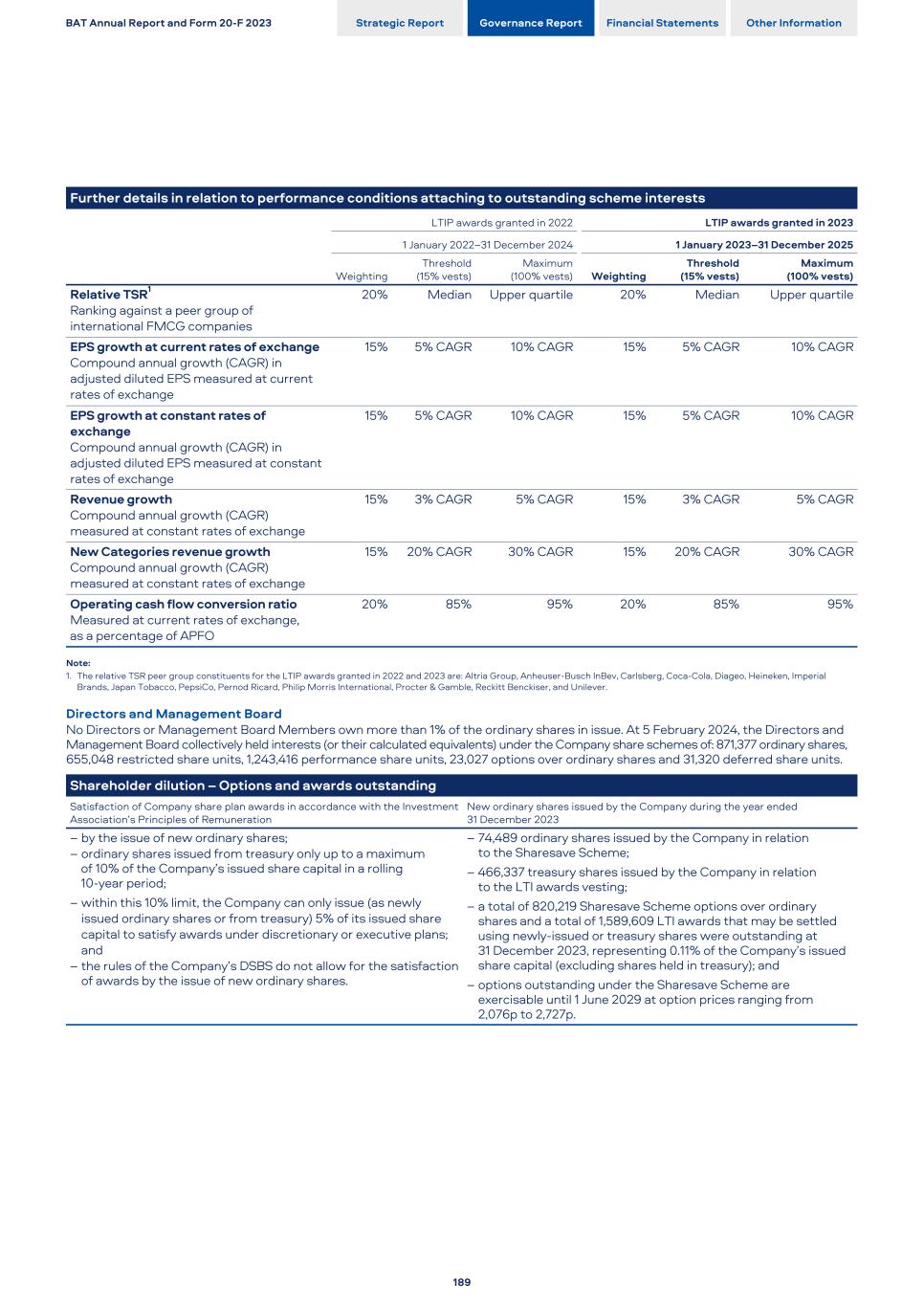

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

OR

For the fiscal year ended December 31 , 2023

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number 001-38159

(Exact name of Registrant as specified in its charter)

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Fax: +44 (0)20 7240 0555

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

| each representing one ordinary share | ||||||||

* Listed, not for trading, but only in connection with the listing of the applicable Registrant’s American Depositary Shares issued in respect thereof.

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Emerging growth company | |||||||||

If an emerging growth company that prepares its financial statements in accordance with US GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| US GAAP | Other ☐ | |||||||||||||

| ☐ | International Accounting Standards Board ☒ | |||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

| Name of the auditor’s firm | |||||

| Auditors’ firm ID/ PCAOB issued Audit Firm Identifier | |||||

| Auditors’ Location – City, State/Province, Country | |||||

This Annual Report and Accounts on Form 20-F contains forward-looking non-GAAP measures used by management to monitor the Group’s performance. For the non-GAAP information contained in this Annual Report and Accounts on Form 20-F, no comparable GAAP or IFRS information is available on a forward-looking basis and our forward-looking revenue and other components of the Group’s results, including the revenue generated from combustibles, cannot be estimated with reasonable certainty due to, among other things, the impact of foreign exchange, pricing and volume, which could be significant, are highly variable. As such, no reconciliations for this forward-looking non-GAAP information are available.

1

British American Tobacco p.l.c. (No. 3407696) Annual Report 2023 This document constitutes the Annual Report and Accounts of British American Tobacco p.l.c. (the Company) and the British American Tobacco Group prepared in accordance with UK requirements and the Annual Report on Form 20-F prepared in accordance with the U.S. Securities Exchange Act of 1934 (the Exchange Act) and the rules promulgated thereunder for the year ended 31 December 2023, except that certain phrases, paragraphs or similar sections denoted with a ‘@’ symbol do not form part of the Annual Report on Form 20-F as filed with the U.S. Securities and Exchange Commission (the SEC) and certain phrases, paragraphs or similar sections denoted with a ‘»’ symbol do not form part of the Annual Report and Accounts. In addition, the Report of Independent Registered Public Accounting Firm on pages 206 and 207 will only be included in the Annual Report on Form 20-F. Moreover, the information in this document may be updated or supplemented only for purposes of the Annual Report on Form 20-F at the time of filing with the SEC or later amended if necessary. Any such updates, supplements or amendments will also be denoted with a ‘»’ symbol. Insofar as this document constitutes the Annual Report and Accounts, it has been prepared and is presented in accordance with, and reliance upon, applicable English company law and the liabilities of the Directors in connection with this report shall be subject to the limitations and restrictions provided by such law. This document is made up of the Strategic Report, the Governance Report, the Financial Statements and Notes, and certain other information. Our Strategic Report, pages 4 to 129, includes our purpose and strategy, global market overview, business model, global performance, as well as our financial performance and principal Group risks. The Strategic Report has been approved by the Board of Directors and signed on its behalf by Caroline Ferland, Company Secretary. Our Governance Report on pages 130 to 192 contains detailed corporate governance information, our Committee reports. The Directors’ Report on pages 130 to 160 (the Governance pages) and pages 330 to 402 (the Additional Disclosure and Shareholder Information pages) has been approved by the Board of Directors and signed on its behalf by Caroline Ferland, Company Secretary. Our Financial Statements and Notes are on pages 194 to 329. The Other Information section commences on page 330. This document provides alternative performance measures (APMs) which are not defined or specified under the requirements of International Financial Reporting Standards (IFRS). We believe these APMs provide readers with important additional information on our business. We have included a Non- GAAP measures section on pages 335 to 349 which provides a comprehensive list of the APMs that we use, an explanation of how they are calculated, why we use them and a reconciliation to the most directly comparable IFRS measure where relevant. British American Tobacco p.l.c. has shares listed on the London Stock Exchange (BATS), the Johannesburg Stock Exchange (BTI), and, as American Depositary Shares, on the New York Stock Exchange (BTI). The Annual Report is published on bat.com. A printed copy is mailed to shareholders on the UK main register who have elected to receive it. Otherwise, shareholders are notified that the Annual Report is available on the website and will, at the time of that notification, receive a short Performance Summary (which sets out an overview of the Group’s performance, headline facts and figures and key dates in the Company’s financial calendar) and Proxy Form. Specific local mailing and/or notification requirements will apply to shareholders on the South Africa branch register. References in this publication to ‘British American Tobacco’, ‘BAT’, ‘Group’, ‘we’, ‘us’ and ‘our’ when denoting opinion refer to British American Tobacco p.l.c. and when denoting business activity refer to British American Tobacco p.l.c. and its subsidiaries, collectively or individually as the case may be, as well as in some circumstances those who work for them. When denoting business activity these collective expressions are used for ease of reference only and do not imply any other relationship between British American Tobacco p.l.c. and its subsidiaries. The companies in which British American Tobacco p.l.c. directly and indirectly has an interest are separate and distinct legal entities. The material in this Annual Report and Form 20-F is provided for the purpose of giving information about the Company to investors only and is not intended for general consumers. The Company, its Directors, employees, agents or advisers do not accept or assume responsibility to any other person to whom this material is shown or into whose hands it may come and any such responsibility or liability is expressly disclaimed. The material in this Annual Report is not provided for product advertising, promotional or marketing purposes. This material does not constitute and should not be construed as constituting an offer to sell, or a solicitation of an offer to buy, any of our products. Our products are sold only in compliance with the laws of the particular jurisdictions in which they are sold. References in this document to information on websites, including the web address of BAT, have been included as inactive textual references only. These websites and the information contained therein or connected thereto are not intended to be incorporated into or to form part of the Annual Report and Form 20-F. Cautionary statement This document contains forward-looking statements. For our full cautionary statement, please see page 386. Strategic Report Overview Our Global Business ........................................….. 2 Our Multi-Category Portfolio ........................… 4 Chair’s Introduction .................................…........... 6 Chief Executive’s Review ..............................…. 8 Our Year in Numbers .......................................…. 10 Our ESG Roadmap ...........................................…. 11 Interim Finance Director’s Overview .......... 12 Our Strategy Our Strategic Navigator .................................. 14 Strategy Summary .........................................…. 16 Our Business Model ........................................…. 18 Non-Financial and Sustainability Information Statement ..................................... 20 Engaging with Our Stakeholders .............…. 22 Investment Case ...............................................…. 24 Our Markets and Megatrends ..................…. 26 Quality Growth Strategic Pillar Overview ..........................…..... 28 Our Vapour Products ..................................….... 30 Our Heated Products ......................................... 32 Our Modern Oral Products .........................…. 34 Our Traditional Oral Products .................….. 36 Our Combustible Products ........................…. 37 Beyond Nicotine ..............................................…. 39 Dynamic Business Strategic Pillar Overview ................................ 40 Capital Efficiency ..............…............................... 42 U.S. ...........................................…................................ 44 AME .........................................…................................ 46 APMEA ...................................…................................ 48 Financial Performance Summary ........…... 50 Treasury and Cash Flow .............................….. 56 Other .....................................................................….. 58 Sustainable Future Strategic Pillar Overview .............................…. 60 Advancing Sustainability for A Better Tomorrow™ .............................….. 64 Leading in Sustainability and Integrity ........................................................…. 66 Sustainability Highlights ................................... 68 Sustainability Policies, Procedures and Standards .........................…. 72 Double Materiality Assessment ..............….. 74 Our Material Sustainability Topics: Harm Reduction ................…................................. 78 Climate Change .................…................................ 80 Circular Economy .............…................................. 82 Biodiversity and Ecosystems ........................ 84 Water ......................................…................................. 86 Employees, Diversity and Culture............…. 88 Human Rights ......................…............................... 92 Farmer Livelihoods

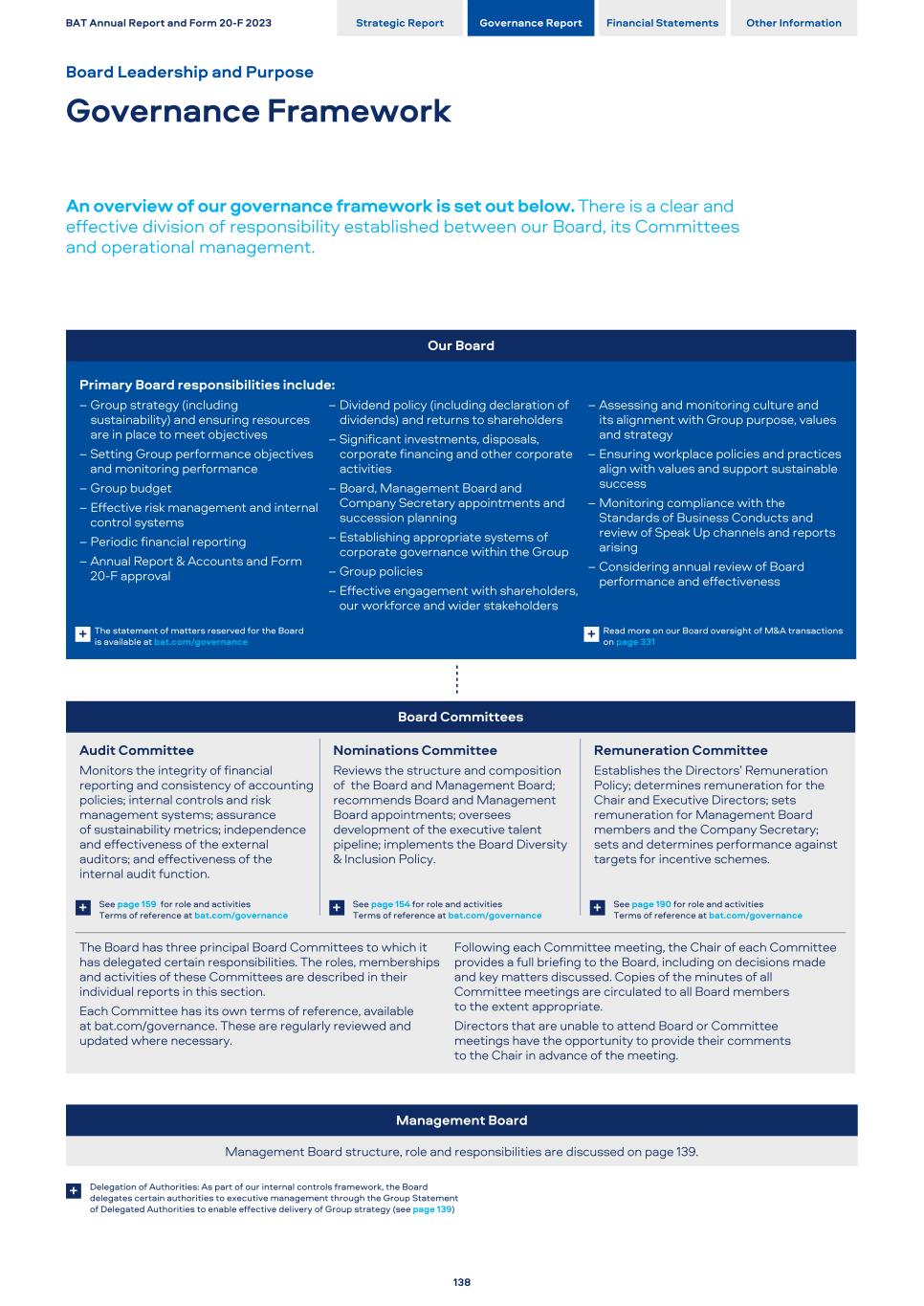

and Communities ..... 94 Marketing and Communications ................ 96 Ethics and Integrity ............................................. 98 Supplier Engagement ....…............................... 100 TCFD Reporting ..............................................….. 102 Our approach to TNFD disclosures ........... 117 Group Principal Risks ......................................... 121 Governance Directors’ Report Chair’s Introduction on Governance .................................................... 130 Board of Directors ............................................. 132 Management Board ......................................… 136 Governance Framework .............................… 138 Board Leadership.............................................… 139 Values and Culture .........................................… 140 Board Activities in 2023 .................................. 142 Board Engagement with Stakeholders .............................................. 144 Principal Decisions Made by the Board .......................................................... 149 Division of Responsibilities ........................… 150 Board Effectiveness ......................................... 152 Nominations Committee .............................. 154 Audit Committee ............................................… 159 Remuneration Report Annual Statement on Remuneration ...... 170 Financial Statements Group Financial Statements Report of Independent Registered Public Accounting Firm>> ............................. 206 Group Companies and Undertakings ..... 312 Other Information Additional Disclosures .................................... 330 Shareholder Information ........................….... 387 BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Inside This Report 1

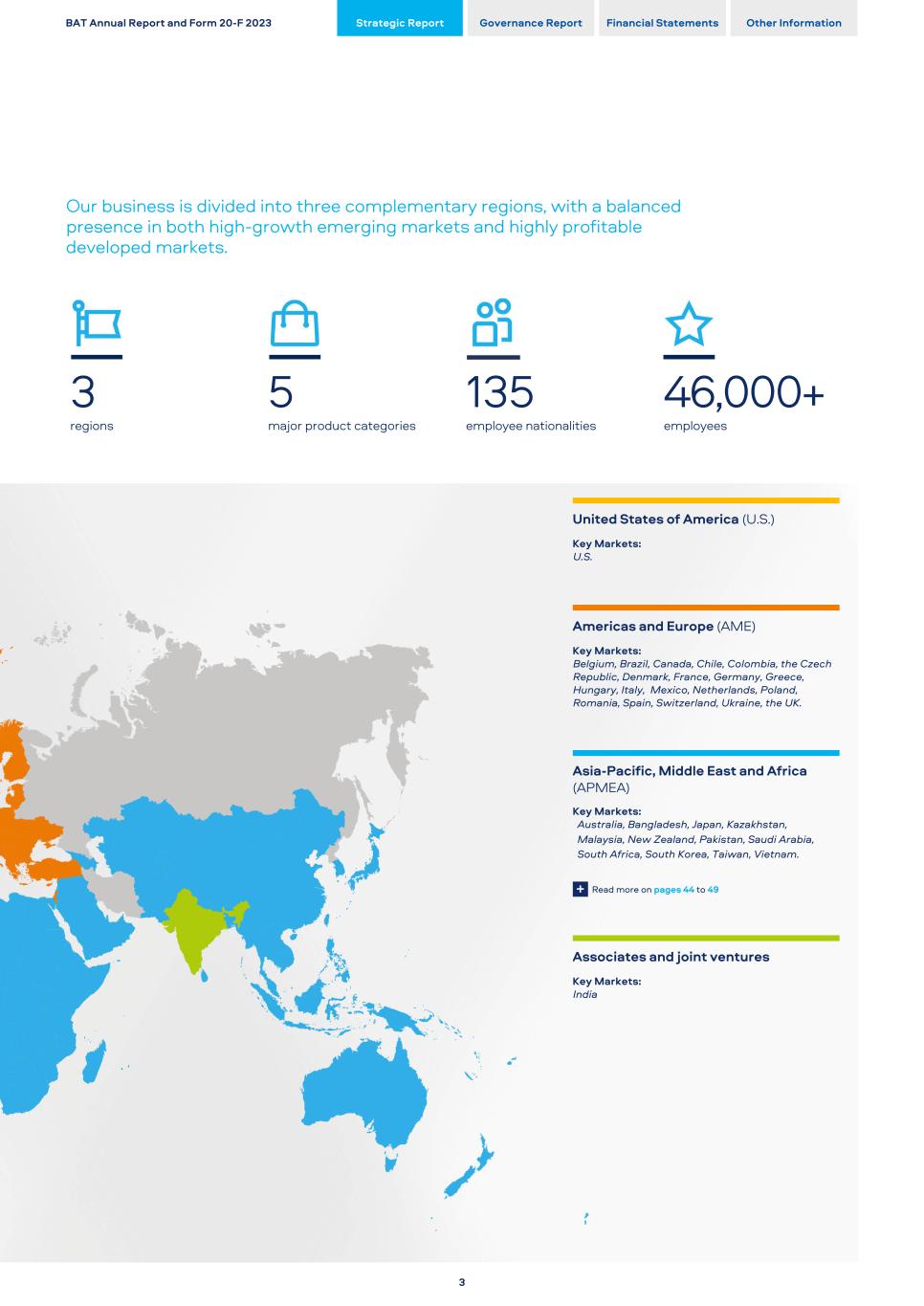

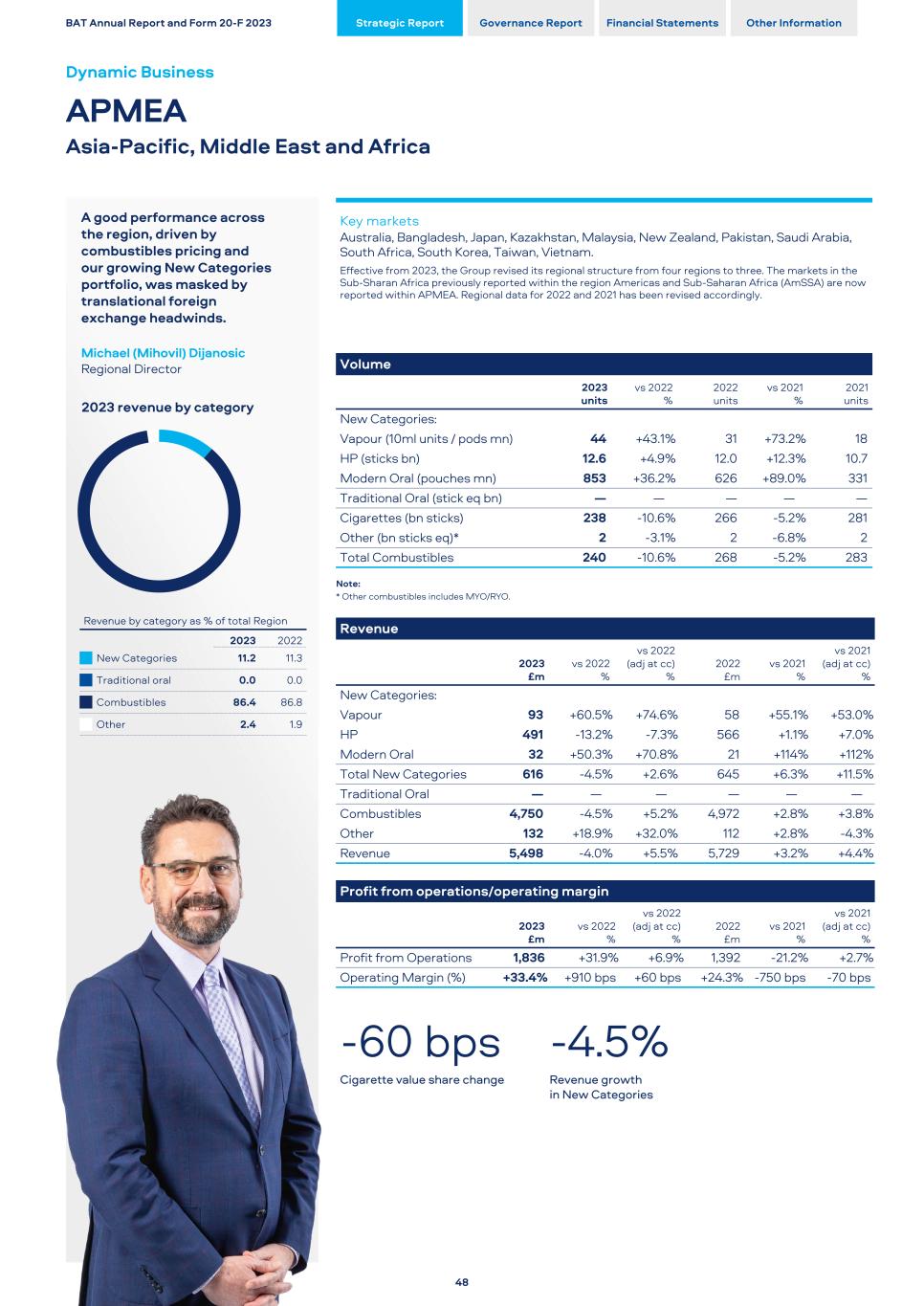

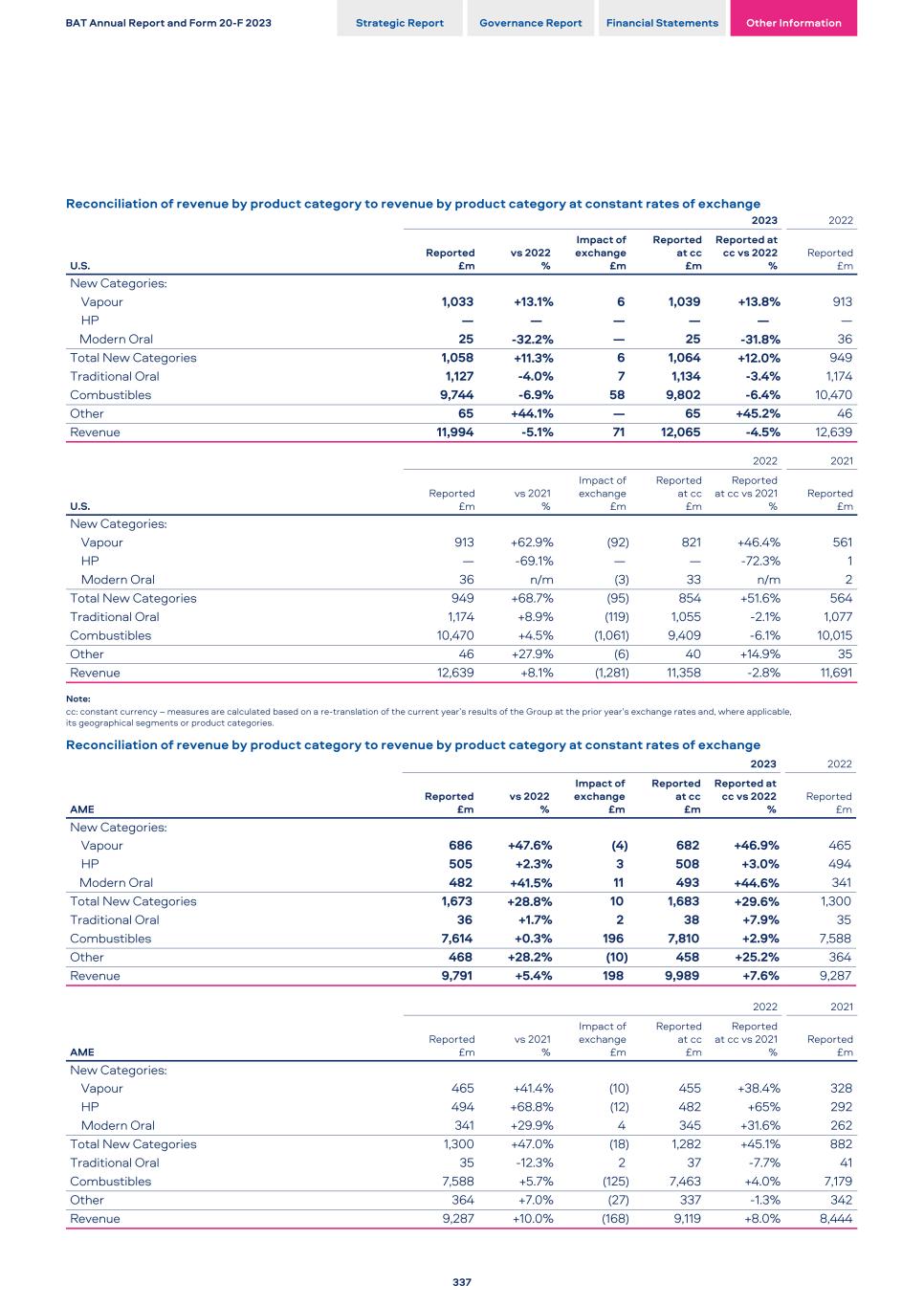

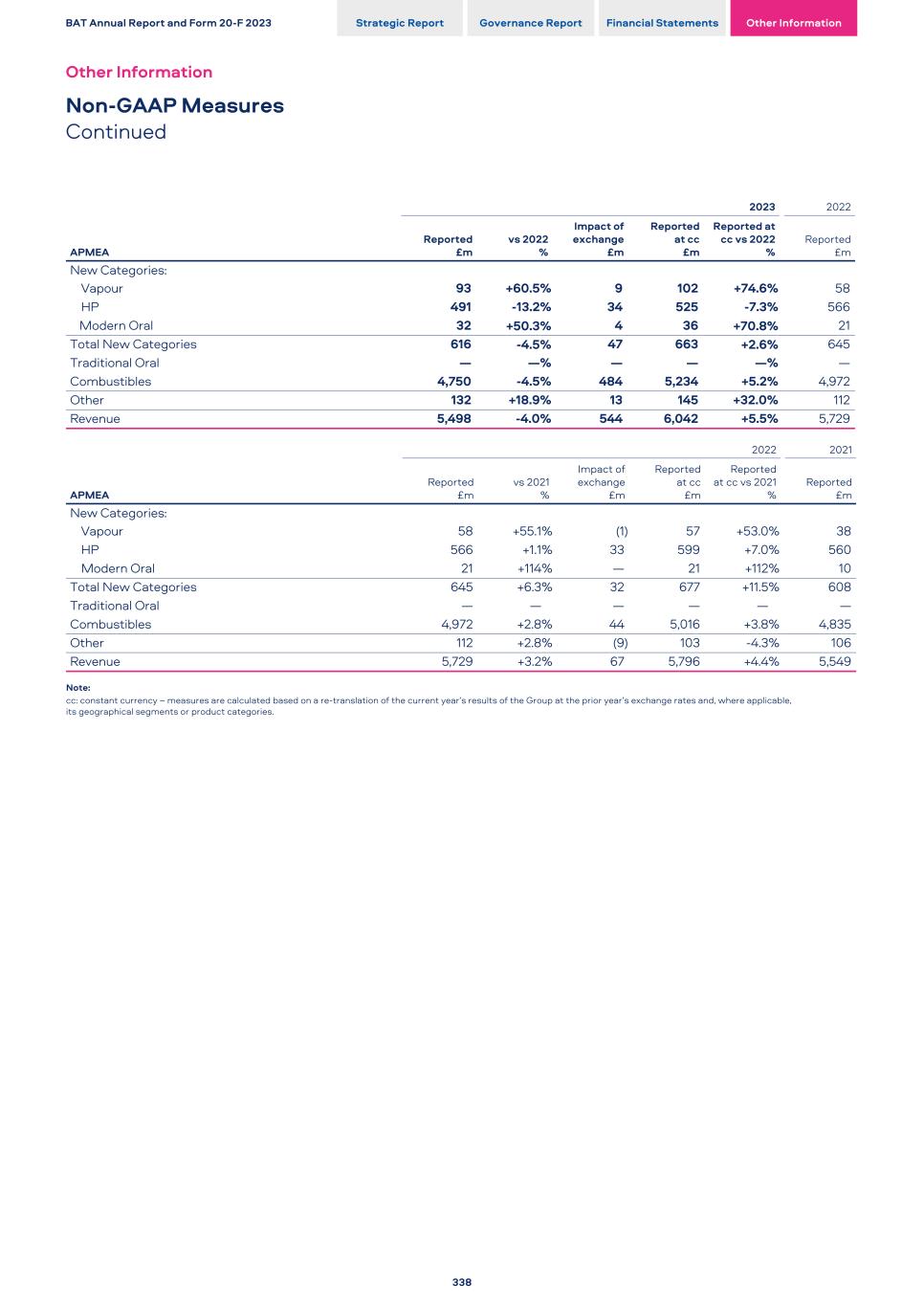

Our regional profile maximises opportunities for quality growth in our sector. Each of our markets is accountable for its own performance and driving growth. Our in-depth marketplace analysis delivers insights on consumer trends and segmentation, which facilitates our geographic brand prioritisation across our regions and markets. Consumer preferences and technology are evolving rapidly, and we are staying ahead of the curve with our digital hubs and innovation centres. We are also leveraging the expertise of our external partners and are looking forward to exciting results from our venturing initiative, Btomorrow Ventures. Read more about our Markets and Megatrends on page 26+ Revenue by Region £27,283m Total revenue U.S. £11,994m AME £9,791m APMEA £5,498m For more key detail on our Regional Performance, see pages 44 to 49+ Our Three Complementary Regions Map is accurate as at 31 December 2023 and is representative of general geographic regions and does not suggest that the Group operates in each country of every region. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Overview Our Global Business 2

Our business is divided into three complementary regions, with a balanced presence in both high-growth emerging markets and highly profitable developed markets. 3 5 135 46,000+ regions major product categories employee nationalities employees United States of America (U.S.) Key Markets: U.S. Americas and Europe (AME) Key Markets: Belgium, Brazil, Canada, Chile, Colombia, the Czech Republic, Denmark, France, Germany, Greece, Hungary, Italy, Mexico, Netherlands, Poland, Romania, Spain, Switzerland, Ukraine, the UK. Asia-Pacific, Middle East and Africa (APMEA) Key Markets: Australia, Bangladesh, Japan, Kazakhstan, Malaysia, New Zealand, Pakistan, Saudi Arabia, South Africa, South Korea, Taiwan, Vietnam. + Read more on pages 44 to 49 Associates and joint ventures Key Markets: India BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 3

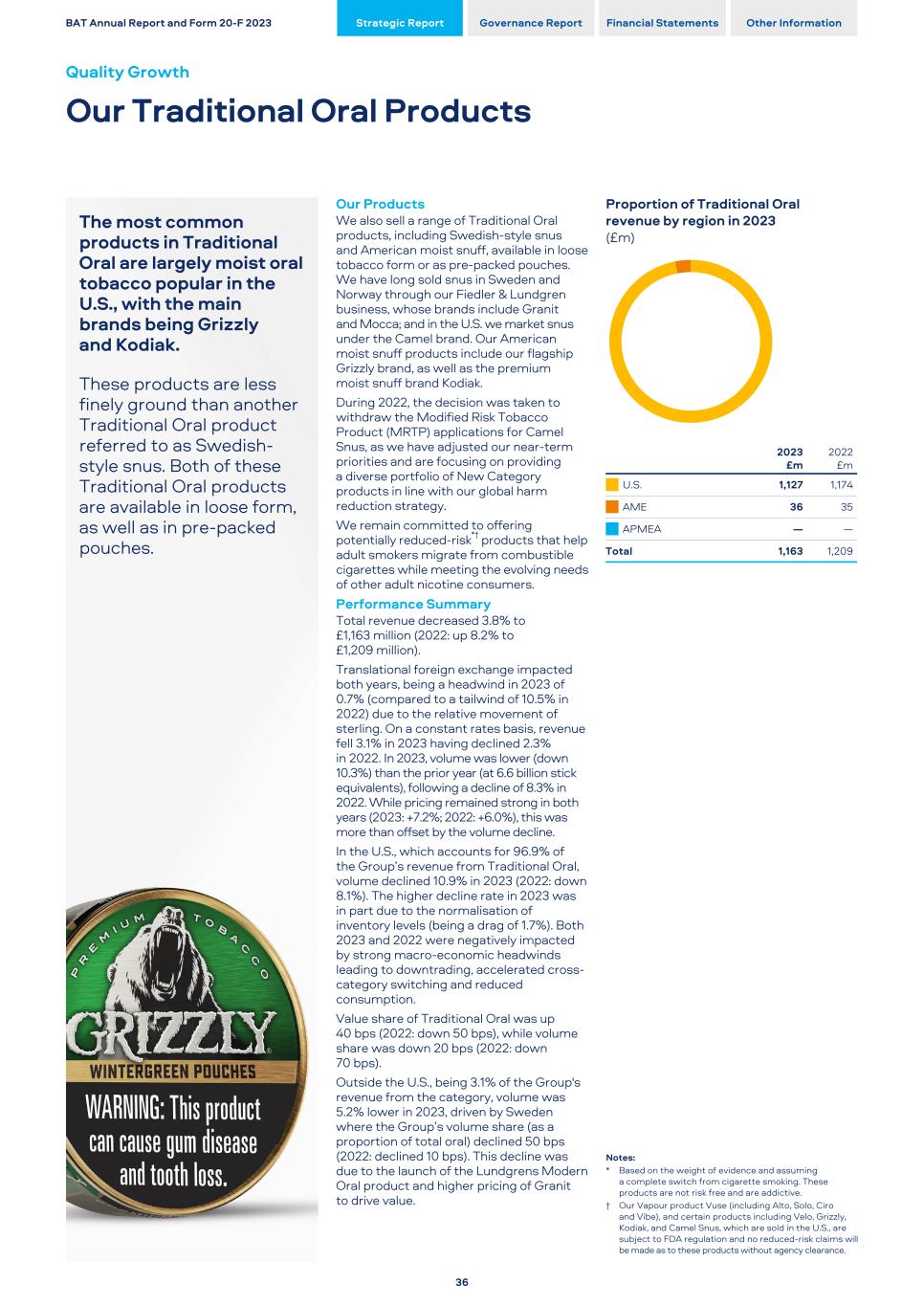

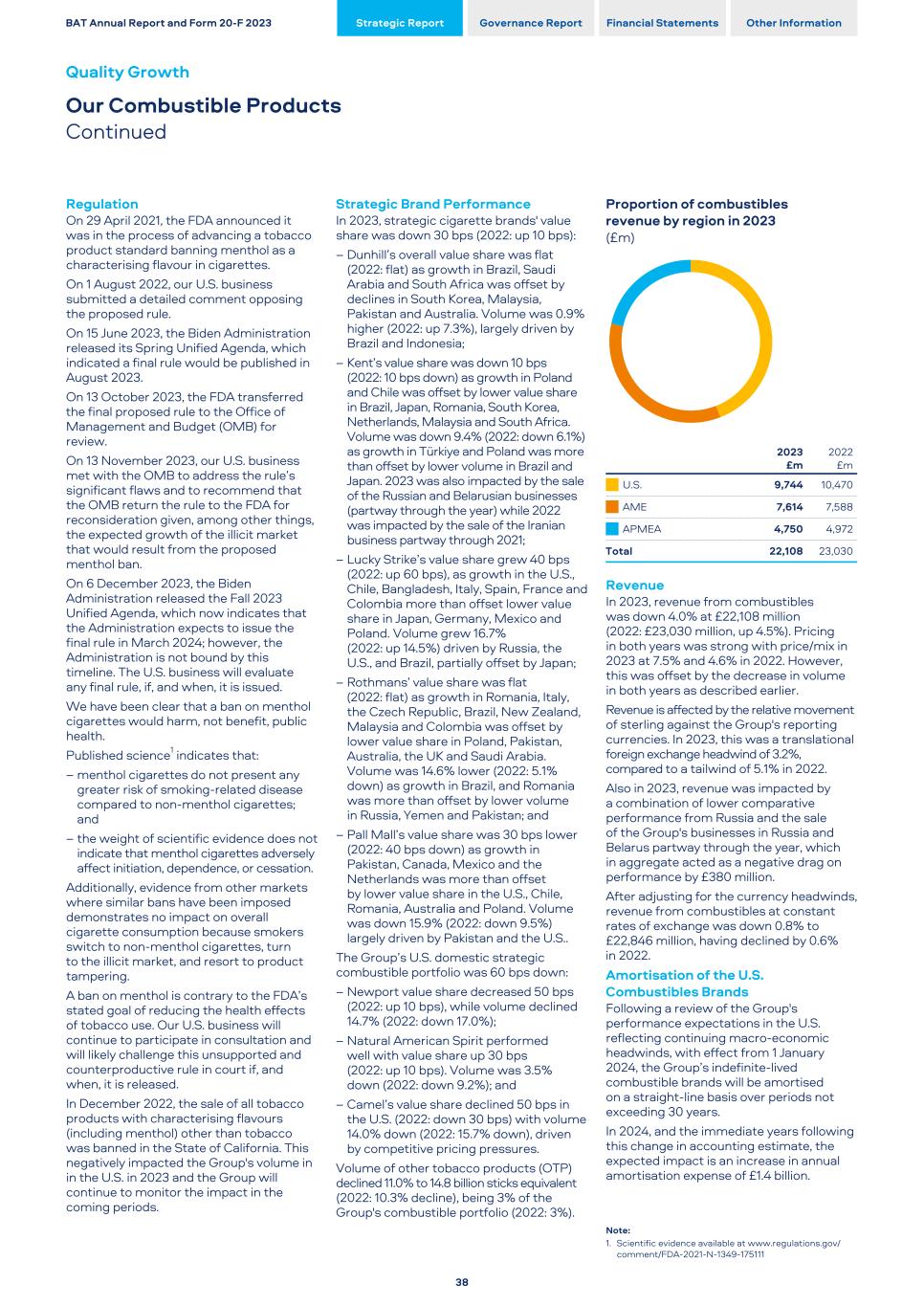

Revenue by Product Category New Categories £3,347m 12.3% Traditional Oral £1,163m 4.2% Combustibles £22,108m 81.0% Other £665m 2.5% £27,283m Total revenue Strategic Portfolio These are our key brands in both the combustible and Non-Combustible categories. This ensures focus and investment on the brands and categories that will underpin the Group’s future performance. The strategic portfolio is: Non-Combustibles All brands within New Categories and the strategic Traditional Oral brands in moist and snus. Combustibles Dunhill, Kent, Lucky Strike, Pall Mall, Rothmans, Newport (U.S.), Natural American Spirit (U.S.), Camel (U.S.). Notes: BAT’s New Category products are not smoking cessation devices and are not marketed for that purpose. * Based on the weight of evidence and assuming a complete switch from cigarette smoking. These products are not risk free and are addictive. † Our Vapour product Vuse (including Alto, Solo, Ciro and Vibe), and certain products, including Velo, Grizzly, Kodiak, and Camel Snus, which are sold in the U.S., are subject to FDA regulation and no reduced-risk claims will be made as to these products without agency clearance. Category O ur s m ok el es s po rt fo lio Vapour Vapour products are battery-powered devices that heat e-liquids to produce an inhalable aerosol, commonly known as vapour. Although e-liquids usually contain nicotine, there is no tobacco in Vapour products. Heated Products Heated Products (HPs) comprise two main functional parts; an electronic handheld device that contains a lithium-ion battery that powers a heating chamber: and a specially designed consumable that is inserted into the device. Everything has been designed so that nicotine and flavour are released through precision heating. Modern Oral Modern Oral products are pouches which contain high purity nicotine, water, and other high-quality ingredients. Consumers place the disposable pouch between their gum and upper lip, typically for around 30 minutes, during which time nicotine and flavours are released and the nicotine is absorbed through the tissues lining the mouth. Traditional Oral Traditional Oral products include snus and snuff. Snus is a moist form of oral tobacco originating from Sweden. It is available in loose form or as pouches. The tobacco is typically mixed with water, salt and aromas. Combustibles The Group sold 555 billion cigarette sticks and 15 billion OTP (stick equivalents) in 2023. The Group operates internationally, with 38 fully integrated cigarette manufacturing facilities in 36 markets. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Strategic Management Our Multi-Category Portfolio BAT is a consumer-focused business operating internationally. Our multi-category approach means we are well placed to provide adult consumers with products designed for every mood and moment. Our portfolio reflects our commitment to meeting the evolving and varied needs of today’s adult consumers. 4 Read more on page 30+ Read more on page 32+ Read more on page 34+ Read more on page 36+ Read more on page 37+

Global Drive Brands Market Footprint 63 markets where our Vapour products are currently available 31 markets where our HPs are currently available 34 markets where our Modern Oral products are currently available 3 markets where our Traditional Oral products are currently available U.S. Specific BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 5

Our strategy and purpose were discussed extensively during 2023. The result of these discussions was the decision to provide greater clarity on what we mean by A Better Tomorrow™. It means we are committed to Building a Smokeless World. Luc Jobin Chair Dear Fellow Shareholders, During 2023, the world continued to experience a period of extensive and prolonged uncertainty. The global economy has entered an era of upheaval, as geopolitical tensions continue to destabilise economies and societies. Cost-of-living pressures are being compounded by inflation, and this represents a significant challenge for major economies. This has resulted in re-adjustments in work habits and in consumer behaviour. Ambiguity and uncertainty have long occupied discussions in boardrooms, but I cannot recall a time when this was so pronounced. As always, my colleagues around the world have responded to the operating environment with resilience and resourcefulness. I would like to thank them, on behalf of the Board, for their ongoing dedication and diligence. Leadership for the Future In May 2023, the Board announced a change in the leadership of BAT, with Tadeu Marroco appointed as Chief Executive. With 30 years of experience across the entire business, Tadeu was the outstanding choice to lead BAT into the next chapter of its history. With his track record of delivering transformation, building strong teams and ensuring financial discipline, Tadeu is well placed to build on our A Better Tomorrow™ strategy that was first articulated in 2020. Following his appointment, in June 2023 Tadeu reshaped his Management Board to support a greater focus on improved execution and operational excellence. Having also appointed a new Chief People Officer and with a new Chief Financial Officer due to join us from 1 May 2024, the Board believes the management team at BAT is well placed to execute on the strategy of the business to deliver long-term value for stakeholders. Refining our Strategy and Purpose In the context of a rapidly changing world, it is important that shareholders have a holistic view of BAT and our place in it. This is the second year that we have embedded our sustainability data into our Annual Report. Our Combined Annual and Sustainability Report again represents the fullest depiction of BAT’s business strategy and performance. Our strategy and purpose were discussed extensively during 2023. The result of these discussions was the decision to provide greater clarity on what we mean by A Better Tomorrow™. It means we are committed to Building a Smokeless World. This is a commitment to migrate our cigarette consumers actively, sustainably and responsibly to reduced risk*†, smokeless alternatives. In so doing, BAT will deliver for consumers, investors and society, while employees will benefit from a purpose-driven business that they can feel excited about. Built around the three pillars of Quality Growth, Sustainable Future and Dynamic Business the Board believes this refined strategy is right for the long-term success of BAT. Tadeu discusses this in more detail on page 8 and further information on the refined strategy can be found on page 14. The refined strategy is a natural extension of the foundations that were laid in 2020 and provides clarity on what BAT intends to focus on in the years to come. The Board has been engaged in much discussion during the year about 'what' the business should deliver in the future. It is, of course, important for shareholders to understand 'how' we have delivered this year and how we think success should be measured against the refined strategy going forward. Our Combined Annual and Sustainability Report seeks to do that, while honing our non-financial disclosures towards the reporting requirements of the EU Corporate Sustainability Reporting Directive (CSRD). Our Values and Culture A strategy is little without the right culture instilled across the organisation to deliver it. A truly dynamic business is one where the people within it understand the strategic aims and the expected behaviours to achieve them. Values are an important facet of continuing to be an exciting and winning company. It is why the Board was pleased to see a set of rearticulated values being developed in parallel with the refined strategy. Long-Term View of the Business Despite an increasingly turbulent external environment, the fundamentals of the tobacco and nicotine sector remain attractive, and the Board believes BAT is in a strong position to realise its potential. The growth of adult smokers seeking smokeless alternatives is a long-term, sectoral trend. There remain more than one billion adult smokers in the world and there are many jurisdictions which, with the right regulatory approach, could see smoking rates decline faster through greater acceptance of smokeless products. With our multi-category portfolio, BAT is well placed to capitalise on this consumer shift to smokeless products while continuing to manage the combustible cigarette business in a responsible manner. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Overview Chair’s Introduction Transformation in Action 6

Ambiguity and uncertainty have long occupied discussions in boardrooms, but I cannot recall a time when this was so pronounced. As always, my colleagues around the world have responded to the operating environment with resilience and resourcefulness. A truly dynamic business is one where the people within it understand the strategic aims and the expected behaviours to achieve them. Despite an increasingly turbulent external environment, the fundamentals of the tobacco and nicotine sector remain attractive, and BAT is well placed to realise its potential. The growth of adult smokers seeking smokeless alternatives is a long-term, sectoral trend. With our geographic footprint and multi-category portfolio, BAT is well placed to capitalise on this consumer shift to smokeless products, while managing the combustible cigarette business in a responsible manner. BAT’s Board and leadership team remain focused on securing long-term, sustainable value creation, by nurturing BAT’s culture, building our brands, and delivering A Better Tomorrow™. We believe that growth within the smokeless category will be driven by sustained investment in our brands and targeted innovation to respond to evolving consumer preferences and tastes. Combined with active portfolio management, we believe that continuing to invest in our brands is fundamental to sustaining BAT's performance for the future. Dividends Reflecting the confidence in our business and its future prospects, the Board has declared a dividend of 235.52p per ordinary share, payable in four equal instalments of 58.88p per ordinary share, to shareholders registered on the UK main register or the South Africa branch register and to American Depository Shares (ADS) holders, each on the applicable record dates. The dividends receivable by ADS holders in US dollars will be calculated based on the exchange rate on the applicable payment dates. Further information on dividends can be found on page 55 of the Financial Performance Summary and page 388 in the Shareholder Information section. Board Changes I was very pleased to welcome Murray Kessler and Serpil Timuray to our Board this year. Both Murray and Serpil join the Board as independent Non-Executive Directors and members of the Nominations and Remuneration Committees. Murray possesses extensive leadership experience in growing consumer product companies and managing regulated businesses. From left to right, Group Chair, Luc Jobin, Non-Executive Director Kandy Anand and Chief Executive, Tadeu Marroco Serpil also brings experience in growing consumer and enterprise product companies, as well as managing global strategy, marketing, innovation and digital transformation. I am looking forward to their respective contributions as we accelerate our strategy to build A Better Tomorrow™. Summary and Outlook While sustained volatility and uncertainty will continue to present challenges, we believe BAT remains well-positioned and resilient. We are diversified by category, price point and geography. Our smokeless portfolio has been designed to take advantage of sectoral shifts. Our people are highly engaged and have a track record of delivery during uncertain times. Additionally, our continued investment in our brands and deep understanding of our consumers position us well to capture opportunities in tobacco, nicotine and beyond, markets we believe have very attractive fundamentals. BAT’s Board and leadership team remain focused on securing long-term, sustainable value creation, by nurturing BAT’s culture, building our brands, and delivering A Better Tomorrow™. Notes: * Based on the weight of evidence and assuming a complete switch from cigarette smoking. These products are not risk free and are addictive. † Our Vapour product Vuse (including Alto, Solo, Ciro and Vibe), and certain products, including Velo, Grizzly, Kodiak, and Camel Snus, which are sold in the U.S., are subject to FDA regulation and no reduced-risk claims will be made as to these products without agency clearance. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 7

For BAT, A Better Tomorrow™ is very clear. We will work to Build a Smokeless World. The way we will do this is by switching as many smokers as we can to our smokeless products. Tadeu Marroco Chief Executive Dear Stakeholders, I was very proud to be appointed Chief Executive in May 2023. Having worked at BAT for over three decades, it was an honour to be given the opportunity to lead the business. Despite an increasingly difficult external environment, I believe we are at a moment of enormous potential for BAT and the tobacco and nicotine sector as a whole. In order to realise that potential, we must address a number of strategic choices. Fundamentally, BAT today is a business built to deliver resilient performance, even during uncertain times. Our geographical diversity and multi- category product portfolio are underpinned by long-term investments in our brands. Combined with a culture that values delivery today while pursuing future opportunities, we are well positioned to continue delivering stakeholder value over the years to come. Full-Year 2023 Performance During 2023, the underlying strengths of BAT were reflected in our performance, despite a challenging environment. While total Group revenue declined 1.3%, revenue at constant currency was up 1.6%, despite the negative impact due to the sale of Russia and Belarus partway through the year. I was pleased with the performances of AME (with revenue up 5.4%) and APMEA, although APMEA was impacted by a translational foreign exchange headwind which masked a good operating performance as revenue declined 4.0% (up 5.5% at constant rates1). As a result of a particularly difficult macro-economic environment, the U.S. was down 5.1%. There was another strong performance from our New Categories which are now profitable at the category contribution level (two years ahead of our original plan), driven by higher revenue (up 15.6%, or 17.8% on a constant currency basis). We currently have 24 million consumers of Non-Combustible products and revenue from these products now accounts for 16.5% of Group revenue. 2023 has brought some unique challenges to the Group, including: – Having concluded it was no longer sustainable in the current environment, I was pleased that we completed the sale of our Russian and Belarusian businesses in September 2023. As a result, we no longer have a presence in Russia or Belarus and will receive no financial gain from ongoing sales in these markets; and – Reflecting the difficult trading environment in the U.S., uncertainty regarding the impact of the potential menthol ban and continued drag on our legal Vapour business by illicit single-use products, we have impaired certain U.S. assets (including goodwill and our combustible trademarks), recognising a non-cash charge of £27.3 billion. In the face of significant turbulence in our operating environment, I am assured by the resilience demonstrated by the business. However, the prospect of ongoing volatility means that there is no room for complacency and this necessitates greater strategic clarity. A Refined Strategy As I have said before, the direction of our strategy that was laid out in 2020 remains the right one. What is required now is a clearer articulation of our vision and an improved focus on sharper execution. The ongoing success of our New Categories business, combined with the underlying strengths of BAT, mean that we are well placed to realise our potential. Delivering long-term, multi-stakeholder value has long been our aim. What is now required is a clearer picture of how that can create A Better Tomorrow™. As such, we have refined our strategy to map out how we plan to deliver for stakeholders going forward. Underpinning this is a revised set of values for our employees. Further details on our strategy and values can be found on pages 14-17. For BAT, A Better Tomorrow™ is very clear. We will work toward Building a Smokeless World. The way we will do this is by switching as many smokers as we can to our smokeless products. As a business, we are committed to becoming a predominantly smokeless business, targeting 50% of our revenue from Non-Combustibles by 2035. With a refined strategy, having refreshed my Management Board and having a new set of Group-wide values, I believe the business now clearly understands the areas we need to focus on. These areas fall under three pillars: Quality Growth, Sustainable Future and Dynamic Business. Quality Growth Quality Growth marks our transition from the first stage of our transformation journey. Where our New Categories focus was weighted toward revenue growth, it will now pivot to a more balanced focus on top-line and bottom-line delivery. Key to delivering this is a focus on brands and innovation, efficiency and margin delivery across our business. We will do this while maintaining our competitive position, and progressing our pilot launches for the long-term into categories Beyond Nicotine. A core part of this pillar will be stabilising the performance of our U.S. business. Despite recent challenges, the U.S. remains the most profitable tobacco and nicotine market in the world and a core part of our future plans to Build a Smokeless World. While the FDA and state level regulatory proposals have driven some uncertainty in the U.S. operating environment, our long track record of managing regulatory change gives us confidence that we will be able to navigate these issues. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Overview Chief Executive’s Review Building a Smokeless World 8

Despite an increasingly difficult external environment, I believe we are at a moment of enormous potential for BAT and the tobacco and nicotine sector as a whole. We have rearticulated our purpose to clarify our intention to move our business beyond cigarettes. As part of our refined strategy, the areas we will focus on fall under three pillars: Quality Growth, Sustainable Future and Dynamic Business. Key to delivering on our refined strategy are the people who underpin this business, our employees, and the culture that they operate in. Science will continue to be a primary driver of our efforts. We will work to enable more consumers around the world to have access to smokeless products. Further embedding sustainability and integrity into all of our activities will continue to be a priority. It is an exciting time to be part of BAT and I look forward to working with colleagues around the globe to Build a Smokeless World and drive A Better Tomorrow™. Sustainable Future The Sustainable Future pillar re- emphasises our overarching goal of creating A Better Tomorrow™. Science will continue to be a primary driver of our efforts. We will support the science behind smokeless products through more active external engagement, including with regulators. We will work to provide more consumers around the world with access to smokeless products in a responsible manner. Of course, further embedding sustainability and integrity into all of our activities will continue to be a priority and you can read more about our efforts there on page 60. Dynamic Business The Dynamic Business pillar highlights our commitment to strengthening our already winning organisation and ensuring we are efficient and effective in all of our operations. By focusing here and being data-driven, we believe we can create the financial flexibility to invest in our people, our products and provide returns to our investors. Key to delivering on our refined strategy are the thousands of people around the world who work at BAT and the culture that they operate in. Notes: 1 Please refer to the Non-GAAP section from page 335 for the Non-GAAP measures definitions. * Based on the weight of evidence and assuming a complete switch from cigarette smoking. These products are not risk free and are addictive. † Our Vapour product Vuse (including Alto, Solo, Ciro and Vibe), and certain products, including Velo, Grizzly, Kodiak, and Camel Snus, which are sold in the U.S., are subject to FDA regulation and no reduced-risk claims will be made as to these products without agency clearance. From left to right, Johan Vandermeulen, COO, Tadeu Marroco, Chief Executive, and Usman Zahur, Area Director Central Europe Our new Chief People Officer, Dr Cora Koppe-Stahrenberg, and I will be working closely together, to foster the kind of human-centric, skills-enabled and performance-driven organisation that is essential to driving forward our strategic agenda. Increasing our financial flexibility is another core part of the Dynamic Business pillar. Continuing our disciplined approach to capital allocation and debt management will be crucial. Having moved into the middle of our leverage range, we have increasing flexibility to deliver long-term value while taking into account macro- economic and regulatory developments. Facing the Future with Confidence Looking to the future, it is clear to me that the fundamentals of our strategy remain correct. We have rearticulated our purpose to clarify our intention to move our business beyond cigarettes, and we will continue to address the difficult decisions that this purpose entails. We are sharpening our executional focus to enable high quality, repeatable growth, supported by science, stakeholder engagement and with sustainability and integrity at the core. We are an organisation ready to deliver, with operational excellence and an ability to flexibly manage our capital allocation decisions for the benefit of all stakeholders. It is an exciting time to be part of BAT and I look forward to working with colleagues around the globe to Build a Smokeless World and drive A Better Tomorrow™. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 9

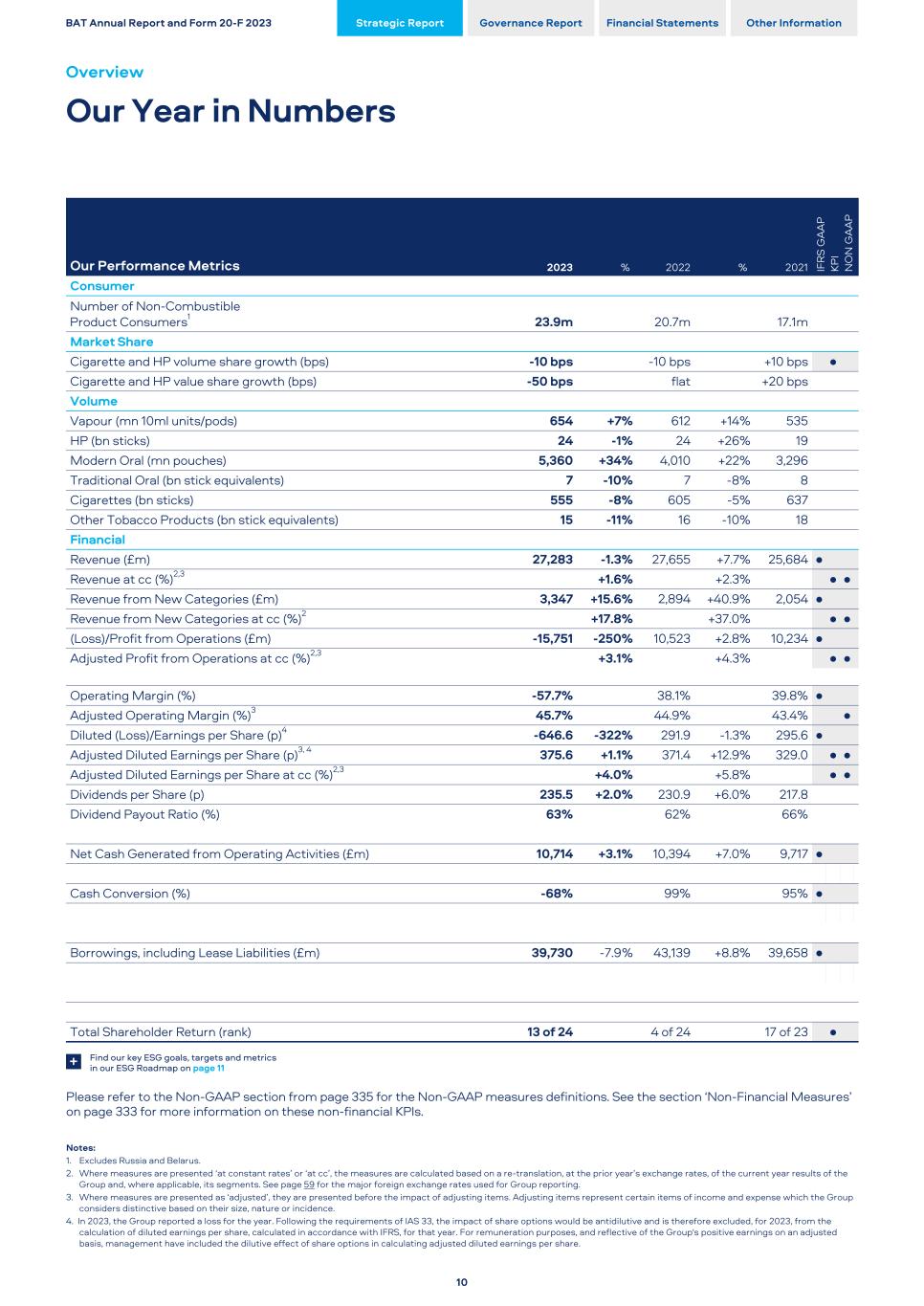

Our Performance Metrics 2023 % 2022 % 2021 IF R S G A A P KP I N O N G A A P Consumer Number of Non-Combustible Product Consumers1 23.9m 20.7m 17.1m Market Share Cigarette and HP volume share growth (bps) -10 bps -10 bps +10 bps • Cigarette and HP value share growth (bps) -50 bps flat +20 bps Volume Vapour (mn 10ml units/pods) 654 +7 % 612 +14 % 535 HP (bn sticks) 24 -1 % 24 +26 % 19 Modern Oral (mn pouches) 5,360 +34 % 4,010 +22 % 3,296 Traditional Oral (bn stick equivalents) 7 -10 % 7 -8 % 8 Cigarettes (bn sticks) 555 -8 % 605 -5 % 637 Other Tobacco Products (bn stick equivalents) 15 -11 % 16 -10 % 18 Financial Revenue (£m) 27,283 -1.3 % 27,655 +7.7 % 25,684 • Revenue at cc (%)2,3 +1.6 % +2.3 % • • Revenue from New Categories (£m) 3,347 +15.6 % 2,894 +40.9 % 2,054 • Revenue from New Categories at cc (%)2 +17.8 % +37.0 % • • (Loss)/Profit from Operations (£m) -15,751 -250 % 10,523 +2.8 % 10,234 • Adjusted Profit from Operations at cc (%)2,3 +3.1 % +4.3 % • • Operating Margin (%) -57.7% 38.1% 39.8% • Adjusted Operating Margin (%)3 45.7% 44.9% 43.4% • Diluted (Loss)/Earnings per Share (p)4 -646.6 -322 % 291.9 -1.3 % 295.6 • Adjusted Diluted Earnings per Share (p)3, 4 375.6 +1.1 % 371.4 +12.9 % 329.0 • • Adjusted Diluted Earnings per Share at cc (%)2,3 +4.0 % +5.8 % • • Dividends per Share (p) 235.5 +2.0 % 230.9 +6.0 % 217.8 Dividend Payout Ratio (%) 63% 62% 66% Net Cash Generated from Operating Activities (£m) 10,714 +3.1 % 10,394 +7.0 % 9,717 • Cash Conversion (%) -68% 99% 95% • Borrowings, including Lease Liabilities (£m) 39,730 -7.9 % 43,139 +8.8 % 39,658 • Total Shareholder Return (rank) 13 of 24 4 of 24 17 of 23 • Find our key ESG goals, targets and metrics in our ESG Roadmap on page 11+ Please refer to the Non-GAAP section from page 335 for the Non-GAAP measures definitions. See the section ‘Non-Financial Measures’ on page 333 for more information on these non-financial KPIs. Notes: 1. Excludes Russia and Belarus. 2. Where measures are presented ‘at constant rates’ or ‘at cc’, the measures are calculated based on a re-translation, at the prior year’s exchange rates, of the current year results of the Group and, where applicable, its segments. See page 59 for the major foreign exchange rates used for Group reporting. 3. Where measures are presented as ‘adjusted’, they are presented before the impact of adjusting items. Adjusting items represent certain items of income and expense which the Group considers distinctive based on their size, nature or incidence. 4. In 2023, the Group reported a loss for the year. Following the requirements of IAS 33, the impact of share options would be antidilutive and is therefore excluded, for 2023, from the calculation of diluted earnings per share, calculated in accordance with IFRS, for that year. For remuneration purposes, and reflective of the Group's positive earnings on an adjusted basis, management have included the dilutive effect of share options in calculating adjusted diluted earnings per share. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Overview Our Year in Numbers 10

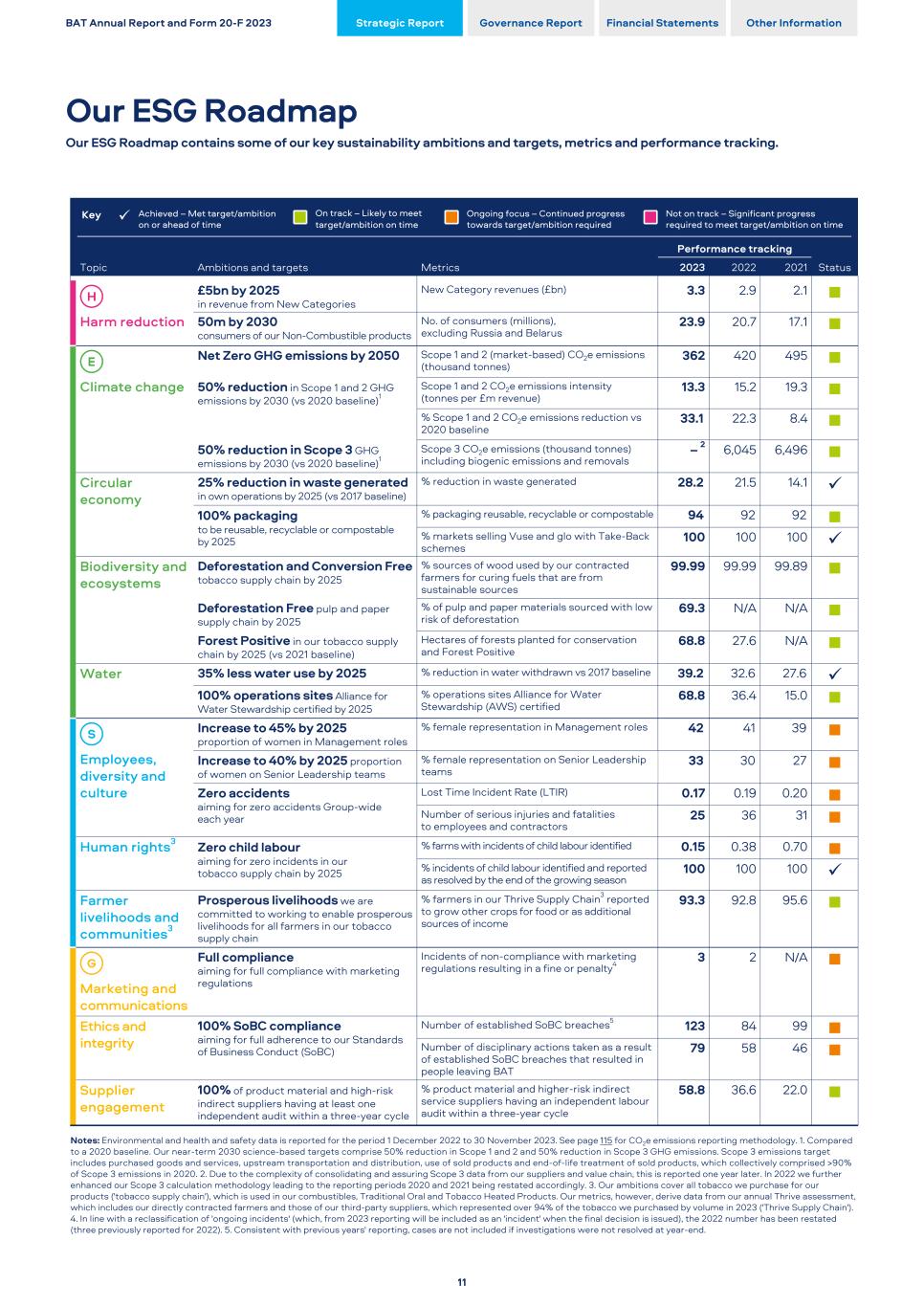

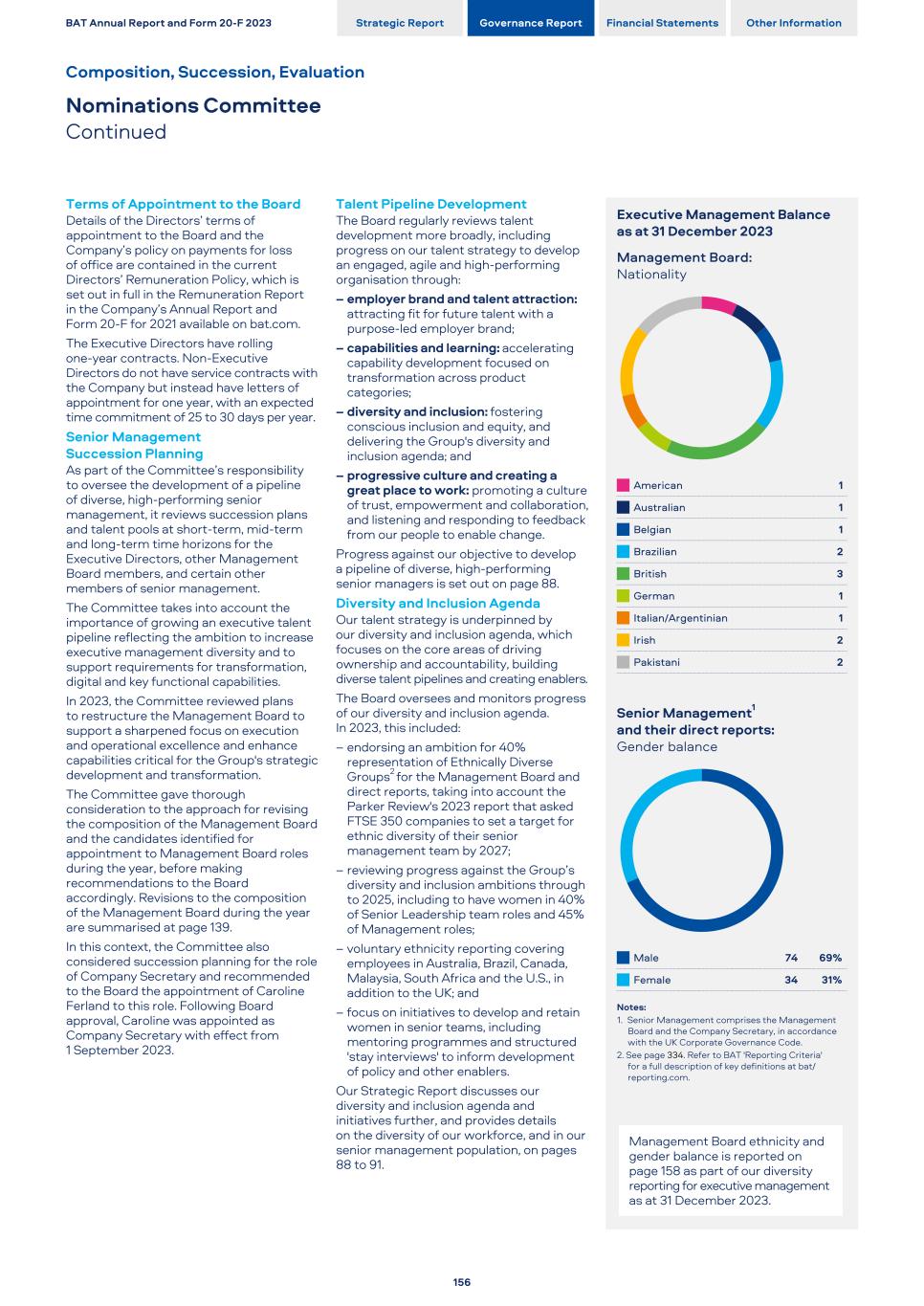

Ambitions and targets Metrics Performance tracking Topic 2023 2022 2021 Status Harm reduction £5bn by 2025 in revenue from New Categories New Category revenues (£bn) 3.3 2.9 2.1 n 50m by 2030 consumers of our Non-Combustible products No. of consumers (millions), excluding Russia and Belarus 23.9 20.7 17.1 n Climate change Net Zero GHG emissions by 2050 Scope 1 and 2 (market-based) CO2e emissions (thousand tonnes) 362 420 495 n 50% reduction in Scope 1 and 2 GHG emissions by 2030 (vs 2020 baseline)1 Scope 1 and 2 CO2e emissions intensity (tonnes per £m revenue) 13.3 15.2 19.3 n % Scope 1 and 2 CO2e emissions reduction vs 2020 baseline 33.1 22.3 8.4 n 50% reduction in Scope 3 GHG emissions by 2030 (vs 2020 baseline)1 Scope 3 CO2e emissions (thousand tonnes) including biogenic emissions and removals – 2 6,045 6,496 n Circular economy 25% reduction in waste generated in own operations by 2025 (vs 2017 baseline) % reduction in waste generated 28.2 21.5 14.1 ü 100% packaging to be reusable, recyclable or compostable by 2025 % packaging reusable, recyclable or compostable 94 92 92 n % markets selling Vuse and glo with Take-Back schemes 100 100 100 ü Biodiversity and ecosystems Deforestation and Conversion Free tobacco supply chain by 2025 % sources of wood used by our contracted farmers for curing fuels that are from sustainable sources 99.99 99.99 99.89 n Deforestation Free pulp and paper supply chain by 2025 % of pulp and paper materials sourced with low risk of deforestation 69.3 N/A N/A n Forest Positive in our tobacco supply chain by 2025 (vs 2021 baseline) Hectares of forests planted for conservation and Forest Positive 68.8 27.6 N/A n Water 35% less water use by 2025 % reduction in water withdrawn vs 2017 baseline 39.2 32.6 27.6 ü 100% operations sites Alliance for Water Stewardship certified by 2025 % operations sites Alliance for Water Stewardship (AWS) certified 68.8 36.4 15.0 n Employees, diversity and culture Increase to 45% by 2025 proportion of women in Management roles % female representation in Management roles 42 41 39 n Increase to 40% by 2025 proportion of women on Senior Leadership teams % female representation on Senior Leadership teams 33 30 27 n Zero accidents aiming for zero accidents Group-wide each year Lost Time Incident Rate (LTIR) 0.17 0.19 0.20 n Number of serious injuries and fatalities to employees and contractors 25 36 31 n Human rights3 Zero child labour aiming for zero incidents in our tobacco supply chain by 2025 % farms with incidents of child labour identified 0.15 0.38 0.70 n % incidents of child labour identified and reported as resolved by the end of the growing season 100 100 100 ü Farmer livelihoods and communities3 Prosperous livelihoods we are committed to working to enable prosperous livelihoods for all farmers in our tobacco supply chain % farmers in our Thrive Supply Chain3 reported to grow other crops for food or as additional sources of income 93.3 92.8 95.6 n Marketing and communications Full compliance aiming for full compliance with marketing regulations Incidents of non-compliance with marketing regulations resulting in a fine or penalty4 3 2 N/A n Ethics and integrity 100% SoBC compliance aiming for full adherence to our Standards of Business Conduct (SoBC) Number of established SoBC breaches5 123 84 99 n Number of disciplinary actions taken as a result of established SoBC breaches that resulted in people leaving BAT 79 58 46 n Supplier engagement 100% of product material and high-risk indirect suppliers having at least one independent audit within a three-year cycle % product material and higher-risk indirect service suppliers having an independent labour audit within a three-year cycle 58.8 36.6 22.0 n Notes: Environmental and health and safety data is reported for the period 1 December 2022 to 30 November 2023. See page 115 for CO2e emissions reporting methodology. 1. Compared to a 2020 baseline. Our near-term 2030 science-based targets comprise 50% reduction in Scope 1 and 2 and 50% reduction in Scope 3 GHG emissions. Scope 3 emissions target includes purchased goods and services, upstream transportation and distribution, use of sold products and end-of-life treatment of sold products, which collectively comprised >90% of Scope 3 emissions in 2020. 2. Due to the complexity of consolidating and assuring Scope 3 data from our suppliers and value chain, this is reported one year later. In 2022 we further enhanced our Scope 3 calculation methodology leading to the reporting periods 2020 and 2021 being restated accordingly. 3. Our ambitions cover all tobacco we purchase for our products ('tobacco supply chain'), which is used in our combustibles, Traditional Oral and Tobacco Heated Products. Our metrics, however, derive data from our annual Thrive assessment, which includes our directly contracted farmers and those of our third-party suppliers, which represented over 94% of the tobacco we purchased by volume in 2023 ('Thrive Supply Chain'). 4. In line with a reclassification of 'ongoing incidents' (which, from 2023 reporting will be included as an 'incident' when the final decision is issued), the 2022 number has been restated (three previously reported for 2022). 5. Consistent with previous years' reporting, cases are not included if investigations were not resolved at year-end. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Our ESG Roadmap Our ESG Roadmap contains some of our key sustainability ambitions and targets, metrics and performance tracking. 11 Key ü Achieved – Met target/ambition on or ahead of time On track – Likely to meet target/ambition on time Ongoing focus – Continued progress towards target/ambition required Not on track – Significant progress required to meet target/ambition on time

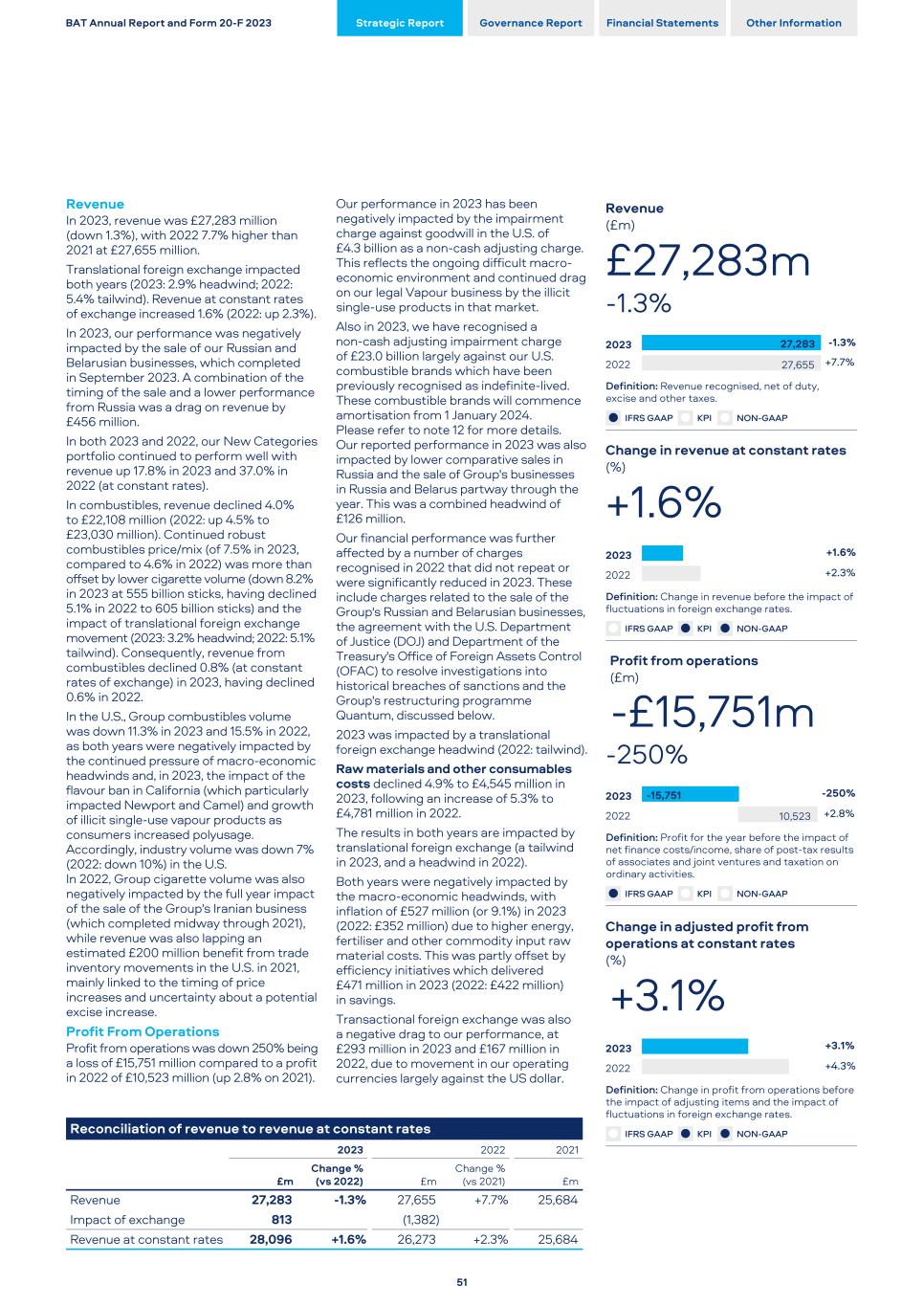

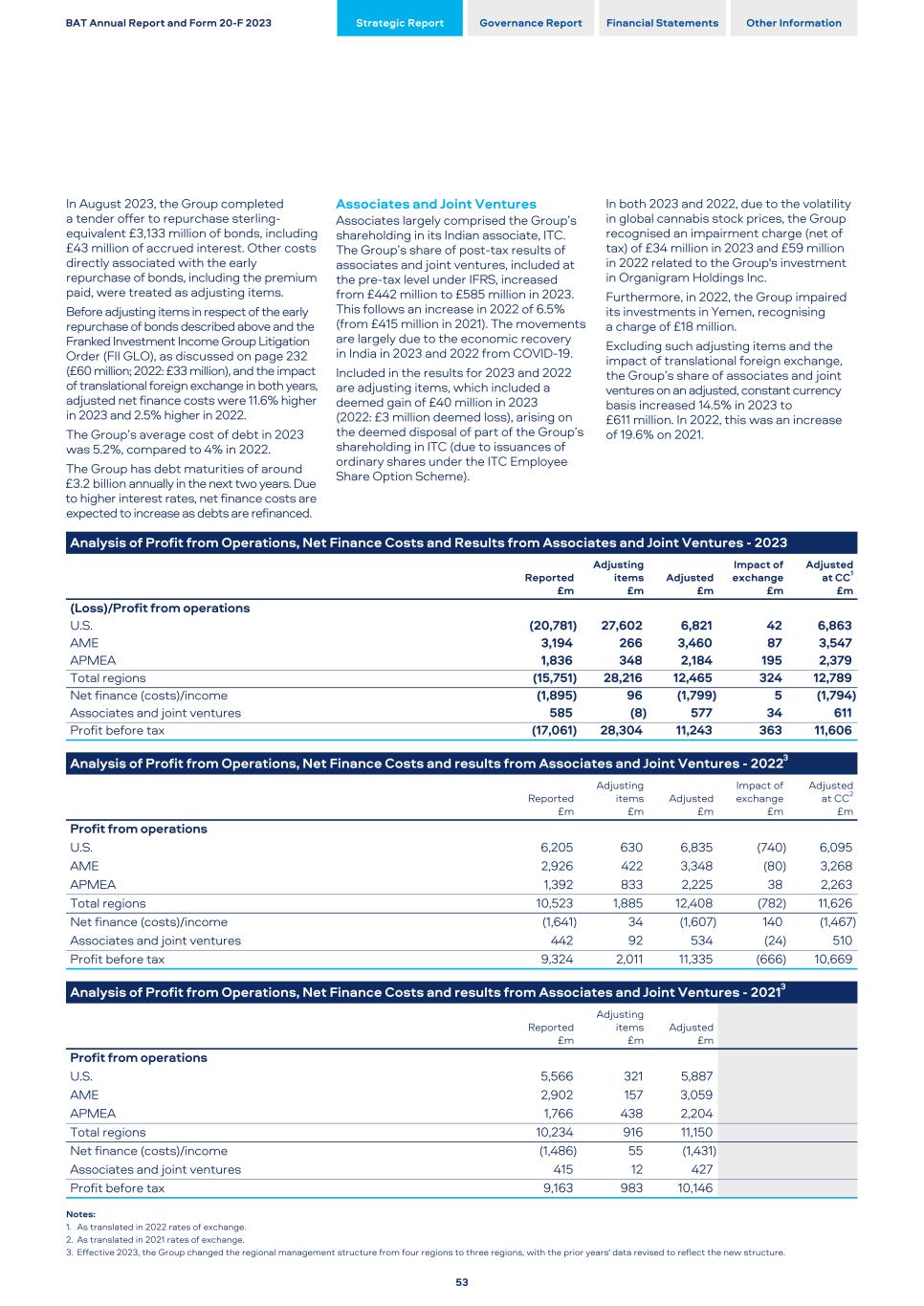

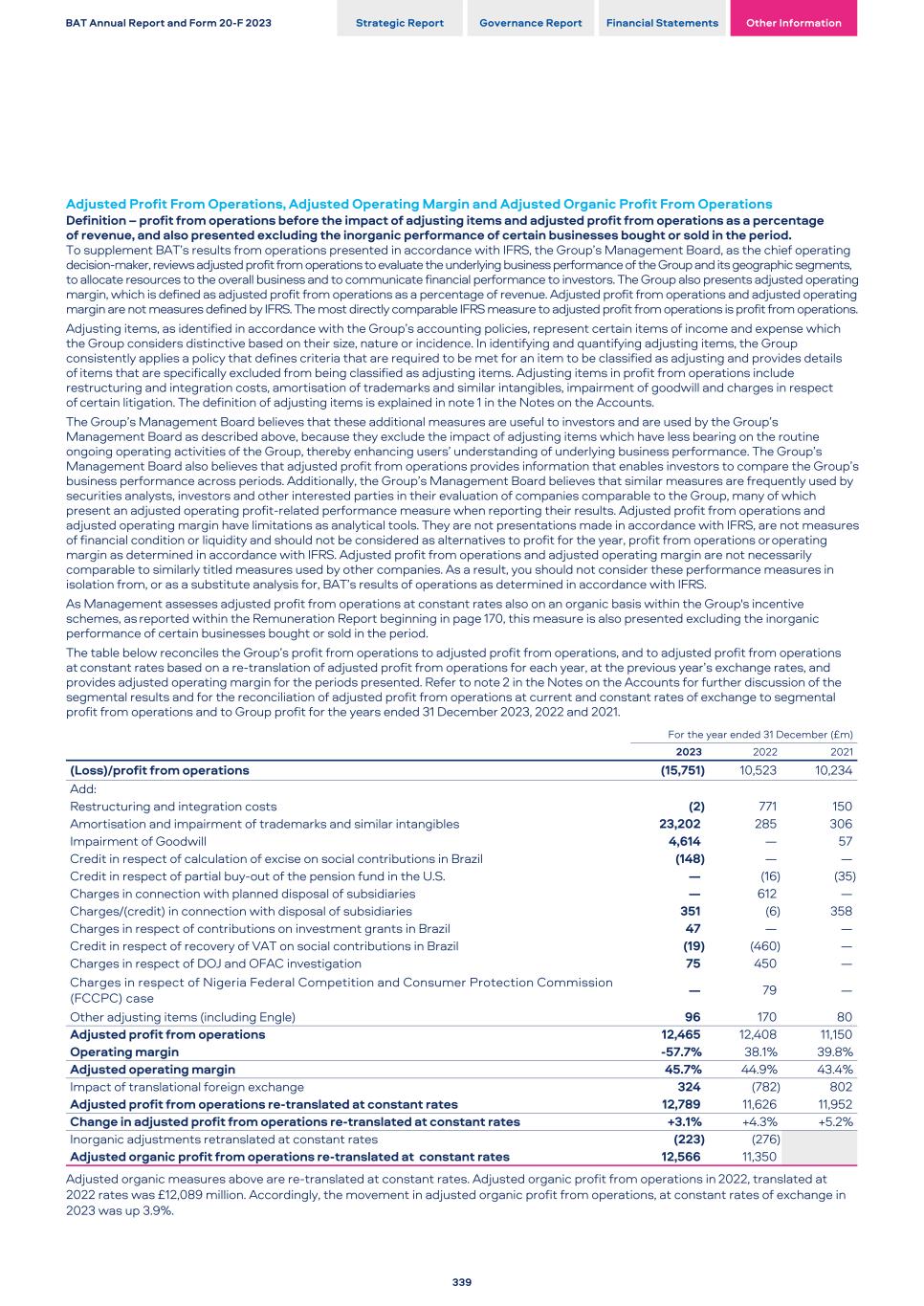

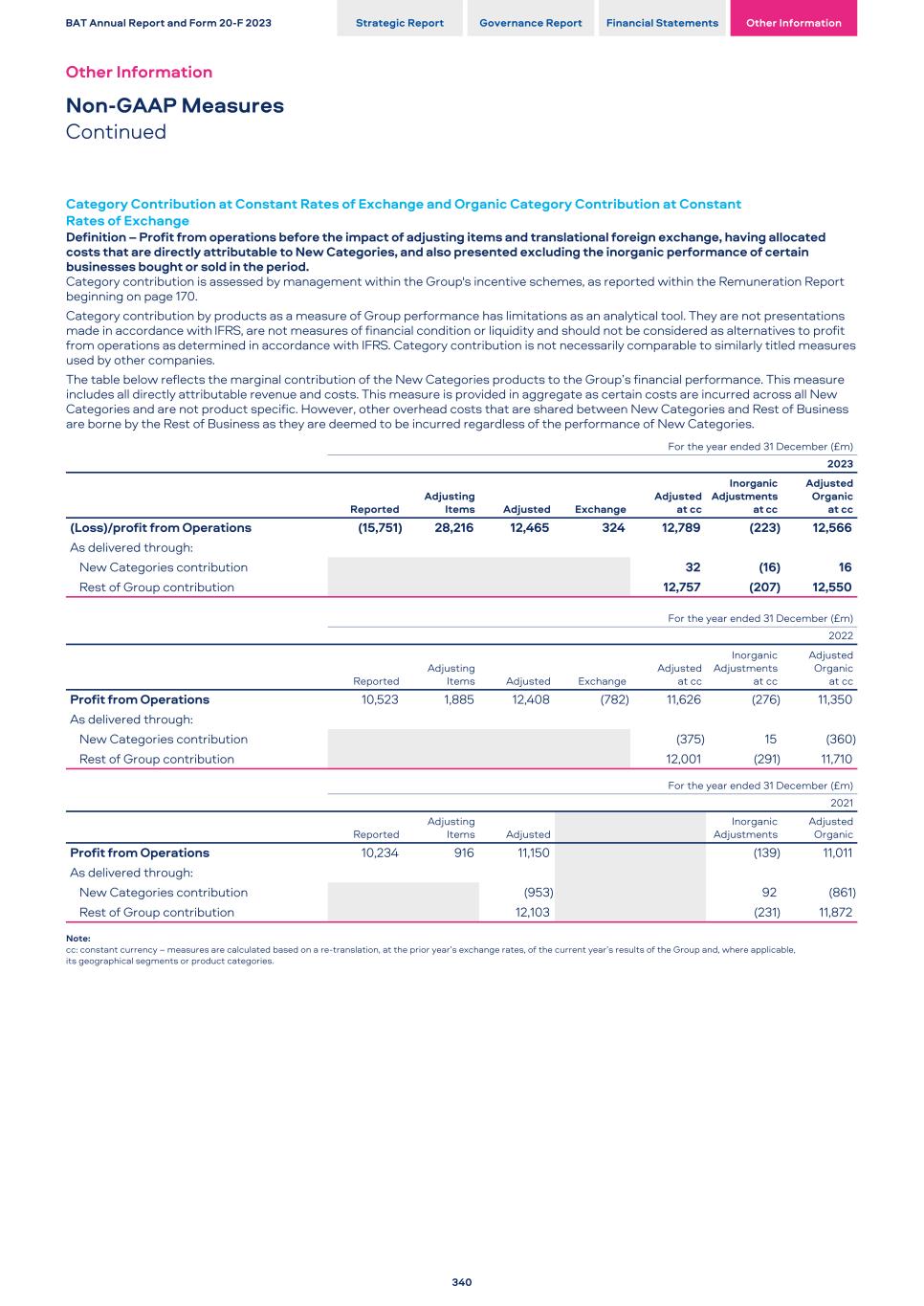

Despite the U.S. impairment negatively impacting our reported results, the Group's operational financial performance demonstrates the resilience of the business. We are highly cash generative and remain committed to our capital allocation framework. Javed Iqbal Interim Finance Director 2023 has been a challenging year as we navigated a number of issues in our performance. Our New Categories business is already profitable (at the category contribution level), two years earlier than our original plan, while our global footprint allows us to deliver on our financial priorities despite a challenging U.S. environment. We remain highly cash generative, allowing us to balance investment in the future while rewarding shareholders with a further increase in dividends (up 2.0% to 235.5p, being 25 years of annual dividend increases). The sale of our businesses in Russia and Belarus was completed in September 2023, and due to the timing of the transaction partway through the year, this was a headwind on our comparative performance as 2023 does not include a full year's performance from those markets. Combined with a lower underlying performance in Russia as we reduced investment and focus, the comparative impact on revenue was £456 million. During 2023, we have observed an acceleration of the decline rates in cigarette volume in the U.S., after a period of instability in market trends driven by the COVID-19 pandemic. In response to these increased decline rates, we have revised our forecast performance for the U.S. market, reflecting the ongoing difficult macro-economic environment, uncertainty regarding the impact of the potential menthol ban and continued drag on our legal Vapour business by the illicit single-use products. Accordingly, we have recognised a non-cash impairment charge of £27.3 billion, of which £4.3 billion is in respect of goodwill. The balance of £23.0 billion mainly relates to the acquired U.S. combustibles brands of Newport, Camel, Natural American Spirit and Pall Mall which are now considered to have a useful economic life not exceeding 30 years, rather than into perpetuity, aligned with our strategy to Build a Smokeless World. We will, therefore, be commencing amortisation of the U.S. cigarette brands (previously recognised for accounting purposes as indefinite-lived) from 1 January 2024. This non-cash charge of £1.4 billion per annum will be treated as an adjusting item. Total Group revenue declined 1.3% to £27,283 million in 2023 (having grown 7.7% in 2022 to £27,655 million). However, excluding foreign exchange movements (which were a headwind of 2.9% in 2023 and a tailwind of 5.4% in 2022) on a constant currency basis, revenue was up 1.6% in 2023 and 2.3% in 2022. This was driven by: – New Categories revenue, up 17.8% in 2023 and 37.0% in 2022; and – continued combustibles pricing, with Group price/mix of 7.5% in 2023 (4.6% in 2022); and partly offset by: – the impact of the sale of the Russian and Belarusian businesses; and – lower combustibles volume (down 8.3% in 2023) largely due to the difficult trading in the U.S. where volume was 11.3% lower. Profit from operations declined 250% to be a loss of £15,751 million, compared to a profit of £10,523 million in 2022, an increase of 2.8%. The decline in 2023 was due to the impairment charges referred to earlier in respect of the U.S. (goodwill and brands). 2022 was negatively impacted by a number of other adjusting charges which did not repeat or were substantially lower in 2023. These include the previously disclosed charges in respect of: – The sale of the Russian (and Belarusian) business (2023: £353 million, 2022: £612 million); – Restructuring and integration programmes, including Quantum, being a release in 2023 of £2 million from the previously recognised provision, which was a charge of £771 million in 2022; – The agreement with the United States Department of Justice (DOJ) and the United States Department of the Treasury’s Office of Foreign Assets Control (OFAC) to resolve historical breaches of sanctions (2023: £75 million, 2022: £450 million); and – A charge in 2022 of £79 million related to the conclusion of the investigation into alleged violations of the Nigerian Competition and Consumer Protection Act and National Tobacco Control Act. These charges were partly offset by a net credit of £167 million (2022: £460 million) in Brazil as the Group revised the calculation of VAT and excise on social contributions in prior periods following updated guidance and the conclusion of litigation. Our operating margin was consequently 95.8 ppts lower at -57.7% in 2023 (2022: down 170 bps to 38.1%). BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Overview Interim Finance Director’s Overview 12

We aim to continue to reward shareholders and our financial performance allows us to further increase our dividend by 2.0% - marking 25 years of annual dividend increases. Strong, sustainable, cash flow generation underpins confidence in the future. Profit from operations was down -250% (2022: up 2.8%), impacted by the impairment charges largely in respect of the U.S. goodwill and brands. Strong cash generation has enabled us to return £5.1 billion of cash to shareholders in 2023, while still deleveraging. Excluding these significant adjusting items, and a translational foreign exchange headwind of 2.6%, on an adjusted constant currency basis (which we believe reflects the operational performance of the Group) profit from operations grew by 3.1% (2022: up 4.3%), due to the continued reduction in losses from New Categories, which are now profitable at a category contribution level- two years ahead of our original plan. Adjusted operating margin (at current rates) increased 80 bps to 45.7% (2022: up 150 bps to 44.9%) driven by the reduction in New Categories losses in both years, combined with the impact of the disposal of the Group's businesses in Russia and Belarus, as the margins of those businesses were lower than the Group average. EPS Impacted by U.S. Impairment, Offsetting Resilient Operating Performance On a reported basis, basic EPS was down 320% at -646.6p (2022: down 1.2% at 293.3p) with diluted EPS 322% lower at -646.6p (2022: down 1.3% to 291.9p), as 2023 was impacted by the impairment charges recognised in respect of the U.S. Excluding both the adjusting items (discussed on pages 52 and 53) and the effect of foreign exchange on the Group’s results, adjusted diluted earnings per share, at constant rates, increased by 4.0% to 386.4p, building on the 5.8% growth in 2022. The performance in 2023 was also impacted by the timing of the sale of the Group's businesses in Russia and Belarus during the year, a negative headwind on the performance of 1.2%. Active Capital Allocation Framework Ensures Deleverage, Investment and Investor Returns We remain committed to our active capital allocation framework, which we expect will deliver long-term value to our shareholders, driven by our cash flow generation and deleverage plans. These include: – Continuing to grow the dividend; – Maintaining our target leverage corridor; – Potential bolt-on M&A opportunities; and – Share buy-backs to enhance shareholder returns. The Group remains highly cash generative, realising £10.7 billion (2022: £10.4 billion) of net cash generated from operating activities. This allowed for a net repayment of borrowings in the year, with total borrowings (including lease liabilities) down from £43,139 million in 2022 to £39,730 million in 2023. Consequently, our leverage ratio has improved towards the middle of our range. Our liquidity profile remains strong, with average debt maturity close to 10.5 years and maximum debt maturities in any one calendar year of around £4 billion, with a current rating of Baa2 (positive outlook), BBB+ (negative outlook), BBB (positive outlook) from Moody's, S&P and Fitch*, respectively. In August 2023, the Group completed a tender offer to repurchase sterling- equivalent £3,133 million of bonds, including £43 million of accrued interest, reducing future refinancing risk. The Group has debt maturities of around £3.2 billion annually in the next two years. Due to higher interest rates, net finance costs are expected to increase as debts are refinanced. 25 Years of Consistent Dividend Growth We are extremely proud of our long history of dividend growth. 2023 marks the 25th consecutive year of sterling dividend increases, with a further increase of 2.0% to 235.52p (with a dividend payout ratio of 62.7%). Facing the Future with Increasing Confidence Our business is well placed for the future. With a diversified geographic and product portfolio, and a track record of delivering robust and consistent cash generation, we believe the Group is well positioned to continue to invest for future growth while navigating the near-term macro-economic uncertainties and challenges. Notes: * A credit rating is not a recommendation to buy, sell or hold securities. A credit rating may be subject to withdrawal or revision at any time. Each rating should be evaluated separately of any other rating. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 13

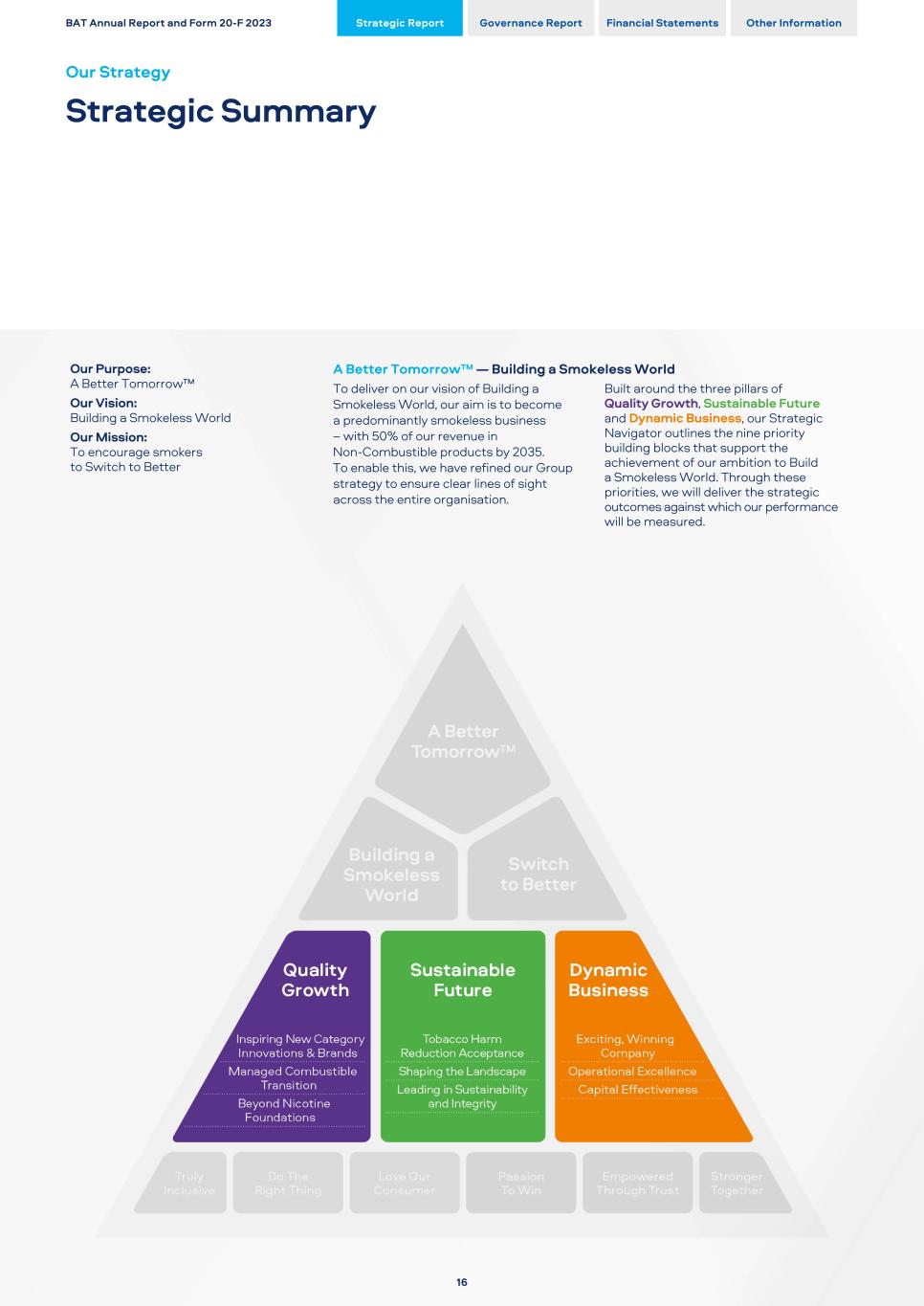

The tobacco and nicotine industry has undergone a seismic shift in recent years. Increasing numbers of adult smokers are migrating to smokeless products like Vapour products, Heated Products and Modern Oral nicotine pouches. With an increasing amount of scientific research behind these products, they represent an opportunity for Tobacco Harm Reduction on a global scale. We have played a significant part in the ongoing industry transformation towards Tobacco Harm Reduction. Our multi- category strategy continues to be the right one to meet the evolving preferences of adult consumers around the world and deliver business growth. We have built a portfolio of three powerful smokeless product brands: Vuse, glo and Velo, which have delivered more than £3 billion of annual revenue in just a decade. After significant early-stage investments, we are encouraged that our New Categories are profitable (at a category contribution level) two years ahead of our original target. Our focus on driving revenue growth and margin expansion will continue. To accelerate the next phase of our transformation, we are committing to Building a Smokeless World. This means we will deploy our global multi-category portfolio to actively encourage smokers to switch to smokeless products – in nicotine and beyond. In essence, to encourage smokers to ‘Switch to Better’. In turn, this will realise the multi-stakeholder benefits of A Better Tomorrow™. At a business level, our aim is to become a predominantly smokeless business, with 50% of our revenue from Non-Combustibles by 2035. To deliver this, we have refined our Group strategy to ensure clear lines of sight across the entire organisation. Built around the three pillars of Quality Growth, Sustainable Future and Dynamic Business, our Strategic Navigator outlines the nine priority building blocks that support the achievement of our ambition to Build a Smokeless World. Through these priorities, we will deliver the strategic outcomes against which our performance will be measured. Quality Growth Transitioning to a more balanced focus on top-line and bottom-line delivery, focusing on our brands and innovation, and continuing to seek long-term opportunities Beyond Nicotine. Sustainable Future Seeking to actively migrate consumers away from cigarettes and to smokeless alternatives sustainably, responsibly and with integrity. Dynamic Business Building a future-fit, data-driven organisation and ensuring we are efficient and effective in all of our operations. This will create the greatest financial flexibility possible to invest in our people, our products and provide returns to our investors. For BAT, A Better Tomorrow™ is very clear. We will work to Build a Smokeless World. The way we will do this is by switching as many smokers as we can to our smokeless products. Tadeu Marroco Chief Executive BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Our Strategy Our Refined Strategy To accelerate the next phase of our transformation, we are committing to Building a Smokeless World. This means we will deploy our global multi-category portfolio to actively encourage smokers to switch to smokeless products – in nicotine and beyond. 14

BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Our Strategic Navigator 15

Our Purpose: A Better Tomorrow™ Our Vision: Building a Smokeless World Our Mission: To encourage smokers to Switch to Better A Better Tomorrow™ — Building a Smokeless World To deliver on our vision of Building a Smokeless World, our aim is to become a predominantly smokeless business – with 50% of our revenue in Non-Combustible products by 2035. To enable this, we have refined our Group strategy to ensure clear lines of sight across the entire organisation. Built around the three pillars of Quality Growth, Sustainable Future and Dynamic Business, our Strategic Navigator outlines the nine priority building blocks that support the achievement of our ambition to Build a Smokeless World. Through these priorities, we will deliver the strategic outcomes against which our performance will be measured. BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Our Strategy Strategic Summary 16

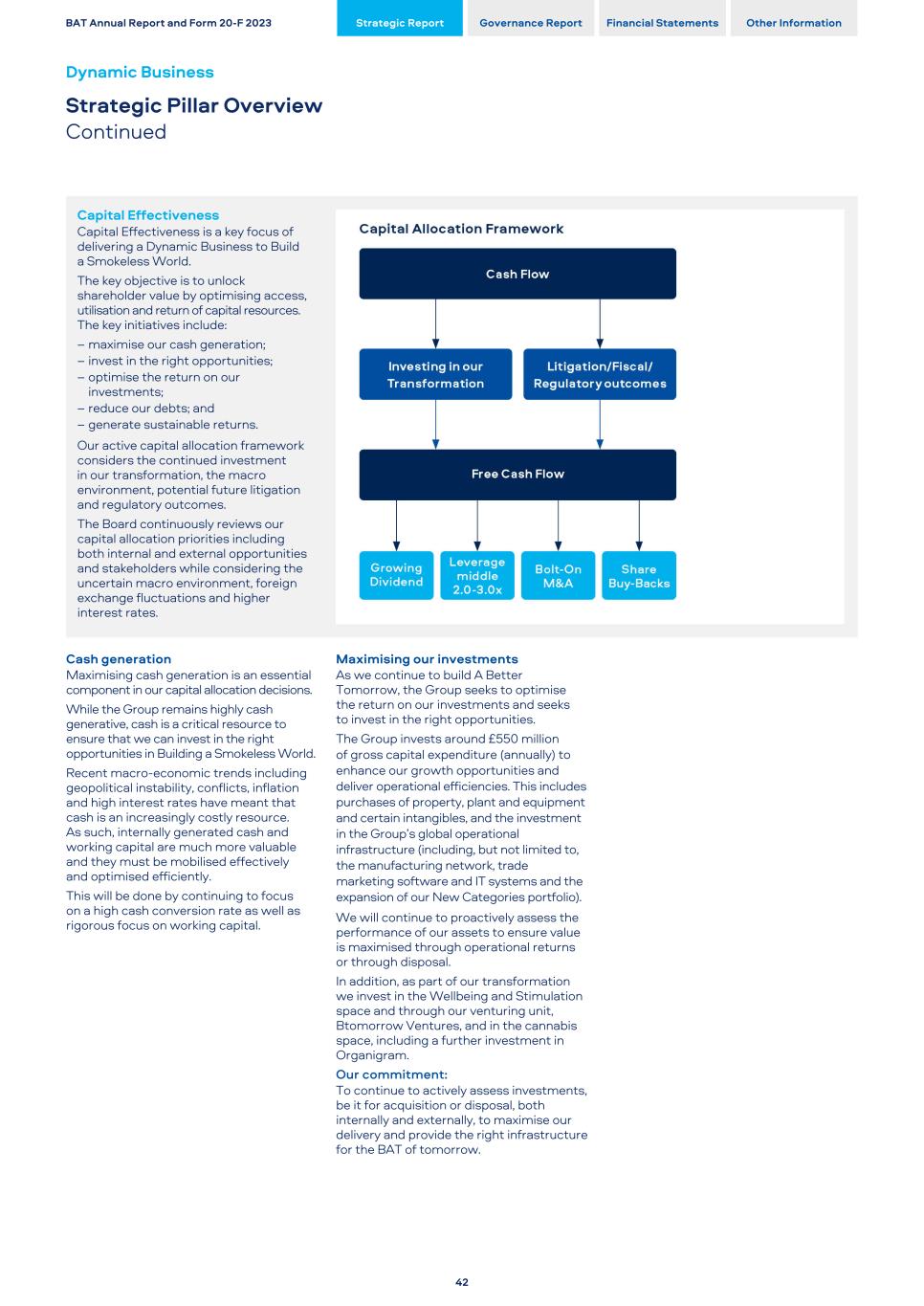

Transitioning to a more balanced focus on top-line and bottom-line delivery, focusing on our brands and innovation, and continuing to seek long-term opportunities Beyond Nicotine. In the tobacco and nicotine industry, stable combustibles revenues and accretive New Category growth underpin continued revenue growth. Yet, only around 10% of the world’s one billion smokers have made the Switch to Better and replaced combustibles with smokeless products. The long-term opportunity for growth, as we strive to accelerate this transformation, remains vast. Prioritising where and what products to focus on, via our market archetype model, will guide our human and financial resource allocation decisions. We will enhance our innovation ecosystem with a single-minded aim: developing an outstanding pipeline of new, scientifically substantiated products. Our combustibles business remains essential to funding our transformation and continuing to reward our shareholders. In Beyond Nicotine, we will build a pathway to a new portfolio of non-nicotine-based products that can enhance BAT's growth beyond 2025. Within Beyond Nicotine there are two categories that BAT is exploring: Wellbeing and Stimulation – functional consumable products that help people manage their mood and wellbeing; and cannabis. Our commitments under Quality Growth: Progressing toward quality, margin- accretive growth in smokeless products FMC volume decline but expecting continuing value delivery Sensibly investing for the future Beyond Nicotine For more details on the Quality Growth pillar of our refined strategy,see page 28+ Seeking to actively migrate consumers away from cigarettes and to smokeless alternatives sustainably, responsibly and with integrity. There has been significant progress in the global Tobacco Harm Reduction (THR) journey over the past decade. Today, there are three significant global smokeless tobacco and nicotine product categories: Vapour products, Heated Products and Modern Oral nicotine products. Our ambition is to reduce the health impact of our business via THR – migrating more smokers to smokeless products and advocating for the right regulatory environments for these products to flourish. We must do this responsibly and with integrity. We recognise and support the objective of governments to reduce smoking rates and its associated health impact. Combustible tobacco products pose serious health risks. The only way to avoid these risks is not to start or to quit smoking. For those adults who would otherwise continue to smoke or start smoking, we believe they should be able to make better choices by opting for smokeless alternatives instead of cigarettes. Science will be a primary driver of our efforts, supported by more active external engagement with regulators and other key stakeholders, while embedding sustainability across our organisation. As we transition from cigarettes to smokeless products, our transformation must be comprehensive – addressing not only our products' public health impact but also our other material sustainability topics. Our commitments under Sustainable Future: Building a Smokeless World Investing in the products, science and engagement to make A Better Tomorrow™ a reality Conducting our business sustainably and with integrity For more details on the Sustainable Future pillar of our refined strategy see page 60+ Building a future-fit, data-driven organisation and ensuring we are efficient and effective in all of our operations. We believe we can create the financial flexibility to invest in our people, our products and provide returns to our investors. We are committed to building a company where people and performance come together to create the extraordinary. That is why creating an Exciting, Winning Company is one of the building blocks under the Dynamic Business pillar. Additionally, generating shareholder value, via sustainable returns, remains an integral part of our strategic ambition. Over the past 25 years we have consistently grown the dividend per ordinary share in absolute terms. Reducing debt is another core component of the Dynamic Business pillar. Given current geopolitical and economic challenges, the Group aims to de-lever its gross debt levels (c.£39.7 billion in 2023) and moderate the annual Net Financing Cost levels (c.£1.9 billion in 2023) to better support the overall strategy of the Group. Our commitments under Dynamic Business: Creating a diverse, inclusive and people-oriented place to work Being data-driven and delivering operational excellence/cost management Focused on investors returns For more details on the Dynamic Business pillar of our refined strategy,see page 40+ BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 17

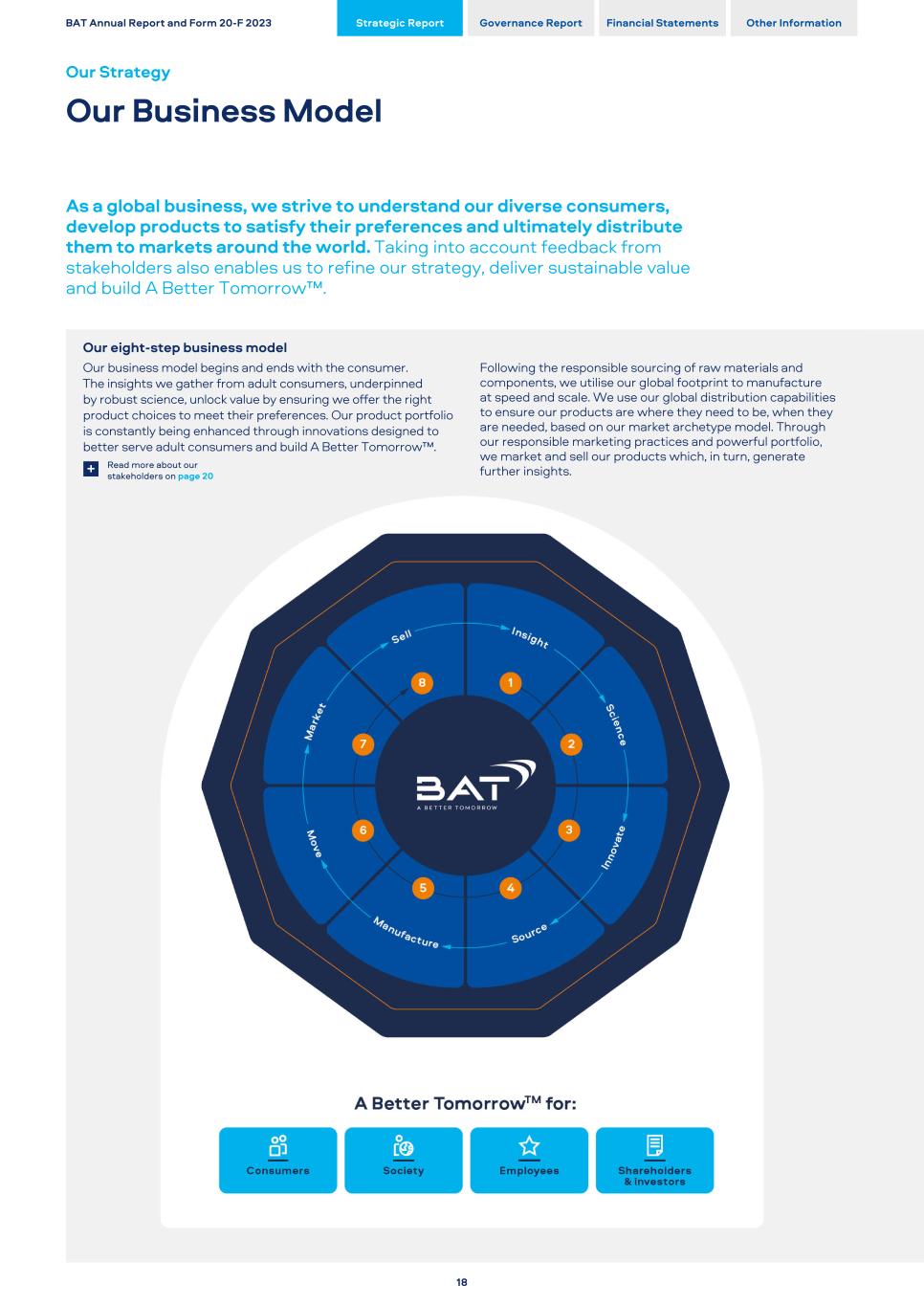

Our eight-step business model Our business model begins and ends with the consumer. The insights we gather from adult consumers, underpinned by robust science, unlock value by ensuring we offer the right product choices to meet their preferences. Our product portfolio is constantly being enhanced through innovations designed to better serve adult consumers and build A Better Tomorrow™. Following the responsible sourcing of raw materials and components, we utilise our global footprint to manufacture at speed and scale. We use our global distribution capabilities to ensure our products are where they need to be, when they are needed, based on our market archetype model. Through our responsible marketing practices and powerful portfolio, we market and sell our products which, in turn, generate further insights.Read more about our stakeholders on page 20+ BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information Our Strategy Our Business Model As a global business, we strive to understand our diverse consumers, develop products to satisfy their preferences and ultimately distribute them to markets around the world. Taking into account feedback from stakeholders also enables us to refine our strategy, deliver sustainable value and build A Better Tomorrow™. 18

Seeing over the horizon As one of the most long-standing and established tobacco and nicotine businesses in the world, we have a unique view of the consumer across our product categories. This is increasingly driven by powerful data and analytics. These insights ensure that the development and responsible marketing of our products are fit to satisfy consumer preferences. Powered by our data-driven consumer insight platform, we focus on product categories and consumer segments across our global business that have the best potential for long- term sustainable growth. Link to Principal Risks Tobacco, New Categories and other regulation interrupts growth strategy; Inability to develop, commercialise and deliver the New Categories strategy; Climate change and circular economy; Cyber security Tobacco Harm Reduction Acceptance World-class science is required to substantiate the quality, product safety and reduced-risk potential of our New Category products. This is crucial for building consumer and regulators' trust and encouraging adult smokers to completely switch to less risky alternatives*†. We have an extensive scientific research programme in a broad spectrum of scientific fields, including molecular biology, toxicology and chemistry. We are transparent about our science and publish details of our research programmes on our dedicated website, www.bat- science.com, and the results of our studies in peer-reviewed journals. Link to Principal Risks Competition from illicit trade; Tobacco, New Categories and other regulation interrupts growth strategy; Significant increases or structural changes in tobacco, nicotine and New Categories related taxes; Inability to develop, commercialise and deliver the New Categories strategy Read more about our science on pages 30, 32, 34, 66 and 78+ Staying ahead of the curve As consumer preferences and technology rapidly evolve, we rely on our growing global network of digital hubs, innovation hubs, world-class R&D laboratories, external partnerships and our corporate venturing initiative, Btomorrow Ventures. Driving sustainable growth is at the core of our innovation. We make significant investments in research and development to deliver innovations that satisfy or anticipate consumer preferences and generate growth for the business. Led by our strength in developing consumer insights, each innovation helps us on our journey to build A Better Tomorrow™ by reducing the health impact of our business. Link to Principal Risks Inability to develop, commercialise and deliver the New Categories strategy; Climate change and circular economy; Cyber security Sourcing materials responsibly The majority of our tobacco is sourced by BAT Group's vertically integrated Leaf Operations through direct contracts with c.91,000 farmers. Of the remainder, the majority is from third-party suppliers that, in turn, contract with an estimated 155,000 farmers. The vast majority of tobacco farms in our supply chain are smallholder family farms. Beyond tobacco, we source product materials like paper and filters for cigarettes and, for our New Category products, we have a growing supply chain in consumer electronics and e-liquids. We also have a vast number of suppliers of indirect goods and services that are not related to our products, such as for IT services and facilities management. Link to Principal Risks Geopolitical tensions; Supply chain disruption; Inability to develop, commercialise and deliver the New Categories strategy; Injury, illness or death in the workplace; Solvency and liquidity; Foreign exchange rate exposures; Climate change and circular economy; Cyber security Read more about our supply chain on page 41+ Utilising our global manufacturing footprint We manufacture high-quality products in facilities all over the world. We also ensure that these products and the tobacco leaf we purchase are optimised for distribution and sale. Our New Category products are manufactured in a mix of our own and third-party factories. We work to ensure that our costs are globally competitive and that we use our resources as effectively as possible. Link to Principal Risks Geopolitical tensions; Supply chain disruption; Disputed taxes, interest and penalties; Injury, illness or death in the workplace; Solvency and liquidity; Foreign exchange rate exposures; Climate change and circular economy Moving our products seamlessly everywhere By applying modern technologies, including AI and machine learning, we ensure our products are where they are needed when they are needed. Our products are sold around the world and distributed effectively and efficiently using a variety of distribution models suited to local circumstances and conditions. These distribution models include retailers, supplied through our direct distribution capability or exclusive distributors, and our Direct-to- Consumer business – which has been accelerated through the deployment of owned e-commerce sites. Link to Principal Risks Geopolitical tensions; Tobacco, New Categories and other regulation interrupts growth strategy; Supply chain disruption; Inability to develop, commercialise and deliver the New Categories strategy; Foreign exchange rate exposures; Climate change and circular economy; Cyber security Marketing our products responsibly Tobacco and nicotine products should be marketed responsibly to adults only and not designed to appeal to the underage. Through a globally responsible approach to marketing, we seek to help raise standards and prevent under-age access, while growing our market share by encouraging adult consumers to choose our products over those of our competitors. Our International Marketing Principles (IMP) govern our marketing across all our tobacco, nicotine and nicotine-free products and brands. They include strict requirements to be responsible, accurate and targeted at adult consumers only. Our IMP are applied even when they are stricter than local laws. Link to Principal Risks Competition from illicit trade; Tobacco, New Categories and other regulation interrupts growth strategy; Inability to develop, commercialise and deliver the New Categories strategy; Litigation; Foreign exchange rate exposures Read more about responsible marketing on page 96+ Offering the consumer choice We have a powerful brand portfolio that we are very proud of. This includes our combustibles portfolio and our portfolio of smokeless product brands which will contribute to Building a Smokeless World. Our global brands are well positioned, with leading-edge insights, science and innovation behind our product pipeline. We offer adult consumers a range of products, including combustible products, Vapour, Modern Oral and Heated Products, in markets around the world. Our range of high-quality products covers all segments, from value-for-money to premium. Link to Principal Risks Competition from illicit trade; Geopolitical tensions; Tobacco, New Categories and other regulation interrupts growth strategy; Supply Chain disruption; Litigation; Significant increases or structural changes in tobacco, nicotine and New Categories related taxes; Inability to develop, commercialise and deliver the New Categories strategy; Disputed taxes, interest and penalties; Foreign exchange rate exposures; Climate change and circular economy BAT Annual Report and Form 20-F 2023 Strategic Report Governance Report Financial Statements Other Information 19