UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE | |

ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to _________

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE | |

ACT OF 1934 |

Date of event requiring this shell company report

Commission file number:

(Exact name of Registrant as specified in its charter)

Not Applicable | The Kingdom of |

(Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organization) |

(Address of principal executive offices)

Chief Executive Officer

Evaxion Biotech A/S

Tel: +

E-mail:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol |

| Name of each exchange on which registered |

| ||||

Ordinary Shares, nominal value of DKK 1 per share* |

*Not for trading, but only in connection with the registration of American Depositary Shares on the Nasdaq Stock Market LLC representing such Ordinary shares pursuant to requirements of the U.S. Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. The number of outstanding shares as of December 31, 2023, was:

Title of each class |

| Number of Shares Outstanding at December 31, 2023 |

Ordinary share, nominal value DKK1 per share | ||

(including shares underlying American Depository Shares) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company (as defined in Rule 12b-2 of the Act).

Large Accelerated Filer ☐ | Accelerated Filer ☐ | |

Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Auditor Firm ID | |

Auditor Name | |

Auditor Location | Copenhagen, |

TABLE OF CONTENTS

Page | ||

2 | ||

3 | ||

3 | ||

3 | ||

5 | ||

7 | ||

7 | ||

7 | ||

93 | ||

174 | ||

175 | ||

190 | ||

206 | ||

208 | ||

209 | ||

210 | ||

236 | ||

236 | ||

237 | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 237 | |

238 | ||

239 | ||

239 | ||

239 | ||

240 | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 240 | |

240 | ||

240 | ||

245 | ||

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 245 | |

245 | ||

245 | ||

246 | ||

246 | ||

II-1 | ||

II-3 | ||

F-2 | ||

1

CERTAIN DEFINITIONS

Unless otherwise indicated and except where the context otherwise requires, references in this annual report on Form 20-F to:

| ● | “ADSs” are to our American Depositary Shares, each of which represents ten ordinary shares of Evaxion Biotech A/S; |

| ● | “ADRs” are to the American depositary receipts that evidence our ADSs; |

| ● | “Exchange Act” are to the United States Securities Exchange Act of 1934, as amended; |

| ● | “FDA” are to the United States Food and Drug Administration; |

| ● | “Evaxion,” the “Company,” “we,” “us” and “our” refer to Evaxion Biotech A/S and our wholly owned subsidiaries; |

| ● | “Group” are to the consolidated entities of Evaxion Biotech A/S, Evaxion Biotech Australia Pty Ltd and Evaxion Biotech, Inc.; |

| ● | “IND” are to Investigational New Drug Application; |

| ● | “ordinary shares” are to our ordinary shares, each of DKK 1 nominal value; |

| ● | “SEC” are to the United States Securities and Exchange Commission; |

| ● | “Securities Act” are to the Securities Act of 1933, as amended; |

| ● | “$,” “USD,” “US$” and “U.S. dollar” are to the United States dollar; and |

| ● | “DKK,” “Krone,” and “Kroner” are to the Danish Krone |

On January 22, 2024, the Company made effective a change to its ratio of ADSs to its ordinary shares, DKK 1 nominal value (the “ADS Ratio”). The ratio has been changed from one ADS representing one ordinary share to a new ADS Ratio of one ADS representing ten ordinary shares of the Company. The change was made to enable the Company to regain compliance with the Nasdaq minimum bid price requirement. Unless specified otherwise, all references in this annual report to ADS share and ADS per share data have been adjusted, including historical data which has been retroactively adjusted, to give effect to the ADS Ratio change.

2

PRESENTATION OF FINANCIAL INFORMATION

This annual report contains our audited consolidated financial statements as of December 31, 2023, and 2022 and for the years ended December 31, 2023, 2022 and 2021 (our “audited consolidated financial statements”), prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”).

Our financial information is presented in our presentation currency, U.S. Dollar, or USD. Our parent Company’s functional currency is the Danish Krone, or DKK. Certain Danish Krone amounts in this annual report have been translated solely for convenience into USD at an assumed exchange rate of DKK 6.7447 per $1.00, which was the official exchange rate of such currencies as of December 31, 2023, rounded to four decimal places, as reported by Danmarks Nationalbank.

Foreign currency transactions are translated into our functional currency, DKK, using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognized as financial income or financial expenses in the statements of comprehensive loss. Non-monetary items in foreign currency, which are measured at cost at the statements of financial position date are translated into our functional currency, DKK, using the exchange rates at the date of the transaction. Such DKK translated amounts are not necessarily indicative of the amounts of DKK that could have actually been purchased with the underlying currency being exchanged into DKK at the dates indicated.

Assets and liabilities in our functional currency are translated to our presentation currency, USD, at the exchange rate applicable on December 31, 2023. Income and expenses in our functional currency are translated to USD at the average exchange rate, which corresponds to an approximation of the exchange rates prevailing on each individual transaction date. Translation differences arising in the translation to presentation currency are recognized in other comprehensive income. Such USD amounts are not necessarily indicative of the amounts of USD that could actually have been purchased upon exchange of DKK at the dates indicated.

We have made rounding adjustments to some of the figures contained in this annual report. Accordingly, numerical figures shown as totals in some tables may not be exact arithmetic aggregations of the figures that preceded them.

TRADEMARKS, SERVICE MARKS AND TRADENAMES

This annual report includes trademarks, tradenames and service marks, certain of which belong to us and others that are the property of other organizations. Solely for convenience, trademarks and tradenames referred to in this annual report appear without the and ™ symbols, but the absence of those references is not intended to indicate, in any way, that we will not assert our rights or that the applicable owner will not assert its rights to these trademarks and tradenames to the fullest extent under applicable law. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply a relationship with, or endorsement or sponsorship of us by, these other parties.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements concerning our business, operations and financial performance and condition, as well as our plans, objectives and expectations for our business operations and financial performance and condition. Many of the forward-looking statements contained in this annual report can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “goal,” “intend,” “may,” “might,” “plan,” “potential,” “should,” “target,” “would” and other similar expressions that are predictions of or indicate future events and future trends, although not all forward-looking statements contain these identifying words.

3

Forward-looking statements appear in a number of places in this annual report and include, but are not limited to, statements regarding intent, belief or current expectations. Forward-looking statements are based on the current beliefs and assumptions of the management of Evaxion and on information currently available to such management. While the management of Evaxion believes that these forward-looking statements are reasonable as and when made, there can be no assurance that future developments will be as anticipated. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to of various factors, including, but not limited to, those identified under the section “Item 3. Key Information—D. Risk Factors” in this annual report. These risks and uncertainties include factors relating to:

| ● | the initiation, timing, progress, results, and cost of our research and development programs and our current and future pre-clinical studies and clinical trials, including statements regarding the timing of initiation and completion of studies or trials and related preparatory work, the period during which the results of the trials will become available and our research and development programs; |

| ● | our ability to enter in partnerships which is a key element of our refocused strategy; |

| ● | the timing of and our ability to obtain and maintain regulatory approval for our product candidates; |

| ● | our ability to identify research opportunities and discover and develop investigational medicines; |

| ● | the ability and willingness of our third-party collaborators to continue research and development activities relating to our development candidates and investigational medicines; |

| ● | our expectations regarding the size of the patient populations for our product candidates, if approved for commercial use; |

| ● | our estimates of our expenses, ongoing losses, future revenue and capital requirements and our needs for or ability to obtain additional financing; |

| ● | our ability to identify, recruit and retain key personnel; |

| ● | our and our collaborators’ ability to protect and enforce our intellectual property protection for our proprietary and collaborative product candidates, and the scope of such protection; |

| ● | the development of and projections relating to our competitors or our industry; |

| ● | our and our collaborators’ ability to commercialize our product candidates, if approved; |

| ● | the pricing and reimbursement of our investigational medicines, if approved; |

| ● | the rate and degree of market acceptance of our investigational medicines; |

| ● | the amount of and our ability to use our net operating losses, or NOLs, and research and development credits to offset future taxable income; |

| ● | our ability to manage our development and expansion; |

| ● | regulatory developments in the United States, Europe, Australia and other foreign countries; |

| ● | our ability to manufacture our product candidates with advantages in turnaround times or manufacturing cost; |

| ● | our ability to implement, maintain and improve effective internal controls; |

| ● | our expectations regarding the time during which we will be an emerging growth company under the JOBS Act and a foreign private issuer; |

4

| ● | adverse effects on our business condition and results for operation from general economic and market conditions and overall fluctuations in the United States and international equity markets, including deteriorating market conditions due to investor concerns regarding inflation and hostilities between Russia and Ukraine and other global conflicts such as ongoing in the Middle East; and |

| ● | other risk factors discussed under “Item 3. Key Information—D. Risk Factors”. |

Our actual results or performance could differ materially from those expressed in, or implied by, any forward-looking statements relating to those matters. Accordingly, no assurances can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what impact they will have on our results of operations, cash flows or financial condition. Except as required by law, we are under no obligation, and expressly disclaim any obligation, to update, alter or otherwise revise any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise.

Summary of Material Risks Associated with Our Business

The principal risks and uncertainties affecting our business include the following:

| ● | We are a clinical stage TechBio company with only product candidates currently in clinical development. |

| ● | We have a limited operating history and no vaccine has been approved using our technology, and none may ever be approved. |

| ● | We are dependent upon successfully concluding partnerships to advance our product candidates to monetize our assets. |

| ● | We have incurred significant losses since our inception, and we anticipate that we will continue to incur significant losses for the foreseeable future. |

| ● | We will require substantial additional financing to achieve our goals, and a failure to obtain this capital on acceptable terms, or at all, could force us to delay, limit, scale back or cease our product development activities or any other or all operations. |

| ● | We will need to develop and expand our company, and we may encounter difficulties in managing this development and expansion, which could disrupt our operations. |

| ● | We are substantially dependent on the success of product candidates, which may not be successful in nonclinical studies or clinical trials, receive regulatory approval or be successfully commercialized. |

| ● | Clinical drug development involves a lengthy and expensive process with uncertain outcomes, and we may encounter substantial delays in our clinical studies. Furthermore, results of earlier studies and trials may not be predictive of results of future trials. |

| ● | Interim and preliminary data from our clinical trials that we announce or publish from time to time may change as more patient data become available and are subject to audit and verification procedures that could result in material changes in the final data. |

| ● | Pharmaceutical product development is inherently uncertain, and there is no guarantee that any of our product candidates will receive marketing approval. |

| ● | Competition in the biotechnology and pharmaceutical industries is intense and our competitors may discover, develop or commercialize products faster or more successfully than us. If we are unable to compete effectively our business, results of operations and prospects will suffer. |

5

| ● | The effects of the invasion of Ukraine by Russia, the resulting conflict and retaliatory measures by the global community have created global security concerns, including the possibility of expanded regional or global conflict, which have had, are likely to continue to have, short-term and likely longer-term adverse impacts on Ukraine and Europe and around the globe, which could adversely affect our business and results of operations. The same applies to other global conflicts such as the ongoing conflict in the Middle East. |

| ● | Our product candidates may not work as intended, may cause undesirable side effects or may have other properties that could delay or prevent their regulatory approval, limit the commercial profile of an approved label or result in significant negative consequences following marketing approval, if any. |

| ● | The regulatory approval processes of the U.S. Food and Drug Administration, the European Medicines Agency and comparable authorities are lengthy, time consuming, and inherently unpredictable. If we are ultimately unable to obtain regulatory approval for our product candidates, our business will be substantially harmed. |

| ● | Our future partners, if any, may not be able to obtain regulatory approval for products, if any, derived from our product candidates under applicable United States, European and other international regulatory requirements. |

| ● | Even if products derived from our product candidates receive regulatory approval, such products may not gain market acceptance and our future partners, if any, may not be able to effectively commercialize them. |

| ● | If we are not successful in developing our product candidates and our future partners, if any, are not successful in commercializing any products derived from our product candidates, our ability to expand our business and achieve our strategic objectives will be impaired. |

| ● | We rely on third-parties to manufacture preclinical, clinical and commercial supplies of our products, product candidates and their components. In addition, we rely on third-parties in the conduct of significant aspects of our pre-clinical studies and clinical trials, and we intend to rely on third parties in the conduct of future clinical trials. If these third parties do not successfully carry out their contractual duties, fail to comply with applicable regulatory requirements and/or fail to meet expected deadlines, we may be unable to obtain regulatory approval for our product candidates. |

| ● | Our future partners, if any, may encounter difficulties in manufacturing, product release, shelf life, testing, storage, supply chain management and/or shipping, and/or all of which could materially adversely affect our business operations. |

| ● | Certain of our product candidates may be uniquely manufactured for each patient and we and/or our future partners may encounter difficulties in production, particularly with respect to the scaling of manufacturing capabilities. |

| ● | If our and our future partners’, if any, efforts to obtain, maintain, protect, defend and/or enforce the intellectual property related to our product candidates and technologies are not adequate, we may not be able to compete effectively in our market. |

| ● | We may be involved in lawsuits to protect or enforce our intellectual property or the intellectual property of our licensors, or to defend against third-party claims that we infringe, misappropriate or otherwise violate such third party’s intellectual property. |

The summary risk factors described above should be read together with the text of the full risk factors below in the section entitled “Risk Factors” and the other information set forth in this Annual Report on Form 20-F, including our consolidated financial statements and the related notes, as well as in other documents that we file with the United States Securities and Exchange Commission. The risks summarized above or described in full below are not the only risks that we face. Additional risks and uncertainties not precisely known to us or that we currently deem to be immaterial may also materially adversely affect our business, financial condition, results of operations, and future growth prospects.

6

PART I

Item 1.Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2.Offer Statistics and Expected Timetable

Not applicable.

Item 3.Key Information

3.A. Reserved

3.B. Capitalization and Indebtedness

Not applicable.

3.C. Reasons for the Offer and Use of Proceeds

Not applicable.

3.D. Risk Factors

We are a clinical-stage TechBio company with an ambition to partner on targets, pipeline and responders with no pharmaceutical products approved for commercial sale. Also, we have not yet made out-licensing agreements. Our business faces significant risks. You should carefully consider all of the information set forth in this annual report and in our other filings with the SEC, including the following risk factors which we face, and which are faced by our industry. Our business, financial condition, results of operations or prospects could be materially adversely affected by any of these risks. This annual report also contains forward- looking statements that involve risks and uncertainties. Our results could materially differ from those anticipated in these forward-looking statements, as a result of certain factors including the risks described below and elsewhere in this report and our other SEC filings. See “Special Note Regarding Forward-Looking Statements” above.

Risks Related to our Financial Condition and Capital Requirements

We have incurred significant losses since our inception and we anticipate that we will continue to incur significant losses for the foreseeable future, which makes it difficult to assess our future viability. We have not generated significant revenue and may never be profitable.

We have incurred net losses in each year since our inception in 2008, including net losses of $22.1 million, $23.2 million, and $24.5 million for the years ended December 31, 2023, 2022, and 2021, respectively. As of December 31, 2023, we had an accumulated deficit of $108.0 million.

7

We have devoted most of our financial resources to research and development, including our pre- clinical and clinical development activities and the development of our AI-Immunology™ platform. To date, we have financed our operations primarily through the sale of equity securities, issuance of convertible debt instruments and through private and governmental grants. The amount of our future net losses will depend, in part, on the rate of our future expenditures and our ability to obtain funding through equity or debt financings, sales of assets, collaborations, including our out-licensing arrangements, if any, and grants. We believe that the cost and expense of most clinical testing, regulatory and marketing approval and commercialization of our product candidates are beyond the resources of all but the large biopharmaceutical and pharmaceutical companies. Therefore, we currently intend to develop our vaccines through pre- clinical or clinical proof of concept, or PoC, and then enter into partnership arrangements with large biopharmaceutical and pharmaceutical companies to conduct further clinical trials, regulatory and marketing approval and commercialization of our product candidates. We have so far entered into one partnership arrangement at an early stage but may be unable to do so on economically viable terms large scale. As a result, clinical trials, including late-stage clinical trials as well as pivotal clinical trials for our product candidates have not been commenced under any such partnership arrangements and even if such trials are commenced in the near future, it will be several years, if ever, before we, or our partners, if any, have a product candidate ready for commercialization. Even if our future partners, if any, obtain regulatory approval to market a product candidate, our future revenues will depend upon the size of any markets in which our product candidates receive such approval, upfront, milestone and any other payments we receive from our future partners, if any, and our future partners’, if any,’, ability to achieve sufficient market acceptance, reimbursement from third-party payors, and adequate market share in those markets. We may never achieve profitability.

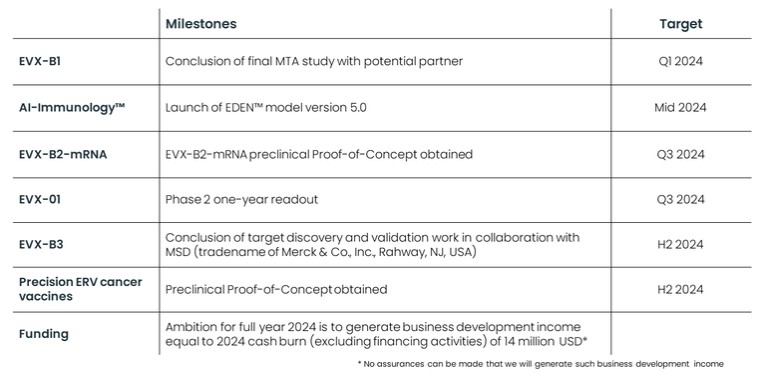

Our ability to generate revenue and achieve profitability depends on our ability to successfully complete the development of, and our partners’ ability to obtain the regulatory approvals necessary to commercialize, our product candidates. We have the ambition to generate revenue from business development deals equal to 2024 cash burn (excluding financing activities) of $14.0 million, although no assurances can be made that we will generate such revenue and do not anticipate generating substantial revenue in the near future.

We expect to continue to incur significant expenses and operating losses for the foreseeable future. For the current year the primary cost drivers are:

| ● | continue our research or development of our programs in pre-clinical and clinical development; |

| ● | continue to invest in our AI-Immunology™ platform to improve its predictive capabilities and identify novel vaccines targets; |

| ● | invest in generated needed pre-clinical evidence to support our partnership strategy; |

| ● | change or add more suppliers; |

| ● | add more infrastructure to our quality control, quality assurance, legal, accounting, compliance and other groups to support our operations including our operation as a public company; |

| ● | attract and retain skilled personnel; |

| ● | make milestone or other payments under any in-license agreements; and |

| ● | maintain, protect, defend, enforce and expand our intellectual property portfolio. |

Our ability to generate future revenues from our potential commercialization partnerships depends heavily on our success in:

| ● | completing research and pre-clinical development, and successfully entering into partnership arrangements with large biopharmaceutical and pharmaceutical companies to conduct clinical trials, regulatory and marketing approval and commercialization of our product candidates for both our immuno-oncology and infectious disease product candidates to validate our AI-Immunology™ platform; and other business efforts; |

| ● | seeking, negotiating and obtaining agreements with future partners, if any, on favorable terms for the completion of clinical trials, and United States and non- United States marketing approvals and commercialization of our product candidates; |

8

| ● | Our relationships with our third-party manufacturers in order to provide adequate (in amount and quality) products and services to support clinical development of our product candidates; |

| ● | our future partners, if any, obtaining market acceptance of our product candidates as treatment options; |

| ● | our future partners, if any, launching and commercializing our product candidates for which marketing approval and reimbursement have been obtained; |

| ● | addressing any competing technological and market developments; |

| ● | implementing additional internal systems and infrastructure; |

| ● | maintaining, defending, protecting, enforcing and expanding our portfolio of intellectual property rights, including patents, trade secrets and know-how; and attracting, hiring and retaining qualified personnel. |

Our operating results may fluctuate significantly, which makes our future operating results difficult to predict. If our operating results fall below expectations, the market price of the ADSs could decline.

Our financial condition and operating results have varied in the past and will continue to fluctuate from one financial period to the next due to a variety of factors, many of which are beyond our control. Factors relating to our business that may contribute to these fluctuations include the following, as well as other factors described elsewhere in this Form 20-F:

| ● | delays or failures in advancement of existing or future product candidates into pre-clinical studies or clinical trials; |

| ● | failures in further development of our AI-Immunology™ platform; |

| ● | failure to enter into new partnerships critical for realization of our strategy; |

| ● | the ability of our future partners, if any, to manufacture and successfully commercialize our product candidates; |

| ● | our ability to manage development of the Company; |

| ● | the outcomes of research programs, pre-clinical studies and clinical trials, and other product development or approval processes conducted by us and/or our future partners, if any; |

| ● | our relationships, and any associated exclusivity terms, with partners; |

| ● | our contractual or other obligations to provide resources to fund our product candidates; |

| ● | our operations in a net loss position for the foreseeable future; |

| ● | risks associated with the international aspects of our business outside of Denmark, including the conduct of clinical trials in multiple locations; |

| ● | our and our partners’, to the extent relevant, consistent ability to have our products and product candidates manufactured by third parties; |

| ● | our ability to develop programs to fit into a clinical work-flow and treatment regimen; |

| ● | our ability to accurately report our financial results in a timely manner; |

| ● | our dependence on, and the need to attract and retain, key management and other personnel; |

| ● | our and our partners’ ability to obtain, protect, maintain, defend and enforce our intellectual property rights; |

9

| ● | our and our partners’ ability to prevent the theft or infringement, misappropriation or other violation of our intellectual property, trade secrets, know-how or technologies; |

| ● | potential advantages that our competitors and potential competitors may have in securing funding, obtaining the rights to critical intellectual property or developing competing technologies or products; |

| ● | our ability to obtain additional capital that may be necessary to expand our business; |

| ● | our future partners’, if any, ability to obtain additional capital that may be necessary to develop and commercialize products under any future collaboration or licensing agreements; |

| ● | business interruptions such as power outages, strikes, acts of terrorism, pandemics or natural disasters; |

| ● | the effects of climate change on our operations; |

| ● | the effects of the continuing conflict between Russian and the Ukraine and in the Middle East may have on our business and operations; and |

| ● | our ability to use our net operating loss, or NOL, carryforwards to offset future taxable income. |

Due to the various factors mentioned above, and others, the projected financial information included in this Form 20-F should not be relied upon as indications of our future operating performance.

We have a history of losses and will require additional funding to support ongoing operational needs.

We have incurred recurring losses since inception. We expect to continue to incur significant expenses related to the research, development, and manufacturing of our product candidates and in connection with conducting clinical studies related thereto. Additionally, we may encounter unforeseen difficulties, complications, development delays and other unknown factors that require additional expense. As a result of these expenditures, we expect to continue to incur significant losses in the foreseeable future.

We have not yet established a source of revenue sufficient to cover our operating costs, and as such, we have financed our operations through successive capital increases, collaboration agreements and receipt of research grants.

These facts and conditions raise substantial doubt about our ability to continue as a going concern, and our independent registered public accounting firm has included an explanatory paragraph regarding going concern in its audit report. While we have entered arrangements for financing with Lincoln Park Capital Fund, LLC (“Lincoln Park”) and Global Growth Holdings, those facilities are not yet operational or effective and may never be. The failure to raise additional funding may have a material adverse effect on our business, results of operations and financial position, and may adversely affect our ability to continue as a going concern. If we do not become consistently profitable, our accumulated deficit will grow larger and our cash balances will decline further, and we will require further financing to continue operations. Any such financing may not be accessible on acceptable terms, if at all.

If we are unable to obtain funding on a timely basis, we may be required to significantly curtail, delay or discontinue one or more of our research and development programs of our product candidates or be required to file for reorganization or liquidation under applicable reorganization or bankruptcy laws.

We will need substantial additional financing to achieve our goals, which may not be available on acceptable terms, or at all. Failure to obtain this necessary capital could force us to delay, limit, reduce or terminate our product development programs, commercialization efforts or other operations.

Our cash and cash equivalents were $5.6 million as of December 31, 2023. The net proceeds from our IPO completed in February 2021 was $25.3 million, based on the initial public offering price of $100.00 per ADS, after deducting underwriting discounts and commissions and offering expenses. The net proceeds from our follow-on offering completed in November 2021 was $24.9 million, based on the public offering price of $70.00 per ADS after deducting underwriting discounts and commissions and offering expenses.

10

In August 2020, we executed a loan agreement, or the EIB Loan Agreement, with the European Investment Bank, or EIB, for a principal amount of €20.0 million, divided into three tranches of tranche 1 in the amount of €7.0 million, tranche 2 in the amount of €6.0 million and tranche 3 in the amount of €7.0 million, or the EIB Loan. Under the EIB Loan Agreement, the EIB Loan tranche balances are due six years from their respective disbursement dates. In connection with disbursement of each tranche, EIB is entitled to receive certain warrants, or the “EIB Warrants”. In November 2020, we initiated the process to receive the funds from the disbursement of tranche 1 of the EIB Loan in the aggregate amount of €7.0 million but due to the timing of our IPO we did not finalize a disbursement offer. In connection therewith, EIB received 351,036 EIB Warrants, which vested immediately, pursuant to the terms of a separate warrant agreement, or the EIB Warrant Agreement. We received the proceeds from the drawdown of the first tranche of the EIB loan of €7.0 million on February 17, 2022. The remaining two tranches have become void.

In June 2022, we entered into a purchase agreement, or the LPC Purchase Agreement, with Lincoln Park, pursuant to which we may, from time to time and at our sole discretion, for a period of 36-months, direct Lincoln Park to purchase up to 4,649,250 of our ordinary shares represented by the ADSs, subject to the development in the ADS price. If the ADS price is between $5.00 and $40.00 the number of purchase shares is limited to 50,000. If the price is not below $40.00 the purchase share limit may be increased to 60,000 purchase shares and if the price is not below $60.00 the purchase shares limit may be increased to 70,000 purchase shares. Under the terms of the LPC Purchase Agreement, we may receive up to $40.0 million in aggregate gross proceeds from any sales of our ordinary shares represented by ADSs that we make to Lincoln Park thereunder. In connection with the LPC Purchase Agreement, we issued 428,572 ADSs representing ordinary shares to Lincoln Park as consideration for a commitment fee of $1.2 million for Lincoln Park’s agreement to purchase ordinary shares represented by ADSs under the LPC Purchase Agreement, or the Commitment Shares. As of the date of this annual report, Lincoln Park has not purchased any additional ordinary shares represented by the ADSs and we have not received any proceeds therefrom. At current, not all conditions to make the LPC Purchase Agreement operational have been met.

In October 2022, we initiated an at-the-market, or ATM, program with JonesTrading Institutional Services LLC, or JonesTrading, acting as sales agent, relating to the sale of up to $14,439,000 of the ADSs. As of the date of this annual report, we have raised gross proceeds of $9.2 million from the sale of ADSs under this ATM program.

On July 31, 2023, we entered into an agreement with Global Growth Holding Limited, or GGH, for the issuance of, and subscription to, convertible notes, or the Notes, convertible into ADSs representing new ordinary shares, nominal value DKK 1, or the ordinary shares, or the GGH Agreement. Pursuant to the GGH Agreement, we may elect to sell to GGH up to $20,000,000 in such Notes, subject to certain limitations and conditions set forth in therein. The Notes are subject to conversion into new ordinary shares at any time upon submission of a request for conversion by GGH. Pursuant to the GGH Agreement, on any business day over the 36-month term of the GGH Agreement, we have the right, but not the obligation, at our sole discretion and subject to certain conditions, to direct GGH to purchase tranches of up to $700,000 in aggregate value of Notes, or a Tranche. The Notes carry a zero coupon and will be issued at a subscription price corresponding to their par value. The conversion price of the Notes will be determined as 83.5% of the second lowest closing VWAP of the ADSs for the eight (8) trading days immediately preceding the issuance of each conversion request by GGH, unless the lowest closing VWAP of the ADSs over the such eight (8) trading days is the most recent trading day in which case the conversion price will be 85% of the lowest closing VWAP of the ADSs over such eight (8) day period. The facility has by December 31, 2023, not been used as the registration statement has not been filed with the SEC yet as other registrations have been prioritized.

On December 18, 2023, we entered into a Securities Purchase Agreement (“SPA”) and an Investment Agreement (the “Investment Agreement”, and together with the SPA referred to herein as the “Purchase Agreements”), with a group certain investors including all members of our Management and Board of Directors, and MSD Global Health Innovation Fund (“MSD GHI”), a corporate venture capital arm of Merck & Co., Inc., Rahway, NJ USA, accounting for some 25% of the total offering amount (collectively, the “2023 SPA Investors”), for the issuance and sale in private placement of 9,726,898 ordinary shares, DKK 1 nominal value represented by ADSs, and accompanying warrants to purchase up to 9,726,898 ordinary shares represented by ADSs at a purchase price of $0.54 per ordinary share (the “2023 SPA Investor Warrants”). The 2023 SPA Investor Warrants are exercisable immediately upon issuance and expire three years after the closing date of the private placement and have an exercise price equal to $0.71 per ordinary share. The gross proceeds to us from the private placement were $5.3 million, with up to an additional $6.8 million of net proceeds upon cash exercise of the 2023 SPA Investor Warrants, before deducting offering expenses payable by us.

11

On February 5, 2024, we closed a public offering with net proceeds of $12.6 million including prefunded warrants at a market price of $4.00 per ADS and accompanying warrants to purchase up to 37,500,000 ordinary shares represented by ADSs at a purchase price of $0.40 per ordinary share (the “2024 PO Investor Warrants”). An amount of $4.3 million is held in an escrow account until exercise of the prefunded warrants.The 2024 PO Investor Warrants are exercisable immediately upon issuance and will result in up to $15.0 million of net proceeds upon cash exercise.

We expect that the net proceeds from our IPO, our follow-on offering, our private placement in December 2023, our public offering in February 2024 and the net proceeds, we have received and may receive in the future under the ATM program and our existing cash and cash equivalents will be sufficient to fund our operating expenses and capital expenditures into April 2025 under the assumption that prefunded warrants are exercised before February 2025. However, our operating plan may change as a result of many factors currently unknown to us, and we may need to seek additional funds sooner than planned, through public or private equity or debt financings, government or other third-party funding, sales of assets, other collaborations and licensing arrangements, or a combination of these approaches. In any event, we will require additional capital to achieve our goals. We will seek additional capital if market conditions are favorable, if needed for continuing our operational activities or if we have specific strategic considerations. Our spending will vary based on new and ongoing development and corporate activities. Due to high uncertainty of the length of time and activities associated with discovery and development of our product candidates, we are unable to estimate the actual funds we will require for our development activities.

Our future funding requirements, both near and long term, will depend on many factors, including, without limitation:

| ● | the initiation, progress, timing, costs, and results of pre-clinical studies and clinical trials for our product candidates; |

| ● | the results of research and our other platform activities; |

| ● | the clinical development plans we establish for our product candidates; |

| ● | the terms of any agreements with our future partners, if any; |

| ● | the number and characteristics of any technology that we develop or may in-license; |

| ● | the outcome, timing and cost of meeting regulatory requirements established by the FDA, the EMA, the TGA and other comparable regulatory authorities; |

| ● | the cost of filing, prosecuting, obtaining, maintaining, protecting, defending and enforcing our patent claims and other intellectual property rights, including actions for patent and other intellectual property infringement, |

| ● | misappropriation and other violations brought by third parties against us regarding our product candidates or actions by us challenging the patent or intellectual property rights of others; |

| ● | the effect of competing technological and market developments, including other products that may compete with one or more of our product candidates; |

| ● | the cost and timing of completion and further expansion of clinical scale manufacturing activities by third parties sufficient to support all of our current and future programs. |

| ● | the effects of climate change on the global economy and our business; and |

| ● | the effects of the continued conflict between Russia and the Ukraine and in the Middle East region on the global economy and our business. |

12

To date, we have financed our operations primarily through the sale of equity securities, the EIB loan and from private and governmental grants and we cannot be certain that additional funding will be available on favorable terms, or at all. Until we can generate sufficient upfront fees, milestone payments and royalty revenues from our agreements with future partners, if any, to finance our operations, which we may never do, we expect to finance our future cash needs through a combination of public or private equity offerings, debt financings, sales of assets, out-licensing arrangements, and other product development arrangements. Any fundraising efforts may divert our management from their day-to-day activities, which may adversely affect our ability to develop our product candidates, the AI-Immunology™ platform as well as establishing partnerships. In addition, we cannot guarantee that future financing will be available in sufficient amounts, at the right time, on favorable terms, or at all. Negative clinical trial data or setbacks, or perceived setbacks, in our programs or with respect to our technology could impair our ability to raise additional financing on favorable terms, or at all. Moreover, the terms of any financing may adversely affect the holdings or the rights of our shareholders, and the issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of the ADSs to decline. If we raise additional funds through public or private equity offerings, the terms of these securities may include liquidation or other preferences that may adversely affect our securityholders’ rights.

The amount of NOLs and research and development credits and our ability to use the same to offset future taxable income may be subject to certain limitations and uncertainty.

In Denmark, we have unused tax loss carryforwards for corporate taxes, though we have not recognized deferred tax assets related to such loss carryforwards for IFRS reporting purposes. In general, NOL carryforwards in Denmark do not expire. They are, however, subject to review and possible adjustment by the Danish tax authorities. Furthermore, under current Danish tax laws, certain substantial changes in our ownership structure and business may further limit the amount of NOL carryforwards that can be used annually to offset future taxable income, if any. In addition, we may in the future have United States federal and state NOL carryforwards in the United States, and in other jurisdictions where we maintain a subsidiary.

We may not be able to utilize a material portion of our NOLs or credits in either Denmark, the United States, or other jurisdictions where we maintain a subsidiary or otherwise engage in business. In addition, the rules regarding the timing of revenue and expense recognition for tax purposes in connection with various transactions are complex and uncertain in many respects, and our recognition could be subject to challenge by taxing authorities. In the event any such challenge is sustained, our NOLs could be materially reduced or we could be determined to be a material cash taxpayer for one or more years. Furthermore, our ability to use our NOLs or credits is conditioned upon our attaining profitability and generating taxable income. As described above, we have incurred significant net losses since our inception and anticipate that we will continue to incur significant losses for the foreseeable future. We do not know whether or when we will generate the taxable income necessary to utilize our NOL or credit carryforwards.

We will need substantial additional financing to achieve our goals, which may not be available on acceptable terms, or at all. Failure to obtain this necessary capital could force us to delay, limit, reduce or terminate our product development programs, commercialization efforts or other operations.

We will need to develop our company, and we may encounter difficulties in managing this development, which could disrupt our operations.

As of December 31, 2023, we had 49 full-time equivalent employees and, in connection with the development and advancement of our pipeline, partnerships and becoming a public company, we expect to keep developing our operations. To manage our anticipated development, we must continue to implement and improve our managerial, operational, legal, compliance and financial systems, and retain as well as recruit and train additional qualified personnel. Also, our management may need to divert a disproportionate amount of its attention away from its day-to-day activities and devote a substantial amount of time to managing these development activities.

As a developing TechBio company, we are actively pursuing technologies, drug classes, platforms, and product candidates in more therapeutic areas and across a wide range of diseases. Successfully developing product candidates for and fully understanding the regulatory and manufacturing pathways to all of these therapeutic areas and disease states requires significant human capital resources with a depth of talent, and corporate processes in order to allow simultaneous execution across multiple areas. Due to our limited resources, we may not be able to effectively manage this simultaneous execution and the development of our operations or recruit and train additional qualified personnel. This may result in weaknesses in our infrastructure, give rise to operational mistakes, legal or regulatory compliance failures, loss of business opportunities, loss of employees and reduced productivity among remaining employees.

13

In addition, the commitments resulting from being Nasdaq listed and low liquidity in the capital markets may lead to significant costs and may divert financial resources from other projects, such as the development of our product candidates. If our management is unable to effectively manage our expected development, our expenses may increase more than expected, our ability to generate or increase our revenue could be reduced and we may not be able to implement our business strategy. Our future financial performance and our ability to compete effectively and develop our product candidates will depend in part on our ability to effectively manage the future development of our company.

We have identified a material weakness in our internal control over financial reporting. If we are unable to remediate the material weakness, or if we experience additional material weaknesses in the future, we may not be able to accurately or timely report our financial condition or results of operations and investors may lose confidence in our financial reports and the market price of the ADSs could be adversely affected.

As a public company, we are required to maintain internal control over financial reporting. Section 404 of the Sarbanes-Oxley Act requires that we evaluate and determine the effectiveness of our internal control over financial reporting and provide a management report on internal control over financial reporting. The Sarbanes-Oxley Act also requires that our management report on internal control over financial reporting be attested to by our independent registered public accounting firm, to the extent we are no longer an “emerging growth company,” as defined by the JOBS Act. We do not expect to have our independent registered public accounting firm attest to our management report on internal control over financial reporting for so long as we are an emerging growth company.

Our management assessed the effectiveness of our internal control over financial reporting as of December 31, 2023. In making this assessment, it used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission (COSO 2013) in the Internal Control-Integrated Framework. Based on its assessment and those criteria, our management identified the material weakness listed below in our internal control over financial reporting and therefore determined that our internal control over financial reporting was not effective at the reasonable assurance level as of December 31, 2023.

As defined in the standards established by the U.S. Public Company Accounting Oversight Board, a “material weakness” is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our company’s annual or interim consolidated financial statements will not be prevented or detected on a timely basis.

We have in 2023 implemented and documented a SOX program including a description of controls to monitor and provide oversight over the design and operating effectiveness of internal control over financial reporting in order to comply with the requirements of Section 404 of the Sarbanes-Oxley Act. This includes elements of the COSO framework such as a documented control environment, information and communication, control activities and monitoring of control activities.

We have in 2023 hired replacements for the key employees we lost in 2022. However, the impacts from newly hired personnel, resulted in deficiencies of the documentation and review of controls due to a lack of knowledge of the required documentation. We have assessed that we lacked sufficient internal controls to support effective financial reporting as of December 31, 2023, which constitutes a material weakness.

As a result of the identified material weakness, we will continue to invest in upgrading the risk culture and understanding of internal control requirements through comprehensive training to both dedicated resources that assist in driving internal controls and control owners and control performers across different functions to strengthen control execution, control documentation, and control monitoring.

While we have implemented and intend to continue implementing our plans to remediate these material weaknesses, we cannot predict the success of such plans or if they will result in remediation of these material weaknesses or that additional material weaknesses will not be identified in the future. If we are unable to remediate these material weaknesses or if we experience additional material weaknesses in the future or otherwise continue to fail in maintaining an effective system of internal controls, we may not be able to accurately or timely report our financial condition or results of operations. Our investors may lose confidence in the accuracy and completeness of our financial reports, the market price of the ADSs could be adversely affected, and we could become subject to investigations by the stock exchange on which our securities are listed, the SEC, or other regulatory authorities, which could require additional financial and management resources.

14

Our insurance policies are expensive and protect us only from some business risks, which leaves us exposed to significant uninsured liabilities.

We do not carry insurance for all categories of risk that our business may encounter. We do not know if we will be able to maintain existing insurance with adequate levels of coverage, and any liability insurance coverage we acquire in the future may not be sufficient to reimburse us for any expenses or losses we may suffer. If our future partners, if any, obtain marketing approval for any product candidates that we or our future partners, if any, may develop, we intend to acquire insurance coverage to include the sale of commercial products, but we may be unable to obtain such insurance on commercially reasonable terms or in adequate amounts, if at all. If our losses exceed our insurance coverage, our financial condition would be adversely affected. In the event of contamination or injury, we could be held liable for damages or be penalized with fines in an amount exceeding our resources. Clinical trials or regulatory approvals for any of our product candidates could be suspended, which could adversely affect our results of operations and business, including by preventing or limiting the development and commercialization of any product candidates that we or our future partners, if any, may develop. Operating as a public company makes it more expensive for us to obtain director and officer liability insurance, and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified individuals to serve on our Board, our board committees or our management team.

Adverse developments affecting financial institutions, companies in the financial services industry or the financial services industry generally, such as actual events or concerns involving liquidity, defaults or non-performance, could adversely affect our operations and liquidity.

Actual events involving limited liquidity, defaults, non-performance or other adverse developments that affect financial institutions or other companies in the financial services industry or the financial services industry generally, or concerns or rumors about any events of these kinds, have in the past and may in the future lead to market-wide liquidity problems. For example, on March 10, 2023, Silicon Valley Bank, or SVB, was closed by the California Department of Financial Protection and Innovation, which appointed the Federal Deposit Insurance Corporation, or the FDIC, as receiver.

While a statement by the U.S. Department of the Treasury, the Federal Reserve and the FDIC stated that all depositors of SVB would have access to all of their money, uncertainty and liquidity concerns in the broader financial services industry remain. Inflation and rapid increases in interest rates have led to a decline in the trading value of previously issued government securities with interest rates below current market interest rates. The U.S. Department of Treasury, FDIC and Federal Reserve Board have announced a program to provide up to $25 billion of loans to financial institutions secured by such government securities held by financial institutions to mitigate the risk of potential losses on the sale of such instruments. However, widespread demands for customer withdrawals or other needs of financial institutions for immediate liquidity may exceed the capacity of such program. There is no guarantee that the U.S. Department of Treasury, FDIC and Federal Reserve Board will provide access to uninsured funds in the future in the event of the closure of other banks or financial institutions in a timely fashion or at all.

While we maintain our cash and cash equivalents in multiple financial institutions worldwide, our access to our cash and cash equivalents in amounts adequate to finance our operations could be significantly impaired by the financial institutions with which we have arrangements directly facing liquidity constraints or failures. In addition, investor concerns regarding the U.S. or international financial systems could result in less favorable commercial financing terms, including higher interest rates or costs and tighter financial and operating covenants, or systemic limitations on access to credit and liquidity sources, thereby making it more difficult for us to acquire financing on acceptable terms or at all. Any material decline in available funding or our ability to access our cash and cash equivalents could adversely impact our ability to meet our operating expenses, result in breaches of our contractual obligations or result in violations of federal or state wage and hour laws, any of which could have material adverse impacts on our operations and liquidity.

15

Inflation could adversely affect our business and results of operations.

While inflation in the United States has been relatively low in recent years, from 2021 to 2023, the economy in the United States encountered a material level of inflation. The impact of COVID-19, geopolitical developments such as the Russia-Ukraine and Middle East conflicts and global supply chain disruptions continue to increase uncertainty in the outlook of near-term and long-term economic activity, including whether inflation will continue and how long, and at what rate. Increases in inflation raise our costs for commodities, labor, materials and services and other costs required to grow and operate our business, and failure to secure these on reasonable terms may adversely impact our financial condition. Additionally, increases in inflation, along with the uncertainties surrounding COVID-19, geopolitical developments, and global supply chain disruptions, have caused, and may in the future cause, global economic uncertainty and uncertainty about the interest rate environment, which may make it more difficult, costly or dilutive for us to secure additional financing. A failure to adequately respond to these risks could have a material adverse impact on our financial condition, results of operations or cash flows.

Risks Related to our Business and Industry

Our AI approach to the discovery of product candidates is novel and unproven, and we do not know whether we or our future partners, if any, will be able to develop any products of commercial value. If we or our future partners, if any, are unable to advance our product candidates in clinical development, obtain regulatory approval and ultimately commercialize our product candidates, or experience significant delays in doing so, our business will be materially harmed.

We are leveraging our AI-Immunology™ platform to create a pipeline of vaccine candidates for cancer treatment and for preventing bacterial and viral infectious for patients whose diseases have not been adequately addressed to date by other approaches, and, together with our partners, if any, to design and conduct efficient clinical trials with a potentially greater likelihood of success. We will also aim at out-licensing identified targets or product candidates earlier in the development process as well as partner on target discovery. While we believe that applying our AI-Immunology™ platform to create medicines for defined patient populations may potentially enable drug discovery research that is more efficient than conventional drug research, our approach is both novel and unproven and, therefore, the cost and time needed to develop our product candidates either by us or our future partners, if any, is difficult to predict. Our efforts may not result in the discovery and development of commercially viable medicines. We may also be incorrect about the effects of our product candidates on the diseases of our targeted patient populations, which may limit the utility of our approach or the perception of the utility of our approach. Furthermore, our defined patient populations available for study and treatment may be lower than expected, which could adversely affect our, or our partners, ability to conduct clinical trials and may also adversely affect the size of any market for medicines we, or our partners, may successfully commercialize. Our approach may not result in clinical effect, time savings, higher success rates or reduced costs as we expect and, if not, we may not attract future partners, if any, or develop new drug candidates as quickly or cost effectively as expected and therefore our future partners, if any, may not be able to commercialize our approach as originally expected.

Our AI approach may fail to help us discover and develop additional product candidates, which could materially harm our business, financial condition, results of operations and prospects.

Any drug discovery that we are conducting using our AI platform technologies may not be successful in identifying compounds that have commercial value or therapeutic utility. Our AI platform technologies may initially show promise in identifying potential product candidates, yet fail to yield viable product candidates for clinical development or commercialization for a number of reasons, including:

| ● | we may not be successful in our efforts to identify new product candidates as well as in securing partnerships for these. If we are unable to identify suitable additional compounds attractive to partners for pre-clinical and clinical development, our ability to develop product candidates and generate revenue in future periods could be compromised, which could result in significant harm to our financial position and adversely impact the market price of the ADSs; |

| ● | compounds found through our AI-Immunology™ platform may not demonstrate efficacy, safety or tolerability; |

| ● | potential product candidates may, on further study, be shown to have harmful side effects or other characteristics that indicate that they are unlikely to receive marketing approval and achieve market acceptance; |

| ● | competitors may develop alternative therapies that render our potential product candidates non-competitive or less attractive; |

16

| ● | a product candidate may not be capable of being manufactured at an acceptable cost and speed; or |

| ● | we may not be able to scale up manufacturing of personalized therapies to a commercial scale. |

We may experience challenges with the acquisition, development, enhancement or deployment of technology necessary for our AI-Immunology™ platform.

Our business requires sophisticated computer systems and software. Some of the technologies are changing rapidly and we must continue to adapt to these changes in a timely and effective manner at an acceptable cost. There can be no guarantee that we will be able to develop, acquire, enhance, deploy, or integrate new technologies, that these new technologies will meet our needs or achieve our expected goals, or that we will be able to do so as quickly or cost-effectively as our competitors. Significant technological change could render our AI-Immunology™ platform obsolete. Our continued success will depend on our ability to adapt to changing technologies, manage and process ever-increasing amounts of data and information and improve the performance features of our AI-Immunology™ platform in response to an ever- changing patient population. We may experience difficulties that could delay or prevent the successful design, development, testing, and introduction of advanced versions of our AI-Immunology™ platform, limiting our ability to identify new product candidates. Any of these failures could have a material adverse effect on our operating results and financial condition.

Our product candidates may not work as intended, may cause undesirable side effects or may have other properties that could delay or prevent their regulatory approval, limit the commercial profile of an approved label, or result in significant negative consequences following marketing approval, if any, which could materially harm our business, financial condition, results of operations and prospects.

As with most biological and vaccine products, use of our product candidates could be associated with side effects or adverse events which can vary in severity from minor reactions to death and in frequency from infrequent to prevalent. The potential for adverse events is especially acute in the oncology setting, where patients may have advanced disease, have compromised immune and other systems and be receiving numerous other therapies. Undesirable side effects or unacceptable toxicities caused by our product candidates could cause us, our future partners, if any, or regulatory authorities to interrupt, delay or halt clinical trials and could result in a more restrictive label or the delay or denial of regulatory approval by the FDA, the EMA, the TGA or comparable regulatory authorities. Results of clinical trials of our product candidates could reveal a high and unacceptable severity and prevalence of side effects.

If unacceptable side effects arise in the development of our product candidates, we, our future partners, if any, the FDA, the EMA, the TGA, competent authorities of the European Union member states, ethics committees, the institutional review boards, or IRBs, at the institutions in which clinical trials of our product candidates are conducted, or a Data Safety Monitoring Board, or DSMB, could suspend or terminate our clinical trials. The FDA, the EMA, the TGA or comparable regulatory authorities could also order us or our future partners, if any, to cease clinical trials or deny approval of our product candidates for any or all targeted indications. Treatment-related side effects could also affect patient recruitment or the ability of enrolled patients to complete any of our or our partners’ clinical trials or result in potential product liability claims. In addition, these side effects may not be appropriately recognized or managed by the treating medical staff. We expect that we or our future partners, if any, may have to train medical personnel using our product candidates to understand the side effect profiles for our clinical trials and upon any commercialization of any of our product candidates. Inadequate training in recognizing or managing the potential side effects of our product candidates could result in patient injury or death. Any of these occurrences may materially harm our business, financial condition, results of operations and prospects.

17

Monitoring the safety of patients receiving our product candidates is challenging, which could adversely affect our and our partners’ ability to obtain regulatory approval and commercialize our product candidates.

In our ongoing and planned clinical trials, we have contracted with and are expected to continue to contract with academic medical centers and hospitals experienced in the assessment and management of toxicities arising during clinical trials. Nonetheless, these centers and hospitals may have difficulty observing patients and treating toxicities, which may be more challenging due to personnel changes, inexperience, shift changes, house staff coverage or related issues. This could lead to more severe or prolonged toxicities or even patient deaths, which could result in us, our future partners, if any, or the FDA, EMA, TGA or other comparable regulatory authority delaying, suspending or terminating one or more of our clinical trials, and which could jeopardize regulatory approval. We also expect the centers using our product candidates, if approved, on a commercial basis could have similar difficulty in managing adverse events. Medicines used at centers to help manage adverse side effects of our product candidates may not adequately control the side effects and may have a detrimental impact on the treatment. Use of these medicines may increase with new physicians and centers administering our product candidates.

In addition, even if our future partners, if any, successfully advance one or more of our product candidates into and through late stage clinical trials, such trials will likely only include a limited number of subjects and limited duration of exposure to our product candidates. As a result, we cannot be assured that adverse effects of our product candidates will not be discovered when a significantly larger number of patients are exposed to the product candidate. Further, any clinical trials may not be sufficient to determine the effect and safety consequences of taking our product candidates over a multi-year period.

If any of our product candidates were to receive marketing approval and we, our future partners, if any, or others later identify undesirable side effects caused by such products, a number of potentially significant negative consequences could result, including:

| ● | regulatory authorities may withdraw their approval of products derived from one or more of our product candidates; |

| ● | our future partners, if any, may be required to recall products derived from one or more of our product candidates or change the way such products are administered to patients; |

| ● | additional restrictions may be imposed on the marketing of the products derived from one or more of our product candidates or the manufacturing processes for such products or any component thereof; |

| ● | regulatory authorities may require the addition of labeling statements, such as a “black box” warning or a contraindication; |

| ● | our future partners, if any, may be required to implement a Risk Evaluation and Mitigation Strategy, or REMS, or create a Medication Guide outlining the risks of such side effects for distribution to patients; |

| ● | we or our future partners, if any, could be sued and held liable for harm caused to patients; |

| ● | the products derived from one or more of our product candidates may become less competitive; and |

| ● | our reputation may suffer. |

Any of the foregoing events could prevent our future partners, if any, from achieving or maintaining market acceptance of the particular product candidate, even if approved, and result in the loss of significant revenues to us, which would materially and adversely affect our results of operations and business. In addition, if one or more of our product candidates generally prove to be unsafe, our AI platform technologies and product pipeline could be affected, which would have a material adverse effect on our business, financial condition, results of operations and prospects.

18

Pre-clinical development, including the timeline from target identification to clinical development, is uncertain. Our pre-clinical programs may experience delays or may never advance to clinical trials, which would adversely affect our partners’ ability to obtain regulatory approvals or commercialize these programs on a timely basis or at all and would have an adverse effect on our business, financial condition, results of operations and prospects.