UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission file number

(Exact name of Registrant as specified in its charter) |

N/A |

(Translation of Registrant’s name into English) |

Federative Republic of |

(Jurisdiction of incorporation or organization) |

(Address of principal executive offices) (Zip code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange in which registered |

|

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

The total number of issued shares of each class of stock of GERDAU S.A. as of December 31, 2023 was:

1,156,540,608 Preferred Shares, no par value per share |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Accelerated filer ◻ |

| Non-accelerated filer ◻ |

| Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

|

|

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes

TABLE OF CONTENTS

Page | ||

1 | ||

3 | ||

3 | ||

3 | ||

3 | ||

18 | ||

52 | ||

52 | ||

73 | ||

88 | ||

92 | ||

95 | ||

98 | ||

QUANTITATIVE AND QUALITATIVE DISCLOSURES REGARDING MARKET RISK | 114 | |

116 | ||

117 | ||

117 | ||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 117 | |

117 | ||

118 | ||

118 | ||

118 | ||

119 | ||

119 | ||

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 120 | |

120 | ||

120 | ||

121 | ||

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTION | 122 | |

122 | ||

122 | ||

124 | ||

124 | ||

125 | ||

126 | ||

i

INTRODUCTION

Unless otherwise indicated, all references herein to:

| (i) | “CPI” means consumer price index, “CDI” means Interbanking Deposit Rates (Certificados de Depósito Interfinanceiro), “IGP-M” means Consumer Prices Index (Índice Geral de Preços do Mercado), measured by FGV (Fundação Getulio Vargas), “LIBOR” means London Interbank Offered Rate, “GDP” means Gross Domestic Product; |

| (ii) | “Gerdau Açominas” is a reference to Gerdau Açominas S.A. |

| (iii) | “Installed capacity” means the annual projected capacity for a particular facility (excluding the portion that is not attributable to our participation in a facility owned by a joint venture), calculated based upon operations for 24 hours each day of a year and deducting scheduled downtime for regular maintenance; |

| (iv) | “Preferred Shares” and “Ordinary Shares” refer to the Company’s authorized and outstanding preferred stock and ordinary stock, designated as ações preferenciais and ações ordinárias, respectively, all without par value. All references herein to the “real”, “reais” or “R$” are to the Brazilian real, the official currency of Brazil. All references to (i) “U.S. dollars”, “dollars”, “U.S.$” or “$” are to the official currency of the United States, (ii) “Euro” or “€” are to the official currency of members of the European Union, (iii) “billions” are to thousands of millions, (iv) “km” are to kilometers, and (vi) “tonnes” are to metric tonnes; |

| (v) | “proven” or “probable mineral reserves” have the meanings defined by SEC in Regulation S-K, ⸹229.1300. |

| (vi) | “Shipments” means the volumes shipped and “Consolidated shipments” means the combined volumes shipped from all our operations in Brazil, South America, North America and Asia, excluding our joint ventures and associate companies; |

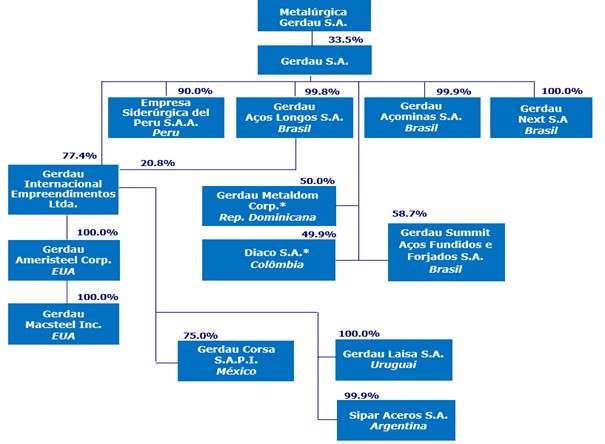

| (vii) | the “Company”, “Gerdau”, “we” or “us” are references to Gerdau S.A., a corporation organized under the laws of the Federative Republic of Brazil (“Brazil”) and its consolidated subsidiaries; |

| (viii) | “Tonne” means a metric tonne, which is equal to 1,000 kilograms or 2,204.62 pounds; |

| (ix) | “Worldsteel” means World Steel Association, “IABr” means Brazilian Steel Institute (Instituto Aço Brasil) and “AISI” means American Iron and Steel Institute; |

The Company has prepared the Consolidated Financial Statements included herein in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS Accounting Standards”). The following investments are accounted following the equity method: Bradley Steel Processor and MRM Guide Rail, all in North America, of which Gerdau Ameristeel holds 50% of the total capital, the investment in the holding company Gerdau Metaldom Corp., in which the Company held a 50% stake, in the Dominican Republic, the investment in Gerdau Corsa S.A.P.I. de C.V., in Mexico, in which the Company holds a 75% stake, the investment in Dona Francisca Energética S.A, in Brazil, in which the Company holds a 51.82% stake, the investment in Newave Energia S.A., in Brazil, in which the Company holds a 33.33% stake, the investment in Diaco S.A., in Colombia, in which the Company held a 49.85% stake, the investment in Gerdau Summit Aços Fundidos e Forjados S.A., in Brazil, in which the Company holds a 58.73% stake, the investments in Addiante S.A. and Ubiratã Tecnologia S.A., in Brazil, in which the Company holds a 50% stake, the investment in Brasil ao Cubo S.A., in Brazil, in which the Company holds a 44.66% stake and the investment in Juntos Somos Mais Fidelização S.A., in Brazil, in which the Company holds a 27.16% stake.

On January 17, 2024, the Company signed an agreement for the sale of all its equity interests of 49.85% in the joint venture Diaco S.A. (and subsidiaries) and 50.00% in the joint venture Gerdau Metaldom Corp (and subsidiaries). On February 1, 2024, after compliance with the corresponding conditions precedent, the sale of the 50.00% equity interest in the joint venture Gerdau Metaldom Corp. (and subsidiaries) was concluded. On March 14, 2024, after compliance with the corresponding conditions precedent, the sale of the 49.85% in the joint venture Diaco S.A. (and subsidiaries) was concluded.

Unless otherwise indicated, all information in this Annual Report is stated as of December 31, 2023.

1

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of the Private Securities Litigation Act of 1995. These statements relate to our future prospects, developments and business strategies.

Statements that are predictive in nature, that depend upon or refer to future events or conditions or that include words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates” and similar expressions are forward-looking statements. Although we believe that these forward-looking statements are based upon reasonable assumptions, these statements are subject to several risks and uncertainties and are made considering information currently available to us.

It is possible that our future performance may differ materially from our current assessments due to several factors, including the following:

| ● | general economic, political and business conditions in our markets, both in Brazil and abroad, including demand and prices for steel products; |

| ● | interest rate fluctuations, inflation and exchange rate movements of the real in relation to the U.S. dollar and other currencies in which we sell a significant portion of our products or in which our assets and liabilities are denominated; |

| ● | our ability to obtain financing on satisfactory terms; |

| ● | prices and availability of raw materials; |

| ● | changes in international trade; |

| ● | changes in laws and regulations; |

| ● | electric energy shortages and government responses to them; |

| ● | the performance of the Brazilian and the global steel industries and markets; |

| ● | global, national and regional competition in the steel market; |

| ● | protectionist measures imposed by steel-importing countries; and |

| ● | other factors identified or discussed under “Risk Factors.” |

Our forward-looking statements are not guarantees of future performance, and actual results or developments may differ materially from the expectations expressed in the forward-looking statements. As for the forward-looking statements that relate to future financial results and other projections, actual results will be different due to the inherent uncertainty of estimates, forecasts and projections. Because of these uncertainties, potential investors should not rely on these forward-looking statements.

We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future events or otherwise.

2

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable, as the Company is filing this Form 20-F as an annual report.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable, as the Company is filing this Form 20-F as an annual report.

ITEM 3. KEY INFORMATION

A. [RESERVED]

B. CAPITALIZATION AND INDEBTEDNESS

Not required, as the Company is filing this Form 20-F as an annual report.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not required, as the Company is filing this Form 20-F as an annual report.

D. RISK FACTORS

We are subject to various risks and uncertainties resulting from changing competitive, economic, political and social conditions that could harm our business, results of operations or financial condition. The risks described below could adversely affect our business, consolidated financial position, results of operations or cash flows. These risks are not the only ones we face. Other risks that we do not presently know about or that we presently believe are not material could also adversely affect us.

Risks Relating to our Business and the Steel Industry

Demand for steel is cyclical and a reduction in prevailing world prices for steel could adversely affect the Company’s results of operations.

The steel industry is highly cyclical. Consequently, the Company is exposed to substantial swings in the demand for steel products, which in turn causes volatility in the prices of most of its products and eventually could cause write-downs of its inventories. In addition, the demand for steel products, and hence the financial condition and results of operations of companies in the steel industry, including the Company itself, are generally affected by macroeconomic changes in the world economy and in the domestic economies of steel-producing countries, including general trends in the steel, construction and automotive industries. A material decrease in demand for steel or exports by countries not able to consume their production could have a significant adverse effect on the Company’s financial condition and results of operations.

Global crises and subsequent economic slowdowns may adversely affect global steel demand. As a result, the Company’s financial condition and results of operations may be adversely affected.

Historically, the steel industry has been highly cyclical and deeply impacted by economic conditions in general, such as world production capacity and fluctuations in steel imports/exports and the respective import duties. After a steady period of growth between 2004 and 2008, the marked drop in demand resulting from the global economic crisis of 2008-2009 once again demonstrated the vulnerability of the steel market to volatility of international steel prices and raw materials. That crisis was caused by the dramatic increase of high real estate risk financing defaults and foreclosures in the United States, with serious consequences for bank and financial markets throughout the world. Developed markets, such as North America and Europe, experienced a strong recession due to the collapse of real estate financings and the shortage of global credit. As a result, the demand for steel products suffered a decline in 2009, but since 2010 has been experiencing a gradual recovery, principally in the developing economies.

3

The global economy can negatively impact the consuming markets, affecting the business environment with respect to the following:

| ● | Decrease in international steel prices; |

| ● | Slump in international steel trading volumes; |

| ● | Crisis in the automotive industry, infrastructure sectors, construction (residential and non-residential); and |

| ● | Lack of liquidity in the international market. |

If the Company is not able to remain competitive in these shifting markets, our profitability, margins and income may be negatively affected. A decline in this trend could result in a decrease in the Company’s shipments and revenues. As a result, the Company’s financial condition and results of operations may be adversely affected.

Our results and financial condition are affected by global and local market conditions that we do not control and cannot predict

We are subject to the risks arising from adverse changes in domestic and global economic and political conditions. Our industry is cyclical by nature and fluctuates with economic cycles, including the current global economic instability. Recessions and significant disruptions in the global financial markets may affect the Company. Our operations experienced significant disruptions in 2008 and the United States, Europe and other economies went into recession. New challenges include the effects of the United Kingdom’s withdrawal from the European Union (BREXIT) and increasing political uncertainty and instability in a number of countries.

In 2020, the Pandemic resulted in the temporary closing of several industries, including the steel industry. Measures were taken to contain the virus spread among employees, in accordance with regulations promulgated by local authorities. The effects extended to operations and impacted the Company’s results, mainly in April, May and June of that year.

The risk of trade protection measures in favor of local producers of competing products and the disruption in existing trade agreements or increased trade friction between countries (e.g., the U.S. and China) could have a negative effect on our business and results of operations by restricting the free flow of goods and services across borders and exacerbating global economic conditions. Global economic weakness may prompt banks to limit or deny lending to us or to our customers, which could have a material adverse effect on our liquidity, on our operations and on our ability to carry out our announced capital investment programs and may prompt our customers to slow down or reduce the purchase of our products. In addition, COVID-19 has also had significant economic and social impacts.

We may experience longer sales cycles, difficulty in collecting sales proceeds and lower prices for our products. We cannot provide any assurance that any of these events will not have a material adverse effect on market conditions, the prices of our securities, our ability to obtain financing and our results of operations and financial condition.

The continuing impact of the Russian invasion of Ukraine and any widening of the conflict, the Israel-Hamas conflict in Gaza or any other global conflicts could have a materially adverse impact on our results of operations and financial condition.

The continuing Russian invasion of Ukraine and any widening of the conflict could have a material adverse effect on the overall macroeconomic environment, which might include demand for steel and iron ore and prices, as well as increasing energy costs.

Both the conflict itself and the sanctions imposed (and further sanctions that may be imposed) could have further destabilizing effects on financial markets and certain commodity markets. Any substantial escalation would have a material adverse effect on macroeconomic conditions. In addition, sanctions may remain in place beyond the duration of any military conflict and have a long-lasting impact regionally and globally and could adversely impact the Company’s results of operations and financial condition.

Similarly, the Israel-Hamas conflict in Gaza and any other global conflicts could have a similar material adverse effect on the overall macroeconomic environment, impacting financial markets and certain commodity markets, with a materially adverse impact on our results of operations and financial condition.

4

Gerdau faces significant competition in relation to their steel products, including with regard to prices of other domestic and foreign producers, which may adversely affect its profitability and market share.

The global steel industry is highly competitive with respect to price, quality of products and customer service, as well as in relation to technological advances that allow the reduction of production costs. Brazilian exports of steel products are influenced by several factors, including protectionist policies of other countries, foreign exchange policy and the growth rate of the world economy. Moreover, continuous advances in material sciences and the resulting technologies facilitate the improvement of products such as plastic, aluminum, ceramics and glass, permitting them to serve as substitutes for steel.

Due to the high initial investment costs, the operation of a steel plant on a continuous basis may encourage mill operators to maintain high production levels, even in periods of low demand, which results would increase the pressure on industry profit margins. That said, a competitive pressure that forces the fall in steel prices can also affect the profitability of Gerdau.

The steel industry has historically suffered from excess of production capacity, which has worsened due to a substantial increase in production capacity in emerging countries, particularly China and India and other emerging markets, in which China is currently the largest global steel producer.

Favorable conditions in China and steel-exporting countries can significantly impact steel prices in other markets. China, as the world’s largest steel producer and consumer, influences global steel demand and supply dynamics. Factors such as infrastructure development, urbanization, and government policies can bolster steel demand within China, affecting global prices. Additionally, steel-exporting countries, benefiting from lower production costs, efficient supply chains, and economies of scale, can exert competitive pressures on international steel prices, particularly when coupled with government subsidies or trade agreements. These combined factors create a complex interplay of supply and demand forces that can swiftly impact steel prices worldwide.

In 2023, steel companies in Brazil faced strong competition from imported products, mainly due to the global excess in steel production, culminating in a reduction in demand for local steel products, increasing the competitive imbalance, mainly driven by predatory steel imports from China. According to the Brazil Steel Institute, steel imports in Brazil reached 5 million tonnes in 2023, the highest level since 2010, up 50% over 2022, contributing to a decline in the main markets where Gerdau operates and impacting the Company’s results. Although Gerdau is a modern and highly efficient producer, the Company cannot compete with heavily subsidized imports, which may adversely affect the competitiveness of the industry, its financial condition, and results of operations in the future.

An increase in China’s steelmaking capacity or a slowdown in China’s steel consumption could have a material adverse effect on domestic and global steel pricing and could result in increased steel imports into the markets in which the Company operates.

One significant factor in the global steel market has been China’s high steel production capacity. However, very substantial consumers of steel have lost relevance in the Chinese economy, causing a deep and structural imbalance between steel supply and demand in the Chinese domestic market.

China is currently the world’s largest steel producer and has favorable conditions such as excess steel capacity, devalued currency and a job maintenance policy. In addition, the Chinese government subsidizing surplus steel production, exporting these volumes at prices below production costs in several countries in the transoceanic region that have not yet taken trade defense measures against unfair trade practices, such as Brazil, and consequently pushing down international steel prices. Trade defense measures against predatory practices are legal and supported by the World Trade Organization. Some countries such as the United States, Mexico, Turkey and the other 27 countries of the European Union have adopted relevant measures to combat the entry of subsidized Chinese steel, strengthening their economies, their industries, and their jobs.

In 2023, steel imports in Brazil increased by 50% compared to 2022 and reached a record volume in the annual historical series, according to the Brazil Steel Institute. Over 2023, Gerdau faced a shocking increase in the penetration of imported steel in Brazil, particularly from China. For these reasons, players in the sector have been defending the need for a review of import tariffs in Brazil to ensure fairer and more competitive conditions for the national steel market. If the Brazilian government does not implement measures against subsidized steel imports and the high level of imports continues without measures that guarantee fair competition with the local market, Gerdau’s financial condition and results of operations may be negatively affected in the future. In addition to direct steel imports, the Brazilian industry also faces competition from imported finished products, which negatively affects the entire steel supply and production chain.

5

Higher steel scrap prices or a reduction in supply could adversely affect production costs and operating margins.

The main metal input for the Company’s mini mills is steel scrap. Although international steel scrap prices are determined essentially by scrap prices in the U.S. local market, because the United States is the main scrap exporter, scrap prices in the Brazilian market are set by domestic suppliers and demand. The price of steel scrap in Brazil varies from region to region and reflects demand and transportation costs. Should scrap prices increase significantly without a corresponding increase in finished steel selling prices, the Company’s profits and margins could be adversely affected. An increase in steel scrap prices or a shortage in the supply of scrap to its units would affect production costs and potentially reduce operating margins and revenues. As a result, the Company’s financial condition and results of operations may be adversely affected.

Increases in iron ore and coal prices, or reductions in market supply, and price increases in other inputs, could adversely affect the Company’s operations.

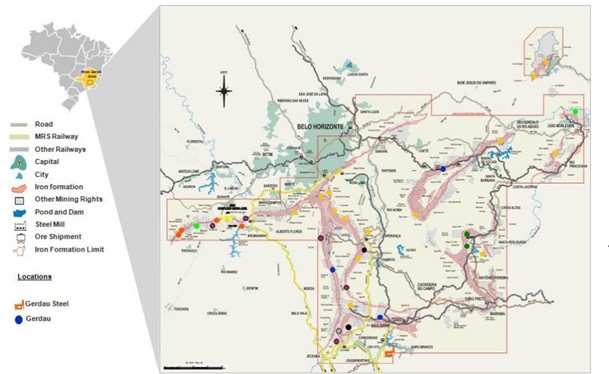

When the prices of raw materials, particularly iron ore and coking coal, increase, and the Company needs to produce steel in its integrated facilities, the production costs in its integrated facilities also increase. The Company uses iron ore to produce hot pig iron at its Ouro Branco, Barão de Cocais, Sete Lagoas and Divinópolis mills located in the state of Minas Gerais.

The Ouro Branco mill is the Company’s largest mill in Brazil, and its main metal input to produce steel is iron ore. This unit represented 61.7% of the total crude steel output (in volume) of the Brazil Business Segment in 2023. A shortage of iron ore in the domestic market may adversely affect the steel producing capacity of the Brazilian units, and an increase in iron ore prices could reduce profit margins.

The Company has iron ore mines in the Brazilian state of Minas Gerais. To mitigate its exposure to the volatility in iron ore prices, the Company invested in expanding the production capacity of these mines.

All the Company’s coking coal requirements for its Brazilian units are imported due to the low quality of Brazilian coal. Coking coal is the main energy input at the Ouro Branco mill and is used at the coking facility. Although this mill is not dependent on coke supplies, a contraction in the supply of coking coal could adversely affect the integrated operations at this site. The coking coal used in this mill is imported from the United States, Australia, Peru and Colombia. We have entered long-term contracts with negotiable prices periodically to minimize the risks of shortages. A shortage of coking coal in the international market would adversely affect the steel producing capacity of the Ouro Branco mill. In addition, an increase in prices could reduce profit margins. Another related risk is the currency depreciation to which the Ouro Branco Mill is exposed, since all coking coal consumed by the operation is imported.

Volatility in the supply and prices of these and other raw materials, energy and transportation, could adversely affect the Company’s results of operations. We are vulnerable to inflationary cost pressures, especially in relation to the prices of electricity, natural gas and CO2. There were inflationary cost pressures as a consequence of the Russian invasion of Ukraine in 2022, resulting in disruption of markets and supply chains and sanctions impacts.

Such events could adversely affect the Company’s financial condition and results of operations.

Risks Relating to our Operations

The Company’s projects are subject to risks that may result in increased costs or delay or prevent their successful implementation.

The Company invested to further increase productivity of its operations. These projects are subject to several risks that may adversely affect the Company’s growth prospects and profitability, including the following:

| ● | the Company may encounter delays, availability problems or higher than expected costs in obtaining the necessary equipment, services and materials to build and operate a project; |

| ● | the Company’s efforts to develop projects according to schedule may be hampered by a lack of infrastructure, including availability of overburden and waste disposal areas as well as reliable power and water supplies; |

6

| ● | the Company may fail to obtain, lose, or experience delays or higher than expected costs in obtaining or renewing the required permits, authorizations, licenses, concessions and/or regulatory approvals to build or continue a project; and |

| ● | changes in market conditions, laws or regulations may make a project less profitable than expected or economically or otherwise unfeasible. |

Any one or a combination of the factors described above may materially and adversely affect the Company’s financial condition and results of operations.

Unexpected equipment failures may lead to production curtailments or shutdowns.

Unexpected interruptions in the production capabilities at Gerdau’s principal sites and installations would increase production costs, reducing shipments and earnings for the affected period. These interruptions result from: (i) unpredictable/periodic equipment failures, which are essential to the development of the production processes of Gerdau, such as steelmaking equipment, such as its electric arc furnaces, continuous casters, gas-fired reheat furnaces, rolling mills and electrical equipment, including high-output transformers; and/or (ii) unanticipated events such as fires, explosions or violent weather conditions. As a result, Gerdau has experienced and may in the future experience material plant shutdowns or periods of reduced production. Unexpected interruptions in production capabilities would adversely affect Gerdau’s productivity and results of operations. Moreover, any interruption in production capability may require Gerdau to make additions to fixed assets to remedy the problem, which would reduce the amount of cash available for operations. Gerdau’s insurance may not cover the losses. In addition, long-term business disruption could harm the Company’s reputation and result in a loss of customers, which could adversely affect the business, results of operations, cash flows and financial condition.

Failure to obtain the necessary permits and licenses could adversely affect our operations.

We depend on the issuance of permits and licenses from governmental agencies to undertake some of our activities that are considered polluting or potentially polluting. For obtaining said licenses, certain investments in conservation are required to offset any such impact. The operational licenses require, among other things, that we periodically report our compliance with emissions standards set by environmental agencies. Failure to obtain, renew or comply with our operating licenses may cause delays in our deployment of new activities, increased costs, monetary fines or even suspension of the affected activity, which may materially adversely affect us.

Climate change may negatively affect our business, financial condition, results of operations and cash flows.

A significant number of scientists, environmentalists, international organizations, regulators and other commentators sustain that global climate change has contributed, and will continue to contribute, to the increasing unpredictability, frequency and severity of natural disasters (including, but not limited to, hurricanes, droughts, tornadoes, freezes, other storms and fires) in certain parts of the world. As a result, several legal and regulatory measures as well as social initiatives have been introduced in numerous countries in an effort to reduce carbon dioxide and other greenhouse gas (GHG) emissions and combat global climate change. Such reductions in GHG emissions could result in increased energy, transportation and raw material costs and may require us to make additional investments in facilities and equipment. Although we cannot predict the impact of changing global climate conditions without certain assumptions, or of legal, regulatory and social responses to concerns about global climate change, any such occurrences may negatively affect our business, financial condition, results of operations and cash flows.

Laws and regulations seeking to reduce GHG emissions can be enacted in the future, which could have a significant adverse impact on the operating results, cash flows, and the financial condition of the Company.

One of the possible effects of the increasing requirements related to the reduction of GHG emissions is the increase in costs, mainly due to the demand to reduce the consumption of fossil fuels and the implementation of new technologies in the production chain.

The Company believes that the operations in the countries where it operates may be affected in the future by federal, state and municipal initiatives related to climate change, intended to deal with the issue of GHG.

7

In Brazil, there is a legislative proposal in the National Congress to establish a carbon market and it is pending the next steps in the Federal Senate. At state levels, there are demands for accounting for the inventory of greenhouse gases and reporting to regulatory bodies as well as discussions about decarbonization strategies.

In the U.S., future federal and/or state carbon regulation potentially presents impact to our operations. To date, the U.S. Congress has not legislated carbon constraints. In the absence of comprehensive federal carbon legislation, numerous state, regional and federal regulatory initiatives are under development or are becoming effective, thereby creating a disjointed approach to GHG control and potential carbon pricing impacts.

The Inflation Reduction Act, passed by the U.S. Congress in August 2022, contains significant energy security and climate related measures, such as investments in renewable energy production and tax credits aimed at reducing carbon emissions. Agencies are finalizing guidance on labor standards and domestic content requirements. The expansion and extension of solar tax credits is expected to have a meaningful impact on the solar energy sector, a significant and growing market for our North America Segment.

Mexico has advanced in consolidating its carbon market, through an Emissions Trading System (ETS) and it could affect our operations in the future.

On March 6, 2024, the SEC approved new rules that will require significant climate-related disclosures by public companies, including evaluation and disclosure of material climate-related risks and opportunities, GHG emissions inventory, climate-related targets and goals, and financial impacts of physical and transition risks (the “SEC Climate Rules”). As a result of the SEC Climate Rules, our legal, accounting, and other compliance expenses may increase significantly, and compliance efforts may divert management time and attention. We may also be exposed to legal or regulatory action or claims as a result of these new regulations. Although the Company is in the process of evaluating the new rules, some of these risks could have a material adverse effect on our business, financial condition, results of operations and the prices of our securities.

The Company’s operations are energy-intensive, and energy shortages or higher energy prices could have an adverse effect.

Crude steel production is an energy-intensive process, especially in melt shops with electric arc furnaces. Electricity represents an important production component at these units, as also does natural gas, although to a lesser extent. Electricity cannot be replaced at Gerdau’s mills and power rationing or shortages could adversely affect production at those units. As a result, the Company’s financial condition and results of operations may be adversely affected.

Layoffs in the Company’s labor force could generate costs or negatively affect the Company’s operations.

A substantial number of our employees are represented by labor unions and are covered by collective bargaining or other labor agreements, which are subject to periodic negotiation. Strikes or work stoppages have occurred in the past and could reoccur in connection with negotiations of new labor agreements or during other periods for other reasons, including the risk of layoffs during a down cycle that could generate severance costs. Moreover, the Company could be adversely affected by labor disruptions involving unrelated parties that may provide goods or services to the Company. Strikes and other labor disruptions at any of the Company operations could adversely affect the operation of facilities and the timing of completion and the cost of capital of our projects.

In the course of 2023, certain Gerdau units in Brazil experienced workforce contract suspensions lasting up to five months. This occurrence was attributable to the substantial increase in predatory steel imports to the Brazilian market, resulting in a negative impact on production levels. By the end of 2023, aligning the workforce size with the prevailing production volume, approximately 900 employees were laid off from the Company.

If the Brazilian government does not implement measures against subsidized steel and the high level of imports persist without measures that guarantee fair competition with the local market, Gerdau may consider restructuring its operations in Brasil. This could involve shutdown of some production capacities and, consequently, a recalibration of the workforce size.

8

We could be harmed by a failure or interruption of our information technology systems or automated machinery.

We rely on our information technology systems and automated machinery to effectively manage our production processes and operate our business. Advanced technology systems and machinery are nonetheless subject to defects, interruptions and breakdowns. Any failure of our information technology systems and automated machinery to perform as we anticipate could disrupt our business and result in production errors, processing inefficiencies and the loss of sales and customers, which in turn could result in decreased revenue, increased overhead costs and excess or out-of-stock inventory levels resulting in a material adverse effect on our business results. Although we have procedures in place to prevent and minimize the impact of a potential failure, including a data back-up system for our management systems, 24/7 monitoring of our servers, and a cybersecurity program that maintains a Corporate Information Security Policy and a Data Privacy Policy in place, there is no assurance that these will work properly or that there will not be an impact on our results of operations or financial condition.

In addition, our information technology systems and automated machinery may be vulnerable to damage or interruption from circumstances beyond our control, including fire, natural disasters, systems failures, viruses, cyber-attacks and other security breaches, including breaches of our production processing systems that could result in damage to our automated machinery, production interruptions or access to our confidential financial, operational or customer data. Any such damage or interruption could have a material adverse effect on our business results, including as a result of our facing significant fines, customer notice obligations or costly litigation, harming our reputation with our customers or requiring us to expend significant time and expense developing, repairing or upgrading our information technology systems and automated machinery.

Further, while we have some backup data-processing systems that could be used in the event of a failure of our primary systems, we do not yet have a disaster recovery plan or a backup data center that covers all of our units. While we endeavor to prepare for failures of our network by providing backup systems and procedures, we cannot guarantee that our current backup systems and procedures will operate satisfactorily in the event of a regional emergency. Any substantial failure of our backup systems to respond effectively or on a timely basis could have a material adverse effect on our business and results of operations.

We are subject to information technology risks related to breaches of security pertaining to sensitive company, customer, employee and vendor information as well as breaches in the technology used to manage operations and other business processes.

Cybersecurity is a significant concern due to the importance of information technology to the successful conduct of our business operations.We have an executive dedicated to leading the Information Security and Data Protection effort as well as an internal team with qualified specialists and analysts to conduct and evaluate the adequacy of the security and data protection controls. Additionally, we also have an incident response service provider to support our team to prevent and respond to cyber incidents.

We rely upon secure information technology systems for data capture, processing, storage and reporting. Despite careful security and controls design, implementation, updating and independent third-party verification, that also includes specific policies, procedures, and specialized software tools for cybersecurity and data protection, our information technology systems, and those of our third-party providers, could become subject to employee error or malfeasance, natural disasters or be susceptible to cyberattacks. Network, system, application, and data breaches could result in operational disruptions or information misappropriation. Access to internal applications required to plan our operations, source materials, manufacture and goods and account for orders could be denied or misused. Theft of intellectual property or trade secrets, and inappropriate disclosure of confidential company, employee, customer or vendor information, could stem from such incidents. Any of these operational disruptions and/or misappropriation of information could result in lost sales, business delays, negative publicity and could have a material effect on our business. We also could be required to spend significant financial and other resources to remedy the damage caused by a security breach, including to repair or replace networks and information technology systems, liability for stolen information, increased cybersecurity protection costs, litigation expense and increased insurance premiums.

9

Outbreaks of disease and health epidemics could have a negative impact on our business revenues and results of operations.

In late December 2019 a notice of pneumonia of unknown cause originating from Wuhan, Hubei province of China was reported to the World Health Organization. A new corona virus called COVID-19 virus was identified, with cases soon confirmed in multiple provinces in China, as well as in several other countries. The Chinese government placed Wuhan and multiple other cities in Hubei province under quarantine, with approximately 60 million people affected. Since that time the virus has been identified in virtually every country, and travel to and from China, most Europe, India, the United States and other countries, including Brazil, has been suspended or restricted by certain air carriers and foreign governments. On March 2, 2020, the World Health Organization declared the coronavirus outbreak a “pandemic”, which is disease that is widespread around the world with an impact on society. The term has been applied to only a few diseases in history, including the deadly flu of 1918, the H1N1 flu in 2009 and HIV/AIDS. The ongoing COVID-19 pandemic has resulted in extended shutdowns of certain businesses and other activities in many countries, including the United States, Europe and Brazil.

The COVID-19 pandemic impacted the Company production and delivery of steel, resulting in interruption of production in some steel mills as of the second half of March, 2020. The Company followed all COVID-19 pandemic prevention guidelines issued by the competent health agencies in the countries in which it operates. For this reason, the Company has adopted a series of measures to mitigate the risk of transmission in the workplace, such as using home office, creating crisis committees, canceling national and international trips and participation in external events.

The Company monitors the outbreaks of disease and health epidemics scenario and the impacts that this situation brings to the routines of employees, contractors, suppliers, customers and other business partners may be prevented from conducting certain business activities for an indefinite period of time, including due to shutdowns that may be requested or mandated by governmental authorities or otherwise elected by companies as a preventive measure. In addition, mandated government authority measures or other measures elected by companies as preventative measures may lead to our customers being unable to complete purchases or other activities.

Demand for our steel products is directly linked to overall economic activity within those international markets in which we sell our products. A decline in the level of activity in either the domestic or the international markets within which we operate as a consequence of future outbreaks of disease and health epidemics scenario and related measures to contain them could adversely affect and impact both the demand and the price of our products and have a material adverse effect on us. Furthermore, the nature of our business is complex and, to keep operating, most of our work cannot be performed remotely. Our focus is on protecting the health of our employees, therefore we encourage them to take care of their health, since operational continuity is key to people’s jobs, to local communities and to the economies of the countries and regions where we operate.

The deterioration of Brazilian and global economic conditions could, among other things:

| ● | further negatively impact global demand for steel, or further lower market prices for our products, which could result in a continued reduction of our sales, operating income and cash flows; |

| ● | make it more difficult or costly for us to obtain financing for our operations or investments or to refinance our debt in the future; |

| ● | impair the financial condition of some of our customers, suppliers or counterparties, thereby increasing customer bad debts or non-performance by suppliers or counterparties; and |

| ● | decrease the value of certain of our investments. |

10

Risks Relating to our Mining Operations

Estimates of Gerdau’s mineral resources are based on interpretations and assumptions, involving a level of uncertainty, and may differ substantially from the quantities that can be extracted.

Gerdau’s mineral resources refer to estimated quantities of iron ore and minerals. There are several uncertainties that are inherent to such estimates of resources, including many factors that are beyond our control, such as geological and technological factors.

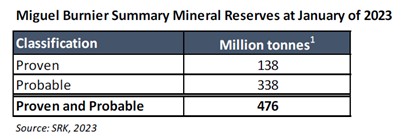

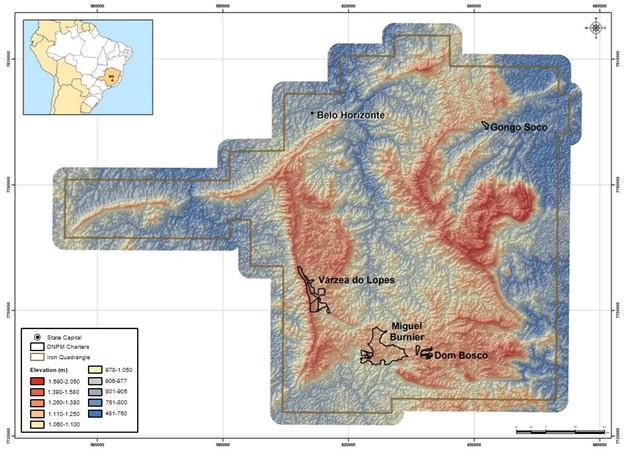

However, Gerdau observed a relevant reduction in the risk related to its mining operations because of the certification of its main iron ore reserve in Minas Gerais state. In 2023, Gerdau received the certification report for the iron ore reserves at the mine located in Miguel Burnier District, municipality of Ouro Preto (MG - Brazil). The report was prepared by the independent certifier SRK Consulting, and according to the report, the Company had certified reserves of 476 million dry metric tons of iron ore. These mining operations are an integral part of Brazil Business Segment, with the focus on supplying iron ore for it. All estimates of Gerdau’s mineral resources and reserves are based on interpretations and assumptions that involve a level of uncertainty. If the amount of mineral resources that actually can be extracted differs materially from our estimates, our business, results of operations and financial condition could be materially adversely impacted.

¹Dry metric tons

The Company has one mining dam for the disposal of tailings, and any accident or defect that affects the structural integrity could affect its image, operating results, cash flows and financial condition.

Gerdau has one mining dam, downstream, for the disposal of tailings in the state of Minas Gerais, the Alemães Dam, which has been in operation since 2011 and is regularly monitored. In 2023, this structure had its construction methodology changed to downstream heightening from originally upstream heightening, and therefore fully complying with the Brazilian regulations. Furthermore, following Gerdau’s decision. the tailings disposal at the Dam was interrupted by February 2023, and therefore the Company will dispose of its tailings 100% through dry stacking.

The Alemães Dam is classified as Class B (low risk) in accordance with the National Mining Dam Registry available on the website of the National Mining Agency (ANM). Gerdau adopts rigorous standards for engineering control and environmental supervision and conducts a half-yearly Geotechnical Stability Audit to ensure the stability of the dam. Gerdau maintains a Mining Dam Emergency Action Plans that are filed at the regulatory agencies, as required by applicable regulations.

The Company also has other structures that are treated as Mining Dams by the ANM: UTM 2 Bays, North Dike of Waste Pile 01, and North and South Bays of Waste Pile A. These are structures that receive stormwater runoff and/or effluents from drainage at the Ore Treatment Units to enable the sedimentation of solid waste before the water is returned to the environment.

All the structures also undergo external audits that attest to their geotechnical stability, as well as regular inspections and monitoring.

11

An accident involving any of these dams could have serious adverse consequences, including:

| ● | Temporary/permanent shutdown of mining activities and consequently the need to buy iron ore to supply mills; |

| ● | High expenditures on contingencies and on recovering the regions and people affected; |

| ● | High investments to resume operations; |

| ● | Payment of fines and damages; |

| ● | Potential environmental impacts. |

Any of these consequences could have a material adverse impact on the Company’s operating results, cash flow and financial condition.

Financial Risks

Any downgrade in the Company’s credit ratings could adversely affect the availability of new financing and increase its cost of capital.

In 2007, the international rating agencies, Fitch Ratings and Standard & Poor’s, classified the Company’s credit risk as “investment grade”, enabling the Company to access more attractive borrowing rates. During reviews in 2022, despite a lower local sovereign credit rating, the Company maintained its investment grade with S&P and Fitch, respectively, with stable outlook and was upgraded to Baa3 from Ba1 rating with Moody’s with stable outlook, reflecting the Company’s history of conservative capital allocation, combined with the expectation of strong operating performance throughout the year.

The loss of any one or more of Gerdau’s investment grade ratings could increase its cost of capital, impair its ability to obtain capital and adversely affect its financial condition and results of operations.

The Company’s level of indebtedness could adversely affect its ability to raise additional capital to fund operations, limit the ability to react to changes in the economy or the industry and prevent it from meeting its obligations under its debt agreements.

The Company’s degree of leverage, together with a resulting change in rating by the credit rating agencies, could have important consequences, including the following:

| ● | It may limit the ability to obtain additional financing for working capital, additions to fixed assets, product development, debt service requirements, acquisitions and general corporate or other purposes; |

| ● | It may limit the ability to declare dividends on its shares; |

| ● | A portion of the cash flows from operations must be dedicated to the payment of interest on existing indebtedness and is not available for other purposes, including operations, additions to fixed assets and future business opportunities; |

| ● | It may limit the ability to adjust to changing market conditions and place the Company at a competitive disadvantage compared to its competitors that have less debt; |

| ● | The Company may be vulnerable in a downturn in general economic conditions; and |

| ● | The Company may be required to adjust the level of funds available for additions to fixed assets. |

As a result, the Company’s financial condition and results of operations may be adversely affected.

12

Variations in the foreign exchange rates between the U.S. dollar and the currencies of countries in which the Company operates may increase the cost of servicing its debt denominated in foreign currency and adversely affect its overall financial performance.

The Company’s results of operations are affected by fluctuations in the foreign exchange rates between the Brazilian real, the currency in which the Company prepares its financial statements, and the currencies of the countries in which it operates.

For example, the North America Business Segment reports its results in U.S. dollars. Therefore, fluctuations in the exchange rate between the U.S. dollar and the Brazilian real could affect its results of operations. The same occurs with all other businesses located outside Brazil with respect to the exchange rate between the local currency of the respective subsidiary and the Brazilian real.

Export revenue and margins are also affected by fluctuations in the exchange rate of the U.S. dollar and other local currencies of the countries where the Company produces in relation to the Brazilian real. The Company’s production costs are denominated in local currency, but its export sales are generally denominated in U.S. dollars. Revenues generated by exports denominated in U.S. dollars are reduced when they are translated into Brazilian real in periods during which the Brazilian currency appreciates in relation to the U.S. dollar.

The Brazilian real depreciated against the U.S. dollar by 7.4% in 2021. In 2022, the Brazilian real appreciated against the U.S. dollar by 5.3% and by 8.0% in 2023. To date in 2024, the Brazilian real has depreciated by 2.9% by the end of February 2024.

The Company held debt denominated in foreign currency, mainly U.S. dollars, in an aggregate amount of R$ 7.4 billion on December 31, 2023, representing 68% of its consolidated gross debt (loans, financings, and debentures). Significant further depreciation in the Brazilian real in relation to the U.S. dollar or other currencies could reduce the Company’s ability to service its obligations denominated in foreign currencies, particularly since a significant part of its net sales revenue is denominated in Brazilian reais. As a result, the Company’s financial condition and results of operations may be adversely affected.

Exchange rate instability also may adversely affect the amount of dividends we can distribute to our shareholders, including the holders of our ADSs and the market price of our shares and ADSs.

We are involved in several tax, environmental, civil and labor disputes involving significant monetary claims. Unfavorable outcomes in judicial, administrative and regulatory litigation may negatively affect our results of operations, cash flows and financial condition.

In the ordinary course of our business dealings, we are, and may become, party to numerous tax, environmental, civil and labor disputes involving, among other remedies, significant monetary claims. An unfavorable outcome against us may result in our being required to pay substantial amounts of money, including penalties and interest, which could materially adversely affect our reputation, results of operations, cash flows and financial condition. For certain of these legal proceedings and claims, we have not established a provision on our balance sheet or have only established provisions for part of the amounts in question, based on our external or internal counsels’ judgment as to the likelihood of an outcome unfavorable to us. Additionally, the amounts provisioned for legal proceedings may increase and existing provisions may become insufficient due to unfavorable outcomes in disputes against us. Although we are contesting existing proceedings and claims, the outcome of each specific proceeding and claim is uncertain and may result in obligations that could materially and adversely affect us. For further information concerning the principal pending matters, see Item 5--“Provisions for tax, civil and labor claims”, Item 8, “Legal Proceedings” and Note 19 to the Consolidated Financial Statements appearing elsewhere in this Annual Report.

Default by our clients or not receiving amounts invested with financial institutions could adversely affect the Company’s financial condition.

Gerdau may suffer losses from the default of our clients. Gerdau has a broad base of active clients and, in the case of default of a group of clients, Gerdau may suffer an adverse effect on its business, financial condition, results of operations and cash flows.

This risk arises from the possibility of the Company not receiving amounts arising from sales to customers or investments made with financial institutions, which could also have an adverse effect on the business, financial condition, results of operations and cash flows of Gerdau.

13

Regulatory Risks

Restrictive measures on trade in steel products may affect the Company’s business by increasing the price of its products or reducing its ability to export.

Gerdau is a steel producer that supplies both the domestic market in Brazil and several international markets. The Company’s exports face competition from other steel producers, as well as restrictions imposed by importing countries in the form of quotas, ad valorem taxes, tariffs or increases in import duties, any of which could increase the costs of products and make them less competitive or prevent Gerdau from selling in these markets. There are no assurances that importing countries will not impose quotas, ad valorem taxes, tariffs or increase import duties, which could adversely affect the Company’s financial condition and results of operations.

Costs related to compliance with environmental regulations could increase if requirements become stricter, which could have a negative effect on the Company’s results of operations.

The Company’s industrial units and other activities must comply with a series of federal, state and municipal laws and regulations regarding the environment and the operation of plants in the countries in which they operate. These regulations include procedures relating to control of air emissions, disposal of liquid effluents and the handling, processing, storage, disposal and reuse of solid waste, hazardous or not, as well as other controls necessary for a steel company and with mining activities.

Non-compliance with environmental and regulatory laws and regulations could result in administrative, civil or criminal sanctions and closure orders, in addition to the obligation of repairing damage caused to third parties and the environment, such as clean-up of contamination. If current and future laws become stricter, spending on fixed assets and costs to comply with legislation could increase and negatively affect the Company’s financial condition. Moreover, future acquisitions could subject the Company to additional spending and costs in order to comply with environmental and regulatory legislation. As a result, the Company’s financial condition and results of operations may be adversely affected.

Laws and regulations to reduce greenhouse gases and other atmospheric emissions could be enacted in the near future, with significant, adverse effects on the results of the Company’s operations, cash flows and financial condition.

One of the possible effects of the expansion of greenhouse gas reduction requirements is an increase in costs, mainly resulting from the demand for renewable energy and the implementation of new technologies in the productive chain. On the other hand, demand is expected to grow constantly for recyclable materials such as steel, which, being a product that could be recycled numerous times without losing its properties, results in lower emissions during the lifecycle of the product.

The Company expects operations overseas to be affected by future federal, state and municipal laws related to climate change, seeking to deal with the question of greenhouse gas (GHG) and other atmospheric emissions. Thus, one of the possible effects of this increase in legal requirements could be an increase in energy costs. As a result, the Company’s financial condition and results of operations may be adversely affected.

The European Union (EU) Carbon Border Adjustment Mechanism (CBAM), aims to avoid “carbon leakage”, ensuring that its climate policies are not undermined by production relocating to countries with less ambitious green standards or by the replacement of EU products by more carbon-intensive imports. EU has the EU Emissions Trading System (ETS) in place. EU importers of some goods, including steel will have to report on the volume of their imports and GHG emissions embedded during their production, but without paying any financial adjustment at this stage. The transitional phase, which started in October 2023, will last until 2026, when the definitive period starts. As of that date, importers will need to buy and surrender the number of “CBAM certificates” corresponding to the GHG emissions embedded in imported CBAM goods. This new mechanism will not only impact our operations, which may lead to increased costs for our customers who are importers, but it can also shift the flow of steel products. Any products that do not meet the criteria set forth by the CBAM or any other future mechanism will be less competitive in these markets. However, they may still be accepted in countries or regions without a carbon border adjustment mechanism in place, resulting in an increase in the volume of steel with less ambitious green standards in the market. This will lead to competition with steel that is differentiated based on GHG emissions.

14

Our operations expose us to risks and challenges associated with conducting business in compliance with applicable anti-bribery, anti-corruption and antitrust laws and regulations.

We have operations in Brazil and other countries in South America and North America. We face several risks and challenges inherent in conducting business internationally, where we are subject to a wide range of laws and regulations such as the Brazilian Anti-Corruption Law (Law 12,846/2013), Antitrust Law (Law 12,529/2011), the U.S. Foreign Corrupt Practices Act, or FCPA, and similar anti-bribery, anti-corruption and antitrust laws in other jurisdictions. In recent years, there has been an increased focus on corruption in Brazil and also the investigation and enforcement activities of the United States under the FCPA and by other governments under similar laws and regulations. These laws generally prohibit corrupt payments to governmental officials and certain payments, gifts or remunerations to or from clients and suppliers.

Violations of these laws and regulations could result in fines, criminal penalties and/or other sanctions against the Company, our officers or our employees, requirements to impose more stringent compliance programs, and prohibitions on the conduct of the Company’s business and our ability to participate in public biddings. The Company may incur expenses and have to recognize provisions and other charges in respect of such matters. In addition, the increased attention focused upon liability issues as a result of investigations, lawsuits and regulatory and environmental proceedings could harm our brand or otherwise impact the growth of our business. The retention and renewal of many of our contracts depends on creating a sense of trust with our customers and any violation of these laws and regulations may irreparably undermine that trust and may lead to termination of such relationships, as well as have a material adverse effect on our financial condition and results of operations. If any of these risks materialize, our reputation, strategy, international expansion efforts and our ability to attract and retain employees could be negatively impacted, and, consequently our business, financial condition and results of operations could be adversely affected.

Our governance and compliance processes may fail to prevent regulatory penalties and reputational harm.

The Company operates in a global environment and our activities extend over multiple jurisdictions and complex regulatory frameworks, with increased enforcement activities worldwide. Our governance and compliance processes, which include the review of internal controls over financial reporting, may not be able to prevent future breaches of legal, accounting or governance standards. We may be subject to breaches of our Code of Ethics and Conduct, anti-corruption policies and business conduct protocols, as well as to cases of fraudulent behavior, corrupt practices and dishonesty by our employees, contractors and other agents. The Company’s failure to comply with applicable laws and other standards could subject it to fines, loss of operating licenses and reputational harm.

Risks Relating to Brazil

Any further downgrading of Brazil’s credit rating could adversely affect the price of our shares.

We can be adversely affected by investors’ perceptions of risks related to Brazil’s sovereign debt credit rating. Rating agencies regularly evaluate Brazil and its sovereign ratings, which are based on a number of factors including macroeconomic and industry trends, fiscal and budgetary conditions, indebtedness metrics and the perspective of changes in any of these factors.

On December 19, 2023, S&P Global Ratings upgraded Brazil’s sovereign credit rating to “BB” from “BB-” following tax reform approval and reflecting the expectation the country will make progress addressing fiscal imbalances balanced by a strong external position and monetary policy but still weak economic prospects. Therefore, Brazil is still rated below investment grade by the three main credit rating agencies. Over the next 2 years a potential fiscal deterioration and a higher-than-expected debt level could lead to ratings downgrades and benefits from the set of structural and microeconomic reforms, additionally to some progress at addressing fiscal imbalances, stabilizing debt levels could lead to an upgrade.

Brazil continues to experience political instability, which may adversely affect the Company.

Brazil’s political environment has historically influenced, and continues to influence, the performance of the country’s economy. Political crises have affected and continue to affect the confidence of investors and the general public, which have historically resulted in economic deceleration and heightened volatility in the securities issued by Brazilian companies.

15

In addition, the Brazilian economy remains subject to government policies, which may affect our operations and financial performance. Governmental policies and actions, if unsuccessful or poorly implemented, may affect our operations and financial performance. Uncertainty regarding the implementation by the administration of promised transformational changes in monetary, fiscal and pension policies, as well as the enactment of the corresponding legislation, could contribute to economic instability.

Inflation and government actions to combat inflation may contribute significantly to economic uncertainty in Brazil and could adversely affect the Company’s business.

If Brazil experiences high levels of inflation once again, the country’s rate of economic growth could slow, which would lead to lower demand for the Company’s products in Brazil. Inflation is also likely to increase some costs and expenses which the Company may not be able to pass on to its customers and, as a result, may reduce its profit margins and net income. In addition, high inflation generally leads to higher domestic interest rates, which could lead the cost of servicing the Company’s debt denominated in Brazilian reais to increase. Inflation may also hinder its access to capital markets, which could adversely affect its ability to refinance debt. Inflationary pressures may also lead to the imposition of additional government policies to combat inflation that could adversely affect our business. As a result, the Company’s financial condition and results of operations may be adversely affected.

Developments and the perception of risks in other countries, especially in the United States and emerging market countries, may adversely affect the market prices of our shares.

The market for securities issued by Brazilian companies is influenced, in some degree, by economic and market conditions in the United States and emerging market countries, especially other Latin American countries. The reaction of investors to economic developments in one country may cause the capital markets in other countries to fluctuate. Developments or adverse economic conditions in other emerging market countries have at times resulted in significant reductions of the investments from investment funds and declines in the amount of foreign currency invested in Brazil.

The Brazilian economy is also affected by international economic and market conditions, especially economic and market conditions in the United States. Share prices on the B3, for example, have historically been sensitive to fluctuations in United States interest rates as well as movements of the major United States stocks indexes.

Economic developments in other countries and securities markets could adversely affect the market prices of our shares, which could make it more difficult for us to access the capital markets and finance our operations in the future on acceptable terms, besides having a material adverse effect on our financial condition and results of operations.

Risks Related to our Corporate Structure

The interests of the controlling shareholder may conflict with the interests of the non-controlling shareholders.

Subject to the provisions of the Company’s bylaws, the controlling shareholder has powers to:

| ● | elect a majority of the directors and nominate executive officers, establish the administrative policy and exercise full control of the Company´s management; |

| ● | sell or otherwise transfer the Company´s shares; and |

| ● | approve any action requiring the approval of shareholders representing a majority of the outstanding capital stock, including corporate reorganization, acquisition and sale of assets, and payment of any future dividends. |

By having such power, the controlling shareholder can make decisions that may conflict with the interest of the Company and other shareholders, which could adversely affect the financial condition and the results of operations of the Company.

16

The loss of members of the senior management and executives of the Company can have an adverse impact on our business.

Gerdau has various programs to attract, incentivize and retain its senior management and executives, backed up by an inclusive and diverse culture. The Company also carries out evaluations of performance, potential and readiness for the advancement to senior management and executives. Gerdau’s ability to remain competitive depends to a large degree on the continuity of efforts and services rendered by its senior management and executives. The loss of members of the senior management and executives can result in an adverse impact on our business, since it can negatively affect our capacity to develop and implement our strategy, with an adverse impact on our operations and our financial and operating condition, possibly impacting investors’ investment decisions. Senior management and executives have left Gerdau in the past and others may do so in the future, such that we cannot predict the impact of the departure of senior management or executives or the consequence on the achievement of our business objectives.

As a foreign issuer, we have different disclosure and other requirements than U.S. domestic registrants.

As a foreign issuer, we may be subject to different disclosure and other requirements than domestic U.S. registrants. For example, as a foreign issuer, in the United States, we are not subject to the same disclosure requirements as a domestic U.S. registrant under the United States Securities Exchange Act of 1934, as amended (the Exchange Act), including the requirements to prepare and issue quarterly reports on Form 10-Q or to file current reports on Form 8-K upon the occurrence of specified significant events, the proxy rules applicable to domestic U.S. registrants under Section 14 of the Exchange Act or the insider reporting and short-swing profit rules applicable to domestic U.S. registrants under Section 16 of the Exchange Act. In addition, we intend to rely on exemptions from certain U.S. rules which will permit us to follow Brazilian legal requirements rather than certain of the requirements that are applicable to U.S. domestic registrants.

Furthermore, foreign issuers are required to file their annual report on Form 20-F within 120 days after the end of each fiscal year, while U.S. domestic issuers that are accelerated filers are required to file their annual report on Form 10-K within 75 days after the end of each fiscal year. As a result of the above, even though we are required to file reports on Form 6-K disclosing the information which we have made or are required to make public pursuant to Brazilian law, or are required to distribute to shareholders generally, and that is material to us, you may not receive information of the same type or amount that is required to be disclosed to shareholders of a U.S. company.

As a foreign issuer, we are permitted to, and we do, rely on exemptions from certain NYSE corporate governance standards, including the requirement that a majority of our board of directors consist of independent directors. This may afford less protection to our shareholders.

The NYSE’s rules require listed companies to have, among other things, a majority of their board members be independent and to have independent director oversight of executive compensation, nomination of directors and corporate governance matters. As a foreign issuer and a controlled Company, we are permitted to, and we will, follow home country practice in lieu of the above requirements. Brazilian law, the law of our home country, does not require that a majority of our board consist of independent directors or the implementation of a compensation committee or nominating a corporate governance committee, and our board include fewer, independent directors than would be required if we were subject to the NYSE rules applicable to most U.S. companies. As long as we rely on the foreign issuer exemptions to the NYSE rules, a majority of our board of directors is not required to consist of independent directors, our compensation committee is not required to be comprised entirely of independent directors, and we will not be required to have a nominating and corporate governance committee. Therefore, our board’s approach may be different from that of a board with a majority of independent directors, and, as a result, the management team’s oversight of the Company may be more limited than if we were subject to the NYSE rules applicable to most U.S. companies.

17

Risks Relating to Our Preferred Shares and ADSs

If we do not maintain a registration statement and no exemption from the Securities Act registration is available, U.S. Holders of ADSs may be unable to exercise preemptive rights with respect to our preferred shares.