UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended December 31, 2023

[ ] Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to .

Commission File No. 001-35343

Chesapeake Granite Wash Trust

(Exact name of registrant as specified in its charter)

| Delaware | 45-6355635 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| The Bank of New York Mellon Trust Company, N.A., Trustee Global Corporate Trust | ||||||||

| 601 Travis Street, Floor 16 | ||||||||

| Houston, Texas | 77002 | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

| (Registrant’s telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name on each exchange on which registered | ||||||||||||

| None | Not applicable | Not applicable | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [X] No [ ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ ] No [X]

The registrant is a voluntary filer of reports required to be filed by certain companies under Section 13 or 15(d) of the Securities Exchange Act of 1934 and has filed all reports that would have been required to have been filed by the registrant during the preceding 12 months had it been subject to such filing requirements during the entirety of such period.

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [ ] No [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [X] | Smaller reporting company [ ] | Emerging growth company [ ] | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements

of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the 23,000,000 Common Units representing beneficial interests in Chesapeake Granite Wash Trust held by non-affiliates of the registrant, computed using the closing sale price of $1.18 on June 30, 2023, was approximately $27.14 million.

As of March 28, 2024, 46,750,000 Common Units representing beneficial interests in Chesapeake Granite Wash Trust were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Listed below is the only document parts of which are incorporated herein by reference and the parts of this Annual Report into which the document is incorporated:

None

CHESAPEAKE GRANITE WASH TRUST

2023 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| PART I | Page | |||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

Item 1C. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

All references to “we,” “us,” “our,” or the “Trust” refer to Chesapeake Granite Wash Trust. The royalty interests conveyed on November 16, 2011 by Chesapeake Energy Corporation from its interests in certain properties in the Colony Granite Wash formation in Oklahoma and held by the Trust are referred to as the “Royalty Interests.” References to "Chesapeake" refer to Chesapeake Energy Corporation and, where the context requires, its subsidiaries. References to "Tapstone" refer to Tapstone Energy Holdings, LLC or its wholly owned subsidiary Tapstone Energy LLC, as applicable. References to "Diversified" refer to Diversified Energy Company PLC and, where the context requires, its subsidiaries. References to "Operator" refer to (i) Diversified Energy Company PLC and, where the context requires, its subsidiaries at all times after consummation of the Merger (as defined below), (ii) Tapstone Energy, LLC at all times from December 11, 2020 and prior to the consummation of the Merger, and (iii) Chesapeake at all times prior to December 11, 2020. Commencing as of December 7, 2021, Diversified, through Tapstone, its wholly owned subsidiary, owns and operates all Underlying Properties (as defined below) held by the

Trust. Additional information about Diversified, including its presentation of the Merger is available on Diversified's website at www.div.energy.

RISK FACTOR SUMMARY

Our business involves certain risks and uncertainties. The following is a description of significant risks that might cause our future financial condition or results of operations to differ materially from those expected. In addition to the risks and uncertainties described below, we may face other risks and uncertainties, some of which may be unknown to us and some of which we may deem immaterial. A summary of our risk factors is as follows (capitalized terms being defined in the Glossary below):

•Producing oil, natural gas, and NGL on the Underlying Properties is a high-risk activity with many uncertainties.

•Oil, natural gas, and NGL prices fluctuate widely, and lower prices for an extended period of time are likely to have a material adverse effect on proceeds to the Trust and cash distributions to unitholders.

•Actual reserves and future production may be less than current estimates, which could reduce cash distributions by the Trust and the value of the Trust units.

•The sale of the Underlying Properties of the Trust may result in the ownership and management of the Trust by a party that is unfamiliar with the operation of the Trust or the Underlying Properties.

•Due to the Trust's lack of industry and geographic diversification, adverse developments in the Trust's existing area of operation could adversely impact its financial condition, results of operations and cash flows and reduce its ability to make distributions to the unitholders.

•The generation of proceeds for distribution by the Trust depends in part on access to and the operation of gathering, transportation and processing facilities. Any limitation in the availability of those facilities could interfere with sales of oil, natural gas and NGL production from the Underlying Properties.

•The Trust units may lose value and cash available for distribution may be reduced as a result of title deficiencies with respect to the Underlying Properties.

•The oil, natural gas and NGL reserves estimated to be attributable to the Underlying Properties are depleting assets and production from those reserves will diminish over time.

•An increase in the differential between the prices realized by the Operator for oil, natural gas and NGL produced from the Underlying Properties and the NYMEX or other benchmark price of oil or natural gas could reduce the proceeds to the Trust and therefore the cash distributions by the Trust and the value of Trust units.

•Oil and natural gas producing operations can be hazardous and may expose the Operator to liabilities.

•Climate change and the effects of energy transition could result in significant operational changes and expenditures, reduce demand for our services and adversely affect business.

•Negative public perception regarding the Operator or the oil and gas industry could have an adverse effect on the Operator's operations.

•Increases in interest rates may cause the value of the Trust units to decline.

•The amount of cash available for distribution by the Trust will be reduced by post-production expenses and applicable taxes associated with the Royalty Interests and Trust expenses.

•The Trust is passive in nature and will have no voting rights in the Operator managerial, contractual or other ability to influence the Operator, or control over the field operations of, sales of oil, natural gas and NGL from, or development of, the Underlying Properties.

•Financial information of the Trust is not prepared in accordance with U.S. GAAP.

•The Trust is precluded from acquiring other oil and natural gas properties or royalty interests to replace the depleting assets and production.

•The Trustee may, under certain circumstances, sell the Royalty Interests and dissolve the Trust.

•The Trust is administered by a Trustee who cannot be replaced except at a special meeting of Trust unitholders.

•Trust unitholders have limited ability to enforce provisions of the Royalty Interest conveyances, and the Operator's liability to the Trust is limited.

•Courts outside of Delaware may not recognize the limited liability of the Trust unitholders provided under Delaware law.

•Diversified may sell Trust units in the public or private markets and such sales could have an adverse impact on the trading price of the common units.

•Conflicts of interest could arise between the Operator and the Trust.

•The Operator may sell all or a portion of its retained interest in the Underlying Properties, subject to and burdened by the Royalty Interests.

•The Trust units are listed quoted for trading on the OTC Pink marketplace.

•The Operator is subject to extensive governmental regulation, including environmental, which can change and could adversely impact the Operator's business.

•The Trust could be negatively affected by cybersecurity threats.

•The Trust's tax treatment depends on its status as a partnership for U.S. federal income tax purposes.

•The U.S. federal income tax treatment of the Development Royalty Interest is not entirely free from doubt.

•The tax treatment of an investment in Trust units could be affected by recent and potential legislative changes, possibly on a retroactive basis.

•If the IRS contests the tax positions the Trust takes, the value of the Trust units may be adversely affected, the cost of any IRS contest will reduce the Trust's cash available for distribution to Trust unitholders.

•Trust unitholders will be required to pay taxes on their share of the Trust's income even if they do not receive any cash distributions from the Trust.

•Tax gain or loss on the disposition of the Trust units could be more or less than expected.

•Tax-exempt entities and non-U.S. persons face unique tax issues from owning the Trust units that may result in adverse tax consequences to them.

•The Trust will treat each purchaser of Trust units as having the same economic attributes without regard to the actual Trust units purchased.

•The Trust prorates its items of income, gain, loss and deduction between transferors and transferees of the Trust units each quarter based upon the record ownership of the Trust units on the quarterly record date in such quarter, instead of on the basis of the date a particular Trust unit is transferred.

•A Trust unitholder whose Trust units are loaned to a “short seller” to cover a short sale of Trust units may be considered as having disposed of those Trust units.

•The Trust has adopted certain valuation methodologies that may affect the income, gain, loss and deduction allocable to the Trust unitholders.

•Trust unitholders may be subject to state and local taxes and return filing requirements in jurisdictions where they do not live as a result of investing in Trust units.

GLOSSARY OF CERTAIN TERMS

In this Annual Report, the following terms have the meanings specified below. Other terms are defined in the text of this Annual Report.

Administrative Servicer. The company providing the Trust with certain accounting, tax preparation, bookkeeping and information services related to the Royalty Interests and the Registration Rights Agreement in accordance with the Administrative Services Agreement (defined below). Pursuant to an agreement between Tapstone and Chesapeake following the divestiture of the Underlying Properties, (i) Chesapeake served as the Administrative Servicer through the filing of the 2020 Annual Report with the SEC and (ii) Tapstone is the Administrative Servicer for all periods subsequent to the filing of the 2020 Annual Report with the SEC. Following consummation of the Merger (as defined in Part I Item 1. Business), all duties previously performed by Tapstone and its subsidiaries with respect to the Trust are now performed by Diversified.

Administrative Services Agreement. An administrative services agreement the Trust entered into on November 16, 2011 with the Administrative Servicer, effective July 1, 2011, pursuant to which the Administrative Servicer provides the Trust with certain accounting, tax preparation, bookkeeping and information services related to the Royalty Interests and the Registration Rights Agreement.

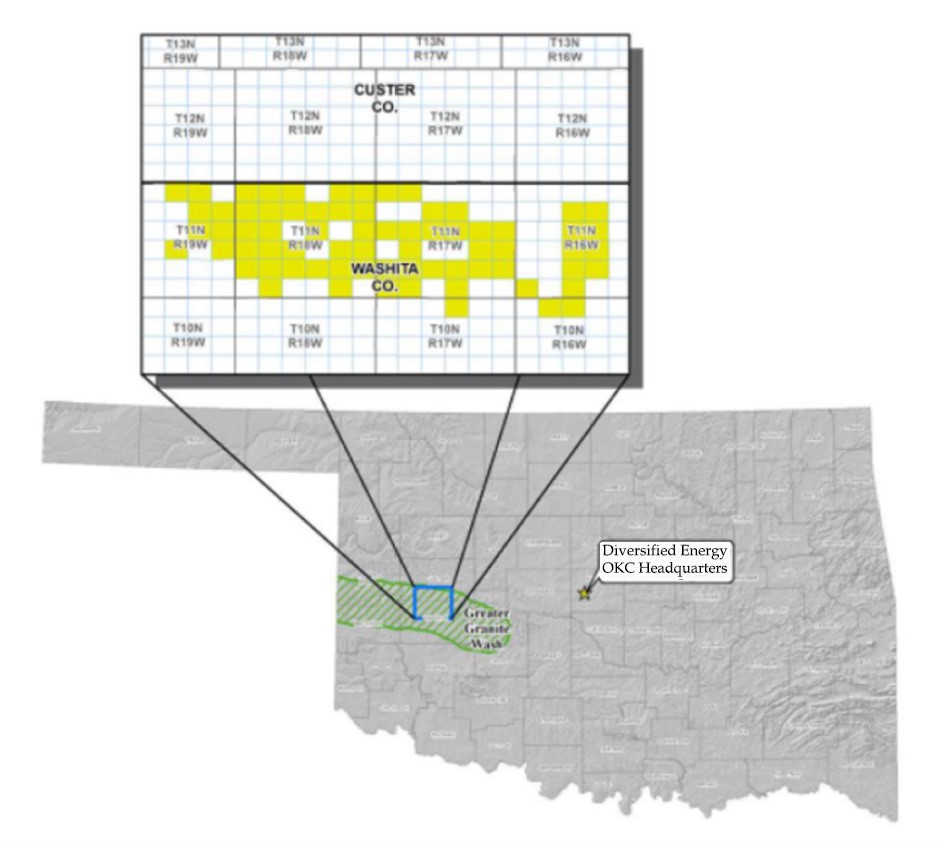

AMI. The area of mutual interest, or AMI, lies within Washita County in western Oklahoma and is limited to the Colony Granite Wash formation in the area identified below, consisting of approximately 40,500 gross acres (26,400 net acres) held by Tapstone as of December 31, 2023.

Assignment Agreement. Assignment and Assumption Agreement, dated as of December 11, 2020, by and among Chesapeake, Chesapeake Exploration, L.L.C., Chesapeake E&P Holding, L.L.C., and Tapstone, pursuant to which Tapstone agreed to assume all duties and obligations of Chesapeake and its subsidiaries under each of the Trust Agreement, the Administrative Services Agreement, the royalty conveyances and the Registration Rights Agreement following the divestiture by Chesapeake of the Underlying Properties and 23,750,000 common units.

Bbl. One stock tank barrel, or 42 U.S. gallons liquid volume, used herein in reference to crude oil or other liquid hydrocarbons.

Boe. Barrel of oil equivalent. Oil equivalent is based on six mcf of natural gas to one barrel of oil or one barrel of NGL. This ratio reflects an energy content equivalency and not a price or revenue equivalency. Despite holding this ratio constant at six mcf to one bbl, prices have historically often been higher or substantially higher for oil than natural gas on an energy equivalent basis, although there have been periods in which they have been lower or substantially lower.

Btu. British thermal unit, which is the quantity of heat required to raise the temperature of a one-pound mass of water from 58.5 to 59.5 degrees Fahrenheit.

Completion. The process of treating a drilled well followed by the installation of permanent equipment for the production of oil, natural gas or natural gas liquids, or in the case of a dry well, reporting to the appropriate authority that the well has been abandoned.

Condensate. A mixture of hydrocarbons that exists in the gaseous phase at the original reservoir temperature and pressure, but that, when produced, is in the liquid phase at surface pressure and temperature.

Developed Acreage. The number of acres which are allocated or assignable to producing wells or wells capable of production.

Development Costs. Costs incurred to obtain access to proved reserves and to provide facilities for extracting, treating, gathering and storing the oil and natural gas. More specifically, development costs, including depreciation and applicable operating costs of support equipment and facilities and other costs of development activities, are costs incurred to (a) gain access to and prepare well locations for drilling, including surveying well locations for the purpose of determining specific development drilling sites, clearing ground, draining, road building and relocating public roads, gas lines and power lines, to the extent necessary in developing the proved reserves, (b) drill and equip Development Wells, development-type stratigraphic test wells and service wells, including the costs of platforms and of well equipment such as casing, tubing, pumping equipment, and the wellhead assembly, (c) acquire, construct and install production facilities such as leases, flow lines, separators, treaters, heaters, manifolds, measuring devices and production storage tanks, natural gas cycling and processing plants, and central utility and waste disposal systems, and (d) provide improved recovery systems.

Development Well. As defined by the SEC, a development well is a well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive. For the purposes of the Trust and as used herein, references to “Development Wells” refer to the 118 horizontal development wells that, since July 1, 2011, have been drilled on properties held by the Operator in the AMI and in which the Trust has received an interest.

Dry Well. A well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion as an oil or natural gas well.

Economically Producible. The term economically producible, as it relates to a resource, means a resource which generates revenue that exceeds, or is reasonably expected to exceed, the costs of the operation. The value of the products that generate revenue is determined at the terminal point of oil and gas producing activities as defined in Rule 4-10(a)(16) of Regulation S-X under the Securities Act.

Estimated Future Net Revenues. The result of applying current prices of oil, natural gas and NGL to estimated future production from oil, natural gas and NGL proved reserves, reduced by estimated future expenditures, based on current costs to be incurred, in developing and producing the proved reserves, excluding overhead.

Field. An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition. There may be two or more reservoirs in a field which are separated vertically by intervening impervious strata, or laterally by local geologic barriers, or both. Reservoirs that are associated by being in overlapping or adjacent fields may be treated as a single or common operational field. The geological terms "structural feature" and "stratigraphic condition" are intended to identify localized geological features as opposed to the broader terms of basins, trends, provinces, plays or areas of interest.

GAAP. Generally Accepted Accounting Principles in the United States.

Gross Acres or Gross Wells. The total acres or wells, as the case may be, in which a working interest is owned.

IRS. The Internal Revenue Service of the United States federal government.

Mbbl. One thousand barrels of crude oil or other liquid hydrocarbons.

Mboe. One thousand barrels of oil equivalent.

Mcf. One thousand cubic feet.

Mmcf. One million cubic feet.

Net Acres or Net Wells. The sum of the fractional working interest owned in gross acres or gross wells, respectively.

Net Revenue Interest. A share of production after all burdens, such as royalty and overriding royalty interests, have been deducted from the working interest.

Natural Gas Liquids (NGL). Hydrocarbons in natural gas that are separated from the gas as liquids through the process of absorption, condensation, adsorption or other methods in gas processing or cycling plants. Natural gas liquids primarily include ethane, propane, butane, isobutene, pentane, hexane and natural gasoline.

NYMEX. New York Mercantile Exchange.

Operator. The company that holds the AMI, owns the Underlying Properties and is bound by the terms of the Trust Agreement. Following the consummation of the Merger (as defined below), Diversified Energy Company PLC and, where the context requires, its subsidiaries, became the Operator.

Participation Agreement. Participation Agreement, dated October 2, 2020, by and between Operator and OCM Denali Holdings, LLC, which agreement was not in existence as of the date of the Conveyances and is a permitted encumbrance under the Conveyances. The agreement relates to the Underlying Properties.

Plugging and Abandoning. Refers to the sealing off of fluids in the strata penetrated by a well so that the fluids from one stratum will not escape into another or to the surface. Oklahoma regulations require plugging of abandoned wells.

Present Value of Estimated Future Net Revenues or PV-10 (non-GAAP). When used with respect to oil, natural gas and NGL reserves, present value of estimated future net revenues, or PV-10, means the estimated future revenue to be generated from the production of proved reserves, net of estimated production and future development costs, using prices calculated as the average oil and natural gas price during the preceding 12-month period prior to the end of the current reporting period, (determined as the unweighted arithmetic average of prices on the first day of each month within the 12-month period) and costs in effect at the determination date (unless such costs are subject to change pursuant to contractual provisions), without giving effect to non-property related expenses such as general and administrative expenses, debt service and future income tax expense or to depreciation, depletion and amortization, discounted using an annual discount rate of 10%. PV-10 is a non-GAAP financial measure and generally differs from the standardized measure of discounted net cash flows, or Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes on future net revenues. Because the Trust will not bear income tax expense, the PV-10 and Standardized Measure attributable to the Royalty Interests are the same.

Price Differential. The difference in the price of oil, natural gas or NGL received at the sales point and the NYMEX price.

Producing Well. As defined by the SEC, a producing well is a well that is found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of such production exceed production expenses and taxes. For the purposes of the Trust and as used herein, references to “Producing Wells” refer to the 69 existing horizontal wells in which Chesapeake conveyed an interest to the Trust effective as of July 1, 2011.

Production Expenses. Costs incurred to operate and maintain wells and related equipment and facilities, including depreciation and applicable operating costs of support equipment and facilities and other costs of operating and maintaining those wells and related equipment and facilities. They become part of the cost of oil, natural gas and NGL produced. Examples of production expenses (sometimes called lifting expenses) are:

•costs of labor to operate the wells and related equipment and facilities;

•repairs and maintenance;

•materials, supplies and fuel consumed as well as supplies utilized in operating the wells and related equipment and facilities;

•property taxes and insurance applicable to proved properties and wells and related equipment and facilities; and

•production taxes.

Some support equipment or facilities may serve two or more oil and natural gas producing activities and may also serve transportation, refining and marketing activities. To the extent that the support equipment and facilities are used in oil and gas producing activities, their depreciation and applicable operating costs become exploration, development or production expenses, as appropriate. Depreciation, depletion and amortization of capitalized acquisition, exploration, and development costs are not production expenses but also become part of the cost of oil and natural gas produced along with production (lifting) costs identified above.

Productive Well. A well that is not a dry well. Productive wells include producing wells and wells that are mechanically capable of production.

Prospectus. The Trust Prospectus dated November 10, 2011 and filed with the SEC on November 14, 2011, in connection with the initial public offering of the Trust's common units.

Proved Developed Reserves. Proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well.

Proved Reserves. As used in this report, proved reserves has the meaning given to such term in Rule 4-10(a)(22) of Regulation S-X, which states in part proved oil and natural gas reserves are those quantities of oil and natural gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible - from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations - prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation.

Proved Undeveloped Reserves (PUDs). Proved reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively high expenditure is required. Reserves on undrilled acreage are limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances.

Registration Rights Agreement. Registration Rights Agreement dated as of November 16, 2011, by and among Tapstone (as successor to Chesapeake and Chesapeake Exploration, L.L.C.) and the Trust.

Reserves. Estimated remaining quantities of oil and natural gas and related substances anticipated to be economically producible as of a given date, by application of development projects to known accumulations. In addition, there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil and natural gas or related substances to market, and all permits and financing required to implement the project. Reserves should not be assigned to adjacent reservoirs isolated by major, potentially sealing, faults until those reservoirs are penetrated and evaluated as economically producible. Reserves should not be assigned to areas that are clearly separated from a known accumulation by a non-productive reservoir (i.e., absence of reservoir, structurally low reservoir, or negative test results). Such areas may contain prospective resources (i.e., potentially recoverable resources from undiscovered accumulations).

Reservoir. A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

SEC. The United States Securities and Exchange Commission.

Standardized Measure. The discounted future net cash flows relating to proved reserves based on the means of the estimated future gross revenue to be generated from the production of proved reserves, net of estimated production and future development costs, using prices calculated as the average oil and natural gas price during the preceding 12-month period prior to the end of the current reporting period (determined as the unweighted arithmetic average of prices on the first day of each month within the 12-month period). The standardized measure differs from the PV-10 measure only because the former includes the effects of estimated future income tax expenses.

Underlying Properties. Interests in specified oil and natural gas properties located in the Colony Granite Wash play in Washita County in the Anadarko Basin of western Oklahoma.

Undeveloped Acreage. Acreage on which wells have not been drilled or completed to a point that would permit the production of economic quantities of oil and natural gas regardless of whether such acreage contains proved reserves.

Working Interest. The operating interest which gives the owner the right to drill, produce and conduct operating activities on the property and a share of production.

DISCLOSURES REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (“Annual Report” or "Form 10-K") includes “forward-looking statements” about the Trust and the Operator and other matters discussed herein that are subject to risks and uncertainties that are intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995, and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). All statements other than statements of historical fact included in this document are forward-looking statements, including, without limitation, statements under “Trustee’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of Part II and “Risk Factors” in Item 1A of Part I and elsewhere herein regarding market factors, market prices, the proved oil, natural gas and NGL reserves associated with the properties underlying the Royalty Interests, the Trust’s or the Operator's future financial position, business strategy, budgets, projected costs and plans and objectives for future operations, information regarding target distributions, statements pertaining to future development activities and costs and information regarding production and reserve growth, statements regarding the continued trading of the Trust's common units on the Pink Open Market operated by OTC Markets Group, Inc. (the "OTC Pink"), statements regarding the expected impact of geopolitical events, including the ongoing conflicts in Ukraine and Israel, and actions by, or disputes among or between, members of the Organization of the Petroleum Exporting Countries and its allies, in each case on our and the Operator's business, financial condition, results of operations and cash flows. Our forward-looking statements are generally accompanied by words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “could,” “may,” “foresee,” “seek,” “plan,” “goal,” “assume,” “target,” “should,” “intend," "ability," "will," "would," "forecast" or other words that convey the uncertainty of future events or outcomes. Actual outcomes and results may differ materially from those projected. These forward-looking statements are based on certain assumptions made by the Trust, and by the Operator in light of its experience and perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate under the circumstances. However, whether actual results and developments will conform with such expectations and predictions is subject to a number of risks and uncertainties, including the risk factors discussed in Item 1A of Part I of this Annual Report, which could affect the future results of the energy industry in general, and the Trust and the Operator in particular, and could cause those results to differ materially from those expressed in such forward-looking statements. These factors should not be construed as exhaustive, and there may also be other risks that we are unable to predict at this time. The actual results or developments anticipated may not be realized or, even if substantially realized, they may not have the expected consequences to or effects on the Operator's business and the Trust. Such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in such forward-looking statements. The Trustee relies on the Operator for information regarding the Royalty Interests, the Underlying Properties and the Operator itself. The Trust undertakes no obligation to publicly update or revise any forward-looking statements and expressly disclaims any obligation to do so, except as required by applicable law.

PART I

ITEM 1.Business

Introduction

The Trust is a statutory trust formed in June 2011 under the Delaware Statutory Trust Act pursuant to an initial trust agreement by and among the Operator, as Trustor, The Bank of New York Mellon Trust Company, N.A., as Trustee (the “Trustee”), and The Corporation Trust Company, as Delaware Trustee (the “Delaware Trustee”). The Trust maintains its offices at the office of the Trustee, which is located at 601 Travis Street, Floor 16, Houston, Texas 77002, and the telephone number of the Trustee is (512) 235-6555.

The Trustee maintains a website for filings by the Trust with the SEC. Electronic filings by the Trust with the SEC are available free of charge through the Trust's website at www.chkgranitewashtrust.com and through the SEC's website at www.sec.gov. The Trust will also provide electronic and paper copies of its recent filings free of charge upon request to the Trustee. Documents and information on the Trust's website are not incorporated by reference herein.

General

The Trust was created to own the Royalty Interests for the benefit of Trust unitholders pursuant to a trust agreement dated as of June 29, 2011 and subsequently amended and restated as of November 16, 2011 by and among Tapstone (as successor to Chesapeake and Chesapeake Exploration, L.L.C., a wholly owned subsidiary of Chesapeake), the Trustee and the Delaware Trustee (the “Trust Agreement”). The Royalty Interests are derived from the Underlying Properties. Chesapeake conveyed the Royalty Interests to the Trust from Chesapeake's interests in the Producing Wells and the Development Wells.

The business and affairs of the Trust are managed by the Trustee. The Trust Agreement limits the Trust's business activities generally to owning the Royalty Interests and any activity reasonably related to such ownership, including activities required or permitted by the terms of the conveyances applicable to the Royalty Interests. The royalty interests in the Producing Wells (the “PDP Royalty Interest”) entitle the Trust to receive 90% of the proceeds (exclusive of any production or development costs but after deducting certain post-production expenses and any applicable taxes) from the sales of oil, natural gas and NGL production attributable to the Operator's net revenue interest in the Producing Wells. The royalty interests in the Development Wells (the “Development Royalty Interest”) entitle the Trust to receive 50% of the proceeds (exclusive of any production or development costs but after deducting certain post-production expenses and any applicable taxes) from the sales of oil, natural gas and NGL production attributable to the Operator's net revenue interest in the Development Wells.

Through an initial public offering in November 2011, the Trust sold to the public 23,000,000 common units, representing beneficial interests in the Trust, for cash proceeds of approximately $409.7 million, net of offering costs. The Trust delivered the net proceeds of the initial public offering, along with 12,062,500 common units and 11,687,500 subordinated units, to certain wholly owned subsidiaries of Chesapeake in exchange for the conveyance of the Royalty Interests to the Trust. Upon completion of these transactions, there were 46,750,000 Trust units issued and outstanding, consisting of 35,062,500 common units and 11,687,500 subordinated units, which were converted into common units on a one-for-one basis as of June 30, 2017. On December 11, 2020, Chesapeake sold its 23,750,000 common units to Tapstone in a sale that included the Underlying Properties of the Trust.

On October 6, 2021, Tapstone Energy Holdings, LLC, a Delaware limited liability company and the parent of Tapstone, ("Tapstone Holdings"), entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Diversified, the parent of Diversified Production LLC (“Diversified Production”), and certain of its affiliates, including Diversified Production. Upon the terms and subject to the conditions set forth in the Merger Agreement, a wholly owned subsidiary of Diversified merged with and into Tapstone Holdings with Tapstone Holdings as the surviving entity, resulting in Tapstone Holdings and Tapstone becoming wholly owned subsidiaries of Diversified. The transactions provided for under the Merger Agreement were consummated on December 7, 2021, and Tapstone Holdings became a wholly owned subsidiary of Diversified on such date (the “Merger”). Following the Merger, the 23,750,000 common units previously held by Tapstone Energy LLC were transferred to Diversified Production, another indirect, wholly-owned subsidiary of Diversified. Subsequently, on September 22, 2023, the 23,750,000

1

common units were transferred to DP Bluegrass LLC ("DP Bluegrass"), an indirect, wholly-owned subsidiary of Diversified Production.

Following consummation of the Merger, duties previously performed by Tapstone and its subsidiaries with respect to the Trust are now performed by Diversified.

Tapstone’s right, title and interest in and to, and all of their duties and obligations under all documents related to the Trust (including the Amended and Restated Trust Agreement (dated as of November 16, 2011), the Administrative Services Agreement (dated as of November 16, 2011) and the related royalty interest conveyances) remain unchanged as a result of the Merger, although there have been certain changes in the management of the Underlying Properties. However, as a result of the Merger, Diversified may be deemed the beneficial owner of the 23,750,000 common units of the Trust, now held by DP Bluegrass, representing the entire 50.8% beneficial ownership interest in the Trust held by Tapstone immediately prior to the effective time of the Merger.

Neither the Trust nor the Trustee is responsible for, or has any control over, any operating or capital costs of the Underlying Properties. The Trust's cash receipts with respect to the Royalty Interests in the Underlying Properties are determined after deducting certain post-production expenses and any applicable taxes associated with the Royalty Interests. Post-production expenses generally consist of costs incurred to gather, store, compress, transport, process, treat, dehydrate and market the oil, natural gas and NGL produced. However, the Trust is not responsible for costs of marketing services provided by affiliates of the Operator. Cash distributions to unitholders will continue to be reduced by the Trust's general and administrative expenses.

The Trust will dissolve and begin to liquidate on June 30, 2031 (the “Termination Date”), or earlier upon certain events, and will soon thereafter wind up its affairs and terminate. At the Termination Date, (a) 50% of the total Royalty Interests conveyed by the Operator (the “Term Royalties”) will revert automatically to the Operator and (b) 50% of the total Royalty Interests conveyed by the Operator (the “Perpetual Royalties”) will be retained by the Trust and thereafter sold. The net proceeds of the sale of the Perpetual Royalties, as well as any remaining Trust cash reserves, will be distributed to the unitholders on a pro rata basis. The Operator will have a right of first refusal to purchase the Perpetual Royalties retained by the Trust at the Termination Date.

The Trust is required to make quarterly cash distributions of substantially all of its quarterly cash receipts, after deducting the Trust's administrative expenses and any cash reserves, on or about 60 days following the completion of each quarter through (and including) the quarter ending June 30, 2031. Quarterly distributions to Trust unitholders will generally include royalty income attributable to sales of oil, natural gas and NGL for three months, including the first two months of the quarter just ended and the last month of the quarter prior to that one. The first quarterly distribution was made on December 28, 2011 to record unitholders as of December 15, 2011.

Actual cash distributions to the Trust unitholders will fluctuate quarterly based on the quantity of oil, natural gas, and NGL sold from the Underlying Properties, the prices received for such sales, the timing of the Operator's receipt of payment for such sales, the Trust's expenses and other factors. Target distributions will decline over time as a result of the depletion of the reserves in the Underlying Properties.

For the year ended December 31, 2023, the Trust declared and paid the following cash distributions:

| Production Period | Distribution Date | Cash Distribution per Common Unit | ||||||||||||

| June 2023 – August 2023 | November 30, 2023 | $ | 0.0336 | |||||||||||

| March 2023 - May 2023 | August 31, 2023 | $ | 0.0178 | |||||||||||

| December 2022 - February 2023 | June 1, 2023 | $ | 0.0487 | |||||||||||

| September 2022 - November 2022 | March 1, 2023 | $ | 0.0757 | |||||||||||

___________________________________________________

2

Subsequent Distribution. The Trust's quarterly income available for distribution was $0.0214 per common unit for the production period from September 1, 2023 to November 30, 2023. On February 5, 2024, the Trust declared a cash distribution of $0.0214 per common unit attributable to such production period. The distribution was paid on February 29, 2024 to record unitholders as of February 19, 2024. All Trust unitholders share on a pro rata basis in the Trust's distributable income.

As of March 28, 2024, DP Bluegrass held 23,750,000 common units, which represent 50.8% of the outstanding Trust units. Diversified is the ultimate parent company of DP Bluegrass, and therefore is deemed to beneficially own the common units held by DP Bluegrass.

Administrative Services Agreement

In return for the services provided by the Administrative Servicer under the Administrative Services Agreement, the Trust pays the Administrative Servicer an annual fee of $200,000, which is paid in equal quarterly installments and remains fixed for the life of the Trust. The Administrative Servicer is also entitled to receive reimbursement for its actual out-of-pocket fees, costs and expenses incurred in connection with the provision of any of the services under the agreement.

The Administrative Services Agreement will terminate upon the earliest to occur of (a) the date the Trust shall have been wound up in accordance with the Trust Agreement, (b) the date that all of the Royalty Interests have been terminated or are no longer held by the Trust, (c) with respect to services to be provided with respect to any Underlying Properties being transferred by the Operator, the date that either the Administrative Servicer or the Trustee may designate by delivering 90-days prior written notice, provided that the transferee of such Underlying Properties assumes responsibility to perform the services in place of the Administrative Servicer or (d) a date mutually agreed by the Administrative Servicer and the Trustee.

Description of the Trust

Common Units. Each Trust unit is a unit of the beneficial interest in the Trust and is entitled to receive cash distributions from the Trust on a pro rata basis. The Trust has 46,750,000 Trust units issued and outstanding, all of which are common units.

Distributions and Income Computations. The Trust is required to make quarterly cash distributions to unitholders from its available funds for such calendar quarter. Royalty Interest payments due to the Trust with respect to any calendar quarter are based on actual sales volumes attributable to the Trust's interests in the Underlying Properties (as measured at the Operator's metering systems) for the first two months of the quarter just ended as well as the last month of the immediately preceding quarter and actual revenues, net of post-production expenses received for such volumes. The Operator makes the Royalty Interest payments to the Trust within 35 days of the end of each calendar quarter. Taking into account the receipt and disbursement of all such amounts, the Trustee determines for such calendar quarter the amount of funds available for distribution to the Trust unitholders. Available funds are the excess cash, if any, received by the Trust over the Trust's expenses for that quarter. Available funds are reduced by any cash the Trustee decides to hold as a reserve against future liabilities.

The Trustee distributes cash approximately 60 days (or the next succeeding business day following such day if such day is not a business day) following each calendar quarter to each person who is a Trust unitholder of record on the quarterly record date together with interest expected to be earned on the amount of such quarterly distribution from the date of receipt thereof by the Trustee to the payment date.

Unless otherwise advised by counsel or the IRS, the Trustee treats the income and expenses of the Trust for each quarter as belonging to the Trust unitholders of record on the quarterly record date that occurs in such quarter. Trust unitholders recognize income and expenses for tax purposes in the quarter the Trust receives or pays those amounts, rather than in the quarter the Trust distributes them. Minor variances may occur. For example, the Trustee could establish a reserve in one quarter that would not result in a tax deduction until a later quarter. The Trustee could also make a payment in one quarter that would be amortized for tax purposes over several months.

Transfer of Trust Units. Trust unitholders may transfer their Trust units in accordance with the Trust Agreement. The Trustee does not require either the transferor or transferee to pay a service charge for any transfer of a Trust unit. The Trustee may require payment of any tax or other governmental charge imposed for a transfer. The Trustee may treat the owner of any Trust unit as shown by its records as the owner of the Trust unit. The Trustee will not be

3

considered to know about any claim or demand on a Trust unit by any party except the record owner. A person who acquires a Trust unit after any quarterly record date will not be entitled to the distribution relating to that quarterly record date. Delaware law will govern all matters affecting the title, ownership or transfer of Trust units.

Periodic Reports. The Trustee files all required Trust federal and state income tax and information returns. The Trustee prepares and mails to Trust unitholders a Schedule K-1 and also causes to be prepared and filed reports required to be filed under the Exchange Act, and by the rules any securities exchange or quotation system on which the Trust units are listed or admitted to trading.

Each Trust unitholder and his representatives have the right, at his own expense and during reasonable business hours upon reasonable prior notice, to examine and inspect the records of the Trust and the Trustee in reference thereto for any purpose reasonably related to the Trust unitholder's interest as a Trust unitholder.

Liability of Trust Unitholders. Under the Delaware Statutory Trust Act, Trust unitholders are entitled to the same limitation of personal liability extended to stockholders of private corporations for profit under the General Corporation Law of the State of Delaware. No assurance can be given, however, that the courts in jurisdictions outside of Delaware will give effect to such limitation.

Voting Rights of Trust Unitholders. The Trustee or Trust unitholders owning at least 10% of the outstanding Trust units may call meetings of Trust unitholders. The Trust does not intend to hold annual meetings of the Trust unitholders. The Trust is responsible for all costs associated with calling a meeting of Trust unitholders unless such meeting is called by the Trust unitholders, in which case the Trust unitholders are responsible for all costs associated with calling such meeting of Trust unitholders. Meetings must be held in such location as is designated by the Trustee in the notice of such meeting. The Trustee must send written notice of the time and place of the meeting and the matters to be acted upon to all of the Trust unitholders at least 20 days and not more than 60 days before the meeting. Trust unitholders representing a majority of Trust units outstanding must be present or represented to have a quorum. Each Trust unitholder is entitled to one vote for each Trust unit owned. Abstentions and broker non-votes shall not be deemed to be a vote cast.

Unless otherwise required by the Trust Agreement, a matter may be approved or disapproved by the vote of a majority of the Trust units held by the Trust unitholders voting in person or by proxy at a meeting where there is a quorum. Accordingly, a matter may be approved even if a majority of the total outstanding Trust units does not approve it.

Until such time as Diversified and its affiliates own less than 10% of the outstanding Trust units, the affirmative vote of the holders of a majority of common units (excluding common units owned by Diversified and its affiliates) and a majority of Trust units voting in person or by proxy at a meeting of such holders at which a quorum is present is required to:

•dissolve the Trust (except in accordance with its terms);

•remove the Trustee or the Delaware Trustee;

•amend the Trust Agreement, the royalty conveyances, the Administrative Services Agreement and the development agreement (except with respect to certain matters that do not adversely affect the rights of Trust unitholders in any material respect);

•merge, consolidate or convert the Trust with or into another entity; or

•approve the sale of all or any material part of the assets of the Trust.

At any time when Diversified and its affiliates own less than 10% of the outstanding Trust units, the vote of the holders of a majority of Trust units, including units owned by Diversified, voting in person or by proxy at a meeting of such holders at which a quorum is present will be required to take the actions described above. Notwithstanding the foregoing, there are conflicting interpretations that the Trust Agreement requires the exclusion of the common units owned by Diversified and its affiliates in a vote following Tapstone's acquisition of the Underlying Properties from Chesapeake even if Diversified and its affiliates own over 10% of the outstanding Trust units.

Certain amendments to the Trust Agreement may be made by the Trustee without approval of the Trust unitholders. The Trustee must consent before all or any part of the Trust assets can be sold except in connection with the dissolution of the Trust or limited sales directed by Diversified in conjunction with its sale of Underlying Properties.

4

Description of the Trust Agreement. The Trust was created under Delaware law as a separate legal entity to acquire and hold the Royalty Interests for the benefit of the Trust unitholders pursuant to the Trust Agreement among the Operator, the Trustee and the Delaware Trustee. The Royalty Interests are passive in nature and neither the Trust nor the Trustee has any control over, or responsibility for, costs relating to the operation of the Underlying Properties. Neither the Operator nor other operators of the Underlying Properties have any contractual commitments to the Trust to provide additional funding for, to conduct further drilling on or to maintain their ownership interest in any of these properties.

The Trust Agreement provides that the Trust's business activities are generally limited to owning the Royalty Interests and any activities reasonably related thereto, including activities required or permitted by the terms of the conveyances related to the Royalty Interests. As a result, the Trust is not generally permitted to acquire other oil, natural gas and NGL properties or royalty interests. The Trust is not able to issue any additional Trust units.

Contractual Rights and Assets of the Trust. Contractual rights of the Trust include those contained in the development agreement and the Administrative Services Agreement. The assets of the Trust consist of the Royalty Interests and any cash and temporary investments being held for the payment of expenses and liabilities and for distribution to the Trust unitholders.

Duties and Powers of the Trustee. The duties and powers of the Trustee are specified in the Trust Agreement and by the laws of the State of Delaware, except as modified by the Trust Agreement. The Trust Agreement provides that the Trustee shall not have any duties or liabilities, including fiduciary duties, except as expressly set forth in the Trust Agreement and the duties and liabilities of the Trustee as set forth in the Trust Agreement replace any other duties and liabilities, including fiduciary duties, to which the Trustee might otherwise be subject.

The Trustee's principal duties consist of:

•collecting cash proceeds attributable to the Royalty Interests;

•paying expenses, charges and obligations of the Trust from the Trust's assets;

•making cash distributions to the unitholders and the Operator (with respect to incentive distributions) in accordance with the Trust Agreement;

•causing to be prepared and distributed a Schedule K-1 for each Trust unitholder and preparing and filing tax returns on behalf of the Trust; and

•causing to be prepared and filed reports required to be filed under the Exchange Act, and by the rules of any securities exchange or quotation system on which the Trust units are listed or admitted to trading.

The Administrative Servicer will provide administrative and other services to the Trust in fulfillment of certain of the foregoing duties pursuant to the Administrative Services Agreement.

The Trustee may create a cash reserve to pay for future expenses of the Trust. If the Trustee determines that the cash on hand and the cash to be received are insufficient to cover the Trust's expenses, the Trustee may cause the Trust to borrow funds required to pay the expenses. The Trust may borrow the funds from any person, including the Trustee or its affiliates or, as described below, the Operator. The terms of such indebtedness, if funds were loaned by the entity serving as Trustee or Delaware Trustee, must be similar to the terms which such entity would grant to a similarly situated, unaffiliated commercial customer, and such entity shall be entitled to enforce its rights with respect to any such indebtedness as if it were not then serving as Trustee or Delaware Trustee. If the Trust borrows funds, the Trust unitholders will not receive distributions until the borrowed funds are repaid (except in certain circumstances where the Trust borrows funds from the Operator).

5

Each quarter, the Trustee will pay Trust obligations and expenses and distribute to the Trust unitholders the remaining proceeds received from the Royalty Interests. The cash held by the Trustee as a reserve against future liabilities must be invested in:

•interest-bearing obligations of the U.S. government;

•money market funds that invest only in U.S. government securities;

•repurchase agreements secured by interest-bearing obligations of the U.S. government; or

•bank certificates of deposit.

Alternatively, cash held for distribution at the next distribution date may be held in a non-interest bearing account.

The Trustee withheld approximately $1.0 million from the first distribution to establish an initial cash reserve available for Trust expenses. If the Trustee uses its cash reserve (or any portion thereof) to pay or reimburse Trust liabilities or expenses, no further distributions will be made to unitholders (except in respect of any previously determined quarterly cash distribution amount) until the cash reserve is replenished. Additional cash reserves may also be established from time to time as determined by the Trustee to pay for future expenses of the Trust. This cash reserve will be part of the Trust estate and will bear interest at the same rate as other cash on hand in the Trust estate. Upon the dissolution of the Trust, after payment of Trust liabilities, the balance of the cash reserve (including accrued interest thereon) will be distributed to Trust unitholders on a pro rata basis.

The Trust may not acquire any asset except the Royalty Interests, the other assets described above under Contractual Rights and Assets of the Trust and cash and temporary cash investments, and it may not engage in any investment activity except investing cash on hand.

The Trust Agreement provides that the Trustee will not make business decisions affecting the assets of the Trust. However, the Trustee may:

•prosecute or defend, and settle, claims of or against the Trust or its agents;

•retain professionals and other third parties to provide services to the Trust;

•charge for its services as Trustee;

•retain funds to pay for future expenses and deposit them with one or more banks or financial institutions (which may include the Trustee to the extent permitted by law);

•lend funds at commercial rates to the Trust to pay the Trust's expenses; and

•seek reimbursement from the Trust for its out-of-pocket expenses.

In discharging its duty to Trust unitholders, the Trustee may act in its discretion and will be liable to the Trust unitholders only for willful misconduct, bad faith or gross negligence, and certain taxes, fees and other charges based on fees, commissions or compensation received by the Trustee in connection with the transactions contemplated by the Trust Agreement. The Trustee is not liable for any act or omission of its agents or employees unless the Trustee acts with willful misconduct, bad faith or gross negligence in its selection and retention. The Trustee will be indemnified individually or as the Trustee for any liability or cost that it incurs in the administration of the Trust, except in cases of willful misconduct, bad faith or gross negligence. The Trustee has a lien on the assets of the Trust as security for this indemnification and its compensation earned as Trustee. Trust unitholders are not liable to the Trustee for any indemnification. The Trustee is obligated to ensure that all contractual liabilities of the Trust are limited to the assets of the Trust.

The Trust may merge or consolidate with or into, or convert into, one or more limited partnerships, general partnerships, corporations, business trusts, limited liability companies, or associations or unincorporated businesses if such transaction is agreed to by the Trustee and approved by the vote of the holders of a majority of the Trust units and a majority of the common units (excluding common units owned by Diversified and its affiliates) in each case voting in person or by proxy at a meeting of such holders at which a quorum is present and such transaction is permitted under the Delaware Statutory Trust Act and any other applicable law. At any time that Diversified and its affiliates collectively own less than 10% of the outstanding Trust units, however, the standard for approval will be the vote of a majority of the Trust units, including units owned by Diversified voting in person or by proxy at a meeting of such holders at which a quorum is present. Notwithstanding the foregoing, there are conflicting interpretations that

6

the Trust Agreement requires the exclusion of the common units owned by Diversified and its affiliates in a vote following Tapstone's acquisition of the Underlying Properties from Chesapeake even if Diversified and its affiliates own over 10% of the outstanding Trust units.

Trustee's Power to Sell Trust Assets. The Trustee may sell Trust assets, including the Royalty Interests, under any of the following circumstances:

•the sale is requested by Diversified, in accordance with the provisions of the Trust Agreement; or

•the sale is approved by the vote of holders representing a majority of the Trust units and a majority of the common units (excluding common units owned by Diversified and its affiliates) in each case voting in person or by proxy at a meeting of such holders at which a quorum is present; except that at any time that Diversified and its affiliates collectively own less than 10% of the outstanding Trust units, the standard for approval will be the vote of a majority of the Trust units, including units owned by Diversified voting in person or by proxy at a meeting of such holders at which a quorum is present. Notwithstanding the foregoing, there are conflicting interpretations that the Trust Agreement requires the exclusion of the common units owned by Diversified and its affiliates in a vote following Tapstone's acquisition of the Underlying Properties from Chesapeake even if Diversified and its affiliates own over 10% of the outstanding Trust units.

Upon dissolution of the Trust, the Trustee must sell the remaining Royalty Interests. No Trust unitholder approval is required in this event.

The Trustee will distribute the net proceeds from any sale of the Royalty Interests and other assets to the Trust unitholders after payment or reasonable provision for payment of the liabilities of the Trust.

Dispute Resolution. To the fullest extent permitted by law, any dispute, controversy or claim that may arise between the Operator and the Trustee relating to the Trust will be submitted to binding arbitration before a panel of three arbitrators.

Trust Fees and Expenses. It is expected that the Trust will only incur liabilities for routine administrative expenses, such as legal, accounting, audit, tax advisory, engineering, printing and other administrative and out-of-pocket fees and expenses incurred by or at the direction of the Trustee or the Delaware Trustee, including tax return and Schedule K-1 preparation and mailing costs; independent auditor fees; and registrar and transfer agent fees. The Trust is also responsible for paying costs associated with annual and quarterly reports to unitholders. Moreover, the Trustee's and the Delaware Trustee's compensation, and the fee payable to the Administrative Servicer pursuant to the Administrative Services Agreement, are paid out of the Trust's assets.

The Operator's Obligation to Fund Trust Expenses in Certain Circumstances. The Operator has agreed that, if at any time the Trust's cash on hand (including available cash reserves) is not sufficient to pay the Trust's ordinary course expenses as they become due, the Operator will lend funds to the Trust necessary to pay such expenses. Any funds loaned by the Operator pursuant to this commitment will be limited to the payment of current accounts payable or other obligations to trade creditors in connection with obtaining goods or services or the payment of other accrued current liabilities arising in the ordinary course of the Trust's business, and may not be used to satisfy Trust indebtedness for borrowed money. If the Operator lends funds pursuant to this commitment, unless the Operator agrees otherwise, no further distributions will be made to unitholders (except in respect of any previously determined quarterly cash distribution amount) until such loan is repaid. Any such loan will be on an unsecured basis. There were no loans outstanding as of December 31, 2023 or December 31, 2022.

Duration of the Trust; Sale of Royalty Interests. The Trust will dissolve and begin to liquidate on the Termination Date, or earlier upon the occurrence of certain events, and will soon thereafter wind up its affairs and terminate. At the Termination Date, the Term Royalties will revert automatically to the Operator. Following the Termination Date, the Perpetual Royalties will be sold by the Trust and the net proceeds of the sale, as well as any remaining Trust cash reserves, will be distributed to the unitholders pro rata. The Operator will have a right of first refusal to purchase the Perpetual Royalties from the Trust following the Termination Date.

7

The Trust will not dissolve until the Termination Date, unless:

•the Trust sells all of the Royalty Interests;

•the aggregate quarterly cash distribution amounts for any four consecutive quarters is less than $1.0 million;

•the holders of a majority of the Trust units and a majority of the common units (excluding common units owned by Diversified and its affiliates) in each case voting in person or by proxy at a meeting of such holders at which a quorum is present vote in favor of dissolution; except that at any time that Diversified and its affiliates collectively own less than 10% of the outstanding Trust units, the standard for approval will be a majority of the Trust units, including units owned by Diversified, voting in person or by proxy at a meeting of such holders at which a quorum is present; notwithstanding the foregoing, there are conflicting interpretations that the Trust Agreement requires the exclusion of the common units owned by Diversified and its affiliates in a vote following Tapstone's acquisition of the Underlying Properties from Chesapeake even if Diversified and its affiliates own over 10% of the outstanding Trust units; or

•the Trust is judicially dissolved.

In the case of any of the foregoing, the Trustee would sell all of the Trust's assets, either by private sale or public auction, and distribute the net proceeds of the sale to the Trust unitholders after payment, or reasonable provision for payment, of all Trust liabilities.

Federal Income Tax Considerations

The Trust's federal income tax reporting position is that it is classified as a partnership for federal and applicable state income tax purposes. This position relies on the opinion of Bracewell LLP, former counsel to the Operator and the Trust, rendered in connection with the initial public offering of the Trust units in 2011, in which counsel opined that at least 90% of the Trust's gross income is qualifying income within the meaning of Section 7704 of the Internal Revenue Code of 1986, as amended. The Trust's federal income tax reporting positions are consistent with the Federal Income Tax Considerations section in the Prospectus filed by the Trust with the SEC on November 14, 2011, in connection with the initial public offering of its common units (the “Federal Income Tax Considerations Section in the Prospectus”). However, as discussed in detail below under Item 1A. Risk Factors – Tax Risks Related to the Units, the Trust has not requested a ruling from the IRS regarding its U.S. federal income tax reporting positions and its positions may not be sustained by a court or if contested by the IRS.

Additional information regarding the opinion and material tax matters is discussed in the Federal Income Tax Considerations Section in the Prospectus.

Competition and Markets

The oil and natural gas industry is highly competitive. The Operator competes with both major integrated and other independent oil and natural gas companies in all aspects of its business to explore, develop and operate its properties and market its production. Some of the Operator's competitors may have larger financial and other resources than the Operator. Competitive conditions may be affected by future legislation and regulations as the United States develops new energy and climate-related policies. In addition, some of the Operator's competitors may have a competitive advantage when responding to factors that affect demand for oil and natural gas production, such as changing prices, domestic and foreign political conditions, weather conditions, the price and availability of alternative fuels, the proximity and capacity of natural gas pipelines and other transportation facilities, and overall economic conditions. The Operator also faces indirect competition from alternative energy sources, including wind, solar and electric power. The Operator believes that its technological expertise, combined with its exploration, land, drilling and production capabilities and the experience of its management team enable it to compete effectively.

Recent volatility in oil, natural gas and NGL prices has impacted, and will continue to directly impact, Trust distributions, estimates of reserves attributable to the Trust's interest, and estimated and actual future net revenues to the Trust. In view of the many uncertainties that affect the supply and demand for oil, natural gas and NGL, neither the Trust nor the Operator can make reliable predictions of future supply and demand for oil, natural gas and NGL, future oil, natural gas and NGL prices or the effect of future oil, natural gas and NGL prices on the Trust.

8

Public Policy and Government Regulation

All of the Operator's operations are conducted onshore in the United States. The U.S. oil and natural gas industry is subject to a wide range of regulations, laws, rules, taxes, fees and other policy implementation actions that have been pervasive and are under constant review for amendment or expansion. Numerous government agencies have issued extensive regulations that are binding on our industry, some of which carry substantial penalties for failure to comply. These laws and regulations increase the cost of doing business and consequently affect profitability. Additionally, currently unforeseen environmental incidents may occur or past non-compliance with environmental laws or regulations may be discovered. The Operator has advised the Trustee that the Operator actively monitors regulatory developments applicable to our industry in order to anticipate, design and implement required compliance activities and systems. The following are significant areas of government control and regulation affecting the Operator's operations.

Exploration and Production, Environmental, Health and Safety, and Occupational Laws and Regulations

The Operator's operations are subject to federal, tribal, state, and local laws and regulations. These laws and regulations relate to matters that include, but are not limited to, the following:

•reporting of workplace injuries and illnesses;

•industrial hygiene monitoring;

•worker protection and workplace safety;

•approval or permits to drill and to conduct operations;

•provision of financial assurances (such as bonds) covering drilling and well operations;

•calculation and disbursement of royalty payments and production taxes;

•seismic operations and data;

•hydraulic fracturing;

•location, drilling, cementing and casing of wells;

•well design and construction of pad and equipment;

•construction and operations activities in sensitive areas, such as wetlands, coastal regions or areas that contain endangered or threatened species, their habitats, or sites of cultural significance;

•method of completing wells and hydraulic fracturing;

•water withdrawal;

•well production and operations, including processing and gathering systems;

•emergency response, contingency plans and spill prevention plans;

•emissions and discharges permitting;

•climate change;

•use, transportation, storage and disposal of fluids and materials incidental to oil and gas operations;

•surface usage, maintenance, monitoring and the restoration of properties associated with well pads, pipelines, impoundments and access roads;

•plugging and abandoning of wells; and

•transportation of production.

Failure to comply with these laws and regulations can lead to the imposition of remedial liabilities, fines or penalties or injunctions limiting the Operator's operations in affected areas. Moreover, multiple environmental laws provide for citizen suits that allow environmental organizations to act in the place of the government and sue operators for alleged violations of environmental law. The Operator considers the costs of environmental protection and of safety and health compliance to be necessary, manageable parts of its business. The Operator has been able to plan for and comply with environmental, safety and health initiatives without materially altering its operating strategy or incurring significant unreimbursed expenditures. However, based on regulatory trends and increasingly stringent laws, the Operator's capital expenditures and operating expenses related to the protection of the

9

environment and safety and health compliance have increased over the years and may continue to increase. The Operator cannot predict with any reasonable degree of certainty its future exposure concerning such matters.

The Operator's operations also are subject to conservation regulations, including the regulation of the size of drilling and spacing units or proration units, the number of wells that may be drilled in a unit, the rate of production allowable from oil and gas wells, and the unitization or pooling of oil and gas properties. In the United States, some states allow the forced pooling or integration of tracts to facilitate exploration, while other states rely on voluntary pooling of lands and leases, which may make it more difficult to develop oil and gas properties. In addition, federal and state conservation laws generally limit the venting or flaring of natural gas, and state conservation laws impose certain requirements regarding the ratable purchase of production. These regulations limit the amounts of oil and gas the Operator can produce from its wells and the number of wells or the locations at which it can drill. For further discussion, see Item 1A. Risk Factors - The Operator is subject to extensive governmental regulation, which can change and could adversely impact the Operator's business.

Regulatory proposals in some states and local communities have been initiated to require or make more stringent the permitting and compliance requirements for hydraulic fracturing operations. Federal and state agencies have continued to assess the potential impacts of hydraulic fracturing, which could spur further action toward federal, state and/or local legislation and regulation. Further restrictions of hydraulic fracturing could make it prohibitive to conduct operations, and also reduce the amount of oil, natural gas and NGL that the Operator is ultimately able to produce in commercial quantities from its properties.

Certain of the Operator's U.S. natural gas and oil leases are granted or approved by the federal government and administered by the Bureau of Land Management (BLM) or Bureau of Indian Affairs (BIA) of the Department of the Interior. Such leases require compliance with detailed federal regulations and orders that regulate, among other matters, drilling and operations on lands covered by these leases and calculation and disbursement of royalty payments to the federal government, tribes or tribal members. The federal government has been particularly active in recent years in evaluating and, in some cases, promulgating new rules and regulations regarding competitive lease bidding, venting and flaring, oil and gas measurement and royalty payment obligations for production from federal lands. In addition, permitting activities on federal lands are subject to frequent delays.

Delays in obtaining permits or an inability to obtain new permits or permit renewals could inhibit the Operator's ability to execute its drilling and production plans. Failure to comply with applicable regulations or permit requirements could result in revocation of the Operator's permits, inability to obtain new permits and the imposition of fines and penalties. For further discussion, see Item 1A. Risk Factors - Oil and natural gas drilling and producing operations can be hazardous and may expose the Operator to liabilities.

Human Capital

The Trust does not have any employees, directors, or executive officers.

Operating Hazards and Insurance