UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

[ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2018

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

Commission File Number: 001-35404

EMX ROYALTY

CORPORATION

(Formerly Eurasian Minerals Inc.)

(Exact name of Registrant as specified in its charter)

British Columbia, Canada

(Jurisdiction of

incorporation or organization)

Suite 501, 543 Granville Street, Vancouver, British

Columbia, Canada V6C 1X8

(Address of principal executive offices)

Christina Cepeliauskas, Chief Financial Officer

Telephone No.: 604-688-6390

Facsimile No.: 604-688-1157

Suite 501, 543 Granville Street, Vancouver, British Columbia,

Canada V6C 1X8

(Name, Telephone, Email and/or Facsimile

number and Address of Company Contact Person)

Securities to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name on each exchange on which registered |

| Common Shares, without par value | NYSE American LLC |

Securities to be registered pursuant to Section 12(g) of the

Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the Company’s classes of capital or common stock as of the close of the period covered by the annual report: 80,991,155

Indicate by check mark if the registrant is a well-known seasoned Company, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past ninety days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer", "accelerated filer,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [X] |

| Emerging growth company [ ] |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAA P [ ] | International Financial Reporting Standards as issued | Other [ ] | |

| by the International Accounting Standards Board [X] |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 [ ] Item 18 [ ]

If this is an annual report, indicate by check mark whether the

registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

Indicate by check mark whether the registrant has filed all

documents and reports required to be filed by Sections 12, 13 or 15(d) of the

Securities Exchange Act of 1934 subsequent to the distribution of securities

under a plan confirmed by a court.

Yes [ ] No [X]

2

EMX ROYALTY CORPORATION

TABLE OF CONTENTS

3

Glossary of Geological and Mining Terms

Certain terms used in this Form 20-F are defined as follows:

Alunite: a hydrated aluminium potassium, sulfate mineral [(KAl3(SO4)2(OH)6].

AMR: advance minimum royalty

Andesite: an extrusive igneous rock of intermediate composition with a fine grained to porphyritic texture.

Argillic Alteration: hydrothermal alteration of rock which introduces clay minerals including kaolinite, smectite and illite.

Assay: a quantitative chemical analysis of an ore, mineral or concentrate to determine the amount of specific elements.

Breccia: a coarse-grained clastic rock composed of broken rock fragments held together by a mineral cement or in a fine-grained matrix.

Carbonate: a sedimentary rock made mainly of calcium carbonate (CaCO3).

Dacite: an extrusive igneous rock with a fine grained to porphyritic texture and intermediate in composition between andesite and rhyolite.

Diorite: a grey to dark-grey intermediate intrusive igneous rock composed principally of plagioclase feldspar, biotite, hornblende, and/or pyroxene.

Dike: a tabular igneous intrusion that cuts across the country rock, generally vertical in nature.

Doré: a mixture of predominantly gold and silver produced by a mine, usually in a bar form, before separation and refining into gold and silver by a refinery.

Epithermal: said ofa hydrothermal mineral deposit formed within about 1 kilometer of the Earth’s surface and in the temperature range of 50oC to 200oC.

Feasibility Study: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable Modifying Factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate, at the time of reporting, that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a Pre-Feasibility Study.

Foliation: repetitive layering in metamorphic rocks.

Footwall: the underlying side of a fault, ore body, or mine working; particularly the wall rock beneath an inclined vein or fault.

Formation: a persistent body of igneous, sedimentary, or metamorphic rock, having easily recognizable boundaries that can be traced in the field without recourse to detailed paleontologic or petrologic analysis, and large enough to be represented on a geologic map as a practical or convenient unit for mapping and description.

Gneiss: a type of rock formed by high-grade regional metamorphic processes from pre-existing formations of igneous or sedimentary rocks.

Granodiorite: a group of plutonic rocks intermediate in composition between quartz diorite and quartz monzonite.

Greenfields: conceptual exploration; relying on the predictive power of ore genesis models to search for mineralization in relatively unexplored ground.

1

Hanging wall: the overlying side of an ore body, fault, or mine working, especially the wall rock above an inclined vein or fault.

Hornfels: a fine-grained rock composed of a mosaic of equidimensional grains without preferred orientation and typically formed by contact metamorphism.

Hydrothermal: of or pertaining to hot water, to the action of hot water, or to the products of this action, such as a mineral deposit precipitated from a hot aqueous solution, with or without demonstrable association with igneous processes.

Igneous rock: rock that is magmatic in origin.

Indicated mineral resource: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource and may only be converted to a Probable Mineral Reserve.

Inferred mineral resource: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

Intercalated: said of layered material that exists or is introduced between layers of a different character; especially said of relatively thin strata of one kind of material that alternates with thicker strata of some other kind, such as beds of shale intercalated in a body of sandstone.

Jasperoid: a dense chert-like siliceous rock, in which chalcedony or cryptocrystalline quartz has replaced the carbonate materials of limestone or dolomite.

Kriging: a weighted, moving-average interpolation method in which the set of weights assigned to samples minimizes the estimation variance, which is computed as a function of the variogram model and locations of the samples relative to each other, and to the point or block being estimated.

Leach: to dissolve minerals or metals out of ore with chemicals.

Limestone: a sedimentary rock consisting predominantly of calcium carbonate.

Lithocap: the shallow part of porphyry copper systems typically above the main Cu-Au/-Mo zone; upper alteration zone.

Measured mineral resource: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated Mineral Resource or an Inferred Mineral Resource. It may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve.

Meta: a prefix that, when used with the name of a sedimentary or igneous rock, indicates that the rock has been metamorphosed.

Metamorphic rock: rock which has been changed from igneous or sedimentary rock through heat and pressure into a new form of rock.

Mineral Reserve: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The reference point at which Mineral Reserves are defined, usually the point where the ore is delivered to the processing plant, must be stated. It is important that, in all situations where the reference point is different, such as for a saleable product, a clarifying statement is included to ensure that the reader is fully informed as to what is being reported. The public disclosure of a Mineral Reserve must be demonstrated by a Pre-Feasibility Study or Feasibility Study.

2

Mineral Resource: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

Modifying factors: is defined in the CIM Definition Standards (2014) as the considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

NSR: net smelter return.

Net smelter return royalty or NSR royalty: a type of royalty based on a percentage of the proceeds, net of smelting, refining and transportation costs and penalties, from the sale of metals extracted from concentrate and doré by the smelter or refinery.

NI 43-101: National Instrument 43-101 Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

Oxide: a compound of ore that has been subjected to weathering and alteration as a result of exposure to oxygen for a long period of time.

Pegmatite: a very coarse-grained igneous rock that has a grain size of 20 millimetres or more.

Phyllite: a regional metamorphic rock, intermediate in grade between slate and schist. Minute crystals of sericite and chlorite impart a silky sheen to the surfaces exposed by cleavage.

Plagioclase: a series of tectosilicate minerals within the feldspar family.

Plutonic: intrusive igneous rock that is crystallized from magma slowly cooling below the surface of the Earth.

Porphyry: igneous rock consisting of large-grained crystals dispersed in a fine-grained matrix or groundmass.

Pre-Feasibility Study: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the Modifying Factors and the evaluation of any other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the Mineral Resource may be converted to a Mineral Reserve at the time of reporting. A Pre-Feasibility Study is at a lower confidence level than a Feasibility Study.

Preliminary Economic Assessment: is defined in NI 43-101 and NI 43-101CP as a study, other than a pre-feasibility or feasibility study that includes an economic analysis of the potential viability of mineral resources. The term preliminary economic assessment can include a study commonly referred to as a scoping study. A preliminary economic assessment might be based on measured, indicated, or inferred mineral resources, or a combination of any of these. These types of economic analyses include disclosure of forecast mine production rates that might contain capital costs to develop and sustain the mining operation, operating costs, and projected cash flows.

Probable mineral reserve: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as the economically mineable part of an Indicated, and in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve. The Qualified Person(s) may elect to convert Measured Mineral Resources to Probable Mineral Reserves if the confidence in the Modifying Factors is lower than that applied to a Proven Mineral Reserve.

3

Proven mineral reserve: is defined in the CIM Definition Standards (2014) as referenced by NI 43-101 as the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the Modifying Factors. Application of the Proven Mineral Reserve category implies that the Qualified Person has the highest degree of confidence in the estimate with the consequent expectation in the minds of the readers of the report. The term should be restricted to that part of the deposit where production planning is taking place and for which any variation in the estimate would not significantly affect the potential economic viability of the deposit. Proven Mineral Reserve estimates must be demonstrated to be economic, at the time of reporting, by at least a Pre-Feasibility Study.

Pyroclastic: pertaining to clastic rock material formed by volcanic explosion or aerial expulsion from a volcanic vent; also, pertaining to rock texture of explosive origin.

Qualified Person: is defined in NI 43-101 as an individual who (a) is an engineer or geoscientist with a university degree, or equivalent accreditation, in an area of geoscience, or engineering, relating to mineral exploration or mining; (b) has at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these, that is relevant to his or her professional degree or area of practice; (c) has experience relevant to the subject matter of the mineral project and the technical report; (d) is in good standing with a professional association; and (e) in the case of a professional association in a foreign jurisdiction, has a membership designation that (i) requires attainment of a position of responsibility in their profession that requires the exercise of independent judgment; and (ii) requires A. a favourable confidential peer evaluation of the individual’s character, professional judgement, experience, and ethical fitness; or B. a recommendation for membership by at least two peers, and demonstrated prominence or expertise in the field of mineral exploration or mining;

Run-of-mine: ore in its natural state as it is removed from the mine that has not been subjected to additional size reduction.

Schist: a strongly foliated crystalline rock, which readily splits into sheets or slabs as a result of the planar alignment of the constituent crystals. The constituent minerals are commonly specified (e.g. “quartz-muscovite-chlorite schist”).

Shear zone: a tabular zone of rock that has been crushed and brecciated by parallel fractures due to “shearing” along a fault or zone of weakness. These can be mineralized with ore-forming solutions.

Silicification/Silicified: the introduction of, or replacement by, silica, generally resulting in the formation of fine-grained quartz, chalcedony, or opal, which may fill pores and replace existing minerals.

Skarn: metamorphic zone developed in the contact area around igneous rock intrusions when carbonate sedimentary rocks are invaded by large amounts of silicon, aluminum, iron, and magnesium.

Spectrography: the process of using a spectrograph to map or photograph a spectrum.

Stockwork: a complex, cross -cutting system of structurally controlled or randomly oriented veins.

Strata: layers of sedimentary rock with internally consistent characteristics that distinguish them from other layers.

Strike: the direction, or course or bearing of a vein or rock formation measured on a level surface.

Stratabound: confined to a particular stratigraphic layer or unit.

Stratiform: occurring as or arranged in strata.

Strip (or stripping) ratio: the tonnage or volume of waste material that must be removed to allow the mining of one tonne of ore in an open pit.

Sulfides or sulphides: compounds of sulfur (or sulphur) with other metallic elements.

Tailing: material rejected from a mill after the recoverable valuable minerals have been extracted.

Terrane: a rock formation or assemblage of rock formations that share a common geologic history.

Tuff: a general term for consolidated pyroclastic rocks.

Vein: sheet-like body of minerals formed by fracture filling or replacement of host rock.

4

Vuggy: containing small cavities in a rock or vein, often with a mineral lining of different composition from that of the surrounding rock.

5

| Linear Measurements | ||

| 1 inch | = | 2.54 centimeters |

| 1 foot | = | 0.3048 meter |

| 1 yard | = | 0.9144 meter |

| 1 mile | = | 1.609 kilometers |

| Area Measurements | ||

| 1 acre | = | 0.4047 hectare |

| 1 hectare | = | 2.471 acres |

| 1 square mile | = | 640 acres or 259 hectares or 2.59 square kilometers |

| Units of Weight | ||

| 1 short ton | = | 2000 pounds or 0.893 long ton |

| 1 long ton | = | 2240 pounds or 1.12 short tons |

| 1 metric tonne | = | 2204.62 pounds or 1.1023 short tons |

| 1 pound (16 oz.) | = | 0.454 kilograms or 14.5833 troy ounces |

| 1 troy oz. | = | 31.1035 grams |

| 1 troy oz. per short ton | = | 34.2857 grams per metric tonne |

| Analytical | percent | grams per metric tonne | troy oz per short ton |

| 1% | 1% | 10,000 | 291.667 |

| 1 gram/tonne | 0.0001% | 1 | 0.029167 |

| 1 troy oz./short ton | 0.003429% | 34.2857 | 1 |

| 10 ppb | nil | 0.01 | 0.00029 |

| 100 ppm | 0.01 | 100 | 2.917 |

| Temperature Conversion Formulas | ||

| Degrees Fahrenheit | = | (°C x 1.8) + 32 |

| Degrees Celsius | = | (°F - 32) x 0.556 |

6

Frequently Used Abbreviations and Symbols

| AA | atomic absorption spectrometry |

| Ag | silver |

| As | arsenic |

| Au | gold |

| °C | degrees Celsius (centigrade) |

| CIM | Canadian Institute of Mining, Metallurgy and Petroleum |

| cm | centimeter |

| C.P.G. | Certified Professional Geologist |

| CSAMT | Controlled source audio-frequency magnetotellurics |

| Cu | copper |

| ESIA | Environmental & Social Impact Assessment |

| F | fluorine |

| °F | degrees Fahrenheit |

| g | gram(s) |

| g/t | grams per tonne |

| Hg | mercury |

| HSE | high sulphidation epithermal |

| ICP AES | inductively coupled plasma atomic emission spectroscopy |

| ICP MS | inductively coupled plasma mass spectroscopy |

| ICP MS/AAS | inductively coupled plasma mass spectroscopy/atomic absorption spectroscopy |

| IOCG | iron-oxide-copper-gold |

| IP | Induced polarization |

| JORC | Joint Ore Reserves Committee |

| JV | joint venture |

| kg | kilogram |

| km | kilometer |

| m | meter(s) |

| Ma | million years ago |

| Mn | manganese |

| Mo | molybdenum |

| n | number or count |

| oz | troy ounce |

| opt | ounce per short ton |

| oz/ton | ounce per short ton |

| oz/tonne | ounce per metric tonne |

| Pb | lead |

| PEA | Preliminary Economic Assessment |

| PGE | platinum group element |

| ppb | parts per billion |

| ppm | parts per million |

| QA | quality assurance |

| QC | quality control |

| QP | Qualified Person |

| sq | square |

7

Frequently Used Abbreviations and Symbols

| Sb | antimony |

| VMS | volcanogenic massive sulfide |

| Zn | zinc |

8

INTRODUCTION

EMX Royalty Corporation (the “Company” or “EMX”) was incorporated under the laws of the Yukon Territory of Canada on August 21, 2001 as 33544 Yukon Inc. and, on October 10, 2001, changed its name to Southern European Exploration Ltd. On November 24, 2003, the Company completed the reverse take-over of Marchwell Capital Corp., a TSX Venture Exchange (“TSX-V”) listed company incorporated in Alberta on May 13, 1996 and which subsequently changed its name to Eurasian Minerals Inc. On September 21, 2004, EMX continued into British Columbia from Alberta under the Business Corporations Act. On July 19, 2017, EMX changed its name to EMX Royalty Corporation to better reflect the nature of its business.

EMX’s head office is located at Suite 501 – 543 Granville Street, Vancouver, British Columbia V6C 1X8, Canada, and its registered and records office is located at Northwest Law Group, Suite 704 – 595 Howe Street, Vancouver, British Columbia V6C 2T5, Canada.

EMX is a reporting company under the securities legislation of British Columbia and Alberta and is listed on the TSX-V, as a Tier 1 Company, and the NYSE American LLC (“NYSE American”). EMX’s common shares without par value (“Common Shares”) are traded on the TSX-V and the NYSE American under the symbol “EMX”.

BUSINESS OF EMX ROYALTY CORPORATION

EMX is principally in the business of exploring for, and generating royalties from minerals properties, as well as identifying mineral property royalty opportunities for purchase. Under the royalty generation business model, the Company acquires and advances early-stage mineral exploration projects and then sells the projects to, other parties in consideration of a retained royalty interest, as well as annual advance royalty and other pre-production cash or share payments and work commitments. Through its various agreements, EMX may also provide technical and commercial assistance to such companies as the projects advance. By selling interests in its projects for a royalty interest, EMX:

| (a) |

reduces its exposure to the costs and risks associated with mineral exploration and project development, | |

| (b) |

receives near term cash flow from scheduled pre-production and milestone based bonus payments, | |

| (c) |

maintains the opportunity to participate in exploration upside, and | |

| (d) |

develops a pipeline for potential production royalty payments and associated greenfields discoveries in the future. |

This approach helps preserve the Company’s treasury, which can be utilized for further project acquisitions and other business initiatives.

Strategic investments are an important complement to the Company’s royalty acquisition and royalty generation initiatives. These investments are made in under-valued exploration companies identified by the Company. EMX helps to develop the value of these assets, with exit strategies that can include royalty positions or equity sales, or a combination of both.

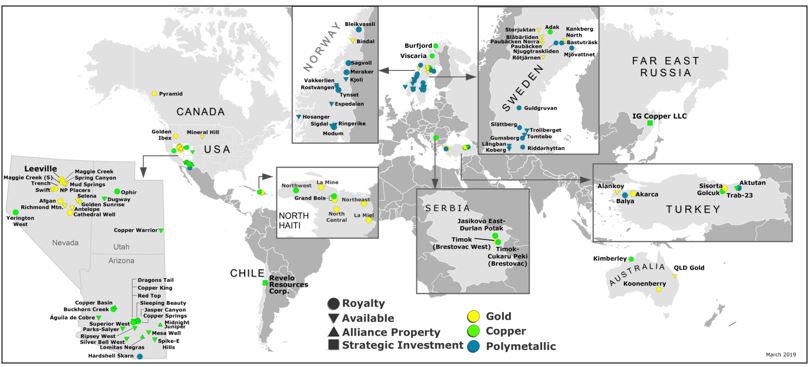

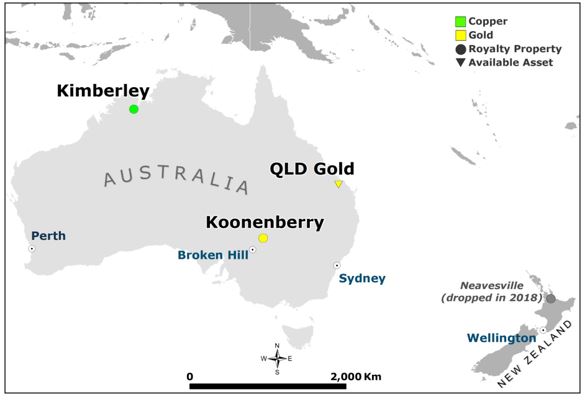

EMX started receiving royalty income as of August 17, 2012 when it acquired Bullion Monarch Mining, Inc. (“Bullion Monarch” or “BULM”). The Company’s royalty and royalty generation portfolio mainly consists of properties in North America, Turkey, Europe, Haiti, and Australia.

FINANCIAL AND OTHER INFORMATION

In this Annual Report, unless otherwise specified, all dollar amounts are expressed in Canadian Dollars (“C$” or “$”). References to “US$” are to United States dollars. The Government of Canada permits a floating exchange rate to determine the value of the Canadian dollar against the U.S. dollar.

FORWARD-LOOKING STATEMENTS

The Company is a “foreign private issuer” as defined in Rule 3b-4 under the Exchange Act and Rule 405 under the Securities Act of 1933, as amended (the “Securities Act”). Equity securities of the Company are accordingly exempt from Sections 14(a), 14(b), 14(c), 14(f) and 16 of the Exchange Act pursuant to Rule 3a12-3 thereunder.

9

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report, including the documents incorporated by reference herein, may contain forward-looking statements. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, operating costs, cash flow estimates, production estimates and similar statements relating to the economic viability of a project, timelines, strategic plans, completion of transactions, market prices for metals or other statements that are not statements of fact. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. Statements concerning mineral resource estimates may also be deemed to constitute “forward-looking statements” to the extent that they involve estimates of the mineralization that will be encountered if the property is developed.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects”, “anticipates”, “believes”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “potential”, “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are based on a number of material assumptions, including those listed below, which could prove to be significantly incorrect:

- the Company’s ability to achieve production at any of its mineral properties;

- estimated capital costs, operating costs, production and economic returns;

- estimated metal pricing, metallurgy, mineability, marketability and operating and capital costs, together with other assumptions underlying the Company’s resource and reserve estimates;

- the Company’s expected ability to develop adequate infrastructure at a reasonable cost;

- assumptions that all necessary permits and governmental approvals will be obtained;

- assumptions made in the interpretation of drill results, the geology, grade and continuity of the Company’s mineral deposits;

- the Company’s expectations regarding demand for equipment, skilled labor and services needed for exploration and development of mineral properties; and

- the Company’s activities will not be adversely disrupted or impeded by development, operating or regulatory risks.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those reflected in the forward-looking statements, including, without limitation:

- uncertainty of whether there will ever be production at the Company’s mineral exploration and development properties;

- uncertainty of estimates of capital costs, operating costs, production and economic returns;

- uncertainties relating to the assumptions underlying the Company’s resource and reserve estimates, such as metal pricing, metallurgy, mineability, marketability and operating and capital costs;

- risks related to the Company’s ability to commence production and generate material revenues or obtain adequate financing for its planned exploration and development activities;

- risks related to the Company’s ability to finance the development of its mineral properties through external financing, joint ventures or other strategic alliances, the sale of property interests or otherwise;

- risks related to the third parties on which the Company depends for its exploration and development activities;

- dependence on cooperation of joint venture partners in exploration and development of properties;

- credit, liquidity, interest rate and currency risks;

- risks related to market events and general economic conditions;

- uncertainty related to inferred mineral resources;

- risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of the Company’s mineral deposits;

- risks related to lack of adequate infrastructure;

- mining and development risks, including risks related to infrastructure, accidents, equipment breakdowns, labor disputes or other unanticipated difficulties with or interruptions in development, construction or production;

- the risk that permits and governmental approvals necessary to develop and operate mines on the Company’s properties will not be available on a timely basis or at all;

- commodity price fluctuations;

10

- risks related to governmental regulation and permits, including environmental regulation;

- risks related to the need for reclamation activities on the Company’s properties and uncertainty of cost estimates related thereto;

- uncertainty related to title to the Company’s mineral properties;

- uncertainty as to the outcome of potential litigation;

- risks related to increases in demand for equipment, skilled labor and services needed for exploration and development of mineral properties, and related cost increases;

- increased competition in the mining industry;

- the Company’s need to attract and retain qualified management and technical personnel;

- risks related to hedging arrangements or the lack thereof;

- uncertainty as to the Company’s ability to acquire additional commercially mineable mineral rights;

- risks related to the integration of potential new acquisitions into the Company’s existing operations;

- risks related to unknown liabilities in connection with acquisitions;

- risks related to conflicts of interest of some of the directors of the Company;

- risks related to global climate change;

- risks related to adverse publicity from non-governmental organizations;

- risks related to political uncertainty or instability in countries where the Company’s mineral properties are located;

- uncertainty as to the Company’s passive foreign investment company (“PFIC”) status;

- uncertainty as to the Company’s status as a “foreign private issuer” and “emerging growth company” in future years;

- uncertainty as to the Company’s ability to maintain the adequacy of internal control over financial reporting; and

- risks related to regulatory and legal compliance and increased costs relating thereto.

This list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to under the heading “Key Information” (as defined below), which is incorporated by reference herein.

The Company’s forward-looking statements are based on the beliefs, expectations and opinions of management on the date of this Annual Report, and the Company does not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change, except as required by law. For the reasons set forth above, investors should not place undue reliance on forward-looking statements.

11

CAUTIONARY NOTE TO UNITED STATES INVESTORS REGARDING RESERVE AND RESOURCE INFORMATION

Unless otherwise indicated, all resource estimates, and any future reserve estimates, included or incorporated by reference in this annual report or Form 10-K have been, and will be, prepared in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum Definition Standards for Mineral Resources and Mineral Reserves (“CIM Definition Standards”). NI 43-101 is a rule developed by the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects.

Canadian standards, including NI 43-101, differ significantly from the requirements of the SEC, and reserve and resource information contained or incorporated by reference into this annual report on Form 20-F may not be comparable to similar information disclosed by U.S. companies. In particular, and without limiting the generality of the foregoing, the term “resource” does not equate to the term “reserves”. Under SEC Industry Guide 7, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. SEC Industry Guide 7 does not define and the SEC’s disclosure standards normally do not permit the inclusion of information concerning “measured mineral resources”, “indicated mineral resources” or “inferred mineral resources” or other descriptions of the amount of mineralization in mineral deposits that do not constitute “reserves” by U.S. standards in documents filed with the SEC. U.S. investors should also understand that “inferred mineral resources” have a great amount of uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resourceand must not be converted to a mineral reserve. It is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral Resources with continued exploration. Under Canadian rules, estimated “inferred mineral resources” may not form the basis of feasibility or pre-feasibility studies except in rare cases. Investors are cautioned not to assume that all or any part of an “inferred mineral resource” exists or is economically or legally mineable. Disclosure of “contained ounces” or "contained pounds" in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in-place tonnage and grade without reference to unit measures. The requirements of NI 43-101 for identification of “reserves” are also not the same as those of the SEC, and any reserves reported by us in the future in compliance with NI 43-101 may not qualify as “reserves” under SEC standards. Accordingly, information concerning mineral deposits set forth herein may not be comparable to information made public by companies that report in accordance with United States standards.

12

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE Not applicable.

ITEM 3. KEY INFORMATION

3.A.1. and 3.A.2 Selected Financial Data

The selected financial data of the Company for the fiscal years ending December 31, 2018, 2017, 2016, 2015, and 2014 was derived from the financial statements of the Company that have been audited by Davidson and Company LLP, Independent Registered Public Accountants, as indicated in their audit report, which are included elsewhere in this Annual Report.

The Company has not declared any dividends since incorporation and does not anticipate that it will do so in the foreseeable future. The present policy of the Company is to retain all available funds for use in its operations and the expansion of its business.

Table No. 3 is derived from the financial statements of the Company, which have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board.

Table No. 3

Selected Financial Data

(C$)

3.A.3. Exchange Rates

In this Annual Report, unless otherwise specified, all dollar amounts are expressed in Canadian Dollars (“C$”). The Government of Canada permits a floating exchange rate to determine the value of the Canadian Dollar against the U.S. Dollar (“US$”).

Table No. 4 sets forth the exchange rates for the Canadian Dollar at the end of five most recent fiscal years ended December 31, the average rates for the period, and the range of high and low rates for the period. The data for each month during the most recent six months is also provided.

13

For purposes of this table, the exchange rate means the Bank of Canada noon rate.

3.B. Capitalization and Indebtedness

Not applicable

3.C. Reasons For The Offer And Use Of Proceeds

Not applicable

3.D. Risk Factors

Investment in the Common Shares involves a significant degree of risk and should be considered speculative due to the nature of the Company’s business and the present stage of its development. Prospective investors should carefully review the following factors together with other information contained in this Annual Report before making an investment decision.

Mineral Property Exploration Risks

The business of mineral exploration and extraction involves a high degree of risk. Few properties that are explored ultimately become producing mines. The Company mitigates this risk by cost-sharing with exploration partners and by continuously evaluating the economic potential of each mineral property at every stage of its life cycle. At present, none of the Company’s properties has a known commercial ore deposit. The main operating risks include ensuring ownership of and access to mineral properties, which the Company mitigates by confirmation that licenses, claims and leases are in good standing and by obtaining permits for drilling and other exploration activities.

The market prices for precious and base metals can be volatile and there is no assurance that a profitable market will exist for a production decision to be made or for the ultimate sale of the metals even if commercial quantities of precious and other metals are discovered.

Revenue and Royalty Risks

The Company cannot predict future revenues or operating results of the area of mining activity. Management expects future revenues from the Carlin Trend Royalty Claim Block, including the Leeville royalty property in Nevada, to fluctuate depending on the level and location of future production and the price of gold. Specifically, there is a risk that the operator of the property, Newmont Mining Corporation (“Newmont”), will cease to operate in the Company’s area of interest, therefore there can be no assurance that ongoing royalty payments will materialize or be received by EMX.

14

Financing and Share Price Fluctuation Risks

EMX has limited financial resources and has no assurance that additional funding will be available for further exploration and development of its projects. Further exploration and development of one or more of the Company’s projects may be dependent upon the Company’s ability to obtain financing through equity or debt financing or other means. Failure to obtain this financing could result in delay or indefinite postponement of further exploration and development of its projects which could result in the loss of one or more of its properties.

The securities markets can experience a high degree of price and volume volatility, and the market price of securities of many companies, particularly those considered to be development stage companies, such as EMX, may experience wide fluctuations in share prices which may not necessarily be related to their operating performance, underlying asset values or prospects. There can be no assurance that share price fluctuations will not occur in the future, and if they do occur, the severity of the impact on EMX’s ability to raise additional funds through equity issues.

Foreign Countries and Political Risks

The Company operates and owns royalty interests in countries with varied political and economic environments. As such, it is subject to certain risks, including currency fluctuations and possible political or economic instability which may result in the impairment or loss of mineral concessions or other mineral rights, opposition from environmental or other nongovernmental organizations, and mineral exploration and mining activities may be affected in varying degrees by political stability and government regulations relating to the mineral exploration and mining industry. Any changes in regulations or shifts in political attitudes are beyond the control of the Company and may adversely affect its business. Exploration and development may be affected in varying degrees by government regulations with respect to restrictions on future exploitation and production, price controls, export controls, foreign exchange controls, income taxes, expropriation of property, environmental legislation and mine and site safety.

Notwithstanding any progress in restructuring political institutions or economic conditions, the present administration, or successor governments, of some countries in which EMX operates or owns royalty interests may not be able to sustain any progress. If any negative changes occur in the political or economic environment of these countries, it may have an adverse effect on the Company’s operations in those countries. The Company does not carry political risk insurance.

Competition

The Company competes with many companies that have substantially greater financial and technical resources than it in the acquisition of mineral properties and royalty interests and development of projects as well as for the recruitment and retention of qualified employees.

We do not intend to pay any cash dividends in the foreseeable future.

The Company has not declared or paid any dividends on our Common Shares. Our current business plan requires that for the foreseeable future, any future earnings be reinvested to finance the growth and development of our business. We do not intend to pay cash dividends on the Common Shares in the foreseeable future. We will not declare or pay any dividends until such time as our cash flow exceeds our capital requirements and will depend upon, among other things, conditions then existing including earnings, financial condition, restrictions in financing arrangements, business opportunities and conditions and other factors, or our Board determines that our shareholders could make better use of the cash.

15

No Assurance of Titles or Borders

The acquisition of the right to exploit mineral properties is a very detailed and time consuming process. There can be no guarantee that the Company has acquired title to any such surface or mineral rights or that such rights will be obtained in the future. To the extent they are obtained, titles to the Company’s surface or mineral properties may be challenged or impugned and title insurance is generally not available. The Company’s surface or mineral properties may be subject to prior unregistered agreements, transfers or claims and title may be affected by, among other things, undetected defects. Such third party claims could have a material adverse impact on the Company’s operations and ownership of royalty interests.

Unknown Defects or Impairments in Our Royalty Interests

Unknown defects in or disputes relating to the royalty interests we hold or acquire may prevent us from realizing the anticipated benefits from our royalty interests, and could have a material adverse effect on our business, results of operations, cash flows and financial condition. It is also possible that material changes could occur that may adversely affect management’s estimate of the carrying value of our royalty interests and could result in impairment charges. While we seek to confirm the existence, validity, enforceability, terms and geographic extent of the royalty interests we acquire, there can be no assurance that disputes over these and other matters will not arise. Confirming these matters, as well as the title to mining property on which we hold or seek to acquire a royalty interest, is a complex matter, and is subject to the application of the laws of each jurisdiction to the particular circumstances of each parcel of mining property and to the documents reflecting the royalty or stream interest. Similarly, royalty interests in many jurisdictions are contractual in nature, rather than interests in land, and therefore may be subject to change of control, bankruptcy or the insolvency of operators. We often do not have the protection of security interests over property that we could liquidate to recover all or part of our investment in a royalty interest. Even if we retain our royalty interests in a mining project after any change of control, bankruptcy or insolvency of the operator, the project may end up under the control of a new operator, who may or may not operate the project in a similar manner to the current operator, which may negatively impact us.

Operators’ Interpretation of Our Royalty Interests; Unfulfilled Contractual Obligations

Our royalty interests generally are subject to uncertainties and complexities arising from the application of contract and property laws in the jurisdictions where the mining projects are located. Operators and other parties to the agreements governing our royalty interests may interpret our interests in a manner adverse to us or otherwise may not abide by their contractual obligations, and we could be forced to take legal action to enforce our contractual rights. We may or may not be successful in enforcing our contractual rights, and our revenues relating to any challenged royalty interests may be delayed, curtailed or eliminated during the pendency of any such dispute or in the event our position is not upheld, which could have a material adverse effect on our business, results of operations, cash flows and financial condition. Disputes could arise challenging, among other things:

- the existence or geographic extent of the royalty interest;

- methods for calculating the royalty interest, including whether certain operator costs may properly be deducted from gross proceeds when calculating royalties determined on a net basis;

- third party claims to the same royalty interest or to the property on which we have a royalty interest;

- various rights of the operator or third parties in or to the royalty interest;

- production and other thresholds and caps applicable to payments of royalty interests;

- the obligation of an operator to make payments on royalty interests; and

- various defects or ambiguities in the agreement governing a royalty interest.

Limited Access to Data and Disclosure for Royalty Interests

The Company has varying access to data on the operations on the properties covered by its royalty interests, making it difficult in some instances to accurately assess the value of the royalty interests. In addition, some royalty interests may be subject to confidentiality agreements that govern the disclosure of information about the royalties, and as a result the Company may not be in a position to publicly disclose non-public information with respect to certain royalties. The limited access to data and disclosure may result in a material and adverse effect on the Company’s profitability, results of operation and financial condition. The Company mitigates this risk by building relationships, and where feasible, contractual disclosure obligations, with operators and counterparties concerning information sharing.

16

Currency Risks

Certain of the Company’s royalty interests are denominated in US dollars, and therefore expose the Company to foreign currency fluctuations. In addition, the Company’s equity financings are sourced in Canadian dollars but much of its expenditures are in local currencies or U.S. dollars. At this time, the Company has no currency hedges in place. Therefore, currency fluctuation could have an adverse impact on the value of royalty payments and a weakening of the Canadian dollar against the U.S. dollar or local currencies could have an adverse impact on the amount of exploration funds available and work conducted.

Exploration Funding Risk

The Company’s exploration strategy is to seek exploration partners through options to fund exploration and project development. The main risk of this strategy is that the funding parties may not be able to raise sufficient capital in order to satisfy exploration and other expenditure terms in a particular agreement. As a result, exploration and development of one or more of the Company’s property interests may be delayed depending on whether EMX can find another party or has enough capital resources to fund the exploration and development on its own.

Insured and Uninsured Risks

In the course of exploration, development and production of mineral properties, the Company is subject to a number of risks and hazards in general, including adverse environmental conditions, operational accidents, labor disputes, unusual or unexpected geological conditions, changes in the regulatory environment and natural phenomena such as inclement weather conditions, floods, and earthquakes. Such occurrences could result in the damage to the Company’s property or facilities and equipment, personal injury or death, environmental damage to properties of the Company or others, delays, monetary losses and possible legal liability.

Although the Company may maintain insurance to protect against certain risks in such amounts as it considers reasonable, its insurance may not cover all the potential risks associated with its operations. The Company may also be unable to maintain insurance to cover these risks at economically feasible premiums or for other reasons. Should such liabilities arise, they could reduce or eliminate future profitability and result in increased costs, have a material adverse effect on the Company’s results and a decline in the value of the securities of the Company.

Some work is carried out through independent consultants and the Company requires all consultants to carry their own insurance to cover any potential liabilities as a result of their work on a project.

Environmental Risks and Hazards

The activities of the Company are subject to environmental regulations issued and enforced by government agencies. Environmental legislation is evolving in a manner that will require stricter standards and enforcement and involve increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects, and a heightened degree of responsibility for companies and their officers, directors and employees. There can be no assurance that future changes in environmental regulation, if any, will not adversely affect the Company’s operations. Environmental hazards may exist on properties in which the Company holds interests which are unknown to the Company at present.

We or the mining properties in which we have an interest are subject to substantial government regulation in the United States and in the other jurisdictions in which we operate. Changes to regulation or more stringent implementation could have a material adverse effect on our results of operations and financial condition.

Mining and exploration activities are subject to various laws and regulations relating to the protection of the environment, such as the federal Clean Water Act and the Nevada Water Pollution Control Law. Although we currently believe that we are in compliance with existing environmental and mining laws and regulations and that our proposed exploration programs will also meet those standards, no assurance can be given that we will remain in compliance with applicable regulations or that new rules and regulations will not be enacted or that existing rules and regulations will not be applied in a manner that could limit or curtail production or development of our properties.

Reform of the General Mining Law could adversely impact our results of operations.

A majority of our mining properties in the United States consist of unpatented mining claims on federal lands. Legislation has been introduced regularly in the U.S. Congress over the last decade to change the General Mining Law of 1872, as amended (the "Mining Law"), under which we hold these unpatented mining claims. It is possible that the Mining Law may be amended or replaced by less favorable legislation in the future. Previously proposed legislation contained a production royalty obligation, new environmental standards and conditions, additional reclamation requirements and extensive new procedural steps which would likely result in delays in permitting. The ultimate content of future proposed legislation, if enacted, is uncertain. At present, there is no royalty payable to the United States on production from unpatented mining claims, although legislative attempts to impose a royalty have occurred in recent years. Amendments to current laws and regulations governing our operations and activities of exploration, development mining and milling or more stringent implementation thereof could have a material adverse effect on our business, financial condition and results of operations and cause increases in exploration expenses, capital expenditures or production costs or reduction in levels of production or require delays or abandonment in the development of new mining properties. If a royalty on unpatented mining claims were imposed, the profitability of our U.S. unpatented mining claims could be materially adversely affected.

17

Any such reform of the Mining Law could increase the costs of mining activities on unpatented mining claims, or could materially impair our ability to develop or continue operations which derive ore from federal lands, and as a result, could have an adverse effect on us and our results of operations.

Mineral reserves are only estimates which may be unreliable.

Although mineralization may not be classified as a “reserve” unless the mineralization can be economically and legally extracted or produced at the time the “reserve” determination is made, “mineral reserves” are estimates only, and no assurance can be given that the anticipated tonnages and grades will be achieved, that the indicated level of recovery will be realized or that mineral reserves can be mined or processed profitably. Mineral reserve and mineral resource estimates may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing and other relevant issues. There are numerous uncertainties inherent in estimating mineral reserves and mineral resources, including many factors beyond our control. Such estimation is a subjective process, and the accuracy of any mineral reserve or mineral resource estimate is a function of the quantity and quality of available data, the nature of the mineralized body and of the assumptions made and judgments used in engineering and geological interpretation. These estimates may require adjustments or downward revisions based upon further exploration or development work or actual production experience.

Fluctuations in metal prices, results of drilling, metallurgical testing and production, the evaluation of mine plans after the date of any estimate, permitting requirements or unforeseen technical or operational difficulties may require revision of mineral reserve estimates. Prolonged declines in the market price of precious and base metals may render mineral reserves containing relatively lower grades of mineralization uneconomical to recover and could materially reduce our mineral reserves. Should reductions in mineral reserves occur, we may be required to take a material write-down of our investment in mining properties, reduce the carrying value of one or more of our assets or delay or discontinue production or the development of new projects, resulting in increased net losses and reduced cash flow. Mineral reserves should not be interpreted as assurances of mine life or of the profitability of current or future operations. There is a degree of uncertainty attributable to the calculation and estimation of mineral reserves and corresponding grades being mined and, as a result, the volume and grade of mineral reserves mined and processed and recovery rates may not be the same as currently anticipated. Any material reductions in estimates of mineral reserves, or of our ability to extract these mineral reserves, could have a material adverse effect on our results of operations and financial condition.

Fluctuating Metal Prices

Factors beyond the control of the Company have a direct effect on global metal prices, which have fluctuated widely, particularly in recent years, and there is no assurance that a profitable market will exist for a production decision to be made or for the ultimate sale of the metals even if commercial quantities of precious and other metals are discovered on any of the Company’s properties. Consequently, the economic viability of any of the Company’s exploration projects and its ability to finance the development of its projects cannot be accurately predicted and may be adversely affected by fluctuations in metal prices.

Extensive Governmental Regulation and Permitting Requirements Risks

Exploration, development and mining of minerals are subject to extensive laws and regulations at various governmental levels governing the acquisition of the mining interests, prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. In addition, the current and future operations of EMX, from exploration through development activities and production, require permits, licenses and approvals from some of these governmental authorities. EMX has obtained all government licenses, permits and approvals necessary for the operation of its business to date. However, additional licenses, permits and approvals may be required. The failure to obtain any licenses, permits or approvals that may be required or the revocation of existing ones would have a material and adverse effect on EMX, its business and results of operations.

18

Failure to comply with applicable laws, regulations and permits may result in enforcement actions thereunder, including orders issued by regulatory or judicial authorities requiring the Company’s operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or remedial actions. EMX may be required to compensate those suffering loss or damage by reason of its mineral exploration activities and may have civil or criminal fines or penalties imposed for violations of such laws, regulations and permits. Any such events could have a material and adverse effect on EMX and its business and could result in EMX not meeting its business objectives.

In addition, we are required to expend significant resources to comply with numerous corporate governance and disclosure regulations and requirements adopted by U.S. federal and state and Canadian federal and provincial governments, as well as the TSX and NYSE American. These additional compliance costs and related diversion of the attention of management and key personnel could have a material adverse effect on our business, financial condition and results of operations.

Key Personnel Risk

The Company’s success is dependent upon the performance of key personnel working in management and administrative capacities or as consultants. The loss of the services of senior management or key personnel could have a material and adverse effect on the Company, its business and results of operations. The Company does not carry “key personnel” insurance.

Conflicts of Interest

In accordance with the laws of British Columbia and the United States, the directors and officers of a Company are required to act honestly, in good faith and in the best interests of the Company. EMX’s directors and officers may serve as directors or officers of other companies or have significant shareholdings in other resource companies and, to the extent that such other companies may participate in ventures in which the Company may participate, such directors and officers may have a conflict of interest in negotiating and concluding terms respecting the extent of such participation. If such a conflict of interest arises at a meeting of the Company’s directors, a director with such a conflict will abstain from voting for or against the approval of such participation or such terms.

Passive Foreign Investment Company

U.S. investors in common shares should be aware that based on current business plans and financial expectations, EMX currently expects that it will be classified as a passive foreign investment company (“PFIC”) for the tax year ending December 31, 2018 and expects to be a PFIC in future tax years. If EMX is a PFIC for any tax year during a U.S. shareholder’s holding period, then such U.S. shareholder generally will be required to treat any gain realized upon a disposition of common shares, or any so-called “excess distribution” received on its common shares, as ordinary income, and to pay an interest charge on a portion of such gain or distributions, unless the U.S. shareholder makes a timely and effective “qualified electing fund” election (“QEF Election”) or a “mark-to-market” election with respect to the common shares. A U.S. shareholder who makes a QEF Election generally must report on a current basis its share of the Company’s net capital gain and ordinary earnings for any year in which EMX is a PFIC, whether or not EMX distributes any amounts to its shareholders. For each tax year that EMX qualifies as a PFIC, EMX intends to: (a) make available to U.S. shareholders, upon their written request, a “PFIC Annual Information Statement” as described in Treasury Regulation Section 1.1295 -1(g) (or any successor Treasury Regulation) and (b) upon written request, use commercially reasonable efforts to provide all additional information that such U.S. shareholder is required to obtain in connection with maintaining such QEF Election with regard to EMX. EMX may elect to provide such information on its website www.EMXRroyalty.com. This paragraph is qualified in its entirety by the discussion below the heading “Taxation – Certain United States Federal Income Tax Considerations.” Each U.S. investor should consult its own tax advisor regarding the PFIC rules and the U.S. federal income tax consequences of the acquisition, ownership and disposition of common shares.

Corporate Governance and Public Disclosure Regulations

The Company is subject to changing rules and regulations promulgated by a number of United States and Canadian governmental and self-regulated organizations, including the United States Securities and Exchange Commission (“SEC”), the British Columbia and Alberta Securities Commissions, the NYSE American and the TSX-V. These rules and regulations continue to evolve in scope and complexity and many new requirements have been created, making compliance more difficult and uncertain. The Company’s efforts to comply with the new rules and regulations have resulted in, and are likely to continue to result in, increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities.

19

Internal Controls over Financial Reporting

Applicable securities laws require an annual assessment by management of the effectiveness of the Company’s internal control over financial reporting. The Company may, in the future, fail to achieve and maintain the adequacy of its internal control over financial reporting, as such standards are modified, supplemented or amended from time to time, and the Company may not be able to ensure that it can conclude on an ongoing basis that it has effective internal control over financial reporting. Future acquisitions may provide the Company with challenges in implementing the required processes, procedures and controls in its acquired operations. Acquired Corporations may not have disclosure controls and procedures or internal control over financial reporting that are as thorough or effective as those required by securities laws currently applicable to the Company.

No evaluation can provide complete assurance that the Company’s internal control over financial reporting will detect or uncover all failures of persons within the Company to disclose material information otherwise required to be reported. The effectiveness of the Company’s controls and procedures could also be limited by simple errors or faulty judgments. In addition, should the Company expand in the future, the challenges involved in implementing appropriate internal control over financial reporting will increase and will require that the Company continue to improve its internal control over financial reporting.

ITEM 4. INFORMATION ON THE COMPANY

4.A. History and Development of the Company

General Background

EMX Royalty Corporation was incorporated under the laws of the Yukon Territory of Canada on August 21, 2001 as 33544 Yukon Inc. and, on October 10, 2001, changed its name to Southern European Exploration Ltd. On November 24, 2003, the Company completed the reverse take-over of Marchwell Capital Corp., a TSX-V-listed company incorporated in Alberta on May 13, 1996 and which subsequently changed its name to Eurasian Minerals Inc. On September 21, 2004, EMX continued into British Columbia from Alberta under the Business Corporations Act. On July 19, 2017, EMX changed its name to EMX Royalty Corporation to better reflect the nature of its business.

EMX is a reporting issuer under the securities legislation of British Columbia and Alberta, and is listed on the TSX-V Exchange as a Tier 1 issuer and the NYSE American Exchange, with both listings under the symbol “EMX”.

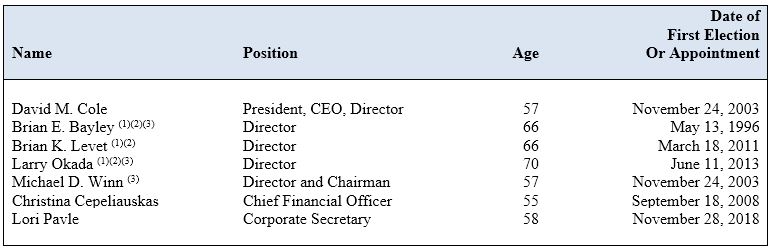

The Company’s corporate office is located at Suite 501, 543 Granville Street, Vancouver, British Columbia, Canada V6C 1X8, and its telephone number is 604-688-6390. The Company’s registered and records office is located at Suite 704, 595 Howe Street, Vancouver, British Columbia, V6C 2T5. The Company’s technical office is located at 10001 W. Titan Road, Littleton, Colorado, United States of America, 80125, and its telephone number is 303-973-8585. The contact person is Lori Pavle, Corporate Secretary.

20

Fiscal Year ended December 31, 2016

| • |

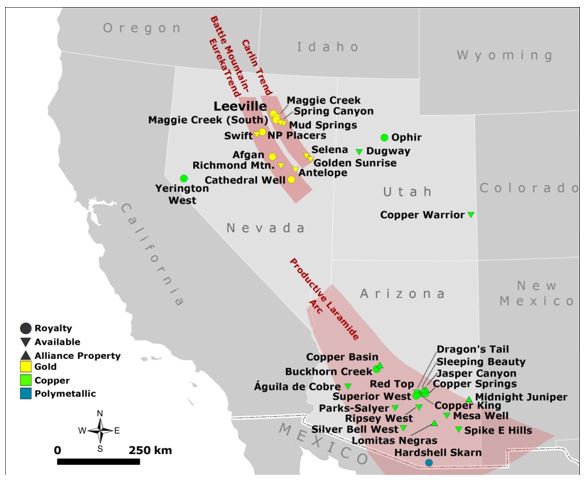

On February 23, 2016 the Company announced the execution of a purchase agreement (the “Golden Predator Agreement”) for net smelter return royalty interests on the Maggie Creek and Afgan gold properties from Golden Predator US Holding Corp. (“Golden Predator”), a wholly-owned subsidiary of Till Capital Ltd. ("TCL"). Golden Predator had a 2% NSR royalty on all precious metals and a 1% NSR royalty on all other minerals for the Maggie Creek property, which is located north-northeast of Newmont Mining Corporation's ("Newmont") Gold Quarry open pit operations on the Carlin Trend, and a 1% NSR royalty on all minerals for the Afgan property, which occurs on the Battle Mountain-Eureka Trend. The addition of these two royalty assets strengthened the Company's growing Nevada gold portfolio that includes the Leeville royalty property on the Northern Carlin Trend, as well as the Maggie Creek South royalty property located south-southeast of Gold Quarry. |

| A summary of the Golden Predator Agreement's commercial terms includes: |

| - |

Purchase by the Company of Golden Predator’s NSR royalties covering the Maggie Creek (2% NSR on precious metals and 1% NSR royalty on all other minerals) and Afgan (1% NSR royalty) properties; | |

| - |

Issuance by the Company of 250,000 EMX shares to TCL as consideration for the purchase; and | |

| - |

Approval by the TSX-V and NYSE American as a condition precedent to closing the transaction. |

| • |

On March 7, 2016 the Company announced that the purchase of net smelter return royalty interests had been completed for the Maggie Creek and Afgan gold properties from Golden Predator after receiving approvals from the TSX Venture and NYSE American Exchanges. |

| • |

In Q1 2016, EMX sold its 100% controlled Grand Bois project in Haiti, which was outside the Joint Venture with Newmont, to a privately held Nevada corporation. EMX retained a 0.5% NSR royalty interest in the Grand Bois project and the right to acquire any properties proposed to be abandoned or surrendered from the Grand Bois project in the future. |

| • |

On July 25, 2016 the Company reported that IGC advised that approval to advance the Malmyzh copper-gold project had been received from the Government Commission on Monitoring Foreign Investment (the "Commission") chaired by Prime Minister Dmitry Medvedev. The Malmyzh exploration and mining licenses are held by IGC (51%) and Freeport- McMoRan Exploration Corporation (49%) (the "Joint Venture"), with IGC operating and managing the project. The Commission's approval marks a pivotal milestone in the development of the Malmzyh project. EMX is IGC’s largest shareholder. |

|

IGC advised that the Commission's approval represents the successful completion of the review process required for “strategically significant” deposits according to Russian law (i.e., the Law on Foreign Investments in Strategic Industries, also termed the Strategic Industries Law or "SIL"). The SIL approval process commenced after the Joint Venture, through its Russian subsidiary Amur Minerals LLC, received certified “on balance C1+C2 reserves” from the GKZ (State Reserves Committee) that exceeded thresholds for both copper and gold defining Malmyzh as a "strategically significant" mineral deposit. EMX emphasizes that the Malmyzh “C1+C2 reserves” were estimated according to the rules and regulations of the Russian Federation, and are not the same as reserves under NI 43-101 or SEC Industry Guide 7. According to IGC, highlights of the Commission's approval included: |

| - |

The Joint Venture, as a majority foreign owned business entity, has been approved to retain control of the Malmyzh project exploration and mining licenses. | |

| - |

The Joint Venture, therefore, maintains mining and production rights for the Malmyzh and Malmyzh North exploration and mining licenses. | |

| - |

The Joint Venture holds 100% of the rights for the Malmyzh and Malmyzh North exploration and mining licenses, and is entitled to recover all minerals of economic value including copper, gold and by- product minerals. |

The conclusion of the SIL process initiated a new, multi-year phase in the project's development, including additional technical work (i.e., drilling, exploration, metallurgy, engineering, and hydrology), as well as environmental, social, and economic assessments. This next phase of work will ultimately conclude as a detailed "TEO1 of Permanent Conditions" report, which is considered to be a precursor to commencement of exploitation and mining.

1 Technico-Economicheskiye Obosnovaniye (Technical-Economic Basis)

21

|

• |

On August 3, 2016, the Company announced the sale of EBX Madencilik A.S., the wholly-owned EMX subsidiary that controls the Sisorta gold property (the “Sisorta Property”) in Turkey, to Bahar Madencilik Sinayi ve Ticaret Ltd Sti ("Bahar"), a privately owned Turkish company, pursuant to a Share Purchase Agreement (the “Sisorta Agreement”) with Bahar. |

| The Sisorta Agreement provides for Bahar's staged payments to EMX as summarized below (all amounts in USD): |

| - |

$250,000 cash payment to EMX upon closing of the sale. | |

| - |

Annual cash payments of $125,000 (“Advance Cash Payments”) payable on each anniversary of the closing date until commencement of commercial production from the Sisorta Property. | |

| - |

3.5% of production returns after certain deductions (“NSR Payment") for ore mined from the Sisorta Property that is processed on-site (increased to 5% if the ore is processed off-site). | |

| - |

The Advance Cash Payments will be credited at a rate of 80% against the NSR Payment payable after commercial production commences. | |

| - |

The NSR Payment is uncapped and cannot be bought out or reduced. |

|

Bahar intends to conduct advanced exploration and development work on the Sisorta project. | |

| • |

On August 8, 2016 the Company announced the sale of AES Madencilik A.S., the wholly-owned EMX subsidiary that controls the Akarca gold-silver project (the “Akarca Property”) in western Turkey, to Çiftay Insaat Taahhüt ve Ticaret A.S. ("Çiftay"), a privately owned Turkish company. The Akarca Property is an EMX grassroots discovery highlighted by six separate gold-silver mineralized centers occurring within a district-scale area. |

|

The terms of the sale provide payments to EMX as summarized below (all dollar amounts in United States dollars and all gold payments can be as gold bullion or the cash equivalent): |

|

$2,000,000 cash payment to EMX upon closing of the sale (completed). | ||

| -- |

500 ounces of gold every six months commencing February 1, 2017 up to a cumulative total of 7,000 ounces of gold. | |

| - |

7,000 ounces of gold within 30 days after the commencement of commercial production from the Akarca Property provided that prior gold payments will be credited against this payment. | |

| - |