UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

OR

For

the fiscal year ended

OR

OR

Date of event requiring this shell company report

For the transition period from to

Commission

file number

(Exact name of Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

People’s

Republic of

(Address of principal executive offices)

Telephone:

of08@dogness.com

People’s

Republic of

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: Class A Common Shares and Class B Common Shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐

Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐

Yes ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |||

| Emerging

growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

☐

Yes ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements in this annual report with respect to the Company’s current plans, estimates, strategies and beliefs and other statements that are not historical facts are forward-looking statements about the future performance of the Company. Forward-looking statements include, but are not limited to, those statements using words such as “believe,” “expect,” “plans,” “strategy,” “prospects,” “forecast,” “estimate,” “project,” “anticipate,” “aim,” “intend,” “seek,” “may,” “might,” “could” or “should,” and words of similar meaning in connection with a discussion of future operations, financial performance, events or conditions. From time to time, oral or written forward-looking statements may also be included in other materials released to the public. These statements are based on management’s assumptions, judgments and beliefs in light of the information currently available to it. The Company cautions investors that a number of important risks and uncertainties could cause actual results to differ materially from those discussed in the forward-looking statements, including but not limited to, our ability to continue as a going concern, product and service demand and acceptance, changes in technology, economic conditions, the impact of competition and pricing, government regulation, and other risks contained in reports filed by the company with the Securities and Exchange Commission. Therefore, investors should not place undue reliance on such forward-looking statements. Actual results may differ significantly from those set forth in the forward-looking statements.

All such forward-looking statements, whether written or oral, and whether made by or on behalf of the company, are expressly qualified by the cautionary statements and any other cautionary statements which may accompany the forward-looking statements. In addition, the company disclaims any obligation to update any forward-looking statements to reflect events or circumstances after the date hereof.

Part I

We are not a Chinese operating company but a British Virgin Islands holding company with operations conducted by our subsidiaries established in Delaware, mainland China, Hong Kong Special Administrative Region of the People’s Republic of China and British Virgin Islands. Therefore, investing in our securities involves unique and a high degree of risk. You should carefully read and consider the risk factors of this report (beginning on page 8), especially the risk factors under the caption “Risks Related to Our Corporate Structure and Operation” (beginning on Page 20 ) and “Risks Related to Doing Business in China” (beginning on Page 29).

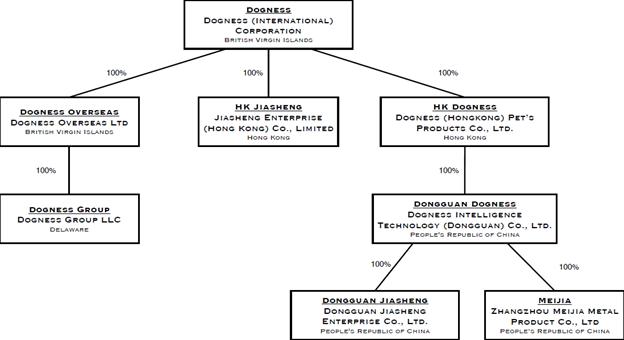

Unless otherwise indicated or the context requires otherwise, references in this prospectus to “China” or the “PRC” are to the mainland of People’s Republic of China, Taiwan, Hong Kong Special Administrative Region of the People’s Republic of China (“HKSAR” or “Hong Kong”), and the special administrative regions of Macau (for the purposes of this prospectus only); “mainland China” are to the mainland of the People’s Republic of China, excluding Taiwan Hong Kong, and Macau (for the purposes of this prospectus only); “Mainland China Subsidiaries” refer to our subsidiaries incorporated in mainland China, including Dogness Intelligent Technology (Dongguan) Co., Ltd., a mainland China company (“Dongguan Dogness”), Dongguan Jiasheng Enterprise Co., Ltd., a mainland China company (“Dongguan Jiasheng”), Zhangzhou Meijia Metal Product Co., Ltd, a mainland China company (“Meijia”), and Dogness Intelligence Technology Co., Ltd., a mainland China company (“Intelligence Guangzhou”); “Hong Kong Subsidiaries” refer to our subsidiaries incorporated in Hong Kong, including Jiasheng Enterprise (Hongkong) Co., Limited, a Hong Kong company (“HK Jiasheng”) and Dogness (Hongkong) Pet’s Products Co., Limited, a Hong Kong company (“HK Dogness”). We will also refer to all of our subsidiaries, as the “Subsidiaries”.

The Securities registered under the Securities Act and the Exchange Act are of the off-shore holding company Dogness (International) Corporation (the “Company”), a British Virgin Islands company, which owns equity interests, directly or indirectly, of the operating subsidiaries. Subsidiaries conduct operations in China and the holding company does not conduct operations in China.

We are subject to legal and operational risks associated with being based in and having the majority of the company’s operations in mainland China and Hong Kong. These risks include, among others, the following:

| ● | PRC government interference. The Chinese government may intervene or influence the operation of our Hong Kong and mainland China operating entities and exercise significant oversight and discretion over the conduct of their business and may intervene in or influence their operations at any time with little advance notice, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or the value of our Class A Common Shares. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer Securities to investors and cause the value of such securities to significantly decline or be worthless. See Risk Factors – Risks Related to Doing Business in China – “China’s economic, political and social conditions, as well as changes in any government policies, laws and regulations may be quick with little advance notice and, could have a material adverse effect on our business and the value of our Class A Common Shares” and “The Chinese government exerts substantial influence over the manner in which we must conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Class A Common Shares” and “The Chinese government exerts oversight and control over overseas offerings and listing conducted by China-based issuers under the Listing Records Rules and/or the Confidentiality Provisions, which could significantly limit or completely hinder our ability to offer or continue to offer our Class A Common Shares to investors and could cause the value of our Class A Common Shares to significantly decline or become worthless”. | |

| ● | Uncertain PRC legal enforcement. The mainland China legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. We conduct our business primarily through our subsidiaries established in China. These subsidiaries are generally subject to laws and regulations applicable to foreign investment in China. However, since these laws and regulations are relatively new and the mainland China legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to us. See Risk Factors – Risks Related to Doing Business in China – “Uncertainties with respect to the mainland China legal system could have a material adverse effect on us”. | |

| ● | Shareholder enforcement risk. Since we conduct a significant portion of our operations in mainland China, the majority of our assets are located in mainland China, and all of our directors, officers or senior management other than Yunhao Chen, are located in mainland China, it may be more difficult for shareholders to enforce liabilities and enforce judgments on those individuals. Our PRC legal counsel, Guangdong Jiamao Law Firm, has advised us that mainland China does not have treaties providing for the reciprocal recognition and enforcement of judgments of courts with the Cayman Islands and many other countries and regions. Therefore, recognition and enforcement in mainland China of judgments of a court in any of these jurisdictions outside mainland China in relation to any matter not subject to a binding arbitration provision may be difficult or impossible. See Risk Factors – Risks Related to Doing Business in China – “You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions in mainland China against us or Hong Kong or other foreign laws, and the ability of U.S. authorities to bring actions in mainland China may also be limited”. |

| 1 |

| ● | Repatriation of offering proceeds to PRC. In utilizing the proceeds of this offering in the manner described in “Use of Proceeds,” as an offshore holding company of our PRC operating subsidiary, we may decide to make loans or additional contributions to our PRC subsidiary or the VIE. Certain governmental registrations, submissions or approvals need to be completed or obtained in this regard. Failure to complete such registrations, submissions or obtain such approvals, our ability to use the proceeds from our initial public offering and to capitalize or otherwise fund our PRC operations may be negatively affected. See Risk Factors – Risks Related to Doing Business in China – “We must remit the offering proceeds to China before they may be used to benefit our business in China, the process of which may be time-consuming, and we cannot assure that we can finish all necessary governmental registration processes in a timely manner” and “PRC regulation of loans and direct investment by offshore holding companies to mainland China entities may delay or prevent us from using the proceeds of this Offering to make loans or additional capital contributions to our Mainland China Subsidiary, which could materially and adversely affect our liquidity and our ability to fund and expand our business”. |

| ● | Restriction on currency conversion. The PRC government imposes control on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of mainland China. We receive a majority of our revenues in Renminbi, which currently is not a freely convertible currency. Restrictions on currency conversion imposed by the PRC government may limit our ability to use revenues generated in Renminbi to fund our expenditures denominated in foreign currencies or our business activities outside mainland China. See Risk Factors – Risks Related to Doing Business in China – “Governmental control of currency conversion may limit our ability to use our revenues effectively and the ability of our Mainland China Subsidiaries to obtain financing”. | |

| ● | Restrictions on dividend payment. As a holding company, we rely principally on dividends and other distributions on equity from our subsidiaries, including those based in China, for our cash requirements, including for services of any debt we may incur. Our Mainland China Subsidiaries’ ability to distribute dividends is based upon their distributable earnings. Current PRC regulations permit our Mainland China Subsidiaries to pay dividends to their respective shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, if our Mainland China Subsidiaries incur debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments to us. Any limitation on the ability of our Mainland China Subsidiaries to distribute dividends or other payments to their respective shareholders could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends or otherwise fund and conduct our business. See Risk Factors – Risks Related to Doing Business in China – “We may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in the PRC, for our cash and financing requirements we may have, and any limitation on the ability of our Mainland China Subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business”. | |

| ● | Possibility to be classified as “Resident Enterprise.” Under the Enterprise Income Tax Law, Dogness may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our shareholders outside of mainland China, including repayment of any underpayments and penalties for underpayment. See Risk Factors – Risks Related to Doing Business in China – “We may be classified as a “resident enterprise” for mainland China enterprise income tax purposes; such classification could result in unfavorable tax consequences to us and our non-mainland China shareholders”. |

Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, adopting new measures to impose filing requirements on China-based companies for their initial public offerings or listings in overseas stock markets and extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly released the Opinions on Severely Cracking Down on Illegal Securities Activities According to Law, or the Opinions. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection requirements, etc. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future.

| 2 |

On February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the relevant system and rules for the management of overseas listing records, which will be implemented from March 31, 2023. A total of six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”) and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement, misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the listing and trading of our Class A Common Shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required. Further, we believe, as of the date of this annual report, none of the circumstances prohibiting the overseas offering and listing by domestic companies established in mainland China as listed above applies to us, and we can offer and continue to offer our Class A Common Shares on Nasdaq.

In accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we have been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our Mainland China Subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our Mainland China Subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

Further, on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which will come into effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators, any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws and regulations. Once effective, any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected of committing a crime. As of the date of this annual report, we believe that we and our subsidiaries have not provided or publicly disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. We intend to strictly comply with the Confidentiality Provisions and other relevant PRC laws and regulations in our offering and listing on Nasdaq in future.

| 3 |

However, any failure of us or our Mainland China Subsidiaries to fully comply with the Listing Records Rules and/or the Confidentiality Provisions, once effective, may significantly limit or completely hinder our ability to offer or continue to offer our Class A Common Shares on Nasdaq, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our Class A Common Shares to significantly decline in value or become worthless. See “Risk Factor — Risks Related to Doing Business in China — The Chinese government exerts oversight and control over overseas offerings and listing conducted by China-based issuers under the Listing Records Rules and the Confidentiality Provisions, which could significantly limit or completely hinder our ability to offer or continue to offer our Class A Common Shares to investors and could cause the value of our Class A Common Shares to significantly decline or become worthless.”

We or our Subsidiaries may also be subject to PRC laws relating to the use, sharing, retention, security and transfer of confidential and private information, such as personal information and other data. On November 14, 2021, the Cyberspace Administration of China (“CAC”) released the Regulations on the Network Data Security Management (Draft for Comments), or the Data Security Management Regulations Draft, to solicit public opinion and comments till December 13, 2021, which has not been promulgated as of the date of this annual report. Pursuant to the Data Security Management Regulations Draft, data processors holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. Data processing activities refers to activities such as the collection, retention, use, processing, transmission, provision, disclosure, or deletion of data. According to the latest amended Cybersecurity Review Measures, which was promulgated on November 16, 2021 and became effective on February 15, 2022, an online platform operator holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. As of the date of this annual report, we have not been informed by any PRC governmental authority of any requirement that we or our Subsidiaries file for approval for this offering. We don’t believe that we or any of our Subsidiaries will be subject to either the amended Cybersecurity Review Measures or the Data Security Management Regulations Draft since none of us hold more than one million users/users’ individual information. However, it is uncertain how the above mentioned new laws or regulations will be enacted, interpreted or implemented, and whether it will affect us. Since the regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our Subsidiaries’ daily business operation, their ability to accept foreign investments, and our ability to continue to list or offer securities on an U.S. exchange. See “Risk Factor — Risks Related to Doing Business in China — The Chinese government exerts substantial influence over the manner in which we must conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Class A Common Shares.”

On February 7, 2021, the Anti-Monopoly Committee of the State Council promulgated the Anti-monopoly Guidelines for the Platform Economy Sector, or the Anti-monopoly Guideline, aiming to improve anti-monopoly administration on online platforms. The Anti-monopoly Guideline, operating as the compliance guidance under the then-existing PRC anti-monopoly regulatory regime for platform economy operators, specifically prohibits certain acts of the platform economy operators that may have the effect of eliminating or limiting market competition, such as concentration of undertakings. The PRC anti-monopoly regulatory regime started with the Anti-Monopoly Law promulgated by the Standing Committee of the National People’s Congress of China (“SCNPC”) on August 30, 2007 and effective on August 1, 2008, which requires that transactions which are deemed concentrations and involve parties with specified turnover thresholds must be cleared by the Ministry of Commerce of China (“MOFCOM”) before they can be completed. In addition, on February 3, 2011, the General Office of the State Council promulgated a Notice on Establishing the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, or Circular 6, which officially established a security review system for mergers and acquisitions of domestic enterprises by foreign investors. Further, on August 25, 2011, MOFCOM promulgated the Regulations on Implementation of Security Review System for the Merger and Acquisition of Domestic Enterprises by Foreign Investors, or the MOFCOM Security Review Regulations, which became effective on September 1, 2011, to implement Circular 6. Under Circular 6, a security review is required for mergers and acquisitions by foreign investors having “national defense and security” concerns and mergers and acquisitions by which foreign investors may acquire the “de facto control” of domestic enterprises with “national security” concerns. Under the MOFCOM Security Review Regulations, MOFCOM will focus on the substance and actual impact of the transaction when deciding whether a specific merger or acquisition is subject to security review. If MOFCOM decides that a specific merger or acquisition is subject to security review, it will submit it to the Inter-Ministerial Panel, an authority established under the Circular 6 led by the NDRC, and MOFCOM under the leadership of the State Council, to carry out the security review. The regulations prohibit foreign investors from bypassing the security review by structuring transactions through trusts, indirect investments, leases, loans, control through contractual arrangements or offshore transactions.

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable for annual reports on Form 20-F.

Item 2. Offer Statistics and Expected Timetable

Not applicable for annual reports on Form 20-F.

Item 3. Key Information

| 4 |

Dividend Distributions and Cash Transfer among Dogness and the Subsidiaries

As a holding company, we may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in mainland China, for our cash and financing requirements. If any of our Mainland China Subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. To date, none of the Subsidiaries has made any dividends or distributions to Dogness, and Dogness has not made any dividends or distributions to our shareholders. We anticipate that we will retain any earnings to support operations and to finance the growth and development of our business. Therefore, we do not expect to pay Company cash dividends in the foreseeable future. Under British Virgin Islands law, we may only pay dividends from surplus (the excess, if any, at the time of the determination of the total assets of our company over the sum of our liabilities, as shown in our books of account, plus our capital), and we must be solvent before and after the dividend payment in the sense that we will be able to satisfy our liabilities as they become due in the ordinary course of business; and the realizable value of assets of our company will not be less than the sum of our total liabilities, other than deferred taxes as shown on our books of account, and our capital. If we determine to pay dividends on any of our Common Shares in the future, as a holding company, we will be dependent on receipt of funds from our Hong Kong subsidiaries, HK Jiasheng and HK Dogness. Current PRC regulations permit the Mainland China Subsidiaries to pay dividends to HK Dogness only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in mainland China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in mainland China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and, in certain cases, the remittance of currencies out of mainland China. We receive a majority of our revenues in Renminbi, which currently is not a freely convertible currency. Restrictions on currency conversion imposed by the PRC government may limit our ability to use revenues generated in Renminbi to fund our expenditures denominated in foreign currencies or our business activities outside China. Under China’s existing foreign exchange regulations, Renminbi may be freely converted into foreign currency for payments relating to current account transactions, which include among other things dividend payments and payments for the import of goods and services, by complying with certain procedural requirements. Our Mainland China Subsidiaries are able to pay dividends in foreign currencies to us without prior approval from the related government agencies, by complying with certain procedural requirements. Our Mainland China Subsidiaries may also retain foreign currency in their respective current account bank accounts for use in payment of international current account transactions. However, we cannot assure you that the PRC government will not at its discretion take measures in the future to restrict access to foreign currencies for current account transactions.

Conversion of Renminbi into foreign currencies, and of foreign currencies into Renminbi, for payments relating to capital account transactions, which principally includes investments and loans, generally requires the approval of China’s State Administration of Foreign Exchange (“SAFE”) or other relevant PRC governmental authorities. Any foreign loans procured by our Mainland China Subsidiaries is required to be registered with SAFE or its local branches or satisfy relevant requirements. According to the relevant PRC regulations on foreign-invested enterprises in China, capital contributions to our Mainland China Subsidiaries are subject to the approval of or filing with State Administration for Market Regulation in its local branches, the Ministry of Commerce in its local branches and registration with a local bank authorized by SAFE. For these capital account transactions, we must take the steps legally required under the PRC laws, for example, we will open a special foreign exchange account, remit the offering proceeds into such special foreign exchange account, and apply for settlement of the foreign exchange. The timing of the process is difficult to estimate because the efficiencies of different SAFE branches can vary materially. In light of the various requirements imposed by PRC regulations on loans to, and direct investment in, mainland China entities by offshore holding companies, we cannot assure you that we will be able to complete the necessary government registrations or obtain the necessary government approvals on a timely basis, if at all, with respect to future loans by us to our Mainland China Subsidiaries or with respect to future capital contributions by us to our Mainland China Subsidiaries. If we fail to complete such registrations or obtain such approvals, our ability to use the proceeds from this offering and to capitalize or otherwise fund our mainland China operations may be negatively affected, which could materially and adversely affect our liquidity, our ability to fund and expand our business and our Common Shares. On the other hand, restrictions on the convertibility of the Renminbi for capital account transactions could affect the ability of our Mainland China Subsidiaries to make investments overseas or to obtain foreign currency through debt or equity financing, including by means of loans or capital contributions from us. We cannot assure you that the registration process will not delay or prevent the conversion of Renminbi for use outside of China. Currently, we have installed cash management policies or procedures in place that dictate how funds are transferred, under an umbrella of corporate policies and financial reporting policies. Even though our policies do not specifically address the limitations, as discussed above, on the amount of funds the Company can transfer out of China, if we decide to transfer cash out of China in the future, all relevant transfers will be conducted in compliance with such limitations. Please see “Risk Factor — Risks Related to Doing Business in China — China’s economic, political and social conditions, as well as changes in any government policies, laws and regulations, could have a material adverse effect on our business”; “Risk Factor — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in mainland China, for our cash and financing requirements we may have, and any limitation on the ability of our Mainland China Subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business”; “Risk Factor — Risks Related to Doing Business in China — PRC regulation of loans and direct investment by offshore holding companies to mainland China entities may delay or prevent us from using the proceeds of this Offering to make loans or additional capital contributions to our Mainland China Subsidiary, which could materially and adversely affect our liquidity and our ability to fund and expand our business”; “Risk Factor — Risks Related to Doing Business in China — Governmental control of currency conversion may limit our ability to use our revenues effectively and the ability of our Mainland China Subsidiaries to obtain financing”; and ‘Risk Factor — Risks Related to Doing Business in China — We must remit the offering proceeds to China before they may be used to benefit our business in China, the process of which may be time-consuming, and we cannot assure that we can finish all necessary governmental registration processes in a timely manner.”

| 5 |

In addition, the transfer of funds among our Mainland China Subsidiaries are subject to the Provisions of the Supreme People’s Court on Several Issues Concerning the Application of Law in the Trial of Private Lending Cases (2020 Revision, the “Provisions on Private Lending Cases”), which was implemented on August 20, 2020 to regulate the financing activities between natural persons, legal persons and unincorporated organizations. The Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary to fund the operations of another subsidiary in China. As of the date of this annual report, no cash generated from one subsidiary has been used to fund another subsidiary’s operations, expect for the financing obtained by the Company be transferred to operating entities for their operations. We have not been notified of any other restriction which could limit our Mainland China Subsidiaries’ ability to transfer cash between subsidiaries in China, and do not anticipate any difficulties or limitations in our ability to transfer cash between subsidiaries. As of the date of this annual report, no cash generated from one subsidiary has been used to fund another subsidiary’s operations; for that reason, our cash management policies do not specifically address this type of transfers between subsidiaries. We do not anticipate any occasions where cash generated from one subsidiary needs to be transferred to another subsidiary and will comply with PRC laws discussed above should we decide to conduct such a transfer.

Cash flow between Dogness and the Subsidiaries primarily consists of transfers from Dogness to these Subsidiaries for short-term working capital loan, which is mainly used in payment of operating expenses and investments. To date, there are no other assets transferred between Dogness and the Subsidiaries except for the below cash transfers:

| ● | For the year ended June 30, 2021, Dogness transferred $505,850 to the Delaware subsidiary, Dogness Group LLC, for short term working capital loan purpose and transferred $2,581,533 to HK Dogness for short term working capital loan purpose. The source of funds was the registered direct public offering we completed on January 20,2021 with net proceeds of $6.6 million. For the year ended June 30, 2021, Dogness also received cash repayment transferred from HK Dogness in the amount of $304. |

| ● | For the year ended June 30, 2022, Dogness transferred $186,500 to the Delaware subsidiary, Dogness Group LLC, for working capital loan purpose and transferred $15,577,896 to HK Dogness for working capital loan purpose. The source of the funds was mainly from the equity financing and the exercise of warrants in fiscal 2022. For the year ended June 30, 2022, Dogness also received cash payment transferred from HK Dogness in the amount of $1,999,787. |

| ● | For the year ended June 30, 2023, Dogness transferred $13.3 million to HK Dogness for working capital loan purpose. The source of the funds was mainly from the equity financing and the exercise of warrants in fiscal 2022. |

In the future, cash proceeds raised from overseas financing activities may be transferred by Dogness to the Subsidiaries via capital contribution or shareholder loans, as the case may be.

| 6 |

A. Selected Financial Data

In the table below, we provide you with historical selected financial data for the fiscal years ended June 30, 2023, 2022, and 2021. This information is derived from our consolidated financial statements included elsewhere in this annual report. Historical results are not necessarily indicative of the results that may be expected for any future period. When you read this historical selected financial data, it is important that you read it along with the historical financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this annual report. Our audited consolidated financial statements are prepared and presented in accordance with Generally Accepted Accounting Principles in the United States of America, or U.S. GAAP.

| For Fiscal | For Fiscal | For Fiscal | ||||||||||

| Year Ended | Year Ended | Year Ended | ||||||||||

| June 30, | June 30, | June 30, | ||||||||||

| 2023 | 2022 | 2021 | ||||||||||

| US$ | US$ | US$ | ||||||||||

| (audited) | (audited) | (audited) | ||||||||||

| Statement of operation data: | ||||||||||||

| Revenues | $ | 17,584,454 | $ | 27,095,197 | $ | 24,320,121 | ||||||

| Gross profit | 3,661,288 | 10,139,065 | 9,155,213 | |||||||||

| Operating expenses | 13,225,261 | 10,065,009 | 7,297,420 | |||||||||

| Income (loss) from operations | (9,563,973 | ) | 74,056 | 1,857,793 | ||||||||

| Other income | 877,050 | 164,208 | 82,695 | |||||||||

| Income taxes (benefit) expense | (1,227,449 | ) | (2,777,868 | ) | 641,460 | |||||||

| Net income (loss) | $ | (7,459,474 | ) | $ | 3,016,132 | $ | 1,299,028 | |||||

| Earnings (loss) per share, basic and diluted | $ | (0.18 | ) | $ | 0.10 | $ | 0.05 | |||||

| Weighted average Ordinary Shares outstanding (basic) | 39,668,780 | 33,711,659 | 27,499,367 | |||||||||

Balance sheet data:

| As of June 30, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Current assets | $ | 14,003,843 | $ | 23,354,676 | $ | 14,266,131 | $ | 11,627,458 | $ | 25,922,624 | ||||||||||

| Total assets | 97,871,328 | 100,796,722 | 93,845,408 | 63,551,261 | 69,023,927 | |||||||||||||||

| Current liabilities | 9,317,966 | 6,485,021 | 21,262,335 | 10,769,734 | 8,072,423 | |||||||||||||||

| Total liabilities | 21,526,023 | 12,320,746 | 28,943,003 | 12,043,333 | 8,072,423 | |||||||||||||||

| Total equity | $ | 76,345,305 | $ | 88,475,976 | $ | 64,902,405 | $ | 51,507,928 | $ | 60,951,504 | ||||||||||

Exchange Rate Information

Our financial information is presented in U.S. dollars. The financial position and results of the operations of HK Dogness, HK Jiasheng, Dongguan Dogness, Dongguan Jiasheng, Meijia and Intelligence Guangzhou are determined using the Chinese Renminbi (“RMB”), the local currency, as the functional currency. Dogness Japan uses Japanese Yen as the functional currency (the shares held in Dogness Japan were sold on November 28, 2020 during the fiscal year ended June 30, 2021), while Dogness Overseas and Dogness Group use U.S Dollar as their functional currency.

The results of operations and the consolidated statements of cash flows denominated in foreign currencies are translated at the average rate of exchange during the reporting period. Assets and liabilities denominated in foreign currencies at the balance sheet date are translated at the applicable rates of exchange in effect at that date. The equity denominated in the functional currency is translated at the historical rate of exchange at the time of capital contribution. Because cash flows are translated based on the average translation rate, amounts related to assets and liabilities reported on the consolidated statements of cash flows will not necessarily agree with changes in the corresponding balances on the consolidated balance sheets. Translation adjustments arising from the use of different exchange rates from period to period are included as a separate component of accumulated other comprehensive income included in consolidated statements of changes in equity. Gains and losses from foreign currency transactions are included in the consolidated statement of income and comprehensive income.

| 7 |

The relevant exchange rates are listed below:

| June 30, 2023 | June 30, 2022 | June 30, 2021 | ||||||

| Year-end spot rate | US$1=RMB7.2513 | US$1=RMB6.6981 | US$1=RMB 6.4566 | US$1=JPY 111.1 | ||||

| Average rate | US$1=RMB6.9536 | US$1=RMB6.4554 | US$1=RMB 6.6221 | US$1=JPY 106.6 | ||||

We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. We do not currently engage in currency hedging transactions.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated.

| Midpoint of Buy and Sell Prices for U.S. Dollar per RMB | ||||||||||||||||

| Period | Period-End | Average | High | Low | ||||||||||||

| 2015 | 6.4917 | 6.2288 | 6.4917 | 6.0933 | ||||||||||||

| 2016 | 6.9448 | 6.6441 | 7.0672 | 6.4494 | ||||||||||||

| 2017 | 6.5074 | 6.7578 | 6.9535 | 6.4686 | ||||||||||||

| 2018 | 6.8776 | 6.6163 | 7.1786 | 6.6822 | ||||||||||||

| 2019 | 6.9618 | 6.9081 | 7.1786 | 6.6822 | ||||||||||||

| 2020 | 6.5250 | 6.9042 | 7.1681 | 6.5208 | ||||||||||||

| 2021 | 6.3839 | 6.4668 | 6.5716 | 6.3674 | ||||||||||||

| 2022 | 6.8983 | 6.7328 | 7.3055 | 6.3094 | ||||||||||||

| 2023 (through October 10, 2023) | 7.2954 | 7.0406 | 7.3430 | 6.7030 | ||||||||||||

As of October 10, 2023, the exchange rate is RMB 7.2954 to $1.00.

B. Capitalization and Indebtedness

Not applicable for annual reports on Form 20-F.

C. Reasons for the Offer and Use of Proceeds

Not applicable for annual reports on Form 20-F.

D. Risk Factors

Before you decide to purchase our Class A Common Shares, you should understand the high degree of risk involved. You should consider carefully the following risks and other information in this report, including our consolidated financial statements and related notes. If any of the following risks actually occur, our business, financial condition and operating results could be adversely affected. As a result, the trading price of our Class A Common Shares could decline, perhaps significantly.

Please also read carefully the section below entitled “Cautionary Note Regarding Forward-Looking Statements.”

| 8 |

Summary of Major Risk Factors

| ● | PRC government interference. The Chinese government may intervene or influence the operation of our Hong Kong and mainland China operating entities and exercise significant oversight and discretion over the conduct of their business and may intervene in or influence their operations at any time with little advance notice, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or the value of our Class A Common Shares. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer Securities to investors and cause the value of such securities to significantly decline or be worthless. See Risk Factors – Risks Related to Doing Business in China – “China’s economic, political and social conditions, as well as changes in any government policies, laws and regulations may be quick with little advance notice and, could have a material adverse effect on our business and the value of our Class A Common Shares” and “The Chinese government exerts substantial influence over the manner in which we must conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Class A Common Shares” and “The Chinese government exerts oversight and control over overseas offerings and listing conducted by China-based issuers under the Listing Records Rules and/or the Confidentiality Provisions, which could significantly limit or completely hinder our ability to offer or continue to offer our Class A Common Shares to investors and could cause the value of our Class A Common Shares to significantly decline or become worthless”. | |

| ● | Uncertain PRC legal enforcement. The mainland China legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. We conduct our business primarily through our subsidiaries established in China. These subsidiaries are generally subject to laws and regulations applicable to foreign investment in China. However, since these laws and regulations are relatively new and the mainland China legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to us. See Risk Factors – Risks Related to Doing Business in China – “Uncertainties with respect to the mainland China legal system could have a material adverse effect on us”. | |

| ● | Shareholder enforcement risk. Since we conduct a significant portion of our operations in mainland China, the majority of our assets are located in mainland China, and all of our directors, officers or senior management other than Yunhao Chen, are located in mainland China, it may be more difficult for shareholders to enforce liabilities and enforce judgments on those individuals. Our PRC legal counsel, Guangdong Jiamao Law Firm, has advised us that mainland China does not have treaties providing for the reciprocal recognition and enforcement of judgments of courts with the Cayman Islands and many other countries and regions. Therefore, recognition and enforcement in mainland China of judgments of a court in any of these jurisdictions outside mainland China in relation to any matter not subject to a binding arbitration provision may be difficult or impossible. See Risk Factors – Risks Related to Doing Business in China – “You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions in mainland China against us or Hong Kong or other foreign laws, and the ability of U.S. authorities to bring actions in mainland China may also be limited”. | |

| ● | Repatriation of offering proceeds to PRC. In utilizing the proceeds of this offering in the manner described in “Use of Proceeds,” as an offshore holding company of our PRC operating subsidiary, we may decide to make loans or additional contributions to our PRC subsidiary or the VIE. Certain governmental registrations, submissions or approvals need to be completed or obtained in this regard. Failure to complete such registrations, submissions or obtain such approvals, our ability to use the proceeds from our initial public offering and to capitalize or otherwise fund our PRC operations may be negatively affected. See Risk Factors – Risks Related to Doing Business in China – “We must remit the offering proceeds to China before they may be used to benefit our business in China, the process of which may be time-consuming, and we cannot assure that we can finish all necessary governmental registration processes in a timely manner” and “PRC regulation of loans and direct investment by offshore holding companies to mainland China entities may delay or prevent us from using the proceeds of this Offering to make loans or additional capital contributions to our Mainland China Subsidiary, which could materially and adversely affect our liquidity and our ability to fund and expand our business”. |

| 9 |

| ● | Restriction on currency conversion. The PRC government imposes control on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of mainland China. We receive a majority of our revenues in Renminbi, which currently is not a freely convertible currency. Restrictions on currency conversion imposed by the PRC government may limit our ability to use revenues generated in Renminbi to fund our expenditures denominated in foreign currencies or our business activities outside mainland China. See Risk Factors – Risks Related to Doing Business in China – “Governmental control of currency conversion may limit our ability to use our revenues effectively and the ability of our Mainland China Subsidiaries to obtain financing”. | |

| ● | Restrictions on dividend payment. As a holding company, we rely principally on dividends and other distributions on equity from our subsidiaries, including those based in China, for our cash requirements, including for services of any debt we may incur. Our Mainland China Subsidiaries’ ability to distribute dividends is based upon their distributable earnings. Current PRC regulations permit our Mainland China Subsidiaries to pay dividends to their respective shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, if our Mainland China Subsidiaries incur debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments to us. Any limitation on the ability of our Mainland China Subsidiaries to distribute dividends or other payments to their respective shareholders could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends or otherwise fund and conduct our business. See Risk Factors – Risks Related to Doing Business in China – “We may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in the PRC, for our cash and financing requirements we may have, and any limitation on the ability of our Mainland China Subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business”. | |

| ● | Possibility to be classified as “Resident Enterprise.” Under the Enterprise Income Tax Law, Dogness may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our shareholders outside of mainland China, including repayment of any underpayments and penalties for underpayment. See Risk Factors – Risks Related to Doing Business in China – “We may be classified as a “resident enterprise” for mainland China enterprise income tax purposes; such classification could result in unfavorable tax consequences to us and our non-mainland China shareholders”. |

Risks Related to Our Business

We face risks related to health epidemics that could impact our sales and operating results.

Our business could be adversely affected by the effects of a widespread outbreak of contagious disease, including the recent outbreak of respiratory illness caused by a novel coronavirus first identified in Wuhan, Hubei Province, China. Any outbreak of contagious diseases, and other adverse public health developments, particularly in China, could have a material and adverse effect on the business operations of us and our Subsidiaries. These could include disruptions or restrictions on our ability to resume the general shipping agency services, as well as temporary closures of our facilities and ports or the facilities of our customers and third-party service providers. Any disruption or delay of our customers or third-party service providers would likely impact our operating results and the ability of the Company to continue as a going concern. In addition, a significant outbreak of contagious diseases in the human population could result in a widespread health crisis that could adversely affect the economies and financial markets of China and many other countries, resulting in an economic downturn that could affect demand for our services and significantly impact our operating results.

| 10 |

The coronavirus disease 2019 (COVID-19) has had a significant impact on our operations since January 2020 and could materially adversely affect our business and financial results for the remaining months of the 2023 calendar year.

Our ability to manufacture and/or sell our products may be impaired by damage or disruption to our manufacturing, warehousing or distribution capabilities, or to the capabilities of our suppliers, logistics service providers or distributors as a result of the impact from the COVID-19. This damage or disruption could result from events or factors that are impossible to predict or are beyond our control, such as raw material scarcity, pandemics, government shutdowns, disruptions in logistics, supplier capacity constraints, adverse weather conditions, natural disasters, fire, terrorism or other events.

The COVID-19 pandemic, which has spread rapidly across the globe, resulted in adverse economic conditions and business disruptions. In reaction to this outbreak, governments worldwide have imposed varying degrees of preventative and protective actions, such as temporary travel bans, forced business closures, and stay-at-home orders, all in an effort to reduce the spread of the virus. Since this outbreak, business activities in China and many other countries including U.S. have been disrupted by a series of emergency quarantine measures taken by the government. The Chinese government has employed measures including city lockdowns, quarantines, travel restrictions, suspension of business activities and school closures. Due to difficulties resulting from the COVID-19 outbreak, including, but not limited to, the temporary closure of the factory and operations beginning in early February until late March 2020, limited support from the employees, delayed access to raw material supplies and inability to deliver products to customers on a timely basis, our business was negatively impacted. While the spread of the disease has gradually returned under control in China, COVID-19 could still adversely affect the business operation our Mainland China Subsidiaries and Hong Kong Subsidiaries and our financial results in the future. As a result, there is a possibility that the Company’s revenues and operating cash flows may be significantly lower than expected for fiscal year 2023.

We and our Subsidiaries may incur liability for unpaid taxes, including interest and penalties.

In the normal course of business, we and our Subsidiaries may be subject to challenges from various PRC taxing authorities regarding the amounts of taxes due. PRC taxing authorities may take the position that we or our Subsidiaries owe more taxes than it has paid. We recorded tax liabilities of$1.0 million, $1.6 million, and $4.4 million as of June 30, 2023, 2022, and 2021, respectively, for the possible underpayment of income and business taxes. It is possible that the tax liability of for past taxes may be higher than those amounts, if the PRC authorities determine that penalties are applicable or that the correct amount has not been paid. Although the Company’s management believes it may be able to negotiate with local PRC taxing authorities a reduction to any amounts that such authorities may believe are due and a reduction to any interest or penalties thereon, we have no guarantee that we will be able to negotiate such a reduction. To the extent we are able to negotiate such amounts, national-level taxing authorities may take the position that localities are without power to reduce such liabilities, and such PRC taxing authorities may attempt to collect unpaid taxes, interest and penalties in amounts greatly exceeding management’s estimates.

| 11 |

If our largest customers reduce their orders with us, such revenues would be very difficult to replace.

Although we have also sold our products through distributors and trading companies, some of our largest customers are Petco and Pet Value, which are by far the largest pet specialty chains in North America. Petco has around 1600 stores in the US and Pet Valu has around 600 stores in Canada. There is not another brick-and-mortar customer that presents the opportunity that these customers present to us. As a result, if we were to lose these accounts or if these customers purchased less of our products in the future, it would be difficult to replace those lost revenues.

Our smart products have only recently entered distribution.

While we are optimistic that our smart products such as collars, harnesses, feeders and robots will be important products for our company in the future, we only recently begun to sell them and thus do not know whether they will prove popular with consumers. We have exhibited these products at expos in multiple countries and have begun to receive orders, but our revenues for all smart products was approximately $7.4 million, 13.5 million, and $7.8 million, during the years ended June 30, 2023, 2022, and 2021, respectively. As a result, we do not have an accurate gauge of how well accepted they will be by consumers. If consumers do not appreciate our smart products, we may not sell enough products to grow our market share in this new industry.

Our smart products are not as well-known as those of our competitors.

There are a variety of competitors providing smart collars, smart feeders and smart treaters for dogs and cats that are more well-known than our products. We are aware of more than a dozen competitors to our smart products, some of which have been on the market for several years. Because smart collars are still a relatively new industry, we do not believe that there is a single leader. Nevertheless, we face competition from more well-known products like the Whistle GPS Pet Tracker and Tractive, as well as products from more well-established, better capitalized companies in the United States such as Garmin, which produces varieties of dog training and tracking devices. Similarly, companies such as PetSafe, Petzi, Petcube, Arf Pets, and Furbo market food and treat dispensers with functionalities that in some cases are similar to our products. If we are unable to achieve recognition for our technology or if consumers opt to use products from companies they recognize more than our company, our smart collar and harness products may not be well accepted.

Our smart collars and harnesses are currently between generations.

We debuted our C2 and H2 smart collars and harnesses in 2016. These products were designed to operate over 2G telephone technology. While this platform was sufficient to meet the needs of the products, 2G speeds lag far behind currently available 4G and now 5G technology. As a result, our C2 and H2 products have thus far obtained a very limited customer base. For this reason, we have been researching and developing our next generation of smart collars and harnesses to operate with today’s higher internet speeds in mind. We are close to the roll out of the C6 which relies on 4G network and C5 and C5 mini which rely on NB network. Before we are able to bring these products to market fully, we anticipate that our sales of smart collars and harnesses, along with subscriptions for ongoing cellular services for those products, will be nominal. If and when we are able to introduce our next generation of smart collars and harnesses, we are unable to predict the extent to which consumers will be drawn to such new products.

| 12 |

Our smart collars rely on third-party cellular telephone companies and application developers for functionality.

One of the features of our smart collars is the ability to communicate between the owner’s cell phone and the collar, even when the two are too far away to communicate directly. We achieve this by having a SIM card in the smart collar so that, so long as the collar has a cell phone signal, it will communicate with the telephone. We cooperate with cell phone companies in our target markets to provide cellular service to these SIM cards. If this cooperation were to end or if the cellular service we receive is not reliable or more expensive than we anticipate, the market for our products could be harmed.

In addition, the Dogness smartphone App on which our smart collars rely are still under development and test by a company, Dogness Network Technology Co., Ltd (“Dogness Network”), in which we have a minority interest. Our company owns 10% of Dogness Network. Dogness Network plans to derive its revenues from subscriptions for services provided through the Dogness smartphone App in the near future, and we will purchase such products from Dogness Network and resell to our customers. We may benefit only by virtue of our 10% interest in Dogness Network. If Dogness Network were to stop supporting the application or impair its functionality, our smart collars and harnesses could become unusable or have decreased value to end users.

To the extent we were unable to cooperate with such third parties in the future, we would need to locate and cooperate with other service providers, and we cannot guarantee that we would be able to do so under terms that are satisfactory to us, if at all.

Our software platform may not interface with applications consumers want to be integrated.

In the connected home, consumers are increasingly aware of the interconnection among applications and devices, such as speakers that can turn on lights or adjust the temperature. Some customers purchase products based on how they will interact with other services and products that the customers already use. If we are unable to anticipate and accommodate these desires, customers may choose other products that do interact with their preferred services. Although we may incorporate such functionality in future generations of our products, not all of our current products integrate into Apple’s, Google’s or Amazon’s smart home platforms. Our Dogness CAM feeder, App feeder, and App mini feeder work with Amazon Alexa.

We are also dependent on third party application stores that may prevent us from timely updating our current products or uploading new products. In addition, our products interoperate with servers, mobile devices and software applications predominantly through the use of protocols, many of which are created and maintained by third parties. We therefore depend on the interoperability of our products with such third-party services, mobile devices and mobile operating systems, as well as cloud-enabled hardware, software, networking, browsers, database technologies and protocols that we do not control. Any changes in such technologies that degrade the functionality of our products or give preferential treatment to competitive services could adversely affect adoption and usage of our platform. Also, we may not be successful in developing or maintaining relationships with key participants in the mobile industry or in developing products that operate effectively with a range of operating systems, networks, devices, browsers, protocols and standards. In addition, we may face different fraud, security and regulatory risks from transactions sent from mobile devices than we do from personal computers. If we are unable to effectively anticipate and manage these risks, or if it is difficult for our customers to access and use our platform, our business, results of operations and financial condition may be harmed.

| 13 |

Price increases in raw materials and sourced products could harm the Company’s financial results.

Our primary raw materials are plastic, leather, nylon, polyester, chemical fiber blended fabric, metal, GPPS and HIPS, most of which are extracted from crude oil. These raw materials are subject to price volatility and inflationary pressures. Our success is dependent, in part, on our continued ability to reduce our exposure to increases in those costs through a variety of programs, including sales price adjustments based on adjustments in such raw material costs, while maintaining and improving margins and market share. We also rely on third-party manufacturers as a source for a minor portion of components for our products. These manufacturers are also subject to price volatility and labor cost and other inflationary pressures, which may, in turn, result in an increase in the amount we pay for sourced products. Raw material and sourced product price increases may more than offset our productivity gains and price increases and may adversely impact our financial results.

Our plan to vertically integrate our production may not provide the benefits we foresee.

Over the last several years, we have increasingly produced our products in-house. We have made this strategic decision because of our belief that it will facilitate our control over the costs of components in our products. The price of components is extremely important where the per-unit sales price is as low as it is in our industry. Thus, we believe it is important to control costs as much as possible.

That being said, when we produce components in-house that we previously purchased from a third-party supplier, we may not benefit from the economies of scale that a dedicated third-party supplier could see. Moreover, we invest in infrastructure for such production, such as buying machines and leasing additional facility space; in the event new technology is developed to produce components of our products more cheaply than we can with our existing infrastructure, we could find that our operating results are negatively impacted, compared with what we would see if we were purchasing from third parties. In such case, our products could be more expensive than those of our competitors that purchase from third-party suppliers, which could make our products less attractive to customers.

Our reliance on third party logistics providers may put us at risk of service failures for our customers.

We rely on third parties to ship our products from China to our customers. We compete based on price, quality and reliability, so a failure to deliver our products on time to our large customers could harm our reputation. To the extent we are unable to meet their demand for products or do not deliver products on time, we stand a substantial risk of losing key accounts. Because we rely on third parties for logistics services, we may be unable to avoid supply chain failures, even if we are able to meet our manufacturing obligations to customers.

| 14 |

If we fail to protect our intellectual property rights, it could harm our business and competitive position.

We rely on a combination of patent, trademark, domain name and trade secret laws and non-disclosure agreements and other methods to protect our intellectual property rights. Our Mainland China Subsidiaries own 135 patents and 188 trademarks in China and 66 patents and 47 trademarks outside China, all of which have been properly registered with regulatory agencies such as the State Intellectual Property Office and Trademark Office of China’s State Administration for Industry and Commerce (“SAIC”). This intellectual property has allowed our products to earn market share in the pet products industry.

The process of seeking patent protection can be lengthy and expensive, our patent applications may fail to result in patents being issued, and our existing and future patents may be insufficient to provide us with meaningful protection or commercial advantage. Our patents and patent applications may also be challenged, invalidated or circumvented.

We also rely on trade secret rights to protect our business through non-disclosure provisions in employment agreements with employees. If our employees breach their non-disclosure obligations, we may not have adequate remedies in China, and our trade secrets may become known to our competitors.

In accordance with Chinese intellectual property laws and regulations, we will have to renew our trademarks once the terms expire. However, patents are not renewable. Some of our patents, particularly utility mode and design patents, have only 10 years of protection and will end in the near future. Once these patents expire, our prodCompany: Please update if the numbers have changeducts may lose some market share if they are copied by our competitors. Then, our business revenue might suffer some loss as well.

Implementation of PRC intellectual property-related laws has historically been lacking, primarily because of ambiguities in the PRC laws and enforcement difficulties. Accordingly, intellectual property rights and confidentiality protections in China may not be as effective as in the United States or other western countries. Furthermore, policing unauthorized use of proprietary technology is difficult and expensive, and we may need to resort to litigation to enforce or defend patents issued to us or to determine the enforceability, scope and validity of our proprietary rights or those of others. Such litigation and an adverse determination in any such litigation, if any, could result in substantial costs and diversion of resources and management attention, which could harm our business and competitive position.

Our Chinese patents and registered marks may not be protected outside of China due to territorial limitations on enforceability.

In general, patent and trademark rights have territorial limitations in law and are valid only within the countries in which they are registered.

At present, Chinese enterprises may register their trademarks overseas through two methods. One is to file an application for trademark registration in each single country or region in which protection is desired, while the other is to apply via the Madrid system for international trademark registration. By the second way, under the provisions of the Madrid Agreement concerning the International Registration of Marks (the “Madrid Agreement”) or the Protocol Relating to the Madrid Agreement concerning the International Registration of Marks (the “Madrid Protocol”), applicants may designate their marks in one or more member countries via the Madrid system for international registration.

As of the date of the filing, we have registered 188 trademarks in China. We have also registered our key trademarks in Japan, Australia, Korea, Hong Kong, Taiwan and the United States.

| 15 |