UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter) |

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

People's Republic of

(Address of principal executive offices)

Telephone: + 86‑

Email:

At the address of the Company set forth above

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

|

| The |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

An aggregate of

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

* | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☐

|

|

International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

* | If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐ |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes

TABLE OF CONTENTS

2 | ||

|

| |

4 | ||

|

|

|

4 | ||

|

|

|

4 | ||

|

|

|

4 | ||

|

|

|

36 | ||

|

|

|

63 | ||

|

|

|

64 | ||

|

|

|

79 | ||

|

|

|

86 | ||

|

|

|

87 | ||

|

|

|

87 | ||

|

|

|

88 | ||

|

|

|

95 | ||

|

|

|

96 | ||

|

| |

97 | ||

|

|

|

97 | ||

|

|

|

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 97 | |

|

|

|

98 | ||

|

|

|

99 | ||

|

|

|

99 | ||

|

|

|

99 | ||

|

|

|

100 | ||

|

|

|

100 | ||

|

|

|

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 100 | |

|

|

|

100 | ||

|

|

|

100 | ||

|

|

|

101 | ||

|

|

|

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | 101 | |

|

|

|

101 | ||

|

|

|

101 | ||

|

| |

102 | ||

|

|

|

102 | ||

|

|

|

102 | ||

|

|

|

102 | ||

| 1 |

| Table of Contents |

INTRODUCTION

In this annual report on Form 20‑F, unless the context otherwise requires, references to:

| · | “China” or the “PRC” are to the People’s Republic of China; |

|

|

|

| · | “Class A ordinary shares” are to the Class A ordinary shares, no par value, of CN Energy (as defined below); |

|

|

|

| · | “Class B ordinary shares” are to the Class B ordinary shares, no par value, of CN Energy. Holders of Class A ordinary shares and Class B ordinary shares have the same rights except for voting and conversion rights. In respect of matters requiring a vote of all shareholders, each holder of Class A ordinary shares will be entitled to one vote per one Class A ordinary share and each holder of Class B ordinary shares will be entitled to 50 votes per one Class B ordinary share. The Class A ordinary shares are not convertible into shares of any other class. The Class B ordinary shares are convertible into Class A ordinary shares at any time after issuance at the option of the holder on a one-to-one basis; |

|

|

|

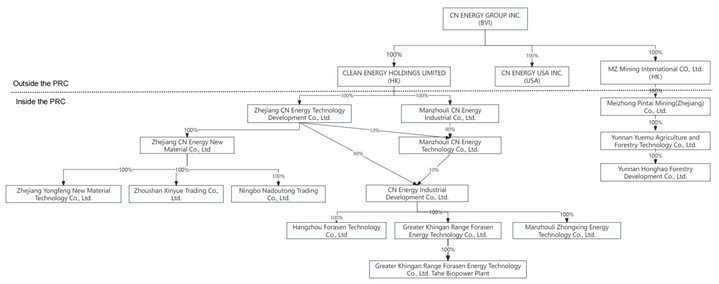

| · | “CN Energy,” “we,” “us,” “our,” “our Company,” and the “Company” are to CN ENERGY GROUP. INC. (also referred to as 中北能源集团有限公司 in Chinese), a business company limited by shares incorporated under the laws of British Virgin Islands; |

|

|

|

| · | “CN Energy Development” are to CN Energy Industrial Development Co., Ltd. (also referred to as 中北能源产业发展有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is jointly owned by Zhejiang CN Energy and Manzhouli CN Technology (as defined below); |

|

|

|

| · | “Energy Holdings” are to CN Energy’s wholly owned subsidiary, CLEAN ENERGY HOLDINGS LIMITED (also referred to as 清洁能源控股有限公司 in Chinese), a Hong Kong corporation; |

|

|

|

| · | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; |

|

|

|

| · | “Hangzhou Forasen” are to Hangzhou Forasen Technology Co., Ltd. (also referred to as 杭州富来森科技有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by CN Energy Development; |

|

|

|

| · | “Khingan Forasen” are to Greater Khingan Range Forasen Energy Technology Co., Ltd. (also referred to as 大兴安岭富来森能源科技有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by CN Energy Development; |

|

|

|

| · | “Manzhouli CN Energy” are to Manzhouli CN Energy Industrial Co., Ltd. (also referred to as 满洲里市中北能实业有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by Energy Holdings; |

|

|

|

| · | “Manzhouli CN Technology” are to Manzhouli CN Energy Technology Co., Ltd. (also referred to as 满洲里市中北能科技有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is jointly owned by Zhejiang CN Energy (as defined below) and Manzhouli CN Energy; |

|

|

|

| · | “MZ HK” are to MZ Mining International Co., Ltd, a Hong Kong company acquired by the Company on November 11, 2022; |

|

|

|

| · | “MZ Pintai” are to MZ Pintai Mining (Zhejiang) Co., Ltd (also referred to as 美中品泰矿业(浙江)有限公司 in Chinese), a company incorporated under the laws of the PRC which is wholly owned by MZ HK; |

|

|

|

| · | “Ningbo Nadoutong” are to Ningbo Nadoutong Trading Co., Ltd. (also referred to as 宁波哪都通贸易有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by CN Energy Development; |

|

|

|

| · | “operating entities” are to CN Energy Development and its subsidiaries; |

|

|

|

| · | “RMB” or “Renminbi” are to the legal currency of China; |

| 2 |

| Table of Contents |

| · | “SEC” are to the U.S. Securities and Exchange Commission; |

|

|

|

| · | “Securities Act” are to the Securities Act of 1933, as amended; |

|

|

|

| · | “Tahe Biopower Plant” are to Greater Khingan Range Forasen Energy Technology Co., Ltd. Tahe Biopower Plant (also referred to as 大兴安岭富来森能源科技有限公司塔河生物发电厂 in Chinese), the branch office of Khingan Forasen; |

|

|

|

| · | “Yunnan Honghao” are to Yunnan Honghao Forestry Development Co., Ltd. (also referred to as 云南宏灏林业发展有限公司 in Chinese), a company incorporated in the PRC with limited liability, which is wholly owned by Yunnan Yuemu (as defined below); |

|

|

|

| · | “Yunnan Yuemu” are to Yunnan Yuemu Agriculture and Forestry Technology Co., Ltd (also referred to as 云南岳沐农林科技有限公司 in Chinese), a company incorporated in the PRC and wholly owned by MZ Pintai; |

|

|

|

| · | “Zhejiang CN Energy” are to Zhejiang CN Energy Technology Development Co., Ltd. (also referred to as 浙江中北能源科技开发有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by Energy Holdings; |

|

|

|

| · | “Zhejiang New Material” are to Zhejiang CN Energy New Material Co., Ltd. (also referred to as 浙江中北能新材料有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by CN Energy Development; |

|

|

|

| · | “Zhejiang Yongfeng New Material” are to Zhejiang Yongfeng New Material Technology Co., Ltd. (also refers to as 浙江咏丰新材料科技有限公司 in Chinese), a company with limited liability organized under the PRC, which is wholly owned by Hangzhou Forasen; |

|

|

|

| · | “Zhongxing Energy” are to Manzhouli Zhongxing Energy Technology Co., Ltd. (also referred to as 满洲里市众兴能源科技有限公司 in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by CN Energy Development; and |

|

|

|

| · | “Zhoushan Xinyue” are to Zhoushan Xinyue Trading Co., Ltd. (also referred to as 舟山信跃贸易有限公司in Chinese), a company with limited liability organized under the laws of the PRC, which is wholly owned by Hangzhou Forasen. |

This annual report on Form 20‑F includes our audited consolidated financial statements for the fiscal years ended September 30, 2023, 2022, and 2021. In this annual report, we refer to assets, obligations, commitments, and liabilities in our consolidated financial statements in United States dollars. These dollar references are based on the exchange rate of RMB to United States dollars, determined as of a specific date or for a specific period. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of United States dollars which may result in an increase or decrease in the amount of our obligations and the value of our assets.

This annual report contains translations of certain RMB amounts into U.S. dollars at specified rates. Unless otherwise stated, the following exchange rates are used in this annual report:

|

|

|

| September 30, |

|

|

|

US$ Exchange Rate |

| 2023 |

| 2022 |

| 2021 |

|

At the end of the year – RMB |

| RMB7.2960 to $1 |

| RMB7.1135 to $1 |

| RMB6.4599 to $1 |

|

Average rate for the year - RMB |

| RMB7.0533 to $1 |

| RMB6.5728 to $1 |

| RMB6.5104 to $1 |

|

| 3 |

| Table of Contents |

Part I

Item 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

Item 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

Item 3. KEY INFORMATION

We are incorporated in the British Virgin Islands and conduct our operations primarily in China. As a holding company with no material operations of our own, our operations are conducted in China through the operating entities. Our ordinary shares are shares of CN Energy, the offshore holding company in the British Virgin Islands, instead of shares of our operating companies in China. Therefore, our shareholders will not directly hold any equity interests in our operating companies.

Wholly owned subsidiaries of CN Energy Development include Khingan Forasen, Hangzhou Forasen, Zhongxing Energy, and Zhejiang New Material, Ningbo Nadoutong Trading Co., Ltd., Zhoushan Xinyue, and Zhejiang Yongfeng New Material, all of which were established as companies with limited liabilities pursuant to PRC laws. Khingan Forasen produces activated carbon and biomass electricity through its branch office, Tahe Biopower Plant, which houses the operating entities’ current manufacturing facility; Hangzhou Forasen is engaged in the marketing of activated carbon products; Zhongxing Energy is expected to hold the operating entities’ second biopower plant and produce activated carbon and heat in the future; Zhejiang New Material is expected to be engaged in the manufacturing and marketing of activated carbon products used for water treatment and purification in 2023; Ningbo Nadoutong is engaged in the marketing of activated carbon products; Zhoushan Xinyue is engaged in the marketing of activated carbon products; and Zhejiang Yongfeng New Material is expected to be engaged in the marketing of activated carbon products.

Wholly owned subsidiaries of MZ HK include MZ Pintai, Yunnan Yuemu and Yunnan Honghao, all of which were incorporated as companies with limited liabilities in pursuant to PRC laws. MZ HK is a holding company with no business operation; MZ Pintai is engaged in sales of minerals, stone, metal materials, construction materials, wood, chemical materials and products, rubber products, and paper products; Yunnan Yuemu is engaged in management and conversion of forest and natural ecosystem; and Yunnan Honghao is engaged in forest acquisition, rights transfer, and nurturing, and timber harvesting and processing.

| 4 |

| Table of Contents |

2023 Corporate Restructuring

In December 2023, we conducted a corporate reorganization, which represented a strategic shift to streamline management control and enhance our operational efficiency. This restructuring is marked by four equity transfer agreements that redefine our corporate landscape.

On December 12, 2023, Zhejiang CN Energy and CN Energy Development entered into an equity transfer agreement. According to the terms of that agreement, CN Energy Development transferred 100% of the equity of Zhejiang New Material to Zhejiang CN Energy for no consideration. This equity transfer resulted in Zhejiang New Material being a wholly-owned subsidiary of Zhejiang CN Energy.

On December 15, 2023, Hangzhou Forasen and Zhejiang New Material signed an equity transfer agreement. Under this agreement, Hangzhou Forasen agreed to transfer 100% of its equity in Zhoushan Xinyue to Zhejiang New Material for no consideration. Upon the completion of this equity transfer, Zhoushan Xinyue became a wholly-owned subsidiary of Zhejiang New Material. On the same date, Zhejiang New Material and CN Energy Development entered into an equity transfer agreement, pursuant to which CN Energy Development transferred all its equity interest in Ningbo Nadoutong to Zhejiang New Material for no consideration. After this transfer, Ningbo Nadoutong became a wholly-owned subsidiary of Zhejiang New Material.

On December 21, 2023, Hangzhou Forasen and Zhejiang New Material entered into another equity transfer agreement, under which Hangzhou Forasen transferred 100% of its equity in Zhejiang Yongfeng New Material to Zhejiang New Material for no consideration. Upon the completion of this equity transfer, Zhejiang Yongfeng New Material became a wholly-owned subsidiary of Zhejiang New Material.

As of the date of this annual report, we have completed our corporate restructuring. The following diagram illustrates our corporate structure as of the date of this annual report.

| 5 |

| Table of Contents |

Notes: All percentages reflect the voting ownership interests instead of the equity interests held by each of our shareholders given that each holder of Class B ordinary shares will be entitled to 50 votes per one Class B ordinary share and each holder of Class A ordinary shares will be entitled to one vote per one Class A ordinary share.

Share Consolidation

On December 20, 2023, our board of directors approved a resolution that resulted in (i) a share consolidation of 30 issued Class A ordinary shares with no par value into one Class A ordinary share, and (2) a share consolidation of 30 issued Class B ordinary shares into one Class B ordinary share (collectively, the “Share Consolidation”). Immediately after the Share Consolidation, each of our shareholder’s percentage ownership interest and proportional voting power remained unchanged, except for minor changes and adjustments resulting from the treatment of fractional shares. The rights and privileges of the holders of ordinary shares remained substantially unaffected by the Share Consolidation. The Share Consolidation was effective at 5:00 p.m. British Virgin Islands time on January 18, 2024. Beginning with the opening of trading on January 19, 2024, our Class A ordinary shares started to trade on a post-Share Consolidation basis on the Nasdaq Capital Market. The Share Consolidation was primarily being effectuated to regain compliance with Nasdaq Listing Rule 5450(a)(1) related to the minimum price per share of our Class A ordinary shares.

Risks Associated with Our Corporate Structure

Our holding company structure involves certain risks in terms of dividend distribution, direct investment in PRC entities, and obtaining benefits under relevant tax treaty. See “—D. Risk Factors—Risks Related to Doing Business in the PRC—We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirement we may have, and any limitation on the ability of our subsidiaries to make payments to us and any tax we are required to pay could have a materially adverse effect on our ability to conduct our business,” “—D. Risk Factors—Risks Related to Doing Business in the PRC—PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using proceeds from our future financing activities to make loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business,” “—D. Risk Factors—Risks Related to Doing Business in the PRC—PRC regulations relating to offshore investment activities by PRC residents may limit our PRC subsidiaries’ ability to increase their registered capital or distribute profits to us, or otherwise expose us or our PRC resident shareholders to liabilities or penalties,” and “—D. Risk Factors—Risks Related to Doing Business in the PRC—Under the EIT Law, we may be classified as a ‘resident enterprise’ of China, which could result in unfavorable tax consequences to us and our non-PRC shareholders.” See also “Item 4. Information on the Company—B. Business Overview—Regulations—PRC Regulations Relating to Foreign Exchange.”

Risks Associated with Doing Business in the PRC

We are subject to certain legal and operational risks associated with having the majority of our operations in China, which could significantly limit or completely hinder our ability to offer securities to investors and cause the value of our securities to significantly decline or be worthless. See “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in the PRC—Any actions by the Chinese government, including any decision to intervene or influence the operating entities’ operations or to exert control over any offering of securities conducted overseas and/or foreign investment in China-based issuers, may cause them to make material changes to their operations, may limit or completely hinder their ability to offer or continue to offer securities to investors, and may cause the value of such securities to significantly decline or be worthless.” Recently, the PRC government adopted a series of regulatory actions and issued statements to regulate business operations in China, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. As of the date of this annual report, we and our subsidiaries have not been involved in any investigations on cybersecurity review initiated by any PRC regulatory authority, nor has any of them received any inquiry, notice or sanction. As of the date of this annual report, we are not subject to cybersecurity review by the Cyberspace Administration of China (the “CAC”), since we currently do not have over one million users’ personal information and do not anticipate that we will be collecting over one million users’ personal information in the foreseeable future, which we understand might otherwise subject us to the Cybersecurity Review Measures. We are not subject to network data security review by the CAC if the Draft Regulations on the Network Data Security Administration (Draft for Comments) (the “Security Administration Draft”) are enacted as proposed, because we currently do not have over one million users’ personal information, we do not collect data that affect or may affect national security and we do not anticipate that we will be collecting over one million users’ personal information or data that affect or may affect national security in the foreseeable future, which we understand might otherwise subject us to the Security Administration Draft. See “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in the PRC—Greater oversight by the CAC over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact the operating entities’ business and our offerings.”

| 6 |

| Table of Contents |

On February 17, 2023, the China Securities Regulatory Commission (the “CSRC”) promulgated the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Measures”) and five supporting guidelines, which came into effect on March 31, 2023. As our registration statement on Form F-1 was declared effective on February 4, 2021 and we completed our initial public offering and listing on February 9, 2021, we are currently not required to complete the filing procedures pursuant to the Trial Measures. However, in the event that we undertake new offerings or fundraising activities in the future, we may be required to complete the filing procedures. Other than the foregoing, as of the date of this annual report, according to our PRC counsel, Universal Law Offices of Hangzhou, no relevant PRC laws or regulations in effect require that we obtain additional permission from any PRC authorities to issue securities to foreign investors, and we have not received any inquiry, notice, warning, sanction, or any regulatory objection to our offerings from the CSRC, the CAC, or any other PRC authorities that have jurisdiction over our operations. The Standing Committee of the National People’s Congress (the “SCNPC”) or PRC regulatory authorities may in the future promulgate additional laws, regulations, or implementing rules that require us and/or our subsidiaries to obtain regulatory approval from Chinese authorities for our continued listing in the U.S. If we do not receive or maintain such approval, or inadvertently conclude that such approval is not required, or applicable laws, regulations, or interpretations change such that we are required to obtain approval in the future, we may be subject to an investigation by competent regulators, fines or penalties, or an order prohibiting us from conducting a subsequent offering, and these risks could result in a material adverse change in our operations and the value of our Class A ordinary shares, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. See “Item 3. Key Information—D. Risk Factors—Risks Relating to Doing Business in the PRC—Given the Chinese government’s significant oversight and discretion over the conduct of the operating entities’ business, the Chinese government may intervene or influence the operating entities’ operations at any time, which could result in a material change in their operations and/or the value of our ordinary shares.”

Since 2021, the Chinese government has strengthened its anti-monopoly supervision, mainly in three aspects: (i) establishing the National Anti-Monopoly Bureau; (ii) revising and promulgating anti-monopoly laws and regulations, including: the Anti-Monopoly Law of the PRC (amended on June 24, 2022 and effective on August 1, 2022), the anti-monopoly guidelines for various industries, and the Detailed Rules for the Implementation of the Fair Competition Review System; and (iii) expanding the anti-monopoly law enforcement targeting Internet companies and large enterprises. As of the date of this annual report, the Chinese government’s recent statements and regulatory actions related to anti-monopoly concerns have not impacted our or our operating entities’ ability to conduct business, our ability to accept foreign investments or issue our securities to foreign investors because neither we nor our operating entities engage in monopolistic behaviors that are subject to these statements or regulatory actions

Permissions Required from PRC Authorities

As of the date of this annual report, we and the operating entities (i) are not covered by additional permissions or approval requirements from any governmental agency that is required to approve the operating entities’ operations, (ii) have received from PRC authorities all requisite licenses, permissions, and approvals needed to engage in the businesses currently conducted in the PRC, and (iii) no such permission or approval has been denied.

As advised by our PRC counsel, Universal Law Offices of Hangzhou, other than those requisite for a domestic company in China to engage in the businesses similar to those of the operating entities, the operating entities are not required to obtain any additional permission from Chinese authorities, including the CSRC, the CAC, or any other governmental agency that is required to approve the operating entities’ operations. However, we cannot assure you that the PRC regulatory agencies, including the CAC or the CSRC, would take the same view as we do, and there is no assurance that our operating entities are always able to successfully update or renew the licenses or permits required for the relevant business in a timely manner or that these licenses or permits are sufficient to conduct all of their present or future business. If the operating entities (i) do not receive or maintain required permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, or (iii) applicable laws, regulations, or interpretations change and our operating entities are required to obtain such permissions or approvals in the future, they could be subject to fines, legal sanctions, or an order to suspend their relevant services, which may materially and adversely affect our financial condition and results of operations and cause our securities to significantly decline in value or become worthless.

| 7 |

| Table of Contents |

According to the Notice on the Administrative Arrangements for the Filing of the Overseas Securities Offering and Listing by Domestic Companies from the CSRC, or “the CSRC Notice,” the domestic companies that have already been listed overseas before the effective date of the Trial Measures (namely, March 31, 2023) shall be deemed as existing issuers (the “Existing Issuers”). Existing Issuers are not required to complete the filing procedures immediately, and they shall be required to file with the CSRC for any subsequent offerings. Based on the foregoing, as our registration statement on Form F-1 in connection with our initial public offering was declared effective on February 4, 2021 and we completed our initial public offering and listing on February 9, 2021, we are currently not required to complete the filing procedures pursuant to the Trial Measures. However, in the event that we undertake new offerings or fundraising activities in the future, we may be required to complete the filing procedures.

The General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the “Opinions on Severely Cracking Down on Illegal Securities Activities According to Law,” or the “Opinions,” which were made available to the public on July 6, 2021. The Opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision over overseas listings by Chinese companies. The Opinions proposed to take effective measures, such as promoting the construction of relevant regulatory systems, to deal with the risks and incidents facing China-based overseas-listed companies and the demand for cybersecurity and data privacy protection. The aforementioned policies and any related implementation rules to be enacted may subject us to additional compliance requirements in the future. Given the current regulatory environment in the PRC, we are still subject to the uncertainty of different interpretation and enforcement of the rules and regulations in the PRC adverse to us, which may take place quickly with little advance notice. See “—D. Risk Factors—Risks Relating to Doing Business in the PRC—The Opinions issued by the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council may subject the operating entities to additional compliance requirement in the future.”

Transfer of Funds and Other Assets Between Our Company and Our Subsidiaries

As of the date of this annual report, CN Energy has transferred the net proceeds from our initial public offering, through Energy Holdings and Zhejiang CN Energy, to CN Energy Development and its subsidiaries, including RMB64,134,688.25 (approximately $9,537,500) to CN Energy Development, RMB103,921,379 (approximately $15,848,010) to Hangzhou Forasen, and RMB12,891,800 (approximately $1,966,000) to Zhongxing Energy.

Our finance department is supervising cash management, following the instructions of our management. Our finance department is responsible for establishing our cash operation plan and coordinating cash management matters among our subsidiaries and departments. Each subsidiary and department initiates a cash request by putting forward a cash demand plan, which explains the specific amount and timing of cash requested, and submits it to our finance department. The finance department reviews the cash demand plan and prepares a summary for the management of our Company. Management examines and approves the allocation of cash based on the sources of cash and the priorities of the needs. Other than the above, we currently do not have other cash management policies or procedures that dictate how funds are transferred.

Dividends or Distributions and Tax Consequences

As of the date of this annual report, none of our subsidiaries have made any dividends or distributions to CN Energy and CN Energy has not made any dividends or distributions to its shareholders. We intend to keep any future earnings to finance the expansion of our business, and we do not anticipate that any cash dividends will be paid in the foreseeable future. Subject to the passive foreign investment company (“PFIC”) rules, the gross amount of distributions we make to investors with respect to our ordinary shares (including the amount of any taxes withheld therefrom) will be taxable as a dividend, to the extent that the distribution is paid out of our current or accumulated earnings and profits, as determined under U.S. federal income tax principles.

Pursuant to the BVI Business Companies Act, 2004 as amended from time to time (the “BVI Act”), and our third amended and restated memorandum and articles of association, our board of directors may authorize and declare a dividend to shareholders at such time and of such an amount as they think appropriate, if they are satisfied on reasonable grounds that immediately following the dividend payment, the value of our assets will exceed our liabilities and we will be able to pay our debts as they become due. There is no further British Virgin Islands statutory restriction on the amount of funds which may be distributed by us by dividends.

| 8 |

| Table of Contents |

If we determine to pay dividends on any of our ordinary shares in the future, as a holding company, we will be dependent on receipt of funds from our Hong Kong subsidiaries, Energy Holdings and MZ HK, and our U.S. subsidiary, CN Energy USA Inc.

Current PRC regulations permit our indirect PRC subsidiaries to pay dividends to Energy Holdings only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation.

The PRC government imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC (excluding the special administrative regions of Hong Kong and Macau). Under the applicable PRC regulations, RMB is freely convertible only to the extent of current account items, such as trade-related receipts and payments, interest, and dividends. Conversion of RMB into a foreign currency such as U.S. dollars for capital account items, such as direct equity investments, loans, and repatriation of investment, requires prior approval from the State Administration of Foreign Exchange or its local branch. Such approval, however, does not guarantee the availability of foreign currency conversion. Furthermore, the value of the RMB against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in China’s political and economic conditions. The RMB may not be stable against the U.S. dollar or other foreign currency. To the extent that we seek to convert RMB into U.S. dollars, depreciation of the RMB against the U.S. dollar would have an adverse effect on the U.S. dollar amount we receive from the conversion. Therefore, we may experience difficulties in complying with the administrative requirements necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries and affiliates in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenue from our operations, we may be unable to pay dividends on our ordinary shares.

Cash dividends, if any, on our ordinary shares will be paid in U.S. dollars. Energy Holdings or MZ HK may be considered a non-resident enterprise for PRC tax purposes. Any dividends that our PRC subsidiaries pay to Energy Holdings may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10%. See “Item 10. Additional Information—E. Taxation—People’s Republic of China Taxation.”

In order for us to pay dividends to our shareholders, we will rely on payments made from (i) CN Energy Development’s subsidiaries to CN Energy Development and from CN Energy Development to Zhejiang CN Energy and indirectly to Manzhouli CN Energy, and the distribution of such payments to Energy Holdings and then to our Company and (ii) MZ Pintai’s subsidiaries to MZ Pintai, and the distribution of such payments to MZ HK and then to our Company. According to the EIT Law, such payments from subsidiaries to parent companies in China are subject to the PRC enterprise income tax at a rate of 25%. In addition, if CN Energy Development or MZ Pintai or their subsidiaries incur debt on their own behalf, the instruments governing the debt may restrict its ability to pay dividends or make other distributions to us.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income (the “Double Tax Avoidance Arrangement”), the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC project. The 5% withholding tax rate, however, does not automatically apply and certain requirements must be satisfied, including without limitation that (a) the Hong Kong project must be the beneficial owner of the relevant dividends; and (b) the Hong Kong project must directly hold no less than 25% share ownership in the PRC project during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong project must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Avoidance Arrangement with respect to any dividends paid by our PRC subsidiaries to their immediate holding company, Energy Holdings and MZ HK. As of the date of this annual report, we have not applied for the tax resident certificate from the relevant Hong Kong tax authority. Energy Holdings intends to apply for the tax resident certificate if and when Zhejiang CN Energy and Manzhouli CN Energy plan to declare and pay dividends to Energy Holdings and MZ HK intends to apply for the tax resident certificate if and when MZ Pintai plans to declare and pay dividends to MZ HK. See “—D. Risk Factors—Risks Relating to Doing Business in the PRC—There are significant uncertainties under the EIT Law relating to the withholding tax liabilities of our PRC subsidiaries, and dividends payable by our PRC subsidiaries to our Hong Kong subsidiaries may not qualify to enjoy certain treaty benefits.”

| 9 |

| Table of Contents |

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to Our Business

The operating entities’ financial results could be materially and adversely affected by an interruption of supply of raw materials.

The operating entities are dependent on a variety of raw materials (including forestry residues, little fuelwood, and wood wastes) that support their manufacturing activities. The operating entities’ ability to meet their customers’ needs depends heavily on an uninterrupted supply of these materials. Although the operating entities source strategic raw materials from multiple suppliers whenever possible and have instituted back-up procedures or contracted with a secondary supplier for any raw material that is sourced primarily from one location or supplier, production problems, lack of capacity, breach of contractual obligations by their third-party suppliers, changes in third-party suppliers’ financial or business condition, or planned and unplanned shutdowns of their production facilities that affect their ability to supply the operating entities with raw materials that meet the operating entities’ specifications, or at all, could disrupt the operating entities’ ability to supply products to their customers. In addition, interruptions in raw material supply caused by events outside their suppliers’ control, such as wildfires, labor disputes, or transportation disruptions, could also disrupt the operating entities’ ability to meet customer demand. These supply disruptions could cause the operating entities to miss deliveries and breach their contracts, which could damage their relationships with their customers and subject the operating entities to claims for damages under their contracts. If any of these events were to occur for more than a temporary period, the operating entities may not be able to make arrangements for transition supply and qualified replacement suppliers on terms acceptable to the operating entities or at all, which could have a material adverse effect on their business and financial results.

Increases in the prices of raw materials could materially and adversely affect the operating entities’ financial results.

If the prices the operating entities have to pay for raw materials under their existing supply contracts or under replacement supply contracts increase, they could face significantly higher production costs. Although the operating entities’ long-term supply contracts typically provide for a specific price, increases in raw material prices could adversely affect their ability to renew these contracts on similar terms or at all. Similarly, increases in raw material prices could adversely affect their ability to enter into shorter-term supply agreements at favorable prices. The operating entities may not be able to pass the whole price increase through to their customers, which could have a material adverse effect on their financial results.

A majority of the operating entities’ activated carbon sales are currently derived from a small number of customers. If any of these customers experiences a material business disruption, the operating entities would likely incur substantial losses of revenue.

For the fiscal year ended September 30, 2023, three major customers accounted for 13%, 13%, and 10% of the Company’s total sales, respectively. For the fiscal year ended September 30, 2022, one major customer accounted for approximately 58% of the operating entities’ total sales. For the fiscal year ended September 30, 2021, three major customers accounted for approximately 44%, 33%, and 11% of the operating entities’ total sales, respectively. The operating entities’ major customers may change as they adjust marketing strategies, and any material business disruption affecting the operating entities’ major customers or any decrease in sales to their major customers may negatively impact their operations and cash flows if they fail to increase sales to other customers.

The operating entities have sourced their raw materials primarily from a limited number of suppliers. If they lose one or more of their suppliers, their operations may be disrupted, and their results of operations may be adversely and materially impacted.

For the fiscal year ended September 30, 2023, the operating entities sourced 14% and 12% of their raw materials and activated carbon from their top two suppliers, respectively. For the fiscal year ended September 30, 2022, the operating entities sourced 35% and 14% of their raw materials from their top two suppliers, respectively. For the fiscal year ended September 30, 2021, the operating entities sourced 26%, 25%, and 16% of their raw materials and activated carbon from their top three suppliers, respectively. If they lose one or more of these suppliers and are unable to swiftly engage new suppliers, the operating entities’ production operations may be disrupted or even suspended, and they may not be able to deliver products to their customers on time. The operating entities may also have to pay a higher price to source from a different supplier on short notice. While the operating entities are actively searching for and negotiating with new suppliers, there is no guarantee that they will be able to locate appropriate new suppliers in their desired timeline. As a result, the operating entities’ results of operations may be adversely and materially impacted.

| 10 |

| Table of Contents |

A disruption or delay in production at the operating entities’ existing production facilities could have a material adverse effect on their financial results.

If the operating entities’ production facilities were to cease production unexpectedly in whole or in part, their sales and financial results could be materially and adversely affected. Such a disruption could be caused by a number of different events, including:

| · | maintenance outages; |

|

|

|

| · | prolonged power failures; |

|

|

|

| · | equipment failures or malfunctions; |

|

|

|

| · | fires, floods, tornadoes, earthquakes, or other catastrophes; |

|

|

|

| · | potential unrest or terrorist activities; |

|

|

|

| · | labor difficulties; or |

|

|

|

| · | other construction, design, or operational problems, including those related to the granting, or the timetable for granting, of permits. |

If any of these or other events were to result in a material disruption of the operating entities’ current manufacturing operations, production of their products may be delayed and their ability to meet the production capacity targets and satisfy customer requirements may be materially adversely affected or the operating entities may be required to recognize impairment charges, any of which could have a material adverse effect on their financial results. In addition, a prolonged shutdown of any of the operating entities’ production facilities could cause them to miss deliveries and breach their contracts, which could damage their relationships with their customers and subject them to claims for damages under their contracts. Any of these events could have a material adverse effect on the operating entities’ business and financial results.

| 11 |

| Table of Contents |

The operating entities rely on third-party manufacturers to produce some of their activated carbon products and problems with, or loss of, these manufacturers could harm the operating entities’ business and operating results.

The operating entities have outsourced some of their customer orders to third-party manufacturers to keep up with the demand for the operating entities’ activated carbon products. The operating entities face the risk that these third-party manufacturers may not produce and deliver activated carbon products on a timely basis, or at all. The operating entities may also experience difficulties with their third-party manufacturers since they do not have the same manufacturing processes or quality control as the operating entities do. These difficulties include reductions in the availability of production capacity, errors in complying with product specifications and regulatory and customer requirements, failures to meet production deadlines, failure to achieve the operating entities’ product quality standards, increases in costs of materials, and manufacturing or other business interruptions. The ability of the operating entities’ third-party manufacturers to effectively satisfy their production requirements could also be impacted by manufacturer financial difficulty or damage to their operations caused by fire, a terrorist attack, natural disasters, or other events. Although the operating entities carefully select third–party manufacturers, the failure of any manufacturer to perform to the operating entities’ expectations could result in supply shortages or delays for the operating entities’ activated carbon products and harm their business. If the operating entities experience significantly increased demand, or if they need to replace an existing manufacturer due to lack of performance, the operating entities may be unable to supplement or replace their manufacturing capacity on a timely basis, or identify manufacturers with the same or similar quality controls in place as the existing manufacturers do, or on terms that are acceptable to the operating entities, which may increase their costs, reduce their margins, and harm their ability to deliver activated carbon products on time.

The operating entities may incur delays and budget overruns with respect to any facilities it constructs. Any such delays or cost overruns may have a material adverse effect on the operating entities’ operating results.

The operating entities currently have no construction projects. If the operating entities launch any construction projects in the future, such projects may entail significant risks that can give rise to delays or cost overruns, including the following:

| · | insufficient capital to complete construction; |

|

|

|

| · | shortage of material or skilled labor; |

|

|

|

| · | unforeseen engineering, environmental, or geological problems; |

|

|

|

| · | work stoppages; |

|

|

|

| · | weather interference; |

|

|

|

| · | floods, typhoons, and other natural disasters; |

|

|

|

| · | delays or failures in obtaining the requisite construction licenses, permits, and certificates; |

|

|

|

| · | unanticipated cost increases; and |

|

|

|

| · | legal or political challenges. |

The anticipated costs and construction periods are based upon budgets, conceptual design documents, and construction estimates prepared by the operating entities in consultation with their architects and contractors. Construction, equipment, staffing requirements, and problems or difficulties in obtaining and maintaining any of the requisite licenses, permits, allocations, or authorizations from regulatory authorities can increase the costs or delay the construction or commencement of production or otherwise affect the planned design and features of the facility. We cannot be sure that the operating entities will not exceed the budgeted costs of the facility or that the facility will commence production within the contemplated time frame, if at all. Budget overruns and delays with respect to the construction could have a material adverse impact on the operating entities’ results of operations.

| 12 |

| Table of Contents |

The operating entities’ financial condition, results of operations, and cash flows have been adversely affected by the COVID-19 pandemic.

Since early 2020, the COVID-19 pandemic has significantly impacted the business operations of the operating entities. In response to the COVID-19 pandemic, the Chinese government implemented the shelter-in-place orders and travel restrictions. As a result, the employees of Tahe Biopower Plant and Hangzhou Forasen could not return to work on time after the Chinese New Year of 2020 and the transportation of raw materials and activated carbon was delayed or even stopped in January and February 2020, which adversely impacted the operating entities’ production and sales during that period, as well as the construction of their new facility in Manzhouli City. In addition, the operating entities suspended the construction of their new facility in Manzhouli City due to the impact of COVID-19 and bad weather. During fiscal year 2021, the operating entities’ production, sales, and construction of the new facility in Manzhouli City were disrupted several times by government regulations in response to the COVID-19 pandemic. In 2022, the repeated COVID-19 outbreaks in China have continued to impact the operating entities’ production, sales, and construction activities. Due to regulations of the Chinese government in response to the COVID-19 pandemic, the operating entities had to halt the transportation of raw materials several times, which led to higher costs of raw materials and transportation. The construction of the new facility in Manzhouli City was also disrupted several times. From late 2022 to early 2023, the Chinese government gradually released controls on the COVID-19 pandemic, and the operating entities returned to normal operation step-by-step. Despite this progress, the wood market in Northeast China has been slow to recover, continuing to experience lower trading volumes than pre-pandemic levels. During 2023, this significantly impacted the operating entities’ supply chain in Northeast China, placing a strain on its ability to secure sufficient raw materials for daily production. Consequently, the operating entities’ business was still affected by the COVID-19 pandemic during the fiscal year ended September 30, 2023.

The COVID-19 pandemic may continue to adversely impact the operating entities’ business operations and operating results, including decreasing their revenue, slowing the collection of accounts receivables, generating additional allowance for doubtful accounts, disrupting their supply chain, and increasing the costs of raw materials. Because of the significant uncertainties surrounding the COVID-19 pandemic, the operating entities cannot reasonably estimate the extent of its impact on their business operations and financial condition at this time.

Uncertainties as to the future of existing and planned environmental and health and safety laws and regulations, as well as delays of or changes to these laws and regulations, could have a material adverse effect on demand for the operating entities’ products.

The operating entities’ strategic growth initiatives rely significantly upon the enactment of restrictive environmental and health and safety laws and regulations, particularly those that would require industrial facilities to reduce the quantity of air and water pollutants they release. If stricter regulations are delayed, are not enacted as proposed, are enacted but subsequently repealed or amended to be less strict, or are enacted with prolonged phase-in periods, demand for the operating entities’ products could be materially and adversely affected and they may not be able to meet sales growth and return on invested capital targets, which could materially and adversely affect the operating entities’ financial results.

For example, a significant market driver for the operating entities’ activated carbon products and biomass electricity is the Notice on Issuing the Work Plan for Greenhouse Gas Emission Control During the 14th Five-Year Plan Period (the “Work Plan”) of the State Council of the PRC (the “State Council”), which supports the development of clean energy, including biomass electricity, and restricts the emission of industrial pollutants. Although the Work Plan would potentially promote the use of activated carbon products, we are unable to predict with certainty when and how the Work Plan will affect demand for the operating entities’ products. Changes to, or delays in implementing, the Work Plan could reduce or delay an expected increase in future demand for the operating entities’ products, which could have a material adverse effect on the operating entities’ business and financial results.

On the other hand, increased costs to utilities and other potential customers in complying with environmental regulations could limit production and reduce or delay an expected increase in demand for the operating entities’ products, which could also have a material adverse effect on the operating entities’ business and financial results.

Disclosure of the operating entities’ trade secrets and other proprietary information, or a failure to adequately protect these or the operating entities’ other intellectual property rights, could result in increased competition and have a material adverse effect on the operating entities’ business and financial results.

The operating entities’ ability to compete effectively depends in part on their ability to obtain, maintain, and protect their trade secrets, proprietary information, and other intellectual property rights. The operating entities rely on a combination of trade secret, patent, trademark, and copyright laws, as well as contractual restrictions and physical security measures, to protect the operating entities’ proprietary information and other intellectual property rights.

| 13 |

| Table of Contents |

Where we believe patent protection is not appropriate or obtainable, the operating entities rely on trade secret laws and practices to protect their proprietary technology and processes, including physical security, limited dissemination and access, and confidentiality agreements with their employees, customers, consultants, business partners, potential licensees and others, to protect their trade secrets and other proprietary information. However, trade secrets are difficult to protect, and courts outside the PRC may be less willing to protect their trade secrets. There can be no assurance that the operating entities’ protective measures will effectively prevent disclosure or unauthorized use of proprietary information or provide an adequate remedy in the event of misappropriation, infringement, or other violations of the operating entities’ proprietary information and other intellectual property rights.

Existing laws afford only limited protection for the operating entities’ intellectual property rights. Despite the operating entities’ efforts, they may not be able to protect some of their technology, or the protection that they receive may not be sufficient. The operating entities face additional risks that their protective measures, including their patents and trademarks, could prove to be inadequate, including:

| · | the steps the operating entities take to prevent circumvention, misappropriation, or infringement of the operating entities’ proprietary rights may not be successful; |

|

|

|

| · | confidentiality agreements may be intentionally or unintentionally breached, be deemed unenforceable, or not provide adequate recourse against the disclosing party; |

|

|

|

| · | intellectual property laws may not sufficiently support the operating entities’ proprietary rights or may change in the future in a manner adverse to them; |

|

|

|

| · | patent or trademark rights may not be granted or construed as they expect, or may be challenged, narrowed, or invalidated; |

|

|

|

| · | intellectual property protection, including patents, may lapse or expire which may result in key technology becoming widely available which may hurt the operating entities’ competitive position; |

|

|

|

| · | effective protection of intellectual property rights may be unavailable or limited in some countries in which they operate or plan to do business; |

|

|

|

| · | third parties may independently develop or obtain comparable information and technology, and in some jurisdictions, obtain intellectual property protection for such technology; and |

|

|

|

| · | third parties may commercialize the operating entities’ products in countries in which they do not have adequate intellectual property protection. |

From time to time, the operating entities may seek to enforce their intellectual property and proprietary rights against third parties. Policing unauthorized use of intellectual property can be difficult and expensive. The operating entities may not be successful in their attempts to enforce their intellectual property rights against third parties. Any such litigation may result in substantial diversion of financial and management resources and, if decided unfavorably to us, could have a material adverse effect on the operating entities’ business and financial results.

Third parties may claim that the operating entities’ products or processes infringe their intellectual property rights, which may cause them to pay unexpected litigation costs or damages or prevent them from selling their products.

It is the operating entities’ intention to avoid infringing, misappropriating, or otherwise violating the intellectual property rights of others. We cannot, however, be certain that the conduct of the operating entities’ business or their products or processes do not infringe or otherwise violate these rights. From time to time, the operating entities may become subject to legal proceedings, including allegations and claims of alleged infringement or misappropriation by them of the patents and other intellectual property rights of third parties. As the operating entities’ business expands and faces increasing competition, the number of such claims may grow. In addition, attempts to enforce the operating entities’ own intellectual property claims may subject them to counterclaims that their intellectual property rights are invalid, unenforceable, or are licensed to the party against whom they are asserting the claim or that they are infringing that party’s alleged intellectual property rights.

| 14 |

| Table of Contents |

Legal proceedings involving intellectual property rights, regardless of merit, are highly uncertain and can involve complex legal and scientific analyses, can be time consuming, expensive to litigate or settle, and can significantly divert resources. The operating entities’ failure to prevail in such matters could result in loss of intellectual property rights or judgments awarding substantial damages and injunctive or other equitable relief against us. If the operating entities were to be held liable or discover or be notified that their products or processes potentially infringe or otherwise violate the intellectual property rights of others, they may face a loss of reputation, may not be able to exploit some or all of the operating entities’ intellectual property rights or technology, and may need to obtain licenses from third parties or substantially re-engineer the operating entities’ products or processes in order to avoid infringement. The operating entities might not be able to obtain the necessary licenses on acceptable terms, or at all, or be able to re-engineer the operating entities’ products or processes successfully or cost effectively and these efforts may cause them to delay or stop selling and marketing their products or processes.

Any of the foregoing may require considerable effort and expense, result in substantial increases in operating costs, delay or inhibit sales, and may preclude them from effectively competing in the marketplace, which in turn could have a material adverse effect on the operating entities’ business and financial results.

Compliance with environmental and other laws and regulations could result in significant costs and liabilities.

The operation and expansion of the operating entities’ manufacturing facilities are subject to strict environmental laws and regulations at the state, provincial, and local level in various jurisdictions, and, over the next several years, we expect that the operating entities and the industry in general will become subject to new or more stringent environmental requirements. These laws and regulations generally require the operating entities to obtain and comply with various environmental registrations, licenses, permits, inspections, and other approvals. In compliance with existing laws and regulations, Khingan Forasen obtained the License of Pollutant Discharges on February 27, 2020, which was valid for three years. With the expiration of this license in 2023, Khingan Forasen took proactive measures and temporarily ceased related productions to ensure compliance with current legal and regulatory standards. As of the date of this annual report, Khingan Forasen's delay in renewing its license did not have a material adverse effect on our business operations. Moving forward, our operating entities may apply for new licenses, a process expected to span three to six months, to resume related production activities.

Under certain environmental, health, and safety laws, the operating entities could be held responsible for any and all liabilities and consequences arising out of past or future releases of hazardous materials, human exposure to these substances, and other environmental damage, in some cases, without regard to fault. The discovery of contamination at any of the operating entities’ current site or at locations at which they dispose of waste may expose them to clean-up expenditures and other damages imposed by government agencies. In addition, private parties may have the right to pursue legal action to enforce compliance as well as to seek damages for non-compliance with such laws and regulations or for personal injury or property damage. Currently, the operating entities do not carry insurance that covers environmental risks and costs. Although the operating entities intend to procure environmental insurance in the future, such insurance may not cover all environmental risks and costs or may not provide sufficient coverage in the event an environmental claim is made against us.

The operating entities’ operations emit carbon dioxide and other greenhouse gases. Currently, the operating entities are subject to the PRC environmental laws and regulations on air pollution prevention in general. Additionally, businesses within the activated carbon industry are mandated to adhere to specific industrial standards, including the Comprehensive Emission Standards for Air Pollutants (GB 16297-1996), Emission Standards for Air Pollutants from Industrial Furnace Kilns (GB 9078-1996) and Comprehensive Wastewater Emission Standards (GB 8978-1996). A number of other legislative and regulatory measures to address greenhouse gas emissions, including the Kyoto Protocol and the Draft Emission Standards of Activated Carbon Industrial Pollutants, are in various phases of implementation or discussion. The systems and measures could result in increased costs for them to install new controls to reduce hazardous air emissions from the operating entities’ facilities, to purchase air emissions credits or allowances, or to monitor and inventory greenhouse gas emissions from the operating entities’ operations.

Even though the operating entities devote considerable efforts to comply with environmental laws, regulations, and permits, there can be no assurance that the operating entities’ operations will at all times be in compliance with them. The enactment of new environmental laws and regulations, the more stringent interpretation or enforcement of existing requirements, or the imposition of liabilities under environmental laws could force them to incur costs for compliance, capital upgrades, or liabilities relating to damage claims or limit the operating entities’ current or planned operations, any of which could have a material adverse effect on the operating entities’ business and financial results.

The operating entities’ operations are subject to various litigation risks that could increase the operating entities’ expenses and have a material adverse effect on their business and financial results.

The nature of the operating entities’ operations exposes them to possible litigation claims, including environmental damage and remediation, intellectual property, workers’ compensation and other employee-related matters, insurance coverage, and property rights and easements. Any claim could be adversely decided against us, which could have a material adverse effect on the operating entities’ business and financial results. Similarly, the costs associated with defending claims could dramatically increase the operating entities’ expenses as litigation is often very expensive, divert management’s attention, and impact their profitability. If the operating entities become involved in any litigation, they may be forced to direct their resources to defending or prosecuting the claim, which in turn could have a material adverse effect on the operating entities’ business and financial results.

| 15 |

| Table of Contents |

The operating entities may not be able to keep up with competitive changes affecting the activated carbon industry.

The activated carbon industry is characterized by evolving industry and end-market standards, changing regulation, frequent enhancements to existing products and technologies, introduction of new products and changing customer demand, all of which can result in unpredictable product transitions, shortened lifecycles and increased importance of being first to market with new products. The success of the operating entities’ new products depends on their initial and continued acceptance by their customers. If the operating entities are not able to anticipate changes or develop and introduce new and enhanced products that are accepted by the operating entities’ customers on a timely basis and compete with new technologies, their ability to remain competitive may be adversely affected. In addition, the operating entities may experience difficulties in the research, development, production, or marketing of new products, which may delay them in bringing new products to market and prevent them from recouping or realizing a return on the operating entities’ investments. Any of the foregoing could have a material adverse effect on the operating entities’ business and financial results.

The activated carbon industry is highly competitive, and if the operating entities are unable to compete effectively with existing competitors, or with new entrants, the operating entities’ business and financial results could be materially and adversely affected.

The operating entities compete in the PRC market with producers and importers of activated carbon. The operating entities’ business faces significant competition from other PRC producers of activated carbon, some of which may from time to time have revenue and capital resources exceeding ours, which they may use to develop more advanced or more cost-effective technologies, increase market share, or leverage their distribution networks. In addition, new competitors and alliances may emerge to take market share away from us. The operating entities’ competitive position in the market in which they operate depends upon the relative strength of these competitors in the market and the relative resources they devote to competing in the market. The operating entities could experience reduced sales and loss of market share, which could lead to lower prices and decreased revenue, gross margins, and profits, any of which could have a material and adverse effect on the operating entities’ results of operations.

Development of competitive technologies could materially and adversely affect the operating entities’ business and financial results.

Activated carbon is utilized in various applications as a cost-effective solution to address the operating entities’ customers’ needs. If other competitive technologies or alternative processes or combinations of technologies or processes, such as alternate sorbents, resins, certain types of membranes, ozone, and ultraviolet, are advanced to the stage at which they could compete on a cost-effective basis with activated carbon technologies, they could experience a decline in demand for the operating entities’ products, which could have a material adverse effect on the operating entities’ business and financial results.

Competitive technologies and new regulations may also affect the operating entities’ customers, and therefore us. For example, a shift away from coal-burning technology due to environmental trends and regulations or new technologies could diminish future demand for the operating entities’ activated carbon products, which could have a material adverse effect on the operating entities’ business and financial results.

If the operating entities fail to hire, train, and retain qualified managerial and other employees, the operating entities’ business and results of operations could be materially and adversely affected.

The operating entities place substantial reliance on the activated carbon and biomass electricity market experience and knowledge of their senior management team as well as their relationships with other industry participants. The operating entities do not carry, and do not intend to procure, key person insurance on any of their senior management team. The loss of the services of one or more members of their senior management team due to their departure, or otherwise, could hinder the operating entities’ ability to effectively manage their business and implement their growth strategies. Finding suitable replacements for the operating entities’ current senior management could be difficult, and competition for such personnel of similar experience is intense. If the operating entities fail to retain their senior management, the operating entities’ business and results of operations could be materially and adversely affected.

The market for engineers and other individuals with the required technical expertise to succeed in the operating entities’ business is highly competitive. There may be a limited supply of qualified individuals in some of the cities in China where the operating entities have operations and other cities into which they intend to expand. The operating entities must hire and train qualified managerial and other employees on a timely basis to keep pace with the operating entities’ rapid growth while maintaining consistent quality of services across the operating entities’ operations in various geographic locations. The operating entities must also provide continuous training to their managerial and other employees so that they are equipped with up-to-date knowledge of various aspects of the operating entities’ operations and can meet the operating entities’ demand for high-quality products. If they fail to do so, the quality of their products may decrease in one or more of the markets where they operate, which in turn, may cause a negative perception of the operating entities’ brand and adversely affect the operating entities’ business.

| 16 |

| Table of Contents |

The lease agreements of the operating entities’ leased properties have not been registered with the relevant PRC government authorities as required by PRC laws, which may expose them to potential fines.

Under PRC laws, all lease agreements are required to be registered with the local land and real estate administration bureau. Although failure to do so does not in itself invalidate the leases, the lessees may not be able to defend these leases against bona fide third parties and may also be exposed to potential fines if they fail to rectify such non-compliance within the prescribed time frame after receiving notice from the relevant PRC government authorities.

The penalty ranges from RMB1,000 to RMB10,000 for each unregistered lease, at the discretion of the relevant authority. As of the date of this annual report, the operating entities have not registered the lease agreements for their headquarters or the leased properties of Tahe Biopower Plant with the relevant PRC government authorities. In the event that any fine is imposed on the operating entities for their failure to register their lease agreements, the operating entities may not be able to recover such losses from the lessors. However, as the fines, if any, will be minor, the operating entities’ business and financial results will not be materially affected.

Unexpected termination of leases or other arrangements, failure to negotiate satisfactory terms for or duly perform leases or other arrangements, failure to renew the leases or other arrangements of the existing premises of the operating entities or to renew such leases or other arrangements at acceptable terms could materially and adversely affect our business, financial condition, results of operations and prospects.