UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

OR

For the fiscal year ended December 31 , 2023

OR

OR

Commission file number 001-35788

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Ordinary Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S‐T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer," "accelerated filer" and "emerging growth company” in Rule 12b-2 of the Exchange Act.

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange

Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ International Financial Reporting Standards as issued by the International Accounting Standards

Board ☒ Other ☐

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

Table of contents

| Management report | Page | ||||

| Introduction | |||||

| Company overview | |||||

| History and development of the Company | |||||

| Cautionary Statement regarding forward-looking statements | |||||

Key transactions and events in 2023 | |||||

Sustainable development highlights - striving to be a leader in the decarbonization of the steel industry | |||||

Risk Factors and Control | |||||

| Business overview | |||||

| Business strategy | |||||

| Research and development | |||||

| Sustainable development | |||||

| Products | |||||

| Sales and marketing | |||||

| Intellectual property | |||||

| Government regulations | |||||

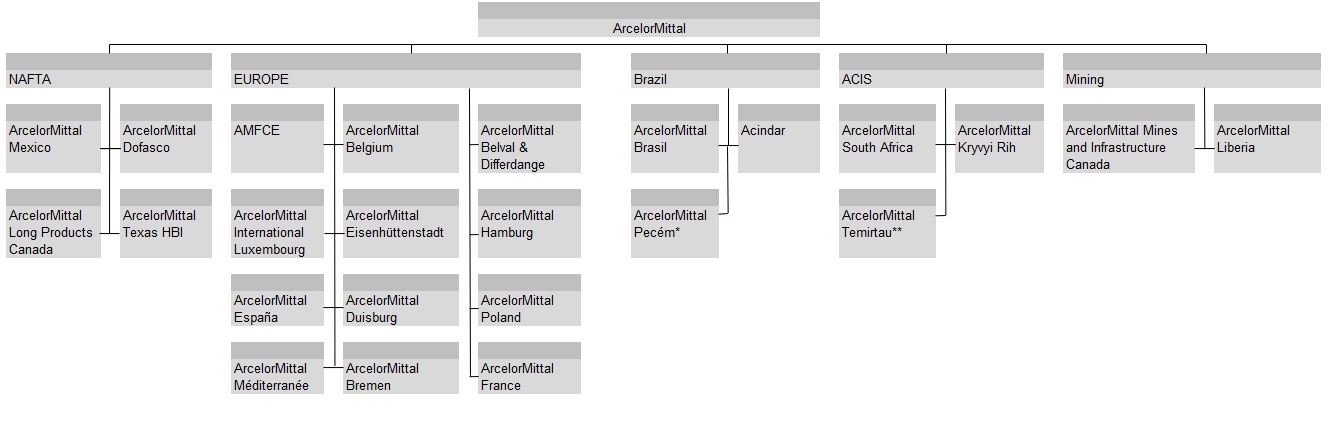

| Organizational structure | |||||

| Properties and capital expenditures | |||||

| Property, plant and equipment | |||||

| Capital expenditures | |||||

Mineral reserves and resources | |||||

| Operating and financial review | |||||

| Key factors affecting results of operations | |||||

| Operating results | |||||

| Liquidity and capital resources | |||||

| Disclosures about market risk | |||||

| Outlook | |||||

| Management and employees | |||||

| Directors and senior management | |||||

| Compensation | |||||

| Employees | |||||

| Corporate governance | |||||

| Shareholders and markets | |||||

| Major shareholders | |||||

| Related party transactions | |||||

| Markets | |||||

| New York Registry Shares | |||||

| Dividend distributions | |||||

| Purchases of equity securities by the issuer and affiliated purchasers | |||||

| Share capital | |||||

| Additional information | Page | ||||

| Memorandum and Articles of Association | |||||

| Material contracts | |||||

| Exchange controls and other limitations affecting security holders | |||||

| Taxation | |||||

| Evaluation of disclosure controls and procedures | |||||

| Management’s report on internal control over financial reporting | |||||

| Principal accountant fees and services | |||||

| Glossary - definitions, terminology and principal subsidiaries | |||||

| Exhibits | |||||

| Signature | |||||

Reports of Independent Registered Public Accounting Firms ( (Deloitte Audit S.à r.l., PCAOB ID | |||||

| Consolidated financial statements | |||||

| Consolidated statements of operations | |||||

| Consolidated statements of other comprehensive income | |||||

| Consolidated statements of financial position | |||||

| Consolidated statements of changes in equity | |||||

| Consolidated statements of cash flows | |||||

| Notes to the consolidated financial statements | |||||

Form 20-F Cross Reference Guide

| Item | Form 20-F Caption | Reference in current report | Page | ||||||||

| Glossary - definitions, terminology and principal subsidiaries | |||||||||||

Cautionary statement regarding forward-looking statements | Cautionary statement regarding forward-looking statements | ||||||||||

Part I | |||||||||||

Item 1. | Identity of Directors, Senior Management and Advisers | Not applicable | |||||||||

Item 2. | Offers Statistics and Expected Timetable | Not applicable | |||||||||

Item 3. | Key Information | ||||||||||

A. | [Reserved] | Not applicable | |||||||||

B. | Capitalization and indebtedness | Not applicable | |||||||||

C. | Reasons for the offer and use of proceeds | Not applicable | |||||||||

Risk Factors and Control | |||||||||||

Item 4. | Information on the Company | ||||||||||

History and development of the Company, Key transactions and events in 2023, Recent Developments, Sustainable development highlights - striving to be a leader in the decarbonization of the steel industry, Capital expenditures, Raw materials, Sources and uses of cash | |||||||||||

| Business strategy, Market information, Competitive strengths, Sustainable development, Products, Sales and marketing, Insurance, Intellectual property, Government regulations, Risk management process | |||||||||||

| Organizational structure | |||||||||||

| Property, plant and equipment, Capital expenditures, Reserves and Resources (iron ore and coal) | |||||||||||

Item 4A. | Unresolved staff comments | None | |||||||||

Item 5. | Operating and Financial Review and Prospects | ||||||||||

| Key factors affecting results of operations, Operating results | |||||||||||

| Liquidity and capital resources | |||||||||||

C. | Research and development, patents and licenses, etc. | Competitive strengths, Research and development | |||||||||

| Outlook and Key factors affecting results of operations | |||||||||||

E. | Critical Accounting Estimates | Critical accounting policies and use of judgments and estimates | |||||||||

Item 6. | Directors, Senior Management and Employees | ||||||||||

| Directors and senior management | |||||||||||

| Compensation | |||||||||||

| Corporate governance, Directors and senior management | |||||||||||

| Employees | |||||||||||

| Management share ownership, Compensation | |||||||||||

| F. | Disclosure of a registrant’s action to recover erroneously awarded compensation. | Not applicable | |||||||||

Item 7. | Major Shareholders and Related Party Transactions | ||||||||||

| Major shareholders | |||||||||||

| Related party transactions | |||||||||||

C. | Interest of experts and counsel | Not applicable | |||||||||

Item 8. | Financial Information | ||||||||||

A. | Consolidated statements and other financial information | Consolidated financial statements as of and for the year ended December 31, 2023, Export sales, Legal proceedings, Dividend distribution | |||||||||

B. | Significant changes | Not applicable | |||||||||

Item 9. | The Offer and Listing | ||||||||||

A. | Offer and listing details | Markets | |||||||||

B. | Plan of distribution | Not applicable | |||||||||

| Markets | |||||||||||

D. | Selling shareholders | Not applicable | |||||||||

E. | Dilution | Not applicable | |||||||||

F. | Expenses of the issue | Not applicable | |||||||||

Item 10. | Additional Information | ||||||||||

| Share capital | |||||||||||

| Memorandum and Articles of Association | |||||||||||

| Material contracts | |||||||||||

| Exchange controls and other limitations affecting security holders | |||||||||||

| Taxation | |||||||||||

F. | Dividends and paying agents | Paying agents and Earnings distribution | |||||||||

G. | Statements by experts | Reserves and Resources (iron ore and coal) and Exhibits 15.1, 15.2, 15.3, 15.4, 15.5, 15.6, 15.7, 15.8, 15.9, 15.10, 15.11 and 15.12 | |||||||||

H. | Documents on display | History and development of the Company | |||||||||

I. | Subsidiary information | Not applicable | |||||||||

| J. | Annual Report to Security Holders | Not applicable | |||||||||

Item 11. | Disclosures about market risk | ||||||||||

Item 12. | Description of Securities Other Than Equity Securities | ||||||||||

A. | Debt Securities | Not applicable | |||||||||

B. | Warrants and Rights | Not applicable | |||||||||

C. | Other Securities | Not applicable | |||||||||

| New York Registry Shares | |||||||||||

Part II | |||||||||||

Item 13. | Defaults, Dividend Arrearages and Delinquencies | None | |||||||||

Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | None | |||||||||

Item 15. | Controls and Procedures | Evaluation of disclosure controls and procedures, Management’s report on internal control over financial reporting and Internal control procedures | |||||||||

Item 16A. | Audit committee financial expert | Corporate governance | |||||||||

Item 16B. | Code of Ethics | Corporate governance — Code of Business Conduct | |||||||||

Item 16C. | Principal Accountant Fees and Services | Principal accountant fees and services | |||||||||

Item 16D. | Exemptions from the Listing Standards for Audit Committees | None | |||||||||

Item 16E. | Purchases of equity securities by the issuer and affiliated purchasers | ||||||||||

Item 16F. | Change in Registrant’s Certifying Accountant | Not applicable | |||||||||

Item 16G. | Corporate Governance | Corporate governance | |||||||||

| Item 16H. | Mine Safety Disclosure | Not applicable | |||||||||

| Item 16I. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | Not applicable | |||||||||

Item 16J. | Insider Trading Policies | Not applicable | |||||||||

Item 16K | Cybersecurity | Risk Factors and Control — Cybersecurity | |||||||||

Part III | |||||||||||

Item 17. | Financial statements | Consolidated financial statements | |||||||||

Item 18. | Financial statements | Consolidated financial statements | |||||||||

Item 19. | Exhibits | Exhibits | |||||||||

| Management report | ||

INTRODUCTION

Company overview

ArcelorMittal is one of the world’s leading integrated steel and mining companies. ArcelorMittal is the largest steel producer in Europe and among the largest in the Americas, and a growing presence in Asia including India through its joint venture AMNS India.

*Iron ore production includes production from ArcelorMittal Mining Canada G.P. and ArcelorMittal Infrastructure G.P. ("AMMC"), ArcelorMittal Liberia and captive mines.

ArcelorMittal has steel-making operations in 15 countries, including 37 integrated and mini-mill steel-making facilities. As of December 31, 2023, ArcelorMittal had approximately 126,756 employees.

ArcelorMittal produces a broad range of high-quality finished and semi-finished steel products ("semis"). Specifically, ArcelorMittal produces flat products, including sheet and plate, and long products, including bars, rods and structural shapes. It also produces pipes and tubes for various applications. ArcelorMittal sells its products primarily in local markets and to a diverse range of customers in approximately 140 countries, including the automotive, appliance, engineering, construction and machinery industries. ArcelorMittal’s mining operations produce various types of mining products including iron ore lump, fines, concentrate, pellets, sinter feed and coking coal.

As a global steel producer, the Company is able to meet the needs of different markets. Steel consumption and product requirements clearly differ between developed markets and developing markets. Steel consumption in developed economies is weighted towards flat products and a higher value-added mix, while developing markets utilize a higher proportion of long

products and commodity grades. To meet these diverse needs, the Company maintains a high degree of product diversification and seeks opportunities to increase the proportion of higher value-added products in its product mix.

History and development of the Company

ArcelorMittal results from the merger in 2007 of its predecessor companies Mittal Steel Company N.V. and Arcelor, each of which had grown through acquisitions over many years. Since its creation ArcelorMittal has experienced periods of external growth as well as consolidation and deleveraging (including through divestment).

ArcelorMittal's success is built on its core values of sustainability, safety, quality and leadership and the entrepreneurial boldness that has empowered its emergence as the first truly global steel and mining company. Acknowledging that a combination of structural issues and macroeconomic conditions will continue to challenge returns in its sector, the Company has adapted its footprint to the new demand realities, redoubled its efforts to control costs and repositioned its operations with a view toward outperforming its competitors. ArcelorMittal’s research and development capability is strong and includes several major research centers as well as strong academic partnerships with universities and other scientific bodies.

Against this backdrop, ArcelorMittal's strategy is to leverage four distinctive attributes that will enable it to capture leading positions in the most attractive areas of the steel industry’s value chain, from mining at one end to distribution and first-stage processing at the other: global scale and scope; superior technical capabilities; a diverse portfolio of steel and related businesses, one of which is mining; and financial capabilities. The Company’s strategy is further detailed under “Business overview—Business strategy”.

ArcelorMittal’s steel-making operations have a high degree of geographic diversification. In 2023, approximately 39%

of its crude steel was produced in the Americas, approximately 50% was produced in Europe and approximately 11% was produced in other countries, such as South Africa and Ukraine. In addition, ArcelorMittal’s sales of steel products are spread over both developed and developing markets, which have different consumption characteristics. ArcelorMittal’s mining operations, including captive mines are present in North America, South America, Africa, Europe and the CIS region. Captive mines are integrated into the Company's global steel-making facilities.

3

| Management report | ||

Competitive strengths

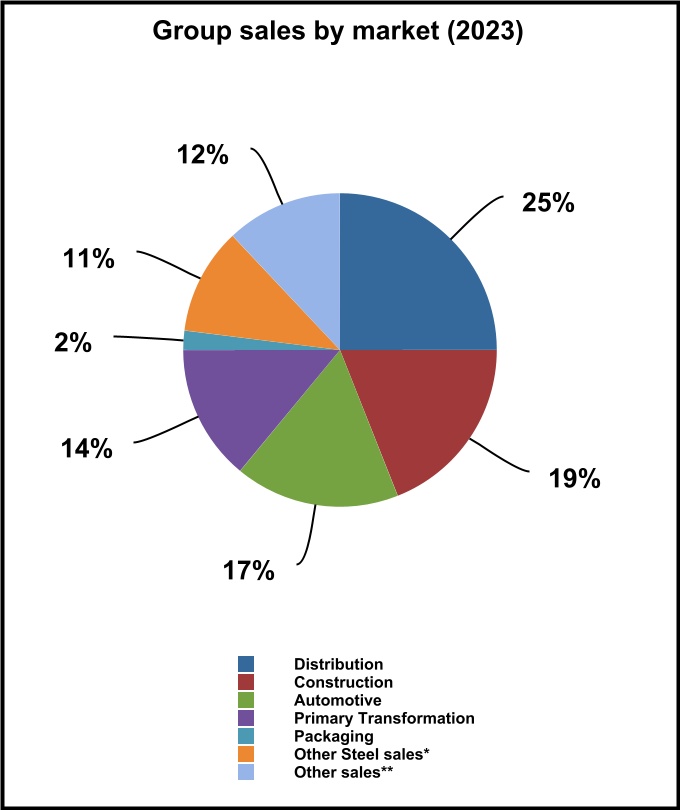

As shown by the following graph, ArcelorMittal has a diversified portfolio of steel and mining products to meet a wide range of customer needs across many steel-consuming sectors, including automotive, appliance, engineering, construction, energy and machinery and via distributors.

* Other steel sales mainly represent metal processing, machinery, electrical equipment and domestic appliances

**Other sales mainly represent mining, chemicals & water, slag, waste, sale of energy and shipping

The Company believes that the following factors contribute to ArcelorMittal’s success in the global steel and mining industry:

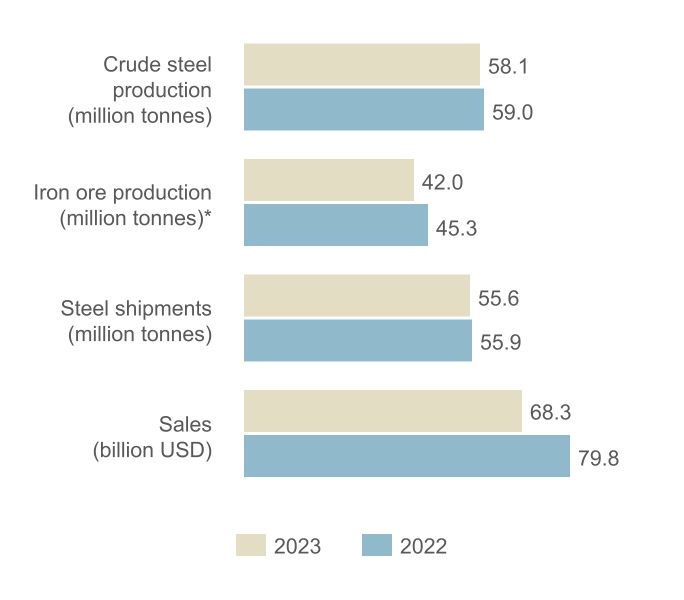

Market leader in steel. ArcelorMittal had annual achievable production capacity of approximately 81.0 million tonnes of crude steel for the year ended December 31, 2023. Steel shipments for the year ended December 31, 2023 totaled 55.6 million tonnes. ArcelorMittal has significant operations in many countries which are described in "Properties and capital expenditures". In addition, many of ArcelorMittal’s operating units have access to developing markets that are expected to experience, over time, above-average growth in steel consumption (such as Central and Eastern Europe, South America, India, Africa, CIS and Southeast Asia).

The Company sells its products in local markets and through a centralized marketing organization to customers in approximately 140 countries. ArcelorMittal’s diversified product offering, together with its distribution network and research and development (“R&D”) programs, enable it to build strong relationships with customers, which include many of the world’s major automobile and appliance manufacturers. The Company is a strategic partner to many major original equipment manufacturers (“OEMs”) and has the capability to build long-term contractual relationships with them based on early vendor involvement, contributions to global OEM platforms and common value-creation programs.

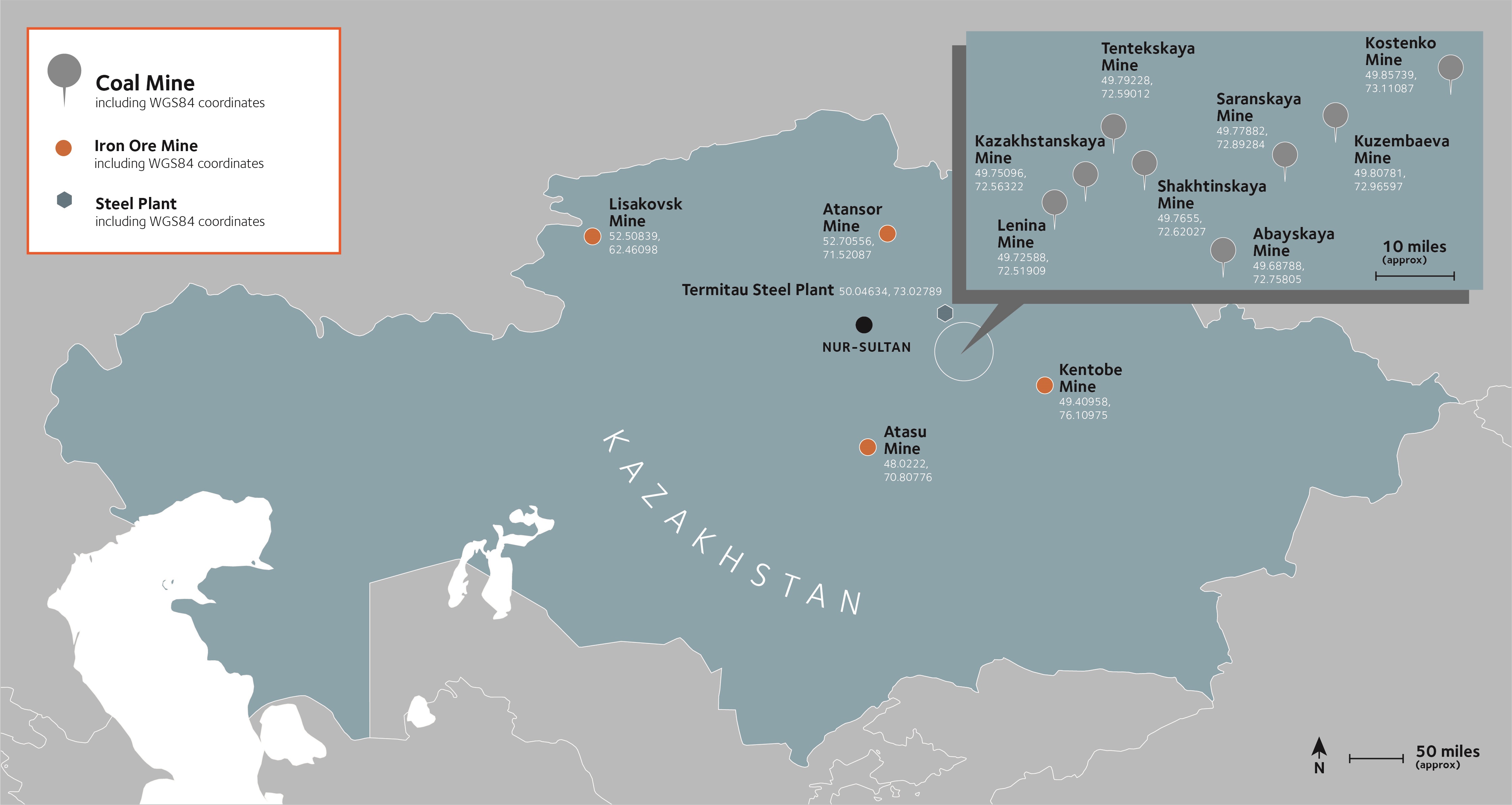

A world-class mining business. ArcelorMittal has a global portfolio of 9 (following the disposal of Kazakhstan iron ore and coal mining operations) operating units with mines in operation and development and is among the largest iron ore producers in the world. In 2023, ArcelorMittal sourced a large portion of its raw materials from its own mines and facilities including leases. The table below reflects ArcelorMittal's self-sufficiency through its mining operations in 2023.

| Millions of metric tonnes | Consumption | Sourced from own mines/facilities2, 3 | Self-sufficiency % | ||||||||||||||||||||

| Iron ore | 74.1 | 42.0 | 57% | ||||||||||||||||||||

PCI & coal1 | 29.9 | 2.0 | 7% | ||||||||||||||||||||

| Coke | 17.3 | 17.0 | 98% | ||||||||||||||||||||

| Scrap & DRI | 26.1 | 15.5 | 59% | ||||||||||||||||||||

1.Includes coal only for the steelmaking process and excludes steam coal for power generation. ArcelorMittal's consumption of PCI and coal was 5.8 million tonnes and 24.1 million tonnes, respectively, for the year ended December 31, 2023.

2.Assumes 100% consumption of ArcelorMittal's iron ore and coal shipments.

3.Includes Kazakhstan iron ore and coal mining operations, which were sold on December 7, 2023. Iron ore and coal production is included in the table through the transaction closing date. See "Properties and capital expenditures—Mineral reserve and resources" and "Introduction—Key transactions and events in 2023".

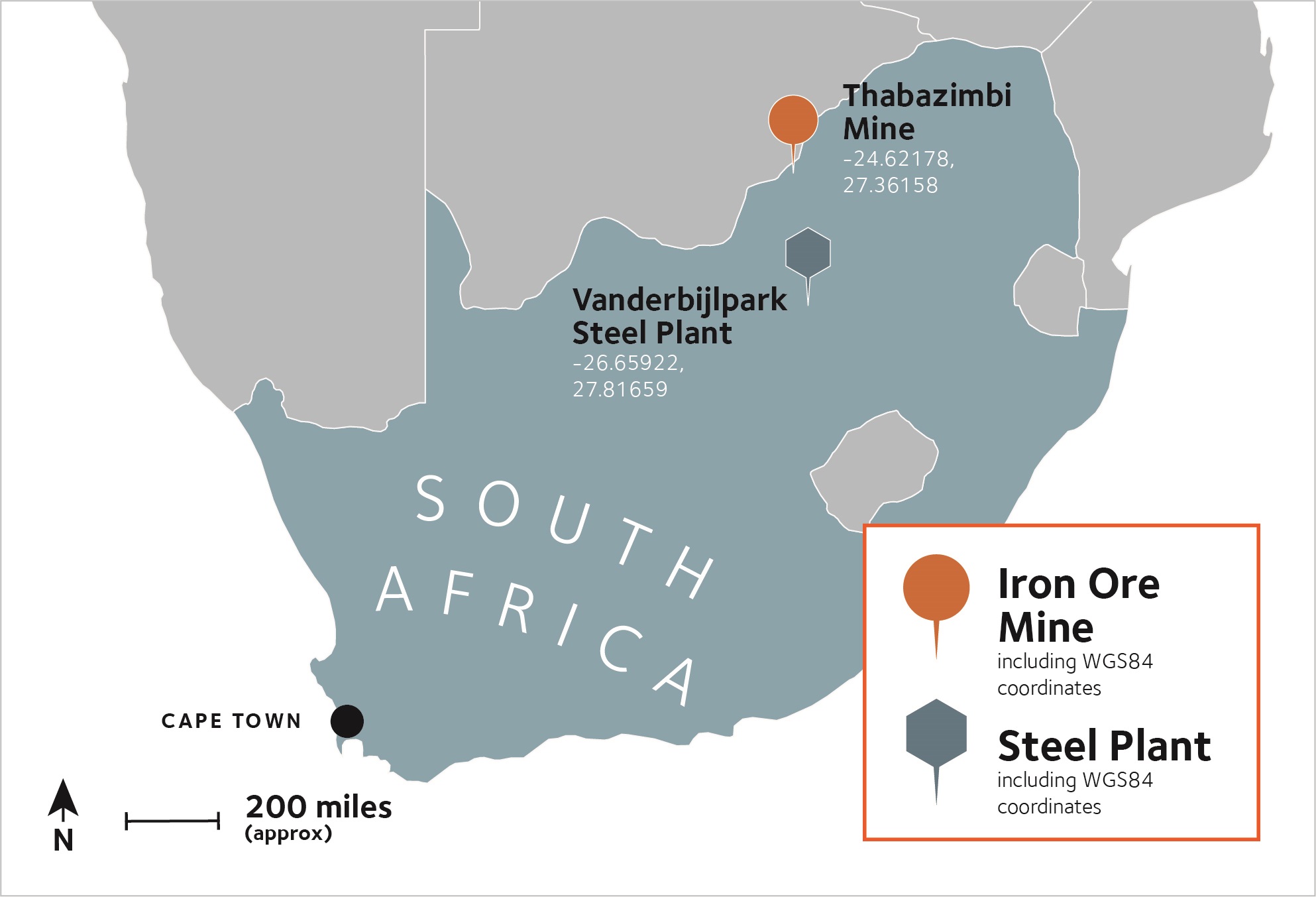

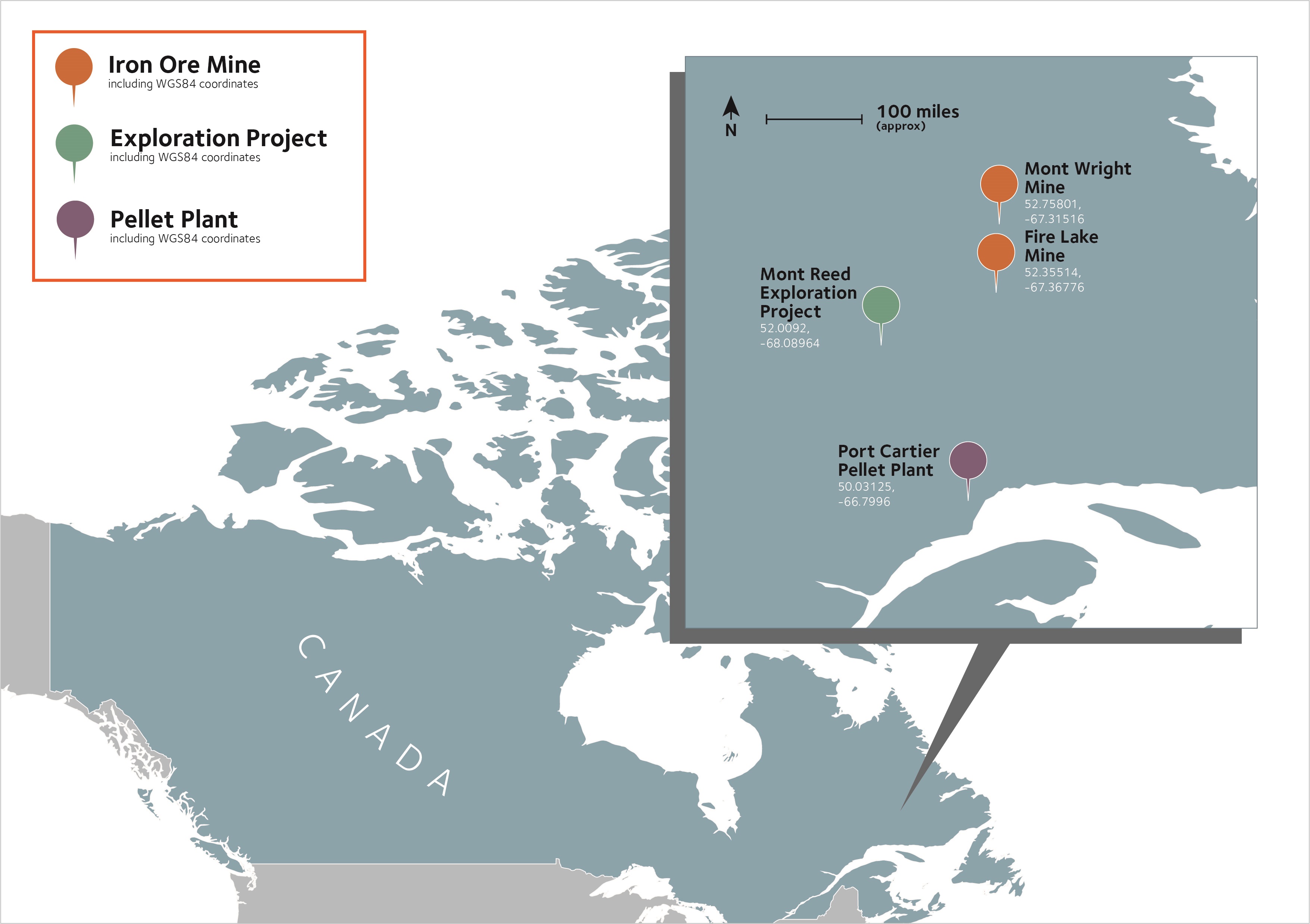

The Company has iron ore mining activities in Brazil, Bosnia, Canada, Liberia, Mexico, Ukraine, South Africa and through its joint venture in India and associate in Canada (Baffinland). On December 7, 2023, the Company divested its mining operations in Kazakhstan in the context of the sale of ArcelorMittal Temirtau, see "—Key transactions and events in 2023". ArcelorMittal’s main mining products include iron ore lump, fines, concentrate, pellets and sinter feed. In addition, ArcelorMittal produces substantial amounts of direct reduced iron ("DRI") which is a scrap substitute used in its mini-mill facilities to supplement external metallic purchases and also a vital material for the production of steel through the electric arc furnace ("EAF") route which will grow substantially in the context of decarbonization. As of December 31, 2023, ArcelorMittal’s iron ore reserves (including reserves at mines where ArcelorMittal owns less than 100%, based on ArcelorMittal's

4

| Management report | ||

ownership percentage even if ArcelorMittal is entitled to mine all the reserves, and including reserves for which use is restricted) were estimated at 3,937 million tonnes run of mine. See “Properties and capital expenditures—Mineral reserves and resources” for a detailed list of the entities with mineral reserves and resources and ownership structure. The Company’s long-life iron ore reserves and resources provide a measure of security of supply and an important natural hedge against raw material volatility and global supply constraints. The seaborne iron ore mining business is managed as a separate segment which enhances ArcelorMittal’s ability to optimize capital allocation.

ArcelorMittal’s facilities have good access to shipping facilities, including through ArcelorMittal’s own, or partially owned, 17 deep-water port facilities and linked railway sidings.

Market-leading automotive steel business. ArcelorMittal has a leading market share (approximately 15% of the worldwide market) in automotive, and is a leader in the fast-growing advanced high-strength steels ("AHSS") segment, specifically for flat products. ArcelorMittal is the first steel company in the world to embed its own engineers within an automotive customer to provide engineering support. The Company begins working with OEMs as early as five years before a vehicle reaches the showroom, to provide generic steel solutions, co-engineering and help with the industrialization of the project. These relationships are founded on the Company’s continuing investment in R&D and its ability to provide well-engineered solutions that help make vehicles lighter, safer and more fuel-efficient.

In 2023, ArcelorMittal extended the S-in Motion® catalog according to the automotive market trends. The S-in Motion® battery electric vehicles ("BEV") catalog of steel solutions has been adapted to include specific products for BEV's including new designs focused on battery protection. Advanced and especially ultra-high strength steels, innovative press hardened steels, and laser welded blanks are especially highlighted as key solutions for optimal performance (passenger safety/lightweighting) and battery protection. The growth of various types of electric vehicles will impact design and manufacturing leading to demand for different materials and steel grades, and more AHSS for battery protection. For instance, both the battery box and body structure have to protect the battery in the event of a crash. AHSS products are among the most affordable solutions on the market for these specific applications. In a context where the supply of electric vehicles, and especially BEVs, is expected to grow quickly.

Recently, the automotive industry’s priority has turned towards the simplification of the vehicle manufacturing complexity linked to the rising importance of electrical vehicles. ArcelorMittal’s response is the ArcelorMittal Multi-Part Integration™ ("MPI")

concept integrating a large number of parts into one single component combining PHS (Usibor®) and laser welding technology. On top of further lightweighting opportunities, the new solutions offer concepts to simplify operations by optimizing the amount of robots, by reducing the shop floor size, and by cutting the hours of labor per vehicle in the assembly shop by up to 30%. These achievements were mainly possible with the combination of extra-large laser welded blanks and the new generation of Press Hardening steels Usibor® 2000 and Ductibor® 1000.

In the automotive industry, ArcelorMittal mainly supplies the geographic markets where its production facilities are located, which are Europe, North and South America, South Africa and China through Valin ArcelorMittal Automotive Steel Co., Ltd (“VAMA”), a joint venture with Hunan Valin. VAMA’s product mix is oriented toward higher value products and mainly toward the OEMs to which the Company sells tailored solutions based on its products. With sales and service offices worldwide and production facilities in North and South America, South Africa, Europe and China, ArcelorMittal believes that it is uniquely positioned to supply global automotive customers with the same products worldwide. The Company has multiple joint ventures and has also developed a global downstream network of partners through its distribution solutions activities. This provides the Company with a proximity advantage in virtually all regions where its global customers are present.

Examples of MPI are the rear H-Frame and the double door ring. Following the launch of H-frame project in China with Dongfeng Voyah in 2022, the Company launched several new projects in 2023 (including designing and structure strengthening projects) for OEMs. Furthermore, after the initial success of MPI Door-Ring concepts in the U.S. and China with both legacy and newcomer OEMs, in 2023, the Company succeeded in a breakthrough of the Door-Ring concept with several OEMs in Europe as well. As of December 31, 2023, more than 50 different vehicles are designed by ArcelorMittal with the Door-Ring concept and approximately 100 projects are currently in progress.

Sustainability (with focus on CO2 emission reduction in the supply chain) has become a key requirement in the automotive industry linked to the importance of sustainability in the holistic electrical vehicle marketing concept. In 2021, ArcelorMittal launched two solutions under the XCarb™ brand: XCarb™ green steel certificates and XCarb™ recycled and renewably produced ("RRP"), which was well received in automotive industry and markets. The first XCarb® RRP steels were successfully launched in Europe and in North America, exhibiting potential for reduction in CO2 emissions. In 2023, the Company entered into an agreement with General Motors for supplying XCarb® RRP steels in North America.

5

| Management report | ||

For further details on the new products under development, see "Business overview—Research and development”.

Diversified and efficient producer. As a global steel manufacturer with a leading position in many markets, ArcelorMittal benefits from scale and production cost efficiencies in various markets and a measure of protection against the cyclicality of the steel industry and raw materials prices.

•Diversified production process. In 2023, approximately 43.2 million tonnes of crude steel were produced through the basic oxygen furnace process ("BOF") and approximately 14.9 million tonnes through the electric arc furnace ("EAF") process. This provides ArcelorMittal with greater flexibility in its raw material and energy use, and increased ability to meet varying customer requirements in the markets it serves.

•Product and geographic diversification. By operating a portfolio of assets diversified across product segments and geographic areas, ArcelorMittal benefits from a number of natural hedges. As a global steel producer with a broad range of high-quality finished and semi-finished steel products, ArcelorMittal is able to meet the needs of diverse markets. Steel consumption and product requirements vary between mature economy markets and developing economy markets. Steel consumption in mature economies is largely from flat products and a higher value-added mix, while developing markets utilize a higher proportion of long products and commodity grades. As developing economies mature and markets evolve, local customers will require increasingly advanced steel products. To meet these diverse needs, ArcelorMittal maintains a high degree of product diversification and seeks opportunities to increase the proportion of its product mix consisting of higher value-added products.

•Upstream integration. ArcelorMittal believes that its own raw material production provides it with a competitive advantage over time. Additionally, ArcelorMittal benefits from the ability to optimize its steel-making facilities’ efficient use of raw materials, its global procurement strategy and the implementation of Company-wide knowledge management practices with respect to raw materials. Certain of the Company’s operating units also have access to infrastructure, such as deep-water port facilities, railway sidings and engineering workshops that lower transportation and logistics costs.

•Downstream integration. ArcelorMittal’s downstream integration, primarily through its Europe segment for distribution solutions, enables it to provide customized steel solutions to its customers more effectively. The

Company’s downstream assets have cut-to-length, slitting and other processing facilities, which provide value additions and help it to maximize operational efficiencies.

Dynamic responses to market challenges and opportunities. ArcelorMittal’s management team has a strong track record and extensive experience in the steel and mining industries.

In 2020, the Company successfully reduced fixed costs, including through temporary measures, in line with lower production resulting from the impacts of the COVID-19 pandemic. These savings limited the increase in fixed costs as activity and production levels recovered, thus leading to lower fixed costs per tonne. In total, $1.0 billion of structural cost improvements were identified within this fixed cost reduction program. In 2021, the Company achieved $0.6 billion of fixed cost savings relating to its previously announced $1.0 billion structural improvement plan. Savings were achieved through productivity gains and footprint optimization (following closures at Kraków, coke plant in Florange, and Saldanha); and SG&A savings including a 20% reduction in corporate office costs including headcount reduction. The Company did not make progress on its plan related to repairs and maintenance following the decision taken to maintain such expenditures at higher levels to ensure operational reliability.

In February 2022, the Company announced a new three-year $1.5 billion value plan ($1.4 billion scope adjusted for the sale of ArcelorMittal Temirtau operations on December 7, 2023) focused on creating value through well-defined commercial and operational initiatives. This plan did not include the impact of strategic capital expenditure projects (which are followed separately). The plan includes commercial initiatives, including volume/mix improvements and operational improvements (primarily in variable costs). The plan aims at protecting operating income potential of the business from rising inflationary pressures, improving its relative competitive position vis-à-vis its peers and supporting sustainably higher profits. The plan progressed during 2023, and the actions taken in 2022 and 2023 have so far yielded cumulative benefits of $0.8 billion (approximately 60% of the scope adjusted target). These include $0.3 billion of commercial initiatives, $0.3 billion of variable costs savings and $0.2 billion of fixed and logistic cost savings. With the ongoing focus to execute and deliver the value plan initiatives, the Company expects to achieve the remainder of the targets as planned in 2024.

Proven expertise in acquisitions

ArcelorMittal’s management team has proven expertise in successfully acquiring and subsequently integrating operations. The Company takes a disciplined approach to investing and uses teams with diverse areas of expertise from different

6

| Management report | ||

business units across the Company to evaluate opportunities, conduct due diligence and monitor integration and post-acquisition performance. The Company introduces focused capital expenditure programs, implements Company-wide best practices, balances working capital, ensures adequate management resources and introduces safety and environmental improvements at acquired facilities. ArcelorMittal believes that these operating and financial measures have improved the operating performance and the quality of steel produced at such facilities.

In recent years, the Company has focused on portfolio optimization including assets disposals and strategic M&A activity (see also "— Key transactions and events in 2023"). In 2022, ArcelorMittal acquired a 80% interest in voestalpine's world-class Hot Briquetted Iron ("HBI") plant in Texas and in 2023, the Company completed the acquisition of Companhia Siderúrgica do Pecém ("CSP") renamed ArcelorMittal Pecém in Brazil, a world-class operation, producing high-quality slab at a globally competitive cost. To further support its decarbonization strategy, ArcelorMittal completed the acquisitions of Riwald Recycling and Italpannelli Germany, which complement the Company's existing geographic presence and strengthen the product portfolio of ArcelorMittal Downstream Solutions' construction business.

Sustainability leadership.

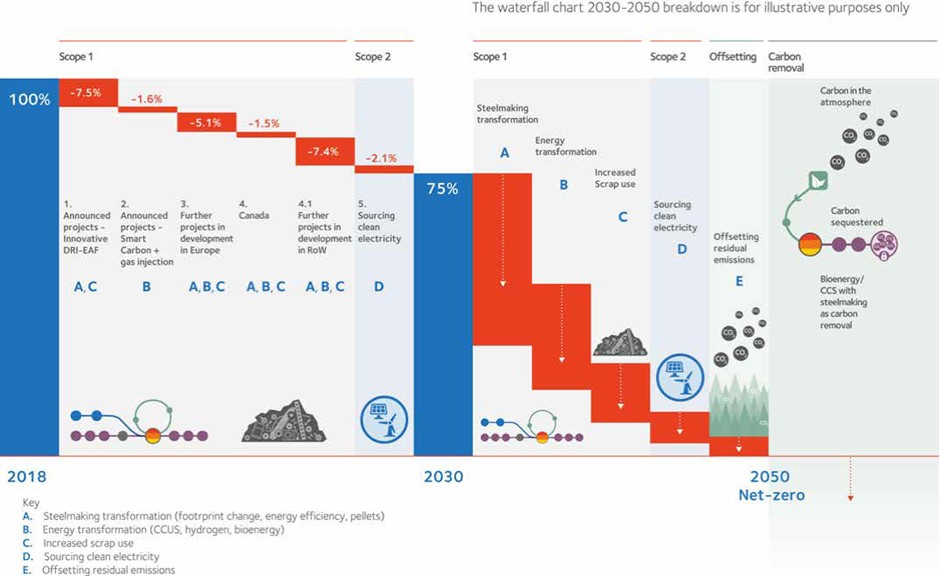

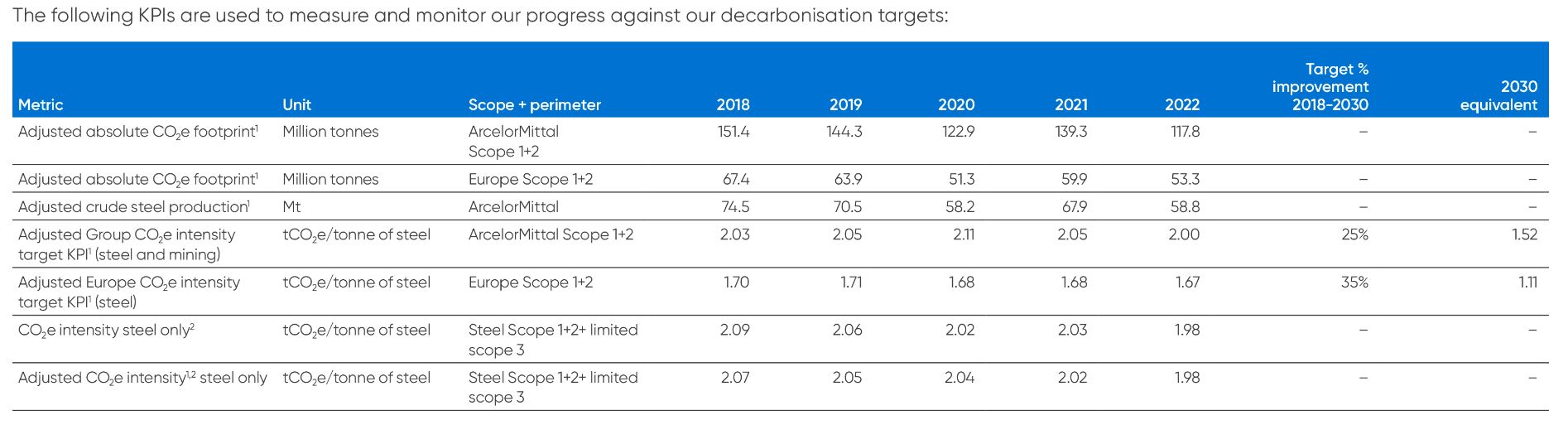

ArcelorMittal is committed to leading the industry’s efforts to decarbonize, and to being part of the solution to the world reaching net-zero by 2050. As a milestone to its 2050 net-zero target, the Company has set a group target of reducing its CO2 emissions intensity by 25% by 2030, and in its European operations, by 35% by 2030 (scope 1 and 2 emissions). As innovation is central to the Company's success given the onus it places on research and development ("R&D") with the goal of ensuring ArcelorMittal is at the forefront of the evolution of steelmaking processes and products, the Company has developed the industry’s broadest and most flexible suite of low-emissions steelmaking technologies and has integrated them into two pathways, Smart Carbon and Innovative-DRI, both of which hold the potential to deliver carbon-neutral steelmaking.

Other information

ArcelorMittal is a public limited liability company (société anonyme) that was incorporated for an unlimited period under the laws of the Grand Duchy of Luxembourg on June 8, 2001. ArcelorMittal is registered at the R.C.S. Luxembourg under number B 82.454.

The mailing address and telephone number of ArcelorMittal’s registered office are:

| ArcelorMittal | ||

| 24-26, Boulevard d’Avranches | ||

| L-1160 Luxembourg | ||

| Grand Duchy of Luxembourg | ||

| Telephone: +352 4792-1 | ||

ArcelorMittal’s agent for U.S. federal securities law purposes is:

| ArcelorMittal Sales & Administration LLC | ||

| 833 W. Lincoln Highway, Suite 200E, | ||

| Schererville, IN 46375 | ||

| Telephone: +219 256 7303 | ||

Internet site

ArcelorMittal maintains an Internet site at www.arcelormittal.com. Information contained on or otherwise accessible through this Internet site is not a part of this annual report. All references in this annual report to this Internet site and to any other Internet sites (other than to specific documents furnished to or filed with the SEC and specifically incorporated by reference herein) are inactive textual references and are for information only. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.

ArcelorMittal produces a range of publications to inform its shareholders. These documents are available in various formats: they can be viewed online or downloaded. Please refer to www.arcelormittal.com, where they can be located within the Investors menu, under Financial Reports, or within the Corporate Library. Any request for documents may be sent to: company.secretary@arcelormittal.com or ArcelorMittal’s registered office.

Sustainable development

ArcelorMittal’s sustainable development information is detailed in the Integrated Annual Review available within the Corporate Library on www.arcelormittal.com. The 2023 information is expected to be published during the second quarter of 2024. For further information, please refer to the section "Sustainable Development".

ArcelorMittal as parent company of the ArcelorMittal group

ArcelorMittal, incorporated under the laws of Luxembourg, is the parent company of the ArcelorMittal group and is expected to continue this role during the coming years. The Company has no branch offices.

Listings

ArcelorMittal’s shares (also referred to as "ordinary shares" or "common shares" throughout this report) are traded on several exchanges: New York (MT), Amsterdam (MT), Paris (MT), Luxembourg (MT) and on the Spanish Stock Exchanges of

7

| Management report | ||

Barcelona, Bilbao, Madrid and Valencia (MTS). Its primary stock exchange regulator is the Luxembourg CSSF ("Commission de Surveillance du Secteur Financier"). ArcelorMittal’s CSSF issuer number is E-0001.

On May 19, 2023, ArcelorMittal's outstanding 5.50% Mandatorily Convertible Subordinated Notes ("MCNs") matured and were converted into shares, leaving no MCNs outstanding or listed on the NYSE.

Indexes

ArcelorMittal is a member of more than 145 indices including: STOXX Europe 600, S&P Europe 350, CAC40, MSCI Pan-Euro, Bloomberg World Index, IBEX 35, Euronext Paris CAC Basic Materials Index, DAXglobal Steel EUR Price and Euronext

Amsterdam AEX Basic Materials Index. Recognized for its commitments to sustainable development, ArcelorMittal is also included in the FTSE4Good Index, Euronext Vigeo Europe 120 and the Euronext Most Advanced Benelux 20. Furthermore, ArcelorMittal has been participating in the Carbon Disclosure Project since 2005 and the United National Global Compact since 2003.

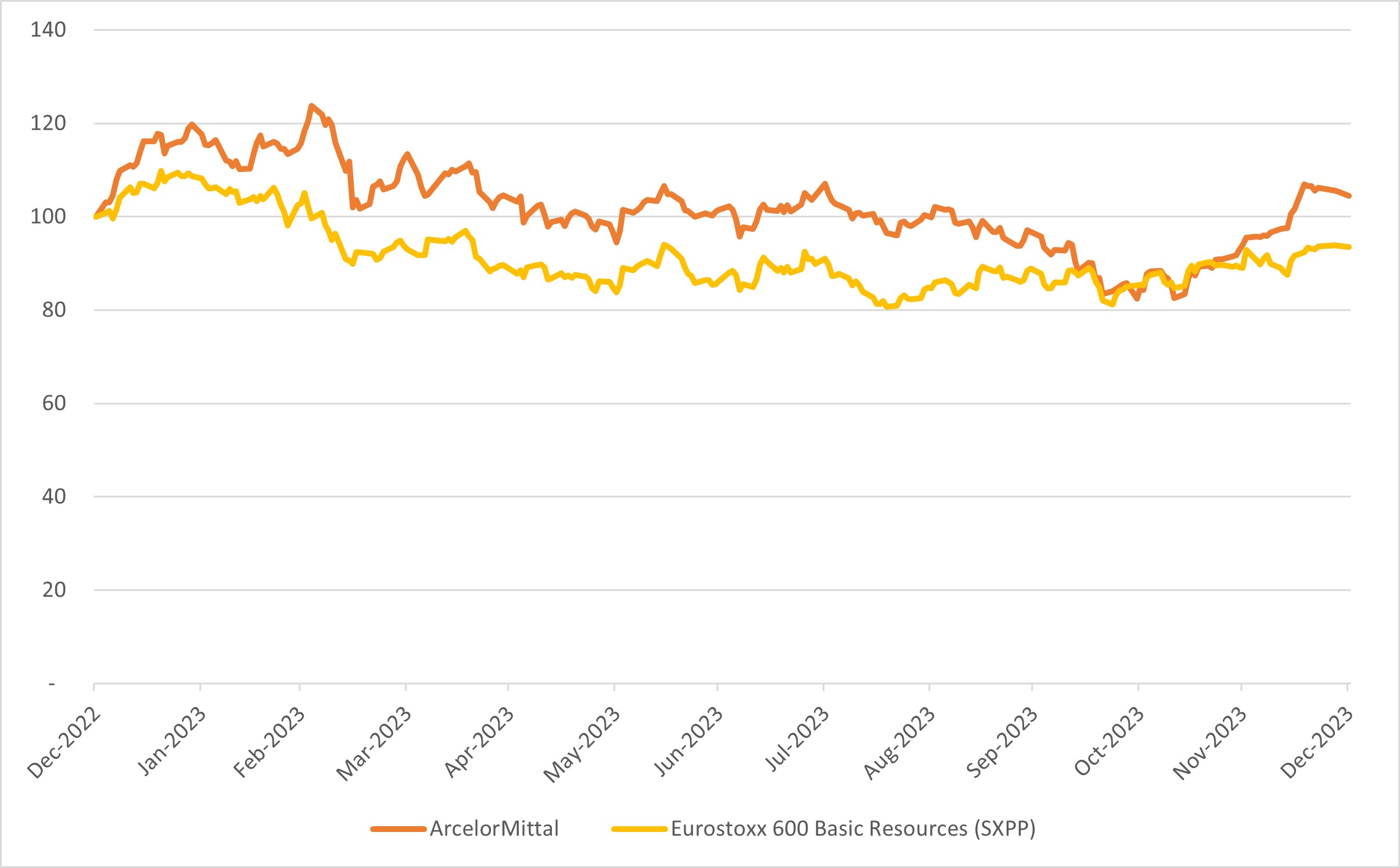

Share price performance

During 2023, the price of ArcelorMittal shares increased by 8.2% in dollar terms compared to 2022 year on year; the chart below shows a comparison between the performance of ArcelorMittal’s shares and the Eurostoxx600 Basic Resource (SXPP).

Capital return policy

On May 2, 2023, at the annual general meeting of shareholders ("AGM"), the shareholders approved the dividend of $0.44 per share proposed by the Board of Directors. The dividend amounted to $369 million and payment included two installments; the first installment of $185 million was paid on June 15, 2023 and the second installment of $184 million was paid on December 7, 2023.

In accordance with its capital return policy, the Company expects to pay a base annual dividend (to be progressively

increased over time). In addition, a minimum of 50% of the amount of free cash flow (calculated as net cash provided by operating activities less purchases of property, plant and equipment and intangibles ("capital expenditures") less dividends paid to non-controlling shareholders) remaining after paying the base annual dividend is allocated to a share buyback program. Should the ratio of net debt to operating income (loss) less depreciation, impairment and special items be greater than 1.5x then the share buyback will not be made.

8

| Management report | ||

During 2023, as part of its capital return policy and pursuant to the authorization given by the annual general meeting of shareholders on May 4, 2022, ArcelorMittal completed a share buyback program on March 31, 2023. On May 5, 2023, the Company announced another share buyback program pursuant to the authorization of the AGM held on May 2, 2023, which remains outstanding as of the date of this annual report. Including the $8.6 billion from share buyback programs that were completed from 2020 to 2022 and $1.2 billion from shares repurchased during 2023, the Company returned in total $12 billion to shareholders under the above-mentioned capital return policy. Additional buybacks under the outstanding buyback program announced in May 2023 will be allocated to the 2024 capital return (targeting 50% of post-dividend free cash flow as per the policy). For further information on buybacks, see "Purchases of equity securities by the issuer and affiliated purchasers".

In February 2024, the Board of Directors recommended a 14% increase of the base annual dividend to $0.50/share (from $0.44/share paid in 2023) to be paid in two equal installments in June 2024 and December 2024, subject to the approval of shareholders at the annual general meeting of shareholders in April 2024.

Investor relations

ArcelorMittal has a dedicated investor relations team at the disposal of analysts and investors. By implementing high standards of financial information disclosure and providing clear, regular, transparent and even-handed information to all its shareholders, ArcelorMittal aims to be the first choice for investors in the sector.

To meet this objective and provide information to fit the needs of all parties, ArcelorMittal implements an active and broad investor communications policy: conference calls, road shows with the financial community, regular participation at investor conferences, plant visits and meetings with individual investors.

ArcelorMittal’s senior management plans to meet investors and shareholder associations in such events throughout 2024.

Investors may use the following e-mails or contact numbers to reach the investor relations team:

| investor.relations@arcelormittal.com | +44 203 214 2893 | ||||

| creditfixedincome@arcelormittal.com | +33 1 7192 1026 | ||||

Sustainable responsible investors

The Investor Relations team is also a source of information for the growing sustainable responsible investment community. The team organizes special events on ArcelorMittal’s corporate responsibility strategy and answers all requests for information

sent to the Group at investor.relations@arcelormittal.com or may be contacted at +44 7435 192 206.

Financial calendar

The schedule is available on ArcelorMittal’s website www.arcelormittal.com under Investors, Financial calendar.

| Financial results*: | |||||

| Results for the 1st quarter 2024 | May 2, 2024 | ||||

| Results for the 2nd quarter 2024 and 6 months 2024 | August 1, 2024 | ||||

| Results for the 3rd quarter 2024 | November 7, 2024 | ||||

| Meeting of shareholders: | |||||

| Annual general meeting of shareholders | April 30, 2024 | ||||

* Earnings results are issued before the opening of the stock exchanges on which ArcelorMittal is listed.

Cautionary Statement Regarding Forward-Looking Statements

This annual report contains forward-looking statements based on estimates and assumptions. This annual report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include, among other things, statements concerning the business, future financial condition, results of operations and prospects of ArcelorMittal, including its subsidiaries. These statements usually contain the words “believes”, “plans”, “expects”, “anticipates”, “intends”, “estimates” or other similar expressions. For each of these statements, you should be aware that forward-looking statements involve known and unknown risks and uncertainties. Although it is believed that the expectations reflected in these forward-looking statements are reasonable, there is no assurance that the actual results or developments anticipated will be realized or, even if realized, that they will have the expected effects on the business, financial condition, results of operations or prospects of ArcelorMittal.

These forward-looking statements speak only as of the date on which the statements were made, and no obligation has been undertaken to publicly update or revise any forward-looking statements made in this annual report or elsewhere as a result of new information, future events or otherwise, except as required by securities and other applicable laws and regulations. A detailed discussion of principal risks and uncertainties which may cause actual results and events to differ materially from such forward-looking statements is included in the section titled “Risk factors”.

All information that is not historical in nature and disclosed under “Operating and financial review” is deemed to be a forward-looking statement.

9

| Management report | ||

Market information

This annual report includes industry data and projections about the Company’s markets obtained from industry surveys, market research, publicly available information and industry publications. Statements on ArcelorMittal’s competitive position contained in this annual report are based primarily on public sources including, but not limited to, published information from the Company's competitors. Industry publications generally state that the information they contain has been obtained from sources believed to be reliable but that the accuracy and completeness of such information is not guaranteed and that the projections they contain are based on a number of significant assumptions. The Company has not independently verified this data or determined the reasonableness of such assumptions. In addition, in many cases the Company has made statements in this annual report regarding its industry and its position in the industry based on internal surveys, industry forecasts and market research, as well as the Company’s experience. While these statements are believed to be reliable, they have not been independently verified.

Financial information

This annual report contains the audited consolidated financial statements of ArcelorMittal and its consolidated subsidiaries, including the consolidated statements of financial position as of December 31, 2023 and 2022, and the consolidated statements of operations, other comprehensive income, changes in equity and cash flows for each of the years ended December 31, 2023, 2022 and 2021. ArcelorMittal’s consolidated financial statements were prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

The financial information and certain other information presented in a number of tables in this annual report have been rounded to the nearest whole number or the nearest decimal. Therefore, the sum of the numbers in a column may not conform exactly to the total figure given for that column. In addition, certain percentages presented in the tables in this annual report reflect calculations based upon the underlying information prior to rounding and, accordingly, may not conform exactly to the percentages that would be derived if the relevant calculations were based on the rounded numbers. This annual report includes net debt, operating working capital, gearing and free cash flow, which are non-GAAP financial measures. ArcelorMittal believes net debt, operating working capital, gearing and free cash flow to be relevant to enhance the understanding of its financial position and provides additional information to investors and management with respect to the Company’s operating cash flows, capital structure and credit assessment. In addition, it refers to “special” items in its capital return policy which will be used to determine if the base dividend will be paid. “Special” items relate to events or charges that the

Company does not consider to be part of the normal income generating potential of the business. Items may qualify as “special” although they may have occurred in prior years or are likely to recur in following years. Non-GAAP financial measures should be read in conjunction with and not as an alternative for, ArcelorMittal’s financial information prepared in accordance with IFRS. Such non-GAAP measures may not be comparable to similarly titled measures applied by other companies.

Key transactions and events in 2023

During 2023, ArcelorMittal completed several financing and liability management transactions. Please refer to "Operating and financial review—Liquidity and capital resources—Financings" of this report for a summary of these transactions.

•On April 3, 2023, the Company announced that it had completed the 60,431,380 shares buyback program announced on July 29, 2022 under the authorization given by the annual general meeting of shareholders of May 4, 2022.

•On April 28, 2023, the Company announced that 25 million treasury shares were cancelled to keep the number of treasury shares the Company holds within appropriate levels.

•On May 5, 2023, ArcelorMittal announced the commencement of a new buyback program of up to 85 million shares under the authorization given by the annual general meeting of shareholders of May 2, 2023, to be completed by May 2025. The actual amount of shares that will be repurchased pursuant to this program will depend on the level of post-dividend free cash flow generated over the period (the Company’s defined policy is to return a minimum of 50% of post-dividend annual free cash flow), the continued authorization by shareholders, and market conditions.

•On May 19, 2023, the Company delivered a total of 57,057,991 treasury shares upon mandatory conversion of the 24,290,025 outstanding 5.50% mandatorily convertible subordinated notes due May 18, 2023.

•On October 28, 2023, ArcelorMittal confirmed that earlier in the day, a tragic accident occurred at its Kostenko coal mine which resulted ultimately in 46 fatalities. No words can adequately convey the devastation the Company feels following this accident. ArcelorMittal and the government of Kazakhstan signed a preliminary agreement for a transaction that would transfer ownership to the Republic of Kazakhstan, and on December 8, 2023, ArcelorMittal announced the completion of the sale of ArcelorMittal Temirtau to Qazaqstan Investment Corporation ("QIC"), a state-controlled direct investment fund. Under the terms of the transaction, on closing ArcelorMittal received

10

| Management report | ||

consideration of $286 million and a further $250 million as repayment of outstanding intra-group dues. ArcelorMittal will also receive an additional sovereign-fund guaranteed payment of $450 million, paid in four equal annual installments, as repayment of an intra-group loan. All ArcelorMittal Temirtau assets were transferred on an ‘as is’ operational basis, meaning QIC assumed control and accountability for ArcelorMittal Temirtau’s operations, which were subsequently renamed.

•On December 22, 2023, ArcelorMittal announced that it had engaged dss+, a leading provider of sustainable operations management consulting services, to conduct a Company-wide audit of its safety practices.

In addition, the Company completed the following additional acquisitions:

•On January 3, 2023 and March 10, 2023, ArcelorMittal completed the acquisition of Riwald Recycling ("Riwald"), a state-of-the-art ferrous scrap metal recycling business based in the Netherlands in the framework of its decarbonization strategy and Italpannelli Germany, a German insulation panel manufacturer which complements the existing geographic presence and strengthens the product portfolio of ArcelorMittal Downstream Solutions' construction business, respectively. The total cash consideration paid for both acquisitions was €144 million ($154 million).

•On March 9, 2023, ArcelorMittal announced that following receipt of customary regulatory approvals it had completed the acquisition of Companhia Siderúrgica do Pecém (‘CSP’) (renamed ArcelorMittal Pecém) in Brazil for an enterprise value of approximately $2.2 billion. CSP is a world-class operation, producing high-quality slab at a globally competitive cost. Its facility, located in the state of Ceará in northeast Brazil was commissioned in 2016. It operates a three-million tonne capacity blast furnace and has access via conveyors to the Port of Pecém, a large-scale, deepwater port located 10 kilometers from the plant. The acquisition offers significant operational and financial synergies and brings with it the potential for further expansions, such as the option to add primary steelmaking capacity (including direct reduced iron) and rolling and finishing capacity. Given its location, CSP also presents an opportunity to create a new low-carbon steelmaking hub, capitalizing on the state of Ceará’s ambition to develop a low-cost green hydrogen hub in Pecém.

Recent Developments

•On February 20, 2024, ArcelorMittal announced the decision of Italian Government to place Acciaierie d’Italia SpA (‘ADI’) into extraordinary administration subsequent to the request of Invitalia, thereby passing

control of the company from its current shareholders, ArcelorMittal and Invitalia, to government appointed commissioners. This ends ArcelorMittal’s involvement in ADI, which started in 2018. Since 2018, ArcelorMittal has been fully committed to the people and assets of ADI, then known as Ilva, investing over €2 billion. This very significant investment enabled ADI to complete an extensive €800 million environmental program on time that ensured compliance with the Integrated Environmental Authorization set out by the Italian Government, as well as invested €1.2 billion in upgrading equipment at all sites. ADI also benefited from hundreds of millions of euros of credit through the provision of raw materials by ArcelorMittal. ArcelorMittal had been keen to address the significant discrepancy in capital investment into ADI by the two shareholders. In recent discussions, ArcelorMittal put forward pragmatic proposals to address this while continuing the public-private partnership with Invitalia that was established in April 2021. When the shareholders were not able to agree on acceptable terms, ArcelorMittal also offered to sell its shareholding in ADI to Invitalia. The discussions, despite ArcelorMittal’s best efforts, were not successful. This situation could have been avoided if ADI had been able (after April 2021) to access traditional debt financing and been able to raise the working capital required to fund its ongoing needs, rather than relying on equity injections from its shareholders as its sole source of capital. Unfortunately, the conditions precedent to allow ADI to convert its lease of the assets into a formal purchase – conditions that ADI has no control over, were originally set to be completed before May 2022, and subsequently extended to May 2024, remain unsatisfied as of date. ADI’s financial situation has been further impacted by the Italian Government delivering less than one-third of the €2 billion of support measures it offered to ADI, at the time the public-private partnership with Invitalia was established.

Sustainable development highlights - striving to be a leader in the decarbonization of the steel industry

•On January 27, 2023, ArcelorMittal announced it invested $36 million in Boston Metal. The transaction was the Company’s largest single initial investment to date through its XCarb® Innovation Fund. ArcelorMittal’s investment led a $120 million Series C fundraising round undertaken by Boston Metal. Other participants in the round include Microsoft’s Climate Innovation Fund and Site Ground Capital, who joined Boston Metal’s existing shareholder register which includes Breakthrough Energy Ventures,

11

| Management report | ||

mining majors Vale and BHP, BMW i Ventures and several cleantech venture capital funds.

•On April 18, 2023, ArcelorMittal announced that ArcelorMittal Brasil, would form the joint venture partnership Ventos de Santo Antonio Comercializadora de Energia S.A. ("VdSA") with Casa dos Ventos, one of Brazil’s largest developers and producers of renewable energy projects, to develop a 554 MW wind power project. ArcelorMittal Brasil holds a 55% stake in the joint venture, with Casa dos Ventos holding the remaining 45%. The transaction was approved by the Brazilian antitrust authority, CADE, on April 13 and was completed on May 5, 2023. The $0.8 billion project aims to secure and decarbonize a considerable proportion of ArcelorMittal Brasil’s future electricity needs and is estimated to provide 38% of ArcelorMittal’s Brasil’s total electricity needs in 2030. VdSA is equity accounted, and ArcelorMittal’s total equity investment will be $0.15 billion. The project is located in the central region of Bahia, north-east Brazil. The site location has been selected due to several competitive advantages, including high-capacity forecast load factors (in excess of 50%) and a short distance (23 kilometers) to connect to the national electricity grid. There is also the potential to expand the capacity of the project by adding a further 100 MW of solar power. Environmental and regulatory permitting is in the process of finalization; construction work started in 2023 with operational commissioning expected in 2025. ArcelorMittal Brasil will enter into a 20-year power purchase agreement with VdSA for the supply of electricity.

•On June 14, 2023, ArcelorMittal and LanzaTech Global Inc. announced the successful commencement of production from ArcelorMittal’s commercial flagship carbon capture and utilization ("CCU") facility in Ghent, Belgium. The €200 million ‘Steelanol’ facility is a first of its kind for the European steel industry, deploying technology developed by leading carbon utilization company LanzaTech. This is the first step toward full operation of a commercial scale facility that will capture carbon-rich waste gases from steelmaking and biologically convert them into advanced ethanol through LanzaTech’s biobased process. Unlike traditional fermentation, the process ferments gases instead of sugars and uses a biocatalyst instead of yeast. The facility was inaugurated in December 2022, with cold commissioning taking place thereafter. The biocatalyst has now been introduced into the facility (a process called inoculation) to begin growth and verify production of new molecules. In May 2023, the first gases from the steel mill’s blast furnace were safely introduced to LanzaTech’s biocatalyst. After a successful inoculation, initial samples that contained ethanol were produced during the second week of June 2023, demonstrating that the carbon in the gases is being converted into new chemical products.

Commercial-scale ethanol production from the bioreactors commenced in November 2023, and further ramp-up of production is ongoing. This advanced ethanol can then be used as a building block to produce a variety of products, including sustainable transport fuels, packaging materials, apparel, and even cosmetic fragrances, hence helping to advance the decarbonization efforts of the global chemical sector. The ethanol will be jointly marketed by ArcelorMittal and LanzaTech under the Carbalyst® brand name. The Steelanol plant has the annual capacity to produce 80 million liters of ethanol, around half of the total current demand in Belgium. It expects to reduce carbon emissions from the Ghent plant by 125,000 tonnes annually, thereby advancing the EU’s 2030 Climate Target Plan to reduce greenhouse gas ("GHG") emissions by 55% by the end of the decade. Project partners include Primetals Technologies and E4tech with support from CINEA, the European Climate, Infrastructure and Environment Executive Agency. The product samples from the facility mark an important step toward the circular use of carbon and the end of single-use carbon, whereby gases are no longer regarded as waste but as raw materials. In addition, the recycling of carbon means Steelanol’s process of Carbalyst® ethanol production does not compete in any way with food crops, as is the case for traditional methods of ethanol production. The LanzaTech process implemented at the Ghent site is fully flexible: not only can it use industrial gases from today’s steel production methods but it can also adapt as industry transitions to future steel production technologies with increased green hydrogen input. This versatility enables the carbon recycling application to evolve with available residue, waste streams, and green H2. LanzaTech’s process is already employed by three operational commercial facilities, and LanzaTech launched two additional commercial facilities in Asia in 2023. Funding for the commercial Steelanol facility was obtained from various sources, including the Flemish government, the Belgian federal government and the European Union’s Horizon 2020 research and innovation program under grant agreement No 656437. Part of the funding was also secured with a loan from the European Investment Bank. The Steelanol facility reached full operational capacity in November 2023.

•On June 14, 2023, ArcelorMittal and John Cockerill announced plans to develop an industrial scale low temperature, iron electrolysis plant. The Volteron™ (a carbon free, cold direct electrolysis process that extracts iron from iron ore using electricity; on a pilot scale plant, the process has proved to be highly efficient using standard iron ore; the iron plates created during the electrolysis process are then processed into steel in an electric arc furnace) plant is targeted in a first phase to produce

12

| Management report | ||

between 40,000 and 80,000 tonnes a year of iron plates and to start production in 2027. Once the technology has been proven at this scale, the intention is to increase the plant’s annual capacity to between 300,000 and 1,000,000 tonnes.

•On June 16, 2023, ArcelorMittal confirmed its plan to invest €67 million in a new EAF at its Belval site. This investment is part of a series of projects that were the subject of an MoU signed in September 2022 between ArcelorMittal Luxembourg and the Ministry of the Economy. The MoU confirmed the willingness of the Luxembourg government to financially support this type of strategic investment, through the various applicable aid mechanisms.

•On June 19, 2023, ArcelorMittal and SEKISUI CHEMICAL announced that their carbon recycling project achieved target ahead of schedule. Both companies have been partnering on a project to capture and reuse CO2 emitted during steelmaking. As part of this partnership, ArcelorMittal and SEKISUI CHEMICAL have been supported by the New Energy and Industrial Technology Development Organization (NEDO), Japan’s national research and development agency, and have launched an “International collaboration on CCU for circular carbon in Steelmaking” (hereafter, the NEDO project), scheduled for three years from 2021. One of the research topics is to develop a fundamental technology for Synthesis Gas (carbon monoxide and hydrogen) production using SEKISUI CHEMICAL’s unique chemical looping technology.

•On June 21, 2023, the Labour Inspectorate of the French government ordered the temporary administrative closure of part of the Fos-sur-Mer site due to dust and crystalline silica at the Company's steel works. The decision was subsequently suspended after being reviewed by the Marseille Administrative Court. ArcelorMittal's action plan to strengthen health protection measures has been accelerated (in consultation with the Labour Inspectorate and Trade Unions). The plan contains more than 80 actions including the search for a product to replace crystalline silica used in continuous casting with the support of our R&D team, an intensive industrial cleaning campaign. All dust collection, ventilation and capture systems are being reviewed and improved where necessary. In addition, intensive awareness-raising and training initiatives are continuing, in particular as part of the accelerated introduction of ventilated breathing masks (by the end of July 2023, 687 of such masks were distributed to all relevant employees at the steel mill).

•On July 20, 2023, the European Commission approved €850 million state aid for ArcelorMittal's Dunkirk site for the construction of a 2.5 million tonne DRI facility and 2 new EAFs. This followed the European Commission approval on

June 22, 2023, of €280 million in state aid to be provided by the Belgian authorities for the Company's DRI – EAF decarbonization project in Belgium (2.5 million tonne DRI and 2 new EAFs). The overall support that ArcelorMittal will receive from the Belgian and French authorities is commensurate with the Company's broader ask to its host governments for its decarbonization projects. Funding approval decisions for the Company's German project remain outstanding.

•On July 11, 2023, ArcelorMittal announced that its XCarb™ Innovation Fund was launching an accelerator program to fund and support the next wave of breakthrough ideas on decarbonization emerging from India. With the XCarb™ India Accelerator Program, ArcelorMittal, collaborating with the Indian Institute of Technology Madras, whose pedigree in nurturing ideas and mentoring will be applied to support start-ups or early stage companies selected, enables them to scale their technologies and business models from lab to the market. The program will also be supported by ArcelorMittal’s joint venture AMNS India which is actively developing its own decarbonization strategy and initiatives for lower emissions domestic steel manufacturing. Successful participants will have access to expertise, resources and advice from ArcelorMittal and AMNS India.

•On November 15, 2023, ArcelorMittal announced its entry into the additive manufacturing (AdM) market as a steel powder supplier. The Company is building an industrial-scale inert gas atomizer in Aviles, Spain, to produce steel powders for AdM technologies such as laser powder bed fusion (LPBF), binder jetting (BJ) and direct energy deposition (DED). The atomizer, which started production in January 2024, will have a large batch-size production capability, from 200 kg to 3 tonnes, and an initial annual capacity of 1,000 tonnes. This will enable ArcelorMittal to supply significant volumes of steel powders with consistent quality, reliability and traceability, meeting the high standards and specifications of the AdM industry. In line with ArcelorMittal's sustainability and decarbonization efforts, the Company is committed to advancing the sustainability of additive manufacturing.

•On November 15, 2023, ArcelorMittal and Schneider Electric, a leader in the digital transformation of energy management and automation, announced a partnership whereby ArcelorMittal will supply Schneider Electric with XCarb® recycled and renewably produced steel for its electrical cabinets and enclosures. Produced at ArcelorMittal’s site in Sestao, Spain, XCarb® recycled and renewably produced steel is made using a very high proportion of recycled steel in an electric arc furnace, powered with 100% renewable electricity. This results in CO₂ emissions which are close to 70% lower than the same product made without XCarb® recycled and renewably

13

| Management report | ||

produced steel. ArcelorMittal’s XCarb® recycled and renewably produced steel will be used by Schneider Electric to manufacture the new PanelSeT SFN floor-standing enclosures built to protect large electrical panels for industrial automation, power distribution and electronic applications. As these enclosures are built to withstand tough operating environments, the XCarb® recycled and renewably produced steel is also coated with Magnelis®, a metallic coating offering high corrosion protection. The partnership is the result of several months of technical partnership and collaboration between ArcelorMittal Steel Services Centre Europe and Schneider Electric to find the right grade of steel and coating for the project.

•On November 28, 2023, ArcelorMittal announced that ArcelorMittal Asturias had signed a contract with industrial engineering company Sarralle, to build a new electric EAF in Gijón, as part of the company’s decarbonization plan for Spain. Civil works on the site will start early 2024. Once the new 1.1 million tonne EAF is operational, the site will be able to switch to producing low carbon-emissions steel for the long products sector, specifically rails and wire rod, making the site highly competitive, in particular for sectors with stringent carbon criteria for public procurement contracts. Currently, these products are made via the blast furnace route. In addition, a de-dusting system and waste heat recovery unit will be installed by Sarralle, as part of the project and in order to maximize energy efficiency in the new EAF. The project is part of ArcelorMittal Europe’s commitment to reduce CO2 emissions by 35% by 2030.

•On December 20, 2023, ArcelorMittal Belgium commissioned its Torero plant, which converts waste wood into bio-coal for use in the blast furnace at its Ghent steelmaking site. The first bio-coal made in the Torero plant, through a process known as torrefaction, was successfully used in a blast furnace in Ghent on December 18, 2023. The project will reduce annual carbon emissions from the plant by 112,500 tonnes, by reducing the use of fossil coal in the blast furnace. The Torero industrial-scale demonstration plant will convert 88,000 tonnes of waste wood into 37,500 tonnes of bio-coal annually. The use of bio-coal in the blast furnace process will result in the production of bio-gas, which will be captured and transformed into ethanol by ArcelorMittal Ghent’s Steelanol facility.

Recent Developments

•On January 3, 2024, ArcelorMittal announced that it had established a partnership with the Indian Institute of Technology Madras ("IIT Madras") and is working closely with IIT Madras’ Hyperloop Technology teams - Avishkar Hyperloop, student team and TuTr Hyperloop, a start-up incubated at IIT Madras, which are developing cost-

effective Hyperloop technologies for passenger and cargo mobility at scale.

•On January 15, 2024, Bruno Le Maire, the French Minister for Economy and Finance was welcomed to the Company's Dunkirk steelworks by Eric Niedziela, Chairman, ArcelorMittal France, and members of the French executive management team. The visit was designed to update Mr Le Maire on the decarbonization plans and progress at ArcelorMittal's French steelmaking operations. ArcelorMittal’s decarbonization plans in France have also received a boost through a letter of intent signed on the same date with French state-owned energy supplier EDF Energy for the long-term supply of low-carbon electricity to its French steelmaking sites in Dunkirk and Fos-sur-Mer.

•On January 16, 2024, ArcelorMittal announced that it has established a partnership with Vestas, the energy industry’s global partner on sustainable energy solutions, to launch a low carbon-emissions steel offering that significantly reduces the lifetime carbon dioxide emissions from the production of wind turbine towers. The low carbon-emissions steel is produced using 100% steel scrap which is melted in an electric arc furnace powered by 100% wind energy at the ArcelorMittal steel mill, Industeel Charleroi, in Belgium. The steel slabs are then transformed into heavy plates used for the manufacture of wind turbine towers, at ArcelorMittal’s heavy plate mill in Gijón, Spain. These heavy plates, made with XCarb® recycled and renewably produced heavy plate steel, are initially suitable for the entire onshore wind turbine towers and the top section of offshore wind turbine towers.

14

Risk Factors and Control

Risk factors

ArcelorMittal’s business, financial condition, results of operations, reputation or prospects could be materially and adversely affected by one or more of the risks and uncertainties described below.

I. Risks related to the global economy and the mining and steel industry

Prolonged low steel and (to a lesser extent) iron ore prices and/or low steel demand would have an adverse effect on ArcelorMittal’s results of operations.

As an integrated producer of steel and iron ore, ArcelorMittal’s results of operations are sensitive to the market prices of, and demand for, steel and iron ore in its markets and globally. The impact of market steel prices on its results is direct while the impact of market iron ore prices is both direct and indirect, as ArcelorMittal sells iron ore on the market to third parties (in which case it benefits from higher iron ore market prices), and indirect, as iron ore is a principal raw material used in steel production and fluctuations in its market price are typically and eventually (with the timing dependent on steel market conditions) passed through to steel prices (with any lags in passing on higher prices “squeezing” steel margins, as discussed below). Steel and iron ore prices are affected by supply and demand trends and inventory cycles. In terms of demand, steel and iron ore prices are sensitive to trends in cyclical industries, such as the automotive, construction, appliance, machinery, equipment and transportation industries, which are significant markets for ArcelorMittal’s products (with automotive being particularly significant). More generally, steel and iron ore prices are sensitive to macroeconomic fluctuations in the global economy which are impacted by many factors ranging from trade and geopolitical tensions to global and regional monetary policy to specific disruptive events such as pandemics, wars and natural disasters. In the past, substantial price decreases during periods of economic weakness have not always been offset by commensurate price increases during periods of economic strength. In addition, as further discussed below, excess supply relative to demand for steel in local markets generally results in increased exports and drives down regional or global prices. In terms of inventory, steel stocking and destocking cycles affect apparent demand for steel and hence steel prices and steel producers’ profitability. For example, steel distributors may accumulate substantial steel inventories in periods of low prices and, in periods of rising real demand for steel from end-users, steel distributors may sell steel from inventory (destock), thereby delaying the effective implementation of steel price increases. Conversely, steel price decreases can sometimes develop their own momentum, as customers adopt a “wait and see” attitude and destock in the expectation of further price decreases.

As a result of these factors, steel and iron ore prices fluctuate substantially and have come under pressure at various points in recent periods. See “Operating and financial review—Key factors affecting results of operations”.

More specifically in terms of near to mid-term risks for the Company in this respect, the fall in international spot steel prices in 2022 and 2023 stemmed from a broader trend in slowing steel demand. Macroeconomic conditions are fragile and uncertain, including due to geopolitical developments, particularly Russia’s invasion of Ukraine and the Israel-Hamas conflict, and actions taken by central banks to combat inflation (in particular raising interest rates sharply in 2022 and 2023). As interest rates remain high, the risk of a global recession remains. Significant energy supply and cost issues in Europe increase the risk of manufacturers being unable to operate at full capacity, potentially lowering demand for steel and straining steel prices. Many steel customers began to destock and adopt a “wait and see” approach in the summer of 2022, and steel demand, particularly in Europe, continued to decline during the second half of 2023, causing steel users to destock further, resulting in a second consecutive year of destocking. The fragility of the Chinese economy, which suffered from the negative effects of repeated strict lockdowns that ran until December 2022 and more recently from a weak real estate sector, slowing economic growth, accelerating deflation and general uncertainty also add to risks of a global slowdown and lower global steel demand and prices. Prior recessions have generally resulted in lower steel demand and steel prices, with consequential material adverse impacts on steel companies’ results. Any significant decline in steel prices also increases the risk of inventory-related charges, such as those that ArcelorMittal recorded in 2019 and 2022. In addition, the impact of lower steel prices on ArcelorMittal’s results is subject to a lag effect (due to its contracts), and therefore the impact is felt beyond the duration of any decline in spot steel prices.

The trajectory of steel demand and prices going forward, in particular in 2024, is difficult to predict due to such variables as the duration of the ongoing conflict in Ukraine, the Israel-Hamas conflict and the risk of additional conflicts in the region, related risks on global energy supply and hence on industrial production and consequentially demand for steel, import volumes (in particular from China given trends in domestic supply and demand) and tariff levels and inventories. Any economic downturn globally or in certain regions may result in lower steel demand and lower steel and iron ore prices. A scenario of

15

| Management report | ||

prolonged low steel and (to a lesser extent or if simultaneous) iron ore prices, whether or not combined with low steel demand, would have a material adverse effect on ArcelorMittal’s results of operations and financial condition.