UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________

FORM

____________________________

OR

For the fiscal year ended

OR

OR

Commission File Number

____________________________

Itaú Unibanco Holding S.A.

(Exact Name of Registrant as Specified in its Charter)

Itaú

Unibanco Holding S.A.

(Translation of Registrant’s name into English)

The Federative Republic of Brazil

(Jurisdiction of incorporation or organization)

____________________________

Group Head of Investor Relations

Itaú Unibanco Holding S.A.

+

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

_____________________________________________________________________________

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading Symbol (s) | Name of each exchange on which registered |

| Preferred Shares, without par value | |

New York Stock Exchange* |

| |

______________

*Not for trading purposes, but only in connection with the listing on the New York Stock Exchange of American Depositary Shares representing those Preferred Shares.

____________________________

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the period covered by the annual report:

Common Shares, no par value per share

4,842,576,301 Preferred Shares, no par value per share

Indicate by check mark if the registrant

is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act

☒

If this annual report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐

Yes ☒

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of

its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public

accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☐ U.S. GAAP | ☒ |

☐ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐

Yes

| Audit Firm Id: |

Auditor Name: |

Auditor Location: |

Table of Contents

INTRODUCTION

Certain Terms and Conventions

All references in this annual report to (i) “Itaú Unibanco Holding,” “Itaú Unibanco Group,” “we,” “us” or “our” are references to Itaú Unibanco Holding S.A. and its consolidated subsidiaries and affiliates, except where specified or differently required by the context; (ii) the “Brazilian government” are references to the federal government of the Federative Republic of Brazil, or Brazil; (iii) “preferred shares” are references to our authorized and outstanding preferred shares with no par value; and (iv)“common shares” are references to our authorized and outstanding common shares with no par value. All references to “ADSs” are to American Depositary Shares, each representing one preferred share, without par value. The ADSs are evidenced by American Depositary Receipts, or “ADRs,” issued by The Bank of New York Mellon, or BNY Mellon. All references herein to the “real,” “reais” or “R$” are to the Brazilian real, the official currency of Brazil. All references to “US$,” “dollars” or “U.S. dollars” are to United States dollars.

Additionally, unless specified or the context indicates otherwise, the following definitions apply throughout this annual report:

| • | “Itaú Unibanco” means Itaú Unibanco S.A., together with its consolidated subsidiaries; |

| • | “Itaú BBA” means Banco Itaú BBA S.A., together with its consolidated subsidiaries; |

| • | “Central Bank” means the Central Bank of Brazil; |

| • | “CLP” means the Chilean peso, the official currency of Chile; |

| • | “CMN” means the Brazilian National Monetary Council; and |

| • | “CVM” means the Securities and Exchange Commission of Brazil. |

Additionally, acronyms used repeatedly, defined and technical terms, specific market expressions and the full names of our main subsidiaries and other entities referenced in this annual report are explained or detailed in the section entitled “Glossary”.

| 1 |

Forward-Looking Statements

This annual report contains statements that are or may constitute forward-looking statements within the meaning of Section 27A of the U.S Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or Exchange Act. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting our business. These forward-looking statements are subject to risks, uncertainties and assumptions including, among other risks:

| • | Political instability in Brazil, including developments and the perception of risks in connection with the Brazilian elected government, as well as ongoing corruption and other investigations and increasing fractious relations and infighting within the administration of the Brazilian government, as well as policies and potential changes to address these matters or otherwise, including economic and fiscal reforms, any of which may negatively affect growth prospects in the Brazilian economy as a whole; |

| • | General economic, political, and business conditions in Brazil and variations in inflation indices, interest rates, foreign exchange rates, and the performance of financial markets in Brazil and the other markets in which we operate; |

| • | Global economic and political conditions, as well as geopolitical instability, in particular in the countries where we operate, including in relation to the United States, the Russian invasion of Ukraine and the Israel – Hamas conflict; |

| • | Changes in laws or regulations, including in respect of tax matters, compulsory deposits and reserve requirements, that adversely affect our business; |

| • | The effect of any changes in tax law, tax reforms or review of the tax treatment on our activities, our operations and profitability; |

| • | Disruptions and volatility in the global financial markets; |

| • | Costs and availability of funding; |

| • | Failure or hacking of our security and operational infrastructure or systems; |

| • | Our ability to protect personal data; |

| • | Our level of capitalization; |

| • | Increases in defaults by borrowers and other loan delinquencies, which result in increases in loan loss allowances; |

| • | Competition in our industry; |

| • | Changes in our loan portfolio and changes in the value of our securities and derivatives; |

| • | Customer losses or losses of other sources of revenues; |

| • | Our ability to execute our strategies and capital expenditure plans and to maintain and improve our operating performance; |

| • | Our exposure to Brazilian public debt; |

| • | Incorrect pricing methodologies for insurance, pension plan and premium bond products and inadequate reserves; |

| • | The effectiveness of our risk management policies; |

| • | Our ability to successfully integrate acquired or merged businesses; |

| • | Adverse legal or regulatory disputes or proceedings; |

| • | Environmental damage and climate change and effects from socio-environmental issues, including new and/or more stringent regulations relating to these issues; and |

| • | Other risk factors as set forth under “Item 3D. Risk Factors.” |

The words “believe”, “may”, “will”, “estimate”, “continue”, “anticipate”, “intend”, “expect” and similar words are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We undertake no obligation to update publicly or revise any forward-looking statements because of new information, future events or otherwise. In light of these risks and uncertainties, the forward-looking information, events and circumstances discussed in this annual report might not occur. Our actual results and performance could differ substantially from those anticipated in such forward-looking statements.

| 2 |

Presentation of Financial and Other Information

The information found in this annual report is accurate only as of the date of such information or as of the date of this annual report, as applicable. Our activities, our financial position and assets, the results of transactions and our prospects may have changed since that date.

Information contained in or accessible through our website or any other websites referenced herein does not form part of this annual report unless we specifically state that it is incorporated by reference and forms part of this annual report. All references in this annual report to websites are inactive textual references and are for information only.

Effect of Rounding

Certain amounts and percentages included in this annual report, including in the section of this annual report entitled “Item 5. Operating and Financial Review and Prospects” have been rounded for ease of presentation. Percentage figures included in this annual report have not been calculated in all cases on the basis of the rounded figures but on the basis of the original amounts prior to rounding. For this reason, certain percentage amounts in this annual report may vary from those obtained by performing the same calculations using the figures in the consolidated financial statements. Certain other amounts that appear in this annual report may not sum due to rounding.

Market and Industry Data

This annual report contains information, including statistical data, about certain markets and our competitive position. Except as otherwise indicated, this information is taken or derived from external sources. We indicate the name of the external source in each case where industry data is presented in this annual report. We cannot guarantee and we have not independently verified the accuracy of information taken from external sources, or that, in respect of internal estimates, a third party using different methods would obtain the same estimates as the estimates we present in this annual report.

About our financial Information

The reference date for the quantitative information for balances found in this annual report is as of December 31, 2023 and the reference date for results is the year ended December 31, 2023, except where otherwise indicated.

Our fiscal year ends on December 31 and, in this annual report, any reference to any specific fiscal year is to the twelve-month period ended on December 31 of that year.

The accounting principles and standards adopted in Brazil applicable to institutions authorized to operate by the Central Bank, or BRGAAP, include those established under Brazilian Corporate Law, by the Accounting Pronouncements Committee ("Comitê de Pronunciamentos Contábeis") or CPC which started issuing standards in 2007, and by the Federal Accounting Council (“Conselho Federal de Contabilidade”) or CFC. In the case of companies subject to regulation by the Central Bank, such as us, the effectiveness of the accounting pronouncements issued by entities such as the CPC depends on approval of the pronouncement by the CMN,which also establishes the date of effectiveness of any pronouncements with respect to financial institutions. Additionally, CVM and other regulatory bodies, such as SUSEP and the Central Bank, provide additional industry-specific guidelines.

The CMN establishes that financial institutions must present consolidated financial statements in accordance with the International Financial Reporting Standards, issued by the International Accounting Standards Board IASB, currently described as “IFRS Accounting Standards” by the IFRS Foundation.

Our consolidated financial statements, included elsewhere in this annual report, are prepared in accordance with IFRS Accounting Standards. Unless otherwise stated all consolidated financial information related to the years ended December 31, 2023, 2022 and 2021 included in this annual report was prepared in accordance with IFRS Accounting Standards as issued by IASB.

Our books and records are maintained in Brazilian reais, the official currency in Brazil and we use BRGAAP for our reports to Brazilian stockholders and calculation of payments of dividends.

For further information about the main differences between our management reporting systems and the consolidated financial statements prepared in accordance with IFRS Accounting Standards as issued by the IASB see “Note 30 – Segment Information” to our consolidated financial statements.

Our consolidated financial statements as of December 31, 2023 and 2022 and for each of the years ended December 31, 2023, 2022 and 2021 were by PricewaterhouseCoopers Auditores Independentes Ltda., or PwC, independent registered public accounting firm, as stated in its audit report contained in this Form 20-F.

| 3 |

PART I

ITEM 1. |

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS |

Not applicable.

|

ITEM 2. |

OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

|

ITEM 3. |

KEY INFORMATION |

ITEM 3A. [RESERVED]

3B. Capitalization and Indebtedness

Not applicable.

3C. Reasons for the Offer and Use of Proceeds

Not applicable.

3D. Risk Factors

This section addresses the risks we consider material to our business and an investment in our securities. Should any of the following risks actually occur, our business and financial condition, as well as the value of any investments made in our securities, will be adversely affected. Accordingly, investors should carefully assess the risk factors described below and the information disclosed in this annual report before making an investment decision. The risks described below are those that we currently believe may adversely affect us. Other risks that we do not presently consider material, emerging risks or risks not currently known to us may also adversely affect us.

Summary of Risk Factors

Macroeconomic and Geopolitical Risks

| • | Changes in macroeconomic and geopolitical conditions may adversely affect us. |

| • | Developments and the perception of risk of other countries may adversely affect the Brazilian economy and the market price of Brazilian securities. |

| • | The Brazilian government has exercised, and continues to exercise, influence over the Brazilian economy. This influence, as well as Brazilian political and economic conditions, may adversely affect us. |

| • | Inflation and fluctuation in interest rates could have a material adverse effect on our business, financial condition and results of operations. |

| • | Political instability in Brazil may adversely affect us. |

| • | Exchange rate instability may adversely affect the Brazilian economy and, as a result, us. |

| • | Any downgrading of Brazil’s credit rating may adversely affect us. |

Communicable Diseases

| • | The outbreak of communicable diseases around the world has led and may continue to lead to higher volatility in the global capital markets, adversely affecting the trading price of our shares. |

Regulatory, Compliance and Legal

| • | We are subject to regulation on a consolidated basis and may be subject to liquidation or intervention on a consolidated basis. |

| • | Changes in applicable law or regulations may have a material adverse effect on our business. |

| • | Increases in compulsory deposit requirements may have a material adverse effect on us. |

| 4 |

| • | Any changes in tax law, tax reforms or review of the tax treatment of our activities may adversely affect our operations and profitability. |

| • | Our insurance operations are subject to oversight by regulatory agencies and we may be negatively affected by penalties imposed by them. |

| • | We are subject to financial and reputational risks arising from legal and regulatory proceedings. |

Market

| • | The value of our investment securities and derivative financial instruments is subject to market fluctuations due to changes in Brazilian or international economic conditions and, as a result, may subject us to material losses. |

| • | Mismatches between our loan portfolio and our sources of funds regarding interest rates and maturities could adversely affect us and our ability to expand our loan portfolio. |

Credit

| • | Our historical loan losses may not be indicative of future loan losses and changes in our business may adversely affect the quality of our loan portfolio. |

| • | Default by other financial institutions may adversely affect the financial markets in general and us. |

| • | Exposure to Brazilian government debt could have a material adverse effect on us. |

| • | We may incur losses associated with counterparty exposure risks. |

Liquidity

| • | We face risks relating to liquidity of our capital resources. |

| • | Adverse developments affecting the financial services industry, such as actual events or concerns involving liquidity, defaults, or nonperformance by financial institutions or transactional counterparties, could adversely affect our current and projected business operations, financial condition and results of operations. |

| • | A downgrade of our credit ratings may adversely affect our access to funding or to the capital markets, increase our cost of funding or trigger additional collateral or funding requirements |

Business Operations

| • | A failure in, or breach of, our operational, security or IT systems could temporarily interrupt our businesses, increasing our costs and causing losses. |

| • | As the regulatory framework for artificial intelligence and machine learning technology evolves, our business, financial condition and results of operations may be adversely affected. |

| • | Failure to protect personal information could adversely affect us. |

| • | Failure to adequately protect ourselves against risks relating to cybersecurity could materially adversely affect us. |

| • | The loss of senior management, or our inability to attract and maintain key personnel could have a material adverse effect on us. |

| • | We may not be able to prevent our officers, employees or third parties acting on our behalf from engaging in situations that qualify as corruption in Brazil or in any other jurisdiction, which could expose us to administrative and judicial sanctions, as well as have an adverse effect to us. |

| • | We operate in international markets which subject us to risks associated with the legislative, judicial, accounting, regulatory, political and economic risks and conditions specific to such markets, which could adversely affect us or our foreign units. |

Strategy

| • | The integration of acquired or merged businesses involves certain risks that may have a material adverse effect on us. |

| • | Our controlling stockholder has the ability to direct our business. |

| 5 |

Management and Financial Reporting

| • | Our policies, procedures and models related to risk control may be ineffective and our results may be adversely affected by unexpected losses. |

| • | Inadequate pricing methodologies for insurance, pension plan and premium bond products may adversely affect us. |

Competition

| • | The increasingly competitive environment and consolidations in the Brazilian banking industry may have a material adverse effect on us. |

| • | We are subject to Brazilian antitrust legislation and that of other countries in which we operate or will possibly operate. |

Reputational Risk

| • | Damage to our reputation could harm our business and outlook. |

Concentration Risk

| • | We face risks related to market concentration. |

Environmental, Social and Climate Change Risks

| • | We may incur financial and reputational losses as a result of environmental and social risks. |

| • | Climate change may have adverse effects on our business and financial condition. |

Risk Factors for ADS Holders

| • | Holders of our shares and ADSs may not receive any dividends. |

| • | The relative price volatility and limited liquidity of the Brazilian capital markets may significantly limit the ability of our investors to sell the preferred shares underlying our ADSs, at the price and time they desire. |

| • | The preferred shares underlying our ADSs do not have voting rights, except in specific circumstances. |

| • | Holders of ADSs may be unable to exercise preemptive rights with respect to our preferred shares. |

| • | The surrender of ADSs may cause the loss of the ability to remit foreign currency abroad and of certain Brazilian tax advantages. |

| • | The holders of ADSs have rights that differ from those of stockholders of companies organized under the laws of the U.S. or other countries. |

Macroeconomic and Geopolitical Risks

Changes in macroeconomic and geopolitical conditions may adversely affect us.

Our operations are affected by changes in macroeconomic and geopolitical conditions globally, especially in Brazil and in other countries where we have operations.

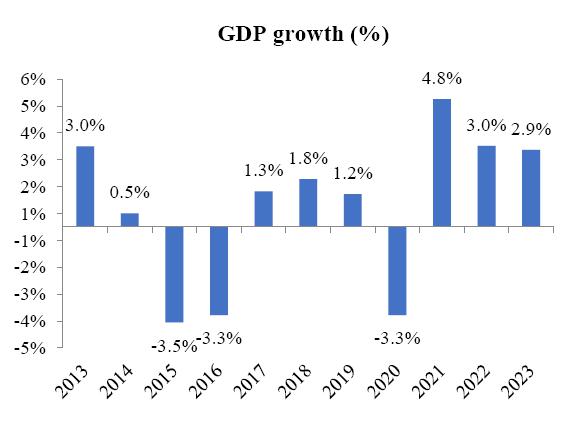

In Brazil, the demand for credit and financial services, as well as our clients’ ability to make payments when due, is directly impacted by macroeconomic variables, such as economic growth, income, unemployment, inflation, and fluctuations in interest and foreign exchange rates. Brazilian GDP increased by 4.8%, 3.0% and 2.9% in 2021, 2022 and 2023, respectively. For 2024, we expect that the GDP will increase by 2.3%. In addition, the unemployment rate has decreased throughout 2023 and reached 8.0% at the end of the year (compared to 8.5% in 2022 and 11.6% in 2021). These two indicators have a direct impact on the purchasing power of the Brazilian population and, consequently, on their ability to meet their financial and contractual obligations.

In the global scenario, the conflict between Russia and Ukraine and tensions between Russia and the U.S., the North Atlantic Treaty Organization, or NATO”, the European Union and the United Kingdom (“U.K”) resulted in the imposition of several financial and economic sanctions, as well as export controls against certain Russian organizations and/or individuals. The conflict and related developments could have further negative impacts on regional and global financial markets and economic conditions, which in turn could cause restrictions on our and our clients’ ability to enter into transactions with counterparties in Russia, higher volatility in foreign currency exchange rates, among other negative results. Escalation of other geopolitical issues, such as the conflict between Israel and Hamas, heightened tensions between Israel and some Arab countries, and/or enhanced geopolitical disputes between China and the U.S. could lead to constraints in commodity supply, causing a widespread rise in energy and food prices. Tighter monetary policies and financial conditions could impact economic growth. Higher interest rates in developed economies could also result in a reversal of capital flows to these countries, leading to the depreciation of the real, acceleration of inflation expectations and increase of domestic interest rates.

| 6 |

In addition, any material disruption and volatility in the global financial markets, including with respect to prices of securities, interest rates, inflation and foreign exchange rates, may adversely impact us. Higher uncertainty and volatility may result in a slowdown in the credit market and the economy, which, in turn, could lead to higher unemployment rates and a reduction in the purchasing power of the population in Brazil and in other countries where we have operations. In addition, such events may significantly impair our clients’ ability to perform their obligations and increase overdue or non-performing loans, resulting in an increase in the risk associated with our lending activity. All of these events could cause a material adverse effect on our business, results of operations and financial condition.

Developments and the perception of risk of other countries may adversely affect the Brazilian economy and the market price of Brazilian securities.

Economic and market conditions in other countries, including the U.S, the European Union and emerging market countries, may affect to varying degrees the market value of securities of Brazilian issuers, like us. Although economic conditions in these countries may differ significantly from economic conditions in Brazil, investors’ reactions to developments in these other countries may have a material adverse effect on the market value of securities of Brazilian issuers, the availability of credit in Brazil and the amount of foreign investment in Brazil. Crisis in the European Union, the U.S. and emerging market countries may diminish investor interest in securities of Brazilian issuers, including us. This could materially and adversely affect the market price of our securities and could also make it more difficult for us to access the capital markets and finance our operations in the future on acceptable terms or at all.

Banks located in countries considered to be emerging markets, like us, may be particularly susceptible to disruptions and reductions in the availability of credit or increases in financing costs, which could have a material adverse impact on our financial condition. In addition, the availability of credit to entities that operate within emerging markets is significantly influenced by levels of investor confidence in such markets as a whole and any factor that impacts market confidence (for example, a decrease in credit ratings or state or central bank intervention in one market) could materially and adversely affect the price or availability of funding for entities within any of these markets.

The Brazilian government has exercised, and continues to exercise, influence over the Brazilian economy. This influence, as well as Brazilian political and economic conditions, may adversely affect us.

The Brazilian government from time to time intervenes in the Brazilian economy and makes changes in policies and regulations. The Brazilian government’s actions have involved, in the past, among other measures, changes in interest rates, tax policies, price controls, monetary, restrictions on selected imports, and foreign exchange policies. Our business, financial condition, and results of operations may be materially and adversely affected by changes in policies or regulations involving or affecting factors, such as:

| • | interest rates; |

| • | reserve and capital requirements; |

| • | liquidity of capital, financial and credit markets; |

| • | general economic growth, inflation and currency fluctuations; |

| • | tax and regulatory policies; |

| • | restrictions on remittances abroad and other exchange controls; |

| • | increase in unemployment rates, decreases in wage and income levels; |

| • | other factors that influence our customers’ ability to meet their obligations with us; and |

| • | other political, diplomatic, social and economic developments within and outside Brazil that affect the country. |

Uncertainty over whether the Brazilian government will implement changes in policies or regulations affecting these and other factors in the future may contribute to heightened volatility in the Brazilian securities markets and in the securities of Brazilian issuers, which in turn may have a material adverse effect on us and, as a consequence, on the market price of our securities.

| 7 |

Inflation and fluctuation in interest rates could have a material adverse effect on our business, financial condition and results of operations.

Inflation and interest rate volatility have in the past caused material adverse effects in the Brazilian economy. Sudden increases in prices and long periods of high inflation may cause, among other effects, loss of purchasing power and distortions in the allocation of resources in the economy.

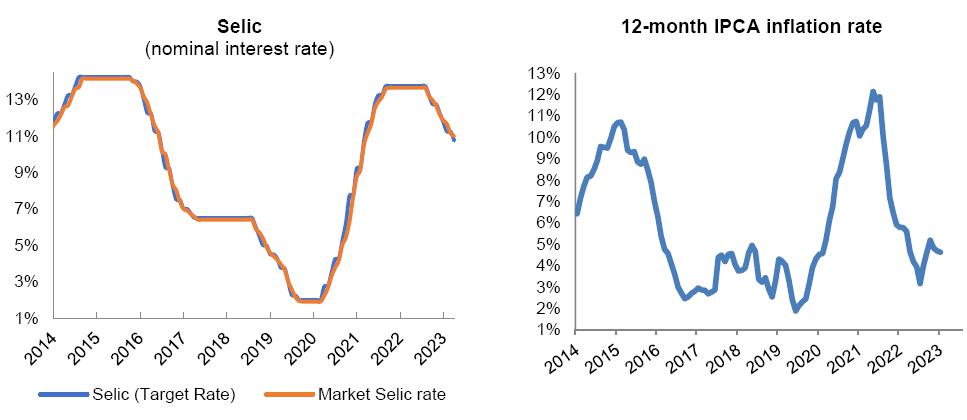

Historically, Brazil has experienced high inflation rates. Inflation and certain actions taken by the Central Bank to limit inflation may have significant negative effects on the Brazilian economy. Brazil’s General Price Index (Índice Geral de Preços – Mercado), or IGP-M index, recorded deflation of 3.2% in 2023, inflation of 5.5% in 2022 and inflation of 17.8% in 2021. Brazil’s National Broad Consumer Price Index (Índice Nacional de Preços ao Consumidor Amplo), or IPCA index, recorded inflation of 4.6% in 2023, 5.8% in 2022 and 10.1% in 2021. While inflation has clear negative impacts on household´s real income and ability to meet financial commitments, fighting inflationary pressures is not costless, Specifically, measures to combat high inflation rates include a tightening of monetary policies, with an increase in interest rates, resulting in restrictions on credit and short-term liquidity.

In Brazil, the Central Bank’s Monetary Policy Committee, or COPOM, is responsible for setting the Brazilian official interest rate, or the SELIC rate. The COPOM adjusts the official base interest rates to meet the economic goals established by the Brazilian government´s National Monetary Council. After reaching a historical low of 2.0% in August 2020, the COPOM began increasing interest rates in March 2021 and, as a result, the SELIC rate reached 9.25% in December 2021 and 13.75% in August 2022, where it remained until July 2023. In August 2023, the COPOM started easing interest rates and decreased the SELIC rate in 50 basis points, to 13.25%. At subsequent meetings it maintained this pace, and the SELIC rate reached 11.75% in December 2023 and 10.75% in March 2024.

The rise in inflation in several developed economies has led the authorities of these countries to begin reversing the strongly stimulative policies implemented during the COVID-19 pandemic. The U.S. Federal Reserve, or Fed, increased interest rates from 0.08% in 2021 to 4.33% in 2022 and to 5.38% in 2023. Monetary tightening, combined with the resolution of supply bottlenecks and the fall in commodity prices in 2023, has contributed to lower inflation rates for both goods and services. The central banks of developed markets should start easing interest rates in 2024. However, resilient activity and services inflation are likely to lead the Fed to cut rates only once this year, in December.

In the international scenario, inflation reached record highs in 2021 and 2022. In the U.S., the Consumer Price Index, or CPI, rose by 7.0% in 2021, 6.5% in 2022 and 3.4% in 2023. In Europe, consumer inflation measured by the Harmonised Index of Consumer Prices, or HICP, reached 5.0% in 2021, 9.2% in 2022, and 2.9% in 2023.

Significant changes in inflation and interest rates may have a material effect on our net margins, since they impact our costs of funding and granting credit. In addition, increases in interest rates could reduce demand for credit and increase the costs of our reserves and the risk of default by our clients. Conversely, decreases in interest rates could reduce our gains from interest-bearing assets, as well as our net margins.

Political instability in Brazil may adversely affect us.

The Brazilian economy has been and continues to be affected by political events in Brazil, which have also affected the confidence of investors and the public in general, adversely affecting the performance of the Brazilian economy and heightening volatility of securities issued by Brazilian companies, including the trading price of our shares and ADSs.

Brazilian markets have experienced heightened volatility due to uncertainties from investigations related to allegations of money laundering, corruption and misconduct by government officials and legal entities and individuals from the private sector carried out by the Brazilian Federal Police and the Office of the Brazilian Federal Prosecutor. Uncertainties derived from these events have adversely affected the Brazilian economy and political environment. We have no control over and cannot predict developments in these investigations nor whether future investigations or allegations will result in further political and economic instability, which could adversely affect the trading price of securities issued by Brazilian companies, including ours.

In October 2022, Brazil held elections for President, senators, federal legislators, state governors, state legislators and former President Luiz Inácio Lula da Silva was elected, representing distinctly opposing political ideologies as compared to those of the previous president Jair Bolsonaro. Political bipolarization between the left and right wings tends to enhance political instability, which could adversely affect the economy and therefore us.

In 2022, the Brazilian Congress enacted the transition constitutional amendment (“Transition PEC”) upon the election of the President Luiz Inácio Lula da Silva and transition to the newly elected government. The Transition PEC implied a significant increase in public spending in 2023, which, along with the settlement of court-ordered payments being fully classified as primary expenditures, resulted in a primary budget deficit of 2.3% of the GDP in 2023, compared with a surplus equivalent to 1.2% of GDP in 2022.

The Brazilian government has the power to determine policies and issue governmental acts related to the Brazilian economy that affect the operations and financial performance of companies, including us. We cannot predict which policies will be adopted or if these policies or changes in current policies may have an adverse effect on us or the Brazilian economy.

In August 2023, a new fiscal framework was approved by the Brazilian Congress. The approval and implementation of measures to rebuild government revenues will be key for the success of the fiscal framework and for the promised convergence of the primary budget result. We expect primary budget deficit of 0.6% of GDP in 2024 and 0.9% in 2025. The gross debt increased from 71.7% of GDP in 2022 to 74.4% in 2023, and we expect that it will increase to 77.2% and 80.6% in 2024 and 2025, respectively. For further information on Brazil’s economic performance and key indicators, see “ Item 5. Operating and Financial Review and Prospects – Brazilian Context.”

| 8 |

Uncertainty regarding political developments and the policies the Brazilian federal government may adopt or alter, as well as the government's willingness to limit expenses, may have material adverse effects on the macroeconomic environment in Brazil, as well as on the operations and financial performance of businesses operating in Brazil, including ours. These uncertainties may heighten the volatility of the Brazilian securities market, including in relation to our shares and ADSs.

Any of the above factors may create additional political uncertainty, which could have a material impact on the Brazilian economy and on our business, financial condition and results of operations.

Exchange rate instability may adversely affect the Brazilian economy and, as a result, us.

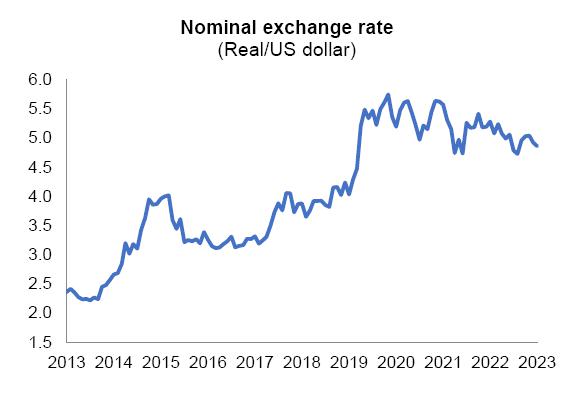

The real has suffered significant depreciations and appreciations in relation to the U.S. dollar and other strong foreign currencies in the last four decades. During this period, the Brazilian government implemented several economic plans and exchange rate policies, including sudden devaluations, periodic mini- devaluations, exchange controls, dual exchange rate markets and a floating exchange rate system.

In 2021, the Brazilian real depreciated by 7.4% against the U.S. dollar and on December 31, 2021, the real/U.S. dollar selling exchange rate was R$5.5805 per US$1.00. In 2022, the real appreciated by 6.5% against the U.S. dollar and on December 31, 2022, the real/U.S. dollar selling exchange rate was R$5.2177 per US$1.00. As of December 31, 2023, the real appreciated against the U.S. dollar, with the exchange rate reaching R$4.8413 per US$1.00.

We cannot assure you that the real will not significantly appreciate or depreciate in relation to the U.S. dollar and we have no control over and cannot predict the Brazilian foreign exchange policy. Depreciation of the real may create additional inflationary pressures in Brazil and cause increases in interest rates, which may negatively affect the overall Brazilian economy and, consequently, us, due to decreased consumption and increased costs. Appreciation could impair competitiveness and affect the creditworthiness of firms in exporting sectors.

Communicable Diseases

The outbreak of communicable diseases around the world has led and may continue to lead to higher volatility in the global capital markets, adversely affecting the trading price of our shares

The COVID-19 pandemic and governmental responses thereto had a severe impact on global and Brazilian macro-economic and financial conditions, including the disruption of supply chains and the closures or interruptions of many businesses, leading to losses of revenues, increased unemployment and economic stagnation and contraction. The COVID-19 pandemic also resulted in materially increased volatility in both Brazilian and international financial markets and economic indicators, including exchange rates, interest rates and credit spreads.

In Brazil, the stock market experienced automatic suspensions, known as “circuit-breakers,” as a result of significant volatility in stock trading caused by investors’ reactions to the uncertainty related to the COVID-19 pandemic in the global economy and the recessionary effect on the Brazilian economy. The B3 Index (IBOVESPA) dropped by 36.9% from January 1, 2020, to March 31, 2020, following the sharp drop in international equity markets. The trading piece of our shares was also adversely affected.

Measures that may be taken by governmental authorities worldwide, including in Brazil, to stabilize markets and support economic growth in the case of an outbreak of an epidemic or pandemic may not be sufficient to control volatility or to prevent serious and prolonged reductions in economic activity. These measures may have adverse macroeconomic effects and negatively influence the behavior of the consumer market and the population in general.

The effects of an outbreak of an epidemic or pandemic on our business will depend on, among other factors, the ultimate geographic spread of the disease, the duration of the outbreak and the extent and overall economic effects of the governmental response to it. In addition, the effects of the outbreak may exacerbate the effects of the other risk factors disclosed in this section of this annual report, including potential effects on the price and performance of our shares.

| 9 |

Regulatory, Compliance and Legal

We are subject to regulation on a consolidated basis and may be subject to liquidation or intervention on a consolidated basis.

We, through our subsidiaries, operate in several sectors related to the provision of credit and financial services. For purposes of regulation and supervision, the Central Bank deems Itaú Unibanco, its subsidiaries and affiliates to be a single financial institution. While our consolidated capital base provides financial strength and flexibility to our subsidiaries and affiliates, their individual activities could indirectly put our capital base at risk. Any investigation or intervention by the Central Bank in, the affairs of any of our subsidiaries and affiliates could have a material adverse impact on our other subsidiaries and affiliates and ultimately on us. If we or any of our financial subsidiaries become insolvent, the Central Bank may carry out an intervention or liquidation process on a consolidated basis rather than conduct such procedures for each individual entity. In the event of an intervention or a liquidation process on a consolidated basis, our creditors would have direct claims on our assets and the assets of our consolidated financial subsidiaries. In this case, claims of creditors of the same nature held against us and our consolidated financial subsidiaries would rank equally in respect of payment. Conversely, if the Central Bank carries out a liquidation or intervention process with respect to us or any of our financial subsidiaries on an individual basis, our creditors would not have a direct claim on the assets of such financial subsidiaries, and the creditors of such financial subsidiaries would have priority in relation to our creditors in connection with such financial subsidiaries’ assets. In addition, the Central Bank also has the authority to carry out other corporate reorganizations or transfers of control under an intervention or liquidation process, which may adversely affect us.

Changes in applicable law or regulations may have a material adverse effect on our business.

Brazilian banks, including us, are subject to extensive and continuous regulations and regulatory supervision by the Brazilian government, principally by the Central Bank. Changes in the law or regulations applicable to financial institutions in Brazil may adversely affect our operations, especially regulations imposing:

| • | minimum capital requirements; |

| • | reserve and compulsory deposit requirements; |

| • | insurance regulations; |

| • | restrictions on credit card and payroll loans activities, among other products and services offered by us; |

| • | minimum levels for federal housing and rural sector lending; |

| • | funding restrictions; |

| • | lending limits, earmarked lending and other credit restrictions; |

| • | limits on investments in property, plant and equipment; |

| • | environmental, social, and corporate governance requirements; |

| • | restrictions on remittances abroad and other exchange controls; |

| • | limitations on charging of commissions and fees by financial institutions for services to retail clients and the amount of interest financial institutions can charge; |

| • | accounting and statistical requirements; and |

| • | other requirements or limitations in the context of a global financial crisis. |

The regulatory framework governing Brazilian financial institutions, including banks, broker-dealers and leasing companies, and Brazilian insurance companies is continuously evolving. Disruptions and volatility in the global financial markets resulting in liquidity problems at major international financial institutions could lead the Brazilian government to change laws and regulations applicable to Brazilian financial institutions based on international developments. Any such changes or new laws and regulations could adversely affect us.

Moreover, there are several proposed bills under consideration in the Brazilian Congress that, if approved into law as currently drafted, could adversely affect us.

| 10 |

We also have operations outside of Brazil, including, but not limited to, Bahamas, the Cayman Islands, Chile, Colombia, Paraguay, Portugal, Switzerland, the United Kingdom, the U.S and Uruguay. Changes in the laws or regulations applicable to our business in the countries where we operate, or the adoption of new laws, and related regulations, may have an adverse effect on us.

For more information on the regulations applicable to our business, see "Item 4B. Business Overview-Supervision and Regulation".

Increases in compulsory deposit requirements may have a material adverse effect on us.

The Central Bank has periodically changed the level of reserves and compulsory deposits that financial institutions in Brazil are required to maintain with the Central Bank. The Central Bank may increase the reserve and compulsory deposits requirements or impose new requirements. Increases in reserve and compulsory deposit requirements reduce our liquidity to make loans and other investments and, as a result, may have a material adverse effect on business, financial condition and results of our operations.

Any changes in tax law, tax reforms or review of the tax treatment of our activities may adversely affect our operations and profitability.

As part of our ordinary course of business, we are subject to inspections by federal, municipal, and state tax authorities. The Brazilian government regularly amends tax laws and regulations, that may create new taxes, modify tax rates and change the calculation basis, taking into account that some of the changes may be applicable solely to the banking industry. Some of these amendments may increase, directly or indirectly, our tax burden, which may adversely affect our profitability.

In addition, certain tax laws may be subject to controversial interpretations. If the tax authorities interpret the tax laws inconsistently with our interpretation, we may be adversely affected, including the payment in full of taxes due, plus charges and penalties, which could adversely affect our results of operations. For instance, in February 2023 the Federal Supreme Court (Supremo Tribunal Federal) ruled that a final and unappealable decision on a tax matter that currently applies to the legal entity may lose its effects when there is a contrary judgment by the STF. This ruling may negatively impact taxpayers in general, including us, as it may lead to the obligation to pay for taxes that were not originally due.

Our insurance operations are subject to oversight by regulatory agencies and we may be negatively affected by penalties imposed by them.

We offer certain insurance products, including but not limited to health, life and car insurance. Insurance companies are subject to regulation and supervision from the Superintendence of Private Insurance ("Superintendência de Seguros Privados"), or SUSEP, including the possibility of intervention and/or liquidation in case of insufficient resources, technical reserves, or poor economic condition. In addition, insurance companies are subject to pecuniary penalties, warnings, suspension of authorization of activities and disqualification to engage in business activities.

As we provide health insurance products, we are also subject to the regulations of the Brazilian Health Agency (Agência Nacional de Saúde), or ANS. Health insurance companies facing financial distress or carrying out activities irregularly may be subject to penalties by ANS that range from warnings to the cancellation of the company’s authorization to operate and sale of its portfolio. In addition, ANS may also impose fiscal or technical direction regime or extrajudicial liquidation. Any changes in regulations imposed and penalties applied by SUSEP and ANS may adversely affect our insurance operations.

We are subject to financial and reputational risks arising from legal and regulatory proceedings.

As part of the ordinary course of our business, we face risks of losses arising from legal and regulatory proceedings, including but not limited to civil, labor and tax proceedings, that could subject us to inspections, monetary judgements, regulatory enforcement actions, compensation for damages, fines and penalties. We cannot predict the outcome of pending proceedings, or the potential loss, fines and penalties related to each pending matter. Accordingly, lawsuits and regulatory enforcement actions have resulted and will likely continue to result in judgments, settlement orders, penalties and fines that could have a material adverse effect on us.

For example, as described in note 29 to our consolidated financial statements, we are a defendant in lawsuits for the collection of understated inflation adjustment for savings resulting from the economic plans implemented in the 1980s and 1990s by the Brazilian government as a measure to combat inflation. While the Superior Court of Justice (Superior Tribunal de Justiça) has issued decisions favorable to holders of savings accounts, the Supreme Court of Brazil (Supremo Tribunal Federal), or STF has not ruled on the constitutionality of such economic plans and whether they are even applicable to savings accounts. In December 2017, representatives of banks and holders of savings accounts entered into a settlement agreement, but the low adherence to the agreement and the possible unfavorable judgment by the Supreme Court of Brazil may result in significant costs to the Brazilian banks and losses significantly higher than the amount of our provisions, which could have an adverse effect on our financial condition. In addition, we record reserves for probable losses that can be reasonably estimated or as otherwise required by Brazilian law. In case we are required to pay amounts for which we have no provisions, or that are higher than the provisions we made, we may be materially adversely affected.

| 11 |

Market

The value of our investment securities and derivative financial instruments is subject to market fluctuations due to changes in Brazilian or international economic conditions and, as a result, may subject us to material losses

In the ordinary course of our business, we use derivative financial instruments to hedge against currency risks and risk of losses due to movements in financial market prices in each of our business units, but we cannot guarantee that such use of derivatives will be sufficient to protect us against the aforementioned risks.

These investment securities and derivative financial instruments may cause us to record gains and losses at the time of sale or when they are marked to market, as the case may be, and may fluctuate considerably from period to period due to Brazilian and international economic conditions, including risks associated with transactions subject to variations in foreign exchange rates, interest rates, price indices, equity and commodity prices.

We cannot predict the amount of realized or unrealized gains or losses for any future period. Gains or losses on our investment securities and derivative financial instruments may not contribute to our net revenue in the future or may cease to contribute to our net revenue at levels consistent with more recent periods or at all. In addition, we may not successfully realize the appreciation or depreciation in our consolidated investment securities and derivative financial instruments or any portion thereof. Any of these factors may materially adversely affect our results of operations and financial condition.

Mismatches between our loan portfolio and our sources of funds regarding interest rates and maturities could adversely affect us and our ability to expand our loan portfolio

We are exposed to certain mismatches regarding interest rates and maturities between our credit portfolio and our sources of funds. A portion of our credit portfolio consists of floating and fixed interest rate and the profitability of credit operations depends on our ability to balance the cost to obtain funds with the interest rates charged to our clients. An increase in market interest rates in Brazil may increase our borrowing cost, especially the cost of time deposits, reducing the spread on loans, adversely affecting our operations. Any mismatch between our loan operations and related sources of funding may materially and adversely affect us.

An increase in the total cost of funding sources may result in an increase in the interest rates that we charge on the loans we grant and may consequently affect our ability to attract new customers. A decrease in the growth of our credit operations, as well as the illiquidity resulting from an inability to raise funds continuously, could adversely affect us.

Credit

Our historical loan losses may not be indicative of future loan losses and changes in our business may adversely affect the quality of our loan portfolio

As of December 31, 2023, our loan portfolio without endorsements and guarantees was R$910.6 billion, compared to R$909.4 billion as of December 31, 2022. Our allowance for loan losses was R$50.9 billion, representing 5.6% of our total loan portfolio, as of December 31, 2023, compared to R$ 52.3 billion, representing 5.8% of our total loan portfolio, as of December 31, 2022. Our historical loan loss experience may not be indicative of our future loan losses. While the quality of our loan portfolio is associated with the default risk of our clients and the sectors in which we operate, risks related to changes in our business resulting from organic growth and mergers and acquisitions, expansion of our loan portfolio to new sectors and clients, particularly individuals and small and middle-market companies. Changes in the Brazilian economic and political conditions, an increase in market competition, changes in regulation and in the tax regimes applicable to the sectors in which we operate and other related changes in countries in which we operate and in the international economic conditions, may also adversely affect the quality of our loan portfolio. Adverse changes affecting any large clients or the sectors to which we have significant lending exposure may have a material adverse impact on our business and our results of operations.

For example, historically, when Brazilian banks increased their loan portfolio to consumers, particularly in the retail sector, there was increased demand for credit card financing, which has been followed by a significant rise in the level of consumer indebtedness, leading to high nonperforming loan rates.

Our results of operations and financial condition depend on our ability to evaluate losses associated with the risks to which we are exposed. We recognize an allowance for loan losses based on our current assessment and expectations regarding various factors that affect the quality of our loan portfolio. We cannot guarantee that our assessment will result in fully sufficient provisions for the risks we are exposed to.

| 12 |

In addition, our provisioning models depend on the veracity of the financial information available from the companies we grant loans to, accordingly, any fraud or misstatement in this information may lead us to misrecord provisions or to not make provisions when we should have made them.

If we are unable to control or reduce the level of nonperforming or low-quality loans, we may be adversely affected.

Default by other financial institutions may adversely affect the financial markets in general and us

The safety and soundness of several financial institutions may be closely interrelated as a result of credit, negotiation, settlement or other transactions among financial institutions. Accordingly, concerns regarding the default of a financial institution could cause significant liquidity problems, losses and/or default by other financial institutions. This systemic risk may adversely affect financial intermediaries, including clearing agencies, clearing houses, banks, securities companies and stock exchanges with which we interact daily, including us.

If the Central Bank intervenes any other relevant Brazilian financial institution, we, together with medium-sized and smaller financial institutions, may be subject to deposit withdrawals and decreases in investments, which could adversely affect us.

Exposure to Brazilian government debt could have a material adverse effect on us

Like most Brazilian banks, we also invest in debt securities issued by the Brazilian government. As of December 31, 2023, approximately 20.5% of all our assets and 57.8% of our securities portfolio were comprised of these public debt securities. Any failure by the Brazilian government to make timely payments under the terms of these securities, or a significant decrease in their market value, could negatively affect our results directly, through portfolio losses, and indirectly, through instabilities that a default in public debt could cause to the banking system as a whole.

We may incur losses associated with counterparty exposure risks

We routinely conduct transactions with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks, mutual and hedge funds and other institutional clients. We may incur losses if any of our counterparties fail to honor their contractual obligations, including as a result of bankruptcy, lack of liquidity, operational failure or other reasons outside our control. This risk may arise, for example, from our entering into reinsurance agreements or credit agreements pursuant to which counterparties have obligations to make payments to us and are unable to do so, or from our carrying out transactions in the foreign currency market (or other markets) that fail to be settled at the specified time due to non-delivery by the counterparty, clearing house or other financial intermediary. Any failure by a counterparty to meet its contractual obligations may adversely affect our financial performance.

Liquidity

We face risks relating to liquidity of our capital resources.

Liquidity risk, as we understand it, is the risk that we will not have sufficient financial resources to meet our obligations by the respective maturity dates or that we will honor such obligations but at an excessive cost. This risk is inherent in the activities of any commercial or retail bank.

Our capacity and cost of funding, including the availability of retail deposits, may be impacted by several factors, such as changes in market conditions (e.g., in interest rates), credit supply, regulatory changes, systemic shocks in the banking sector, and changes in the market’s perception of us, among other factors. The occurrence of any of these factors could materially adversely affect our financial position and results of operations, including by increasing the amount of retail deposit withdrawals by our customers in a short period of time.

In scenarios where access to funding is scarce and/or becomes too expensive, and the access to capital markets is either not possible or is limited, we may have to increase the return rate paid to deposits made to attract more clients and/or to settle assets not compromised and/or potentially devalued so that we will be able to meet our obligations. If the market liquidity is reduced, the demand pressure may have a negative impact on prices, since natural buyers may not be immediately available. Should this happen, we may have a significant decrease in the value of the assets, which will impact our results and financial position. The persistence or worsening of such adversemarket conditions or rises in basic interest rates may have a material adverse impact on our capacity to access capital markets and on our cost of funding, which may adversely affect our results of operation and financial condition.

| 13 |

Adverse developments affecting the financial services industry, such as actual events or concerns involving liquidity, defaults, or nonperformance by financial institutions or transactional counterparties, could adversely affect our current and projected business operations, financial condition and results of operations

Events involving reduced or limited liquidity, defaults, non-performance or other adverse developments that affect financial institutions or other companies in the financial services industry or the financial services industry generally, or concerns or rumors about any events of these kinds, have in the past and may in the future lead to market-wide liquidity problems. For example, on March 10, 2023, Silicon Valley Bank, was closed by the California Department of Financial Protection and Innovation, which appointed the Federal Deposit Insurance Corporation as receiver. Similarly, on March 12, 2023, Signature Bank and Silvergate Capital Corp. were each swept into receivership. These events increase investor concerns regarding the U.S. or international financial systems which can affect commercial financing terms, including higher interest rates or costs and tighter financial and operating covenants, or systemic limitations on access to credit and liquidity sources, thereby making it more difficult for us to acquire financing. If other banks and financial institutions enter receivership or become insolvent in the future in response to financial conditions affecting the banking system and financial markets, our ability to access our cash and cash equivalents and investments in marketable securities may be threatened. Any decline in available funding or access to our cash and liquidity resources could, among other risks, adversely impact our ability to meet our operating expenses, financial obligations or fulfill our other obligations, or result in breaches of our financial and/or contractual obligations. Any of these impacts, or any other impacts resulting from the factors described above or other related or similar factors not described above, could have material adverse impacts on our liquidity and our current and/or projected business operations and financial condition and results of operations.

A downgrade of our credit ratings may adversely affect our access to funding or to the capital markets, increase our cost of funding or trigger additional collateral or funding requirements

Our ability to raise funds and the costs of such financing may be directly impacted by our credit ratings, which are opinions periodically expressed by independent rating agencies on our creditworthiness. A potential downgrade in our credit ratings could have an adverse impact on our liquidity, access to credit markets, funding costs, competitive position, and certain trading revenues, particularly in those businesses where counterparty creditworthiness is critical. Additionally, a downgrade of our credit ratings may trigger certain obligations or requirements under our financing agreements that could result in an immediate need to deliver additional collateral to counterparties or to take other actions under some of our financing and derivative contracts, adversely affecting our cash flow, interest margins and results of operations.

Business Operations

A failure in, or breach of, our operational, security or IT systems could temporarily interrupt our businesses, increasing our costs and causing losses.

Due to the high volume of daily data processing, we are dependent on technology and management of information, which exposes us to the risk of unavailability of systems and infrastructure, such as power outages, breakdowns, interruption of telecommunication services, and generalized system failures, as well as internal and external events that may affect third parties with which we do business or that are crucial to our business activities (including stock exchanges, clearing houses, financial dealers or service providers) and events resulting from wider political or social issues, such as cyberattacks or unauthorized disclosures of personal information in our possession. Additionally, we operate in many geographic locations and are frequently subject to the occurrence of events beyond our control. The contingency plans we have in place may not be sufficient to prevent our ability to conduct business from being adversely impacted by failures in the infrastructure that supports our business. We are strongly dependent on technology and thus are vulnerable to viruses, worms and other malicious software, including “bugs” and other problems that could unexpectedly interfere with the operation of our systems and result in data leakage.

Operating failures, including those that result from human error or fraud, not only increase our costs and cause losses, but may also give rise to conflicts with our clients, lawsuits, punitive damage to third parties, regulatory fines, sanctions, interventions, and other indemnity costs, all of which may have a material adverse effect on our business, reputation and results of operations.

Additionally, we depend on certain third-party services for the proper functioning of our business and technology infrastructure, such as call centers, networks, internet and systems, among others, provided by external or outsourced companies, and rely to some extent on third-party data management providers. Interruptions in the provision of these services or data, caused by the lack of supply or the poor quality of the contracted services, among other factors, can affect the conduct of our business as well as our clients.

As the regulatory framework for artificial intelligence and machine learning technology evolves, our business, financial condition and results of operations may be adversely affected.

The adoption of Artificial Intelligence (AI) presents both significant challenges and opportunities. Compliance with personal data regulations and specific AI regulations is essential, as risks related to privacy, data security, and potential algorithmic biases are significant in these technologies. On the other hand, the potential for disruptive innovations through the use of AI is undeniable, as it can optimize operations, personalize customer services, and increase efficiency, bringing significant competitive advantages. Public perception and acceptance of AI, along with potential impacts on reputation stemming from technology failures, highlight the importance of robust risk and data management and the adoption of ethical, transparent, and responsible AI practices.

| 14 |

Failure to protect personal information could adversely affect us.

We manage and hold confidential personal information of identified or identifiable natural persons, including clients in the ordinary course of our business. Although we have procedures and controls to safeguard personal information in our possession, unauthorized disclosures or security breaches could subject us to legal action and administrative sanctions, as well as damage that could materially and adversely affect our operating results, reputation, financial condition and prospects.

Administrative sanctions include, but are not limited to, sanctions for non-compliance with foreign data protection laws, as applicable, and with the Brazilian General Data Protection Law, or Law No. 13,709/2018 ("Lei Geral de Proteção de Dados"), or LGPD, which sets forth the scenarios in which personal data can be handled, either by physical or digital means, and protects the data subjects from improper use of their data.

In addition, pursuant to the LGPD, we may be required to report incidents related to cybersecurity issues, incidents where client information may be compromised, unauthorized access and other security breaches, to the relevant regulatory authority and to the subjects affected. Any material disruption or slowdown of our systems could cause information, including data related to client requests, to be lost or to be delivered to our clients with delays or errors, which could reduce demand for our services, and subject us to administrative sanctions. All of these factors could cause a material adverse effect on our reputation, business, results of operations and financial condition.

Failure to adequately protect ourselves against risks relating to cybersecurity could materially adversely affect us.

We are exposed to failures, deficiency or inadequacy of our internal processes, human error or misconduct and cyberattacks. Our information systems may be vulnerable to service interruptions and security breaches by hackers and cyberterrorists, which continue to evolve in scope and sophistication, causing us to incur significant costs in our ever-evolving efforts to enhance our protective measures against such attacks, or to investigate or remediate any vulnerability or resulting breach.

Risks related to cybersecurity incidents include but are not limited to: (i) penetration into our information technology systems and platforms, by ill-intentioned third parties, (ii) infiltration of malware and viruses into our systems, (iii) contamination of our networks and systems by third parties with whom we exchange data, (iv) unauthorized access to confidential information by persons inside or outside the organization, and (v) cyber-attacks causing systems degradation or service unavailability that may result in business losses.

We have seen in recent years computer systems of companies and organizations being targeted, not only by cyber criminals, but also by activists and rogue states. We are exposed to this risk over the entire lifecycle of information, from the moment it is collected to its processing, transmission, storage, analysis and destruction.

For example, in 2020, SolarWinds Inc., one of our third-party software services providers, was subject to a data security incident. In 2021, we detected the Log4J vulnerability which allowed remote code execution, with the inclusion of untrusted data (malicious) in the message recorded in an affected version of Apache Log4j, affecting large amounts of systems worldwide. Other examples include Spring4Shell (2022), a critical vulnerability in the Spring Java framework, and an Atlassian Confluence zero day in 2023 referenced as CVE-2023-22515. Our studies have concluded that these incidents have had no material adverse impact to us. We cannot assure that similar incidents may occur to other services providers or other relevant vulnerability might be identified, since the entire providers and technologies landscape and the inherent risk of the technology exposes us to cyber threats on a daily basis.

A successful cyberattack may result in unavailability of our services used by our clients, leak or compromise of the integrity of information and could give rise to the loss of significant amounts of client data and other sensitive information, as well as damage to our reputation, directly affecting our clients and partners.

There are also requirements related to the information security process that we are required to comply with, such as the Brazilian Data Protection Law - Law No. 13,709/18 ("Lei Geral de Proteção de Dados"), or LGPD, CVM Resolution No. 35/2021, CMN Resolution No. 4,893/2021, Central Bank Resolution No. 85/2021, the SUSEP Circular No.638/2021,the new rules adopted by the SEC in 2023 on cybersecurity risk management, strategy, governance and incident disclosure, among others rules and regulations. Noncompliance with these rules and regulations could subject us to penalties and fines.

While we continue monitoring cyber risks related controls to ensure its effectiveness, failures in our cybersecurity systems or our failure to prevent or identify cyber-attacks may materially adversely affect our operating results and financial condition.

| 15 |

The loss of senior management, or our inability to attract and maintain key personnel could have a material adverse effect on us.

Our ability to maintain our competitive position and implement our strategy depends on our senior management and key personnel.

Competition for qualified personnel in the financial services industry is intense, particularly from emerging competitors, such as fintechs and start-ups. Our performance and success depend on highly skilled individuals, and on the technical skills of certain key personnel (such as data scientists, product managers, designers and others) who are difficult to be replaced. Moreover, we face the challenge to provide a new experience to employees, so that we are able to attract and retain qualified professionals who value a work environment offering equal, diverse and meritocratic opportunities and who wish to build up their careers in dynamic and cooperative workplaces.

In addition, the increased competition and the entry of technological companies in the financial sector have forced us to invest not only in traditional career paths but also in career strands more aligned with newest and future generations.

The loss of some of the members of our senior management, including successors to crucial leadership positions, as well as their relationships with our clients, or our inability to attract, develop, motivate and retain qualified personnel, could have a material adverse effect on our operations, performance and our ability to implement our strategy.

We may not be able to prevent our officers, employees or third parties acting on our behalf from engaging in situations that qualify as corruption in Brazil or in any other jurisdiction, which could expose us to administrative and judicial sanctions, as well as have an adverse effect to us.

We are subject to Brazilian anticorruption legislation, and similarly focused legislation of the other countries where we have branches and operations, as well as other anticorruption laws and regulatory regimes with a transnational scope. These laws require the adoption of integrity procedures to mitigate the risk that any person acting on our behalf may offer an improper advantage to a public agent in order to obtain benefits of any kind. Applicable transnational legislation, such as the U.S. Foreign Corrupt Practices Act and U.K. Bribery Act, as well as the applicable Brazilian legislation mainly Brazilian Law No. 12,846/2013 – ("Lei Anticorrupção Brasileira"), or the Brazilian Anticorruption Law, require us, among other things, policies and procedures aimed at preventing any illegal or improper activities related to corruption involving government entities and officials in order to secure any business advantage, and require us to maintain accurate books and a system of internal controls to ensure the accuracy of our books and prevent illegal activities. We have policies and procedures designed to prevent bribery and other corrupt practices. See “Item 4B. Business Overview — Supervision and Regulation” for further details. However, unauthorized actions by our officers, employees or third parties acting on our behalf in breach of our internal policies may qualify as corruption in Brazil or in other jurisdiction and we could be exposed to administrative and judicial sanctions, accounting errors or adjustments, monetary losses and reputational damages or other adverse effects. The perception or allegations that we, our employees, our affiliates or other persons or entities associated with us have engaged in any such improper conduct, even if unsubstantiated, may cause significant reputational harm and other adverse effects.

We operate in international markets which subject us to risks associated with the legislative, judicial, accounting, regulatory, political and economic risks and conditions specific to such markets, which could adversely affect us or our foreign units

We operate in various jurisdictions outside of Brazil through branches, subsidiaries and affiliates, and we expect to continue to expand our international presence.

We face, and expect to continue to face, additional risks in the case of our existing and future international operations, including:

| • | political instability, adverse changes in diplomatic relations and unfavorable economic and business conditions in the markets in which we currently have international operations or into which we may expand; |

| • | more restrictive or inconsistent government and local central banks’ regulation of financial services, which could result in increased compliance costs and/or otherwise restrict the manner in which we provide our services; and |