UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One) | |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended | |

OR | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission file number

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Chief Executive Officer

E-mail:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer ☐ | Non-accelerated filer ☐ | |

Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

TABLE OF CONTENTS

Page | ||

ii | ||

ii | ||

ii | ||

iv | ||

v | ||

1 | ||

1 | ||

1 | ||

25 | ||

50 | ||

50 | ||

67 | ||

76 | ||

77 | ||

79 | ||

79 | ||

85 | ||

86 | ||

87 | ||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 87 | |

87 | ||

88 | ||

88 | ||

88 | ||

89 | ||

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 89 | |

89 | ||

89 | ||

90 | ||

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | 90 | |

90 | ||

90 | ||

91 | ||

91 | ||

91 | ||

MANCHESTER UNITED PLC GROUP HISTORICAL FINANCIAL INFORMATION | ||

i

GENERAL INFORMATION

In this annual report on Form 20-F (“Annual Report”), references to “Manchester United,” “the Company,” “our Company,” “our business,” “we,” “us” and “our” are, as the context requires, to Manchester United plc together with its consolidated subsidiaries as a consolidated entity.

Throughout this Form 20-F, we refer to the following football leagues and cups:

| ● | the English Premier League (the “Premier League”); |

| ● | the Emirates FA Cup (the “FA Cup”); |

| ● | the English Football League Cup (the “EFL Cup”); |

| ● | the Union of European Football Associations Champions League (the “Champions League”); |

| ● | the Union of European Football Associations Europa League (the “Europa League”); and |

| ● | the Union of European Football Associations Europa Conference League (the “Europa Conference League”). |

The term “Matchday” refers to all domestic and European football match day activities from Manchester United men’s games at Old Trafford, the Manchester United football stadium, along with receipts for domestic cup (such as the EFL Cup and the FA Cup) games not played at Old Trafford plus receipts from Manchester United women’s home games. Fees for arranging other events at the stadium are also included as Matchday revenue.

PRESENTATION OF FINANCIAL AND OTHER DATA

We report under International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (the “IASB”), and IFRS Interpretations Committee interpretations. None of the financial statements were prepared in accordance with generally accepted accounting principles in the United States.

All references in this Annual Report to (i) “pounds sterling,” “pence,” “p” or “£” are to the currency of the United Kingdom, (ii) “US dollar,” “USD” or “$” are to the currency of the United States, and (iii) “Euro” or “€” are to the currency introduced at the start of the third stage of European economic and monetary union pursuant to the treaty establishing the European Community, as amended.

FORWARD-LOOKING STATEMENTS

This Annual Report contains estimates and forward-looking statements. Our estimates and forward-looking statements are mainly based on our current expectations and estimates of future events and trends, which affect or may affect our businesses and operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to numerous risks and uncertainties and are made in light of information currently available to us. Many important factors, in addition to the factors described in this Annual Report, may adversely affect our results as indicated in forward-looking statements. You should read this Annual Report completely and with the understanding that our actual future results may be materially different and worse from what we expect.

All statements other than statements of historical fact are forward-looking statements. The words “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “seek,” “believe,” “estimate,” “predict,” “potential,” “continue,” “contemplate,” “possible” and similar words are intended to identify estimates and forward-looking statements.

Our estimates and forward-looking statements may be influenced by various factors, including without limitation:

| ● | the effect of adverse economic conditions on our operations; |

| ● | maintaining, enhancing and protecting our brand and reputation in order to expand our follower and sponsorship base; |

| ● | our ability to attract and retain key personnel, including players; |

| ● | our dependence on the performance and popularity of our men’s first team; |

| ● | our ability to renew or replace key commercial agreements on similar or better terms or attract new sponsors; |

| ● | the negotiation, pricing and terms of key media contracts, which are outside of our control; |

| ● | our reliance on European competitions as a source of future income; |

| ● | the impact of the United Kingdom’s exit from the European Union (the “EU”) on the movement of players or other regulations; |

| ● | our dependence on relationships with certain third parties; |

ii

| ● | our relationship with merchandising, licensing, sponsor and other commercial partners; |

| ● | our exposure to credit related losses in connection with key media, commercial and transfer contracts; |

| ● | our dependence on Matchday revenue; |

| ● | our exposure to competition, both in football and the various commercial markets in which we do business; |

| ● | our ability to protect ourselves from and resolve and remediate cyber-attacks and data breaches on our IT systems; |

| ● | actions taken by other Premier League clubs that are contrary to our interests; |

| ● | our relationship with the various leagues to which we belong and the application of their respective rules and regulations; |

| ● | our ability to execute a digital media strategy that generates the revenue we anticipate; |

| ● | the impact resulting from serious injuries or losses of the playing staff; |

| ● | our ability to maintain, train and build an effective international sales and marketing infrastructure, and manage the risks associated with such an expansion; |

| ● | uncertainty with regard to exchange rates, our tax rate and our cash flow; |

| ● | brand impairments resulting from failures to adequately protect our intellectual property and curbing sales of counterfeit merchandise; |

| ● | our ability to adequately protect against media piracy and identity theft of our followers’ account information; |

| ● | our exposure to the effects of seasonality in our business; |

| ● | maintaining our match attendance at Old Trafford; |

| ● | any natural disasters, terrorist incidents or other events beyond our control, such as a pandemic, epidemic or outbreak of an infectious disease, that adversely affect our operations; |

| ● | the effect of our indebtedness on our financial health and competitive position; |

| ● | estimates and estimate methodologies used in preparing our consolidated financial statements; and |

| ● | the future trading prices of our Class A ordinary shares and the impact of securities analysts’ reports on these prices. |

Other sections of this Annual Report include additional factors that could adversely impact our business and financial performance, principally “Item 3. Key Information — D. Risk Factors.” Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Therefore, you are cautioned not to place undue reliance on these forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements contained in this Annual Report, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

iii

MARKET AND INDUSTRY DATA

This Annual Report contains industry, market, and competitive position data that are based on the industry publications and studies conducted by third parties listed below as well as our own internal estimates and research. These industry publications and third-party studies generally state that the information that they contain has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that each of these publications and third-party studies is reliable, we have not independently verified the market and industry data obtained from these third-party sources. While we believe our internal research is reliable and the definition of our market and industry are appropriate, neither such research nor these definitions have been verified by any independent source.

References to our “1.1 billion fans and followers” are based on the Survey commissioned by us, conducted by Kantar Media (Media Division of Kantar and division of WPP plc) (“Kantar”) in 2019, and paid for by us. As in the Survey conducted by Kantar, we defined the term “fans” as those individuals who answered survey questions, unprompted, with the answer that Manchester United was their favorite football team in the world and the term “followers” as those individuals who answered survey questions, unprompted, with the answer that Manchester United is a football team that they proactively follow in addition to their favorite football team. For example, we directed Kantar to include in the definition of “follower” a respondent who watched live Manchester United matches, followed highlights coverage or read or talked about Manchester United regularly.

The Survey was conducted during the first six months of 2019 and included over 54,000 respondents across 39 countries. It repeated a similar 2011 survey, also conducted by Kantar, to ensure comparability of approach, methodology and results. The Survey included questions on:

| ● | demographics, age, gender and socio-economic background; |

| ● | viewership of Manchester United matches, social media following and engagement; |

| ● | relationship, awareness and attitudes to commercial partners; and |

| ● | interest in Manchester United products, including merchandise. |

The Survey indicated that Manchester United has 1.1 billion combined fans and followers worldwide, comprised of 467 million fans and 635 million followers (compared to 277 million and 382 million, respectively, in 2011), including:

| ● | a total of 731.7 million fans and followers in the Asia Pacific region (compared to 324.7 million in 2011); |

| ● | a total of 296.1 million fans and followers in Europe, the Middle East and Africa (compared to 262.9 million in 2011); and |

| ● | a total of 74 million fans and followers in the Americas (compared to 71.7 million in 2011). |

We expect there to be differences in the level of engagement with our brand between “followers” and “fans”, as defined in the Survey. We have not identified any practical way to measure these differences in consumer behavior and any references to our fans and followers should be viewed in that light.

To calculate the number of fans and followers from the approximately 54,000 responses, Kantar applied assumptions based on third-party data sets covering certain factors including population size, country specific characteristics such as wealth and GDP per capita, and affinity for sports and media penetration. Kantar then extrapolated the results to the rest of the world, representing an extrapolated adult population of 5 billion people. However, while Kantar believes the extrapolation methodology was robust and consistent with consumer research practices, as with all surveys, there are inherent limitations in extrapolating survey results to a larger population than those actually surveyed. As a result of these limitations, our number of followers and fans may be significantly less or significantly more than the extrapolated survey results. Kantar’s extrapolated results also accounted for non-internet users. To do so, Kantar had to make assumptions about the preferences and behaviors of non-internet users in those countries surveyed. For surveyed markets with especially low internet penetration, these assumptions reduced the number of our followers in those countries and there is no guarantee that the assumptions applied are accurate. Survey results also account only for claimed consumer behavior rather than actual consumer behavior and as a result, survey results may not reflect real consumer behavior with respect to football or the consumption of our content and products. The Survey indicates that the information that it contains has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that the survey results are reliable, we have not independently verified the data contained in the survey.

In addition to the Survey, this Annual Report references the following industry publications and third-party studies:

| ● | television viewership data compiled by futures sports + entertainment—Mediabrands International Limited for the 2022/23 season (the “Futures Data”); and |

| ● | a paper published by AT Kearney, Inc. in 2014 entitled “Winning in the Business of Sports” (“AT Kearney”). |

iv

SELECTED FINANCIAL DATA

We prepare our consolidated financial statements in accordance with IFRS as issued by the IASB. The selected consolidated financial data (including statement of profit or loss data, other data and balance sheet data) presented as of and for the years ended 30 June 2023, 2022, 2021, 2020 and 2019 has been derived from our audited consolidated financial statements and the notes thereto (our audited consolidated financial statements as of and for the years ended 30 June 2020 and 2019 are not included in this Annual Report). Our historical results for any prior period are not necessarily indicative of results expected in any future period.

The selected historical financial information presented in the tables below should be read in conjunction with, and is qualified in its entirety by reference to, our audited consolidated financial statements and accompanying notes. The audited consolidated financial statements and the accompanying notes as of 30 June 2023 and 2022 and for the years ended 30 June 2023, 2022 and 2021 have been included elsewhere in this Annual Report.

Unless otherwise specified, all financial information included in this Annual Report has been stated in pounds sterling.

Year ended 30 June | ||||||||||

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 | |

Statement of profit or loss data: | (£’000, unless otherwise indicated) | |||||||||

Revenue from contracts with customers (1) | 648,401 | 583,201 | 494,117 | 509,041 | 627,122 | |||||

Analyzed as: | ||||||||||

Commercial revenue | 302,886 | 257,820 | 232,205 | 279,044 | 275,093 | |||||

Broadcasting revenue |

| 209,095 |

| 214,847 |

| 254,815 |

| 140,203 |

| 241,210 |

Matchday revenue |

| 136,420 |

| 110,534 |

| 7,097 |

| 89,794 |

| 110,819 |

Operating expenses — before exceptional items |

| (681,117) |

| (667,828) |

| (538,424) |

| (522,204) |

| (583,337) |

Analyzed as: |

|

|

|

|

|

|

| |||

Employee benefit expenses |

| (331,374) |

| (384,141) |

| (322,600) |

| (284,029) |

| (332,356) |

Other operating expenses |

| (163,211) |

| (117,911) |

| (76,467) |

| (92,876) |

| (108,977) |

Depreciation and impairment |

| (13,848) |

| (14,314) |

| (14,959) |

| (18,543) |

| (12,850) |

Amortization |

| (172,684) |

| (151,462) |

| (124,398) |

| (126,756) |

| (129,154) |

Operating expenses — exceptional items |

| — |

| (24,692) |

| — |

| — |

| (19,599) |

Total operating expenses |

| (681,117) |

| (692,520) |

| (538,424) |

| (522,204) |

| (602,936) |

Other operating income | 1,112 | — | — | — | — | |||||

Operating (loss)/profit before profit on disposal of intangible assets |

| (36,104) |

| (109,319) |

| (44,307) |

| (13,163) |

| 24,186 |

Profit on disposal of intangible assets |

| 20,424 |

| 21,935 |

| 7,381 |

| 18,384 |

| 25,799 |

Operating (loss)/ profit |

| (11,180) |

| (87,384) |

| (36,926) |

| 5,221 |

| 49,985 |

Finance costs |

| (44,917) |

| (85,915) |

| (36,411) |

| (27,391) |

| (25,470) |

Finance income |

| 23,523 |

| 23,676 |

| 49,310 |

| 1,352 |

| 2,961 |

Net finance (costs)/income |

| (21,394) |

| (62,239) |

| 12,899 |

| (26,039) |

| (22,509) |

(Loss)/profit before income tax |

| (32,574) |

| (149,623) |

| (24,027) |

| (20,818) |

| 27,476 |

Income tax credit/(expense)(2) |

| 3,896 |

| 34,113 |

| (68,189) |

| (2,415) |

| (8,595) |

(Loss)/profit for the year(1)/(2) |

| (28,678) |

| (115,510) |

| (92,216) |

| (23,233) |

| 18,881 |

Weighted average number of ordinary shares (thousands) |

| 163,062 |

| 163,001 |

| 162,939 |

| 164,253 |

| 164,526 |

Diluted weighted average number of ordinary shares (thousands)(3) |

| 163,062 |

| 163,001 |

| 162,939 |

| 164,253 |

| 164,666 |

Basic (loss)/earnings per share (pence) (1)/(2) |

| (17.59) |

| (70.86) |

| (56.60) |

| (14.14) |

| 11.48 |

Diluted (loss)/earnings per share (pence) (1)/(2)/(3) |

| (17.59) |

| (70.86) |

| (56.60) |

| (14.14) |

| 11.47 |

| (1) | Revenue for the years ended 30 June 2021 and 30 June 2020 was significantly impacted by the novel coronavirus COVID-19 (“COVID-19”) pandemic and governmental measures to manage the spread of the disease. |

v

For the year ended 30 June 2021, the Old Trafford Stadium, Museum and Stadium Tour operations remained closed to visitors throughout the financial year until part way through the fourth fiscal quarter. In line with government guidelines, and with a variety of safety measures and protocols in place, including reduced fan capacity, Old Trafford Stadium welcomed back 10,000 supporters for the final home match of the season. All matches prior to this were played behind closed doors. Furthermore, the first team’s pre-season tour, scheduled for the start of fiscal 2021, had to be cancelled due to travel restrictions and the Old Trafford Megastore was closed for parts of the year due to government-imposed restrictions. The impact of the above is a reduction in Matchday and Commercial revenues for the year ended 30 June 2021. This was partially offset by increased Broadcasting revenues due to the men’s first team’s participation in the Union of European Football Association (“UEFA”) Champions League, strong performance in both the Premier League and the UEFA Europa League, and the impact of completing the 2019/20 domestic and UEFA competitions at the start of fiscal 2021 as well as a decrease in other operating expenses due to reduced business activity as a result of COVID-19. The Group did not rely on the government furlough scheme available during the COVID-19 pandemic. Accordingly, the above resulted in a loss for the year ended 30 June 2021 and basic and diluted loss per share.

For the year ended 30 June 2020, government-imposed restrictions resulted in the suspension of all Premier League, FA Cup and UEFA Europa League matches beginning 13 March 2020. The Premier League and FA Cup resumed in June 2020 and the UEFA Europa League resumed in August 2020. All remaining matches were played behind closed doors. The postponement resulted in the deferral of a number of matches, originally expected to be played in the financial year ended 30 June 2020, as well as the remaining matches being played behind closed doors, the impact of which was to reduce Broadcasting and Matchday revenues for the year ended 30 June 2020. Broadcasting revenue was further impacted by rebates due to broadcasters following disruption of the 2019/20 competitions. Further, Old Trafford and its flagship Megastore operations as well as Museum, Stadium Tour and Red Café operations were closed in mid-March 2020. The Old Trafford Megastore re-opened during June 2020 with a variety of safety measures in place in line with Government guidance. The stadium and Museum and Stadium Tour operations remained closed. This has been partially offset by a decrease in other operating expenses due to reduced business activity as a result of COVID-19. The Group did not rely on the government furlough scheme available during the COVID-19 pandemic. Accordingly, the above resulted in a loss for the year ended 30 June 2020 and basic and diluted loss per share.

vi

Year ended 30 June | ||||||||||

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 | |

Other data: | (£’000, unless otherwise indicated) | |||||||||

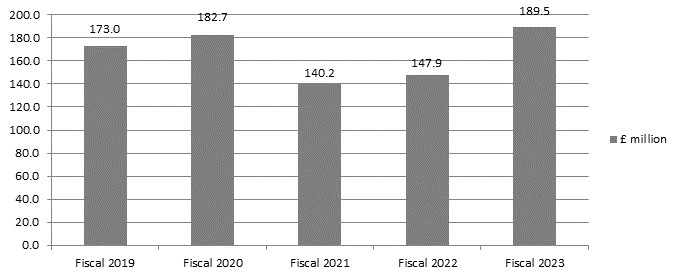

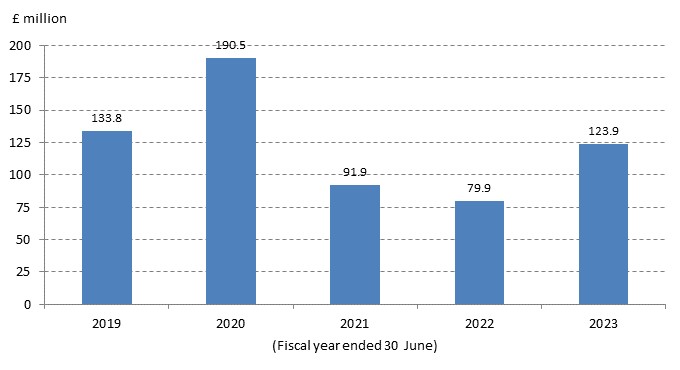

Commercial revenue | 302,886 | 257,820 | 232,205 | 279,044 | 275,093 | |||||

Analyzed as: |

|

| ||||||||

Sponsorship revenue | 189,496 |

| 147,881 |

| 140,209 |

| 182,709 |

| 173,010 | |

Retail, merchandising, apparel & products licensing revenue | 113,390 |

| 109,939 |

| 91,996 |

| 96,335 |

| 102,083 | |

|

| |||||||||

Dividends declared per share ($) | — |

| 0.27 |

| 0.09 |

| 0.18 |

| 0.18 | |

Dividends declared per share (£ equivalent) | — | 0.21 | 0.07 |

| 0.14 |

| 0.14 | |||

As of 30 June | ||||||||||

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 | |

Balance sheet data: | (£’000) | |||||||||

Cash and cash equivalents | 76,019 | 121,223 | 110,658 | 51,539 | 307,637 | |||||

Total assets |

| 1,317,944 |

| 1,293,665 | 1,260,310 |

| 1,383,466 |

| 1,496,525 | |

Total liabilities |

| 1,213,994 |

| 1,166,157 | 987,798 |

| 1,032,234 |

| 1,081,323 | |

Total equity |

| 103,950 |

| 127,508 | 272,512 |

| 351,232 |

| 415,202 | |

We define Adjusted EBITDA as (loss)/profit for the year before depreciation and impairment, amortization, profit on disposal of intangible assets, exceptional items, net finance costs/income, and tax. Adjusted EBITDA is a non-IFRS measure and not a uniformly or legally defined financial measure. Adjusted EBITDA is not a substitute for IFRS measures in assessing our overall financial performance. Because Adjusted EBITDA is not a measurement determined in accordance with IFRS, and is to varying calculations, Adjusted EBITDA may not be comparable to other similarly titled measures presented by other companies. Adjusted EBITDA is included in this Annual Report because it is a measure of our operating performance and we believe that Adjusted EBITDA is useful to investors because it is frequently used by securities analysts, investors and other interested parties in their evaluation of the operating performance of companies in industries similar to ours. We also believe Adjusted EBITDA is useful to our management and investors as a measure of comparative operating performance from year to year and among companies as it is reflective of changes in pricing decisions, cost controls and other factors that affect operating performance, and it removes the effect of our asset base (primarily depreciation, impairment and amortization), material volatile items (primarily profit on disposal of our intangible assets and exceptional items), capital structure (primarily finance costs/income), and items outside the control of our management (primarily taxes).

Our management also uses Adjusted EBITDA for planning purposes, including the preparation of our annual operating budget and financial projections. Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for an analysis of our results as reported under IFRS as issued by the IASB.

vii

The following is a reconciliation of (loss)/profit for the years presented to Adjusted EBITDA:

| Year ended 30 June | |||||||||

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 | |

(£’000) | ||||||||||

(Loss)/profit for the year | (28,678) |

| (115,510) |

| (92,216) |

| (23,233) |

| 18,881 | |

Adjustments: |

|

|

|

|

|

|

|

|

| |

Tax (credit)/expense | (3,896) |

| (34,113) |

| 68,189 |

| 2,415 |

| 8,595 | |

Net finance costs/(income) | 21,394 |

| 62,239 |

| (12,899) |

| 26,039 |

| 22,509 | |

Profit on disposal of intangible assets | (20,424) |

| (21,935) |

| (7,381) |

| (18,384) |

| (25,799) | |

Exceptional items(a) | — |

| 24,692 |

| — |

| — |

| 19,599 | |

Amortization | 172,684 |

| 151,462 |

| 124,398 |

| 126,756 |

| 129,154 | |

Depreciation and impairment | 13,848 |

| 14,314 |

| 14,959 |

| 18,543 |

| 12,850 | |

Adjusted EBITDA | 154,928 |

| 81,149 |

| 95,050 |

| 132,136 |

| 185,789 | |

| 2023 | 2022 | 2021 |

| 2020 |

| 2019 | |||||

2022/23 | 2021/22 | 2020/21 | 2019/20 | 2019/20 | 2018/19 | |||||||

Home games played(4): |

|

|

|

|

|

|

|

|

|

|

|

|

Premier League |

| 19 |

| 19 |

| 19 |

| 3 |

| 16 |

| 19 |

European Games |

| 6 |

| 4 |

| 7 |

| 1 |

| 4 |

| 5 |

Domestic Cups |

| 8 |

| 3 |

| 4 |

| — |

| 4 |

| 2 |

Away games played(4): |

|

|

|

|

|

|

|

|

|

|

|

|

Premier League |

| 19 |

| 19 |

| 19 |

| 3 |

| 16 |

| 19 |

European Games |

| 6 |

| 4 |

| 8 |

| 2 |

| 5 |

| 5 |

Domestic Cups |

| 4 |

| — |

| 4 |

| 1 |

| 6 |

| 3 |

Total games played(4): |

|

|

|

|

|

|

|

|

|

|

|

|

Premier League |

| 38 |

| 38 |

| 38 |

| 6 |

| 32 |

| 38 |

European Games |

| 12 |

| 8 |

| 15 |

| 3 |

| 9 |

| 10 |

Domestic Cups |

| 12 |

| 3 |

| 8 |

| 1 |

| 10 |

| 5 |

| (a) | See Notes 2.7 and 6 to our audited consolidated financial statements included elsewhere in this Annual Report for more information. |

| (4) | As a direct consequence of COVID-19, and the resulting government-imposed restrictions, all Premier League, FA Cup and UEFA Europa League matches were suspended beginning 13 March 2020. The Premier League and FA Cup resumed in June 2020 and completed in July 2020 and August 2020 respectively. The UEFA Europa League resumed and completed in August 2020. The temporary postponement of all competitions resulted in four home and six away matches relating to 2019/20 competitions being played at the start of the 2020/21 financial year. This includes three home and three away Premier League matches, the FA Cup semi-final, one Europa League home match and the Europa League single-leg quarter-final and semi-final. From June 2020 until mid-May 2021, all matches were played behind closed doors. The final home match of the 2020/21 season and the UEFA Europa League final were played with fans in attendance at a reduced capacity. All matches in the 2021/22 and 2022/23 season operated at full capacity. |

viii

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. | RESERVED |

B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

C. | REASONS FOR THE OFFER AND USE OF PROCEEDS |

Not applicable.

D. | RISK FACTORS |

Investment in our Class A ordinary shares involves a high degree of risk. We expect to be exposed to some or all of the risks described below in our future operations. Any of the risk factors described below, as well as additional risks of which we are not currently aware, could affect our business operations and have a material adverse effect on our business, results of operations, financial condition, cash flow and prospects and cause the value of our shares to decline. Moreover, if and to the extent that any of the risks described below materialize, they may occur in combination with other risks which would compound the adverse effect of such risks on our business, results of operations, financial condition, cash flow and prospects.

Risks Related to Our Business

If we are unable to maintain and enhance our brand and reputation, particularly in new markets, or if events occur that damage our brand and reputation, our ability to expand our follower base, sponsors, and commercial partners or to sell significant quantities of our products may be impaired.

The success of our business depends on the value and strength of our brand and reputation. Our brand and reputation are also integral to the implementation of our strategies for expanding our follower base, sponsors and commercial partners. To be successful in the future we believe we must preserve, grow and leverage the value of our brand across all of our revenue streams. For instance, we have in the past experienced, and we expect that in the future we will continue to receive, a high degree of media coverage. Unfavorable publicity regarding our men’s first team’s performance in league and cup competitions or their behavior off the field, our ability to attract and retain certain players and coaching staff or actions by or changes in our ownership, could negatively affect our brand and reputation. Failure to respond effectively to negative publicity could also further erode our brand and reputation. In addition, events in the football industry, even if unrelated to us, may negatively affect our brand or reputation. As a result, the size, engagement and loyalty of our follower base and the demand for our products may decline. Damage to our brand or reputation or loss of our followers’ commitment for any of these reasons could impair our ability to expand our follower base, sponsors and commercial partners or our ability to sell significant quantities of our products, which would result in decreased revenue across our revenue streams and have a material adverse effect on our business, results of operations, financial condition and cash flow, as well as require additional resources to rebuild our brand and reputation.

In addition, maintaining and enhancing our brand and reputation may require us to make substantial investments. We cannot assure you that such investments will be successful. Failure to successfully maintain and enhance the Manchester United brand or our reputation or excessive or unsuccessful expenses in connection with this effort could have a material adverse effect on our business, results of operations, financial condition and cash flow.

1

Our business is dependent upon our ability to attract and retain key personnel, including players.

We are highly dependent on members of our management, coaching staff and our players. Competition for talented players and staff is, and will continue to be, intense. Our ability to attract and retain the highest quality players for our men’s first team and youth academy, as well as coaching staff, is critical to our men’s first team’s success in league and cup competitions, increasing popularity and, consequently, critical to our business, results of operations, financial condition and cash flow. Our success and many achievements over the last twenty years does not necessarily mean that we will continue to be successful in the future, whether as a result of changes in player personnel, coaching staff or otherwise. A downturn in the performance of our men’s first team could adversely affect our ability to attract and retain coaches and players. Further, in 2020, the United Kingdom formally left the EU and as a result we are no longer able to rely on European regulations relating to the movement of players between the United Kingdom and the European Economic Area (“EEA”). See “—The departure of the United Kingdom from the European Union may adversely affect our operations and financial results.” In addition, our popularity in certain countries or regions may depend, at least in part, on fielding certain players from those countries or regions. While we enter into employment contracts with each of our key personnel with the aim of securing their services for the term of the contract, the retention of their services for the full term of the contract cannot be guaranteed due to possible contract disputes or approaches by other clubs. Our failure to attract and retain key personnel could have a negative impact on our ability to effectively manage and grow our business.

We are dependent upon the performance and popularity of our men’s first team.

Our revenue streams are driven by the performance and popularity of our men’s first team. Significant sources of our revenue are the result of historically strong performances in English domestic and European competitions, specifically the Premier League, the FA Cup, the EFL Cup, the Champions League and the Europa League. Our revenue varies significantly depending on our men’s first team’s participation and performance in these competitions. Our men’s first team’s performance can affect all four of our revenue streams:

| ● | sponsorship revenue through sponsorship relationships; |

| ● | retail, merchandising, apparel & product licensing revenue through product sales; |

| ● | Broadcasting revenue through the frequency of appearances, performance based share of league broadcasting revenue, Champions League/Europa League/Europa Conference League distributions and MUTV distribution through linear and digital platforms; and |

| ● | Matchday revenue through ticket sales. |

Our men’s first team currently plays in the Premier League, the top football league in England. Our performance in the Premier League directly affects, and a weak performance in the Premier League could adversely affect, our business, results of operations, financial condition and cash flow. For example, our revenue from the sale of products, media rights, tickets and hospitality would fall considerably if our men’s first team were relegated from, or otherwise ceased to play in, the Premier League, the Champions League, the Europa League or the Europa Conference League.

We cannot ensure that our men’s first team will be successful in the Premier League or in the other leagues and tournaments in which it plays. Relegation from the Premier League or a general decline in the success of our men’s first team, particularly in consecutive seasons, would negatively affect our ability to attract or retain talented players and coaching staff, as well as supporters, sponsors and other commercial partners, which would have a material adverse effect on our business, results of operations, financial condition and cash flow.

It may not be possible to renew or replace key commercial agreements on similar or better terms, or attract new sponsors.

Our Commercial revenue for each of the years ended 30 June 2023, 2022 and 2021 represented 46.7%, 44.2% and 47.0% of our total revenue, respectively. The substantial majority of our Commercial revenue is generated from commercial agreements with our sponsors, and these agreements have finite terms. When these contracts expire, we may not be able to renew or replace them with contracts on similar or better terms or at all. Our most important commercial contracts include contracts with global, regional and supplier sponsors representing industries including sportswear, remote connectivity software, blockchain, spirits, automotive, Wi-Fi, betting and kitchen and bathroom fixtures and generators, which typically have contract terms of two to five years.

If we fail to renew or replace these key commercial agreements on similar or better terms, we could experience a material reduction in our Commercial revenue. Such a reduction could have a material adverse effect on our overall revenue and our ability to continue to compete with the top football clubs in England and Europe.

2

As part of our business plan, we intend to continue to grow our commercial portfolio by developing and expanding our product categorized approach, which will include partnering with additional sponsors. We may not be able to successfully execute our business plan in promoting our brand to attract new sponsors. We cannot assure you that we will be successful in implementing our business plan or that our Commercial revenue will continue to grow at the same rate as it has in the past or at all. Any of these events could negatively affect our ability to achieve our development and commercialization goals, which could have a material adverse effect on our business, results of operations, financial condition and cash flow.

The underlying probability of being unable to renew or replace key contracts on similar or more favorable terms, or to partner with additional sponsors, has increased as economic pressures are felt across the global economy. As a result, there may be a shift in focus for the majority of companies in the short- to medium-term, as these companies reduce perceived “excess” spend on marketing in favor of protecting the operational and financial stability of the entity.

Negotiation, pricing and terms of key media contracts are outside of our control and those contracts may change in the future.

For each of the years ended 30 June 2023, 2022 and 2021, 83.4%, 65.3% and 67.5% of our Broadcasting revenue, respectively, was generated from the media rights for Premier League matches, and 13.7%, 31.4% and 29.0% of our Broadcasting revenue, respectively, was generated from the media rights for UEFA matches. Contracts for these media rights and certain other revenue for those competitions (both domestically and internationally) are negotiated collectively by the Premier League and UEFA respectively. We are not a party to the contracts negotiated by the Premier League and UEFA. Further, we do not participate in and therefore do not have any direct influence on the outcome of contract negotiations. As a result, we may be subject to media rights contracts with media distributors with whom we may not otherwise contract or media rights contracts that are not as favorable to us as we might otherwise be able to negotiate individually with media distributors. Furthermore, the limited number of media distributors bidding for Premier League and UEFA club competition media rights may result in reduced prices paid for those rights and, as a result, a decline in revenue received from media contracts.

In addition, although an agreement has been reached for the sale of Premier League broadcasting rights through the end of the 2024/25 football season and for the sale of UEFA club competition broadcasting rights through the end of the 2023/24 football season, future agreements may not maintain our current level of Broadcasting revenue.

Future intervention by the European Commission (“EC”), the Court of Justice of the European Union (“CJEU”), UK authorities, or other competent authorities and courts having jurisdiction may also have a negative effect on our revenue from media rights in the EEA. Enforcement of competition laws and changes to copyright regimes may require changes to sales models that could negatively affect the amount which copyright holders, such as the Premier League, are able to derive from the exploitation of rights within the EU. As a result, our Broadcasting revenue from the sale of those rights could decrease.

It is likely that there will be future regulatory intervention by the EC relating to the grant of exclusive licenses of content on a territorial basis within the EEA insofar as they prohibit or limit the cross-border provision by satellite or internet transmission of retail pay-TV services in response to unsolicited demand (so-called “passive sales”). In the cases of the Premier League & others vs. QC Leisure & Others / Karen Murphy vs. Media Protection Services, the CJEU ruled that EU free movement rules prevented enforcement of national laws to prevent importation and sale of decoding devices marketed in other Member States. The CJEU held further that EU competition rules prohibit any agreement designed to guarantee absolute territorial exclusivity by restricting passive sales within the EU (i.e. by obliging broadcasters not to meet unsolicited demand for decoding devices enabling access to the right holder’s protected subject-matter with a view to their use outside the territory covered by the license agreement).

3

Subsequently, in January 2014 the EC launched a competition investigation into exclusive licensing arrangements between US Studios and various platforms in Europe (the major platform in each of the five largest Member States). In July 2015, the EC issued a Statement of Objections in Case COMP/40023 – Cross-border access to pay-TV setting out its preliminary view that certain provisions in the license agreements between the studios and Sky UK would eliminate cross-border competition and constitute a violation of EU competition rules. According to the EC, these provisions require Sky UK to block or limit access to films through geo-blocking its online services or through its satellite pay-TV services to consumers outside of the United Kingdom and Ireland (and thus prevent Sky UK from responding to passive sales requests). The EC was carrying out parallel investigations into cross-border access to pay-TV services in France, Italy, Germany and Spain. Studios and platforms argue that EU law does not preclude enforcement of their copyright and that the restrictions are necessary to ensure adequate financing of content creation because content value varies considerably across Member States.

On 22 April 2016, the EC announced that Paramount had offered to settle the case by offering a series of commitments, including an undertaking not to enter into pay-TV agreements that prohibit their licensees from responding to passive sales requests. The commitments cover both linear pay-TV services and (when covered by the broadcaster’s licenses) subscription video-on-demand services. The EC accepted these commitments on 27 July 2016. On 8 December 2016, the French TV broadcaster Groupe Canal + brought an action seeking annulment of the EC’s decision to accept the commitments. On 12 December 2018, the EU General Court dismissed the appeal and upheld the EC decision as lawful in identifying competition concerns and finding the commitments suitable to resolve them. Shortly before and on the same and following day of the General Court’s judgment, Disney, NBC Universal, Sony Pictures, Warner Bros. and Sky also offered commitments, which the EC accepted on 7 March 2019 and closed the investigation. The commitments foresee that the restrictive clauses will not be applied nor re-introduced in the film licensing contracts, without prejudice to the studios’ rights under copyright law or the Portability Regulation.

On 20 December 2020, the CJEU overturned the General Court’s judgment of 12 December 2018; the CJEU found that the General Court had erred in law in its assessment of the proportionality of the adverse effects on the interests of third parties, such as Canal +, resulting from the EC acceptance of the commitments offered by Paramount. In particular, the CJEU considered that the General Court could not refer such contracting partners to the national courts in order to have their contractual rights enforced; national courts could not decide contrary to an EC decision by declaring the relevant clauses compatible or requiring an operator to breach its commitments which have been made binding by that decision. On 31 March 2021 the EC withdraw its decision of 7 March 2019 accepting the commitments by Sky and four Hollywood studios and closed the proceedings in the case. While these investigations had targeted film content, any future decision could be applicable to any pay-TV content, including sport.

In addition to this regulatory action, the EU as part of its Digital Single Market (“DSM”) strategy adopted on 8 June 2017 the Portability Regulation, which is designed to enable consumers to access their content services while travelling across Europe. The Portability Regulation became applicable in the EU on 1 April 20. The EU has also adopted a regulation on unjustified geo-blocking, which became applicable on 3 December 2018. Copyright protected content is excluded but the EC must review and report on the exclusion.

As part of the DSM initiative, the EC has also sought to modernize EU copyright rules to allow for wider access to online content across the EU, including by extending rights clearance mechanisms in the Satellite and Cable Directive. The EC published its proposal for a Regulation on Online Transmissions on 14 September 2016, which in particular contains the proposal that the country of origin principle be extended to online broadcast services. In practice, this would mean that licenses for simulcast and catch-up rights, for example, for the United Kingdom would be construed as covering the entire EEA (as long as the United Kingdom remains subject to EU law). The European Parliament and the Council subsequently turned the draft Regulation on Online Transmissions into a Directive, including substantial amendments limiting the country of origin principle. As a result, the country of origin principle will apply to radio broadcasts, but not to television broadcasts of sports events. In parallel, the revised Copyright Directive has inter alia strengthened the position of rights owners by making online platforms responsible for taking certain actions against user-uploaded content which violates copyright. Both Directives were adopted in April 2019. On 15 February 2023, the EC referred 11 Member States to the CJEU for failing to implement the Directives into national law including Bulgaria, Denmark, Finland, Latvia, Poland and Portugal.

In addition, also as part of the DSM initiative, the European Parliament and the Council adopted on 6 November 2018, a revision of the Audiovisual Media Services. This Directive applies to traditional TV broadcasters, with the revision inter alia extending the scope for some provisions to also cover video-sharing platforms. The revision has not affected Article 14 on the possibility of national measures ensuring the non-exclusive broadcast of events of major importance for society.

Finally, as part the DSM initiative and following stakeholder consultations, on 15 December 2020, the EC proposed two legislative initiatives to upgrade rules governing digital services in the EU: the Digital Services Act (“DSA”) and the Digital Markets Act

4

(“DMA”). The DSA seeks to update the rules concerning e-commerce, for instance, by providing for enforceable obligations and increased accountability rules for all digital services that connect consumers to goods, services, or content, in relation to, for example, users’ safety and trust, harmful/illegal online content, content moderation and removal, and advertisement targeting. These rules will be enforced by designated national competent authorities. The DMA, which will be enforced by the EC, seeks to address market imbalances associated with large online platforms acting as gatekeepers, defined under certain criteria (e.g., Facebook, Google, Apple or Amazon). To this end, the DMA foresees obligations on their daily operations, for example, by enabling transparency for advertisers, ensuring portability of data to end users and business users of the online platforms, including the provision of continuous and real time access to such data, ensuring interoperability with competing third-party software in certain cases, and prohibiting gatekeepers to block users from un-installing software or apps. The DMA entered into force on 1 November 2022 and became applicable on 2 May 2023. The EC will adopt the decisions designating gatekeepers and their covered services at the beginning of September 2023. The gatekeepers will then have 6 months to comply with the DMA (ETA: March 2023). The DSA entered into force on 16 November 2022 and the provisions will apply to all in-scope providers by 17 February 2024. The United Kingdom has introduced a new regulatory regime for the digital sector analogous to the DMA, which was enacted by the Digital Markets, Competition and Consumers Bill published on 25 April 2023. The regime will apply to providers of digital services designated as having ‘strategic market status’. The Bill could come into force in the autumn of 2023, at the earliest, which would mean that conduct requirements would kick in in Q2 2024.

European competitions cannot be relied upon as a source of income.

Qualification for the Champions League is largely dependent upon our men’s first team’s performance in the Premier League and, in some circumstances, the Champions League or Europa League in the previous season. Qualification for the Champions League cannot, therefore, be guaranteed. Failure to qualify for the Champions League would result in a material reduction in revenue for each season in which our men’s first team did not participate. To help mitigate this impact the majority of playing contracts for our men’s first team include step-ups in remuneration which are contingent on participation in the group stage of the Champions League. Inclusive of Broadcasting revenue, prize money and Matchday revenue, our combined Broadcasting and Matchday revenue related to European competitions was £37.5 million, £75.0 million and £73.8 million for each of the years ended 30 June 2023, 2022 and 2021, respectively. As a result of our men’s first team performance during the 2022/23 season, our men’s first team will participate in the 2023/24 Champions League.

In addition, our participation in the Champions League, Europa League or Europa Conference League may be influenced by other factors beyond our control. For example, the number of places in each European competition available to the clubs of each national football association in Europe can vary from year to year based on a ranking system. If the performance of English clubs in Europe declines, the number of places in each European competition available to English clubs may decline and it may be more difficult for our men’s first team to qualify for European competition in future seasons. Further, the rules governing qualification for European competitions (whether at the European or national level) may change and make it more difficult for our men’s first team to qualify for European competition in future seasons.

We are a founder member of the European Club Association (“ECA”), an independent organization set up to work with football governing bodies to protect and promote the interests of football clubs at the European level. In addition, UEFA Club Competitions SA (“UCC SA”) was established by UEFA to advise and make recommendations to UEFA on strategic business matters and opportunities concerning club competitions. Half of the administration board is appointed by UEFA and the other half by the ECA.

The current format of the Champions League is structured so that the top four clubs from the four top-ranked UEFA national associations (of which England is currently one) qualify automatically for the group stage of the Champions League. With respect to the financial distribution methodology, there is a four pillar system being starting fee, performance fees, market pool and individual club coefficient. The individual club coefficient is determined by reference to past performance in UEFA club competitions over a ten-year period with additional points for historical winners of UEFA club competitions.

In addition to the Champions League, UEFA host the UEFA Europa League and the UEFA Europa Conference League. The UEFA Europa Conference League (“Europa Conference League”), was introduced in 2021/22 and all three competitions are currently held with 32 teams competing. The winner of the Europa Conference League is entitled to enter the following season’s UEFA Europa League group stage, while the winner of the Europa League is entitled to enter the following season’s UEFA Champions League. The top four clubs from the four top-ranked UEFA national associations automatically qualify for the Champions League group stage. The team finishing in fifth position in the Premier League and the FA Cup winners qualify for the Europa League group stage, unless the FA Cup winners finish in positions one to five in the Premier League, in which case the team finishing in sixth position also qualifies for the Europa League group stage. The EFL Cup winners qualify for the Europa Conference League play-offs unless they have

5

already qualified for the Champions League or Europa League, in which case the team finishing in sixth position (or seventh position if the sixth has already qualified for the Champions League or Europa League) take their place.

In May 2022, UEFA announced a new format for the UEFA Champions League which will begin in the 2024/25 season. This format sees the introduction of a new league-style format, the number of participating teams increased from 32 to 36 and the number of Group Stage matches increased from 6 to 8. The new format provides scope for one more place for an English club in the competition dependent on the collective performance of clubs from that nation in the previous season. Two places in the competition will be allocated in this manner, one to each nation that performed best collectively in the preceding season. The new format will also see a change to the financial distribution methodology. Whilst exact details are yet to be confirmed, this will be a three pillar system being starting fee, performance fee and a new value fee which is a combination of market pool and club coefficient. The club coefficient will now be based on a five-year period, compared to a ten-year period under the current methodology.

Moreover, because of the prestige associated with participating in the European competitions, particularly the Champions League, failure to qualify for any European competition could negatively affect our ability to attract and retain talented players and coaching staff, as well as supporters, sponsors and other commercial partners. On 21 July 2023, we signed an extension to our agreement with adidas under which a £10 million deduction from the minimum annual guarantee is made for each season of non-Champions League qualification from 2025/26 to 2034/35. Any one or more of these events could have a material adverse effect on our business, results of operation, financial condition and cash flow.

Our business depends in part on relationships with certain third parties.

We consider the development of our commercial assets to be central to our ongoing business plan and a driver of future growth. For example, our current contract with adidas that began with the 2015/16 season provides them with certain global technical sponsorship and dual-branded licensing rights. While we expect to be able to continue to execute our business plan in the future with the support of adidas, we remain subject to these contractual provisions and our business plan could be negatively impacted by non-compliance or poor execution of our strategy by adidas. Further, any interruption in our ability to obtain the services of adidas or other third parties or deterioration in their performance could negatively impact this portion of our operations. Furthermore, if our arrangement with adidas is terminated or modified against our interest, we may not be able to find alternative solutions for this portion of our business on a timely basis or on terms favorable to us or at all.

In the future, we may enter into additional arrangements permitting third parties to use our brand and trademarks. The steps we take to carefully select our partners may not lead to successful arrangements. Our partners may fail to fulfill their obligations under their agreements or have interests that differ from or conflict with our own. For example, we are dependent on our sponsors and commercial partners to effectively implement quality controls over products using our brand and/or trademarks. The inability of such sponsors and commercial partners to meet our quality standards could negatively affect consumer confidence in the quality and value of our brand, which could result in lower product sales. Any one or more of these events could have a material adverse effect on our business, results of operation, financial condition and cash flow.

We are exposed to credit related losses in the event of non-performance by counterparties to Premier League and UEFA media contracts as well as our key commercial and transfer contracts.

We derive the substantial majority of our Broadcasting revenue from media contracts negotiated by the Premier League and UEFA with media distributors, and although the Premier League obtains guarantees to support certain of its media contracts, typically in the form of letters of credit issued by commercial banks, it remains our single largest credit exposure. We derive our Commercial and sponsorship revenue from certain corporate sponsors, including global, regional and supplier sponsors (which includes new businesses operating in emerging markets) in respect of which we may manage our credit risk by seeking advance payments, installments and/or bank guarantees where appropriate. The substantial majority of this revenue is derived from a limited number of sources. We are also exposed to other football clubs globally for the payment of transfer fees on players. Depending on the transaction, some of these fees are paid to us in installments. We try to manage our credit risk with respect to those clubs by requiring payments in advance or, in the case of payments on installment, requiring bank guarantees on such payments in certain circumstances. However, we cannot ensure these efforts will eliminate our credit exposure to other clubs. A change in credit quality at one of the media broadcasters for the Premier League or UEFA, one of our sponsors or a club to whom we have sold a player can increase the risk that such counterparty is unable or unwilling to pay amounts owed to us. The failure of a major television broadcaster for the Premier League or UEFA club competitions to pay outstanding amounts owed to its respective league or the failure of one of our key sponsors or a club to pay outstanding amounts owed to us could have a material adverse effect on our business, results of operations, financial condition and cash flow.

6

Matchday revenue from our supporters is a significant portion of overall revenue.

A significant amount of our revenue derives from ticket sales and other Matchday revenue for our men’s first team matches at Old Trafford and our share of gate receipts from domestic cup matches. In particular, the revenue generated from ticket sales and other Matchday revenue at Old Trafford will be highly dependent on the continued attendance at matches of our individual and corporate supporters as well as the number of home matches we play each season. During each of the 2022/23, 2021/22 and 2020/21 seasons, we played 33, 26 and 34 home matches respectively and our Matchday revenue was £136.4 million, £110.5 million and £7.1 million for the years ended 30 June 2023, 2022 and 2021, respectively. Matchday revenue for the year ended 30 June 2021 was significantly impacted by the COVID-19 pandemic with 33 of our 34 home matches being played behind closed doors. Fans were in attendance for the final home match of the season at a reduced capacity in line with government guidelines. All matches during the years ended 30 June 2023 and 30 June 2022 were played with Old Trafford operating at full capacity. Match attendance is influenced by a number of factors, some of which are partly or wholly outside of our control. These factors include the success of our men’s first team, broadcasting coverage and general economic conditions in the United Kingdom, which affect personal disposable income and corporate marketing and hospitality budgets. A reduction in Matchday attendance could have a material adverse effect on our Matchday revenue and our overall business, results of operations, financial condition and cash flow.

The markets in which we operate are highly competitive, both within Europe and internationally, and increased competition could cause our profitability to decline.

We face competition from other football clubs in England and Europe. In the Premier League, investment from wealthy team owners has led to teams with deep financial backing that are able to acquire top players and coaching staff, which could result in improved performance from those teams in domestic and European competitions. As the Premier League continues to grow in popularity, the interest of wealthy potential owners may increase, leading to additional clubs substantially improving their financial position. Competition from European clubs also remains strong. Despite the adoption of the UEFA Financial Sustainability regulations, a set of financial monitoring rules on clubs participating in the Champions League, Europa League and Europa Conference League and the Premier League Profitability and Sustainability Rules, a similar set of rules monitoring Premier League clubs, European and Premier League football clubs are spending substantial sums on transfer fees and player salaries. Competition from inside and outside the Premier League has led to higher salaries for our players as well as increased competition on the field. The increase in competition could result in our men’s first team finishing lower in the Premier League than we have in the past and jeopardizing our qualification for or results in European competitions. Competition within England could also cause our men’s first team to fail to advance in the FA Cup and EFL Cup.

In addition, from a commercial perspective, we actively compete across many different industries and within many different markets. We believe our primary sources of competition, both in Europe and internationally, include, but are not limited to:

| ● | other businesses seeking corporate sponsorships and commercial partners such as sports teams, other entertainment events and television and digital media outlets; |

| ● | providers of sports apparel and equipment seeking retail, merchandising, apparel & product licensing opportunities; |

| ● | digital content providers seeking consumer attention and leisure time, advertiser income and consumer e-commerce activity; |

| ● | other types of television programming seeking access to broadcasters and advertiser income; and |

| ● | alternative forms of corporate hospitality and live entertainment for the sale of Matchday tickets such as other live sports events, concerts, festivals, theater and similar events. |

All of the above forms of competition could have a material adverse effect on any of our four revenue streams and our overall business, results of operations, financial condition and cash flow.

A cyber-attack on, or disruption to, our IT systems or other systems utilized in our operations could compromise our operations, adversely impact our reputation and subject us to liability.

As a high-profile brand we are susceptible to the risk of a cyber-attack on our IT systems or other third-party systems utilized in our operations. We experience cyber-attacks and other security incidents of varying degrees from time to time. For example, we experienced such an attack in or about November 2020, which resulted in certain non-consumer data being compromised and the disruption of our enterprise systems and applications, prior to restoration of secure computing operations. In response, we have implemented controls and taken other preventative actions to strengthen our systems against such attacks. However, we cannot assure you that such measures will provide absolute security, that we will be able to react in a timely manner, or that our remediation efforts following any past or future attacks will be successful. A cyber-attack could disable the information technology systems we use or depend on to operate our business and give rise to the loss of significant amounts of personal data or other sensitive information,

7

potentially subjecting us to criminal or civil sanctions or other liability. See “—We are subject to governmental regulation and other legal obligations related to privacy, data protection, data security and safeguarding. Our actual or perceived failure to comply with such obligations could harm our business.” Similarly, any disruption to or failures in our IT systems or other third-party systems utilized in our operations could have an adverse impact on our ability to operate our business and lead to reputational damage. Any of these events could have a material adverse effect on our business, results of operations, financial condition and cash flow. Furthermore, as attempted attacks continue to evolve in scope and sophistication, we may incur significant costs in modifying or enhancing our IT security systems and processes in an attempt to defend against such attacks. There can be no assurance, however, that any security systems or processes we, or third party providers on which we rely, currently have in place or that may be implemented in the future will be successful in preventing or mitigating the harm from such attacks.

We are subject to special rules and regulations regarding insolvency and bankruptcy.

We are subject to, among other things, special insolvency or bankruptcy-related rules of the Premier League and the Football Association (the “FA”). Those rules empower the Premier League board to direct certain payments otherwise due to us to the FA and its members, associate members and affiliates, certain other English football leagues and certain other entities if it is reasonably satisfied that we have failed to pay certain creditors including other football clubs, the Premier League and the Football League.

If we experience financial difficulty, we could also face sanctions under the Premier League rules, including suspension from the Premier League, European competitions, the FA Cup and certain other competitions, the deduction of league points from us in the Premier League or Football League and loss of control of player registrations. For example, the Premier League could prevent us from playing, thereby cutting off our income from ticket sales and putting many of our other sources of revenue at risk. Any of these events could have a material adverse effect on our business, results of operation, financial condition, or cash flow, as well as our ability to meet our financial obligations.

Premier League voting rules may allow other clubs to take action contrary to our interests.

The Premier League is governed by its 20 club shareholders with most rule changes requiring the support of a minimum of 14 of the clubs. This allows a minority of clubs to block changes they view as unfavorable to their interests. In addition, it allows a concerted majority of the clubs to pass rules that may be disadvantageous to the remaining six clubs. Our interests may not always align with the majority of clubs and it may be difficult for us to effect changes that are advantageous to us. At the same time, it is possible that other clubs may take action that we view as contrary to our interests. If the Premier League clubs pass rules that limit our ability to operate our business as we have planned or otherwise affect the payments made to us, we may be unable to achieve our goals and strategies or increase our revenue.

Our digital media strategy may not generate the revenue we anticipate.

We maintain contact with, and provide entertainment to, our global follower base through a number of digital and other media channels, including the internet, mobile services and applications, and social media. While we have attracted a significant number of followers to our digital media assets, including our website and mobile application, the associated future revenue and income potential is uncertain. You should consider our business and prospects in light of the challenges, risks and difficulties we may encounter in this new and rapidly evolving market, including:

| ● | our ability to retain our current global follower base, build our follower base and increase engagement with our followers through our digital media assets, particularly those on third-party digital media platforms; |

| ● | our ability to enhance the content offered through our digital media assets and increase our subscriber base; |

| ● | our ability to effectively generate revenue from interaction with our followers through our digital media assets; |

| ● | our ability to attract new sponsors and advertisers, retain existing sponsors and advertisers and demonstrate that our digital media assets will deliver value to them; |

| ● | our ability to develop our digital media assets in a cost-effective manner and operate our digital media services profitably and securely; |

| ● | our ability to identify and capitalize on new digital media business opportunities; and |

| ● | our ability to compete with other sports and other media for users’ time. |

In addition, as we expand our digital and other media channels, including mobile services, applications, and social media, revenue from our other business sectors may decrease, including our Broadcasting revenue. As a consequence of our utilization of third-party media platforms, particularly social media, we are subject to third-party algorithms which we do not have control over. A change to these algorithms or the business strategy and operating models of these platforms may have a knock-on impact on our business.

8

Moreover, the increase in subscriber base in some of these digital and other media channels may limit the growth of the subscriber base and popularity of other channels. Further, governmental or other regulatory actions against social media platforms could result in a loss of some or all of our social media followers on such platform. Failure to successfully address these risks and difficulties could affect our overall business, financial condition, results of operations, cash flow, liquidity and prospects.

Serious injuries to or losses of playing staff may affect our performance, and therefore our results of operations and financial condition.

Injuries to members of the playing staff, particularly if career-threatening or career-ending, could have a detrimental effect on our business. Such injuries could have a negative effect upon our men’s first team’s performance and may also result in a loss of the income that would otherwise have resulted from a transfer of that player’s registration. In addition, depending on the circumstances, we may write down the carrying value of a player on our balance sheet and record an impairment charge in our operating expenses to reflect any losses resulting from career-threatening or career-ending injuries to that player. Our strategy is to maintain a squad of men’s first team players sufficient to mitigate the risk of player injuries. However, this strategy may not be sufficient to mitigate all financial losses in the event of an injury, and as a result such injury may affect the performance of our men’s first team, and therefore our business, results of operations financial condition and cash flow.

Inability to renew our insurance policies could expose us to significant losses.

We insure against the accidental death (including death by natural causes) or permanent disablement (resulting in an inability to continue their playing career with Manchester United and/or any other club in one of the top five European leagues) of certain members of our men’s first team, although typically not at such player’s full market value. Such insurance also excludes incidents which occur while playing matches or training. We also have catastrophe coverage in the event of an incident (such as travel or terrorist related incidents) that results in the accidental death or permanent disablement of multiple members of our men’s first team playing squad. We also carry non-player related insurance typical for our business (including combined liability, property damage, business interruption, terrorism and directors and officers insurance). When any of our insurance policies expire, it may not be possible to renew them on the same terms, or at all. In such circumstances, some of our business activities and/or assets may be uninsured. If any of these uninsured business activities or assets were to suffer damage, we could suffer a financial loss. Our most valuable tangible asset is the Old Trafford stadium. An inability to renew insurance policies covering our players, Old Trafford, the Carrington training ground (“Carrington”) or other valuable assets could expose us to significant losses.