UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended | |

|

|

OR | |

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. | |

For the transition period from to

Commission file number

(Exact name of Registrant as specified in its charter) |

|

(Jurisdiction of incorporation or organization) |

|

People’s Republic of |

(Address of principal executive offices) |

|

Contact Person: Chief Financial Officer + People’s Republic of |

* (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

9698 | The Stock Exchange of Hong Kong | |||

|

|

* Not for trading, but only in connection with the registration of American Depositary Shares representing such Class A ordinary shares pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Title of class |

| Number of shares outstanding |

Class A ordinary shares were outstanding as of December 31, 2022 | ||

Class B ordinary shares were outstanding as of December 31, 2022 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

⌧

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ⌧

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

⌧

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

⌧

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Accelerated filer ☐ | Non-accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

GDS HOLDINGS LIMITED

FORM 20-F ANNUAL REPORT

FISCAL YEAR ENDED DECEMBER 31, 2022

7 | |||

7 | |||

7 | |||

7 | |||

85 | |||

147 | |||

147 | |||

180 | |||

198 | |||

200 | |||

201 | |||

202 | |||

212 | |||

213 | |||

218 | |||

218 | |||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 218 | ||

219 | |||

219 | |||

220 | |||

220 | |||

220 | |||

PURCHASE OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 220 | ||

220 | |||

221 | |||

222 | |||

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | 223 | ||

223 | |||

223 | |||

223 | |||

223 | |||

224 | |||

i

Conventions That Apply to This Annual Report on Form 20-F

Unless we indicate otherwise, references in this annual report on Form 20-F to:

| ● | “2019 PRC Foreign Investment Law” are to the PRC Foreign Investment Law promulgated by the National People’s Congress in March 2019, which became effective on January 1, 2020; |

| ● | “ADSs” are to our American depositary shares, each of which represents eight Class A ordinary shares, and “ADRs” are to the American depositary receipts that evidence our ADSs; |

| ● | “area committed” are to that part of our area in service which is committed to customers pursuant to customer agreements remaining in effect; |

| ● | “area held for future development” are to the estimated net floor area that we have secured for potential future development by different means, which are not actively under construction; |

| ● | “area in service” are to the entire net floor area of data centers (or phases of data centers) which are ready for service; |

| ● | “area pre-committed” are to that part of our area under construction which is pre-committed to customers pursuant to customer agreements remaining in effect; |

| ● | “area under construction” are to the entire net floor area of data centers (or phases of data centers) which are actively under construction and have not yet reached the stage of being ready for service; |

| ● | “area utilized” are to that part of our area in service that is committed to customers and revenue generating pursuant to the terms of customer agreements remaining in effect; |

| ● | “Articles” or “Articles of Association” are to our Articles of Association (as amended from time to time), adopted on June 29, 2021 and effective on June 29, 2021; |

| ● | “build-operate-transfer data centers” or “B-O-T data centers” are to data centers that we undertake to build and operate for specific customers for their exclusive use, and transfer to such customers at the end of the contract period; |

| ● | “carrier-neutral” or “cloud-neutral” are to data centers that are not owned, operated, or tied to any one network or cloud service provider, respectively; |

| ● | “CBIRC” are to the China Banking and Insurance Regulatory Commission, the predecessor of the State Administration for Financial Regulation of the PRC; |

| ● | “CCASS” are to the Central Clearing and Settlement System established and operated by Hong Kong Securities Clearing Company Limited, a wholly-owned subsidiary of Hong Kong Exchanges and Clearing Limited; |

| ● | “China” and the “PRC” are to the People’s Republic of China, excluding, for the purposes of this annual report only, Taiwan, and the special administrative regions of Hong Kong and Macau; |

| ● | “Circular 82” are to the Notice Regarding the Determination of Chinese-controlled Offshore-Incorporated Enterprises as PRC Tax Resident Enterprises on the basis of de facto management bodies, issued on April 22, 2009 and further amended on December 29, 2017; |

| ● | “Class A ordinary shares” are to Class A ordinary shares in the share capital of our company with a par value of US$0.00005 each, conferring a holder of a Class A ordinary share to one vote per share on any resolution tabled at our general meeting; |

1

| ● | “Class B ordinary shares” are to Class B ordinary shares in the share capital of our company with a par value of US$0.00005 each, conferring weighted voting rights in our company such that a holder of a Class B ordinary share is entitled to 20 votes per share on resolutions tabled at our general meeting for (i) the election or removal of a simple majority, or six, of our directors; and (ii) any change to our Articles of Association that would adversely affect the rights of Class B shareholders, and which are convertible into Class A ordinary shares, and will automatically convert into Class A ordinary shares under certain circumstances; |

| ● | “commitment rate” are to the ratio of area committed to area in service; |

| ● | “Companies (WUMP) Ordinance” are to the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32 of the Laws of Hong Kong), as amended or supplemented from time to time; |

| ● | “Controlling Shareholders” are to Mr. Huang and STT GDC, unless the context otherwise requires; such term has the meaning ascribed to it under the Hong Kong Listing Rules; |

| ● | “CSRC” are to the China Securities Regulatory Commission; |

| ● | “Data Center Operation Management Platform” are to the platform we developed and operate which provides real-time information on many aspects of data center operating performance; |

| ● | “DTC” are to The Depository Trust Company, the central book-entry clearing and settlement system for equity securities in the United States and the clearance system for our ADSs; |

| ● | “Entity List” are to the list maintained by the United States or U.S. Department of Commerce identifying foreign entities believed to be involved, or pose a significant risk of being or becoming involved, in activities contrary to the national security or foreign policy interests of the United States and which are prohibited from acquiring some or all items subject to the U.S. Export Administration Regulations, or EAR; |

| ● | “ESG report” or “Environmental, Social and Governance Report” are to all ESG reports that we have issued, namely, our 2020 ESG report, which is accessible via hyperlink in our press release, Exhibit 99.1 to our Form 6-K (File No. 001-37925), furnished to the SEC on November 30, 2021, and our 2021 ESG report, which is accessible via hyperlink in our press release, Exhibit 99.1 to our Form 6-K (File No. 001-37925), furnished to the SEC on December 1, 2022; |

| ● | “foreign private issuer” are to such term as defined in Rule 3b-4 under the U.S. Exchange Act; |

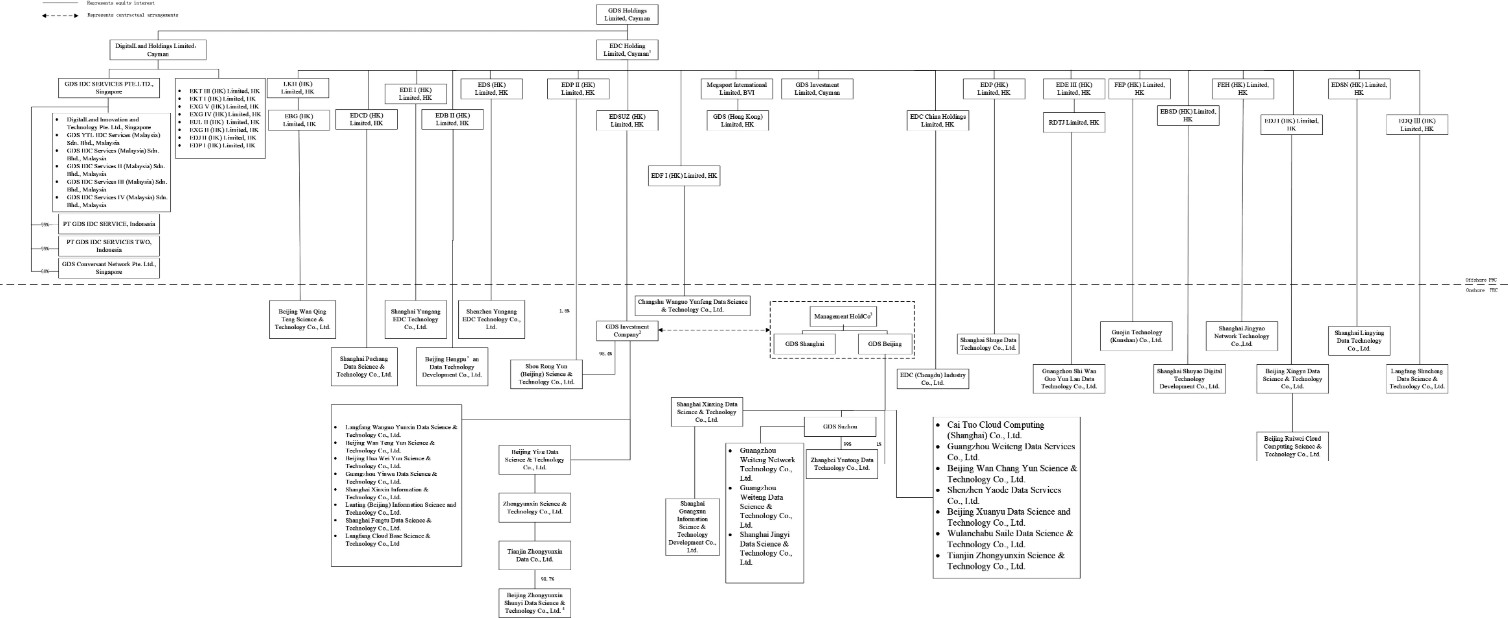

| ● | “GDS Beijing” are to Beijing Wanguo Chang’an Science and Technology Co., Ltd., a limited liability company established in the PRC on May 30, 2006 and a wholly-owned subsidiary of Management HoldCo; |

| ● | “GDS Holdings,” “company,” “our company,” “we,” “our” or “us” are to GDS Holdings Limited, a company incorporated in the Cayman Islands with limited liability on December 1, 2006 and, where the context requires, its consolidated subsidiaries and the consolidated affiliated entities, including the variable interest entities and their subsidiaries, from time to time; |

| ● | “GDS International”, are to DigitalLand Holdings Limited, a company incorporated in the Cayman Islands with limited liability on May 18, 2022, which is the holding company of its consolidated subsidiaries and the consolidated affiliated entities conducting international business and operation outside mainland China; |

| ● | “GDS Investment Company” are to GDS (Shanghai) Investment Co., Ltd. (formerly known as Shanghai Free Trade Zone GDS Management Co., Ltd.), a limited liability company established in the PRC on December 30, 2015 and our wholly-owned indirect subsidiary; |

| ● | “GDS Shanghai” are to Shanghai Shu’an Data Services Co., Ltd., a limited liability company established in the PRC on May 4, 2011 and a wholly-owned subsidiary of Management HoldCo; |

2

| ● | “GDS Suzhou” are to Global Data Solutions Co., Ltd., a limited liability company established in the PRC on September 30, 2000 and a wholly-owned subsidiary of GDS Beijing; |

| ● | “GIC” are to GIC Private Limited, Singapore’s sovereign wealth fund; |

| ● | “gross floor area” are either to the total internal area of buildings which we own, or to the total area under lease with respect to buildings which we lease; |

| ● | “Group,” “our Group” or “the Group” are to GDS Holdings Limited and its subsidiaries (including the variable interest entities) from time to time; |

| ● | “HK$,” “Hong Kong dollars” or “HK dollars” are to Hong Kong dollars, the lawful currency of Hong Kong; |

| ● | “Hong Kong,” “HK” or “Hong Kong S.A.R.” are to the Hong Kong Special Administrative Region of the PRC; |

| ● | “Hong Kong Listing Rules” are to the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited, as amended or supplemented from time to time; |

| ● | “Hong Kong Share Registrar” are to Computershare Hong Kong Investor Services Limited; |

| ● | “Hong Kong Stock Exchange” are to The Stock Exchange of Hong Kong Limited; |

| ● | “IDC(s)” are to internet data center(s); |

| ● | “M&A Rules” are to the Rules on the Merger and Acquisition of Domestic Enterprises by Foreign Investors jointly issued by MOFCOM, SASAC, STA, CSRC, SAIC and SAFE on August 8, 2006, effective on September 8, 2006 and further amended on June 22, 2009 by MOFCOM; |

| ● | “Macau” or “Macau S.A.R.” are to the Macau Special Administrative Region of the PRC; |

| ● | “Management HoldCo” are to Shanghai Xinwan Enterprise Management Co., Ltd., a limited liability company established in the PRC on October 16, 2019; as of February 28, 2023, the shareholders of Management HoldCo were Yilin Chen (senior vice president, product and service and Southeast Asia business), Yan Liang (senior vice president, design, operation and delivery), Kejing Zhang (senior vice president, sales), Andy Wenfeng Li (general counsel, compliance officer, and company secretary) and Qi Wang (senior vice president, cloud and network business); such shareholders were designated by the board of directors of our company; |

| ● | “Memorandum” or “Memorandum of Association” are to our memorandum of association (as amended from time to time); |

| ● | “MIIT” are to the Ministry of Industry and Information Technology; |

| ● | “MOFCOM” are to the Ministry of Commerce of the PRC; |

| ● | “move-in period” are to the period commencing when part of the area committed under a particular customer agreement becomes area utilized and ending when all of the area committed under such customer agreement becomes area utilized in accordance with the terms of such customer agreement remaining in effect; |

| ● | “Mr. Huang” are to Mr. William Wei Huang, the founder, chairman of the board, and chief executive officer of our company and a Controlling Shareholder; |

| ● | “Nasdaq” are to the Nasdaq Global Market; |

3

| ● | “NDRC” are to the National Development and Reform Commission; |

| ● | “Negative List (2021)” are to the Special Administrative Measures (Negative List) for Foreign Investment Access, most recently jointly promulgated by the MOFCOM and the NDRC on December 27, 2021 and which became effective on January 1, 2022, as amended, supplemented or otherwise modified from time to time; |

| ● | “net floor area” are to the total internal area of the computer rooms within each data center where customers can house, power and cool their computer systems and networking equipment; |

| ● | “ordinary shares” are to, collectively, our Class A ordinary shares and Class B ordinary shares, par value US$0.00005 per share; |

| ● | “PBOC” are to the People’s Bank of China; |

| ● | “PCAOB” are to the Public Company Accounting Oversight Board; |

| ● | “PRC government” or “State” are to the central government of the PRC, including all political subdivisions (including provincial, municipal and other regional or local government entities) and its organs or, as the context requires, any of them; |

| ● | “pre-commitment rate” are to the ratio of area pre-committed to area under construction; |

| ● | “Principal Share Registrar” are to Conyers Trust Company (Cayman) Limited; |

| ● | “PUE” are to power usage effectiveness; |

| ● | “PUE ratio” are to power usage effectiveness ratio, a metric used to determine the energy efficiency of a data center; it is determined by dividing the total amount of power consumed by the data center by the total amount of power consumed directly by customers to operate their IT systems housed in the data center; |

| ● | “ready for service” are to data centers (or phases of data centers) which have passed commissioning and testing, obtained government approvals for operation, are fully supplied with power, and contain one or more computer rooms fully equipped and fitted out ready for utilization by customers; |

| ● | “RMB” or “Renminbi” are to Renminbi, the lawful currency of the PRC; |

| ● | “SAFE” are to the State Administration of Foreign Exchange of the PRC, the PRC governmental agency responsible for matters relating to foreign exchange administration, including local branches, when applicable; |

| ● | “SAFE Circular 37” are to the Circular on Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Offshore Investment and Financing and Roundtrip Investment through Special Purpose Vehicles promulgated by SAFE with effect from July 4, 2014; |

| ● | “SAIC” or “SAMR” are to the State Administration for Industry and Commerce of the PRC, currently known as the PRC State Administration for Market Regulation; |

| ● | “SASAC” are to the State-owned Assets Supervision and Administration Commission of the State Council; |

| ● | “SCNPC” are to the Standing Committee of the National People’s Congress of the PRC; |

| ● | “SEC” are to the United States Securities and Exchange Commission; |

4

| ● | “self-developed data centers” are to data centers operated by us that we either purpose-build from the ground up, develop from building shells purpose-built for us, convert from existing buildings, acquire, or build, operate, and transfer pursuant to contacts with specific customers; |

| ● | “SFO” are to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong), as amended or supplemented from time to time; |

| ● | “shareholder(s)” are to holder(s) of ordinary shares and, where the context requires, ADSs; |

| ● | “sqm” are to square meters; |

| ● | “STA” are to the State Taxation Administration of the PRC; |

| ● | “State Council” are to the PRC State Council; |

| ● | “STT GDC” are to STT GDC Pte. Ltd., a private limited liability company incorporated in Singapore on November 21, 2012, and a wholly owned subsidiary of STT Communications Ltd., which is in turn a wholly owned subsidiary of Singapore Technologies Telemedia Pte. Ltd., or ST Telemedia; |

| ● | “Takeovers Codes” are to the Codes on Takeovers and Mergers and Share Buy-backs issued by the Securities and Futures Commission of Hong Kong; |

| ● | “third-party data centers” are to data center net floor area operated by us that we lease on a wholesale basis from other data center providers and use to provide data center services to our customers; |

| ● | “Tier 1 markets” are to the areas in and around the cities of Shanghai, Beijing, Shenzhen, Guangzhou, Hong Kong, Chengdu and Chongqing; |

| ● | “total area committed” are to the sum of area committed and area pre-committed; |

| ● | “UK” or “United Kingdom” are to the United Kingdom of Great Britain and Northern Ireland; |

| ● | “U.S.” or “United States” are to the United States of America, its territories, its possessions and all areas subject to its jurisdiction; |

| ● | “U.S. Exchange Act” are to the United States Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder; |

| ● | “U.S. GAAP” are to accounting principles generally accepted in the United States; |

| ● | “U.S. Securities Act” are to the United States Securities Act of 1933, as amended, and the rules and regulations promulgated thereunder; |

| ● | “US$” or “U.S. dollars” are to the legal currency of the United States; |

| ● | “utilization rate” are to the ratio of area utilized to area in service; |

| ● | “variable interest entities,” “VIE” or “VIEs” are to the variable interest entities that are 100% owned by PRC citizens or by PRC entities owned by PRC citizens, where applicable, that hold the VATS licenses, or other business operation licenses or approvals, in which foreign investment is restricted or prohibited, and are consolidated into our consolidated financial statements in accordance with U.S. GAAP as if they were our wholly-owned subsidiaries; |

5

| ● | “VAT” are to value-added tax; all amounts are exclusive of VAT in this annual report except where indicated otherwise; |

| ● | “VATS” are to value-added telecommunications services; |

| ● | “VIE structure” or “Contractual Arrangements with Affiliated Consolidated Entities” or “contractual arrangements with the consolidated VIEs” are to the variable interest entity structure; and |

| ● | “WFOE(s)” are to wholly foreign owned enterprise(s) incorporated in the PRC which is/are directly or indirectly wholly owned by our company. |

Unless specifically indicated otherwise or unless the context otherwise requires, all references to our ordinary shares exclude Class A ordinary shares issuable upon (i) conversion of our convertible senior notes and (ii) conversion of our convertible preferred shares.

This annual report contains translations between Renminbi and U.S. dollars solely for the convenience of the reader. The translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report were made at a rate of RMB6.8972 to US$1.00, the exchange rate set forth in the H.10 statistical release of the Federal Reserve Board on December 30, 2022. We make no representation that the Renminbi or U.S. dollar amounts referred to in this annual report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

This annual report includes our audited consolidated financial statements for the years ended December 31, 2020, 2021 and 2022.

Our ADSs are listed on the Nasdaq under the ticker symbol “GDS.” Our ordinary shares are listed on the Hong Kong Stock Exchange under the stock code “9698.”

Special Note Regarding Forward-Looking Statements

This annual report contains forward-looking statements that involve risks and uncertainties, including statements based on our current expectations, assumptions, estimates and projections about us and our industry. These forward-looking statements are made under the “safe harbor” provision under Section 21E of the U.S. Exchange Act and as defined in the Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. In some cases, these forward-looking statements can be identified by words or phrases such as “may”, “will”, “expect”, “anticipate”, “aim”, “estimate”, “intend”, “plan”, “believe”, “potential”, “continue”, “is/are likely to” or other similar expressions. The forward-looking statements included in this annual report relate to, among others:

| ● | our goals and strategies; |

| ● | our expansion plans; |

| ● | our future business development, financial condition and results of operations; |

| ● | the expected growth of the data center and cloud services market; |

| ● | our expectations regarding demand for, and market acceptance of, our services; |

| ● | our expectations regarding maintaining and strengthening our relationships with customers; |

| ● | the completion of any proposed acquisition transactions, including the regulatory approvals and other conditions that must be satisfied or waived in order to complete the acquisition transactions; |

| ● | international trade policies, protectionist policies and other policies that could place restrictions on economic and commercial activity; |

6

| ● | general economic and business conditions in the regions where we operate; and |

| ● | assumptions underlying or related to any of the foregoing. |

In addition, any projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate is necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Item 3. Key Information—D. Risk Factors” and elsewhere in this annual report. You should not place undue reliance on these forward-looking statements.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we have referred to in this annual report and have filed as exhibits hereto completely and with the understanding that our actual future results may be materially different from what we expect.

Other sections of this annual report include additional factors that could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not required.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not required.

ITEM 3. KEY INFORMATION

Our Corporate Structure and Contractual Arrangements with the Consolidated Affiliated Entities

GDS Holdings Limited is not an operating company in China, but instead is a Cayman Islands holding company. PRC laws and regulations impose certain restrictions or prohibitions on foreign ownership of companies that engage in telecommunications-related businesses, including the provision of VATS. Our internet data center businesses are classified as VATS by the PRC government. Accordingly, we operate substantially all of these business operations in China through the consolidated VIEs and their subsidiaries, as well as through our subsidiaries, and rely on contractual arrangements, described below, to control the business operations of the consolidated VIEs. GDS Holdings Limited has no equity ownership in the consolidated VIEs. Revenues contributed by the VIEs and their subsidiaries accounted for 95.0%, 96.1% and 96.1% of our total revenues for the years of 2020, 2021 and 2022, respectively. As used in this annual report, “we,” “us,” “our company,” “the Company” or “our” refers to a company incorporated in the Cayman Islands and, where the context requires, its consolidated subsidiaries and the consolidated affiliated entities, including the variable interest entities and their subsidiaries, from time to time. Investors in our ADSs are not purchasing an equity interest in the consolidated VIEs and their subsidiaries in China, but instead are purchasing an equity interest in a Cayman Islands holding company and its subsidiaries (excluding the VIEs and their subsidiaries).

7

Our wholly-owned PRC subsidiaries, the consolidated VIEs and their shareholders have entered into a series of contractual arrangements, including equity interest pledge agreements, shareholder voting rights proxy agreements, exclusive technology license and service agreements, intellectual property rights license agreements, exclusive call option agreements and loan agreements. The terms in each set of contractual arrangements with the consolidated VIEs and their shareholders are substantially similar. For more details of these contractual arrangements, see “Item 4. Information on the Company—C. Organizational Structure—Contractual Arrangements with Affiliated Consolidated Entities.” We rely on these contractual arrangements to control the business operations of the consolidated VIEs. As a result of these contractual arrangements, we are the primary beneficiary of Management HoldCo, GDS Shanghai, GDS Beijing and their respective subsidiaries, and, therefore, have consolidated their financial results in our consolidated financial statements in accordance with U.S. GAAP.

However, these contractual arrangements may not be as effective as direct ownership in providing us with control over the consolidated VIEs and we may have to incur substantial costs and expend significant resources to enforce such arrangements in reliance on legal remedies under PRC law. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We rely on contractual arrangements with the consolidated VIEs and their shareholders for our China operations, which may not be as effective as direct ownership in providing operational control and otherwise have a material adverse effect as to our business” and “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—The individual management shareholders of our Management HoldCo may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.”

There are also substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations and rules regarding the status of the rights of our Cayman Islands holding company with respect to the contractual arrangements. It is uncertain whether our corporate structure will be seen as violating the foreign investment rules as we are currently leveraging the contractual arrangements to operate businesses which are classified as VATS by the PRC government and are prohibited or restricted to foreign investment. Furthermore, if future legislation mandates further actions to be taken by companies with respect to existing contractual arrangements, we may face substantial uncertainties as to whether we can complete such actions in a timely manner, or at all. If we fail to take appropriate and timely measures to comply with any of these or similar regulatory compliance requirements, our current corporate structure, corporate governance, and business operations could be materially and adversely affected. Further, if our corporate structure or contractual arrangements were found to be in violation of any existing or future PRC laws or regulations, we could be subject to severe penalties, and the relevant regulatory authorities would have broad discretion in dealing with such violations. As a result, we would be unable to direct the activities of the consolidated VIEs and their subsidiaries, receive their economic benefits and/or claim our contractual control rights over the assets of the VIEs and their subsidiaries that conduct substantially all of our operations in China, we would no longer be able to consolidate such VIEs and their subsidiaries in our consolidated financial statements in accordance with U.S. GAAP, which would likely materially and adversely affect our financial condition and results of operations, and cause the value of our securities to significantly decline or become worthless. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government deems that the contractual arrangements in relation to the consolidated VIEs do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in the operations of the consolidated VIEs and their subsidiaries.” and “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure -Substantial uncertainties exist with respect to the interpretation and implementation of the 2019 PRC Foreign Investment Law and how it may impact the viability of our current corporate structure, corporate governance and business operations.”

In addition, we face various risks and uncertainties related to doing business in China. Our business operations are primarily conducted in China, and we are subject to complex and evolving PRC laws and regulations. For example, we face risks associated with regulatory approvals on offshore offerings, anti-monopoly regulatory actions, and oversight on cybersecurity and data security and protection, which may impact our ability to conduct certain businesses, accept foreign investments or financing, or list on a United States, Hong Kong or other foreign exchange. These risks could result in a material adverse change in our operations and the value of our ADSs, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause the value of our securities to significantly decline or become worthless. For more details of the risks we face related to doing business in China, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in People’s Republic of China.”

8

The PRC government’s significant authority in regulating our operations, as well as its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations of this nature may cause the value of our securities to significantly decline or become worthless. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in People’s Republic of China—Our business operations are extensively impacted by the policies and regulations of the PRC government. Any policy or regulatory change may cause us to incur significant compliance costs.” and “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in People’s Republic of China—We face various legal and operational risks and uncertainties as a company based in and primarily operating in China.”

Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our ADSs. For more details, see “Item 3. Key Information—D. Risk Factors—There are uncertainties with respect to the PRC legal system, including uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations, and sudden or unexpected changes in policies, laws, rules and regulations in the PRC that could adversely affect us.”

Cash Flows through our Organization

GDS Holdings Limited is a holding company with no material operations of its own. As a result, although other means are available for us to obtain financing at the holding company level, our company’s ability to pay dividends to the shareholders and to service any debt it may incur may depend upon dividends paid by our subsidiaries. We conduct our operations primarily through our subsidiaries and consolidated VIEs and their subsidiaries. GDS Holdings Limited provides continuing financial support to our subsidiaries for business expansion, while our subsidiaries also obtain financings through borrowings from various financial institutions. Meanwhile, for compliance purpose, the VIEs and their subsidiaries are the contracting party for our IDC service agreements, and our subsidiaries, as the owners of most of the self-developed data center assets, provide outsourcing and other services to the VIEs. Once the VIEs and their subsidiaries receive service fee from the customers, they can settle the corresponding outsourcing and service fees to our subsidiaries accordingly. For more details, see “Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources.”

Under PRC laws and regulations, our subsidiaries and the VIEs and their subsidiaries incorporated in China are subject to certain restrictions with respect to paying dividends or otherwise transferring any of their net assets to us. Remittance of dividends by a wholly foreign-owned enterprise out of China is also subject to examination by the banks designated by SAFE. As of December 31, 2022, the restricted net assets were RMB24,955.7 million (US$3,618.2 million), including those of the VIEs and their subsidiaries of RMB284.6 million (US$41.3 million) and our subsidiaries of RMB24,671.1 million (US$3,577.0 million), which mainly consisted of paid-in registered capital. For risks relating to the fund flows of our operations in China, see “Item 3. Key Information—Risk Factors—Risks Related to Our Corporate Structure —We rely to a significant extent on dividends and other distributions on equity paid by our principal operating subsidiaries to fund offshore cash and financing requirements.”

Under PRC laws, GDS Holdings Limited may provide funding to our PRC subsidiaries only through capital contributions or intercompany loans, and to our VIEs and their subsidiaries only through intercompany loans, subject to satisfaction of applicable government registration and approval requirements.

In the years ended December 31, 2020, 2021 and 2022, GDS Holdings Limited, through the intermediate holding companies, made capital contribution or provided intercompany loans to the non-VIE subsidiaries of RMB4,940.0 million, RMB9,935.4 million and RMB6,312.5 million (US$915.2 million), respectively.

In the years ended December 31, 2020, 2021 and 2022, GDS Holdings Limited and our subsidiaries did not provide any additional intercompany loans to the VIEs or their subsidiaries and the VIEs and their subsidiaries did not repay any existing intercompany loans to GDS Holdings Limited and our subsidiaries.

9

The Holding Foreign Companies Accountable Act

The Holding Foreign Companies Accountable Act, or the HFCA Act, was signed into law on December 18, 2020 and amended pursuant to the Consolidated Appropriations Act, 2023 on December 29, 2022. Under the HFCA Act and the rules issued by the SEC and the PCAOB thereunder, if we have retained a registered public accounting firm to issue an audit report where the registered public accounting firm has a branch or office that is located in a foreign jurisdiction and the PCAOB has determined that it is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction, the SEC will identify us as a “covered issuer”, or SEC-identified issuer, shortly after we file with the SEC a report required under the Securities Exchange Act of 1934, or the Exchange Act (such as our annual report on Form 20-F) that includes an audit report issued by such accounting firm; and if we were to be identified as an SEC-identified issuer for two consecutive years, the SEC would prohibit our securities (including our shares or ADSs) from being traded on a national securities exchange or in the over-the-counter trading market in the United States.

In December 2021, the PCAOB made its determinations, or the 2021 determinations, pursuant to the HFCA Act that it was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China or Hong Kong including our auditor, KPMG Huazhen LLP. After we filed our annual report on Form 20-F for the fiscal year ended December 31, 2021 that included an audit report issued by KPMG Huazhen LLP on April 28, 2022, the SEC conclusively identified us as an SEC-identified issuer on May 26, 2022. As such, we are required to satisfy additional disclosure requirement for SEC-identified issuers that are also foreign issuers in this annual report. See “Item 16I. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections.”

Following the Statement of Protocol signed between the PCAOB and the CSRC and the Ministry of Finance of the PRC, or MOF, in August 2022 and the on-site inspections and investigations conducted by the PCAOB staff in Hong Kong from September to November 2022, the PCAOB Board voted in December 2022 to vacate the previous 2021 determinations, and as a result, our auditor, KPMG Huazhen LLP, is no longer a registered public accounting firm that the PCAOB is unable to inspect or investigate completely as of the date of this annual report or at the time of issuance of the audit report included herein. As such, we do not expect to be identified as an SEC-identified issuer again in 2023. However, the PCAOB may change its determinations under the HFCA Act at any point in the future. In particular, if the PCAOB finds its ability to completely inspect and investigate registered public accounting firms headquartered in mainland China or Hong Kong is obstructed by the PRC authorities in any way in the future, the PCAOB may act immediately to consider the need to issue new determinations consistent with the HFCA Act. We cannot assure you that the PCAOB will always have complete access to inspect and investigate our auditor, or that we will not be identified as an SEC-identified issuer again in the future.

If we are identified as an SEC-identified issuer again in the future, we cannot assure you that we will be able to change our auditor or take other remedial measures in a timely manner, and if we were to be identified as an SEC-identified issuer for two consecutive years, we would be delisted from the Nasdaq and our securities (including our shares and ADSs) will not be permitted for trading “over-the-counter” either. If our securities are prohibited from trading in the United States, or threatened with such a prohibition, the risk and uncertainty associated with delisting would have a negative impact on the price of our ADSs and ordinary shares. Also, such a prohibition or any threat thereof would significantly affect our ability to raise capital on terms acceptable to us, or at all, which would have a material adverse impact on our business, financial condition, and prospects. Moreover, the implementation of the HFCA Act and other efforts to increase the U.S. regulatory access to audit information could cause investor uncertainty as to China-based issuers’ ability to maintain their listings on the U.S. national securities exchanges and the market price of the securities of China-based issuers, including us, could be adversely affected.

Permissions Required from the PRC Authorities for Our Operations

We conduct our business primarily through our subsidiaries, the consolidated VIEs and their subsidiaries in China. Our operations in China are governed by PRC laws and regulations. As of the date of this annual report, our PRC subsidiaries, the consolidated VIEs and their subsidiaries have obtained the requisite licenses and permits from the PRC government authorities that are material for the business operations of our subsidiaries, the consolidated VIEs and their subsidiaries in China, including, among others, the VATS licenses, fixed-asset investment project filings and energy conservation review opinions. Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we may be required to obtain additional licenses, permits, filings or approvals for our business in the future. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Our Business and Industry—We may fail to obtain, maintain and update licenses or permits necessary to conduct our operations in the PRC, and our business may be materially and adversely affected as a result of any changes in the laws and regulations governing the VATS industry in the PRC.”

10

Furthermore, in connection with our previous issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this annual report, we, our PRC subsidiaries, the consolidated VIEs and their subsidiaries, (i) are not required to obtain permissions from the CSRC, (ii) are not required to go through cybersecurity review by the Cyberspace Administration of China, or the CAC, and (iii) have not been asked to obtain such permissions by any PRC authority.

However, the PRC government has indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in the People’s Republic of China—The approval of, or filing with the CSRC or other PRC government authorities may be required in connection with acquisitions conducted by foreign investors or future offshore offerings under PRC law, and, if required, we cannot predict whether or for how long it will take to obtain such approval or complete such filing.”

A. [Reserved]

B. Capitalization and Indebtedness

Not required.

C. Reasons for the Offer and Use of Proceeds

Not required.

D. Risk Factors

Summary of Risk Factors

An investment in our ADSs and/or ordinary shares involves significant risks. Below is a summary of material risks we face, organized under relevant headings. These risks are discussed more fully in Item 3. Key Information—D. Risk Factors.

Risks Relating to Our Business and Industry

| ● | A slowdown in the demand for data center capacity or managed services could have a material adverse effect on us; |

| ● | Any inability to manage the growth of our operations could disrupt our business and reduce our profitability; |

| ● | If we are not successful in expanding our service offerings, we may not achieve our financial goals and our results of operations may be adversely affected; |

| ● | Our business requires us to make significant capital expenditures and resource commitments prior to recognizing revenue for those services; |

| ● | The data center business is capital-intensive, and we expect our capacity to generate capital in the short term will be insufficient to meet our anticipated capital requirements; |

| ● | Our net revenue is highly dependent on a limited number of customers, and the loss of, or any significant decrease in business from, any one or more of our major customers could adversely affect our financial condition and results of operations; |

| ● | We are expanding our operations to new markets outside of mainland China and Hong Kong, which subject us to additional regulatory, economic and political risks, and we may not be able to effectively implement our international expansion plans; and |

11

| ● | As we further expand in Southeast Asia, specifically in Singapore, Malaysia and Indonesia, adverse developments in the economic, political, or regulatory environment of these countries may materially adversely affect our business and operating results. |

Risks Related to Our Corporate Structure

| ● | If the PRC government deems that the contractual arrangements in relation to the consolidated VIEs do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in the operations of the consolidated VIEs and their subsidiaries; |

| ● | Our contractual arrangements with the consolidated VIEs may result in adverse tax consequences to us; and |

| ● | We rely on contractual arrangements with the consolidated VIEs and their shareholders for our China operations, which may not be as effective as direct ownership in providing operational control and otherwise have a material adverse effect as to our business. |

Risks Related to Doing Business in the People’s Republic of China

| ● | Changes in the political and economic policies of the PRC government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies; and |

| ● | We face various legal and operational risks and uncertainties as a company based in and primarily operating in China. |

Risks Related to Our ADSs and Class A Ordinary Shares

| ● | The trading prices of our ADSs and ordinary shares may be volatile, which could result in substantial losses to you; |

| ● | If securities or industry analysts do not publish research or publish inaccurate or unfavorable research about our business, the market price for our ADSs and/or ordinary shares and trading volume could decline; |

| ● | Techniques employed by short sellers may drive down the market price of our ADSs and/or ordinary shares; |

| ● | Because we do not expect to pay dividends in the foreseeable future, you must rely on price appreciation of our ADSs and/or ordinary shares for return on your investment; and |

| ● | The different characteristics of the capital markets in Hong Kong and the U.S. may negatively affect the trading prices of our ADSs and/or ordinary shares. |

Risks Relating to Our Business and Industry

A slowdown in the demand for data center capacity or managed services could have a material adverse effect on us.

Adverse developments in the data center market, in the industries in which our customers operate, or in demand for cloud computing could lead to a decrease in the demand for data center capacity or managed services, which could have a material adverse effect on us. We face risks including:

| ● | a decline in the technology industry, such as a decrease in the use of mobile or web-based commerce, business layoffs or downsizing, relocation of businesses, increased costs of complying with existing or new government regulations and other factors; |

12

| ● | a reduction in cloud adoption or a slowdown in the growth of the internet generally as a medium for commerce and communication and the use of cloud-based platforms and services in particular; |

| ● | a downturn in the market for data center capacity generally, which could be caused by an oversupply of or reduced demand for space, and a downturn in cloud-based data center demand in particular; and |

| ● | the rapid development of new technologies or the adoption of new industry standards that render our or our customers’ current products and services obsolete or unmarketable and, in the case of our customers, that contribute to a downturn in their businesses, increasing the likelihood of a default under their service agreements or that they become insolvent. |

| ● | a downturn in the overall economic environment, which causes material challenges to our customers in their own business, as a result of which they may move-in more slowly to our data centers, reduce the area utilized by them, pay only the minimum billable amount stated in customer agreements, or seek to renegotiate, terminate early, or not renew such agreements at expiry. |

To the extent that any of these or other adverse conditions occur, they are likely to impact market demand and pricing for our services.

Any inability to manage the growth of our operations could disrupt our business and reduce our profitability.

We have experienced significant growth in recent years. Our net revenue grew from RMB5,739.0 million in 2020 to RMB7,818.7 million in 2021, representing an increase of 36.2%, and further increased to RMB9,325.6 million (US$1,352.1 million) in 2022, representing an increase of 19.3%. We derive net revenue primarily from colocation services and, to a lesser extent, managed services. In addition, we also sell IT equipment either on a stand-alone basis or bundled in a managed service agreement and provide consulting services. Our net revenues from colocation services were RMB4,710.9 million, RMB6,514.3 million and RMB7,943.3 million (US$1,151.7 million) in 2020, 2021 and 2022, representing 82.1%, 83.3% and 85.2% of total net revenue over the same periods, respectively. Our net revenues from managed services and other services were RMB1,006.0 million, RMB1,300.1 million and RMB1,374.6 million (US$199.3 million) in 2020, 2021 and 2022, representing 17.5%, 16.6% and 14.7% of total net revenue over the same periods, respectively. Our net revenue from IT equipment sales were RMB22.1 million, RMB4.3 million and RMB7.7 million (US$1.1 million) in 2020, 2021 and 2022, representing 0.4%, 0.1% and 0.1% of total net revenue over the same periods, respectively.

Our operations have also expanded in recent years through increases in the number and size of the data center facilities we operate, which we expect will continue to grow. Our rapid growth has placed, and will continue to place, significant demands on our management and our administrative, operational and financial systems. Continued expansion increases the challenges we face in:

| ● | obtaining suitable sites or land to build new data centers; |

| ● | establishing new operations at additional data centers and maintaining efficient use of the data center facilities we operate; |

| ● | managing a large and growing customer base with increasingly diverse requirements; |

| ● | expanding our service portfolio to cover a wider range of services, including managed cloud services; |

| ● | creating and capitalizing on economies of scale; |

| ● | being exposed to protectionist or national security policies that restrict our ability to invest in or acquire companies or develop, import or export certain technologies; |

| ● | obtaining additional capital to meet our future capital needs; |

| ● | recruiting, training and retaining a sufficient number of skilled technical, sales and management personnel; |

13

| ● | maintaining effective oversight over personnel and multiple data center locations; |

| ● | coordinating work among sites and project teams; and |

| ● | developing and improving our internal systems, particularly for managing our continually expanding business operations. |

In addition, we have grown our business through acquisitions in the past and intend to continue selectively pursuing strategic partnerships and acquisitions to expand our business. From time to time, we may have a number of pending investments and acquisitions that are subject to closing conditions. There can be no assurance that we will be able to identify, acquire and successfully integrate other businesses and, if necessary, to obtain satisfactory debt or equity financing to fund those acquisitions. See “-We have expanded in the past and expect to continue to expand in the future through acquisitions of other companies, each of which may divert our management’s attention, result in additional dilution to shareholders or use resources that are necessary to operate our business.”

If we fail to manage the growth of our operations effectively, our businesses and prospects may be materially and adversely affected.

If we are not successful in expanding our service offerings, we may not achieve our financial goals and our results of operations may be adversely affected.

We have been expanding, and plan to continue to expand, the nature and scope of our service offerings, particularly into the area of managed cloud services, including direct private connection to major cloud platforms, an innovative service platform for managing hybrid clouds. The success of our expanded service offerings depends, in part, upon demand for such services by new and existing customers and our ability to meet their demand in a cost-effective manner. We may face a number of challenges in expanding our service offerings, including:

| ● | acquiring or developing the necessary expertise in IT; |

| ● | maintaining high-quality control and process execution standards; |

| ● | maintaining productivity levels and implementing necessary process improvements; |

| ● | controlling costs; and |

| ● | successfully attracting existing and new customers for new services we develop. |

A failure by us to effectively manage the growth of our service portfolio could damage our reputation, cause us to lose business and adversely affect our results of operations. In addition, because managed cloud services may require significant upfront investment, we expect that continued expansion into these services will reduce our profit margins. In the event that we are unable to successfully grow our service portfolio, we could lose our competitive edge in providing our existing colocation and managed services, since significant time and resources that are devoted to such growth could have been utilized instead to improve and expand our existing colocation and managed services.

14

Our business requires us to make significant capital expenditures and resource commitments prior to recognizing revenue for those services.

We have a long selling cycle for our services, which typically requires significant investment of capital, human resources and time by both our customers and us. Constructing, developing and operating our data centers require significant capital expenditures. A customer’s decision to utilize our colocation services, our managed solutions or our other services typically involves time-consuming contract negotiations regarding the service level commitments and other terms, and substantial due diligence on the part of the customer regarding the adequacy of our infrastructure and attractiveness of our resources and services. Furthermore, we may expend significant time and resources in pursuing a particular sale or customer, and we do not recognize revenue for our services until such time as the services are provided under the terms of the applicable agreement. Our efforts in pursuing a particular sale or customer may not be successful, and we may not always have sufficient capital on hand to satisfy our working capital needs between the date on which we sign an agreement with a new customer and when we first receive revenue for services delivered to the customer. If our efforts in pursuing sales and customers are unsuccessful, or our cash on hand is insufficient to cover our working capital needs over the course of our long selling cycle, our financial condition could be negatively affected.

The data center business is capital-intensive, and we expect our capacity to generate capital in the short term will be insufficient to meet our anticipated capital requirements.

The costs of constructing, developing and operating data centers are substantial. Further, we may encounter development delays, excess development costs, or delays in developing space for our customers to utilize. We also may not be able to secure suitable land or buildings for new data centers or at a cost on terms acceptable to us. We are required to fund the costs of constructing, developing and operating our data centers with cash retained from operations, as well as from financings from bank and other borrowings. Moreover, the costs of constructing, developing and operating data centers have increased in recent years, and may further increase in the future, which may make it more difficult for us to expand our business and to operate our data centers profitably. Based on our current expansion plans, we do not expect that our net revenue in the short term will be sufficient to offset increases in these costs, or that our business operations in the short term will generate capital sufficient to meet our anticipated capital requirements. If we cannot generate sufficient capital to meet our anticipated capital requirements, our financial condition, business expansion and future prospects could be materially and adversely affected.

Our substantial level of indebtedness could adversely affect our ability to raise additional capital to fund our operations, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under our indebtedness.

We have substantial indebtedness. As of December 31, 2022, we had total consolidated indebtedness of RMB42,891.0 million (US$6,218.6 million), including borrowings, finance lease and other financing obligations and convertible bonds. Based on our current expansion plans, we expect to continue to finance our operations through the incurrence of debt. Our indebtedness could, among other consequences:

| ● | make it more difficult for us to satisfy our obligations under our indebtedness, exposing us to the risk of default, which, in turn, would negatively affect our ability to operate as a going concern; |

| ● | require us to dedicate a substantial portion of our cash flows from operations to interest and principal payments on our indebtedness, reducing the availability of our cash flows for other purposes, such as capital expenditures, acquisitions and working capital; |

| ● | limit our flexibility in planning for, or reacting to, changes in our business and the industries in which we operate; |

| ● | increase our vulnerability to general adverse economic and industry conditions; |

| ● | place us at a disadvantage compared to our competitors that have less debt; |

| ● | expose us to fluctuations in the interest rate environment because the interest rates on borrowings under our project financing agreements are variable; |

15

| ● | increase our cost of borrowing; |

| ● | limit our ability to borrow additional funds; and |

| ● | require us to sell assets to raise funds, if needed, for working capital, capital expenditures, acquisitions or other purposes. |

As a result of the covenants and restrictions, we are limited in how we conduct our business, and we may be unable to raise additional debt or equity financing to compete effectively or to take advantage of new business opportunities. Our current or future borrowings could increase the level of financial risk to us and, to the extent that the interest rates are not fixed and rise, or that borrowings are refinanced at higher rates, our available cash flow and financial condition could be adversely affected. Increases in the target range for China’s loan prime rate (LPR) and the federal funds rate adopted by the Federal Open Market Committee of the U.S. Federal Reserve System could significantly increase our borrowing costs, reduce our available cash flow and adversely affect our financial condition.

The terms of any future indebtedness we may incur could include more restrictive covenants. A breach of any of these covenants could result in a default with respect to the related indebtedness. If a default occurs, the relevant lenders could elect to declare the indebtedness, together with accrued interest and other fees, to be due and payable immediately. This, in turn, could cause our other debt, to become due and payable as a result of cross-default or acceleration provisions contained in the agreements governing such other debt. In the event that some or all of our debt is accelerated and becomes immediately due and payable, we may not have the funds to repay, or the ability to refinance, such debt.

Loans under certain of our data center financing arrangements are subject to a heightened risk of repayment being required on an immediate or accelerated basis, which could reduce our available cash flow and adversely affect our financial condition.

We have financing arrangements in place with various lenders to support specific data center construction projects. Certain of these financing arrangements are secured by share pledge over equity interests of our subsidiaries, our accounts receivable, property and equipment and land use rights. The terms of these financing arrangements may impose covenants and obligations on the part of our borrowing subsidiaries and/or GDS Beijing and its subsidiaries, and our company as guarantor. For example, some of these agreements contain requirements to maintain a specified minimum cash balance at all times or require that the borrowing subsidiary maintain a certain debt-to-equity ratio. We cannot provide any assurances that we will always be able to meet any covenant tests under our financing arrangements. Other loan facility agreements of ours require that STT GDC, one of our major shareholders, maintain (i) an ownership percentage in our company of at least 25%, or (ii) have the power (whether by way of ownership of shares, proxy, contract, agency or otherwise) to control the casting of, at least 25% of the votes that may be cast at a meeting of the board of directors (or similar governing body) of our company, or (iii) its status as the single largest shareholder of our company. If any of the abovementioned conditions were not maintained, pursuant to the terms of relevant facility agreements we could be obligated to notify the lender or repay any loans outstanding immediately or on an accelerated repayment schedule. In addition, the majority of our loan facility agreements require that the IDC license of GDS Beijing or the borrowing subsidiaries, other affiliated entities or the authorization by GDS Beijing to one such subsidiary to operate the data center business and provide IDC services under the auspices of the IDC license held by GDS Beijing, be maintained and renewed on or before the expiry date of the IDC license or authorization thereunder, as applicable. However, we have learned that the MIIT will not allow subsidiaries authorized to provide IDC services by an IDC license holder to renew its current authorization in the future; instead, the MIIT will require subsidiaries of IDC license holders to apply for their own IDC licenses. See “—Risks Related to Doing Business in the People’s Republic of China—We may be regarded as being non-compliant with the regulations on VATS due to the lack of IDC licenses for which penalties may be assessed that may materially and adversely affect our business, financial condition, growth strategies and prospects.” If the subsidiaries of GDS Beijing cannot renew their authorizations to provide IDC services under the auspices of GDS Beijing’s IDC license timely, and such subsidiaries cannot apply for and obtain their own IDC licenses, we also could be obligated to notify the lender or repay any loans outstanding immediately or on an accelerated repayment schedule.

16

In May 2019, one of GDS Beijing’s subsidiaries, GDS Suzhou, obtained its own IDC license. In September and November 2019, the other two of GDS Beijing’s subsidiaries, Beijing Wan Chang Yun Science & Technology Co., Ltd., or Beijing Wan Chang Yun, and Shenzhen Yaode Data Services Co., Ltd., or Shenzhen Yaode obtained their own IDC license, respectively. Two other subsidiaries of the VIEs plan to apply for and obtain their own IDC licenses prior to the expiry of the existing authorizations under which they provide IDC services. While we do not foresee any legal impediment based on our experience with IDC license applications, there can be no assurance that these subsidiaries will be able to obtain approvals from the MIIT for their own IDC licenses in a timely manner or at all, or obtain such approvals for an expansion of authorization by GDS Beijing to allow the other subsidiaries of the VIEs to provide IDC services under the auspices of GDS Beijing’s IDC license. There also can be no assurance that we will be able to renew such authorizations and expansions in due course.

In mid-August 2019, the PBOC decided to reform the formation mechanism of the Loan Prime Rate, or LPR, and authorized the National Interbank Funding Center to release LPR monthly, which may impact the interest rate on our variable rate debt. Uncertainty on future LPR reforms and rate changes may impact our indebtedness. In addition, the interest rates of our offshore credit facilities are based on a spread over Secured Overnight Financing Rate, or SOFR, Hong Kong Interbank Offer Rate, or HIBOR, and Kuala Lumpur InterBank Offered Rate, or KLIBOR. As a result, the interest expenses associated with such indebtedness will be subject to the potential impact of any fluctuation in SOFR, HIBOR and KLIBOR. Uncertainty on future SOFR, HIBOR and KLIBOR reforms and rate changes may impact our indebtedness.

We will likely require additional capital to meet our future capital needs, which may adversely affect our financial position and result in additional shareholder dilution.

To grow our operations, we will be required to commit a substantial amount of operating and financial resources. Our planned capital expenditures, together with our ongoing operating expenses, will cause substantial cash outflows. In the near term, we will likely be unable to fund our expansion plans solely through our operating cash flows. Accordingly, we have raised and will likely need to continue to raise additional funds through equity, equity-linked, debt, offshore fund financings and disposal of assets in the future in order to meet our operating and capital needs. In this regard, at our annual general meeting, or AGM, held on June 30, 2022, our shareholders passed ordinary resolutions authorizing our board of directors to approve the allotment or issuance, in the 12-month period from the date of the AGM, of ordinary shares or other equity or equity-linked securities of our company up to an aggregate thirty percent (30%) of our existing issued share capital at the date of the AGM, whether in a single transaction or a series of transactions (other than any allotment or issues of shares on the exercise of any options that have been granted by our company). Additional debt or equity financing may not be available when needed or, if available, may not be available on satisfactory terms. The Russia-Ukraine conflict, the deterioration of the U.S.-China relationship, and increased regulatory scrutiny have limited, and may continue to limit, our ability to raise, and our flexibility in raising, additional funds. Our inability to obtain additional debt and/or equity financing or to generate sufficient cash from operations may require us to prioritize projects or curtail capital expenditures and could adversely affect our results of operations.

If we raise additional funds through further issuances of equity or equity-linked securities, our existing shareholders could suffer significant dilution in their percentage ownership of our company, and any new equity securities we issue could have rights, preferences and privileges senior to those of the holders of our ordinary shares. In addition, any debt financing that we may obtain in the future could have restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities, including potential acquisitions.

If Mr. Huang’s beneficial ownership in our company falls below 5%, our dual-class share structure will terminate and a change of control would be triggered under certain of our material commercial and loan agreements, and our business development, financial condition and future prospects may be materially and adversely affected.

Subject to the provisions of our Articles of Association, our Class B ordinary shares will automatically convert into Class A ordinary shares upon the occurrence of an automatic conversion event, which events include, among others, Mr. Huang having beneficial ownership in less than 5% of our issued share capital on an as converted basis. As of March 15, 2023, Mr. Huang beneficially owned (whether in the form of ordinary shares or ADSs) 84,047,840 ordinary shares, representing 5.39% of our total issued share capital.

17

Mr. Huang has in the past entered into, and may in the future enter into, certain transactions from time to time, including derivative transactions, that have and could have the effect of reducing Mr. Huang’s beneficial ownership in our company. Mr. Huang informed our company that certain variable pre-paid forward sale contract transactions in respect of 42,457,504 ordinary shares beneficially owned by him, which transactions he originally entered into between May 2020 and June 2022,would expire between March 2023 and December 2023. If Mr. Huang chooses to settle these transactions by transferring ownership of the 42,457,504 ordinary shares to the counterparties, his beneficial ownership interest in our total issued share capital may decrease to below 5%, which would trigger an automatic conversion event, unless the 5% threshold contained in our Articles of Association is reduced or he otherwise acquires beneficial ownership of additional shares to keep his beneficial ownership at or above 5% or such other threshold if so reduced.

Should this happen, all Class B ordinary shares would automatically convert into Class A ordinary shares, and the dual-class share structure would thereby be terminated. This would constitute a change of control for the purposes of certain of our, or our subsidiaries’ and the consolidated entities’, sales agreements and domestic loan facility agreements, and if such provisions under the domestic loan agreements are triggered, which could give the lenders the right to demand early repayment under these domestic loan agreements. Such change of control may result in actual, potential or alleged breaches or early termination of other contracts or agreements. The change of control potentially may also have implications for the purposes of China’s national security review regime and anti-monopoly merger filing requirements, if applicable. The occurrence of any of the foregoing may have a material and adverse effect on our business development, financial condition and future prospects.

On March 30, 2023, Mr. Huang acquired beneficial ownership of an additional 3,888,000 of our ordinary shares, representing 0.25% of our total issued share capital through the accelerated vesting of certain restricted share units previously granted to him under our 2016 share incentive plan. The Compensation Committee and our board of directors approved this accelerated vesting as a temporary measure to provide Mr. Huang with the flexibility of settling part of the aforementioned variable pre-paid forward sale contract transactions with other of his shareholdings without triggering an automatic conversion event that would otherwise result in the termination of the dual-class shareholding structure and the occurrence of the change of control implications described above. The ordinary shares Mr. Huang received upon the accelerated vesting of the foregoing restricted share units are subject to a lock-up (including a prohibition on pledges or derivative transactions) as well as a claw-back arrangement with us, pending a longer-term solution to the issues surrounding the potential change in control trigger. In addition, the automatic conversion event could be triggered if Mr. Huang is further diluted due to our financing activities in which we issue additional equity or equity-linked securities. If we issue additional equity or equity-linked securities in any further financings, Mr. Huang’s shareholdings could fall below the 5% which would trigger an automatic conversion event in our dual-class structure, and this could happen even if he cash settles the variable pre-paid forward contracts described above.

Our board of directors continues to explore additional possible measures to maintain the stability of its corporate governance structure and dual-class shareholding structure in the best interests of the Company, with due consideration given to the possible negative ramifications of a potential automatic conversion event on the operations and prospects of our group.

The ongoing COVID-19 pandemic could materially and adversely affect our business, results of operations and financial condition.