UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended 31 December 2023

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-14642

(Exact name of Registrant as specified in its charter)

ING GROUP

(Translation of Registrant’s name into English)

The Netherlands

(Jurisdiction of incorporation or organization)

The Netherlands

(Address of principal executive offices)

Telephone: +31 20 564 7705

E-mail: Erwin.Olijslager@ing.com

The Netherlands

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class | Trading symbols | Name of each exchange on which registered | ||

1.726% Callable Fixed-to-Floating Rate Senior Notes due 2027 | ||||

2.727% Callable Fixed-to-Floating Rate Senior Notes due 2032 | ||||

4.017% Callable Fixed-to-Floating Rate Senior Notes due 2028 | ||||

3.869% Callable Fixed-to-Floating Rate Senior Notes due 2026 | ||||

4.252% Callable Fixed-to-Floating Rate Senior Notes due 2033 | ||||

6.083% Callable Fixed-to-Floating Rate Senior Notes due 2027 | ||||

$500,000,000 Callable Floating Rate Senior Notes due 2027 | ||||

(i)Not for trading, but only in connection with the registration of American Depositary Shares

representing such ordinary shares, pursuant to the requirements of the Securities and Exchange

Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act.None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of

the close of the period covered by the annual report.

Ordinary Shares, nominal value EUR 0.01 per Ordinary Share3,498,194,469

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act. ☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file

reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13

or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or

15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that

the registrant was required to file such reports), and (2) has been subject to such filing requirements for the

past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File

required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant was required to submit and post such

files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-

accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” accelerated

filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

company☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP,

indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange

Act. ☐

† | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s

assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the

Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its

audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial

statements of the registrant included in the filing reflect the correction of an error to previously issued

financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery

analysis of incentive based compensation received by any of the registrant’s executive officers during the

relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial

statements included in this filing:

U.S. GAAP☐ | issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial

statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in

Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

Contents

Part I

8 | |||

Part II

16K | CYBERSECURITY |

Part III

Additional information

Presentation of information

In this Annual Report, and unless otherwise stated or the context otherwise dictates, references to "ING

Groep N.V.", "ING Groep NV", "ING Groep" and "ING Group" refer to ING Groep NV and references to "ING",

the "Company", the "Group", "we" and "us" refer to ING Groep NV and its consolidated subsidiaries. ING

Groep N.V.'s primary banking subsidiary is ING Bank N.V. (together with its consolidated subsidiaries, "ING

Bank"). References to "Executive Board" and "Supervisory Board" refer to the Executive Board or Supervisory

Board of ING Groep N.V., respectively.

ING presents its consolidated financial statements in euros, the currency of the European Economic and

Monetary Union. Unless otherwise specified or the context otherwise requires, references to “$”, “US$” and

“Dollars” are to the United States dollars and references to "€" and “EUR” are to euros.

ING prepares financial information in accordance with International Financial Reporting Standards as issued

by the International Accounting Standards Board (“IFRS-IASB”) for purposes of reporting with the U.S.

Securities and Exchange Commission (“SEC”), including financial information contained in this Annual Report

on Form 20-F. ING Group’s accounting policies and its use of various options under IFRS-IASB are described

under Note '1.2 Basis of preparation of the Consolidated financial statements’ in the consolidated financial

statements. In this document the term “IFRS-IASB” is used to refer to IFRS-IASB as applied by ING Group.

The published 2023 Financial Statements of ING Group, however, are prepared in accordance with IFRS-EU.

IFRS-EU refers to International Financial Reporting Standards (“IFRS”) as adopted by the European Union

(“EU”), including the decisions ING Group made with regard to the options available under IFRS as adopted

by the EU (IFRS-EU).

IFRS-EU differs from IFRS-IASB, in respect of certain paragraphs in IAS 39 ‘Financial Instruments: Recognition

and Measurement’ regarding hedge accounting for portfolio hedges of interest rate risk. Under IFRS-EU, ING

Group applies fair value hedge accounting for portfolio hedges of interest rate risk (fair value macro hedges)

in accordance with the EU “carve-out” version of IAS 39. Under the EU “IAS 39 carve-out”, hedge accounting

may be applied, in respect of fair value macro hedges, to core deposits and hedge ineffectiveness is only

recognised when the revised estimate of the amount of cash flows in scheduled time buckets falls below the

original designated amount of that bucket, and is not recognised when the revised amount of cash flows in

scheduled time buckets is more than the original designated amount. Under IFRS-IASB, hedge accounting

for fair value macro hedges cannot be applied to core deposits and hedge ineffectiveness arises whenever

the revised estimate of the amount of cash flows in scheduled time buckets is either more or less than the

original designated amount of that bucket. IFRS-IASB financial information is prepared by reversing the

hedge accounting impacts that are applied under the EU “carve-out” version of IAS 39. Financial information

under IFRS-IASB accordingly does not take account of the possibility that, had ING Group applied IFRS-IASB

as its primary accounting framework, it might have applied alternative hedge strategies where those

alternative hedge strategies could have qualified for IFRS-IASB compliant hedge accounting. These decisions

could have resulted in different shareholders’ equity and net result amounts compared to those indicated in

this Annual Report on Form 20-F.

Other than for the purpose of SEC reporting, ING Group intends to continue to prepare its Financial

Statements under IFRS-EU. A reconciliation between IFRS-EU and IFRS-IASB for shareholders’ equity and net

result is included in Note 1 ‘Basis of preparation and material accounting policy information’ to the

consolidated financial statements.

Certain amounts set forth herein, such as percentages, may not sum due to rounding.

ING Group Annual Report 2023 on Form 20-F 5

CAUTIONARY STATEMENT WITH RESPECT TO

FORWARD-LOOKING STATEMENTS

Certain of the statements contained herein are not historical facts, including, without limitation, certain

statements made of future expectations and other forward-looking statements that are based on

management’s current views and assumptions and involve known and unknown risks and uncertainties that

could cause actual results, performance or events to differ materially from those expressed or implied in

such statements. Actual results, performance or events may differ materially from those in such statements

due to a number of factors, including, without limitation,

•changes in general economic conditions and customer behaviour, in particular economic conditions in

ING’s core markets, including changes affecting currency exchange rates and the regional and global

economic impact of the invasion of Russia into Ukraine and related international response measures

•changes affecting interest rate levels

•any default of a major market participant and related market disruption

•changes in performance of financial markets, including in Europe and developing markets

•fiscal uncertainty in Europe and the United States

•discontinuation of or changes in ‘benchmark’ indices

•inflation and deflation in our principal markets

•changes in conditions in the credit and capital markets generally, including changes in borrower and

counterparty creditworthiness

•failures of banks falling under the scope of state compensation schemes

•non-compliance with or changes in laws and regulations, including those concerning financial services,

financial economic crimes and tax laws, and the interpretation and application thereof

•geopolitical risks, political instabilities and policies and actions of governmental and regulatory

authorities, including in connection with the invasion of Russia into Ukraine and related international

response measures

•legal and regulatory risks in certain countries with less developed legal and regulatory frameworks

•prudential supervision and regulations, including in relation to stress tests and regulatory restrictions on

dividends and distributions, (also among members of the group)

•ING’s ability to meet minimum capital and other prudential regulatory requirements

•changes in regulation of US commodities and derivatives businesses of ING and its customers

•application of bank recovery and resolution regimes, including write-down and conversion powers in

relation to our securities

•outcome of current and future litigation, enforcement proceedings, investigations or other regulatory

actions, including claims by customers or stakeholders who feel misled or treated unfairly, and other

conduct issues

•changes in tax laws and regulations and risks of non-compliance or investigation in connection with tax

laws, including FATCA

•operational and IT risks, such as system disruptions or failures, breaches of security, cyber-attacks,

human error, changes in operational practices or inadequate controls including in respect of third parties

with which we do business and including any risks as a result of incomplete, inaccurate, or otherwise

flawed outputs from the algorithms and data sets utilized in artificial intelligence

•risks and challenges related to cybercrime including the effects of cyberattacks and changes in

legislation and regulation related to cybersecurity and data privacy, including such risks and challenges

as a consequence of the use of emerging technologies, such as advanced forms of artificial intelligence

and quantum computing

•changes in general competitive factors, including ability to increase or maintain market share

•inability to protect our intellectual property and infringement claims by third parties

•inability of counterparties to meet financial obligations or ability to enforce rights against such

counterparties

•changes in credit ratings

•business, operational, regulatory, reputation, transition and other risks and challenges in connection with

climate change and Environmental, Social and Governance (ESG)-related matters, including data and

reporting

•inability to attract and retain key personnel

•future liabilities under defined benefit retirement plans

•failure to manage business risks, including in connection with use of models, use of derivatives, or

maintaining appropriate policies and guidelines

•changes in capital and credit markets, including interbank funding, as well as customer deposits, which

provide the liquidity and capital required to fund our operations, and

•the other risks and uncertainties detailed in the most recent annual report of ING Groep N.V. (including

the Risk Factors contained therein) and ING’s more recent disclosures, including press releases, which are

available on www.ing.com.

This document may contain ESG-related material that has been prepared by ING on the basis of publicly

available information, internally developed data and other third-party sources believed to be reliable. ING

has not sought to independently verify information obtained from public and third-party sources and makes

no representations or warranties as to accuracy, completeness, reasonableness or reliability of such

information.

Materiality, as used in the context of ESG, is distinct from, and should not be confused with, such term as

defined in the Market Abuse Regulation or as defined for Securities and Exchange Commission (‘SEC’)

ING Group Annual Report 2023 on Form 20-F 6

reporting purposes. Any issues identified as material for purposes of ESG in this annual report are therefore

not necessarily material as defined in the Market Abuse Regulation or for SEC reporting purposes. In

addition, there is currently no single, globally recognized set of accepted definitions in assessing whether

activities are “green” or “sustainable.” Without limiting any of the statements contained herein, we make no

representation or warranty as to whether any of our securities constitutes a green or sustainable security or

conforms to present or future investor expectations or objectives for green or sustainable investing. For

information on characteristics of a security, use of proceeds, a description of applicable project(s) and/or

any other relevant information, please reference the offering documents for such security.

This annual report contains inactive textual addresses to internet websites operated by us and third parties.

Reference to such websites is made for information purposes only, and information found at such websites

is not incorporated by reference into this annual report. ING does not make any representation or warranty

with respect to the accuracy or completeness of, or take any responsibility for, any information found at

any websites operated by third parties. ING specifically disclaims any liability with respect to any

information found at websites operated by third parties. ING cannot guarantee that websites operated by

third parties remain available following the filing of this annual report or that any information found at such

websites will not change following the filing of this annual report. Many of those factors are beyond ING’s

control.

Any forward-looking statements made by or on behalf of ING speak only as of the date they are made, and

ING assumes no obligation to publicly update or revise any forward-looking statements, whether as a result

of new information or for any other reason.

This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any securities in

the United States or any other jurisdiction.

ING Group Annual Report 2023 on Form 20-F 7

PART I

Item 1.Identity of Directors, Senior

Management And Advisors

Not applicable.

Item 2.Offer Statistics and Expected

Timetable

Not applicable.

Item 3.Key Information

A. Selected financial data

Not applicable.

B. Capitalization and indebtedness

This item does not apply to annual reports on Form 20-F.

C. Reasons for the offer and use of proceeds

This item does not apply to annual reports on Form 20-F.

D. Risk Factors

Summary of Risk factors

The following is a summary of the principal risk factors that could have a material adverse effect on the

reputation, business activities, financial condition, results and prospects of ING. Please carefully consider all

of the information discussed in this section “Risk Factors” for a detailed description of these risks.

Risks related to financial conditions, market environment and general economic trends

•Our revenues and earnings are affected by the volatility and strength of the economic, business,

liquidity, funding and capital markets environments of the various geographic regions in which we

conduct business, including Russia and Ukraine, as well as by changes in customer behaviour in these

regions, and an adverse change in any one region could have an impact on our business, results and

financial condition.

•Inflation, interest volatility and other interest rate changes may adversely affect our business, results

and financial condition.

•The default of a major market participant could disrupt the markets and may have an adverse effect on

our business, results and financial condition.

•Continued risk of political instability and fiscal uncertainty in Europe and the United States, as well as

ongoing volatility in the financial markets and the economy generally have adversely affected, and may

continue to adversely affect, our business, results and financial condition.

•Discontinuation of interest rate benchmarks may negatively affect our business, results and financial

condition.

•Market conditions, including those observed over the past few years, may increase the risk of loans being

impaired and have a negative effect on our results and financial condition.

•We may incur losses due to failures of banks falling under the scope of state compensation schemes.

ING Group Annual Report 2023 on Form 20-F 8

Risks related to the regulation and supervision of the Group

•Non-compliance with laws and/or regulations concerning financial services or financial institutions,

including with respect to financial economic crimes, could result in fines and other liabilities, penalties or

consequences for us, which could materially affect our business and reputation and reduce our

profitability.

•Changes in laws and/or regulations governing financial services or financial institutions or the application

of such laws and/or regulations may increase our operating costs and limit our activities.

•We are subject to additional legal and regulatory risk in certain countries with less developed or

predictable legal and regulatory frameworks.

•We are subject to the regulatory supervision of the ECB and other regulators with extensive supervisory

and investigatory powers.

•Failure to meet minimum capital and other prudential regulatory requirements as applicable to us from

time to time may have a material adverse effect on our business, results and financial condition and on

our ability to make payments on certain of our securities.

•Our US commodities and derivatives business is subject to CFTC and SEC regulation under the Dodd-Frank

Act.

•We are subject to several other bank recovery and resolution regimes that include statutory write-down

and conversion as well as other powers, which remains subject to significant uncertainties as to the

scope and impact on us.

Risks related to litigation, enforcement proceedings and investigations and to changes

in tax laws

•We may be subject to litigation, enforcement proceedings, investigations or other regulatory actions,

and adverse publicity.

•We are subject to different tax regulations in each of the jurisdictions where we conduct business, and

are exposed to changes in tax laws and risks of non-compliance with proceedings or investigations with

respect to tax laws.

•We may be subject to US tax investigation if we fail to comply with our obligations as a Participating

Financial Institution in respect of the Foreign Account Tax Compliance Act (FATCA) and as a Qualified

Intermediary in respect of other US tax regulations

•ING is exposed to the risk of claims from customers who feel misled or treated unfairly because of advice

or information received.

Risks related to the Group’s business and operations

•ING may be unable to meet internal or external aims or expectations or requirements with respect to

ESG-related matters.

•ING may be unable to adapt its products and services to meet changing customer behaviour and

demand, including as a result of ESG-related matters.

•ING’s business and operations are exposed to physical risks, including as a direct result of climate

change.

•ING’s business and operations are exposed to transition risks related to climate change.

•Operational and IT risks, such as system disruptions or failures, breaches of security, cyber attacks,

human error, changes in operational practices, inadequate controls including in respect of third parties

with which we do business or outbreaks of communicable diseases may adversely impact our

reputation, business and results.

•We are subject to increasing risks related to cybercrime and compliance with cybersecurity regulation.

•Because we operate in highly competitive markets, including our home market, we may not be able to

increase or maintain our market share, which may have an adverse effect on our results.

•We may not always be able to protect our intellectual property developed in our products and services

and may be subject to infringement claims, which could adversely impact our core business, inhibit

efforts to monetise our internal innovations and restrict our ability to capitalise on future opportunities.

•The inability of counterparties to meet their financial obligations or our inability to fully enforce our rights

against counterparties could have a material adverse effect on our results.

•A downgrade or a potential downgrade in our credit ratings could have an adverse impact on our results

and net results.

•An inability to retain or attract key personnel may affect our business and results.

•We may incur further liabilities in respect of our defined benefit retirement plans if the value of plan

assets is not sufficient to cover potential obligations, including as a result of differences between actual

results and underlying actuarial assumptions and models.

Risks related to the Group’s risk management practices

•Risks relating to our use of quantitative models or assumptions to model client behaviour for the

purposes of our market calculations may adversely impact our reputation or results.

•We may be unable to manage our risks successfully through derivatives.

Risks related to the Group’s liquidity and financing activities

•Adverse conditions in the capital and credit markets, or significant withdrawals of customer deposits,

may impact our liquidity, borrowing and capital positions, as well as the cost of liquidity, borrowings and

capital.

ING Group Annual Report 2023 on Form 20-F 9

•As a holding company, ING Groep N.V. is dependent for liquidity on payments from its subsidiaries, many

of which are subject to regulatory and other restrictions on their ability to transact with affiliates.

Additional risks relating to ownership of ING shares

•Holders of ING shares may experience dilution of their holdings and may be impacted by any share

buyback programme.

•Because we are incorporated under the laws of the Netherlands and many of the members of our

Supervisory and Executive Board and our officers reside outside of the United States, it may be difficult to

enforce judgements of US courts against ING or the members of our Supervisory and Executive Boards or

our officers.

Risk factors

Any of the risks described below could have a material adverse effect on the business activities, financial

condition, results and prospects of ING as well as ING’s reputation. ING may face a number of the risks

described below simultaneously and some risks described below may be interdependent. While the risk

factors below have been divided into categories, some risk factors could belong in more than one category

and investors should carefully consider all of the risk factors set out in this section. Additional risks of which

the Company is not presently aware, or that are currently viewed as immaterial, could also affect the

business operations of ING and have a material adverse effect on ING’s business activities, financial

condition, results and prospects. The market price of ING shares or other securities could decline due to any

of those risks including the risks described below, and investors could lose all or part of their investments.

Although the most material risk factors have been presented first within each category, the order in which

the remaining risk factors are presented is not necessarily an indication of the likelihood of the risks actually

materialising, of the potential significance of the risks or of the scope of any potential negative impact to

our business, results, financial condition and prospects.

Risks related to financial conditions, market environment and general economic trends

Our revenues and earnings are affected by the volatility and strength of the economic,

business, liquidity, funding and capital markets environments of the various geographic

regions in which we conduct business, as well as by changes in customer behaviour in

these regions, and an adverse change in any one region could have an impact on our

business, results and financial condition.

Because ING is a multinational banking and financial services corporation, with a global presence and

serving 40 million customers, corporate clients and financial institutions in 38 countries, ING’s business,

results and financial condition may be significantly impacted by turmoil and volatility in the worldwide

financial markets or in the particular geographic areas in which we operate. In Retail Banking, our products

include savings, payments, investments, loans and mortgages. In Wholesale Banking, we provide specialised

lending, tailored corporate finance, debt and equity market solutions, payments & cash management, trade

and treasury services. Negative developments in relevant financial markets and/or countries or regions have

in the past had and may in the future have a material adverse impact on our business, results and financial

condition, including as a result of the potential consequences listed below.

Factors such as inflation or deflation, interest rates, securities prices, credit spreads, liquidity spreads,

exchange rates, consumer spending, changes in customer behaviour, climate change, business investment,

real estate values and private equity valuations, government spending the volatility and strength of the

capital markets, political events and trends, supply chain disruptions, shortages, terrorism, pandemics and

epidemics (such as the recent Covid-19 pandemic) or other widespread health emergencies all impact the

business and economic environment and, ultimately, our solvency, liquidity and the amount and

profitability of business we conduct in a specific geographic region. Some of these risks are often

experienced globally as well as in specific geographic regions and are described in greater detail below

under the headings: 'Interest rate volatility and other interest rate changes may adversely affect our

business, results and financial condition'; 'Inflation and deflation may negatively affect our business, results

and financial condition'; 'Market conditions, including those observed over the past few years may increase

the risk of loans being impaired and have a negative effect on our results and financial condition'; and

'Continued risk of political instability and fiscal uncertainty in Europe and the United States, as well as

ongoing volatility in the financial markets and the economy generally have adversely affected, and may

continue to adversely affect, our business, results and financial condition'. All of these are factors in local

and regional economies as well as in the global economy, and we may be affected by changes in any one

of these factors in any one country or region, and more if more of these factors occur simultaneously and/

or in multiple countries or regions or on a global scale.

In case one or more of the factors mentioned above adversely affects the profitability of our business, this

might also result, among other things, in the following:

•inadequate reserves or provisions, in relation to which losses could ultimately be realised through profit

and loss and shareholders’ equity;

•the write-down of tax assets impacting net results and/or equity;

•impairment expenses related to goodwill and other intangible assets, impacting our net result and

equity; and/or

•movements in risk-weighted assets for the determination of required capital.

In particular, we are exposed to financial, economic, market and political conditions in the Benelux countries

and Germany, from which we derive a significant portion of our revenues in both Retail Banking and

ING Group Annual Report 2023 on Form 20-F 10

Wholesale Banking, and which could present risks of economic downturn. Though less material, we also

derive substantial revenues in the following geographic regions: United States, Türkiye, Poland and the

remainder of Eastern Europe, Southern Europe, East Asia (primarily Singapore among others) and Australia.

In an economic downturn affecting some or all of these jurisdictions, we expect that higher unemployment,

lower family income, lower corporate earnings, higher corporate and private debt defaults, lower business

investments and lower consumer spending would adversely affect the demand for banking products, and

that ING may need to increase its reserves and provisions, each of which may result in overall lower

earnings. Securities prices, real estate values and private equity valuations may also be adversely impacted,

and any such losses would be realised through profit and loss and shareholders’ equity. We also offer a

number of financial products that expose us to risks associated with fluctuations in interest rates, securities

prices, corporate and private default rates, the value of real estate assets, exchange rates and credit

spreads. Further, while the Covid-19 pandemic and related response measures have eased, the effects of

these measures (including consequences for commercial real estate occupancies and valuations as a result

of the increased prevalence of work-from-home or hybrid working arrangements) are still being felt in the

financial performance and stability of certain of our business customers. As a result, their impact may

continue to affect our business. We also have wholesale banking activities in both Russia and Ukraine, as

well as investments in Russia, some of which are denominated in local currency. In response to Russia’s

invasion of Ukraine, the international community imposed various punitive measures, including sanctions,

capital controls, restrictions on SWIFT access and restrictions on central bank activity. These measures have

significantly impacted, and may continue to significantly impact, Russia’s economy and have contributed to

heightened instability in global markets and increased inflation due in part to supply chain constraints, as

well as higher energy and commodity prices. Should prices remain elevated for an extended period, most

businesses and households would be negatively impacted, and our business in Russia and Ukraine, as well

as our broader business, may be adversely affected, including through spill-over risk to the entire wholesale

banking portfolio (e.g. commodities financing, energy and utilities and energy-consuming clients).

Environmental and/or climate risks may also directly and indirectly impact ING, for example through,

among other things, losses suffered as a result of extreme weather events, the impact of climate-related

transition risk on the risk and return profile or value of security or operations of certain categories of

customer to which ING has exposure. In addition, these risks may also increase ING’s reputational and

litigation risk if the economic activity that ING supports is not in line with community expectations or ING’s

external commitments or legal or regulatory requirements (this includes, but is not limited to, greenwashing

risk).

For further information on ING’s exposure to particular geographic areas, see Note 31 ‘Information on

geographical areas’ to the consolidated financial statements.

Market conditions, including those observed over the past few years, may increase the

risk of loans being impaired and have a negative effect on our results and financial

condition.

We are exposed to the risk that our borrowers (including sovereigns) may not repay their loans according to

their contractual terms and that the collateral securing the payment of these loans may be insufficient. We

may see adverse changes in the credit quality of our borrowers and counterparties, for example, as a result

of their inability to refinance their indebtedness or in the case of a decline in financial performance. Adverse

changes in the credit quality of our borrowers and/or decreasing collateral values would result in increased

capital requirements and provisions, and any deterioration of market conditions may lead to increasing

delinquencies, defaults and insolvencies across a range of sectors. This may lead to impairment charges on

loans and other assets, higher costs and additions to loan loss provisions. A significant increase in the size of

our provision for loan losses could have a material adverse effect on our business, results and financial

condition.

If we are significantly exposed to a concentrated set of customers or counterparties, an adverse event

affecting these parties could lead to increased losses for the Group, and adversely affect our business,

results and financial condition.

We may incur losses due to failures of banks falling under the scope of state

compensation schemes.

While prudential regulation is intended to minimise the risk of bank failures, in the event such a failure

occurs, given our size, we may incur significant compensation payments to be made under the Dutch

Deposit Guarantee Scheme (DGS), which we may be unable to recover from the bankrupt estate, and

therefore the consequences of any future failure of such a bank could be significant to ING. Such costs and

the associated costs to be borne by us may have a material adverse effect on our results and financial

condition. On the basis of the EU Directive on deposit guarantee schemes, ING pays quarterly risk-weighted

contributions into a DGS-fund. The DGS-fund is to grow to a target size of 0.8 percent of all deposits

guaranteed under the DGS, which is expected to be reached in July 2024. In case of failure of a Dutch bank,

depositor compensation is paid from the DGS-fund. If the available financial means of the fund are

insufficient, Dutch banks, including ING, may be required to pay extraordinary ex-post contributions not

exceeding 0.5 percent of their covered deposits per calendar year. In exceptional circumstances, and with

the consent of the competent authority, higher contributions may be required. However, extraordinary ex-

post contributions may be temporarily deferred if, and for so long as, they would jeopardise the solvency or

liquidity of a bank. Depending on the size of the failed bank, the available financial means in the fund, and

the required additional financial means, the impact of the extraordinary ex-post contributions on ING may

be material.

ING Group Annual Report 2023 on Form 20-F 11

Since 2015, the EU has been discussing the introduction of a pan-European deposit guarantee scheme

(EDIS), which would (partly) replace or complement national compensation schemes.

On 18 April 2023, the European Commission published its proposals for the revision of the common

framework for bank crisis management and deposit insurance (CMDI) that focuses on small and medium-

sized banks, but will affect all EU banks. The CMDI framework consists of the Bank Recovery and Resolution

Directive (BRRD), the Single Resolution Mechanism (SRMR) and the Deposit Guarantee Schemes Directive

(DGSD). The revision of the CMDI framework is part of the debate on the completion of the Banking Union

and in particular its third and missing pillar EDIS. As at the date hereof, EDIS has not yet been adopted by

the European Commission.

Risks related to the regulation and supervision of the Group

Non-compliance with applicable laws and/or regulations, including with respect to

financial economic crimes, could result in fines and other liabilities, penalties or

consequences for us, which could materially affect our business and reputation and

reduce our profitability.

ING has faced, and in the future may continue to face, the consequences of non-compliance with applicable

laws and regulations, including the potential commencement of regulatory investigations or legal

proceedings. For additional information on legal proceedings, see Note 42 ‘Legal proceedings’ in the

consolidated financial statements. There are potential risks in areas where applicable regulations may be

unclear: subject to multiple interpretations or under development; where regulations may conflict with one

another; or where regulators revise their previous guidance or courts overturn previous rulings. These could

result in our failure to meet applicable standards. Regulators and other authorities have the power to bring

investigations and/or administrative or judicial proceedings against us, which could result, among other

things, in suspension or revocation of our licences, cease and desist orders, fines, civil penalties, criminal

penalties or other disciplinary action, which could materially harm our results and financial condition as well

as ING’s reputation. If we fail to address, or appear to fail to address, any of these matters appropriately, our

reputation could be harmed and we could be subject to additional legal risk, which could, in turn, increase

the size and number of claims and damages brought against us or subject us to enforcement actions, fines

and penalties.

Furthermore, as a financial institution, we are exposed to the risk of unintentional involvement in criminal

activity in connection with financial economic crimes, including sanctions circumvention and money

laundering and the funding of terrorist and other criminal activities. The failure or perceived failure by us to

comply with legal and regulatory requirements with respect to financial economic crimes may result in

adverse publicity, claims and allegations, litigation and regulatory investigations and sanctions, which may

have a material adverse effect on our business, results, financial condition and/or prospects in any given

period. For further discussion on the impact of litigation, enforcement proceedings, investigations or other

regulatory actions with respect to financial economic crimes, see 'We may be subject to litigation,

enforcement proceedings, investigations or other regulatory actions, and adverse publicity' below.

Changes in laws and/or regulations governing financial services or financial institutions

or the application of such laws and/or regulations may increase our operating costs and

limit our activities.

We are subject to detailed banking laws and financial regulations in the jurisdictions in which we conduct

business. Regulation of the industries in which we operate has become more extensive and complex, while

also attracting supervisory scrutiny. Compliance with applicable and new laws and regulations is resource-

intensive, and may materially increase our operating costs. Moreover, these regulations intend to protect

our customers, markets and society as a whole and can limit or redirect our activities, among others,

through stricter net capital, market conduct and transparency requirements and restrictions on the

businesses in which we can operate or invest.

Our revenues and profitability and those of our industry have been and will continue to be impacted by

requirements relating to capital, additional loss-absorbing capacity, leverage, minimum liquidity and long-

term funding levels, requirements related to resolution and recovery planning, derivatives clearing and

margin rules and levels of regulatory oversight, as well as limitations on which and, if permitted, how certain

business activities may be carried out by financial institutions.

We are subject to additional legal and regulatory risk in certain countries where we

operate with less developed or predictable legal and regulatory frameworks.

In certain countries in which we operate or where our clients reside, judiciary and dispute resolution systems

may be less effective. As a result, in case of a breach of contract, we may have difficulties in making and

enforcing claims against contractual counterparties and, if claims are made against us, we might encounter

difficulties in mounting a defence against such allegations. If we become party to legal proceedings in a

market with an insufficiently developed judicial system, it could have an adverse effect on our operations

and net results.

In addition, as a result of our operations in certain countries, we are subject to risks of possible

nationalisation, expropriation, price controls, exchange controls and other restrictive government actions, as

well as the outbreak of hostilities and/or war, in these markets. In particular, we have wholesale banking

activities in both Russia and Ukraine, as well as investments in Russia, some of which are denominated in

local currency. Furthermore, the current economic environment in certain countries in which we operate

ING Group Annual Report 2023 on Form 20-F 12

may increase the likelihood for regulatory initiatives to enhance consumer protection or to protect

homeowners from foreclosures. Any such regulatory initiative could have an adverse impact on our ability

to protect our economic interest, for instance in the event of defaults on residential mortgages.

We are subject to the regulatory supervision of the ECB and other regulators with

extensive supervisory and investigatory powers.

In its capacity as principal prudential supervisor in the EU, the ECB has extensive supervisory and

investigatory powers, including the ability to issue requests for information, to conduct regulatory

investigations and on-site inspections, and to impose monetary and other sanctions. For example, under the

Single Supervisory Mechanism (SSM), the relevant (national) competent authorities, including the ECB, may

conduct stress tests and have discretion to impose capital surcharges on financial institutions for risks that

are not otherwise recognised in risk-weighted assets or other surcharges depending on the individual

situation of the bank, and take or require other measures, such as restrictions on or changes to the Group’s

business. Competent authorities may also prohibit the Group from making dividend payments to

shareholders or distributions to holders of its regulatory capital instruments if the Group fails to comply with

regulatory requirements, in particular with supervisory actions, minimum capital requirements (including

buffer requirements) or with liquidity requirements, or if there are shortcomings in its governance and risk

management processes. A failure to comply with prudential or conduct regulations could have a material

adverse effect on the Group’s business, results and financial condition.

Failure to meet minimum capital and other prudential regulatory requirements as

applicable to us from time to time may have a material adverse effect on our business,

results and financial condition and on our ability to make payments on certain of our

securities.

ING is subject to a variety of regulations that require us to comply with minimum requirements for capital

(own funds) and additional loss-absorbing capacity, as well as for liquidity, and to comply with leverage

restrictions. In addition, such capital, liquidity and leverage requirements and their application and

interpretation may change. Any changes may require us to maintain more capital or to raise a different

type of capital by disqualifying existing capital instruments from continued inclusion in regulatory capital,

requiring replacement with new capital instruments that meet the new criteria. Sometimes changes are

introduced subject to a transitional period during which the new requirements are being phased in,

gradually progressing to a fully phased-in, or fully-loaded, application of the requirements.

Any failure to comply with these requirements, or to adapt to changes in such requirements, may have a

material adverse effect on our business, results and financial condition, and may require us to seek

additional capital. Failures to meet minimum capital or other prudential requirements may also result in ING

being prohibited from making payments on certain of our securities. Because implementation phases and

transposition into EU or national regulation where required may often involve a lengthy period, the impact

of changes in capital, liquidity and leverage regulations on our business, results and financial condition, and

on our ability to make payments on certain of our securities, is often unclear.

Our US commodities and derivatives business is subject to CFTC and SEC regulation

under the Dodd-Frank Act.

Our affiliate ING Capital Markets LLC is registered with the Commodity Futures Trading Commission (CFTC) as

a swap dealer and is subject to CFTC regulation of the off-exchange derivatives market pursuant to Title VII

of the US Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank). Operating as a swap

dealer requires compliance with CFTC regulatory requirements, which may be burdensome, impose

additional compliance costs and could adversely affect the profitability of this business, as well as exposing

ING to the risk of non-compliance with these regulations.

ING Capital Markets LLC is also registered with the SEC as a security-based swap dealer. Operating as a

security-based swap dealer requires compliance with SEC regulatory requirements, which may be

burdensome, impose additional compliance costs and could adversely affect the profitability of this

business, as well as exposing ING to the risk of non-compliance with these regulations. While most of these

SEC requirements apply to ING Capital Markets LLC, in addition to its CFTC swap dealer requirements, SEC

rules have permitted an Alternative Compliance Mechanism that allows for compliance, subject to eligibility

requirements, with CFTC capital and margin rules applying to swap dealers in lieu of SEC capital and margin

rules applying to security-based swap dealers. ING Capital Markets LLC has elected to use the Alternative

Compliance Mechanism. However, should ING Capital Markets LLC in the future be ineligible for the

Alternative Compliance Mechanism it would be subject to SEC security-based swap dealer rules for margin,

capital, and related financial reporting instead of the CFTC swap dealer rules which could be more capital-

intensive.

On 15 December 2021, the SEC proposed new rules that would for the first time impose public reporting

requirements for some significant security-based swaps positions. The rules would apply even to trades

between non-US counterparties, including ING Bank, provided that the issuer of the reference securities

underlying the security-based swaps is organised in the US, the issuer of the reference securities underlying

the security-based swaps has its principal place of business in the US, or the securities are in certain

categories registered with the SEC.

These proposed regulations, if adopted in their current form, could constrain trading activity in security-

based swaps. In addition, there are, or may be in the future, regulatory requirements or limitations related

to other categories of equity derivatives, such as options or forwards, that could similarly constrain trading

activity in such instruments as well. These various requirements and limitations with respect to equity

ING Group Annual Report 2023 on Form 20-F 13

derivatives generally could have a significant impact on the liquidity and utility of these markets, materially

impacting ING’s business in this market.

In addition, position limits requirements have been imposed by the CFTC for enumerated listed futures

referencing twenty-five physical commodities. In addition, on 1 January 2023, these position limits were

extended to certain positions in swaps that are “economically equivalent” to the enumerated futures

contracts. The position limits on futures and related swaps could limit ING’s position sizes in these swaps

referencing specified physical commodities and similarly limit the ability of counterparties to utilise certain

of our products, to the extent that hedging exemptions from the position limits are unavailable. Any of the

foregoing factors, and any further regulatory developments with respect to commodities and derivatives,

could have a material impact on our business, results and financial condition.

We are subject to several other bank recovery and resolution regimes that include

statutory write-down and conversion as well as other powers, which remains subject to

significant uncertainties as to scope and impact on us.

We are subject to several recovery and resolution regimes, including the Single Resolution Mechanism (SRM),

the ‘Bank Recovery and Resolution Directive’ (BRRD) as implemented in national legislation, such as the

Dutch Financial Supervision Act. The SRM applies to banks that are supervised by the ECB under the SSM,

with the aim of ensuring an orderly resolution of failing banks at minimum cost for taxpayers and the real

economy. The BRRD establishes a common framework for the recovery and resolution of banks within the

European Union, with the aim of providing supervisory authorities and resolution authorities with common

tools and powers to address banking crises pre-emptively to safeguard financial stability and minimise

taxpayers’ exposure to losses. Any application of statutory write-down and conversion or other powers

would not be expected to constitute an event of default under our securities entitling holders to seek

repayment. If any of these powers were to be exercised in respect of ING, there could be a material adverse

effect on both ING and on holders of ING securities, including through a material adverse effect on credit

ratings and/or the price of our securities. Investors in our securities may lose their investment if resolution

measures are taken under current or future regimes.

Risks related to litigation, enforcement proceedings and investigations and to changes

in tax laws

We may be subject to litigation, enforcement proceedings, investigations or other

regulatory actions, and adverse publicity.

We are involved in governmental, regulatory, arbitration and legal proceedings and investigations involving

claims by and against us which arise in the ordinary course of our businesses, including in connection with

our activities as financial services provider, employer, investor and taxpayer. As a financial institution, we

are subject to specific laws and regulations governing financial services and/or financial institutions. See

'Risks related to the regulation and supervision of the Group. Changes in laws and/or regulations governing

financial services or financial institutions or the application of such laws and/or regulations may increase our

operating costs and limit our activities' and 'Our US commodities and derivatives business is subject to CFTC

and SEC regulation under the Dodd-Frank Act' above. Financial reporting irregularities involving other large

and well-known companies, possible findings of government authorities in various jurisdictions which are

investigating several processes, notifications made by whistleblowers, increasing regulatory and law

enforcement scrutiny of ‘know your customer’ anti-money laundering regulations, tax evasion, prohibited

transactions with countries or persons subject to sanctions, and bribery or other anti-corruption measures

and anti-terrorist-financing procedures and their effectiveness, regulatory investigations of the banking

industry, and litigation that arises from the failure or perceived failure by us to comply with legal,

regulatory, tax and compliance requirements could result in adverse publicity and reputational harm, lead

to increased regulatory supervision, affect our ability to attract and retain customers and employees and

maintain access to the capital markets, result in cease and desist orders, claims, enforcement actions, fines

and civil and criminal penalties, other disciplinary action or have other material adverse effects on us in

ways that are not predictable. With respect to sanctions, Russia’s invasion of Ukraine has fundamentally

changed the global political landscape, resulting in a world-wide response, whereby new and significant

sanctions packages were imposed against Russia and Belarus during 2022 and 2023. During 2023, there

have been several noteworthy developments highlighting the increasing focus of the EU, US, and other

governments on the potential circumvention of sanctions against Russia, and the roles of third countries

and companies in facilitating the circumvention or undermining of such sanction’s measures. This has

prompted a concerted effort by governments to impose pressure on companies operating in these

jurisdictions, and to stop the sanctions measures from being sidestepped by targeted Russian parties. The

EU introduced additional measures combating sanctions circumvention and several locations have come

into focus as potential diversion hubs. While various sanctions include grace periods before full compliance

is required, there is no guarantee that ING will be able to implement all required procedures within the

applicable grace periods. In addition, some claims and allegations may be brought by or on behalf of a class

and claimants may seek large or indeterminate amounts of damages, including compensatory, liquidated,

treble and punitive damages. Our reserves for litigation liabilities may prove to be inadequate. Claims and

allegations, should they become public, need not be well founded, true or successful to have a negative

impact on our reputation. In addition, press reports and other public statements that assert some form of

wrongdoing could result in inquiries or investigations by regulators, legislators and law enforcement

officials, and responding to these inquiries and investigations, regardless of their ultimate outcome, is time

consuming and expensive. Adverse publicity, claims and allegations, litigation and regulatory investigations

and sanctions may have a material adverse effect on our business, results, financial condition and/or

prospects in any given period.

ING Group Annual Report 2023 on Form 20-F 14

We are subject to different tax regulations in each of the jurisdictions where we

conduct business, and are exposed to changes in tax laws, and risks of non-compliance

with or proceedings or investigations with respect to, tax laws.

Changes in tax laws (including case law) and tax treaties (including the termination thereof) could increase

our taxes and our effective tax rates and could materially impact our tax receivables and liabilities as well as

deferred tax assets and deferred tax liabilities, which could have a material adverse effect on our business,

results and financial condition. Changes in tax laws could also make certain ING products less attractive,

which could have adverse consequences for our businesses and results. On 7 June 2021, the Dutch

government received a formal notice of termination of the Dutch-Russian tax treaty from Russia, and as a

result, the tax treaty was terminated as of 1 January 2022. The termination of the Dutch-Russian tax treaty

or any other similar developments may have adverse effects on ING and ING’s customers.

Because of the geographic spread of its business, ING may be subject to tax audits, investigations and

procedures in numerous jurisdictions at any point in time. Although we believe that we have adequately

provided for all our tax positions, the ultimate resolution of these audits, investigations and procedures may

result in liabilities which are different from the amounts recognized. In addition, increased bank taxes in

countries where the Group is active result in increased taxes on ING’s banking operations, which could

negatively impact our operations, financial condition and liquidity.

We may be subject to tax investigations under EU, US and local laws if we fail to comply

with our obligations

Due to the nature of its business, ING is subject to various provisions of EU, US, and other local tax laws in

relation to its customers. These include amongst others the Foreign Account Tax Compliance Act (“FATCA”),

which requires ING to provide certain information for the US Internal Revenue Service (IRS), the Qualified

Intermediary (QI) requirements, which require withholding tax on certain US-source payments, and the

Common Reporting Standards (CRS) which requires ING to provide certain information to local tax

authorities. Failure to comply with these requirements and regulations could harm our reputation and could

subject the Group to enforcement actions, fines and penalties, which could have a material adverse effect

on our business, reputation, revenues, results, financial condition and prospects.

ING is exposed to the risk of claims from customers or stakeholders who feel misled or

treated unfairly because of advice or information received.

Our products and services, including banking products and advice services for third-party products are

exposed to claims from customers who might allege that they have received insufficient advice or

misleading information from advisers (both internal and external) as to which products were most

appropriate for them, or that the terms and conditions of the products, the nature of the products or the

circumstances under which the products were sold, were misrepresented to them. When new financial

products are brought to the market, it is ING’s policy to engage in a multidisciplinary product approval

process in connection with the development and distribution of such products, including production of

appropriate marketing and communication materials. Notwithstanding these processes, customers may

make claims against ING if the products do not meet their expectations , either at the purchase/execution of

the product and/or through the life of the product. Customer protection regulations, as well as changes in

interpretation and perception by both the public at large and governmental authorities of acceptable

market practices, influence customer expectations

Products distributed through person-to-person sales forces have a higher exposure to such claims as the

sales forces may provide face-to-face financial planning and advisory services. Complaints may also arise if

customers feel that they have not been treated reasonably or fairly, or that the duty of care has not been

complied with. While a considerable amount of time and resources have been invested in reviewing and

assessing historical sales practices and products that were sold in the past, and in the maintenance of risk

management, legal and compliance procedures to monitor current sales practices, there can be no

assurance that all of the issues associated with current and historical sales practices have been or will be

identified, nor that any issues already identified will not be more widespread than presently estimated.

The negative publicity associated with any sales practices, any compensation payable in respect of any

such issues and regulatory changes resulting from such issues, has had and could have a material adverse

effect on our reputation, business, results, financial condition and prospects. For additional information

regarding legal proceedings or claims, see Note 45 ‘Legal proceedings’ to the consolidated financial

statements.

Risks related to the Group’s business and operations

ING may be unable to meet internal or external aims or expectations or requirements

with respect to ESG-related matters.

Environmental, Social and Governance (ESG) is an area of significant and increased focus for governments

and regulators, investors, ING’s customers and employees, and other stakeholders or third parties (e.g., non-

governmental organisations or NGOs). As a result, an increasing number of laws, regulations and legislative

actions have been introduced to address climate change, sustainability and other ESG-related matters,

including in relation to the financial sector’s operations and strategy. Such recent regulations include the EU

Sustainable Finance Disclosure Regulation (SFDR), EU Taxonomy regulation and EU Green Bond Standards,

which broadly focus on disclosure obligations, standardized definitions and classification frameworks for

environmentally sustainable activities, and the EU Corporate Sustainability Reporting Directive (CSRD), which

requires certain companies, including us, to disclose information on what they see as the risks and

ING Group Annual Report 2023 on Form 20-F 15

opportunities arising from social and environmental issues, and on the impact of their activities on people

and the environment. Third parties may pursue litigation against ING in connection with ESG-related

matters, such as the recently announced potential claims by Friends of the Earth Netherlands

(Milieudefensie) in connection with financing provided by ING to certain companies whose business is reliant

on fossil fuels.

These laws, regulations and legislative frameworks may directly and indirectly impact the business

environment in which ING operates and may expose ING to significant risks, including amongst others,

greenwashing risk and the risk of litigation if governmental standards or community expectations are not

met.

National or international regulatory actions or developments may also result in financial institutions coming

under increased pressure from internal and external stakeholders regarding the management and

disclosure of their ESG risks and related lending and investment activities. ING may from time to time

disclose ESG-related initiatives or aims in connection with the conduct of its business and operations.

However, there is no guarantee that ING will be able to implement such initiatives or meet such aims within

anticipated timeframes, or at all. ING may fail to fulfil internal or external ESG-related initiatives, aims or

expectations, or may be perceived to fail to do so, or may fail to adequately or accurately report

performance or developments with respect to such initiatives, aims or expectations. ING could therefore be

criticised or held responsible for the scope of its initiatives or goals regarding such matters. In addition, ING

might face requests for specific strategies, plans or commitments to address ESG-related matters, which

may or may not be viewed as satisfactory to the relevant internal and external stakeholders (including

NGOs). Any of these factors may have an adverse impact on ING’s reputation and brand value, or on ING’s

business, financial condition and operating results.

ING may be unable to adapt its products and services to meet changing customer

behaviour and demand, including as a result of ESG-related matters.

Customers or other counterparties may increasingly assess sustainability or other ESG-related matters in

their economic decisions. For instance, customers may choose investment products or services based on

sustainability or other ESG criteria, or may look at a financial institution’s ESG-related lending strategy when

choosing to make deposits. To remain competitive and to safeguard its reputation, ING is required to

continuously adapt its business strategy, products and services to respond to emerging, increasing or

changing sustainability and other ESG-related demands from customers, investors and other stakeholders.

However, there is no guarantee that ING’s current or future products or services will meet applicable ESG-

related regulatory requirements, customer preferences or investor expectations.

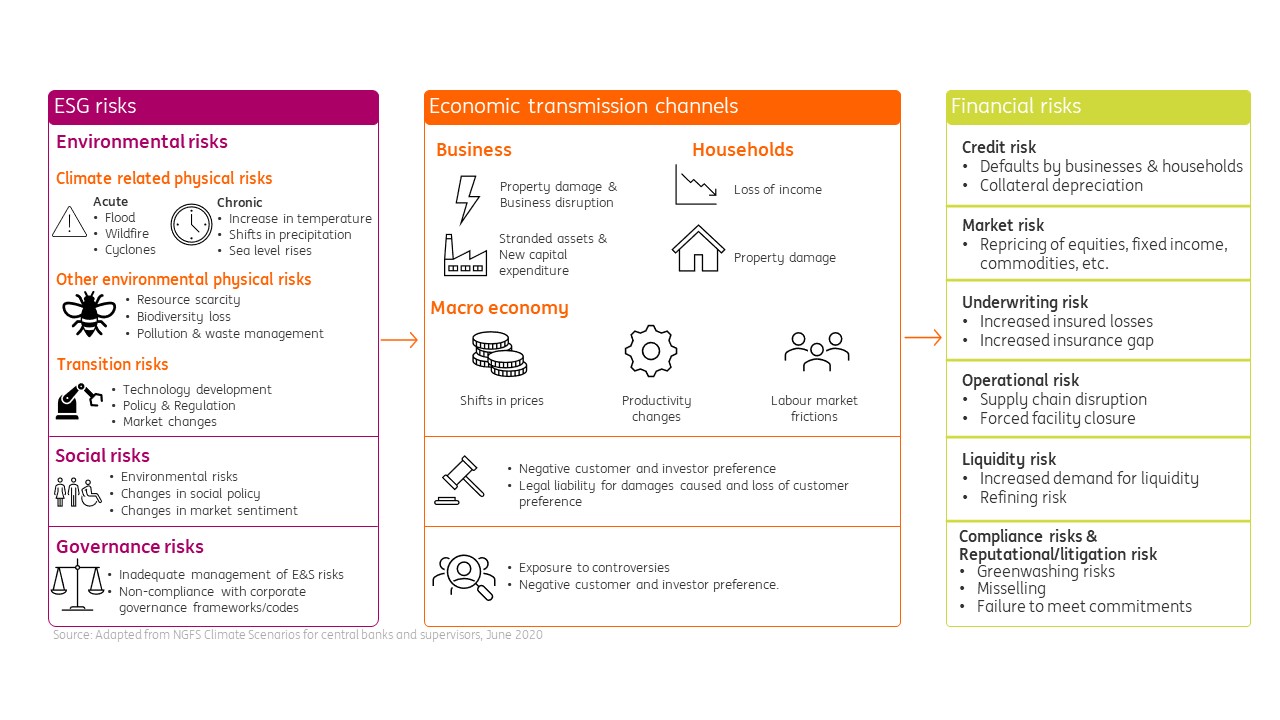

ING’s business and operations are exposed to transition risks related to climate change.

The transition to a low-carbon or net-zero economy gives rise to risks and uncertainties associated with

climate change-related laws, regulations and oversight, changing or new technologies, and shifting

customer sentiment. For instance, ING may be required to change its lending portfolio to comply with new

climate change-related regulations and other ESG-related demands from customers, investors and other

stakeholders. As a result, it might be unable and unwilling to lend to certain prospective customers, or lead

to the termination of certain existing relationships with certain customers. This could result in claims or legal

challenges from such customers against ING. This transition may also adversely impact the business and

operations of ING’s customers and other counterparties. Further, there is a risk that changing community

standards and market expectations could lead to a reduction in demand and a decline in valuations for

certain assets, which may affect the value of collateral we hold or the financial strength of certain of our

portfolios. If ING fails to adequately factor in such risks in its lending or other business decisions, ING could

be exposed to losses.

The low carbon or net zero transition may also require ING to modify or implement new compliance

systems, internal controls and procedures or governance frameworks. The integration and automation of

internal governance, compliance, and disclosure and reporting frameworks across ING could lead to

increased operational costs for ING and other execution and operational risks. The implementation cost of

these systems may especially be higher in the near term as ING seeks to adapt its business, or address

overlapping, duplicative or conflicting regulatory or other requirements in this fast-developing area.

Furthermore, ING’s ongoing implementation of appropriate systems, controls and frameworks increasingly

requires ING to develop adequate climate change-related risk assessment and modelling capabilities (as

there is currently no standard approach or methodology available), and to collect customer, third party or

other data. There are significant risks and uncertainties inherent in the development of new risk modelling

methodologies and the collection of data, potentially resulting in systems or frameworks that could be

inadequate, inaccurate or susceptible to incorrect customer, third party or other data.

Any delay or failure in developing, implementing or meeting ING’s climate change-related commitments

and regulatory requirements may have a material adverse impact on our business, financial condition,

operating results and reputation, and lead to climate change or ESG-related investigations, enforcement

proceedings or litigation.

ING’s business and operations are exposed to physical risks, including as a direct result

of climate change.

ING’s business and operations may be exposed to the impacts of physical risks arising from climate and

weather-related events, including heatwaves, droughts, flooding, storms, rising sea levels, other extreme

weather events or natural disasters, and to the impacts of physical risks arising from the environmental

ING Group Annual Report 2023 on Form 20-F 16

degradation, including loss of biodiversity, water or resources scarcity, pollution or waste management.

Such physical risks could disrupt ING’s business continuity and operations or impact ING’s premises or

property portfolio, as well as its customers’ property, business or other financial interests. These risks could

potentially result in impairing asset values, financial losses, declining creditworthiness of customers and

increased defaults, delinquencies, write-offs and impairment charges in ING’s portfolio, etc. In particular,

changing climate patterns resulting in more frequent and extreme weather events, such as the severe

flooding that occurred in Western Europe in July 2021, the long-lasting bushfires in Australia in February

2021 or the severe flooding in the eastern states of Australia in early 2022, could lead to unexpected

business interruptions or losses for ING or its customers.

For a description of physical risks to our operations and business other than resulting from natural disasters

as a result of climate change, see 'Operational and IT risks, such as systems disruptions or failures, breaches

of security, cyber attacks, human error, changes in operational practices, inadequate controls including in

respect of third parties with which we do business or outbreaks of communicable diseases may adversely

impact our reputation, business and results' below.

Operational and IT risks, such as systems disruptions or failures, breaches of security,

human error, changes in operational practices, inadequate controls including in respect

of third parties with which we do business or outbreaks of communicable diseases may

adversely impact our reputation, business and results.

Operational and IT risks are inherent to our business. Our clients depend on our ability to process and report

a large number of transactions efficiently and accurately. In addition, we routinely transmit, receive and

store personal, confidential and proprietary information electronically. Losses can result from inadequately

trained or skilled personnel, IT failures (including due to a cyber attack), inadequate or failed internal control

processes and systems (including, as the role of Artificial Intelligence in the finance industry and in our

business increases, any errors as a result of incomplete, inaccurate, or otherwise flawed outputs from the

algorithms and data sets utilized), regulatory breaches, human errors, employee misconduct, including

fraud, or from natural disasters or other external events that interrupt normal business operations. Such

losses may adversely affect our reputation, business and results.

We depend on the secure processing, storage and transmission of confidential and other information in our

computer systems and networks. The equipment and software used in our computer systems and networks

may not always be capable of processing, storing or transmitting information as expected. Despite our

business continuity plans and procedures, certain of our computer systems and networks may have

insufficient recovery capabilities in the event of a malfunction or loss of data. We are consistently managing

and monitoring our IT risk profile globally. ING is subject to increasing regulatory requirements including EU

General Data Protection Regulation (GDPR) and EU Payment Services Directive (PSD2) and the new Digital

Operational Resilience Act (DORA) which will enter into force in January 2025. Failure to appropriately

manage and monitor our IT risk profile could affect our ability to comply with these regulatory

requirements, to securely and efficiently serve our clients or to timely, completely or accurately process,

store and transmit information, and may adversely impact our reputation, business and results. For further

description of the particular risks associated with cybercrime, which is a specific risk to ING as a result of its

strategic focus on technology and innovation, see 'We are subject to increasing risks related to cybercrime

and compliance with cybersecurity regulation' below.

In addition, as finance industry participants are increasingly incorporating Artificial Intelligence into their

processes and systems, the risk of data and information leaks is correspondingly increasing. Our or our

customers’ sensitive, proprietary, or confidential information could be leaked, disclosed, or revealed as a

result of or in connection with our or our third-party providers’ use of generative or other Artifical

Intelligence technologies. Any such information that we input into a third-party generative or other Artificial

Intelligence or machine learning platform could be revealed to others, including if information is used to

train the third party's Artificial Intelligence models. Additionally, where an Artificial Intelligence model

ingests personal information and makes connections using such data, those technologies may reveal other

sensitive, proprietary, or confidential information generated by the model.

Widespread outbreaks of communicable diseases may impact the health of our employees, increasing

absenteeism, or may cause a significant increase in the utilisation of health benefits offered to our

employees, either or both of which could adversely impact our business. Further, as a result of the Covid-19