Table of Contents

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Title of Each Class |

Trading Symbol |

Name of Each Exchange on Which Registered | ||

| each representing four Class A ordinary shares |

Large accelerated filer |

Non-accelerated filer |

Emerging growth company |

| |

International Financial Reporting Standards as issued by the International Accounting Standards Board |

Other |

Table of Contents

TABLE OF CONTENTS

| Page | ||||

| 1 | ||||

| 4 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

9 | |||

| 9 | ||||

| 10 | ||||

| 12 | ||||

| 12 | ||||

| 12 | ||||

| 13 | ||||

| 63 | ||||

| 63 | ||||

| 64 | ||||

| 91 | ||||

| 92 | ||||

| 92 | ||||

| 92 | ||||

| 93 | ||||

| 99 | ||||

| 104 | ||||

| 104 | ||||

| 105 | ||||

| 109 | ||||

| 109 | ||||

| 112 | ||||

| 113 | ||||

| 118 | ||||

| 119 | ||||

| F. DISCLOSURE OF A REGISTRANT’S ACTION TO RECOVER ERRONEOUSLY AWARDED COMPENSATION |

119 | |||

i

Table of Contents

| Page | ||||

| 120 | ||||

| 120 | ||||

| 121 | ||||

| 127 | ||||

| 127 | ||||

| 127 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 139 | ||||

| 139 | ||||

| 139 | ||||

| 145 | ||||

| 145 | ||||

| 145 | ||||

| 145 | ||||

| 146 | ||||

| ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

146 | |||

| ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES |

146 | |||

| 146 | ||||

| 147 | ||||

| 147 | ||||

| 147 | ||||

| 148 | ||||

| 148 | ||||

| ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

148 | |||

ii

Table of Contents

| Page | ||||

| 149 | ||||

| 150 | ||||

| 150 | ||||

| 150 | ||||

| 150 | ||||

| ITEM 16D. EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES |

151 | |||

| ITEM 16E. PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

151 | |||

| 151 | ||||

| 151 | ||||

| 151 | ||||

| ITEM 16I. DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

151 | |||

| 152 | ||||

| 153 | ||||

| 154 | ||||

| 154 | ||||

| 154 | ||||

| 155 | ||||

| 160 | ||||

| F-1 | ||||

iii

Table of Contents

INTRODUCTION

In this annual report on Form 20-F, unless otherwise indicated:

| • | “2018 Project Facility” refers to the senior secured project facility, dated January 28, 2013 and as amended from time to time, entered into between, among others, Studio City Company, as borrower, and certain subsidiaries as guarantors, comprising a term loan facility of HK$10,080,460,000 (equivalent to US$1.3 billion) and revolving credit facility of HK$775,420,000 (equivalent to US$100 million), and which was amended, restated and extended by the 2021 Studio City Senior Secured Credit Facility; |

| • | “2021 Studio City Senior Secured Credit Facility” refers to the facility agreement dated November 23, 2016 with, among others, Bank of China Limited, Macau Branch, to amend, restate and extend the 2018 Project Facility to provide for senior secured credit facilities in an aggregate amount of HK$234.0 million (equivalent to US$30.0 million), which consist of a HK$233.0 million (equivalent to US$29.9 million) revolving credit facility and a HK$1.0 million (equivalent to US$0.1 million) term loan facility, and which would have matured on November 30, 2021, and was amended, restated and extended by the 2028 Studio City Senior Secured Credit Facility; |

| • | “2024 Notes” refers to the 7.25% senior notes due 2024 in an aggregate principal amount of US$600,000,000 issued by Studio City Finance on February 11, 2019 and as to which no amount remains outstanding following the redemption of all remaining outstanding amounts in February 2021; |

| • | “2024 Notes Tender Offer” refers to the conditional tender offer by Studio City Finance to purchase for cash any and all of the outstanding 2024 Notes, which commenced and settled in January 2021; |

| • | “2025 Notes” refers to the 6.00% senior notes due 2025 in an aggregate principal amount of US$500,000,000 issued by Studio City Finance on July 15, 2020; |

| • | “2025 Notes Tender Offer” refers to the conditional tender offer by Studio City Finance pursuant to which it purchased for cash an aggregate principal amount of US$100.0 million of the outstanding 2025 Notes in November 2023; |

| • | “2027 Notes” refers to the 7.00% senior secured notes due 2027 in an aggregate principal amount of US$350,000,000 issued by Studio City Company on February 16, 2022; |

| • | “2028 Notes” refers to the 6.50% senior notes due 2028 in an aggregate principal amount of US$500,000,000 issued by Studio City Finance on July 15, 2020; |

| • | “2028 Studio City Senior Secured Credit Facility” refers to the facility agreement dated March 15, 2021 with, among others, Bank of China Limited, Macau Branch, to amend, restate and extend the 2021 Studio City Senior Secured Credit Facility to provide for senior secured credit facilities in an aggregate amount of HK$234.0 million (equivalent to US$30.0 million), which consist of a HK$233.0 million (equivalent to US$29.9 million) revolving credit facility and a HK$1.0 million (equivalent to US$0.1 million) term loan facility, with the maturity date of January 15, 2028; |

| • | “2029 Notes” refers to the 5.00% senior notes due 2029 in an aggregate principal amount of US$1,100,000,000 issued by Studio City Finance, of which US$750,000,000 was issued on January 14, 2021 (the “First 2029 Notes”) and US$350,000,000 was issued on May 20, 2021 (the “Additional 2029 Notes”); |

| • | “ADSs” refers to our American depositary shares, each of which represents four Class A ordinary shares; |

| • | “Altira Macau” refers to an integrated resort located in Taipa, Macau; |

| • | “board” and “board of directors” refer to the board of directors of our Company or a duly constituted committee thereof; |

1

Table of Contents

| • | “China” and “PRC” refer to the People’s Republic of China, excluding the Hong Kong Special Administrative Region of the PRC (Hong Kong), the Macau Special Administrative Region of the PRC (Macau) and Taiwan from a geographical point of view; |

| • | “City of Dreams” refers to an integrated resort located in Cotai, Macau, which currently features casino areas and four luxury hotels, including a collection of retail brands, a wet stage performance theater (temporarily closed since June 2020) and other entertainment venues; |

| • | “Concession Contract” refers to the concession contract executed between the Macau Special Administrative Region and the Gaming Operator on December 16, 2022, that provides for the terms and conditions of the concession granted to the Gaming Operator, which expires on December 31, 2032; |

| • | “DICJ” refers to the Direcção de Inspecção e Coordenação de Jogos (the Gaming Inspection and Coordination Bureau), a department of the Public Administration of Macau; |

| • | “DSEC” refers to the Statistics and Census Service of Macau, a department of the government of Macau; |

| • | “Greater China” refers to mainland China, Hong Kong and Macau, collectively; |

| • | “HK$” and “H.K. dollar(s)” refer to the legal currency of Hong Kong; |

| • | “Management and Shared Services Arrangements” refer to, collectively, (i) the Master Services Agreement (the “Master Services Agreement”) entered into on December 21, 2015 by and between Studio City Entertainment, Studio City Hotels, Studio City Retail Services Limited, Studio City Developments, Studio City Ventures Limited, Studio City Services Limited and the Company (the “Studio City Entities,” each a “Studio City Entity”) and the Master Service Providers, and (ii) the individual work agreements (the “Work Agreements,” each a “Work Agreement”) which sets out the terms and conditions that apply to certain services to be provided thereunder and other arrangements for the provision of non-gaming services at Studio City by the Master Service Providers to the Studio City Entities and vice versa; |

| • | “Master Service Providers” refer to certain of our affiliates with whom we entered into a master services agreement and a series of work agreements with respect to the non-gaming services at the properties in Macau, and that are also subsidiaries of Melco Resorts, including Melco Crown (COD) Developments Limited (now known as COD Resorts Limited), Altira Developments Limited (now known as Altira Resorts Limited), the Gaming Operator, MPEL Services Limited (now known as Melco Resorts Services Limited), Golden Future (Management Services) Limited, MPEL Properties (Macau) Limited, Melco Crown Security Services Limited (now known as Melco Resorts Security Services Limited), MCE Travel Limited (now known as Melco Resorts Travel Limited), MCE Transportation Limited and MCE Transportation Two Limited (now known as MCO Transportation Two Limited); |

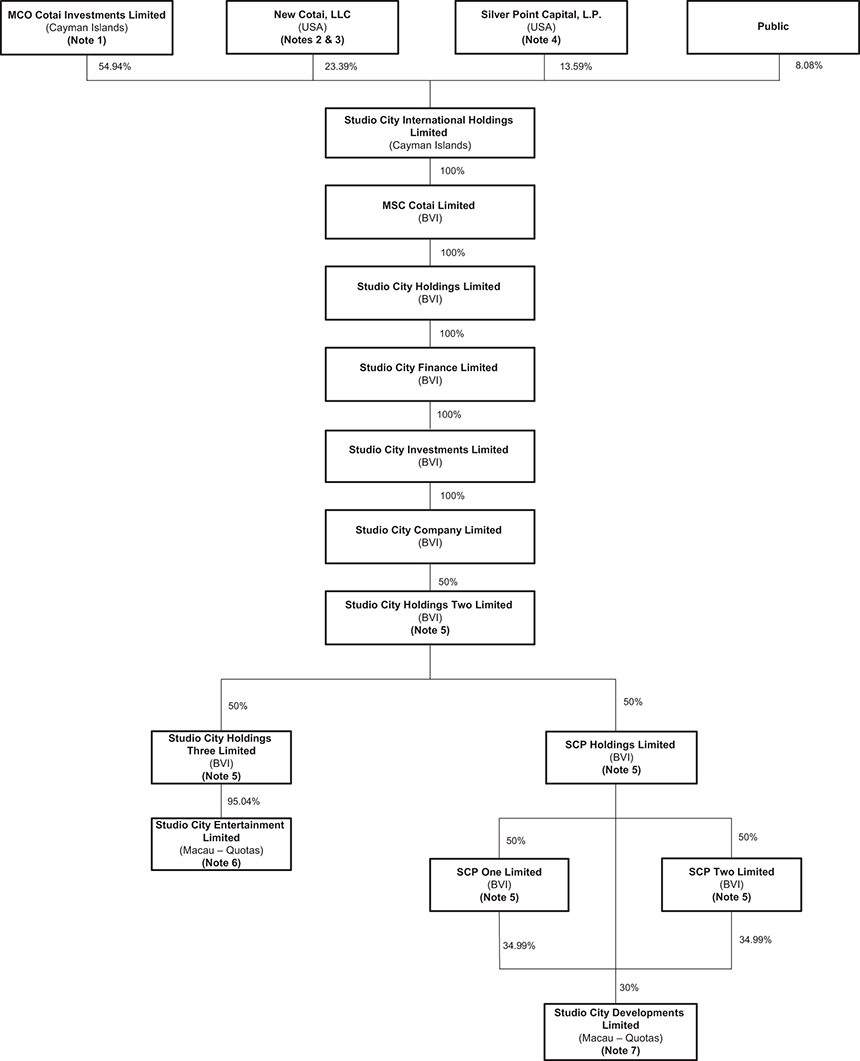

| • | “MCO Cotai” refers to MCO Cotai Investments Limited (formerly known as MCE Cotai Investments Limited), a subsidiary of Melco Resorts and a shareholder of our Company; |

| • | “Melco International” refers to Melco International Development Limited, a Hong Kong-listed company; |

| • | “Melco Resorts” refers to Melco Resorts & Entertainment Limited, a Cayman Islands company and with its American depositary shares listed on the Nasdaq Global Select Market; |

| • | “Melco Resorts Macau” or the “Gaming Operator” refers to Melco Resorts (Macau) Limited, a company incorporated under the laws of Macau that is a subsidiary of Melco Resorts, the holder of a concession under the Concession Contract and the operator of Studio City Casino. The equity interest of the Gaming Operator is 85% owned by Melco Resorts and 15% owned by Mr. Lawrence Ho, the managing director of the Gaming Operator; |

2

Table of Contents

| • | “MOP” and “Pataca(s)” refer to the legal currency of Macau; |

| • | “MSC Cotai” refers to our subsidiary, MSC Cotai Limited, which is a company incorporated in the British Virgin Islands with limited liability; |

| • | “New Cotai” refers to New Cotai, LLC, a Delaware limited liability company; |

| • | “Renminbi” and “RMB” refer to the legal currency of the PRC; |

| • | “Studio City” refers to a cinematically-themed integrated resort in Cotai, an area of reclaimed land located between the islands of Taipa and Coloane in Macau; |

| • | “Studio City Casino” refers to the gaming areas being operated within Studio City; |

| • | “Studio City Casino Agreement” (previously referred to as the Services and Right to Use Arrangements) refers to the agreement entered into among Melco Resorts Macau and Studio City Entertainment, dated May 11, 2007 and amended on June 15, 2012 and June 23, 2022 and any other agreements or arrangements entered into from time to time, which may amend, supplement or relate to the aforementioned agreements or arrangements; |

| • | “Studio City Company” refers to our subsidiary, Studio City Company Limited, which is a company incorporated in the British Virgin Islands with limited liability; |

| • | “Studio City Developments” refers to our subsidiary, Studio City Developments Limited, a Macau company; |

| • | “Studio City Entertainment” refers to our subsidiary, Studio City Entertainment Limited, a Macau company; |

| • | “Studio City Finance” refers to our subsidiary, Studio City Finance Limited, which is a company incorporated in the British Virgin Islands with limited liability; |

| • | “Studio City Hotel” refers to the hotel owned by Studio City Developments which includes the four hotel towers at Studio City; |

| • | “Studio City Hotels” refers to our subsidiary, Studio City Hotels Limited, a Macau company; |

| • | “Studio City Investments” refers to our subsidiary, Studio City Investments Limited, which is a company incorporated in the British Virgin Islands with limited liability; |

| • | “US$” and “U.S. dollar(s)” refer to the legal currency of the United States; |

| • | “U.S. GAAP” refers to the U.S. generally accepted accounting principles; and |

| • | “we,” “us,” “our,” “our Company” and “the Company” refer to Studio City International Holdings Limited and, as the context requires, its predecessor entities and its consolidated subsidiaries. |

This annual report on Form 20-F includes our audited consolidated financial statements for the years ended December 31, 2023, 2022 and 2021 and as of December 31, 2023 and 2022.

Certain monetary amounts, percentages, and other figures included in this annual report have been subject to rounding adjustments. Certain other amounts that appear in this annual report may not sum due to rounding. Figures shown as totals in certain tables may not be an arithmetic aggregation of the figures preceding them.

3

Table of Contents

GLOSSARY

| “average daily rate” or “ADR” | calculated by dividing total room revenues including complimentary rooms (less service charges, if any) by total rooms occupied, including complimentary rooms, i.e., average price of occupied rooms per day | |

| “cage” | a secure room within a casino with a facility that allows patrons to carry out transactions required to participate in gaming activities, such as exchange of cash for chips and exchange of chips for cash or other chips | |

| “chip” | round token that is used on casino gaming tables in lieu of cash | |

| “concession” | a government grant for the operation of games of fortune and chance in casinos in Macau under an administrative contract pursuant to which a concessionaire, or the entity holding the concession, is authorized to operate games of fortune and chance in casinos in Macau | |

| “dealer” | a casino employee who takes and pays out wagers or otherwise oversees a gaming table | |

| “drop” | the amount of cash to purchase gaming chips and promotional vouchers that is deposited in a gaming table’s drop box, plus gaming chips purchased at the casino cage | |

| “drop box” | a box or container that serves as a repository for cash, chip purchase vouchers, credit markers and forms used to record movements in the chip inventory on each table game | |

| “electronic gaming table” | table with an electronic or computerized wagering and payment system that allow players to place bets from multiple-player gaming seats | |

| “gaming machine” | slot machine and/or electronic gaming table | |

| “gaming machine handle” | the total amount wagered in gaming machines | |

| “gaming machine win rate” | gaming machine win (calculated before non-discretionary incentives (including the point-loyalty programs) as administered by the Gaming Operator and allocating casino revenues related to goods and services provided to gaming patrons on a complimentary basis) expressed as a percentage of gaming machine handle | |

| “gaming promoter” | an individual or corporate entity who, for the purpose of promoting rolling chip and other gaming activities, arranges customer transportation and accommodation, provides credit in its sole discretion if authorized by a gaming operator and arranges food and beverage services and entertainment in exchange for commissions or other compensation from a gaming concessionaire | |

| “integrated resort” | a resort which provides customers with a combination of hotel accommodations, casinos or gaming areas, retail and dining facilities, MICE space, entertainment venues and spas | |

| “junket player” | a player sourced by gaming promoters to play in the VIP gaming rooms or areas | |

| “marker” | evidence of indebtedness by a player to the casino or gaming operator | |

| “mass market patron” | a customer who plays in the mass market segment | |

| “mass market segment” | consists of both table games and gaming machines played by mass market patrons primarily for cash stakes | |

4

Table of Contents

| “mass market table games drop” | the amount of table games drop in the mass market table games segment | |

| “mass market table games hold percentage” | mass market table games win (calculated before discounts, commissions, non-discretionary incentives (including the point-loyalty programs) as administered by the Gaming Operator and allocating casino revenues related to goods and services provided to gaming patrons on a complimentary basis) as a percentage of mass market table games drop | |

| “mass market table games segment” | the mass market segment consisting of mass market patrons who play table games | |

| “MICE” | Meetings, Incentives, Conventions and Exhibitions, an acronym commonly used to refer to tourism involving large groups brought together for an event or specific purpose | |

| “net rolling” | net turnover in a non-negotiable chip game | |

| “non-negotiable chip” | promotional casino chip that is not to be exchanged for cash | |

| “non-rolling chip” | chip that can be exchanged for cash, used by mass market patrons to make wagers | |

| “occupancy rate” | the average percentage of available hotel rooms occupied, including complimentary rooms, during a period | |

| “premium direct player” | a rolling chip patron who is a direct customer of the concessionaire and is attracted to the casino through marketing efforts of the gaming operator | |

| “progressive jackpot” | a jackpot for a gaming machine or table game where the value of the jackpot increases as wagers are made; multiple gaming machines or table games may be linked together to establish one progressive jackpot | |

| “revenue per available room” or “REVPAR” | calculated by dividing total room revenues including complimentary rooms (less service charges, if any) by total rooms available, thereby representing a combination of hotel average daily room rates and occupancy | |

| “rolling chip” or “VIP rolling chip” | non-negotiable chip primarily used by rolling chip patrons to make wagers | |

| “rolling chip patron” | a player who primarily plays on a rolling chip or VIP rolling chip tables and typically plays for higher stakes than mass market gaming patrons | |

| “rolling chip segment” | consists of table games played in private VIP gaming rooms or areas by rolling chip patrons who are either premium direct players or junket players | |

| “rolling chip volume” | the amount of non-negotiable chips wagered and lost by the rolling chip market segment | |

| “rolling chip win rate” | rolling chip table games win (calculated before discounts, commissions, non-discretionary incentives (including the point-loyalty programs) as administered by the Gaming Operator and allocating casino revenues related to goods and services provided to gaming patrons on a complimentary basis) as a percentage of rolling chip volume | |

| “slot machine” | traditional slot or electronic gaming machine operated by a single player | |

| “subconcession” | an agreement for the operation of games of fortune and chance in casinos between the entity holding the concession, or the concessionaire, and a subconcessionaire, pursuant to which the subconcessionaire is authorized to operate games of fortune and chance in casinos in Macau | |

5

Table of Contents

| “table games win” | the amount of wagers won net of wagers lost on gaming tables that is retained and recorded as casino revenues. Table games win is calculated before discounts, commissions, non-discretionary incentives (including the point-loyalty programs) as administered by the Gaming Operator and allocating casino revenues related to goods and services provided to gaming patrons on a complimentary basis | |

| “VIP gaming room” | gaming rooms or areas that have restricted access to rolling chip patrons and typically offer more personalized service than the general mass market gaming areas | |

6

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements relate to future events, including our future operating results and conditions, our prospects and our future financial performance and condition, all of which are largely based on our current expectations and projections. Known and unknown risks, uncertainties and other factors may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. See “Item 3. Key Information — D. Risk Factors” for a discussion of some risk factors that may affect our business and results of operations. Moreover, because we operate in a heavily regulated and evolving industry where the amended gaming law was adopted and implemented by the Macau government, may become highly leveraged and operate in Macau, a market with intense competition, new risk factors may emerge from time to time. It is not possible for our management to predict all risk factors, nor can we assess the impact of these factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those expressed or implied in any forward-looking statement.

In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. We have based the forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, among other things, statements relating to:

| • | our goals and strategies; |

| • | pace of recovery from the impact of the global COVID-19 outbreak on our business, financial results and liquidity; |

| • | the reduced access to our target markets due to travel restrictions, and the potential long-term impact on customer retention; |

| • | the expected growth of the gaming and leisure market in Macau and visitation in Macau; |

| • | restrictions or conditions on visitation by citizens of the PRC to Macau; |

| • | the impact on the travel and leisure industry from factors such as an outbreak of an infectious disease, such as the COVID-19 pandemic or the period of time required for tourism to return to pre-pandemic levels (if at all), extreme weather patterns or natural disasters, military conflicts and any future security alerts and/or terrorist attacks or other acts of violence; |

| • | general domestic or global political and economic conditions, including in the PRC and Hong Kong, which may impact levels of travel, leisure and consumer spending; |

| • | our ability to successfully operate Studio City; |

| • | our compliance with conditions and covenants under the existing and future indebtedness; |

| • | laws, rules and regulations which could bar the trading of the American depositary shares of our Company in the United States, such as the Holding Foreign Companies Accountable Act and the rules promulgated thereunder; |

| • | capital and credit market volatility; |

| • | our ability to raise additional capital, if and when required; |

| • | increased competition from other casino hotel and resort projects in Macau and elsewhere in Asia, including the concessionaires in Macau; |

7

Table of Contents

| • | government policies, laws and regulations relating to the leisure and gaming industry in Macau, including the implementation of the amended gaming law, and the legalization of gaming in other jurisdictions; |

| • | the uncertainty of tourist behavior related to spending and vacationing at casino resorts in Macau; |

| • | fluctuations in occupancy rates and average daily room rates in Macau; |

| • | the liberalization of travel restrictions on PRC citizens and convertibility of the Renminbi; |

| • | the tightened control of certain cross-border fund transfers from the PRC; |

| • | significantly increased regulatory scrutiny on Macau gaming promoters’ operations that has resulted in the cessation of business by many gaming promoters in Macau; |

| • | the completion of infrastructure projects in Macau; |

| • | our ability to retain and gain new customers; |

| • | our ability to offer new services and attractions; |

| • | our future business development, financial condition and results of operations; |

| • | the expected growth, size of and trends in the market in Macau; |

| • | expected changes in our revenues, costs or expenditures; |

| • | our expectations regarding demand for our services and market acceptance of our brand and business; |

| • | our ability to continue to develop new technologies and/or upgrade our existing technologies; |

| • | cybersecurity risks including misappropriation of customer information or other breaches of information security; |

| • | our ability to protect our intellectual property rights; |

| • | growth of and trends of competition in the gaming and leisure market in Macau; |

| • | general economic and business conditions globally and in Macau; |

| • | our ability to comply with the New York Stock Exchange’s (“NYSE”) continued listing standards and maintain the listing of our ADSs on the New York Stock Exchange; and |

| • | other factors described under “Item 3. Key Information — D. Risk Factors.” |

The forward-looking statements made in this annual report on Form 20-F relate only to events or information as of the date on which the statements are made in this annual report on Form 20-F. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report on Form 20-F and the documents that we referenced in this annual report on Form 20-F and have filed as exhibits with the U.S. Securities and Exchange Commission, or the SEC, completely and with the understanding that our actual future results may be materially different from what we expect.

EXCHANGE RATE INFORMATION

Our reporting currency is the U.S. dollar and functional currencies are the U.S. dollar, Hong Kong dollar and Pataca. This annual report on Form 20-F contains translations of certain Pataca, Hong Kong dollar and Renminbi amounts into U.S. dollars for the convenience of the reader. Unless otherwise stated, all translations of Hong Kong dollar and Renminbi amounts into U.S. dollars in this annual report on Form 20-F were made at the rates of HK$7.811768 to US$1.00 and RMB7.119414 to US$1.00, respectively.

8

Table of Contents

The H.K. dollar is freely convertible into other currencies (including the U.S. dollar). Since October 17, 1983, the H.K. dollar has been officially linked to the U.S. dollar at the rate of HK$7.80 to US$1.00. The market exchange rate has not deviated materially from the level of HK$7.80 to US$1.00 since the peg was first established. However, in May 2005, the Hong Kong Monetary Authority broadened the trading band from the original rate of HK$7.80 per U.S. dollar to a rate range of HK$7.75 to HK$7.85 per U.S. dollar. The Hong Kong government has stated its intention to maintain the link at that rate range and, acting through the Hong Kong Monetary Authority, has a number of means by which it may act to maintain exchange rate stability. However, no assurance can be given that the Hong Kong government will maintain the link at HK$7.75 to HK$7.85 per U.S. dollar or at all.

The Pataca is pegged to the H.K. dollar at a rate of HK$1.00 = MOP1.03. All translations from Patacas to U.S. dollars and Singapore dollars to U.S. dollars in this annual report on Form 20-F were made at the exchange rate of MOP8.046088 = US$1.00 and SGD1.319838 to US$1.00, respectively.

We make no representation that any Pataca, Hong Kong dollar, Renminbi, Singapore dollar or U.S. dollar amounts referred to in this annual report on Form 20-F could have been, or could be, converted into U.S. dollar, Pataca, Hong Kong dollar, Renminbi or Singapore dollar, as the case may be, at any particular rate or at all.

In this annual report, U.S. dollar equivalents of H.K. dollar amounts of indebtedness are based on the prevailing exchange rate on the relevant transaction date, except for the indebtedness balance translations as of the balance sheet date, which are based on the prevailing exchange rate on the applicable balance sheet date.

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

9

Table of Contents

| ITEM 3. | KEY INFORMATION |

Studio City International Holdings Limited is a company incorporated under the laws of the Cayman Islands. We are not a Chinese operating company but a Cayman Islands holding company with operations conducted by our subsidiaries in Macau, Hong Kong and Singapore. We do not have any operations or maintain any office or personnel in mainland China. All of our current operations, and administrative and corporate functions are conducted in Macau, Hong Kong and Singapore. We conduct our operations in Macau and we do not have any assets or operations in the PRC. Our principal executive offices are located in Singapore and Hong Kong. We have no variable interest entities in our corporate structure.

We face various legal and operational risks and uncertainties as a company operating in Macau. Since we derive all of our revenues from our Macau business and a significant number of our customers come from, and are expected to continue to come from, the PRC, our results of operations and financial condition may be materially and adversely affected by significant regulatory developments in the PRC. Actions by the PRC government can also significantly affect our business by, for example, placing limits on the ability of PRC residents to travel or remit currency outside of the PRC or by restricting gaming-related marketing activities in China. See “Item 3. Key Information — D. Risk Factors — Risks Relating to Conducting Business and Operating in Macau — Policies, campaigns and measures adopted by the PRC and/or Macau governments from time to time could materially and adversely affect our operations.”

The PRC may also intervene or influence our operations in Macau, Hong Kong or elsewhere at any time, or may exert more control over offerings conducted overseas and/or foreign investment in issuers in China, which could result in a material change in our operations and/or the value of our ordinary shares. For example, in recent years, the PRC government has enhanced regulation in areas such as anti-monopoly, anti-unfair competition, cybersecurity and data privacy. See “— Risks Relating to Our Business — Failure to protect the integrity and security of company staff, supplier and customer information and comply with cybersecurity, data privacy, data protection or any other laws and regulations related to data may materially and adversely affect our business, financial condition and results of operations, and/or result in damage to reputation and/or subject us to fines, penalties, lawsuits, restrictions on our use or transfer of data and other risks” and “— Claims or regulatory actions against us under China’s competition laws may result in fines, constraints on our business and damage to our reputation.” These laws and regulations can be complex and stringent, and many are subject to change and uncertain interpretations, which could result in claims, changes to our data and other business practices, regulatory investigations, penalties, increased cost of operations, or declines in customer growth or engagement, or otherwise affect our business. As a result, the trading prices of our ADSs and ordinary shares could significantly decline or become worthless.

Additionally, the Chinese government has in the past made statements indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers and any such action could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless. There are risks and uncertainties which we cannot foresee for the time being, and rules and regulations in China can change quickly with little or no advance notice. See “ — Risks Relating to Conducting Business and Operating in Macau — Changes in law, regulations and policies in the PRC and uncertainties in the legal systems in the PRC may expose us to risks. In addition, rules and regulations in the PRC can change quickly with little advance notice” and “— The PRC government may influence our operations in Macau or elsewhere or intervene in our offerings conducted overseas or foreign investments in us. Its oversight and discretion over our business could result in material adverse changes in our operations and the value of our ordinary shares and ADSs.”

We also face risks associated with interpretations of or changes to gaming laws in Macau, including the interpretation of the amended gaming law in Macau, as well as the continued ability by the U.S. Public Company Accounting Oversight Board, or PCAOB, to inspect our auditors.

10

Table of Contents

On May 4, 2022, we were identified as a Commission-Identified Issuer under the Holding Foreign Companies Accountable Act (“HFCAA”) and the rules promulgated thereunder because our auditor at that time was Ernst & Young, located in Hong Kong, which was a PCAOB-Identified Firm as of May 4, 2022. On August 16, 2022, we changed our auditor from Ernst & Young, located in Hong Kong, to Ernst & Young LLP, located in Singapore, which is not a PCAOB-Identified Firm. In December 2022, the PCAOB announced that it secured complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong. As a result, until such time as the PCAOB issues any new determination, we do not believe we are at risk of being a Commission-Identified Issuer nor at risk of having our securities subject to a trading prohibition under the HFCAA.

Permissions, Approvals, Licenses, Certificates and Permits Required from the PRC, Hong Kong and Macau Authorities for Our Operations and for the Offering of Our Securities to Foreign Investors

As of the date of this annual report, we have obtained the requisite permissions, approvals, licenses, certificates and permits from the PRC, Hong Kong and Macau government authorities that are material for our business operations in those jurisdictions, and none have been denied. See “Item 4. Information on the Company — B. Business Overview — Regulations.”

Given the uncertainties of interpretation and implementation of relevant laws and regulations and enforcement practice by PRC government authorities, we may be required to obtain additional licenses, permits, filings or approvals for our business operations in the future, and may not be able to maintain or renew our current licenses, permits, filings or approvals. In addition, rules and regulations in China can change quickly with little advance notice. Uncertainties due to evolving laws and regulations could impede our ability to obtain or maintain certificates, permits or licenses required to conduct business in China. In the absence of required certificates, permits or licenses, governmental authorities could impose material sanctions or penalties on us.

Furthermore, in connection with our issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this annual report, we do not believe we are currently required to obtain permissions from or complete any filing with the China Securities Regulatory Commission, or CSRC, or required to go through cybersecurity review by the Cyberspace Administration of China, or CAC. In addition, we have not been asked to obtain such permissions by any PRC authority or received any denial to do so. However, the PRC government has in the past made statements indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment by issuers like us and may do so in the future. There remains significant uncertainty as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities.

If (i) we incorrectly conclude that certain regulatory permissions and approvals are not required or (ii) applicable laws, regulations, or interpretations change in a way that requires us to complete such filings or obtain such approvals in the future, and (iii) we are required to obtain such permissions or approvals in the future, but fail to receive or maintain such permissions or approvals, we may face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on us, limit our operations, limit our ability to pay dividends outside of China, limit our ability to list on stock exchanges outside of China or offer our securities to foreign investors or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities.

Cash Flows Through Our Organization

Cash from financings and operations is primarily retained by our operating subsidiaries for the purposes of funding our operating activities and capital expenditures. Cash within our group is primarily transferred between our subsidiaries through intercompany loan arrangements. Financing raised by Studio City International Holdings Limited has been transferred to our financing and operating subsidiaries through the use

11

Table of Contents

of equity capital contributions or intercompany loan arrangements. In 2023, excluding cash transferred for the purpose of the settlement of intragroup charges, no cash has been transferred to our holding company, Studio City International Holdings Limited, from its subsidiaries. See also “Item 4. Information on the Company — B. Business Overview — Taxation” and “Item 8. Financial Information — A. Consolidated Statements and Other Financial Information — Dividend Policy.” There are no regulatory or foreign exchange restrictions or limitations on our ability to transfer cash within our corporate group or to declare dividends to holders of our ADSs, except that our subsidiaries incorporated in Macau are required to set aside a specified amount of the entity’s profit after tax as a legal reserve which is not distributable to the shareholders of such subsidiaries. See “Item 4. Information on the Company — B. Business Overview — Regulations — Restrictions on Distribution of Profits Regulations” and “Item 10. Additional Information — D. Exchange Controls.”

We currently intend to retain most, if not all, of our available funds and any future earnings to repay or refinance our debt, fund our ongoing operations and fund the development and growth of our business. As a result, we do not expect to pay any cash dividends in the foreseeable future. See “Item 8. Financial Information — A. Consolidated Statements and Other Financial Information — Dividend Policy” and note 17 to the consolidated financial statements included elsewhere in this annual report.

You should carefully consider all of the information in this annual report before making an investment in the ADSs.

A. [RESERVED]

B. CAPITALIZATION AND INDEBTEDNESS

Not applicable.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

12

Table of Contents

D. RISK FACTORS

Studio City International Holdings Limited is a company incorporated under the laws of the Cayman Islands. We are not a Chinese operating company but a Cayman Islands holding company with operations conducted by our subsidiaries in Macau, Hong Kong and Singapore. We do not have any operations or maintain any office or personnel in mainland China. All of our current operations, and administrative and corporate functions are conducted in Macau, Hong Kong and Singapore. We conduct our operations in Macau and we do not have any assets or operations in the PRC. Our principal executive offices are located in Singapore and Hong Kong. We have no variable interest entities in our corporate structure.

We face various legal and operational risks and uncertainties as a company operating in Macau. Since we derive all of our revenues from our Macau business and a significant number of our customers come from, and are expected to continue to come from, the PRC, our results of operations and financial condition may be materially and adversely affected by significant regulatory developments in the PRC. Actions by the PRC government can also significantly affect our business by, for example, placing limits on the ability of PRC residents to travel or remit currency outside of the PRC or by restricting gaming-related marketing activities in China. See “Item 3. Key Information — D. Risk Factors — Risks Relating to Conducting Business and Operating in Macau — Policies, campaigns and measures adopted by the PRC and/or Macau governments from time to time could materially and adversely affect our operations.”

The PRC may also intervene or influence our operations in Macau, Hong Kong or elsewhere at any time, or may exert more control over offerings conducted overseas and/or foreign investment in issuers in China, which could result in a material change in our operations and/or the value of our ordinary shares. For example, in recent years, the PRC government has enhanced regulation in areas such as anti-monopoly, anti-unfair competition, cybersecurity and data privacy. See “— Risks Relating to Our Business — Failure to protect the integrity and security of company staff, supplier and customer information and comply with cybersecurity, data privacy, data protection or any other laws and regulations related to data may materially and adversely affect our business, financial condition and results of operations, and/or result in damage to reputation and/or subject us to fines, penalties, lawsuits, restrictions on our use or transfer of data and other risks” and “— Claims or regulatory actions against us under China’s competition laws may result in fines, constraints on our business and damage to our reputation.” These laws and regulations can be complex and stringent, and many are subject to change and uncertain interpretations, which could result in claims, changes to our data and other business practices, regulatory investigations, penalties, increased cost of operations, or declines in customer growth or engagement, or otherwise affect our business. As a result, the trading prices of our ADSs and ordinary shares could significantly decline or become worthless.

Additionally, the Chinese government has in the past made statements indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers and any such action could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless. There are risks and uncertainties which we cannot foresee for the time being, and rules and regulations in China can change quickly with little or no advance notice. See “Item 3. Key Information — D. Risk Factors — Risks Relating to Conducting Business and Operating in Macau — Changes in law, regulations and policies in the PRC and uncertainties in the legal systems in the PRC may expose us to risks. In addition, rules and regulations in the PRC can change quickly with little advance notice” and “— The PRC government may influence our operations in Macau or elsewhere or intervene in our offerings conducted overseas or foreign investments in us. Its oversight and discretion over our business could result in material adverse changes in our operations and the value of our ordinary shares and ADSs.”

We also face risks associated with interpretations of or changes to gaming laws in Macau, including the interpretation of the amended gaming law in Macau, as well as the continued ability by the U.S. Public Company Accounting Oversight Board, or PCAOB, to inspect our auditors.

13

Table of Contents

On May 4, 2022, we were identified as a Commission-Identified Issuer under the HFCAA and the rules promulgated thereunder because our auditor at that time was Ernst & Young, located in Hong Kong, which was a PCAOB-Identified Firm as of May 4, 2022. On August 16, 2022, we changed our auditor from Ernst & Young, located in Hong Kong, to Ernst & Young LLP, located in Singapore, which is not a PCAOB-Identified Firm. In December 2022, the PCAOB announced that it secured complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong. As a result, until such time as the PCAOB issues any new determination, we do not believe we are at risk of being a Commission-Identified Issuer nor at risk of having our securities subject to a trading prohibition under the HFCAA.

Permissions, Approvals, Licenses, Certificates and Permits Required from the PRC, Hong Kong and Macau Authorities for Our Operations and for the Offering of Our Securities to Foreign Investors

As of the date of this annual report, we have obtained the requisite permissions, approvals, licenses, certificates and permits from the PRC, Hong Kong and Macau government authorities that are material for our business operations in those jurisdictions, and none have been denied. See “Item 4. Information on the Company — B. Business Overview — Regulations.”

Given the uncertainties of interpretation and implementation of relevant laws and regulations and enforcement practice by PRC government authorities, we may be required to obtain additional licenses, permits, filings or approvals for our business operations in the future, and may not be able to maintain or renew our current licenses, permits, filings or approvals. In addition, rules and regulations in China can change quickly with little advance notice. Uncertainties due to evolving laws and regulations could impede our ability to obtain or maintain certificates, permits or licenses required to conduct business in China. In the absence of required certificates, permits or licenses, governmental authorities could impose material sanctions or penalties on us.

Furthermore, in connection with our issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this annual report, we do not believe we are currently required to obtain permissions from or complete any filing with the CSRC or required to go through cybersecurity review by the CAC. In addition, we have not been asked to obtain such permissions by any PRC authority or received any denial to do so. However, the PRC government has in the past made statements indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment by issuers like us and may do so in the future. There remains significant uncertainty as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities.

If (i) we incorrectly conclude that certain regulatory permissions and approvals are not required or (ii) applicable laws, regulations, or interpretations change in a way that requires us to complete such filings or obtain such approvals in the future, and (iii) we are required to obtain such permissions or approvals in the future, but fail to receive or maintain such permissions or approvals, we may face sanctions by the CSRC, the CAC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on us, limit our operations, limit our ability to pay dividends outside of China, limit our ability to list on stock exchanges outside of China or offer our securities to foreign investors or take other actions that could have a material adverse effect on our business, financial condition, results of operations and prospects, as well as the trading price of our securities.

Cash Flows Through Our Organization

Cash from financings and operations is primarily retained by our operating subsidiaries for the purposes of funding our operating activities and capital expenditures. Cash within our group is primarily transferred between our subsidiaries through intercompany loan arrangements. Financing raised by Studio City International Holdings Limited has been transferred to our financing and operating subsidiaries through the use

14

Table of Contents

of equity capital contributions or intercompany loan arrangements. In 2023, excluding cash transferred for the purpose of the settlement of intragroup charges, no cash has been transferred to our holding company, Studio City International Holdings Limited, from its subsidiaries. See also “Item 4. Information on the Company — B. Business Overview — Taxation” and “Item 8. Financial Information — A. Consolidated Statements and Other Financial Information — Dividend Policy.” There are no regulatory or foreign exchange restrictions or limitations on our ability to transfer cash within our corporate group or to declare dividends to holders of our ADSs, except that our subsidiaries incorporated in Macau are required to set aside a specified amount of the entity’s profit after tax as a legal reserve which is not distributable to the shareholders of such subsidiaries. See “Item 4. Information on the Company — B. Business Overview — Regulations — Restrictions on Distribution of Profits Regulations” and “Item 10. Additional Information — D. Exchange Controls.”

We currently intend to retain most, if not all, of our available funds and any future earnings to repay or refinance our debt, fund our ongoing operations and fund the development and growth of our business. As a result, we do not expect to pay any cash dividends in the foreseeable future. See “Item 8. Financial Information — A. Consolidated Statements and Other Financial Information — Dividend Policy” and note 17 to the consolidated financial statements included elsewhere in this annual report.

You should carefully consider all of the information in this annual report before making an investment in the ADSs. The following summarizes some, but not all, of the risks provided below. Please carefully consider all of the information discussed in this Item 3.D. “Risk Factors” in this annual report for a more thorough description of these and other risks.

You should carefully consider the following risk factors in addition to the other information set forth in this annual report. Our business, financial condition and results of operations can be affected materially and adversely by any of the following risk factors.

Risks Relating to Our Business

| • | Risks relating to recovery from the COVID-19 pandemic. |

| • | Risks relating to our reliance on the operation of the Studio City Casino under the Studio City Casino Agreement. |

| • | Risks relating to our short operating history. |

| • | Risks relating to our sole operation of Studio City. |

| • | Risks relating to our history of net losses. |

| • | Risks relating to the inability to generate sufficient cash flow to meet our debt service obligations. |

| • | Risks relating to our compliance with credit facility and debt instruments. |

| • | Risks relating to our current and potential future indebtedness and our need for additional financing. |

| • | Risks relating to depending on the continued efforts or our senior management and retaining qualified personnel. |

| • | Risks relating to failure to comply with anti-corruption laws and anti-money laundering policies. |

| • | Risks relating to cybersecurity and failure to protect the integrity and security of data, including customer information. |

| • | Risks relating to being based in or having all of our operations in Singapore, Hong Kong and Macau, uncertainties in the legal systems in the PRC, and policies, campaigns and measures adopted by the PRC and/or Macau governments from time to time. |

| • | Risks relating to inadequate insurance coverage. |

15

Table of Contents

Risks Relating to Operating in the Gaming Industry in Macau

| • | Risks relating to the Gaming Operator’s Concession Contract. |

| • | Risks relating to facing intense competition. |

| • | Risks relating to the interpretation of the Macau gaming law amended in 2022 and related laws and their implementation by the Macau government. |

| • | Risks relating to adverse changes or developments in gaming laws or regulations in Macau. |

Risks Relating to Our Relationship with Melco Resorts

| • | Risks relating to our dependence on our shareholder, Melco Resorts. |

Risks Relating to Conducting Business and Operating in Macau

| • | Risks relating to restrictions on export of Renminbi. |

Risks Relating to Our Shares and ADSs

| • | Risks relating to compliance with the New York Stock Exchange requirements for continued listing. |

Risks Relating to Our Business

We continue to recover from the impact of, and disruptions caused by, COVID-19 on our operations, and the pace of recovery may continue to materially affect our business, prospects, financial condition and results of operations.

While quarantine-free travel within Greater China has resumed and pandemic measures have been lifted, negative impacts of COVID-19 on the PRC economy and nearby Asian regions are still being experienced. The pace of our business recovery from COVID-19 is highly uncertain and will depend on the impact of potentially higher unemployment rates, declines in income levels and loss of personal wealth resulting from COVID-19 outbreaks. There is no guarantee that travel and consumer sentiment will rebound quickly or at all.

According to the DSEC, visitor arrivals to Macau increased by 395% on a year-over-year basis in 2023 as compared to 2022 while, according to the DICJ, gross gaming revenues in Macau increased by 334% on a year-over-year basis in 2023. However, visitor arrivals in 2023 were still 28% lower than in 2019, and gross gaming revenues in 2023 were still 37% lower than in 2019. As we derive all of our revenues from our business and operations in Macau, our business has been materially affected and continues to be adversely affected by the disruptions from the COVID-19 pandemic.

The COVID-19 outbreak also caused severe disruptions to the businesses of our tenants and other business partners, which has increased the risk of them defaulting on their contractual obligations with us, which may adversely affect our business, financial condition and results of operations, including causing increases in our bad debts.

The disruptions to our business caused by COVID-19 outbreaks have had an adverse effect on our operations. For the years ended December 31, 2023, 2022 and 2021, our total operating revenues generated amounted to US$445.5 million, US$11.5 million and US$106.9 million, respectively.

Lower operating revenues in 2021 and 2022 were mainly due to the effects of COVID-19. As we continue to recover from the impact of, and disruptions caused by, COVID-19, such impact and disruptions could materially affect our business, prospects, financial condition and results of operations.

16

Table of Contents

Because neither we nor any of our subsidiaries hold a gaming license in Macau, Studio City Casino is operated by the Gaming Operator through the Studio City Casino Agreement under the Gaming Operator’s concession. Any failure by the Gaming Operator to comply with its obligations as a concessionaire or any failure by the Gaming Operator or us to comply with its or our respective obligations under the Studio City Casino Agreement, including any regulatory requirements thereunder, may have a material adverse effect on the operation of the Studio City Casino.

The Gaming Operator and our subsidiary, Studio City Entertainment, have entered into the Studio City Casino Agreement under which the Gaming Operator has agreed to operate Studio City Casino since we do not hold a gaming license in Macau. Under the Studio City Casino Agreement, the Gaming Operator, among other things, manages the day-to-day operations at the Studio City Casino, including determining the number and mix of gaming tables and gaming machines operated at the Studio City Casino, and recruits all casino staff, including dealers, cashiers, security and surveillance personnel and managers. The Gaming Operator deducts gaming taxes and the costs incurred in connection with its operations from Studio City Casino’s gross gaming revenues and we receive the residual amount and recognize such residual amount as revenue from the Studio City Casino Agreement. While the Studio City Casino Agreement obligates the Gaming Operator to manage the day-to-day operations of the Studio City Casino in a manner intended to appeal to the VIP and mass gaming markets at a standard of quality of service set by the Gaming Operator in line with the overall development and operational strategy determined by the Company, the Studio City Casino Agreement does not require the Gaming Operator to operate a minimum number of gaming tables or gaming machines at the Studio City Casino or any specified mix of gaming tables and gaming machines. Accordingly, while 250 gaming tables, including 15 gaming tables for VIP rolling chip operations, and 552 gaming machines are currently available for operation at the Studio City Casino, there is no assurance that such number and mix of gaming tables and gaming machines will be maintained by the Gaming Operator and the number of gaming tables and/or gaming machines may be reduced or increased by the Gaming Operator as it may determine pursuant to the terms and conditions of the Studio City Casino Agreement.

The Studio City Casino Agreement was initially approved by the Macau government and was subject to the satisfaction of certain conditions imposed by the Macau government on the Gaming Operator and us in connection with granting its approval. Such conditions included but were not limited to Studio City Entertainment being subject to Macau government supervision applicable to gaming concessionaires. Upon the execution of the amendment to the Studio City Casino Agreement on June 23, 2022, such conditions ceased to apply. As a substantial part of our revenues and cash flows are generated from the Gaming Operator’s operation of Studio City Casino, any failure by the Gaming Operator to comply with any statutory, contractual or any other duties imposed on it as a concessionaire, or any failure by the Gaming Operator or us to comply with its or our respective obligations under the Studio City Casino Agreement, may have a material adverse effect on the operation of Studio City Casino, including its suspension or cessation, and may cause the suspension or termination of the Gaming Operator’s concession.

Any changes in Macau’s gaming law or other requirements applicable to the concession granted to the Gaming Operator by the Macau government that necessitate amendments to, or termination of, the Studio City Casino Agreement, would have a material adverse effect on the operation of the Studio City Casino and, in turn, our financial condition and results of operations. If the Studio City Casino Agreement terminates, we may not be able to enter into a new similar agreement. In addition, any amended or replaced terms of the Studio City Casino Agreement may not be comparable to our current arrangements and may not be, totally or partially, acceptable to us. In addition, if the Gaming Operator’s concession terminates, the Gaming Operator will discontinue operating the Studio City Casino and the Studio City Casino Agreement will terminate and we may not be able to enter into an arrangement for the operation of Studio City Casino with another concessionaire on terms that are comparable or acceptable to us or at all, and the Studio City Casino premises and gaming equipment will revert or be transferred to the Macau government without compensation. Furthermore, the Gaming Operator has exclusive access to the customer database of the gaming operations at Studio City Casino and in the event of termination of the arrangement under the Studio City Casino Agreement, we may not be able to gain access to such database.

17

Table of Contents

Any material dispute with the Gaming Operator or any failure by the Gaming Operator to comply with its obligations under its concession, or by the Gaming Operator or us to comply with its or our respective obligations under, or any termination of, the Studio City Casino Agreement may have a material adverse effect on the operation of Studio City Casino and in turn affect our financial condition and results of operations and may also result in a default under the terms of our existing and/or future indebtedness obligations and other agreements.

We have a short operating history compared to many of our competitors and are therefore subject to significant risks and uncertainties. Our short operating history may not be indicative of our future operating results and prospects.

We have a short business operating history compared to many of our competitors, and there is limited historical information available about us upon which you can base your evaluation of our business and prospects. Studio City commenced operations in October 2015 and Phase 2 progressively opened in April and September of 2023. As a result, you should consider our business and prospects in light of the risks, expenses, uncertainties and challenges that we may face given our short operating history in the intensely competitive market of the gaming business. The historical performance at the other casinos operated by the Gaming Operator should not be taken as an indication of Studio City Casino’s future performance or the performance of our Phase 2 project.

We may encounter risks and difficulties frequently experienced by companies with early stage operations, and those risks and difficulties may be heightened by challenging market conditions of the gaming business in Macau and other challenges our business faces. Certain of these risks relate to our ability to:

| • | operate, support, expand and develop our operations and our facilities, including new operations and facilities introduced with Phase 2; |

| • | respond to economic uncertainties, including the social and economic disruptions caused by the COVID-19 outbreaks and other global or regional health events; |

| • | respond to competitive market conditions; |

| • | fulfill conditions precedent to draw down or roll over funds from current and future credit facilities; |

| • | comply with covenants under our existing and future debt issuances and credit facilities; |

| • | respond to changing financial requirements and raise additional capital, as required; |

| • | attract and retain customers and qualified staff; |

| • | maintain effective control of our operating costs and expenses; |

| • | maintain internal personnel, systems, controls and procedures to assure compliance with the extensive regulatory requirements applicable to our business as well as regulatory compliance as a public company; and |

| • | assure compliance with, and respond to changes in, the regulatory environment and government policies. |

If we are unable to successfully manage one or more of such risks, we may be unable to operate our businesses in the manner we contemplate and generate revenues in the amounts and at the rate we anticipate. If any of these events were to occur, it may have a material adverse effect on our business, prospects, financial condition, results of operations and cash flows.

We rely on services provided by subsidiaries of Melco Resorts, including hiring and training of personnel for Studio City.

According to the Studio City Casino Agreement, the Gaming Operator, a subsidiary of Melco Resorts, is responsible for the operation of the Studio City Casino facilities, including hiring, employing, training and

18

Table of Contents

supervising casino personnel. The Gaming Operator deducts gaming taxes and the costs incurred in connection with its operations, including staff costs from Studio City Casino’s gross gaming revenues. We expect the Gaming Operator to continue managing all recruitment and training-related matters for staff that have been deployed at Studio City Casino.

In addition, under the Management and Shared Services Arrangements, we receive certain services from certain members of the Melco Resorts group. We rely on the Master Service Providers to recruit, allocate, train, manage and supervise a substantial majority of the staff who are all solely dedicated to our property to perform our corporate and administrative functions and carry out other non-gaming activities, including food and beverage management, retail management, hotel management, entertainment projects, mall development and sales and marketing activities, among others. In addition, pursuant to the Management and Shared Services Arrangements, certain shared services staff including certain senior management from the Master Service Providers are not solely dedicated to our property and may not devote all of their time and attention to the operation of Studio City. These shared services staff work for other properties owned by Melco Resorts, which may directly and indirectly compete with us. Any expansion of the business of Melco Resorts, whether effectuated through the Gaming Operator or other companies, could divert the attention and time of these shared services staff from the operations of Studio City and adversely affect us.

With the lifting of COVID-19 travel restrictions in Macau and the increase in business volumes and opening of Phase 2, Studio City will need more personnel to operate at full capacity, with a significant portion of these vacancies expected to be filled by non-resident workers for which Macau government-issued quotas are required. If the Gaming Operator or the Master Service Providers are unable to attract and retain a sufficient number of qualified staff or to provide satisfactory services to us or the costs of qualified staff increase significantly, our business, financial condition and results of operations could be materially and adversely affected.

The costs associated with the Studio City Casino Agreement and the Management and Shared Services Arrangements may not be indicative of the actual costs we could have incurred as an independent company.

Under the Studio City Casino Agreement, the Gaming Operator deducts gaming taxes and the costs of operation of Studio City Casino. We receive the residual gross gaming revenues and recognize these amounts as our revenue from casino contract.

Under the Management and Shared Services Arrangements, certain of our corporate and administrative functions as well as operational activities are administered by staff employed by certain subsidiaries of Melco Resorts, including senior management services, centralized corporate functions and operational and venue support services. Payment arrangements for the services are provided for in the individual work agreements and may vary depending on the services provided. Corporate services are charged at pre-negotiated rates, subject to a base fee and cap. Senior management service fees and staff costs on operational services are allocated to us based on percentages of efforts on the services provided to us. Other costs in relation to shared office equipment are allocated based on a percentage of usage.

We believe the costs incurred under the Studio City Casino Agreement and the allocation methods under the Management and Shared Services Arrangements are reasonable and the consolidated financial statements reflect our cost of doing business. However, such allocations may not be indicative of the actual expenses we would have incurred had we operated as an independent company.

19

Table of Contents

We face concentration risk in relation to our sole operation of Studio City.

We are dependent upon the operation of Studio City to generate our revenue and cash flows. Given that our operations are conducted only at Studio City in Macau, we are subject to greater risks than a company with several operating properties in several markets. These risks include, but are not limited to:

| • | changes in Macau laws and regulations, including gaming laws and regulations, or interpretations thereof, as well as PRC travel and visa policies; |

| • | dependence on the gaming, tourism and leisure market in Macau; |

| • | limited diversification of our business and sources of revenue; |

| • | a decline in air, land or ferry passenger traffic to Macau from the PRC or other areas or countries due to higher ticket costs, fears concerning travel, travel restrictions or otherwise, including as a result of the outbreak of widespread health epidemics or pandemics, such as the outbreak of COVID-19; |

| • | a decline in economic and political conditions in Macau, the PRC or Asia; |

| • | an increase in competition within the gaming industry in Macau or generally in Asia; |

| • | inaccessibility to Macau due to inclement weather, road construction or closure of primary access routes; |

| • | austerity measures imposed now or in the future by the governments in the PRC or other countries in Asia; |

| • | tightened control of cross-border fund transfers, foreign exchange and/or anti-money laundering regulations or policies effected by the PRC or Macau governments; |

| • | any enforcement or legal measures taken by the PRC government to deter gaming activities and/or marketing thereof; |

| • | lower than expected rate of increase or decrease in the number of visitors to Macau; |

| • | natural and other disasters, including typhoons, outbreaks of infectious diseases, terrorism or violent criminal activities, affecting Macau; |

| • | relaxation of regulations on gaming laws in other regional economies that could compete with the Macau market; |

| • | government restrictions on growth of gaming markets, including policies on gaming table allocation and caps; and |

| • | a decrease in gaming activities and other spending at Studio City Casino. |

See also “Risks Relating to Conducting Business and Operating in Macau.”

Any of these developments or events could have a material adverse effect on our business, cash flows, financial condition, results of operations and prospects.

Furthermore, Macau is a limited gaming concession market nearing its land capacity for the development of integrated resorts and there are no opportunities to expand our operations.

Studio City Casino’s VIP rolling chip operations may cause volatility in our financial condition and results of operations due to changes in the economic and regulatory environments and Studio City Casino’s ability to attract and retain VIP rolling chip players.

Studio City Casino has and is expected to incur costs associated with the VIP rolling chip operations, while the expected revenues to be generated from the VIP rolling chip operations may be volatile primarily due

20

Table of Contents

to high bets and the resulting high winnings and losses. Gross win per VIP table per day were approximately US$8,400, US$2,000 and US$2,400 in 2023, 2022 and 2021, respectively. VIP rolling chip operations are also more vulnerable to changes in the economic environment and therefore inherently more volatile than mass market operations. Moreover, VIP rolling chip operations may involve commissions to gaming promoters, if any are engaged to provide services to Studio City Casino, and, as a result, the margins associated with VIP rolling chip operations are usually lower than the margins for the mass market operations and may be volatile from period to period due to significant variances in winnings and losses. As a result, Studio City Casino’s business, results of operations and cash flows may become more volatile, while VIP rolling chip operations continue, compared to that of other casinos with only mass market gaming operations.

Further, the VIP rolling chip players pool is limited and we cannot assure you that the existing VIP rolling chip players at Studio City Casino will be recurring players. If Studio City Casino loses its existing VIP rolling chip players or fails to attract new VIP rolling chip players, our revenues and cash flows from the revenue from casino contract could be materially and adversely affected. In addition, the VIP rolling chip segment may be particularly susceptible to certain changes in government policies, regulations and enforcement actions. For instance, the anti-corruption campaign of the PRC government has had a negative effect on the VIP rolling chip segment in Macau. In addition, in November 2021, the Court of Final Appeal in Macau issued a final unappealable decision that a gaming operator is jointly liable with a gaming promoter for the refund of funds deposited with such gaming promoter and the Macau authorities arrested executives from a gaming promoter for alleged illegal overseas gaming related activities. In January 2022, the Macau authorities also arrested an executive from another gaming promoter and certain related individuals and certain of these individuals were sentenced to jail terms in addition to the payment of monetary compensation to the Macau government in January 2023. Any further changes in government policies, regulations and enforcement actions may negatively affect the numbers of VIP rolling chip players in Macau and in turn, may materially and adversely affect our business.

We have a history of net losses and may not achieve profitability in the future.

Studio City may not be financially successful or generate the cash flows that we anticipate. We generated net income attributable to Studio City International Holdings Limited of US$33.6 million for the years ended December 31, 2019, while we had net losses attributable to Studio City International Holdings Limited of US$133.5 million, US$326.5 million, US$252.6 million, US$321.6 million, US$21.6 million, US$76.4 million and US$242.8 million for the years ended December 31, 2023, 2022, 2021, 2020, 2018, 2017 and 2016, respectively, primarily because of the impact of COVID-19 outbreaks in the case of the years ended December 31, 2022, 2021 and 2020 and also due to Studio City having commenced operations only in October 2015 and was ramping up operations. In addition, we incurred negative operating cash flows of US$18.9 million, US$178.8 million, US$136.8 million, US$167.4 million and US$113.1 million in 2023, 2022, 2021, 2020 and 2015, respectively.

We expect our costs and expenses to increase in absolute amounts due to the continued expansion of our operations, which will cause us to incur increased costs and expenses associated with the operation of our businesses.

We also expect that we will continue to incur capital expenditures as we continue to expand our existing operations. These efforts may be more costly than we expect and our revenue may not increase sufficiently to offset these expenses. We may continue to take actions and make investments that do not generate optimal short-term financial results and may even result in increased operating losses in the short term with no assurance that we will eventually achieve the intended long-term benefits or profitability. These factors may adversely affect our ability to achieve profitability and service debt obligations and interest payments under any of our existing or future financing facilities.

21

Table of Contents

We have a substantial amount of existing indebtedness and may incur additional indebtedness, which could have significant effects on our business and future operations.

We have a substantial amount of existing indebtedness. As of December 31, 2023, we had total principal amount of outstanding indebtedness of US$2.35 billion, representing the outstanding principal balances of our existing notes and credit facility. See “Item 5. Operating and Financial Review and Prospects — B. Liquidity and Capital Resources — Indebtedness.” Significant interest and principal payments are required to meet our obligations under the existing indebtedness. This substantial indebtedness could have important consequences for you and significant effects on our business and future operations. For example: