Table of Contents

As filed with the Securities and Exchange Commission on April 22, 2024

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

SEAC II Corp.*

(Exact name of registrant as specified in its charter)

| Cayman Islands* | 7812 | N/A | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

955 Fifth Avenue

New York, NY 10075

(310) 209-7280

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Eli Baker

President and Chief Financial Officer

Screaming Eagle Acquisition Corp.

955 Fifth Avenue

New York, NY 10075

Telephone: (310) 209-7280

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Joel L. Rubinstein Jonathan P. Rochwarger White & Case LLP 1221 Avenue of the Americas New York, NY 10020 (212) 819-8200 |

David Coll-Black Goodmans LLP 333 Bay Street Toronto, Canada, ON M5H 2S7 |

David E. Shapiro Wachtell, Lipton, Rosen & Katz 51 West 52nd Street New York, New York 10019 (212) 403-1000 |

Kimberly Burns Bennett Wong Dentons Canada LLP 250 Howe Street, 20th Floor Vancouver, British Columbia Canada, V6C 3R8 |

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

| * | Prior to the consummation of the Business Combination described herein, the Registrant intends to effect a deregistration pursuant to and in accordance with Sections 206 through 209 of the Cayman Islands Companies Act (as revised) and a continuation and domestication as a British Columbia company in accordance with the Business Corporations Act (British Columbia), pursuant to which the Registrant’s jurisdiction of incorporation will be changed from the Cayman Islands to British Columbia, Canada. In connection with the Business Combination, the Registrant intends to change its name to Lionsgate Studios Corp. |

The registrant (the “Registrant”) hereby amends this registration statement (the “Registration Statement”) on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

This registration statement registers the resale of up to 25,110,168 common shares (the “Offering Shares”), without par value, of SEAC II Corp., a Cayman Islands exempted company, by the Selling Shareholders named in this prospectus (or their permitted transferees) (the “Selling Shareholders”). The Selling Shareholders are expected to be issued the PIPE Shares (as defined below) in private placements immediately after the Amalgamations (as defined below) in connection with the proposed business combination and immediately prior to the consummation of the Business Combination by and among Screaming Eagle Acquisition Corp. (“SEAC”), SEAC II Corp., a Cayman Islands exempted company and a wholly-owned subsidiary of SEAC (“New SEAC” or “Pubco” following the consummation of the Business Combination), Lions Gate Entertainment Corp., a British Columbia company (“Lions Gate Parent” or “Lionsgate”), LG Sirius Holdings ULC, a British Columbia unlimited liability company and a wholly-owned subsidiary of Lions Gate Parent (“Studio HoldCo”), LG Orion Holdings ULC, a British Columbia unlimited liability company and a wholly-owned subsidiary of Lions Gate Parent (“StudioCo”), SEAC MergerCo, a Cayman Islands exempted company and a direct, wholly-owned subsidiary of New SEAC (“MergerCo”), and 1455941 B.C. Unlimited Liability Company, a British Columbia unlimited liability company and a direct, wholly-owned subsidiary of SEAC (“New BC Sub”).

The Offering Shares will not be issued and outstanding at the time of the extraordinary general meetings (the “SEAC Meetings”) of SEAC’s shareholders and public warrantholders relating to the Business Combination. Further, the holders of the Offering Shares will not receive any proceeds from the trust account established in connection with SEAC’s initial public offering in the event SEAC does not consummate an initial business combination by the June 15, 2024 deadline set forth in its amended and restated memorandum and articles of association, as amended (the “SEAC Articles”). In the event the Business Combination is not approved by SEAC Shareholders or the other conditions precedent to the consummation of the Business Combination are not met or waived, the PIPE Shares will not be issued and New SEAC will seek to withdraw the registration statement prior to its effectiveness.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be issued until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and does not constitute the solicitation of an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 22, 2024

PRELIMINARY PROSPECTUS

SEAC II CORP.

25,110,168 Common Shares

This prospectus relates to the resale from time to time by the Selling Shareholders named in this prospectus or their permitted transferees (collectively, the “Selling Shareholders”) of up to 25,110,168 common shares (the “Offering Shares”), without par value, of SEAC II Corp., a Cayman Islands exempted company limited by shares (“New SEAC” or “Pubco”), which are expected to be issued to PIPE Investors (as defined below) in private placements immediately after the Amalgamations (as defined below) contemplated by the Business Combination (as defined below) pursuant to the terms of the Subscription Agreements (as defined below) in connection with the Business Combination. If the Business Combination is not consummated, the Offering Shares registered pursuant to this prospectus will not be issued.

On December 21, 2023, the board of directors of New SEAC (the “New SEAC Board”) and the board of directors of Screaming Eagle Acquisition Corp. (“SEAC” and its board of directors, the “SEAC Board”), respectively, approved a Business Combination Agreement, by and among SEAC, the parent company of New SEAC, New SEAC, Lions Gate Entertainment Corp., a British Columbia company (“Lions Gate Parent” or “Lionsgate”), LG Sirius Holdings ULC, a British Columbia unlimited liability company and a wholly-owned subsidiary of Lions Gate Parent (“Studio HoldCo”), LG Orion Holdings ULC, a British Columbia unlimited liability company and a wholly-owned subsidiary of Lions Gate Parent (“StudioCo”), SEAC MergerCo, a Cayman Islands exempted company and a direct, wholly-owned subsidiary of New SEAC (“MergerCo”), and 1455941 B.C. Unlimited Liability Company, a British Columbia unlimited liability company and a direct, wholly-owned subsidiary of SEAC (“New BC Sub”) (as amended on April 11, 2024 and as may be amended, supplemented or otherwise modified from time to time, the “Business Combination Agreement”). Pursuant to the Business Combination Agreement, among other things and subject to the terms and conditions contained therein and the plan of arrangement (i) SEAC will merge with and into MergerCo (the “SEAC Merger”) with MergerCo surviving the SEAC Merger as a direct, wholly-owned subsidiary of New SEAC (the resulting entity referred to herein as MergerCo or, where specified, the “SEAC Merger Surviving Company”), (ii) SEAC Merger Surviving Company will distribute all of its assets lawfully available for distribution to New SEAC by way of a cash dividend (the “Cash Distribution”), (iii) SEAC Merger Surviving Company will transfer by way of continuation from the Cayman Islands to British Columbia in accordance with the Cayman Islands Companies Act (as revised) (the “Companies Act”) and the Business Corporations Act (British Columbia) (the “BC Act”) and convert to a British Columbia unlimited liability company in accordance with the BC Act (the “MergerCo Domestication and Conversion”), (iv) New SEAC will transfer by way of continuation from the Cayman Islands (the “New SEAC Domestication”, and together with the MergerCo Domestication and Conversion, the “Domestications”) to British Columbia in accordance with the Companies Act and continue as a British Columbia company in accordance with the applicable provisions of the BC Act, and (v) pursuant to an arrangement under Division 5 of Part 9 of the BC Act (the “Arrangement”), on the terms and subject to the conditions set forth in the Plan of Arrangement, (A) SEAC Merger Surviving Company and New BC Sub will amalgamate (the “MergerCo Amalgamation”) to form one corporate entity (“MergerCo Amalco”), in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement, (B) New SEAC and MergerCo Amalco will amalgamate (the “SEAC Amalgamation”) to form one corporate entity (“SEAC Amalco”), in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement, and (C) StudioCo and SEAC Amalco will amalgamate (the “StudioCo Amalgamation” and together with the MergerCo Amalgamation and the SEAC Amalgamation, the “Amalgamations”) to form one corporate entity (“Pubco”), in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement. The SEAC Merger, the Cash Distribution, the Domestications and the Arrangement (which includes the Amalgamations), together with the other transactions contemplated by the Business Combination Agreement, the Plan of Arrangement and all other agreements, certificates and instruments entered into in connection therewith, are referred to herein as the “Business Combination.” If the Business Combination

Table of Contents

Agreement and the SEAC Merger are approved and adopted by SEAC’s shareholders and the closing conditions contemplated by the Business Combination Agreement are satisfied, New SEAC intends to effect a deregistration pursuant to and in accordance with Sections 206 through 209 of the Cayman Islands Companies Act (as revised) and a continuation and domestication as a British Columbia company in accordance with the Business Corporations Act (British Columbia), pursuant to which the New SEAC’s jurisdiction of incorporation will be changed from the Cayman Islands to British Columbia, Canada. In connection with the Business Combination, New SEAC intends to change its name to Lionsgate Studios Corp.

In connection with the Business Combination, concurrently with the execution of the Business Combination Agreement on December 22, 2023, and on April 11, 2024, SEAC, New SEAC and Lions Gate Parent entered into subscription agreements with the PIPE Investors pursuant to which the PIPE Investors have agreed, subject to the terms and conditions set forth therein, to subscribe for and purchase from Pubco, immediately following the Amalgamations, an aggregate of approximately 23,091,217 common shares of Pubco (the “PIPE Shares”), at a purchase price of $9.63 per share and $10.165 per share, respectively, for an aggregate cash amount of $225,000,000. Additionally, the Subscription Agreements provide certain PIPE Investors with certain reduction rights, pursuant to which the PIPE Investors may offset their total commitments under their respective Subscription Agreements to the extent such PIPE Investors purchase SEAC Class A Ordinary Shares (as defined below) in the open market or otherwise own such shares as of the date of the Subscription Agreement.

The Selling Shareholders may offer, sell or distribute all or a portion of the PIPE Shares registered hereby publicly or through private transactions at prevailing market prices or at negotiated prices. We will pay certain offering fees and expenses and fees in connection with the registration of the PIPE Shares and will not receive proceeds from the sale of the PIPE Shares by the Selling Shareholders. Class A ordinary shares, par value $0.0001 per share, of SEAC (a “SEAC Class A Ordinary Share”) and public warrants of SEAC (“SEAC Warrants”) are currently listed on the Nasdaq Capital Market (“Nasdaq”) and trade under the symbols “SCRM” and “SCRMW”, respectively. In addition, certain of the SEAC Class A Ordinary Shares and the SEAC Public Warrants currently trade as part of the SEAC Units, which are listed on Nasdaq under the symbol “SCRMU”. Upon consummation of the Business Combination (the “Closing” and the date of the Closing, the “Closing Date”), SEAC Public Shareholders who do not redeem their SEAC Class A Ordinary Shares will ultimately (as a result of the SEAC Merger and the Amalgamations) receive one (1) common share of Pubco (“Pubco Common Share”) for each SEAC Class A Ordinary Share held by them immediately prior to the SEAC Merger. One business day prior to the Closing Date and prior to the SEAC Merger, subject to the approval by the public warrantholders of SEAC (the “SEAC Public Warrantholders”), each then issued and outstanding SEAC Public Warrant will be automatically exchanged for $0.50 in cash. In addition, all of the SEAC Private Placement Warrants will be forfeited and cancelled for no consideration. It is anticipated that upon the Closing, the Pubco Common Shares will be listed on Nasdaq under the ticker symbol “LION”. Pubco will have no units or warrants traded following the Closing.

INVESTING IN OUR SECURITIES INVOLVES RISKS THAT ARE DESCRIBED IN THE “RISK FACTORS” SECTION BEGINNING ON PAGE 21 OF THIS PROSPECTUS.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this prospectus or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is April , 2024.

Table of Contents

| 1 | ||||

| 7 | ||||

| 10 | ||||

| 19 | ||||

| 21 | ||||

| 41 | ||||

| Unaudited Pro Forma Condensed Combined Financial Information |

42 | |||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations of SEAC |

65 | |||

| 75 | ||||

| Business of LG Studios and Certain Information About StudioCo |

135 | |||

| 149 | ||||

| 152 | ||||

| 154 | ||||

| 155 | ||||

| 159 | ||||

| 167 | ||||

| 215 | ||||

| 221 | ||||

| 228 | ||||

| 230 | ||||

| 231 | ||||

| 232 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus. No one has been authorized to provide you with information that is different from that contained in this prospectus. This prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this prospectus is accurate as of any date other than that date.

For investors outside the United States: We have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

i

Table of Contents

Unless otherwise stated or unless the context otherwise requires, the term“SEAC” refer to Screaming Eagle Acquisition Corp., the terms “we,” “us,” “our,” “New SEAC” refer to SEAC II Corp. and “Pubco,” “combined company” and “post-combination company” refer to SEAC II Corp. (to be renamed as Lionsgate Studios Corp.) and its subsidiaries following the consummation of the Business Combination.

Unless the context otherwise requires, references in this prospectus to:

| • | “A&R Registration Rights Agreement” are to that certain amended and restated registration rights agreement Pubco, Studio HoldCo and SEAC Sponsor will enter into concurrently with the Closing. |

| • | “Adjusted OIBDA” are to a non-GAAP measure calculated as operating income (loss) before adjusted depreciation and amortization (“OIBDA”), adjusted for adjusted share-based compensation, purchase accounting and related adjustments, restructuring and other costs, certain charges (benefits) related to the COVID-19 global pandemic, certain programming and content charges as a result of management changes and/or changes in strategy, and unusual gains or losses (such as goodwill and intangible asset impairment and charges related to Russia’s invasion of Ukraine), when applicable. |

| • | “Aggregate Transaction Proceeds” are to an amount equal to the sum of (a) the amount of cash available in the Trust Account at Closing (subject to certain adjustments and after, for the avoidance of doubt, giving effect to redemptions but, for the avoidance of doubt, prior to the SEAC Public Warrant Exchange or the payment of any transaction expenses) plus (b) the aggregate cash proceeds actually received or deemed received by Pubco, SEAC, New SEAC or any of their applicable successors or assigns in respect of the PIPE. |

| • | “Amalgamations” are to the SEAC Amalgamation, the MergerCo Amalgamation and the StudioCo Amalgamation, collectively. |

| • | “Arrangement” are to an arrangement proposed by New BC Sub under Part 9, Division 5 of the BC Act on the terms and subject to the conditions set forth in the Plan of Arrangement, subject to any amendments or variations to the Plan of Arrangement made in accordance with the terms of the Business Combination Agreement or the provisions of the Plan of Arrangement or made at the directions of the Court in the Interim Order or Final Order with the prior written consent of SEAC and Lions Gate Parent, such consent not to be unreasonably withheld, conditioned or delayed. |

| • | “BC Act” are to the Business Corporations Act (British Columbia). |

| • | “Business Combination” are to the transactions, including the SEAC Merger, the Cash Distribution, the Domestications and the Amalgamations, contemplated by the Business Combination Agreement, the Plan of Arrangement and all other agreements entered into in connection therewith. |

| • | “Business Combination Agreement” are to that certain Business Combination Agreement, dated December 22, 2023, as amended on April 11, 2024, by and among SEAC, New SEAC, Lions Gate Parent, Studio HoldCo, StudioCo, MergerCo and New BC Sub. |

| • | “Class B Conversion” are to any remaining SEAC Class B Ordinary Shares being deemed cancelled and surrendered for no consideration pursuant to a surrender letter in connection with each of the 2,010,000 remaining SEAC Class B Ordinary Shares automatically converting into one SEAC Class A Ordinary Share immediately following the Sponsor Securities Repurchase. |

| • | “Closing” are to the closing of the Business Combination. |

| • | “Closing Date” are to the date of Closing. |

| • | “Code” are to the U.S. Internal Revenue Code of 1986, as amended. |

| • | “Companies Act” are to the Cayman Islands Companies Act (as amended). |

1

Table of Contents

| • | “Court” are to the Supreme Court of British Columbia. |

| • | “Deadline Date” are to the date by which SEAC must complete an Initial Business Combination, in accordance with the SEAC Articles. |

| • | “Domestication(s)” are to the transfer of New SEAC and/or MergerCo by way of continuation from the Cayman Islands to British Columbia, Canada in accordance with the memorandum and articles of association of respective entities and the Companies Act and BC Act and the domestication of New SEAC and/or MergerCo as British Columbia company(y/ies) in accordance with the applicable provisions of the BC Act, including all matters necessary or ancillary in order to effect such transfer by way of continuation, including the adoption of the notice of articles and articles in connection with the continuation into British Columbia under the BC Act. |

| • | “Exchange Act” are to the U.S. Securities Exchange Act of 1934, as amended. |

| • | “Final Order” are to the final order of the Court pursuant to section 291 of the BC Act, approving the Arrangement, in a form acceptable to SEAC and Lions Gate Parent, each acting reasonably, as such order may be amended, modified, supplemented or varied by the Court with the consent of SEAC and Lions Gate Parent, such consent not to be unreasonably withheld, conditioned or delayed, at any time prior to the effective time of the Arrangement or, if appealed, then, unless such appeal is withdrawn or denied, as affirmed or amended, on appeal, provided that any such affirmation or amendment is acceptable to each of SEAC and Lions Gate Parent, each acting reasonably. |

| • | “Form S-4/A” are to New SEAC’s Form S-4/A (File No. 333-276414), last filed with the SEC on April 12, 2024. |

| • | “GAAP” are to generally accepted accounting principles. |

| • | “Initial Business Combination” are to SEAC’s initial merger, amalgamation, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more business. |

| • | “Interim Order” are to the interim order of the Court contemplated by Section 2.02 of the Business Combination Agreement and made pursuant to section 291 of the BC Act, providing for, among other things, the calling and holding of the SEAC Shareholders’ Meeting, as the same may be amended, modified, supplemented or varied by the Court with the consent of SEAC and Lions Gate Parent, such consent not to be unreasonably withheld, conditioned or delayed, provided that any such amendment is reasonably acceptable to each of SEAC and Lions Gate Parent. A copy of the Interim Order is attached as Annex P to the Form S-4/A. |

| • | “Investment Canada Act” are to the Investment Canada Act (Canada) and the regulations made thereunder. |

| • | “IRS” are to the U.S. Internal Revenue Service. |

| • | “ITA” are to the Income Tax Act (Canada) and the regulations made thereunder as amended from time to time. |

| • | “LG Internal Restructuring” are to a series of transactions, which, if completed in their entirety, will result in the transfer of the Studio Business from Lions Gate Parent to StudioCo and the retention of Lions Gate Parent of the Starz Business. |

| • | “Lions Gate Parent” or “Lionsgate” are to Lions Gate Entertainment Corp., a British Columbia company. |

| • | “LG Parties” are to Lions Gate Parent, Studio HoldCo and StudioCo. |

| • | “LG Studios” are to StudioCo assuming, unless the context otherwise requires, the completion of the LG Internal Restructuring pursuant to which StudioCo shall, directly or indirectly, own the Studio Business. |

2

Table of Contents

| • | “Lock-Up Agreement” are to the lock-up agreement by which the SEAC Sponsor and its transferees and holders of Pubco Common Shares affiliated with Lions Gate Parent (collectively, the “Lockup Shareholders”) will become bound on the Closing Date pursuant to the Business Combination Agreement and as set forth in the Plan of Arrangement. |

| • | “Maximum Redemption Scenario” are to the redemption scenario assuming that holders of an additional 5,531,192 SEAC Class A Ordinary Shares, or approximately 32% of the currently outstanding SEAC Class A Ordinary Shares following the Extension Meeting, exercise redemption rights with respect to such shares for their pro rata share of the funds in the Trust Account. As the Business Combination Agreement includes a Minimum Cash Condition that, at the Closing, Aggregate Transaction Proceeds be at least equal to $350.0 million in cash, including (i) at least $125.0 million in cash from the Trust Account (subject to adjustments and after reduction for the aggregate amount of payments required to be made in connection with any redemptions), plus (ii) the aggregate amount of cash that has been funded pursuant to the PIPE. Thus, the redemption of 5,531,192 SEAC Class A Ordinary Shares represents the estimated maximum number of SEAC Class A Ordinary Shares that can be redeemed while still achieving the Minimum Cash Condition. |

| • | “MergerCo” are to SEAC MergerCo, a Cayman Islands exempted company and a direct wholly-owned subsidiary of New SEAC, through the continuation into British Columbia under the BC Act. |

| • | “MergerCo Amalgamation” are to the amalgamation of SEAC Merger Surviving Company and New BC Sub pursuant to the Plan of Arrangement to form one corporate entity (“MergerCo Amalco”), in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement. |

| • | “MergerCo Class A Common Shares” are to the Class A common shares in the authorized share structure of SEAC Merger Surviving Company. |

| • | “Nasdaq” are to The Nasdaq Stock Market LLC. |

| • | “New BC Sub” are to 1455941 B.C. Unlimited Liability Company, and a British Columbia unlimited liability company and a direct, wholly-owned subsidiary of SEAC. |

| • | “New SEAC” are to SEAC II Corp., a Cayman Islands exempted company and a wholly-owned subsidiary of SEAC, which in connection with the Business Combination will effect a deregistration pursuant to and in accordance with the Companies Act and a continuation and domestication as a British Columbia company in accordance with the BC Act, pursuant to which jurisdiction of New SEAC will be changed from the Cayman Islands to British Columbia, Canada. |

| • | “New SEAC Domestication” are to New SEAC transferring by way of continuation from the Cayman Islands to British Columbia in accordance with the Companies Act and continuing as a British Columbia company in accordance with the applicable provisions of the BC Act. |

| • | “Newly Issued Reduction Right Shares” means any newly issued SEAC Class A Ordinary Shares that may be issued to such PIPE Investors in connection with their purchase of the Reduction Right Shares. |

| • | “No Redemption Scenario” or “No Additional Redemption Scenario” are to the redemption scenario assuming that none of the holders of SEAC Class A Ordinary Shares exercise redemption rights with respect to such shares in connection with the Business Combination (but takes into account redemptions that already occurred in connection with the Extension Meeting). |

| • | “Offering Shares” are to PIPE Shares being registered herein. |

| • | “Outside Date” are to June 15, 2024, which can be extended to July 31, 2024 by SEAC or Lions Gate Parent subject to the conditions in the Business Combination Agreement. |

| • | “Pubco Sponsor Options” are to the options of Pubco to be issued to SEAC Sponsor in connection with the Closing, each of which is exercisable to purchase one Pubco Common Share. |

3

Table of Contents

| • | “PIPE” are to a private placement to close immediately following the Amalgamations and conditioned upon the effectiveness of the consummation of the Business Combination, for an aggregate investment price equal to $225,000,000. |

| • | “PIPE Investors” are to those certain investors participating in the PIPE pursuant to the Subscription Agreements. |

| • | “PIPE Shares” are to the 23,091,217 Pubco Common Shares to be issued to the PIPE Investors in connection with the Business Combination. |

| • | “Plan of Arrangement” are to the Plan of Arrangement in respect of the Arrangement, the form of which is attached as Annex B to the Form S-4/A, subject to any amendments or variations to such plan made in accordance with the Business Combination Agreement and the Plan of Arrangement or made at the direction of the Court in the Final Order with the prior written consent of StudioCo and SEAC, each acting reasonably. |

| • | “Private Placement” are to the issuance of an aggregate of 23,091,217 Pubco Common Shares pursuant to the Subscription Agreements to the PIPE Investors immediately following the Amalgamations, at a purchase price of $9.63 per share and $10.165 per share, as applicable. |

| • | “Pubco” are to New SEAC, as such entity exists on the date hereof and as it is continued and amalgamated in connection with the Business Combination. Pubco intends to change its name to Lionsgate Studios Corp. following the Business Combination. |

| • | “Pubco Board” are to the board of directors of Pubco following the StudioCo Amalgamation. |

| • | “Pubco Closing Articles” are to the notice of articles and articles of Pubco to be adopted at the StudioCo Amalgamation Effective Time. |

| • | “Pubco Common Shares” are to, collectively, the Pubco common shares in the authorized share capital of Pubco. |

| • | “Pubco Shareholders” are to subsequent to the StudioCo Amalgamation, the shareholders of Pubco. |

| • | “Reduction Right Shares” are to shares purchased by the PIPE Investors for which they have exercised their reduction right in accordance with the terms of the Subscription Agreements. |

| • | “Registration Statement” are to this registration statement on Form S-1 filed with the SEC by Pubco, as it may be amended or supplemented from time to time, of which this prospectus forms a part. |

| • | “Sarbanes-Oxley Act” are to the U.S. Sarbanes-Oxley Act of 2002. |

| • | “SEAC” are to Screaming Eagle Acquisition Corp., a Cayman Islands exempted company. |

| • | “SEAC Amalgamation” are to the amalgamation of New SEAC and MergerCo Amalco pursuant to the Plan of Arrangement to form one corporate entity (“SEAC Amalco”), in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement. |

| • | “SEAC Articles” are to the amended and restated memorandum and articles of association of SEAC, adopted by Special Resolution dated January 4, 2022, effective on January 5, 2022, and as amended on April 9, 2024, as may be further amended and/or restated from time to time. |

| • | “SEAC Board” are to the board of directors of SEAC. |

| • | “SEAC Class A Ordinary Shares” are to SEAC’s Class A ordinary shares, par value $0.0001 per share, which are subject to possible redemption. |

| • | “SEAC Class B Ordinary Shares” are to SEAC’s Class B ordinary shares, par value $0.0001 per share. |

| • | “SEAC Entities” are to, collectively, New SEAC, MergerCo and New BC Sub. |

| • | “SEAC Founder Shares” are to the issued and outstanding SEAC Class B Ordinary Shares. |

4

Table of Contents

| • | “SEAC Insiders” are to SEAC Sponsor and the directors and officers of SEAC. |

| • | “SEAC IPO” are to SEAC’s initial public offering of SEAC Units, which closed on January 10, 2022. |

| • | “SEAC management” are to SEAC’s officers and directors. |

| • | “SEAC Meetings” are to the SEAC Shareholders’ Meeting and the SEAC Public Warrantholders’ Meeting. |

| • | “SEAC Merger” are to SEAC’s merger with MergerCo, where SEAC merges into MergerCo, with MergerCo being the surviving entity (the resulting entity referred to herein as MergerCo or, where specified, the “SEAC Merger Surviving Company”). |

| • | “SEAC Ordinary Shares” are to the SEAC Class A Ordinary Shares and the SEAC Class B Ordinary Shares. |

| • | “SEAC Private Placement Warrants” are to the warrants issued to SEAC Sponsor in a private placement simultaneously with the closing of the SEAC IPO. |

| • | “SEAC Public Shareholders” are to the holders of SEAC Public Shares. |

| • | “SEAC Public Shares” are to SEAC Class A Ordinary Shares sold as part of the SEAC Units in the SEAC IPO (whether they were purchased in the SEAC IPO or thereafter in the open market). |

| • | “SEAC Public Warrantholders’ Meeting” are to the extraordinary general meeting of SEAC Public Warrantholders that is the subject of this prospectus and any adjournments thereof. |

| • | “SEAC Public Warrantholders” are to the holders of SEAC Public Warrants. |

| • | “SEAC Public Warrants” are to the warrants sold as part of the SEAC Units in the SEAC IPO (whether they were purchased in the SEAC IPO or thereafter in the open market). |

| • | “SEAC Securities” are to SEAC Units, SEAC Ordinary Shares and SEAC Warrants, collectively. |

| • | “SEAC Shareholders” are to, collectively, the SEAC Sponsor and the SEAC Public Shareholders. |

| • | “SEAC Shareholders’ Meeting” are to the extraordinary general meeting of SEAC Shareholders to be held on May 7, 2024 and any adjournments thereof. |

| • | “SEAC Sponsor” are to Eagle Equity Partners V, LLC, a Delaware limited liability company. |

| • | “SEAC Sponsor Options” are to the 2,200,000 SEAC Sponsor Options to be issued to the SEAC Sponsor one business day prior to the Closing, as a partial consideration for the Sponsor Securities Repurchase. Each of SEAC Sponsor Options will entitle SEAC Sponsor to purchase one SEAC Class A Ordinary Share at $0.0001 per share if certain vesting conditions are met within 5 years of the Closing Date. In connection with the Business Combination, the SEAC Sponsor Options will ultimately become options to purchase Pubco Common Shares pursuant to the terms of the Sponsor Option Agreement. |

| • | “SEAC Units” are to the units of SEAC sold in the SEAC IPO, each of which consists of one SEAC Class A Ordinary Share and one-third of one SEAC Public Warrant. |

| • | “SEAC Warrant Agreement” are to the Warrant Agreement, dated January 10, 2022, between SEAC and Continental Stock Transfer & Trust Company, as warrant agent. |

| • | “SEAC Warrant Agreement Amendment” are to an amendment to the SEAC Warrant Agreement, pursuant to which, one business day prior to the Closing, each then issued and outstanding SEAC Public Warrant will be automatically exchanged for $0.50 in cash, and all of the issued and outstanding SEAC Private Placement Warrants will be forfeited and cancelled for no consideration, the form of which is attached as Annex F to the Form S-4/A. |

| • | “SEAC Warrants” are to the SEAC Private Placement Warrants and the SEAC Public Warrants, collectively. |

| • | “SEAC Warrant Support Investors” are to those certain SEAC Public Warrantholders who entered into Warrantholder Support Agreements. |

5

Table of Contents

| • | “SEAC Sponsor” are to Eagle Equity Partners V, LLC, a Delaware limited liability company. |

| • | “SEC” are to the U.S. Securities and Exchange Commission. |

| • | “Securities Act” are to the U.S. Securities Act of 1933, as amended. |

| • | “Special Resolution” are to a resolution passed by a majority of not less than two-thirds (66 2/3%) of the SEAC Shareholders as, being entitled to do so, vote in person or, where proxies are allowed, by proxy at the SEAC Shareholders’ Meeting. |

| • | “Sponsor Support Agreement” are to that certain letter agreement dated as of December 22, 2023, by and among SEAC Sponsor, SEAC, StudioCo and Lions Gate Parent, a copy of which is attached hereto as Annex G to the Form S-4/A. |

| • | “Sponsor Option Agreement” are to the sponsor option agreement that SEAC, New SEAC and the Sponsor will enter into, in connection with the Sponsor Securities Repurchase, one business day prior to the Closing, a copy of which is attached as Annex H to the Form S-4/A. |

| • | “Starz Business” are to substantially all of the assets and liabilities constituting Lions Gate Parent’s Media Networks segment. |

| • | “StudioCo” are to LG Orion Holdings ULC, a British Columbia unlimited liability company. |

| • | “StudioCo Amalgamation” are to the amalgamation of StudioCo’s and SEAC Amalco pursuant to the Plan of Arrangement to form one corporate entity (“Pubco”), in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement. |

| • | “StudioCo Amalgamation Effective Time” are to the effective time of the StudioCo Amalgamation. |

| • | “Studio Business” are to substantially all of the assets and liabilities constituting Lions Gate Parent’s Motion Picture and Television Production segments and a substantial portion of Lions Gate Parent’s corporate general and administrative functions. |

| • | “Studio HoldCo” are to LG Sirius Holdings ULC, a British Columbia unlimited liability company and a wholly owned subsidiary of Lions Gate Parent. |

| • | “Subscription Agreements” are to, the subscription agreements SEAC, New SEAC and Lions Gate Parent entered into with the PIPE Investors concurrently with the execution of the Business Combination Agreement and on April 11, 2024, a form of which is attached as Annex D to the Form S-4/A. |

| • | “Transfer Agent” are to Continental Stock Transfer & Trust Company, as transfer agent of SEAC. |

| • | “Trading Price” are to the daily closing price of the Pubco Common Shares (as adjusted for share splits, share dividends, reorganizations, recapitalizations and the like) for any twenty (20) trading days within a period of thirty (30) consecutive trading days beginning thirty (30) days or more after the Closing. |

| • | “Trust Account” are to the trust account that holds proceeds from the SEAC IPO and the concurrent private placement of the SEAC Private Placement Warrants, established by SEAC for the benefit of the SEAC Public Shareholders, maintained by Continental Stock Transfer & Trust Company, acting as trustee. |

| • | “Warrantholder Support Agreements” are to those certain investor rights agreements entered into between StudioCo and certain SEAC Public Warrantholders concurrently with the execution of the Business Combination Agreement. |

6

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements contained in this prospectus constitute forward-looking statements within the meaning of the federal securities laws. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. Forward-looking statements reflect SEAC’s, Lions Gate Parent’s or StudioCo’s current views, as applicable, with respect to, among other things, their respective capital resources, performance and results of operations. Likewise, all of Lions Gate Parent’s and StudioCo’s statements regarding anticipated growth in operations, anticipated market conditions, demographics and results of operations are forward-looking statements. In some cases, you can identify these forward-looking statements by the use of terminology such as “outlook”, “believe”, “expect”, “potential”, “continue”, “may”, “will”, “should”, “could”, “seek”, “approximately”, “predict”, “intend”, “plan”, “estimate”, “anticipate” or the negative version of these words or other comparable words or phrases.

The forward-looking statements contained in this prospectus reflect SEAC’s, Lions Gate Parent’s or StudioCo’s current views, as applicable, about future events and are subject to numerous known and unknown risks, uncertainties, assumptions and changes in circumstances that may cause actual results to differ significantly from those expressed in any forward-looking statement. None of SEAC, Lions Gate Parent or StudioCo guarantees that the transactions and events described will happen as described (or that they will happen at all). The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

| • | possible delays in closing the Business Combination, whether due to the inability to obtain SEAC Shareholder Approval or SEAC Public Warrantholder Approval, or failure to satisfy any of the conditions to closing the Business Combination, as set forth in the Business Combination Agreement; |

| • | the inability of the Business Combination, or an alternate business combination, to be completed by the Deadline Date, and the potential failure of SEAC to obtain an extension of the Deadline Date if sought by SEAC; |

| • | any waivers of the conditions to Closing as may be permitted in the Business Combination Agreement; |

| • | general economic uncertainty; |

| • | the volatility of currency exchange rates; |

| • | StudioCo’s ability to manage growth; |

| • | Pubco’s ability to obtain or maintain the listing of Pubco Common Shares on Nasdaq or any other national exchange following the Business Combination; |

| • | risks related to the rollout of StudioCo’s business and expansion strategy; |

| • | the effects of competition on StudioCo’s future business; |

| • | potential disruption in Lions Gate Parent’s employee retention as a result of the Business Combination; |

| • | the impact of and changes in governmental regulations or the enforcement thereof, tax laws and rates, accounting guidance and similar matters in regions in which Pubco operates or will operate in the future; |

| • | international, national or local economic, social or political conditions that could adversely affect the companies and their business; |

| • | the effectiveness of Pubco’s internal controls and its corporate policies and procedures; |

| • | changes in personnel and availability of qualified personnel; |

| • | the volatility of the market price and liquidity of SEAC Units, SEAC Public Shares and SEAC Public Warrants; |

7

Table of Contents

| • | potential write-downs, write-offs, restructuring and impairment or other charges required to be taken by Pubco subsequent to the Business Combination; |

| • | the possibility that the SEAC Board’s valuation of StudioCo was inaccurate, including the failure of SEAC’s diligence review to identify all material risks associated with the Business Combination; |

| • | the volatility of the market price and liquidity of Pubco Common Shares; |

| • | factors relating to the business, operations and financial performance of LG Studios and its subsidiaries and the Studio Business, including: |

| • | the anticipated benefits of the Business Combination may not be achieved; |

| • | changes in LG Studios’ business strategy, plans for growth or restructuring may increase its costs or otherwise affect its profitability; |

| • | LG Studios’ revenues and results of operations may fluctuate significantly; |

| • | the Studio Business relies on a few major retailers and distributors and the loss of any of those could reduce its revenues and operating results; |

| • | the Studio Business does not have long-term arrangements with many of its production or co- financing partners; |

| • | protecting and defending against intellectual property claims may have a material adverse effect on the Studio Business; |

| • | changes in consumer behavior, as well as evolving technologies and distribution models, may negatively affect the Studio Business, financial condition or results of operations; |

| • | LG Studios could be adversely affected by labor disputes, strikes or other union job actions; |

| • | LG Studios will be subject to risks associated with possible acquisitions, dispositions, business combinations, or joint ventures; and |

| • | business interruptions from circumstances or events out of LG Studios’ control could adversely affect LG Studios’ operations. |

Forward-looking statements regarding expected ownership of Pubco Common Shares by existing SEAC Shareholders and Lions Gate Parent Shareholders following the Business Combination have been calculated based on each of SEAC’s and StudioCo’s outstanding share capital, each as of the date of this prospectus. The statements contained under the heading “LG Studios Projected Financial Information” in this prospectus are considered forward-looking statements. Forward-looking statements representing post-closing expectations are inherently uncertain. Estimates such as expected revenue, production, operating expenses, Adjusted OIBDA, general and administrative expenses, capital expenditures, free cash flow, net debt, reserves and other measures are preliminary in nature. There can be no assurance that the forward-looking statements will prove to be accurate and reliance should not be placed on these estimates in making investment decisions. See the other cautionary statements under “LG Studios Projected Financial Information” for further information.

The forward-looking statements contained herein are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by the forward-

looking statements. For a further discussion of the risks and other factors that could cause SEAC’s, StudioCo’s or Pubco’s future results, performance or transactions to differ significantly from those expressed in any forward-looking statements, please see the section entitled “Risk Factors”. There may be additional risks that SEAC, StudioCo and/or Lions Gate Parent do not presently know or that SEAC, StudioCo and/or Lions Gate Parent currently believes are immaterial, that could also cause actual results to differ from those contained in the forward-looking statements. Should one or more of these risks or uncertainties materialize, or should any of the assumptions made in making these forward-looking statements prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. While such forward-looking

8

Table of Contents

statements reflect SEAC’s, StudioCo’s and Lions Gate Parent’s good faith beliefs, as applicable, they are not guarantees of future performance. SEAC, StudioCo and Lions Gate Parent disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes after the date of this prospectus, except as required by applicable law. You should not place undue reliance on any forward-looking statements, which are based only on information currently available to SEAC, StudioCo and Lions Gate Parent, as applicable.

9

Table of Contents

This summary highlights selected information included in this prospectus and does not contain all of the information that may be important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations of SEAC,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations of the Studio Business of Lions Gate Entertainment Corp.” and the financial statements included elsewhere in this prospectus.

Information About the Parties to the Business Combination

SEAC

SEAC is a blank check company incorporated as a Cayman Islands exempted company on November 3, 2021, for the purpose of effecting a merger, amalgamation, share exchange, asset acquisition, share purchase, reorganization or similar business combination involving SEAC and one or more target businesses.

SEAC’s securities are traded on Nasdaq under the ticker symbols “SCRM”, “SCRMU” and “SCRMW”. In connection with the Closing, the SEAC Securities will be delisted from Nasdaq.

SEAC’s sponsor is Eagle Equity Partners V, LLC, a Delaware limited liability company. The sole managing member of SEAC Sponsor is EEP Holdings – SC, LLC (“EEP Holdings”), a Delaware limited liability company. EEP Holdings is controlled by Eli Baker, Harry E. Sloan and Jeff Sagansky, each of whom is a U.S. person. The business of SEAC Sponsor is to invest in the securities of SEAC.

The mailing address of SEAC’s principal executive office is 955 Fifth Avenue, New York, NY 10075, and its telephone number is (310) 209-7280.

New SEAC

New SEAC is SEAC II Corp., a Cayman Islands exempted company and a wholly-owned subsidiary of SEAC. Prior to the consummation of the Business Combination described herein, New SEAC intends to effect a deregistration pursuant to and in accordance with Sections 206 through 209 of the Companies Act and a continuation and domestication as a British Columbia company in accordance with the BC Act, pursuant to which jurisdiction of incorporation of New SEAC will be changed from the Cayman Islands to British Columbia, Canada. In connection with the Business Combination, New SEAC (which we refer to as Pubco following the Business Combination) intends to change its name to Lionsgate Studios Corp.

MergerCo

MergerCo is SEAC MergerCo, a Cayman Islands exempted company and a wholly-owned subsidiary of New SEAC.

New BC Sub

New BC Sub is 1455941 B.C. Unlimited Liability Company, a British Columbia unlimited liability company and a wholly-owned subsidiary of SEAC.

Lions Gate Parent

Lions Gate Parent, or Lionsgate, is Lions Gate Entertainment Corp., a British Columbia corporation. Lions Gate Parent was incorporated under the Canada Business Corporations Act using the name 3369382 Canada Limited

10

Table of Contents

on April 28, 1997, amended its articles on July 3, 1997 to change its name to Lions Gate Entertainment Corp., and on September 24, 1997, continued under the Business Corporations Act (British Columbia).

Lions Gate Parent, and its Studio Business, encompasses a world-class motion picture and television studio operations, designed to bring a unique and varied portfolio of entertainment to consumers around the world. Its film, television and location-based entertainment businesses are backed by a more than 20,000-title library and a valuable collection of iconic film and television franchises.

Lions Gate Parent’s securities are traded on the New York Stock Exchange under the ticker symbols “LGF.A” and “LGF.B”.

The mailing address of Lions Gate Parent’s principal executive office is 2700 Colorado Avenue, Santa Monica, CA 90404, and its telephone number is (310) 449-9200. Lions Gate Parent’s head office address is located at 250 Howe Street, 20th Floor, Vancouver, British Columbia V6C 3R8.

Studio HoldCo

Studio HoldCo is LG Sirius Holdings ULC, a British Columbia unlimited liability company and a wholly owned subsidiary of Lions Gate Parent.

StudioCo

StudioCo is LG Orion Holdings ULC, a British Columbia unlimited liability company and a wholly-owned subsidiary of Lions Gate Parent. StudioCo exists for the purpose of holding Lions Gate Parent’s Studio Business and amalgamating with New SEAC in connection with the transactions described in this prospectus. Prior to the contribution of the Studio Business to StudioCo by Lions Gate Parent, which will occur prior to the StudioCo Amalgamation, StudioCo will have no operations other than those incidental to the transactions contemplated in the Business Combination Agreement and the potential completion of one or more financing transactions as further described in this prospectus.

Following the completion of the LG Internal Restructuring and prior to the Closing, StudioCo shall, directly or indirectly, own the assets and assume the liabilities of the Studio Business, which we refer to as LG Studios. LG Studios encompasses world-class motion picture and television studio operations, designed to bring a unique and varied portfolio of entertainment to consumers around the world. LG Studios’ film, television and location-based entertainment businesses are backed by a more than 20,000-title library and a valuable collection of iconic film and television franchises. A digital age company driven by its entrepreneurial culture and commitment to innovation, the Lionsgate brand is synonymous with bold, original, relatable entertainment for audiences worldwide. LG Studios manages and reports its operating results through two reportable business segments: Motion Picture and Television Production. See the section entitled “Business of LG Studios and Certain Information About StudioCo” for more information.

The mailing address of StudioCo’s principal executive office is 2700 Colorado Avenue, Santa Monica, CA 90404, and its telephone number is (310) 449-9200.

The Business Combination

On December 22, 2023, SEAC, New SEAC, Lions Gate Parent, Studio HoldCo, StudioCo, MergerCo and New BC Sub, entered into the Business Combination Agreement, which was amended on April 11, 2024, pursuant to which, among other things and subject to the terms and conditions contained in the Business Combination Agreement and the Plan of Arrangement, (i) SEAC will merge with and into MergerCo with SEAC Merger

11

Table of Contents

Surviving Company as the resulting entity, (ii) SEAC Merger Surviving Company will distribute all of its assets lawfully available for distribution to New SEAC by way of a cash dividend, (iii) SEAC Merger Surviving Company will transfer by way of continuation from the Cayman Islands to British Columbia in accordance with the Companies Act and the BC Act and convert to a British Columbia unlimited liability company in accordance with the applicable provisions of the BC Act, (iv) New SEAC will transfer by way of continuation from the Cayman Islands to British Columbia in accordance with the Companies Act and continue as a British Columbia company in accordance with the applicable provisions of the BC Act, and (v) in pursuant to an arrangement under Division 5 of Part 9 of the BC Act (the “Arrangement”) and on the terms and subject to the conditions set forth in the Plan of Arrangement, (A) SEAC Merger Surviving Company and New BC Sub will amalgamate to form MergerCo Amalco, in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement, (B) New SEAC and MergerCo Amalco will amalgamate to form SEAC Amalco, in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement and (C) StudioCo and SEAC Amalco will amalgamate to form Pubco, in accordance with the terms of, and with the attributes and effects set out in, the Plan of Arrangement. The Arrangement is subject to the approval by the Court under the BC Act. Details regarding the terms and conditions of the Business Combination are contained in the Business Combination Agreement.

If the Business Combination Agreement and the SEAC Merger are approved and adopted and the Business Combination is consummated, New SEAC will effect a deregistration pursuant to and in accordance with Sections 206 through 209 of the Cayman Islands Companies Act (as revised) and a continuation and domestication as a British Columbia company in accordance with the Business Corporations Act (British Columbia), pursuant to which the New SEAC’s jurisdiction of incorporation will be changed from the Cayman Islands to British Columbia, Canada. In connection with the Business Combination, New SEAC intends to change its name to Lionsgate Studios Corp.

12

Table of Contents

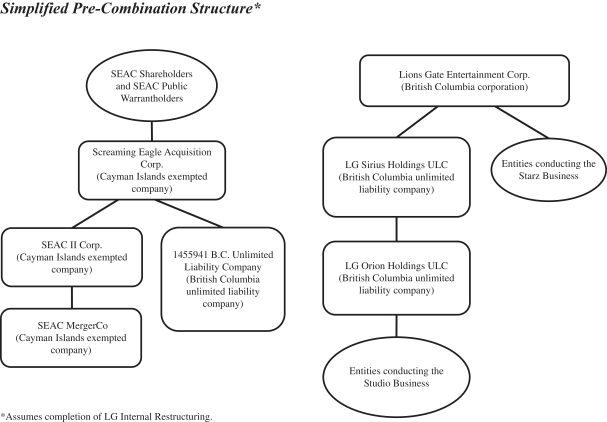

Structure of the Business Combination

The following diagram illustrates the organizational structure of SEAC and LG Studios immediately prior to the Business Combination:

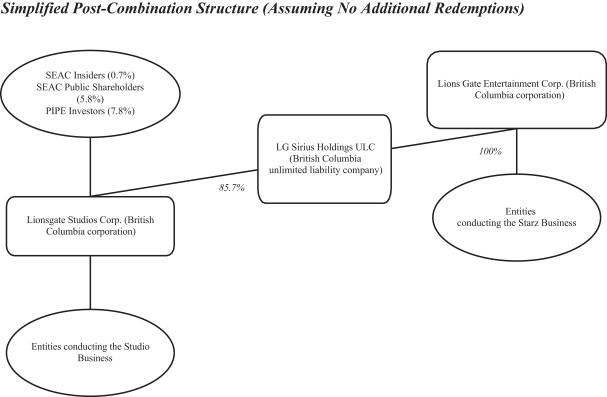

The following diagram illustrates the structure of Pubco immediately following the Business Combination. The percentages shown reflect the voting power and economic interests in Pubco on a combined basis, assuming no additional redemptions. Interests shown exclude any Pubco Common Shares that may be issuable to SEAC Sponsor upon vesting of the Pubco Sponsor Options after the Closing. Please see the subsection entitled “Ownership of Pubco Common Shares After Closing” for additional assumptions used in calculating such percentages.

13

Table of Contents

14

Table of Contents

The Private Placement

Concurrently with the execution of the Business Combination Agreement and on April 11, 2024, SEAC, New SEAC and Lions Gate Parent entered into subscription agreements with the PIPE Investors pursuant to which the PIPE Investors have agreed, subject to the terms and conditions set forth therein, to subscribe for and purchase from Pubco, immediately following the Amalgamations, an aggregate of approximately 23,091,217 PIPE Shares, at a purchase price of $9.63 per share and $10.165 per share, respectively, for an aggregate cash amount of $225,000,000. Additionally, the Subscription Agreements provide certain PIPE Investors with certain reduction rights, pursuant to which the PIPE Investors may offset their total commitments under their respective Subscription Agreements to the extent such PIPE Investors purchase SEAC Class A Ordinary Shares in the open market or otherwise own such shares as of the date of the Subscription Agreement, for up to an additional 2,018,951 PIPE Shares that may be issued to PIPE Investors who exercise such reduction rights.

Stock Exchange Listing

Listing of Pubco Common Shares on Nasdaq

New SEAC will apply to have the Pubco Common Shares listed on Nasdaq. Listing is subject to the approval of Nasdaq, respectively, in accordance with their respective original listing requirements. There is no assurance that Nasdaq will approve Pubco’s listing applications. Any such listing of the Pubco Common Shares will be conditional upon Pubco fulfilling all of the listing requirements and conditions of Nasdaq. It is anticipated that upon the Closing the Pubco Common Shares will be listed on Nasdaq under the ticker symbol “LION”.

Delisting of SEAC Securities and Deregistration of SEAC

SEAC and Lions Gate Parent anticipate that, following consummation of the Business Combination, the SEAC Class A Ordinary Shares, SEAC Units and SEAC Warrants will be delisted from Nasdaq, and SEAC will be deregistered under the Exchange Act.

Summary of Risk Factors

Investing in our securities involves risks. You should carefully consider the risks described in “Risk Factors” beginning on page 22 before making a decision to invest in Pubco Common Shares. If any of these risks actually occurs, our business, financial condition and results of operations would likely be materially adversely affected. Some of the risks related to Pubco and StudioCo’s business and industry and the Business Combination are summarized below.

Risks Related to the Studio Business

| • | LG Studios faces substantial capital requirements and financial risks. |

| • | LG Studios may incur significant write-offs if its projects do not perform well enough to recoup costs. |

| • | Changes in LG Studios’ business strategy, plans for growth or restructuring may increase its costs or otherwise affect its profitability. |

| • | LG Studios’ revenues and results of operations may fluctuate significantly. |

| • | LG Studios’ content licensing arrangements, primarily those relating to the distribution of films in foreign territories, may include minimum guarantee arrangements which, absent such arrangements, could adversely affect our results of operations. |

15

Table of Contents

| • | The Studio Business does not have long-term arrangements with many of its production or co- financing partners. |

| • | The Studio Business relies on a few major retailers and distributors and the loss of any of those could reduce its revenues and operating results. |

| • | A significant portion of the Studio Business’ library revenues comes from a small number of titles. |

| • | Changes in consumer behavior, as well as evolving technologies and distribution models, may negatively affect LG Studios’ business, financial condition or results of operations. |

| • | LG Studios expects to face substantial competition in all aspects of its business. |

| • | LG Studios faces economic, political, regulatory, and other risks from doing business internationally. |

| • | LG Studios will be subject to risks associated with possible acquisitions, dispositions, business combinations, or joint ventures. |

| • | If Entertainment One Canada Ltd. loses Canadian status, it could lose licenses, incentives and tax credits. |

| • | Lions Gate Parent may fail to realize the anticipated benefits of the acquisition of eOne. |

| • | LG Studios’ success will depend on attracting and retaining key personnel and artistic talent. |

| • | Global economic turmoil and regional economic conditions could adversely affect LG Studios’ business. |

| • | LG Studios could be adversely affected by labor disputes, strikes or other union job actions. |

| • | Business interruptions from circumstances or events out of LG Studios’ control could adversely affect LG Studios’ operations. |

| • | LG Studios’ business is dependent on the maintenance and protection of its intellectual property and pursuing and defending against intellectual property claims may have a material adverse effect on LG Studios’ business. |

| • | The Studio Business involves risks of liability claims for content of material, which could adversely affect LG Studios’ business, results of operations and financial condition. |

| • | Piracy of films and television programs could adversely affect LG Studios’ business over time. |

| • | LG Studios may rely upon “cloud” computing services to operate certain aspects of its service and any disruption of or interference with its use of its “cloud” computing servicer could impact its operations and its business could be adversely impacted. |

| • | LG Studios’ activities are subject to stringent and evolving obligations which may adversely impact its operations. LG Studios’ actual or perceived failure to comply with such obligations could lead to regulatory investigations or actions, litigation, fines and penalties, disruptions of its business operations, reputational harm, loss of revenue or profits, loss of customers or sales, and other adverse business consequences. |

| • | Service disruptions or failures of LG Studios or its third-party service providers’ information systems may disrupt its businesses, damage its reputation, expose it to regulatory investigations, actions, litigation, fines and penalties or have a negative impact on its results of operations including but not limited to a loss of revenue or profit, loss of customers or sales and other adverse consequences. |

| • | LG Studios may incur debt obligations that could adversely affect its business and profitability and its ability to meet other obligations. |

16

Table of Contents

| • | The terms of the Lions Gate Parent Credit Agreement (as defined below) and the Lions Gate Parent Indenture (as defined below) restrict LG Studios’ current and future operations, particularly LG Studios’ ability to respond to changes or to take certain actions. |

| • | The U.S. Internal Revenue Service may not agree that Pubco should be treated as a non-U.S. corporation for U.S. federal tax purposes and may not agree that its U.S. affiliates should not be subject to certain adverse U.S. federal income tax rules. |

| • | Future changes to U.S. and non-U.S. tax laws could adversely affect Pubco. |

| • | Changes in foreign, state and local tax incentives may increase the cost of original programming content to such an extent that they are no longer feasible. |

| • | Pubco’s tax rate is uncertain and may vary from expectations. |

| • | Legislative or other governmental action in the U.S. could adversely affect Pubco’s business. |

| • | Changes in, or interpretations of, tax rules and regulations, and changes in geographic operating results, may adversely affect Pubco’s effective tax rates. |

Risks Related to Ownership of Pubco’s Securities

| • | Pubco cannot be certain that an active trading market for its common shares will develop or be sustained after the Business Combination, and following the completion of the Business Combination, its share price may fluctuate significantly as a result of numerous factors beyond Pubco’s control. |

| • | Pubco does not expect to pay any cash dividends for the foreseeable future. |

| • | If securities or industry analysts do not publish research or publish misleading or unfavorable research about Pubco’s business, Pubco’s share price and trading volume could decline. |

| • | Upon consummation of the Business Combination, the rights and obligations of a Pubco shareholder will be governed by British Columbia law and may differ from the rights and obligations of shareholders of companies organized under the laws of other jurisdictions. |

Controlled Company Exemption

Following the completion of the Business Combination, Lions Gate Parent will control a majority of the voting power of the outstanding Pubco Common Shares. As a result, Pubco will be a “controlled company” within the meaning of the Nasdaq rules, and Pubco may qualify for and rely on exemptions from certain corporate governance requirements. Under Nasdaq corporate governance standards, a company of which more than 50% of the voting power for the election of directors is held by an individual, a group or another company is a “controlled company” and may elect not to comply with certain corporate governance requirements, including the requirements to:

| • | have a board that includes a majority of “independent directors”, as defined under Nasdaq rules; |

| • | have a compensation committee of the board that is comprised entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; and |

| • | have independent director oversight of director nominations. |

17

Table of Contents

Pubco may rely on the exemption from having a board that includes a majority of “independent directors” as defined under Nasdaq rules. Pubco may elect to rely on additional exemptions and it will be entitled to do so for as long as Pubco is considered a “controlled company”, and to the extent it relies on one or more of these exemptions, holders of Pubco Common Shares will not have the same protections afforded to shareholders of companies that are subject to all of the Nasdaq corporate governance requirements.

18

Table of Contents

| Issuer |

SEAC II Corp. |

| In connection with and prior to the consummation of the Business Combination, New SEAC will effect a deregistration pursuant to and in accordance with Sections 206 through 209 of the Cayman Islands Companies Act (as revised) and a continuation and domestication as a British Columbia company in accordance with the Business Corporations Act (British Columbia), pursuant to which the New SEAC’s jurisdiction of incorporation will be changed from the Cayman Islands to British Columbia, Canada. In connection with the Business Combination, the New SEAC intends to change its name to Lionsgate Studios Corp. If the Business Combination is not consummated, the Pubco Common Shares registered pursuant to this prospectus will not be issued. |

| Pubco Common Shares offered by the Selling Shareholders |

Up to 25,110,168 shares of Pubco Common Shares, which include 23,091,217 PIPE Shares that are expected to be issued immediately following the Amalgamations and prior to the consummation of the Business Combination pursuant to the terms of the Subscription Agreements, an additional 2,018,951 PIPE Shares that may be issued to PIPE Investors who exercise reduction rights, which we refer to herein as “Newly Issued Reduction Right Shares.” |

| SEAC Ordinary Shares outstanding prior to the consummation of the Business Combination |

35,925,223 Ordinary Shares issued and outstanding in the aggregate as of April 22, 2024. Of these 35,925,223 Ordinary Shares, 17,175,223 were SEAC Class A Ordinary Shares and 18,750,000 were SEAC Class B Ordinary Shares. |

| Pubco Common Shares outstanding after the consummation of the Business Combination |

295,712,234 Pubco Common Shares under the No Redemption Scenario and 290,181,042 Pubco Common Shares under the Maximum Redemptions Scenario issued and outstanding after the Closing, which amounts exclude any additional shares that may be issued to PIPE Investors who exercise their reduction rights. |

| Use of proceeds |

We will not receive any of the proceeds from the sale of the Pubco Common Shares by the Selling Shareholders. |

| Market for SEAC Class A ordinary shares and Pubco Common Shares |

SEAC Class A Ordinary Shares, SEAC’s units and SEAC Public Warrants are currently traded on Nasdaq under the ticker symbols “SCRM”, “SCRMU” and “SCRMW,” respectively. We intend to list the Pubco Common Shares on Nasdaq under the ticker symbol “LION” upon the Closing. Pubco will not have units or warrants traded. |

19

Table of Contents

| Risk factors |

Any investment in the securities offered hereby is speculative and involves a high degree of risk. You should carefully consider the information set forth under “Risk Factors” and elsewhere in this prospectus. |

20

Table of Contents

An investment in our securities involves a high degree of risk. You should carefully consider the following risk factors, together with all of the other information included in this prospectus, before making an investment decision. Our business, prospects, financial condition or operating results could decline due to any of these risks and, as a result, you may lose all or part of your investment.

Risks Related to the Studio Business

LG Studios faces substantial capital requirements and financial risks.

The production, acquisition and distribution of motion picture and television content requires substantial capital. A significant amount of time may elapse between expenditure of funds and the receipt of revenues after release or distribution of such content. LG Studios cannot assure you that it is able to successfully implement arrangements to reduce the risks of production exposure such as tax credit, government or industry programs. Additionally, LG Studios may experience delays and increased costs due to disruptions or events beyond its control and if production incurs substantial budget overruns, LG Studios may have to seek additional financing or fund the overrun itself. LG Studios cannot make assurances regarding the availability of such additional financing on terms acceptable to it, or that it will recoup these costs. Increased costs or budget overruns incurred with respect to a particular film may prevent its completion of release, or may result in a delayed release and the postponement to a potentially less favorable date. This could adversely affect box office performance, and the overall financial success of such film. Any of the foregoing could have a material adverse effect on LG Studios’ business, financial condition, operating results, liquidity and prospects.

LG Studios may incur significant write-offs if its projects do not perform well enough to recoup costs.

LG Studios will be required to amortize capitalized production costs over the expected revenue streams as it recognizes revenue from films or other projects. The amount of production costs that will be amortized each quarter depends on, among other things, how much future revenue LG Studios expects to receive from each project. Unamortized production costs are evaluated for impairment each reporting period on a project-by-project basis when events or changes in circumstances indicate that the fair value of a film is less than its unamortized cost. These events and changes in circumstances include, among others, an adverse change in the expected performance of a film prior to its release, actual costs substantially in excess of budgeted cost for the film, delays or changes in release plans and actual performance subsequent to the film’s release being less than previously expected performance estimates. In any given quarter, if LG Studios lowers its previous forecast with respect to total anticipated revenue from any film or other project or increases its previous forecast of cost of making or distribution of the film, LG Studios may be required to accelerate amortization or record impairment charges with respect to the unamortized costs, even if it previously recorded impairment charges for such film or other project. Such impairment charges could adversely impact the business, operating results and financial condition.

Changes in LG Studios’ business strategy, plans for growth or restructuring may increase its costs or otherwise affect its profitability.

As changes in LG Studios’ business environment occur, it may adjust its business strategies to meet these changes, which may include growing a particular area of business or restructuring a particular business or asset. In addition, external events including changing technology, changing consumer patterns, acceptance of its theatrical offerings and changes in macroeconomic conditions may impair the value of its assets. When these occur, LG Studios may incur costs to adjust its business strategy and may need to write down the value of assets. LG Studios may also invest in existing or new businesses. Some of these investments may have negative or low short-term returns and the ultimate prospects of the businesses may be uncertain or may not develop at a rate that supports its level of investment. In any of these events, LG Studios’ costs may increase, it may have significant charges associated with the write-down of assets, or returns on new investments may be lower than prior to the change in strategy, plans for growth or restructuring.

21

Table of Contents

LG Studios’ revenues and results of operations may fluctuate significantly.

LG Studios’ results of operations will depend significantly upon the commercial success of the motion picture, television and other content that it sells, licenses or distributes, which cannot be predicted with certainty. In particular, if one or more motion pictures underperform at the box office in any given period, its revenue and earnings results for that period (and potentially, subsequent periods) may be less than anticipated. LG Studios’ results of operations may also fluctuate due to the timing, mix, number and availability of theatrical motion picture and home entertainment releases, as well as license periods for content. Moreover, low ratings for television programming produced by LG Studios may lead to the cancellation of a program which may result in significant programming impairment charges in a given period, and can negatively affect license fees for the cancelled program in future periods. Other than non-renewals or cancellation of television programs or series that may occur from time to time, Lions Gate Parent is not aware of any current material cancellation of television programming releases or of content that it sells, licenses or distributes. In addition, the comparability of results may be affected by changes in accounting guidance or changes in LG Studios’ ownership of certain assets and businesses. As a result of the factors above, LG Studios’ results of operations may fluctuate and differ from period to period, and therefore, may not be indicative of the results for any future periods or directly comparable to prior reporting periods.

LG Studios’ content licensing arrangements, primarily those relating to the distribution of films in foreign territories, may include minimum guarantee arrangements which, absent such arrangements, could adversely affect our results of operations.

LG Studios generates revenue principally from the licensing of content in domestic theatrical exhibition, home entertainment (e.g., digital media and packaged media), television, and international market places. Certain of such content licensing arrangements, primarily those relating to the distribution of films by third parties in foreign territories, may include a minimum guarantee. Revenue from these minimum guarantee arrangements amounted to approximately $101.3 million, $51.1 million and $29.8 million for the years ended March 31, 2023, 2022 and 2021 respectively, and $100.0 million and $29.6 million for the nine months ended December 31, 2023 and 2022, respectively.