UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report ____

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

+65 8877 3871

(Address of principal executive offices)

Chief Executive Officer

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| * | Effective from July 13, 2023, the ratio of ADSs representing the Class A ordinary shares changed from one (1) ADS representing one (1) Class A ordinary shares to one (1) ADS representing fifty (50) Class A ordinary shares. |

| ** | Not for trading, but only in connection with the listing on The Nasdaq Capital Market of our American depositary shares, each representing one Class A ordinary share. |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2023,

there were 203,093,850 ordinary shares outstanding, being the sum of

Indicate by check mark if

the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

If this annual report is

an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934. ☐ Yes ☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether

the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days. ☒

Indicate by check mark whether

the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit

such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “accelerated filer and large accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer ☐ | Accelerated filer ☐ | Emerging growth company |

If an emerging growth company

that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use

the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section

13(a) of the Exchange Act.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether

the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control

over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm

that prepared or issued its audit report.

If securities are registered

pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing

reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has been to prepare the financial statements included in this filing:

| International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report,

indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☒ Yes ☐ No

TABLE OF CONTENTS

i

INTRODUCTION

Unless otherwise indicated and except where the context otherwise requires, references in this annual report to:

“$,” “USD,” “US$” and “U.S. dollar” each refers to the United States dollar.

“2019 Warrant” means a warrant to purchase shares of common stock of Proficient issued in Proficient’s Initial Public Offering and simultaneous private placements. Each Warrant entitles the holder thereof to purchase one share of common stock of Proficient at a price of $11.50 per share.

“2020 Debentures” means the senior secured convertible debentures, convertible into 800,000 ADSs, which will mature in 30 months from the dates of issuance pursuant to the 9% Senior Secured Convertible Debenture dated December 14, 2020.

“2020 Warrants” means, together, the Series A Warrant, the Series B Warrant and the Series C Warrant.

“2020 December Private Placement” means the 2020 Debentures and the 2020 Warrants owned by ATW Opportunities Master Fund, L.P. and issued by the Company pursuant to Securities Purchase Agreement dated December 11, 2020.

“2021 February Warrants” means, together, the Series D Warrant, Series E Warrant and the Series F Warrant.

“2021 February Private Placement” means the Series A Convertible Preferred Shares and the 2021 Warrants owned by ATW Opportunities Master Fund, L.P. and issued by the Company pursuant to Securities Purchase Agreement dated February 15, 2021.

“2022 August Debentures” means the senior secured convertible debentures, convertible into ADSs, which will mature on August 9, 2025 pursuant to a Senior Secured Convertible Debenture dated August 10, 2022.

“2022 December Debentures” means the senior secured convertible debentures, convertible into ADSs, which will mature on December 7, 2025 pursuant to a Senior Secured Convertible Debenture dated December 7, 2022.

“A-Share” refers to the stocks that are denominated in Renminbi and traded in Shanghai and Shenzhen Stock Exchange in PRC. Hong Kong stock means the stocks that are traded in Hong Kong Exchange.

“ADSs” refers to our American depositary shares, each of which represents one Class A Ordinary Share.

“Amended and Restated Memorandum and Articles of Association” means the currently effective amended and restated memorandum and articles of association of Lion Group Holding Ltd.

“Business Combination Agreement” means the Business Combination Agreement, dated as of March 10, 2020, which is later amended and restated as of May 12, 2020, by and among us, Proficient, Merger Sub, Lion, the Sellers and the other parties thereto.

“Business Combination” means the Merger and the Share Exchange, and other transactions contemplated by the Business Combination Agreement.

“CFD” means a contract for differences, an agreement between an investor and a CFD broker to exchange the difference in the value of a financial product between the time the contract opens and closes.

“Class A Ordinary Shares” means our Class A ordinary shares, par value $0.0001 per share.

“Class B Ordinary Shares” means our Class B ordinary shares, par value $0.0001 per share.

“Code” means the Internal Revenue Code of 1986, as amended.

“Companies Act” means the Companies Act (2020 Revision) of the Cayman Islands, as may be amended from time to time.

“Escrow Shares” means 45% of the Exchange Shares otherwise issuable to the Sellers at the Closing set aside in escrow upon the closing of the Business Combination.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Exchange Shares” means the ordinary shares that Sellers received in exchange of their original holdings in Lion Financial Group Limited upon the consummation of the Business Combination.

ii

“Founder Shares” means shares of Proficient common stock, 2,875,000 of which are currently outstanding and were issued to the Initial Stockholders prior to the Initial Public Offering of Proficient.

“HK$” or “Hong Kong dollars” means the legal currency of Hong Kong.

“Initial Public Offering” means the initial public offering of Proficient, consummated on June 3, 2019.

“Initial Stockholders” means the holders of Founder Shares.

“iResearch” means iResearch Consulting Group.

“JOBS Act” means the Jumpstart Our Business Startups Act.

“Lion” means Lion Financial Group Limited, a corporation organized under the laws of the British Virgin Islands.

“Merger” means the merger of Merger Sub with Proficient, with Proficient surviving such merger, prior security holders of Proficient receiving our securities and Proficient becoming a wholly-owned subsidiary of us.

“Merger Sub” means Lion MergerCo I, Inc., a Cayman Islands exempted company.

“Nasdaq” means the Nasdaq Stock Market LLC.

“Ordinary Shares” means our ordinary shares, par value $0.0001 per share, including Class A Ordinary Shares and Class B Ordinary Shares, unless otherwise specified.

“PIPE Warrants” means the warrant represents the right to purchase one Class A Ordinary Share in the form of ADSs at a price of $3.00 per share or $3.00 per ADS.

“Private Warrants” or “Private Placement Warrants” means the Warrants sold to Sponsor simultaneously with the closing of the Initial Public Offering, each of which is exercisable for one share of common stock of Proficient, in accordance with its terms.

“Proficient”, “PAAC” or “Purchaser” means Proficient Alpha Acquisition Corp., currently known as Lion Group North America Corp., a Nevada corporation.

“PRC” or “China” refers to the People’s Republic of China, excluding, for the purpose of this annual report, Taiwan.

“Public Warrants” means the Warrants included in the Units sold in the Initial Public Offering, each of which is exercisable for one share of common stock of Proficient, in accordance with its terms.

“Purple Tee” means Purple Tee Capital Limited, an independent third party industry consultant.

“Rights” means the rights included in the Units sold in the Initial Public Offering, each of which is exercisable for one-tenth (1/10) of one share of common stock of Proficient, in accordance with its terms.

“RMB” and “Renminbi” each refers to the legal currency of China.

“SEC” means the U.S. Securities and Exchange Commission.

“Sellers” means the shareholders of Lion named as seller parties to the Business Combination Agreement dated March 10, 2020.

“Series A Convertible Preferred Shares” means our 8% Series A Convertible Preferred Shares, par value $0.0001 per share, and stated value $1,000.00 per share.

“Series A Warrant” means a warrant until on or prior to 5:00 p.m. (New York City time) on December 14, 2027 exercisable into 1,200,000 ADSs at an exercise price of $2.45 per ADS pursuant to the Series A American Depositary Shares Purchase Warrant dated December 14, 2020.

iii

“Series B Warrant” means a 2-year warrant exercisable into 5,000,000 ADSs at an exercise price of $2.00 per ADS pursuant to the Series B American Depositary Shares Purchase Warrant dated December 14, 2020.

“Series C Warrant” means a 7-year warrant exercisable into 7,500,000 ADSs at an exercise price of $2.45 per ADS pursuant to the Series C American Depositary Shares Purchase Warrant dated December 14, 2020.

“Series D Warrant” means a warrant until on or prior to 5:00 p.m. (New York City time) on the five year anniversary of the closing date of the February Private Placement exercisable into 2,333,333 ADSs at an exercise price of $3.00 per ADS pursuant to the Series D American Depositary Shares Purchase Warrant dated February 18, 2021.

“Series E Warrant” means a one-year warrant exercisable into 13,333,333 ADSs at an exercise price of $3.00 per ADS which entitles the Series E warrant holder pursuant to the Series E American Depositary Shares Purchase Warrant dated February 18, 2021, each exercise of which entitles the Series E Warrant holder to receive one ADS and a 8% cash discount.

“Series F Warrant” means a five-year warrant exercisable into 13,333,333 ADSs at an exercise price of $3.00 per ADS pursuant to the Series F American Depositary Shares Purchase Warrant dated February 18, 2021, but the exercisability of which shall vest ratably from time to time in proportion to the exercise of the Series E Warrants by the holder of the Series E Warrant.

Series G Warrant” means a five-year warrant exercisable into 2,285,715 ADSs at an exercise price of $2.50 per ADS pursuant to the Series G American Depositary Shares Purchase Warrant dated December 13, 2021, but the exercisability of which shall vest ratably from time to time in proportion to the exercise of the Series G Warrants by the holder of the Series G Warrant.

“Share Exchange” means the exchange of 100% of the ordinary shares of Lion for our capital shares.

“Sponsor” means Complex Zenith Limited, a British Virgin Islands company controlled by Shih-Chung Chou, a director of Proficient. Shih-Chung Chou had served as the sponsor of Proficient since its Initial Public Offering until March 12, 2020, when he entered into an agreement with Complex Zenith Limited and assigned all of his equity interest in Proficient and his rights and obligations as a sponsor to Complex Zenith Limited.

“Strategic Cooperation Agreement” means the strategic cooperation agreement, dated as of January 6, 2021, by and among us and Yao Yongjie.

“Trust Account” means the trust account that holds a portion of the proceeds of the Initial Public Offering and the concurrent sale of the Private Placement Warrants.

“Units” means units issued in the Initial Public Offering, each consisting of one share of common stock of Proficient, one Warrant and one Right.

“U.S.” means the United States of America.

“U.S. GAAP” means United States generally accepted accounting principles.

“Warrant” means a warrant to purchase shares of common stock of Proficient issued in the Initial Public Offering and simultaneous private placements. Each Warrant entitles the holder thereof to purchase one share of common stock of Proficient at a price of $11.50 per share.

“we,” “our,” “us,” “the company,” “the Group” and other similar terms refer to Lion Group Holding Ltd. and its consolidated subsidiaries.

This annual report contains translations of Hong Kong dollars into U.S. dollars solely for the convenience of the reader. The conversion of Hong Kong dollars into U.S. dollars are based on the exchange rates set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. Unless otherwise noted, all translations from Hong Kong dollars to U.S. dollars and from U.S. dollars to Hong Kong dollars in this annual report were made at a rate of HK$7.81 to US $1.00, buying rate at closing in effect as of December 31, 2023.

iv

FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements that involve risks and uncertainties. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigations Reform Act of 1995.

You can identify these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “likely to” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to, statements about:

| ● | our goals and strategies; |

| ● | our ability to retain and increase the number of users, members and advertising customers, and expand our service offerings; |

| ● | our future business development, financial condition and results of operations; |

| ● | expected changes in our revenues, costs or expenditures; |

| ● | competition in our industry; |

| ● | relevant government policies and regulations relating to our industry; |

| ● | general economic and business conditions globally and in China, Hong Kong, and Southeast Asia; and |

| ● | assumptions underlying or related to any of the foregoing. |

You should read this annual report and the documents that we refer to in this annual report and have filed as exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect. Other sections of this annual report discuss factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements.

You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

v

PART I.

Lion Group Holding Ltd. is incorporated in Cayman Islands. As a holding company with no material operations of our own, we conduct our substantial operations through our subsidiaries in Hong Kong, Singapore, the Cayman Islands, and the United States, and our apps are available to download in the app stores of China and most of our users are PRC citizens. As such, the Chinese government may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time. Such governmental actions:

| ● | could result in a material change in our operations; |

| ● | could hinder our ability to continue to offer securities to investors; and |

| ● | may cause the value of our ADSs to significantly decline or be worthless. |

Currently, we are not aware there are any material restrictions on foreign exchange, the ability to transfer cash between our entities, or the ability to distribute earnings to investors outside of China. Further, we are aware that, the Chinese government recently initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using entity variable interest entity (“VIE”) structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on the Company’s business operations in China, the ability to accept foreign investments and list on an U.S. or other foreign exchange. We do not have any VIE agreements with our subsidiaries, instead, we hold equity interests in our subsidiaries. As of the date of this annual report, we do not have a subsidiary incorporated in mainland China. Any future action by the Chinese government expanding the categories of industries and companies whose foreign securities offerings are subject to government review could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless. For a detailed description of the risks related to doing business in the PRC and our securities, see “Risks Related to Doing Business in Jurisdictions We Operate” and “Risks Related to our ADSs and our Securities” in the Risk Factors section.

Risks Associated with Having Part of the Company’s Operations in China

Although the substantial operation of us is based in Hong Kong, Singapore, and the Cayman Islands, we launched our apps in the app stores of China and most of our users are PRC citizens, which may subject us to certain laws and regulations in China, and expose us to legal and operational risks associated with our operations in China. The PRC government has significant authority to exert influence on the ability of a company with operations in China, including us, to conduct its business. Changes in China’s economic, political or social conditions or government policies could materially and adversely affect our business and results of operations. We are subject to risks due to the uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to the risks of uncertainty about any future actions of the PRC government on U.S. listed companies. We may also be subject to sanctions imposed by PRC regulatory agencies, including the China Securities Regulatory Commission, or CSRC, if we fail to comply with their rules and regulations. Any actions by the PRC government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in companies having operations in China, including us, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors, and cause the value of our securities to significantly decline or become worthless. These China-related risks could result in a material change in our operations and/or the value of our securities, or could significantly limit or completely hinder our ability to offer securities to investors in the future and cause the value of such securities to significantly decline or become worthless.

The PRC government may exert, at any time, substantial intervention and influence over the manner our operations. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, adopting new measures to extend the scope of cybersecurity reviews and new laws and regulations related to data security, and expanding the efforts in anti-monopoly enforcement.

1

The regulatory framework for the collection, use, safeguarding, sharing, transfer and other processing of personal information and important data worldwide is rapidly evolving in PRC and is likely to remain uncertain for the foreseeable future. Regulatory authorities in China have implemented and are considering a number of legislative and regulatory proposals concerning data protection. For example, the PRC Cybersecurity Law, which became effective in June 2017, established China’s first national-level data protection for “network operators,” which may include all organizations in China that connect to or provide services over the internet or other information network. The PRC Data Security Law, which was promulgated by the Standing Committee of PRC National People’s Congress, or the SCNPC, on June 10, 2021 and became effective on September 1, 2021, outlines the main system framework of data security protection.

In December 2021, the Cyberspace Administration of China (the “CAC”) promulgated the amended Measures of Cybersecurity Review which require cyberspace operators with personal information of more than one million users to file for cybersecurity review with the Cybersecurity Review Office (“CRO”), in the event such operators plan for an overseas listing. The amended Measures of Cybersecurity Review provide that, among others, an application for cybersecurity review must be made by an issuer that is a “critical information infrastructure operator” or a “data processing operator” as defined therein before such issuer’s securities become listed in a foreign country, if the issuer possesses personal information of more than one million users, and that the relevant governmental authorities in the PRC may initiate cybersecurity review if such governmental authorities determine an operator’s cyber products or services, data processing or potential listing in a foreign country affect or may affect China’s national security. The amended Measures of Cybersecurity Review took effect on February 15, 2022. In August 2021, the Standing Committee of the National People’s Congress of China promulgated the Personal Information Protection Law which became effective on November 1, 2021. The Personal Information Protection Law provides a comprehensive set of data privacy and protection requirements that apply to the processing of personal information and expands data protection compliance obligations to cover the processing of personal information of persons by organizations and individuals in China, and the processing of personal information of persons outside of China if such processing is for purposes of providing products and services to, or analyzing and evaluating the behavior of, persons in China. The Personal Information Protection Law also provides that critical information infrastructure operators and personal information processing entities who process personal information meeting a volume threshold to be set by Chinese cyberspace regulators are also required to store in China the personal information generated or collected in China, and to pass a security assessment administered by Chinese cyberspace regulators for any export of such personal information. Moreover, pursuant to the Personal Information Protection Law, persons who seriously violate this law may be fined for up to RMB50 million or 5% of annual revenues generated in the prior year and may also be ordered to suspend any related activity by competent authorities.

In November 2021, the CAC released the Regulations on Network Data Security (draft for public comments) and accepted public comments until December 13, 2021. The draft Regulations on Network Data Security provide more detailed guidance on how to implement the general legal requirements under laws such as the Cybersecurity Law, Data Security Law and the Personal Information Protection Law. The draft Regulations on Network Data Security follow the principle that the state will regulate based on a data classification and multi-level protection scheme, under which data is largely classified into three categories: general data, important data and core data. Under the current PRC cybersecurity laws in China, critical information infrastructure operators that intend to purchase internet products and services that may affect national security must be subject to the cybersecurity review. On July 30, 2021, the State Council of the PRC promulgated the Regulations on the Protection of the Security of Critical Information Infrastructure, which took effect on September 1, 2021. The regulations require, among others, that certain competent authorities shall identify critical information infrastructures. If any critical information infrastructure is identified, they shall promptly notify the relevant operators and the Ministry of Public Security.

Currently, the cybersecurity laws and regulations have not directly affected our business and operations, but in anticipation of the strengthened implementation of cybersecurity laws and regulations and the expansion of our business, we face potential risks if we are deemed as a critical information infrastructure operator under the Cybersecurity Law. In such case, we must fulfill certain obligations as required under the Cybersecurity Law and other applicable laws, including, among others, storing personal information and important data collected and produced within the PRC territory during our operations in China, which we are already doing in our business, and we may be subject to review when purchasing internet products and services. As of the date of this annual report, we have not been involved in any investigations on cybersecurity review made by the CAC on such basis, and we have not received any inquiry, notice, warning, or sanctions in such respect. Based on the foregoing, we do not expect that, as of the date of this annual report, the current applicable PRC laws on cybersecurity would have a material adverse impact on our business.

2

On September 1, 2021, the PRC Data Security Law became effective, which imposes data security and privacy obligations on entities and individuals conducting data-related activities, and introduces a data classification and hierarchical protection system based on the importance of data in economic and social development, as well as the degree of harm it will cause to national security, public interests, or legitimate rights and interests of individuals or organizations when such data is tampered with, destroyed, leaked, or illegally acquired or used. As of the date of this annual report, we have not been involved in any investigations on data security compliance made in connection with the PRC Data Security Law, and we have not received any inquiry, notice, warning, or sanctions in such respect. Based on the foregoing, we do not expect that, as of the date of this annual report, the PRC Data Security Law would have a material adverse impact on our business.

On July 6, 2021, the relevant PRC governmental authorities published the Opinions on Strictly Cracking Down Illegal Securities Activities in Accordance with the Law. These opinions require the relevant regulators to coordinate and accelerate amendments of legislation on the confidentiality and archive management related to overseas issuance and listing of securities, and to improve the legislation on data security, cross-border data flow and management of confidential information. These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies and proposed to take effective measures, such as promoting the construction of relevant regulatory systems to deal with the risks and incidents faced by China-based overseas-listed companies. As these opinions were recently issued, official guidance and related implementation rules have not been issued yet and the interpretation of these opinions remains unclear at this stage. As of the date of this annual report, we have not received any inquiry, notice, warning, or sanctions from the CSRC or any other PRC government authorities. Based on the foregoing and the currently effective PRC laws, we are of the view that, as of the date of this annual report, these opinions do not have a material adverse impact on our business.

On February 17, 2023, the CSRC released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Overseas Listing Trial Measures, which have come into effect on March 31, 2023. As a supplement to the Overseas Listing Trial Measures, on February 24, 2023, the CSRC, together with other authorities, jointly revised the Provisions on Strengthening Confidentiality and Archives Administration for Overseas Securities Offering and Listing, collectively with the Overseas Listing Trial Measures, the Overseas Listing Regulations, which have come into effect on March 31, 2023. The Overseas Listing Regulations set out new filing requirements, report obligations and guidance for confidentiality and achieves administration with the CSRC for PRC domestic companies seeking direct or indirect listings and offerings in overseas markets. An overseas listing will constitute an “indirect listing” where the issuer meets both of the following conditions: (i) 50% or more of the issuer’s operating revenue, total profit, total assets or net assets for the most recent accounting year is accounted for by its PRC subsidiaries; and (ii) main parts of the business activities are conducted within mainland China, or main place of business are located in mainland China, or a majority of the senior managers in charge of business operation and management are Chinese citizens or domiciled in mainland China. Based on our management’s assessment, we do not believe we will be subject to the filing and reporting requirement under the Overseas Listing Regulations since our business activities and management team do not meet either of the conditions. However, as the Overseas Listing Regulations were recently released and their interpretation and implementation remain uncertain.

As there are still uncertainties regarding these new laws and regulations as well as the amendment, interpretation and implementation of the existing laws and regulations related to cybersecurity and data protection, We cannot assure you that we will be able to comply with these laws and regulations in all respects. The regulatory authorities may deem our activities or services non-compliant and therefore require us to suspend or terminate its business. We may also be subject to fines, legal or administrative sanctions and other adverse consequences, and may not be able to become in compliance with relevant laws and regulations in a timely manner, or at all. These may materially and adversely affect its business, financial condition, results of operations and reputation.

3

Since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, our ability to accept foreign investments and conduct follow-on offerings, and listing or continuing listing on a U.S. or other foreign exchanges. In addition, the PRC government has recently published new policies that significantly affected certain industries such as the education and internet industries, and we cannot rule out the possibility that it will in the future release regulations or policies regarding any other industry including the industry in which we operate, which could adversely affect our business, financial condition and results of operations. See “Item 3. Key Information—D. Risk Factors—Risk Factors— Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in laws and regulations in China could adversely affect us.” for more details.

Risks Associated with the Holding Foreign Companies Accountable Act.

The Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted into U.S. law on December 18, 2020. The HFCA Act states that if the SEC determines that a company has filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the Public Company Accounting Oversight Board of the United States (the “PCAOB”) for three consecutive years beginning in 2021, the SEC shall prohibit its securities from being traded on a national securities exchange or in the over-the-counter trading market in the U.S. On December 16, 2021, the PCAOB issued a Determination Report which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (i) mainland China, and (ii) Hong Kong.

On December 2, 2021, the SEC adopted final amendments implementing congressionally mandated submission and disclosure requirements of the HFCA Act. On December 23, 2022 the AHFCA Act was enacted, which amended the HFCA Act by requiring the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. On December 29, 2022, a legislation entitled the Consolidated Appropriations Act, was signed into law by President Biden. The Consolidated Appropriations Act contained, among other things, an identical provision to AHFCA Act, which reduces the number of consecutive non-inspection years required for triggering the prohibitions under the Holding Foreign Companies Accountable Act from three years to two. Whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control. The PCAOB is continuing to demand complete access in mainland China and Hong Kong moving forward and is already making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has indicated that it will act immediately to consider the need to issue new determinations with the HFCA Act if needed, without having to wait another year to reassess its determinations. In the future, if there is any regulatory change or step taken by PRC regulators that does not permit our auditor to provide audit documentations located in China or Hong Kong to the PCAOB for inspection or investigation, or the PCAOB expands the scope of the determination so that we are subject to the HFCA Act, as the same may be amended, you may be deprived of the benefits of such inspection which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities, including trading on the national exchange and trading on “over-the-counter” markets, may be prohibited under the HFCA Act.

Lack of access to PCAOB inspections prevents the PCAOB from fully evaluating audits and quality control procedures of the accounting firms headquartered in mainland China or Hong Kong. As a result, investors in companies using such auditors may be deprived of the benefits of such PCAOB inspections. On August 26, 2022, the CSRC, the Ministry of Finance of the PRC, and PCAOB signed a Statement of Protocol, or the Protocol, governing inspections and investigations of audit firms based in China and Hong Kong. Pursuant to the Protocol, the PCAOB has independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong in 2022, and the PCAOB board vacated its previous determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control. The PCAOB is continuing to demand complete access in mainland China and Hong Kong moving forward and is already making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed.

4

Neither UHY LLP nor HTL International, LLC is included in the list of determinations announced by the PCAOB on December 21, 2021 in their HFCA Act Determination Report under PCAOB Rule 6100. If notwithstanding this new framework, the PCAOB was unable to fully inspect UHY LLP or HTL International, LLC (or any other auditor of the Company) in the future, or if PRC or American authorities further regulate auditing work of Chinese or Hong Kong companies listed on the U.S. stock exchanges in a manner that would restrict UHY LLP or HTL International, LLC (or any future auditor of the Company) from performing work in Hong Kong, the Company may be required to change its auditor. Furthermore, there can be no assurance that the SEC, Nasdaq, or other regulatory authorities would not apply additional and more stringent criteria to the Company in connection with audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency of resources, geographic reach or experience as it relates to the audit of the Company’s financial statements. The failure to comply with the requirement in the HFCA Act, as amended by the AHFCA Act, that the PCAOB be permitted to inspect the issuer’s public accounting firm within two years, would subject us to consequences including the delisting of our securities in the future if the PCAOB is unable to inspect the Company’s accounting firm (whether UHY LLP, HTL International, LLC, or another firm) at such future time.

The HFCA Act also imposes additional certification and disclosure requirements for Commission Identified Issuers, and these requirements apply to issuers in the year following their listing as Commission Identified Issuers. The additional requirements include a certification that the issuer is not owned or controlled by a governmental entity in the Relevant Jurisdiction, and the additional requirements for annual reports include disclosure that the issuer’s financials were audited by a firm not subject to PCAOB inspection, disclosure on governmental entities in the Relevant Jurisdiction’s ownership in and controlling financial interest in the issuer, the names of Chinese Communist Party, or CCP, members on the board of the issuer or its operating entities, and whether the issuer’s article’s include a charter of the CCP, including the text of such charter. For more detailed information, see “Our ADSs and warrants may be delisted or prohibited from being traded “over-the-counter” under the Holding Foreign Companies Accountable Act (as amended by the Accelerating Holding Foreign Companies Accountable Act) if the PCAOB were unable to fully inspect the company’s auditor.”

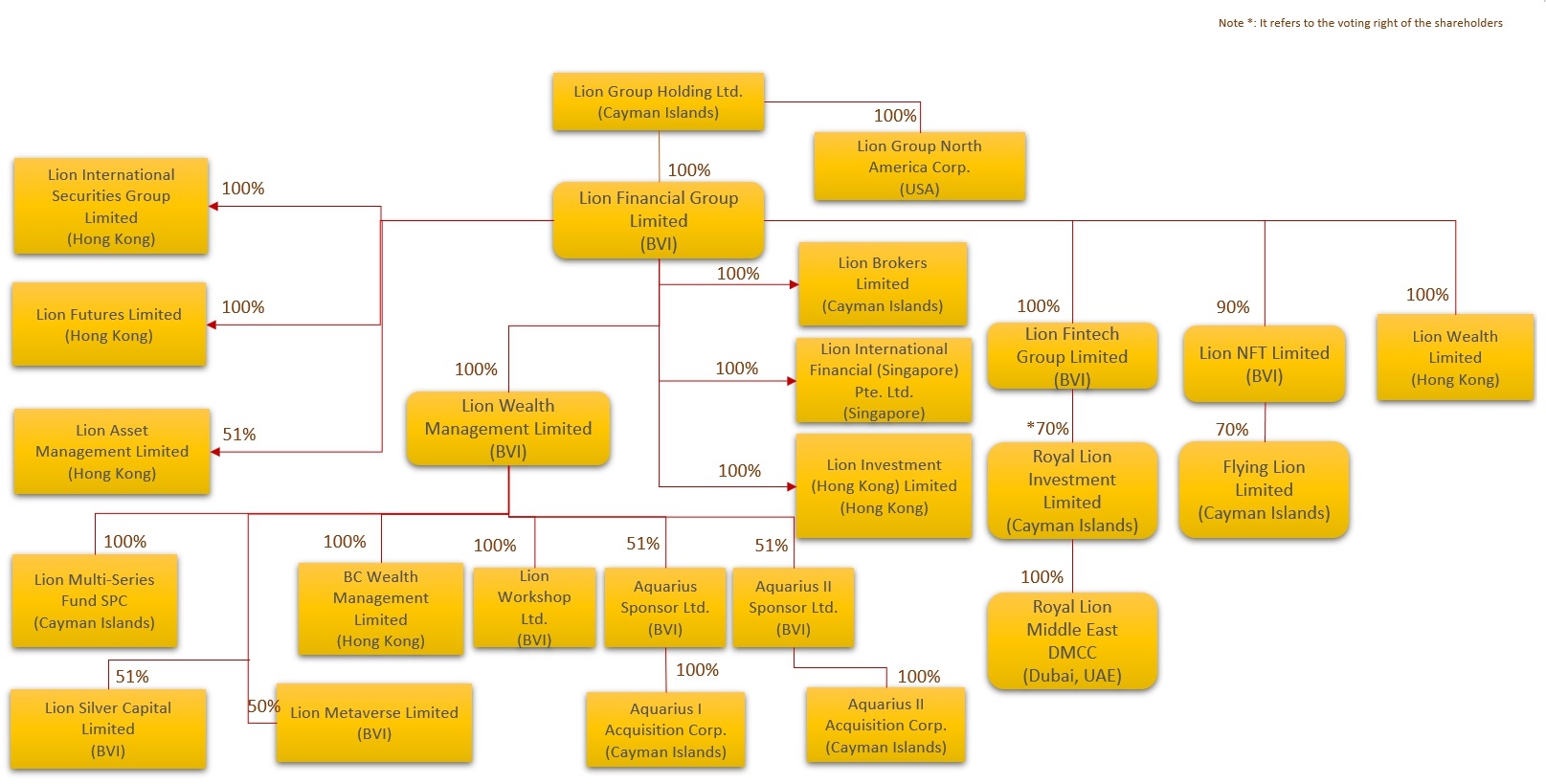

How Cash is Transferred through Our Organization

We were incorporated in Cayman Islands on February 11, 2020, to be the ultimate parent company of the Group upon the consummation of a business combination on June 16, 2020. As a holding company with no material operations of our own, we conduct our substantial operations through our subsidiaries in Hong Kong and the Cayman Islands and our apps are available to download in the app stores of China and most of our users are PRC citizens, which may subject us to certain laws and regulations in China. Lion Group Holding Ltd is permitted under the laws of Cayman Islands to provide funding to our subsidiaries in Hong Kong and Cayman Islands through loans or capital contributions without restrictions on the amount of the funds. Lion Group Holding Ltd. can distribute earnings from its businesses, including subsidiaries, to the U.S. investors. Our operations in Hong Kong and the Cayman Islands were in loss position since the second half of 2020, and the Company has raised capital through equity and debt financing transactions and provided funding to our operations in Hong Kong and the Cayman Islands.

Our operating subsidiaries are permitted under the laws of Hong Kong, Cayman Islands, Singapore, British Virgin Islands, and the United States, respectively, to provide funding to Lion Group Holding Ltd, the holding company incorporated in the Cayman Islands through dividend distributions. Our Group currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. We currently do not have any dividend policy, any future determination will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deems relevant, and subject to the restrictions contained in any future financing instruments.

Currently, we conduct our substantial operations through our subsidiaries in Hong Kong and the Cayman Islands. We have established Lion Group (Hangzhou) Investment Limited, our PRC subsidiary, holding through Lion Wealth Limited in May 2021. The PRC subsidiary was established solely for purpose of passive equity investment in China with no substantial business activities, which does not require contractual arrangements or variable interest entity, or VIE, to operate. Since Hong Kong is a special administrative region of the PRC and the basic policies of the PRC regarding Hong Kong are reflected in the Basic Law, providing Hong Kong with a high degree of autonomy and executive, legislative and independent judicial powers, including that of final adjudication under the principle of “one country, two systems”. We are dependent on our customers in the PRC, the laws and regulations of the PRC currently have restrictions on currency conversion, cross-border remittance and offshore investment for PRC citizens. See “Item 3. Key Information — D. Risk Factors — Risks Related to Our Business and Industry — PRC governmental control of currency conversion, cross-border remittance and offshore investment could have a direct impact on the trading volume on our platform, and the PRC government could further tighten restrictions on converting Renminbi to foreign currencies and/or deems our practices to be in violation of PRC laws and regulations.” for more information on the risk of PRC governmental control of currency conversion, cross-border remittance and offshore investment with respect to our operations. However, the laws and regulations of the PRC do not currently have any material impact on transfer of cash from the Company to our Cayman Islands and Hong Kong subsidiaries to or from Cayman Islands and Hong Kong subsidiaries to the Company and the investors in the U.S. As a result, cash can be transferred freely between the Company and its operating subsidiaries, across borders, and to U.S. investors.

5

Subject to the Companies Act and our Amended and Restated Memorandum and Articles of Association, our board of directors may authorize and declare a dividend to shareholders from time to time out of the profits from the Company, realized or unrealized, or out of the share premium account, provided that the Company will remain solvent, meaning the Company is able to pay its debts as they come due in the ordinary course of business. There is no further Cayman Islands statutory restriction on the amount of funds which may be distributed by us in the form of dividends.

The following are the aggregate transfers from the Company to its subsidiaries for the years ended December 31, 2022 and 2023:

| Year ended December 31, | ||||||||

| 2023 | 2022 | |||||||

| US$ | US$ | |||||||

| Subsidiary | ||||||||

| Lion Broker Limited (1) | $ | 3,340,771 | $ | 12,173,814 | ||||

| Lion Futures Limited (2) | - | - | ||||||

| Lion International Securities Group Limited (3) | - | - | ||||||

| Lion Wealth Limited (4) | 6,626,137 | 2,908,002 | ||||||

| BC Wealth Management Limited (5) | - | - | ||||||

| Lion International Financial (Singapore) Pte. Ltd. (6) | - | - | ||||||

| Lion Financial Group Limited (7) | 1,313,535 | 2,024,304 | ||||||

| Lion Wealth Management Limited | - | 1,422,951 | ||||||

| Lion Group North American Corp. (8) | 832,680 | 880,000 | ||||||

| Total | $ | 12,113,123 | $ | 19,409,071 | ||||

| (1) | Lion Broker Ltd was incorporated in under the laws of the Cayman Islands in March 2017. |

| (2) | Lion Futures Limited was incorporated in Hong Kong in May 2016. |

| (3) | Lion International Securities Group Limited was incorporated in under the laws of the Hong Kong in May 2016. |

| (4) | Lion Wealth Limited was incorporated in Hong Kong in October 2018. |

| (5) | BC Wealth Management Limited was incorporated in Hong Kong in October 2014 and became a wholly owned subsidiary of the Group in May 2016. |

| (6) | Lion International Financial (Singapore) Pte. Ltd. was incorporated in Singapore in July 2019. |

| (7) | Lion Financial Group Limited was incorporated in the British Virgin Islands in June 2015. |

| (8) | Lion Group North American Corp was incorporated under the laws of the State of Nevada in July 2018. |

The following are the aggregate transfers from its subsidiaries to the Company for the years ended December 31, 2022 and 2023:

| Year ended December 31, | ||||||||

| 2023 | 2022 | |||||||

| US$ | US$ | |||||||

| Subsidiary | ||||||||

| Lion Broker Limited (1) | $ | 12,365,221 | $ | 18,203,025 | ||||

| Lion Futures Limited (2) | - | - | ||||||

| Lion International Securities Group Limited (3) | - | - | ||||||

| Lion Wealth Limited (4) | 1,971,385 | 6,500,000 | ||||||

| BC Wealth Management Limited (5) | - | - | ||||||

| Total | $ | 14,336,606 | $ | 24,703,025 | ||||

| (1) | Lion Broker Ltd was incorporated in under the laws of the Cayman Islands in March 2017. |

| (2) | Lion Futures Limited was incorporated in Hong Kong in May 2016. |

| (3) | Lion International Securities Group Limited was incorporated in under the laws of the Hong Kong in May 2016. |

| (4) | Lion Wealth Limited was incorporated in Hong Kong in October 2018. |

| (5) | BC Wealth Management Limited was incorporated in Hong Kong in October 2014 and became a wholly owned subsidiary of the Group in May 2016. |

6

We did not pay any dividends to our shareholders in 2023 and 2022. We are able to distribute earnings from our operating subsidiaries, to the parent company and U.S. investors and settle amounts owed, although we currently do not have any dividend policy. There were no dividends or distributions that a subsidiary made to the holding company during the period. If we determine to pay dividends on any of our ADSs in the future, as a holding company, we will be dependent on receipt of funds from our operating subsidiaries in Hong Kong and Cayman Islands. Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us, and under the current laws of the Cayman Islands, we are also not subject to tax on income or capital gains and withholding tax is not imposed upon payments of dividends from the Company to its shareholders.

There are no restrictions or limitations under the laws of Hong Kong imposed on the conversion of HK dollar into foreign currencies and the remittance of currencies out of Hong Kong, nor are there any restriction on any foreign exchange to transfer cash between the Company and its subsidiaries, across borders and to investors outside of PRC, nor is there any restrictions and limitations to distribute earnings from the subsidiaries, to the Company and investors outside of PRC and amounts owed. There are no exchange controls in Cayman Islands.

For more detailed information, see “Liquidity of our Subsidiaries” and “Item 3. Key Information — D. Risk Factors — Risk Related to Our Corporate Structure — We may rely on dividends and other distributions on equity paid by our subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business.”

Limitation on Oversea Listing and Share Issuances

Although the substantial operation of us is based in Singapore, Hong Kong and the Cayman Islands and all of the data and personal information we collected are stored in servers outside mainland China, we launched our apps in the app stores of China and most of our users are PRC citizens, which may subject us to certain laws and regulations in China. Recent cybersecurity regulations mandate clearance of cybersecurity review of internet platform operator holding personal information of more than one million users before applying for listing at a foreign stock exchange, and relevant governmental authorities in the PRC may initiate cybersecurity review if they determine an operator’s data processing activities affect or may affect national security. However, it remains unclear as to whether relevant requirements will be applicable to companies that have already been listed in the United States, such as us, for our future offerings, and the laws and regulations then effective as of our previous listing did not require any issuer to obtain pre-approval from the Cybersecurity Administration Committee, or CAC, before listing at a foreign stock exchange. As of the date of this annual report, we do not hold personal information of more than one million users and our business activities do not involve risk factors regarding national security as stipulated in the Cybersecurity Review Measures. We have not been informed by any government authorities that we are deemed as a critical information infrastructure operator, and we have not received any inquiry or notice of and is not currently subject to any proceedings initiated by the CAC. Based on the foregoing and our management’s assessment, we believe that we are not required to apply for pre-approval from CAC before the issuance of our securities to foreign investors and we are not subject to mandatory application requirement for cybersecurity review under the current PRC laws and regulations. However, no detailed rules or implementation rules regarding the cybersecurity review have been issued and the PRC government authorities may have wide discretion in the interpretation and enforcement of the applicable laws. We cannot assure you that we would not be deemed as a critical information infrastructure operator or carrying out data processing activities that affect or may affect national security, which may subject us to order of clearance of cybersecurity review or other specific actions.

7

In addition, the Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies requires an overseas special purpose vehicle formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals to obtain the approval of the CSRC, prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. Based on our management’s assessment, we believe that the CSRC’s approval is not required for our listing, trading of our securities on Nasdaq, given that our disposed-PRC subsidiary was incorporated as wholly foreign-owned enterprises by means of direct investment rather than by merger or acquisition of equity interest or assets of a PRC domestic company owned by PRC companies or individuals as defined under the M&A Rules that are our beneficial owners. As of the date of this annual report, we do not have any equity interest in any corporations incorporated in mainland China or have any contractual arrangements with any corporations incorporated in mainland China. However, there remains some uncertainty as to how the M&A Rules will be interpreted or implemented in the context of an overseas offering and its opinions summarized above are subject to any new laws, rules and regulations or detailed implementations and interpretations in any form relating to the M&A Rules. We cannot assure you that relevant PRC government agencies, including the CSRC, would reach the same conclusion as we do.

Furthermore, the Overseas Listing Regulations set out new filing requirements, report obligations and guidance for confidentiality and achieves administration with the CSRC for PRC domestic companies seeking direct or indirect listings and offerings in overseas markets. Based on our management’s assessment, we do not believe we will be subject to the Overseas Listing Regulations since our business activities and identity of management team do not meet either of the conditions and our offering will not be determined as indirect overseas offering under the Overseas Listing Trial Measures. However, as the Overseas Listing Regulations were recently released and their interpretation and implementation remain uncertain.

The substantial operation of us is based in Singapore, Hong Kong and the Cayman Islands, and we do not operate through any VIE agreement with our subsidiaries in China or own any equity interest in corporations incorporated in mainland China. However, if it is determined that any CSRC approval, filing, cybersecurity review or other governmental authorization is required for our previous or future offering, we may face sanctions by the CSRC, the CAC or other PRC regulatory agencies for failure to do so, and if we are denied from PRC authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange, which would materially affect the interest of the investors.

For more detailed information, see “Item 3. Key Information — D. Risk Factors —The Chinese government may exercise significant oversight and discretion over the conduct of business in the PRC and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of our securities,” “Item 3. Key Information — D. Risk Factors — The PRC government may intervene or influence our business operations at any time or may exert more control over offerings conducted overseas and foreign investment in China based issuers, which could result in a material change in our business operations or the value of our securities. Additionally, the approval or other administration requirements of the CSRC, or other PRC governmental authorities, may be required under a PRC regulation or any new laws, rules or regulations to be enacted, and if required, we cannot assure you that we will be able to obtain such approval. The regulation also establishes more complex procedures for acquisitions conducted by foreign investors that could make it more difficult for us to grow through acquisitions.”

8

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Uncertainties with respect to the PRC legal system could affect us

Changes in the policies, regulations, rules, and the enforcement of laws of the PRC government may be quick with little advance notice and could have a significant impact upon our ability to operate profitably in the PRC.

The Chinese government may exercise significant oversight and discretion over the conduct of business in the PRC and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of our securities. We are also currently not required to obtain approval from Chinese authorities to list on U.S. exchanges, however, if we are required to obtain approval in the future and are denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange, which would materially affect the interest of the investors.

The PRC government may intervene or influence our business operations at any time or may exert more control over offerings conducted overseas and foreign investment in China based issuers, which could result in a material change in our business operations or the value of our securities. Additionally, the governmental and regulatory interference could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. see “Risks Related to Doing Business in Jurisdictions We Operate” and “Risks Related to our ADSs and our Securities” in the Risk Factors section.

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not Applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

| D. | Risk Factors |

Summary of Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may materially and adversely affect our business, financial condition, results of operations, cash flows and prospects that you should consider before making a decision to invest in our ADSs. You should carefully consider the matters discussed under “Item 3. Key Information — D. Risk factors” in our Form 20-F.

Risks Related to Our Business and Industry

| ● | We operate in a heavily regulated industry, and are subject to extensive and evolving regulatory requirements in the jurisdictions in which we operate. |

| ● | We had incurred net losses in the past, and we may incur losses again in the future. |

| ● | We may not be able to obtain or maintain all necessary licenses, permits and approvals and to make all necessary registrations and filings for our business activities in multiple jurisdictions and related to residents therein, especially in the PRC or otherwise relating to PRC residents. |

9

| ● | PRC governmental control of currency conversion, cross-border remittance and offshore investment could have a direct impact on the trading volume on our platform, and the PRC government could further tighten restrictions on converting Renminbi to foreign currencies and/or deems our practices to be in violation of PRC laws and regulations. |

| ● | We may be unable to retain existing clients or attract new clients, or we may fail to offer services to address the needs of our clients as they evolve. |

| ● | Our level of commission and fee rates may decline in the future. Any material reduction in our commission or fee rates could reduce our profitability. |

| ● | We cannot guarantee the profitability of our clients’ investments or ensure that our clients will make rational investment judgements. |

| ● | We may incur material trading losses from our market making activities. |

| ● | Failure to comply with regulatory capital requirements set by local regulatory authorities could materially and negatively affect our business operation and overall performance. |

| ● | Our total return swap (TRS) trading services may not be successful, and we may not find adequate funding at reasonable costs to successfully operate our TRS trading business. |

| ● | We depend on the services of prime brokers and clearing agents to assist in providing us with access to liquidity in CFD trading. The loss of one or more of our prime brokerage relationships could lead to increased transaction costs and capital posting requirements, as well as having a negative impact on our ability to verify our open positions, collateral balances and trade confirmations. |

| ● | We rely on a number of external service providers for technology, processing and supporting functions, and if they fail to provide these services, it could adversely affect our business and harm our reputation. |

| ● | We may be liable for improper collection, use or appropriation of personal information provided by our customers. |

| ● | We may encounter potential conflicts of interest from time to time, and the failure to identify and address such conflicts of interest could adversely affect our business. |

| ● | We face risks related to our know-your-customer, or KYC procedures when our clients provide outdated, inaccurate, false or misleading information. |

| ● | Our clients may engage in fraudulent or illegal activities on our platform. |

| ● | The current trade war between the U.S. and China may dampen growth in China and other markets where the majority of our clients reside. |

10

Risk Related to Our Corporate Structure

| ● | We may rely on dividends and other distributions on equity paid by our subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business. |

Risks Related to Doing Business in Jurisdictions We Operate

| ● | A downturn in the Hong Kong, China or global economy, and economic and political policies of China could materially and adversely affect our business and financial condition. |

| ● | The Hong Kong legal system embodies uncertainties which could limit the legal protections available to Lion. |

| ● | Hong Kong regulatory requirement of prior approval for transfer of shares in excess of certain threshold may restrict future takeovers and other transactions. |

| ● | Uncertainties with respect to the PRC legal system could adversely affect us. |

| ● | Changes in the policies, regulations, rules, and the enforcement of laws of the PRC government may be quick with little advance notice and could have a significant impact upon our ability to operate profitably in the PRC. |

| ● | The Chinese government may exercise significant oversight and discretion over the conduct of business in the PRC and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of our securities. |

| ● | The PRC government may intervene or influence our business operations at any time or may exert more control over offerings conducted overseas and foreign investment in China based issuers, which could result in a material change in our business operations or the value of our securities. Additionally, the approval or other administration requirements of the CSRC, or other PRC governmental authorities, may be required under a PRC regulation or any new laws, rules or regulations to be enacted, and if required, we cannot assure you that we will be able to obtain such approval. The regulation also establishes more complex procedures for acquisitions conducted by foreign investors that could make it more difficult for us to grow through acquisitions. |

Risks Related to our ADSs and our Securities

| ● | The price of our ADSs may be volatile. |

| ● | Reports published by analysts, including projections in those reports that differ from our actual results, could adversely affect the price and trading volume of our ADSs. |

| ● | Holders of our ADSs may not have the same voting rights as our registered shareholders and might not receive voting materials in time to be able to exercise their right to vote. |

| ● | The voting rights ADSs holders are limited by the terms of the deposit agreement, and ADSs holders may not be able to exercise rights to direct how the Class A Ordinary Shares represented by ADSs are voted. |

11

Risks Related to Our Business and Industry

Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in laws and regulations in China could adversely affect us.

Although the substantial operation of us is based in Hong Kong and the Cayman Islands, we launched our apps in the app stores of China and most of our users are PRC citizens, which may subject us to certain laws and regulations in China. The PRC government has recently published new policies that significantly affected certain industries such as the education and internet industries, and we cannot rule out the possibility that it will in the future release regulations or policies regarding our industry that could affect our business, financial condition and results of operations. Furthermore, since the PRC legal system continues to evolve rapidly, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to us. Furthermore, the PRC legal system is based in part on government policies and internal rules, some of which are not published on a timely basis or at all and may have retroactive effect. As a result, we may not be aware of our violation of these policies and rules until sometime after the violation. Such uncertainties could adversely affect our business that relates to China or PRC citizens.

The PRC government has significant authority to exert influence on the ability of a company with operations in China, including us, to conduct its business. Changes in China’s economic, political or social conditions or government policies could materially and adversely affect our business and results of operations. We are subject to risks due to the uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to the risks of uncertainty about any future actions of the PRC government on U.S. listed companies. We may also be subject to sanctions imposed by PRC regulatory agencies, including CSRC, if we fail to comply with their rules and regulations. Any actions by the PRC government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in companies having operations in China, including us, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors, and cause the value of our securities to significantly decline or become worthless. These China-related risks could result in a material change in our operations and/or the value of our securities, or could significantly limit or completely hinder our ability to offer securities to investors in the future and cause the value of such securities to significantly decline or become worthless.

The PRC government may exert, at any time, substantial intervention and influence over the manner our operations. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, adopting new measures to extend the scope of cybersecurity reviews and new laws and regulations related to data security, and expanding the efforts in anti-monopoly enforcement.

The regulatory framework for the collection, use, safeguarding, sharing, transfer and other processing of personal information and important data worldwide is rapidly evolving in PRC and is likely to remain uncertain for the foreseeable future. Regulatory authorities in China have implemented and are considering a number of legislative and regulatory proposals concerning data protection. For example, the PRC Cybersecurity Law, which became effective in June 2017, established China’s first national-level data protection for “network operators,” which may include all organizations in China that connect to or provide services over the internet or other information network. The PRC Data Security Law, which was promulgated by the Standing Committee of PRC National People’s Congress, or the SCNPC, on June 10, 2021 and became effective on September 1, 2021, outlines the main system framework of data security protection.

12

In December 2021, the Cyberspace Administration of China (the “CAC”) promulgated the amended Measures of Cybersecurity Review which require cyberspace operators with personal information of more than one million users to file for cybersecurity review with the Cybersecurity Review Office (“CRO”), in the event such operators plan for an overseas listing. The amended Measures of Cybersecurity Review provide that, among others, an application for cybersecurity review must be made by an issuer that is a “critical information infrastructure operator” or a “data processing operator” as defined therein before such issuer’s securities become listed in a foreign country, if the issuer possesses personal information of more than one million users, and that the relevant governmental authorities in the PRC may initiate cybersecurity review if such governmental authorities determine an operator’s cyber products or services, data processing or potential listing in a foreign country affect or may affect China’s national security. The amended Measures of Cybersecurity Review took effect on February 15, 2022. In August 2021, the Standing Committee of the National People’s Congress of China promulgated the Personal Information Protection Law which became effective on November 1, 2021. The Personal Information Protection Law provides a comprehensive set of data privacy and protection requirements that apply to the processing of personal information and expands data protection compliance obligations to cover the processing of personal information of persons by organizations and individuals in China, and the processing of personal information of persons outside of China if such processing is for purposes of providing products and services to, or analyzing and evaluating the behavior of, persons in China. The Personal Information Protection Law also provides that critical information infrastructure operators and personal information processing entities who process personal information meeting a volume threshold to be set by Chinese cyberspace regulators are also required to store in China the personal information generated or collected in China, and to pass a security assessment administered by Chinese cyberspace regulators for any export of such personal information. Moreover, pursuant to the Personal Information Protection Law, persons who seriously violate this law may be fined for up to RMB50 million or 5% of annual revenues generated in the prior year and may also be ordered to suspend any related activity by competent authorities.

In November 2021, the CAC released the Regulations on Network Data Security (draft for public comments) and accepted public comments until December 13, 2021. The draft Regulations on Network Data Security provide more detailed guidance on how to implement the general legal requirements under laws such as the Cybersecurity Law, Data Security Law and the Personal Information Protection Law. The draft Regulations on Network Data Security follow the principle that the state will regulate based on a data classification and multi-level protection scheme, under which data is largely classified into three categories: general data, important data and core data. Under the current PRC cybersecurity laws in China, critical information infrastructure operators that intend to purchase internet products and services that may affect national security must be subject to the cybersecurity review. On July 30, 2021, the State Council of the PRC promulgated the Regulations on the Protection of the Security of Critical Information Infrastructure, which took effect on September 1, 2021. The regulations require, among others, that certain competent authorities shall identify critical information infrastructures. If any critical information infrastructure is identified, they shall promptly notify the relevant operators and the Ministry of Public Security.

Currently, the cybersecurity laws and regulations have not directly affected our business and operations, but in anticipation of the strengthened implementation of cybersecurity laws and regulations and the expansion of our business, we face potential risks if we are deemed as a critical information infrastructure operator under the Cybersecurity Law. In such case, we must fulfill certain obligations as required under the Cybersecurity Law and other applicable laws, including, among others, storing personal information and important data collected and produced within the PRC territory during our operations in China, which we are already doing in our business, and we may be subject to review when purchasing internet products and services. The amended Measures of Cybersecurity Review became effective in February 2022, we may be subject to review when conducting data processing activities, and may face challenges in addressing its requirements and make necessary changes to our internal policies and practices in data processing. As of the date of this annual report, we have not been involved in any investigations on cybersecurity review made by the CAC on such basis, and we have not received any inquiry, notice, warning, or sanctions in such respect. Based on the foregoing, we do not expect that, as of the date of this annual report, the current applicable PRC laws on cybersecurity would have a material adverse impact on our business.