SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

(Exact name of registrant as specified in its charter)

|

(Jurisdiction of incorporation or organization) |

(Company Registration No. 201406588W)

4911 (Primary Standard Industrial

Classification Code Number) +65 6351 1780 |

Not Applicable (I.R.S. Employer Identification No.) |

Telephone: +

Facsimile: +44 20 7519 7070

|

Title of Each Class

|

Trading Symbol

|

Name of Each Exchange on Which Registered

|

||

|

|

|

|

|

Large accelerated filer☐

|

|

Non-accelerated filer ☐

|

Emerging growth company

|

|

U.S. GAAP ☐

|

Standards Board ☒ |

Other ☐

|

| 1 | |||

| A. |

1 | ||

| B. |

1 | ||

| C. |

1 | ||

| ITEM 2. | 1 | ||

| A. |

1 | ||

| B. |

1 | ||

| ITEM 3. | 1 | ||

| A. |

Reserved | 1 | |

| B. |

1 | ||

| C. |

1 | ||

| D. |

1 | ||

| ITEM 4. | 59 | ||

| A. |

59 | ||

| B. |

59 | ||

| C. |

144 | ||

| D. |

144 | ||

| ITEM 4A. | Unresolved Staff Comments | 144 | |

| ITEM 5. | 144 | ||

| A. |

165 | ||

| B. |

171 | ||

| C. |

184 | ||

| D. |

185 | ||

| E. |

187 | ||

| F. | 187 | ||

| ITEM 6. | 187 | ||

| A. |

187 | ||

| B. |

190 | ||

| C. |

190 | ||

| D. |

193 | ||

| E. |

193 | ||

| ITEM 7. | 194 | ||

| A. |

194 | ||

| B. |

194 | ||

| C. |

195 | ||

| ITEM 8. | 195 | ||

| A. |

195 | ||

| B. |

195 | ||

| ITEM 9. | 195 | ||

| A. |

195 | ||

| B. |

195 | ||

| C. |

195 | ||

| D. |

196 | ||

| E. |

196 | ||

| F. |

196 | ||

| ITEM 10. | 196 | ||

| A. |

196 | ||

| B. |

Constitution | 196 | |

| C. |

209 | ||

| D. |

209 | ||

| E. |

209 | ||

| F. |

216 | ||

| G. |

216 | ||

| H. |

216 | ||

| I. |

216 | ||

| J. |

216 | ||

| ITEM 11. | 216 | ||

| ITEM 12. | 217 | ||

| A. |

217 | ||

| B. |

217 | ||

| C. |

217 | ||

| D. |

217 | ||

| • |

“CPV” means the CPV Group (i.e., CPV Power Holdings LP, Competitive

Power Ventures Inc. and CPV Renewable Energy Company Inc.), a business engaged in the development, construction and management of power

plants running conventional energy (powered by natural gas) and renewable energy in the United States, which was acquired in January 2021

by CPV Group LP, an entity in which OPC indirectly holds a 70% interest; |

| • |

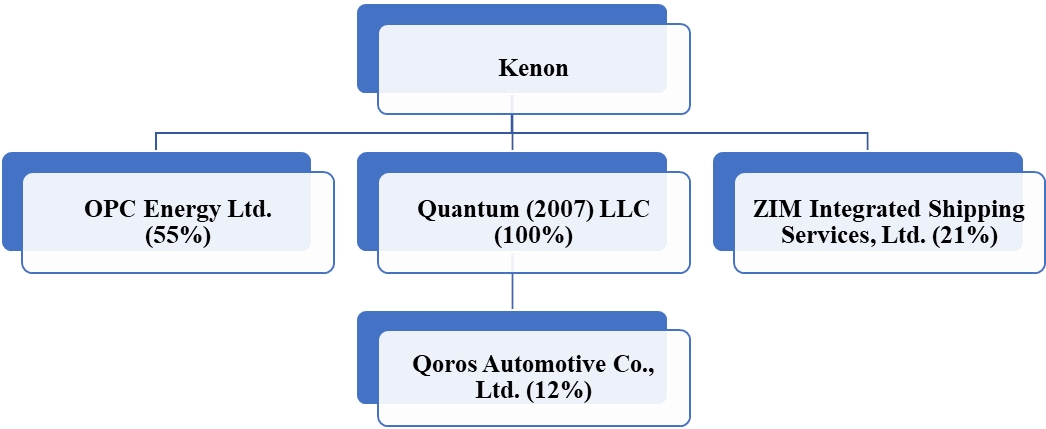

OPC Energy Ltd. (“OPC”), an owner, developer and operator

of power generation facilities in the Israeli and United States power markets, in which Kenon has an approximately 55% interest;

|

| • |

Qoros Automotive Co., Ltd. (“Qoros”), a Chinese automotive

company based in China, in which Kenon, through its 100%-owned subsidiary Quantum (as defined below), has a 12% interest; and |

| • |

ZIM Integrated Shipping Services, Ltd. (“ZIM”), an Israeli

global container shipping company, in which Kenon has an approximately 21% interest. |

| • |

“Ansonia” means Ansonia Holdings Singapore B.V., a company

organized under the laws of Singapore, which owns approximately 62% of the outstanding shares of Kenon; |

| • |

“Chery” means Chery Automobile Co. Ltd., a supplier to and

shareholder of Qoros; |

| • |

“IC” means Israel Corporation Ltd., an Israeli corporation

traded on the Tel Aviv Stock Exchange, or the “TASE,” and Kenon’s former parent company; |

| • |

“IC Power” means IC Power Ltd., formerly IC Power Pte. Ltd,

a Singaporean company and a wholly-owned subsidiary of Kenon; |

| • |

“Inkia” means Inkia Energy Limited, a Bermuda corporation,

which was wholly-owned subsidiary of IC Power. In December 2017, Inkia sold all of its Latin American and Caribbean businesses and has

since been wound up; |

| • |

“Inkia Business” means Inkia’s Latin American and Caribbean

power generation and distribution businesses, which were sold in December 2017; |

| • |

“Kallpa” means Kallpa Generación SA, a company within

the Inkia Business. Kallpa was owned by Inkia until December 2017; |

| • |

“Majority Qoros Shareholder” means the China-based investor

related to Shenzhen Baoneng Investment Group Co., Ltd. (“Baoneng Group”) that holds 63% of Qoros; |

| • |

“our businesses” shall refer to each of our subsidiaries

and associated company, collectively, as the context may require; |

| • |

“Quantum” means Quantum (2007) LLC, a Delaware limited liability

company, a wholly-owned subsidiary of Kenon, which is the direct owner of our interest in Qoros; |

| • |

“Spin-off” shall refer to (i) IC’s January 7, 2015

contribution to Kenon of its interests in IC Power, Qoros, ZIM and other entities, and (ii) IC’s January 9, 2015 distribution of

Kenon’s issued and outstanding ordinary shares, via a dividend-in-kind, to IC’s shareholders; and |

| • |

“Tower” means Tower Semiconductor Ltd., an Israeli specialty

foundry semiconductor manufacturer, listed on the NASDAQ stock exchange and the TASE, in which Kenon used to hold an interest until June

30, 2015. |

| • |

“availability factor” refers to the number of hours that

a generation facility is available to produce electricity divided by the total number of hours in a year; |

| • |

“BCM” means a billion cubic meters of natural gas, a unit

of energy, specifically natural gas production and distribution; |

| • |

“Carbon capture” technology refers to a set of chemical processes

that are designed to capture CO2 from the exhaust gas stream of a fossil fuel power generation or industrial process, often referred to

as point source carbon capture technology; the primary goal of this technology is to reduce the release of CO2 into the atmosphere;

|

| • |

“COD” means the commercial operation date of a development

project; |

| • |

“distribution” refers to the transfer of electricity from

the transmission lines at grid supply points and its delivery to consumers at lower voltages through a distribution system; |

| • |

“EA” means Israeli Electricity Authority; |

| • |

“EPC” means engineering, procurement and construction;

|

| • |

“Energean” means Energean Israel Ltd which holds 100% interest

in Karish and Tanin gas fields. |

| • |

“firm capacity” means the amount of energy available for

production that, pursuant to applicable regulations, must be guaranteed to be available at a given time for injection to a certain power

grid; |

| • |

“Gat Partnership” means Alon Energy Centers—Gat Limited

Partnership, a limited partnership that holds interests in the Kiryat Gat Power Plant; |

| • |

“Gnrgy” means Gnrgy Ltd.; |

| • |

“GW” means gigawatt; |

| • |

“GWh” means gigawatt per hour (one GWh is equal to 1,000

MWh); |

| • |

“Hadera Energy Center” means OPC Hadera’s boilers and

a steam turbine. The Hadera Energy Center currently serves as back-up for the OPC-Hadera power plant’s supply for steam; |

| • |

the “IEC” means Israel Electric Corporation, a government-owned

entity, which generates and supplies the majority of electricity in Israel, transmits and distributes all of the electricity in Israel,

acts as the system operator of Israel’s electricity system, determines the dispatch order of generation units, grants interconnection

surveys, and sets spot prices, among other roles; |

| • |

“Infinya” means Infinya Ltd. (formerly Hadera Paper Ltd.),

an Israeli corporation; |

| • |

“installed capacity” means the intended full-load sustained

output of energy that a generation unit is designed to produce (also referred to as name-plate capacity); |

| • |

“IPP” means independent power producer, excluding co-generators

and generators for self-consumption; |

| • |

“Karish Reservoir” refers to the Karish and Tanin natural

gas fields situated in the Mediterranean Sea offshore Israel and are owned and operated by Energean; Karish reservoir is estimated to

contain 1.41 tcf of gas and 317 Mboe, the Tanin field is estimated to hold 921 bcf of gas and 171.7 Mboe; |

| • |

“Kiryat Gat Power Plant” or “Kiryat Gat” means

a combined-cycle power plant powered by conventional energy with installed capacity of 75 MW located in the Kiryat Gat area, which began

commercial operation in November 2019; |

| • |

“kWh” means kilowatt per hour; |

| • |

“Mboe” means one thousand barrels of oil equivalent;

|

| • |

“Minimum Price” means the minimum price of gas in USD set

forth in gas purchase agreements between Tamar Group and each of OPC-Hadera and OPC-Rotem based on a natural gas price formula described

in the agreements that may be affected by generation component tariff; |

| • |

“MW” means megawatt (one MW is equal to 1,000 kilowatts or

kW); |

| • |

“MWdc” means megawatts, direct current; |

| • |

“MWh” means megawatt per hour; |

| • |

“Noga” means Noga – Independent System Operator Ltd,

which acts as the System Operator company; |

| • |

“capacity” or “installed capacity” means, with

respect to each asset, 100% of the capacity of such asset, regardless of OPC’s ownership interest in the entity that owns such asset;

|

| • |

“OPC-Hadera” is an Israeli corporation, in which OPC has

a 100% interest; |

| • |

“OPC-Rotem” means O.P.C. Rotem Ltd., an Israeli corporation,

in which OPC Israel has an 100% interest; |

| • |

“OPC Israel” or OPC Holdings Israel Ltd, is an Israeli corporation

which owns and operates OPC’s businesses in Israel, in which OPC holds an 80% interest; |

| • |

“OPC Power” means OPC Power Ventures LP; |

| • |

“PPA” means power purchase agreement; |

| • |

“Samay I” means Samay I S.A., a Peruvian corporation;

|

| • |

“Sorek 2” means OPC Sorek 2 Ltd.; |

| • |

the “System Operator” has the meaning as defined in Section

1 of the Israeli Electricity Sector Regulations (Private Conventional Electricity Producer), 2005 entrusted by the Israeli government

to manage and operate Israeli electrical grid; currently Noga acts as the System Operator; |

| • |

“Tamar” means Tamar reservoir, a gas field located 90 km

west of Haifa, Israel with estimated reserves of natural gas of approximately 13.17 tcf or approximately 373 BCM; the gas field is owned

and operated by the Tamar Group consisting of Isramco Negev 2 Limited Partnership, Chevron Mediterranean Ltd., Tamar Investment 1 RSC

Limited, Tamar Investment 2 RSC Limited, Dor Gas Exploration Limited Partnership, Everest Infrastructure Limited Partnership and Tamar

Petroleum Ltd.; |

| • |

“tcf” means trillion cubic feet, a volume measurement

of natural gas; |

| • |

“Title V” refers to a United States federal program designed

to standardize air quality permits and the permitting process for major sources of emissions across the country. which requires the Environmental

Protection Agency (“EPA”) to establish a national, operating permit program; |

| • |

“transmission” refers to the bulk transfer of electricity

from generating facilities to the distribution system at load center station in which the electricity is stabilized by means of the transmission

grid; |

| • |

“Tzomet” means Tzomet Energy Ltd., an Israeli corporation

in which OPC has a 100% interest; |

| • |

“Veridis” means Veridis Power Plants Ltd which owns 20% of

OPC Israel; OPC and Veridis are party to a shareholders’ agreement which governs the relationship between OPC and Veridis in OPC

Israel; and |

| • |

the “War” refers to a deadly attack by the Hamas terrorist

organization on communities in the Gaza Strip in the southern part of Israel on October 7, 2023 and the military actions that followed.

|

| • |

“cooperation agreements” means one or more vessel sharing

arrangements, swap agreements and slot sharing arrangements; |

| • |

“LNG” means liquified natural gas; |

| • |

“strategic alliance” means a more extensive type of cooperation

arrangement and is longer-term than a strategic cooperation. It involves cooperation arrangements and usually includes all of ZIM’s

East/West routes, such as Asia-Europe, Asia-Med, Cross Atlantic and Trans Pacific; |

| • |

“strategic cooperation” means a more extensive type of cooperation

arrangement, generally being longer term and involving more trade routes. It involves some joint planning mechanism, but joint planning

is less extensive as compared to a strategic alliance. A strategic cooperation can take the form of one or a combination of cooperation

arrangements; and |

| • |

“TEU” means twenty-foot equivalent unit. |

| • |

our goals and strategies; |

| • |

the strategies, business plans and funding requirements of our businesses;

|

| • |

expected trends in the industries and markets in which each of our businesses

operate; |

| • |

our tax status and treatment and expected status and treatment under

relevant regulations; |

| • |

our share repurchase program; |

| • |

our treasury activities; |

| • |

statements relating to litigation and arbitration; and |

| • |

critical accounting estimates and the expected effect of new accounting

standards on Kenon; |

| • |

with respect to OPC: |

| • |

OPC’s and CPV’s strategy; |

| • |

the expected cost and timing of commencement and completion

of development and construction projects and projects under development, as well as the anticipated installed capacities and expected

performance (e.g., efficiency) of such projects, including the required license and approvals for the development of and financing for

projects; |

| • |

expected macroeconomic trends in Israel and the US, including the expected

growth in energy demand; |

| • |

potential new projects and existing projects; |

| • |

gas supply agreements; |

| • |

dividend policy; |

| • |

expected trends in energy consumption; |

| • |

regulatory developments; |

| • |

anticipated capital expenditures, and the expected sources of funding

for capital expenditures; |

| • |

projections for growth and expected trends in the electricity market

in Israel and the US; |

| • |

the gas supply arrangements; and |

| • |

the impact of the War. |

| • |

with respect to Qoros:

|

| • |

statements relating to the agreement to sell Kenon’s remaining

interest in Qoros to the Majority Qoros Shareholder; and |

| • |

statements with respect to the litigation and arbitration relating to

Qoros. |

| • |

with respect to ZIM: |

| • |

expectations regarding general market conditions; |

| • |

expectations regarding trends related to the global container shipping

industry, including with respect to fluctuations in vessel and container supply, industry consolidation, demand for containerized shipping

services, bunker and alternative fuel prices, charter and freights rates, container values and other factors affecting supply and demand;

|

| • |

plans regarding ZIM’s business strategy, areas of possible expansion

and expected capital spending or operating expenses; |

| • |

anticipated ability to obtain additional financing in the future to fund

expenditures; |

| • |

expectation of modifications with respect to ZIM’s and other shipping

companies’ operating fleet and lines, including the utilization of larger vessels within certain trade zones and modifications made

in light of environmental regulations; |

| • |

the expected benefits of cooperation agreements and strategic partnerships;

|

| • |

formation of new alliances among global carriers, changes in and disintegration

of existing alliances and collaborations, including alliances and collaborations to which ZIM is not a party to; |

| • |

anticipated insurance costs; |

| • |

beliefs regarding the availability of crew; |

| • |

expectations regarding ZIM’s environmental and regulatory conditions,

including changes in laws and regulations or actions taken by regulatory authorities, and the expected effect of such regulations;

|

| • |

beliefs regarding potential liability from current or future litigation;

|

| • |

plans regarding hedging activities; |

| • |

ability to pay dividends in accordance with ZIM’s dividend policy;

and |

| • |

expectations regarding ZIM’s competition and ability to compete

effectively. |

| ITEM 1. |

Identity of Directors, Senior Management and Advisers

|

| A. |

Directors and Senior Management |

| B. |

Advisers |

| C. |

Auditors |

| ITEM 2. |

Offer Statistics and Expected Timetable |

| A. |

Offer Statistics |

| B. |

Methods and Expected Timetable |

| ITEM 3. |

Key Information |

| A. |

Reserved |

| B. |

Capitalization and Indebtedness |

| C. |

Reasons for the Offer and Use of Proceeds |

| D. |

Risk Factors |

| • |

OPC had $1,530 million of outstanding indebtedness and OPC’s proportionate

share of debt (including accrued interest) of CPV associated companies was $839 million, and |

| • |

ZIM had outstanding indebtedness (mostly lease liabilities) of approximately

$5.9 billion. |

| • |

minimum equity; |

| • |

debt service coverage ratio; |

| • |

limits on the incurrence of liens or the pledging of certain assets;

|

| • |

limits on the incurrence of debt; |

| • |

limits on the ability to enter into transactions with affiliates, including

us; |

| • |

limits on the ability to pay dividends to shareholders, including us;

|

| • |

limits on the ability to sell assets; and |

| • |

other non-financial covenants and limitations and various reporting obligations.

|

| • |

Transaction Risk—exists

where sales or purchases are denominated in overseas currencies and the exchange rate changes after our entry into a purchase or sale

commitment but prior to the completion of the underlying transaction itself; |

| • |

Translation Risk—exists

where the currency in which the results of a business are reported differs from the underlying currency in which the business’ operations

are transacted; |

| • |

Economic Risk—exists where

the manufacturing cost base of a business is denominated in a currency different from the currency of the market into which the business’

products are sold; and |

| • |

Reinvestment Risk—exists

where our ability to reinvest earnings from operations in one country to fund the capital needs of operations in other countries becomes

limited. |

| • |

economic volatility; |

| • |

unfavorable changes in laws or regulations; |

| • |

fluctuations in revenues, operating margins and/or other financial measures

due to currency exchange rate fluctuations and restrictions on currency and earnings repatriation; |

| • |

unfavorable changes in regulated electricity tariffs; |

| • |

import or export restrictions or other trade protection measures and/or

licensing requirements; |

| • |

costs and risks associated with managing a number of operations across

a number of countries; |

| • |

issues related to occupational safety, work hazard, and adherence to

local labor laws and regulations; |

| • |

adverse tax developments; |

| • |

geopolitical events such as military actions; |

| • |

changes in the general political, social and/or economic conditions in

the countries where we operate; and |

| • |

the presence of corruption in certain countries. |

| ITEM 4. |

Information on the Company |

| A. |

History and Development of the Company |

| • |

an approximately 55% interest in OPC, an owner, developer and operator

of power generation facilities in the Israeli and US power market; |

| • |

an approximately 20.7% interest in ZIM, a large provider of global container

shipping services; and |

| • |

a 12% interest in Qoros, a China-based automotive company. |

| B. |

Business Overview |

| • |

Israel. OPC

manages its activities through OPC Israel, in which OPC holds 80%, with the remaining 20% held by Veridis. OPC is engaged in generation

and supply of electricity and energy to private customers and to Noga (the System Operator) and the development, construction and operation

of power plants and energy generation facilities using natural gas and renewable energy in Israel. |

| • |

Renewable Energy

in the U.S. in which OPC (through its 70% interest in CPV Group) is engaged in the initiation, development, construction and operation

of power plants using renewable energy in the United States (solar and wind) and supply of electricity from renewable sources to customers;

and |

| • |

Energy Transition in the U.S.

in which OPC (through its 70% interest in CPV Group) is engaged mainly in the initiation, development, construction and operation of conventional

energy power plants in the United States, which supply efficient and reliable electricity. All active power plants in this area of operation

are held through associates (which are not consolidated in OPC’s or our financial statements). |

|

Power plant/ energy generation

facilities |

Capacity(1) (MW) |

Method of presentation in the

OPC financial statements |

Location |

Type of project / technology

|

Year of commercial operation

| |||||

|

OPC-Rotem |

466 |

Consolidated |

Mishor Rotem |

Natural gas, combined cycle |

2013 | |||||

|

Tzomet(2) |

396 |

Consolidated |

Plugot Intersection |

Natural gas, open-cycle |

2023 | |||||

|

OPC-Hadera(3) |

144 |

Consolidated |

Hadera |

Natural–gas—cogeneration |

2020 | |||||

|

Kiryat Gat(4) |

75 |

Consolidated |

Kiryat Gat industrial park |

Natural gas, combined cycle |

2019 |

| (1) |

As stipulated in the relevant generation license. |

| (2) |

Reached COD on June 22, 2023. |

| (3) |

Hadera holds the Hadera Energy Center (boilers and turbines located at the premises of

Infinya), which serves as back-up for steam generated by the Hadera power plant. Since the end of 2020, the turbine at the Hadera Energy

Center is not operating. |

| (4) |

Purchased in 2023. |

|

As of December 31, 2023 |

As of December 31, 2022 |

|||||||||||||||||||||||

|

Entity |

Installed Capacity (MW) |

Net

energy generated (GWh)(1) |

Availability

factor (%)(2) |

Installed Capacity (MW) |

Net

energy generated (GWh)(1) |

Availability

factor (%)(2) |

||||||||||||||||||

|

OPC-Rotem

|

466 |

3,514 |

93.4 |

% |

466 |

3,285 |

90.5 |

% | ||||||||||||||||

|

Tzomet(3)

|

396 |

283 |

16.3 |

% |

— |

— |

— |

|||||||||||||||||

|

OPC-Hadera

|

144 |

939 |

90.7 |

% |

144 |

800 |

73.6 |

% | ||||||||||||||||

|

Kiryat Gat(4)

|

87 |

433 |

94.4 |

% |

— |

— |

— |

|||||||||||||||||

|

OPC Total

|

1,081 |

4,085 |

610 |

4,495 |

||||||||||||||||||||

| (1) |

The net generation is the gross production capacity during the year, less energy consumed

by the power plant for its own use. |

| (2) |

The availability factor is the period during which the power plant was available for

electricity generation, including scheduled and non-scheduled maintenance work. |

| (3) |

The commercial operation date of Tzomet is June 2023. Tzomet is a peaker plant.

|

| (4) |

Since completion of the acquisition in March 2023. |

|

Power plants / energy generation

facilities |

Status |

Location |

||

|

Sorek 2 |

Under construction |

On the premises of the Sorek B seawater desalination

facility | ||

|

Energy generation facilities on the consumers’ premises

|

Various stages of development/construction(3)

|

On consumers’ premises across Israel

| ||

|

Hadera 2 |

Preliminary development |

Hadera, adjacent to the Hadera power plant

| ||

|

The Ramat Beka Solar Project |

Preliminary development |

Neot Hovav Local Industrial Council |

|

Plant |

Location |

CPV

Ownership Interest |

Field/

technology |

Installed Capacity

(MW) |

Year of commercial operation | |||||

|

Conventional

Energy Projects | ||||||||||

|

Fairview

|

Pennsylvania |

25% |

Conventional gas-fired, combined cycle |

1,050 |

2019 | |||||

|

Towantic

|

Connecticut |

26% |

Conventional gas-fired (dual fuel / two fuels),

combined cycle |

805 |

2018 | |||||

|

Maryland

|

Maryland |

25% |

Conventional gas-fired, combined cycle |

745 |

2017 | |||||

|

Shore

|

New Jersey |

37.53% |

Conventional gas-fired, combined cycle |

725 |

2016 | |||||

|

Valley

|

New York |

50% |

Conventional gas-fired, dual-fuel, combined cycle

|

720 |

2018 | |||||

|

Three Rivers

|

Illinois |

10%(1)

|

Natural gas, combined cycle |

1,258 |

2023 | |||||

|

Renewable

Energy Projects | ||||||||||

|

Keenan II

|

Oklahoma |

100%(2)

|

Wind |

152 |

2010 | |||||

|

Mountain Wind(3)

|

Maine |

100% |

Wind |

82 |

Various between 2008 and 2017 | |||||

|

CPV Maple Hill Solar LLC (“Maple Hill”) |

Pennsylvania |

100%

(subject to the tax equity partner’s share)

(4) |

Solar |

126 MWdc |

Second half of 2023 | |||||

| (1) |

Three Rivers power plant commenced its operations in July 2023 (CPV holds a 10% interest

in the power plant). The total construction costs of the project amounted to approximately NIS 4.8 billion (approximately $1.3 billion).

|

| (2) |

In April 2021, CPV acquired the remaining 30% interest in this project and, therefore,

has 100% ownership interest. |

| (3) |

Acquired in April 2023. |

| (4) |

On May 12, 2023, the CPV Group entered into an agreement with

a “tax equity partner” for an investment in the project. According to the agreement, the tax equity partner’s investment

in the project is predicated on the achievement of defined milestones, with part (20%) due at the time of completion of the construction

works, and the remainder (80%) due at the commercial operation date, which was achieved on December 1, 2023. As all milestones were

met the tax equity partner completed its $82 million investment on December 15, 2023. The agreement allows the tax equity partner

the option to sell its equity to CPV Group for a specified amount. |

|

2023 |

2022 |

|||||||||||||||||||||||

|

Net Electricity

generation (GWh)(1) |

Actual Generation(2)

(%) |

Actual Availability Percentage (%) |

Net Electricity

generation (GWh)(1) |

Actual Generation (%)(3)

|

Actual Availability Percentage (%)(4)

|

|||||||||||||||||||

|

Conventional

Energy Projects |

||||||||||||||||||||||||

|

Fairview

|

7,213 |

81.1 |

% |

84.2 |

% |

7,607 |

85.6 |

% |

87.3 |

% | ||||||||||||||

|

Towantic

|

5,551 |

77.5 |

% |

91.2 |

% |

4,960 |

69.3 |

% |

83.5 |

% | ||||||||||||||

|

Maryland

|

4,162 |

64.5 |

% |

93.0 |

% |

3,779 |

69.8 |

% |

90.9 |

% | ||||||||||||||

|

Shore

|

4,000 |

63.3 |

% |

83.4 |

% |

4,422 |

69.8 |

% |

96.0 |

% | ||||||||||||||

|

Valley

|

4,392 |

72.3 |

% |

77.6 |

% |

4,831 |

80.0 |

% |

88.6 |

% | ||||||||||||||

|

Three Rivers

|

2,814 |

64.0 |

% |

74.8 |

% |

n/a |

n/a |

n/a |

||||||||||||||||

|

Renewable

Energy Projects |

||||||||||||||||||||||||

|

Keenan II

|

271 |

20.4 |

% |

93.6 |

% |

286 |

21.5 |

% |

92.3 |

% | ||||||||||||||

|

Mountain Wind

|

140 |

22.0 |

% |

79.6 |

% |

— |

— |

— |

||||||||||||||||

|

Maple Hill

|

4.9 |

99.8 |

% |

6.6 | % |

— |

— |

— |

||||||||||||||||

| (1) |

The net electricity generation is the gross generation during the period less the electricity

consumed for the self-use of the power plants. |

| (2) |

The actual generation percentage is the electricity produced by the power plants relative

to the maximum generation capacity during the year and is affected by unplanned outages or maintenance in the power plants which are conducted

in regular time intervals. Major planned maintenance normally takes 30 to 40 days and reduces the power plants’ scope of production

and capacity until maintenance is completed. |

| (3) |

The actual generation percentage is the electricity produced by the power plants relative

to the maximum amount of generation capacity during the period and is affected by ordinary course maintenance activities at the power

plants which are scheduled at fixed intervals. Such maintenance activities typically last for approximately 30–50 days and reduce

the power plants’ generation and availability until such maintenance has been completed. The variances regarding the availability

of the production and capacity for the Fairview, Shore and Valley in 2023 compared with 2022 was mainly due to major maintenance outages

taken in 2023. CPV Group's projects may be under planned and unplanned maintenance from time to time, including as occurred in 2023. In

2024, no major planned maintenances are expected in projects (aside from immaterial planned tests). In 2023, Fairview, Shore, and

Valley underwent material planned maintenance. |

| (4) |

The availability of Fairview’s & Valley’s production and capacity compared

with 2022 was mainly affected by planned hot gas path inspections. In addition, in the fourth quarter of 2023, planned maintenance

work was performed in the Fairview power plant, which led to variances regarding the availability of its production and capacity. Shore

performed its planned major inspection. Keenan experienced curtailments in generation. |

|

Project |

Location |

Type of project/ technology |

Planned Capacity (MW) |

Year of construction start |

Projected date of commercial operation |

Expected construction cost for 100% of the project | ||||||

|

CPV Stagecoach Solar, LLC (“Stagecoach”)(1)

|

Georgia |

Solar |

102 MWdc |

Q2 2022 |

First half 2024 |

Approximately $112 million | ||||||

|

CPV Backbone Solar, LLC (“Backbone”)(2)

|

Maryland |

Solar |

179 MWdc |

June 2023 |

Second half of 2025 |

Approximately $304 million |

| (1) |

The Stagecoach project entered into a PPA with a utility company for the supply of all the electricity to be produced for a period

of up to 30 years from the project’s commercial operation date, at market prices, sale to a global company of 100% of the

project’s Solar Renewable Energy Credits (RECs), as well as a hedge covering the entire electricity price of the quantity that shall

be produced and sold to the utility company, at a fixed price, for a period of 20 years from the date of commercial operation of the project.

|

| (2) |

The Backbone project has signed a connection agreement and electricity supply agreement with the global e–commerce company

for a period of 10 years from the start of the commercial operation, for supply of 90% of the electricity expected to be generated by

the project in the said period, and sale of solar renewable energy certificates (“SREC”), which is valid up to 2035. The balance

of the project’s capacity (10%) will be used for supply to customers, retail supply of electricity of the CPV Group or for

sale in the market. |

|

Power plants / energy generation

facilities |

Status |

Capacity (MW)(1) |

Location |

Technology |

Expected commercial operation

date |

Main customer/ consumer

|

Total expected construction

cost (in NIS million) | |||||||

|

Sorek 2 |

Under construction |

Approx, 87 |

On the premises of the Sorek B seawater desalination

facility |

Natural gas—Cogeneration |

Second half of 2024(2)

|

Onsite consumers and the System Operator

|

200 | |||||||

|

Energy generation facilities on the consumers’

premises |

Various stages of development/construction(3)

|

The cumulative amount of the agreements is about

approximately 127 MW. Construction works in respect of approximately 20 MW have been completed but commercial operations has not yet began,

except for immaterial part of the projects in the operation stage; Approximately 25MW are under construction. The remaining capacity of

(83MW) is under various development stages. (4)

|

On the premises of consumers throughout Israel

|

Natural gas, renewable energy (solar) and storage

|

Gradually

from the second half of 2023 and through

the end of 2025, |

Yard consumers and the System Operator.

|

An average of about 4 per MW (a total of about

480) |

| (1) |

As stipulated in the relevant generation license. |

| (2) |

Currently, certain actions and conditions associated with the

construction and operation of the project have not been completed. Sorek 2 is taking measures to obtain adequate extensions. In addition,

in the fourth quarter of 2023, the construction contractor of the Sorek 2 project delivered a force majeure notification due to outbreak

of the War and Sorek 2 project delivered on its behalf a force majeure notification to the initiator of the desalination facility. The

EA extended project completion dates due to the defense (security) such that an extension of two months was allowed for date of the financial

closing. OPC is currently assessing the impact of such notification on the timeframe for the construction of the project. Completion

of the construction and operation of the Sorek 2 generation facility are subject to fulfillment of conditions and factors that do not

yet exist, including receipt of permits and reaching a financial closing. Ultimately, the date expected for completion of the construction

and commencement of the operation could be delayed as a result of, among other things, a delay in completion of the construction work

(including construction of the desalination facility), delays in receipt of the required permits, disruptions in arrival of equipment,

force majeure events, the occurrence of risk factors to which OPC is exposed, including delays relating to the war or its consequences.

Such delays could impact the project’s costs and could also trigger and increase in costs (beyond the expected cost indicated above)

and/or could constitute non compliance with liabilities to third parties. |

| (3) |

The construction of several projects was completed and they are in different stages of

testing and connection to the grid. The remaining projects are in various development stages with certain preconditions for execution

of the projects for construction of facilities for generation of electricity on the customer’s premises (or any of them) had not

yet been fulfilled, and the fulfillment thereof is subject to various factors, such as, licensing, permits, connection to infrastructures

and construction. Due to the War, OPC delivered a force majeure notification to customers. The War and its impacts could have an adverse

impact on the compliance with the expected dates for the commercial operation and the expected costs of the projects. |

| (4) |

Each facility with a capacity of up to 16 megawatts. |

|

Power plant/ energy

generation facilities

|

Status |

Location |

Technology |

Additional details | ||||

|

The Ramat Beka Solar Project |

Advanced Development |

Neot Hovav Local Industrial Council |

Photovoltaic in combination with storage

|

In May 2023, OPC won the tender issued by ILA for planning and an

option to purchase leasehold rights in land for the construction of renewable energy electricity generation facilities with a capacity

about 245 MW with integration of storage of about 1,375 MWh in relation to three compounds in the Neot Hovav Industrial Regional Council.

On February 5, 2024, the government authorized OPC to prepare on its behalf national infrastructure plans for photovoltaic electricity

generation projects and to submit them to the National Committee for Planning and Building of National Infrastructures. The estimated

construction cost of the project is in the range of NIS 1.93 to NIS 2.0 billion (approximately $532 million to $551 million). |

||||

|

Hadera 2 |

Initial development |

Hadera, adjacent to the Hadera power plant

|

Conventional with storage capability |

On December 27, 2021, the National Infrastructure Committee

submitted National Infrastructure Plan (“NIP”) 20B for government approval under Section 76C (9) of the Planning and Building

Law, 1965. In December 2022, a renewable option agreement was signed with Infinya Ltd., which awards Hadera 2 an annual option, which

may be renewed for a period of up to 5 years, during which it will be allowed to lease the land adjacent to the Hadera Power plant for

the project. On May 28, 2023, the Israeli government did not approve NIP 20B and returned it to the National Committee for Planning

and Building of National Infrastructures for further discussion. Following this, OPC submitted a petition on behalf of Hadera 2 in respect

of the government decision, which was summarily dismissed on July 19, 2023 on the grounds of failure to exhaust proceedings. OPC continues

to promote NIP 20B and awaits recommencement of the above discussions. | ||||

|

Intel Israel facilities |

Initial development |

Kiryat Gat |

Conventional |

On March 3, 2024, OPC Power Plants signed a non-binding memorandum

of understanding with Intel Electronics (“Intel”), an OPC existing customer, pursuant to which OPC Israel will construct and

operate a power plant, which will supply electricity to Intel’s facilities, including expansion of the facilities currently being

constructed, for a period of 20 years from the operation date. |

|

Project |

Location |

Installed Capacity (MW) |

CPV

ownership interest |

Year of commercial operation |

Type of project/ technology / client |

Regulated

market | ||||||

|

CPV Fairview, LLC (“Fairview”)

|

Pennsylvania |

1,050 |

25% |

2019 |

Gas-fired, combined cycle |

PJM

MAAC | ||||||

|

CPV

Towantic, LLC (“Towantic”) |

Connecticut |

805 |

26% |

2018 |

Gas-fired (with dual fuel), Combined cycle

|

ISO-NE

CT | ||||||

|

CPV

Maryland, LLC (“Maryland”) |

Maryland |

745 |

25% |

2017 |

Gas-fired, Combined cycle |

PJM

SW

MAAC | ||||||

|

CPV Shore Holdings, LLC (“Shore”) |

New Jersey |

725 |

37.53% |

2016 |

Gas-fired, Combined cycle |

PJM EMAAC | ||||||

|

CPV Valley Holdings, LLC (“Valley”) |

New York |

720 |

50% |

2018 |

Gas-fired, Combined cycle |

NYISO

Zone G | ||||||

|

CPV Three Rivers LLC (“Three

Rivers”) |

Illinois |

1,258 |

10% |

2023(1)

|

Natural gas, combined cycle |

PJM | ||||||

|

Renewable

Energy Projects | ||||||||||||

|

CPV Keenan II Renewable Energy Company, LLC (“Keenan II”) |

Oklahoma |

152 |

100%(2)

|

2010 |

Wind |

SPP

(Long-term PPA) | ||||||

|

CPV Mountain Wind(3)

|

Maine |

82 |

100% |

Between 2008 and 2017 |

Wind (4 wind power plants) |

ISO-NE market | ||||||

|

CPV Maple Hill Solar LLC

(“Maple Hill”) |

Pennsylvania |

126 MWdc |

100%(4)

(subject to tax equity partner’s share)

|

Second half of 2023 |

Solar |

PJM

MAAC + PA SRECs

| ||||||

| (1) |

Three Rivers power plant, which commenced commercial operation in July 2023, is entitled

to receive capacity payments from June 2023. |

| (2) |

On April 7, 2021, CPV acquired 30% of the rights in Keenan II from its tax equity partner.

|

| (3) |

In April 2023, CPV acquired all rights (100%) in four active wind power plants (the “Mountain

Wind Project”). CPV received (indirectly, through a 100%-held corporation) all of the seller’s rights in the Mountain Wind

Project in consideration for approximately NIS 625 million (approximately $ 175 million) (after adjustments). The purchase consideration

was funded by way of capital injection by CPV’s investors at the total amount of approximately $ 100 million (of which OPC’s

share is 70%), and the remaining balance was funded by a loan from a bank under a financing agreement. |

| (4) |

On May 12, 2023, CPV entered into an agreement with a “tax

equity partner” for an investment in the project. According to the agreement, the tax equity partner’s investment in the project

is predicated on the achievement of defined milestones, with part (20%) due at the time of completion of the construction works, and the

remainder (80%) due at the commercial operation date, which was achieved on December 1, 2023. As all milestones were met, the tax

equity partner completed its $82 million investment on December 15, 2023. The agreement gives the tax equity partner the option

to sell its equity to CPV for a specified amount. |

|

Project |

Location |

Planned Capacity (MW) |

CPV

Ownership Interest |

Year of construction start |

Projected date of commercial operation |

Type of project/ technology |

Tax Equity |

Expected construction cost for 100% of the project | ||||||||

|

CPV Stagecoach Solar, LLC (“Stagecoach”) |

Georgia |

102 MWdc |

100% |

Q2 2022 |

First half of 2024 |

Solar |

Approximately $52 million(1)

|

Approximately $112 million(2)

| ||||||||

|

CPV Backbone Solar, LLC (“Backbone”) |

Maryland |

179 MWdc |

100% |

June 2023 |

Second half of 2025 |

Solar |

Approximately $130 million(3)

|

Approximately $304 million(4)

|

| (1) |

The CPV Group has signed a non-binding memorandum of understanding

with a tax equity partner, whereby approximately $43 million of such amount is expected to be received on the project’s commercial

operation date and the balance is expected to be received over a period of 10 years. The investment of the tax equity partner is subject

to negotiations and signing of binding agreements. Regarding projects that are entitled to tax benefits of the type of Production Tax

Credits (the “PTC”), CPV’s estimate with respect to the scope of the tax equity partner’s investment is based

on the IRA and estimates with respect to tax equity partners, a tax benefit for every KW/hr of generation, and does not depend on the

anticipated cost of the investment (i.e., does not depend of initiation fees and reimbursement of pre-construction development expenses).

|

| (2) |

Includes financing costs under the financing agreement (see, “Item

5 Operating and Financial Review and Prospects—OPC’s Liquidity and Capital Resources—OPC’s Material Indebtedness—United

States”). The project’s expected cost of investment is subject to changes. |

| (3) |

The project is located on a former coal mine and, therefore, it is expected to be entitled

to higher tax benefits of 40% in accordance with the IRA. The CPV Group intends to sign an agreement with a tax equity partner in respect

of approximately 40% of the cost of the project and use of the tax credits that are available to the project (subject to appropriate regulatory

arrangements). |

| (4) |

Excludes development fees but includes financing costs under

the financing agreement. CPV Group intends to provide the project with solar panels through its existing master agreement for the purchase

of solar panels. The total cost of such project is expected to be approximately $330 million, approximately 40% of which is expected to

be financed by a tax equity partner such that the net investment cost for CPV Group is estimated to be approximately $150 million. In

addition, CPV Group is working to obtain a short term revolving financing facility for part of the remainder of the project cost. Customary

collateral with a value of about $17 million is expected to be provided for purposes of the agreement covering connection to the network

(grid) and the PPA as well as additional development expenses in the project. Construction of the project commenced in June 2023 and commercial

operation in PJM is expected to be reached in the third quarter of 2025. |

|

Technology |

Advanced |

Early stage |

Total* |

|||||||||

|

Solar (1) |

1,550 |

1,050 |

2,600 |

|||||||||

|

Wind (2) |

250 |

1,000 |

1,250 |

|||||||||

|

Total renewable energy |

1,800 |

2,050 |

3,650 |

|||||||||

|

Carbon capture projects (natural gas |

||||||||||||

|

with reduced emissions) |

1,300 |

4,000 |

5,300 |

|||||||||

| (1) |

The capacities in the solar technology projects in the advanced development

stages and in the early development stages are about 1,200 MWac and about 850 MWac. |

| (2) |

Includes the Rogue’s Wind project, with a capacity of

114 MW in Pennsylvania, which signed a long-term PPA agreement, the terms of which have been improved, and which project is in an advanced

stage of development, the start date of which is expected to be in the first half of 2024. The expected cost of the investment in the

project is estimated at about NIS 1.2 billion (about $0.3 billion), the investment of the tax equity partner is estimated at about NIS

0.5 billion (about $0.1 billion). |

|

Project |

Location |

Capacity (MW) |

OPC

Ownership Interest |

Projected Year of construction start |

Projected date of commercial operation |

Type of project/ technology |

Activity area and electricity region |

Tax Equity |

Expected construction cost ($ millions) | |||||||||

|

CPV Rogue’s Wind, LLC

(“Rogue’s Wind”) |

Pennsylvania |

Approx.

114

MW |

100%(1)

|

Second half of

2024 |

First half of

2026(2)

|

Wind |

PJM MAAC |

Approximately $135 million |

Approximately $377 million(3)

|

| (1) |

Upon consummation of an agreement with a “tax equity partner” CPV will have

100% of Class B rights. Class A rights are held by tax equity investors, who have excess tax benefits and dividend rights until a certain

return (Tax Flip) is achieved. |

| (2) |

The expected date of operation for Rogue’s Wind may be delayed due to delays in

connection with PJM’s interconnection process, including construction works or upgrade works (the project has been issued with interconnection

agreement). Delays may affect Rogue Wind’s ability to meet certain schedule obligations with counterparties and may result in liquidated

damages payments. |

| (3) |

Does not include development fees, but includes financing costs under the financing agreement.

|

| • |

Gas Supply: a

base contract for purchase and transmission of natural gas which provides for supply of natural

gas at a quantity of up to 180,000 MMBtu per day at a price that is linked to market prices set forth in the agreement. Pursuant to the

agreement, the gas supplier is responsible for transport of natural gas to the designated supply point and is permitted to transport ethane

in lieu of natural gas for up to 25% of the agreed supply quantity. The agreement is valid up to May 31, 2025. |

| • |

Maintenance: a maintenance

agreement (MA) with its original equipment manufacturer, for the provision of maintenance services for the combustion turbines.

In consideration for the maintenance services, Fairview pays a fixed and a variable amount as of the date stipulated in the agreement.

The MA period is 25 years beginning in 2016 or ends earlier when specific milestones are reached on the basis of usage and wear and tear.

Fairview has paid an average of approximately $9 million (all-in costs) each year for the past two years. |

| • |

Operation: an agreement

for operation and maintenance of the facility. The initial period of the agreement is three years from the completion date of construction

of the facility and includes an extension/renewal clause for a period of one year, unless one of the parties gives notice of termination

of the agreement in accordance with its provisions. The agreement is currently under the automatic annual one-year renewal option. Fairview

has paid an average of approximately $5 million each year over the past two years. |

| • |

Hedging: a hedge

agreement on electricity margins of the Revenue Put Option (“RPO”). The RPO is intended to provide CPV a minimum

margin for the term of the agreement. Calculation of the amount for the minimum margin is determined for each contractual year, with the

actual netting dates taking place every three months in respect of the respective partial amount and an annual adjustment is made to calculate

the total annual margin for the year. The RPO has an annual exercise price that covers an exercise period of a fiscal year. To calculate

the gross margin pursuant to the agreement, specific parameters are taken into account, such as utilization, heat rate, the expected generation

levels, forward prices for electricity and gas, gas transmission costs and other specific project costs. The RPO ends on May 31,

2025. |

| • |

Management: A CPV entity

served as the asset manager for Fairview until September 2022. In accordance with an inter-company management agreement, one of the other

investors in the project replaced the CPV entity, in accordance with the terms of the agreement. This other investor of the project assumed

the role of asset manager for Fairview starting at October 1, 2022 and the CPV entity will provide certain limited scope services to the

other investor on behalf of Fairview. |

| • |

Gas Supply & Transmission:

|

| • |

an agreement for the guaranteed gas

transmission of 2,500 MMBtu per day, at the AFT 1 Tariff. The agreement’s initial term ends on March 31, 2025. The agreement

renews automatically for periods of one year each time, unless one of the parties terminates the agreement. |

| • |

an agreement for the supply of gas,

pursuant to which up to 125,000 MMBtus per day will be supplied at a price linked to market prices. The agreement has an initial term,

which commenced on April 1, 2023, and ends on March 31, 2025. |

| • |

Maintenance: a services

agreement (CSA) with its original equipment manufacturer, for the provision of maintenance services for the combustion turbines.

In consideration for the maintenance services, Towantic pays a fixed and a variable amount as of the date stipulated in the agreement.

The agreement term is 20 years, beginning in 2016 or ends earlier when specific milestones are reached on the basis of usage and

wear and tear. Towantic has paid an average of approximately $8 million (all-in costs) each year for the past two years. |

| • |

Operation: an agreement

for operation and maintenance of the facility, which commenced in May 2018. The consideration includes a fixed and variable amount,

a performance-based bonus, and reimbursement for employment expenses, including payroll costs and taxes, subcontractor costs and other

costs. In July 2021, the agreement was extended and the agreement term is from 2022 to 2024. The agreement includes an extension/renewal

clause for a period of one year, unless one of the parties gives a termination notice in accordance with that provided in the agreement.

Towantic has paid an average of approximately $5 million (all-in costs) each year for the past two years. |

| • |

Gas Supply: an agreement

for the supply of firm natural gas, pursuant to which up to 132,000 MMBtu per day will be supplied at a price linked to market

prices. The agreement is effective until October 31, 2024. |

| • |

Gas Transmission: a natural

gas transmission agreement for guaranteed capacity of up to 132,000 MMBtu/d. The agreement term is 20 years from May 31, 2016,

with an option for Maryland to extend it by an additional 5 years. |

| • |

Maintenance: a services

agreement with its original equipment manufacturer for the provision of maintenance services for the combustion turbines. In consideration

for the maintenance services, Maryland pays a fixed and a variable amount as of the date stipulated in the agreement. The agreement

period is 20 years beginning in 2014 or ends earlier when specific milestones are reached on the basis of usage and wear and tear. Maryland

has paid an average of approximately $6 million (all-in costs) each year for the past two years. |

| • |

Operation: an agreement

for operation and maintenance of the facility. The consideration includes fixed annual management fees, a performance-based bonus,

and reimbursement of employment expenses, payroll costs and taxes, subcontractor costs and other costs. In March 2021, the agreement was

extended to continue until July 23, 2028 and may be renewed for one-year periods, unless one of the parties gives a termination notice

in accordance with agreement. Maryland has paid an average of approximately $4 million (all-in costs) each year for the past two years.

|

| • |

Engineering, Procurement and

Construction Agreement. Maryland signed an Engineering, Procurement and Construction Agreement dated October 31, 2022, for the

construction of a Black Start facility in the event of grid power outages around the Maryland’s site which is expected to commence

operation during 2024. Total contract cost is approximately $30 million to be paid in accordance with a progress payment schedule incorporated

into the agreement. Most of the consideration is financed through a financing agreement entered into by Maryland. |

| • |

Gas Supply: an agreement

for supply of natural gas. Pursuant to the agreement, the gas supplier supplies 120,000 MMBtu of gas per day at a price linked

to the market price. The agreement is effective through October 31, 2024. |

| • |

Gas Transmission: two

agreements with interstate pipeline companies for the use of 2 different pipeline systems, one of which was operational since 2015

and the second of which became operational in late 2021. Pursuant to the agreements, natural gas connection and transmission services

are provided to Shore by means of a pipeline the start of which is an existing interstate pipe and allows for gas to reach the facility’s

connection point. Shore paid a down payment to one of the pipeline companies for these services. The period of the gas transmission agreements

are 15 years (until April 2030) for one interconnection, with an option to extend the agreement twice by ten years, and 20 years

(until September 2041) for the other interconnection, with an option to extend annually. |

| • |

Maintenance: an amended

services agreement with its original equipment manufacturer for the provision of maintenance services for the turbines. In consideration

for the maintenance services, Shore pays a fixed and a variable amount as of the date stipulated in the agreement. The agreement

period is 20 years beginning in 2014 or ends earlier when specific milestones are reached on the basis of usage and wear and tear. Shore

has paid an average of approximately $6 (all-in costs) million each year for the past two years. |

| • |

Operation:

an agreement for operation of the facility. The consideration includes fixed annual management

fees, a performance-based bonus and reimbursement of employment expenses, including, payroll and taxes, subcontractor costs and other

costs as provided in the agreement. The agreement includes an extension/renewal clause for a period of one year, unless one of the parties

gives a termination notice in accordance with that provided in the agreement. The agreement is currently under the automatic annual one

year renewal option. Shore has paid an average of approximately $4 million (all-in costs) each year over the past two years. |

| • |

Gas Supply: an agreement

for the supply of natural gas of up to 127,200 MMBtu of natural gas per day at a price linked to the market price. Pursuant to

the agreement, the supplier is responsible for transmission of natural gas to the designated supply point and the agreement is effective

through October 31, 2025. |

| • |

Gas Transmission: an

agreement with an interstate pipeline company for the licensing, construction, operating and maintenance

of a pipeline and measurement and regulating facilities, from the interstate pipeline system for transmission of natural gas up to the

facility. The supplier provides 127,200 MMBtu per day of firm natural gas delivery at an agreed price during a period ending March 31,

2033, with an option to extend by up to three five-year additional periods. Valley signed an additional agreement for provision of transmission

services (firm) of 35,000 MMBtu per day, for a period of 15 years ending on March 31, 2033, which can deliver gas from a different

location into the firm transportation agreement referenced above. |

| • |

Maintenance: an agreement

with its original equipment manufacturer for maintenance services for the fire turbines. The consideration includes fixed and variable

amounts. The agreement period is the earlier of: (i) 132,800 equivalent base load hours; or (ii) 29 years from 2015. Valley

has paid an average of approximately $6 million (all-in costs) each year for the past two years. |

| • |

Operation: an operation

and maintenance agreement with one of the partners in the project. The consideration includes fixed annual management fees, an

operation bonus, and reimbursement of certain costs set out in the agreement. The period of the agreement is five years from the completion

date of construction of the facility, and the agreement may be renewed for additional three-year periods unless one of the parties gives

a termination notice in accordance with the agreement. The agreement is currently under the automatic three year renewal option. Valley

has paid an average of approximately $5 million (all-in costs) each year for the past two years. |

| • |

Hedging: a

hedge agreement on electricity margins of the RPO type. The RPO is intended to provide CPV a minimum margin for the duration of

the agreement term. Calculation of the amount for the minimum margin is determined for each contractual year, with the actual netting

dates taking place every three months with respect to the respective partial amount and an annual adjustment is made to calculate the

total annual margin, which includes each year for the RPO an annual exercise price covering the exercise period or a fiscal year. To calculate

the minimum gross margin, specific parameters are taken into account, such as utilization, heat rate, the expected generation levels,

forward prices for electricity and gas, gas transport costs and other specific project costs. The RPO ended on May 31, 2023.

|

| • |

Gas Supply: two agreements

for the supply of natural gas. The agreements supply 139,500 MMBtu in natural gas per day to the facility, from the operation date

of the facility for a period of five years, and a reduced quantity of 25,000 MMBtu per day from the fifth year of operation of the facility

and up to the tenth year. The price of natural gas delivered under these agreements is linked to the day-ahead electricity prices in the

PJM market. The agreements include an obligation to purchase such fixed volume of natural gas, with a right to resell surplus gas.

|

| • |

GSPA. Three Rivers entered

into a Contract for Sale and Purchase of Natural Gas (GSPA) on December 15, 2022. The GSPA requires the supplier to provide gas supply

of up to 200,000 MMBtu/day at a price indexed to market. The agreement had an initial term until January 31, 2023. The agreement is automatically

renewed month-to-month unless one of the parties terminates by notification no less than 5 business days prior to the last day of the

month. |

| • |

Gas Interconnection:

two connection agreements for transmission of gas, whereby each of them is sufficient for the

full demand of the facility. |

| • |

One agreement is an interconnection agreement with an interstate pipeline

company for transmission of natural gas. The agreement sets forth the responsibility of the parties in connection with the design, construction,

ownership, operation and management of a pipeline as well as the connection and pressure equipment. Based on the agreement, Three Rivers

will bear the costs of all the facilities. |

| • |

The second agreement is an additional interconnection agreement with

an interstate pipeline company for transmission of natural gas. As part of the agreement, the counterparty is responsible for the design

and construction to connect to the existing pipeline. The counterparty to the agreement will remain the owner of these facilities and

will operate them, and Three Rivers will bear the development and construction costs. |

| • |

Gas Transmission: an

agreement for transmission of gas with an interstate pipeline company and its Canadian affiliate,

for firm transmission of natural gas from Alberta, Canada to the facility. The agreements include capacity of 36.2 MMcf per day, at agreed

prices. The agreement term is 11 years from the signing date of the agreement on November 1, 2020; the counterparty may extend the

agreement for an additional year by means of prior notice of 12 months. |

| • |

Equipment: an agreement

for acquisition of equipment for the purchase of power generation equipment and ancillary services, with an international company

specializing in design and manufacture of equipment, including that required for an electricity generation facility. The equipment includes

two units, with each consisting of the following main components: a gas or combustion turbine; a steam generator for heat recovery; a

steam turbine; a generator; a continuous control system for emissions and additional related equipment. The equipment supplier is responsible

for supply and installation in accordance with the agreement. In addition, the supplier is to provide technical consulting services to

Three Rivers in order to support the installation process, commissioning, inspections and operation of the equipment. Pursuant to the

terms and conditions of the agreement, Three Rivers will pay the third party in installments based on reaching milestones. |

| • |

EPC: an EPC

agreement with an international engineering, acquisition and construction contractor. Pursuant to the agreement, the contractor

will design and construct the required components of the facility, to integrate all the equipment required for the power plant. Three

Rivers achieved substantial completion in July 2023 and will achieve final completion upon the satisfaction of a final performance test

but no later than the maximum period set in the agreement. |

| • |

Maintenance:

a services agreement with its original equipment manufacturer for the provision of maintenance services for the combustion turbines.

In consideration for the maintenance services. Three Rivers pays a fixed and a variable payment. The agreement period is 25 years

beginning in 2020; or ends earlier when specific milestones are reached on the basis of usage and wear and tear. On average, Three

Rivers is expected to pay approximately $6 million (all-in costs) each year. |

| • |

Operation: an agreement

for operation and maintenance of the facility. The consideration includes fixed annual management fees, a performance-based bonus,

and reimbursement of employment expenses, payroll costs and taxes, subcontractor costs and other costs. The agreement period will commence

during the construction period, and will continue for approximately 3 years from the construction completion date of the facility,

which occurred in June 2023. On average, Three Rivers is expected to pay approximately $6 million (all-in costs) each year. |

| • |

Equity Purchase Agreement:

an agreement for the purchase of the 100% of the outstanding equity interests in Keenan. As a

result of the acquisition in April 2021, CPV holds all of the rights to Keenan. |

| • |

PPA:

a wind power energy agreement for sale of renewable energy. Pursuant to the terms and conditions

of the agreement, the purchaser is to receive all of the electricity generated by the wind farm, credits, certificates, similar rights

or other environmental allotments. The consideration includes a fixed payment. The period of the agreement is 20 years, ending in

2030. The purchaser is permitted, with proper notice, to extend the agreement for another five-year period, and to acquire an option to

purchase the project at the end of the agreement period or renewal period at its fair market value, as defined in the agreement and pursuant

to the terms and conditions stipulated therein. |

| • |

O&M Agreement: an

agreement for the operation and maintenance of the wind farm which commenced in February 2016. The consideration includes fixed annual

management fees and the agreement lasts for 15 years from the commencement date. On average, Keenan paid approximately $5 million each

year for the past two years. |

| • |

Operation:

a master services agreement and an operations agreement with its original equipment manufacturer

for the operation, maintenance and repair of the wind turbines. The consideration includes fixed annual fees, performance-based bonus

(or liquidated damages) and reimbursement of expenses for additional work. The agreement expires in February 2031. Keenan has paid an

average of approximately $6 million (all-in costs) each year for the past 2 years. |

| • |

Maintenance: a

master services agreement for the management and maintenance of the four wind facilities (Beaver Ridge, Canton Mountain, Saddleback

Ridge, Spruce Mountain) entered into by Mountain Wind. Staff is shared between the four projects. At all projects except for Beaver Ridge,

the services agreement applies only to work outside the scope of the turbine services which is performed by the original equipment manufacturers.

At Beaver Ridge, where there is no agreement with the original equipment manufacturer, the agreement also covers the direct maintenance

of the wind turbines. The agreement commenced on April 5, 2023 and has an initial two year term. Mountain Wind will pay approximately

$3 million (all-in costs) per year. |

| • |

Services Agreements and Operation

Agreements: a master service agreement

and an operation agreement with its original equipment manufacturer for the operation, maintenance,

and repair of the wind turbines is entered by each of Mountain Wind Project with the exception of Beaver Ridge; maintenance at Beaver

Ridge is performed under an agreement by a third-party provider. The agreements for Saddleback Ridge and Canton Mountain were entered

in 2016 and both have 20 years terms with a sunset date of September 16, 2035. The agreement for Spruce Mountain was entered in December

2023 and has an 8-year term. The Beaver Ridge agreement was entered in April 2023 and has a 2-year term. On average, the four projects

are expected to pay approximately $4 million (all-in costs) each year. |

| • |

Other contracts:

The projects are engaged in contracts to sell 100% of the electricity and RECs, under separate contracts (PPAs) with local utility companies

and councils, generally for a period of the next 15 to 20 years from the acquisition of the projects by CPV, while most of the capacity

is sold under separate contracts for the next 12 years from the acquisition of the projects by CPV (the periods of the contracts may change

according to termination clauses determined in each agreement). |

| • |

Maintenance.

An operating and maintenance agreement with a third-party service provider for services related

to the ongoing operation and maintenance of the Maple Hill solar power generation facility. The agreement has an initial term of three

years, commencing on the date that the service provider actually begins providing services, which occurred in November 2023 and can be

renewed for 2 one-year terms unless one of the parties provides notice on non-renewal in accordance with the agreement. On average, Maple

Hill is expected to pay approximately $0.4 million (all-in costs) each year. |

| • |

SREC. An agreement

with an international energy company for the sale of 100% of the SRECs generated in the project through 2027 to an international energy

company. CPV provided collateral for its obligations under the agreement, which include delivery of SRECs generated by the project.

|

| • |

Virtual PPA. An

agreement with a third party for the sale of 48% of the total generated electricity, where the electricity price calculation is

performed based on financial netting between the parties for 10 years from the commercial date of operation. In accordance with the agreement,

a net calculation will be made of the difference between the variable price that Maple Hill receives from the system operator and which

is published (the spot price) and the fixed price set with a third party. CPV provided collateral for its obligations under the

agreement which include making certain payments to the other party as part of the settlement of the virtual PPAs. The agreement includes

an option to transition to a physical PPA with a fixed price on fulfillment of certain terms and conditions, which have yet to be met.

|

| • |

Energy Sale Agreement (non-firm).

In March 2022, Stagecoach entered into an agreement to sell 100% of non-firm energy to a utility company. The utility company is to receive

all of the energy and ancillary services produced by Stagecoach. The agreement excludes tax attributes arising from the ownership of the

solar project and any environmental attributes generated by Stagecoach. The consideration is based on the hourly avoided energy rate for

each hour of generation up to a maximum energy output as defined in the agreement. The agreement is for a period of 30 years from the

commercial operation date of Stagecoach. The agreement provides for sale to a global utility company of 100% of the project’s SRECs,

as well as a hedge covering the entire electricity price of the quantity that shall be produced and sold to the utility company, at a

fixed price, for a period of 20 years from the date of commercial operation of the project |

| • |

Agreement to sell renewable

solar energy credits. In April 2022, Stagecoach entered into an agreement with a global company to sell 100% of the renewable solar

energy credits produced by the solar project, along with a full hedge of the electricity price of the energy that will be generated and

sold under the agreement with the utility company, at a fixed price for 20 years from the commercial operation date. |

| • |

EPC. In May 2022, Stagecoach

signed an EPC agreement with an international contractor. Pursuant to the agreement, the contractor is to design, engineer, procure, install,

construct, test, and commission the solar project on a turnkey, guaranteed-completion-date basis. The total consideration to be paid to

the contractor is a fixed amount payable under a milestone schedule. |

| • |

Operation and Maintenance Agreement.

In August 2022, Stagecoach entered into an operating and maintenance agreement with a third-party service provider to provide services

during the mobilization and operational period of the Stagecoach solar facility. The agreement is for an initial 3-year term starting

on the date when the service provider actually started rendering operational period services, which is expected to commence in the first

half of 2024. The term of the agreement may be renewed for a maximum of two one-year renewals, unless one of the parties delivers a notice

of non-renewal in accordance with the terms of the agreement. |

| • |