or Superintendency of Banks of Panama

|

|

|

SBS

|

Superintendencia de Banca, Seguros y Administradoras Privadas de Fondos de Pensiones or Superintendence of Banks, Insurance and

Pension Funds – Peru

|

|

|

SCTR

|

Seguro Complementario de Trabajo de Riesgo or Complementary Work Risk Insurance

|

|

|

SEAH

|

Solución Empresa Administradora Hipotecaria S.A.

|

|

|

SEC

|

U.S. Securities and Exchange Commission

|

|

|

SFC

|

Superintendencia Financiera de Colombia or Financial Superintendence of Colombia

|

|

|

SME

|

Small and Medium Enterprise

|

|

|

SME – Business

|

SME-Business Credicorp Segment

|

|

|

SME – Pyme

|

SME-Pyme Credicorp Segment

|

|

|

SMV

|

Superintendencia del Mercado de Valores or Superintendence of the Securities Market – Peru

|

|

|

SOFR

|

Secured Overnight Financing Rate

|

|

|

SUNAT

|

Superintendencia Nacional de Aduanas y de Administración Tributaria or Superintendence of Tax Administration – Peru

|

|

|

SUSALUD

|

Superintendencia Nacional de Salud del Perú or National Health Superintendence of Peru

|

|

|

Soles

|

Peruvian currency (S/ - PEN)

|

|

|

Tenpo

|

Tenpo SpA (formerly Krealo SpA)

|

|

|

Tyba

|

Credicorp Capital Negocios Digitales S.A.S.

|

|

|

U.S. Dollar

|

United States currency (also $, US$, Dollars or U.S. Dollars)

|

|

|

USA

|

United States of America (USA, U.S.A., US or U.S.)

|

|

|

USDPEN

|

Currency exchange rate between the U.S. Dollar and the Peruvian Sol

|

|

|

Usury Law Regulation

|

Law No. 31143, Ley que protege de la usura a los consumidores de los servicios financieros

|

|

|

VaR

|

Value at Risk

|

|

|

VAT

|

Value-added tax

|

|

|

Wally

|

Wally POS S.A.C.

|

|

|

WBG

|

Wholesale Banking Group

|

|

|

WHO

|

World Health Organization

|

|

|

WTI

|

West Texas Intermediate

|

Credicorp Ltd. is a Bermuda exempted company (and is referred to in this Annual Report as Credicorp, the Company, the Group, we, or us, each of which means either Credicorp Ltd.

as a separate entity or as an entity together with our consolidated subsidiaries, as the context may require). We maintain our financial books and records in Peruvian Soles and present our financial statements in accordance with International

Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB). IFRS differ in certain respects from Generally Accepted Accounting Principles (GAAP) in the United States.

We operate primarily through our four lines of business (LoBs): Universal Banking, Microfinance, Insurance & Pensions, and Investment Banking & Wealth Management.

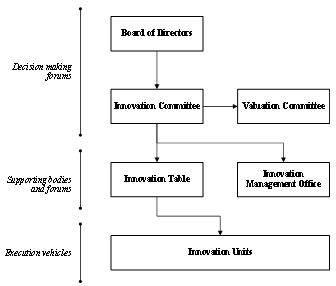

Additionally, we complement the operations of our LoBs through our innovation portfolio which is managed by the Innovation Committee at the Credicorp level. For more information about our innovation portfolio and strategy, please review “ITEM 4.

INFORMATION ON THE COMPANY – 4.B Business Overview – (1) Credicorp Overview – Our Innovation Strategy”.

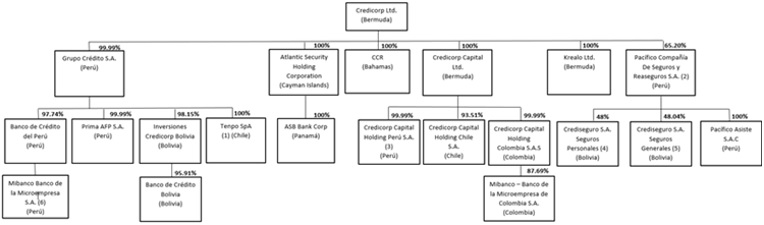

Our eight main operating subsidiaries are:

| • |

Within Universal Banking: (i) Banco de Crédito del Perú S.A. (BCP Stand-alone), a Peruvian financial institution; and (ii) Banco de Crédito de Bolivia S.A. (BCP Bolivia) a commercial bank that operates in Bolivia and that we hold through

Inversiones Credicorp Bolivia S.A. (ICBSA);

|

| • |

Within Microfinance: (iii) Mibanco, Banco de la Microempresa S.A. (Mibanco), a Peruvian banking entity oriented toward the micro and small business sector; and (iv) Mibanco – Banco de la Microempresa de Colombia S.A. (Mibanco Colombia),

which resulted from the merger between Banco Compartir S.A. (Bancompartir) and Edyficar S.A.S. (Encumbra), which we hold through Credicorp Holding Colombia S.A.S.;

|

| • |

Within Insurance and Pensions: (v) Pacífico Compañía de Seguros y Reaseguros S.A. (Pacífico Seguros and, together with its consolidated subsidiaries, Grupo Pacífico), an entity that contracts and manages all types of general risk and

life insurance, reinsurance and property investment and financial operations; and (vi) Prima AFP, a private pension fund; and

|

| • |

Finally, within Investment Banking and Wealth Management: (vii) Credicorp Capital Ltd. (together with its subsidiaries) was formed in 2012, and (viii) ASB Bank Corp., resulted from the merger between ASB Bank Corp. and Atlantic Security

Bank, which we hold through Atlantic Security Holding Corporation (ASHC).

|

For information about these LoBs, see “ITEM 4. INFORMATION ON THE COMPANY – 4.B Business Overview – (2) Lines of Business (LoBs)”.

As of and for the year ended December 31, 2022, BCP Stand-alone represented 75.1% of our total assets and 70.4% of our equity attributable to Credicorp’s equity holders (that

is, its shareholders). Unless otherwise specified, the financial information for BCP Stand-alone, BCP Bolivia, Mibanco, Mibanco Colombia, ASB Bank Corp., Grupo Pacífico, Prima AFP and Credicorp Capital included in this Annual Report is presented in

accordance with IFRS and before eliminations for consolidation purposes. See “ITEM 3. KEY INFORMATION – 3.A Selected Financial Data” and “ITEM 4. INFORMATION ON THE COMPANY – 4.A History and Development of the Company”. We refer to BCP Stand-alone,

BCP Bolivia, Mibanco, Mibanco Colombia, Grupo Pacífico, Prima AFP, Credicorp Capital and ASB as our main operating subsidiaries.

“ITEM 3. KEY INFORMATION – 3.A Selected Financial Data” contains key information related to our performance. This information was obtained mainly from our consolidated financial

statements as of December 31, 2020, 2021 and 2022.

Unless otherwise specified or the context otherwise requires, references in this Annual Report to “S/”, “Sol”, “local currency” or “Soles” are to Peruvian Soles (each Sol is

divided into 100 centimos (cents)), and references to “$”, “US$,” “Dollars”, “US Dollars” or “U.S. Dollars” are to United States Dollars. In addition, references to USDPEN are the currency exchange rate between the U.S. Dollar and the Peruvian Sol.

Some of our subsidiaries, namely Atlantic Security Holding and five of its subsidiaries (Atlantic Security International Financial Services Inc (ASIF), ASB Bank Corp., Atlantic

Private Equity Investment Advisor, Atlantic Security Private Equity General Partner, Credicorp Capital Cayman GP), Credicorp Capital USA Inc. (with its subsidiaries Credicorp Capital Advisors LLC., Credicorp Capital LLC. and Tyba LLC.) and

Credicorp Capital Asset Management Administradora General de Fondos maintain their operations and balances in US Dollars and other currencies. As a result, in certain instances throughout this Annual Report, we have translated US Dollars and other

currencies to Soles. You should not construe any of these translations as representations that the US Dollar amounts actually represent such equivalent Sol amounts or that such US Dollar amounts could be converted into Soles at the rate indicated,

as of the dates mentioned herein, or at all. Unless otherwise indicated, these Sol amounts have been translated from US Dollar amounts at an exchange rate of S/3.814= US$1.00, which is the December 31, 2022 exchange rate set by the Peruvian

Superintendence of Banks, Insurance and Pension Funds (Superintendencia de Banca, Seguros y Administradoras Privadas de Fondos de Pensiones or SBS by its Spanish initials), S/3,987 and S/3,621 per dollar as of December 31, 2021 and 2020,

respectively. Converting US Dollars to Soles on a specified date (at the prevailing exchange rate on that date) may result in the presentation of Sol amounts that are different from the Sol amounts that would result by converting the same amount of

US Dollars on a different specified date (at the prevailing exchange rate on such date). Our Bolivian subsidiary operates in Bolivianos (BOB). For consolidation purposes, our Bolivian subsidiary’s financial statements are also presented in Soles.

Our Colombian and Chilean subsidiaries operate in Colombian Pesos (COP) and Chilean Pesos (CLP), respectively, and their financial statements are also converted into Soles for consolidation purposes.

Our management’s criteria for translating foreign currency, for the purpose of preparing Credicorp’s consolidated financial statements, are described in “ITEM 5. OPERATING AND

FINANCIAL REVIEW AND PROSPECTS – 5.A Operating Results – (3) Critical Accounting Policies – 3.3 Foreign Exchange”.

Certain statements contained in this Annual Report are not historical facts, including, without limitation, certain statements made in the sections titled “ITEM 3. KEY

INFORMATION”, “ITEM 4. INFORMATION ON THE COMPANY”, “ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS” and “ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT RISK MANAGEMENT”, which are forward-looking statements within the meaning of

Section 27A of the U.S. Securities Act of 1933, as amended, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended (the Exchange Act). You can find many of these statements by looking for words such as “believes”, “expects”,

“anticipates”, “estimates”, “intends”, “plans”, “goal”, “seek”, “project”, “strategy”, “future”, “likely”, “should”, “will”, “would”, “may”, or other similar expressions referring to future periods.

Forward-looking statements are based only on our management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual

results, performance, or events to differ materially from those expressed or implied in the forward-looking statements. Therefore, actual results, performance, or events may be materially different from those in the forward-looking statements due

to, without limitation, the following factors:

| a) |

Economic conditions and regulatory framework in Peru and markets in which we operate;

|

| b) |

The occurrence of natural disasters or political or social instability in Peru and markets in which we operate;

|

| c) |

The adequacy of the dividends that our subsidiaries are able to pay to us, which may affect our ability to pay dividends to shareholders and corporate expenses;

|

| d) |

Performance of, and volatility in, financial markets, including in Latin America and other emerging markets;

|

| e) |

The frequency, severity, and types of insured loss events;

|

| f) |

Fluctuations in interest rate and liquidity levels;

|

| g) |

Foreign currency exchange rates, including the Sol/US Dollar exchange rate;

|

| h) |

Deterioration in the quality of our loan portfolio;

|

| i) |

Increasing levels of competition in Peru and markets in which we operate;

|

| j) |

Developments and changes in laws and regulations affecting the financial sector and adoption of new international guidelines;

|

| k) |

Changes in the policies of central banks and/or foreign governments;

|

| l) |

Effectiveness of our risk management policies and of our operational and security systems;

|

| m) |

Emerging cybersecurity and environmental risks;

|

| n) |

Losses associated with counterparty exposures;

|

| o) |

The coronavirus disease 2019 (COVID-19) pandemic and/or other public health crises beyond our control; and

|

| p) |

Changes in Bermuda laws and regulations applicable to so-called non-resident entities.

|

See “ITEM 3. KEY INFORMATION - 3.D Risk Factors” and “ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS” for additional information and other such factors.

Any forward-looking statement made by us in this Annual Report is based only on information currently available to us and is made only as of the date on which it is made, and

you are cautioned not to place any undue reliance on any such statement. We are not under any obligation to, and we expressly disclaim any obligation to, update or alter any forward-looking statements contained in this Annual Report, whether as a

result of new information, future events or otherwise.

| ITEM 1. |

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

|

Not applicable.

| ITEM 2. |

OFFER STATISTICS AND EXPECTED TIMETABLE

|

Not applicable.

| ITEM 3. |

KEY INFORMATION

|

| A. |

Selected Financial Data

|

The following table presents a summary of our consolidated financial information at the dates and for the periods indicated. This selected financial data is presented in Soles.

You should read this information in conjunction with and qualify this information in its entirety by reference to, the consolidated financial statements, which are also presented in Soles.

The summary of our consolidated financial data as of, and for the years ended, December 31, 2020, 2021 and 2022 were derived from the consolidated financial statements audited

by Gaveglio, Aparicio y Asociados S.C.R.L, a member firm of PricewaterhouseCoopers International Limited, independent registered public accountants.

The report of Gaveglio, Aparicio y Asociados S.C.R.L on the consolidated financial statements as of December 31, 2021, and 2022 and for the years ended December 31, 2020, 2021

and 2022 appears elsewhere in this Annual Report.

SELECTED FINANCIAL DATA

|

Year ended December 31,

|

||||||||||||||||

|

2020

|

2021

|

2022

|

2022

|

|||||||||||||

|

(In thousands of Soles, except percentages, ratios, and per common share data)

|

In thousands

of US Dollars (1)

|

|||||||||||||||

|

INCOME STATEMENT DATA:

|

||||||||||||||||

|

IFRS:

|

||||||||||||||||

|

Interest and similar income

|

11,547,648

|

11,850,406

|

15,011,282

|

3,935,837

|

||||||||||||

|

Interest and similar expenses

|

(2,978,696

|

)

|

(2,490,802

|

)

|

(3,493,187

|

)

|

(915,885

|

)

|

||||||||

|

Net Interest, similar income and expenses

|

8,568,952

|

9,359,604

|

11,518,095

|

3,019,952

|

||||||||||||

|

Provision for credit losses on loan portfolio (2)

|

(6,080,289

|

)

|

(1,558,951

|

)

|

(2,158,555

|

)

|

(565,957

|

)

|

||||||||

|

Recoveries of written-off loans

|

159,781

|

346,728

|

347,017

|

90,985

|

||||||||||||

|

Provision for credit losses on loan portfolio, net of recoveries

|

(5,920,508

|

)

|

(1,212,223

|

)

|

(1,811,538

|

)

|

(474,972

|

)

|

||||||||

|

Net interest, similar income and expenses, after provision for credit losses on loan portfolio

|

2,648,444

|

8,147,381

|

9,706,557

|

2,544,980

|

||||||||||||

|

Commissions and fees

|

2,912,778

|

3,493,734

|

3,640,319

|

954,462

|

||||||||||||

|

Net gain on foreign exchange transactions

|

638,238

|

922,917

|

1,084,151

|

284,256

|

||||||||||||

|

Net gain on securities

|

523,082

|

28,650

|

5,468

|

1,434

|

||||||||||||

|

Net gain on derivatives held for trading

|

(13,401

|

)

|

221,064

|

65,187

|

17,092

|

|||||||||||

|

Net result from exchange differences

|

58,539

|

(3,215

|

)

|

(16,158

|

)

|

(4,236

|

)

|

|||||||||

|

Other income

|

289,037

|

266,567

|

329,382

|

86,361

|

||||||||||||

|

Total non-interest income

|

4,408,273

|

4,929,717

|

5,108,349

|

1,339,369

|

||||||||||||

|

Net premiums earned

|

2,428,060

|

2,671,530

|

2,873,295

|

753,355

|

||||||||||||

|

Net claims incurred for life, general and health insurance contracts

|

(1,708,113

|

)

|

(2,341,917

|

)

|

(1,929,890

|

)

|

(506,002

|

)

|

||||||||

|

Acquisition cost

|

(361,814

|

)

|

(333,334

|

)

|

(281,807

|

)

|

(73,888

|

)

|

||||||||

|

Total other expenses (3)

|

(7,190,689

|

)

|

(7,740,561

|

)

|

(8,620,615

|

)

|

(2,260,256

|

)

|

||||||||

|

Profit before income tax

|

224,161

|

5,332,816

|

6,855,889

|

1,797,558

|

||||||||||||

|

Income tax

|

109,977

|

(1,660,987

|

)

|

(2,110,501

|

)

|

(553,356

|

)

|

|||||||||

|

Net profit

|

334,138

|

3,671,829

|

4,745,388

|

1,244,202

|

||||||||||||

|

Attributable to:

|

||||||||||||||||

|

Credicorp’s equity holders

|

346,894

|

3,584,582

|

4,633,096

|

1,214,760

|

||||||||||||

|

Non-controlling interest

|

(12,756

|

)

|

87,247

|

112,292

|

29,442

|

|||||||||||

|

Number of shares as adjusted to reflect changes in capital (4)

|

79,467,865

|

79,531,948

|

79,533,095

|

-

|

||||||||||||

|

Net basic earnings per common share attributable to Credicorp’s equity holders (5)

|

4.37

|

45.09

|

58.26

|

15.28

|

||||||||||||

|

Net dilutive earnings per common share attributable to Credicorp’s equity holders (5)

|

4.36

|

44.99

|

58.13

|

15.24

|

||||||||||||

|

Cash dividends declared per common share Soles (6)

|

5.0

|

15.0

|

-

|

-

|

||||||||||||

|

As of December 31,

|

||||||||||||||||

|

2020

|

2021

|

2022

|

2022

|

|||||||||||||

|

(In thousands of Soles, except percentages, ratios, and per common share data)

|

In thousands

of US Dollars (1)

|

|||||||||||||||

|

STATEMENT OF FINANCIAL POSITION DATA:

|

||||||||||||||||

|

IFRS:

|

||||||||||||||||

|

Total assets

|

237,406,163

|

244,846,740

|

236,753,609

|

62,074,884

|

||||||||||||

|

Total loans (7)

|

137,659,885

|

147,597,412

|

148,626,374

|

38,968,635

|

||||||||||||

|

Allowance for loan losses (2)

|

(10,435,623

|

)

|

(9,071,011

|

)

|

(8,530,986

|

)

|

(2,236,756

|

)

|

||||||||

|

Total deposits (8)

|

141,660,321

|

149,596,545

|

147,020,787

|

38,547,663

|

||||||||||||

|

Equity attributable to Credicorp’s equity holders

|

24,945,870

|

26,496,767

|

28,988,140

|

7,600,456

|

||||||||||||

|

Non-controlling interest

|

499,777

|

540,672

|

591,569

|

155,105

|

||||||||||||

|

Total equity

|

25,445,647

|

27,037,439

|

29,579,709

|

7,755,561

|

||||||||||||

|

As of and for the year ended December 31,

|

||||||||||||

|

2020

|

2021

|

2022

|

||||||||||

|

SELECTED RATIOS

|

||||||||||||

|

IFRS:

|

||||||||||||

|

Net interest margin (NIM) (9)

|

4.30

|

%

|

4.10

|

%

|

5.09

|

%

|

||||||

|

Return on average total assets (ROAA) (10)

|

0.16

|

%

|

1.49

|

%

|

1.92

|

%

|

||||||

|

Return on average equity (ROAE) (11)

|

1.36

|

%

|

13.94

|

%

|

16.70

|

%

|

||||||

|

Operating efficiency (12)

|

45.09

|

%

|

44.96

|

%

|

43.66

|

%

|

||||||

|

Operating expenses as a percentage of average assets (13)

|

3.11

|

%

|

3.12

|

%

|

3.49

|

%

|

||||||

|

Equity attributable to Credicorp’s equity holders as a percentage of period end total assets

|

10.51

|

%

|

10.82

|

%

|

12.24

|

%

|

||||||

|

Regulatory capital as a percentage of risk weighted assets – BIS ratio (14)

|

16.44

|

%

|

16.71

|

%

|

19.31

|

%

|

||||||

|

Total internal overdue loan amounts as a percentage of total loans (15)

|

3.40

|

%

|

3.77

|

%

|

4.00

|

%

|

||||||

|

Allowance for direct loan losses as a percentage of total loans

|

7.19

|

%

|

5.74

|

%

|

5.30

|

%

|

||||||

|

Allowance for loan losses as a percentage of total loans and other off-balance-sheet items (16)

|

6.58

|

%

|

5.32

|

%

|

5.03

|

%

|

||||||

|

Allowance for direct loan losses as a percentage of total internal overdue loans (17)

|

211.26

|

%

|

152.40

|

%

|

132.40

|

%

|

||||||

|

Allowance for direct loan losses as a percentage of impaired loans (18)

|

100.94

|

%

|

75.13

|

%

|

73.79

|

%

|

||||||

|

Dividend payout ratio (19)

|

114.42

|

%

|

33.27

|

%

|

-

|

|||||||

|

Equity to assets ratio (20)

|

11.05

|

%

|

10.21

|

%

|

10.46

|

%

|

||||||

|

Shareholders’ equity to assets ratio (21)

|

11.28

|

%

|

10.41

|

%

|

10.24

|

%

|

||||||

Note: Total internal overdue loans include overdue and under legal collection loans.

| (1) |

Translated for convenience only from Sol amounts to US Dollar amounts using exchange rates of S/3.814 = US$1.00, which is the December 31, 2022 exchange rate set by the SBS, for statement of financial position data and of S/3.838 =

US$1.00, which is the average exchange rate on a monthly basis in 2022, for income statement data (for consistency with the annual amounts being translated).

|

| (2) |

Allowance for loan losses include provisions and reserves with respect to direct loans losses and indirect loans losses or off-balance sheet items such as guarantees and standby letters, performance bonds, and import and export letters

of credit. The 2022 provision for credit losses decreased from 2021. This decrease was mainly due to the flow of write-offs carried out during 2022, which mainly impacted the BCP consumer segment and to the small and microenterprise segment

in both BCP and Mibanco Perú; In addition, it was due, although to a lesser extent, to the decrease in the US$/Sol exchange rate. The above effects were partially offset by the deterioration of the macroeconomic component, which had a

greater impact on the consumer and small and microenterprise segments at BCP, and by entering segments of greater profitability and risk in small and microenterprises at BCP.

|

| (3) |

Total other expenses include salaries and employee benefits, administrative expenses, depreciation and amortization, depreciation for right-of-use assets, impairment loss on goodwill and others.

|

| (4) |

The number of shares consists of capital stock (see Note 18(a) to the consolidated financial statements) less treasury stock (see Note 18 (b) to the consolidated financial statements).

|

| (5) |

Basic earnings per share is calculated by dividing the net profit for the year attributable to Credicorp’s equity holders by the weighted average number of ordinary shares outstanding during the year, excluding the average number of

ordinary shares purchased and held as treasury stock (see Note 30 to the consolidated financial statements). Dilutive earnings per share is calculated by dividing by the weighted average number of ordinary shares outstanding during the

year, including the average number of ordinary shares purchased and held as treasury stock.

|

| (6) |

Dividends declared per share based on net profit attained for the financial years 2020 and 2021 were declared in Soles and paid in US Dollars on October 7, 2021, and June 10, 2022, respectively, using the weighted exchange rate

registered by the SBS for the transactions at the close of business on October 7, 2021, and June 10, 2022, respectively. As of the date of this Annual Report, no dividends have been declared in 2023.

|

| (7) |

“Total loans” refers to “loans, net of unearned income” as disclosed in our consolidated financial statements, which equals direct loans plus accrued interest minus unearned interest. See Note 7 to the consolidated financial statements.

In addition to loans outstanding, we had off-balance-sheet items, including those mentioned in Note (2) above that amounted to S/20,973.8 million, S/22,914.3 and S/20,928.1 million, as of December 31, 2020, 2021 and 2022, respectively. See

Note 21 to the consolidated financial statements.

|

| (8) |

Total deposits exclude interest payable. See Note 14 to the consolidated financial statements.

|

| (9) |

Net interest similar income and expenses as a percentage of average interest-earning assets, computed as the average of period-beginning and period-ending balances.

|

| (10) |

Net profit attributable to Credicorp’s equity holders as a percentage of average total assets, computed as the average of period-beginning and period-ending balances.

|

| (11) |

Net profit attributable to Credicorp’s equity holders as a percentage of average equity attributable to our equity holders, computed as the average of period-beginning and period-ending balances.

|

| (12) |

Sum of salaries and employee benefits, administrative expenses, depreciation and amortization, acquisition cost and association in participation, all as percentage of the sum of net interest income, commissions and fees, net gain from

exchange differences, net gain in associates, net premiums earned, net gain on foreign exchange transactions and net result on derivatives held for trading. Acquisition cost includes net fees, underwriting expenses and underwriting income.

|

| (13) |

Sum of salaries and employee benefits, administrative expenses, depreciation and amortization and acquisition cost, all as percentage of average total assets.

|

| (14) |

Regulatory capital calculated in accordance with guidelines established by the Basel Committee on Banking Regulations and Supervisory Practices of International Settlements (Basel Committee Accord) as adopted by the SBS. See “ITEM 5.

OPERATING AND FINANCIAL REVIEW AND PROSPECTS – 5.B Liquidity and Capital Resources - (1) Capital Adequacy Requirements for Credicorp.”

|

| (15) |

Depending on the type of loan, BCP Stand-alone and Mibanco consider corporate, large business and medium business loans to be internal overdue loans for after 15 days; and overdrafts, small and micro business to be internal overdue loans

after 30 days. For consumer, mortgage and leasing loans the past-due installments are considered internal overdue after 30 to 90 days and after 90 days, the outstanding balance of the loan is considered internal overdue. ASB considers

internal overdue loans all overdue loans when the scheduled principal and/or interest payments are overdue for more than 30 days. BCP Bolivia considers loans as internal overdue after 30 days.

|

| (16) |

Other off-balance-sheet items primarily consist of guarantees and stand-by letters, performance bonds, and import and export letters of credit. See Note 21 to the consolidated financial statements.

|

| (17) |

Allowance for direct loan losses, as a percentage of all internal overdue loans without accounting for collateral securing such loans.

|

| (18) |

Allowance for direct loan losses as a percentage of direct loans classified as impaired debt. See “ITEM 4. INFORMATION ON THE COMPANY - 4.B Business Overview – (7) Selected Statistical Information – 7.3 Loan Portfolio – 7.3.7

Classification of the Loan Portfolio”.

|

| (19) |

Dividends declared based on net profit attained for the financial years 2020 and 2021 divided by net profit attributable to our equity holders of the year 2020 and 2021, respectively. Dividends for 2022 results have not been declared

yet.

|

| (20) |

Average equity attributable to our equity divided by average total assets, both averages computed as the average of month-ending balances.

|

| (21) |

Average equity attributable to our equity shareholders divided by average total assets, both averages computed as the average of month-ending balances.

|

| 3. B |

Capitalization and Indebtedness

|

Not applicable.

| 3. C |

Reasons for the Offer and Use of Proceeds

|

Not applicable.

| 3. D |

Risk Factors

|

Our businesses are affected by many external and other factors in the markets in which we operate. Different risk factors can impact our businesses, our ability to operate

effectively and our business strategies. You should consider the risk factors carefully and read them in conjunction with all the information in this document. You should note that the risk factors described below are not the only risks to

consider. Rather, these are the risks that we currently consider material. There may be additional risks that we consider immaterial or of which we are unaware, and any of these risks could have similar effects to those set forth below.

Macroeconomic Risks

Our geographic location exposes us to risks related to Peruvian political, social, and economic conditions.

Our geographic location exposes us to risks related to Peruvian political, social, and economic conditions.

Most operations of BCP Stand-alone, Grupo Pacífico, Prima AFP, and a significant part of Credicorp Capital’s and Mibanco operations are located in Peru. In

addition, while ASB Bank Corp. is based in Panama rather than in Peru, most of its customers are located in Peru. Therefore, our results primarily depend on economic activity in Peru. Changes in economic conditions, both international and domestic,

government policies or social uncertainty can alter the financial health and normal development of our businesses. These changes may include, but are not limited to, high inflation, currency depreciation, currency exchange controls, caps on

interest rates, confiscation of private property, financial regulation, among others. Similarly, terrorist activity, political and social unrest and corruption scandals can adversely impact our operations.

According to the IMF staff concluding statement of the 2023 article IV mission (February 9), the outlook is very uncertain and downside risks prevail. The

main external risks to their outlook include: spillovers from Russia’s war in Ukraine, an abrupt global slowdown with an associated commodity price volatility, and a possible de-anchoring of inflation expectations forcing a further tightening in

the global financial conditions. Domestic risks to the outlook include an intensification of political uncertainty, social unrest over political developments and natural disasters.

Peru experienced one of its worst social and political crises in decades after a failed coup on December 7, 2022, by former president Pedro Castillo, caused

massive protests. On the day of a debate by Peru’s congress on a third motion to impeach Castillo, in a message to the Nation, Castillo announced the temporary dissolution of Peru’s congress, new elections for a congress with the power to reform

Peru’s constitution and the restructuring of Peru’s justice system. The police and armed forces released a joint statement saying that any act contrary to the established constitutional order is a violation of the constitution and that they will

not abide by it. Within hours of his speech, Peru’s congress had voted to remove Castillo from office due to moral incapacity and he was arrested on charges of rebellion and conspiracy. In turn, Vice President Dina Boluarte was sworn in as Peru’s

first female president and has indicated that she plans to govern until 2026, which is the year Castillo’s term would have ended.

Since Boluarte took office, social unrest exacerbated and erupted, mainly in southern regions of Peru, where Castillo has more support. Protesters have demanded the resignation of President Boluarte, the shutdown of Peru’s congress and immediate general elections. Protests have been violent; as of late January 2023, more than 50 civilians had died

during social demonstrations, there have been many road blockages, and several regional airports have had to suspend operations temporarily as infrastructure was damaged. These protests were ongoing and concentrated in Puno as of late March 2023,

and there could be no assurance as to when these protests would stop, despite reports in March that there were signs that the protests had started to wane.

On December 20, 2022, Peru’s congress approved a bill that sought to end the current presidential mandate in July 2024 and called for general elections.

However, as the bill constituted a constitutional amendment, a second vote was required. On March 14, 2023, the congress’s constitutional commission rejected the initiative to advance the general elections to 2023. It was the fifth time the

constitutional reform bill was rejected since December. The current presidential mandate is scheduled to end in 2026.

It is important to recall that the general elections of 2021 resulted in an environment of political and social polarization, as Pedro

Castillo, a leader of a teachers’ union and of indigenous heritage, was elected president in a very narrow (only 44,263 votes of difference) second round win against the right-wing candidate Keiko Fujimori, who is the daughter of ex-president

Alberto Fujimori. Between July 2021 and December 2022, Castillo appointed 5 different prime ministers and named more than 70 ministers. In October 2022, Castillo was also accused by Peru’s top prosecutor of overseeing a criminal organization run

from the presidential palace with the purpose of monopolizing, controlling and steering bidding processes in order to obtain illicit gains. The complaint also included two ministers who served under

Castillo.

Among the main risks presented by the next government are intentions to impose more state control over the economy, potential changes to Peru’s current constitution (which was

enacted in 1993), strict interest rate controls and lack of technical expertise. For a new constitution to replace the current one through a constituent assembly, a constitutional reform proposal would need to be approved by Peru’s congress, either

through an absolute majority (87 votes) in two consecutive legislatures or simple a majority (66 votes) ratified in a referendum.

Social and political instability in Peru is not new. The country has experienced various instances of instability ranging from domestic terrorism (during

the 1980’s) to military coups and a succession of regimes. Although the risk of renewed domestic terrorism is not expected, any violence derived from the drug trade, or a resumption of large-scale terrorist activities could hurt our operations.

Additionally, some regimes during the 1970s and 1980s heavily intervened in the economy in pursuit of various economic policies and priorities, including expropriation, nationalization and new taxation policies. These interventions altered the

country’s economic environment, financial system and agricultural sector, among other components.

There have also been several political disputes between the government and the opposition in recent decades. Since 2001, more than ten different political

organizations have nominated candidates for President in each of the five election processes, showing low approval rating for all candidates (usually around 20%–30% approval ratings). Since August 2016 until February 2023, Peru has had 6

presidents, 3 congresses and 16 prime ministers.

According to the Peruvian National institute of Statistic and Informatic (Instituto

Nacional de Estadísticas e Informática or INEI by its Spanish initials), high levels of poverty in Peru have historically been a contributing factor to social conflict. Between 2004 and 2019 (pre pandemic) according to INEI, Peru’s poverty

rate decreased from almost 60% of the population to 20%. In 2020, due to the economic shock resulting from the COVID-19 pandemic, the poverty rate increased to 30%, erasing nearly all gains from the last decade. Even though the poverty rate fell to

26% in 2022, it remains above pre-pandemic levels.

There can be no assurance that Peru will not continue facing political, economic or social problems in the future or that these problems will not adversely

affect our business, financial conditions, and results of operations. There is always the possibility that, as has happened before, a political faction could promote policies to respond to social unrest with a speech that includes, among other

things, expropriation, nationalization, suspension of the enforcement of creditors’ rights and new taxation policies.

Another source of risk is related to political and social unrest in areas where mining and oil and gas operations take place. In recent years,

Peru has experienced protests against mining projects in several regions around the country. In 2021, as Peru’s then president, Castillo called for the nationalization of certain gas and mining

operations. Mining is an important part of the Peruvian economy. According to INEI, the mining and hydrocarbons sector represented 14.4% of GDP (mining 12.2% and hydrocarbons 2.2%) in 2022. The country’s exports are highly concentrated in the

mining industry; in 2022 free on board (FOB) exports of metallic mining represented 52.5% of total exports (copper represents half of this mining exports), with tax revenues from the sector representing 14.4% of total tax revenue in 2022.

On several occasions, local communities have opposed these operations and accused them of polluting the environment, specifically rivers, hurting

agricultural and other traditional economic activities, as well as complained of not receiving the benefits in terms of growth and wealth generated by the mining projects. For example, in 2021, politicized social unrest in Apurimac surrounded the

Las Bambas mining project, which produced approximately 11% of Peru’s total copper production in 2022. Las Bambas’ majority owner, MMG, stated that if the routes to the mine continued to be blocked by different politicized members of communities

surrounding the mine and routes to the mine, they will not be able to operate. In April 2022, Las Bambas shut down for 51 days, after protesters from two communities entered the mine and settled inside. The recent social protests of late 2022 and

early 2023 have also affected Las Bambas’ operations as road blockages prevented the arrival of key inputs. In another example, on January 12, 2023, Minsur announced the temporary suspension of operations in its San Rafael tin mine, in Peru’s Puno

region, as a measure of solidarity with the families of people who died in recent protests in the region. And on February 6, 2023, Buenaventura temporarily suspended operations at its Julcani silver mine after protesters entered and destroyed part

of the mine's facilities.

These and other delays or cancellations of mining projects could reduce Peruvian economic growth and business confidence, thereby hurting the financial

system both directly (many mining projects are at least partially financed by local financial institutions) and indirectly (overall economic activity could decelerate). Any such effect on the financial system could have a material adverse effect on

our business and result of operations.

Beyond the mining, and oil and gas sectors, the ongoing protests may also have negatively affected the tourism, hospitality, transportation, and retail

sectors. These sectors have also been affected by other developments in recent years, such as climate change. These Peruvian political and social developments may also affect foreign investment sentiment and therefore economic development. Having

said that, and due to ongoing social and political risks, in January 2023, Moody’s changed Peru’s credit rating outlook from stable to negative and kept the rating in Baa1.

Our banking and capital market operations in neighboring countries expose us to risk related to political and

economic conditions in those countries.

ICBSA, Credicorp Capital Holding Colombia, Credicorp Capital Holding Chile and ASB Bank Corp. expose us to risks related to Bolivian,

Colombian, Chilean and Panamanian political and economic conditions, respectively. These economies suffered unprecedented GDP contractions in 2020 due to the COVID-19 pandemic and have experienced an

uneven recovery as a result of different policy responses and economic structures. Colombia and Chile returned to pre-pandemic levels in 2021 while Panama and Bolivia did so in 2022. The negative effect of the pandemic on poverty and inequality,

combined with inflation rates (driven by high energy and food prices) not seen in these countries in decades, inflamed an already complex social environment characterized by elevated levels of inequality and dissatisfaction with authorities.

According to data from the World Bank, Colombia is the second most unequal country in the region, as measured by the Gini index. In general, the higher the Gini index, which measures the rate of social inequality, of a country, the more unequal

it is. Brazil has the highest Gini index in the region; Panama has the third-highest.

In recent years, neighboring countries in Latin America in which we have banking and capital market operations have experienced widespread social unrest and

several left-wing leaders have been chosen as presidents:

| • |

Chile: In October 2019, Chile experienced massive and violent demonstrations that forced Sebastian Piñera’s government to sign off on a referendum on a new constitution. In late 2021, Gabriel Boric, a

36-year-old left-wing leader, was elected as Chile’s president for a four-year term. After voters rejected the text for a new constitution in September 2022, Chile’s congress approved a new constituent process, which will likely result in

ongoing uncertainty in the political and social arenas until the next referendum on forming a constituent assembly takes place.

|

| • |

Colombia: In 2021, the proposal of an unpopular tax reform triggered its most serious public unrest in recent memory. Gustavo Petro, also a left-wing candidate and former guerrilla fighter, won the 2022

general election, making history as the first left-wing president to be elected in the country. He was also elected for a four-year term.

|

| • |

Panama: In 2022, rising living costs, especially of gasoline prices (which at one point in 2022 were almost 80% higher than at the same point in 2021), sparked the largest social protests in at least three

decades. The next presidential election will be held in May 2024.

|

| • |

Bolivia: Luis Arce, also from the left-wing, was elected president for a five-year term in 2020. Between late 2022 and January 2023, protests took place in Santa Cruz, which represents a larger proportion of

Bolivia’s GDP than any other city.

|

These protests have had a negative effect on economic activity and businesses in general in countries in which we have operations. Given these developments,

we cannot provide any assurance that Peru will not experience any residual effects from events in neighboring countries, such as the possibility of the base of protesters in Peru extending to the middle class, which may have a materially adverse

effect on our business and result of operations. Significant changes to Bolivian, Colombian, Chilean and Panamanian political and economic conditions could have an adverse effect on our business, financial conditions, and results of operations.

Bolivia

During 2022, the Bolivian economy continued to recover, supported by the performance of several economic sectors including transport, services, energy and

construction. Moreover, the war between Russia and Ukraine prolonged the rise in various commodity prices, which supported revenue from the exports of minerals, gas and some agricultural products. The effects of price inflation caused by the war,

however, were cushioned by subsidies implemented by Bolivia’s government. However, the increase in the price of oil generated additional pressure on Bolivia’s trade balance during the last quarter of 2022, reducing the surplus relative to 2021.

Similar to 2021, in 2022, there was slight increase in foreign currency deposits in the financial system, while the foreign-exchange reserves maintained the decreasing trend observed since 2015.

Notwithstanding increased government revenues from the mining sector and the end of certain pandemic-related emergency measures, which lowered Bolivia’s

fiscal deficit from 12.7% of GDP in 2020 to 9.3% of GDP in 2021, Bolivia has continued to fund approximately one-third of its budget deficit through its central bank. This has caused a marked decrease in Bolivia’s international reserves. According

to data published by the Bolivian Central Bank on February 8, 2023, its foreign reserves stood at US$ 3.5 billion (down from a peak of more than US$ 15 billion in 2014), the lowest level since 1996, of which gold reserves were US$ 2.6 billion and

foreign currency reserves stood at US$ 372 million. While the official exchange rate remained at approximately 6.96 bolivianos per Dollar, the unofficial exchange rate had reached as high as 7.40 bolivianos per Dollar as of February 8, 2023.

Consequently, in recent weeks, the Bolivian Central Bank began the direct sale of Dollars from its already low foreign reserves to meet public demand and exchanged most of its holdings of Special Drawing Rights (SDRs), which are international

reserve assets created by the International Monetary Fund to supplement the official reserves of its member countries, with the Central Bank’s holdings of SDRs decreasing from US$ 538 million as of February 8, to US$ 225 million as of February 28,

2023. The Bolivian Central Bank is also negotiating loans of up to US$1.4 billion from multilateral organizations, and as of March 2023, the Bolivian congress had approved loans from multiple lenders totaling approximately US$ 770 million. On March

14, 2023, Fitch cut Bolivia's sovereign rating from B to B-, and its outlook from stable to negative; and on March 24 Moody’s downgraded Bolivia’s rating from B2 to Caa1 and placed it on review for further downgrade.

According to local estimates, Bolivia’s GDP grew by approximately 4.0% in 2022. For 2023, the Ministry of Economy and the Central Bank have projected a

growth rate of 4.9%, driven by internal consumption, high commodities’ prices, and economic policies that promote macroeconomic stability and the industrialization of certain key economic sectors. Furthermore, the government expects a progressive

reduction in the fiscal deficit in 2023 (7.5% of GDP) and a stable level of inflation (3.3% by the end of the year). However, the continued possibility of political conflicts and social unrest constitutes a risk factor that may affect the economic

outlook for 2023.

Additionally, the lending quotas and caps on interest rates that were established in the financial services law (Ley de Servicios Financieros, No. 393),

which was enacted in 2013, and the mandatory deferrals and refinancings schemes instituted in 2020 and 2021 to mitigate the impacts of the COVID-19 pandemic, continued to negatively impact interest margins on banks, therefore reducing their ability

to generate enough capital to maintain the growth in their lending portfolios.

Colombia

According to the Colombian National Statistics Bureau (DANE), the Colombian economy exhibited a GDP growth of 7.5% in 2022, one of the highest growth rates globally. The strong

performance of the Colombian economy has been related to the highest level of terms of trade in several decades, as well as the remarkable evolution of consumption as household spending maintained strong momentum throughout the year amid

record-high remittances from abroad and a continuous reopening of the economy, which pushed services consumption. On its part, the government maintained an expansionary stance, similar to that observed during the first year of the COVID-19

pandemic, which also significantly supported domestic demand.

While economic activity consistently outperformed expectations in 2022, persistent challenges remain. First, despite the ongoing normalization in the monetary policy stance,

inflation pressures remain acute, postponing the period when it is expected to reach the target range of the monetary authority (early 2025). Thus, the estimate of the real neutral interest rate has increased and now is near 2.5%, compared to 1.5%

before the pandemic. Second, despite the favorable terms of trade observed last year, the current account deficit remains one of the largest among emerging countries (close to 5.7% of GDP in 2021 and 6.2% in 2022). The accumulated inflation was

superior than 13% in a context with an reference interest rate of 12%. Finally, although the fiscal deficit in 2022 was better than initially expected (5.5% as GDP) and the updated fiscal framework points towards its further reduction in 2023 (3.8%