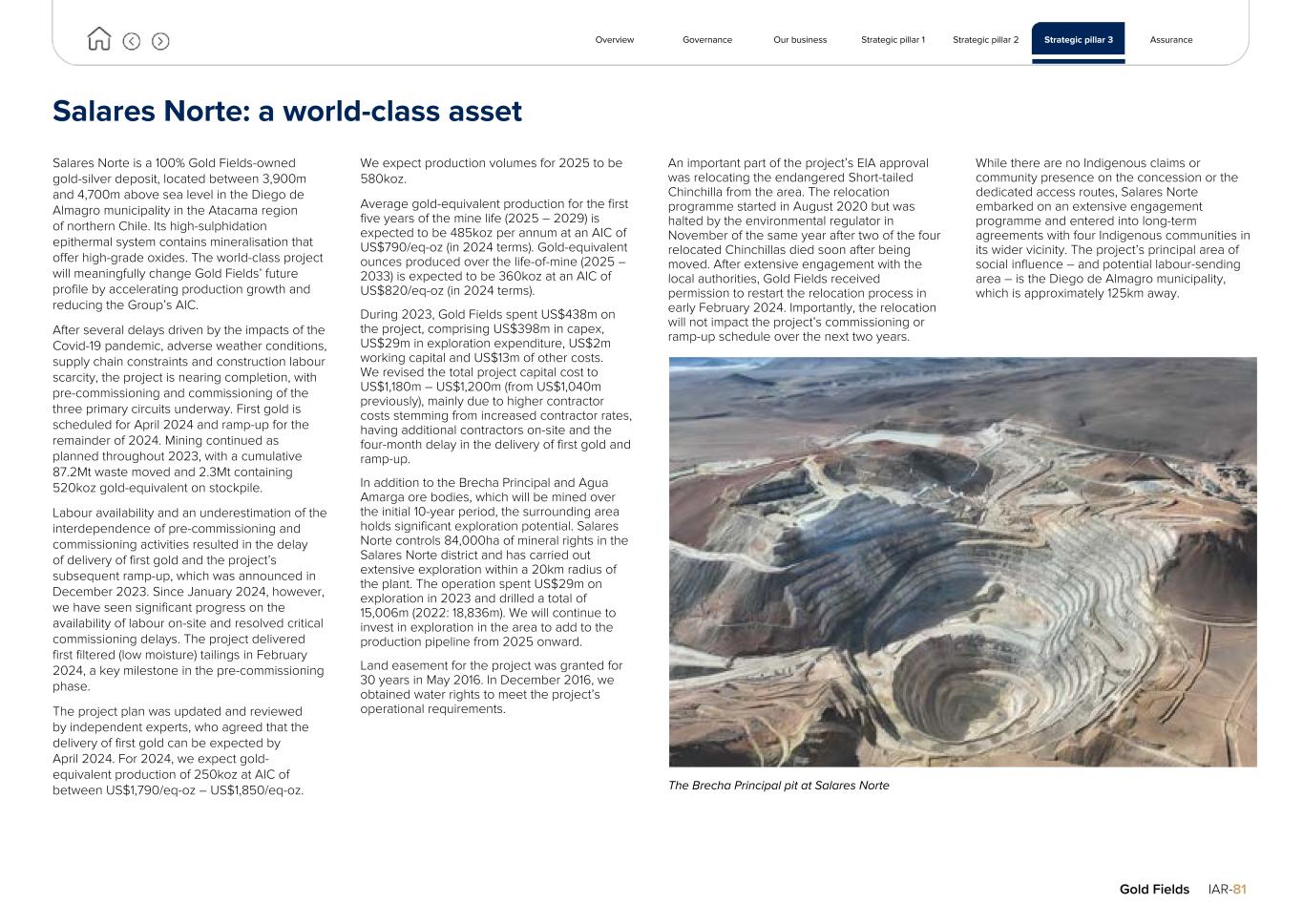

gfi-20231231false2023FY000117272400011727242023-01-012023-12-310001172724dei:BusinessContactMember2023-01-012023-12-310001172724gfi:ADR1Member2023-01-012023-12-3100011727242023-12-31xbrli:shares0001172724gfi:YearOneMember2023-12-31iso4217:USDutr:oz0001172724gfi:YearOneMember2022-12-310001172724gfi:YearOneMember2021-12-310001172724gfi:YearTwoMember2023-12-310001172724gfi:YearTwoMember2022-12-310001172724gfi:YearTwoMember2021-12-310001172724gfi:YearThreeMember2023-12-310001172724gfi:YearThreeMember2022-12-310001172724gfi:YearThreeMember2021-12-310001172724gfi:YearFourMember2023-12-310001172724gfi:YearFourMember2022-12-310001172724gfi:YearFourMember2021-12-310001172724gfi:YearFiveOnwardsMember2023-12-310001172724gfi:YearFiveOnwardsMember2022-12-310001172724gfi:YearFiveOnwardsMember2021-12-31iso4217:ZARutr:kgiso4217:AUDutr:oziso4217:USDutr:t0001172724country:GH2023-12-310001172724country:GH2022-12-310001172724country:GH2021-12-310001172724country:PE2022-12-310001172724country:PE2021-12-310001172724country:CL2023-12-310001172724country:CL2022-12-310001172724country:CL2021-12-310001172724country:ZA2023-01-012023-12-31xbrli:pure0001172724country:ZA2022-01-012022-12-310001172724country:ZA2021-01-012021-12-310001172724country:GH2023-01-012023-12-310001172724country:GH2022-01-012022-12-310001172724country:GH2021-01-012021-12-310001172724country:PE2023-01-012023-12-310001172724country:PE2022-01-012022-12-310001172724country:PE2021-01-012021-12-310001172724country:AU2023-01-012023-12-310001172724country:AU2022-01-012022-12-310001172724country:AU2021-01-012021-12-310001172724country:CL2023-01-012023-12-310001172724country:CL2022-01-012022-12-310001172724country:CL2021-01-012021-12-310001172724gfi:SouthDeepMember2023-01-012023-12-310001172724gfi:SouthDeepMember2022-01-012022-12-310001172724gfi:SouthDeepMember2021-01-012021-12-310001172724gfi:TarkwaMember2023-01-012023-12-310001172724gfi:TarkwaMember2022-01-012022-12-310001172724gfi:TarkwaMember2021-01-012021-12-310001172724gfi:DamangMember2023-01-012023-12-310001172724gfi:DamangMember2022-01-012022-12-310001172724gfi:DamangMember2021-01-012021-12-310001172724gfi:CerroCeronaMember2023-01-012023-12-310001172724gfi:CerroCeronaMember2022-01-012022-12-310001172724gfi:CerroCeronaMember2021-01-012021-12-310001172724gfi:StivesMember2023-01-012023-12-310001172724gfi:StivesMember2022-01-012022-12-310001172724gfi:StivesMember2021-01-012021-12-310001172724gfi:AgnewMember2023-01-012023-12-310001172724gfi:AgnewMember2022-01-012022-12-310001172724gfi:AgnewMember2021-01-012021-12-310001172724gfi:GrannySmithMember2023-01-012023-12-310001172724gfi:GrannySmithMember2022-01-012022-12-310001172724gfi:GrannySmithMember2021-01-012021-12-310001172724gfi:GruyereMember2023-01-012023-12-310001172724gfi:GruyereMember2022-01-012022-12-310001172724gfi:GruyereMember2021-01-012021-12-310001172724gfi:SalaresNorteMember2023-01-012023-12-310001172724gfi:SalaresNorteMember2022-01-012022-12-310001172724gfi:SalaresNorteMember2021-01-012021-12-310001172724currency:ZARgfi:YearOneMember2023-01-012023-12-31gfi:ExchangeRates0001172724currency:ZARgfi:YearOneMember2022-01-012022-12-310001172724currency:ZARgfi:YearOneMember2021-01-012021-12-310001172724gfi:YearTwoMembercurrency:ZAR2023-01-012023-12-310001172724gfi:YearTwoMembercurrency:ZAR2022-01-012022-12-310001172724gfi:YearTwoMembercurrency:ZAR2021-01-012021-12-310001172724gfi:YearThreeMembercurrency:ZAR2023-01-012023-12-310001172724gfi:YearThreeMembercurrency:ZAR2022-01-012022-12-310001172724gfi:YearThreeMembercurrency:ZAR2021-01-012021-12-310001172724gfi:YearFourMembercurrency:ZAR2023-01-012023-12-310001172724gfi:YearFourMembercurrency:ZAR2022-01-012022-12-310001172724gfi:YearFourMembercurrency:ZAR2021-01-012021-12-310001172724gfi:YearFiveOnwardsMembercurrency:ZAR2023-01-012023-12-310001172724gfi:YearFiveOnwardsMembercurrency:ZAR2022-01-012022-12-310001172724gfi:YearFiveOnwardsMembercurrency:ZAR2021-01-012021-12-310001172724currency:AUDgfi:YearOneMember2023-01-012023-12-310001172724currency:AUDgfi:YearOneMember2022-01-012022-12-310001172724currency:AUDgfi:YearOneMember2021-01-012021-12-310001172724currency:AUDgfi:YearTwoMember2023-01-012023-12-310001172724currency:AUDgfi:YearTwoMember2022-01-012022-12-310001172724currency:AUDgfi:YearTwoMember2021-01-012021-12-310001172724currency:AUDgfi:YearThreeMember2023-01-012023-12-310001172724currency:AUDgfi:YearThreeMember2022-01-012022-12-310001172724currency:AUDgfi:YearThreeMember2021-01-012021-12-310001172724currency:AUDgfi:YearFourMember2023-01-012023-12-310001172724currency:AUDgfi:YearFourMember2022-01-012022-12-310001172724currency:AUDgfi:YearFourMember2021-01-012021-12-310001172724currency:AUDgfi:YearFiveOnwardsMember2023-01-012023-12-310001172724currency:AUDgfi:YearFiveOnwardsMember2022-01-012022-12-310001172724currency:AUDgfi:YearFiveOnwardsMember2021-01-012021-12-31iso4217:USD00011727242022-12-310001172724gfi:PeruCashGeneratingUnitMember2023-01-012023-12-310001172724gfi:PeruCashGeneratingUnitMember2022-01-012022-12-310001172724gfi:TarkwaCashGeneratingUnitMember2023-01-012023-12-310001172724gfi:TarkwaCashGeneratingUnitMember2022-01-012022-12-3100011727242022-01-012022-12-3100011727242021-01-012021-12-310001172724gfi:YearOneToThreeMemberifrs-full:BottomOfRangeMember2023-12-310001172724gfi:YearOneToThreeMemberifrs-full:TopOfRangeMember2023-12-310001172724gfi:YearOneToThreeMemberifrs-full:BottomOfRangeMember2022-12-310001172724gfi:YearOneToThreeMemberifrs-full:TopOfRangeMember2022-12-310001172724gfi:YearFourOnwardsMember2023-12-310001172724gfi:YearFourOnwardsMember2022-12-310001172724gfi:AsankoGoldMember2023-12-212023-12-210001172724gfi:AsankoGoldMembergfi:ImpairmentExpenseMemberifrs-full:DiscontinuedOperationsMember2023-01-012023-12-310001172724gfi:AsankoGoldMembergfi:ImpairmentExpenseMemberifrs-full:DiscontinuedOperationsMember2022-01-012022-12-310001172724gfi:CanadianSubsidiaryMember2023-05-022023-05-020001172724gfi:WindfallProjectMember2023-05-022023-05-020001172724currency:ZAR2023-12-310001172724currency:USD2023-12-310001172724currency:CAD2023-12-310001172724currency:ZAR2022-12-310001172724currency:USD2022-12-310001172724currency:ZAR2021-12-310001172724currency:USD2021-12-310001172724currency:ZAR2023-01-012023-12-310001172724currency:USD2023-01-012023-12-310001172724currency:CAD2023-01-012023-12-310001172724currency:ZAR2022-01-012022-12-310001172724currency:USD2022-01-012022-12-310001172724currency:ZAR2021-01-012021-12-310001172724currency:USD2021-01-012021-12-31iso4217:USDxbrli:shares0001172724ifrs-full:DiscontinuedOperationsMember2023-01-012023-12-310001172724ifrs-full:DiscontinuedOperationsMember2022-01-012022-12-310001172724ifrs-full:DiscontinuedOperationsMember2021-01-012021-12-310001172724gfi:ShareCapitalMember2020-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2020-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2020-12-310001172724ifrs-full:RetainedEarningsMember2020-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2020-12-310001172724ifrs-full:NoncontrollingInterestsMember2020-12-3100011727242020-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001172724ifrs-full:RetainedEarningsMember2021-01-012021-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2021-01-012021-12-310001172724ifrs-full:NoncontrollingInterestsMember2021-01-012021-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2021-01-012021-12-310001172724gfi:ShareCapitalMember2021-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2021-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2021-12-310001172724ifrs-full:RetainedEarningsMember2021-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2021-12-310001172724ifrs-full:NoncontrollingInterestsMember2021-12-3100011727242021-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001172724ifrs-full:RetainedEarningsMember2022-01-012022-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2022-01-012022-12-310001172724ifrs-full:NoncontrollingInterestsMember2022-01-012022-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2022-01-012022-12-310001172724gfi:ShareCapitalMember2022-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2022-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2022-12-310001172724ifrs-full:RetainedEarningsMember2022-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2022-12-310001172724ifrs-full:NoncontrollingInterestsMember2022-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001172724ifrs-full:RetainedEarningsMember2023-01-012023-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2023-01-012023-12-310001172724ifrs-full:NoncontrollingInterestsMember2023-01-012023-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2023-01-012023-12-310001172724gfi:ShareCapitalMember2023-12-310001172724ifrs-full:AccumulatedOtherComprehensiveIncomeMember2023-12-310001172724ifrs-full:MiscellaneousOtherReservesMember2023-12-310001172724ifrs-full:RetainedEarningsMember2023-12-310001172724ifrs-full:EquityAttributableToOwnersOfParentMember2023-12-310001172724ifrs-full:NoncontrollingInterestsMember2023-12-310001172724gfi:GoldProductsMember2023-01-012023-12-310001172724gfi:GoldProductsMember2022-01-012022-12-310001172724gfi:GoldProductsMember2021-01-012021-12-310001172724gfi:CopperMember2023-01-012023-12-310001172724gfi:CopperMember2022-01-012022-12-310001172724gfi:CopperMember2021-01-012021-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2022-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2021-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2020-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2023-01-012023-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2022-01-012022-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2021-01-012021-12-310001172724gfi:GoldFieldsLimitedTwoThousandTwelveSharePlanMembergfi:PerformanceShares1Member2023-12-310001172724gfi:PerformanceShares1Membergfi:GoldFieldsLimited2012SharePlanAmendedMember2023-01-012023-12-310001172724gfi:PerformanceShares1Membergfi:GoldFieldsLimited2012SharePlanAmendedMember2022-01-012022-12-310001172724gfi:PerformanceShares1Membergfi:GoldFieldsLimited2012SharePlanAmendedMember2021-01-012021-12-31iso4217:ZARxbrli:shares0001172724ifrs-full:TopOfRangeMemberifrs-full:OrdinarySharesMember2023-12-310001172724ifrs-full:OrdinarySharesMember2023-12-310001172724country:AU2023-01-012023-12-310001172724country:AU2022-01-012022-12-310001172724country:AU2021-01-012021-12-310001172724country:GH2023-01-012023-12-310001172724country:GH2022-01-012022-12-310001172724country:GH2021-01-012021-12-310001172724country:PE2023-01-012023-12-310001172724country:PE2022-01-012022-12-310001172724country:PE2021-01-012021-12-310001172724country:CL2023-01-012023-12-310001172724country:CL2022-01-012022-12-310001172724country:CL2021-01-012021-12-310001172724gfi:OtherMember2023-01-012023-12-310001172724gfi:OtherMember2022-01-012022-12-310001172724gfi:OtherMember2021-01-012021-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2023-01-012023-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2022-01-012022-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2021-01-012021-12-310001172724gfi:PeruCashGeneratingUnitMember2021-01-012021-12-310001172724gfi:TarkwaCashGeneratingUnitMember2021-01-012021-12-310001172724ifrs-full:OtherPropertyPlantAndEquipmentMember2023-01-012023-12-310001172724ifrs-full:OtherPropertyPlantAndEquipmentMember2022-01-012022-12-310001172724ifrs-full:OtherPropertyPlantAndEquipmentMember2021-01-012021-12-310001172724gfi:LepantoConsolidatedMiningCompanyMembergfi:FarSoutheastGoldResourcesIncorporatedMember2021-01-012021-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedFSEMember2022-12-310001172724gfi:PeruCashGeneratingUnitMember2021-12-310001172724gfi:PeruCashGeneratingUnitMember2022-12-310001172724gfi:PeruCashGeneratingUnitMember2023-12-310001172724gfi:TarkwaCashGeneratingUnitMember2021-12-310001172724gfi:TarkwaCashGeneratingUnitMember2022-12-310001172724ifrs-full:ExplorationAndEvaluationAssetsMember2023-01-012023-12-310001172724ifrs-full:ExplorationAndEvaluationAssetsMember2022-01-012022-12-310001172724ifrs-full:ExplorationAndEvaluationAssetsMember2021-01-012021-12-310001172724gfi:RedundantAssetsInPeruMember2023-01-012023-12-310001172724gfi:RedundantAssetsInPeruMember2022-01-012022-12-310001172724gfi:RedundantAssetsInPeruMember2021-01-012021-12-310001172724gfi:RedundantAssetsInChileMember2023-01-012023-12-310001172724gfi:RedundantAssetsInChileMember2022-01-012022-12-310001172724gfi:RedundantAssetsInChileMember2021-01-012021-12-310001172724gfi:PeruCashGeneratingUnitMember2023-01-012023-12-310001172724gfi:TarkwaMember2022-01-012022-12-310001172724gfi:PeruCashGeneratingUnitMember2022-01-012022-12-310001172724gfi:YamanaMember2022-01-012022-12-310001172724country:ZA2023-01-012023-12-310001172724country:ZA2022-01-012022-12-310001172724country:ZA2021-01-012021-12-31gfi:Times0001172724ifrs-full:TopOfRangeMembercountry:ZA2023-01-012023-12-310001172724ifrs-full:BottomOfRangeMembergfi:RangeOneMember2023-01-012023-12-310001172724ifrs-full:TopOfRangeMembergfi:RangeOneMember2023-01-012023-12-310001172724gfi:GoldRoyaltyMembergfi:RangeOneMember2023-01-012023-12-310001172724ifrs-full:BottomOfRangeMembergfi:RangeTwoMember2023-01-012023-12-310001172724ifrs-full:TopOfRangeMembergfi:RangeTwoMember2023-01-012023-12-310001172724gfi:RangeTwoMembergfi:GoldRoyaltyMember2023-01-012023-12-310001172724gfi:RangeThreeMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001172724gfi:RangeThreeMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001172724gfi:RangeThreeMembergfi:GoldRoyaltyMember2023-01-012023-12-310001172724gfi:RangeFourMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001172724gfi:RangeFourMembergfi:GoldRoyaltyMember2023-01-012023-12-310001172724country:PEifrs-full:BottomOfRangeMember2023-01-012023-12-310001172724country:PEifrs-full:TopOfRangeMember2023-01-012023-12-310001172724gfi:SouthAfricanTaxationMember2023-01-012023-12-310001172724gfi:SouthAfricanTaxationMember2022-01-012022-12-310001172724gfi:SouthAfricanTaxationMember2021-01-012021-12-310001172724gfi:ForeignTaxationMember2023-01-012023-12-310001172724gfi:ForeignTaxationMember2022-01-012022-12-310001172724gfi:ForeignTaxationMember2021-01-012021-12-310001172724gfi:CerroCeronaMember2023-01-012023-12-310001172724gfi:CerroCeronaMember2022-01-012022-12-310001172724gfi:CerroCeronaMember2021-01-012021-12-310001172724gfi:DamangAndTarkwaMember2023-01-012023-12-310001172724gfi:DamangAndTarkwaMember2022-01-012022-12-310001172724gfi:DamangAndTarkwaMember2021-01-012021-12-310001172724gfi:YamanaMember2022-01-012022-12-310001172724gfi:ForeignTaxationMembergfi:DamangAndTarkwaMember2022-01-012022-12-310001172724gfi:CerroCeronaMember2023-12-310001172724gfi:CerroCeronaMember2022-12-310001172724gfi:DeferredTaxAssetsNotRecognizedMember2021-12-310001172724gfi:DeferredTaxAssetsNotRecognizedMembergfi:CerroCeronaAndDamangMember2021-12-310001172724gfi:CerroCeronaAndDamangMember2021-01-012021-12-310001172724gfi:DeferredTaxAssetsNotRecognizedMembergfi:GhanaianOperationsMember2023-12-310001172724gfi:DeferredTaxAssetsNotRecognizedMembergfi:GhanaianOperationsMember2022-12-310001172724gfi:DeferredTaxAssetsNotRecognizedMembergfi:GhanaianOperationsMember2021-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:GhanaianOperationsMember2023-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:GhanaianOperationsMember2022-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:GhanaianOperationsMember2021-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:DamangMember2023-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:DamangMember2022-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:DamangMember2021-12-310001172724gfi:DamangMembergfi:DeferredTaxAssetsNotRecognizedMember2023-12-310001172724gfi:DamangMembergfi:DeferredTaxAssetsNotRecognizedMember2022-12-310001172724gfi:DamangMembergfi:DeferredTaxAssetsNotRecognizedMember2021-12-310001172724gfi:SalariesNorteMember2021-01-012021-12-310001172724gfi:SouthAfricanTaxationMembergfi:NonMiningTaxMember2023-01-012023-12-310001172724gfi:SouthAfricanTaxationMembergfi:NonMiningTaxMember2022-01-012022-12-310001172724gfi:SouthAfricanTaxationMembergfi:NonMiningTaxMember2021-01-012021-12-310001172724gfi:CompanyTaxRateMembergfi:SouthAfricanTaxationMember2023-01-012023-12-310001172724gfi:CompanyTaxRateMembergfi:SouthAfricanTaxationMember2022-01-012022-12-310001172724gfi:CompanyTaxRateMembergfi:SouthAfricanTaxationMember2021-01-012021-12-310001172724gfi:AustraliaTaxMembergfi:NonMiningTaxMember2023-01-012023-12-310001172724gfi:AustraliaTaxMembergfi:NonMiningTaxMember2022-01-012022-12-310001172724gfi:AustraliaTaxMembergfi:NonMiningTaxMember2021-01-012021-12-310001172724gfi:GhanaTaxMembergfi:NonMiningTaxMember2023-01-012023-12-310001172724gfi:GhanaTaxMembergfi:NonMiningTaxMember2022-01-012022-12-310001172724gfi:GhanaTaxMembergfi:NonMiningTaxMember2021-01-012021-12-310001172724gfi:PeruTaxMembergfi:NonMiningTaxMember2023-01-012023-12-310001172724gfi:PeruTaxMembergfi:NonMiningTaxMember2022-01-012022-12-310001172724gfi:PeruTaxMembergfi:NonMiningTaxMember2021-01-012021-12-310001172724gfi:MiningTaxMember2021-12-312021-12-310001172724gfi:MiningTaxMember2022-12-312022-12-31iso4217:ZAR0001172724gfi:MiningTaxMember2023-01-012023-12-310001172724gfi:MiningTaxMember2022-01-012022-12-310001172724gfi:MiningTaxMember2021-01-012021-12-310001172724srt:ScenarioForecastMembergfi:SouthAfricanTaxationMembergfi:NonMiningTaxMember2024-01-012024-12-310001172724gfi:SouthAfricanTaxationMembergfi:GoldFieldsOperationsLimitedMember2023-12-310001172724gfi:SouthAfricanTaxationMembergfi:GoldFieldsOperationsLimitedMember2022-12-310001172724gfi:SouthAfricanTaxationMembergfi:GFIJointVentureHoldingsProprietaryLimitedMember2023-12-310001172724gfi:SouthAfricanTaxationMembergfi:GFIJointVentureHoldingsProprietaryLimitedMember2022-12-310001172724gfi:GoldFieldsHoldingsCompanyLimitedMembergfi:SouthAfricanTaxationMember2023-12-310001172724gfi:GoldFieldsHoldingsCompanyLimitedMembergfi:SouthAfricanTaxationMember2022-12-310001172724gfi:SouthAfricanTaxationMember2023-12-310001172724gfi:SouthAfricanTaxationMember2022-12-310001172724gfi:ExplorationEntitiesMembergfi:InternationalOperationsMember2023-12-310001172724gfi:ExplorationEntitiesMembergfi:InternationalOperationsMember2022-12-310001172724gfi:MineraGoldFieldsSalaresNorteMembergfi:InternationalOperationsMember2023-12-310001172724gfi:MineraGoldFieldsSalaresNorteMembergfi:InternationalOperationsMember2022-12-310001172724gfi:AbossoGoldfieldsLimitedMembergfi:InternationalOperationsMember2023-12-310001172724gfi:AbossoGoldfieldsLimitedMembergfi:InternationalOperationsMember2022-12-310001172724gfi:GoldFieldsGhanaLimitedMembergfi:InternationalOperationsMember2023-12-310001172724gfi:GoldFieldsGhanaLimitedMembergfi:InternationalOperationsMember2022-12-310001172724gfi:InternationalOperationsMember2023-12-310001172724gfi:InternationalOperationsMember2022-12-310001172724gfi:ExplorationEntitiesMember2023-01-012023-12-310001172724gfi:ExplorationEntitiesMember2022-01-012022-12-310001172724gfi:ExplorationEntitiesMembergfi:TaxLossesExpiringBetweenOneAndTwoYearsMember2023-01-012023-12-310001172724gfi:ExplorationEntitiesMembergfi:TaxLossesExpiringBetweenOneAndTwoYearsMember2022-01-012022-12-310001172724gfi:ExplorationEntitiesMembergfi:TaxLossesExpiringBetweenTwoAndFiveYearsMember2023-01-012023-12-310001172724gfi:ExplorationEntitiesMembergfi:TaxLossesExpiringBetweenTwoAndFiveYearsMember2022-01-012022-12-310001172724gfi:TaxLossesExpiringBetweenFiveAndTenYearsMembergfi:ExplorationEntitiesMember2023-01-012023-12-310001172724gfi:TaxLossesExpiringBetweenFiveAndTenYearsMembergfi:ExplorationEntitiesMember2022-01-012022-12-310001172724gfi:ExplorationEntitiesMembergfi:TaxLossesExpiringAfterTenYearsMember2023-01-012023-12-310001172724gfi:ExplorationEntitiesMembergfi:TaxLossesExpiringAfterTenYearsMember2022-01-012022-12-310001172724gfi:NoExpiryDateMembergfi:ExplorationEntitiesMember2023-01-012023-12-310001172724gfi:NoExpiryDateMembergfi:ExplorationEntitiesMember2022-01-012022-12-310001172724gfi:TaxLossesExpireInThreeYearsMembergfi:AbossoGoldfieldsLimitedMember2023-01-012023-12-310001172724gfi:TaxLossesExpireInThreeYearsMembergfi:AbossoGoldfieldsLimitedMember2022-01-012022-12-310001172724gfi:TaxLossesExpireInFourYearsMembergfi:AbossoGoldfieldsLimitedMember2023-01-012023-12-310001172724gfi:TaxLossesExpireInFourYearsMembergfi:AbossoGoldfieldsLimitedMember2022-01-012022-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:DamangMember2023-01-012023-12-310001172724gfi:DeferredTaxAssetsRecognizedMembergfi:DamangMember2022-01-012022-12-310001172724srt:MinimumMember2023-12-310001172724gfi:FinalDividendsMember2022-01-012022-12-310001172724gfi:FinalDividendsMember2021-01-012021-12-310001172724gfi:FinalDividendsMember2020-01-012020-12-310001172724gfi:FinalDividendsMember2023-01-012023-12-310001172724gfi:InterimDividendsMember2023-01-012023-12-310001172724gfi:InterimDividendsMember2022-01-012022-12-310001172724gfi:InterimDividendsMember2021-01-012021-12-310001172724gfi:ApprovedDividendMember2023-01-012023-12-310001172724gfi:LoansToContractorsMember2023-01-012023-12-310001172724gfi:LoansToContractorsMember2022-01-012022-12-310001172724gfi:LoansToContractorsMember2021-01-012021-12-310001172724gfi:DamangMemberifrs-full:TradeReceivablesMember2023-01-012023-12-310001172724gfi:DamangMemberifrs-full:TradeReceivablesMember2022-01-012022-12-310001172724gfi:DamangMemberifrs-full:TradeReceivablesMember2021-01-012021-12-310001172724gfi:TarkwaMemberifrs-full:TradeReceivablesMember2023-01-012023-12-310001172724gfi:TarkwaMemberifrs-full:TradeReceivablesMember2022-01-012022-12-310001172724gfi:TarkwaMemberifrs-full:TradeReceivablesMember2021-01-012021-12-310001172724gfi:TradeAndOtherPayables12023-01-012023-12-310001172724gfi:LoansToContractorsExcl.InterestMember2023-01-012023-12-310001172724gfi:DamangMemberifrs-full:TradeReceivablesMember2023-12-310001172724gfi:TarkwaMemberifrs-full:TradeReceivablesMember2022-12-310001172724gfi:LoansToContractorsExcl.InterestMember2022-12-310001172724gfi:LoansToContractorsExcl.InterestMember2021-12-310001172724gfi:LoansToContractorsExcl.InterestMember2022-01-012022-12-310001172724gfi:LoansToContractorsExcl.InterestMember2023-12-310001172724gfi:GoldFieldsAndEngineersAndPlannersMembergfi:TwarkaAndDamangMembergfi:LoansToContractorsMember2020-12-310001172724gfi:GoldFieldsAndEngineersAndPlannersMembergfi:TwarkaAndDamangMembergfi:LoansToContractorsMember2023-12-310001172724gfi:LoanAdvancedContractorMemberifrs-full:LifetimeExpectedCreditLossesMember2022-12-310001172724gfi:GoldFieldsAndEngineersAndPlannersMembergfi:TwarkaAndDamangMembergfi:LoansToContractorsMember2022-12-310001172724gfi:EarningsMembergfi:AsankoGoldMemberifrs-full:DiscontinuedOperationsMember2023-01-012023-12-310001172724gfi:EarningsMembergfi:AsankoGoldMemberifrs-full:DiscontinuedOperationsMember2022-01-012022-12-310001172724gfi:EarningsMembergfi:AsankoGoldMemberifrs-full:DiscontinuedOperationsMember2021-01-012021-12-310001172724gfi:AsankoGoldMembergfi:ImpairmentExpenseMemberifrs-full:DiscontinuedOperationsMember2021-01-012021-12-310001172724gfi:GalianoGoldIncformerlyAsankoGoldIncMembergfi:AsankoGoldMember2023-12-310001172724srt:ScenarioForecastMembergfi:AsankoGoldMember2025-12-312025-12-310001172724srt:ScenarioForecastMembergfi:AsankoGoldMember2026-12-312026-12-310001172724gfi:AsankoGoldMembergfi:DeferredConsiderationMember2023-12-310001172724srt:ScenarioForecastMembergfi:AsankoGoldMember2023-12-212023-12-210001172724ifrs-full:ContingentConsiderationMembergfi:AsankoGoldMember2023-12-310001172724srt:ScenarioForecastMembergfi:AsankoGoldMember2024-01-012026-12-310001172724gfi:AsankoGoldMember2023-01-012023-12-310001172724gfi:GalianoGoldIncformerlyAsankoGoldIncMembergfi:AsankoGoldMember2023-01-012023-12-310001172724gfi:GhanaGovernmentMembergfi:AsankoGoldMember2023-01-012023-12-310001172724srt:ScenarioForecastMembergfi:AsankoGoldMember2024-01-012024-03-31utr:oz0001172724gfi:GalianoGoldIncformerlyAsankoGoldIncMember2023-01-012023-12-310001172724gfi:GalianoGoldIncformerlyAsankoGoldIncMembersrt:MaximumMember2023-12-310001172724ifrs-full:OtherDisposalsOfAssetsMembergfi:AsankoGoldMember2024-03-042024-03-040001172724gfi:GalianoGoldIncformerlyAsankoGoldIncMemberifrs-full:OtherDisposalsOfAssetsMember2024-03-040001172724gfi:AsankoGoldInvestmentMember2023-12-310001172724gfi:AsankoGoldInvestmentMember2022-12-310001172724gfi:AsankoGoldJointVentureMember2023-12-310001172724gfi:AsankoGoldJointVentureMember2022-12-310001172724gfi:AsankoRedeemablePreferenceSharesMember2023-12-310001172724gfi:AsankoRedeemablePreferenceSharesMember2022-12-310001172724gfi:RusoroMiningLimitedMember2023-12-310001172724gfi:RusoroMiningLimitedMember2022-12-310001172724srt:ScenarioForecastMembergfi:AsankoGoldMember2024-01-012026-12-310001172724gfi:RusoroMiningLimitedMemberifrs-full:OtherDisposalsOfAssetsMember2024-01-090001172724gfi:RusoroMiningLimitedMemberifrs-full:OtherDisposalsOfAssetsMember2024-01-092024-01-09utr:D0001172724gfi:RusoroMiningLimitedMember2023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:GrossCarryingAmountMember2021-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2021-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2021-12-310001172724ifrs-full:GrossCarryingAmountMember2021-12-310001172724ifrs-full:GrossCarryingAmountMember2022-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2022-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2022-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:GrossCarryingAmountMember2022-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:GrossCarryingAmountMember2022-01-012022-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2022-01-012022-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2022-01-012022-12-310001172724ifrs-full:GrossCarryingAmountMember2022-01-012022-12-310001172724ifrs-full:GrossCarryingAmountMember2023-01-012023-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2023-01-012023-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2023-01-012023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:GrossCarryingAmountMember2023-01-012023-12-310001172724ifrs-full:GrossCarryingAmountMember2023-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2021-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2021-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2021-12-310001172724ifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2021-12-310001172724ifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-01-012022-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-01-012022-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-01-012022-12-310001172724ifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2022-01-012022-12-310001172724ifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-01-012023-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-01-012023-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-01-012023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-01-012023-12-310001172724ifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMemberifrs-full:AccumulatedDepreciationAmortisationAndImpairmentMember2023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMember2022-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMember2022-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMember2022-12-310001172724gfi:RightOfUseAssetsRelatingToMineDevelopmentInfrastructureAndOtherAssetsMember2023-12-310001172724gfi:MineDevelopmentInfrastructureAndOtherAssetsMember2023-12-310001172724gfi:LandMineralRightsAndRehabilitationAssetsMember2023-12-310001172724gfi:SalaresNorteProjectMember2023-01-012023-12-310001172724gfi:SalaresNorteProjectMember2022-01-012022-12-310001172724gfi:OsiskoMiningIncorporatedMembergfi:WindfallProjectMember2023-05-022023-05-0200011727242023-05-02gfi:director0001172724gfi:WindfallProjectMember2023-05-022023-12-31iso4217:CAD0001172724gfi:WindfallProjectMember2023-07-312023-07-310001172724gfi:WindfallProjectMember2023-12-312023-12-310001172724gfi:A300mEnvironmentalImpactAssessmentEIAPermitMembergfi:WindfallProjectMember2023-12-310001172724gfi:A300mEnvironmentalImpactAssessmentEIAPermitMembergfi:WindfallProjectMember2023-05-020001172724gfi:A75mDevelopmentalExplorationProjectsAndTargetsMembergfi:WindfallProjectMember2023-12-310001172724gfi:A75mDevelopmentalExplorationProjectsAndTargetsMembergfi:WindfallProjectMember2023-05-020001172724gfi:WindfallProjectMember2023-05-032023-12-310001172724gfi:A300mEnvironmentalImpactAssessmentEIAPermitMembergfi:WindfallProjectMember2023-05-032023-12-310001172724gfi:A75mDevelopmentalExplorationProjectsAndTargetsMembergfi:WindfallProjectMember2023-05-032023-12-310001172724gfi:WindfallProjectMember2023-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2023-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2022-12-310001172724gfi:AsankoGoldMemberifrs-full:NoncurrentAssetsHeldForSaleMember2023-12-310001172724gfi:AsankoGoldMember2022-12-310001172724gfi:WindfallProjectMember2023-12-310001172724gfi:WindfallProjectMember2022-12-310001172724gfi:OtherAssociatesMember2023-12-310001172724gfi:OtherAssociatesMember2022-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2023-01-012023-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2022-01-012022-12-310001172724gfi:FarSoutheastGoldResourcesIncorporatedMember2021-01-012021-12-310001172724gfi:EarningsMembergfi:AsankoGoldMember2023-01-012023-12-310001172724gfi:EarningsMembergfi:AsankoGoldMember2022-01-012022-12-310001172724gfi:EarningsMembergfi:AsankoGoldMember2021-01-012021-12-310001172724gfi:AsankoGoldMembergfi:ImpairmentExpenseMember2023-01-012023-12-310001172724gfi:AsankoGoldMembergfi:ImpairmentExpenseMember2022-01-012022-12-310001172724gfi:AsankoGoldMembergfi:ImpairmentExpenseMember2021-01-012021-12-310001172724gfi:WindfallProjectMembergfi:ImpairmentExpenseMember2023-01-012023-12-310001172724gfi:WindfallProjectMembergfi:ImpairmentExpenseMember2022-01-012022-12-310001172724gfi:WindfallProjectMembergfi:ImpairmentExpenseMember2021-01-012021-12-310001172724gfi:OtherAssociatesMember2023-01-012023-12-310001172724gfi:OtherAssociatesMember2022-01-012022-12-310001172724gfi:OtherAssociatesMember2021-01-012021-12-310001172724ifrs-full:AggregateContinuingAndDiscontinuedOperationsMember2023-01-012023-12-310001172724ifrs-full:AggregateContinuingAndDiscontinuedOperationsMember2022-01-012022-12-310001172724ifrs-full:AggregateContinuingAndDiscontinuedOperationsMember2021-01-012021-12-310001172724gfi:LepantoConsolidatedMiningCompanyMember2023-01-012023-12-310001172724gfi:AsankoGoldGhanaLimitedMember2023-01-012023-12-310001172724gfi:ShikaGroupFinanceLimitedMember2023-01-012023-12-310001172724gfi:AdansiGoldCompanyGhanaLimitedMember2023-01-012023-12-310001172724gfi:AsankoGoldMember2023-12-310001172724gfi:AsankoGoldMember2023-01-012023-12-310001172724gfi:AsankoGoldMember2022-01-012022-12-310001172724gfi:AsankoGoldMember2023-12-310001172724gfi:AsankoGoldMember2022-12-310001172724gfi:AsankoGoldMembergfi:ImpairmentTriggerDuringTwoThousandTwentyMember2021-01-012021-12-310001172724gfi:WindfallProjectMember2023-07-312023-12-310001172724gfi:WindfallProjectMember2023-01-012023-12-310001172724gfi:WindfallProjectMember2022-12-310001172724gfi:WindfallProjectMember2023-12-310001172724gfi:LunnonMetalsLimitedMember2023-12-310001172724gfi:LunnonMetalsLimitedMember2022-12-310001172724gfi:RusoroMiningLimitedMember2022-12-310001172724gfi:LunnonMetalsLimitedMember2023-01-012023-12-310001172724gfi:LunnonMetalsLimitedMember2022-01-012022-12-310001172724gfi:RusoroMiningLimitedMember2023-01-012023-12-310001172724gfi:RusoroMiningLimitedMember2022-01-012022-12-310001172724gfi:RusoroMiningLimitedMember2016-08-222016-08-220001172724gfi:RusoroMiningLimitedMember2017-12-062017-12-060001172724gfi:RusoroMiningLimitedMember2018-10-190001172724gfi:RusoroMiningLimitedMember2023-07-100001172724gfi:GruyereGoldProjectMember2016-12-132016-12-130001172724ifrs-full:JointOperationsMember2023-12-31iso4217:AUD0001172724ifrs-full:JointOperationsMember2022-12-310001172724gfi:RedeemablePreferredStockMember1Membergfi:AsankoGoldMember2023-12-310001172724gfi:RedeemablePreferredStockMember1Membergfi:AsankoGoldMember2022-12-310001172724gfi:MagmaticResourcesLimitedMember2023-12-310001172724gfi:MagmaticResourcesLimitedMember2022-12-310001172724gfi:ChakanaCopperCorpMember2023-12-310001172724gfi:ChakanaCopperCorpMember2022-12-310001172724gfi:LefroyExplorationLimitedMember2023-12-310001172724gfi:LefroyExplorationLimitedMember2022-12-310001172724gfi:TorqResourcesIncMember2023-12-310001172724gfi:TorqResourcesIncMember2022-12-310001172724gfi:TesoroGoldLimitedMember2023-12-310001172724gfi:TesoroGoldLimitedMember2022-12-310001172724gfi:MineralResourcesLimitedMember2023-12-310001172724gfi:MineralResourcesLimitedMember2022-12-310001172724country:ZA2023-12-310001172724country:ZA2022-12-310001172724country:GH2023-12-310001172724country:GH2022-12-310001172724gfi:GoldSalesMember2023-12-310001172724gfi:GoldSalesMember2022-12-310001172724gfi:CopperConcentrateMember2023-12-310001172724gfi:CopperConcentrateMember2022-12-310001172724gfi:OtherMember2023-12-310001172724gfi:OtherMember2022-12-310001172724country:AU2023-12-310001172724country:AU2022-12-310001172724country:PE2023-12-310001172724country:PE2022-12-310001172724ifrs-full:OrdinarySharesMember2022-12-310001172724ifrs-full:OrdinarySharesMember2021-12-310001172724ifrs-full:OrdinarySharesMember2023-01-012023-12-310001172724ifrs-full:OrdinarySharesMember2022-01-012022-12-31gfi:votesPerShare0001172724ifrs-full:TopOfRangeMember2023-12-310001172724srt:MinimumMembergfi:GoldFieldsLtdMember2023-01-012023-12-310001172724gfi:PublicInvestmentCorporationMember2023-12-310001172724gfi:VanEckVectorsGoldMinersETFMember2023-12-310001172724gfi:DeferredTaxLiabilitiesMiningAssetsMember2023-12-310001172724gfi:DeferredTaxLiabilitiesMiningAssetsMember2022-12-310001172724ifrs-full:RightofuseAssetsMember2023-12-310001172724ifrs-full:RightofuseAssetsMember2022-12-310001172724gfi:DeferredTaxLiabilitiesEnvironmentalTrustFundsMember2023-12-310001172724gfi:DeferredTaxLiabilitiesEnvironmentalTrustFundsMember2022-12-310001172724gfi:DeferredTaxLiabilitiesInventoriesMember2023-12-310001172724gfi:DeferredTaxLiabilitiesInventoriesMember2022-12-310001172724gfi:DeferredTaxLiabilitiesOthersMember2023-12-310001172724gfi:DeferredTaxLiabilitiesOthersMember2022-12-310001172724gfi:DeferredTaxAssetsProvisionsMember2023-12-310001172724gfi:DeferredTaxAssetsProvisionsMember2022-12-310001172724gfi:DeferredTaxAssetsTaxLossesMember2023-12-310001172724gfi:DeferredTaxAssetsTaxLossesMember2022-12-310001172724gfi:DeferredTaxAssetsUnredeemedCapitalExpenditureMember2023-12-310001172724gfi:DeferredTaxAssetsUnredeemedCapitalExpenditureMember2022-12-310001172724gfi:DeferredTaxAssetsLeaseLiabilityMember2023-12-310001172724gfi:DeferredTaxAssetsLeaseLiabilityMember2022-12-310001172724gfi:FiveHundredMillionFiveYearNotesIssueMember2023-12-310001172724gfi:FiveHundredMillionFiveYearNotesIssueMember2023-01-012023-12-310001172724gfi:FiveHundredMillionFiveYearNotesIssueMember2022-12-310001172724gfi:FiveHundredMillionTenYearNotesIssueMember2023-12-310001172724gfi:FiveHundredMillionTenYearNotesIssueMember2023-01-012023-12-310001172724gfi:FiveHundredMillionTenYearNotesIssueMember2022-12-310001172724gfi:UsOneFiftyMillionRevolvingSeniorSecuredCreditFacilityNewMember2023-12-310001172724gfi:UsOneFiftyMillionRevolvingSeniorSecuredCreditFacilityNewMember2022-12-310001172724gfi:UsHundredMillionRevolvingCreditFacilitymemberMember2023-12-310001172724gfi:UsHundredMillionRevolvingCreditFacilitymemberMember2022-12-310001172724gfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMember2023-12-310001172724gfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMember2022-12-310001172724gfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2023-12-310001172724gfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2022-12-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2023-12-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2022-12-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMember2023-12-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMember2023-01-012023-12-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMember2022-12-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMember2023-12-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMember2023-01-012023-12-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMember2022-12-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2023-05-250001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2023-12-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2022-12-310001172724gfi:ROneThousandFiveHundredMillionNedbankRevolvingCreditFacilityMember2023-12-310001172724gfi:ROneThousandFiveHundredMillionNedbankRevolvingCreditFacilityMember2022-12-310001172724gfi:RFiveHundredMillionNedbankRevolvingCreditFacilityMember2023-12-310001172724gfi:RFiveHundredMillionNedbankRevolvingCreditFacilityMember2022-12-310001172724gfi:RfivehundredmillionrandmerchantbankrevolvingcreditfacilityMember2023-12-310001172724gfi:RfivehundredmillionrandmerchantbankrevolvingcreditfacilityMember2022-12-310001172724gfi:ROneThousandMillionRandMerchantBankRevolvingCreditFacilityMember2023-12-310001172724gfi:ROneThousandMillionRandMerchantBankRevolvingCreditFacilityMember2022-12-310001172724gfi:RFiveHundredMillionABSABankRevolvingCreditFacilityMember2023-12-310001172724gfi:RFiveHundredMillionABSABankRevolvingCreditFacilityMember2022-12-310001172724gfi:RFiveHundredMillionABSABankRevolvingCreditFacilityNewMember2023-12-310001172724gfi:RFiveHundredMillionABSABankRevolvingCreditFacilityNewMember2022-12-310001172724gfi:RFiveHundredMillionStandardBankRevolvingCreditFacilityMember2023-12-310001172724gfi:RFiveHundredMillionStandardBankRevolvingCreditFacilityMember2022-12-310001172724gfi:ShorttermRandUncommittedCreditFacilitiesMember2023-12-310001172724gfi:ShorttermRandUncommittedCreditFacilitiesMember2022-12-310001172724gfi:UsFiveHundredMillionFiveYearNotesMember2019-05-090001172724gfi:FiveHundredMillionFiveYearNotesIssueMember2019-05-092019-05-090001172724gfi:UsFiveHundredMillionTenYearNotesMember2019-05-090001172724gfi:FiveHundredMillionTenYearNotesIssueMember2019-05-092019-05-0900011727242019-05-092019-05-090001172724gfi:UsFiveHundredMillionFiveYearNotesMember2023-12-310001172724gfi:UsFiveHundredMillionFiveYearNotesMember2022-12-310001172724gfi:UsFiveHundredMillionTenYearNotesMember2023-12-310001172724gfi:UsFiveHundredMillionTenYearNotesMember2022-12-310001172724gfi:UsOneFiftyMillionRevolvingSeniorSecuredCreditFacilityNewMembergfi:RevolvingCreditFacility1Member2021-04-150001172724gfi:UsHundredMillionRevolvingCreditFacilitymemberMembergfi:RevolvingCreditFacility1Member2021-09-270001172724gfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMembergfi:RevolvingCreditFacility1Member2020-11-190001172724gfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMembergfi:RevolvingCreditFacility1Member2023-09-260001172724gfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMembergfi:RevolvingCreditFacilityAccordionOptionMember2020-11-19gfi:priority0001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2019-07-250001172724gfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2019-07-25gfi:tranche0001172724gfi:TranchesOneMembergfi:ThreeYearsRevolvingCreditFacilityMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2019-07-250001172724gfi:TranchesOneMembergfi:ThreeYearsRevolvingCreditFacilityMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2019-07-252019-07-250001172724gfi:FiveYearsRevolvingCreditFacilitMembergfi:GoldFieldsGhanaHoldingsMembergfi:TranchesTwoMembergfi:RevolvingCreditFacility1Member2019-07-250001172724gfi:FiveYearsRevolvingCreditFacilitMembergfi:GoldFieldsGhanaHoldingsMembergfi:TranchesTwoMembergfi:RevolvingCreditFacility1Member2019-07-252019-07-250001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2020-07-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMembergfi:GoldFieldsGhanaHoldingsMember2020-07-310001172724gfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2020-07-012020-07-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Memberifrs-full:NotLaterThanOneYearMember2020-07-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMemberifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2020-07-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMemberifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2020-07-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMemberifrs-full:LaterThanTwoYearsAndNotLaterThanThreeYearsMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2020-07-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2021-07-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMembergfi:GoldFieldsGhanaHoldingsMember2021-07-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Memberifrs-full:NotLaterThanOneYearMember2021-07-310001172724gfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Memberifrs-full:NotLaterThanOneYearMember2021-07-012021-07-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMembergfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2021-07-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2021-07-012021-07-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Memberifrs-full:NotLaterThanOneYearMember2021-07-310001172724gfi:FacilityAUsSixHundredsMillionThreeYearsRevolvingCreditFacilityMemberifrs-full:LaterThanOneYearAndNotLaterThanThreeYearsMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2021-07-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMemberifrs-full:LaterThanOneYearAndNotLaterThanThreeYearsMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Member2021-07-310001172724gfi:FacilityBUSSixHundredsMillionFiveYearsRevolvingCreditFacilityMembergfi:GoldFieldsGhanaHoldingsMembergfi:RevolvingCreditFacility1Memberifrs-full:LaterThanThreeYearsAndNotLaterThanFiveYearsMember2021-07-310001172724gfi:RevolvingCreditFacilityNewMembergfi:GoldFieldsGhanaHoldingsMember2023-05-250001172724gfi:RevolvingCreditFacilityNewMembergfi:GoldFieldsGhanaHoldingsMember2023-05-252023-05-25gfi:term0001172724gfi:WindfallMiningGroupPartnershipMembergfi:RevolvingCreditFacilityNewMember2023-10-310001172724gfi:ROneThousandFiveHundredMillionNedbankRevolvingCreditFacilityMember2023-05-080001172724gfi:RFiveHundredMillionNedbankRevolvingCreditFacilityMember2023-05-080001172724gfi:RfivehundredmillionrandmerchantbankrevolvingcreditfacilityMember2020-04-150001172724gfi:ROneThousandMillionRandMerchantBankRevolvingCreditFacilityMember2023-04-190001172724gfi:RFiveHundredMillionABSABankRevolvingCreditFacilityNewMember2023-05-050001172724gfi:RFiveHundredMillionStandardBankRevolvingCreditFacilityMember2023-05-080001172724currency:USDgfi:FiveHundredMillionFiveYearNotesIssueMember2022-12-310001172724currency:USDgfi:FiveHundredMillionFiveYearNotesIssueMember2021-12-310001172724currency:USDgfi:FiveHundredMillionFiveYearNotesIssueMember2023-01-012023-12-310001172724currency:USDgfi:FiveHundredMillionFiveYearNotesIssueMember2022-01-012022-12-310001172724currency:USDgfi:FiveHundredMillionFiveYearNotesIssueMember2023-12-310001172724currency:USDgfi:FiveHundredMillionTenYearNotesIssueMember2022-12-310001172724currency:USDgfi:FiveHundredMillionTenYearNotesIssueMember2021-12-310001172724currency:USDgfi:FiveHundredMillionTenYearNotesIssueMember2023-01-012023-12-310001172724currency:USDgfi:FiveHundredMillionTenYearNotesIssueMember2022-01-012022-12-310001172724currency:USDgfi:FiveHundredMillionTenYearNotesIssueMember2023-12-310001172724currency:USDgfi:UsOneFiftyMillionRevolvingSeniorSecuredCreditFacilityNewMember2022-12-310001172724currency:USDgfi:UsOneFiftyMillionRevolvingSeniorSecuredCreditFacilityNewMember2021-12-310001172724currency:USDgfi:UsOneFiftyMillionRevolvingSeniorSecuredCreditFacilityNewMember2023-12-310001172724currency:AUDgfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMember2023-01-012023-12-310001172724currency:AUDgfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMember2022-01-012022-12-310001172724currency:AUDgfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMember2023-12-310001172724currency:AUDgfi:AUFiveHundredMillionDollarSyndicatedRevolvingCreditFacilityOldMember2022-12-310001172724currency:AUDgfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2023-01-012023-12-310001172724currency:AUDgfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2021-01-012021-12-310001172724currency:AUDgfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2022-01-012022-12-310001172724currency:AUDgfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2023-12-310001172724currency:AUDgfi:AufivehundredmilliondollarsyndicatedrevolvingcreditfacilitynewMember2022-12-310001172724currency:USDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2023-01-012023-12-310001172724currency:USDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2022-01-012022-12-310001172724currency:USDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2023-12-310001172724currency:USDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesOldMember2022-12-310001172724currency:AUDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2023-01-012023-12-310001172724currency:AUDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2022-01-012022-12-310001172724currency:AUDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2023-12-310001172724currency:AUDgfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2022-12-310001172724currency:AUD2023-12-310001172724currency:AUD2022-12-310001172724gfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2023-01-012023-12-310001172724gfi:WindfallProjectMembergfi:USOneThousandTwoHundredsMillionRevolvingCreditFacilitiesNewMember2023-01-012023-12-310001172724currency:CAD2022-12-310001172724ifrs-full:NotLaterThanOneYearMember2023-12-310001172724ifrs-full:NotLaterThanOneYearMember2022-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMember2023-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMember2022-12-310001172724ifrs-full:LaterThanTwoYearsAndNotLaterThanThreeYearsMember2023-12-310001172724ifrs-full:LaterThanTwoYearsAndNotLaterThanThreeYearsMember2022-12-310001172724ifrs-full:LaterThanThreeYearsAndNotLaterThanFiveYearsMember2023-12-310001172724ifrs-full:LaterThanThreeYearsAndNotLaterThanFiveYearsMember2022-12-310001172724gfi:YearOneMembercountry:ZA2023-12-310001172724gfi:YearTwoMembercountry:ZA2023-12-310001172724gfi:YearThreeMembercountry:ZA2023-12-310001172724gfi:YearFourOnwardsMembercountry:ZA2023-12-310001172724country:GHgfi:YearOneMember2023-12-310001172724gfi:YearTwoMembercountry:GH2023-12-310001172724gfi:YearThreeMembercountry:GH2023-12-310001172724gfi:YearFourOnwardsMembercountry:GH2023-12-310001172724country:GHifrs-full:BottomOfRangeMember2023-12-310001172724country:GHifrs-full:TopOfRangeMember2023-12-310001172724country:AUgfi:YearOneMember2023-12-310001172724gfi:YearTwoMembercountry:AU2023-12-310001172724gfi:YearThreeMembercountry:AU2023-12-310001172724gfi:YearFourOnwardsMembercountry:AU2023-12-310001172724country:AUifrs-full:BottomOfRangeMember2023-12-310001172724country:AUifrs-full:TopOfRangeMember2023-12-310001172724country:PEgfi:YearOneMember2023-12-310001172724gfi:YearTwoMembercountry:PE2023-12-310001172724gfi:YearThreeMembercountry:PE2023-12-310001172724gfi:YearFourOnwardsMembercountry:PE2023-12-310001172724gfi:YearOneMembercountry:CL2023-12-310001172724gfi:YearTwoMembercountry:CL2023-12-310001172724gfi:YearThreeMembercountry:CL2023-12-310001172724gfi:YearFourOnwardsMembercountry:CL2023-12-310001172724country:CL2023-12-310001172724gfi:YearOneMembercountry:ZA2022-12-310001172724gfi:YearTwoMembercountry:ZA2022-12-310001172724gfi:YearThreeMembercountry:ZA2022-12-310001172724gfi:YearFourOnwardsMembercountry:ZA2022-12-310001172724country:GHgfi:YearOneMember2022-12-310001172724gfi:YearTwoMembercountry:GH2022-12-310001172724gfi:YearThreeMembercountry:GH2022-12-310001172724gfi:YearFourOnwardsMembercountry:GH2022-12-310001172724country:GHifrs-full:BottomOfRangeMember2022-12-310001172724country:GHifrs-full:TopOfRangeMember2022-12-310001172724country:AUgfi:YearOneMember2022-12-310001172724gfi:YearTwoMembercountry:AU2022-12-310001172724gfi:YearThreeMembercountry:AU2022-12-310001172724gfi:YearFourOnwardsMembercountry:AU2022-12-310001172724country:AUifrs-full:BottomOfRangeMember2022-12-310001172724country:AUifrs-full:TopOfRangeMember2022-12-310001172724country:PEgfi:YearOneMember2022-12-310001172724gfi:YearTwoMembercountry:PE2022-12-310001172724gfi:YearThreeMembercountry:PE2022-12-310001172724gfi:YearFourOnwardsMembercountry:PE2022-12-310001172724gfi:YearOneMembercountry:CL2022-12-310001172724gfi:YearTwoMembercountry:CL2022-12-310001172724gfi:YearThreeMembercountry:CL2022-12-310001172724gfi:YearFourOnwardsMembercountry:CL2022-12-310001172724country:CL2022-12-310001172724gfi:SilicosisMember2023-12-310001172724gfi:SilicosisMember2022-12-310001172724gfi:SilicosisMembergfi:GovernmentBondsMember2023-12-310001172724gfi:SilicosisMembergfi:GovernmentBondsMember2022-12-310001172724country:CA2022-12-310001172724gfi:LaterThanOneYearsAndNotLaterThanFiveYearsMember2023-12-310001172724gfi:LaterThanOneYearsAndNotLaterThanFiveYearsMember2022-12-310001172724ifrs-full:LaterThanFiveYearsMember2023-12-310001172724ifrs-full:LaterThanFiveYearsMember2022-12-310001172724gfi:SalaresNorteMember2023-12-310001172724gfi:SalaresNorteMember2022-12-310001172724gfi:SouthAfricanPeruvianGhanaianAndAustralianOperationsMember2023-12-310001172724gfi:SouthAfricanPeruvianGhanaianAndAustralianOperationsMember2022-12-310001172724gfi:RandgoldAndExplorationSummonsMembergfi:AllegedTheftsMember2023-12-310001172724gfi:SilicosisMember2023-12-31gfi:company0001172724gfi:SilicosisMember2022-12-310001172724gfi:SilicosisMemberifrs-full:TopOfRangeMember2023-12-310001172724gfi:SilicosisMemberifrs-full:BottomOfRangeMember2023-12-310001172724gfi:SilicosisMember2023-01-012023-12-310001172724gfi:SilicosisMember2022-01-012022-12-310001172724gfi:DividendsDeclaredMember2024-02-232024-02-230001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:FinancialAssetsAtFairValueThroughProfitOrLossMandatorilyMeasuredAtFairValueCategoryMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:AtFairValueMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:GrossCarryingAmountMemberifrs-full:FinancialAssetsAtFairValueThroughOtherComprehensiveIncomeCategoryMember2023-12-310001172724ifrs-full:GrossCarryingAmountMemberifrs-full:FinancialAssetsAtAmortisedCostCategoryMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724ifrs-full:GrossCarryingAmountMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724ifrs-full:AtFairValueMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMemberifrs-full:GrossCarryingAmountMemberifrs-full:FinancialLiabilitiesAtFairValueThroughProfitOrLossCategoryMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMemberifrs-full:AtFairValueMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:GrossCarryingAmountMemberifrs-full:FinancialLiabilitiesAtFairValueThroughProfitOrLossCategoryMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:AtFairValueMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMembergfi:OtherFinancialLiabilitiesMeasuredAtAmortisedCostCategoryMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:AtFairValueMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A75mDevelopmentalExplorationProjectsAndTargetsMembergfi:OtherFinancialLiabilitiesMeasuredAtAmortisedCostCategoryMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A75mDevelopmentalExplorationProjectsAndTargetsMemberifrs-full:GrossCarryingAmountMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A75mDevelopmentalExplorationProjectsAndTargetsMemberifrs-full:AtFairValueMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:FinancialAssetsAtFairValueThroughProfitOrLossMandatorilyMeasuredAtFairValueCategoryMemberifrs-full:GrossCarryingAmountMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:GrossCarryingAmountMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:AtFairValueMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:GrossCarryingAmountMemberifrs-full:FinancialAssetsAtFairValueThroughOtherComprehensiveIncomeCategoryMember2022-12-310001172724ifrs-full:GrossCarryingAmountMemberifrs-full:FinancialAssetsAtAmortisedCostCategoryMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724ifrs-full:GrossCarryingAmountMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724ifrs-full:AtFairValueMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMembergfi:OtherFinancialLiabilitiesMeasuredAtAmortisedCostCategoryMemberifrs-full:GrossCarryingAmountMember2022-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMembergfi:OtherFinancialLiabilitiesMeasuredAtAmortisedCostCategoryMemberifrs-full:AtFairValueMember2022-12-310001172724gfi:FiveHundredMillionFiveYearNotesIssueMember2022-01-012022-12-310001172724gfi:FiveHundredMillionTenYearNotesIssueMember2022-01-012022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMemberifrs-full:Level1OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMemberifrs-full:Level2OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMemberifrs-full:Level3OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMemberifrs-full:Level1OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMemberifrs-full:Level2OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:EnvironmentalTrustFundsMemberifrs-full:Level3OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level2OfFairValueHierarchyMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level2OfFairValueHierarchyMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMembergfi:TradeReceivablesFromProvisionalCopperConcentrateSalesMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:ListedInvestmentsMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMembergfi:ListedInvestmentsMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:ListedInvestmentsMemberifrs-full:Level2OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMembergfi:ListedInvestmentsMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:ListedInvestmentsMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMembergfi:ListedInvestmentsMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:ListedInvestmentsMemberifrs-full:Level2OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMembergfi:ListedInvestmentsMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMemberifrs-full:Level1OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMemberifrs-full:Level2OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMemberifrs-full:Level3OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMemberifrs-full:Level1OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMemberifrs-full:Level2OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialAssetsAtFairValueMembergfi:AsankoRedeemablePreferenceSharesMemberifrs-full:Level3OfFairValueHierarchyMember2022-12-310001172724gfi:EnvironmentalTrustFundsMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724gfi:EnvironmentalTrustFundsMemberifrs-full:Level1OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724gfi:EnvironmentalTrustFundsMemberifrs-full:Level2OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724gfi:EnvironmentalTrustFundsMemberifrs-full:Level3OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724gfi:EnvironmentalTrustFundsMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724gfi:EnvironmentalTrustFundsMemberifrs-full:Level1OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724gfi:EnvironmentalTrustFundsMemberifrs-full:Level2OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724gfi:EnvironmentalTrustFundsMemberifrs-full:Level3OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724gfi:LoanAdvancedContractorMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724ifrs-full:Level1OfFairValueHierarchyMembergfi:LoanAdvancedContractorMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724gfi:LoanAdvancedContractorMemberifrs-full:Level2OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724ifrs-full:Level3OfFairValueHierarchyMembergfi:LoanAdvancedContractorMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2023-12-310001172724gfi:LoanAdvancedContractorMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724ifrs-full:Level1OfFairValueHierarchyMembergfi:LoanAdvancedContractorMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724gfi:LoanAdvancedContractorMemberifrs-full:Level2OfFairValueHierarchyMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724ifrs-full:Level3OfFairValueHierarchyMembergfi:LoanAdvancedContractorMembergfi:FinancialAssetsNotMeasuredAtFairValueMember2022-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMemberifrs-full:Level2OfFairValueHierarchyMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMember2023-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMember2022-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMember2022-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMemberifrs-full:Level2OfFairValueHierarchyMember2022-12-310001172724ifrs-full:FinancialLiabilitiesAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMembergfi:A300mEnvironmentalImpactAssessmentEIAPermitMember2022-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:Level2OfFairValueHierarchyMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMember2023-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMember2022-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:Level1OfFairValueHierarchyMember2022-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:Level2OfFairValueHierarchyMember2022-12-310001172724gfi:FinancialLiabilitiesNotMeasuredAtFairValueMemberifrs-full:Level3OfFairValueHierarchyMember2022-12-310001172724gfi:CounterPartyExposureMember2023-01-012023-12-310001172724ifrs-full:CreditRiskMembergfi:EnvironmentalTrustFundsMember2023-12-310001172724ifrs-full:CreditRiskMembergfi:EnvironmentalTrustFundsMember2022-12-310001172724ifrs-full:CreditRiskMemberifrs-full:TradeReceivablesMember2023-12-310001172724ifrs-full:CreditRiskMemberifrs-full:TradeReceivablesMember2022-12-310001172724gfi:LoanAdvancedContractorMemberifrs-full:CreditRiskMember2023-12-310001172724gfi:LoanAdvancedContractorMemberifrs-full:CreditRiskMember2022-12-310001172724ifrs-full:CreditRiskMembergfi:CashAndCashEquivalentMember2023-12-310001172724ifrs-full:CreditRiskMembergfi:CashAndCashEquivalentMember2022-12-310001172724ifrs-full:TradeReceivablesMember2023-12-310001172724ifrs-full:TradeReceivablesMember2022-12-310001172724ifrs-full:CreditRiskMembercountry:GH2023-12-310001172724ifrs-full:CreditRiskMembercountry:GH2022-12-310001172724ifrs-full:CreditRiskMembercountry:AU2023-12-310001172724ifrs-full:CreditRiskMembercountry:AU2022-12-310001172724ifrs-full:CreditRiskMembercountry:PE2023-12-310001172724ifrs-full:CreditRiskMembercountry:PE2022-12-310001172724ifrs-full:CreditRiskMember2023-12-310001172724ifrs-full:CreditRiskMember2022-12-310001172724gfi:LoanAdvancedContractorMember2023-12-310001172724gfi:LoanAdvancedContractorMemberifrs-full:LifetimeExpectedCreditLossesMember2023-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMember2023-12-310001172724gfi:UsDollarBorrowingsMemberifrs-full:NotLaterThanOneYearMember2023-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMembergfi:UsDollarBorrowingsMember2023-12-310001172724gfi:UsDollarBorrowingsMemberifrs-full:LaterThanFiveYearsMember2023-12-310001172724gfi:UsDollarBorrowingsMember2023-12-310001172724gfi:CanadaDollarBorrowingsMemberifrs-full:NotLaterThanOneYearMember2023-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMembergfi:CanadaDollarBorrowingsMember2023-12-310001172724gfi:CanadaDollarBorrowingsMemberifrs-full:LaterThanFiveYearsMember2023-12-310001172724gfi:CanadaDollarBorrowingsMember2023-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMember2022-12-310001172724gfi:UsDollarBorrowingsMemberifrs-full:NotLaterThanOneYearMember2022-12-310001172724ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMembergfi:UsDollarBorrowingsMember2022-12-310001172724gfi:UsDollarBorrowingsMemberifrs-full:LaterThanFiveYearsMember2022-12-310001172724gfi:UsDollarBorrowingsMember2022-12-310001172724currency:ZARgfi:ClosingForeignExchangeRateMember2023-12-310001172724currency:ZARgfi:ClosingForeignExchangeRateMember2022-12-310001172724ifrs-full:LiquidityRiskMembergfi:UsDollarBorrowingsMember2023-12-310001172724ifrs-full:LiquidityRiskMembergfi:UsDollarBorrowingsMember2022-12-310001172724ifrs-full:CreditRiskMembergfi:CanadaDollarBorrowingsMember2023-12-310001172724gfi:SouthAfricaAndGhanaMember2023-12-310001172724gfi:SouthAfricaAndGhanaMember2022-12-310001172724ifrs-full:MarketRiskMembergfi:GhanaOilHedgeMember2023-01-012023-12-310001172724ifrs-full:MarketRiskMembergfi:GhanaOilHedgeMember2022-01-012022-12-310001172724ifrs-full:MarketRiskMembergfi:GhanaOilHedgeMember2021-01-012021-12-310001172724gfi:PeruCopperHedgeMemberifrs-full:MarketRiskMember2023-01-012023-12-310001172724gfi:PeruCopperHedgeMemberifrs-full:MarketRiskMember2022-01-012022-12-310001172724gfi:PeruCopperHedgeMemberifrs-full:MarketRiskMember2021-01-012021-12-310001172724gfi:AustraliaGoldHedgeMemberifrs-full:MarketRiskMember2023-01-012023-12-310001172724gfi:AustraliaGoldHedgeMemberifrs-full:MarketRiskMember2022-01-012022-12-310001172724gfi:AustraliaGoldHedgeMemberifrs-full:MarketRiskMember2021-01-012021-12-310001172724ifrs-full:MarketRiskMembergfi:AustraliaOilHedgeMember2023-01-012023-12-310001172724ifrs-full:MarketRiskMembergfi:AustraliaOilHedgeMember2022-01-012022-12-310001172724ifrs-full:MarketRiskMembergfi:AustraliaOilHedgeMember2021-01-012021-12-310001172724gfi:SalaresNorteForeignCurrencyHedgeMemberifrs-full:MarketRiskMember2023-01-012023-12-310001172724gfi:SalaresNorteForeignCurrencyHedgeMemberifrs-full:MarketRiskMember2022-01-012022-12-310001172724gfi:SalaresNorteForeignCurrencyHedgeMemberifrs-full:MarketRiskMember2021-01-012021-12-310001172724gfi:MaverixWarrantsGainOnFairValueMemberifrs-full:MarketRiskMember2023-01-012023-12-310001172724gfi:MaverixWarrantsGainOnFairValueMemberifrs-full:MarketRiskMember2022-01-012022-12-310001172724gfi:MaverixWarrantsGainOnFairValueMemberifrs-full:MarketRiskMember2021-01-012021-12-310001172724ifrs-full:MarketRiskMember2023-01-012023-12-310001172724ifrs-full:MarketRiskMember2022-01-012022-12-310001172724ifrs-full:MarketRiskMember2021-01-012021-12-310001172724gfi:UnrealisedGainlossAndPriorYearMarktomarketReversalsOnDerivativeContractsMemberifrs-full:MarketRiskMember2023-01-012023-12-310001172724gfi:UnrealisedGainlossAndPriorYearMarktomarketReversalsOnDerivativeContractsMemberifrs-full:MarketRiskMember2022-01-012022-12-310001172724gfi:UnrealisedGainlossAndPriorYearMarktomarketReversalsOnDerivativeContractsMemberifrs-full:MarketRiskMember2021-01-012021-12-310001172724ifrs-full:MarketRiskMembergfi:RealisedLossGainOnDerivativeContractsMember2023-01-012023-12-310001172724ifrs-full:MarketRiskMembergfi:RealisedLossGainOnDerivativeContractsMember2022-01-012022-12-310001172724ifrs-full:MarketRiskMembergfi:RealisedLossGainOnDerivativeContractsMember2021-01-012021-12-310001172724ifrs-full:CurrencyRiskMember2022-12-310001172724ifrs-full:CurrencyRiskMember2023-12-310001172724gfi:DecreaseOfTenPercentageMember2023-01-012023-12-310001172724gfi:DecreaseOfFivePercentageMember2023-01-012023-12-310001172724gfi:IncreaseOfFivePercentageMember2023-01-012023-12-310001172724gfi:IncreaseOfTenPercentageMember2023-01-012023-12-310001172724gfi:DecreaseOfTenPercentageMember2022-01-012022-12-310001172724gfi:DecreaseOfFivePercentageMember2022-01-012022-12-310001172724gfi:IncreaseOfFivePercentageMember2022-01-012022-12-310001172724gfi:IncreaseOfTenPercentageMember2022-01-012022-12-310001172724gfi:DecreaseOfTwoAndAHalfPercentageMember2023-01-012023-12-310001172724gfi:IncreaseOfTwoAndAHalfPercentageMember2023-01-012023-12-310001172724gfi:DecreaseOfTwoAndAHalfPercentageMember2022-01-012022-12-310001172724gfi:IncreaseOfTwoAndAHalfPercentageMember2022-01-012022-12-310001172724gfi:OneYearEarlierMember2023-01-012023-12-310001172724gfi:OneYearLaterMember2023-01-012023-12-310001172724gfi:OneYearEarlierMember2022-01-012022-12-310001172724gfi:OneYearLaterMember2022-01-012022-12-310001172724gfi:DecreaseOfOnePercentageMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePercentageMember2023-01-012023-12-310001172724gfi:SixMonthsEarlierMember2023-01-012023-12-310001172724gfi:SixMonthsLaterMember2023-01-012023-12-310001172724gfi:RevolvingCreditFacilityNewMember2023-12-310001172724ifrs-full:InterestRateRiskMembergfi:InterestBearingBorrowingsMember2023-12-310001172724ifrs-full:InterestRateRiskMembergfi:InterestBearingBorrowingsMember2022-12-310001172724gfi:RevolvingCreditFacilityNewMember2022-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMembergfi:DecreaseOfOnePointFivePercentageMember2023-01-012023-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMembergfi:DecreaseOfOnePercentageMember2023-01-012023-12-310001172724gfi:DecreaseOfZeroPointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2023-01-012023-12-310001172724gfi:IncreaseOfZeroPointPercentagePointsMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2023-01-012023-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMembergfi:DecreaseOfOnePointFivePercentageMember2023-01-012023-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMembergfi:DecreaseOfOnePercentageMember2023-01-012023-12-310001172724gfi:DecreaseOfZeroPointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2023-01-012023-12-310001172724gfi:IncreaseOfZeroPointPercentagePointsMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2023-01-012023-12-310001172724ifrs-full:InterestRateRiskMembergfi:DecreaseOfOnePointFivePercentageMember2023-01-012023-12-310001172724ifrs-full:InterestRateRiskMembergfi:DecreaseOfOnePercentageMember2023-01-012023-12-310001172724gfi:DecreaseOfZeroPointFivePercentageMemberifrs-full:InterestRateRiskMember2023-01-012023-12-310001172724gfi:IncreaseOfZeroPointPercentagePointsMemberifrs-full:InterestRateRiskMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePercentageMemberifrs-full:InterestRateRiskMember2023-01-012023-12-310001172724gfi:IncreaseOfOnePointFivePercentageMemberifrs-full:InterestRateRiskMember2023-01-012023-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMembergfi:DecreaseOfOnePointFivePercentageMember2022-01-012022-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMembergfi:DecreaseOfOnePercentageMember2022-01-012022-12-310001172724gfi:DecreaseOfZeroPointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2022-01-012022-12-310001172724gfi:IncreaseOfZeroPointPercentagePointsMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2022-01-012022-12-310001172724gfi:IncreaseOfOnePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2022-01-012022-12-310001172724gfi:IncreaseOfOnePointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInLondonInterbankOfferedRateSecuredOvernightFinancingRateAndCanadianDollarOfferedRateMember2022-01-012022-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMembergfi:DecreaseOfOnePointFivePercentageMember2022-01-012022-12-310001172724ifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMembergfi:DecreaseOfOnePercentageMember2022-01-012022-12-310001172724gfi:DecreaseOfZeroPointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2022-01-012022-12-310001172724gfi:IncreaseOfZeroPointPercentagePointsMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2022-01-012022-12-310001172724gfi:IncreaseOfOnePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2022-01-012022-12-310001172724gfi:IncreaseOfOnePointFivePercentageMemberifrs-full:InterestRateRiskMembergfi:ChangeInBankBillSwapBidRateMember2022-01-012022-12-310001172724ifrs-full:InterestRateRiskMembergfi:DecreaseOfOnePointFivePercentageMember2022-01-012022-12-310001172724ifrs-full:InterestRateRiskMembergfi:DecreaseOfOnePercentageMember2022-01-012022-12-310001172724gfi:DecreaseOfZeroPointFivePercentageMemberifrs-full:InterestRateRiskMember2022-01-012022-12-310001172724gfi:IncreaseOfZeroPointPercentagePointsMemberifrs-full:InterestRateRiskMember2022-01-012022-12-310001172724gfi:IncreaseOfOnePercentageMemberifrs-full:InterestRateRiskMember2022-01-012022-12-310001172724gfi:IncreaseOfOnePointFivePercentageMemberifrs-full:InterestRateRiskMember2022-01-012022-12-310001172724gfi:ChangeInBankBillSwapBidRateMembergfi:ClosingForeignExchangeRateMember2023-01-012023-12-310001172724gfi:ChangeInBankBillSwapBidRateMembergfi:ClosingForeignExchangeRateMember2022-01-012022-12-310001172724gfi:ExecutiveCommitteeAndNonexecutiveDirectorsMember2023-12-310001172724gfi:ExecutiveCommitteeAndNonexecutiveDirectorsMember2022-12-310001172724gfi:ExecutiveCommitteeAndNonexecutiveDirectorsMember2021-12-310001172724gfi:YsulemanMembergfi:IndependentNonExecutiveDirectorsMember2023-01-012023-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:BacchusMember2023-01-012023-12-310001172724gfi:SreidMembergfi:IndependentNonExecutiveDirectorsMember2023-01-012023-12-310001172724gfi:TgoodlaceMembergfi:IndependentNonExecutiveDirectorsMember2023-01-012023-12-310001172724gfi:AandaniMembergfi:IndependentNonExecutiveDirectorsMember2023-01-012023-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:PSibiyaMember2023-01-012023-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:JMcGillMember2023-01-012023-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:CBitarMember2023-01-012023-12-310001172724gfi:CSmitMembergfi:IndependentNonExecutiveDirectorsMember2023-01-012023-12-310001172724gfi:IndependentNonExecutiveDirectorsMember2023-01-012023-12-310001172724gfi:CcarolusMembergfi:IndependentNonExecutiveDirectorsMember2022-01-012022-12-310001172724gfi:YsulemanMembergfi:IndependentNonExecutiveDirectorsMember2022-01-012022-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:BacchusMember2022-01-012022-12-310001172724gfi:SreidMembergfi:IndependentNonExecutiveDirectorsMember2022-01-012022-12-310001172724gfi:TgoodlaceMembergfi:IndependentNonExecutiveDirectorsMember2022-01-012022-12-310001172724gfi:AandaniMembergfi:IndependentNonExecutiveDirectorsMember2022-01-012022-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:PSibiyaMember2022-01-012022-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:JMcGillMember2022-01-012022-12-310001172724gfi:IndependentNonExecutiveDirectorsMembergfi:CBitarMember2022-01-012022-12-310001172724gfi:IndependentNonExecutiveDirectorsMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:MpreeceMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:PschmidtMember2023-01-012023-12-310001172724gfi:ExecutiveDirectorsMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:BMokoatleMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:LriveraMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:NchohanMember2023-01-012023-12-310001172724gfi:BmattisonMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:TLeishmanMember2023-01-012023-12-310001172724gfi:AnagaserMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724gfi:SmathewsMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724gfi:RbardienMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:JMortotiMember2023-01-012023-12-310001172724gfi:KCarterMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:JMagagulaMember2023-01-012023-12-310001172724gfi:FSwanepoelMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724gfi:PrescribedOfficerMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMember2023-01-012023-12-310001172724gfi:PschmidtMember2023-01-012023-12-310001172724gfi:BmattisonMember2023-01-012023-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:CGriffithMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:PschmidtMember2022-01-012022-12-310001172724gfi:ExecutiveDirectorsMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:MpreeceMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:LriveraMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:RbutcherMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:NchohanMember2022-01-012022-12-310001172724gfi:BmattisonMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:TLeishmanMember2022-01-012022-12-310001172724gfi:AnagaserMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724gfi:SmathewsMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724gfi:RbardienMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMembergfi:JMortotiMember2022-01-012022-12-310001172724gfi:PrescribedOfficerMemberifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724ifrs-full:KeyManagementPersonnelOfEntityOrParentMember2022-01-012022-12-310001172724gfi:CGriffithMember2022-01-012022-12-310001172724gfi:PschmidtMember2022-01-012022-12-310001172724gfi:BmattisonMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:ZAgfi:SouthDeepMember2023-01-012023-12-310001172724gfi:TarkwaMemberifrs-full:OperatingSegmentsMembercountry:GH2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:DamangMembercountry:GH2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:GH2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CerroCoronaMembercountry:PE2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:SalaresNorteMembercountry:CL2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembersrt:SouthAmericaMembergfi:SalaresNorteMember2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:StivesMember2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:AgnewLawlersMember2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:GrannySmithMembercountry:AU2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:GruyereAustraliaMember2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AU2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CorporateAndOtherDomain2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMember2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:AsankoMembercountry:GHifrs-full:DiscontinuedOperationsMember2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:ZAgfi:SouthDeepMember2023-12-310001172724gfi:TarkwaMemberifrs-full:OperatingSegmentsMembercountry:GH2023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:DamangMembercountry:GH2023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:GH2023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CerroCoronaMembercountry:PE2023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:SalaresNorteMembercountry:CL2023-12-310001172724ifrs-full:OperatingSegmentsMembersrt:SouthAmericaMembergfi:SalaresNorteMember2023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:StivesMember2023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:AgnewLawlersMember2023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:GrannySmithMembercountry:AU2023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:GruyereAustraliaMember2023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AU2023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CorporateAndOtherDomain2023-12-310001172724ifrs-full:OperatingSegmentsMember2023-12-310001172724ifrs-full:OperatingSegmentsMembergfi:AsankoMembercountry:GHifrs-full:DiscontinuedOperationsMember2023-12-310001172724ifrs-full:AggregateContinuingAndDiscontinuedOperationsMember2023-12-310001172724gfi:SouthDeepMember2023-01-012023-12-310001172724gfi:PurchasePriceAllocationFairValueAdjustmentMembergfi:AsankoGoldMemberifrs-full:DiscontinuedOperationsMember2023-01-012023-12-310001172724gfi:AsankoMember2023-12-310001172724gfi:CorporateAndOtherDomain2023-01-012023-12-310001172724ifrs-full:OperatingSegmentsMembercountry:ZAgfi:SouthDeepMember2022-01-012022-12-310001172724gfi:TarkwaMemberifrs-full:OperatingSegmentsMembercountry:GH2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:DamangMembercountry:GH2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:GH2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CerroCoronaMembercountry:PE2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:SalaresNorteMembercountry:CL2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembersrt:SouthAmericaMembergfi:SalaresNorteMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:StivesMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:AgnewLawlersMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:GrannySmithMembercountry:AU2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:GruyereAustraliaMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AU2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CorporateAndOtherDomain2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:AsankoMembercountry:GHifrs-full:DiscontinuedOperationsMember2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:ZAgfi:SouthDeepMember2022-12-310001172724gfi:TarkwaMemberifrs-full:OperatingSegmentsMembercountry:GH2022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:DamangMembercountry:GH2022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:GH2022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CerroCoronaMembercountry:PE2022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:SalaresNorteMembercountry:CL2022-12-310001172724ifrs-full:OperatingSegmentsMembersrt:SouthAmericaMembergfi:SalaresNorteMember2022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:StivesMember2022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:AgnewLawlersMember2022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:GrannySmithMembercountry:AU2022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:GruyereAustraliaMember2022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AU2022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CorporateAndOtherDomain2022-12-310001172724ifrs-full:OperatingSegmentsMember2022-12-310001172724ifrs-full:OperatingSegmentsMembergfi:AsankoMembercountry:GHifrs-full:DiscontinuedOperationsMember2022-12-310001172724ifrs-full:AggregateContinuingAndDiscontinuedOperationsMember2022-12-310001172724gfi:SouthDeepMember2022-01-012022-12-310001172724gfi:PurchasePriceAllocationFairValueAdjustmentMembergfi:AsankoGoldMemberifrs-full:DiscontinuedOperationsMember2022-01-012022-12-310001172724gfi:AsankoMember2022-12-310001172724gfi:CorporateAndOtherDomain2022-01-012022-12-310001172724ifrs-full:OperatingSegmentsMembercountry:ZAgfi:SouthDeepMember2021-01-012021-12-310001172724gfi:TarkwaMemberifrs-full:OperatingSegmentsMembercountry:GH2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:DamangMembercountry:GH2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:GH2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CerroCoronaMembercountry:PE2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:SalaresNorteMembercountry:CL2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembersrt:SouthAmericaMembergfi:SalaresNorteMember2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:StivesMember2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:AgnewLawlersMember2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:GrannySmithMembercountry:AU2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:GruyereAustraliaMember2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AU2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CorporateAndOtherDomain2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMember2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:AsankoMembercountry:GHifrs-full:DiscontinuedOperationsMember2021-01-012021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:ZAgfi:SouthDeepMember2021-12-310001172724gfi:TarkwaMemberifrs-full:OperatingSegmentsMembercountry:GH2021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:DamangMembercountry:GH2021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:GH2021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CerroCoronaMembercountry:PE2021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:SalaresNorteMembercountry:CL2021-12-310001172724ifrs-full:OperatingSegmentsMembersrt:SouthAmericaMembergfi:SalaresNorteMember2021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:StivesMember2021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:AgnewLawlersMember2021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:GrannySmithMembercountry:AU2021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AUgfi:GruyereAustraliaMember2021-12-310001172724ifrs-full:OperatingSegmentsMembercountry:AU2021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:CorporateAndOtherDomain2021-12-310001172724ifrs-full:OperatingSegmentsMember2021-12-310001172724ifrs-full:OperatingSegmentsMembergfi:AsankoMembercountry:GHifrs-full:DiscontinuedOperationsMember2021-12-310001172724ifrs-full:AggregateContinuingAndDiscontinuedOperationsMember2021-12-310001172724gfi:SouthDeepMember2021-01-012021-12-310001172724gfi:PurchasePriceAllocationFairValueAdjustmentMembergfi:AsankoGoldMemberifrs-full:DiscontinuedOperationsMember2021-01-012021-12-310001172724gfi:AsankoMember2021-12-310001172724gfi:CorporateAndOtherDomain2021-01-012021-12-310001172724gfi:AbossoGoldfieldsLimitedMembergfi:ClassASharesMember2023-12-310001172724gfi:AbossoGoldfieldsLimitedMembergfi:ClassASharesMember2022-12-310001172724gfi:AbossoGoldfieldsLimitedMembergfi:ClassASharesMember2023-01-012023-12-310001172724gfi:AbossoGoldfieldsLimitedMembergfi:ClassASharesMember2022-01-012022-12-310001172724gfi:ClassBSharesMembergfi:AbossoGoldfieldsLimitedMember2023-12-310001172724gfi:ClassBSharesMembergfi:AbossoGoldfieldsLimitedMember2022-12-310001172724gfi:ClassBSharesMembergfi:AbossoGoldfieldsLimitedMember2023-01-012023-12-310001172724gfi:ClassBSharesMembergfi:AbossoGoldfieldsLimitedMember2022-01-012022-12-310001172724gfi:AgnewGoldMiningCompanyProprietaryLimitedMember2023-12-310001172724gfi:AgnewGoldMiningCompanyProprietaryLimitedMember2022-12-310001172724gfi:AgnewGoldMiningCompanyProprietaryLimitedMember2023-01-012023-12-310001172724gfi:AgnewGoldMiningCompanyProprietaryLimitedMember2022-01-012022-12-310001172724gfi:DarlotMiningCompanyProprietaryLimitedMember2023-12-310001172724gfi:DarlotMiningCompanyProprietaryLimitedMember2022-12-310001172724gfi:DarlotMiningCompanyProprietaryLimitedMember2023-01-012023-12-310001172724gfi:DarlotMiningCompanyProprietaryLimitedMember2022-01-012022-12-310001172724gfi:GFIJointVentureHoldingsProprietaryLimitedMember2023-12-310001172724gfi:GFIJointVentureHoldingsProprietaryLimitedMember2022-12-310001172724gfi:GFIJointVentureHoldingsProprietaryLimitedMember2023-01-012023-12-310001172724gfi:GFIJointVentureHoldingsProprietaryLimitedMember2022-01-012022-12-310001172724gfi:GFLMiningServicesLimitedMember2023-12-310001172724gfi:GFLMiningServicesLimitedMember2022-12-310001172724gfi:GFLMiningServicesLimitedMember2023-01-012023-12-310001172724gfi:GFLMiningServicesLimitedMember2022-01-012022-12-310001172724gfi:GoldFieldsGhanaLimitedMember2023-12-310001172724gfi:GoldFieldsGhanaLimitedMember2022-12-310001172724gfi:GoldFieldsGhanaLimitedMember2023-01-012023-12-310001172724gfi:GoldFieldsGhanaLimitedMember2022-01-012022-12-310001172724gfi:GoldFieldsGroupServicesProprietaryLimitedMember2023-12-310001172724gfi:GoldFieldsGroupServicesProprietaryLimitedMember2022-12-310001172724gfi:GoldFieldsGroupServicesProprietaryLimitedMember2023-01-012023-12-310001172724gfi:GoldFieldsGroupServicesProprietaryLimitedMember2022-01-012022-12-310001172724gfi:GoldFieldsHoldingsCompanyBVILimitedMember2023-12-310001172724gfi:GoldFieldsHoldingsCompanyBVILimitedMember2022-12-310001172724gfi:GoldFieldsHoldingsCompanyBVILimitedMember2023-01-012023-12-310001172724gfi:GoldFieldsHoldingsCompanyBVILimitedMember2022-01-012022-12-310001172724gfi:GoldFieldsLaCimaSAMember2023-12-310001172724gfi:GoldFieldsLaCimaSAMember2022-12-310001172724gfi:GoldFieldsLaCimaSAMember2023-01-012023-12-310001172724gfi:GoldFieldsLaCimaSAMember2022-01-012022-12-310001172724gfi:GoldFieldsOperationsLimitedMember2023-12-310001172724gfi:GoldFieldsOperationsLimitedMember2022-12-310001172724gfi:GoldFieldsOperationsLimitedMember2023-01-012023-12-310001172724gfi:GoldFieldsOperationsLimitedMember2022-01-012022-12-310001172724gfi:GoldFieldsOrogenHoldingsBVILimitedMember2023-12-310001172724gfi:GoldFieldsOrogenHoldingsBVILimitedMember2022-12-310001172724gfi:GoldFieldsOrogenHoldingsBVILimitedMember2023-01-012023-12-310001172724gfi:GoldFieldsOrogenHoldingsBVILimitedMember2022-01-012022-12-310001172724gfi:GruyereMiningCompanyProprietaryLimitedMember2023-12-310001172724gfi:GruyereMiningCompanyProprietaryLimitedMember2022-12-310001172724gfi:GruyereMiningCompanyProprietaryLimitedMember2023-01-012023-12-310001172724gfi:GruyereMiningCompanyProprietaryLimitedMember2022-01-012022-12-310001172724gfi:GSMMiningCompanyProprietaryLimitedMember2023-12-310001172724gfi:GSMMiningCompanyProprietaryLimitedMember2022-12-310001172724gfi:GSMMiningCompanyProprietaryLimitedMember2023-01-012023-12-310001172724gfi:GSMMiningCompanyProprietaryLimitedMember2022-01-012022-12-310001172724gfi:MineraGoldFieldsSalaresNorteSpAMember2023-12-310001172724gfi:MineraGoldFieldsSalaresNorteSpAMember2022-12-310001172724gfi:MineraGoldFieldsSalaresNorteSpAMember2023-01-012023-12-310001172724gfi:MineraGoldFieldsSalaresNorteSpAMember2022-01-012022-12-310001172724gfi:NewshelfEightNineNineProprietaryLimitedMembergfi:ClassASharesMember2023-12-310001172724gfi:NewshelfEightNineNineProprietaryLimitedMembergfi:ClassASharesMember2022-12-310001172724gfi:NewshelfEightNineNineProprietaryLimitedMembergfi:ClassASharesMember2023-01-012023-12-310001172724gfi:NewshelfEightNineNineProprietaryLimitedMembergfi:ClassASharesMember2022-01-012022-12-310001172724gfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMember2023-12-310001172724gfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMember2022-12-310001172724gfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMember2023-01-012023-12-310001172724gfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMember2022-01-012022-12-310001172724gfi:StivesGoldMiningCompanyProprietaryLimitedMember2023-12-310001172724gfi:StivesGoldMiningCompanyProprietaryLimitedMember2022-12-310001172724gfi:StivesGoldMiningCompanyProprietaryLimitedMember2023-01-012023-12-310001172724gfi:StivesGoldMiningCompanyProprietaryLimitedMember2022-01-012022-12-310001172724gfi:AbossoGoldfieldsLimitedMember2023-12-310001172724gfi:AbossoGoldfieldsLimitedMember2022-12-310001172724gfi:AbossoGoldfieldsLimitedMember2023-01-012023-12-310001172724gfi:AbossoGoldfieldsLimitedMember2022-01-012022-12-310001172724gfi:GoldFieldsOperationsLimitedMembergfi:ClassASharesMember2023-12-310001172724gfi:ClassBSharesMembergfi:SouthDeepBeeMember2023-12-310001172724gfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMembergfi:NotLaterThanTenYearsMember2023-01-012023-12-310001172724gfi:LaterThanTenYearsAndNotLaterFifeteenYearsMembergfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMember2023-01-012023-12-310001172724gfi:ClassBSharesMembergfi:NewshelfEightNineNineProprietaryLimitedMembergfi:LaterThanFifeteenYearsAndNotLaterTwentyYearsMember2023-01-012023-12-310001172724gfi:SouthDeepBeeMember2023-01-012023-12-310001172724gfi:ClassBSharesMembergfi:SouthDeepBeeMember2023-01-012023-12-310001172724ifrs-full:AssociatesMembergfi:RusoroMiningLimitedMember2023-12-310001172724ifrs-full:AssociatesMembergfi:RusoroMiningLimitedMember2022-12-310001172724ifrs-full:AssociatesMembergfi:RusoroMiningLimitedMember2023-01-012023-12-310001172724ifrs-full:AssociatesMembergfi:RusoroMiningLimitedMember2022-01-012022-12-310001172724ifrs-full:AssociatesMembergfi:LunnonMetalsLimitedMember2023-12-310001172724ifrs-full:AssociatesMembergfi:LunnonMetalsLimitedMember2022-12-310001172724ifrs-full:AssociatesMembergfi:LunnonMetalsLimitedMember2023-01-012023-12-310001172724ifrs-full:AssociatesMembergfi:LunnonMetalsLimitedMember2022-01-012022-12-310001172724ifrs-full:JointVenturesMembergfi:FarSoutheastGoldResourcesIncorporatedMember2023-12-310001172724ifrs-full:JointVenturesMembergfi:FarSoutheastGoldResourcesIncorporatedMember2022-12-310001172724ifrs-full:JointVenturesMembergfi:FarSoutheastGoldResourcesIncorporatedMember2023-01-012023-12-310001172724ifrs-full:JointVenturesMembergfi:FarSoutheastGoldResourcesIncorporatedMember2022-01-012022-12-310001172724ifrs-full:JointVenturesMembergfi:AsankoGoldGhanaLimitedMember2023-12-310001172724ifrs-full:JointVenturesMembergfi:AsankoGoldGhanaLimitedMember2022-12-310001172724ifrs-full:JointVenturesMembergfi:AsankoGoldGhanaLimitedMember2023-01-012023-12-310001172724ifrs-full:JointVenturesMembergfi:AsankoGoldGhanaLimitedMember2022-01-012022-12-310001172724gfi:AdansiGoldCompanyLimitedMemberifrs-full:JointVenturesMember2023-12-310001172724gfi:AdansiGoldCompanyLimitedMemberifrs-full:JointVenturesMember2022-12-310001172724gfi:AdansiGoldCompanyLimitedMemberifrs-full:JointVenturesMember2023-01-012023-12-310001172724gfi:AdansiGoldCompanyLimitedMemberifrs-full:JointVenturesMember2022-01-012022-12-310001172724ifrs-full:JointVenturesMembergfi:ShikaGroupFinanceLimitedMember2023-12-310001172724ifrs-full:JointVenturesMembergfi:ShikaGroupFinanceLimitedMember2022-12-310001172724ifrs-full:JointVenturesMembergfi:ShikaGroupFinanceLimitedMember2023-01-012023-12-310001172724ifrs-full:JointVenturesMembergfi:ShikaGroupFinanceLimitedMember2022-01-012022-12-310001172724ifrs-full:JointVenturesMembergfi:WindfallMiningGroupPartnershipMember2023-12-310001172724ifrs-full:JointVenturesMembergfi:WindfallMiningGroupPartnershipMember2022-12-310001172724ifrs-full:JointVenturesMembergfi:WindfallMiningGroupPartnershipMember2023-01-012023-12-310001172724ifrs-full:JointVenturesMembergfi:WindfallMiningGroupPartnershipMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:GalianoGoldIncformerlyAsankoGoldIncMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:GalianoGoldIncformerlyAsankoGoldIncMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:GalianoGoldIncformerlyAsankoGoldIncMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:GalianoGoldIncformerlyAsankoGoldIncMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TorqResourcesIncMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TorqResourcesIncMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TorqResourcesIncMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TorqResourcesIncMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TesoroGoldLimitedMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TesoroGoldLimitedMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TesoroGoldLimitedMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:TesoroGoldLimitedMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:HamelinGoldLimitedMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:HamelinGoldLimitedMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:HamelinGoldLimitedMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:HamelinGoldLimitedMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:RareXLimitedMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:RareXLimitedMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:RareXLimitedMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:RareXLimitedMember2022-01-012022-12-310001172724gfi:VizslaCopperCorporationMemberifrs-full:EquityInvestmentsMember2023-12-310001172724gfi:VizslaCopperCorporationMemberifrs-full:EquityInvestmentsMember2022-12-310001172724gfi:VizslaCopperCorporationMemberifrs-full:EquityInvestmentsMember2023-01-012023-12-310001172724gfi:VizslaCopperCorporationMemberifrs-full:EquityInvestmentsMember2022-01-012022-12-310001172724gfi:LefroyExplorationLimitedMemberifrs-full:EquityInvestmentsMember2023-12-310001172724gfi:LefroyExplorationLimitedMemberifrs-full:EquityInvestmentsMember2022-12-310001172724gfi:LefroyExplorationLimitedMemberifrs-full:EquityInvestmentsMember2023-01-012023-12-310001172724gfi:LefroyExplorationLimitedMemberifrs-full:EquityInvestmentsMember2022-01-012022-12-310001172724gfi:MagmaticResourcesLimitedMemberifrs-full:EquityInvestmentsMember2023-12-310001172724gfi:MagmaticResourcesLimitedMemberifrs-full:EquityInvestmentsMember2022-12-310001172724gfi:MagmaticResourcesLimitedMemberifrs-full:EquityInvestmentsMember2023-01-012023-12-310001172724gfi:MagmaticResourcesLimitedMemberifrs-full:EquityInvestmentsMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:MineralResourcesLimitedMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:MineralResourcesLimitedMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:MineralResourcesLimitedMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:MineralResourcesLimitedMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:OrsuMetalsCorporationMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:OrsuMetalsCorporationMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:OrsuMetalsCorporationMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:OrsuMetalsCorporationMember2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:ChakanaCopperCorp3Member2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:ChakanaCopperCorp3Member2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:ChakanaCopperCorp3Member2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:ChakanaCopperCorp3Member2022-01-012022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:AmarcResourcesLimitedMember2023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:AmarcResourcesLimitedMember2022-12-310001172724ifrs-full:EquityInvestmentsMembergfi:AmarcResourcesLimitedMember2023-01-012023-12-310001172724ifrs-full:EquityInvestmentsMembergfi:AmarcResourcesLimitedMember2022-01-012022-12-31