Table of Contents

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Not applicable |

||

(Translation of Registrant’s name into English) |

(Jurisdiction of incorporation or organization) |

Title of each class |

Trading Symbol(s) |

Name of exchange on which registered | ||

| Large accelerated filer | ☐ | ☒ | ||||

Non-accelerated filer |

☐ | Emerging growth company | ||||

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

| U.S. GAAP | ☐ | Other | ☐ |

Table of Contents

TABLE OF CONTENTS

i

Table of Contents

ii

Table of Contents

Conventions That Apply to This Annual Report on Form 20-F

In this annual report on Form 20-F, unless otherwise designated, the terms “we” “us” “our,” “Lanvin Group,” “the Company” and “our Company” refer to Fosun Fashion Group (Cayman) Limited (“FFG”) and its consolidated subsidiaries, prior to the consummation of the Business Combination and to Lanvin Group Holdings Limited (“LGHL”) and its consolidated subsidiaries following the Business Combination, as the context requires. The term “PCAC” refers to Primavera Capital Acquisition Corporation prior to the consummation of the Business Combination.

Unless we indicate otherwise, references in this annual report to:

“Amended Articles” means the amended and restated memorandum and articles of association of the Company.

“Assignment, Assumption and Amendment Agreement” means certain amendment and restatement of the Existing Warrant Agreement, dated March 23, 2022, by and among PCAC, LGHL, and Continental Stock Transfer & Trust Company.

“Business Combination” or “Transactions” means the Mergers and the other transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of March 23, 2022 and as amended October 17, 2022, October 20, 2022, October 28, 2022 and December 2, 2022, by and among PCAC, FFG, LGHL, Lanvin Group Heritage I Limited (“Merger Sub 1”) and Lanvin Group Heritage II Limited (“Merger Sub 2”).

“Cayman Companies Act” means the Companies Act (As Revised) of the Cayman Islands as the same may be amended from time to time.

“China” and the “PRC” means the People’s Republic of China, including the Hong Kong Special Administrative Region and the Macao Special Administrative Region (unless the context otherwise requires) but excluding, for the purposes of this annual report only, Taiwan.

“Convertible Preference Share” means the convertible preference share, par value $0.000001 per share, of the Company, which is convertible into an aggregate number of up to 15,000,000 non-voting ordinary shares and/or Ordinary Shares (subject to adjustment as a result of any share subdivision or consolidation of the shares of LGHL) at the election of Meritz upon the occurrence of certain events. On December 14, 2023, pursuant to the Meritz SBSA (as defined below), the Company repurchased from Meritz one Convertible Preference Share.

“Existing Warrant Agreement” means certain warrant agreement, dated January 21, 2021, by and between PCAC and Continental Stock Transfer & Trust Company.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“FFG Collateral Share” means the preferred collateral share, par value EUR0.0001 per share, of FFG purchased by Meritz pursuant to the Meritz Private Placement Subscription Agreement, dated October 16, 2022, entered into by and among FFG, LGHL and Meritz, pursuant to which Meritz agreed to, among other things, subscribe for, and FFG agreed to issue to Meritz 18,569,282 ordinary shares of FFG at a subscription price of $49,999,999 and the FFG Collateral Share at a subscription price of $1, which agreement terminated upon the closing of our Business Combination. The FFG Collateral Share was automatically canceled in exchange for the right to receive one Convertible Preference Share at the Second Merger Effective Time, which means the time when the plan of Second Merger has been registered by the Registrar of Companies of the Cayman Islands or at such later time as may be agreed by FFG and PCAC in writing and specified in the plan of Second Merger (being not later than the 90th day after registration by the Registrar of Companies of the Cayman Islands).

“Fosun Group” means Fosun International and its affiliates.

“Fosun International” or “Fosun” means Fosun International Limited, a company incorporated in Hong Kong with limited liability.

1

Table of Contents

“founder shares” or “PCAC Class B ordinary shares” means Class B ordinary shares of PCAC, par value US$0.0001 per share initially purchased by Primavera Capital Acquisition LLC, or the Sponsor, in a private placement prior to PCAC’s initial public offering.

“Initial Merger Effective Time” means the time when the plan of Initial Merger has been registered by the Registrar of Companies of the Cayman Islands or at such later time as may be agreed by FFG and PCAC in writing and specified in the plan of Initial Merger (being not later than the 90th day after registration by the Registrar of Companies of the Cayman Islands).

“Investor Rights Agreement” means the investor rights agreement in substantially the form attached as an exhibit to the Business Combination Agreement.

“IRS” means the Internal Revenue Service of the United States.

“Mergers” means each of: (i) the merger of PCAC with and into Merger Sub 1, with Merger Sub 1 surviving such merger (the “Initial Merger”); (ii) the merger of Merger Sub 2 with and into FFG, with FFG surviving such merger (FFG is referred to for the periods from and after the Second Merger Effective Time as the “Surviving Company”) (the “Second Merger”); and (iii) the subsequent merger of Merger Sub 1 as the surviving company of the Initial Merger with and into the Surviving Company as the surviving company of the Second Merger, with the Surviving Company surviving such merger (the “Third Merger”). Pursuant to the Mergers, prior unitholders, shareholders and warrant holders of PCAC and FFG received securities of LGHL, and the surviving company became a wholly owned subsidiary of LGHL.

“Meritz” means Meritz Securities Co., Ltd, a Korean incorporated investment fund.

“Amended and Restated Meritz Relationship Agreement” means the relationship agreement, as amended and restated on December 1, 2023, entered into between LGHL and Meritz and setting forth certain rights and obligations of LGHL and Meritz as the holder of Ordinary Shares, which modified the previous relationship agreement dated October 19, 2022.

“Meritz SBSA” means the share buyback and subscription agreement, dated December 1, 2023, pursuant to which Meritz sold and surrendered, and the Company repurchased from Meritz one convertible preference share of the Company and 4,999,999 Ordinary Shares for a price equal to US$54,473,260, and immediately thereafter, Meritz agreed to subscribe for, and the Company issued 19,050,381 Ordinary Shares to Meritz at a total subscription price equal to US$69,473,260.

“Ordinary Shares” means ordinary shares, par value $0.000001 per share, of the Company.

“Private Placement Warrants” means the 11,280,000 warrants originally issued by LGHL on a private placement basis, each exercisable for one Ordinary Share at an exercise price of $11.50 per share, which are substantially identical to Public Warrants, subject to certain limited exceptions.

“Public Warrants” means the 20,699,969 warrants issued by LGHL as part of the Business Combination and listed on NYSE, each of which is exercisable for one Ordinary Share at an exercise price of $11.50 per share, in accordance with its terms.

“SEC” means the United States Securities and Exchange Commission.

2

Table of Contents

“Securities Act” means the Securities Act of 1933, as amended.

“Warrants” means Public Warrants and Private Placement Warrants.

“$,” “USD” and “U. S. dollar” each means the currency in dollars of the United States of America. “U. S.” means the United States of America.

“€,” “EUR” and “Euro” each means the currency introduced at the start of the third stage of European Economic and Monetary Union pursuant to the Treaty on the Functioning of the European Union, as amended.

This annual report includes our audited consolidated financial statements for the years ended December 31, 2021, 2022 and 2023.

Our ordinary shares and warrants are listed on the New York Stock Exchange under the ticker symbols “LANV” and “LANV-WT,” respectively.

3

Table of Contents

FORWARD-LOOKING INFORMATION

This annual report on Form 20-F contains forward-looking statements. Forward-looking statements include all statements that are not historical statements of fact and statements regarding, but not limited to, our expectations, hopes, beliefs, intention or strategies of regarding the future. You can identify these statements by forward-looking words such as “may,” “expect,” “predict,” “potential,” “anticipate,” “contemplate,” “believe,” “estimate,” “intend,” “plan,” “future” “outlook,” “project,” “will” “would” and “continue” or similar words. You should read statements that contain these words carefully because they:

| • | discuss future expectations; |

| • | contain projections of future results of operations or financial condition; or |

| • | state other “forward-looking” information. |

We believe it is important to communicate our expectations to our security holders. However, there may be events in the future that we are not able to predict accurately or over which we have no control. The risk factors and cautionary language discussed in this annual report on Form 20-F provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described by us in such forward-looking statements, including among other things:

| • | changes adversely affecting the business in which we are engaged; |

| • | our projected financial information, anticipated growth rate, profitability and market opportunity may not be an indication of our actual results or our future results; |

| • | management of growth; |

| • | the impact of health epidemics, pandemics and similar outbreaks, including the COVID-19 pandemic on our business; |

| • | our ability to safeguard the value, recognition and reputation of our brands and to identify and respond to new and changing customer preferences; |

| • | the ability and desire of consumers to shop; |

| • | our ability to successfully implement our business strategies and plans; |

| • | our ability to effectively manage our advertising and marketing expenses and achieve desired impact; |

| • | our ability to accurately forecast consumer demand; |

| • | high levels of competition in the personal luxury products market; |

| • | disruptions to our distribution facilities or our distribution partners; |

| • | our ability to negotiate, maintain or renew our license agreements; |

| • | our ability to protect our intellectual property rights; |

| • | our ability to attract and retain qualified employees and preserve craftmanship skills; |

| • | our ability to develop and maintain effective internal controls; |

| • | general economic conditions; |

| • | the result of future financing efforts; and |

4

Table of Contents

| • | other factors discussed elsewhere in this annual report on Form 20-F, including the section entitled “Risk Factors.” |

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this annual report on Form 20-F.

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this annual report on Form 20-F. All forward-looking statements included herein are expressly qualified in their entirety by the cautionary statements contained or referred to in this section as well as any other cautionary statements contained herein. Except to the extent required by applicable laws and regulations, we undertake no obligations to update these forward-looking statements to reflect events or circumstances after the date of this annual report on Form 20-F or to reflect the occurrence of unanticipated events. In light of these risks and uncertainties, you should keep in mind that any event described in a forward-looking statement made in this annual report on Form 20-F or elsewhere might not occur.

5

Table of Contents

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not required.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not required.

| ITEM 3. | KEY INFORMATION |

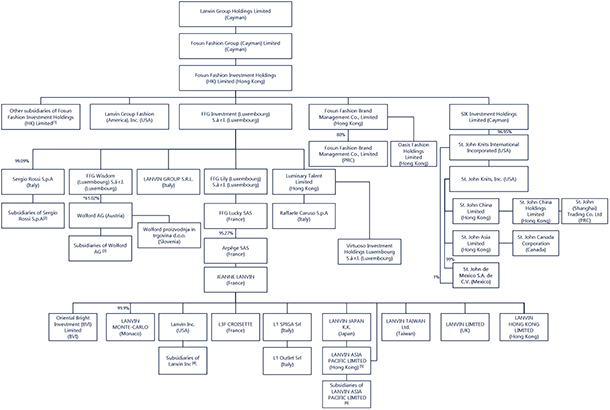

We are a Cayman Islands holding company, and our operations are conducted by our subsidiaries organized in various jurisdictions, including China.

PRC Permissions and Approvals

We conduct a portion (approximately 12.5% of our revenues in 2023) of our operations in the Greater China region, and as of the date of this annual report, we have obtained all requisite permissions and approvals that are material to our operations in China. However, there can be no assurance that we will be able to maintain such permissions and approvals in the future. In addition, laws and regulations in China may change quickly with little advance notice, and the Chinese government may intervene or influence our operations in China at any time. As a result, we may be required to obtain additional permissions and approvals in the future. There can be no assurance that such permissions and approvals can be obtained in a timely manner, or at all, and our business, results of operations and financial condition could be materially and adversely affected.

Under the PRC laws, rules and regulations currently in effect, no prior permission or approval from PRC government authority is required for the transactions completed pursuant to the Business Combination Agreement, including but not limited to the listing of our securities on the NYSE. However, the Chinese government has recently indicated that it may exert more control over offerings conducted overseas and foreign investment in China-based issuers. In particular, on February 17, 2023, the China Securities Regulatory Commission, or the CSRC, released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, which came into effect on March 31, 2023. The Trial Measures will apply to overseas securities offerings and/or listings conducted by (i) companies incorporated in the PRC, or PRC domestic companies, directly and (ii) companies incorporated overseas with operations primarily in the PRC and valued on the basis of interests in PRC domestic companies, or indirect offerings. An equity or equity linked securities offering by an overseas company will be deemed an indirect offering if (i) more than 50% of such overseas company’s consolidated revenues, profit, total assets or net assets that are derived from its audited consolidated financial statements for the most recently completed fiscal year are attributable to PRC domestic companies, and (ii) any of the following three circumstances applies: key components of its operations are carried out in the PRC; its principal places of business are located in the PRC; or the majority of the senior management members in charge of operation and management are PRC citizens or residents.

The Trial Measures requires filings with the CSRC within three business days after the submission of an initial public offering or listing application overseas, or three business days after the completion of a follow-on offering in the same overseas market. If a company that should have been subject to the Trial Measures (i) has completed overseas offering and listing prior to the effectiveness of the Trial Measures; or (ii) (a) has its registration statement declared effective by the SEC prior to the effectiveness of the Trial Measures, and (b) while it is not necessary to fulfill any other regulatory procedures requested by the overseas regulators or overseas stock exchanges, will further complete its overseas offering and listing by September 30, 2023, such company is not required to file for such offering immediately, but should file as required if it is involved in follow-on offerings and other matters that require filing.

Our PRC subsidiaries accounted for less than 50% of our consolidated revenues, profit, total assets and net assets in 2021, 2022 and 2023. However, the interpretation, application and enforcement of the Trial Measures are still evolving and it remains uncertain whether the requirements under the Trial Measures are applicable to a securities offering by us.

6

Table of Contents

On December 28, 2021, the Cyberspace Administration of China, together with certain other government authorities, promulgated the Revised Cybersecurity Review Measures that took effect from February 15, 2022, pursuant to which online platform operators holding over one million users’ information must apply for a cybersecurity review before listing abroad, and operators of “critical information infrastructure” that intend to purchase internet products and services that will or may affect national security must apply for a cybersecurity review. Furthermore, the competent government authorities may also initiate a cybersecurity review against the relevant operators where the authorities believe that the network product or service or data processing activities affect or may affect national security. However, the scope of potential operators of “critical information infrastructure” remains unclear. In addition, the scope of network product or service or data processing activities that will or may affect national security is also unclear and subject to regulatory interpretation. As of the date of this annual report (i) we had not been informed by any PRC governmental authority of any requirement to apply for a cybersecurity review; (ii) we did not hold or process personal information of over one million users; and (iii) we had not received any investigation, notice, warning, or sanctions from applicable government authorities in relation to national security. Nonetheless, the interpretation and implementation of the Revised Cybersecurity Review Measures is subject to uncertainties, and the relevant laws and regulations may also change in the future.

As a result of such regulatory development, government authorities in China could conduct a cybersecurity review over our PRC subsidiaries, which may have a material adverse effect on our business, results of operations and financial condition. See “—D. Risk Factors—Risks Relating to Our Business and Industry—If we were to become subject to the oversight, discretion or control of PRC government authorities over overseas offerings of securities and/or foreign investments, it may result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline, which would materially affect the interests of the investors.”

We are an offshore holding company and have operations in the PRC conducted by our PRC subsidiaries. We may make loans to our PRC subsidiaries subject to the approval from or registration with the governmental authorities and other limitations in the future. These include foreign exchange loan registrations and maximum statutory limit of the loan amount (which is either the difference between the registered capital and the total investment amount of the concerned company or the upper limit calculated based on the formula prescribed in the prevailing regulations). There can be no assurance that such permissions and approvals can be obtained in a timely manner, or at all, and our business, results of operations and financial condition could be materially and adversely affected.

Permissions and Approvals on Transfer and Repatriation of Cash within Our Group

We transfer cash to our subsidiaries through capital injections and shareholder loans. Subject to the cash needs of the subsidiaries, shareholders’ loans as granted may be capitalized (as equity) or repaid.

Cash in the subsidiaries may also be repatriated to us via dividend distribution. Nevertheless, no cash repatriation by way of distribution/dividends was made to us prior to our Business Combination or to LGHL as of the date of this annual report.

Our principal subsidiaries, being our portfolio brands, are based mainly in the U.S. (Delaware) and Europe including Italy, France and Austria. We are subject to certain restrictions or limitations regarding distribution of earnings from the portfolio brands to us, which may in turn limit the cash available to make distributions to our shareholders. For our operating subsidiaries that are Delaware corporations, to which the Delaware General Corporation Law (DGCL) applies, the power and authority to declare dividends/distributions resides with the board of directors of the corporation. Further, the DGCL permits distributions out of either a surplus or net profits (subject to certain limitations). In addition, specific provisions under credit agreements or the relevant subsidiary’s bylaws may impose specific restrictions or approval requirements regarding dividend payment (including a contingent obligation or otherwise). For our Italian subsidiaries, no distribution may be made unless a reserve fund accumulated from net profits reach at least 20% of the relevant subsidiary’s share capital. Our subsidiaries in Italy also face other general restrictions to the shareholders’ right to an earnings distribution. In Austria, our subsidiaries cannot issue a dividend unless the validly adopted financial statements for a financial year show a balance sheet profit, which represents the maximum amount of capital available for the distribution of profits. Loans by us to our subsidiaries in Austria are considered equity substitution if we are in a crisis, and will only be repaid if we are fully restructured.

7

Table of Contents

For our portfolio brands, the cash needs of the brands’ subsidiaries are provided as necessary in the form of shareholder loans or capital injections from us or the relevant parent brand entity. Payments from local subsidiaries to their parent brands are typically for purchase of inventories from the parent brand, and generally do not face any foreign exchange or capital control limitations. However, dividends and loan repayments may face similar restrictions as mentioned above.

Dividends repatriated or paid from our Chinese subsidiaries must be made from retained earnings as per such subsidiary’s financial statements prepared in accordance with Chinese accounting rules. Additionally, each of our Chinese subsidiaries must set aside a statutory reserve fund of at least 50% of its registered capital before it may pay dividends, and a 10% withholding tax or other reduced rate withholding tax under the China-Hong Kong treaty may be applied to the dividends repatriated from our Chinese subsidiaries. Also, approval from or registration with appropriate Chinese government authorities is required where RMB is to be converted into foreign currency and remitted outside of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. However, we do not expect Chinese subsidiaries to declare any dividends or pay capital expenses to our portfolio brands in the near future.

We made capital injections of EUR50.0 million in 2021, EUR50.0 million in 2022 and EUR27.0 million in 2023 into Lanvin brand portfolio through Arpège SAS, as well as EUR7.9 million in Raffaele Caruso S.p.A. in 2021. We also made an advance payment of EUR1.0million in Raffaele Caruso S.p.A in 2023. Caruso also received a shareholder loan of EUR2.5 million, EUR5.5 million and EUR1.0 million from us in 2021, 2022 and 2023, respectively. We have waived part of the repayment of shareholder loan by Caruso. In 2023, we paid EUR11.78 million for the subscription of Wolford shares. In addition, Wolford AG received shareholder loans of EUR10.0 million, EUR22.5 million, and EUR10.8 million from us in 2021, 2022 and 2023, respectively. In 2021, 2022 and 2023, we issued shareholder loans of $35.8 million, $25.5 million and $12.5 million, respectively, to St. John. After we acquired Sergio Rossi in 2021, Sergio Rossi S.p.A received capital injections of EUR5.0 million, EUR13.0 million and EUR11.0 million in 2021, 2022 and 2023, respectively. In 2023, Sergio Rossi S.p.A received a shareholder loan of EUR3.5million from us. We have also made capital injections and intercompany loans totaling RMB1.1 million, $3.7 million and $2.5 million to our Chinese subsidiaries in 2021, 2022 and 2023, respectively.

Other than the loan repayment of $1.0 million by St. John to us in August 2023, none of our direct subsidiaries made any dividends, distributions, or repayments to us in 2021, 2022 and 2023. We have also not made any transfers, dividends, or distributions to our shareholders as of the date of this annual report other than the cash dividend of $1.0 million and $1.0 million paid to Meritz in 2022 and 2023, respectively. On March 30, 2023, Jeanne Lanvin S.A. (“JLSA”) as the borrower, LGHL as the guarantor and Meritz as the lender entered into a facility agreement, pursuant to which Meritz made available to JLSA a facility in the sum of JPY3,714.4 million (the “Facility”). In 2023, a total of JPY502.3 million under the Facility was repaid to Meritz, including both principal and interest. See “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Meritz Private Placement” and “Item 7. Major Shareholders and Other Related Party Transactions—B. Related Party Transactions—Other Related Party Transactions—Shareholder Loans.”

The Holding Foreign Companies Accountable Act

We may be subject to the risk of trading prohibitions under the Holding Foreign Companies Accountable Act, or the HFCA Act. Our independent auditor, Grant Thornton Zhitong Certified Public Accountants LLP, is an independent registered accounting firm based in mainland China. Pursuant to the HFCA Act and related regulations, if we have filed an audit report issued by a registered public accounting firm that the PCAOB has determined is unable to inspect and investigate completely for two consecutive years, the SEC will prohibit our securities from being traded on a national securities exchange or in the over-the-counter trading market in the United States. In August 2022, the PCAOB signed a Statement of Protocol with the relevant PRC authorities governing inspections and investigations of audit firms based in China, pursuant to which the PCAOB determined that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China or Hong Kong in December 2022 and vacated its December 16, 2021 determinations to the contrary. However, there can be no assurance that the PCAOB will continue to have such access. Should PRC authorities fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination, which may affect our ability to maintain the listing of our securities on the U.S. national securities exchanges, including the NYSE, and the trading of them in the over-the-counter trading market. A delisting would substantially impair your ability to sell or purchase our securities when you wish to do so, and the risk and uncertainty associated with a potential delisting would have a negative impact on the price of our securities. For details, see “—D. Risk Factors Risks Related to Our Securities—Our ability to maintain the listing of our securities on the NYSE may be dependent on the PCAOB’s continued access to inspect our independent auditors.”

8

Table of Contents

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not required.

| C. | Reasons for the Offer and Use of Proceeds |

Not required.

| D. | Risk Factors |

Summary of Risk Factors

Investing in our securities involves significant risks. You should carefully consider all of the information in this annual report before making an investment in our securities. Below please find a summary of the principal risks we face, organized under relevant headings:

Risks Relating to Our Business and Industry

| • | We have incurred significant losses in the past and anticipate that we will continue to incur losses for the current year and upcoming future years. |

| • | The re-branding to Lanvin Group is being challenged by the minority shareholders of Arpège SAS. Arpège SAS, one of our subsidiaries, holds our Lanvin brand portfolio including the “Lanvin” brand name. We cannot predict the outcome of such challenge and may have to discontinue the use by us, at the group holding company level, of the Lanvin brand name. |

| • | The success of our luxury fashion businesses depends on the value of our brands and, if the value of any of those brands were to diminish, our business could be adversely affected. |

| • | We face risks related to health epidemics, pandemics and similar outbreaks, such as the COVID-19 pandemic, which has had and may continue to have a material adverse impact on our business, financial condition and results of operations. |

| • | The long-term growth of our business depends on the successful execution of our strategic initiatives and we may not be able to continue to develop and grow our businesses. |

| • | Our growth depends, in part, on our continued retail expansion, and we may not be successful in undertaking such expansion. |

| • | Our business is heavily dependent on the ability and desire of consumers to shop. |

| • | Our inability to effectively execute our e-commerce strategy could materially adversely affect the reputation of our brands and our revenue and our operating results may be harmed. |

| • | We utilize a range of marketing, advertising, and other initiatives to increase existing customers’ spending and to acquire new customers; if the costs of advertising or marketing increase, or if our initiatives fail to achieve their desired impact, we may be unable to grow the business profitably. |

| • | Failure to accurately forecast consumer demand could lead to excess inventories or inventory shortages, which could result in decreased operating margins, reduced cash flows, and harm to our business. |

9

Table of Contents

| • | Counterfeit or ”knock-off” products, as well as products that are “inspired by” our brands may siphon off demand for our brands’ products and may result in customer confusion, harm to our brands, a loss of our market share and/or a decrease in our results of operations. |

| • | We are dependent on suppliers for our products and raw materials, which poses risks to our business operations. |

| • | We face intense competition in the personal luxury goods industry. |

| • | Our customer relationships and sales have been and may be negatively impacted if we do not anticipate and respond to consumer preferences and fashion trends or manage inventory levels appropriately. |

| • | We are subject to certain risks related to the sale of our products through our direct-to-consumer (“DTC”) channel and in particular our directly operated stores. |

| • | A data security or privacy breach could damage our reputation and our relationships with our customers or employees, expose us to litigation risk, and adversely affect our business. |

| • | We are exposed to the risk that personal information of our customers, employees and other parties collected in the course of our operations may be damaged, lost, stolen, divulged or processed for unauthorized purposes. |

| • | Future economic conditions, including volatility in the financial and credit markets, may adversely affect our business. |

| • | Significant inflation could adversely affect our results of operations and financial condition. |

| • | We are dependent on a limited number of distribution facilities operated by us as well as those of our distribution partners. If one or more of our distribution facilities or those of our distribution partners experience operational difficulties or becomes inoperable, it could have a material adverse effect on our business, results of operations and financial condition. |

| • | Our revenues and operating results are affected by the seasonal nature of our business and cyclical trends in consumer spending. |

| • | If our suppliers, licensees, or other business partners, or the suppliers used by our licensees fail to use legal and ethical business practices, our business could suffer. |

| • | Our potential inability to find suitable new targets to drive inorganic business growth and the risk that any acquisitions we do complete may not be successful in achieving intended benefits, cost savings and synergies. |

| • | We could be adversely affected if we are unable to negotiate, maintain or renew our license agreements. |

| • | If our trademarks and intellectual property or other proprietary rights are not adequately protected to prevent use or appropriation by third parties, the value of our brand and other intangible assets may be diminished, and our business may be adversely affected. |

| • | We are subject to certain laws, litigation, regulatory matters and ethical standards, and compliance or our failure to comply with or adequately address developments as they arise could adversely affect our reputation and operations. |

| • | We are subject to legal and regulatory risk. |

| • | Changes to taxation or the interpretation or application of tax laws could have an adverse impact on our results of operations and financial condition. |

| • | We are subject to risks associated with climate change and other environmental impacts and increased focus by stakeholders on environment, social and governance (“ESG”) matters. |

10

Table of Contents

| • | We may lose key employees or may be unable to hire qualified employees. |

| • | We depend on highly specialized craftsmanship and skills. |

| • | We are exposed to fluctuations in currency exchange rates. |

| • | We are subject to risks related to the complexity and uncertainty in interpretation of transfer pricing rules. |

| • | We operate in many countries around the world and, accordingly, we are exposed to various international business, regulatory, social and political risks. |

| • | Changes in global economic, political or social conditions or government policies could have a material adverse effect on our business and operations. |

| • | There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations, and changes in laws, rules and regulations in China could adversely affect us. |

| • | If we were to become subject to the oversight, discretion or control of PRC government authorities over overseas offerings of securities and/or foreign investments, it may result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline, which would materially affect the interests of the investors. |

| • | Changes in tax laws, regulations and policies in jurisdictions in which we operate may materially and adversely affect our results of operations and financial condition. |

| • | Because of the costs and difficulties inherent in managing cross-border business operations, our results of operations may be negatively impacted. |

| • | The conflict in Ukraine and sanctions and export controls imposed in response to the conflict, including on Russia and Belarus, may adversely affect our business and other escalating global trade tensions, wars and conflicts, and the adoption or expansion of economic sanctions, export controls, or other trade restrictions could negatively affect us. |

| • | Adverse developments affecting the financial services industry, such as actual events or concerns involving liquidity, defaults or non-performance by financial institutions or transactional counterparties, could adversely affect our business operations, results of operations and financial condition. |

| • | We rely to a significant extent on dividends and other distributions on equity paid by our principal operating subsidiaries to fund offshore cash and financing requirements. Any limitation on the ability of our operating subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business. |

| • | We expect to incur negative operating cash flows in the next few years and may need to raise substantial additional funding. If we are unable to raise capital or obtain sufficient funding from our shareholders when needed or on attractive terms, we would be forced to delay, scale back or discontinue some of our businesses, operations, investments, acquisitions or other growth initiatives. |

| • | Failure to comply with the terms of our indebtedness could have a material adverse effect on our ability to conduct our business. |

Risks Relating to Our Securities

| • | The trading price of our securities has been and is likely to continue to be volatile, which could result in substantial losses to holders of our securities. |

| • | Sales of a substantial number of our securities in the public market by our existing securityholders could cause the price of our Ordinary Shares and Warrants to fall. |

11

Table of Contents

| • | A certain number of our Warrants will become exercisable for our Ordinary Shares, which would increase the number of shares eligible for future resale in the public market and result in dilution to our shareholders. |

| • | If securities or industry analysts do not publish research, publish inaccurate or unfavorable research or cease publishing research about us, our share price and trading volume could decline significantly. |

| • | Future resales of our Ordinary Shares issued to Fosun and its affiliates may cause the market price of our securities to drop significantly, even if our business is doing well. |

| • | The Existing Warrant Agreement designates the courts of the State of New York or the United States District Court for the Southern District of New York as the sole and exclusive forum for certain types of actions and proceedings that may be initiated by Warrant holders, which could limit the ability of Warrant holders to obtain a favorable judicial forum for disputes with us in connection with such Warrants. |

| • | The requirements of being a public company may strain our resources, divert our management’s attention and affect our ability to attract and retain qualified board members. |

| • | Our ability to maintain the listing of our securities on the NYSE may be dependent on the PCAOB’s continued access to inspect our independent auditors. |

| • | We qualify as a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions applicable to United States domestic public companies and will follow certain home-country corporate governance practices in lieu of certain NYSE requirements applicable to U.S. issuers. |

| • | As a company incorporated in the Cayman Islands, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from NYSE corporate governance listing standards applicable to domestic U.S. companies; these practices may afford less protection to shareholders than they would enjoy if we complied fully with NYSE corporate governance listing standards. |

| • | You may face difficulties in protecting your interests, and your ability to protect your rights through U.S. courts may be limited, because we are incorporated under the laws of the Cayman Islands, we conduct substantially all of our operations, and a majority of our directors and executive officers reside, outside of the United States. The ability of U.S. authorities to bring actions for violations of U.S. securities laws and regulations against us and our directors and executive officers may be limited, and accordingly you may not be afforded the same protection as provided to investors in U.S. domestic companies. |

| • | We may be subject to securities litigation, which is expensive and could divert management attention. |

| • | We may not pay cash dividends in the foreseeable future. |

| • | The exercise price of our Warrants can fluctuate under certain circumstances which, if triggered, can potentially result in material dilution of our then existing shareholders. |

| • | Certain rights granted to Meritz in the Amended and Restated Meritz Relationship Agreement could limit the funds available to us or potentially result in dilution of our then existing shareholders. |

| • | We have identified material weaknesses in our internal control over financial reporting. If we are unable to remediate these material weaknesses or otherwise fail to maintain an effective system of disclosure controls and internal control over financial reporting, our ability to produce timely and accurate financial statements or comply with applicable regulations could be impaired. |

| • | We qualify as an “emerging growth company” within the meaning of the Securities Act, and as we intend to take advantage of certain exemptions from disclosure requirements available to emerging growth companies, it could make our securities less attractive to investors and may make it more difficult to compare our performance to the performance of other public companies. |

12

Table of Contents

| • | We are a “controlled company” within the meaning of NYSE listing rules and, as a result, can rely on exemptions from certain corporate governance requirements that provide protection to shareholders of other companies. |

| • | Fosun, being our controlling shareholder, has substantial influence over us and Fosun’s interests may not be aligned with the interests of our other shareholders, and Fosun losing control of us may materially and adversely impact us and our Securities. |

| • | We have granted in the past, and we will also grant in the future, share incentives and economic beneficiary rights scheme, which may result in increased share-based compensation expenses. |

| • | We may be or become a passive foreign investment company (“PFIC”), which could result in adverse U.S. federal income tax consequences to shareholders who are U.S. persons. |

| • | We may be subject to U.S. foreign investment regulations which may limit certain investors’ ability to purchase our securities. Our existing and future investments in U.S. companies may also be subject to U.S. foreign investment regulations. |

Risks Relating to Our Business and Industry

We have incurred significant losses in the past and anticipate that we will continue to incur losses for the current year and upcoming future years.

We have incurred significant losses in the past and anticipate that we will continue to incur losses in the current year and upcoming years. We incurred losses of €76.5 million, €239.8 million and €146.3 million in the years ended December 31, 2021, 2022 and 2023, respectively. We cannot assure you that we will be able to generate profit in the future. We will need to generate and sustain increased revenue levels in future periods to achieve profitability, and even if we achieve profitability, we may not be able to maintain or increase our level of profitability. Our efforts to grow our business may be more costly than we expect or may not result in the returns we anticipate, and we may not be able to increase our revenue enough to offset our higher operating expenses. As a result, there can be no assurance that we will achieve profitability, and we may continue to experience loss in the future.

The re-branding to Lanvin Group is being challenged by the minority shareholders of Arpège SAS. Arpège SAS, one of our subsidiaries, holds our Lanvin brand portfolio including the “Lanvin” brand name. We cannot predict the outcome of such challenge and may have to discontinue the use by us, at the group holding company level, of the Lanvin brand name.

In 2018, we acquired a controlling stake in Arpège SAS and its subsidiary Jeanne Lanvin SA, which in turn owns the brand “Lanvin”. The shareholders’ agreement entered into by and between FIH and certain minority shareholders of Arpège SAS (as subsequently acceded to by FFG Lily (Luxembourg) S.à.r.1 and then by FFG Lucky SAS, the “Lanvin SHA”) provides that certain matters require an affirmative vote of each member of the board of Arpège SAS representing minority shareholders, including the entry into any related party transactions. The minority shareholders currently own, in the aggregate, 4.73% of the equity securities in Arpège SAS.

In October 2021, after rounds of discussion and negotiation with the minority shareholders, we proposed to the members of the board of Arpège SAS representing minority shareholders that an authorization letter permitting the rest of the Lanvin Group to use the “Lanvin” name and brand as part of an international re-branding of Fosun Fashion Group be approved by the board of Arpège SAS. The re-branding was worldwide and well received by our investors and the press. At that time the minority shareholders did not object to the use of the “Lanvin” corporate name and merely suggested some changes to the terms of the authorization letter. We believed such terms were generally reasonable and would be quickly resolved in an amicable fashion. In March through May 2022, the parties continued discussions and negotiations in what appeared to us to be in an amicable and reasonable fashion. In September 2022, we received a letter (the “Minority Shareholder Letter of September 2022”) from one of the minority shareholders (the “Alleging Shareholder”) alleging that we had improperly used the “Lanvin” corporate name in connection with our re-branding initiative and that they had not given formal approval pursuant to the terms of the Lanvin SHA prior to our re-branding. The Alleging Shareholder had also stated in the same letter that other minority shareholders also object to our use of the “Lanvin” name in connection with our re-branding initiative.

13

Table of Contents

We have sought preliminary legal advice and believe we have strong legal defense to such allegations. No formal legal proceedings have been brought by the minority shareholders to date. Any such proceedings or claims can have an adverse impact on us because of defense and settlement costs, diversion of resources and other factors, and there can be no assurance that we will prevail in any legal proceeding that may be brought by the minority shareholders or that we will be able to settle these allegations on a timely basis or on terms that are acceptable to us, or at all. Accordingly, we might have to cease our use, at the group holding company level, of the “Lanvin” brand name, and change to another name (or revert to our previous name as Fosun Fashion Group) should we not prevail or settle these allegations. However, we do not expect that, even if we do not prevail or settle these allegations, the continued use of the Lanvin name by Arpège SAS and its subsidiaries, which constitute our Lanvin brand portfolio, will be affected.

The success of our luxury fashion businesses depends on the value of our brands and, if the value of any of those brands were to diminish, our business could be adversely affected.

Our success depends on our brands and their value. The brand names such as Lanvin, Wolford and Sergio Rossi are integral to the existing businesses, as well as to our strategies for continuing to grow and expand the business. Our sales and our ability to achieve premium pricing depend on the perception, recognition and reputation of our brands, which, in turn, depend on factors such as product design, the distinctive character and the quality of our products and customer service, the image of our stores and those of our wholesale customers, the success of our advertising and communication activities and our general corporate profile.

The recognition, integrity and reputation of our brands are among our most valuable assets, which are influenced by several factors, some of which are outside of our control. Our brands’ values could diminish significantly due to a number of factors, including changing consumer attitudes regarding social issues and consumer perception that we have acted in an irresponsible manner. Negative claims or publicity regarding our brands or products, including licensed products, especially through social media, and increase the potential scope of negative publicity, could adversely affect the reputation of the brands and sales even if the subject of such publicity is unverified or inaccurate. Other factors that may adversely affect our brands’ image include our inability to respond adequately to the needs and expectations of our customers with regard to the quality, style and design of our products, the dissemination by third parties of information that is untrue or defamatory, the commencement of litigation proceedings against us, as well as factors attributable to the parallel distribution and counterfeiting of our products. Each of these factors could harm the recognition, integrity and reputation of our brands, causing us to lose existing customers or fail to attract new customers, or otherwise having a material adverse effect on our business, results of operations and financial condition.

Our reputation may also suffer as a result of the fact that we are dependent on our suppliers. While we closely monitor our suppliers to ensure that they comply with all applicable laws and regulations by, among other things, reviewing any published violations and media reports relating to actual or alleged violations, as well as conducting internal due diligence, there can be no assurance that these measures will always be effective. If suppliers fail to comply with applicable law, including but not limited to those relating to labor, social security, health and safety, or if they deliver products that are defective or differ from our specifications or quality standards or do not comply with applicable law, this could have adverse effects on our production cycle and/or product quality and cause delays in product deliveries to our customers. Any of the foregoing in turn could damage our reputation, with possible adverse effects on our business, results of operations and financial condition.

We face risks related to health epidemics, pandemics and similar outbreaks, such as the COVID-19 pandemic, which has had and may continue to have a material adverse impact on our business, financial condition and results of operations.

Our business has been and may continue to be materially and adversely affected by health epidemics, pandemics and similar outbreaks, such as the COVID-19 pandemic. For example, as a result of the COVID-19 pandemic, governments and authorities across the world implemented restrictive measures to prevent the spread of the virus. These restrictive measures impacted our operations in a number of respects, including cancelations of or capacity restrictions on certain marketing and brand events and limitations on in-person meetings among our sales teams. In addition, the inability or unwillingness of customers to travel had a significant impact on sales driven by tourism. Restrictive measures in certain regions also resulted in store closures which prevented consumers from purchasing goods directly from stores. In places where our retail stores were open, they generally operated on reduced hours and at reduced occupancy levels and were subject to closure due to health protocols or more limited governmental orders during the COVID-19 pandemic. The impact of the COVID-19 pandemic on some of our wholesale customers resulted in them closing some of their stores. The COVID-19 pandemic also impacted our supply chain partners, including third-party manufacturers, logistics providers and other vendors, as well as the supply chains of our wholesale customers, retail stores and licensees, due to factory closures, labor shortages, imposed restrictions on travel and import/export delays. At the same time, the reduced mobility of customers as a result of the pandemic reduced customers desire to shop and incur spending on personal luxury goods.

14

Table of Contents

Store closures, reduced store hours and occupancy levels, travel restrictions and concerns about the health risks of traveling during the COVID-19 pandemic adversely affected traffic in our stores and our wholesale customers’ stores. Consumer spending behavior was and may continue to be negatively impacted by job losses and reduced incomes, changing needs due to remote working, reduced in-person social interaction, vacation time spent at home and other factors. This can be exemplified by the impact on the formalwear segment of each of our brands, as not going to the office means fewer men are wearing dress shirts and ties and by the impact on our shoe business, as women are wearing and purchasing fewer high heeled shoes for the same reasons. All these factors have and may continue to negatively impact our direct sales to consumers and our sales to our wholesale customers, due to lower sales of our products, and those of our licensees, through their sales channels.

In addition, if sales, which are more difficult to predict due to the uncertainties surrounding the pandemic, exceed or fall below our expectations, we may experience a shortage of products required to meet demand or excess inventory levels, respectively. Inventory levels in excess of consumer demand may result in inventory write-downs and the sale of excess inventory at discounted prices, which could have a material adverse effect on the reputation of our brands and our profitability.

The long-term growth of our business depends on the successful execution of our strategic initiatives and we may not be able to continue to develop and grow our businesses.

A significant portion of our business strategy involves growing our current brands, notwithstanding our intention to invest in new business lines and their development. Our achievement of revenue and profitability growth from these brands will depend largely upon our ability to:

| • | continue to maintain and enhance the distinctive brand identities of the brands; and |

| • | continue to strengthen and expand the brands’ businesses. |

As part of our long-term strategy, we intend to grow our market share and revenue through the following:

| • | unleashing brand heritage and refreshing brand images to connect with today’s consumers; |

| • | optimizing product category mixes within our current brands; |

| • | expanding our channels and footprint across the world; |

| • | reinforcing global digital strategies and customer experiences |

| • | harnessing the strength of our global platform to develop our brands; |

| • | leveraging our unique strategic alliances to drive synergies and sustainable growth; and |

| • | identifying new strategic investments that complement our luxury fashion ecosystem. |

We cannot guarantee that we will be able to successfully execute on these strategic initiatives. For example, we may not be able to successfully increase brand engagement due to the impact of the COVID-19 pandemic and/or unsuccessful marketing campaigns, we may not be able to optimize the customer experience if we are unable to react quickly enough to customer needs and/or complains and our investments in technology may not succeed if we are unable to implement certain digitalization efforts or new technologies and systems do not work as expected. If we are unable to execute on our strategic initiatives, including for reasons due to the challenges we face as a result of the COVID-19 pandemic, our business, results of operations and financial condition could be materially adversely affected.

15

Table of Contents

Further, we believe that our success is largely dependent on the images of our brands and ability to anticipate and respond promptly to changing consumer demands and fashion trends in the design, styling, production, merchandising and pricing of products. If we do not correctly gauge consumer needs and fashion trends and respond appropriately, consumers may not purchase our products and our brand names and the images of our brands may be impaired. Even if we react appropriately to changes in fashion trends and consumer preferences, consumers may consider our brands to be outdated or associate our brands with styles that are no longer popular or trend-setting. Any of these outcomes could have a material adverse effect on our brands, business, results of operations and financial condition.

We cannot assure you that we can successfully execute any of these actions or our growth strategy for our businesses, nor can we assure you that the launch of any additional product lines or businesses by us or that the continued offering of existing lines will achieve the degree of consistent success necessary to generate profits or positive cash flow. Our ability to carry out our growth strategy successfully may be affected by, among other things, our ability to enhance our relationships with existing customers, our ability to attract retail customers to our direct-to-consumer or DTC channels, our ability to develop new relationships with retailers, economic and competitive conditions, changes in consumer spending patterns and changes in consumer tastes and style trends. If we fail to continue to develop and grow the brands’ businesses, our financial condition and results of operations may be materially adversely affected.

Our growth depends, in part, on our continued retail expansion, and we may not be successful in undertaking such expansion.

We believe that our future growth depends not only on serving existing customers, but also on continuing to get new customers and expanding our distribution base internationally, including but not limited to opening of new retail stores. When expanding into new locations and markets, we may face challenges that are different from those we currently encounter, including competitive, merchandising, distribution, hiring, legal and regulatory, and other difficulties. Although we continue to evaluate sales and marketing efforts and other strategies to expand our supplier, customer and distribution bases, there is no assurance that we will be successful. If we are not successful, this could have a material adverse effect on our business, financial condition and results of operations.

Our business is heavily dependent on the ability and desire of consumers to shop.

Reduced consumer traffic and purchasing, whether in our own retail stores or in the stores of our wholesale customers, could have a material adverse effect on our financial condition, results of operations and cash flows. Reductions could result from economic conditions, fuel shortages, increased fuel prices and other circumstances, including adverse weather conditions, natural disasters, war, terrorist attacks or the perceived threat of war or terrorist attacks. Disease epidemics and other health-related concerns, also could result in (and, in the case of the COVID-19 pandemic, resulted in) closed stores, reduced consumer traffic and purchasing (including international tourist traffic and spending), as consumers become ill or limit or cease shopping in order to avoid exposure, or governments impose mandatory business closures, travel restrictions or the like to prevent the spread of disease. Additionally, political or civil unrest and demonstrations also could affect consumer traffic and purchasing.

For example, the COVID-19 pandemic affected our business operations, financial position, and cash flows. This included cancellations or capacity restrictions on marketing events, limitations on sales team meetings, and reduced tourism affecting sales. Store closures in some regions hindered direct consumer purchases. Despite these challenges, we are gradually recovering from the pandemic’s effects. Consumers were also affected, resulting in additional adverse impacts on us. Consumers were unable to purchase our products due to the unwillingness to shop in stores out of fear of exposure. Store closures, reduced store hours and occupancy levels, travel restrictions and concerns about the health risks of traveling adversely affected traffic in our stores and our wholesale customers’ stores. Consumer spending behavior was also and may continue to be negatively impacted by job losses and reduced incomes, changing needs due to remote working, reduced in-person social interaction, vacation time spent at home and other factors. In addition to the factors discussed above, international tourism was also reduced, and negatively affected sales from international tourists at our retail stores or the stores of our wholesale customers.

16

Table of Contents

Other factors that could affect the success of our stores include:

| • | the location of the store or mall, including the location of a particular store within the mall; |

| • | the other tenants occupying space at the mall; |

| • | increased competition in areas where the stores are located; |

| • | the amount of advertising and promotional dollars spent on attracting consumers to the store or mall; |

| • | the changing patterns of consumer shopping behavior; |

| • | increased competition from online retailers; and |

| • | the diversion of sales from our retail stores to our digital commerce sites. |

Our inability to effectively execute our e-commerce strategy could materially adversely affect the reputation of our brands and our revenue and our operating results may be harmed.

E-commerce is the one of the fastest growing areas of our business both with respect to our direct-to-consumer businesses and the wholesale business (i.e., sales to pure play and e-commerce businesses of traditional retailers). The success of our e-commerce businesses depends, in part, on third parties and factors over which we have limited control, including changing consumer preferences and buying trends relating to e-commerce usage and promotional or other advertising initiatives employed by our wholesale customers or other third parties on their e-commerce sites. Any failure on our part, or on the part of our third party digital partners, to provide e-commerce platforms that attract consumers, build our brands and drive repeat consumer purchases could result in diminished brand image, relevance and loyalty and lost revenue. Additionally, as consumers shift purchasing preferences to online channels, the failure of our e-commerce channels to attract consumers who previously made purchases in our stores and those operated by our wholesale partners, will adversely affect our financial condition and results of operations.

Our operation of e-commerce sites pose risks and uncertainties including:

| • | changes in required technology interfaces; |

| • | website downtime and other technical failures; |

| • | costs and technical issues from website software upgrades; |

| • | data and system security; |

| • | computer viruses; and |

| • | changes in applicable laws and regulations. |

Keeping current with technology, competitive trends and the like may increase our costs and may not succeed in increasing sales or attracting consumers. Our failure to respond successfully to these risks and uncertainties might adversely affect the reputation of our brands and our revenue and results of operations.

The success of our e-commerce businesses depends, in part, on consumer satisfaction, including timely receipt of orders. Fulfillment of these orders requires comprehensive fulfillment infrastructure and different logistics operations than for our retail store and wholesale customer operations. We need adequate capacity, systems and operations to support the anticipated growth in our e-commerce businesses. If we encounter difficulties with our distribution facilities or in our relationships with the third parties who operate the facilities, or if any such facilities were to shut down or be limited in capacity for any reason, including as a result of fire, natural disasters, systems disruptions (including as a result of attacks on computer systems, such as ransomware attacks), or labor interruptions, including as a result of disease epidemics and health related concerns (such as the COVID-19 pandemic), we could experience longer lead times or disruption or delay in distributing our products to our consumers, which could result in consumer dissatisfaction and lost sales. Additionally, we might need to incur significantly higher costs than anticipated to ensure smooth and timely operation. Any of the foregoing could have an adverse effect on the reputation of our brands and our revenue and results of operations.

17

Table of Contents

We utilize a range of marketing, advertising, and other initiatives to increase existing customers’ spending and to acquire new customers; if the costs of advertising or marketing increase, or if our initiatives fail to achieve their desired impact, we may be unable to grow the business profitably.

We utilize a range of marketing, advertising and other initiatives to drive customers from awareness to consideration to conversion, and promoting awareness of our brands and products is important to our ability to grow our business, drive customer engagement, and attract new customers. We invest significant resources in advertising communication and marketing, which include activities ranging from pure digital and social media marketing initiatives to events like fashion shows, product collaborations and co-marketing projects. We adopt a strategy with a dual-focus on both local and broader international audience. For details, see “Item 4. Information on the Company—B. Business Overview—Marketing and Advertising.”

If our marketing and advertising efforts are not appropriately tailored to and accepted by our target customers, we may fail to attract customers, and our brands and reputation may be harmed. In addition, our marketing initiatives may become increasingly expensive as competition increases, and generating a meaningful return on those initiatives may be difficult. Our future growth and profitability and the success of our brands will depend in part upon the effectiveness and efficiency of these marketing efforts. Additionally, as the channels through which we conduct our marketing and advertising activities continue to rapidly evolve, we must continue to establish relationships with these channels and may be unable to develop or maintain these relationships on acceptable economic and other terms. Furthermore, we currently receive a significant number of visits to our digital platform via search engine results. Search engines frequently change the algorithms that determine the ranking and display of results of a user’s search, which could reduce the number of visits to our digital platform, and, in turn, reduce new customer acquisition and adversely affect our results of operations. If we are unable to cost-effectively drive traffic to our digital platform, our ability to acquire new customers and our financial condition would suffer. Email marketing efforts are also important to our marketing efforts. If we are unable to successfully deliver emails to our customers or if customers do not engage with our emails, whether out of choice, because those emails are marked as low priority or spam, or for other reasons, our business could be adversely affected.

Our marketing initiatives may become increasingly expensive, and generating a meaningful return on those initiatives may be difficult or unpredictable. Even if we successfully increase net revenue as a result of our marketing efforts, it may not offset the additional marketing expenses we incur. If our marketing efforts are not successful in promoting awareness of our brands or products, driving customer engagement, or attracting new customers, or if we are not able to cost-effectively manage our marketing expenses, our results of operations could be adversely affected.

Failure to accurately forecast consumer demand could lead to excess inventories or inventory shortages, which could result in decreased operating margins, reduced cash flows, and harm to our business.

To meet anticipated demand for our products, we must forecast inventory needs and arrange manufacturing activities based on our estimates of future demand for particular products. Our ability to accurately forecast demand for our products could be affected by many factors, including an increase or decrease in customer demand for our products or for products of our competitors, changing consumer preferences, changing product trends, our failure to accurately forecast consumer acceptance of new products, product introductions by competitors, unanticipated changes in general market conditions, store closures (including, for example, due to the COVID-19 pandemic), and weakening of economic conditions or consumer confidence in future economic conditions. If we fail to accurately forecast consumer demand, we may experience excess inventory levels or a shortage of products available for sale in our stores or for delivery to customers.

Inventory levels in excess of customer demand may result in inventory write-offs, donations by us of our unsold products, inventory write-downs, and/or the sale of excess inventory at discounted prices, any of which could cause our gross margin to suffer, impair the strength and exclusivity of our brands, and have an adverse effect on our results of operations, financial condition, and cash flows.

18

Table of Contents

Conversely, if we underestimate customer demand for our products and fail to arrange sufficient manufacturing capacities in advance, then we may not be able to deliver products to meet our requirements and we may experience inventory shortages. Inventory shortages in our stores or third-party distribution centers could result in delayed shipments to customers, lost sales, a negative customer experience, lower brand loyalty, and damage to our reputation and customer relationships, any of which could have an adverse effect on our results of operations, financial condition, and cash flows.

Counterfeit or “knock-off” products, as well as products that are “inspired by” our brands may siphon off demand for our brands’ products and may result in customer confusion, harm to our brands, a loss of our market share and/or a decrease in our results of operations.

We face competition from counterfeit or “knock-off” products manufactured and sold by third parties in violation of our intellectual property rights, as well as from products that are inspired by our brands’ products, including private label offerings by e-commerce retailers. In the past, third parties have targeted users on Facebook or other social media platforms intending to target individuals interested in our products and sell such individuals products that look like our brands’ products, often at steep discounts.

These activities of third parties may result in customer confusion, require us to incur additional administrative costs to manage customer complaints related to counterfeit goods, divert customers from us, cause us to miss out on sales opportunities, and result in a loss of our market share. We could also be required to increase our marketing and advertising spend. If consumers are confused by these other products and believe them to be actual products from our brands, we could be forced to deal with dissatisfied customers who mistakenly blame us for poor service or poor-quality goods.

In addressing these or similar issues in the future, we may also be required to incur substantial expense to protect our brands and enforce our intellectual property rights, including through legal action in the United States and the EU or other countries in which we and our brands operate, which could negatively impact our results of operations and financial condition.

These and similar issues related to these or similar counterfeit products or products “inspired by” our brands could recur and could again result in customer confusion, harm to our brand, a loss of our market share and/or a decrease in our results of operations.

We are dependent on suppliers for our products and raw materials, which poses risks to our business operations.

Although no single supplier is or is expected to become critical to our production needs, any of the following could materially and adversely affect our ability to produce or deliver our products and, as a result, have a material adverse effect on our business, financial condition and results of operations:

| • | political or labor instability or military conflict involving any of the countries in which we, or our suppliers operate, which could cause a delay in the transportation of our products and raw materials to us and an increase in transportation costs; |

| • | heightened terrorism security concerns, which could subject imported or exported goods to additional, more frequent or more thorough inspections, leading to delays in deliveries or impoundments of goods for extended periods or could result in decreased scrutiny by customs officials for counterfeit goods, leading to lost sales, increased costs for our anti-counterfeiting measures and damage to the reputation of our brands; |

| • | a significant decrease in availability or increase in cost of raw materials, including commodities (particularly cotton, wool and cashmere), or the ability to use raw materials produced in a country that is a major provider due to political, human rights, labor, environmental, animal cruelty or other concerns; |

19

Table of Contents

| • | a significant decrease in factory and shipping capacity or increase in demand for such capacity; |

| • | a significant increase in wage and shipping costs; |

| • | natural disasters, which could result in closed factories and scarcity of raw materials; |

| • | disease epidemics and health related concerns, such as the COVID-19 pandemic, which could result in (and in the case of the COVID-19 pandemic, has resulted in certain of the following) closed factories, reduced workforces, scarcity of raw materials and scrutiny or embargoing of goods produced in infected areas; |

| • | the migration and development of manufacturers, which could affect where our products are or are planned to be produced; |

| • | the adoption of regulations, quotas and safeguards relating to imports and our ability to adjust timely to changes in trade regulations, which, among other things, could limit our ability to produce products in cost-effective countries that have the labor and expertise needed; and |

| • | the implementation of new or increased duties, taxes and other charges on imports. |

We face intense competition in the personal luxury goods industry.

Competition is intense in the luxury consumer goods industry. We compete with numerous luxury fashion designers (whether domestically or globally), brand owners, manufacturers and retailers of apparel, accessories and footwear, some of which have greater resources than we do. In addition, in certain instances, we compete directly with our wholesale customers, as they also sell their own private label products in their stores and online. We compete within the personal luxury goods industry primarily on the basis of:

| • | anticipating and responding to changing consumer tastes, demands and shopping preferences in a timely manner and developing distinctive, attractive, quality products; |

| • | maintaining favorable brand recognition and relevance, including through digital brand engagement and online and social media presence; |

| • | appropriately pricing products and creating an attractive value proposition for customers; |

| • | providing strong and effective marketing support; |

| • | ensuring product availability and optimizing supply chain efficiencies with third party suppliers and retailers; and |

| • | obtaining sufficient retail floor space at retail and effective presentation of our products at retail, on e-commerce sites operated by our department store customers and pure play e-commerce retailers, and on our e-commerce sites. |

Our customer relationships and sales have been and may be negatively impacted if we do not anticipate and respond to consumer preferences and fashion trends or manage inventory levels appropriately.