UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2023

ACT OF 1934

For the transition period from ______________ to _____________

Commission file number: 001-41252

(Exact name of registrant as specified in its charter)

| 7372 | ||||||||||||||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Number) | (IRS Employer Identification Number) | ||||||||||||

(Address of registrant’s principal executive offices) (Zip code)

Registrant’s telephone number, including area code (404 ) 806-9906

Securities registered under Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the issuer (1) has filed reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | |||||||||||

| x | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 USC. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The registrant’s Class A Common Stock began trading on the NASDAQ Stock Exchange on January 31, 2022. As of June 30, 2023, the aggregate market value held by non-affiliates of the registrant, computed by reference to the price at which the registrant’s Class A Common Stock was last sold on the NASDAQ Stock Exchange on such date was $9,543,000 (7,455,469 at a closing price per share of $1.28 on June 30, 2023). As of March 29, 2024, there were 10,101,279 shares of Class A Common Stock, par value $0.01 per share, of the registrant outstanding.

Documents Incorporated by Reference

None

| Auditor Name: | Auditor Location: | Auditor Firm ID: | ||||||||||||

T STAMP INC.

TABLE OF CONTENTS

2

Statement Regarding Forward-Looking Statements

This Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), that involve risks and uncertainties, as well as assumptions that, if they never materialize or prove incorrect, could cause our results to differ materially and adversely from those expressed or implied by such forward-looking statements. Forward-looking statements may include, but are not limited to, statements relating to our outlook or expectations for earnings, revenues, expenses, asset quality or other future financial or business performance, strategies, expectations or business prospects, or the impact of legal, regulatory or supervisory matters on our business, results of operations, or financial condition. Specifically, forward-looking statements may include statements relating to our future business prospects, revenue, income, and financial condition.

Forward-looking statements can be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “target,” or similar expressions. Forward-looking statements reflect our judgment based on currently available information and involve a number of risks and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements.

In addition to those factors discussed under Item 1A—“Risk Factors,” important factors could cause actual results to differ materially from our expectations. These factors include, but are not limited to:

•adverse economic conditions;

•general decreases in demand for our products and services;

•changes in timing of introducing new products into the market;

•intense competition (including entry of new competitors), including among competitors with substantially greater resources than us;

•inadequate capital;

•unexpected costs;

•revenues and net income lower than anticipated;

•litigation;

•becoming delisted from Nasdaq;

•the possible fluctuation and volatility of operating results and financial conditions;

•the impact of legal, regulatory, or supervisory matters on our business, results of operations, or financial condition;

•inability to carry out our marketing and sales plans; and

•the loss of key employees and executives.

All forward-looking statements included in this Form 10-K speak only as of the date of this Form 10-K and you are cautioned not to place undue reliance on any such forward-looking statements. Except as required by law, we undertake no obligation to publicly update or release any revisions to these forward-looking statements to reflect any events or circumstances that arise after the date of this Form 10-K or to reflect the occurrence of unanticipated events. The above list is not intended to be exhaustive and there may be other factors that could preclude us from realizing the predictions made in the forward-looking statements. We operate in a continually changing business environment and new factors emerge from time to time. We cannot predict such factors or assess the impact, if any, of such factors on our financial position or results of operations.

In this Annual Report on Form 10-K, unless the context indicates otherwise, the terms “Trust Stamp”, the “Company”, “we”, “us”, and “our” refer to T Stamp, Inc., a Delaware corporation.

3

PART I.

Item 1. Our Business

Overview

Trust Stamp was incorporated under the laws of the State of Delaware on April 11, 2016 as “T Stamp Inc.” T Stamp Inc. and its subsidiaries (“Trust Stamp”, “we”, or the “Company”) develop and market identity authentication software for enterprise and government partners and peer-to-peer markets.

Trust Stamp develops proprietary artificial intelligence-powered identity and trust solutions at the intersection of biometrics, privacy, and cybersecurity, that enable organizations to protect themselves and their users while empowering individuals to retain ownership of their identity data and prevent fraudulent activity using their identity.

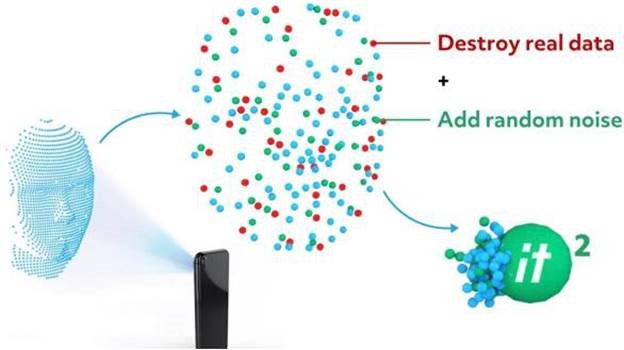

Trust Stamp tackles industry challenges including data protection, regulatory compliance, and financial accessibility, with cutting-edge technology including biometric science, cryptography, and machine learning. Our core technology irreversibly transforms identity information to create tokenized identifiers that enable accurate authentication while minimizing the need to store or share sensitive data. By retaining the usefulness of biometric-derived data while minimizing the risk, we allow businesses to adopt biometrics and other anti-fraud initiatives while protecting personal information from hacks and leaks.

Trust Stamp’s key sub-markets are identity authentication for the purpose of account opening, access, and fraud detection, the creation of tokenized digital identities to facilitate financial and societal inclusion, and in-community case management software for alternatives to detention and other governmental uses.

As biometric solutions proliferate, so does the need to protect biometric data. Stored biometric images and templates represent a growing and unquantified financial, security, and PR liability and are the subject of governmental, media, and public scrutiny since biometric data cannot be “changed” once they are hacked, as they are directly linked to the user’s physical features and/or behaviors. Privacy concerns around biometric technology have led to close attention from regulators, with multiple jurisdictions placing biometrics in a special or sensitive category of personal data and demanding much stronger safeguards around collection and safekeeping.

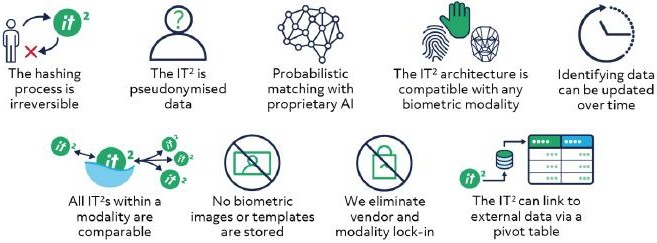

To address this unprecedented danger and increased cross-industry need to establish trust quickly and securely in virtual environments, Trust Stamp has developed its Irreversibly Transformed Identity Token, or IT2TM, solutions, which replace biometric templates with a cryptographic hash that can never be rebuilt into the original data and cannot be used to identify the subject outside the environment for which it is designed.

Trust Stamp’s data transformation and comparison technology is vendor and modality-agnostic, allowing organizations including other biometric services providers to benefit from the increased protection, efficiency, and utility of our proprietary tokenization process. With online and offline functionality, Trust Stamp technology is effective in even the most remote locations in the world.

Trust Stamp also offers end-to-end solutions for multi-factor biometric authentication for account access and recovery, KYC/AML compliance, customer onboarding, and more, which allow organizations to approve more genuine users, keep bad actors from accessing systems and services and retain existing users with a superior user experience.

Markets

Trust Stamp has evaluated the market potential for its services in part by reviewing the following reports, articles, and data sources, none of which were commissioned by the Company, and none of which are to be incorporated by reference:

Data Security and Fraud

•In 2022, 4,145 publicly disclosed breaches exposed over 22 billion records according to the “2021 Year End Report: Data Breach QuickView” published by Flashpoint.

•The cumulative merchant losses to online payment fraud between 2023 and 2027 will exceed $343 billion globally according to a 2022 report titled “Fighting Online Payment Fraud in 2022 & Beyond” published by Juniper Research.

4

Trust Stamp addresses this market with biometric identity verification and biometric authentication solutions — which offer Trust Stamp’s proprietary irreversible identity token to perform biometric-based matching in a secure and tokenized domain, matching tokenized personally identifiable information while implementing liveness detection.

Biometric Authentication

•By 2027, the value of biometrically authenticated remote mobile payments will reach $1.2 trillion globally, according to a 2022 report titled “Mobile Payment Biometrics” published by Juniper Research.

•The global biometric system market size is valued at $41.1 billion per annum in 2023, with a forecast compound growth of 20.4% from 2023 to 2030 with a 2030 revenue forecast of $150.6 billion according to the 2023 report titled “Biometric Technology Market Size, Share & Trends Analysis Report By Component, By Offering, By Authentication Type, By Application, By End-use, By Region, And Segment Forecasts, 2023 — 2030” published by Grand View Research.

Trust Stamp addresses this market through its biometric authentication and liveness detection products — which offer Trust Stamp’s proprietary irreversible identity token to perform biometric matching in a secure and tokenized domain. This permits biometric authentication without the risk of storing pictures and biometric templates.

Financial and Societal Inclusion

•As of 2021, 1.4 billion people were unbanked according to the “Global Findex Database 2021” published by The World Bank.

•131 million small and medium-sized enterprises in emerging markets lack access to finance, limiting their ability to grow and thrive (UNSGSA Financial Inclusion Webpage, Accessed March 2023).

•The global market for Microfinance is estimated at $157 Billion in the year 2020, and is projected to reach $342 billion by 2026 according to the 2022 report titled “Microfinance - Global Market Trajectory & Analytics” published by Global Industry Analysts, Inc.

Trust Stamp’s biometric authentication, liveness detection, and information tokenization enable individuals to verify and establish their identities using data derived from biometrics. While individuals in this market lack traditional means of identity verification, Trust Stamp provides a means to authenticate identity that preserves an individual’s privacy and control over that identity.

Alternatives to Detention (“ATD”)

•The ATD market includes Federal, State, and Municipal agencies for both criminal justice and immigration purposes. Trust Stamp addresses the ATD market with applications built on Trust Stamp’s privacy-preserving solutions allowing individuals to comply with ATD requirements using ethical and humane technology methodologies. Trust Stamp has developed innovative patented technologies for use in the ATD market encompassing biometrics, geolocation, and tokenization as well as a proprietary, tamper-resistant, battery-free “Tap-In-Band” that can complement or replace biometric check-in requirements and provide a lower-cost and more humane alternative to traditional “ankle bracelet” technology.

In addition to its key sub-markets, the Company is developing products and working with partners and industry organizations in other sectors that offer significant market opportunities, in particular, the travel, healthcare, Metaverse platform and cryptographic key and account credential safekeeping sectors. For example, the Company has developed a “crypto key vault” solution that leverages proven facial biometric authentication and irreversible data transformation technology to protect private keys for digital assets while ensuring long-term data protection and access credential availability.

Principal Products and Services

Trust Stamp’s most important technology is the Irreversibly Transformed Identity TokenTM (also known as the IT2 TM, Evergreen HashTM, EgHashTM and MyHashTM) combined with a data architecture that can use one or multiple sources of biometric or other identifying data. Once a “hash translation” algorithm is created, like-modality hashes are comparable regardless of their origin. The IT2 protects against system and data redundancy, providing a lifelong “digital-DNA” that can store (or pivot to) any type of KYC or relationship data with fields individually hashed or (salted and) encrypted,

5

facilitating selective data sharing. Products utilizing the IT2 are Trust Stamp’s primary products, accounting for the majority of its revenues during the year ended December 31, 2023.

We adhere to the best practices outlined in the National Institute of Standards and Technology (“NIST”) and International Organization for Standardization (“ISO”) frameworks, and our policies and procedures in managing personally identifiable information (“PII”) comply with General Data Protection Regulation (“GDPR”) requirements wherever such requirements are applicable.

IT2 Solutions

The IT2 replaces biometric templates and scans with meaningless numbers, letters, and symbols to remove sensitive data from the reach of criminals using a proprietary process by which a deep neural network irreversibly converts biometric and other identifying data, from any source, into the secure tokenized identity. This IT2 is unique to the user, is different every time it is generated from a live subject, and cannot be reverse-engineered and rebuilt into the user’s face or other original identity data.

Each token can be stored and compared to all other tokens from the same modality, allowing the Company’s AI-powered analytics to predict if a single subject has generated two or more tokens, even if the subject has passed conventional KYC with, e.g., falsified identity documents. Using this technology, an IT2 can be employed for re-authentication purposes, including account recovery, password-less login, new account creation, and more, across the organization or even within a consortium of organizations, all in a low-cost and low-friction delivery that is fast and secure.

Our technology is being used for enhanced due diligence, KYC/AML compliance, synthetic identity fraud reduction and “second chance” approval for customer onboarding and account access, together with the delivery of humanitarian and development services. The solution allows organizations to approve more users, keep bad actors from accessing systems and services, and retain existing users with a superior user experience.

6

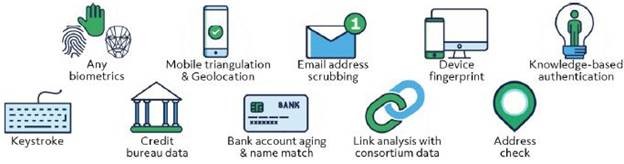

Our hashing and matching technology can maximize the effectiveness of all types of identity data while rendering it safer to use, store, and share. Whatever the source of identity data, it can be stored and compared as an IT2. See the chart below for examples.

Distribution

Through licensing we allow customers to utilize our technology in a wide variety of applications. Uses can include (e.g.):

•The provision of services and hashing to enterprises, NGOs, and government, to overlay on third-party biometric and identity data.

•Hash licensing, translation, and certification services for biometric vendors.

•Management of zero-knowledge-proof services, whether as a tributary between Identity Lakes or operating consortium lakes.

•Tokenized identity creation for large scale deployments, such as humanitarian and government identity programs.

Licensing Agreements

License agreements are typically a hosted offering, on-premise solution, or both pursuant to which the customer pays for the initial product development plus a license fee for the use of Trust Stamp’s technologies on a periodic and/or volume-based basis. In addition to consuming and paying for Trust Stamp’s services for their own use, some key customers also serve as channel partners by offering Trust Stamp products to their own customer base, whether as stand-alone products, or integrated into their own services as upgraded product offerings.

SaaS Agreements

Software-as-a-Service ("SaaS") agreements are typically serviced through the Company’s Orchestration Layer platform, which is being utilized in new global identity authentication system with Fidelity Information Services, LLC ("FIS"). The platform includes our proprietary tokenization technology and is designed to provide easy integration with and access to, Trust Stamp’s products, chargeable on a per-use basis. The Orchestration Layer facilitates no-code and low-code implementations, making adoption faster and even more cost-effective for a broader range of potential customers. It is expected to accelerate the Company’s evolution, from being exclusively a custom solutions provider, to also offering a modular and highly scalable SaaS model with low-code implementation.

Competition

We can potentially work with any identity data from any source, potentially breaking vendor and modality lock-in, but our primary market target is the biometric service industry, which is growing exponentially while being threatened by a consumer, media, and legislative backlash against storing biometric data. The IT2 can potentially be overlaid on any biometric or other identity data provider.

In general, we compete for customer budget with any company in the identity authentication industry. Major competitors in this space include companies such as NEXT Biometrics, IDEMIA, Synaptics, Cognitec, Innovatrics, Suprema, FaceTec, Rank One Computing, Acuant, Jumio, Onfido, Ping, and Mitek. However, we believe that, due to the uniqueness of our technology solution, the Company does not currently have any direct competitors for the core IT2 solutions upon which the growth in our business plan is focused.

The commercial advantage of our solution is our ability to work across providers and modalities and we continue to pursue a first-mover advantage including our global–scale partnership which is achieving a network effect in the global

7

Humanitarian and Development market. We believe that this combination will make it unattractive for a potential competitor to replicate the six-years and multi-million dollars that we have already expended, to try and circumvent our multiple (and continuing) patent filings and/or offer a parallel product based upon a different technology.

We believe that given sufficient time and resources, we can augment any biometric modalities including face, hand, iris, voice, gait, and behavior, together with any other identifying data which places us in a unique position versus providers of biometric services.

We are unaware of any other provider being able to offer or support a proliferation of authentication modalities in this fashion, and therefore we believe there are no other companies that directly compete with us in this space. If our go-to-market strategy is successful, biometric service providers can be channel distributors, and not necessarily competitors.

Growth Strategy

Our strategy is to:

•Expand the scope and range of services that we provide to and through our existing clients.

•Continue to add significant new clients for our current and future services.

•Offer our services via channel partners with substantial distribution networks.

•Offer our technology on a “low code” basis, providing access via an orchestration layer and/or open-APIs to enable implementation by a broader range of clients.

•The addition of alternate authentication tools including non-facial-biometric options and non-biometric-knowledge and device-based tools facilitating two and multi-factor authentication.

•Offer our IT2 technology for use by other biometric and data services providers to protect and extend the usability of their data.

•Provide ready-to-use / customizable platforms that leverage our IT2 technology in specialized markets.

Human Capital

Given the geographic diversity of its team, and to facilitate cost-effective administration, Trust Stamp secures the services of its permanent team members through a variety of administrative structures that include wholly owned subsidiaries, professional employer organizations, and consulting contracts. As of December 31, 2023, the Company had 14 full-time and 1 part-time team member that works out of the United States, 26 full-time members and 1 part-time team member that work out of Malta, 10 full-time team members in Poland and Central Europe, 1 full-time and 4 part-time team members in the United Kingdom, 1 full-time team member in the Isle of Man, 14 full-time team members and 2 part-time team members working in the Philippines, 11 full-time team members working in Rwanda, 2 full-time team members in Denmark, and 1 full-time team member working remotely in India. Our permanent team is augmented as needed by contract development and other staff on both a long and short-term basis.

Outsourcing

We design and develop our own products. We use an outsourcing company, 10Clouds, for additional development staff as needed. 10Clouds is considered a related party. In addition, we also utilize SourceFit, a company in the Philippines, for PEO services, representing approximately 2% of our operating expenses during the year ended December 31, 2023. Amazon Web Services provides cloud hosting and processing services, representing approximately 3% of our operating expenses during the year ended December 31, 2023.

Key Customers

The Company’s initial business consisted of developing proprietary privacy-first identity solutions and then implementing them through custom applications built and maintained for a small number of key customers. In 2022, the Company added to its product offerings a modular and highly scalable SaaS model with low-code or no implementation (“the Orchestration Layer”). Although the Company remains open to significant opportunities to deliver custom solutions, sales of Orchestration Layer products are the primary focus of the Company’s sales and development initiatives. This strategic pivot in the Company’s go-to-market approach negatively impacted revenue in 2023 while we believe that it will substantially increase potential revenue in 2024 and thereafter.

8

Historically, the Company generated most of its income through two long-term partnerships, comprising a relationship with an S&P 500 bank with services provided pursuant to a Master Software Agreement entered into in 2017, together with a relationship with Mastercard International (“Mastercard”) with services provided under the terms of a ten-year technology services agreement entered into in March 2019 (the "TSA”). Both of those relationships remain strong, and the Company anticipates future revenue growth from the two relationships.

Under the TSA, IT2 TM technology is being implemented by Mastercard for Humanitarian & Development purposes as a core element of its Community Pass and Inclusive Identity offerings. Use cases include not only financial services for individuals and businesses but also empowering people and communities to meet basic needs, such as nutritious food, clean water, housing, education, and healthcare. The Company is paid to develop and host software solutions utilizing the IT2 and to support Mastercard’s implementations. In addition, the Company is paid on a “per user per year” basis for all transactions utilizing its technology. In December of 2022, the Company entered into a modification of the agreed pricing schedule with Mastercard to move from a per-use to a per-user-year model to broaden the range of potential use cases. The TSA may be terminated by either party in the event of a material breach by the other party that remains uncured within thirty days after notice is received of such a breach. Either party may terminate the TSA if the other party becomes, including, but not limited to, insolvent, subject to bankruptcy, dissolved, or liquidated. Unless the TSA is terminated, the TSA will automatically renew for additional one year-periods in perpetuity unless either party provides ninety days written notice of intent not to renew. To date, the Company has received guaranteed minimum annual payments on account of usage. According to the October 2023 interview of Mastercard Executive Vice President and Founder of the Community Pass from the article titled “Mastercard’s Community Pass founder says digital ID platform improving lives, digital inclusion” published by Biometric Update. Mastercard’s Community Pass program currently serves approximately 3.5 million users and is targeting 30 million users by 2027. Based upon information provided to us by Mastercard we anticipate user-based revenue starting in 2024 and growing year-on-year thereafter.

In 2022, the Company expanded its key customer base to include a relationship with FIS, a relationship-focused upon the implementation of our Orchestration Layer and underlying technologies in FIS’ Global KYC product offering.

The Orchestration Layer is a low-code platform that is designed to be a one-stop shop for Trust Stamp services and provides easy integration to our products; chargeable on a per-use basis. The Orchestration Layer utilizes the Company’s next-generation identity package, offering rapid deployment across devices and platforms, with custom workflows that seamlessly orchestrate trust across the identity lifecycle for a consistent user experience in processes for onboarding and KYC/AML, multi-factor authentication, account recovery, fraud prevention, compliance, and more. The Orchestration Layer facilitates no-code and low-code implementations of the Company’s technology making adoption and updating faster and cost-effective for a broader range of potential customers.

In the third quarter of 2022, the Company acquired its first 2 new customers on the Orchestration Layer through its partnership with FIS, and in the fourth quarter of 2022, 4 additional FIS customers onboarded. As of December 31, 2023, a total of 40 financial institutions with over $327 billion in assets have been onboarded via FIS, bringing the total number of (FIS and non-FIS) customers either fully implemented or are currently implementing the Orchestration Layer to 43. The first (non-FIS) client onboarded to the Orchestration Layer in the third quarter of 2022 has generated $233 thousand of revenue for the Company to date including $182 thousand during the year ended December 31, 2023. Although each of the institutions onboarded via FIS pays a small onboarding fee, given the typical time taken by a financial institution to test, implement, and roll out any new technology, the Company does not anticipate significant revenue from the new FIS customers until 2024.

Reinforced by the product-market fit indicated by the FIS roll-out, the Company is building an internal direct sales force to offer the Orchestration Layer to non-FIS institutions. A key criterion for the account executives recruited is possessing significant experience and a successful track record in the identity solutions market. The Company anticipates significant banked revenue in 2024.

In Management's opinion, while the unanticipated loss of any one of our current customers, including our channel partnership with FIS, could have an adverse effect on the Company’s financial position, it would not prevent us from continuing our operations.

Regulation

Our business is not currently subject to any licensing requirements in any jurisdiction in which we operate, other than the requirement to hold a business license in the City of Atlanta (with which we are in compliance), and the requirement to

9

hold a trading license in Rwanda (with which we are in compliance). Given the significant focus on the use of biometrics in many countries, we do anticipate additional regulation being introduced in one or more jurisdictions in which we operate, and such requirements could be burdensome and/or expensive or even impose requirements that we are unable to meet.

We are subject to substantial governmental regulation relating to our technology and will continue to be for the lifetime of our Company. By virtue of handling sensitive PII and biometric data, we are subject to numerous statutes related to data privacy, and additional legislation and given the current focus on the collection, storage, and use of biometrics, additional regulation should be anticipated in every jurisdiction in which we operate. Examples of American and European federal statutes we could be subject to are:

•Health Insurance Portability and Accountability Act (HIPAA)

•Health Information Technology for Economic and Clinical Health Act (HITECH)

•The General Data Protection Regulation 2016/679 (GDPR)

•ePrivacy Privacy Directive

•The California Privacy Rights Act (CPRA)

•The California Consumer Privacy Act (CCPA)

•Biometric Information Privacy Act (BIPA)

HIPAA and HITECH

Under the administrative simplification provisions of the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”), as amended by the Health Information Technology for Economic and Clinical Health Act “HITECH”), the U.S. Department of Health and Human Services (“HHS”) issued regulations that establish uniform standards governing the conduct of certain electronic healthcare transactions and requirements for protecting the privacy and security of protected health information (“PHI”), used or disclosed by covered entities and business associates. Covered entities and business associates are subject to HIPAA and HITECH. Our subcontractors that create, receive, maintain, transmit, or otherwise process PHI on behalf of us are HIPAA “business associates” and must also comply with HIPAA as a business associate.

HIPAA and HITECH include privacy and security rules, breach notification requirements, and electronic transaction standards.

The privacy rules cover the use and disclosure of PHI by covered entities and business associates. The privacy rules generally prohibit the use or disclosure of PHI, except as permitted under certain limited circumstances. The privacy rules also set forth individual patient rights, such as the right to access or amend certain records containing his or her PHI, or to request restrictions on the use or disclosure of his or her PHI.

The security rules require covered entities and business associates to safeguard the confidentiality, integrity, and availability of electronically transmitted or stored PHI by implementing administrative, physical, and technical safeguards. Under HITECH’s Breach Notification Rule, a covered entity must notify individuals, the Secretary of the HHS, and in some circumstances, the media of breaches of unsecured PHI.

In addition, we may be subject to state health information privacy and data breach notification laws, which may govern the collection, use, disclosure, and protection of health-related and other personal information. State laws may be more stringent, broader in scope, or offer greater individual rights with respect to PHI than HIPAA, and state laws may differ from each other, which may complicate compliance efforts.

Entities that are found to be in violation of HIPAA as the result of a failure to secure PHI, a complaint about our privacy practices, or an audit by HHS, may be subject to significant civil and criminal fines and penalties and additional reporting and oversight obligations if such entities are required to enter into a resolution agreement and corrective action plan with HHS to settle allegations of HIPAA non-compliance.

GDPR

The European Union's General Data Protection Regulation ("GDPR") imposes onerous accountability obligations requiring data controllers and processors to maintain a record of their data processing and policies. It requires data controllers to implement more stringent operational requirements for processors and controllers of personal data, including, for example,

10

transparent and expanded disclosure to data subjects (in a concise, intelligible, and easily accessible form) about how their personal information is being used, imposes limitations on retention of information, increases requirements pertaining to health data and pseudonymized (i.e., key-coded) data, introduces mandatory data breach notification requirements, and sets higher standards for data controllers to demonstrate that they have obtained valid consent for certain data processing activities. Fines for non-compliance with the GDPR will be significant—the greater of €20 million or 4% of global turnover. The GDPR provides that European Union member states may introduce further conditions, including limitations, to make their own further laws and regulations limiting the processing of genetic, biometric, or health data.

ePrivacy Directive

The ePrivacy directive sets out the rules relating to the processing of personal data across public communications networks. This directive requires businesses to ensure consent requests are made and that consent is received from the user before the use of cookies is made. Businesses must communicate the privacy rules with accurate and specific information regarding the data contained in the cookie. Information must be communicated before the consent requests are made, in plain language. Organizations must ensure that users are able to withdraw consent in the same simple manner as the initial consent request.

CPRA and CCPA

The California Privacy Rights Act ("CPRA") and the California Consumer Privacy Act ("CCPA") define and establish various rights that consumers residing in California have over the privacy of their data along with the responsibilities of businesses when collecting personal information. It requires businesses that control the collection of consumers’ personal information to inform them of the category, purpose, and duration the business intends to retain such information. It lists the consumers’ right to correct their data and have their data deleted. Customers may also exercise their right to limit the sale or sharing of their personal or sensitive personal information. Fines for non-compliance can range from $100 to $750 per consumer per incident. Additionally, in certain cases, the California Privacy Protection Agency may impose administrative fines ranging from $2,500 to $7,500 for each violation.

BIPA

The Biometric Information Privacy Act ("BIPA"), which was enacted in 2008, addresses the collection, use, and retention of biometric information by private entities. Under the law, a private entity must inform an individual, or their legally authorized individual, that the biometric information is being collected and stored, and the specific purpose and the length of time for the collection, storage, and use of the biometric information, before obtaining or possessing their biometric information for the purposes of capturing, storing or sharing it. In addition, prior to collecting any biometric information, the regulation required businesses to obtain a written release for the collection of the biometric information from the individual, or the individual’s legally authorized representative after notice has been given. BIPA provides statutory damages of up to $1,000 for each negligent violation, and up to $5,000 for each intentional or reckless violation.

Intellectual Property

Patents

A summary of the Company’s issued patents and pending patent applications on April 1, 2024 is provided in the table below.

| Matter No. | Application/ Patent No. | Filing/ Issue Date | Title | Priority Information | Status | ||||||||||||

32742-162494 | 63/652,521 | 03/07/2024 | LOSSLESS FUZZY EXTRACTORS | - | PENDING 03/24/2025 Non-Provisional Conversion Deadline | ||||||||||||

32742-160139 | 63/611,799 | 12/19/2023 | LOSSLESS FUZZY EXTRACTORS | - | PENDING 12/19/2024 Non-Provisional Conversion Deadline | ||||||||||||

11

| Matter No. | Application/ Patent No. | Filing/ Issue Date | Title | Priority Information | Status | ||||||||||||

32742-161077 | 18/524,536 | 11/30/2023 | SYSTEMS AND PROCESSES FOR LOSSY BIOMETRIC REPRESENTATIONS | 16/841,269 | PENDING Awaiting Examination | ||||||||||||

32742-159767 | 63/581,409 | 09/08/2023 | MULTI-FACTOR AUTHENTICATION USING TAMPER-PROOF BAND AND BIOMETRIC DATA | - | PENDING 09/08/2024 Non-Provisional Conversion Deadline | ||||||||||||

32742-158589 | 63/520,388 | 08/18/2023 | SEMI-SUPERVISED OR UNSUPERVISED BIOMETRIC PERSON RECOGNITION | - | PENDING 08/18/2024: Non-Provisional Conversion Deadline | ||||||||||||

| 32742-154085 | 18/164,090 | 02/03/2023 | METAPRESENCE SYSTEMS AND PROCESSES FOR USING SAME | 63/306,210 63/327,821 | PENDING Awaiting Examination | ||||||||||||

| 32742-145300 | 18/145,470 | 12/22/2022 | SYSTEMS AND PROCESSES FOR MULTIFACTOR AUTHENTICATION AND IDENTIFICATION | 17/230,684 (Continuation-in-Part) | PENDING Awaiting Examination | ||||||||||||

| 32742-153794 | 18/063,372 | 12/08/2022 | SHAPE OVERLAY FOR PROOF OF LIVENESS | 63/287,276 | PENDING Awaiting Examination | ||||||||||||

| 32742-148653 | 17/725,978 | 04/21/2022 | INTEROPERABLE BIOMETRIC REPRESENATION | 63/177,494 | PENDING Awaiting Examination | ||||||||||||

| 32742-151107 | 17/849,196 | 06/24/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 16/855,606 | PENDING Awaiting Examination | ||||||||||||

| 32742-149248 | 17/745,270 | 05/16/2022 | SECURE REPRESENTATIONS OF AUTHENTICITY AND PROCESSES FOR USING SAME | 63/188,491 | PENDING Awaiting Examination | ||||||||||||

| 32742-147982 | 17/719,975 | 04/13/2022 | PERSONALLY IDENTIFIABLE INFORMATION ENCODER | 63/174,405 | PENDING Awaiting Examination | ||||||||||||

| 32742-147631 | 17/706,132 | 03/28/2022 | SYSTEMS AND METHODS FOR LIVENESS-VERIFIED IDENTITY AUTHENTICATION | 16/403,093 | PENDING 04/15/2024 Response to Final Office Acton Due (extendible 2 months) | ||||||||||||

| 32742-145019 | 17/401,504 | 08/13/2021 | SYSTEMS AND METHODS FOR LIVENESS-VERIFIED, BIOMETRIC-BASED ENCRYPTION | 62/667,133 | PENDING 04/12/2024 Issue Fee Due | ||||||||||||

| 32742-142186 | 17/230,684 | 04/14/2021 | SYSTEMS AND PROCESSES FOR MULTIMODAL BIOMETRICS | 63/009,809 63/011,447 | ABANDONED | ||||||||||||

| 32742-141508 | 17/205,713 | 03/18/2021 | SYSTEMS AND PROCESSES FOR TRACKING HUMAN LOCATION AND TRAVEL VIA BIOMETRIC HASHING | 62/991,352 | ABANDONED | ||||||||||||

| 32742-142411 | 17/324,544 | 05/19/2021 | FACE COVER-COMPATIBLE BIOMETRICS AND PROCESSES FOR GENERATING AND USING SAME | 63/027,072 | ALLOWED 05/22/2024 Issue Fee Payment Due | ||||||||||||

12

| Matter No. | Application/ Patent No. | Filing/ Issue Date | Title | Priority Information | Status | ||||||||||||

| 32742-149163 | 17/702,355 11,886,618 | 03/23/2022 01/30/2024 | SYSTEMS AND PROCESSES FOR LOSSY BIOMETRIC REPRESENTATIONS | 16/841,269 | ISSUED 06/30/2028: First Maintenance Fee Due | ||||||||||||

| 32742-145020 | 17/401,508 11,729,263 | 08/13/2021 08/15/2023 | SYSTEMS AND METHODS FOR IDENTITY VERIFICATION VIA THIRD PARTY ACCOUNTS | 62/486,210 | ISSUED 02/15/2027: First Maintenance Fee Due | ||||||||||||

| 32742-149165 | 17/702,366 11,741,263 | 03/23/2022 08/29/2023 | SYSTEMS AND PROCESSES FOR LOSSY BIOMETRIC REPRESENTATIONS | 16/841,269 | ISSUED 02/28/2027: First Maintenance Fee Due | ||||||||||||

| 32742-130397 | 16/406,978 11,496,315 | 05/08/2019 11/28/2022 | SYSTEMS AND METHODS FOR ENHANCED HASH TRANSFORMS | 62/668,610 | ISSUED 05/08/2026: First Maintenance Fee Due | ||||||||||||

| 32742-130398 | 16/403,093 11,288,530 | 05/03/2019 03/29/2022 | SYSTEMS AND METHODS FOR LIVENESS-VERIFIED IDENTITY AUTHENTICATION | 62/667,130 | ISSUED 09/29/2025: First Maintenance Fee Due | ||||||||||||

| 32742-118398 | 15/342,994 10,924,473 | 11/03/2016 02/16/2021 | TRUST STAMP | 62/253,538 | ISSUED 08/16/2024: First Maintenance Fee Due | ||||||||||||

| 32742-123473 | 15/955,270 11,095,631 | 04/17/2018 08/17/2021 | SYSTEMS AND METHODS FOR IDENTITY VERIFICATION VIA THIRD PARTY ACCOUNTS | 62/486,210 | ISSUED 02/17/2025: First Maintenance Fee Due | ||||||||||||

| 32742-136046 | 16/855,576 11,263,439 | 04/22/2020 03/01/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 15/782,940 | ISSUED 09/01/2025 First Maintenance Fee Due | ||||||||||||

| 32742-136047 | 16/855,580 11,244,152 | 04/22/2020 02/08/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 15/782,940 | ISSUED 08/08/2025 First Maintenance Fee Due | ||||||||||||

| 32742-136048 | 16/855,588 11,263,440 | 04/22/2020 03/01/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 15/782,940 | ISSUED 09/01/2025: First Maintenance Fee Due | ||||||||||||

| 32742-136049 | 16/855,594 11,263,441 | 04/22/2020 03/01/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 15/782,940 | ISSUED 09/01/2025: First Maintenance Fee Due | ||||||||||||

| 32742-136050 | 16/855,598 11,263,442 | 04/22/2020 03/01/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 15/782,940 | ISSUED 09/01/2025: First Maintenance Fee Due | ||||||||||||

| 32742-136051 | 16/855,606 11,373,449 | 04/22/2020 06/28/2022 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 15/782,940 | ISSUED 12/28/2025 First Maintenance Fee Due | ||||||||||||

13

| Matter No. | Application/ Patent No. | Filing/ Issue Date | Title | Priority Information | Status | ||||||||||||

| 32742-130399 | 16/403,106 11,093,771 | 05/03/2019 08/17/2021 | SYSTEMS AND METHODS FOR LIVENESS-VERIFIED, BIOMETRIC-BASED ENCRYPTION | 62/667,133 | ISSUED 02/17/2025: First Maintenance Fee Due | ||||||||||||

| 32742-135668 | 16/841,269 11,301,586 | 04/06/2020 04/12/2022 | SYSTEMS AND PROCESSES FOR LOSSY BIOMETRIC REPRESENTATIONS | 62/829,825 | ISSUED 10/12/2025 First Maintenance Fee Due | ||||||||||||

| 32742-118149 | 15/782,940 10,635,894 | 10/13/2017 04/28/2020 | SYSTEMS AND METHODS FOR PASSIVE-SUBJECT LIVENESS VERIFICATION IN DIGITAL MEDIA | 62/407,717 62/407,852 62/407,693 | ISSUED 10/28/2027: Second Maintenance Fee Due | ||||||||||||

| 32742-152907 | 17/966,355 11,681,787 | 10/14/2022 06/20/2023 | OWNERSHIP VALIDATION FOR CRYPTOGRAPHIC ASSET CONTRACTS USING IRREVERSIBLY TRANSFORMED IDENTITY TOKENS | 63/256,347 | ISSUED 12/20/2026: First Maintenance Fee Due | ||||||||||||

| 32742-139681 | 17/109,693 11,711,216 | 12/02/2020 07/25/2023 | SYSTEMS AND METHODS FOR PRIVACY-SECURED BIOMETRIC IDENTIFICATION AND VERIFICATION | 62/942,311 | ISSUED 01/25/2027: First Maintenance Fee Due | ||||||||||||

| 32742-149164 | 17/702,361 11,861,043 | 03/23/2022 01/02/2024 | SYSTEMS AND PROCESSES FOR LOSSY BIOMETRIC REPRESENTATIONS | 16/841,269 | ISSUED 07/02/2027 First Maintenance Fee Due | ||||||||||||

| 32742-153065 | 17/956,190 11,936,790 | 09/29/2022 03/19/2024 | SYSTEMS AND METHODS FOR ENHANCED HASH TRANSFORMS | 16/406,978 | ISSUED 09/20/2027: First Maintenance Fee Due | ||||||||||||

14

Trademarks

The following is a summary of Trust Stamp’s issued and pending Trademarks as of April 1, 2024.

| Serial / Registration Number | Filing Date | Trademark | Country | Status | ||||||||||

98/379,747 N/A | 1/29/2024 | THE PRIVACY FIRST IDENTITY COMPANY | US | PENDING APPLICATION | ||||||||||

97/892,087 N/A | 04/17/2023 N/A | TRUSTED CHAT | US | PENDING APPLICATION Statement of Use or Request for Extension Due: 04/17/2024 | ||||||||||

97/894,011 N/A | 04/18/2023 N/A |  | US | PENDING Statement of use or Request for Extension Due: 04/17/2024 | ||||||||||

| 97/613,025 N/A | 06/29/2022 N/A | ALTERNATIVES TO DETENTION | US | PENDING APPLICATION Statement of use or Request for Extension Due: 04/17/2024 | ||||||||||

| 97/276,185 N/A | 02/21/2022 N/A | PRIVTECH | US | PENDING APPLICATION Statement of Use Due: 05/08/2024 | ||||||||||

| 97/276,205 N/A | 02/21/2022 N/A | PRIVTECH CERTIFIED | US | PENDING APPLICATION Statement of Use Due: 06/13/2024 | ||||||||||

| 97/276,214 N/A | 02/21/2022 N/A | THE PRIVACY-FIRST IDENTITY COMPANY | US | PENDING APPLICATION Statement of Use Due: 07/17/2024 | ||||||||||

| 87/411,586 5,329,048 | 04/14/2017 11/07/2017 | TRUST STAMP | US | REGISTERED Section 8 & 15 Renewal Filed: 10/24/2023 | ||||||||||

| 87/852,642 5,932,877 | 03/27/2018 12/10/2019 | TRUSTED MAIL | US | REGISTERED Section 8 & 15 Renewal Due: 12/10/2025 | ||||||||||

| 88/256,534 6,103,860 | 01/10/2019 07/14/2020 | IDENTITY LAKE | US | REGISTERED Section 8 & 15 Renewal Due: 07/14/2026 | ||||||||||

| 88/708,795 6,252,645 | 11/27/2019 01/19/2021 | MYHASH | US | REGISTERED Section 8&15 Renewal Due: 01/19/2027 | ||||||||||

| 88/709,274 6,252,649 | 11/27/2019 01/19/2021 | TRUSTED PRESENCE | US | REGISTERED Section 8&15 Renewal Due: 01/19/2027 | ||||||||||

| 90/041,950 6,494,610 | 07/08/2020 09/21/2021 | TRUSTED PAYMENTS | US | REGISTERED Section 8 & 15 Renewal Due: 09/21/2027 | ||||||||||

| 88/674,108 6,775,329 | 10/30/2019 06/28/2022 | TRUSTCARD | US | REGISTERED Section 8 & 15 Renewal Due: 06/28/2028 | ||||||||||

| 97/101,273 6,965,728 | 10/31/2021 01/24/2023 | METAPRESENCE | US | REGISTERED Renewal Due: 01/24/2029 | ||||||||||

15

Subsidiaries and Affiliates

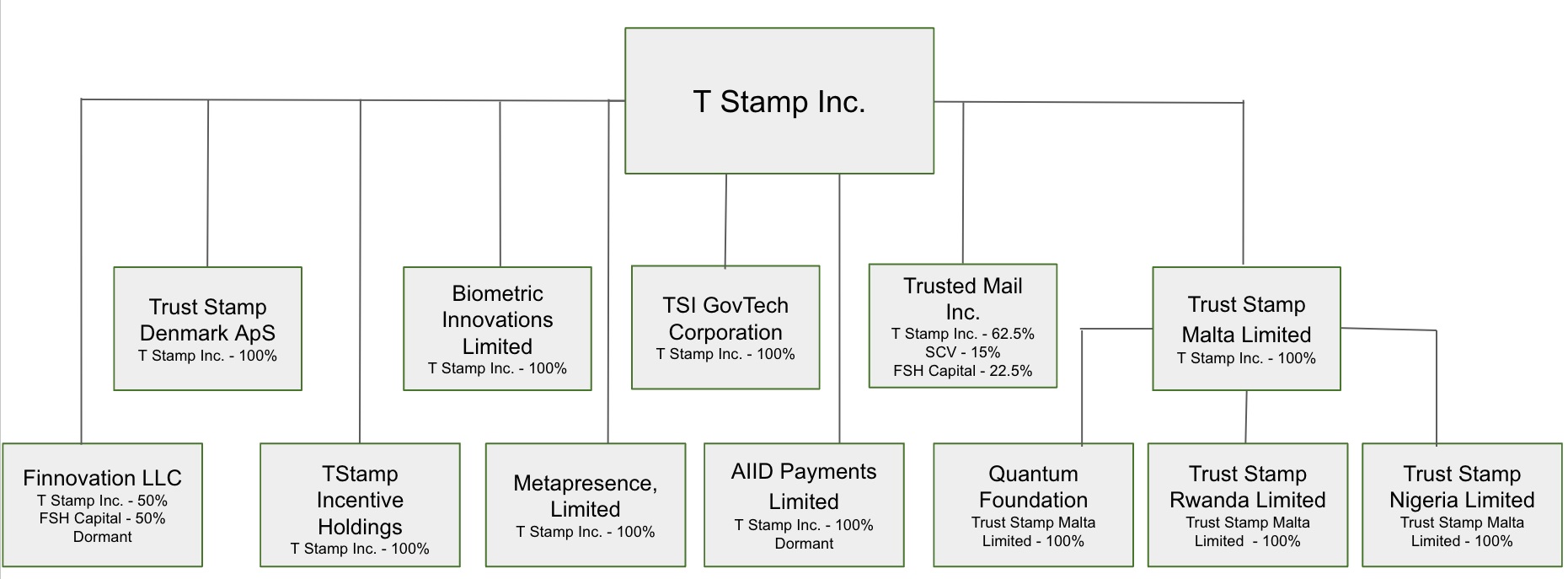

Given the geographic diversity of our team and to facilitate cost-effective administration, Trust Stamp conducts various aspects of its operations through subsidiaries. All subsidiaries share resources across the entire Trust Stamp organization. The officers and directors of Trust Stamp have influence over the operations of all subsidiaries and employees across jurisdictions. Only one of our subsidiaries, Biometric Innovations Limited, has its own management team.

T Stamp Inc. Corporate Structure Chart

Operational Subsidiaries

Tstamp Incentive Holdings. On April 9, 2019, management created a new entity, Tstamp Incentive Holdings (“TSIH”) to which the Company issued 320,513 shares of Class A Common Stock that the Board of Directors of TSIH could use for employee stock awards in the future. The purpose of the entity was to provide an analogous structure to a traditional stock incentive plan. As of December 31, 2023, 54,734 shares of Class A Common Stock are still held by TSIH – however, all of these shares of Class A Common Stock have been allocated for issuance pursuant to employee Restricted Stock Units that vested on January 2, 2024. As of the date of this report, no shares of Class A Common Stock are held by TSIH as all shares have been issued pursuant to employee Restricted Stock Units. The Company has no plans to issue additional equity securities to TSIH and as such, it is expected this entity will become dormant going forward.

Biometric Innovations Limited (formerly “Trust Stamp Fintech Limited”). Biometric Innovations Limited is our Company’s United Kingdom ("UK") operating subsidiary. It was established to act as the contracting entity for development contractors in the UK, and it has its own board and management team. The purpose of this entity was to establish beachhead operations in the country to service a contract entered by the Company with the National Association of Realtors and Property Mark. This entity serves as a sales and marketing function for the product “NAEA” which was developed for the contract between the listed parties. On June 11, 2020, the Company entered into a stock exchange transaction with Biometric Innovations Limited, becoming a 100% owner of the entity. The stock exchange transaction was not pursuant to any formal written agreement.

Trust Stamp Malta Limited. Trust Stamp Malta Limited is a wholly owned subsidiary of T Stamp Inc. It operates an R&D Campus in the Republic of Malta, for which it has entered into a lease with a local commercial landlord in Malta, Vassallo Group Realty Ltd. The goal of Trust Stamp Malta Limited is to advance our biometric authentication technology. As part of the creation of this entity, we entered into an agreement with the government of Republic of Malta for a repayable advance of up to €800,000 to cover 75% of the first 24 months of payroll costs for any employee who begins 36 months from the execution of the agreement on July 8, 2020.

Trust Stamp Rwanda Limited. The Company opened an office in Rwanda, Africa in April 2021. The Company has established an R&D center in Rwanda together with a back-office facility for the purpose of our expansion into Africa.

Metapresence Limited. Trust Stamp established Metapresence Limited on November 23, 2021 as a wholly owned crypto-asset subsidiary in the Isle of Man. Metapresence Limited participates in The Digital Isle of Man Accelerator Program, which provides access to a range of government services including regulatory acceleration support and guided access into

16

the regulatory sandbox, where flexible licensing conditions enable digital asset businesses to explore opportunities and adapt as the technology evolves. Metapresence Limited is intended to market the group’s Metaverse related products for use cases outside the European Union. As of the date of this report, the entity has no operations.

Trust Stamp Denmark ApS. Trust Stamp established Trust Stamp Denmark ApS on June 6, 2021 as a wholly owned subsidiary in Copenhagen, Denmark. Trust Stamp Denmark ApS focuses on developing and marketing GDPR compliant products in Denmark and throughout the European Union from a strategic Danish base that can passport authorized products throughout the European Union. In furtherance of that goal, Trust Stamp Denmark ApS has obtained D-Seal Certification and is working with a prominent Danish law firm to publish opinions on the status of Trust Stamp’s products under GDPR.

Trust Stamp Nigeria Limited — Trust Stamp established Trust Stamp Nigeria Limited on January 31, 2024 as a wholly-owned subsidiary in Lagos, Nigeria. The establishment of the entity is aimed at exploring business opportunities and conducting operations in Nigeria.

Quantum Foundation — Trust Stamp Malta Limited established Quantum Foundation on October 13, 2022 as a wholly-owned subsidiary in the Republic of Malta. The establishment of the entity is to support the development of early-stage leading edge technology companies in the Republic of Malta. Quantum Foundation collaborated with Malta Enterprise and Plug and Play Switzerland to establish a Malta Acceleration Program to foster the start-up community in the country. The Program's intention is to drive innovation in the Republic of Malta, and ensure that everyone is able to enjoy the benefits of the latest technologies.

Non-Operational Subsidiaries

AIID Payments Limited. The Company established AIID Payments Limited to provide payments services to NGO’s and other non-profit and social-welfare entities and activities. As of the date of this report, the entity has no operations, and is essentially dormant.

T Avatar LLC. Trust Stamp established T Avatar LLC to provide anonymized age-verification tools for minors participating in online activities. The Company has completed the process of administratively dissolving T Avatar LLC and the dissolution was effective February 28, 2023.

Finnovation LLC. The Company established Finnovation LLC to provide an innovative FinTech, Blockchain and Digital Identity innovation incubator. As of the date of this report, this entity has no operations, and is essentially dormant.

T Stamp LLC. As described above, the Company was originally founded as “T Stamp LLC”, formed on November 9, 2015 as a Georgia limited liability company. In 2016, the Company effected a “hive down” business reorganization whereby the business of the Company was transferred into to a newly formed, wholly owned subsidiary, which was T Stamp Inc. (i.e. the Company). As of the date of this report, the Company is no longer a subsidiary of T Stamp LLC, and T Stamp LLC is no longer a majority owner of the Company. On January 6, 2022 all shares held by T Stamp LLC were distributed to its members on a pro rata basis according to their respective membership interests. On September 19, 2023, the Company received the Certificate of Termination from the state of Georgia, which represents the completion of dissolving T Stamp LLC.

Sunflower Artificial Intelligence Technologies. Based out of Poland, Trust Stamp established Sunflower Artificial Intelligence Technologies as the contracting entity for development contractors in Poland and Central Europe As of the date of this report, the contractors have entered into direct contracts with T Stamp Inc. On May 10, 2023, the Company received the Termination Resolution from the Polish Department of the National Court Register, which represents the completion of dissolving Sunflower Artificial Intelligence Technologies.

Trusted Mail Inc. The Company established Trusted Mail Inc. for development of an encrypted e-mail product (Trusted Mail ®) using our Company’s facial recognition technology. Trusted Mail technology is held by Trusted Mail, Inc., which is a majority-owned subsidiary of Trust Stamp Inc.. The remainder of Trust Mail Inc. is owned by FSH Capital, LLC and Second Century Ventures, which are related parties of the Company. As of the date of this report, this entity has no operations, and is essentially dormant.

TSI GovTech Corporation. Trust Stamp established TSI GovTech Corporation to contract for data management and server operations in Canada. This entity has had no operations since its inception.

17

Global Server Management Inc. The Company established Global Server Management Inc. to contract for data management and server operations in Canada. This entity has had no operations since its inception.

Available Information

Our website is www.truststamp.ai. As soon as reasonably practicable after such material is electronically filed or furnished to the Securities and Exchange Commission ("SEC"), our annual reports, quarterly reports, and current reports on form 8-K and all amendments to those reports are available on this website, free of charge.

Alternatively, you may access these reports at the SEC’s website at www.sec.gov.

Item 1A. Risk Factors

The SEC requires the Company to identify risks that are specific to its business and its financial condition. The Company is still subject to all the same risks as companies in its business, and all companies in the economy. These include risks relating to economic downturns, political and economic events, and technological developments (such as cyber-attacks and the ability to prevent such attacks). Additionally, early-stage companies are inherently riskier than more developed companies, and the risk of business failure and complete loss of your investment capital is present. You should consider general risks as well as specific risks when deciding whether to invest.

Below is a summary of material risks, uncertainties and other factors that could have a material effect on the Company and its operations:

•We are a comparatively early-stage company that has incurred operating losses in the past, expect to incur operating losses in the future, and may never achieve or maintain profitability.

•Our technology continues to be developed, and there is no guarantee that we will ever successfully develop the technology that is essential to our business to a point at which no further development is needed.

•We may be subject to numerous data protection requirements and regulations.

•We operate in a highly competitive industry that is dominated by a number of exceptionally large, well-capitalized market leaders and the size and resources of some of our competitors may allow them to compete more effectively than we can.

•We rely on third parties to provide services essential to the success of our business.

•We currently have three customers that account for substantially all of our revenues.

•We expect to raise additional capital through equity and/or debt offerings to support our working capital requirements and operating losses.

•Our auditor has included an “Emphasis of Matter Regarding Liquidity” note in its report on our consolidated financial statements for the year ended December 31, 2023. Our consolidated financial statements do not include any adjustments that may result from the outcome of this uncertainty.

•As the vast majority of our revenue is US Dollar denominated and a significant percentage of our expenses are incurred in other currencies, we are subject to risks relating to foreign currency fluctuations.

Risks Related to Our Company

We have a limited operating history upon which you can evaluate our performance and have not yet generated profits. Accordingly, our prospects must be considered in light of the risks that any new company encounters. Our Company was incorporated under the laws of the State of Delaware on April 11, 2016, and we have not yet generated profits. The likelihood of our creation of a viable business must be considered in light of the problems, expenses, difficulties, complications, and delays frequently encountered in connection with the growth of a business, operation in a competitive industry, and the continued development of our technology and products. We anticipate that our operating expenses will increase for the near future, and there is no assurance that we will be profitable in the near future. You should consider our business, operations, and prospects in light of the risks, expenses and challenges faced as an emerging growth company.

18

We have historically operated at a loss, which has resulted in an accumulated deficit. For the fiscal year ended December 31, 2023, we incurred a net loss of $7.64 million, compared to a net loss of $12.09 million for the fiscal year ended December 31, 2022. There can be no assurance that we will ever achieve profitability. Even if we do, there can be no assurance that we will be able to maintain or increase profitability on a quarterly or annual basis. Failure to do so would continue to have a material adverse effect on our accumulated deficit, would affect our cash flows, would affect our efforts to raise capital and is likely to result in a decline in our Class A Common Stock price.

Our consolidated financial statements for the fiscal years ended December 31, 2023 and 2022 have been prepared on a going concern basis. We have not yet generated profits and have an accumulated deficit of $50.85 million as of December 31, 2023. We may not have enough funds to sustain the business until it becomes profitable. Even if we raise additional funding through future financing efforts, we may not accurately anticipate how quickly we may use such funds and whether such funds would be sufficient to bring the business to profitability. The Company’s ability to continue as a going concern in the next twelve months following the date of the consolidated financial statements is dependent upon its ability to produce revenues and/or obtain financing sufficient to meet current and future obligations and deploy such to produce profitable operating results.

Our cash could be adversely affected if the financial institutions in which we hold our cash fail. The Company maintains domestic cash deposits in Federal Deposit Insurance Corporation (“FDIC”) insured banks. The domestic bank deposit balances may exceed the FDIC insurance limits. In addition, given the foreign markets we serve, we maintain cash deposits in foreign banks, some of which are not insured or partially insured by the FDIC or other similar agency. These balances could be impacted if one or more of the financial institutions in which we deposit monies fails or is subject to other adverse conditions in the financial or credit markets.

Our technology continues to be developed, and it is unlikely that we will ever develop our technology to a point at which no further development is required. Trust Stamp is developing complex technology that requires significant technical and regulatory expertise to develop, commercialize and update to meet evolving market and regulatory requirements. While we constantly monitor and adapt our products and technology as criminal methods of breaching cybersecurity advance, there is no guarantee we will consistently be able to develop technology that can effectively counteract such criminal efforts. If we are unable to successfully develop and commercialize our technology and products, it will significantly affect our viability as a company.

If our security measures are breached or unauthorized access to individually identifiable biometric or other personally identifiable information is otherwise obtained, our reputation may be harmed, and we may incur significant liabilities. In the ordinary course of our business, we may collect and store sensitive data, including protected health information (“PHI”), personally identifiable information (“PII”), owned or controlled by ourselves or our customers, and other parties. We communicate sensitive data, including patient data, electronically, and through relationships with multiple third-party vendors and their subcontractors. These applications and data encompass a wide variety of business-critical information, including research and development information, patient data, commercial information, and business and financial information. We face a number of risks relative to protecting this critical information, including loss of access risk, inappropriate use or disclosure, inappropriate modification, and the risk of our being unable to adequately monitor, audit, and modify our controls over our critical information. This risk extends to the third-party vendors and subcontractors we use to manage this sensitive data. As a custodian of this data, Trust Stamp therefore inherits responsibilities related to this data, exposing itself to potential threats. Data breaches occur at all levels of corporate sophistication (including at companies with significantly greater resources and security measures than our own) and the resulting fallout stemming from these breaches can be costly, time-consuming, and damaging to a company’s reputation. Further, data breaches need not occur from malicious attack or phishing only. Often, employee carelessness can result in sharing PII with a much wider audience than intended. Consequences of such data breaches could result in fines, litigation expenses, costs of implementing better systems, and the damage of negative publicity, all of which could have a material adverse effect on our business operations and financial condition.

We are subject to substantial governmental regulation relating to our technology and will continue to be for the lifetime of our Company. By virtue of handling sensitive PII and biometric data, we are subject to numerous statutes related to data privacy and additional legislation and regulation should be anticipated in every jurisdiction in which we operate. Examples of federal (US) and European statutes we could be subject to are:

•Health Insurance Portability and Accountability Act (HIPAA)

•Health Information Technology for Economic and Clinical Health Act (HITECH)

19

Any such access, breach, or other loss of information could result in legal claims or proceedings, liability under federal or state laws that protect the privacy of personal information under HIPAA and/or “HITECH”. Notice of breaches must be made to affected individuals, the Secretary of the Department of Health and Human Services (“HHS”), and for extensive breaches, notice may need to be made to the media or state attorneys general. Penalties for violations of these laws vary. For instance, penalties for failure to comply with a requirement of HIPAA and HITECH vary significantly, and include significant civil monetary penalties and, in certain circumstances, criminal penalties with fines up to $250,000 per violation and/or imprisonment. A person who knowingly obtains or discloses individually identifiable health information in violation of HIPAA may face a criminal penalty of up to $50,000 and up to one-year imprisonment. The criminal penalties increase if the wrongful conduct involves false pretenses or the intent to sell, transfer or use identifiable health information for commercial advantage, personal gain, or malicious harm.

Further, various states, such as California, have implemented similar privacy laws and regulations, such as the California Confidentiality of Medical Information Act, that impose restrictive requirements regulating the use and disclosure of health information and other personally identifiable information. Where state laws are more protective, we have to comply with the stricter provisions. In addition to fines and penalties imposed upon violators, some of these state laws also afford private rights of action to individuals who believe their personal information has been misused. California’s patient privacy laws, for example, provide for penalties of up to $250,000 and permit injured parties to sue for damages. The interplay of federal and state laws may be subject to varying interpretations by courts and government agencies, creating complex compliance issues for us and data we receive, use and share, potentially exposing us to additional expense, adverse publicity, and liability. Further, as regulatory focus on privacy issues continues to increase and laws and regulations concerning the protection of personal information expand and become more complex, these potential risks to our business could intensify. Changes in laws or regulations associated with the enhanced protection of certain types of sensitive data, such as PII or PHI, along with increased customer demands for enhanced data security infrastructure, could greatly increase our cost of providing our services, decrease demand for our services, reduce our revenues and/or subject us to additional liabilities.

Compliance with U.S. and international data protection laws and regulations could cause us to incur substantial costs or require us to change our business practices and compliance procedures in a manner adverse to our business. Moreover, complying with these various laws could require us to take on more onerous obligations in our contracts, restrict our ability to collect, use and disclose data, or in some cases, impact our ability to operate in certain jurisdictions. We rely on our customers to obtain valid and appropriate consents from data subjects whose biometric samples and data we process on such customers’ behalf. Given that we do not obtain direct consent from such data subjects and we do not audit our customers to ensure that they have obtained the necessary consents required by law, the failure of our customers to obtain consents that are in compliance with applicable law could result in our own non-compliance with privacy laws. Such failure to comply with U.S. and international data protection laws and regulations could result in government enforcement actions (which could include civil or criminal penalties), private litigation and/or adverse publicity and could negatively affect our operating results and business. Claims that we have violated individuals’ privacy rights, failed to comply with data protection laws, or breached our contractual obligations, even if we are not found liable, could be expensive and time consuming to defend, could result in adverse publicity and could have a material adverse effect on our business, financial condition and results of operations.

We anticipate sustaining operating losses for the foreseeable future. It is anticipated that we will sustain operating losses into 2024 as we continue with research and development, and strive to gain new customers for our technology and market share in our industry. Our ability to become profitable depends on our ability to expand our customer base, consisting of companies willing to license our technology. There can be no assurance that this will occur. Unanticipated problems and expenses are often encountered in offering new products which may impact whether the Company is successful. Furthermore, we may encounter substantial delays and unexpected expenses related to development, technological changes, marketing, regulatory requirements and changes to such requirements or other unforeseen difficulties. There can be no assurance that we will ever become profitable. If the Company sustains losses over an extended period of time, it may be unable to continue in business.

If our products do not achieve broad acceptance both domestically and internationally, we will not be able to achieve our anticipated level of growth. Our revenues are derived from licensing our identity authentication solutions. We cannot accurately predict the future growth rate or the size of the market for our technology. The expansion of the market for our solutions depends on a number of factors, such as

•the cost, performance and reliability of our solutions and the products and services offered by our competitors;

•customers’ perceptions regarding the benefits of biometrics and other authentication solutions;

20

•public perceptions regarding the intrusiveness of these solutions and the manner in which organizations use biometric and other identity information collected;

•public perceptions regarding the confidentiality of private information;

•proposed or enacted legislation related to privacy of information

•customers’ satisfaction with biometrics solutions; and

•marketing efforts and publicity regarding biometrics solutions.

Even if our technology gains wide market acceptance, our solutions may not adequately address market requirements and may not continue to gain market acceptance. If authentication solutions generally or our solutions specifically do not gain wide market acceptance, we may not be able to achieve our anticipated level of growth and our revenues and results of operations would suffer.

We operate in a highly competitive industry that is dominated by multiple very large, well-capitalized market leaders and is constantly evolving. New entrants to the market, existing competitor actions, or other changes in market dynamics could adversely impact us. The level of competition in the identity authentication industry is high, with multiple exceptionally large, well-capitalized competitors holding a majority share of the market. Currently, we are not aware of any direct competitors of the Company able to offer our main technological offering. Nonetheless, many of the companies in the identity authentication market have longer operating histories, larger customer bases, significantly greater financial, technological, sales, marketing, and other resources than we do. At any point, these companies may decide to devote their resources to creating a competing technology solution which will impact our ability to maintain or gain market share in this industry. Further, such companies will be able to respond more quickly than we can to new or changing opportunities, technologies, standards, or client requirements, more quickly develop new products or devote greater resources to the promotion and sale of their products and services than we can. Likewise, their greater capabilities in these areas may enable them to better withstand periodic downturns in the identity management solutions industry and compete more effectively on the basis of price and production. In addition, new companies may enter the markets in which we compete, further increasing competition in the identity management solutions industry.

We believe that our ability to compete successfully depends on a number of factors, including the type and quality of our products and the strength of our brand names, as well as many factors beyond our control. We may not be able to compete successfully against current or future competitors, and increased competition may result in price reductions, reduced profit margins, loss of market share and an inability to generate cash flows that are sufficient to maintain or expand the development and marketing of new products, any of which would adversely impact our results of operations and financial condition.

We face competition from companies with greater financial, technical, sales, marketing, and other resources, and, if we are unable to compete effectively with these competitors, our market share may decline, and our business could be harmed. We face competition from well established companies. Many of our competitors have longer operating histories, larger customer bases, significantly greater financial, technological, sales, marketing, and other resources than we do. As a result, our competitors may be able to respond more quickly than we can to new or changing opportunities, technologies, standards, or client requirements, more quickly develop new products or devote greater resources to the promotion and sale of their products and services than we can. Likewise, their greater capabilities in these areas may enable them to better withstand periodic downturns in the identity management solutions industry and compete more effectively on the basis of price and production. In addition, new companies may enter the markets in which we compete, further increasing competition in the identity management solutions industry.

We believe that our ability to compete successfully depends on a number of factors, including the type and quality of our products and the strength of our brand names, as well as many factors beyond our control. We may not be able to compete successfully against current or future competitors, and increased competition may result in price reductions, reduced profit margins, loss of market share and an inability to generate cash flows that are sufficient to maintain or expand the development and marketing of new products, any of which would adversely impact our results of operations and financial condition.

The Company may be unable to effectively protect its intellectual property. The Company has many issued patents related to its products and technology, and many pending patent applications as of the date of this report. There is no guarantee that the Company will ever be issued patents on the applications it has submitted. In addition, in order to control costs, we have filed patent applications only in the United States. This may result in our having limited or no protection in other

21

jurisdictions. Our success depends to a significant degree upon the protection of our products and technology. If we are unable to secure patents for our products and technology, or are otherwise unsuccessful at protecting our technology, other companies with greater resources may copy our technology and/or products, or improve upon them, putting us at a disadvantage to our competitors.