UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number:

(Exact Name of Registrant as Specified in Its Charter)

N/A

(Translation of Registrant’s Name into English)

(Jurisdiction of Incorporation or Organization)

(Address of Principal Executive Offices)

(

Email:

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class |

| Trading Symbol(s) |

| Name of Each Exchange On Which Registered |

The |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2023, there were

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

3

INTRODUCTION

Unless otherwise indicated and except where the context otherwise requires, references in this annual report to:

| ● | “Acrotech” are to Acrotech Biopharma L.L.C.; |

| ● | “ANDA” are to abbreviated new drug application; |

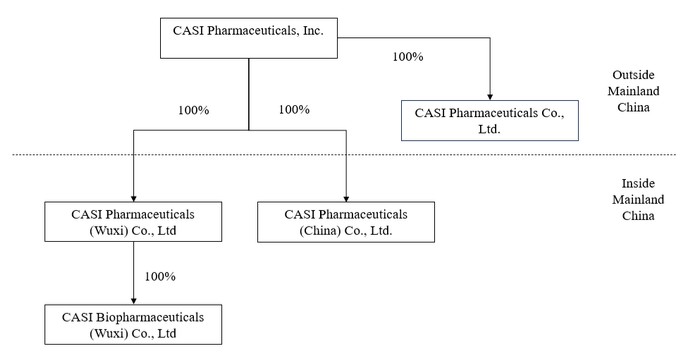

| ● | “CASI”, “us”, “our Company”, “the Company”, “our” and “we” are to (I) CASI Pharmaceuticals, Inc., an exempted company with limited liability incorporated under the laws of the Cayman Islands (“CASI Cayman”) and its subsidiaries after the Redomicile Merger, and (ii) CASI Pharmaceuticals, Inc., a Delaware corporation (“CASI Delaware”) and its subsidiaries prior to the Redomicile Merger, in each case as appropriate based on the context; |

| ● | “CASI China” are to CASI Pharmaceuticals (China) Co., Ltd.; |

| ● | “CASI Wuxi” are to CASI Pharmaceuticals (Wuxi) Co., Ltd.; |

| ● | “CASI Biopharmaceuticals” are to CASI Biopharmaceuticals (WUXI) Co., Ltd; |

| ● | “CASI Hong Kong” are to CASI Pharmaceuticals Co., Limited; |

| ● | “China” or the “PRC” are to the People’s Republic of China, excluding, for the purposes of this annual report only, Hong Kong, Macau and Taiwan; |

| ● | “CDE” are to the China Center for Drug Evaluation; |

| ● | “cGMP” are to current Good Manufacturing Practice; |

| ● | “CTA” are to the Clinical Trial Application; |

| ● | “Companies Act” are to the Companies Act (As Revised) of the Cayman Islands; |

| ● | “EMA” are to the European Medicines Agency; |

| ● | “FDA” are to the U.S. Food and Drug Administration; |

| ● | “IRB” are to institutional review board; |

| ● | “Juventas” are to Juventas Cell Therapy Ltd.; |

| ● | “NMPA” are to the PRC National Medical Products Administration; |

| ● | “ordinary shares” are to our ordinary shares, par value US$0.0001 per share; |

| ● | “PAT” are to Precision Autoimmune Therapeutics, a company established under the laws of China, in which the Company holds an equity investment; |

| ● | “Redomicile Merger” are to a merger between CASI Delaware and CASI Cayman for the purpose of CASI Delaware’s re-domiciliation from the State of Delaware of U.S. to the Cayman Islands, where CASI Delaware merged with and into CASI Cayman with CASI Cayman becoming the surviving entity and the successor issuer; |

| ● | “RMB” and “Renminbi” are to the legal currency of China; |

| ● | “US$,” “U.S. dollars,” “$” and “dollars” are to the legal currency of the United States; and |

| ● | “Wuxi LP” are to Wuxi Huicheng Yuanda Investment Partnership (Limited Partnership) (formerly known as Wuxi Jintou Huicun Investment Enterprise), a limited partnership organized under the laws of the People’s Republic of China. |

4

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements that relate to our current expectations and views of future events. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. These statements are made under the “safe harbor” provisions under Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act and of the U.S. Private Securities Litigations Reform Act of 1995.

You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to,” “potential,” “continue” or other similar expressions. These forward-looking statements include, among others, statements regarding the timing of our commercial launch of products, clinical trials, our cash position and future expenses, and our future revenues. We have based these forward-looking statements largely on our current expectations and projections about future events that we believe may affect our financial condition, results of operations, business strategy and financial needs.

Actual results could differ materially from those currently anticipated due to a number of factors, including: the risk that we may be unable to continue as a going concern as a result of our inability to raise sufficient capital for our operational needs; the possibility that we may be delisted from trading on The Nasdaq Capital Market if we fail to satisfy applicable continued listing standards; the volatility in the market price of our ordinary shares; the risk of substantial dilution of existing shareholders in future share issuances; the difficulty of executing our business strategy on a global basis including China; our inability to enter into strategic partnerships for the development, commercialization, manufacturing and distribution of our proposed product candidates or future candidates; legal or regulatory developments in China that adversely affect our ability to operate in China; our lack of experience in manufacturing products and uncertainty about our resources and capabilities to do so on a clinical or commercial scale; risks relating to the commercialization, if any, of our products and proposed products (such as marketing, safety, regulatory, patent, product liability, supply, competition and other risks); our inability to predict when or if our product candidates will be approved for marketing by the U.S. FDA, EMA, NMPA, or other regulatory authorities; our inability to receive approval for renewal of license of our existing products; the risks relating to the need for additional capital and the uncertainty of securing additional funding on favorable terms; the risks associated with our product candidates, and the risks associated with our other early-stage products under development; the risk that result in preclinical and clinical models are not necessarily indicative of clinical results; uncertainties relating to preclinical and clinical trials, including delays to the commencement of such trials; our ability to protect our intellectual property rights; the lack of success in the clinical development of any of our products and our dependence on third parties; the risks related to our dependence on Juventas to partner with us to co-market CNCT19; risks related to the uncertainty in connection with the ongoing arbitration proceedings between us and Juventas with respect to Juventas’ purported termination of certain CNCT19 license agreements; risks related to our dependence on Juventas to ensure the patent protection and prosecution for CNCT19; risks relating to interests of our largest shareholder and our Chairman and CEO that differ from our other shareholders; and risks related to the success of a new manufacturing facility by CASI Wuxi. Such factors, among others, could have a material adverse effect upon our business, results of operations and financial condition.

You should read this annual report and the documents that we refer to in this annual report and have filed as exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect. Other sections (including “Item 3. Key Information—D. Risk Factors”) of this annual report discuss factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements. We undertake no obligation to publicly release the result of any revision of these forward-looking statements to reflect events or circumstances after the date they are made or to reflect the occurrence of unanticipated events. Additional information about the factors and risks that could affect our business, financial condition and results of operations, are contained in our filings with the U.S. Securities and Exchange Commission (“SEC”), which are available at www.sec.gov.

5

You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

6

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Risks and Uncertainties Relating to Doing Business in China

We face various risks and uncertainties related to doing business in China. Our business operations are primarily conducted in China, and we are subject to complex and evolving PRC laws and regulations. For a detailed description of risks related to doing business in China, please refer to risks disclosed under “Item 3. Key Information — D. Risk Factors — Risks Relating to Our Business Operations in China.”

PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or become worthless. Implementation of industry-wide regulations, including data security or anti-monopoly related regulations, in this nature could result in a material change in our operations and may cause the value of our securities to significantly decline or become worthless. Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our ordinary shares. For example, the China’s government has made in recent years statements and regulatory actions to regulate certain market players or to improve its supervision of the market in general, such as those related to data security or anti-monopoly concerns. While we currently do not believe such regulatory actions have materially impacted our business operations, our ability to accept foreign investments, or our ability to maintain listing with the Nasdaq Stock Market, there is no assurance that any new rules or regulations promulgated in the future will not impose additional requirements on us. If any such rules or regulations is adopted, we may be subject to more stringent regulatory scrutinizes for our operation and financing efforts, which may in turn result in more compliance costs and expenses to be incurred by us, delay our investment and financing activities, or otherwise impact our ability to conduct our business, accept foreign investments, or list on a U.S. or other foreign exchange. For more details, see “Item 3. Key Information — D. Risk Factors — Risks Relating to Our Business Operations in China — The legal system in China embodies uncertainties which could impose additional requirements and obligations on our business, and PRC laws, rules, and regulations can evolve quickly with little advance notice, which may materially and adversely affect our business, financial condition, and results of operations.”

Risks Relating to Our Auditor

Our auditor, the independent registered public accounting firm that issues the audit report contained in our annual report, as an auditor of companies that are traded publicly in the United States and a firm registered with the PCAOB, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess its compliance with the applicable professional standards. Our auditor is located in mainland China, a jurisdiction where the PCAOB was historically unable to conduct inspections and investigations completely before 2022. As a result, we and investors in CASI Delaware’s common stock were deprived of the benefits of such PCAOB inspections. Pursuant to the Holding Foreign Companies Accountable Act, or the HFCAA, if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspections by the PCAOB for two consecutive years, the SEC will prohibit our securities from being traded on a national securities exchange or in the over-the-counter trading market in the United States.

On December 16, 2021, the PCAOB issued a report to notify the SEC of its determination that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong and CASI Delaware’s auditor was subject to that determination. In April 2022, the SEC conclusively listed CASI Delaware as a Commission-Identified Issuer under the HFCAA following the filing of its annual report on Form 10-K for the fiscal year ended December 31, 2021.

7

On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. For this reason, we do not expect we will be identified as a Commission-Identified Issuer under the HFCAA after we file this annual report for the fiscal year ended December 31, 2023.

Each year in the future, the PCAOB will determine whether it can inspect and investigate completely audit firms in mainland China and Hong Kong, among other jurisdictions. If the PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in mainland China and Hong Kong and we use an accounting firm headquartered in one of these jurisdictions to issue an audit report on our financial statements filed with the SEC, we would be identified as a Commission-Identified Issuer following the filing of the annual report for the relevant fiscal year. In accordance with the HFCAA, our ordinary shares would be prohibited from being traded on a national securities exchange or in the over-the-counter trading market in the United States if we are identified as a Commission-Identified Issuer for two consecutive years in the future. If our ordinary shares are prohibited from trading in the United States, there is no certainty that we will be able to list on a non-U.S. exchange or that a market for our ordinary shares will develop outside of the United States. A prohibition of being able to trade in the United States would substantially impair your ability to sell or purchase our ordinary shares when you wish to do so, and the risk and uncertainty associated with delisting would have a negative impact on the price of such shares. Also, such a prohibition would significantly affect our ability to raise capital on terms acceptable to us, or at all, which would have a material adverse impact on our business, financial condition, and prospects.

For more details, see “Item 3. Key Information — D. Risk Factors — Risks Relating to Our Auditor.”

Cash and Asset Transfer among the Company and its Subsidiaries

We provide funding to our subsidiaries from time to time through capital contributions or loans, subject to satisfaction of applicable government registration and approval requirements. For the year ended December 31, 2023, we made funding of US$1.0 million through capital contributions to CASI Hong Kong, our newly incorporated Hong Kong subsidiary.

Our subsidiaries may pay dividends and make other distributions to us subject to satisfaction of applicable government filing and approval requirements. Such dividend or other distributions may be subject to limitations and certain tax consequences, a discussion on which is set forth below. For the year ended December 31, 2023, no dividends or other distributions were made by our subsidiaries.

We also pay service fees to our PRC subsidiaries pursuant to certain sales support service agreement and research and development support service agreement. For the year ended December 31 2023, we paid service fees of US$1.1 million to CASI China, one of our PRC subsidiaries. Under PRC tax laws and regulations, earning of our subsidiaries under such agreements are subject to a statutory tax rate of 25%.

In the year ended December 31, 2023, no assets other than cash were transferred through our organization.

All cash transfers among us and our subsidiaries have been eliminated in our consolidated statement of cash flows.

The existing PRC foreign exchange regulations may limit our ability to initiate and complete the cash transfers within our group. Approval from SAFE and PBOC may be required where RMB are to be converted into foreign currencies, including U.S. dollars, and approval from SAFE and PBOC or their branches may be required where RMB are to be remitted out of China. Please see “Item 3. Key Information — D. Risk Factors —Risks Relating to Our Business Operations in China — Governmental control of currency conversion and payments of RMB out of China may limit our ability to utilize our cash balances effectively and affect the value of your investment.”

CASI Delaware and CASI Cayman have never declared or paid dividends on its common stock or any other securities and we do not anticipate paying any dividends on our ordinary shares in the foreseeable future. We may rely on dividends from our subsidiaries in China to pay dividend and other distributions on our ordinary shares. PRC regulations may restrict the ability of our PRC subsidiaries to pay dividends to us. In addition to applicable foreign exchange limitations, under the current regulatory regime in China, a PRC company may pay dividends only out of their accumulated profit, if any, determined in accordance with PRC accounting standards and regulations, and is required to set aside as general reserves at least 10% of its after-tax profit, until the cumulative amount of such reserves reaches 50% of its registered capital, prior to any dividend distribution. In addition, a PRC company shall not distribute any profits in a given year until any losses from prior fiscal years have been offset.

8

Permission and Filing Procedures Required from the PRC Authorities with respect to the Operations of Our PRC Subsidiaries and Future offering in the US

As the date hereof, our PRC subsidiaries have obtained the requisite licenses and permits from the PRC government authorities that are material for our business operations, including, among others, the Business License, the Drug Distribution License, the Drug Manufacturing Permit, the Clinical Trial Application with the NMPA, and the notification filing for international collaborative clinical trial or the application for international collaborative scientific research with the China Human Genetic Resources Administrative Office (“HGRAO”). We also work with our business partners which have obtained the requisite license and permits for their business collaboration with us, including among others the Import Drug Registration for product(s) we promote and distribute in China. Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we may be required to obtain additional permissions or approvals for our business operations. For more details, see “Item 3. Key Information — D. Risk Factors — Risks Relating to Our Business Operations in China — The legal system in China embodies uncertainties which could impose additional requirements and obligations on our business, and PRC laws, rules, and regulations can evolve quickly with little advance notice, which may materially and adversely affect our business, financial condition, and results of operations.”

As the date hereof, we and our PRC subsidiaries (i) are not required to obtain permissions from the China Securities Regulatory Commission, or the CSRC, (ii) are not required to go through cybersecurity review by the Cyberspace Administration of China, or the CAC, and (iii) have not been asked to obtain or were denied such permissions by any PRC authority. On July 7, 2022, the CAC published the Guidelines for Data Export Security Assessment (《数据出境安全评估办法》) (the “Guidelines”), which took effect on September 1, 2022. Pursuant to the Guidelines, the data processor who intends to transfer certain important data or large volume of personal information outside of China shall complete a prior CAC-led data outbound transfer security assessment. However, as the Guidelines has just come into effect, there is no specific enforcement guidelines or interpretation for such security assessment, including what constitutes “important data”, or how to define “outbound transfer”, which results in uncertainties whether our business will be subject to such CAC-led assessment. For the data we accessed through or obtained from clinical trials, we have complied with the laws and regulations then-in-effective, and completed the registration with HGRAO, but it is unclear if we will be required to go through the CAC-led or CAC-involved security assessment or the current HGRAO registration procedure will be changed in the future. We will closely monitor and review any regulatory development and comply with any new approval or license requirement when necessary. If (i) we inadvertently conclude that such permissions or approvals are not required, or (ii) applicable laws, regulations, or interpretations change and we are required to obtain such permissions or approvals in the future, we may have to expend significant time and costs to procure them. If we are unable to do so, on commercially reasonable terms, in a timely manner or otherwise, we may become subject to sanctions imposed by the PRC regulatory authorities, which could include fines and penalties, proceedings against us, and other forms of sanctions, and our ability to conduct our business, invest into China as foreign investments or accept foreign investments, or be listed on a U.S. or other overseas exchange may be restricted, and our business, reputation, financial condition, and results of operations may be materially and adversely affected.

On February 17, 2023, the CSRC released the Trial Administrative Measures of the Overseas Securities Offering and Listing by Domestic Companies (《境内企业境外发行证券和上市管理试行办法》) and five ancillary interpretive guidelines (collectively, the “Overseas Listing Trial Measures”), which apply to overseas offerings and listing by PRC-based companies, or domestic companies, of equity shares, depository receipts, corporate bonds convertible to equity shares, and other equity securities, and came into effect on March 31, 2023. According to the Overseas Listing Trial Measures, (1) domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedure and report relevant information to the CSRC, and if a overseas-listed PRC-based issuer issues new securities in the same overseas market after the overseas offering and listing, it is also required to file with the CSRC within three business days after the completion of the issuance; if a domestic company fails to complete the filing procedure or conceals any material fact or falsifies any major content in its filing documents, such domestic company may be subject to administrative penalties, such as order to rectify, warnings, fines, and its controlling shareholders, actual controllers, the person directly in charge and other directly liable persons may also be subject to administrative penalties, such as warnings and fines; (2) if a foreign-incorporated issuer meets both of the following conditions, its overseas offering and listing shall be determined as an indirect overseas offering and listing by a domestic company of the PRC: (i) any of the total assets, net assets, revenues or profits of the domestic operating entities of the issuer in the most recent accounting year accounts for more than 50% of the corresponding line items in the issuer’s audited consolidated financial statements for the same period; and (ii) its major operational activities are carried out in China or its main places of business are located in China, or the senior managers in charge of operation and management of the issuer are mostly Chinese citizens or are domiciled in China; and (3) where a domestic company seeks to indirectly offer and list securities in an overseas market

9

(including issuance of new securities after its overseas offering and listing), the issuer shall designate a major domestic operating entity responsible for all filing procedures with the CSRC.

Furthermore, in case any of the following major events occurs after the overseas offering and listing, the issuer is also required to report the relevant information to the CSRC within three business days of the occurrence and the announcement of the relevant events: (1) change of control; (2) the foreign securities regulatory body or the relevant competent authority has taken such measures as investigation and punishment; (3) conversion of listing status or listing board; and (4) voluntary of compulsory termination of listing. Where there is any material change in the major business and operation of the issuer after overseas offering and listing, and such change does not fall within the scope of filing, the issuer shall, within three business days of the occurrence of such change, submit a special report and a legal opinion issued by a domestic law firm to the CSRC to explain the relevant situation.

As substantially all of our operations are currently based in the PRC, our future offerings and major changes shall be subject to the foregoing filing procedures under the Overseas Listing Trial Measures. We cannot assure you that we could meet such requirements, obtain such permit from the relevant government authorities, or complete such filing in a timely manner or at all. Any failure may significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. In addition, as the Overseas Listing Trial Measures was recently promulgated, there remains substantial uncertainties as to its interpretation and implementation and how it may impact our ability to raise or utilize fund and business operation.

A. | [Reserved] |

B. | Capitalization and Indebtedness |

Not applicable.

C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

D. | Risk Factors |

Risks Relating to our Financial Position and Need for Additional Capital

We have incurred significant operating losses since inception and anticipate that we will continue to incur operating losses for the foreseeable future and may never achieve or maintain profitability.

To date, we have been engaged primarily in research and development activities. In the years ended December 31, 2021, 2022 and 2023, we had EVOMELA® sales totaling US$30.0 million, US$38.0 million and US$33.9 million, respectively.

We have experienced losses in each year since inception. Through December 31, 2023, we had an accumulated deficit of US$660.8 million. We expect that we will seek to raise capital to continue our operations and, although we have been successfully funded to date through the sales of our equity securities, our capital-raising efforts may not produce the funding needed to sustain our operations. If we are unable to obtain additional funding for operations, we may not be able to continue operations as proposed, requiring us to modify our business plan, curtail various aspects of our operations or cease operations. In any such event, investors may lose a portion or all of their investment.

We expect that our ongoing preclinical, clinical, marketing and corporate activities will result in operating losses for the foreseeable future. In addition, to the extent we rely on others to develop and commercialize our products, our ability to achieve profitability will depend upon the success of these other parties. To support our research and development of certain product candidates, we may seek and rely on cooperative agreements from governmental and other organizations as a source of support. If a cooperative agreement were to be reduced to any substantial extent, it may impair our ability to continue our research and development efforts. To become and remain profitable, we must successfully commercialize one or more product candidates with significant market potential. This will require us to be successful in a range of challenging activities, including completing clinical trials of our candidates, developing commercial scale manufacturing processes, obtaining marketing approval, manufacturing, marketing and selling any current and future

10

product candidates for which we may obtain marketing approval, and satisfying any post-marketing requirements. We may never succeed in any or all of these activities and, even if we do, we may never generate sufficient revenue to achieve profitability.

We may not have sufficient funds to acquire new product candidates or pay milestone payments.

Our growth strategy relies on our in-license of new product candidates from third parties. Our pipeline will be dependent upon the availability of suitable acquisition candidates at favorable prices and upon advantageous terms and conditions. Even if such opportunities are present, we may not be able to successfully identify appropriate acquisition candidates. Moreover, other companies, many of which may have substantially greater financial resources, are competing with us for the right to acquire such product candidates.

If a product candidate is identified, the third parties with whom we seek to cooperate may not select us as a potential partner or we may not be able to enter into arrangements on commercially reasonable terms or at all. Furthermore, the negotiation and completion of collaborative and license arrangements could cause significant diversion of management’s time and resources and potential disruption of our ongoing business.

Our ability to make additional payments in the future for CASI Wuxi is subject to uncertainty, be difficult to accomplish or take longer than expected. We have established a cGMP injectable products manufacturing line in a state-owned industrial facility in Wuxi Huishan Economic Development Zone and it may fail to meet regulatory standard, which may increase our losses.

We have established a cGMP injectable products manufacturing line in a state-owned industrial facility in Wuxi Huishan Economic Development Zone. The injectable products manufacturing line may fail for validation or to meet regulatory standards for authority’s inspection prior to the commercial manufacture. Our ability to establish and operate a manufacturing facility in China may be adversely affected by changes in Chinese laws and regulations such as those related to, among other things, taxation, import and export tariffs, environmental regulations, land use rights, intellectual property, employee benefits and other matters. The success of CASI Wuxi also relies on our ability to make additional payments in the future, which is uncertain. Our plan may require us to obtain additional debt or equity financing, resulting in additional debt obligations, increased interest expense or dilution of equity ownership. If we are unable to establish a new manufacturing facility, purchase equipment, hire an adequate number of experienced personnel to support our manufacturing efforts or implement necessary process improvements, we may be unable to produce commercial materials or meet demand, if any should develop, for our product candidates. Any one of the factors cited above, or a combination of them, could result in unanticipated costs, which could materially and adversely affect our business and planned operations and earnings in China. In addition, our investment plan in connection with the operation of CASI Wuxi has been changed and remains subject to changes due to factors beyond our control, and our ability to make additional payments is subject to uncertainty, see “Risks replating Our Business — The success of CASI Wuxi is subject to uncertainty in our business plan and government regulatory actions. ”

The current capital and credit market conditions may adversely affect our access to capital, cost of capital, and ability to execute our business plan as scheduled.

Access to capital markets is critical to our ability to operate. Traditionally, we have funded our operations by raising capital in the equity markets. Declines and uncertainties in these markets over the past few years have restricted raising new capital in amounts sufficient to conduct our current operations and have affected our ability to continue to expand or fund additional development efforts. We require significant capital for research and development for our product candidates, clinical trials, and marketing activities. Our inability to access the capital markets on favorable terms because of our low stock price, or upon our delisting from the Nasdaq Capital Market if we fails to satisfy a listing requirement, could affect our ability to execute our business plan as scheduled. Moreover, we rely and intend to rely on third parties, including our clinical research organizations, third party manufacturers, and certain other important vendors and consultants. As a result of the current volatile and unpredictable global economic situation, there may be a disruption or delay in the performance of our third-party contractors and suppliers. If such third parties are unable to adequately satisfy their contractual commitments to us in a timely manner, our business could be adversely affected.

We have limited revenue streams and we are uncertain whether additional funding will be available for our future capital needs and commitments. If we cannot raise additional funding, or access the capital markets, we may be unable to complete the development and commercialization of our products and product candidates.

We will require substantial funds in addition to our existing working capital to develop and commercialize our products and product candidates and to otherwise meet our business objectives. We have never generated sufficient revenue during any period since

11

our inception to cover our expenses and have spent, and expect to continue to spend, substantial funds to continue our clinical development programs and commercialization of our products and product candidates. Any one of the following factors, among others, could cause us to require additional funds or otherwise cause our cash requirements in the future to increase materially:

| ● | progress of our clinical trials or correlative studies; |

| ● | results of clinical trials; |

| ● | changes in or terminations of our relationships with strategic partners; |

| ● | changes in the focus, direction, or costs of our research and development programs; |

| ● | competitive and technological advances; |

| ● | establishment and expansion of marketing and sales capabilities; |

| ● | manufacturing; |

| ● | the regulatory approval process; or |

| ● | product launch and distribution. |

On December 31, 2023, we had cash and cash equivalents of US$17.1 million, and short term investments of US$12.0 million. We may continue to seek additional capital through public or private financing or collaborative agreements in 2024 and beyond. Our operations require significant amounts of cash. We may be required to seek additional capital for the future growth and development of our business. We can give no assurance as to the availability of such additional capital or, if available, whether it would be on terms acceptable to us. If we are not successful in obtaining sufficient capital because we are unable to access the capital markets on favorable terms, it could reduce our research and development efforts and materially adversely affect our future growth, results of operations and financial results. There can be no assurance that we would be able to obtain any required financing on a timely basis or at all.

Risks Relating to Our Business

If we or our partners are ultimately unable to obtain regulatory approval for our drug candidates, our business will be substantially harmed.

The time required to obtain approval by the FDA and the NMPA is unpredictable and typically takes many years following the commencement of preclinical studies and clinical trials and depends on numerous factors, including the substantial discretion of the regulatory authorities.

Our drug candidates could be delayed or fail to receive regulatory approval for many reasons, including:

| ● | failure to begin or complete clinical trials due to disagreements with regulatory authorities; |

| ● | delays in subject enrollment or interruptions in clinical trial supplies or investigational product; |

| ● | failure to demonstrate that a drug candidate is safe and effective or that a biologic candidate is safe, pure, and potent for its proposed indication; |

| ● | failure of clinical trial results to meet the level of statistical significance required for approval; |

| ● | reporting or data integrity issues related to our clinical trials; |

| ● | disagreement with our interpretation of data from preclinical studies or clinical trials; |

| ● | changes in approval policies or regulations that render our preclinical and clinical data insufficient for approval or require us to amend our clinical trial protocols; |

| ● | regulatory requests for additional analyses, reports, data, nonclinical studies and clinical trials, or questions regarding interpretations of data and results and the emergence of new information regarding our drug or biologic candidates or other products; |

| ● | regulatory orders new side effect warnings for existing therapies; |

| ● | failure to satisfy regulatory conditions regarding endpoints, patient population, available therapies and other requirements for our clinical trials in order to support marketing approval on an accelerated basis or at all; |

| ● | our failure to conduct a clinical trial in accordance with regulatory requirements or our clinical trial protocols; and |

| ● | clinical sites, investigators or other participants in our clinical trials deviating from a trial protocol, failing to conduct the trial in accordance with regulatory requirements, or dropping out of a trial. |

12

The FDA, NMPA or a comparable regulatory authority may require more information, including additional preclinical, chemical, manufacturing and controls, and/or clinical data, to support approval, which may delay or prevent approval and our commercialization plans, or we may decide to abandon the development program.

Changes in regulatory requirements and guidance may also occur, and we may need to amend clinical trial protocols submitted to applicable regulatory authorities to reflect these changes. Amendments may require us to resubmit clinical trial protocols to IRBs or ethics committees for re-examination, which may impact the costs, timing or successful completion of a clinical trial.

If we or our partners experience delays in the completion of, or the termination of, a clinical trial of any of our product candidates, the commercial prospects of that candidate may be harmed, and our ability to generate product sales revenues from any of those candidates may be delayed. In addition, any delays in completing our clinical trials will increase our costs, slow down our candidate development and approval process, and jeopardize our ability to commence product sales and generate related revenues for that candidate. Any of these occurrences may harm our business, financial condition and prospects significantly. In addition, many of the factors that cause, or lead to, a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of regulatory approval of our product candidates.

Our success in commercializing these drugs and biologics may be inhibited by a number of factors, including:

| ● | our inability to maintain good collaboration relationship with our partners; |

| ● | our inability to obtain/maintain regulatory approvals; |

| ● | our inability to recruit, train and retain adequate numbers of effective sales and marketing personnel; |

| ● | the inability of sales personnel to obtain access to or educate physicians on the benefits of our products; |

| ● | our lack of experience in manufacturing drugs for commercial sales; |

| ● | our or our partners’ inability to secure widespread acceptance of our products from physicians, healthcare payors, patients and the medical community; |

| ● | our ability to win tenders through the collective tender processes in which we decide to participate; |

| ● | the lack of complementary products to be offered by sales personnel, which may put us at a competitive disadvantage relative to companies with more extensive product lines; |

| ● | unforeseen costs and expenses associated with creating an independent sales and marketing organization; |

| ● | generic and biosimilar competition; and |

| ● | regulatory exclusivities or patents held by competitors that may inhibit our products’ entry to the market. |

If we decide to rely on third parties to manufacture, sell, market and distribute our products and product candidates, we may not be successful in entering into arrangements with such third parties or may be unable to do so on terms that are favorable to us. In addition, our product revenues and our profitability, if any, may be lower if we rely on third parties for these functions than if we were to market, sell and distribute any products that we develop ourselves. We likely will have little control over such third parties, and any of them may fail to devote the necessary resources and attention to sell and market our products effectively. If we do not establish sales, marketing and distribution capabilities successfully, either on our own or in collaboration with third parties, we will not be successful in commercializing our product candidates, which would adversely affect our business and financial condition.

We are substantially dependent on the commercial success of EVOMELA®, FOLOTYN® and CNCT19. Our approved medical products may fail to achieve and maintain the degree of market acceptance and utilization by physicians, patients, third-party payors, and others in the medical community necessary for commercial success.

| ● | EVOMELA® |

The success of our business is substantially dependent on our ability to successfully commercialize EVOMELA®. On December 3, 2018, we received the NMPA approval for importation, marketing and sales in China for EVOMELA®, and on August 12, 2019, we announced the commercial launch of EVOMELA® in China. We will continue to spend our time, resources and efforts on the commercialization of EVOMELA® in China.

13

Reimbursement and hospital listing may be the most critical market access factors for our commercialization success in China. The National Reimbursement Drug List (the “NRDL”) is updating on an annual basis via a negotiation mechanism. Although participating in the NRDL pricing negotiation is voluntarily, it usually results in significant price discount. The Company has no intention to list EVOMELA® in the NRDL any time before a direct competitor’s compound commercially launch, therefore, our market will be limited given only a small portion of the Chinese population would be able to afford EVOMELA® through self-pay.

The government owned hospitals in China usually restrict the drug use outside the hospital formulary. Therefore, being listed in the hospital formulary is critical. In order to list in the hospital formulary, the Company must participate the provincial level tendering process. Winning the tendering does not guarantee the hospital listing. If we were unable to quickly add EVOMELA® to hospitals’ formulary, doctors and patients will have limited access to EVOMELA® through hospital pharmacies, and the demand for EVOMELA® and the revenues from EVOMELA® will be materially and adversely affected. On the other hand, patients are able to purchase EVOMELA® with a prescription from a physician from pharmacies if the product is not available in the hospital, however, the hospitals do not encourage such activities.

The introduction of a generic melphalan for injection product in China represents a significant business risk for EVOMELA®, potentially eroding its market share in the region. Generic medications, often priced more competitively than their branded counterparts, can quickly attract cost-conscious customers, institutions and healthcare providers, leading to a decrease in sales for the branded product. Furthermore, the situation is compounded by the news that another local company is in the process of registering its injectable melphalan, with a potential market launch in 2025. This impending competition not only threatens to further dilute EVOMELA®'s market presence but also intensifies the pressure on pricing and marketing strategies.

Additionally, we currently rely on a single source for our supply of EVOMELA® which has high risk of supply chain disruption. Early in the COVID-19 pandemic we experienced a disruption to our supply chain for EVOMELA®, and there can be no assurance that restrictions will not be imposed again. If suppliers refuse or are unable to provide products for any reason (including the occurrence of an event like the COVID-19 pandemic that makes delivery impractical), we would have to work with Acrotech, our current supplier, to negotiate an agreement with a substitute supplier, which would likely interrupt further manufacturing of EVOMELA®, cause delays or increase our costs.

| ● | FOLOTYN® |

In July 2023, we entered into a tripartite assignment agreement with Mundipharma International Corporation Limited (“MICL”), Mundipharma Medical Company (“MMCo”) and Acrotech Biopharma Inc. (“Acrotech Inc.”), pursuant to which, MICL’s rights and obligations under that certain License, Development and Commercialization Agreement (as amended and restated) dated as of May 29, 2013 for the commercialization of FOLOTYN® (Pralatrexate) in China, with certain terms of such rights and obligations amended as agreed to by the parties, is assigned to us. We announced the first patient received FOLOTYN® treatment in China on February 15, 2024. We will continue to spend our time, resources and efforts on the commercialization of FOLOTYN® in China.

Securing reimbursement and hospital listings are key to our commercial success in China. The NRDL is updated annually through a negotiation process. While joining the NRDL pricing negotiations is optional, it typically leads to substantial price reductions. Our strategy does not include listing FOLOTYN® on the NRDL until a direct competitor's product is launched commercially. Consequently, our market reach will be restricted as only a limited segment of the Chinese population will be able to afford FOLOTYN® out of pocket.

In China, drugs not listed in a hospital's formulary are often restricted, making formulary inclusion essential. To achieve this, a company must successfully navigate the provincial tender process, though winning does not guarantee formulary listing. If FOLOTYN® is not promptly added to hospital formularies, its availability and demand, as well as revenue, could suffer significantly. While patients can technically obtain FOLOTYN® with a prescription at external pharmacies, hospitals discourage this practice.

We also currently rely on a single source for our supply of FOLOTYN® which has high risk of supply chain disruption. If suppliers refuse or are unable to provide products for any reason (including the occurrence of an event like the COVID-19 pandemic that makes delivery impractical), we would have to work with Acrotech, our current supplier, to negotiate an agreement with a substitute supplier, which would likely interrupt further manufacturing of FOLOTYN®, cause delays or increase our costs.

14

| ● | CNCT19 (Inaticabtagene Autoleucel) |

On November 8, 2023, our partner Juventas, a China-based domestic company engaged in cell therapy, announced market approval for CNCT19 in China from NMPA. The Company acquired in June 2019 worldwide license and commercialization rights to CNCT19 from Juventas pursuant to certain Exclusive License Agreement, which provides that Juventas shall continue to be responsible for the clinical development and regulatory submission and maintenance of CNCT19 regulatory applications and we are responsible for the launch and commercial activities of CNCT19 under the direction of a joint steering committee. In September 2020, the Company and Juventas entered a Supplementary Agreement (together with the Exclusive License Agreement, collectively, “CNCT19 Agreements”), pursuant to which Juventas and the Company will jointly market CNCT19, including, but not limited to, establishing medical teams, developing medical strategies, conducting post-marketing clinical studies, establishing Standardized Cell Therapy Centers, establishing and training providers with respect to cell therapy, testing for cell therapy, and monitoring quality controls (cell collection and transfusion, etc.), and patient management (adverse reactions treatment, patients’ follow-up visits, and establishment of a database). The Company also will reimburse Juventas for a portion of Juventas’ marketing expenses as reviewed and approved by a joint commercial committee to be constituted. The Company will continue to be responsible for recruiting and establishing a sales team to commercialize CNCT19.

The affordability and accessibility of CNCT19, the lowest-priced CAR-T therapy in China, are significant barriers to its widespread adoption in a predominantly self-pay healthcare market. Despite its competitive pricing, the cost of RMB 999,000 may still be prohibitively high for many patients, limited further by the variability in health insurance coverage and the economic disparities across different regions of China. These factors collectively restrict the pool of eligible patients, as high out-of-pocket expenses, insufficient insurance reimbursement, and lack of financial support mechanisms make access to this potentially life-saving treatment challenging. Addressing these issues through strategic pricing, enhanced insurance partnerships, and the establishment of financial aid programs is crucial for improving the accessibility and uptake of CNCT19 among the target patient population. Another risk factor for CNCT19 is its exclusion from the NRDL in the foreseeable future, which poses a considerable barrier to its accessibility. The NRDL in China plays a crucial role in determining which drugs are more affordable to the general population through insurance coverage. Without inclusion in the NRDL, CNCT19's out-of-pocket cost for patients remains high, severely limiting its accessibility to only those who can afford it without financial assistance from public health insurance. This exclusion not only restricts the patient base able to benefit from this advanced therapy but also places CNCT19 at a competitive disadvantage compared to treatments that are covered by the NRDL. Consequently, strategies to mitigate this limitation might include advocating for policy changes, exploring alternative financing models, or implementing patient assistance programs to enhance access despite the lack of NRDL coverage.

The slow acceptance and awareness among doctors of new therapies like CNCT19 present significant risks to its market penetration and sales. Physicians’ hesitation, driven by the need for convincing efficacy, safety data, and familiarity with the treatment, can delay its integration into standard care practices. This challenge is compounded by the necessity for specialized training to administer such advanced therapies. Overcoming these barriers requires targeted educational efforts, dissemination of clinical trial results, and collaboration with key medical opinion leaders to foster a quicker adoption process and enhance CNCT19’s market presence.

The side effects of cell therapy like CNCT19 can elevate the risk of financial compensation claims, impacting the company financially and reputationally. Adverse reactions from patients may lead to increased legal and insurance costs, as well as the need for financial reserves for compensation, posing significant financial risks.

Juventas' limited manufacturing capacity restricts its ability to meet market demand, potentially capping revenue growth and market share. This limitation could result in supply shortages and loss of opportunities to competitors.

Juventas serving as the sole supplier and business partner for CNCT19 introduces a significant risk to the Company’s business strategy. Should Juventas refuse to carry out the Exclusive License Agreement and the Supplementary Agreement, it could severely disrupt the Company’s supply chain, impacting the availability of CNCT19 and, by extension, the Company’s ability to meet market demand. This dependency on a single entity for critical aspects of the business makes us vulnerable to operational and strategic risks, potentially leading to revenue loss, market share decline, and damage to stakeholder relationships.

15

We are involved in arbitration proceedings against Juventas in relation to Juventas’ purported termination of the CNCT19 Agreements.

On March 2, 2024, CASI received a notice from Juventas, which purported to terminate the CNCT19 Agreements based on certain alleged non-performance by CASI of its obligations under the CNCT19 Agreements in relation to the preparation for the commercialization of CNCT19. CASI responded to Juventas’ purported termination notice, noting that Juventas was not entitled to unilaterally terminate the CNCT19 Agreements and further demanding that Juventas cease any conduct that may constitute further breach of the CNCT19 Agreements and execute a written undertaking regarding compliance with the CNCT19 Agreements by March 13, 2024. Juventas did not comply with CASI’s demands. On March 20, 2024, CASI submitted a Notice of Arbitration at the Hong Kong International Arbitration Centre (“HKIAC”) against Juventas pursuant to the CNCT19 Agreements’ dispute resolution clauses, claiming that Juventas’ purported termination was invalid and that Juventas breached the CNCT19 Agreements and seeking, among other things, damages and injunctive reliefs. Together with the Notice of Arbitration, CASI also submitted an application for the appointment of an emergency arbitrator, seeking emergency injunctive reliefs. On the same day, Juventas also submitted a Notice of Arbitration at the HKIAC against CASI, alleging, among other things, that the CNCT19 Agreements were validly terminated and that CASI breached the CNCT19 Agreements. The HKIAC has appointed an emergency arbitrator in accordance with CASI’s application. The arbitration proceedings are ongoing. See “—” “Item 8 — Financial Information — A. Consolidated Statements and Other Financial Information – Legal Proceedings”.

The arbitration proceedings are in their early stages and the Company cannot predict right now the outcome of either of these proceedings. If we do not prevail in either of these proceedings completely or in part, or fail to reach a favorable settlement with Juventas, our plan with respect to the commercialization of CNCT 19 may be delayed or otherwise adversely impacted, which will in turn result in adverse impacts on our results of operations, financial condition and prospects

The success of CASI Wuxi is subject to uncertainty in our business plan and government regulatory actions.

In December 2018, together with our partner Wuxi LP, we established CASI Wuxi, to build and operate a manufacturing facility in the Wuxi Huishan Economic Development Zone in Jiangsu Province, China. We initially held 80% of the equity interests in CASI Wuxi and intended to invest, over time, US$80 million in CASI Wuxi. We have paid US$31 million in cash and transferred selected ANDAs. Wuxi LP held 20% of the equity interest in CASI Wuxi through its investment paid in RMB equivalent of US$20 million in cash in 2019.

In November 2019, CASI Wuxi entered into a lease agreement for the right to use state-owned land in Wuxi for the construction of a manufacturing facility. Pursuant to this agreement, CASI Wuxi intended to invest in land use rights and property, plant and equipment of RMB1 billion by August 2022. Construction of the manufacturing facility began in the fourth quarter of 2020.

Since our business focus has been shifted from ANDAs to the hematology-oncology therapeutic area, a substantial investment in GMP manufacturing facilities does not fit the current business focus. Therefore, in December 2022, we returned the land use right to the local Wuxi government for an amount of RMB 44.42 million, equivalent to the original payment for the land use right. Meanwhile, all construction in progress on the land was disposed. The Company recorded a total disposal loss amounted to US$2.2 million.

Since we failed to meet the land development milestone, the local land administration authority requested CASI Wuxi to pay a land vacancy fee equivalent to 20% of the price for the land use rights according to the PRC Land Administration Law. We paid such fee in the amount of RMB 8.88 million to the local land administration authority in December 2022. Additionally, the Company received a government grant for the land development in April 2020 and November 2021, respectively, in the total amount of RMB 18.9 million. We are currently in negotiation with the local Wuxi government on the further treatment of the grant. The Wuxi government may require the Company to fully or partially return the grant and the Company may incur further losses.

CASI Wuxi is now operating a cGMP injectable products manufacturing line in a state-owned industrial facility in Wuxi Huishan Economic Development Zone. The injectable products manufacturing line may fail for validation or to meet regulatory standards for authority’s inspection prior to the commercial manufacture.

In December 2023, the Company entered into a series of agreements, including a capital reduction agreement, a long term borrowing agreement, and four guarantee agreements, with Wuxi LP, CASI China and CASI Wuxi, pursuant to which, (i) CASI Wuxi will reduce its registered capital and return to Wuxi LP the investment principal made by Wuxi LP in CASI Wuxi in the amount of

16

RMB134.2 million (equivalent to its original investment of US$20 million, the “Investment Principal”), together with certain investment return in the amount of RMB26.2 million to be paid in instalments, and Wuxi LP shall cease to be a shareholder of CASI Wuxi, (ii) Wuxi LP shall reinvest the Investment Principal into a three-year long term borrowing to CASI Wuxi (the “Long term borrowing”), which shall have a non-compounding annual interest rate of 4.05% and can, from the beginning date of the Long term borrowing term till the six month anniversary after the maturity of the Long term borrowing, be partially or fully converted into the equity interest of any subsidiaries of the Company at the conversion date fair value, solely at Wuxi LP’s discretion, and (iii) each of the Company and CASI China will provide irrevocable joint and several liability guarantees on the above-mentioned payment obligations. The term of the Long term borrowing will start on December 25, 2023 and end on December 31, 2026.

The provision allowing Wuxi LP to request immediate repayment of the long term borrowing if CASI Wuxi fails to generate revenue for certain threshold for each of the years during the term, which represents a significant liquidity risk for CASI. If Wuxi LP exercises this option, CASI would be required to allocate a substantial portion of its cash reserves or secure additional financing, which could severely impact its operational cash flow. Converting the investment principal into a three-year long term borrowing introduces uncertainties related to future equity dilution and financial stability.

The existence of counterfeit pharmaceutical products in pharmaceutical markets may compromise our brand and reputation and have a material adverse effect on our business, operations and prospects.

Counterfeit products, including counterfeit pharmaceutical products, are a significant problem, particularly in China. Counterfeit pharmaceuticals are products sold or used for research under the same or similar names, or similar mechanism of action or product class, but which are sold without proper licenses or approvals. Such products may be used for indications or purposes that are not recommended or approved or for which there is no data or inadequate data with regard to safety or efficacy. Such products divert sales from genuine products, often are of lower cost, often are of lower quality (having different ingredients or formulations, for example), and have the potential to damage the reputation for quality and effectiveness of the genuine product. If counterfeit pharmaceuticals illegally sold or used for research result in adverse events or side effects to consumers, we may be associated with any negative publicity resulting from such incidents. Consumers may buy counterfeit pharmaceuticals that are in direct competition with our pharmaceuticals, which could have an adverse impact on our revenues, business and results of operations. In addition, the use of counterfeit products could be used in non-clinical or clinical studies, or could otherwise produce undesirable side effects or adverse events that may be attributed to our products as well, which could cause us or regulatory authorities to interrupt, delay or halt clinical trials and could result in the delay or denial of regulatory approval by the FDA or other regulatory authorities and potential product liability claims. With respect to China, although the government has combat the counterfeit pharmaceuticals, there is not yet an effective counterfeit pharmaceutical regulation control and enforcement system in China. As a result, we may not be able to prevent third parties from selling or purporting to sell our products in China. The proliferation of counterfeit pharmaceuticals has grown in recent years and may continue to grow in the future. The existence of and any increase in the sales and production of counterfeit pharmaceuticals, or the technological capabilities of counterfeiters, could negatively impact our revenues, brand reputation, business and results of operations.

We face significant competition from other biotechnology and pharmaceutical companies and our business will suffer if we fail to compete effectively.

If competitors were to develop superior drug candidates, our products could be rendered noncompetitive or obsolete, resulting in a material adverse effect to our business. Developments in the biotechnology and pharmaceutical industries are expected to continue at a rapid pace. Success depends upon achieving and maintaining a competitive position in the development of products and technologies. Competition from other biotechnology and pharmaceutical companies can be intense. Many competitors have substantially greater research and development capabilities, marketing, financial and managerial resources and experience in the industry.

The availability of our competitors’ products could limit the demand, and the price we are able to charge, for product candidates we develop. We will not achieve our business plan if the acceptance of our products is inhibited by price competition or reimbursement issues or if physicians switch to other new drug products or choose to reserve our product candidates for use in limited circumstances. The inability to compete with existing or subsequently introduced drug products would have a material adverse impact on our business, financial condition and prospects.

17

We may need new collaborative partners to further develop and commercialize products, and if we enter into such arrangements, we may lose control over the development and approval process.

We may develop and commercialize our product candidates both with and without corporate alliances and partners. Nonetheless, we intend to explore opportunities for new corporate alliances and partners to help us develop, commercialize and market our product candidates. We may grant to our partners certain rights to commercialize any products developed under these agreements, and we may rely on our partners to conduct research and development efforts and clinical trials on, obtain regulatory approvals for, and manufacture and market any products licensed to them. Each individual partner will seek to control the amount and timing of resources devoted to these activities generally. We anticipate obtaining revenues from our strategic partners under such relationships in the form of research and development payments and payments upon achievement of certain milestones. Since we generally expect to obtain a royalty for sales or a percentage of profits of products licensed to third parties, our revenues may be less than if we retained all commercialization rights and marketed products directly. In addition, there is a risk that our corporate partners will pursue alternative technologies or develop competitive products as a means for developing treatments for the diseases targeted by our product candidates.

We may not be successful in establishing any collaborative arrangements. Even if we do establish such collaborations, we may not successfully commercialize any products under or derive any revenues from these arrangements. There is a risk that we will be unable to manage simultaneous collaborations, if any, successfully. With respect to existing and potential future strategic alliances and collaborative arrangements, we will depend on the expertise and dedication of sufficient resources by these outside parties to develop, manufacture, or market products. If a strategic alliance or collaborative partner fails to develop or commercialize a product to which it has rights, we may not recognize any revenues on that particular product.

We must show the safety and efficacy of our product candidates through clinical trials, the results of which are uncertain.

Before obtaining regulatory approvals for the commercial sale of our products, we must demonstrate, through preclinical studies (animal testing) and clinical trials (human testing), that our proposed products are safe and effective for use in each target indication. Testing of our product candidates will be required, and failure can occur at any stage of testing. Clinical trials may not demonstrate sufficient safety and efficacy to obtain the required regulatory approvals or result in marketable products. The failure to adequately demonstrate the safety and efficacy of a product under development could delay or prevent regulatory approval of the potential product.

Clinical trials for the product candidates we are developing may be delayed by many factors, including that potential patients for testing are limited in number. The failure of any clinical trials to meet applicable regulatory standards could cause such trials to be delayed or terminated, which could further delay the commercialization of any of our product candidates. Newly emerging safety risks observed in animal or human studies also can result in delays of ongoing or proposed clinical trials. Any such delays will increase our product development costs. If such delays are significant, they could negatively affect our financial results and the commercial prospects for our products.

Compliance with ongoing post-marketing obligations for our approved products may uncover new safety information that could give rise to a product recall, updated warnings, or other regulatory actions that could have an adverse impact on our business.

After the FDA approves a drug or biologic for marketing, the product’s sponsor must comply with several post-marketing obligations that continue until the product is discontinued. These post-marketing obligations include the reporting of adverse events to the agency within specified timeframes, the submission of product-specific annual reports that include changes in the distribution, manufacturing, and labeling information, and notification when a drug product is found to have significant deviations from its approved manufacturing specifications (among others). Our ongoing compliance with these types of mandatory reporting requirements could result in additional requests for information from the FDA and, depending on the scope of a potential product issue that the FDA may decide to pursue, potentially also result in a request from the agency to conduct a product recall or to strengthen warnings and/or revise other label information about the product. The FDA may also require or request the withdrawal of the product from the market. Any of these post-marketing regulatory actions could materially affect our sales and, therefore, have the potential to adversely affect our business, financial condition, results of operations and cash flows.

18

Undesirable adverse events caused by our medicines and drug candidates could interrupt, delay or halt clinical trials, delay or prevent regulatory approval, limit the commercial profile of an approved label, or result in significant negative consequences following any regulatory approval.

Undesirable adverse events ("AEs") caused by our medicines and drug candidates could cause us or regulatory authorities to interrupt, delay or halt clinical trials and could result in a more restrictive label or the delay or denial of regulatory approval, or could result in limitations or withdrawal following approvals. If the conduct or results of our trials or patient experience following approval reveal a high and unacceptable severity or prevalence of AEs, our trials could be suspended or terminated and regulatory authorities could order us to cease further development of, or deny approval of, our drug candidates or require us to cease commercialization following approval.

As is typical in the development of pharmaceutical products, drug-related AEs and serious AEs ("SAEs") have been reported in our clinical trials. Some of these events have led to patient deaths. Drug-related AEs or SAEs could affect patient recruitment or the ability of enrolled subjects to complete the trial and could result in product liability claims. Any of these occurrences may harm our reputation, business, financial condition and prospects significantly. In our periodic and current reports filed with the SEC and our press releases and scientific and medical presentations released from time to time we disclose clinical results for our drug candidates, including the occurrence of AEs and SAEs.

Potential products may subject us to product liability for which insurance may not be available or claims may exceed coverage.

The use of our potential products in clinical trials and the marketing of any pharmaceutical products may expose us to product liability claims. We have obtained a level of liability insurance coverage that we believe is adequate in scope and coverage for our current stage of development. However, our present insurance coverage may not be adequate to protect us from liabilities we might incur. In addition, our existing coverage will not be adequate as we further develop products and, in the future, adequate insurance coverage and indemnification by collaborative partners may not be available in sufficient amounts or at a reasonable cost. If a product liability claim or series of claims are brought against us for uninsured liabilities, or in excess of our insurance coverage, the payment of such liabilities could have a negative effect on our business and financial condition.

If we are unable to obtain both adequate coverage and adequate reimbursement from third-party payers for our products before the competitor’s product launch, our revenues and prospects for profitability will suffer.