UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One) | |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended | |

OR | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Date of event requiring this shell company report . . . . . . . . . . . . . . . . . . .

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

+852 2523-3588

(Address of principal executive offices)

Telephone: +

Email:

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

The | ||||

| The |

* Not for trading, but only in connection with the listing on The Nasdaq Global Market of American depositary shares.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2022,

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ⌧

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ⌧

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ⌧

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ⌧

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer ☐ | Non-accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐ Yes ☐ No

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued by the | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

|

| Page |

1 | ||

|

| |

4 | ||

6 | ||

|

| |

19 | ||

19 | ||

19 | ||

19 | ||

80 | ||

165 | ||

165 | ||

183 | ||

194 | ||

197 | ||

198 | ||

199 | ||

215 | ||

216 | ||

|

|

|

218 | ||

218 | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 218 | |

219 | ||

219 | ||

219 | ||

220 | ||

220 | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 220 | |

221 | ||

221 | ||

221 | ||

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 222 | |

|

|

|

222 | ||

222 | ||

222 | ||

222 | ||

|

|

|

225 | ||

i

INTRODUCTION

Unless otherwise indicated or the context otherwise requires, references in this annual report to:

| ● | “ADSs” are to American depositary shares, each of which represents eight Class A ordinary shares; |

| ● | “availability rate” are to the ratio of the total time a service system is capable of being used during the market hours of the relevant equity markets; |

| ● | “average DAUs” are to the average number of DAUs on each trading day during a specific period; |

| ● | “China,” “Mainland China” and the “PRC” are to the People’s Republic of China for the purpose of this annual report and for geographical reference only, except where the context requires, references in this annual report to “China”, “Mainland China” and the “PRC” do not apply to the Hong Kong Special Administrative Region of the PRC, the Macau Special Administrative Region of the PRC and the Taiwan Region; |

| ● | “clients” are to users who open one or more trading accounts with us; |

| ● | “client asset balance” are to the asset balance in the trading accounts of our paying clients; |

| ● | “Class A ordinary shares” are to our Class A ordinary shares, par value US$0.00001 per share; |

| ● | “Class B ordinary shares” are to our Class B ordinary shares, par value US$0.00001 per share; |

| ● | “Consolidated Affiliated Entities” are to entities that we control wholly or partly through the Contractual Arrangements, namely the VIEs and their subsidiaries, details of which are set out in “Item 4. Information on the Company—C. Organizational Structure—Contractual Arrangements with the VIEs and Their Shareholders”; |

| ● | “Contractual Arrangements” are to the series of contractual arrangements entered into between the WFOE, the VIEs and the registered shareholders of each of the VIEs, namely, Mr. Li and Ms. Lei Li (as applicable), as detailed in “Item 4. Information on the Company—C. Organizational Structure—Contractual Arrangements with the VIEs and Their Shareholders”; |

| ● | “CSRC” are to the China Securities Regulatory Commission; |

| ● | “DAUs” are to the number of user accounts and visitors who access our platforms Futubull and/or moomoo, at least once on a given trading day. Some visitors may access our platforms using more than one device on a given trading day and we calculate the number of visitors who access our platforms based on the number of devices used by the visitors to access our platforms; |

| ● | “domestic” are, for the purpose of this annual report and for geographical reference only, to the PRC, an entity organized under PRC laws or an individual who is a holder of PRC nationality and passport, as the context may require; |

| ● | “Futu,” “Group,” “our Group,” “the Group,” “we,” “our” and “us” are to Futu Holdings and its subsidiaries and, in the context of describing our operations and consolidated financial information, also include the Consolidated Affiliated Entities, unless the context otherwise requires; |

| ● | “Futu Australia” are to Futu Securities (Australia) Ltd., a company with limited liability incorporated in Australia on February 15, 2001 and our wholly-owned subsidiary; |

| ● | “Futu Holdings” and “our company” are to Futu Holdings Limited, a company with limited liability incorporated in the Cayman Islands on April 15, 2014; |

1

| ● | “Futu Securities” are to Futu Securities International (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability on April 17, 2012 and our wholly-owned subsidiary; |

| ● | “Hainan Caixuetang” are to Hainan Caixuetang Education Network Technology Co., Ltd., a company established under the laws of PRC with limited liability on December 14, 2020, and a Consolidated Affiliated Entity; |

| ● | “Hainan Futu” are to Hainan Futu Information Services Co., Ltd., a company established under the laws of PRC with limited liability on May 25, 2018, and a Consolidated Affiliated Entity; |

| ● | “HK$” and “Hong Kong dollars” are to the legal currency of Hong Kong; |

| ● | “HK SFC” are to the Securities and Futures Commission of Hong Kong; |

| ● | “Latest Practicable Date” are to March 31, 2023, being the latest practicable date for ascertaining certain information in this annual report; |

| ● | “MAS” are to the Monetary Authority of Singapore; |

| ● | “MAUs” are to the number of user accounts and visitors who access our platforms Futubull and/or moomoo at least once during the calendar month in question. Some visitors may access our platforms using more than one device in a given month and we calculate the number of visitors who access our platforms based on the number of devices used by the visitors to access our platforms; |

| ● | “MIIT” are to the Ministry of Industry and Information Technology of PRC; |

| ● | “Moomoo Financial Singapore” are to Moomoo Financial Singapore Pte. Ltd. (formerly known as Futu Singapore Pte. Ltd.), a company with limited liability incorporated in Singapore on December 17, 2019 and our wholly-owned subsidiary; |

| ● | “Mr. Li” are to Mr. Leaf Hua Li, our founder, chairman of the board of directors and chief executive officer; |

| ● | “NiuNiu/Moo Community” are to our social network services on Futubull or moomoo platform, including the interactive tools and functions offered on such platform; |

| ● | “paying clients” are to clients with assets in their trading accounts with us; |

| ● | “professional investor” are to persons as defined under Part 1 of Schedule 1 to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong), as amended, supplemented or otherwise modified from time to time (including those prescribed by rules made under section 397 of the Securities and Futures Ordinance); |

| ● | “retail investor” are to an individual investor that purchases securities and other investment assets; |

| ● | “RMB” and “Renminbi” are to the legal currency of China; |

| ● | “SCNPC” are to the Standing Committee of the National People’s Congress of the PRC; |

| ● | “SEC” are to the U.S. Securities and Exchange Commission; |

| ● | “shares” and “ordinary shares” are to our Class A ordinary shares and Class B ordinary shares; |

| ● | “Shensi Beijing” and “WFOE” are to Shensi Network Technology (Beijing) Co., Ltd., a wholly foreign-owned enterprise established under the laws of the PRC on September 15, 2014, and our wholly-owned subsidiary; |

2

| ● | “Shenzhen Futu” are to Shenzhen Futu Network Technology Co., Ltd., a company established under the laws of PRC with limited liability on December 18, 2007, a Consolidated Affiliated Entity; |

| ● | “Stock Connect” are to the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect; |

| ● | “US$,” “U.S. dollars,” “$,” and “dollars” are to the legal currency of the United States; |

| ● | “users” are to user accounts registered with our applications or websites; and |

| ● | “VIE(s)” are to Shenzhen Futu and Hainan Futu. |

For each relevant period prior to January 1, 2021, “users,” “MAUs” and “average DAUs” figures disclosed in this annual report are only inclusive of those under Futubull, due to insignificant figures recorded under moomoo. Since January 1, 2021, the numbers disclosed in this annual report include figures under Futubull and moomoo for each subsequent period. The number of users is determined based on the user accounts registered with Futubull and moomoo.

For each relevant period prior to January 1, 2021, “clients,” “paying clients,” “client asset balance,” “trading volume” and other client-based figures disclosed in this annual report are only inclusive of those under Futu Securities, due to insignificant figures recorded under Moomoo Financial Inc. (previous name: Futu Inc.). Since January 1, 2021, the figures disclosed in this annual report include those under Futu Securities, Moomoo Financial Inc., Moomoo Financial Singapore and Futu Australia for each subsequent period.

Our reporting currency is Hong Kong dollars. This annual report contains translations of certain foreign currency amounts into U.S. dollars for the convenience of the reader. Unless otherwise stated, the conversions between U.S. dollars and Hong Kong dollars were made at the rate of HK$7.8015 to US$1.00, the exchange rate on December 30, 2022 set forth in the H.10 statistical release of The Board of Governors of the Federal Reserve Board. We make no representation that any Hong Kong dollars or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Hong Kong dollars, as the case may be, at any particular rate, or at all. Any discrepancies in any table between totals and sums of amounts listed therein are due to rounding.

3

FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements that reflect our current expectations and views of future events. The forward-looking statements are contained principally in the sections entitled “Item 3. Key Information—D. Risk Factors,” “Item 4. Information on the Company—B. Business Overview” and “Item 5. Operating and Financial Review and Prospects.” Known and unknown risks, uncertainties and other factors, including those listed under “Item 3. Key Information—D. Risk Factors,” may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to,” “potential,” “continue” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to, statements relating to:

| ● | our mission, goals and strategies; |

| ● | our future business development, financial conditions and results of operations; |

| ● | the trends in, expected growth and the market size of the online and mobile trading and other financial services industry in China, Hong Kong, the United States, Singapore and globally; |

| ● | expected changes in our revenues, costs or expenditures; |

| ● | our expectations regarding demand for and market acceptance of our products and services; |

| ● | our expectations regarding our relationships with users, clients and third-party business partners; |

| ● | competition in our industry; |

| ● | our proposed use of proceeds; |

| ● | the impact of the COVID-19 pandemic; |

| ● | relevant government policies and regulations relating to our industry; and |

| ● | general economic, business and socio-political conditions in China, Hong Kong, the United States, Singapore and other markets we have businesses or operations. |

These forward-looking statements involve various risks and uncertainties. You should read thoroughly this annual report and the documents that we refer to with the understanding that our actual future results may be materially different from and worse than what we expect. Important risks and factors that could cause our actual results to be materially different from our expectations are generally set forth in “Item 3. Key Information—D. Risk Factors,” “Item 4. Information on the Company—B. Business Overview” and “Item 5. Operating and Financial Review and Prospects” and other sections in this annual report. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time, and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements.

4

This annual report contains certain data and information that we obtained from various government and private publications. Although we believe the data and information to be reliable, we have not independently verified the accuracy or completeness of the data and information contained in these publications. Statistical data in these publications also include projections based on a number of assumptions. The online brokerage and related industries may not grow at the rate projected by market data, or at all. Failure of these markets to grow at the projected rate may have a material and adverse effect on our business and the market price of the ADSs. In addition, the rapidly evolving nature of the online brokerage industry results in significant uncertainties for any projections or estimates relating to the growth prospects or future condition of our market. Furthermore, if any one or more of the assumptions underlying the market data are later found to be incorrect, actual results may differ from the projections based on these assumptions. You should not place undue reliance on these forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we refer to in this annual report and have filed as exhibits to this annual report, of which this annual report is a part, completely and with the understanding that our actual future results may be materially different from what we expect.

5

EXPLANATORY NOTE

Investing in our securities involves a high degree of risk. Please carefully consider the risks discussed under the section entitled “Item 3. Key Information—D. Risk Factors” in this annual report. We provide the following disclosure to help investors better understand our corporate structure, operations in China and the associated risks.

Our Corporate Structure and Operations in China

Futu Holdings is not an operating company but a Cayman Islands holding company conducting a significant portion of our operations through our wholly-owned subsidiaries, including in Hong Kong, Singapore, the United States and Australia. As an exempted company incorporated in the Cayman Islands, Futu Holdings and its wholly-owned PRC subsidiaries are classified, respectively, as a foreign enterprise and foreign-invested enterprises under PRC laws and regulations, and none of them is generally allowed to own more than 50% of the equity interests in PRC companies that are value-added telecommunication service providers or to own any equity interests in PRC companies that are engaging in internet culture service or other services prohibited from foreign investment.

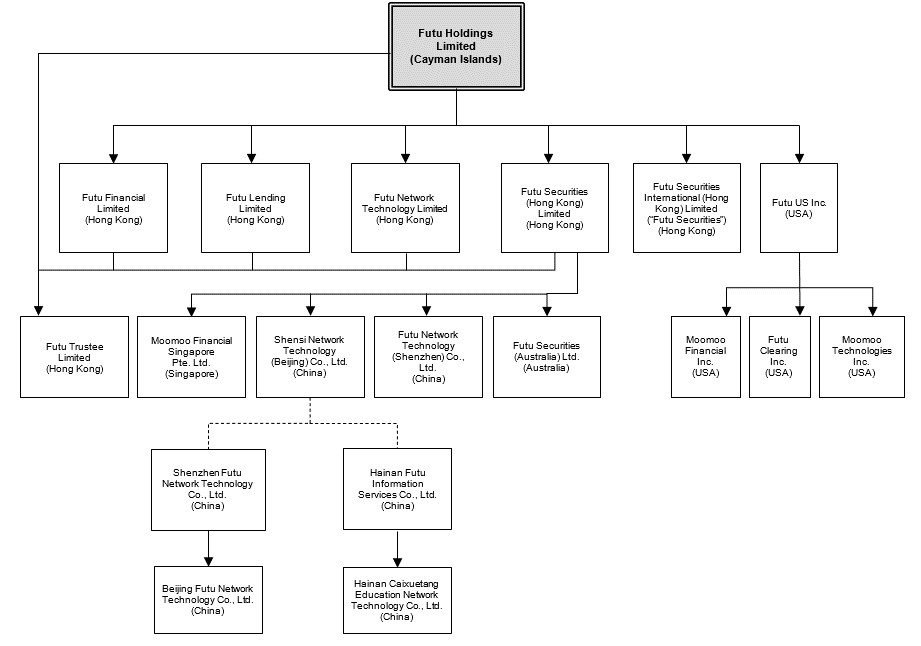

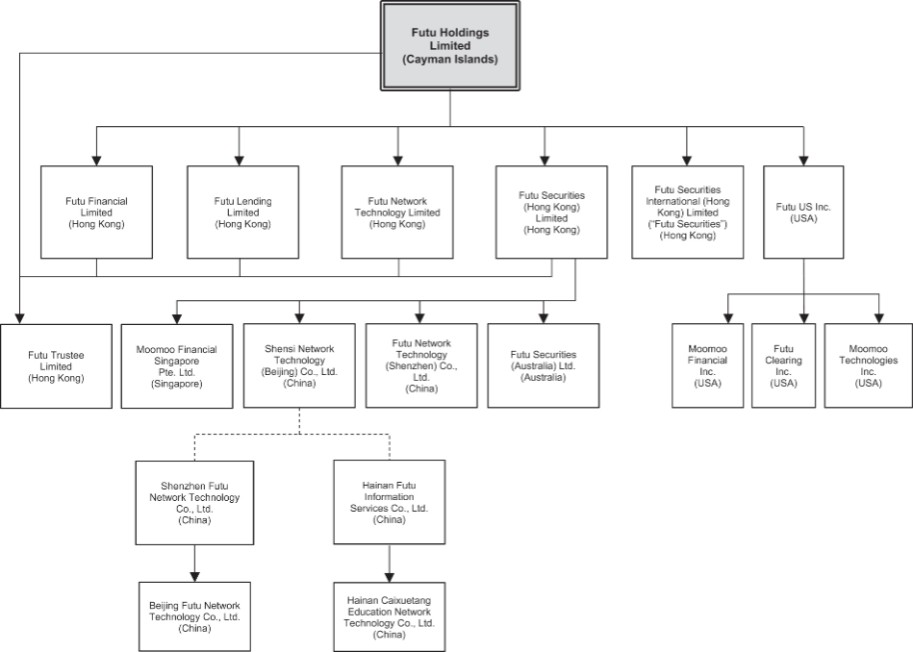

In order to provide certain value-added telecommunication services, internet culture services and other services prohibited from foreign investment in China while ensuring compliance with PRC laws and regulations, Shensi Beijing, our wholly-owned PRC subsidiary, or the WFOE, has entered into a series of contractual arrangements with each of Shenzhen Futu and Hainan Futu, or the VIEs, and their respective shareholders, which we refer to collectively as the Contractual Arrangements in this annual report. The Contractual Arrangements are designed to provide us economic exposure to the VIEs’ operations of value-added telecommunication services, internet cultural services and other services in China where PRC laws prohibit, restrict or impose conditions on direct foreign equity investment in the VIEs. The following diagram illustrates our corporate structure, including our significant subsidiaries and the Consolidated Affiliated Entities, as of the date of this annual report:

6

Notes:

| (1) | “➝” denotes direct legal and beneficial ownership in equity interest (100% ownership unless otherwise indicated). |

| (2) | “┈” denotes the contractual arrangements that provide the WFOE with the ability to direct the activities of the Consolidated Affiliated Entities through (i) the powers of attorney to exercise all shareholders’ rights of the registered shareholders in the VIEs; (ii) exclusive options to acquire all or part of the equity interest in the VIEs; and (iii) equity pledges by the registered shareholders in favor of the WFOE over the equity interests in the VIEs. |

| (3) | As of December 31, 2022, Shenzhen Futu Network Technology Co., Ltd. held a Valued-added Telecommunication Business Operation License, or an ICP License, a Radio and Television Program Production and Operation License and an Internet Culture Operation License; and Hainan Caixuetang Education Network Technology Co., Ltd. held an Internet Culture Operation License, a Radio and Television Program Production and Operation License, an ICP License and a Publication Operation License. |

| (4) | Mr. Leaf Hua Li and Ms. Lei Li hold 85% and 15% equity interests, respectively, in each of Shenzhen Futu Network Technology Co., Ltd. and Hainan Futu Information Services Co., Ltd.. Mr. Li is our founder, chairman of board of directors and chief executive officer. Ms. Lei Li is Mr. Li’s spouse. |

| (5) | Each of Futu Holdings Limited, Futu Financial Limited, Futu Lending Limited, Futu Network Technology Limited and Futu Securities (Hong Kong) Limited owns 20% of the share capital in Futu Trustee Limited. |

7

| (6) | Moomoo Financial Singapore Pte. Ltd. was formerly known as Futu Singapore Pte. Ltd.; Moomoo Financial Inc. was formerly known as Futu Inc.; and Moomoo Technologies Inc. was formerly known as Moomoo Inc.. |

For a detailed description about the Contractual Arrangements, see “Item 4. Information on the Company—C. Organizational Structure—Contractual Arrangements with the VIEs and Their Shareholders.”

As a result of the Contractual Arrangements, Futu Holdings becomes the primary beneficiary of the VIEs and their subsidiaries, or the Consolidated Affiliated Entities, for accounting purposes and treat each of them as a PRC consolidated entity under U.S. GAAP. Neither we nor our investors own any equity ownership in, direct foreign investment in, or control of the Consolidated Affiliated Entities as a result of the Contractual Arrangements. As a result, holders of the ADSs are not purchasing equity interest in the Consolidated Affiliated Entities but instead are purchasing equity interest in Futu Holdings, a Cayman Islands holding company whose consolidated financial results include those of the Consolidated Affiliated Entities under U.S. GAAP.

The Contractual Arrangements have not been tested in a court of law in the PRC and foreign investors may never be allowed to hold equity interests in the Consolidated Affiliated Entities under PRC laws and regulations. PRC regulatory authorities could in the future disallow the Contractual Arrangements, which would likely affect our operations in China. Please see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government deems that the Contractual Arrangements do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations.”

We and the VIEs face various legal and operational risks and uncertainties related to our operations in China, including complex and evolving PRC laws and regulations. For example, the China Securities Regulatory Commission, or the CSRC, has initiated inquires on us concerning matters including the provision of cross-border securities services for domestic investors. Besides, we also face risks associated with regulatory approvals and/or filings in connection with our future offshore offering or listing of securities on a different market, the use of variable interest entities, anti-monopoly regulatory actions, as well as oversight on cybersecurity and data privacy. These risks could result in a material adverse change in our operations and the value of the ADSs, significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause such securities to significantly decline in value, as elaborated below:

| ● | The PRC government has significant authority to regulate or intervene in a company’s operations in China at any time, such as ours, whether such operations are conducted through a subsidiary or a consolidated variable interest entity. Therefore, investors in the ADSs and our business face potential uncertainty from the PRC government’s policy. The PRC government may intervene in or influence our operations at any time, or may exert more oversight and control over our offerings conducted overseas, which could result in a material change in our operations and/or the value of the ADSs. Any actions by the PRC government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China—There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations”; |

8

| ● | We believe that our corporate structure and the Contractual Arrangements are not in violation of the current applicable PRC laws and regulations. As of the date of this annual report, we believe that none of our subsidiaries and the Consolidated Affiliated Entities is required to obtain permission or approval from relevant regulatory authorities to operate their respective business in the telecommunication industry in China or to approve the Contractual Arrangements. However, PRC laws and regulations governing the conditions and the requirements of such approval are uncertain and the relevant government authorities have broad discretion in interpreting these laws and regulations. Accordingly, the PRC regulatory authorities may take a different view. There can be no assurance that the PRC government authorities such as the Ministry of Commerce, or the MOFCOM, the Ministry of Industry and Information Technology, or the MIIT, or other authorities that regulate our activities in China, would agree that our corporate structure or any of the above Contractual Arrangements comply with PRC licensing, registration or other regulatory requirements, with existing policies or with requirements or policies that may be adopted in the future. As of the date of this annual report, we have not received any inquiry, notice, warning, or sanctions regarding our corporate structure and the Contractual Arrangements from any PRC governmental agency. If we, our subsidiaries or the Consolidated Affiliated Entities inadvertently conclude that approvals are not required, or if these regulations change or are interpreted differently and we are required to obtain approval in the future, the ADSs may significantly decline in value or become worthless if we are unable to assert our contractual rights over the economic benefits and assets of the Consolidated Affiliated Entities. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government deems that the Contractual Arrangements do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations”; |

| ● | The PRC government has initiated a series of regulatory actions and released guidelines to regulate business operations in China with little advance notice, including those related to data security or anti-monopoly concerns, which may have an impact on our ability to conduct certain business in China, accept foreign investments, or list on a U.S. or other foreign exchange. If we are unable to address any data security or information protection concerns, any compromise of security that results unauthorized disclosure or transfer of personal data, or to comply with the then applicable laws and regulations, we may incur additional costs and liability and result in governmental enforcement actions, litigation, fines and penalties or adverse publicity and could cause our users and clients to lose trust in us, which could have a material adverse effect on our business, results of operations, financial condition and prospects. If certain of our activities in Mainland China were deemed by relevant regulators as violation of the laws and regulations on anti-monopoly, it may result in governmental investigations, fines and/or other sanctions against us. As of the date of this annual report, we have not been subject to any administrative penalties, regulatory actions or inquires in connection with anti-monopoly or data security or data privacy. We may also be subject to new laws, regulations or standards, or new interpretations of existing laws, regulations or standards, including those in the areas of data security, data privacy and anti-monopoly, which could require us to incur additional costs and restrict our operations. For a detailed description of risks and regulations related to our operations in China, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China”, “Item 4. Information on the Company—B. Business Overview—Regulation—Overview of the Laws and Regulations Relating to Our Business and Operations in China—Regulations on Cybersecurity and Privacy” and “Item 4. Information on the Company—B. Business Overview—Regulation—Overview of the Laws and Regulations Relating to Our Business and Operations in China—Regulations on Anti-Monopoly Matters related to Internet Platform Companies”; and |

| ● | We rely on the Contractual Arrangements for a limited part of our operations in China, which may not be as effective as ownership in providing us with the ability to direct the activities of the Consolidated Affiliated Entities. We rely on the VIEs’ and their shareholders’ compliance with their obligations under the Contractual Arrangements to direct the activities of the Consolidated Affiliated Entities. The shareholders of the VIEs may not act in the best interests of us or may not perform their obligations under these contracts. Such risks exist throughout the period in which we intend to operate in China through the Contractual Arrangements. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We depend on the Contractual Arrangements to operate a part of our business in China and to hold the necessary licenses for our operations, which may not be as effective as ownership in providing us with the ability to direct the activities of the Consolidated Affiliated Entities and otherwise may have a material adverse effect as to our business”. |

9

The Holding Foreign Companies Accountable Act

Pursuant to the Holding Foreign Companies Accountable Act, or the HFCAA, if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspections by the Public Company Accounting Oversight Board, or the PCAOB, for two consecutive years, the SEC will prohibit our shares or the ADSs from being traded on a national securities exchange or in the over-the-counter trading market in the United States. On December 16, 2021, the PCAOB issued a report to notify the SEC of its determination that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in Mainland China and Hong Kong, including our auditor. On April 21, 2022, the SEC conclusively listed us as a Commission-Identified Issuer under the HFCAA following the filing of our annual report on Form 20-F for the fiscal year ended December 31, 2021. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed Mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. For this reason, we do not expect to be identified as a Commission-Identified Issuer under the HFCAA after we file this annual report on Form 20-F for the fiscal year ended December 31, 2022. Each year, the PCAOB will determine whether it can inspect and investigate completely audit firms in Mainland China and Hong Kong, among other jurisdictions. If PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in Mainland China and Hong Kong and we continue to use an accounting firm headquartered in one of these jurisdictions to issue an audit report on our financial statements filed with the SEC, we would be identified as a Commission-Identified Issuer following the filing of the annual report on Form 20-F for the relevant fiscal year. There can be no assurance that we would not be identified as a Commission-Identified Issuer for any future fiscal year, and if we were so identified for two consecutive years, we would become subject to the prohibition on trading under the HFCAA. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China—The ADSs may be delisted and prohibited from trading in the United States under the HFCAA in the future if the PCAOB is unable to inspect or investigate completely auditors located in China, which will materially and adversely affect the value of your investment.”

Financial Information relating to the Consolidated Affiliated Entities

Historically, the Consolidated Affiliated Entities accounted for a small portion of our financial position, results of operations and cash flows. Set forth below are the condensed consolidating schedule showing the financial position as of December 31, 2022 and 2021, and results of operations and cash flows for the years ended December 31, 2022, 2021 and 2020 for (i) Futu Holdings; (ii) our subsidiaries (excluding the WFOE); (iii) the WFOE (which is the primary beneficiary of the Consolidated Affiliated Entities); (iv) the Consolidated Affiliated Entities (primarily Shenzhen Futu and its subsidiaries as Hainan Futu did not conduct substantial business during the periods presented); (v) eliminating adjustments; and (vi) consolidated totals (in thousands of HK dollars).

10

Selected Condensed Consolidating Balance Sheets Information

As of December 31, 2022 | ||||||||||||

Subsidiaries | Consolidated | |||||||||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

| Futu Holdings |

| the WFOE) |

| WFOE |

| Entities |

| Adjustments |

| Totals | |

Selected Condensed Consolidating Balance Sheets Information |

|

|

|

|

|

|

|

|

|

|

|

|

Assets | ||||||||||||

Cash and cash equivalents |

| 87,784 |

| 4,908,308 |

| 5 |

| 32,801 |

| — |

| 5,028,898 |

Cash held on behalf of clients |

| — |

| 50,685,472 |

| — |

| — |

| — |

| 50,685,472 |

Restricted cash |

| — |

| 1,215 |

| — |

| — |

| — |

| 1,215 |

Term deposit |

| — |

| 5,860 |

| — |

| — |

| — |

| 5,860 |

Short-term investments |

| — |

| 675,064 |

| — |

| — |

| — |

| 675,064 |

Amounts due from internal companies(1) |

| 3,557,176 |

| 253,121 |

| 1,924 |

| 222,446 |

| (4,034,667) |

| — |

Loans and advances |

| — |

| 26,713,123 |

| — |

| — |

| — |

| 26,713,123 |

Securities purchased under agreements to resell |

| — |

| 32,000 |

| — |

| — |

| — |

| 32,000 |

Receivables |

| — |

| 9,828,670 |

| — |

| — |

| — |

| 9,828,670 |

Prepaid assets |

| — |

| 25,472 |

| — |

| 3,035 |

| — |

| 28,507 |

Investment in subsidiaries(2) |

| 17,262,541 |

| 120,152 |

| — |

| — |

| (17,382,693) |

| — |

Net assets of the VIEs(2) |

| — |

| — |

| 118,445 |

| — |

| (118,445) |

| — |

Long-term investments |

| — |

| 239,694 |

| — |

| — |

| — |

| 239,694 |

Operating lease right-of-use assets |

| — |

| 175,576 |

| — |

| 21,288 |

| — |

| 196,864 |

Other assets |

| 5,204 |

| 1,032,121 |

| — |

| 30,138 |

| — |

| 1,067,463 |

Total assets |

| 20,912,705 |

| 94,695,848 |

| 120,374 |

| 309,708 |

| (21,535,805) |

| 94,502,830 |

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

Amounts due to related parties |

| — |

| 52,725 |

| — |

| — |

| — |

| 52,725 |

Amounts due to internal companies(1) |

| 21,834 |

| 3,924,124 |

| 222 |

| 88,487 |

| (4,034,667) |

| — |

Payables |

| — |

| 69,176,872 |

| — |

| — |

| — |

| 69,176,872 |

Borrowings |

| — |

| 2,480,532 |

| — |

| — |

| — |

| 2,480,532 |

Lease liabilities |

| — |

| 188,959 |

| — |

| 22,184 |

| — |

| 211,143 |

Accrued expenses and other liabilities |

| 29,327 |

| 1,609,860 |

| — |

| 80,592 |

| — |

| 1,719,779 |

Total liabilities |

| 51,161 |

| 77,433,072 |

| 222 |

| 191,263 |

| (4,034,667) |

| 73,641,051 |

Total shareholders’ equity(2) |

| 20,861,544 |

| 17,262,541 |

| 120,152 |

| 118,445 |

| (17,501,138) |

| 20,861,544 |

Non-controlling interest |

| — |

| 235 |

| — |

| — |

| — |

| 235 |

Total equity |

| 20,861,544 |

| 17,262,776 |

| 120,152 |

| 118,445 |

| (17,501,138) |

| 20,861,779 |

11

| As of December 31, 2021 | |||||||||||

|

| Subsidiaries |

|

| Consolidated |

|

| |||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

Futu Holdings | the WFOE) | WFOE | Entities | Adjustments | Totals | |||||||

Selected Condensed Consolidating Balance Sheets Information |

|

|

|

|

|

|

|

|

|

|

|

|

Assets | ||||||||||||

Cash and cash equivalents |

| 37,574 |

| 4,514,736 |

| 35 |

| 2,751 |

| — |

| 4,555,096 |

Cash held on behalf of clients |

| — |

| 54,734,351 |

| — |

| — |

| — |

| 54,734,351 |

Restricted cash |

| — |

| 2,065 |

| — |

| — |

| — |

| 2,065 |

Term deposit |

| — |

| — |

| — |

| — |

| — |

| — |

Short-term investments |

| 1,169,741 |

| — |

| — |

| — |

| — |

| 1,169,741 |

Amounts due from internal companies(1) |

| 6,969,446 |

| 46,296 |

| 2,102 |

| 190,424 |

| (7,208,268) |

| — |

Loans and advances |

| — |

| 29,587,306 |

| — |

| — |

| — |

| 29,587,306 |

Securities purchased under agreements to resell |

| — |

| 106,203 |

| — |

| — |

| — |

| 106,203 |

Receivables |

| — |

| 10,447,794 |

| — |

| — |

| — |

| 10,447,794 |

Prepaid assets |

| — |

| 11,366 |

| — |

| 6,940 |

| — |

| 18,306 |

Investment in subsidiaries(2) |

| 13,514,216 |

| 80,292 |

| — |

| — |

| (13,594,508) |

| — |

Net assets of the VIEs(2) | — | — | 78,398 | — | (78,398) | — | ||||||

Long-term investments |

| — |

| 23,394 |

| — |

| — |

| — |

| 23,394 |

Operating lease right-of-use assets |

| — |

| 210,887 |

| — |

| 40,415 |

| (7,443) |

| 243,859 |

Other assets |

| 21,620 |

| 614,707 |

| — |

| 14,072 |

| — |

| 650,399 |

Total assets |

| 21,712,597 |

| 100,379,397 |

| 80,535 |

| 254,602 |

| (20,888,617) |

| 101,538,514 |

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

Amounts due to related parties |

| — |

| 87,459 |

| — |

| — |

| — |

| 87,459 |

Amounts due to internal companies(1) |

| 21,955 |

| 7,105,635 |

| 243 |

| 80,435 |

| (7,208,268) |

| — |

Securities sold under agreements to repurchase |

| — |

| 4,467,861 |

| — |

| — |

| — |

| 4,467,861 |

Payables |

| 131 |

| 67,192,372 |

| — |

| — |

| — |

| 67,192,503 |

Borrowings |

| 689,869 |

| 5,667,536 |

| — |

| — |

| — |

| 6,357,405 |

Lease liabilities |

| — |

| 217,694 |

| — |

| 42,628 |

| 257 |

| 260,579 |

Accrued expenses and other liabilities |

| 15,083 |

| 2,129,186 |

| — |

| 53,141 |

| (10,262) |

| 2,187,148 |

Total liabilities |

| 727,038 |

| 86,867,743 |

| 243 |

| 176,204 |

| (7,218,273) |

| 80,552,955 |

Total shareholders’ equity(2) |

| 20,985,559 |

| 13,511,654 |

| 80,292 |

| 78,398 |

| (13,670,344) |

| 20,985,559 |

Selected Condensed Consolidating statements of Comprehensive Income Information

| 2022 | |||||||||||

Subsidiaries | Consolidated | |||||||||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

| Futu Holdings |

| the WFOE) |

| WFOE |

| Entities |

| Adjustments |

| Totals | |

Selected Condensed Consolidating statements of Comprehensive Income Information |

|

|

|

|

|

|

|

|

|

|

|

|

Third-party revenues |

| 12,654 |

| 7,577,739 |

| — |

| 23,634 |

| — |

| 7,614,027 |

Inter-company revenues(3) |

| — |

| — |

| — |

| 202,834 |

| (202,834) |

| — |

Total costs(3) |

| — |

| (1,186,497) |

| — |

| (12,469) |

| 202,834 |

| (996,132) |

Total expenses |

| (78,285) |

| (2,775,272) |

| (28) |

| (195,408) |

| — |

| (3,048,993) |

Equity in gain of subsidiaries(2) |

| 2,977,254 |

| 39,514 |

| — |

| — |

| (3,016,768) |

| — |

Income of the VIEs | — | — | 39,542 | — | (39,542) | — | ||||||

Others, net |

| 15,321 |

| (230,431) |

| — |

| 4,815 |

| — |

| (210,295) |

Income before income tax expenses and share of loss from equity method investments |

| 2,926,944 |

| 3,425,053 |

| 39,514 |

| 23,406 |

| (3,056,310) |

| 3,358,607 |

Income tax expense |

| — |

| (430,098) |

| — |

| 16,136 |

| — |

| (413,962) |

Share of loss from equity method investments |

| — |

| (17,752) |

| — |

| — |

| — |

| (17,752) |

Net income |

| 2,926,944 |

| 2,977,203 |

| 39,514 |

| 39,542 |

| (3,056,310) |

| 2,926,893 |

Net loss attributable to non-controlling interest |

| — |

| 51 |

| — |

| — |

| — |

| 51 |

Net income attributable to ordinary shareholders of Futu Holdings Limited |

| 2,926,944 |

| 2,977,254 |

| 39,514 |

| 39,542 |

| (3,056,310) |

| 2,926,944 |

12

2021 | ||||||||||||

Subsidiaries | Consolidated | |||||||||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

| Futu Holdings |

| the WFOE) |

| WFOE |

| Entities |

| Adjustments |

| Totals | |

Selected Condensed Consolidating statements of Comprehensive Income Information |

|

|

|

|

|

|

|

|

|

|

|

|

Third-party revenues |

| 2,766 |

| 7,090,167 |

| — |

| 22,387 |

| — |

| 7,115,320 |

Inter-company revenues(3) |

| — |

| — |

| — |

| 187,774 |

| (187,774) |

| — |

Total costs(3) |

| — |

| (1,382,062) |

| — |

| (11,776) |

| 187,774 |

| (1,206,064) |

Total expenses |

| (26,854) |

| (2,558,736) |

| (46) |

| (140,807) |

| — |

| (2,726,443) |

Equity in gain of subsidiaries(2) |

| 2,816,673 |

| 52,695 |

| — |

| — |

| (2,869,368) |

| — |

Income of the VIEs | — | — | 52,741 | — | (52,741) | — | ||||||

Others, net |

| 17,625 |

| (14,841) |

| — |

| (306) |

| — |

| 2,478 |

Income before income tax expenses and share of loss from equity method investments |

| 2,810,210 |

| 3,187,223 |

| 52,695 |

| 57,272 |

| (2,922,109) |

| 3,185,291 |

Income tax expense |

| — |

| (370,550) |

| — |

| (4,531) |

| — |

| (375,081) |

Net income |

| 2,810,210 |

| 2,816,673 |

| 52,695 |

| 52,741 |

| (2,922,109) |

| 2,810,210 |

2020 | ||||||||||||

|

| Subsidiaries |

|

| Consolidated |

|

| |||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

Futu Holdings | the WFOE) | WFOE | Entities | Adjustments | Totals | |||||||

Selected Condensed Consolidating statements of Comprehensive Income Information |

|

|

|

|

|

| ||||||

Third-party revenues |

| 3,189 |

| 3,298,700 |

| — |

| 8,933 |

| — |

| 3,310,822 |

Inter-company revenues(3) | — | — | — | 94,500 | (94,500) | — | ||||||

Total costs(3) |

| (191) |

| (777,589) |

| — |

| (12,674) |

| 94,500 |

| (695,954) |

Total expenses |

| (23,388) |

| (1,051,012) |

| (53) |

| (72,554) |

| — |

| (1,147,007) |

Equity in gain of subsidiaries(2) |

| 1,347,485 |

| 21,088 |

| — |

| — |

| (1,368,573) |

| — |

Income of the VIEs | — | — | 20,727 | — | (20,727) | — | ||||||

Others, net |

| (1,572) |

| (17,955) |

| 413 |

| 1,876 |

| — |

| (17,238) |

Income before income tax expenses and share of loss from equity method investments |

| 1,325,523 |

| 1,473,232 |

| 21,087 |

| 20,081 |

| (1,389,300) |

| 1,450,623 |

Income tax expense |

| — |

| (125,439) |

| — |

| 646 |

| — |

| (124,793) |

Share of loss from equity method investments |

| — |

| (307) |

| — |

| — |

| — |

| (307) |

Net income |

| 1,325,523 |

| 1,347,486 |

| 21,087 |

| 20,727 |

| (1,389,300) |

| 1,325,523 |

13

Selected Condensed Consolidating statements of Cash Flows Information

| 2022 | |||||||||||

Subsidiaries | Consolidated | |||||||||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

| Futu Holdings |

| the WFOE) |

| WFOE |

| Entities |

| Adjustments |

| Totals | |

Selected Condensed Consolidating statements of Cash Flows Information |

|

|

|

|

|

| ||||||

Net cash (used in) /generated from operating activities(4) |

| (16,691) |

| 3,456,925 |

| (30) |

| 34,727 |

| — |

| 3,474,931 |

Advances to Group companies |

| (168,018) |

| (8,120) |

| — |

| — |

| 176,138 |

| — |

Receival of advances repayment from Group companies |

| 3,571,337 |

| 8,120 |

| — |

| — |

| (3,579,457) |

| — |

Investments in subsidiaries |

| (703,880) |

| — |

| — |

| — |

| 703,880 |

| — |

Other investing activities |

| 1,187,185 |

| (1,090,125) |

| — |

| (3,201) |

| — |

| 93,859 |

Net cash generated from/(used in) investing activities |

| 3,886,624 |

| (1,090,125) |

| — |

| (3,201) |

| (2,699,439) |

| 93,859 |

Proceeds from advances from Group companies |

| — |

| 168,018 |

| — |

| 8,120 |

| (176,138) |

| — |

Repayment of advances from Group companies |

| — |

| (3,571,337) |

| — |

| (8,120) |

| 3,579,457 |

| — |

Capital contribution from Group companies |

| — |

| 703,880 |

| — |

| — |

| (703,880) |

| — |

Other financing activities |

| (3,819,478) |

| (3,190,043) |

| — |

| — |

| — |

| (7,009,521) |

Net cash (used in)/generated from financing activities |

| (3,819,478) |

| (5,889,482) |

| — |

| — |

| 2,699,439 |

| (7,009,521) |

Effect of exchange rate changes on cash, cash equivalents and restricted cash |

| (244) |

| (133,476) |

| — |

| (1,476) |

| — |

| (135,196) |

Net increase/(decrease) in cash, cash equivalents and restricted cash |

| 50,211 |

| (3,656,158) |

| (30) |

| 30,050 |

| — |

| (3,575,927) |

Cash, cash equivalents and restricted cash at beginning of the year |

| 37,573 |

| 59,251,153 |

| 35 |

| 2,751 |

| — |

| 59,291,512 |

Cash, cash equivalents and restricted cash at end of the year |

| 87,784 |

| 55,594,995 |

| 5 |

| 32,801 |

| — |

| 55,715,585 |

2021 | ||||||||||||

Subsidiaries | Consolidated | |||||||||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

| Futu Holdings |

| the WFOE) |

| WFOE |

| Entities |

| Adjustments |

| Totals | |

Selected Condensed Consolidating statements of Cash Flows Information |

|

|

|

|

|

|

|

|

|

|

|

|

Net cash (used in) /generated from operating activities(4) |

| (16,465) |

| 6,026,081 |

| 15 |

| 2,340 |

| — |

| 6,011,971 |

Advances to Group companies |

| (4,814,377) |

| — |

| — |

| — |

| 4,814,377 |

| — |

Receival of advances repayment from Group companies |

| 2,039,648 |

| — |

| — |

| — |

| (2,039,648) |

| — |

Investments in subsidiaries |

| (5,480,918) |

| — |

| — |

| — |

| 5,480,918 |

| — |

Other investing activities |

| (1,169,715) |

| 209,477 |

| — |

| (3,327) |

| — |

| (963,565) |

Net cash (used in)/generated from investing activities |

| (9,425,362) |

| 209,477 |

| — |

| (3,327) |

| 8,255,647 |

| (963,565) |

Proceeds from advances from Group companies |

| — |

| 4,814,377 |

| — |

| — |

| (4,814,377) |

|

|

Repayment of advances from Group companies |

| — |

| (2,039,648) |

| — |

| — |

| 2,039,648 |

| — |

Proceeds from issuance of ordinary shares |

| 10,856,524 |

| — |

| — |

| — |

| — |

| 10,856,524 |

Capital contribution from Group companies |

| — |

| 5,480,918 |

| — |

| — |

| (5,480,918) |

| — |

Other financing activities |

| (1,414,672) |

| 1,112,366 |

| — |

| — |

| — |

| (302,306) |

Net cash generated from/(used in) financing activities |

| 9,441,852 |

| 9,368,013 |

| — |

| — |

| (8,255,647) |

| 10,554,218 |

Effect of exchange rate changes on cash, cash equivalents and restricted cash |

| 200 |

| 166,930 |

| — |

| — |

| — |

| 167,130 |

Net increase/(decrease) in cash, cash equivalents and restricted cash |

| 225 |

| 15,770,501 |

| 15 |

| (987) |

| — |

| 15,769,754 |

Cash, cash equivalents and restricted cash at beginning of the year |

| 37,349 |

| 43,480,651 |

| 20 |

| 3,738 |

| — |

| 43,521,758 |

Cash, cash equivalents and restricted cash at end of the year |

| 37,574 |

| 59,251,152 |

| 35 |

| 2,751 |

| — |

| 59,291,512 |

14

2020 | ||||||||||||

|

| Subsidiaries |

|

| Consolidated |

|

| |||||

(excluding | Affiliated | Eliminating | Consolidated | |||||||||

Futu Holdings | the WFOE) | WFOE | Entities | Adjustments | Totals | |||||||

Selected Condensed Consolidated statements of Cash Flows Information |

|

|

|

|

|

|

|

|

|

|

|

|

Net cash (used in) /generated from operating activities(4) |

| (30,551) |

| 20,502,112 |

| 3 |

| (14,847) |

| — |

| 20,456,717 |

Advances to Group companies |

| (3,049,229) |

| — |

| — |

| — |

| 3,049,229 |

| — |

Receival of advances repayment from Group companies | 779,604 | — | — | — | (779,604) | — | ||||||

Investments in subsidiaries |

| (1,869,682) |

| — |

| — |

| — |

| 1,869,682 |

| — |

Other investing activities |

| — |

| (261,279) |

| — |

| 17,104 |

| — |

| (244,175) |

Net cash (used in)/generated from investing activities |

| (4,139,307) |

| (261,279) |

| — |

| 17,104 |

| 4,139,307 |

| (244,175) |

Proceeds from advances from Group companies |

| — |

| 3,049,229 |

| — |

| — |

| (3,049,229) |

| — |

Repayment of advances from Group companies | — | (779,604) | — | — | 779,604 | — | ||||||

Proceeds from issuance of ordinary shares |

| 2,339,718 |

| — |

| — |

| — |

| — |

| 2,339,718 |

Capital contribution from Group companies | — | 1,869,682 | — | — | (1,869,682) | — | ||||||

Other financing activities |

| 1,859,532 |

| 4,207,646 |

| — |

| — |

| — |

| 6,067,178 |

Net cash generated from/(used in) financing activities |

| 4,199,250 |

| 8,346,953 |

| — |

| — |

| (4,139,307) |

| 8,406,896 |

Effect of exchange rate changes on cash, cash equivalents and restricted cash |

| (33) |

| (1,084) |

| — |

| — |

| — |

| (1,117) |

Net increase in cash, cash equivalents and restricted cash |

| 29,359 |

| 28,586,702 |

| 3 |

| 2,257 |

| — |

| 28,618,321 |

Cash, cash equivalents and restricted cash at beginning of the year |

| 7,990 |

| 14,893,949 |

| 17 |

| 1,481 |

| — |

| 14,903,437 |

Cash, cash equivalents and restricted cash at end of the year |

| 37,349 |

| 43,480,651 |

| 20 |

| 3,738 |

| — |

| 43,521,758 |

Notes:

| (1) | Represents the elimination of intercompany balances among Futu Holdings, Consolidated Affiliated Entities and our subsidiaries. |

| (2) | Represents the elimination of the investment in Consolidated Affiliated Entities and our subsidiaries by Futu Holdings. |

| (3) | Intercompany Revenues between Shenzhen Futu and Our Subsidiaries (excluding the WFOE). Shenzhen Futu provides software development services and technical consulting services to our subsidiaries. For the years ended December 31, 2020, 2021 and 2022, technical service fees charged by Shenzhen Futu were HK$94.5 million, HK$187.8 million and HK$202.8 million (US$26.0 million), respectively. The intercompany service charge is eliminated at the consolidation level. |

Intercompany Revenues between Shenzhen Futu and the WFOE. Pursuant to the exclusive technology consulting and services agreement entered into in October 2014, between Shenzhen Futu and the WFOE, which was subsequently amended and restated in May 2015 and further in September 2018, the WFOE had the exclusive right to provide Shenzhen Futu with consulting and services related to, among other things, technology research and development, as well as maintenance of software and hardware. Shenzhen Futu agreed to pay the WFOE a service fee in an amount equal to its annual net income. The WFOE may adjust the amount of service fee based on factors such as the complexity, time spent and the commercial value of the services. On September 30, 2021, a termination agreement was entered into among the WFOE, Shenzhen Futu and its shareholders, pursuant to which the parties agreed to terminate the prior contractual arrangements and replaced them with a new set of agreements. Pursuant to the exclusive business cooperation agreement entered into on September 30, 2021 by and among the WFOE, Shenzhen Futu and its shareholders, Shenzhen Futu engaged the WFOE as the exclusive service provider of technical support, consulting services and other services. Shenzhen Futu agrees to pay the WFOE service fees for any fiscal year in an amount equal to 100% of Shenzhen Futu’s consolidated gross profits of such year, after offsetting the accumulated losses of Shenzhen Futu and its subsidiaries in previous fiscal years (if any) and after deducting working capital, expenditure, taxes and other statutory contributions required in such year. For the years ended December 31, 2020, 2021 and 2022, the WFOE did not charge Shenzhen Futu any service fee.

| (4) | For the years ended December 31, 2020, 2021 and 2022, our subsidiaries paid the VIEs technical service fees of HK$33.7 million, HK$189.8 million and HK$148.1 million (US$19.0 million), respectively. |

We expect that the financial position, results of operations and cash flows of the Consolidated Affiliated Entities will constitute an immaterial portion of our consolidated financial information for the foreseeable future. However, there can be no assurance that the risks associated with the Contractual Arrangements, if materialized, would not materially and adversely impact our financial position, results of operations, prospects or the value of the ADSs.

15

Transfer of Cash Within Our Group

Although we consolidate the financial results of the Consolidated Affiliated Entities under U.S. GAAP, we only have access to the assets or earnings of the Consolidated Affiliated Entities through the Contractual Arrangements. The cash flows that have occurred between the Consolidated Affiliated Entities, on the one hand, and Futu Holdings and its subsidiaries, on the other hand, are summarized as follows:

For the year ended December 31, | ||||||||

2020 | 2021 | 2022 | ||||||

| HK$ |

| HK$ |

| HK$ |

| US$ | |

| (in thousands) | |||||||

Cash paid by our subsidiaries to the VIEs for technical service fee |

| 33,669 |

| 189,827 |

| 148,058 |

| 18,978 |

Advances from our subsidiaries to the VIEs |

| — |

| — |

| 8,120 |

| 1,041 |

Repayment of advances to our Group by the VIEs |

| — |

| — |

| (8,120) |

| (1,041) |

Restrictions and Limitations on Transfer of Cash

Futu Holdings is incorporated in the Cayman Islands and its businesses in China are conducted mainly through its PRC subsidiaries and partly through the Consolidated Affiliated Entities. We face various restrictions and limitations on foreign exchange, our ability to transfer cash between entities, across borders and to U.S. investors, and our ability to distribute earnings from our subsidiaries and/or the Consolidated Affiliated Entities, to Futu Holdings and holders of the ADSs as well as the ability to collect amounts owed under the Contractual Arrangements.

Uncertainties regarding the interpretation and implementation of the Contractual Arrangements could limit our ability to enforce such arrangements. If the PRC authorities determine that the Contractual Arrangements do not comply with PRC regulations, or if current regulations change or are interpreted differently in the future, our ability to collect amounts owed under the Contractual Arrangements may be seriously hindered.

Current PRC regulations permit our PRC subsidiaries, including the WFOE, to pay dividends to us only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, each of our PRC subsidiaries and the Consolidated Affiliated Entities are required to set aside at least 10% of their respective accumulated profits each year, if any, to fund certain reserve funds until the total amount set aside reaches 50% of their respective registered capital. Our PRC subsidiaries and the Consolidated Affiliated Entities may also allocate a portion of their after-tax profits based on PRC accounting standards to employee welfare and bonus funds at their discretion. These reserves are not distributable as cash dividends. Furthermore, if the WFOE incurs debt on its own behalf in the future, the instruments governing the debt may restrict its ability to pay dividends or make other payments to us. In addition, the PRC tax authorities may require us to adjust our taxable income under the Contractual Arrangements in a manner that would materially and adversely affect the WFOE’s ability to pay dividends and other distributions to us. Any limitation on the ability of our PRC subsidiaries, including the WFOE, to distribute dividends to us or on the ability of the VIEs to make payments to the WFOE may restrict our ability to satisfy our liquidity requirements. See “Item 4. Information on the Company—B. Business Overview—Regulation—Overview of the Laws and Regulations Relating to Our Business and Operations in China—Regulations on Foreign Exchange—Regulations on Dividend Distribution.”

Futu Securities (Hong Kong) Limited, our wholly-owned subsidiary and the sole registered shareholder of the WFOE, may be considered a non-resident enterprise for tax purposes, so that any dividends paid by our PRC subsidiaries, including the WFOE, to Futu Securities (Hong Kong) Limited may be regarded as China-sourced income and, as a result, may be subject to PRC withholding tax at a rate of up to 10%. If we are required under the PRC Enterprise Income Tax Law to pay income tax for any dividends we receive from PRC subsidiaries, or if Futu Securities (Hong Kong) Limited is determined by the PRC government authority as receiving benefits from reduced income tax rate due to a structure or arrangement that is primarily tax-driven, it would materially and adversely affect the amount of dividends, if any, we may pay to our shareholders and ADS holders. If the PRC tax authorities determine that Futu Holdings is a PRC resident enterprise for enterprise income tax purposes, we may be required to withhold a 10% tax from dividends we pay to our shareholders and ADS holders, in each case that are non-resident enterprises. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China—Dividends payable to our foreign investors and gains on the sale of the ADSs or Class A ordinary shares by our foreign investors may become subject to PRC tax.”

16

In addition, non-resident enterprise shareholders, including holders of the ADSs, may be subject to PRC tax at a rate of 10% on gains realized on the sale or other disposition of ADSs or ordinary shares if such income is treated as sourced from within the PRC. Furthermore, if Futu Holdings were deemed to be a PRC resident enterprise, dividends paid to our non-PRC individual shareholders, including holders of the ADSs, and any gain realized on the transfer of ADSs or ordinary shares by such holders may be subject to PRC tax at a rate of 20% which in the case of dividends may be withheld at source. Any such tax may reduce the returns on your investment in the ADSs or ordinary shares. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China—We may be treated as a resident enterprise for PRC tax purposes under the PRC Enterprise Income Tax Law, and we may therefore be subject to PRC income tax on our global income.”

Our non-PRC entities are permitted under PRC laws and regulations to provide funding to our PRC subsidiaries only through loans or capital contributions, subject to the approval of government authorities and limits on the amount of capital contributions and loans. This may delay or prevent us from using the proceeds from our offshore capital raising activities to make loans or capital contribution to our PRC subsidiaries. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Operations in China—PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using the proceeds of our securities offerings to make loans or additional capital contributions to our PRC subsidiaries and the Consolidated Affiliated Entities.”

Additionally, the PRC government imposes controls on the convertibility of the Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. Under existing PRC foreign exchange regulations, payments of current account items, such as profit distributions and trade and service-related foreign exchange transactions, can be made in foreign currencies without prior approval from the State Administration of Foreign Exchange of the PRC, or the SAFE, by complying with certain procedural requirements. Dividends payments to us by Futu Securities (Hong Kong) Limited in foreign currencies are subject to the condition that the remittance of such dividends outside of the PRC complies with certain procedures under PRC foreign exchange regulations, such as the overseas investment registrations by our shareholders or the ultimate shareholders of our corporate shareholders who are PRC residents. Approvals by or registration with appropriate government authorities is required where Renminbi is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currencies to satisfy our foreign currency demands, our PRC subsidiaries, including the WFOE, may not be able to pay dividends in foreign currencies to us and our access to cash generated from its operations will be restricted. See “Item 3.D. Key Information—Risk Factors—Risks Related to Our Operations in China—We are subject to PRC restrictions on currency exchange.”

Taxation on Dividends or Distributions

Futu Holdings’ source of dividend partly comes from dividends paid by its PRC subsidiaries, including the WFOE, which in part depends on payments received from the VIEs under the Contractual Arrangements. None of our subsidiaries has declared or paid any dividend or distribution to us as of the date of this annual report. We have never declared or paid any dividend on our ordinary shares, and we have no current intention to pay dividends to shareholders or holders of ADSs. We currently intend to retain most, if not all, of our available funds and any future earnings to fund the development and growth of our business. The undistributed earnings that are subject to dividend tax are expected to be indefinitely reinvested for the foreseeable future.

17

Under the current laws of the Cayman Islands, Futu Holdings is not subject to tax on income or capital gains. Upon payments of dividends to our shareholders, no Cayman Islands withholding tax will be imposed. For purposes of illustration, the following discussion reflects the hypothetical taxes that might be required to be paid in Mainland China and Hong Kong, assuming that: (i) we have taxable earnings in the VIEs, and (ii) we determine to pay a dividend in the future:

Hypothetical pre-tax earnings in the VIEs(1) |

| 100.00 |

Tax on earnings at statutory rate of 25% at WFOE level(2) |

| (25.00) |

Amount to be distributed as dividend from WFOE to Futu Securities (Hong Kong) Limited(3) |

| 75.00 |

Withholding tax at tax treaty rate of 5 % | (3.75) | |

Amount to be distributed as dividend at Futu Securities (Hong Kong) Limited level and net distribution to Futu Holdings(4) |

| 71.25 |

Notes:

| (1) | For purposes of this example, the tax calculation has been simplified. The hypothetical book pre-tax earnings amount is assumed to equal PRC taxable income. |

| (2) | Certain of our subsidiaries and the VIEs qualify for a 15% preferential income tax rate in China. However, such rate is subject to qualification, is temporary in nature, and may not be available in a future period when distributions are paid. For purposes of this hypothetical example, the table above reflects a maximum tax scenario under which the full statutory rate would be effective. |

| (3) | The PRC Enterprise Income Tax Law imposes a withholding income tax of 10% on dividends distributed by a Foreign Invested Enterprise to its immediate holding company outside of Mainland China. A lower withholding income tax rate of 5% is applied if the Foreign Invested Enterprise’s immediate holding company is registered in Hong Kong or other jurisdictions that have a tax treaty arrangement with Mainland China, subject to a qualification review at the time of the distribution. There is no incremental tax at Futu Securities (Hong Kong) Limited level for any dividend distribution to Futu Holdings. |

| (4) | If a 10% withholding income tax rate is imposed, the withholding tax will be 7.5 and the amount to be distributed as dividend at Futu Securities (Hong Kong) Limited level and net distribution to Futu Holdings will be 67.5. |

The table above has been prepared under the assumption that all profits of the VIEs will be distributed as fees to the WFOE under tax neutral Contractual Arrangements. If, in the future, the accumulated earnings of the VIEs exceed the service fees paid to the WFOE (or if the current and contemplated fee structure between the intercompany entities is determined to be non-substantive and disallowed by PRC tax authorities), the VIEs could make a non-deductible transfer to the WFOE for the amounts of the stranded cash in the VIEs. This would result in such transfer being non-deductible expenses for the VIEs but still taxable income for the WFOE. Our management believes that there is only a remote possibility that this scenario would happen.

Should all tax planning strategies fail, the VIEs could, as a matter of last resort, make a non-deductible transfer to the WFOE for amounts of stranded cash in the VIEs. This would result in the double taxation of earnings: once at the VIE level (non-deductible expense) and again at the WFOE level (for presumptive earnings on the transfer). This has the impact of reducing the amount available above from 71.25% to approximately 53% of pre-tax income, respectively. Our management believes this scenario to be remote.

18

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. Reserved

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

An investment in our ADSs or ordinary shares involves significant risks. Below please find a summary of the principal risks we face, organized under relevant headings. All the operational risks associated with being based in and having operations in Mainland China also apply to operations in Hong Kong. With respect to the legal risks associated with being based in and having operations in Mainland China, the laws, regulations and the discretion of Mainland China governmental authorities discussed in this annual report are expected to apply to Mainland China entities and businesses, rather than entities or businesses in Hong Kong which operate under a different set of laws from Mainland China.

Risks Related to Our Business and Industry

| ● | Our historical growth rates may not be indicative of our future growth, which makes it difficult to evaluate our future prospects. |

| ● | We are subject to extensive and evolving regulatory requirements in the markets we operate in, non-compliance with which may result in penalties, limitations and prohibitions on our future business activities or suspension or revocation of our licenses and trading rights, and consequently may materially and adversely affect our business, financial condition, operations and prospects. In addition, we are involved in certain inquiries and investigation by relevant regulators. |

| ● | Our online client onboarding procedures historically did not strictly follow the specified steps set out by the relevant authorities in Hong Kong, which may subject us to regulatory actions in addition to remediation, which may include reprimands, fines, limitations or prohibitions on our future business activities and/or suspension or revocation of Futu Securities’ licenses and trading rights, and consequently may adversely affect our business, financial condition, operations, brand reputation and prospects. |

19

| ● | We do not hold any license or permit for providing securities brokerage services in Mainland China. As announced by the CSRC on December 30, 2022, the CSRC has initiated inquiries on us regarding our cross-border operations in Mainland China, including the provision of cross-border securities services for domestic investors. We have taken and may continue to take rectification measures based on our communication with or the requirements from the CSRC. If the CSRC is not satisfied with our rectification measures or the CSRC imposes other further regulatory actions or penalties on us, our business and results of operations may be materially and adversely affected. |