As filed with the Securities and Exchange Commission on April 23, 2024

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31 , 2023

Commission file number 001-35934

Fomento Económico Mexicano, S.A.B. de C.V.

(Exact name of registrant as specified in its charter)

(Translation of registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

(Name, telephone, email and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class: | Trading Symbols: | Name of each exchange on which registered: | ||||||||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

BD Units, each consisting of one Series B Share, two Series D-B Shares and two Series D-L Shares, without par value. The BD Units represent a total of 2,160,796,470 Series B Shares, 4,321,592,940 Series D-B Shares and 4,321,592,940 Series D-L Shares. | ||||||||

| B Units, each consisting of five Series B Shares without par value. The B Units represent a total of 7,085,242,500 Series B Shares. | ||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ | ☐ No | ||||

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes | ☒ | ||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be file by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

☒ | ☐ No | ||||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ | ☐ No | ||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated Filer ☐ | |||||

Non-accelerated Filer ☐ | |||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☒ | ☐ No | ||||

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check market whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ | Other ☐ | |||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 | ☐ Item 18 | ||||

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes | ☒ | ||||

TABLE OF CONTENTS

Corporate History and Information | |||||||||||

25 | |||||||||||

37 | |||||||||||

55 | |||||||||||

i

ii

iii

INTRODUCTION

References

The terms “FEMSA,” “our company,” “the Group,” “we,” “us” and “our” are used in this annual report to refer to Fomento Económico Mexicano, S.A.B. de C.V. and, except where the context otherwise requires, its subsidiaries on a consolidated basis. We refer to our subsidiary Coca-Cola FEMSA, S.A.B. de C.V. as “Coca-Cola FEMSA” and to our subsidiary FEMSA Comercio, S.A. de C.V. as “FEMSA Comercio.” FEMSA Comercio is a holding company that directly and indirectly owns our operating subsidiaries that make up the “Proximity Americas Division, “Fuel Division” and “Health Division.” The “Proximity Europe Division” refers to the small-format retail and foodvenience chains in Europe operated by Valora. The term “Digital@FEMSA” refers to our digital and financial ecosystem business.

The term “S.A.B.” stands for sociedad anónima bursátil, which is the term used in the United Mexican States (“Mexico”) to denominate a publicly traded company under the Mexican Exchange Market Law (Ley del Mercado de Valores or “Mexican Exchange Market Law”).

“U.S. dollars,” “US$,” “dollars” or “$” refer to the lawful currency of the United States of America (“United States”). “Mexican pesos,” “pesos” or “Ps.” refer to the lawful currency of Mexico. “Euros” or “€” refer to the lawful currency of the European Economic and Monetary Union (the “Euro Zone”).

As used in this annual report, “sparkling beverages” refers to non-alcoholic carbonated beverages. “Still beverages” refers to non-alcoholic non-carbonated beverages. “Waters” refers to flavored and non-flavored waters, whether or not carbonated.

Currency Translations and Estimates

This annual report contains translations of certain Mexican peso amounts into U.S. dollars at specified rates solely for the convenience of the reader. These translations should not be construed as representations that the Mexican peso amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the rate indicated. Unless otherwise indicated, such U.S. dollar amounts have been translated from Mexican pesos at an exchange rate of Ps. 16.8998 to US$ 1.00, the noon buying rate for Mexican pesos on December 31, 2023, as published by the U.S. Federal Reserve Board in its H.10 Weekly Release of Foreign Exchange Rates. On April 19, 2024, this exchange rate was Ps. 17.2062 to US$ 1.00.

To the extent estimates are contained in this annual report, we believe that such estimates, which are based on internal data, are reliable. Amounts in this annual report are rounded, and the totals may therefore not precisely equal the sum of the numbers presented.

Per capita growth rates, consumer price indices and population data have been taken from statistics prepared by the National Institute of Statistics, Geography and Information of Mexico (Instituto Nacional de Estadística, Geografía e Informática or “INEGI”), the U.S. Federal Reserve Board and the Mexican Central Bank (Banco de México), local entities in each country where we have operations and upon our estimates.

Forward-Looking Information

This annual report contains words such as “believe,” “expect,” “anticipate” and similar expressions that identify forward-looking statements. Use of these words reflects our views about future events and financial performance. Actual results could differ materially from those projected in these forward-looking statements as a result of various factors that may be beyond our control, including, but not limited to, effects on our company from changes in our relationship with or among our affiliated companies, fluctuation in the prices of raw materials, effects on our company’s points of sale performances from changes in economic conditions, changes or interruptions in our information technology systems, effects on our company from changes to our various suppliers’ business and demands, competition, significant developments in the countries where we operate, our ability to successfully complete or integrate mergers and acquisitions, including those we have completed in recent years and any current or future strategic projects (including the sale of certain of our subsidiaries), our ability to fund our capital expenditures, international economic, social, political or environmental conditions, health epidemics, pandemics and similar outbreaks including future outbreak of diseases and their effect on customer behavior and on economic, political, social and other conditions in the countries where we have operations and globally, and other facts described in “Item 3. Key Information—Risk Factors.” Accordingly, we caution readers not to place undue reliance on these forward-looking statements. In any event, these statements speak only as of their respective dates, and we undertake no obligation to update or revise any of them, whether as a result of new information, future events or otherwise.

1

ITEMS 1-2. NOT APPLICABLE

ITEM 3. KEY INFORMATION

The selected financial information should be read in conjunction with, and is qualified in its entirety by reference to, the Consolidated Financial Statements, including the notes thereto appearing elsewhere in this annual report. The selected financial information as of December 31, 2023 and 2022 and for the years ended December 31, 2023, 2022 and 2021 is derived from the consolidated statements of financial position, consolidated income statements and other comprehensive income, included in the Consolidated Financial Statements appearing elsewhere in this Annual Report. See “Item 5. Operating and Financial Review Prospectus.”

This annual report includes (under Item 18) our audited consolidated statements of financial position as of December 31, 2023 and 2022, and the related consolidated income statements, consolidated statements of comprehensive income, changes in equity and cash flows for the years ended December 31, 2023, 2022 and 2021. Our audited consolidated financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

This annual report presents financial information for 2023, 2022 and 2021 in nominal terms in Mexican pesos, taking into account local inflation of any hyperinflationary economic environment pursuant to IFRS. Our non-Mexican subsidiaries maintain their accounting records in their local currency and in accordance with accounting principles generally accepted in the country where they are located. For presentation in our consolidated financial statements, we adjust these accounting records into IFRS and report in Mexican pesos under these standards.

In the case of Argentina, the economy meets the criteria under IFRS to be treated as a hyperinflationary economy based on various economic factors, including that Argentina’s cumulative inflation over the three-year period prior to December 31, 2023 exceeded 100%, according to available indexes in the country. We therefore adjust the financial information of our Argentine operations to recognize inflationary effects. Our functional currency in Argentina was converted to Mexican pesos for the periods ended December 31, 2023, 2022 and 2021 using the exchange rates at the end of such periods. See Note 3.4 to our audited consolidated financial statements.

As previously announced in February 2023, certain of our non-core operations are classified as discontinued operations for all years presented in the consolidated financial information included in this annual report. See Note 4.3 to our audited consolidated financial statements.

In 2023, as part of our FEMSA Forward strategy, we sold 13.9% of outstanding ordinary shares of Heineken N.V. and Heineken Holding N.V. (collectively, “Heineken”), retaining less than 1% of outstanding ordinary shares of Heineken. See "Item 4—Strategic Development of our Business.” In February 2023, we discontinued the use of the equity method of accounting for Heineken. As a result, in accordance with IFRS 5, Heineken’s operations are classified as discontinued operations for all years presented in the consolidated financial information included in this report. Accordingly, results for all years presented are presented in a single amount as discontinued operations in the consolidated financial information included in this annual report. Therefore, operating and financial information for all years presented herein related to Heineken are presented as discontinued operations. See Note 4.3 to our audited consolidated financial statements.

In October 2023, as part of our FEMSA Forward strategy, we merged Envoy Solutions, LLC (“Envoy Solutions”) with IFS Topco, LLC ("BradyIFS") and obtained an ownership stake of approximately 37% in the combined entity. See "Item 4—Strategic Development of our Business.” As a result, in accordance with IFRS 5, Envoy Solutions’ operations are classified as discontinued operations for all years presented in the consolidated financial information included in this report. Accordingly, results for all years presented are presented in a single amount as discontinued operations in the consolidated financial information included in this annual report. Therefore, operating and financial information presented herein related to Envoy Solutions are presented as discontinued operations, including for periods prior to the sale. See Note 4.3 to our audited consolidated financial statements.

Except when specifically indicated, information in this annual report is presented as of December 31, 2023 and does not give effect to any transaction, financial or otherwise, subsequent to that date. The financial information and results for the Proximity Europe Division for 2022 are included from the date of acquisition, for the last 23 days of October and the entirety of November and December 2022.

Dividends

We have historically declared annual dividends in respect each Series of Shares (including in the form of American Depositary Shares, or “ADSs”), subject to changes in our results and financial position, including due to extraordinary economic events and to the factors described in “Item 3. Key Information—Risk Factors” that affect our

2

financial condition and liquidity. These factors may affect whether or not dividends are declared and the amount of such dividends. We do not expect to be subject to any contractual restrictions on our ability to pay dividends, although our subsidiaries may be subject to such restrictions. Because we are a holding company with no significant operations of our own, we will have distributable profits and cash to pay dividends only to the extent that we receive dividends from our subsidiaries. Accordingly, we cannot assure you that we will pay dividends or as to the amount of any dividends.

The table below sets forth the nominal amount of dividends paid per share in Mexican pesos and translated into U.S. dollars and their respective payment dates for the 2021 to 2023 fiscal years. All dividends were rounded up to the nearest whole number of ordinary shares.

| Fiscal Year | Aggregate | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| with Respect to | Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| which Dividend | of Dividend | Per Series B Share | Per Series B Share | Per Series D Share | Per Series D Share | ||||||||||||||||||||||||||||||||||||||||||||||||

| Date Dividend Paid | was Declared | Declared | Dividend | Dividend(1) | Dividend | Dividend(1) | |||||||||||||||||||||||||||||||||||||||||||||||

| May 6, 2021 and November 5, 2021 | 2020 | Ps. | 7,686,624,026 | Ps. | 0.3833 | $ | 0.0189 | Ps. | 0.4792 | $ | 0.0236 | ||||||||||||||||||||||||||||||||||||||||||

| May 6, 2021 | Ps. | 0.1917 | $ | 0.0095 | Ps. | 0.2396 | $ | 0.0119 | |||||||||||||||||||||||||||||||||||||||||||||

| November 5, 2021 | Ps. | 0.1917 | $ | 0.0094 | Ps. | 0.2396 | $ | 0.0117 | |||||||||||||||||||||||||||||||||||||||||||||

| May 5, 2022 and November 7, 2022 | 2021 | Ps. | 11,358,251,673 | Ps. | 0.5660 | $ | 0.0285 | Ps. | 0.7085 | $ | 0.0357 | ||||||||||||||||||||||||||||||||||||||||||

| May 5, 2022 | Ps. | 0.2830 | $ | 0.0145 | Ps. | 0.3543 | $ | 0.0175 | |||||||||||||||||||||||||||||||||||||||||||||

| November 7, 2022 | Ps. | 0.2830 | $ | 0.0145 | Ps. | 0.3543 | $ | 0.0182 | |||||||||||||||||||||||||||||||||||||||||||||

May 8, 2023 and November 8, 2023 | 2022 | Ps. | 12,246,519,120 | Ps. | 0.6107 | $ | 0.0347 | Ps. | 0.7634 | $ | 0.0433 | ||||||||||||||||||||||||||||||||||||||||||

May 8, 2023 | 0.3054 | $ | 0.0172 | 0.3817 | $ | 0.0215 | |||||||||||||||||||||||||||||||||||||||||||||||

November 8, 2023 | 0.3054 | $ | 0.0175 | 0.3817 | $ | 0.0218 | |||||||||||||||||||||||||||||||||||||||||||||||

(1)Translations to U.S. dollars are based on the exchange rates on the dates the payments were made.

On March 22, 2024, during our annual ordinary general shareholders meeting ("AGM"), our shareholders approved a cash dividend to be paid in four installments on April 18, 2024, July 18, 2024, October 17, 2024 and January 16, 2025, each consisting of Ps. 0.183225 per each Series B Share outstanding on the corresponding payment date and Ps. 0.229025 per each Series D Share outstanding on the corresponding payment date, corresponding to Ps. 0.9161 per each FEMSA "B" unit outstanding on the corresponding payment date and Ps. 1.0993 per each FEMSA "BD" unit outstanding on the corresponding payment date. Additionally, on March 22, 2024, our shareholders approved an extraordinary cash dividend to be paid in four installments on April 18, 2024, July 18, 2024, October 17, 2024 and January 16, 2025, each consisting of Ps. 0.128350 per each Series B Share outstanding on the corresponding payment date and Ps. 0.1604250 per each Series D Share outstanding on the corresponding payment date, corresponding to Ps. 0.6418 per each FEMSA "B" unit outstanding on the corresponding payment date and Ps. 0.7701 per each FEMSA "BD" unit outstanding on the corresponding payment date.

Our shareholders approved our audited consolidated financial statements, together with a report by the board of directors, for the previous fiscal year at the AGM. Once the holders of Series B Shares have approved the audited consolidated financial statements, they determine the allocation of our net profits for the preceding year. Mexican law requires the allocation of at least 5% of net profits to a legal reserve, which is not subsequently available for distribution, until the amount of the legal reserve equals 20% of our paid in capital stock. As of the date of this annual report, the legal reserve of our company is fully constituted. Thereafter, the holders of Series B Shares may determine and allocate a certain percentage of net profits to any general or special reserve, including allocations for open-market purchases of our shares. On March 22, 2024, at the AGM, our shareholders approved an amount of Ps. 34,000 million that may only be used for share repurchases.The remainder of net profits is available for distribution in the form of dividends to our shareholders. Dividends may only be paid if net profits are enough to offset losses from prior fiscal years.

Our bylaws provide that dividends will be allocated among the outstanding and fully paid shares at the time a dividend is declared in such manner that each Series D-B Share and Series D-L Share receives 125% of the dividend distributed in respect of each Series B Share. Holders of Series D-B Shares and Series D-L Shares are entitled to this dividend premium in connection with all dividends paid by us other than payments in connection with the liquidation of our company. See "Item 10. Additional Information - Bylaws - Dividend Rights."

Subject to certain exceptions contained in the deposit agreement dated May 11, 2007, among FEMSA, The Bank of New York Mellon, as ADS depositary and holders and beneficial owners from time to time of our ADSs, evidenced by American Depositary Receipts (“ADRs”), any dividends distributed to holders of our ADSs will be paid to the ADS depositary in Mexican pesos and will be converted by the ADS depositary into U.S. dollars based on the conversion rate as of the date of payment. As a result, restrictions on the conversion of Mexican pesos into foreign

3

currencies may affect the ability of holders of our ADSs to receive U.S. dollars, and exchange rate fluctuations may affect the U.S. dollar amount received by holders of our ADSs. See "Item 10. Additional Information - Taxation - Mexican Taxation." For a description of taxation related to dividends.

Risk Factors

Risks Related to Our Company

Coca-Cola FEMSA’s business depends on its relationship with The Coca-Cola Company, and changes in this relationship may adversely affect Coca-Cola FEMSA’s business, financial condition and results of operations.

Substantially all of Coca-Cola FEMSA’s sales are derived from sales of Coca-Cola trademark beverages. Coca-Cola FEMSA produces, markets, sells and distributes Coca-Cola trademark beverages through standard bottler agreements in the territories where it operates, which we refer to as “Coca-Cola FEMSA’s territories.” Coca-Cola FEMSA is required to purchase concentrate for all Coca-Cola trademark beverages from affiliates of The Coca-Cola Company (“TCCC”), which price is determined from time to time by TCCC in all such territories. Coca-Cola FEMSA is also required to purchase sweeteners and other raw materials only from companies authorized by TCCC. Increases in the cost, disruption of supply or shortage of ingredients for concentrate could have an adverse effect on Coca-Cola FEMSA’s business. See “Item 4. Information on the Company—Coca-Cola FEMSA—Coca-Cola FEMSA’s Territories.”

In addition, under Coca-Cola FEMSA’s bottler agreements, it is prohibited from bottling or distributing any other beverages without TCCC’s authorization or consent, and it may not transfer control of the bottler rights of any of its territories without prior consent from TCCC.

TCCC makes significant contributions to Coca-Cola FEMSA’s marketing expenses, although it is not required to contribute a particular amount. Accordingly, TCCC may discontinue or reduce such contributions at any time.

Coca-Cola FEMSA depends on TCCC to continue with its bottler agreements. Coca-Cola FEMSA’s bottler agreements are automatically renewable for ten-year terms, subject to the right of either party to give prior notice that it does not wish to renew the applicable agreement. In addition, these agreements generally may be terminated in the case of material breach. See “Item 10. Additional Information—Material Contracts—Material Contracts Relating to Coca-Cola FEMSA—Bottler Agreements.” Termination of any such bottler agreement would prevent Coca-Cola FEMSA from selling Coca-Cola trademark beverages in the affected territory. The foregoing and any other adverse changes in Coca-Cola FEMSA’s relationship with TCCC would have an adverse effect on its business, financial condition and results of operations.

The Coca-Cola Company has substantial influence on the conduct of Coca-Cola FEMSA’s business, which may result in Coca-Cola FEMSA taking actions contrary to the interests of Coca-Cola FEMSA’s shareholders other than The Coca-Cola Company.

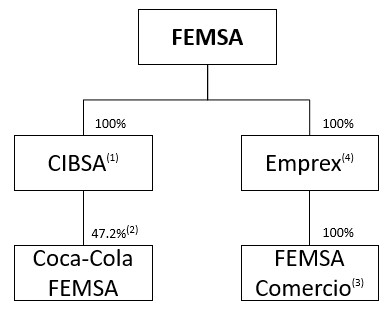

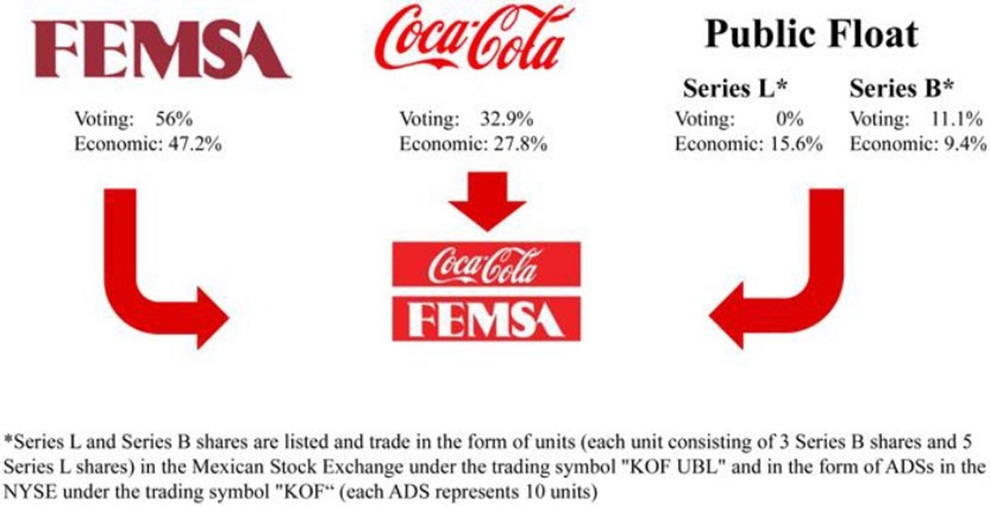

TCCC has substantial influence on the conduct of Coca-Cola FEMSA’s business. As of the date of this report, TCCC indirectly owned 27.8% of Coca-Cola FEMSA’s outstanding capital stock, representing 32.9% of Coca-Cola FEMSA’s capital stock with full voting rights. TCCC is entitled to appoint up to five of Coca-Cola FEMSA’s maximum of 21 directors and the vote of at least two of them is required to approve certain actions by Coca-Cola FEMSA’s board of directors. As of the date of this annual report, we indirectly owned 47.2% of Coca-Cola FEMSA’s outstanding capital stock, representing 56.0% of Coca-Cola FEMSA’s capital stock with full voting rights. We are entitled to appoint up to 13 of Coca-Cola FEMSA’s 21 directors and all of Coca-Cola FEMSA’s executive officers. TCCC and us, or only us in certain circumstances, have the power to determine the outcome of all actions requiring approval by Coca-Cola FEMSA’s board of directors, and TCCC and us, or only us in certain circumstances, have the power to determine the outcome of all actions requiring approval of our shareholders. See “Item 10. Additional Information—Material Contracts—Material Contracts Relating to Coca-Cola FEMSA—Shareholders Agreements.” The interests of TCCC may be different from the interests of Coca-Cola FEMSA’s other shareholders, which may result in Coca-Cola FEMSA taking actions contrary to the interests of such other shareholders.

Proximity Americas Division may not be able to maintain its historic growth rate.

Proximity Americas Division increased the number of OXXO stores at a compound annual growth rate of 5.8% from 2021 to 2023. The growth in the number of OXXO stores has driven growth in total revenue and results of operations at Proximity Americas Division over the same period. As the overall number of stores increases, percentage growth in the number of OXXO stores is likely to slow. In addition, as small-format store penetration in Mexico grows,

4

the number of viable new store locations may decrease, and new store locations may be less favorable in terms of same-store sales, average ticket, and store traffic. As a result, our future results and financial condition may not be consistent with prior periods and may be characterized by lower growth rates in terms of total revenue and results of operations. We cannot assure that the revenues and cash flows of Proximity Americas Division that come from future retail stores will be comparable with those generated by existing retail stores. See “Item 4. Information on the Company—Proximity Americas Division —Store Locations.”

The Health Division’s sales and performance may be affected by a material change in institutional sale trends in some of the markets where it has operations, and by contractual conditions with its suppliers.

In some of the markets where we have operations, the sales of the Health Division are highly dependent on institutional sales, as well as traditional, open-market sales. The institutional market involves public and private health care providers, and the performance of the Health Division could be affected by its ability to maintain and grow its client base.

Additionally, the Health Division acquires the majority of its inventories and healthcare products from a limited number of suppliers. Its ability to maintain favorable conditions in its current commercial agreements could potentially affect the Health Division’s operating and financial performance.

The Fuel Division’s performance may be affected by changes in commercial terms with suppliers, or disruptions to the industry supply chain, and the nature of the Fuel Division’s operations exposes it, and the communities in which it operates, to a range of health, safety, security and environmental risk.

The Fuel Division mainly purchases gasoline and diesel for its operations in Mexico. The fuel market in Mexico has experienced structural changes that could gradually decrease the number of suppliers. In the event of global changes in the industry, commercial terms for the Fuel Division could deteriorate in the future, adversely impacting the financial performance of the Fuel Division.

The nature of the Fuel Division’s operations exposes it to certain risks, particularly at its fuel stations. These risks include equipment failure, work accidents, fires, explosions, vapor emissions, spills and leaks at its facilities, service stations or other sites. These types of hazards and accidents may cause personal injuries or the loss of life, business interruptions and damage or contamination to the environment and the Fuel Division’s property, equipment or reputation. Further, we may be subject to litigation, compensation claims, governmental fines or penalties or other liabilities or losses in relation to such incidents and accidents and may incur significant costs as a result. Such incidents and accidents may also affect our reputation or our brands, leading to a decline in sales of our products and services, and may adversely impact our business, financial condition and results of operations.

Our business expansion strategy may not be successful and may lead to decreased profit margins.

In February 2023, we announced our FEMSA Forward strategy to focus on our core business units of retail, Coca-Cola FEMSA and Digital@FEMSA. See “Item 4. Information on the Company—Recent Developments.” In recent periods, we have entered into new markets and new lines of business through the acquisition of other businesses, and we continue to seek investment opportunities in our core businesses. These new businesses or investments may not result in the same growth rates that we have historically experienced, may experience long lead times before returns on our investment materialize or may be less profitable than our more established businesses.

Key elements to achieving the benefits and expected synergies of these acquisitions are the ability to implement our strategies for these acquisitions, the effectiveness of those strategies, the integration of acquired businesses’ operations into ours in a timely and effective manner, the funding of capital expenditures and the retention of qualified and experienced key personnel. Investments in Digital@FEMSA may also be subject to us selecting the right business to acquire or technology or platform to develop in a highly competitive and dynamic industry. We may incur in unforeseen liabilities in connection with acquiring, taking control of, or managing businesses and may encounter difficulties and unforeseen or additional costs in restructuring and integrating them into our operating structure. Past and future divestitures, such as the potential sale of certain non-core businesses, may lead to a decrease in our profits. We cannot assure you that these efforts will be successful or completed as expected, and our business, financial condition and results of operations could be adversely affected if we are unable to do so.

An erosion of our business reputation could have a material adverse effect on our brand, our ability to secure new resources and our business and results of operations.

Our reputation, trademarks and other proprietary rights are important to our competitive position. Coca-Cola FEMSA and OXXO stores, in particular, benefit from a well-recognized brand, and we are in the process of establishing our brands in Digital@FEMSA.

5

If we are unsuccessful in protecting our intellectual property rights, or if another party prevails in litigation claiming any rights thereto, the value of the brands could be diminished, causing customer confusion and materially adversely impacting our business and financial results. Failure to maintain product safety and quality could materially adversely affect our brand image and reputation and lead to potential product liability claims, governmental agency investigations and damages claims.

Substantially all of Coca-Cola FEMSA’s sales are derived from sales of Coca-Cola trademark beverages owned by TCCC. Maintenance of the reputation and intellectual property rights of these trademarks is essential to Coca-Cola FEMSA’s ability to attract and retain retailers and consumers and is a key driver for its success. Failure to maintain the reputation of Coca-Cola trademarks and/or to effectively protect these trademarks could have a material adverse effect on its business, financial condition and results of operations.

Societal expectations of businesses are also increasing, with a focus on business ethics, contribution to society, safety and minimizing damage to the environment, among others. Also, there is increasing focus on the role of oil and gas and large retail businesses in the context of climate change and energy transition. If we are unable to meet society demands in this regard, our brands, reputation and price of securities could be negatively affected, thus limiting our ability to deliver our strategy, reducing consumer demand for our products, harming our ability to secure new resources and contracts and restricting its ability to access capital markets or attract employees. Many other factors, including the materialization of the risks discussed in several of the other risk factors herein, could negatively affect our reputation and could have a material adverse effect on our business, financial condition and results of operations.

Our businesses highly depend on information technology and a failure, interruption or breach of our IT systems could adversely affect them.

Our businesses rely heavily on advanced IT systems to effectively manage our data, communications, connectivity and other business processes. We invest aggressively in IT to maximize its value generation potential. The development of IT systems, hardware and software needs to keep pace with the businesses’ growth due to the high speed at which the divisions add new services and products to their commercial offerings. If these systems become obsolete or if the planning for future IT investments is inadequate, our businesses could be adversely affected, so we constantly strive to improve and protect our IT systems with advanced security measures, including in Digital@FEMSA.

In order to address risks to our IT systems, we continue to make investments in training personnel, technologies and cyber insurance. We maintain an IT risk management program which is supervised by senior management. Reports on such IT risk management program are presented to the Audit Committee of the board of directors on a quarterly basis. As part of this program, we have a cybersecurity framework, internal policies and functional surveillance and governance.

Cybersecurity incidents, system disruptions and other breaches of network or information technology security could have an adverse effect on our business and our reputation.

We use networks and information systems to operate our business, to process financial information and results of operations for internal reporting purposes and to comply with regulatory financial reporting, legal and tax requirements. Some of these information systems include the Internet and third-party hosted platforms and services used for procurement, supply chain, manufacturing, invoicing and storing client and employee personal data. Because information systems are critical to many of our operating activities, our business and new acquisitions may be impacted by system shutdowns, service disruptions or security breaches, such as failures during routine operations, network or hardware failures, malicious or disruptive software, unintentional or malicious actions of employees or contractors, cyber-attacks by hackers, criminal groups or nation-state organizations or social-activist (hacktivist) organizations, natural disasters, failures or impairments of telecommunication networks or other catastrophic events. Such incidents could result in unauthorized disclosure of material confidential information, and we could experience delays in reporting our financial results. In addition, misuse, leakage or falsification of information could result in violations of data privacy laws and regulations, damage to our reputation and credibility, loss of customers, and, therefore, could have a material adverse effect on our financial condition and results, or may require us to spend significant financial and other resources to prevent future attacks, remedy the damage caused by a security breach or to repair or replace networks and information systems.

We have adopted comprehensive policies and procedures related to our information security and privacy controls that assess compliance on these matters, including the sufficiency of the controls and procedures related to cybersecurity disclosure, through our Chief Information Security Officer as an internal consultant for the Audit Committee and board of directors.

Proximity Americas Division and Digital@FEMSA offer several financial and payments services for their customers. Cyber-security events such as the ones described above could result in unauthorized disclosure of customers’ confidential information, violations of data privacy laws and regulations, or in the total or partial loss of our customers funds, that could therefore require us to spend significant financial and other resources to prevent future attacks, remedy

6

the damage caused by a security breach or to repair or replace networks and information systems. As we grow our digital business, we expect to hold more personal information of our customers. Therefore, we expect these risks to increase.

We make investments in technologies, cyber insurance and training of our personnel. We also maintain an information security program that is presented to and supervised by the Audit Committee and information security committee on a quarterly basis. As part of this information security program based on a risk approach, we have a cybersecurity framework, internal policies and cross-functional surveillance. Despite our investments and focus on risk management programs, we may be subject to unexpected security breaches, and there is no assurance that the measures we implement will be sufficient to prevent such breaches.

We are currently in the process of implementing internal protocols aimed at bolstering and standardizing disclosures pertaining to cybersecurity risk management, strategy, governance, and incidents. This endeavor is designed to enhance transparency, instill confidence among our clients and investors in our operational practices, and promote compliance with international cybersecurity standards and regulations, including applicable rules issued by the U.S. Securities and Exchange Commission (“SEC"). See "Item 16K. Cybersecurity." However, the evolving nature of cybersecurity threats presents an ongoing risk and despite our efforts, our systems may still be vulnerable to breaches or disruptions, which could adversely affect our operations and financial performance.

If we fail to comply with privacy and data protection laws, we could be subject to adverse publicity, business disruption, data loss, government enforcement actions and/or private litigation, any of which could negatively affect our business and operating results.

In the ordinary course of our business, we receive, process, transmit and store information relating to identifiable individuals (“personal data”), including employees, former employees, vendors, third-party personnel, customers, and consumers with whom we interact. As a result, we are subject to a variety of continuously evolving and developing laws and regulations in numerous jurisdictions regarding privacy and data protection, which may include different standards and obligations or may be interpreted and applied differently from jurisdiction to jurisdiction and may create inconsistent or conflicting requirements. Our security controls over personal data and the policies, procedures and practices we have implemented or may implement in the future may not prevent the improper disclosure of personal data by us or the third-party service providers and vendors whose technology, systems and services we use in connection with the receipt, storage and transmission of personal data.

Our distributors, joint venture partners and suppliers have privacy and security controls and policies over personal data that differ in scope and complexity from our policies, procedures and practices, and we may also experience secondary contractual, regulatory, financial and reputational harm as a result of improper disclosure of personal data. Unauthorized access to or improper disclosure of personal data in violation of privacy and data protection laws could harm our reputation, cause loss of consumer confidence, subject us to regulatory enforcement actions (including penalties, fines and investigations), and result in private litigation against us, which could result in loss of revenue, increased costs, liability for monetary damages and/or fines, all of which could negatively affect our business

and operating results. New and increased laws and regulations in this area, including self-regulation and industry standards, increased enforcement activity, and changes in interpretation of laws and regulations, could increase our cost of compliance and operation or otherwise harm our business.

Negative publicity or inaccurate information on social media could adversely affect our reputation.

In recent years, there has been a considerable increase in the use of social media and similar platforms, including weblogs (blogs), social media websites, and other forms of Internet-based communications that allow individual access to a broad audience of consumers and other interested persons. Consumers value readily available information concerning retailers, manufacturers and their goods and services, and often act on such information without further investigation, authentication and without regard to its accuracy. The availability of information on social media platforms and devices is virtually immediate as is its impact. Social media platforms and devices immediately publish the content their subscribers and participants post, often without filters or checks on accuracy of the content posted. The opportunity for dissemination of information, including inaccurate information, is virtually limitless.

Negative publicity or inaccurate information concerning or affecting us, or our brands’ trademarks may be posted at any time on traditional media outlets, social media and similar platforms, including weblogs (blogs), social media websites, and other forms of Internet-based communications which allow individual access to a broad audience of consumers and other interested persons. We may experience additional risks as we grow our Digital@FEMSA business.This information may harm our reputation without affording us an opportunity for redress or correction, which could in turn have a material adverse effect on its business, financial condition and results of operations.

7

Regulatory developments in the countries where we operate may adversely affect our business, financial condition and results of operations.

The principal areas in which we are subject to laws and regulations are labor, zoning, operations, environmental and related local permits, health and safety, anti-bribery, energy, taxation, antitrust, anti-money laundering, cybersecurity, among others. We are also subject to additional regulations applicable to payment providers and fintechs in the markets where we conduct those operations. See “Item 4. Information on the Company—Regulatory Matters—Fintech Regulations.” Changes in existing laws and regulations, the adoption of new laws or regulations, or a stricter interpretation or enforcement thereof in the countries where we have operations may increase our operating and compliance costs or impose restrictions on our operations which, in turn, may adversely affect our business, financial condition and results of operations. We may also be subject to overlapping and potentially conflicting regulations in multiple jurisdictions. In addition, changes in current laws and regulations may negatively impact customer traffic, revenues, operational costs and commercial practices, which may have an adverse effect on results of our operations and financial condition.

Our business could be affected by new safety and environmental regulations enforced by governments, global environmental regulations and new energy technologies. Federal, state, and municipal laws and regulations for the installation and operation of service stations are becoming more stringent. Compliance with these laws and regulations is often difficult and costly. Global trends to reduce the consumption of fossil fuels through incentives and taxes could push sales of these fuels at service stations to slow or decrease in the future and automotive technologies, including efficiency gains in fossil fuel vehicles and increased popularity of alternative fuel vehicles, such as electric and liquefied petroleum gas (“LPG”) vehicles, have caused a reduction in fuel consumption globally. Other new technologies could further reduce the sale of fossil fuels, all of which could adversely affect results of operations and financial condition of the Fuel Division. See “Item 4. Information on the Company—Regulatory Matters—Environmental Regulations.”

Consumers’ increased concerns and changing attitudes about the solid waste streams and environmental responsibility and the related publicity could result in the adoption of such legislation or regulations. If these types of requirements are adopted and implemented on a large scale in any of our territories, they could affect our costs or require changes in our distribution model and packaging, which could reduce net operating revenues and profitability. For example, certain legislative and regulatory reforms have been proposed in some of the territories where Coca-Cola FEMSA operates to restrict the sale of single-use plastics and similar legislation or regulations may be proposed or enacted in the future, which may affect Coca-Cola FEMSA’s use of non-refillable and refillable containers. Such changes in regulations might also affect FEMSA’s ability to meet the key performance indicators required by the sustainability-linked bond. See “Item 4. Information on the Company—Coca-Cola FEMSA—Raw Materials” and “Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources.”

Energy regulatory changes may impact fuel prices and therefore adversely affect our business. The Fuel Division mainly sells gasoline and diesel through owned or leased retail service stations. Previously, the prices of these products were regulated in Mexico by the Energy Regulatory Commission (Comisión Reguladora de Energía, or “CRE”). See “Item 4. Information on the Company—Regulatory Matters—Energy Regulations.”

We are required to comply with anti-money laundering laws and regulations in the jurisdictions in which we have operations, which are particularly applicable to our retail and fintech businesses. Such laws and regulations require FEMSA to adopt and implement policies, procedures and controls designed to detect and prevent transactions with third parties involved in money laundering. Although we have such policies, procedures and controls in place, given the number of transactions made in its stores, we may be subject to the risk that our clients or third parties may misuse our services and engage in money laundering or other related illegal activities. There can be no assurance that FEMSA’s internal policies, procedures and controls will be sufficient to detect or prevent all inappropriate practices, including money laundering, fraud or other violations of law or that any person will not take actions in violation of FEMSA policies, procedures and controls. As we expand and grow our retail and fintech businesses, including Digital@FEMSA, we will be subject to additional regulations applicable to financial technology companies in various jurisdictions. See “Item 4. Information on the Company—Regulatory Matters—Fintech Regulations.”

Voluntary price restraints or statutory price controls have been imposed historically in several of the countries where we operate. See “Item 4. Information on the Company—Regulatory Matters—Price Controls.” We cannot assure you that existing or future laws and regulations in the countries where we operate relating to goods and services (in particular, laws and regulations imposing statutory price controls) will not affect our products, our ability to set prices for our products, or that we will not need to implement price restraints, which could have a negative effect on our business, financial condition and results of operations.

Unfavorable outcome of legal proceedings could have an adverse effect on our business, financial condition, and results of operations.

Our operations and the operations of our business units have from time to time been and may continue to be subject to investigations and proceedings on antitrust, tax, consumer protection, environmental, labor and commercial

8

matters. We cannot assure you that these investigations and proceedings will not have an adverse effect on our business units’ business, financial condition, and results of operations. See “Item 8. Financial Information—Legal Proceedings.”

Taxes could adversely affect our business, financial condition and results of operations.

The imposition of new taxes, increases in existing taxes or changes in the interpretation of tax laws and regulations by tax authorities, may have a material adverse effect on the results of operations and financial condition of our business. The countries where we operate may adopt new tax laws or modify existing tax laws to increase taxes applicable to our business or products. See “Item 4. Information on the Company—Regulatory Matters—Tax Reforms.”

Changes in consumer preferences and public concern about health-related and environmental issues could reduce demand for some of Coca-Cola FEMSA’s products.

The beverage industry is evolving mainly because of changes in consumer preferences and regulatory actions. There have been different plans and actions adopted in recent years by governmental authorities in some of the countries where Coca-Cola FEMSA operates. These include increases in tax rates or the imposition of new taxes on the sale of certain beverages and other regulatory measures, such as restrictions on advertising for some of Coca-Cola FEMSA’s products and additional regulations concerning the labeling or sale of Coca-Cola FEMSA’s products. Moreover, researchers, health advocates and dietary guidelines encourage consumers to reduce their consumption of certain types of beverages sweetened with sugar, artificial sweeteners, and high fructose corn syrup (“HFCS”). In addition, concerns over the environmental impact of plastic may reduce the consumption of Coca-Cola FEMSA’s products sold in plastic bottles or result in additional taxes that could adversely affect consumer demand. Increasing public concern about these issues, new or increased taxes, other regulatory measures or Coca-Cola FEMSA’s failure to meet consumers’ preferences or its inability to successfully introduce new beverage products or replace plastic bottles with more environmentally friendly containers, could reduce demand for some of Coca-Cola FEMSA’s products, which would adversely affect its business, financial condition and results of operations. See “Item 4. Information on the Company—Coca-Cola FEMSA—Business Strategy.”

Competition in the markets where we have operations could adversely affect our business, financial condition and results of operations.

We face strong competition across industries in the countries where we have operations and may face competition from new market participants. The increase in competition may limit the number of new locations available or result in a reduction in revenues. Consequently, future competition may affect our results of operations and financial condition. The shift in the retail sector from brick-and-mortar retailers to online and mobile platforms could also adversely affect FEMSA’s business, results of operations and financial condition. See “Item 4. Information on the Company.” We expect the competitive environment will continue to evolve as new technologies are developed based on changing consumer behavior. Lower pricing and activities by FEMSA’s competitors may affect our business. The continuing migration and evolution of the retail sector and financial services to online and mobile-based platforms for consumers may increase competition that could adversely affect our business, results of operations and financial condition.

FEMSA competes mainly in terms of price, packaging, effective promotional activities, access to retail outlets and sufficient shelf space, customer service, product innovation and product alternatives and the ability to identify and satisfy consumer preferences. See “Item 4. Information on the Company”

Global economic conditions have and may continue to cause an increase in the prices of raw materials, supply chain disruptions or shortages of raw materials and thus increase our cost of goods sold, therefore adversely affecting our business, financial conditions and results of operations.

Our sales volumes and revenues may be affected by economic conditions in the various countries where we have operations. The prices for our raw materials are driven by market prices and local availability, the imposition of import duties and restrictions and fluctuations in exchange rates. Global economic growth slowed in 2022 and continued through 2023. Inflationary pressures first appeared in global markets in 2021 and reached a high point in 2022. Inflation has led to further increases in the costs of raw materials, utilities and services that we use to produce our products and provide services, which would adversely affect our business if we are not able to pass on the increased costs to our customers or successfully implement mitigating actions.

The effects of inflation impact each of our businesses differently. For example, in addition to water, Coca-Cola FEMSA’s most significant raw materials are concentrate, which Coca-Cola FEMSA acquires from affiliates of TCCC, sweeteners and packaging materials. Prices for Coca-Cola trademark beverages concentrate are determined by TCCC. Coca-Cola FEMSA is also required to meet all of its supply needs (including sweeteners and packaging materials) from suppliers approved by TCCC. Coca-Cola FEMSA’s most significant packaging raw material costs arise from the purchase of PET resin, the price of which is related to crude oil prices and global PET resin supply. Crude oil prices have

9

a cyclical behavior and are determined with reference to the U.S. dollar; therefore, high currency volatility and inflation may affect the average price for PET resin in local currencies. Coca-Cola FEMSA cannot anticipate whether the U.S. dollar will appreciate or depreciate with respect to such local currencies in the future, and we cannot assure you that Coca-Cola FEMSA will be successful in mitigating any such fluctuations through derivative instruments or otherwise. See “Item 4. Information on the Company—Coca-Cola FEMSA—Raw Materials.”

For Proximity Americas Division and Proximity Europe Division, price variations of raw materials and supply chain disruptions caused by inflation may increase the cost of the goods sold.

Water shortages or any failure to maintain existing concessions or contracts could adversely affect Coca-Cola FEMSA’s business, financial condition, and results of operations.

Water is an essential component of all of Coca-Cola FEMSA’s products. Coca-Cola FEMSA obtains water from various sources in its territories, including springs, wells, rivers and municipal and state water companies pursuant to either concessions granted by governments in its various territories (including governments at the federal, state or municipal level) or pursuant to contracts.

Coca-Cola FEMSA obtains the vast majority of the water used in its production from municipal utility companies and pursuant to concessions to use wells, which are generally granted based on studies of the existing and projected groundwater supply. Coca-Cola FEMSA’s existing water concessions or contracts to obtain water may be terminated by governmental authorities under certain circumstances and their renewal depends on several factors, including having paid all fees in full, having complied with applicable laws and obligations and receiving approval for renewal from local and/or federal water authorities. Climate change is causing a rise in temperatures in diverse territories and, as a result, is exacerbating water scarcity and droughts. In some of Coca-Cola FEMSA’s territories, its existing water supply may not be sufficient to meet its future production needs, and the available water supply may be adversely affected by shortages or changes in governmental regulations and environmental changes.

We cannot assure that water will be available in sufficient quantities to meet Coca-Cola FEMSA’s future production needs or will prove sufficient to meet its water supply needs. Continued water scarcity in the regions where Coca-Cola FEMSA operates may adversely affect its business, financial condition and results of operations.

Increases in the cost, disruption of supply or shortage of energy or fuel could adversely affect our business and results of operations.

Our business depends heavily on energy and fuel to maintain operations across segments.

An increase in the price, disruption of supply or shortage of fuel and other energy sources in the countries where we operate, which may be caused by increased demand, natural disasters, power outages or government regulations, taxes, policies or programs, including programs designed to reduce greenhouse gas emissions to address climate change, could increase our operating costs and negatively impact our business and results of operations. Changes in government regulations in the countries where we have operations, including reforms related to transmission, sanctions, distribution, and other costs, could lead to a substantial increase in our electricity cost. See “Item 4. Information on the Company—Regulatory Matters.” The price of fuel has also increased not only as a result of inflation and increases in energy demand, but also as a result of the conflict in Ukraine and Russia and subsequent economic sanctions imposed on Russia, which may continue to impact us throughout 2024, particularly in Europe, and may continue to impact us in the future.

Coca-Cola FEMSA’s bottling operations operate large fleets of trucks and other motor vehicles to distribute and deliver beverage products to its business partners and customers. In addition, Coca-Cola FEMSA uses a significant amount of electricity, natural gas and other energy sources to operate its bottling plants and distribution facilities. An increase in the price, disruption of supply or shortage of fuel and other energy sources in the countries where Coca-Cola FEMSA operates, which may be caused by increased demand, natural disasters, power outages or government regulations, taxes, policies or programs, including programs designed to reduce greenhouse gas emissions to address climate change, could increase our operating costs and negatively impact Coca-Cola FEMSA’s business and results of operations.

The performance of FEMSA’s points of sale would be adversely affected by increases in the price of utilities on which the stores and stations depend, such as electricity. Electricity prices could potentially increase further as a result of inflation, shortages, interruptions in supply, changes in the regulatory framework and its interpretation or other reasons, and such an increase could adversely affect the results of operations and financial condition of our business.

10

We are subject to risks related to pandemics and public health crises that may materially and adversely affect our business.

Public health crises such as pandemics, tainted food, food-borne illnesses, food tampering, tampering with or failure of water supply may negatively affect our business, and demand for our products and services. We cannot predict whether there will be future pandemic outbreaks in the future in any of the markets where we operate. A global pandemic could also impact our non-consolidated entities and cause significant volatility in financial markets, undermining investors’ confidence in the growth of countries and businesses. In addition, the longer-term economic effects of a global pandemic may include increased inflation rates, supply-chain disruptions, exchange rates volatility in the countries where we have operations and reduced demand for the products we sell or a shift to lower margin products. These lingering effects could be exacerbated by any additional pandemics or health crises.

Climate change and legal or regulatory responses thereto may have an adverse impact on our business.

There is increasing concern that a gradual rise of global average temperatures due to increased concentration of carbon dioxide and other greenhouse gases in the atmosphere will cause significant changes in weather patterns around the globe and an increase in the frequency and severity of natural disasters. Decreased agricultural productivity in certain regions of the world as a result of changing weather patterns may limit the availability or increase the cost of key agricultural commodities, such as sugarcane, and corn, which are important sources of ingredients for Coca-Cola FEMSA’s products. Increasing concern over climate change also may result in additional legal or regulatory requirements designed to reduce or mitigate the effects of carbon dioxide and other greenhouse gas emissions on the environment. Increased energy or compliance costs and expenses due to increased legal or regulatory requirements may cause disruptions in, or an increase in the costs associated with, the manufacturing and distribution of Coca-Cola FEMSA’s beverage products. Initiatives to address climate change may be aimed at discouraging the use of traditional fuels, which could materially impact the Fuel Division’s business, financial conditions, and results of operations.

We expect increasing levels of regulation, disclosure-related and otherwise, with respect to environmental, social and governance ("ESG”) matters in Mexico, the U.S., and other countries where we operate. For example, on March 6, 2024, the SEC adopted final rules to enhance and standardize climate-related disclosures by requiring registrants to disclose certain climate-related information in registration statements and annual reports. The final rules are subject to challenges in the U.S., and the outcome of ongoing litigation is currently unknown. If the rules become effective and are not overturned, we will be required to provide the enhanced climate-related disclosures. Compliance with these new rules, or similar rules or requirements imposed in other countries where we operate, may require us to incur significant additional costs to comply, including the implementation of significant additional internal controls, processes and procedures regarding matters that have not been subject to in the past, and impose increased oversight obligations on our management and board of directors. We may also be subject to overlapping and potentially conflicting ESG disclosure requirements in multiple jurisdictions. Additionally, many of our suppliers, business partners and others in our value chain may be subject to similar expectations, which may increase or create additional risks, including risks that may not be known to us. For these reasons, increased levels of ESG disclosure requirements could increase our operating costs and negatively impact our business and results of operations.

In addition, from time to time, we establish and publicly announce goals and commitments to reduce our carbon footprint by increasing our use of recycled packaging materials and participating in environmental and sustainability programs and initiatives organized or sponsored by non-governmental organizations and other groups to reduce greenhouse gas emissions industry wide. If we fail to achieve these goals due to restrictions to access or short supply of energy from renewable sources or improperly report on its progress toward achieving our carbon footprint reduction goals and commitments, the resulting negative publicity could adversely affect consumer preference and demand for our products.

Weather conditions and natural disasters may adversely affect our business, financial condition and results of operations.

Lower temperatures, higher rainfall and other adverse weather conditions such as hurricanes, natural disasters such as earthquakes, torrential rains, hurricanes and floods in the countries in which we operate may negatively impact consumer patterns, which may result in reduced sales of our products and at points of sale. Additionally, such adverse weather conditions and natural disasters may affect plant installed capacity, road infrastructure, personnel, assets and points of sale in the territories where we operate. Such events, or the containment measures to prevent or control them could also trigger increases in costs, disruption of supply, shortages of products, or consumer behavior changes including a decrease in an overall consumer mobility, thus affecting our business, financial condition, and results of operations. If any of these events becomes significant in duration, severity and frequency, our financial condition and results of operations could be materially adversely affected. FEMSA’s points of sales and facilities have been affected by hurricanes and other weather events in the past, which have resulted in temporary closures and losses. Also, any of these

11

events could force us to increase our capital expenditures to put our assets back in operation. See “Item 4. Information on the Company—Insurance.”

Risks Related to Mexico and the Other Countries Where We Operate

Adverse economic conditions in Mexico may adversely affect our financial position and results.

We are a Mexican corporation, and our Mexican operations are our single most important geographic territory. For the year ended December 31, 2023, 65% of our consolidated total revenues were attributable to Mexico. During 2023 and 2022, Mexican gross domestic product (“GDP”) increased by approximately 3.2% and 3.1%, respectively, on an annualized basis compared to the previous year as published by the INEGI. We cannot assure that such conditions will be maintained or continue to increase in the future or will not have a material effect on our business, results of operations and financial condition going forward. The Mexican economy continues to be heavily influenced by the U.S. economy, and therefore, deterioration in economic conditions in, or delays in the recovery of, the U.S. economy may hinder any recovery. In the past, Mexico has experienced both prolonged periods of weak economic conditions and deterioration in economic conditions that have had a negative impact on our results.

Our business may be significantly affected by the general condition of the Mexican economy, or by the rate of inflation in Mexico, interest rates in Mexico and exchange rates for, or exchange controls affecting, the Mexican peso. Decreases in the growth rate of the Mexican economy, periods of negative growth and/or increases in inflation or interest rates may result in lower demand for the products we carry in our stores, lower real pricing of products, a shift to lower margin products or decrease in store traffic. Because a large percentage of our costs and expenses are fixed, we may not be able to reduce costs and expenses upon the occurrence of any of these events and our profit margins may suffer as a result.

In addition, an increase in interest rates in Mexico would increase the cost of our debt and would cause an adverse effect on our financial position and results. Mexican peso-denominated debt (including currency hedges) represented 52.5% of our total debt as of December 31, 2023. See “Item 11. Quantitative and Qualitative Disclosures about Market Risk.”

Geopolitical conditions could negatively impact our financial results.

Financial uncertainties in our major markets and unstable geopolitical conditions or events in certain markets, including civil unrest, acts of war, terrorism or governmental changes could undermine global consumer confidence and reduce consumers' purchasing power, thereby reducing demand for our products.

Geopolitical conflicts, including escalation of ongoing conflicts and the ongoing military conflict involving Russia and Ukraine and the resulting economic sanctions imposed on Russia and certain Russian citizens and enterprises, could also cause volatility in commodity markets and significant disruptions in supply chains across the world, which may increase the cost of some of our raw materials and therefore have an adverse effect on our business, financial condition and results of operations. Our presence in Europe through the Valora acquisition positions FEMSA in closer proximity to the conflict in Russia and Ukraine and thus our European operations may be more significantly affected.

Volatility in other regions in which we have operations may also impact our financial results and operations. There can be no assurance that future developments in emerging market countries and in the United States, over which we have no control, will not have a material adverse effect on our financial condition and results.

Foreign exchange rate volatility of the Mexican peso and of our other local currencies could adversely affect our financial position and results.

Foreign exchange rate volatility of the Mexican peso and of our other local currencies increases the cost of a portion of the raw materials we acquire, the price of which is paid in or determined with reference to U.S. dollars, and of our debt obligations denominated in U.S. dollars, and thereby negatively affects our financial position and results. A severe devaluation or depreciation of the Mexican peso, which is our main operating currency, may result in disruption of the international foreign exchange markets and may limit our ability to transfer or to convert Mexican pesos into U.S. dollars and other currencies for the purpose of making timely payments of interest and principal on our U.S. dollar-denominated debt or obligations in other currencies. The Mexican peso is a free-floating currency and, as such, it experiences exchange rate fluctuations relative to the U.S. dollar over time. As of December 31, 2023, the Mexican peso appreciated relative to the U.S. dollar by approximately 13.3% compared to 2022. As of December 31, 2022 and 2021, the Mexican peso experienced fluctuations relative to the U.S. dollar consisting of appreciation of 5.0% and depreciation of 3.1%, respectively, compared to the prior year. Through April 19, 2024, the Mexican peso has depreciated 1.8% since December 31, 2023.

12

While the Mexican government does not currently restrict, and since 1982 has not restricted, the right or ability of Mexican or foreign persons or entities to convert Mexican pesos into U.S. dollars or to transfer other currencies out of Mexico, the Mexican government could impose restrictive exchange rate policies in the future, as it has done in the past. Currency fluctuations may have an adverse effect on our financial position, results, and cash flows in future periods.

When the financial markets are volatile, as they have been in recent periods, our results may be substantially affected by variations in exchange rates and commodity prices and, to a lesser degree, interest rates. These effects include foreign exchange gain and loss on assets and liabilities denominated in U.S. dollars, fair value gain and loss on derivative financial instruments, commodities prices and changes in interest income and interest expense. These effects can be much more volatile than our operating performance and our operating cash flows. See “Item 11. Quantitative and Qualitative Disclosures about Market Risk—Foreign Currency Exchange Rate Risk.”

The devaluation of the local currencies against the U.S. dollar can increase the operating costs for Coca-Cola FEMSA, and depreciation of the local currencies against the Mexican peso can negatively affect the translation of Coca-Cola FEMSA's results. Future currency devaluation or the imposition of exchange controls in any of these countries, or in Mexico, would have an adverse effect on their financial position and results.

Generally, future currency devaluations or the imposition of exchange controls in any of the countries where we have operations may potentially increase our operating costs, which could have an adverse effect on our results of operations and financial condition. See “Item 11. Quantitative and Qualitative Disclosures about Market Risk—Foreign Currency Exchange Rate Risk.”

Political, social and security events and conditions in Mexico and other countries in which we operate could adversely affect our operations.

Mexican political events may significantly affect our operations. We cannot predict whether potential changes in Mexican governmental and economic policy could adversely affect economic conditions in Mexico or the sector in which we operate. The Mexican president and Congress have a strong influence over new policies and governmental actions regarding the Mexican economy, and the current federal administration could implement substantial changes in law, policy and regulations in Mexico, including reforms to the Constitution, which could negatively affect our business, results of operations and financial condition. In response to these actions, opponents of the administration could react with, among other things, riots, protests and looting that could negatively affect our operations.

As of the date of this annual report, the Morena Political Party, in conjunction with its allied political parties, holds a simple majority in the Senate and in the Chamber of Deputies and a strong influence in various local legislatures. We cannot provide any assurances that political developments in Mexico, such as the election of new administrations, changes in laws, public policy or regulations, political disagreements or civil disturbances, over which we have no control, will not have an adverse effect on our business, results of operations and financial condition. Furthermore, national presidential, state government and/or legislative elections took place in 2023 or are scheduled to take place in 2024 in several of the countries where we operate, including Argentina, Panama, Mexico and Uruguay. These countries are or may be facing changes of government, which could introduce potential risks associated with shifts in political leadership and changes in public policies. Uncertainty surrounding the new administration's agenda, regulatory reforms, and economic policies could impact our operations and financial performance.

Mexico has experienced periods of increasing criminal activity and particularly homicide rates, primarily due to organized crime. This poses a risk to our business and might negatively impact business continuity. An increase in crime rates could negatively affect our sales and customer traffic, increase our security expenses, affect our hours of operation and result in higher turnover of personnel or damage to the perception of our brands. Furthermore, this could adversely impact our business and financial results because consumer habits and patterns adjust to the increased perceived and real security risks, as people refrain from going out as much and gradually shift some on-premises consumption to off-premises consumption of food and beverages on certain occasions.

Other countries in which we operate have also experienced periods of increased criminal activity and other security incidents. We cannot assure you that political or social developments in the countries where we operate or elsewhere, such as the election of new administrations, changes in laws, public policy or regulations, political disagreements, civil disturbances and the rise in violence and perception of such rise in violence, over which we have no control, will not have a corresponding adverse effect on the local or global markets or on our business, financial condition and results of operations.

Economic conditions in Mexico and other countries in which we operate could adversely affect our operations.

The markets in which we operate are highly sensitive to economic conditions because a decline in consumer purchasing power is often a consequence of an economic slowdown which, in turn, results in a decline in the overall

13

consumption of main product categories. During periods of economic slowdown, our points of sale may experience a decline in same-store traffic and average ticket per customer, which may result in a decline in overall performance. See “Item 5. Operating and Financial Review and Prospects—Overview of Events, Trends and Uncertainties.”

Many countries worldwide, including Mexico, have suffered significant economic volatility in recent years, and this may occur again in the future. Global instability has been caused by many different factors, including substantial fluctuations in economic growth, high levels of inflation, changes in currency values, changes in governmental economic or tax policies and regulations and overall political, social, and economic instability. We cannot assure you that such conditions will not return or that such conditions will not have a material adverse effect on our financial condition and results.

The Mexican economy and the market value of securities issued by Mexican issuers may be, to varying degrees, affected by economic and market conditions in other emerging market countries and in the United States. Furthermore, economic conditions in Mexico have been highly correlated with economic conditions in the United States primarily as a result of the United States-Mexico-Canada Agreement (“USMCA”), which came into force on July 1, 2020.