UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| OR | ||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| For the fiscal year ended | ||||||||

| OR | ||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| OR | ||

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| Date of event requiring this shell company report | |||||

| For the transition period from | to | ||||||||||

| Commission file number | ||||||||

| (Exact name of Registrant as specified in its charter) | ||

| (Translation of Registrant’s name into English) | ||

| | ||

| (Jurisdiction of incorporation or organization) | ||

| (Address of principal executive offices) | ||

Telephone: +1 ( | ||||||||||||||

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to section 12(b) of the Act.

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Securities registered or to be registered pursuant to section 12(g) of the Act.

| None | ||

| (Title of class) | ||

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

| None | ||

| (Title of class) | ||

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2023, the registrant had | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| X | No | ||||||||||

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act 1934.

| Yes | X | ||||||||||

Note- Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| X | No | ||||||||||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| X | No | ||||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one).

| X | Accelerated filer | Non-accelerated filer | Emerging growth company | ||||||||||||||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

| Yes | No | ||||||||||

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

| Yes | No | ||||||||||

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

| Yes | No | X | |||||||||

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | X | International Financial Reporting Standards as issued by the International Accounting Standards Board | | Other | | ||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

| Item 17 | Item 18 | ||||||||||||||||

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Yes | No | ||||||||||||||||

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

| Yes | No | ||||||||||

INDEX TO REPORT ON FORM 20-F

| PART I | PAGE | |||||||

| ITEM 1. | ||||||||

| ITEM 2. | ||||||||

| ITEM 3. | ||||||||

| ITEM 4. | ||||||||

| ITEM 4A. | ||||||||

| ITEM 5. | ||||||||

| ITEM 6. | ||||||||

| ITEM 7. | ||||||||

| ITEM 8. | ||||||||

| ITEM 9. | ||||||||

| ITEM 10. | ||||||||

| ITEM 11. | ||||||||

| ITEM 12. | ||||||||

| PART II | ||||||||

| ITEM 13. | ||||||||

| ITEM 14. | ||||||||

| ITEM 15. | ||||||||

| ITEM 16A. | ||||||||

| ITEM 16B. | ||||||||

| ITEM 16C. | ||||||||

| ITEM 16D. | ||||||||

| ITEM 16E. | ||||||||

| ITEM 16F. | ||||||||

| ITEM 16G. | ||||||||

| ITEM 16H. | ||||||||

ITEM 16I. | ||||||||

| ITEM 16J. | ||||||||

ITEM 16K. | ||||||||

| PART III | ||||||||

| ITEM 17. | ||||||||

| ITEM 18. | ||||||||

| ITEM 19. | ||||||||

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Matters discussed in this report may constitute forward-looking statements. The Private Securities Litigation Reform Act of 1995 provides safe harbor protections for forward-looking statements in order to encourage companies to provide prospective information about their business. Forward-looking statements include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and other statements, which are other than statements of historical facts.

We desire to take advantage of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and are including this cautionary statement in connection with this safe harbor legislation. This report and any other written or oral statements made by us or on our behalf may include forward-looking statements, which reflect our current views with respect to future events and financial performance. When used in this report, the words “believe”, “anticipate”, “intend”, “estimate”, “forecast”, “projected”, “plan”, “potential”, “continue”, “will”, “may”, “could”, “should”, “would”, “expect” and similar expressions identify forward-looking statements.

The forward-looking statements in this report are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, management’s examination of historical operating trends, data contained in our records and other data available from third parties. Although we believe that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies which are difficult or impossible to predict and are beyond our control, we cannot assure you that we will achieve or accomplish these expectations, beliefs or projections. As a result, you are cautioned not to rely on any forward-looking statements.

In addition to these important factors and matters discussed elsewhere herein, important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements include, among other things:

•our ability and that of our counterparty to meet our respective obligations under the 20-year lease and operate agreement (the “LOA”) with BP Mauritania, a subsidiary of BP p.l.c (“BP”), entered into in connection with the Greater Tortue Ahmeyim Project (the “GTA Project”), including the timing of various project infrastructure deliveries to site such as the floating production, storage and offloading unit (“FPSO”). Delays to contracted deliveries to site could result in incremental costs to both parties to the LOA, delay commissioning works and the start of operations for our floating liquefaction natural gas vessel (“FLNG”) Gimi (“FLNG Gimi”);

•continuing uncertainty resulting from our claim for certain pre-commissioning contractual prepayments that we believe we are entitled to receive from BP pursuant to the LOA, including timing of eventual resolution, whether our claim will be upheld and any eventual recovery or amounts that we may be required to settle;

•the recoverability of other pre-commissioning contractual prepayments that we believe we could be entitled to receive from BP;

•our ability to meet our obligations under the liquefaction tolling agreement (the “LTA”) entered into in connection with the Hilli Episeyo (“FLNG Hilli”);

•our ability to recontract the FLNG Hilli once her current contract ends in July 2026 and other competitive factors in the FLNG industry;

•that an attractive deployment opportunity, or any of the opportunities under discussion for the Mark II FLNG (“Mark II”), one of our FLNG designs, will be converted into a suitable contract. Failure to do this in a timely manner or at all could expose us to losses on our investments in a donor vessel for a prospective Mark II project, the Fuji LNG (the “Fuji LNG”), long-lead items and engineering services to date. Assuming a satisfactory contract is secured, changes in project capital expenditures, foreign exchange and commodity price volatility could have a material impact on the expected magnitude and timing of our return on investment;

•continuing uncertainty resulting from potential future claims from our counterparties of purported force majeure (“FM”) under contractual arrangements, including but not limited to our future projects and other contracts to which we are a party;

•failure of shipyards to comply with schedules, performance specifications or agreed prices;

•failure of our contract counterparties to comply with their agreements with us or other key project stakeholders;

•our ability to close potential future transactions in relation to equity interests in our vessels, including the Golar Arctic, FLNG Hilli and FLNG Gimi or to monetize our remaining equity method investments on a timely basis or at all;

•increases in operating costs as a result of inflation, including but not limited to salaries and wages, insurance, crew provisions, repairs and maintenance, spares and redeployment related modification costs;

•continuing volatility in the global financial markets, including but not limited to commodity prices, foreign exchange rates and interest rates;

•global economic trends, competition and geopolitical risks, including impacts from the length and severity of future pandemic outbreaks, rising inflation and the ongoing conflicts in Ukraine and the Middle East, recent attacks on vessels in the Red Sea and the related sanctions and other measures, including the related impacts on the supply chain for our conversions or commissioning works, the operations of our charterers and customers, our global operations and our business in general;

•changes in our relationship with our equity method investments and the sustainability of any distributions they pay us;

•claims made or losses incurred in connection with our continuing obligations with regard to New Fortress Energy Inc. (“NFE”), Energos Infrastructure Holdings Finance LLC (“Energos”), Cool Company Ltd (“CoolCo”) and Snam S.p.A. (“Snam”);

•the ability of Energos, CoolCo and Snam to meet their respective obligations to us, including indemnification obligations;

•changes in our ability to retrofit vessels as FLNGs or floating storage and regasification units (“FSRUs”) and our ability to secure financing for such conversions on acceptable terms or at all;

•changes to rules and regulations applicable to liquefied natural gas (“LNG”) carriers, FLNGs or other parts of the natural gas and LNG supply chain;

•changes to rules and regulations applicable to companies with securities listed on an European Union (“EU”) regulated market, or with an EU presence, including but not limited to the European Union’s Corporate Sustainability Reporting Directive ("CSRD");

•changes in the supply of or demand for LNG or LNG carried by sea for LNG carriers or FLNGs and the supply of natural gas or demand for LNG in Brazil;

•a material decline or prolonged weakness in charter rates for LNG carriers or tolling rates for FLNGs;

•increased tax liabilities in the jurisdictions where we are currently operating or have previously operated;

•changes in general domestic and international political conditions, particularly where we operate, including in Senegal, or where we seek to operate;

•changes in the availability of vessels to purchase and in the time it takes to build new vessels or convert existing vessels and our ability to obtain financing on acceptable terms or at all;

•actions taken by regulatory authorities that may prohibit the access of LNG carriers and FLNGs to various ports; and

•other factors listed from time to time in registration statements, reports or other materials that we have filed with or furnished to the U.S. Securities and Exchange Commission (the “Commission”), including our annual report on Form 20-F.

Please see our Risk Factors in Item 3 of this report for a more complete discussion of these and other risks and uncertainties. We caution readers of this report not to place undue reliance on these forward-looking statements, which speak only as of their dates. These forward-looking statements are not guarantees of our future performance, and actual results and future developments may vary materially from those projected in the forward-looking statements.

All forward-looking statements included in this report are made only as of the date of this report and, except as required by law, we assume no obligation to revise or update any written or oral forward-looking statements made by us or on our behalf as a result of new information, future events or other factors. If one or more forward-looking statements are revised or updated, no inference should be drawn that additional revisions or updates will be made in the future.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

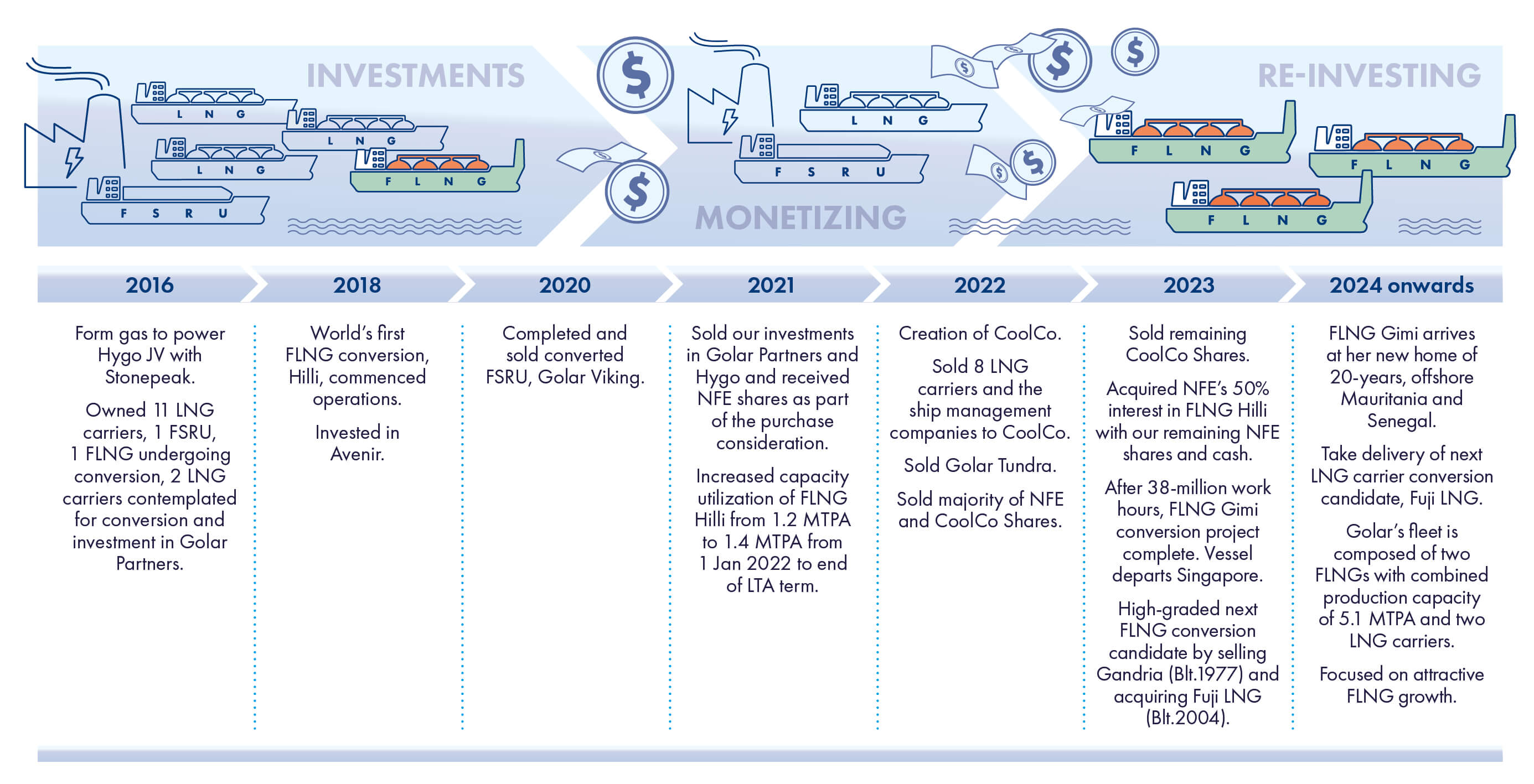

Throughout this report, unless the context indicates otherwise, the “Company”, “Golar”, “Golar LNG”, “we”, “us”, and “our” all refer to Golar LNG Limited or any one or more of its consolidated subsidiaries, including Golar Management Limited, or Golar Management, or to all such entities. References to “Golar Partners” or “GMLP” refer, depending on the context, to our former affiliate Golar LNG Partners LP (previously listed on Nasdaq: GMLP) and to any one or more of its subsidiaries. References to “Hygo” refer to our former affiliate Hygo Energy Transition Ltd and to any one or more of its subsidiaries. References to “Avenir” refer to our affiliate Avenir LNG Limited (Norwegian OTC: AVENIR) and to any one or more of its subsidiaries. References to “NFE” refer to New Fortress Energy Inc. (Nasdaq: NFE), the third-party purchaser of Golar Partners and Hygo, which acquisition closed on April 15, 2021. References to “CoolCo” refer to Cool Company Ltd (Euronext Growth/NYSE: CLCO) and to any one or more of its subsidiaries. Unless otherwise indicated, all references to “USD” and “$” in this report are to U.S. dollars.

A. Reserved

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

The risk factors summarized and detailed below could materially and adversely affect our business, our financial condition, our results of operations and the trading price of our common shares. We have categorized the risks we face based on whether they arise from our FLNG business, projects, financing and operational activities or from the industry in which we operate. We have listed these risks based on management’s assessment of priority. Where relevant, we have grouped together related risks into the following categories:

◦Risks related to our FLNGs and our FLNG growth projects

■Our ability to meet our continuing obligations under the LOA entered into in connection with the FLNG Gimi;

■Continuing uncertainty on the recoverability of certain pre-commissioning contractual prepayments claim pursuant to the LOA;

■Our ability to meet our continuing obligations under the LTA entered into in connection with the FLNG Hilli;

■Our ability to recontract the FLNG Hilli once her current contract ends;

■Our operating revenue is dependent on a high customer concentration wherein a loss of any of our customers could have an adverse effect on our earnings, cash flows and financial condition;

■Our efforts to manage commodity and financial risks through derivative instruments could adversely affect our results of operations and financial condition;

■Our ability to convert Mark II commercial leads into a long-term profitable contract;

■Our ability to complete a Mark II conversion could have a material adverse effect on our business, financial condition, results of operations, cash flow, liquidity and future prospects;

■Our ability to secure funding for our Mark II project; and

■Our heavy reliance on a limited number of contractors and shipyards with relevant specialized experience, given the sophisticated nature of FLNG conversions.

1

◦Risks related to the financing of our business

■We may not be able to obtain new financings to meet our obligations as they fall due or to fund our growth or our future capital expenditures, which could negatively impact our results of operations, financial condition and ability to pay dividends;

■We are exposed to volatility in the Secured Overnight Financing Rate (“SOFR”) and the derivative contracts we have entered into to hedge our exposures to fluctuations in interest rates could result in charges against our results of operations, being higher than market interest rates;

■Most of our financing agreements are secured by our vessels and contain operating and financial restrictions and other covenants that may restrict our business and financing activities;

■We entered into guarantees for certain parties. If these parties are unable to service their debt requirements or comply with certain provisions contained in their loan agreements, this may have a material adverse effect on us;

■The inability of certain parties to satisfy their indemnity obligations to us could have a material adverse effect on our financial condition and results of operations;

■If the Hilli letter of credit (the “Hilli LC”) is not extended, the results of operations and financial condition of Golar Hilli Corp. (“Hilli Corp”) could suffer;

■Servicing our debt agreements substantially limits our funds available for other purposes and our operational flexibility;

■Our consolidated lessor variable interest entity (“VIE”) may enter into different financing arrangements, which could affect our financial condition, results of operations and cash flows; and

■Our cash and cash equivalents and restricted cash are dependent on a limited number of financial institutions, wherein a collapse of any of these financial institutions could have an adverse effect on our cash flows and financial condition.

◦Risks related to our operations

■We are subject to certain risks with respect to our contractual counterparties, and failure of such counterparties to meet their obligations could cause us to suffer losses or otherwise adversely affect our business;

■We may experience increased labor costs, the unavailability of skilled workers or the failure to attract and retain qualified key personnel, which may negatively impact the effectiveness of our management and our results of operations;

■A cyber-attack could materially impact our reputation, operations or financial performance;

■Our operations face several industry risks and events which could cause damage or loss of a vessel, loss of life or environmental consequences that could harm our reputation and ongoing business operations;

■Technical operational risk, human operational errors and wear and tear of equipment may impact uptime and have an associated impact on financial performance of our FLNGs;

■We are subject to the economic, political, social and other conditions in the jurisdictions where we operate;

■Failure to comply with the U.S. Foreign Corrupt Practices Act of 1977 (the “FCPA”), the Bribery Act of the UK (the “UK Bribery Act”) and other anti-bribery legislation in other jurisdictions could result in fines, criminal penalties, and contract terminations;

■Vessel values may fluctuate substantially and, if these values are lower at a time when we are attempting to dispose of vessels or a decrease in their estimated future cash flows during our recoverability assessment, we may incur a loss which will have a material adverse effect on our results of operations;

■We will have to make additional contributions to our pension scheme because it is underfunded;

■We are exposed to U.S. Dollar, Euro, Norwegian Krone, British Pound, Brazilian Real and other foreign currency fluctuations and devaluations that could harm our results of operations;

■We are subject to the risk related to Macaw Energies’ business which may not achieve anticipated profitability as expected or at all; and

■Our equity method investments may not result in sufficient profitability to justify our investment, and could lead to future impairment.

◦Risks related to our industry

■Our results of operations and financial condition depend on demand for natural gas, LNG, FLNGs and LNG carriers;

■Our operations are subject to extensive and changing laws, regulations, reporting requirements and environmental and social attitudes towards fossil fuel, may have an adverse effect on our business; and

■Environmental, social and governance (“ESG”) and sustainability considerations may adversely impact our operations and markets.

2

◦Risks related to our common shares

■The declaration and payment of dividends or repurchases of our own shares are at the discretion of our board of directors;

■Our common share price may be highly volatile and future sales of our common shares could cause the market price of our common shares to decline and could lead to a loss of all or part of a shareholder’s investment;

■We may issue additional common shares or other equity securities without our shareholders’ approval, which would dilute their ownership interests and may depress the market price of our common shares;

■Because we are a Bermuda corporation, our shareholders may have less recourse against us or our directors than shareholders of a U.S. company have against the directors of a U.S. company; and

■Because our offices and most of our assets are outside the U.S., our shareholders may not be able to bring a suit against us, or enforce a judgment obtained against us in the United States.

◦Risks related to tax

■As a Bermuda exempted company incorporated under Bermuda law with subsidiaries in the Marshall Islands and other offshore jurisdictions, our operations may be subject to economic substance requirements;

■A change in tax laws in any country in which we operate could adversely affect us;

■We could be treated as or become a passive foreign investment company (“PFIC”), which could have adverse U.S. federal income tax consequences to U.S. shareholders;

■We may have to pay tax on certain U.S. source income, which would have a negative effect on our business and reduce cash available for distribution; and

■The recent enactment of a corporate income tax in Bermuda could adversely affect us.

Risks related to our FLNGs and our FLNG growth project

•Our ability to meet our continuing obligations under the LOA entered into in connection with the FLNG Gimi.

In February 2019, we entered into the LOA with BP for the lease and operation of FLNG Gimi, for the first phase of the GTA Project, situated off the coast of Mauritania and Senegal, for a period of 20 years. As of March 15, 2024, the FLNG Gimi is awaiting connection to the feedgas pipeline and start of commissioning activities.

Given the GTA Project’s complexity and the interdependencies of certain activities required during project mobilization and commissioning leading to commencement of commercial operations ("COD"), significant delays could result in incremental costs to both parties to the LOA and delay the unlocking of FLNG Gimi Adjusted EBITDA backlog of approximately $4.3 billion, of which we have a 70% ownership interest. If FLNG Gimi does not meet its anticipated profitability or generate sufficient cash flow on time or at all, our cash flows and results of operations may be adversely affected.

In the duration of the LOA, we are exposed to various risks, which encompass BP’s right to terminate the LOA due to specified events of default, non-payment by BP due to disagreements or disputes, assumption of unanticipated liabilities, losses, or costs, and potential financial repercussions in the event the FLNG Gimi fails to meet contracted capacity. Additionally, there is a risk of incurring significant charges such as asset devaluation or restructuring charges. Any of these circumstances or events could have a material adverse effect on our results of operations, cash flow and financial condition.

•Continuing uncertainty on the recoverability of certain pre-commissioning contractual prepayments claim pursuant to the LOA.

As described under note 18 of our audited consolidated financial statements included herein, a LOA contract interpretation dispute regarding parts of pre-commissioning contractual cash flows currently exists between us and BP, regarding Project Delay Payments (“PDPs”) due from BP to Gimi MS Corporation (“Gimi MS”). Gimi MS initiated arbitration proceedings in August 2023. The resolution of this matter is expected to take several months or years, with no guarantee of a favorable outcome for our claim. Pursuing such legal proceedings may incur significant time and legal expenses. In the event of a favorable resolution, we may be entitled to recover all or a portion of our legal costs and fees incurred, from BP. Conversely, an unfavorable resolution may result in the potential forfeiture of our claim in part or in full and we may be required to reimburse all or a portion of BP’s legal costs and fees incurred which could have a material adverse impact on our business, financial position, and results of operations. Additionally, these legal actions carry the risk of negative publicity, potentially impacting our reputation and, consequently, our operational results. As of March 15, 2024, the dispute remains unresolved.

3

•Our ability to meet our continuing obligations under the LTA entered into in connection with the FLNG Hilli.

The FLNG Hilli is currently operating under the terms of the LTA by and between Perenco Cameroon S.A. (“Perenco”) and Société Nationale des Hydrocarbures (“SNH”) (together the “Customer”) which ends in mid-July 2026.

During the duration of the LTA, we are exposed to various risks, including potential challenges in realizing the benefits of the LTA. These risks encompass the Customer’s right to terminate the agreement due to specified events of default, non-payment by the Customer due to financial constraints or disagreements, assumption of unanticipated liabilities, losses, or costs, and potential financial repercussions in the event the FLNG Hilli fails to meet the annual contracted capacity. Additionally, there is a risk of incurring significant charges such as asset devaluation or restructuring charges. Any of these circumstances or events could have a material adverse effect on our results of operations, cash flow and financial condition.

•Our ability to recontract the FLNG Hilli once her current contract ends.

We may be unable to redeploy the FLNG Hilli on another long-term contract at the end of the current LTA. Our inability to redeploy the FLNG Hilli on a new long-term charter may result in increased downtime and decreased revenue, which could adversely impact our financial performance and overall business outlook. Additionally, regulatory changes, competition, or technological advancements, may further influence the vessel’s redeployment prospects. Accordingly, there can be no assurance that the FLNG Hilli meets its anticipated profitability or generates sufficient cash flow to justify our investment.

•Our operating revenue is dependent on a high customer concentration wherein a loss of any of our customers could have an adverse effect on our earnings, cash flows and financial condition.

Our future revenue is dependent on a limited number of customers. The loss of a key customer or a substantial decline in the amount of services requested by a key customer, or the inability of a customer to pay for our services, could have a material adverse effect on our results of operations, cash flows and financial condition. We could lose a customer or the benefits of a contract if:

•the customer fails to make payments because of its financial inability, disagreements with us or otherwise;

•we breach the relevant contract and the customer exercises certain rights to terminate the contract;

•the customer terminates the contract because we fail to deliver the vessel or provide the service within a contracted period of time, the vessel is lost or damaged beyond repair or incurs prolonged periods of off-hire, or we default under the contract;

•the customer terminates the contract due to prolonged FM affecting the customer, including damage to or destruction of relevant facilities, war or geopolitical unrest preventing us from performing services for that customer; or

•the customer becomes subject to sanction laws which directly or indirectly prohibits our ability to lawfully charter our vessel to such customer.

If we lose a key customer or if a customer exercises its right to terminate the contract or charter, we may be unable to acquire an adequate replacement which could have a material adverse effect on our results of operations, cash flows and financial condition.

•Our efforts to manage commodity and financial risks through derivative instruments could adversely affect our results of operations and financial condition.

We use derivative instruments to manage commodity, currency and financial market risks. The extent of our derivative position at any given time depends on our assessments of the markets for these commodities and related exposures. We currently account for all derivatives at fair value, with immediate recognition of changes in the fair value in our earnings. These transactions and other derivative transactions have resulted and may continue to result in substantial volatility in reported results of operations, particularly in periods of significant commodity, currency or financial market variability, or as a result of ineffectiveness of these contracts. Changes in the underlying assumptions or use of alternative valuation methods could affect the reported fair value of these contracts. In addition, our liquidity may be adversely impacted by the cash margin requirements of the commodities exchanges or the failure of a counterparty to perform in accordance with a contract.

4

•Our ability to convert Mark II commercial leads into a long-term profitable contract.

The successful conversion of commercial leads into long-term profitable contracts for our new Mark II, one of our FLNG designs, represents a critical aspect of our business growth strategy. However, this process is subject to various uncertainties and challenges that may impact our ability to secure profitable contracts, attractive financing and achieve sustainable operating cash inflows.

The inherent uncertainty in the energy market, including fluctuations in commodity prices and regulatory changes, may impact the decision-making processes of potential customers. Economic downturns, geopolitical events, or shifts in energy policies can introduce unpredictability and volatility, making it challenging to forecast and convert commercial leads into profitable long-term contracts. Difficulties in converting opportunities to a binding commercial agreement with a counterparty for the deployment of a Mark II design conversion could result in additional costs and could negatively impact our future project prospects.

•Our ability to complete a Mark II conversion could have a material adverse effect on our business, financial condition, liquidity and future prospects.

The intricacies and scale of the FLNG conversion process pose risks, including unforeseen technical challenges or complexities in the Mark II design, especially with the integration of new technologies or modifications to the original design. Delays in the FLNG conversion schedules beyond agreed-upon timelines may impact our ability to meet contractual obligations, resulting in potential financial penalties, strained customer relationships and reputational damage. Such delays may be caused by various factors, including unforeseen technical issues, supply chain disruptions, adverse weather conditions, or regulatory hurdles.

Moreover, the failure of shipyards to adhere to performance specifications could compromise the operational efficiency and effectiveness of the converted FLNG units. This may lead to suboptimal performance, increased maintenance costs, and potential liabilities if the delivered product fails to meet industry standards or regulatory requirements. Deviations from agreed-upon prices with suppliers can result in unexpected financial burdens. Additionally, the global nature of the shipbuilding industry exposes us to geopolitical and economic risks, wherein changes in trade policies, geopolitical tensions, or economic downturns in key regions, may affect the availability of skilled labor, essential materials, and financing, leading to increased project costs and delays.

In addition, changes in regulatory requirements, unexpected permitting delays or the need to comply with evolving environmental, safety, and operational standards may require modifications to the project plan. In the event of non-compliance by shipyards, our ability to enforce contractual terms and secure timely remedies may be subject to legal and regulatory complexities, further exacerbating the adverse impact on our results of operations, cash flow and financial condition.

•Our ability to secure funding for our Mark II project.

The conversion of a FLNG, such as Mark II, takes a number of years and requires a substantial capital investment that is dependent on sufficient funding and commercial interest, among other factors. The availability and cost of financing in the capital markets can be influenced by various external factors, including economic conditions, interest rates, investor sentiment, contingencies and uncertainties that are beyond our control. Unforeseen changes in these factors may lead to fluctuations in the cost of debt or equity financing, potentially affecting the overall financial feasibility of the Mark II project. Further, the complexity and scale of the Mark II may present challenges in structuring financing arrangements. Lenders and investors may have stringent requirements related to project viability, risk allocation, and financial returns, which may necessitate protracted negotiations and due diligence processes. We may be required to use cash from operations, incur additional borrowings or raise capital through the sale of debt or additional equity securities to fund the conversion. Our failure to obtain funds for future capital expenditures could impact our results of operations, cash flow, financial condition and growth prospects.

5

•Our heavy reliance on a limited number of contractors and shipyards with relevant specialized experience, given the sophisticated nature of FLNG conversions.

The conversion of our Mark II design will be the first of its kind. Due to its novelty and the highly technical process related to FLNG conversions, we are reliant on a limited number of contractors and shipyards with relevant FLNG conversion experience. A change of appointed contractors for any reason would likely result in higher costs and a significant delay to any delivery schedules. Our future FLNG vessels may not able to meet certain performance requirements or perform as intended and we may have to accept reduced rates, not be able to contract FLNG vessel or we may be required to recognize an impairment expense in our financial statements in the future. Any of these possibilities would have a negative impact, which could be significant, on our results of operations, cash flow and financial condition.

Risks related to the financing of our business

•We may not be able to obtain new financings, to meet our obligations as they fall due or to fund our growth or our future capital expenditures, which could negatively impact our results of operations, financial condition and ability to pay dividends.

In order to fund future projects, increased working capital levels or other capital expenditures, we may be required to use cash from operations, incur additional borrowings or raise capital through the issuance of debt or additional equity securities.

Our ability to do so may be limited by our financial condition at the time of such financing or offering, as well as by adverse market conditions resulting from, among other things, general economic conditions and contingencies and uncertainties that are beyond our control. Our failure to obtain funds for future capital expenditures could impact our results of operations, financial condition and our ability to pay dividends. Furthermore, our ability to access capital, the overall economic conditions and our ability to secure new customers on a timely basis could limit our ability to fund our growth plans and capital expenditures. If we are successful in issuing equity in order to raise capital, the issuance of additional equity securities would dilute existing shareholders’ equity interests and reduce any pro rata dividend payments without a commensurate increase in cash allocated to dividends, if any. Even if we are successful in obtaining bank financing, paying debt service would limit cash available for working capital and increasing our indebtedness could have a material adverse effect on our business, results of operations, cash flows, financial condition and ability to pay dividends.

•We are exposed to volatility in SOFR and the derivative contracts we have entered into to hedge our exposures to fluctuations in interest rates could result in charges against our results of operations, being higher than market interest rates.

As of December 31, 2023, we had total outstanding debt of $1.2 billion, of which $0.8 billion was exposed to a floating interest rate based on SOFR, which could affect the amount of interest payable on our debt. In order to manage our exposure to interest rate fluctuations, we use interest rate swaps to effectively fix a part of our floating rate debt obligations. As of December 31, 2023, we have interest rate swaps with a notional amount of $0.7 billion representing 88.5% of our total floating rate debt. While we are economically hedged, we do not apply hedge accounting and therefore interest rate swap mark-to-market valuations may adversely affect our results. Entering into swaps and derivative transactions is inherently risky and presents various possibilities for incurring significant expenses. The derivative strategies that we employ currently and in the future may not be successful or effective, and we could, as a result, incur substantial additional interest costs or losses.

In the future, our financial condition could be materially adversely affected to the extent we do not hedge our exposure to interest rate fluctuations under loans that have been advanced at a floating rate. Any hedging activities we engage in may not effectively manage our interest rate exposure or have the desired impact on our financial condition or results of operations.

6

•Most of our financing agreements are secured by our vessels and contain operating and financial restrictions and other covenants that may restrict our business and financing activities.

Most of our obligations are secured by our vessels and guaranteed by our subsidiaries holding the interests in our vessels. Our loan agreements impose, and future financial obligations may impose, operating and financial restrictions on us. These restrictions may require the consent of our lenders, or may prevent or otherwise limit our ability to, among other things: merge into or consolidate with any other entity; to sell or otherwise dispose of, all or substantially all of our assets; make or pay equity distributions, repurchase our own shares; incur additional indebtedness; incur or make any capital expenditures; materially amend, or terminate, any of our current vessel contracts or management agreements.

Our loan agreements and lease financing arrangements also require us to maintain specific financial ratios, including minimum amounts of unrestricted cash, minimum ratios of current assets to current liabilities, excluding but not limited to the current portion of long-term debt, VIE balances, minimum levels of stockholders’ equity and maximum loan amounts to value. If we were to fail to maintain these levels and ratios without obtaining a waiver of covenant compliance or modification to our covenants, we would be in default of our loans and lease financing agreements, which, unless waived by our lenders, could provide our lenders with the right to require us to increase the minimum value held by us under our equity and liquidity covenants, increase our interest payments, pay down our indebtedness to a level where we are in compliance with our loan covenants, sell vessels in our fleet or reclassify our indebtedness as current liabilities and could allow our lenders to accelerate our indebtedness and foreclose their liens on our vessels, which could result in the loss of our vessels. If our indebtedness is accelerated, we may not be able to refinance our debt or obtain new financing, which would impair our ability to continue to conduct our business.

Events beyond our control, including changes in the economic and business conditions in the industries in which we operate, interest rate developments, changes in the funding costs of our banks, changes in vessel earnings and asset valuations, outbreaks of epidemic and pandemic diseases and war or geopolitical unrest, may affect our ability to comply with these financial covenants. We cannot provide any assurance that we will continue to meet these ratios or satisfy our financial or other covenants or that our lenders will waive any failure to do so.

•We entered into certain guarantees for certain parties. If these parties are unable to meet the requirements or comply with certain provisions contained in the agreements, this may have a material adverse effect on us.

We entered into agreements to provide stand-ready guarantees in connection with commercial bank indebtedness, claims, damages or liabilities imposed by governmental authorities for certain parties, including but not limited to Golar Partners, Hygo, Energos, CoolCo, Avenir and Macaw Energies and its investments. Failure by any of these parties to comply with any provisions contained in the agreements, may lead to an event of default under these agreements. In such case, we would need to satisfy the obligations or indemnify the losses of the respective party.

Additionally, if a default occurs under a loan agreement, the lenders could accelerate the outstanding borrowing and declare all amounts outstanding due and payable. In this case, if such party is unable to obtain a waiver or an amendment to the applicable provisions of the loan agreement, or do not have enough cash on hand to repay the outstanding borrowing, the lenders may, among other things, foreclose their liens on the respective asset, or seek repayment of the loan from such party or from us under the guarantee that we have provided.

The occurrence of any of the events described above would have a material adverse effect on our business, results of operations and financial condition, reduce our ability or make us unable to pay dividends to our shareholders for so long as such default is continuing, and may impair our ability to continue as a going concern.

•The inability of certain parties to satisfy their indemnity obligations to us could have a material adverse effect on our financial condition and results of operations.

Pursuant to the entry into agreements to provide stand-ready guarantees to certain parties, we are counter indemnified by certain parties, including CoolCo, NFE and Energos for certain losses we may incur in connection with providing guarantees and indemnities. These parties' abilities may be affected by events beyond either of our control, including prevailing economic, financial, geopolitical and industry conditions. If they are unable to meet their indemnification obligations, our results of operations, financial condition and ability to make cash distributions to our shareholders could be materially adversely affected.

7

•If the Hilli LC is not extended, the results of operations and financial condition of Hilli Corp could suffer.

Pursuant to the terms of the LTA, a financial institution issued a performance guarantee on behalf of Hilli Corp guaranteeing certain payments of Hilli Corp, as required under the LTA. The Hilli LC had an initial expiry date of December 31, 2019, which automatically extended and will extend for successive one-year periods until the tenth anniversary of the final acceptance of the FLNG Hilli under the LTA, unless the financial institution elects to not extend the Hilli LC. The financial institution may elect to not extend the Hilli LC by giving notice at least 90 days prior to December 31, in any subsequent year. If the Hilli LC (i) ceases to be in effect or (ii) the financial institution elects to not extend it, unless replacement security for payment is provided within a certain time, then the LTA may be terminated and Hilli Corp may be liable for a termination fee of up to $100 million. Accordingly, if the financial institution elects at some point in the future to not extend the Hilli LC, Hilli Corp’s financial condition could be materially and adversely affected.

•Servicing our debt agreements substantially limits our funds available for other purposes and our operational flexibility.

Our ability to service our indebtedness will depend upon, among other things, our future financial and operating performance, which will be affected by prevailing economic conditions and financial, regulatory, war or geopolitical unrest and other factors, some of which are beyond our control. If our cash inflows are not sufficient to service our indebtedness, we will be forced to take actions, such as reducing or delaying our business activities, acquisitions, investments or capital expenditures, selling assets, restructuring or refinancing our debt or seeking additional equity capital. We may not be able to effect any of these remedies on satisfactory terms, or at all. In addition, a lack of liquidity in the debt and equity markets could hinder our ability to refinance our debt or obtain additional financing on favorable terms in the future.

•Our consolidated lessor VIE may enter into different financing arrangements, which could affect our results of operations, cash flow and financial condition.

Following the sale and leaseback transaction we have entered into with a subsidiary of a Chinese financial institution that was determined to be lessor VIE, where we are deemed to be the primary beneficiary, we are required by accounting principles generally accepted in the United States of America (“U.S. GAAP”) to consolidate the lessor VIE into our financial results. Although consolidated into our results, we have no control over the funding arrangements negotiated by the lessor VIE such as interest rates, maturity and repayment profiles. The funding arrangements negotiated by the lessor VIE could adversely affect our results of operations, cash flow and financial condition. For additional detail refer to note 5 “Variable Interest Entities” of our consolidated financial statements included herein.

•Our cash and cash equivalents and restricted cash are dependent on a limited number of financial institutions, wherein a collapse of any of these financial institutions could have an adverse effect on our cash flows and financial condition.

As of December 31, 2023, we have $679.2 million of cash and cash equivalents, of which are $481.7 million held in short-term money market deposits carried with a limited number of financial institutions. The collapse of any financial institution or the inability of a financial institution to obtain necessary funding when required, or a banking crisis, could have a material adverse effect on our cash flows and financial condition.

Risks related to our operations

•We are subject to certain risks with respect to our contractual counterparties, and failure of such counterparties to meet their obligations could cause us to suffer losses or otherwise adversely affect our business.

We entered into agreements for the provision of certain technical, crew, transitional corporate and administrative services and have subcontracted the provision of certain corporate and administrative services to ship managers. Such agreements expose us to subcontractor counterparty risks. The ability of each of our subcontractors to perform its obligations under a contract with us will depend on a number of factors that are beyond our control and may include, among other things, general economic conditions, the overall financial condition of our subcontractors, the condition of the maritime and offshore industries and work stoppages or other labor disturbances. Should our subcontractors fail to honor their obligations under agreements with us, we could sustain significant losses, which could have a material adverse effect on our business, reputation, results of operations, cash flow and financial condition.

8

•We may experience increased labor costs, the unavailability of skilled workers or the failure to attract and retain qualified key personnel, which may negatively impact the effectiveness of our management and our results of operations.

We are dependent upon the available labor pool of skilled employees. We compete with other employers to attract and retain qualified personnel with the technical skills and experience required to construct and operate our FLNGs and to provide our customers with the highest quality service. A shortage in the labor pool of skilled workers, remote FLNG locations, increasing cost of living or other general inflationary pressures, changes in applicable laws and regulations or labor disputes could make it more difficult for us to attract and retain qualified personnel and could require an increase in the salaries, wages and benefits packages that we offer, thereby increasing our operating costs. Any increase in our operating costs could materially and adversely affect our business, contracts, results of operations, cash flow and financial condition.

Our success depends, to a significant extent, upon the skills and efforts of our senior executives and certain key employees. While we believe that we have an experienced team, the loss or unavailability of one or more of our senior executives and/or our key employees for any extended period of time could have an adverse effect on our business and results of operations.

•A cyber-attack could materially impact our reputation, operations or financial performance.

We rely on information and operational technology systems and networks in our operations and the administration of our business. The energy industry has become increasingly dependent on digital technologies to conduct day-to-day operations, and the use of mobile communication devices has rapidly increased. Industrial control systems such as supervisory control and data acquisition (“SCADA”) systems now control large-scale processes that can include multiple sites across long distances. In addition, cybersecurity attacks are also becoming more sophisticated and include, but are not limited to, ransomware, credential stuffing, spear phishing, social engineering, use of deepfakes (i.e., highly realistic synthetic media generated by artificial intelligence) and other attempts to gain unauthorized access to data for purposes of extortion or other malfeasance. Our technologies, systems, networks and business partners may become the target of cybersecurity attacks or security breaches.

We have experienced attempted cybersecurity attacks, but have not suffered any material adverse impacts to our business and operations as a result of such unsuccessful attempts. We have implemented security measures that are designed to detect and protect against cyberattacks. No security measure is infallible. Despite these measures and any additional measures, we may implement or adopt in the future, our facilities and systems, and those of our third-party service providers, have been and are vulnerable to security breaches, computer viruses, lost or misplaced data, programming errors, scams, burglary, misdirected wire transfers including security breaches caused by human errors, and other adverse events. Our efforts to improve security and protect data may also identify previously undiscovered instances of security breaches or bad actors with present access to our systems.

Cyber-attacks have increased in number and sophistication in recent years. Our operations could be targeted by individuals or groups seeking to sabotage, compromise or disrupt our information or operational technology systems and networks, to steal or corrupt data, or otherwise disrupt our operations. A successful cyber-attack could materially disrupt our operations, including the safety of our operations, or lead to unauthorized release of information or alteration of information on our systems. Any such attack or other breaches of our information technology and operational technology systems could have a material adverse effect on our business, results of operations, cash flow and financial condition, and may result in the loss of sensitive, confidential information or other assets, as well as litigation, including individual claims or class actions, regulatory enforcement actions, violation of privacy or securities laws and regulations, and remediation costs.

9

•Our operations face several industry risks and events which could cause damage or loss of a vessel, loss of life or environmental consequences that could harm our reputation and ongoing business operations.

Our vessels are exposed to a range of risks, including marine disasters, epidemic and pandemic diseases, piracy, environmental accidents, adverse weather conditions, mechanical failures, and geopolitical events like war and terrorism. Recent attacks in the Red Sea highlight potential consequences, including injury, property loss, and environmental damage. These events have the potential to disrupt cargo delivery, services, routine maintenance, inspections, and equipment management, leading to loss of hire, contract termination, governmental fines, and business restrictions. Additionally, our vessels could be requisitioned during national emergencies, exposing us to higher insurance premiums, potential coverage inadequacy, and uncertainties in claims settlements. Operating in regions designated as "war risk" zones could also increase insurance costs. Uninsured repair costs and the unpredictability of vessel repair cost could pose substantial financial challenges. Environmental incidents, including those from sandstorms, could lead to cleanup liabilities, penalties, and negative media coverage. All of these factors have the potential to materially impact our business, results of operations, cash flows, weaken our financial condition and negatively affect our ability to pay dividends.

•Technical operational risk, human operational errors and wear and tear of equipment may impact uptime and associated impact on financial performance of our FLNGs.

FLNGs are complex floating operation platforms dependent on multiple systems to work in parallel to obtain efficient operations. The various equipment onboard has different operational procedures and maintenance cycles. A breakdown of critical component(s) may adversely impact the overall performance of our FLNG operations, which may lead to economic impacts. Human operational errors, out of cycle maintenance of equipment, failure to routinely conduct maintenance, wear and tear and external impacts may negatively impact our operations and results of operations.

•We are subject to the economic, political, social and other conditions in the jurisdictions in which we operate.

Our main operations located in Cameroon, Senegal, Mauritania and Brazil are subject to various challenges arising from economic, political, social and other conditions and developments in these jurisdictions. Some of these countries have experienced political, security, and social economic instability in recent years and may experience instability in the future, including changes, sometimes frequent or marked, in energy policies or the personnel administering them, expropriation of property, cancellation or modification of contract rights, changes in laws and policies governing operations of foreign-based companies, unilateral renegotiation of contracts by governmental entities, redefinition of international boundaries or boundary disputes, foreign exchange restrictions or controls, currency fluctuations, royalty and tax increases and other risks arising out of governmental sovereignty over the areas in which our operations are and will be conducted, as well as risks of loss due to acts of social unrest, terrorism, corruption and bribery. The governments in certain of these jurisdictions differ widely with respect to structure, constitution, political, economic and social stability and some countries lack mature legal and regulatory systems. As our operations depend on governmental approval and regulatory decisions, we may be adversely affected by changes in the political structure or government representatives in each of the countries in which we operate. In addition, these jurisdictions, particularly emerging countries, are subject to risk of contagion from the economic, political and social developments in other emerging countries and markets.

Furthermore, some of the regions in which we operate have been subject to significant levels of terrorist activity, social and political unrest, particularly in the shipping and maritime industries. In addition to acts of terrorism, vessels trading in these and other regions have also been subject, in limited instances, to piracy. In addition, the ongoing political instability in Ukraine and Middle East may impact our business. Tariffs, trade embargoes and other economic sanctions by the U.S. or other countries against countries in the Middle East, Southeast Asia, Africa or elsewhere as a result of terrorist attacks, hostilities or otherwise may limit trading activities with those countries. This could have a material adverse effect on our business, results of operations, financial condition and our ability to pay cash distributions to our shareholders.

10

•Failure to comply with the FCPA, the UK Bribery Act and other anti-bribery legislation in other jurisdictions could result in fines, criminal penalties, and contract terminations.

We may operate in several countries throughout the world, including countries known to have a reputation for corruption. We are committed to doing business in accordance with applicable anti-corruption laws and have adopted a code of business conduct and ethics which is consistent and in full compliance with the FCPA and the UK Bribery Act. We are subject, however, to the risk that we, our affiliated entities or our or their respective officers, directors, employees and agents may take actions determined to be in violation of such anti-corruption laws, including the FCPA and the UK Bribery Act. Any such violation could result in substantial fines, sanctions, civil and/or criminal penalties, curtailment of operations in certain jurisdictions, and might adversely affect our business, results of operations or financial condition. In addition, actual or alleged violations could damage our reputation and ability to do business. Furthermore, detecting, investigating, and resolving actual or alleged violations is expensive and can consume significant time and attention of our senior management.

To effectively compete in some foreign jurisdictions, we utilize local agents and/or establish entities with local operators or strategic partners. All these activities may involve interaction by our agents with government officials. Even though some of our agents or partners may not themselves be subject to the FCPA, the UK Bribery Act, or other anti-bribery laws to which we may be subjected to, if our agents or partners make improper payments to government officials or other persons in connection with engagements or partnerships with us, we could be investigated and potentially found liable for violation of such anti-bribery laws and could incur civil and criminal penalties and other sanctions, which could have a material adverse effect on our business and results of operations.

•Vessel values may fluctuate substantially and, if these values are lower at a time when we are attempting to dispose of vessels or a decrease in their estimated future cash flows during our recoverability assessment, we may incur a loss which will have a material adverse effect on our results of operations.

Vessel values can fluctuate substantially over time due to several different factors, including:

•prevailing economic and market conditions in the natural gas and energy markets;

•a substantial or extended decline in demand for LNG;

•increases in the supply of vessel capacity without a commensurate increase in demand;

•the type, size and age of a vessel;

•competition from more technologically advanced vessels; and

•the cost of new buildings or retrofitting or modifying existing vessels, as a result of technological advances in vessel design or equipment, changes in applicable environmental or other regulations or standards, customer requirements or otherwise.

As our vessels age, the expenses associated with maintaining and operating them are expected to increase, which could have an adverse effect on our business and operations.

The carrying values of our vessels may not represent their fair market value at any point in time because the market prices of secondhand vessels tend to fluctuate with changes in charter rates, the cost of new build vessels and supply/demand for secondhand vessels. Our vessels are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. Any impairment charges recognized in our consolidated financial statements could negatively affect our business, results of operations, financial condition or the trading price of our common shares and publicly listed debt.

•We will have to make additional contributions to our pension scheme because it is underfunded.

We have two defined benefit pension plans for certain of our current and former marine employees. Members do not contribute to the pension scheme plans and these pension schemes are closed to new entrants. As of December 31, 2023, one of the plans is underfunded by $25.2 million. The underfunded pension liability could change depending on market conditions, interest rate volatility and other key actuarial assumptions. We may need to increase our contributions in order to meet the scheme’s liabilities as they fall due, or, to reduce the deficit. Such contributions could have a material and adverse effect on our cash flows and financial condition.

11

•We are exposed to U.S. Dollar, Euro, Norwegian Krone, British Pound, Brazilian Real and other foreign currency fluctuations and devaluations that could harm our results of operations.

Our principal currency for our operations and financing is the U.S. Dollar. We generate most of our revenues in the U.S. Dollar. Apart from the U.S. Dollar, we incur operating and administrative expenses in multiple currencies. Due to a portion of our expenses being incurred in currencies other than the U.S. Dollar, our expenses may, from time to time, increase relative to our revenues as a result of fluctuations in exchange rates, particularly between the U.S. Dollar and but not limited to the Euro, the Norwegian Krone (“NOK”), the British Pound (“GBP”) and the Brazilian Real (“BRL”), which could affect our earnings. We may use financial derivatives to hedge some of our currency exposures. Our use of financial derivatives involves certain risks, including the risk that losses on a hedged position could exceed the nominal amount invested in the instrument and the risk that the counterparty to the derivative transaction may be unable or unwilling to satisfy its contractual obligations, which could have an adverse effect on our results and cash flows.

•We are subject to the risks related to Macaw Energies' business which may not achieve anticipated profitability as expected or at all.

As of March 15, 2024, we have invested $18.2 million in Macaw Energies, our wholly owned subsidiary, focused on decarbonizing natural gas production through the monetization of flared gas. Macaw Energies has acquired ownership interests in MGAS Comercializadora de Gás Natural Ltda. (“MGAS”) and Logística e Distribuição de Gás S.A. (“LOGAS”). The value of our equity method investments are subject to a variety of risks, including, among others, the risks related to Macaw Energies’ business, such as the risks inherent in the compression of natural gas, risks associated to the effectiveness of Macaw Energies’ technology (flare to gas mobile kit or F2X), inability of Macaw Energies to identify new customers and enter into profitable contracts, inability of Macaw Energies to obtain sufficient financing for any new project it identifies, and other industry, regulatory, economic and political risks similar in nature to the risks faced by us.

•Our equity method investments may not result in sufficient profitability to justify our investment, and could lead to future impairment.

As of December 31, 2023, we held investments in Avenir, Aqualung Carbon Capture AS (“Aqualung”), Egyptian Company for Gas Services S.A.E. (“ECGS”), MGAS and LOGAS. The value of our investments and the income generated from our investments are subject to a variety of risks, including, among others, the inability of our investments to identify and enter into appropriate projects, inability of our investments to obtain sufficient financing for any project it identifies, failure of our investments’ current projects, and other industry, regulatory, economic and political risks impacting our investments’ operations. These may result in future impairment of our equity method investments which may have a material adverse effect on our results of operations in the period that the impairment charges may be recognized.

Risks related to our industry

•Our results of operations and financial condition depend on demand for natural gas, LNG, FLNGs and LNG carriers.

Our results of operations and financial condition depend on continued global and regional demand for LNG, FLNGs and LNG carriers, which could be negatively affected by several factors, including but not limited to geopolitical unrest or war, such as the conflicts in Ukraine and the Israel-Gaza region, fluctuations in natural gas, crude oil and petroleum product prices, changes in the cost and availability of natural gas relative LNG, global oversupply or insufficiency of natural gas liquefaction or receiving capacity.

Other potential risks include technological advancements in land-based regasification and liquefaction systems, developments in alternative floating liquefaction technologies, increase in low-cost natural gas production, expansions of pipeline systems, adverse economic or political conditions in LNG-consuming regions, regulatory changes, incidents involving LNG carriers or facilities, tax or regulatory burdens affecting LNG production, a rise in the number of available FLNGs and LNG carriers, interest rate increases, financing challenges for FLNG projects, and obstacles in obtaining governmental approvals or community acceptance. Any decline in demand for LNG, liquefaction, or transportation, or constraints on LNG production capacity, could have a material adverse effect on prevailing tolling fees, charter rates or the market value of our vessels, which could have a material adverse effect on our results of operations and financial condition.

12

•Our operations are subject to extensive and changing laws, regulations, reporting requirements and social attitudes towards fossil fuel, may have an adverse effect on our business.

Our operations are affected by extensive and changing laws, regulations, reporting requirements and stakeholders’ social attitudes that could create greater reporting obligations and compliance requirements, including those related to environmental protection, handling, use, disposal, and generation of hazardous substances, occupational health and safety, and other matters. We or our customers may be required to obtain permits, licenses, or other authorizations to operate under such laws, which could be costly and time-consuming. Additionally, compliance with these laws, regulations, treaties, conventions, and other requirements, may increase our costs, limit our operations or access to new opportunities or have an adverse effect on our business. Failure to comply can result in administrative and civil penalties, criminal sanctions or the suspension or termination of our operations, including, in certain instances, seizure or detention of our vessels.

•ESG and sustainability considerations may adversely impact our operations and markets.

There is an increasing focus from regulators and stakeholders related to ESG matters. The regulations requirements and stakeholder expectations continue to evolve and criteria used to evaluate ESG practices and metrics may change rapidly at any time, which could result in increased expectations and may cause us to undertake costly initiatives to satisfy any new requirements. Non-compliance with these emerging regulations or a failure to address stakeholder and societal expectations may result in potential cost increases, litigation, fines, penalties, production and sales restrictions, brand or reputational damage, loss of customers, failure to retain and attract talent, lower valuation and higher investor activism activities.

Further, adverse effects upon the oil and gas industry relating to climate change, including growing public concern about the environmental impact of climate change, may also influence demand for our services and could have a significant adverse financial and operational impact on our business that we cannot predict with certainty at this time. For example, 197 countries including Cameroon, Mauritania, Senegal, and the United States, have signed the United Nations-sponsored “Paris Agreement,” agreeing to limit their greenhouse gas (“GHG”) emissions through non-binding, individually determined reduction goals every five years after 2020. Further, in 2023 countries gathered at the 28th Conference of the Parties on the UN Framework Convention on Climate Change (“COP28”), where they entered into an agreement to transition away from fossil fuels in energy systems and increase renewable energy capacity, though no timeline for doing so was set. While non-binding, the agreements coming out of COP28 could result in increased pressure among financial institutions and various stakeholders to reduce or otherwise impose more stringent limitations on funding for and increase potential opposition to the production and use of fossil fuels.

While we may create and publish voluntary disclosures regarding ESG matters from time to time, many of the statements in those voluntary disclosures will be based on hypothetical expectations and assumptions that may or may not be representative of current or actual risks or events or forecasts of expected risks or events, including the costs associated therewith. Such expectations and assumptions are necessarily uncertain and may be prone to error or subject to misinterpretation given the long timelines involved and the lack of an established single approach to identifying, measuring, and reporting on many ESG matters. Additionally, while we may also announce various voluntary ESG targets in the near future, such targets are aspirational and we may not be able to meet such targets in the manner or on a timeline as initially contemplated.

In addition, the European Union’s CSRD that became effective in January 2023 significantly expands mandatory sustainability reporting in accordance with European Sustainability Reporting Standards (“ESRS”), for U.S. companies with operations in the EU. While CSRD rules are prescriptive for the types of data to be reported, the standards to quantify and qualify such data are still evolving and uncertain, and may impose increased costs on us related to complying with our reporting obligations and increase risks of non-compliance with ESRS and the CSRD. We are closely monitoring the rules and regulations related to CSRD and anticipate to fall under the CSRD's scope from 2025, with the initial reporting expected in 2026. Additionally, the Commission released its final rule on climate-related disclosures on March 6, 2024, requiring the disclosure of certain climate-related risks and financial impacts, as well as GHG emissions. Large accelerated filers such as us, will be required to incorporate the applicable climate-related disclosures into their filings beginning in fiscal year 2025, with additional requirements relating to the disclosure of Scope 1 and 2 GHG emissions, if material, and attestation reports for certain large accelerated filers subsequently phasing in. While we are still assessing our obligations under the rule, complying with such obligations may result in increased costs.

13

Risks related to our common shares

•The declaration and payment of dividends or repurchases of our own shares are at the discretion of our board of directors.

The declaration and payment of dividends to holders of our common shares or the repurchase of shares from holders of our common shares will be at the discretion of our board of directors in accordance with applicable law. In determining whether to declare and pay a dividend, or to repurchase our shares, our board of directors will take into account various factors, including actual results of operations, liquidity and financial condition, net cash provided by operating activities, restrictions imposed by applicable law and our debt agreements, our taxable income, our operating expenses, the share price, and other factors our board of directors deem relevant. There can be no assurance that we will resume the payment of dividends in amounts or on a basis consistent with prior distributions, if at all, or approve new share repurchase programs, or pursue share repurchases, even if such a program has been approved. Because we are a holding company and have no direct operations, we will only be able to pay dividends from our available cash on hand and any funds we receive from our subsidiaries and our ability to receive distributions from our subsidiaries may be limited by the financing agreements to which they are subject.

•Our common share price may be highly volatile and future sales of our common shares could cause the market price of our common shares to decline and could lead to a loss of all or part of a shareholder’s investment.

The market price of our common shares has fluctuated widely since they began trading on the NASDAQ Global Select Market (“Nasdaq”). We cannot assure that an active and liquid public market for our common shares will continue.