UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________

FORM

______________________

OR

For the fiscal year ended

OR

For the transition period from __________________ to __________________.

OR

Date of event requiring this shell company report __________________.

Commission file number

______________________

(Exact name of Registrant as specified in its charter) |

Port Central S.A.

(Translation of Registrant’s name into English)

Republic of

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Facsimile: +

Email:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

______________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

| Trading Symbol |

| Name of each exchange on which registered |

|

|

* Not for trading, but only in connection with the registration of American Depositary Shares pursuant to the requirements of the New York Stock Exchange.

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Title of each class |

| Outstanding at December 31, 2022 |

Common shares, nominal value Ps.1.00 per share |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | ☒ | Non-accelerated filer | ☐ | Emerging growth company | ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (§ 15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ | by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes ☐ No ☐

TABLE OF CONTENTS

| 1 |

| ||

| 1 |

| ||

| 1 |

| ||

| 1 |

| ||

| 1 |

| ||

| 1 |

| ||

| 1 |

| ||

| 23 |

| ||

| 25 |

| ||

| 30 |

| ||

| 115 |

| ||

| 115 |

| ||

| 117 |

| ||

| 117 |

| ||

| 117 |

| ||

| 141 |

| ||

| 149 |

| ||

| 150 |

| ||

| 152 |

| ||

| 152 |

| ||

| 152 |

| ||

| 159 |

| ||

| 160 |

| ||

| 163 |

| ||

| 164 |

| ||

| 165 |

| ||

| 165 |

| ||

| 165 |

| ||

| 166 |

| ||

| 166 |

| ||

| 166 |

| ||

| 170 |

| ||

| 170 |

| ||

| 170 |

| ||

| 170 |

| ||

| 170 |

| ||

| 170 |

| ||

| 170 |

| ||

| 170 |

|

ii |

| 170 |

| ||

| 170 |

| ||

| 171 |

| ||

| 176 |

| ||

| 176 |

| ||

| 199 |

| ||

| 207 |

| ||

| 207 |

| ||

| 208 |

| ||

| 208 |

| ||

| 208 |

| ||

| 210 |

| ||

| 210 |

| ||

| 210 |

| ||

| 210 |

| ||

| 210 |

| ||

| 211 |

| ||

Material Modifications to the Rights of Security Holders and Use of Proceeds |

| 211 |

| |

| 211 |

| ||

| 212 |

| ||

| 212 |

| ||

| 212 |

| ||

| 213 |

| ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

| 213 |

| |

| On the tale below, it is described the share repurchases made during 2022: |

| 213 |

|

| 214 |

| ||

| 214 |

| ||

| 217 |

| ||

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

| 217 |

| |

| 217 |

| ||

| 217 |

| ||

| 218 |

|

iii |

CERTAIN DEFINITIONS

In this annual report, except where otherwise indicated or where the context otherwise requires:

| · | “Argentine Corporate Law” refers to Law No. 19,550, as amended; |

| · | “Authorized Generators” refers to electricity generators that do not have contracts in the term market in any of its methods; |

| · | “BCRA” refers to the Argentine Central Bank. |

| · | “BYMA” refers to Bolsas y Mercados Argentinos S.A.; |

| · | “CAMMESA” refers to Compañía Administradora del Mercado Mayorista Eléctrico Sociedad Anónima. See “Item 4.B, Business Overview- The Argentine Electric Power Sector-General Overview of Legal Framework-CAMMESA;” |

| · | “CNV” refers to the Comisión Nacional de Valores, the Argentine Securities Commission; |

| · | “COD” refers to Commercial Operation Date, the day in which a generation unit is authorized by CAMMESA (in Spanish, “Habilitación Comercial”) to sell electric energy through the grid under the applicable commercial conditions; |

| · | “CTM” refers to Centrales Térmicas Mendoza S.A.; |

| · | “CVO” refers to the thermal plant Central Vuelta de Obligado; |

| · | “CVO Agreement” refers to the Agreement for Project Management and Operation, Increase of Thermal Generation Availability and Adaptation of Remuneration for Generation 2008-2011” executed on November 25, 2010 among the Secretariat of Energy and Central Puerto along with other electric power generators; |

| · | “CVOSA” refers to Central Vuelta de Obligado S.A.; |

| · | “Ecogas” refers collectively to Distribuidora de Gas Cuyana (“DGCU”) and Distribuidora de Gas del Centro (“DGCE”); |

| · | “Spot Sales” previously known as “Energía Base,” refers to the regulatory framework established under Resolution SE No. 95/13, as amended, and, from February 2017 to February 2019, regulated by Resolution SEE No. 19/17, from March 2019 to January 2020, regulated by Resolution No. 1/19 of the Secretariat of Renewable Resources and Electric Market of the National Ministry of Economy, from February 2020 to January 2021 regulated by Resolution SEE No. 31/20, from February 2021 to January 2022 regulated by Resolution SEE No. 440/21, from February 2022 to August 2022 by Resolution SEE No. 238/22 and since September 2022 regulated by Resolution SEE No. 826/22. Further, as of February 2023, Resolution SEE No. 59/23 is also applicable as a complementary regulation for combined cycle facilities. See “Item 4.B, Business Overview-The Argentine Electric Power Sector;” |

| · | “Energía Plus” refers to the regulatory framework established under Resolution SE No. 1281/06, as amended. See “Item 4.B, Business Overview-The Argentine Electric Power Sector-Structure of the Industry-Energía Plus;” |

| · | “FODER” refers to Fondo para el Desarrollo de Energías Renovables (Fund for the Development of Renewable Energies). See “Item 4.B, Business Overview-The Argentine Electric Power Sector -Structure of the Industry-Renewable Energy Program;” |

| · | “FONINVEMEM” or “FONI” refers to the Fondo para Inversiones Necesarias que Permitan Incrementar la Oferta de Energía Eléctrica en el Mercado Eléctrico Mayorista (the Fund for Investments Required to Increase the Electric Power Supply) and similar programs, including the CVO Agreement. See “Item 4.B, Business Overview-The Argentine Electric Power Sector-Structure of the Industry-The FONINVEMEM and Similar Programs;” |

| · | “FONINVEMEM Plants” refers to the plants José de San Martín, Manuel Belgrano and Vuelta de Obligado; |

| · | “FX Market” refers to the foreign exchange market; |

| · | “HPDA” refers Hidroeléctrica Piedra del Águila S.A., the corporation that previously owned the Piedra del Águila plant; |

| · | “IEASA” refers to Integración Energética Argentina S.A.; |

| · | “IGCE” refers to Inversora de Gas del Centro S.A.; |

| · | “IGCU” refers to Inversora de Gas Cuyana S.A.; |

| · | “La Plata Plant Sale” refers to the sale of the La Plata plant to YPF EE, effective as of January 5, 2018. For further information on the La Plata Plant Sale, see “Item 4.A. History and development of the Company-La Plata Plant Sale;” |

| · | “La Plata Plant Sale Effective Date” is January 5, 2018. For further information on the La Plata Plant Sale Effective Date, see “Item 4.A. History and development of the Company-La Plata Plant Sale;” |

| · | “LPC” refers to La Plata Cogeneración S.A., the corporation that owned the La Plata plant prior to us; |

| · | “LVFVD” refers to liquidaciones de venta con fecha de vencimientos a definir, or receivables from CAMMESA without a fixed due date. See “Item 4.B, Business Overview-FONINVEMEM and Similar Programs;” |

| · | “MATER” refers to Term Market for Renewable Energy Resolution No. 281-E/17; |

| · | “PPA” refers to Power Purchase Agreements, power capacity and energy supply agreements for a defined period of time or energy quantity; |

| · | “Resolution No. 19/17” or “Res. SEE 19/17” refers to the Resolution No. 19/17 issued on February 2, 2017, by the Secretariat of Electric Energy of the National Ministry of Energy and Mining by which the Secretariat modified the remuneration scheme (for capacity and energy) applicable from February 1, 2017, to Authorized Generators (electricity generators which do not have contracts in the term market in any of its modalities) acting in the WEM |

| · | “Resolution SRRyME No. 1/19” refers to the Resolution No. 1/19 issued on March 1, 2019, by the Secretariat of Renewable Resources and Electric Markey of the National Ministry of Economy by which the Secretariat modified the remuneration scheme (for capacity and energy) applicable to Authorized Generators (electricity generators which do not have contracts in the term market in any of its modalities) acting in the WEM; |

iv |

| · | “Resolution 31/20” or “Res. 31/20” refers to the Resolution No. 31/20 issued on February 27, 2020, by the Secretariat of Energy of the National Ministry of Production Development by which the Secretariat modified the remuneration scheme (for capacity and energy) applicable from February 1, 2020, to Authorized Generators (electricity generators which do not have contracts in the term market in any of its modalities) acting in the WEM; |

| · | “Resolution 440/21” or “Res.440/21” refers to the Resolution No. 440/21 issued on May 21, 2021, by the Secretariat of Energy of the National Ministry of Economy by which the Secretariat modified the remuneration scheme (for capacity and energy) applicable from February 1, 2021, to Authorized Generators (electricity generators which do not have contracts in the term market in any of its modalities) acting in the WEM; |

| · | “Resolution 238/22” or “Res.238/22” refers to the Resolution No. 238/22 issued on April 18, 2022, by the Secretariat of Energy of the National Ministry of Economy by which the Secretariat modified the remuneration scheme (for capacity and energy) applicable from February 1, 2022, to Authorized Generators (electricity generators which do not have contracts in the term market in any of its modalities) acting in the WEM; |

| · | “Resolution 826/22” or “Res.826/22” refers to the Resolution No. 826/22 issued on December 12, 2022, by the Secretariat of Energy of the National Ministry of Economy by which the Secretariat modified the remuneration scheme (for capacity and energy) applicable from September 1, 2022, to Authorized Generators (electricity generators which do not have contracts in the term market in any of its modalities) acting in the WEM; |

| · | “Resolution 59/23” or “Res.59/23” refers to the Resolution No. 59/23 issued on February 5, 2023, by the Secretariat of Energy of the National Ministry of Economy by which the Secretariat modified the remuneration scheme (for capacity and energy) of Authorized Generators with combined cycle units acting in the WEM that have adhered to the agreement set forth in this resolution; |

| · | “SADI” refers to the Argentine Interconnection System; |

| · | “Sales under contracts” refers collectively to (i) term market sales of energy under contracts with private and public sector counterparties, (ii) sales of energy sold under the Energía Plus and (iii) sales of energy under the RenovAr Program; |

| · | “Spot market” refers to energy sold by generators to the WEM and remunerated by CAMMESA pursuant to the framework in place prior to the Spot Sales. See “Item 4.B, Business Overview-The Argentine Electric Power Sector-Structure of the Industry-Electricity Dispatch and Spot Market Pricing prior to Resolution SE No. 95/13;” |

| · | “T6” refers to Terminal 6 Industrial S.A., a company engaged in soybean crushing and biodiesel and refined glycerin production; |

| · | “YPF” refers to YPF S.A., Argentina’s state-owned oil and gas company; |

| · | “YPF EE” refers to YPF Energía Eléctrica S.A., a subsidiary of YPF; and |

| · | “WEM” refers to the Argentine Mercado Eléctrico Mayorista, the wholesale electric power market. See “Item 4.B, Business Overview-The Argentine Electric Power Sector-General Overview of Legal Framework-CAMMESA”. |

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Statements

We maintain our financial books and records and publish our consolidated financial statements (as defined below) in Argentine pesos, which is our functional currency. This annual report contains our audited consolidated financial statements as of December 31, 2022 and 2021 and for each of the years ended December 31, 2022, 2021, and 2020 (our “Audited Consolidated Financial Statements”), which were approved by our board of directors (our “Board of Directors”) on March 8, 2023.

We prepare our Audited Consolidated Financial Statements in Argentine pesos and in conformity with the IFRS as issued by the IASB.

In accordance with IAS 29, the restatement of the financial statements is necessary when the functional currency of an entity is the currency of a hyperinflationary economy. To define a hyperinflationary state, IAS 29 provides a series of non-exclusive guidelines that consist of (i) analyzing the behavior of the population, prices, interest rates and wages before the evolution of price indexes and the loss of the currency’s purchasing power, and (ii) as a quantitative characteristic, verifying if the three-year cumulative inflation rate approaches or exceeds 100%. Due to macroeconomic factors, the triennial inflation was above that figure in 2018 and Argentina has been considered hyperinflationary since July 1, 2018. Such conditions remained during 2020, 2021 and 2022. See “Risks Relating to Argentina-As of July 1, 2018, the Argentine Peso qualifies as a currency of a hyperinflationary economy and we are required to restate our historical financial statements to apply inflationary adjustments, which could adversely affect our results of operations and financial condition and those of our Argentine subsidiaries”.

Therefore, our Audited Consolidated Financial Statements included herein, including the figures for the previous periods (this fact not affecting the decisions taken on the financial information for such periods), and, unless otherwise stated, the financial information included elsewhere in this annual report, were restated to consider the changes in the general purchasing power of the functional currency of the Company (Argentine peso) pursuant to IAS 29 and General Resolution no. 777/2018 of the CNV. Consequently, the consolidated financial statements are stated in the current measurement unit as of December 31, 2022. The information included in our Audited Consolidated Financial Statements is not comparable to the consolidated financial statements previously published by us. For further information, see “Item 5.A. Operating Results-Factors Affecting our Results of Operations-Inflation” and Note 2.1.2 to our Audited Consolidated Financial Statements.

v |

We remind investors that we are required to file financial statements and other periodic reports with the CNV because we are a public company in Argentina. Investors can access our historical financial statements published in Spanish on the CNV’s website at www.cnv.gob.ar. The information found on the CNV’s website is not a part of this annual report. Investors are cautioned not to place undue reliance on our financial statements not included in this annual report.

Currency and Rounding

All references herein to “pesos,” “Argentine pesos” or “Ps”. are to Argentine pesos, the legal currency of Argentina. All references to “U.S. dollars,” “dollars” or “US$” are to U.S. dollars. All references to “SEK$” are to Swedish krona. A “billion” is a thousand million.

Solely for the convenience of the reader, we have translated certain amounts included in this annual report from pesos into U.S. dollars, unless otherwise indicated, using the seller rate for U.S. dollars quoted by the Banco de la Nación Argentina for wire transfers (divisas) as of December 31, 2022, of Ps.177.16 per US$1.00. The Federal Reserve Bank of New York does not report a noon buying rate for pesos. The U.S. dollar equivalent information presented in this annual report is provided solely for the convenience of the reader and should not be construed to represent that the peso amounts have been, or could have been or could be, converted into U.S. dollars at such rates or at any other rate. See “Item 3.A. Selected Financial Data-Exchange Rates”.

Certain figures included in this annual report and in the Audited Consolidated Financial Statements contained herein have been rounded for ease of presentation. Percentage figures included in this annual report have in some cases been calculated on the basis of such figures prior to rounding. For this reason, certain percentage amounts in this annual report may vary from those obtained by performing the same calculations using the figures in this annual report and in the consolidated financial statements contained herein. Certain other amounts that appear in this annual report may not sum due to rounding.

Market Share and Other Information

The information set forth in this annual report with respect to the market environment, market developments, growth rates and trends in the markets in which we operate is based on information published by the Argentine federal and local governments through the Instituto Nacional de Estadísiticas y Censos (the National Statistics and Census Institute, or “INDEC”), the Ministry of Interior, the Secretariat of Electric Energy, the Banco Central de la República Argentina (the “Argentine Central Bank,” or “Central Bank”) CAMMESA, the Dirección General de Estadística y Censos de la Ciudad de Buenos Aires (General Directorate of Statistics and Census of the City of Buenos Aires) and the Dirección Provincial de Estadística y Censos de la Provincia de San Luis (Provincial Directorate of Statistics and Census of the Province of San Luis), as well as on independent third-party data, statistical information and reports produced by unaffiliated entities, as well as on our own internal estimates. In addition, this annual report contains information from Vaisala, Inc. (“Vaisala - 3 Tier”), a company that develops, manufactures and markets products and services for environmental and industrial measurement.

This annual report also contains estimates that we have made based on third-party market data. Market studies are frequently based on information and assumptions that may not be exact or appropriate.

Although we have no reason to believe any of this information or these sources are inaccurate in any material respect, we have not verified the figures, market data or other information on which third parties have based their studies, nor have we confirmed that such third parties have verified the external sources on which such estimates are based. Therefore, we do not guarantee, nor do we assume responsibility for, the accuracy of the information from third-party studies presented in this annual report.

This annual report also contains estimates of market data and information derived therefrom which cannot be gathered from publications by market research institutions or any other independent sources. Such information is based on our internal estimates. In many cases there is no publicly available information on such market data, for example from industry associations, public authorities or other organizations and institutions. We believe that these internal estimates of market data and information derived therefrom are helpful in order to give investors a better understanding of the industry in which we operate as well as our position within this industry. Although we believe that our internal market observations are reliable, our estimates are not reviewed or verified by any external sources. These may deviate from estimates made by our competitors or future statistics provided by market research institutes or other independent sources. We cannot assure you that our estimates or the assumptions are accurate or correctly reflect the state and development of, or our position in, the industry.

vi |

FORWARD-LOOKING STATEMENTS

This annual report contains estimates and forward-looking statements, principally in “Item 3.D. Risk Factors,” “Item 4.B. Business Overview” and “Item 5. Operating and Financial Review and Prospects”.

Our estimates and forward-looking statements are mainly based on our current beliefs, expectations and estimates of future courses of action, events and trends that affect or may affect our business and results of operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to several risks and uncertainties and are made in light of information currently available to us.

Many important factors, in addition to those discussed elsewhere in this annual report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including, among other things:

| · | changes in general economic, financial, business, political, legal, social or other conditions in Argentina; |

| · | changes in conditions elsewhere in Latin America or in either developed or emerging markets; |

| · | changes in capital markets in general that may affect policies or attitudes toward lending to or investing in Argentina or Argentine companies, including volatility in domestic and international financial markets; |

| · | the impact of political developments and uncertainties relating to political and economic conditions in Argentina, on the demand for securities of Argentine companies; |

| · | increased inflation; |

| · | fluctuations in exchange rates, including a significant devaluation of the Argentine peso; |

| · | changes in the law, norms and regulations applicable to the Argentine electric power and energy sector, including changes to the current regulatory frameworks, changes to programs established to incentivize investments in new generation capacity and reductions in government subsidies to consumers; |

| · | our ability to develop our expansion projects and to win awards for new potential projects; |

| · | increases in financing costs or the inability to obtain additional debt or equity financing on attractive terms, which may limit our ability to fund new activities; |

| · | government intervention, including measures that result in changes to the Argentine labor market, exchange market or tax system; |

| · | adverse legal or regulatory disputes or proceedings; |

| · | changes in the price of energy, power and other related services; |

| · | changes in the prices and supply of natural gas or liquid fuels; |

| · | changes in the amount of rainfall and accumulated water; |

| · | changes in environmental regulations, including exposure to risks associated with our business activities; |

| · | risks inherent to the demand for and sale of energy; |

| · | the operational risks related to the generation, as well as the transmission and distribution, of electric power; |

| · | ability to implement our business strategy, including the ability to complete our construction and expansion plans in a timely manner and according to our budget; |

| · | competition in the energy sector, including as a result of the construction of new generation capacity; |

| · | exposure to credit risk due to credit arrangements with CAMMESA; |

| · | our ability to retain key members of our senior management and key technical employees; |

| · | the effects of a pandemic or epidemic, such as COVID-19, and any subsequent mandatory regulatory restrictions or containment measures; |

| · | our relationship with our employees; and |

| · | other factors discussed under “Item 3.D.-Risk Factors” in this annual report. |

The words “believe,” “may,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “forecast” and similar words are intended to identify forward-looking statements. Forward-looking statements include information concerning our possible or assumed future results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements speak only as of the date they were made, and we do not undertake any obligation to update publicly or to revise any forward-looking statements after we distribute this annual report because of new information, future events or other factors, except as required by applicable law. In light of the risks and uncertainties described above, the forward-looking events and circumstances discussed in this annual report might not occur and do not constitute guarantees of future performance. Because of these uncertainties, you should not make any investment decisions based on these estimates and forward-looking statements.

vii |

| Table of Contents |

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Item 3.A [Reserved]

Item 3.B Capitalization and indebtedness

Not applicable.

Item 3.C Reasons for the offer and use of proceeds

Not applicable.

Item 3.D Risk Factors

Summary of Risk Factors

We are subject to several risks related to our business that are described under “Risk Factors” and elsewhere in this annual report. These risks could materially and adversely impact our business, results of operations, financial condition, and future prospects. Among these important risks are the following:

Risks Relating to Argentina

| · | Substantially all our revenues are generated in Argentina and thus are highly dependent on economic and political conditions in Argentina. |

| · | As of July 1, 2018, the Argentine Peso qualifies as a currency of a hyperinflationary economy and we are required to restate our historical financial statements to apply inflationary adjustments, which could adversely affect our results of operations and financial condition and those of our Argentine subsidiaries. |

| · | Significant fluctuations in the value of the peso could adversely affect the Argentine economy and, in turn, adversely affect our results of operations. |

| · | Exchange controls and restrictions on capital inflows and outflows could limit the availability of international credit and could threaten the financial system, adversely affecting the Argentine economy and, as a result, our business. |

| · | Argentina’s ability to obtain financing from international markets is limited, which could affect its capacity to implement reforms and sustain economic growth and may negatively impact our financial condition or cash flows. |

| · | The Argentine economy could be adversely affected by economic developments in other markets and by more general “contagion” effects. |

| · | We may be exposed to adverse effects arising from the ongoing conflict between Russia and Ukraine. |

| · | The Argentine banking system may be subject to instability which may affect our operations. |

| · | Failure to adequately address actual and perceived risks of institutional deterioration and corruption may adversely affect Argentina’s economy and financial condition, which in turn could adversely affect our business, financial condition, and results of operations. |

| · | The Argentine economy is particularly sensitive to local political developments, including the next presidential election which is scheduled for October 2023. |

Risks Relating to the Electric Power Sector in Argentina

| · | The Argentine Government has intervened in the electric power sector in the past and is likely to continue intervening. |

| · | Changes in regulatory frameworks under which we sell our electricity may affect our financial condition and results of operations. |

| · | We have, in the recent past, been unable to collect payments, or to collect them in a timely manner, from CAMMESA and other customers in the electric power sector. |

| · | Argentina has certain energy transmission and distribution limitations that adversely affect the capacity of electric power generators to deliver all of the energy they can produce, which results in reduced sales. |

| · | Restrictions on the supply of energy could negatively affect Argentina’s economy. |

| · | We operate in a heavily regulated sector that imposes significant costs on our business, and we could be subject to fines and liabilities that could have a material adverse effect on our results of operations. |

| · | Risks arise for our business from technological change in the energy market. |

| · | Competition in the Electric Power Sector in Argentina may adversely affect our results of operations. |

| 1 |

| Table of Contents |

Risks Relating to Our Business

| · | Our results depend largely on the compensation established by the Secretariat of Electric Energy and received from CAMMESA. |

| · | Factors beyond our control may affect or delay the completion of the awarded projects or alter our plans for the expansion of our existing plants. |

| · | Our business may require substantial capital expenditures for ongoing maintenance requirements and the expansion of our installed generation capacity. |

| · | Covenants in our indebtedness could adversely restrict our financial and operating flexibility. |

| · | We may be unable to refinance our outstanding indebtedness, or the refinancing terms may be materially less favorable than their current terms, which would have a material adverse effect on our business, financial condition, and results of operations. |

| · | The non-renewal or early termination of the HPDA Concession Agreement would adversely affect our results of operations. |

| · | Our interests in TJSM, TMB were diluted and CVOSA will be significantly diluted. |

| · | Future changes in the rainfall amounts in the Limay River basin could adversely affect the revenues from the Piedra del Águila concession and, therefore, our financial results. |

| · | Our ability to operate wind farms profitably is highly dependent on suitable wind and associated weather conditions. |

| · | Climate change and energy transition could affect our business. |

| · | Our power plants and forest assets are subject to the risk of mechanical or electrical failures, and any resulting unavailability may affect our ability to fulfill our contractual and other commitments and thus adversely affect our business and financial performance. |

| · | Our insurance policies may not fully cover damage, and we may not be able to obtain insurance against certain risks. |

| · | We may be exposed to lawsuits and or administrative proceedings that could adversely affect our financial condition and results of operations. |

| · | Energy demand is seasonal, largely due to climate conditions. |

| · | We may undertake acquisitions and investments to expand or complement our operations that could result in operating difficulties or otherwise adversely affect our financial conditions and results of operations. |

| · | If we were to acquire another energy company in the future, such acquisition could be subject to the Argentine Antitrust Authority’s approval. |

| · | We depend on senior management and other key personnel for our current and future performance. |

| · | We could be affected by material actions taken by the trade unions. |

| · | Our equipment, facilities and operations are subject to environmental, health and safety regulations. |

| · | We are subject to anticorruption, anti-bribery, anti-money laundering and other laws and regulations. |

| · | A cyberattack could adversely affect our business, balance sheet, results of operations and cash flow. |

| · | Our ability to generate electricity at our thermal generation plants partially depends on the availability of natural gas and, to a lesser extent, liquid fuel. |

| · | We may be adversely affected by the phase out of LIBOR, or its replacement rate. |

| · | An outbreak of a disease, including COVID-19, may have material adverse consequences on our operations including new projects. |

| 2 |

| Table of Contents |

Risks Relating to our Shares and ADSs

| · | It may be difficult for you to obtain or enforce judgments against us. |

| · | Restrictions on transfers of foreign exchange and the repatriation of capital from Argentina may impair your ability to receive dividends and distributions on, and the proceeds of any sale of, shares underlying the ADSs. |

| · | We will be traded on more than one market, and this may result in price variations; in addition, investors may not be able to easily move shares for trading between such markets. |

| · | Under Argentine Corporate Law, shareholder rights may be fewer or less well defined than in other jurisdictions. |

| · | Holders of our common shares and the ADSs located in the United States may not be able to exercise preemptive or accretion rights. |

| · | Voting rights, and other rights, with respect to the ADSs are limited by the terms of the deposit agreement. |

| · | The relative volatility and illiquidity of the Argentine securities markets may substantially limit our ADS holders’ ability to sell common shares underlying the ADSs at the price and time they desire. |

| · | If there are substantial sales of our common shares or the ADSs, the price of the common shares or of the ADSs could decline. |

| · | Our shareholders may be subject to liability for certain votes of their securities. |

| · | As a foreign private issuer, we are exempt from several rules under the U.S. securities laws and are permitted to file less information with the Commission than a U.S. company. This may limit the information available to holders of our ADSs. |

| · | As a foreign private issuer, we are not subject to certain NYSE corporate governance rules applicable to U.S. listed companies. |

| · | The market price for our common shares or ADSs could be highly volatile. |

| · | If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud. As a result, shareholders could lose confidence in our financial and other public reporting, which would harm our business and the trading price of our common shares. |

| · | The protections afforded to minority shareholders in Argentina are different from and more limited than those in the United States and may be more difficult to enforce. |

| · | Holders of our common shares may determine not to pay any dividends. |

| · | We may be a passive foreign investment company for U.S. federal income tax purposes. |

| · | The requirements of being a public company may strain our resources and distract our management, which could make it difficult to manage our business. |

Detailed Risk Factors

You should carefully consider the risks described below, as well as the other information in this annual report. Our business, results of operations, financial condition or prospects could be materially and adversely affected if any of these risks occurs, and as a result, the market price of our common shares and ADSs could decline. The risks described below are those known to us and that we currently believe may materially affect us.

Risks Relating to Argentina

Substantially all of our revenues are generated in Argentina and thus are highly dependent on economic and political conditions in Argentina

Central Puerto is an Argentine corporation (sociedad anónima). All of our assets and operations are located in Argentina. Accordingly, our financial condition and results of operations depend to a significant extent on macroeconomic, regulatory, social and political conditions prevailing in Argentina, including but not limited to, the following: (i) international demand and prices for Argentina’s commodity exports; (ii) competitiveness and efficiency of domestic industries and services; (iii) stability and competitiveness of the Argentine peso against foreign currencies; (iv) foreign and domestic investment and financing; (v) level of foreign exchange reserves in the Central Bank of the Argentine Republic (“BCRA”) which may cause abrupt changes in currency values and exchange and capital control regulations (including, to import equipment , payment of cross border indebtedness and other necessities relevant for operations); (vi) high interest and inflation rates to corresponding wage and price controls; (vii) adverse external economic shocks; (viii) effects of the ongoing COVID-19 pandemic and results of the measures adopted by the Argentine government in response; (ix) changes in economic or fiscal policies implemented by the Argentine government; (x) labor disputes and work stoppages; (xi) the level of expenditure by the Argentine government and ability to sustain fiscal balance; (xii) the level of unemployment, political instability and social tensions, such as land-takings and claims in areas where we operate.

The Argentine economy has experienced significant volatility in recent decades, characterized by periods of low or negative growth, high levels of inflation and currency devaluation. Sustainable economic growth in Argentina is dependent on a variety of factors, including the international demand for Argentine exports, the stability and competitiveness of the peso against foreign currencies, confidence among consumers and foreign and domestic investors, a stable rate of inflation, national employment levels and the circumstances of Argentina’s regional trade partners.

Argentina has experienced repeatedly, especially in recent years, periods of high inflation. High inflation rates affect Argentina’s foreign competitiveness, social and economic inequality, negatively impacts employment, consumption and the level of economic activity and undermines the confidence in Argentina’s banking system, which could further limit the availability of and access by local companies to domestic and international credit. If the measures adopted by the Argentine government fail to correct Argentina’s structural inflationary imbalances, inflation may continue or increase and have an adverse effect on Argentina’s economy and on our business, financial condition and results of operations. Inflation can also lead to an increase in Argentina’s local currency-denominated debt and have an adverse effect on Argentina’s ability to service its debt, mainly in the medium and long term when most inflation-indexed debt matures.

Argentina’s fiscal imbalances, its dependence on foreign revenues to cover its fiscal deficit, and material rigidities that have historically limited the ability of the economy to absorb and adapt to external factors, have added to the severity of the current crisis.

| 3 |

| Table of Contents |

In the past, some governments increased direct intervention in the Argentine economy, including the implementation of expropriation measures, price controls, exchange controls and changes in laws and regulations affecting foreign trade and investment. These measures had a material adverse effect on private sector entities, including us. It is possible that similar measures could be adopted by the current or future Argentine Government or that economic, social and political developments in Argentina, over which we have no control, could have a material adverse effect on the Argentine economy and, in turn, adversely affect our financial condition and results of operations. Uncertainty with respect to government policies may lead to additional volatility of Argentine stock market prices including companies that operate in the energy sector, given the degree of state regulation and intervention in this industry.

As in the recent past, Argentina’s economy may be adversely affected if political and social pressures inhibit the implementation by the Argentine Government of policies designed to control inflation, generate growth and enhance consumer and investor confidence, or if policies implemented by the Argentine Government that are designed to achieve these goals are not successful. These events could materially adversely affect our financial condition and results of operations.

The Argentine economy is also particularly sensitive to local political developments. Presidential elections take place in Argentina every four years and legislative elections every two years, resulting in the partial renewal of both chambers of Congress. The next presidential election is scheduled for October 2023. The result of the presidential and legislative elections may lead to changes in government policies that could have an impact on our business. We cannot provide assurance as to whether such policy changes will occur or as to their timing, nor can we estimate the impact they may have on our business and thus on our financial condition and results of operations.

As of July 1, 2018, the Argentine Peso qualifies as a currency of a hyperinflationary economy and we are required to restate our historical financial statements to apply inflationary adjustments, which could adversely affect our results of operations and financial condition and those of our Argentine subsidiaries.

Pursuant to the International Accounting Standard 29, Financial Reporting in Hyperinflationary Economies (“IAS 29”), the financial statements of entities whose functional currency is that of a hyperinflationary economy must be adjusted for the effects of changes in a general price index. IAS 29 does not prescribe when hyperinflation arises and the International Accounting Standards Board (“IASB”) does not identify specific hyperinflationary jurisdictions. However, IAS 29 provides a series of non-exclusive guidelines that consist of (i) analyzing the behavior of the population, prices, interest rates and wages before the evolution of price indexes and the loss of the currency’s purchasing power, and (ii) as a quantitative characteristic, verifying if the three-year cumulative inflation rate approaches or exceeds 100.00%. In June 2018, the International Practices Task Force of the Centre for Quality (“IPTF”), which monitors countries experiencing high inflation, categorized Argentina as a country with projected three-year cumulative inflation rate greater than 100.00%. In addition, certain qualitative macroeconomic factors provided under the International Accounting Standard 29, Financial Reporting in Hyperinflationary Economies (“IAS 29”) were also identified. Therefore, Argentine companies using IFRS, such as us, are required to apply IAS 29 to their financial statements for periods ending on and after July 1, 2018. As a result, our Audited Consolidated Financial Statements included in this annual report, including the figures for the previous periods (this fact not affecting the decisions taken on the financial information for such periods), and, unless otherwise stated, the financial information included elsewhere in this annual report, were restated to consider the changes in the general purchasing power of the functional currency of the Company (Argentine peso) pursuant to IAS 29 and General Resolution No. 777/2018 of the CNV.

Significant fluctuations in the value of the peso could adversely affect the Argentine economy and, in turn, adversely affect our results of operations

The depreciation of the peso has had and may continue to have a negative impact on the ability of certain Argentine businesses to service their foreign currency-denominated debt, lead to inflation, significantly reduce real wages and jeopardize the stability of businesses, such as ours, whose success depends on domestic market demand and adversely affect the Argentine Government’s ability to honor its foreign debt obligations. In 2022, the peso depreciated approximately 72.47%, and 17.98% from December 31, 2022 through March 31, 2023. On March 31, 2023, the exchange rate was Ps.209.01 to US$1.00, as quoted by the Banco de la Nación Argentina for wire transfers (divisas).

The main effects of the devaluation of the Argentine peso on our net results, expressed in pesos, are related to (i) exchange rate differences as a result of our exposure to the dollar, (due to the fact that our functional currency is the Argentine peso); (ii) higher revenues generated by the sale of energy priced in U.S. dollars, and (iii) higher costs generated by expense items priced in U.S. dollars such as financial obligations and certain maintenance contracts among other costs. In addition, the majority of our debt is denominated in currencies other than the peso; consequently, a devaluation of the peso against such currencies will increase the amount of pesos we need to cover our debt service obligations.

If the peso depreciates further, all the negative effects on the Argentine economy related to such depreciation could recur, with adverse consequences to our business, financial condition and results of operations. In addition, a further depreciation of the Argentine Peso against the U.S. dollar may also have an adverse impact on our capital expenditure program and increase the Argentine Peso amount of our trade liabilities and financial debt denominated in U.S. dollars. As of December 31, 2022, 97.00% of our financial liabilities were denominated in U.S. dollars.

| 4 |

| Table of Contents |

The Company remains highly exposed to risks associated with the fluctuation of the Argentine Peso, therefore, a devaluation of the Argentine Peso could have a material adverse effect on our financial condition and results of operations.

Exchange controls and restrictions on capital inflows and outflows could limit the availability of international credit and could threaten the financial system, adversely affecting the Argentine economy and, as a result, our business

The Argentine government and the BCRA have implemented certain measures that control and restrict the ability of companies and individuals to access to the foreign exchange market to purchase foreign currency and to transfer it abroad. Those measures include, among others: (i) restricting access to the Argentine foreign exchange market for the purchase or transfer of foreign currency abroad for any purpose, including the payment of dividends to non-residents stakeholders; (ii) restrictions on the acquisition of any foreign currency to be held as cash in Argentina; (iii) requiring exporters to repatriate and settle in pesos, in the local exchange market, all or a portion of the proceeds of their exports of goods and services; (iv) limitations on the transfer of securities into and from Argentina; (v) establishing certain mandatory refinancing’s; and (vi) the implementation of taxes on certain transactions involving the acquisition of foreign currency.

The exchange controls introduced gave rise to an unofficial U.S. dollar trading market. As of the date of this annual report, the peso/U.S. dollar exchange rate in such market substantially differs from the official peso/U.S. dollar exchange rate. The Argentine government could maintain a single official exchange rate or create multiple exchange rates for different types of transactions, substantially modifying the applicable exchange rate at which we acquire currency to service our outstanding foreign currency denominated liabilities.

There can be no assurance that the BCRA or other government agencies will not increase or relax such controls or restrictions, make modifications to these regulations, impose further mandatory refinancing plans related to our indebtedness payable in foreign currency, establish more severe restrictions on currency exchange, or maintain the current foreign exchange regime or create multiple exchange rates for different types of transactions, substantially modifying the applicable exchange rate at which we acquire currency to service our outstanding liabilities denominated in currencies other than the peso, all of which could affect our ability to comply with our financial obligations when due, raise capital, refinance our debt at maturity, obtain financing, execute our capital expenditure plans, and/or undermine our ability to pay dividends to foreign shareholders. Consequently, these exchange controls and restrictions could materially adversely affect the Argentine economy and/or our business, financial condition, and results of operations. See “Exchange Controls”.

Argentina’s ability to obtain financing from international markets is limited, which could affect its capacity to implement reforms and sustain economic growth, and may negatively impact our financial condition or cash flows

During recent years the Argentine Republic has experienced financial distress, leading to an increase in the incurrence of public debt.

During 2020 the Argentine government engaged in negotiations with Argentina´s creditors to restore the sustainability of its public external debt. In August 2020, the Argentine government restructured approximately US$66.5 billion of its foreign currency global bonds issued under foreign laws exchanging such bonds for new bonds. Moreover, Argentina reached an agreement with the Paris Club members under the Paris Club 2014 Settlement Agreement to extend the maturity of its obligations until March 2022. In addition, the Argentine government-initiated negotiations with the International Monetary Fund (“IMF”) in order to renegotiate the principal maturities of the US$44.1 billion disbursed between 2018 and 2019 under a Stand-By Agreement, originally planned for the years 2021, 2022 and 2023. On March 22, 2022, the Argentine government reached an agreement with the Paris Club for a new extension of the understanding reached in June 2021 (the “Paris Club Agreement”).

On January 28, 2022, the Argentine government and the IMF announced that they had reached an understanding on key policies as part of their ongoing discussions involving an IMF-supported program. Later, on March 3, 2022, the IMF and the Argentine government announced that the agreement is based on what is known as the IMF’s Extended Fund Facility, which includes 10 reviews to be carried out quarterly for two and a half years and disbursements for an amount equivalent to US$44.0 billion, including a disbursement of US$9.6 billion immediately available to Argentina upon approval of the agreement by the IMF executive board (the “EFF Agreement”). The EFF Agreement was approved by the Argentine Congress through Law No. 27,668 on March 17, 2022 (enacted by Decree No. 130/22) and by the executive board of the IMF on its meeting held on March 25, 2022.

On June 25, 2022, the IMF approved Argentina’s first quarterly review under the EFF, authorizing an immediate disbursement of approximately US$4.01 billion. Further, on October 7, 2022 and December 22, 2022, the executive board of the IMF completed the second and third review of the EFF Agreement, allowing for an immediate disbursement of approximately US$3.8 billion and US$6.0 billion, respectively. The remaining disbursements will be made after the completion of each review. The repayment period for each disbursement is ten years, with a grace period of four and a half years, which implies that Argentina shall repay the debt between 2026 and 2034.

| 5 |

| Table of Contents |

On July 25 and September 7, 2022, the Argentine government announced financing agreements with the World Bank for US$200.0 million and US$900.0 million, respectively. These financing agreements are aimed at promoting sustainable growth in Argentina, driven by innovation and focused on the creation of productive technology-based companies, support for entrepreneurs and access to private capital.

On September 10, 2022, the IMF staff and the Argentinean authorities have reached a staff-level agreement on an updated macroeconomic framework and associated policies needed to complete the second review under Argentina’s 30-month SAF arrangement. The agreement was subject to approval by the IMF Executive Board. Upon completion of the review, Argentina would have access to about US$3.9 billion. Most of the quantitative programme targets until end-June 2022 were met, with the exception of the net international reserves floor, mainly due to higher-than-programmed import volume growth and delays in external official support. Subsequently, a period of volatility in the exchange and bond markets was halted following decisive measures that corrected earlier setbacks and rebuilt credibility. On October 5, 2022 the Supreme Court of Justice of the Nation dismissed an extraordinary federal appeal filed by the government against a ruling that condemned it to provide complementary information on the agreements signed in 2018 with the IMF, based on the Law on Access to Public Information. On this basis, the government must provide detailed and complete information on the agreement signed with the IMF.

On October 7, 2022, the IMF approved the second review of the SAF arrangement and authorized the disbursement of approximately US$3.9 billion. Also, in December 2022, the government announced the IMF’s approval of the revision of the third quarter targets, which would allow for a new disbursement before 2023 for a total amount of US$6.0 billion.

On October 28, 2022, the Minister of Economy, Sergio Massa, announced a new agreement with the Paris Club. The agreement is an addendum to the one signed in 2014 by the then Minister of Economy, Axel Kicillof, and recognizes a principal amount of US$1,971 million, extending a repayment period of thirteen semi-annual installments, starting in December 2022 to be finally cancelled on September 2028. The interest rate was improved from 9.00% to 3.90% in the first three installments, with a gradual increase to 4.50%. The payment profile implies an average semi-annual payment of US$170.0 million (principal and interest included). Over the next two years Argentina will repay 40.00% of the principal due.

We cannot assure that the EFF Agreement and the Paris Club Agreement will not affect Argentina’s ability to implement reforms and public policies and boost economic growth. Consequently, there can be no assurance that the implementation of the revenue and expenditure policies of the EFF Agreement regarding the reduction of untargeted energy subsidies would not have material adverse effect on our financial condition and results of operations. Also, we cannot predict the impact of the outcome of such reforms on Argentina’s (and indirectly our) ability to access the international capital markets. Moreover, the long-term impact of these measures and any future measures taken by the current administration on the Argentine economy remains uncertain.

In addition, the Argentine Republic’s future tax revenue and fiscal results may be insufficient to meet its debt service obligations and the Argentine Republic may have to rely in part on additional financing from domestic and international capital markets, the IMF and other potential creditors, in order to meet future debt service obligations. In the future, the Argentine Republic may not be able or willing to access international or domestic capital markets, which could have a material adverse effect on the Argentine Republic’s ability to make payments on its outstanding public debt, and in turn, could materially adversely affect our financial condition and results of operations.

In spite of the restructuring of the Argentine public debt carried out in 2020, the international markets continued showing signs of doubts as to whether Argentina’s debt is sustainable and, therefore, country risk indicators remain high. Without renewed access to the financial market the Argentine government may not have the financial resources to implement reforms and boost growth, which could have a significant adverse effect on the country’s economy and, consequently, on our activities. Likewise, Argentina’s inability to obtain credit in international markets could have a direct impact on the Company’s ability to access those markets to finance its operations and its growth, including the financing of capital investments, which would negatively affect our financial condition, results of operations and cash flows. In addition, we cannot predict the outcome of any future restructuring of Argentine sovereign debt. Any new event of default by the Argentine government could negatively affect their valuation and repayment terms, as well as have a material adverse effect on the Argentine economy and, consequently, our business and results of operations.

The Argentine economy could be adversely affected by economic developments in other markets and by more general “contagion” effects

Financial and securities markets in Argentina and the Argentine economy are influenced by the effects of global or regional financial crisis and market conditions in other markets worldwide. Weak, flat or negative economic growth of any of Argentina’s major trading partners, such as Brazil (Argentina’s main trading partner), China or the United States, could have a material adverse effect on Argentina’s trade balance and adversely affect Argentina’s economic growth. The economic performance of other trading partners such as Chile, Spain and Canada may also affect Argentina’s trade balance.

| 6 |

| Table of Contents |

Global economic instability such as uncertainty about global trade policies, the deterioration of economic conditions in Brazil and of the economies of other major trading partners of Argentina, such as China or the United States, the withdrawal of the United Kingdom from the European Union, geopolitical tensions between the United States and a number of foreign countries, the ongoing conflict between Russia and Ukraine, decisions by the Organization of Petroleum Exporting Countries (OPEC) and other non-OPEC oil-producing nations with respect to oil production that affect oil prices, idiosyncratic, political and social discords, terrorist attacks, sovereign debt downgrades, a pandemic disease, including the result of the ongoing COVID-19 pandemic, could impact the Argentine economy and jeopardize Argentina’s ability to stabilize its economy, among others.

These developments, or the perception that any of them could occur, may have a material adverse effect on global economic conditions and the stability of global financial markets. Any of these factors could depress economic activity and restrict our access to suppliers and have a material adverse effect on our business, financial condition, and results of operations.

The Argentine economy may be affected by “contagion” effects. International investors’ reactions to events occurring in one developing country sometimes appear to follow a “contagion” effect, in which an entire region or investment class is disfavored by international investors.

Consequently, there can be no assurance that the Argentine economy and securities markets will not be adversely impacted by events affecting developed economies, emerging markets, or any of Argentina’s major trading partners, which could in turn adversely affect our business, financial condition, and results of operations, and the market value of our ADSs. Furthermore, a significant devaluation of the currencies of our trading partners or trade competitors may adversely affect the competitiveness of Argentina and consequently, adversely affect Argentina’s economy and our financial condition and results of operations.

We may be exposed to adverse effects arising from the ongoing conflict between Russia and Ukraine

Russia’s military incursion in Ukraine has led to and could continue to give a rise to an escalation of armed action, regional instability and result in heightened economic sanctions by the United States, the European Union, and other countries against Russia. Although the severity and duration of the ongoing conflict is highly unpredictable, its effects could be substantial, and any continuation of the conflict could adversely affect global and regional economic conditions. After a year since the beginning of the armed conflict, military actions keep growing and fears of an escalation to the use of nuclear weapons are rising as a result of the decision from the Russian government to halt its participation under the Strategic Arms Reduction Treaty III.

As of the date of this annual report, the ongoing conflict has led high volatility in commodity prices and international crude oil and gas prices, which has resulted in higher fuel prices and - consequently - in a sharper rise in inflation around the world. Moreover, economic sanctions imposed against Russia may lead to shortage of raw materials and commodities, which could in turn contribute to the increase in inflation worldwide and to interruption to the supply chain in general, and particularly in the energy sector. Such difficulties may consequently derive in constraints to supply the local market. Consequently, this could adversely affect our business, financial condition, or results of operations.

Due to the uncertainties inherent to the scale and duration of these events and its direct and indirect effects, it is not reasonably possible to estimate the impact this conflict will have on the world’s economy and its financial markets, on Argentina’s economy and, consequently, our business, financial condition and results of operations. Any such disruptions caused by Russian military action or resulting sanctions may magnify the impact of other risks described in this annual report.

The Argentine banking system may be subject to instability which may affect our operations

In recent years, the Argentine financial system grew significantly with a marked increase in loans and private deposits, showing a recovery of credit activity. Although the financial system’s deposits continue to grow in nominal terms, they are mostly short-term deposits and the sources of medium and long-term funding for financial institutions are currently limited.

Financial institutions are particularly subject to significant regulation from multiple regulatory authorities, all of whom may, among other things, establish limits on commissions and impose sanctions on the financial institutions. The lack of a stable regulatory framework, or changes to such regulatory framework by the government, could impose significant limitations on the activities of the financial institutions and could induce uncertainty with respect to the financial system stability.

The persistence of the current economic crisis or the instability of one or more of the larger banks, public or private, could have a material adverse effect on the prospects for economic growth and political stability in Argentina, resulting in a loss of consumer confidence, lower disposable income and fewer financing alternatives for consumers. These conditions could also have a material adverse effect on the Argentine banking system, and therefore, on our business, financial condition and results of operations.

Failure to adequately address actual and perceived risks of institutional deterioration and corruption may adversely affect Argentina’s economy and financial condition, which in turn could adversely affect our business, financial condition and results of operations.

| 7 |

| Table of Contents |

A lack of a solid institutional framework and corruption have been identified as, and continue to be, a significant problem for Argentina. Recognizing that the failure to address these issues could increase the risk of political instability, distort decision-making processes and adversely affect Argentina’s international reputation and ability to attract foreign investment, the prior administration had adopted several measures aimed at strengthening Argentina’s institutions and reducing corruption. These measures included the reduction of criminal sentences in exchange for cooperation with the government in corruption investigations, increased access to public information, the seizing of assets from corrupt officials, and establishing a corporate criminal liability regime for corruption offenses aimed at promoting anticorruption compliance, among others. The current Argentine Government’s ability to implement them or promote further transparency and integrity measures is uncertain in a highly polarized political context. Argentina’s political environment has historically influenced, and continues to influence, the performance of the country’s economy. Political crises have affected and continue to affect the confidence of investors and the general public, which have historically resulted in economic deceleration and heightened volatility in the securities with underlying Argentine risk. The recent economic instability in Argentina has contributed to a decline in market confidence in the Argentine economy as well as to a deteriorating political environment.

In addition, various ongoing investigations into allegations of money laundering and corruption being conducted by the Office of the Argentine Federal Prosecutor, have negatively impacted the Argentine economy and political environment. Certain government officials of previous administrations as well as high ranked officers of companies holding government contracts or concessions have faced or are currently facing allegations of corruption and money laundering as a result of these investigations. These individuals are alleged to have accepted or paid, as applicable, bribes by means of kickbacks on contracts granted by the government to several infrastructure, energy and construction companies. We have no control over and cannot predict for how long the corruption investigations will continue nor whether such investigations or allegations (or any other future investigations or allegations) will lead to further political and economic instability. In addition, we cannot predict the outcome of any such allegations nor their effect on the different sectors of the Argentine economy. See also “-We are subject to anticorruption, anti-bribery, anti-money laundering and other laws and regulations”.

Risks Relating to the Electric Power Sector in Argentina

The Argentine Government has intervened in the electric power sector in the past, and is likely to continue intervening

Historically, the Argentine government has played an active role in the electric power industry through the ownership and management of state-owned companies engaged in the generation, transmission and distribution of electric power. Moreover, the Argentine government made a number of material changes to the regulatory framework applicable to the electric power sector since the Argentine economic crisis of 2001, including adopting Law No. 25,561 (the “Public Emergency Law”), which have had significant adverse effects on electric power generation, distribution and transmission companies and included the freezing of distribution margins, the revocation of adjustment and inflation indexation mechanisms for tariffs, a limitation on the ability of electric power distribution companies to pass on to the consumer increases in costs due to regulatory charges and the introduction of a new price-setting mechanism in the WEM, all of which had a significant impact on electric power generators and caused substantial price differences within the market.

Any significant increase in energy prices to consumers (whether through a tariff increase or through a cut in consumer subsidies) could result in a decline in demand for the energy that we generate. Any material adverse effect on electric power demand, in turn, could lead electric power generation companies, like us, to record lower revenues and results of operations than currently anticipated.

It is possible that certain measures may be adopted by the Argentine Government that could have a material adverse effect on our business and results of operations, or that the Argentine Government may adopt emergency legislation similar to the Public Emergency Law or other similar resolutions in the future that could have a direct impact on the regulatory framework of the electric power industry and indirectly adversely affect the electric power generation industry, and therefore, our business, financial condition and results of operations.

Changes in regulatory frameworks under which we sell our electricity may affect our financial condition and results of operations

We cannot assure what further changes the Argentine Government may make to the regulatory frameworks under which we sell power availability or electricity, nor that these changes will not negatively impact our results of operations. Moreover, we cannot assure under what kind of regulatory framework we will be able to sell our generation capacity and electricity in the future. Any further changes in the current applicable laws and regulations, or adverse judicial or administrative interpretations of such laws and regulations, may adversely affect our results of operations. In addition, some of the measures proposed by the Argentine government may also generate political and social opposition, which may in turn prevent the Argentine government from adopting such measures as proposed.

| 8 |

| Table of Contents |

The factors mentioned above for both our operation of power generation and the projects under construction/development, may also lead to an impairment of property, plant and equipment and intangible assets, related to a reduction in the assessed value-in-use of certain assets that may exceed their previously recorded book value.

We have, in the recent past, been unable to collect payments, or to collect them in a timely manner, from CAMMESA and other customers in the electric power sector

A substantial amount of our total revenues comes from our sales to CAMMESA. In addition, we receive significant cash flows from CAMMESA in connection with the FONINVEMEM and similar programs. Payments to us by CAMMESA, depend upon payments that CAMMESA in turn receives from other WEM agents such as electric power distributors as well as subsidies from the Argentine government to certain users, which in turn requires additional funding to CAMMESA from the government to pay to generators.

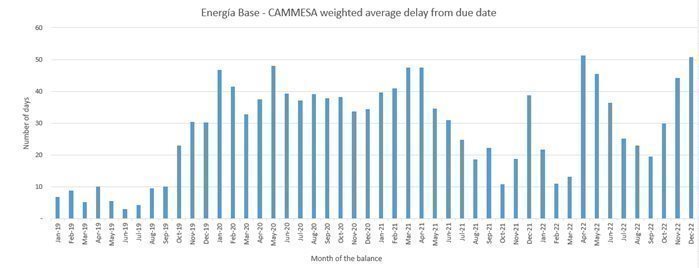

In recent years, due to regulatory conditions and long periods of frozen tariffs in Argentina’s electric power sector that affected the profitability and economic viability of power utilities, certain WEM agents defaulted on their payments to CAMMESA, which adversely affected CAMMESA’s ability to meet its payment obligations with electric power generators, including us. As a consequence of delays in payments that CAMMESA received from other WEM agents, we also saw delays in, receiving payments from CAMMESA more than 90 days of month-end, rather than the required 42 days after the date of billing. Such payment delays resulted in higher working capital requirements that we would typically finance with our own financing sources.

As of the date of this annual report, CAMMESA is facing difficulties to make payments to generators both in respect of energy dispatched and generation capacity availability on a timely basis or in full, which in turn may substantially and adversely affect our financial position and the results of our operations.

Argentina has certain energy transmission and distribution limitations that adversely affect the capacity of electric power generators to deliver all of the energy they can to produce, which results in reduced sales

The energy that generators can deliver to the transmission system for the further delivery to the distribution system at all times depends on the capacity of the transmission and distribution systems that connects them to it. In the past, the transmission and distribution system operated at near full capacity and both transmission and distributors were not able to guarantee an increased supply of electric power to their customers. In the past years, the increase in demand for electric power resulted in blackouts in Buenos Aires and other cities around Argentina, which resulted in excess capacity for generators. As a result, the amount of hydroelectric energy and thermal energy generated was larger than what the transmission and distribution systems are capable of transmitting or distributing. Any transmission or distribution limitation for generators could reduce the energy sold, which could adversely affect our financial condition.

Restrictions on the supply of energy could negatively affect Argentina’s economy

Demand for natural gas and electricity has increased substantially, driven by a recovery in economic conditions and price constraints, which has prompted the government to adopt a series of measures that have resulted in industry shortages and/or costs increase. In particular, Argentina has been importing gas in order to compensate the shortage in local production. In order to pay for those imports the Argentine government has frequently used the Argentine Central Bank reserves due to absence of incoming currencies from investment. Argentina’s foreign exchange reserves are particularly limited and, therefore, Argentina’s ability to deal with significant increases in international oil and gas prices remains limited. If the Argentine government is unable to pay for the gas import in order to produce electricity, business and industries may be affected.

Moreover, the Argentine government has taken a number of measures aimed at alleviating the short-term impact of supply restrictions on residential and industrial users such as importing natural gas from Bolivia, importing liquefied natural gas transported to Argentina in vessels. If these measures prove to be insufficient, or if the investment that is required to increase natural gas production and energy generation over the medium-and long-term fails to materialize on a timely basis, economic activity in Argentina could be curtailed which may have a significant adverse effect on our business.