UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(MARK ONE)

FOR THE FISCAL YEAR ENDED December 31 , 2023

OR

FOR THE TRANSITION PERIOD FROM __TO__

COMMISSION FILE NUMBER: 000-54887

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices)(Zip Code)

Registrant’s telephone number, including area code: 561 -998-2440

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |||||||

| None | Not applicable | |||||||

Securities registered under Section 12(g) of the Act:

Common stock, par value $0.01 per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.4.05 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large - accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large- accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | |||||||||||

| x | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) o Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked prices of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $12,704,754 on June 30, 2023.

As of March 29, 2024 we had 171,557,411 shares of our common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| Page No. | ||||||||

Item 1C. | ||||||||

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This Annual Report on Form 10-K for the year ended December 31, 2023 (this “Annual Report on Form 10-K”) contains forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements generally can be identified by words such as "anticipates," "believes," "estimates," "expects," "intends," "plans," "predicts," "projects," "will be," "will continue," "will likely result," “would, “could” and similar expressions. These forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties, which could cause our actual results to differ materially from those reflected in forward-looking statements. Factors that could cause or contribute to such differences in our actual results include those discussed in this Annual Report on Form 10-K, and in particular, the risks discussed under the caption "Risk Factors" in Item 1A and those discussed in other documents we file with the Securities and Exchange Commission (the "SEC"). Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. We undertake no obligation to revise or update forward-looking statements, except as required by law.

3

PART I

ITEM 1. DESCRIPTION OF BUSINESS

This business description should be read in conjunction with our audited consolidated financial statements and accompanying notes thereto appearing elsewhere in this Annual Report on Form 10-K, which are incorporated herein by this reference.

Unless specifically set forth to the contrary, when used in this Annual Report on Form 10-K the terms “Bright Mountain,” the “Company,” “we,” “our,” “us,” and similar terms refers to Bright Mountain Media, Inc., a Florida corporation, and our subsidiaries.

Business Overview

Organization and Nature of Operations

Bright Mountain Media, Inc. (together with its wholly-owned subsidiaries, the “Company,” “Bright Mountain” or “we”) has an end-to-end digital media and advertising services platform that efficiently connects brands with targeted consumer demographics. We focus on digital publishing, advertising technology, consumer insights, creative and media services.

Digital Publishing

Our digital publishing division focuses on developing content that attracts an audience and monetizes that audience through advertising. The current portfolio of owned and operated websites is focused on moms, parenting, families, and more broadly, women. The portfolio consists of popular websites including Mom.com, Cafemom.com, LittleThings.com, and MamasLatinas.com. This demographic is highly sought after by brands and their advertising agencies. We use internal and external technologies to constantly improve the effectiveness and efficiency of the content we create. Our publishing division monetizes its audiences through both direct and programmatic advertising sales.

Advertising Technology

Our advertising technology division focuses on delivering targeted ads to audiences on owned and operated sites as well as third-party publishers in a cost-effective manner through the deployment of proprietary technologies. By developing our own proprietary technology stack, we are able to pass along efficiencies to both the demand and supply side of the ecosystem. Our goal is to enable and support a streamlined, end-to-end advertising model that addresses both demand (buy side) and publisher supply (sell side) programmatic sales and delivery of digital advertisements using an array of audience targeting tools and advertising formats (display, audio, video, CTV, in-app). Programmatic advertising relies on software programs that leverage data and proprietary algorithms to match the optimal selection of an ad with a bid price offered by advertisers.

Consumer Insights

Our consumer insights division focuses on providing primary and secondary research, competitive intelligence, and expert insight to address customers' strategic issues. We provide cutting-edge and dynamic research, offering clients a comprehensive perspective on their consumers. This insight extends to strategic guidance on the optimal timing and channels to effectively connect with target audiences. Our cutting-edge approach combines advanced data analytics, artificial intelligence, and comprehensive market research, to uncover actionable insights that drive informed decision-making.

Creative Services

Our creative services division transforms data into award-winning campaigns. We are uniquely able to leverage insights teams with highly strategic media planning and buying teams to ensure brands not only position their advertising precisely, but also yield impactful business results. Our goal is to combine data-driven decisions with creativity fueled by a deep understanding of modern culture.

Media Services

Our media services division focuses on advertisers and agencies by providing access to premium inventory, leveraging data to optimize programmatic campaigns. Our aim is to empower clients to access the most sought-after

4

advertising spaces across diverse platforms tailored to their specific needs and preferences. Our data-driven approach ensures that ad placements are not only well-targeted, but also continuously optimized for maximum efficiency and ROI. Our commitment to combining premium inventory access with data-driven programmatic campaign optimization makes us an indispensable partner in the success of our clients' advertising and marketing endeavors.

The Company generates revenue through:

•the selling of advertisements placed on our owned and managed sites and on partner websites where we earn a share of the revenue;

•facilitating the seamless, real-time exchange of advertisements on a large scale, bridging networks of buyers (referred to as "DSPs") and networks of sellers (referred to as "SSPs");

•serving advertisers through providing access to premium resources and leveraging data to optimize programmatic campaigns, where revenue is derived from the planning and execution of creative and media marketing campaigns; and

•providing primary and secondary research, competitive intelligence, and expert insights to address customers' strategic issues, where revenue is primarily derived from providing a single integrated service for such research.

Our Strategy

Leveraging technology, data and insights to power customers’ creative and media strategies.

We Are Built on Advertising Technology

5

Innovative advertising technology built for modern digital media audiences. Our mission is to transform programmatic advertising through more sophisticated technology—with simpler, more straight-forward integrations—and a culture of true partnership.

We are Powered by Our Data Driven Insights

Our global research and analytics division uncovering not just the ‘what’ but the ‘why’ behind customer behavior, supporting clients’ insights needs with agile tools, CX research, branding, product innovation, data analytics, and more. We go beyond research to deliver integrated expertise and products that fine tune your data strategies, drive bottom line growth, and differentiate in today’s marketplace. Through collaboration with your teams to uncover the human truths that help you activate insight and accelerate growth.

A powerhouse of Millennial, Gen Z and Gen Alpha research, our consumer insights division is the foremost authority on emerging trends, generational insights, and youth behavior empowering companies to see tomorrow.

We Are Creative in Love with Our Craft

A modern creative and media shop that positions brands to be lifted by their audiences with contextually crafted work in social, digital, and traditional channels. We aim to understand what is happening now in humanity and culture and getting prepared for what's next.

We Are The Authority On Moms And Motherhood

Our division offers massive global reach through our engaging content and multicultural audiences. We are here for mom throughout her motherhood journey. Helping families raise happy, kind and confident kids. Delivering diverse voices and perspectives on motherhood.

Market Challenge

According to eMarketer's report, "US Ad Spending 2023", published May 2023, digital ad spending in the US faces its slowest growth rate in over a decade, even though almost $20.0 billion more was anticipated to be spent in 2023 compared to 2022. Most of the new money is going to new channels, rather than those that were popular just a few years ago. Total ad spending for 2023 in the U.S. was expected to reach approximately $350.00 billion. Digital was expected to account for 74.6% of that total, or $263.89 billion. Total media ad spending was anticipated to increase by just 3.8% due to negative growth from traditional media. TV, radio, out-of-home (OOH), and print ad spending were anticipated to collectively contract by 6.3% in 2023, with the bulk of the loss coming from TV.

According to eMarketer, CTV ad spending was set to be the second-fastest growing major ad channel in 2023.

According to eMarketer's report, "Advertising Trends to Watch in 2024", published November 2023, after growing at a compound annual rate of 17.6% over the past 15 years, digital ad spending is expected to settle into year over year growth in the low double digits starting in 2024 and through at least 2027. This is a sign of a mature market that should top $270.0 billion in 2024 and account for over three-quarters of all ad spending.

Industry Outlook

Impact on the U.S. Market

In April 2023, a report was published by Interactive Advertising Bureau ("IAB") titled "Internet Advertising Revenue Report, Full-Year 2022 Results." The report reflected how the digital advertising industry showed resilience in the face of a strained economy. Internet advertising revenues grew 10.8% year-over year (YoY), totaling $209.7 billion. After seeing exponential growth coming out of the pandemic, the highest level of growth seen since 2006, a deceleration in advertising revenues was expected. High inflation rates and economic uncertainty throughout 2022 impacted marketing budgets.

The IAB report states that the programmatic growth trend continued in 2022 as it grew 10.5% year over year and increased its share of overall non-search ad revenue to 12.7% (from 10.8% in 2021).

The IAB report indicated that mobile advertising revenues continue to strengthen with 14.1% YoY growth and ad revenues reaching a record high of $154.1 billion. The continued evolution and expansion of digital environments, the

6

increase in consumption of digital audio formats such as podcasts, plus the continued rollout of 5G and its beneficial impact on VR and AR advertising capabilities, were likely to continue to positively impact mobile ad revenues in 2023.

IAB indicated that they expected to see advertising budgets in 2023 continue to migrate to retail media networks as they offer advertisers access to first-party data for personalization and measurement in closed-loop environments.

Per the IAB report, regulatory uncertainty and continued economic challenges will likely threaten industry profit margins and reduce the rate of economic contributions. As user privacy concerns continue to rise and new state-level regulations are being introduced, it’s becoming increasingly evident that the industry needs to adapt and evolve beyond traditional methods.

Impact on the Worldwide Market

In January 2024, eMarketer published a report titled "Worldwide Digital Ad Spending Forecast 2024". The report stated that ad spending growth will accelerate across the board in 2024, and that digital media, traditional media, and total media ad spending will all grow faster worldwide this year than in 2023. After two years of relative malaise, the outlook is positive on a global scale and in every major region of the world. eMarketer indicated that digital advertising had a better 2023 than they originally predicted.

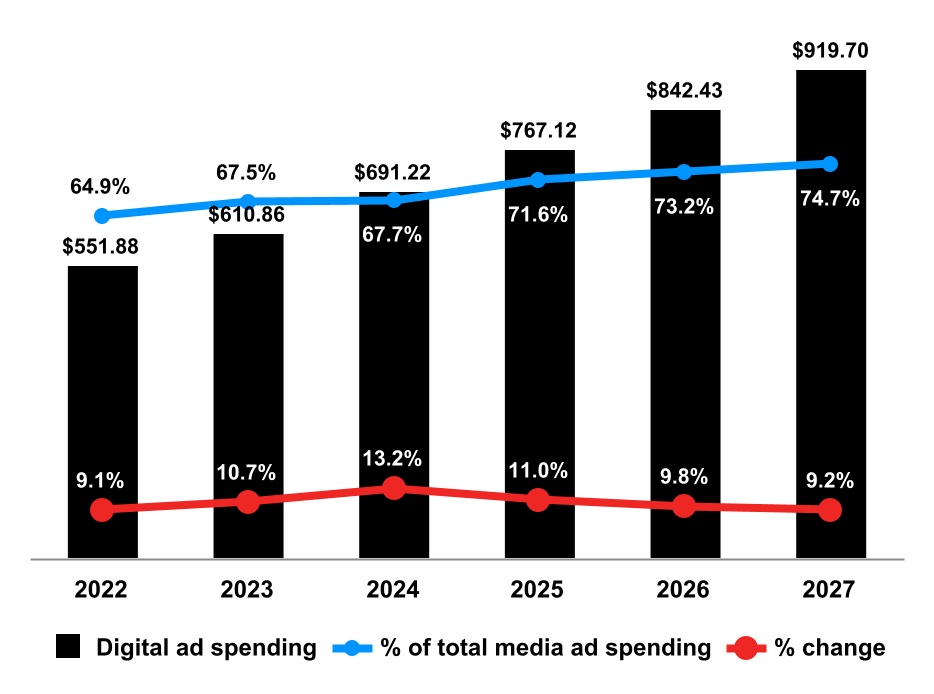

According to eMarketer's report, the US is expected to account for almost 40% of total worldwide ad spending and 44% of digital ad spending in 2024. In 2023, the US posted its slowest digital ad growth in 14 years of 9.7%, but the world's largest economy still produced $23.8 billion in new digital ad dollars. In other words, in a down year, the US produced more new digital ad spending than almost any other country in the world produced in total. The US is expected to return to double-digit growth for both total and digital ad spending this year, and its share of the worldwide spending in both categories is expected to tick up in the coming years, after taking a slight dip in 2023.

Digital Ad Spending Worldwide, 2022-2027 billions, % change and % of total media ad spending | ||||||||

Note: includes advertising that appears on desktop and laptop computers as well as mobile phones, tablets, and other internet-connected devices, and includes all the various formats of advertising on those platforms Source: Insider Intelligence | eMarketer Forecast, Oct 2023 | |||||||||||

| 284093 | www.eMarketer.com | ||||||||||

7

Intellectual Property

We currently rely on a combination of trade secret laws and restrictions on disclosure to protect our intellectual property rights. Our success depends on the protection of the proprietary aspects of our technology as well as our ability to operate without infringing on the proprietary rights of others. We also enter into proprietary information and confidentiality agreements with our employees, consultants and commercial partners and control access to, and distribution of, our software documentation and other proprietary information.

Technology and Product Platforms (Including URL’s)

Our top technical priorities are the security of our systems and the fast and reliable delivery of pages and ads to our users. Our systems are designed to handle processing of personal data, as well as traffic and network growth. We rely on multiple tiers of redundancy/failover and, with respect to our advertising technology business, third-party content delivery networks to achieve our goal of 24 hours-a-day, seven-days-a-week uptime. Regular automated backups protect the integrity of our data. Our servers are continuously monitored by numerous third-party and open-source monitoring and alerting tools.

Competition

We compete with other companies that have significantly greater financial, technical, marketing, and distribution resources.

Most of our competitors have significantly greater financial, technical, marketing and distribution resources as well as greater experience in the industry. There are no assurances we will ever be able to effectively compete in our marketplace. Our websites, ad technology, and monetization solutions may not be competitive with other technologies and/or our websites, ad technology, and monetization solutions may be displaced by newer technology. If this happens, our sales and revenues will likely decline. In addition, our current and potential competitors may establish cooperative relationships with larger companies, to gain access to greater development or marketing resources. Competition may result in price reductions, reduced gross margins and loss of market share.

Customers

Our customers are advertisers, advertising agencies and advertising service organizations seeking to have their respective advertisements placed on one of the many platforms serviced by the Company. For the years ended December 31, 2023 and 2022, two customers represented 23.0% of our revenue and one customer represented 37.7% of our revenue, respectively; both customers have the option to cancel their agreements by providing the Company 10 days and 30 days prior written notice, respectively.

Regulatory Environment

Interest-based advertising, or the use of data to draw inferences about a user’s interests and deliver relevant advertising to that user, has come under increasing scrutiny by legislative, regulatory, and self-regulatory bodies in the U.S. and abroad that focus on consumer protection or data privacy. In particular, this scrutiny has focused on the use of cookies and other technology to collect or aggregate information about Internet users’ online browsing activity. Because we, and our clients, rely upon large volumes of such data collected primarily through cookies, it is essential that we monitor developments in this area domestically and globally, and engage in responsible privacy practices, including providing consumers with notice of the types of data we collect and how we use that data to provide our services.

We rely on IP addresses, geo-location information, and persistent identifiers about Internet users and do not attempt to associate this data with other data that can be used to identify real people. This type of information is considered personal data in some jurisdictions or otherwise may be the subject of future legislation or regulation. The definition of personal data varies by state and country and continues to evolve in ways that may require us to adapt our practices to avoid violating laws or regulations related to the collection, storage, and use of consumer data. For example, some European countries consider IP addresses or unique device identifiers to be personal data subject to heightened legal and regulatory requirements. As a result, our technology platform and business practices must be assessed regularly in each country in which we do business.

8

There are also several specific foreign laws and regulations governing the collection and use of certain types of consumer data relevant to our business.

For instance, the use and transfer of personal data in the European Union (the "EU") member states is currently governed under the EU Data Protection Directive, which generally prohibits the transfer of personal data of EU subjects outside of the EU, unless the party exporting the data from the EU implements a compliance mechanism designed to ensure that the receiving party will adequately protect such data. In addition, the EU has finalized the General Data Protection Regulation (“GDPR”), which became effective in May 2019. The GDPR sets out higher potential liabilities for certain data protection violations, as well as a greater compliance burden for us in the course of delivering our solution in Europe. Among other requirements, the GDPR obligates companies that process large amounts of personal data about EU residents to implement a number of formal processes and policies reviewing and documenting the privacy implications of the development, acquisition, or use of all new products, technologies, or types of data. Further, the EU is expected to replace the EU Cookie Directive governing the use of technologies to collect consumer information with the EU ePrivacy Regulation. The EU ePrivacy Regulation proposes burdensome requirements around obtaining consent and imposes fines for violations that are materially higher than those imposed under the EU Cookie Directive.

Additionally, our compliance with our privacy policy and our general consumer privacy practices are also subject to review by the Federal Trade Commission and state regulators, which may bring enforcement actions to challenge allegedly unfair and deceptive trade practices, including the violation of privacy policies and representations therein. Certain State Attorneys General may also bring enforcement actions based on comparable state laws or federal laws that permit state-level enforcement. Outside of the U.S., our privacy and data practices are subject to regulation by data protection authorities and other regulators in the countries in which we do business.

Human Capital

Because of the service nature of our business, the quality of personnel is of crucial importance to our continuing success and our employees, including creative, digital, research, media and account specialists, and their skills and relationships with clients, are among our most valuable assets. There is keen competition for qualified employees.

As of December 31, 2023, we had 190 employees, of which 173 were employed in the U.S. and 17 outside of the U.S., in Thailand.

We employ a balanced approach in managing our human capital resources. Depending on where a human-capital management function is most effective or efficient, processes are either managed at the holding company or designated to our operating units to adopt strategies appropriate for their client sector, workforce makeup, talent requirements and business demands.

The holding company retains oversight of all human capital resources and activities, setting standards, providing support and policy guidance, and sharing programs. At the corporate center, centralized human capital management processes include development of human resources governance and policy; executive compensation for senior leaders across the Company; benefits programs; performance planning, development and retention of the Company’s senior executives and key roles in the operating units; and executive development.

The Company sets specific standards for human capital management and, on a yearly basis, assesses each operating unit’s performance in managing and developing its workforce. We undertake human capital initiatives with the aim of ensuring that employees have the high level of competence and commitment our business needs to succeed. We formally assess our operating units against their efforts in the areas of people development, diversity and inclusion, performance management, talent acquisition and organization development in order to drive or support the units’ strategic business and growth goals. Accordingly, the operating units create and deploy skills-training programs, management training, employee goal-setting and feedback platforms, applicant-tracking systems, new-employee onboarding processes, and other programs intended to enhance the performance and engagement of the workforce.

Diversity, Equity and Inclusion are essential priorities for the Company. Our goal is that our talent represents the diversity of our communities and consumers, with a corporate culture that drives belonging, well-being and growth. We believe that such a workplace will enable us to provide cultural insights to help our clients make authentic and responsible connections with their customers. The programs we provide in support of diversity, equity and inclusion include, training and curated and bespoke content, research and tools, to foster awareness and action on an array of critical issues that we believe are vital for the recruitment, retention, advancement, well-being and belonging for people who are part of under-represented groups.

9

The Company has a 401(K) plan that covers employees that have reached 18 years of age upon commencement of employment. The plan provides for voluntary employee contribution through salary deductions. For the year ended December 31, 2023, and 2022, there were no employer contribution made.

History of Our Company

We were organized as a Florida corporation in 2010 but remained a development stage company until 2013, when we changed our name to Bright Mountain Holdings, Inc., and began building our digital marketing brand in 2014. In 2015, we changed our name again to Bright Mountain Acquisition Corporation, and then to Bright Mountain Media, Inc., as we began acquiring businesses, including e-commerce businesses, and implementing our strategy to transform into a digital publishing and advertising technology holding company. During 2018, we discontinued our e-commerce product sales segment to focus entirely on the advertising segment. In 2020, we acquired Wild Sky Media in the digital publishing area consistent with our strategy to transform into a digital publishing and advertising technology holding company. In 2023, we expanded our focus when we completed the acquisition of two business units of Big Village (Big Village Insights, Inc and Big Village Agency LLC, (together, the “Big Village Entities”)). Through these acquisitions, we have now expanded how we connect with our customers focusing on consumer insights, and creative and media services. We currently have six subsidiaries: CL Media Holdings LLC, Bright Mountain LLC, Mediahouse, LLC, Slutzky & Winshman Ltd, Big-Village Agency LLC, and BV Insights LLC; each of which offers a unique service to our customers. During the year ended December 31, 2023, we terminated operations of Mediahouse, LLC and Slutzky & Winshman Ltd, which were located in the United States and Israel, respectively. At December 31, 2023, these two entities held no employees but had not been dissolved.

Our principal executive offices are located at 6400 Congress Avenue, Suite 2050, Boca Raton, FL 33487, and our

telephone number is (561) 998-2440.

Available Information

The Company’s Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are available free of charge through the “Investor Relations” section of the Company’s website, www.brightmountainmedia.com, as soon as reasonably practical after they are filed with the Securities and Exchange Commission (“SEC”). The SEC maintains a website, www.sec.gov, which contains periodic reports, proxy and information statements, and other information filed electronically with the SEC by the Company. The information on, or that can be accessed through our website is not incorporated by reference in, or considered part of, this Annual Report on Form 10-K.

10

ITEM 1A. RISK FACTORS

Our business, financial condition, results of operations, prospects and the prevailing market price and performance of our common stock may be adversely affected by a number of factors, including the factors discussed below. You should carefully consider the risk factors set forth below and elsewhere in this Annual Report on Form 10-K, together with all the other information included in this Annual Report on Form 10-K. The risks and uncertainties described in this Annual Report on Form 10-K or in any document incorporated by reference herein are not the only risks and uncertainties that we face. Additional risks that are not presently known to us or that we currently believe to be immaterial may become material and adversely affect our business. If any of the following risks and uncertainties develop into actual events, our business, financial condition, results of operations, prospects or the prevailing market price and performance of our common stock could be materially adversely affected, and you could lose your entire investment in our Company.

Summary of Principal Risk Factors

Risks Relating to Our Financial Condition and Indebtedness

•We have a history of losses.

•We may not be able to refinance, extend or repay our substantial indebtedness owed to Centre Lane, which would have a material adverse effect on our financial condition and ability to continue as a going concern.

•Our secured indebtedness may impair our ability to operate our business.

•We have depended upon sales of equity securities and borrowings under the Centre Lane Senior Secured Credit Facility to provide operating capital.

•Our economic performance has raised substantial doubt about our ability to continue as a going concern.

•If we fail to establish and maintain adequate internal control over our financial and management system, our ability to accurately and timely report our financial results could be adversely affected, resulting in errors in our financial reporting, which could cause a loss of investor confidence.

•We depend upon a substantial portion of our revenues from a limited number of customers.

•We are subject to seasonal fluctuations in our revenues in future periods.

•Our cash could be adversely affected if the financial institutions in which we hold our cash fail.

Risks Related to Our Operations

•Past acquisitions and any future acquisitions, joint ventures, strategic alliances or similar transactions may not perform as expected.

•The acquisition of new businesses is costly, and these acquisitions may not enhance our financial condition.

•If we fail to detect advertising fraud or other actions that impacts our advertising campaign performance, we could harm our reputation with advertisers or agencies, which would cause our revenue and business to suffer.

•If advertising on the internet loses its appeal, our revenue could decline.

•Our success is dependent upon our ability to effectively expand and manage our relationships with our publishers.

•Online security breaches or other disruptions of our information technology systems could harm our business.

•We must generate high quality content in order to attract and retain users, advertisers and strategic buyers.

•We may expend significant resources to protect our content or to defend claims of infringement by third parties, and if we are not successful, we may lose the rights to use material or be required to pay significant fees.

•Failure to protect our intellectual property rights or claims by others that we infringe their intellectual property rights could substantially harm our business.

•Developing and implementing new and updated applications, features and services for our websites may be more difficult than expected, may take longer and cost more than expected and may not result in sufficient increases in revenue to justify the costs.

•If we are unable to obtain or maintain key website addresses, our ability to operate and grow our business may be impaired.

•If we are unable to respond to rapid technological change, our products and services could become obsolete, and our reputation could suffer.

•Our ability to deliver our content depends upon the quality, availability, policies and prices of certain third-party service providers.

•We may be held liable for content or third-party links on our website or content distributed to third parties, and our general liability insurance may not be adequate to compensate us for all liabilities to which we are exposed.

•We depend on our senior management team and other key employees, and the loss of any of them could harm our business.

•We must hire, integrate and/or retain qualified personnel to support our business.

11

•We deliver advertisements to users from third-party advertising services, which exposes our users to content and functionality over which we do not have ultimate control.

•Our services may be interrupted if we experience problems with our network infrastructure.

•Our systems may fail due to natural disasters, telecommunications failures and other events, any of which would limit user traffic.

•We are unable to predict the impacts of COVID-19 and any other future pandemic or outbreak of disease on our business.

•Privacy violations could impair our business.

•We are subject to several regulatory risks, and any failure to comply with various regulations could adversely impact our business.

•Litigation is both costly and time-consuming, and there is no certainty of a favorable result.

•Our industry is intensely competitive, and if we do not effectively compete against current and future competitors, our business, results of operations and financial condition could be harmed.

•We may be adversely affected by the effects of inflation.

•Our platform relies on third-party open source software components.

•The effectiveness of certain services we offer depends on our ability to collect and use online data.

•The rejection of digital advertising by consumers, through opt-in, opt-out or ad-blocking technologies or other means or the restriction on the use of third party-cookies, mobile device identifiers or other tracking technologies, could adversely affect our business, results of operations, and financial condition.

•If ad formats and digital device types develop in ways that prevent advertisements from being delivered to consumers, our business, results of operations, and financial condition may be adversely affected.

•Our intellectual property rights may be difficult to enforce and protect, which could enable others to copy or use aspects of our technology without compensating us, thereby eroding our competitive advantages and having an adverse effect on our business, results of operations, and financial condition.

•We could experience a decline in renewals or demand for our subscription-based research services.

•We may be unable to develop and offer new research products and services.

•Our creative advertising services division may not be able to remain competitive or retain key clients.

Risks Related to the Ownership of Our Securities

•There is a limited public market for our Common Stock.

•We have outstanding convertible notes, options and warrants to purchase approximately 19% of our outstanding Common Stock, which will have a dilutive effect on our existing shareholders if converted or exercised.

•The concentration of stock ownership and control by Centre Lane, and our debt transaction with Centre Lane, may cause conflicts of interests that may adversely affect us.

•Some provisions of our charter documents and Florida law may have anti-takeover effects that could discourage an acquisition of us by others, even if an acquisition would be beneficial to our shareholders and may prevent attempts by our shareholders to replace or remove our current management.

•Our Company has a concentration of stock ownership and control, which may have the effect of delaying, preventing or deterring a change of control.

•We do not anticipate paying any cash dividends on our Common Stock in the foreseeable future and, as such, capital appreciation, if any, of our Common Stock will be your sole source of gain for the foreseeable future.

•We may issue additional shares of preferred stock in the future that may adversely impact your rights as holders of our Common Stock.

RISKS RELATING TO OUR FINANCIAL CONDITION AND INDEBTEDNESS

We have a history of losses.

We incurred significant net losses for the years ended December 31, 2023, and 2022, and at December 31, 2023, we had a significant accumulated deficit. There is substantial doubt that we will be able to significantly increase our revenues and gross profit to a level which supports profitable operations and provides sufficient funds to pay our operating expenses and other obligations as they become due. The Company’s ability to continue as a going concern is dependent on its ability to meet its liquidity needs through a combination of factors. The Company is currently exploring all strategic alternatives, including restructuring or refinancing its debts, seeking additional debt, such as borrowings under the Centre Lane Senior Secured Credit Facility or seeking equity capital. The ability to access the capital market is also dependent on the stock volume and market price of the Company's stock, which cannot be assured. The Company may need to pursue other measures including reducing or delaying certain business activities, reducing general and administrative expenses, and reducing its headcount.

12

We may not be able to refinance, extend or repay our substantial indebtedness owed to Centre Lane, which would have a material adverse effect on our financial condition and ability to continue as a going concern.

We anticipate that we will need a significant amount of cash in the near future in order to repay the portion of our outstanding debt obligations owed under the Centre Lane Senior Secured Credit Facility as and when they mature during 2024. As of December 31, 2023, we owed Centre Lane $70.2 million under the Centre Lane Senior Secured Credit Facility. Of this amount, $879,000, $3.0 million, $879,000 and $879,000 is due on March 31, 2024, June 30, 2024, September 30, 2024 and December 31, 2024, respectively. The balance of $64.6 million is due in 2025 or later. If we have insufficient cash to pay these amounts and we are otherwise unable to extend the maturity dates or refinance these obligations, we would be in default. We cannot provide any assurances that we will be able to raise the necessary amount of capital to repay these obligations or that we will be able to extend the maturity dates or otherwise refinance these obligations. Upon a default in the Centre Lane Senior Secured Credit Facility, Centre Lane would have the right to exercise its rights and remedies to collect, which would include foreclosing on our assets. Accordingly, a default would have a material adverse effect on our business and, if Centre Lane exercises its rights and remedies, we would likely be forced to seek bankruptcy protection.

Our secured indebtedness may impair our ability to operate our business.

As of December 31, 2023, and 2022, we had $70.2 million and $33.1 million in outstanding secured indebtedness under the Centre Lane Senior Secured Credit Facility, respectively. The instruments governing our existing secured indebtedness may inhibit our ability to incur additional debt and require significant payments from the proceeds of any debt or equity sale without the consent of the lender. In addition, we have additional covenants and obligations under the secured indebtedness which may limit our ability to operate our business. Our ability to repay the indebtedness may require us to dedicate a substantial portion of our cash flow for operations to payment of debt service and principal thereby reducing funds available to implement our business strategy. Our level of indebtedness could also provide limits in our ability to adjust to changing market conditions and vulnerability in the event of a downturn in economic conditions in the businesses in which we operate and impair our ability to obtain additional financing for our business strategy. If we are unable to meet our obligations under the secured indebtedness, the lender may call a default and our business could be foreclosed upon.

We have depended upon sales of equity securities and borrowings under the Centre Lane Senior Secured Credit Facility to provide operating capital.

Historically, we have not generated sufficient gross profit to pay our operating expenses and we reported a net loss for the years ended December 31, 2023, and 2022. During 2023 and 2022, we were dependent on borrowings under the Amended and Restated Centre Lane Senior Secured Credit Facility (the "Centre Lane Senior Secured Credit Facility") to support our working capital needs. We are not currently a party to any binding agreements to raise additional capital and there are no assurances we will be able to raise any additional third-party capital. Although we recently improved our gross profit substantially and became cash flow positive, there can be no assurance that this trend will continue, and if it does not continue, and we are unable to raise sufficient additional working capital as needed, we may be unable to grow our Company, and we may not be able to pay our liabilities as they come due.

The Company’s economic performance has raised substantial doubt about our ability to continue as a going concern.

Our audited consolidated financial statements have been prepared assuming we will continue as a going concern. We have experienced substantial and recurring losses from operations, which losses have caused an accumulated deficit of $149.8 million at December 31, 2023. Our independent registered public accounting firm’s report on our audited financial statements includes an explanatory paragraph related to substantial doubt about the Company’s ability to continue as a going concern. Our audited consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

If we fail to establish and maintain adequate internal control over our financial and management system, our ability to accurately and timely report our financial results could be adversely affected, resulting in errors in our financial reporting, which could cause a loss of investor confidence.

We must maintain effective financial and management systems and internal controls to meet our public company reporting obligations. Moreover, the Sarbanes-Oxley ("SOX") requires, among other things, that we maintain effective

13

disclosure controls and procedures and internal control over financial reporting. If we have a material weakness or deficiency in our internal control over financial reporting, we may not detect errors on a timely basis and our financial statements may be materially misstated. Effective internal controls are necessary for us to produce reliable financial reports and are important to prevent fraud. As a result, our failure to maintain effective financial and management systems and internal controls could result in errors in our financial reporting, us being subject to regulatory action and a loss of investor confidence in the reliability of our financial statements.

We depend upon a substantial portion of our revenues from a limited number of customers.

For the year ended December 31, 2023, two customers represented 23.0% of our revenue, and for the year ended December 31, 2022, one customer represented 37.7% of our revenue. The loss of these customers could have a material adverse impact on our results of operations in future periods. There are inherent risks whenever a large percentage of total revenues are concentrated with a limited number of customers. It is not possible for us to predict the future level of demand for our services that will be generated by these customer. In addition, revenues from these customers may fluctuate from time to time based on the commencement and completion of projects, the timing of which may be affected by market conditions or other facts, some of which may be outside of our control. If these customers experiences declining or delayed sales due to market, economic or competitive conditions, we could be pressured to reduce the prices we charge for our services or we could lose two major customers. These customers may generally terminate their business with us upon 10 and 30 days’ notice, respectively. Any such development could have an adverse effect on our margins and financial position and would negatively affect our revenue, results of operations and/or the trading price of our Common Stock.

We are subject to seasonal fluctuations in our revenues in future periods.

Typically advertising technology companies report a material portion of their revenues during the fourth calendar quarter as a result of holiday-related advertising spending. Our experience has been consistent with this trend. Because of seasonal fluctuations, there can be no assurance that the results of any particular quarter will be indicative of results for the full year or for future years or quarters.

Our cash could be adversely affected if the financial institutions in which we hold our cash fail.

The Company maintains domestic cash deposits in Federal Deposit Insurance Corporation (“FDIC”) insured banks. The domestic bank deposit balances may exceed the FDIC insurance limits. Also, in the foreign markets we serve, we also maintain cash deposits in foreign banks, some of which are not insured or partially insured by the FDIC or other similar agency. These balances could be impacted if one or more of the financial institutions in which we deposit monies fails or is subject to other adverse conditions in the financial or credit markets.

RISKS RELATED TO OUR OPERATIONS

Past acquisitions and any future acquisitions, joint ventures, strategic alliances or similar transactions may not perform as expected.

We have consummated and may continue to consummate acquisitions, joint ventures and strategic alliances in order to provide increased capabilities to our existing products, supply new products and services or enhance our distribution channels. We may make strategic acquisitions of and investments in other businesses that offer complementary products, services and technologies, augment our market segment coverage and geographic locations, or enhance our technological capabilities. We may also enter into strategic alliances or joint ventures to achieve these goals. If we fail to integrate acquired businesses successfully into our existing businesses, or if these businesses fail to perform as well as we had anticipated, we could incur unanticipated expenses and losses, and the costs of the acquisition could exceed the benefits either in the short term or the long term.

Risks that could have a material adverse effect on our business, results of operations or financial condition include, without limitation:

•the inability of the acquired business to meet the sales and operating projections provided to us;

•the difficulty of assimilating the operations and personnel of acquired businesses;

•the unexpected loss of customers of the acquired business;

•the diversion of management time and resources and the potential disruption of our ongoing business;

14

•the potential inability of management to maximize our financial and strategic position as a result of an acquisition or investment;

•the potential for costs and delays in implementing, and the potential difficulty in maintaining, uniform standards, controls, procedures and policies, including the integration of different information systems;

•unexpected costs and time associated with upgrading the acquired business's internal accounting systems as well as educating each of its staff as to the proper methods of collecting and recording financial data;

•the risk of entering market segments in which we have no or limited direct prior experience and where competitors in such market segments have stronger market segment positions;

•potential unknown liabilities associated with acquired businesses;

•the risk that there could be deficiencies in the internal controls of any acquired company or investments that could result in a material weakness in our overall internal controls taken as a whole; and

•the potential loss of key employees of an acquired company.

We cannot assure you that we will be successful in overcoming these risks or any other problems encountered with acquisitions and other strategic transactions. These risks may prevent us from realizing the expected benefits from acquisitions and could result in the failure to realize the full economic value of a strategic transaction or the impairment of goodwill and/or intangible assets recognized at the time of an acquisition. These risks could be heightened if we complete a large acquisition or multiple acquisitions within a short period of time.

The acquisition of new businesses is costly, and these acquisitions may not enhance our financial condition.

An element of our growth strategy has been to acquire companies which complement our business. The process to undertake a potential acquisition can be time-consuming and costly. We have expended and expect to continue to expend significant resources to undertake business, financial and legal due diligence on potential acquisition targets. In addition, there is no guarantee that we will acquire the company after completing due diligence. The process of identifying and consummating an acquisition could result in the use of substantial amounts of cash and exposure to undisclosed or potential liabilities of acquired companies. In some instances, we may be required to provide historic audited financial statements for up to two years for acquisition targets in compliance with the rules and regulations of the SEC. The necessity to provide these audited financial statements will increase the costs to us of consummating an acquisition or, if it is determined that the target company cannot obtain the requisite audited financials, we may be unable to pursue an acquisition which might otherwise be accretive to our business. In addition, even if we are successful in acquiring additional companies, there are no assurances that the operations of these businesses will enhance our future financial condition. To the extent that a business we acquire does not meet the performance criteria used to establish a purchase price, some or all of the goodwill related to that acquisition could be charged against our future earnings, if any.

If we fail to detect advertising fraud or other actions that impacts our advertising campaign performance, we could harm our reputation with advertisers or agencies, which would cause our revenue and business to suffer.

Some campaigns may experience fraudulent and other invalid impressions, clicks or conversions that advertisers may perceive as undesirable, such as non-human traffic generated by machines that are designed to simulate human users and artificially inflate user traffic on websites. These activities could overstate the performance of any given advertising campaign and could harm our reputation. It may be difficult for us to detect fraudulent or malicious activity on websites where we do not own content and rely in part on our customers to control such activity. If we fail to detect or prevent fraudulent or other malicious activity, the affected advertisers may experience or perceive a reduced return on their investment and our reputation may be harmed. High levels of fraudulent or malicious activity could lead to dissatisfaction with our solutions, refusals to pay, demands for refunds or future credit or withdrawal of future business.

If advertising on the internet loses its appeal, our revenue could decline.

Our business model may not continue to be effective in the future for a number of reasons, including:

•a decline in the rates that we can charge for advertising and promotional activities;

•our inability to create applications for our customers;

•the fact that internet advertisements and promotions are, by their nature, limited in content relative to other media;

15

•companies may be reluctant or slow to adopt online advertising and promotional activities that replace, limit or compete with their existing direct marketing efforts;

•companies may prefer other forms of Internet advertising and promotions that we do not offer;

•the quality or placement of transactions, including the risk of non-screened, non-human inventory and traffic, could cause a loss in customers or revenue; and

•regulatory actions may negatively impact our business practices.

If the number of companies who purchase online advertising and promotional services from us does not grow, we may experience difficulty in attracting publishers, and our revenue could decline.

Our success is dependent upon our ability to effectively expand and manage our relationships with our publishers.

Outside of our owned and operated websites, we are dependent upon our publishing partners to provide the media we sell. We depend on these publishers to make their respective media inventories available to us to use in connection with the campaigns that we manage, create or market. Our growth depends, in part, on our ability to expand and maintain our publisher relationships within our network and to have access to new sources of media inventory such as new partner websites and Facebook pages that offer attractive demographics, innovative and quality content and growing Web user traffic volume. Our ability to attract new publishers to our networks and to retain Web publishers currently in our networks will depend on various factors, some of which are beyond our control. These factors include, but are not limited to, our ability to introduce new and innovative products and services, our pricing policies, and the cost-efficiency to Web publishers of outsourcing their advertising sales. In addition, the number of competing intermediaries that purchase media inventory from Web publishers continues to increase. In the event we are not able to maintain effective relationships with our publishers, our ability to distribute our advertising campaigns will be greatly hindered which will reduce the value of our services and adversely impact our results of operations in future periods.

Online security breaches or other disruptions of our information technology systems could harm our business.

The efficient operation of our business depends on our information technology systems. We collect, process, store, and share high volumes of personal information which is regulated by various laws. We rely on encryption and authentication technology to effect secure transmission of such information. These systems may be susceptible to damage, disruptions or shutdowns due to attacks by computer hackers, computer viruses, employee error or malfeasance, power outages, hardware failures, telecommunication or utility failures, catastrophes or other unforeseen events. We may need to expend significant resources to protect against security breaches or to address problems caused by breaches.

While we are unaware of any security breaches to date, experienced programmers or “hackers” could penetrate sectors of our systems. Because a hacker who is able to penetrate network security could misappropriate proprietary information or cause interruptions in our services, we may have to expend significant capital and resources to protect against or to alleviate problems caused by hackers. We frequently update and improve our information security environment and assess and adopt new methods, devices, and technologies, but our policies and information security controls may not keep pace with emerging threats. Additionally, we may not have a timely remedy against a hacker who is able to penetrate our network security. Threats to information security evolve constantly and are increasingly sophisticated and complex, which makes detecting and successfully defending against them more difficult. Undetected vulnerabilities may persist in our network environment over long periods of time and could come from or spread to the networks and systems of our suppliers and customers. Such security breaches could materially affect our operations, damage our reputation and expose us to risk of loss or litigation. In addition, the transmission of computer viruses resulting from hackers or otherwise could expose us to significant liability. Our insurance policies may not be adequate to reimburse us for losses caused by security breaches. We also face risks associated with security breaches affecting third parties with whom we have relationships. In addition, government regulators may impose fines, penalties, and other civil or criminal consequences for security breaches and inadequate information security.

We must generate high quality content in order to attract and retain users, advertisers and strategic buyers.

The success of the Wild Sky Media brand depends largely on its ability to provide high quality content which is of interest to its users. If its users do not perceive its existing content to be of high quality, or if we introduce new content or enter into new business ventures that are not favorably perceived by users, we may not be successful in promoting and maintaining the Wild Sky Media brand. Any change in the focus of our operations as a result of the content we provide

16

creates a risk of diluting our brand, confusing users and decreasing the value of our website traffic base to advertisers. If we are unable to maintain or grow the Wild Sky Media brand, our business could be harmed.

We may expend significant resources to protect our content or to defend claims of infringement by third parties, and if we are not successful, we may lose the rights to use material or be required to pay significant fees.

Our success and ability to compete are dependent on our proprietary content. We rely on copyright law to protect our content. While we actively take steps to protect our proprietary rights, these steps may not be adequate to prevent the infringement or misappropriation of our content, which could harm our business. In addition to content written by our employees, we also acquire content from various freelance providers and other third-party content providers. While we attempt to ensure that such content may be freely used by us, other parties may assert claims of infringement against us relating to such content. We may need to obtain licenses from others to refine, develop, market and deliver new content or services. We may not be able to obtain any such licenses on commercially reasonable terms or at all or rights granted pursuant to any licenses may not be valid and enforceable.

Failure to protect our intellectual property rights or claims by others that we infringe their intellectual property rights could substantially harm our business.

Our website domain names are crucial to our business. However, as with phone numbers, we do not have and cannot acquire any property rights in an internet address. The regulation of domain names in the U.S. and in other countries is also subject to change. Regulatory bodies could establish additional top-level domains, appoint additional domain name registrars or modify the requirements for holding domain names. As a result, we might not be able to maintain our domain names or obtain comparable domain names, which could harm our business. We also rely on a combination of trade secret laws and restrictions on disclosure to protect our intellectual property rights. Our success depends on the protection of the proprietary aspects of our technology as well as our ability to operate without infringing on the proprietary rights of others. Despite these measures, any of our intellectual property rights could be challenged, invalidated, circumvented or misappropriated. Others may independently discover our trade secrets and proprietary information, and in such cases, we could not assert any trade secret rights against such parties. Costly and time-consuming litigation could be necessary to enforce and determine the scope of our intellectual property rights. Therefore, in certain jurisdictions, we may be unable to protect our technology and designs adequately against unauthorized third-party use, which could adversely affect our ability to compete.

Developing and implementing new and updated applications, features and services for our websites may be more difficult than expected, may take longer and cost more than expected and may not result in sufficient increases in revenue to justify the costs.

Attracting and retaining users of our websites requires us to continue to provide quality, targeted content and to continue to develop new and updated applications, features and services for our websites. If we are unable to do so on a timely basis or if we are unable to implement new applications, features and services without disruption to our existing ones, our ability to continue to expand our website traffic will be in jeopardy. The costs of development of these enhancements may negatively impact our ability to achieve profitability. There can be no assurance that the revenue opportunities from expanded website content, or updated technologies, applications, features or services will justify the amounts ultimately spent by us.

If we are unable to obtain or maintain key website addresses, our ability to operate and grow our business may be impaired.

Our website addresses, or domain names, are critical to our business. We currently own more than 142 domain names. However, the regulation of domain names is subject to change, and it may be difficult for us to prevent third parties from acquiring domain names that are similar to ours, that infringe our trademarks or that otherwise decrease the value of our brands. If we are unable to obtain or maintain key domain names for the various areas of our business, our ability to operate and grow our business may be impaired.

If we are unable to respond to rapid technological change, our products and services could become obsolete, and our reputation could suffer.

The markets for our products and services are characterized by rapidly changing technology, evolving industry standards and increasingly sophisticated customer requirements. The introduction of products embodying new technology

17

and the emergence of new industry standards can negatively impact the marketability of our existing products and can exert price pressures on existing products. Additionally, if our websites or services do not work as intended, or if we are unable to upgrade the functionality of our websites or services as needed to keep up with the rapid evolution of technology , our websites or services may not operate properly or as efficiently as those of our competitors, which could harm our business. It is critical to our success that we are able to anticipate and react quickly to changes in technology or in industry standards and to successfully develop, introduce, and achieve market acceptance of new, enhanced and competitive products and services on a timely basis and cost-effective basis. Software product design, development and enhancement involve creativity, expense and the use of new development tools and learning processes. Delays in software development processes are common, as are project failures, and either factor could harm our business. There can be no assurance that we will successfully develop new products and services or enhance and improve our existing products and services, that new products and services and enhanced and improved existing products and services will achieve market acceptance or that the introduction of new products and services or enhanced existing products and services by others will not negatively impact us. Our inability to develop products and services that are competitive in technology and price and that meet end-user needs could have a material adverse effect on our business, financial condition or results of operations.

Our ability to deliver our content depends upon the quality, availability, policies and prices of certain third-party service providers.

We rely on third parties to provide website hosting services. In certain instances, we rely on a single service provider for some of these services. In the event the providers were to terminate our relationship or stop providing these services, our ability to operate our websites could be impaired. Our ability to address or mitigate these risks may be limited. The failure of all or part of our website hosting services could result in a loss of access to our websites which would harm our results of operations.

We may be held liable for content or third-party links on our website or content distributed to third parties, and our general liability insurance may not be adequate to compensate us for all liabilities to which we are exposed.

As a publisher and distributor of content over the internet, including links to third-party websites that may be accessible through our websites, or content that includes links or references to a third-party’s website, we face potential liability for defamation, negligence, copyright, patent or trademark infringement and other claims based on the nature, content or ownership of the material that is published on or distributed from our websites. These types of claims have been brought, sometimes successfully, against online services, websites and print publications in the past. Other claims may be based on errors, or false or misleading information provided on linked websites, including information deemed to constitute professional advice such as legal, medical, financial or investment advice. Although we carry general liability insurance, our insurance may not be adequate to indemnify us for all liabilities imposed. Any liability that is not covered by our insurance or is in excess of our insurance coverage could severely harm our financial condition and business. Implementing measures to reduce our exposure to these forms of liability may require us to spend substantial resources and limit the attractiveness of our websites to users.

We depend on our senior management team and other key employees, and the loss of any of them could harm our business.

We rely on our leadership team and other key employees. From time to time, there are changes in our management team resulting from the hiring or departure of executives or other key employees, which could disrupt our business. Although some of our senior management are parties to an employment contract with us, some of our senior management and key employees are employed on an at will basis, which means that they could terminate their employment with us at any time. The loss of one or more of our executive officers or key employees could have a material adverse effect on our business.

We must hire, integrate and/or retain qualified personnel to support our business.

Our success also depends on our ability to attract, train and retain qualified personnel. Competition for qualified personnel is intense and we may experience difficulty in hiring and retaining highly skilled employees with appropriate qualifications. If we fail to attract and retain qualified personnel, our business may suffer.

We deliver advertisements to users from third-party advertising services, which exposes our users to content and functionality over which we do not have ultimate control.

18

We display pay-per-click, banner, cost per acquisition (“CPM”), direct, and other forms of advertisements to users that come from third-party advertising services. We do not control the content and functionality of such third-party advertisements and, while we provide guidelines as to what types of advertisements are acceptable, there can be no assurance that such advertisements will not contain content or functionality that is harmful to users. Our inability to monitor and control what types of advertisements get displayed to users could negatively impact our reputation and have a material adverse effect on our business, financial condition and results of operations.

Our services may be interrupted if we experience problems with our network infrastructure.

Various risks could interrupt access to our primary network infrastructure or data, exposing us to significant costs and other liabilities. Our revenue depends on technology for critical business operations, providing services to our clients, delivering and measuring advertising impressions, operating our ad exchange, and impression placement. That technology further depends on our IT systems' continuing and uninterrupted performance. Our IT infrastructure operates on cloud-based service providers, Software as a Service (SaaS) providers), and managed services housed in third-party commercial data centers, including primary and secondary locations, which are regionally dispersed to mitigate the impact of a localized event. This infrastructure relies on multiple internet service providers (ISPs), content delivery networks (CDNs), domain name systems (DNS providers), and mobile networks for operations. In addition, our systems interact with the systems of buyers and sellers and their contractors.

Any damage to, or failure of, these systems could result in interruptions to the availability or functionality of our service. Moreover, the failure of our data center hosting facilities or any other third-party providers to meet our capacity requirements or dramatically increased costs of such resources, could result in interruptions in the availability or functionality of our solutions or impede our ability to scale our operations. All of these providers and systems are vulnerable to disruption and/or damage from several sources, many of which are beyond our control, including without limitation: (i) loss of adequate power or cooling and telecommunications failures, (ii) fire, flood, earthquake, hurricane, and other natural disasters, (iii) software and hardware errors, failures, or crashes, (iv) financial insolvency, and (v) computer viruses, malware, hacking, terrorism, and similar disruptive problems.

Cyberattacks present a severe threat because they are difficult to prevent and remediate, are constantly evolving and improving, and can be used to defraud our buyers and sellers and their clients to steal confidential or proprietary data from us, our clients, or their users. Artificial intelligence has the potential to exacerbate cybersecurity threats, increasing their frequency and sophistication. Malfunctions or failure of our systems or systems that interact with our systems, or inaccessibility or corruption of data, could disrupt our operations and negatively impact our business. This could impact our business operations to a level in excess of any applicable business interruption insurance, result in potential liability to buyers and sellers, and negatively affect our reputation and ability to sell our solution.

Our systems may fail due to natural disasters, telecommunications failures and other events, any of which would limit user traffic.

Our websites are hosted by third-party providers. Any disruption of the computing platform at these third-party providers could result in a service outage. Fire, floods, earthquakes, power loss, telecommunications failures, break-ins, supplier failures to meet commitments and similar events could damage these systems and cause interruptions in the hosting of our websites or services. Computer viruses, electronic break-ins or other similar disruptive problems could cause users to stop visiting our website and could cause advertisers to terminate their agreements with us. In addition, we could lose advertising revenues during these interruptions and user satisfaction could be negatively impacted if the service is slow or unavailable. If any of these circumstances occurred, our business could be harmed. Our insurance policies may not adequately compensate us for losses that may occur due to any failures of or interruptions in our systems.

Our websites and other services must accommodate high volumes of traffic and deliver frequently updated information. While we have not experienced any systems failures to date, it is possible that we may experience systems failures in the future and that such failures could have a material adverse effect on our business. In addition, our users and clients depend on internet service providers, online service providers and other website operators for access to our websites and services. Many of these providers and operators have experienced significant outages in the past, and could experience outages, delays and other difficulties due to system failures unrelated to our systems and outside of our control. Any of these system failures could harm our business, financial condition and results of operations. We are unable to predict the impacts of COVID-19 and any other future pandemic or outbreak of disease on our business.

We are unable to predict the impacts of COVID-19 and any other future pandemic or outbreak of disease on our business.

19

Our business and operations could be adversely affected by future health pandemics or outbreak of disease, including the COVID-19 pandemic, impacting the markets and communities in which we, our third-party vendors and customers operate. Because our Company operates in the digital advertising industry, unlike a brick and mortar-based company, predicting the impact of the COVID-19 pandemic or other future health pandemics on our Company is difficult.

The COVID-19 pandemic has affected our operations in the past and may continue to do so in the future. For example, with the COVID-19 pandemic, we experienced a pause in marketing campaigns by a limited number of clients and an adverse impact from several suppliers. We also experienced interruptions in our daily operations, including financial reporting process, as a result of certain policies and actions put into place to mitigate the effects of the COVID-19 pandemic. We expect the revenue impact on our industry could vary dramatically by vertical. For example, we would expect to see less advertising demand from the travel, leisure and hospitality verticals and more advertising demand in the health, technology, insurance, and pharmaceutical verticals. We will continue to assess the impact of the COVID-19 pandemic on our Company, however, at this time we are unable to predict all possible impacts on our Company, our operations, and our revenues.

In addition, we cannot predict the impact any future pandemic or outbreak of a disease, or a catastrophic event will have on our business partners and third-party vendors, and we may be adversely impacted as a result of the adverse impact our third-party vendors suffer. We maintain long-standing relationships with Google and others that provide access to hundreds of thousands of advertisers from which most of our Real Time Bidding and digital publishing revenue originates. Any adverse impact on the operations of those companies would have a correspondingly adverse impact on our revenues in future periods. To the extent a pandemic or other catastrophic event adversely affects our business and financial results, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section. Any of the foregoing factors, or other cascading effects of the pandemic that are not currently foreseeable, could adversely impact our business, financial performance and condition, and results of operations.

Privacy violations could impair our business.