UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 20-F

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2023

OR

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Date of event requiring this shell company report: Not applicable

For the transition period from ___________________________ to ___________________________

Commission file number 001-13944

|

|

||

|

(Exact name of Registrant as specified in its charter)

|

||

|

(Translation of Registrant’s name into English)

|

||

|

|

||

|

(Jurisdiction of incorporation or organization)

|

||

|

|

||

|

|

||

|

|

||

|

|

||

|

(Address of principal executive offices)

|

||

|

Tel No. 1 (

|

||

|

(Name, Telephone, E-mail and/or Facsimile number and

Address of Company Contact Person)

|

|

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

||||

|

Title of each class

|

Trading Symbol(s)

|

Name of each exchange on which registered

|

||

|

|

|

|

||

|

Series A Participating Preferred Shares

|

New York Stock Exchange

|

|||

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2023, there were outstanding 208,796,444

common shares of the Registrant, $0.01 par value per share.

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

☒

|

☐ No

|

If this report is an annual report or transition report, indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934.

|

☐ Yes

|

☒

|

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their

obligations under those Sections.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

☒

|

☐ No

|

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T

(§232.405 of this chapter) during this preceding 12 months (or for such shorter period that the registrant was required to submit such files).

|

☒

|

☐ No

|

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition

of “large accelerated filer”, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

Accelerated filer ☐

|

|

Non-accelerated filer ☐

|

Emerging Growth Company

|

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the

extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification

after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over

financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the

financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery

analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the Registrant has used to prepare the financial statements included in this filing:

☒ U.S. GAAP

☐ International Financial Reporting Standards as issued by the International Accounting

Standards Board

☐ Other

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the Registrant has elected to follow.

☐ Item 17

☐ Item 18

If this is an annual report, indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

|

☒ No

|

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934

subsequent to the distribution of securities under a plan confirmed by a court.

|

☐ Yes

|

☐ No

|

|

PART I

|

Page | ||

|

ITEM 1.

|

1

|

||

|

ITEM 2.

|

1

|

||

|

ITEM 3.

|

1

|

||

|

A.

|

1

|

||

| B. | 1 |

||

|

C.

|

1 |

||

|

|

D.

|

1 |

|

|

ITEM 4.

|

31 |

||

|

A.

|

31 |

||

|

B.

|

34 |

||

|

C.

|

51 |

||

|

D.

|

51 |

||

|

ITEM 4A.

|

51 |

||

|

ITEM 5.

|

51 |

||

|

A.

|

51

|

||

|

|

B.

|

55 |

|

|

C.

|

61

|

||

|

D.

|

61

|

||

|

E.

|

61

|

||

|

ITEM 6.

|

64 |

||

|

A.

|

64

|

||

|

B.

|

66 |

||

|

C.

|

66 |

||

|

D.

|

67 |

||

|

E.

|

67 |

||

|

F.

|

67

|

||

|

ITEM 7.

|

67 |

||

|

A.

|

67 |

||

|

B.

|

68 |

||

|

C.

|

68 |

||

|

ITEM 8.

|

68 |

||

|

A.

|

68 |

||

|

B.

|

68 |

||

|

ITEM 9.

|

68 |

||

|

ITEM 10.

|

69 |

||

|

A.

|

69 |

||

|

B.

|

69 |

||

|

C.

|

69 |

||

|

D.

|

69 |

||

|

E.

|

70 |

||

|

F.

|

79 |

||

|

G.

|

79 |

||

|

H.

|

79 |

||

|

I.

|

79 |

||

|

J.

|

80 |

||

|

ITEM 11.

|

80 |

||

|

ITEM 12.

|

80 |

||

|

PART II

|

|||

|

ITEM 13.

|

80 |

||

i

TABLE OF CONTENTS

(continued)

| Page | |||

|

ITEM 14.

|

80 |

||

|

ITEM 15.

|

81 |

||

|

A.

|

81 |

||

|

B.

|

81 |

||

|

C.

|

81 |

||

|

D.

|

82 |

||

|

ITEM 16.

|

82 |

||

|

ITEM 16A.

|

82 |

||

|

ITEM 16B.

|

82 |

||

|

ITEM 16C.

|

82 |

||

|

A.

|

82 |

||

|

B.

|

AUDIT-RELATED FEES | 82 |

|

|

C.

|

82 |

||

|

D.

|

82 |

||

|

E.

|

82 |

||

|

F.

|

83 |

||

|

ITEM 16D.

|

83 |

||

|

ITEM 16E.

|

83 |

||

|

ITEM 16F.

|

83 |

||

|

ITEM 16G.

|

83 |

||

|

ITEM 16H.

|

83 |

||

|

ITEM 16I.

|

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | 83 |

|

|

ITEM 16J.

|

INSIDER TRADING POLICIES | 83 |

|

|

ITEM 16K.

|

CYBERSECURITY | 84 |

|

|

PART III

|

|||

|

ITEM 17.

|

84 |

||

|

ITEM 18.

|

84 |

||

|

ITEM 19.

|

85 |

||

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain matters discussed herein may constitute forward-looking statements. The Private Securities Litigation Reform Act of 1995 provides safe harbor protections for forward-looking statements in

order to encourage companies to provide prospective information about their business. Forward-looking statements include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and

other statements, which are other than statements of historical facts.

The Company desires to take advantage of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and is including this cautionary statement in connection with this safe

harbor legislation. This report and any other written or oral statements made by us or on our behalf may include forward-looking statements, which reflect our current views with respect to future events and financial performance, and are not

intended to give any assurance as to future results. When used in this document, the words “believe,” “expect,” “anticipate,” “estimate,” “intend,” “plan,” “target,” “project,” “likely,” “will,” “would,” “may,” “seek,” “continue,” “possible,”

“might,” “forecast,” “potential,” “should,” “could” and similar expressions, terms, or phrases may identify forward-looking statements.

The forward-looking statements are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, our management’s examination of

historical operating trends, data contained in our records and other data available from third parties. Although we believe that these assumptions were reasonable when made, because these assumptions are inherently subject to significant

uncertainties and contingencies which are difficult or impossible to predict and are beyond our control, we cannot assure you that we will achieve or accomplish these expectations, beliefs or projections. We undertake no obligation to update any

forward-looking statement, whether as a result of new information, future events or otherwise.

Important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements include the strength of world economies and currencies,

general market conditions, including fluctuations in charter rates and vessel values, changes in demand in the tanker market, as a result of changes in the petroleum production levels set by the Organization of the Petroleum Exporting Countries

(“OPEC”), and worldwide oil consumption and storage, changes in our operating expenses, including bunker prices, drydocking and insurance costs, the market for our vessels, availability of financing and refinancing, changes in governmental rules

and regulations or actions taken by regulatory authorities, potential liability from pending or future litigation and potential costs due to environmental damage and vessel collisions, general domestic and international political conditions or

events including “trade wars”, potential disruption of shipping routes due to accidents or political events, severe weather conditions, natural disasters, the length and severity of future epidemics and pandemics and their impact on the demand

for seaborne transportation in the tanker sector, vessel breakdowns and instances of off-hire, failure on the part of a seller to complete a sale of a vessel to us and other important factors described from time to time in the reports filed by

the Company with the Securities and Exchange Commission, or the SEC.

PART I

| ITEM 1. |

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

|

Not applicable

| ITEM 2. |

OFFER STATISTICS AND EXPECTED TIMETABLE

|

Not applicable

| ITEM 3. |

KEY INFORMATION

|

Throughout this annual report, all references to “Nordic American Tankers,” “NAT,” the “Company,” “the Group,” “we,” “our,” and “us” refer to Nordic American Tankers Limited

and its subsidiaries. Unless otherwise indicated, all references to “U.S. dollars,” “USD,” “dollars,” “US$” and “$” in this annual report are to the lawful currency of the United States of America and references to “Norwegian Kroner” or “NOK” are

to the lawful currency of Norway.

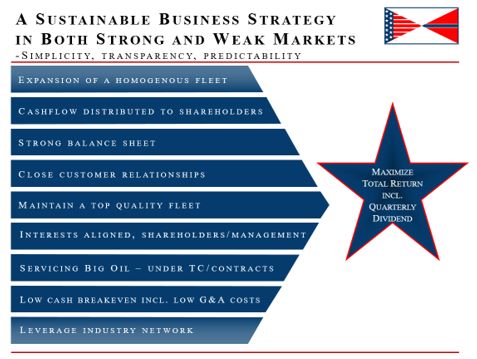

Nordic American Tankers Ltd. is very different from other stock listed tanker companies. No other company has the strategy of NAT. Please see item 4. A. for the NAT overall

strategy.

| A. |

[Reserved]

|

| B. |

Capitalization and Indebtedness

|

Not applicable.

| C. |

Reasons for the offer and use of Proceeds

|

Not applicable.

| D. |

Risk Factors

|

The following constitutes a summary of the material risks relevant to an investment in our company. The occurrence of any of the events described in this section could significantly and negatively affect our

business, financial condition, operating results or cash available for dividends or the trading price of our common stock.

Summary of Risk Factors

| • |

If the Suezmax tanker industry, which historically has been cyclical and volatile, is depressed in the future, our revenues, earnings and available cash flow may decrease.

|

| • |

We are dependent on spot charters and any decrease in spot charter rates in the future may adversely affect our earnings, our ability to pay dividends and our ability to repay our financial liabilities.

|

| • |

Changes in the price of fuel and regulations may adversely affect our profits.

|

| • |

Inability to renew the fleet would adversely affect our business, results of operations, financial condition and ability to pay dividends.

|

| • |

The international Suezmax tanker industry has experienced volatile charter rates and vessel values and there can be no assurance that these charter rates and vessel values will not decrease in the near future.

|

| • |

Our results of operations are subject to seasonal fluctuations, which may adversely affect our financial condition.

|

| • |

A shift in consumer demand from oil towards other energy sources or changes to trade patterns for crude oil or refined oil products may have a material adverse effect on our business.

|

| • |

The value of our vessels may be depressed at the time we decide to sell a vessel.

|

| • |

An over-supply of Suezmax tanker capacity may lead to reductions in charter rates, vessel values, and profitability.

|

| • |

Delays or defaults by the shipyards in the construction of newbuildings could increase our expenses and diminish our net income and cash flows.

|

| • |

Terrorist attacks and international hostilities and instability can affect the tanker industry, which could adversely affect our business.

|

| • |

We rely on our information systems to conduct our business, and failure to protect these systems against security breaches could adversely affect our business and results of operations. Additionally, if these systems fail or become

unavailable for any significant period of time, our business could be harmed.

|

| • |

If we do not manage relationships with customers or successfully integrate any acquired Suezmax tankers, we may not be able to grow or effectively manage our growth.

|

| • |

Because some of our expenses are incurred in foreign currencies, we are exposed to exchange rate fluctuations, which could negatively affect our results of operations.

|

| • |

The operation of Suezmax tankers involves certain unique operational risks.

|

| • |

We operate our Suezmax tankers worldwide and as a result, our vessels are exposed to international risks which may reduce revenue or increase expenses.

|

| • |

The smuggling of drugs or other contraband onto our vessels may lead to governmental claims against us.

|

| • |

Failure to comply with the U.S. Foreign Corrupt Practices Act could result in fines, criminal penalties and an adverse effect on our business.

|

| • |

Acts of piracy on ocean-going vessels could adversely affect our business.

|

| • |

Maritime claimants could arrest one or more of our vessels, which could interrupt our cash flow.

|

| • |

Governments could requisition our vessels during a period of war or emergency resulting in a loss of earnings.

|

| • |

If we purchase secondhand vessels, we may not receive warranties from the builder and operating cost may increase as a result of aging of the fleet.

|

| • |

Our insurance may not be adequate to cover our losses that may result from our operations due to the inherent operational risks of the tanker industry.

|

| • |

An increase in operating costs would decrease earnings and dividends per share.

|

| • |

We may be unsuccessful in competing in the highly competitive international Suezmax tanker market.

|

| • |

We are subject to laws and regulations which can adversely affect our business, results of operations, cash flows and financial condition, and our ability to pay dividends.

|

| • |

Regulations relating to ballast water discharge may adversely affect our revenues and profitability.

|

| • |

Climate change and greenhouse gas restrictions may adversely impact our operations and markets.

|

| • |

If we fail to comply with international safety regulations, we may be subject to increased liability, which may adversely affect our insurance coverage and may result in a denial of access to, or detention in, certain ports.

|

| • |

Developments in safety and environmental requirements relating to the recycling of vessels may result in escalated and unexpected costs.

|

| • |

Servicing our debt limits funds available for other purposes and if we cannot service our debt, we may lose our vessels.

|

| • |

Our borrowing facilities, contains restrictive covenants which could negatively affect our growth, cause our financial performance to suffer and limit our ability to pay dividends.

|

| • |

Variable rate indebtedness could subject us to interest rate risk, which could cause our debt service obligations to increase significantly.

|

| • |

We may not be able to finance our future capital commitments.

|

| • |

The current state of the global financial markets and current economic conditions may adversely impact our results of operation, financial condition, cash flows and ability to obtain financing or refinance our existing and future

credit facilities on acceptable terms.

|

| • |

We cannot assure you that we will be able to refinance our indebtedness.

|

| • |

We are subject to certain risks with respect to our counterparties on contracts, and failure of such counterparties to meet their obligations could cause us to suffer losses or negatively impact our results of operations and cash

flows.

|

| • |

Our share price may continue to be highly volatile, which could lead to a loss of all or part of a shareholder’s investment.

|

| • |

We operate in a cyclical and volatile industry and cannot guarantee that we will continue to make cash distributions.

|

| • |

Future sales of our common stock could cause the market price of our common stock to decline.

|

| • |

Ineffective internal controls could impact the Company’s business and financial results.

|

| • |

Increasing scrutiny and changing expectations from investors, lenders and other market participants with respect to our Environmental, Social and Governance (“ESG”) policies may impose additional costs on us or expose us to additional

risks.

|

| • |

A decision of our Board of Directors and the laws of Bermuda may prevent the declaration and payment of dividends.

|

| • |

We have antitakeover protections which could prevent a change of control.

|

| • |

If our vessels call on ports located in countries or territories that are subject to sanctions or embargoes imposed by the U.S. government, the European Union, the United Nations or other governmental authorities, it could result in

monetary fines or other penalties, and may adversely affect our reputation and the market and trading price of our common stock.

|

| • |

Because we are a foreign corporation, you may not have the same rights that a shareholder in a U.S. corporation may have.

|

| • |

We are incorporated in Bermuda and it may not be possible for our investors to enforce U.S. judgments against us.

|

| • |

We may have to pay tax on United States source income, which would reduce our earnings.

|

| • |

If the United States Internal Revenue Service were to treat us as a “passive foreign investment company,” that could have adverse tax consequences for United States shareholders.

|

| • |

Changes in tax laws and unanticipated tax liabilities could materially and adversely affect the taxes we pay, results of operations and financial results.

|

| • |

We may become subject to taxation in Bermuda which would negatively affect our results.

|

| • |

As a Bermuda exempted company incorporated under Bermuda law with subsidiaries in another offshore jurisdiction, our operations may be subject to economic substance requirements.

|

Risks Related to Our Business and Financial Condition

If the Suezmax tanker industry, which historically has been cyclical and volatile, is depressed in the future, our revenues, earnings and available cash flow may decrease.

It should be noted that we are specializing in Suezmax tankers. Historically, the tanker industry has been highly cyclical, with volatility in profitability, charter rates and asset values

resulting from changes in the supply of and demand for tanker capacity. Fluctuations in charter rates and tanker values result from changes in the supply of and demand for tanker capacity and changes in the supply of and demand for oil and oil

products. These factors may adversely affect the rates payable and the amounts we receive in respect of our vessels. The armed conflicts in Ukraine and in Israel and Gaza have continued to disrupt energy production and trade patterns, including

shipping in the Black Sea, Red Sea and elsewhere, and its impact on energy demand and costs is expected to remain uncertain. Our ability to re-charter our vessels on the expiration or termination of their current spot and time charters and the

charter rates payable under any renewal or replacement charters will depend upon, among other things, economic conditions in the tanker market and we cannot guarantee that any renewal or replacement charters we enter into will be sufficient to

allow us to operate our vessels profitably.

The factors that influence demand for tanker capacity include:

| • |

supply of and demand for oil and oil products;

|

| • |

global and regional economic and political conditions and developments, including developments in international trade, including the increased vessel attacks and piracy in the Red Sea in connection with the conflict between Israel and

Hamas, national oil reserves policies, fluctuations in industrial and agricultural production and armed conflicts;

|

| • |

regional availability of refining capacity and inventories compared to geographies of oil production regions;

|

| • |

environmental and other legal and regulatory developments;

|

| • |

the distance oil and oil products are to be moved by sea;

|

| • |

changes in seaborne and other transportation patterns, including changes in the distances over which tanker cargoes are transported by sea;

|

| • |

increases in the production of oil in areas linked by pipelines to consuming areas, the extension of existing, or the development of new, pipeline systems in markets we may serve, or the conversion of existing non-oil pipelines to oil

pipelines in those markets;

|

| • |

currency exchange rates;

|

| • |

weather and acts of God, natural disasters and health disasters;

|

| • |

changes in consumption of oil and petroleum products due to competition from supply and demand for alternative sources of energy and from other shipping companies and other modes of transport;

|

| • |

international sanctions, embargoes, import and export restrictions, nationalizations, piracy, terrorist attacks and armed conflicts, including the conflicts between Russia and Ukraine and between Israel and Hamas, and potential

physical disruption of shipping routes as a result thereof;

|

| • |

any restrictions on crude oil production imposed by the Organization of the Petroleum Exporting Countries, or OPEC, and non-OPEC oil producing countries;

|

| • |

economic slowdowns caused by public health events such as the diseases and viruses affecting livestock and humans including pandemics; and

|

| • |

regulatory changes including regulations adopted by supranational authorities and/or industry bodies, such as safety and environmental regulations and requirements by major oil companies.

|

The factors that influence the supply of tanker capacity include:

| • |

the demand for alternative energy resources;

|

| • |

current and expected purchase orders for tankers;

|

| • |

the number of tanker newbuilding deliveries;

|

| • |

any potential delays in the delivery of newbuilding vessels and/or cancellations of newbuilding orders;

|

| • |

the scrapping rate of older tankers;

|

| • |

technological advances in tanker design and capacity, propulsion technology and fuel consumption efficiency;

|

| • |

tanker charter rates, which are affected by factors that may affect the rate of newbuilding, swapping and laying up of tankers;

|

| • |

port and canal congestion;

|

| • |

price of steel and vessel equipment;

|

| • |

conversion of tankers to other uses or conversion of other vessels to tankers;

|

| • |

with respect to tanker vessel supply, demand for alternative sources of energy and supply and demand for energy resources and oil and petroleum products;

|

| • |

product imbalances (affecting the level of trading activity) and developments in international trade;

|

| • |

developments in international trade, including refinery additions and closures;

|

| • |

the phasing of maritime shipping into the EU Emission Trading Scheme (the “ETS”), which applies to all large ships of 5,000 gross tonnage or above;

|

| • |

the number of tankers that are out of service; and

|

| • |

changes in environmental and other regulations that may limit the useful lives of tankers.

|

In 2023, the tanker market was strongly impacted by geopolitical events. United States and EU/G7 sanctions against Russian oil products officially took effect on February 5, 2023, which

reinforced the trade on tonne mile recalibration that had already begun in 2022 in anticipation of the sanctions. In early October 2023, a military conflict in the Middle East and subsequent attacks in the region and against vessels forced

several vessels to reroute away from the Red Sea. This added to the ton-mile growth already seen from the sanctions against Russia.

Geopolitical factors and restrictions on Panama Canal transits similarly resulted in longer sailing patterns. The consequent trade recalibration towards longer haul trade led to a change in

tanker freight rates towards higher average levels and increased rate volatility.

The factors affecting the supply and demand for tankers have been volatile and are outside of our control, and the nature, timing and degree of changes in industry conditions are unpredictable,

including those discussed above. Continued volatility may reduce demand for transportation of oil over longer distances and increase supply of tankers to carry that oil, which may have a material adverse effect on our business, financial

condition, results of operations, cash flows, ability to pay dividends and existing contractual obligations.

We anticipate that the future demand for our tankers will be dependent upon economic growth in the world’s economies, seasonal and regional changes in demand, changes in the capacity of the

global tanker fleet and the sources and supply of oil and petroleum products to be transported by sea. Given the low number of new tankers currently on order with shipyards, the capacity of the global tanker fleet seems likely to be muted, but

there can be no assurance as to the timing or extent of future economic growth. Adverse economic, political, social or other developments could have a material adverse effect on our business and operating results, including possible impairment

charges against our earnings.

Declines in oil and natural gas prices or decreases in demand for oil and natural gas for an extended period of time, or market expectations of potential decreases in these prices and demand,

could negatively affect our future growth in the tanker and offshore sector. Sustained periods of low oil and natural gas prices typically result in reduced exploration and extraction because oil and natural gas companies’ capital expenditure

budgets are subject to cash flow from such activities and are therefore sensitive to changes in energy prices. Sustained periods of high oil prices on the other hand may be destructive for demand. These changes in commodity prices can have a

material effect on demand for our services, and periods of low demand can cause excess vessel supply and intensify the competition in the industry, which often results in vessels, particularly older and less technologically advanced vessels,

being idle for long periods of time. We cannot predict the future level of demand for our services or future conditions of the oil and natural gas industry. Any decrease in exploration, development or production expenditures by oil and natural

gas companies or decrease in the demand for oil and natural gas could reduce our revenues and materially harm our business, results of operations and cash available for distribution.

We are dependent on spot charters and any decrease in spot charter rates in the future may adversely affect our earnings, our ability to pay dividends and our ability to repay our financial liabilities.

The 20 vessels that we currently operate are primarily employed in the spot market with the two 2022-built vessels chartered out on six-year time charter agreements, and two vessels on longer

term time-charter agreements expiring in the latter part of 2024. We are therefore highly dependent on spot market charter rates. The spot market is very volatile and there have been and will be periods when spot charter rates decline below the

operating cost of vessels. If future spot charter rates decline, we may be unable to operate our vessels trading in the spot market profitably, meet our obligations, including payments on indebtedness, or pay dividends in the future. Furthermore,

as charter rates for spot charters are fixed for a single voyage which may last up to several weeks, during periods in which spot charter rates are rising, we will generally experience delays in realizing the benefits from such increases.

We will be exposed to prevailing charter rates in the crude tanker sectors when these vessels’ existing charters expire, and to the extent the counterparties to our fixed-rate charter contracts

fail to honor their obligations to us. We will also enter into spot charters in the future. The spot charter market may fluctuate significantly based upon tanker and oil supply and demand.

The successful operation of our vessels in the competitive spot charter market depends on, among other things, obtaining profitable spot charters and minimizing, to the extent possible, time

spent waiting for charters and time spent traveling in ballast to pick up cargo. When the current charters for our fleet expire or are terminated, it may not be possible to re-charter these vessels at similar rates, or at all, or to secure

charters for any vessels we agree to acquire at similarly profitable rates, or at all. As a result, we may have to accept lower rates or experience off hire time for our vessels, which would adversely impact our revenues, results of operations,

including impairment charges against our earnings, and financial condition.

Changes in the price of fuel and regulations may adversely affect our profits.

Fuel, including bunkers, is a significant, if not the largest, expense in our shipping operations, and changes in the price of fuel may adversely affect our profitability. The price and supply

of fuel is unpredictable and fluctuates based on events outside our control, including geopolitical developments, such as the ongoing conflict between Russia and Ukraine and between Israel and Hamas, supply and demand for oil and gas, actions by

OPEC and other oil and gas producers, war and unrest in oil producing countries and regions, regional production patterns and environmental concerns, which may reduce our profitability and have a material adverse effect on our future performance,

results of operations, cash flows and financial position.

Effective January 1, 2020, the International Maritime Organization, or IMO, implemented a new regulation for a 0.50% global sulfur cap on emissions from vessels. Under this new global cap,

vessels must use marine fuels with a sulfur content of no more than 0.50% against the former regulations specifying a maximum of 3.50% sulfur in an effort to reduce the emission of sulfur oxide into the atmosphere.

All of our vessels have transitioned to burning IMO compliant fuels. Low sulfur fuel of 0.50% sulfur content or lower, is presently more expensive than the non-compliant Heavy Fuel Oil

containing 3.5% sulfur and may become more expensive.

Our operations and the performance of our vessels, and as a result our results of operations, cash flows and financial position, may be negatively affected to the extent that compliant sulfur

fuel oils are unavailable, of low or inconsistent quality, or upon occurrence of any of the other foregoing events. Costs of compliance with these and other related regulatory changes may be significant and may have a material adverse effect on

our future performance, results of operations, cash flows and financial position. As a result, an increase in the price of fuel beyond our expectations may adversely affect our profitability at the time of charter negotiation. Further, fuel may

become much more expensive in the future, which may reduce the profitability and competitiveness of our business versus other forms of transportation.

Inability to renew the fleet would adversely affect our business, results of operations, financial condition and ability to pay dividends.

If we do not set aside funds or are unable to borrow or raise funds for vessel replacement, we will be unable to replace the vessels in our fleet upon the expiration of their useful lives. Our

cash flows and income are dependent on the revenues earned by the chartering of our vessels. If we are unable to replace the vessels in our fleet upon the expiration of their useful lives, our business, results of operations, financial condition

and ability to pay dividends would be adversely affected. Any funds set aside for vessel replacement will not be available for dividends.

The international Suezmax tanker industry has experienced volatile charter rates and vessel values and there can be no assurance that these charter rates and vessel values will not decrease in

the near future.

The Baltic Dirty Tanker Index, or the BDTI, a U.S. dollar daily average of charter rates issued by the Baltic Exchange that takes into account input from brokers around the

world regarding crude oil fixtures for various routes and oil tanker vessel sizes, is volatile. In 2023, the BDTI followed seasonal patterns with less volatility than seen in 2022, with the average for the year coming in at 1,149, slightly lower

than the 1,390 reached in 2022. The 2022-numbers are somewhat inflated by the Russian invasion in Ukraine and the following sanctions regime. The Baltic Exchange omitted two Russia related trade routes from the BDTI index from 4Q 2022 that helps

explain the lower average for 2023. During 2023, the BDTI reached a high of 1,648 and a low of 713 compared to a high of 2,496 and a low of 679 in 2022. The Baltic Clean Tanker Index, or BCTI, a comparable index to the BDTI, has similarly been

strong with a high of 1,250 and a low of 563 in 2023. This compares to a high of 2,143 and a low of 543 in 2022. Similar to the BDTI, the BCTI saw higher volatility and higher levels in 2022 compared to 2023 due to trades included in the index

that was not necessarily representative for the broader tanker market. Although slightly lower, markets in 2024 have continued their solid performance, and the BDTI and BCTI were at 1,173 and 995, respectively, as of April 16, 2024.There can be

no assurance that the crude oil and petroleum products charter market will increase or continue at the current levels, and the market could again decline. This volatility in charter rates depends, among other factors, on changes in the supply and

demand for tanker capacity and changes in the supply and demand for oil and oil products, the demand for crude oil and petroleum products, the inventories of crude oil and petroleum products in the United States and in other industrialized

nations, oil refining volumes, oil prices, and any restrictions on crude oil production imposed by OPEC and non-OPEC oil producing countries.

Charter rates in the Suezmax tanker industry are volatile. We anticipate that future demand for our vessels, and in turn our future charter rates, will be dependent upon economic growth in the

world’s economies, as well as seasonal and regional changes in demand and changes in the capacity of the world’s fleet. There can be no assurance that economic growth will not stagnate or decline leading to a decrease in vessel values and charter

rates. A decline in vessel values and charter rates would have an adverse effect on our business, financial condition, results of operation and ability to pay dividends.

Our results of operations are subject to seasonal fluctuations, which may adversely affect our financial condition.

We operate our vessels in markets that have historically exhibited seasonal variations in demand and, as a result, charter rates. Seaborne trading and distribution patterns are primarily

influenced by the relative advantage of the various sources of production, locations of consumption, pricing differentials and seasonality. Changes to the trade patterns of oil and oil products may have a significant negative or positive impact

on the ton-mile and therefore the demand for our tankers. This could have a material adverse effect on our future performance, results of operations, cash flows and financial position.

A shift in consumer demand from oil towards other energy sources or changes to trade patterns for crude oil or refined oil products may have a material adverse effect on our

business.

A significant portion of our earnings are related to the oil industry. A shift in or disruption of consumer demand from oil towards other energy sources such as electricity, natural gas,

liquified natural gas, renewable energy, hydrogen or ammonia will potentially affect the demand for our vessels. A shift from the use of internal combustion engine vehicles may also reduce the demand for oil. These factors could have a material

adverse effect on our future performance, results of operations, cash flows and financial position.

“Peak oil” is the year when the maximum rate of extraction of oil is reached. The International Energy Agency (“IEA”) recently announced a forecast of “peak oil” during the late 2020s. OPEC

maintains that “peak oil” will not be reached until at least 2040, despite transition toward other energy sources. Irrespective of “peak oil”, the continuing shift in consumer demand from oil towards other energy resources such as wind energy,

solar energy, hydrogen energy, nuclear energy or renewable energy, which appears to be accelerating as a result of shifts in government commitments and support for energy transition programs, may have a material adverse effect on our future

performance, results of operations, cash flows and financial position.

Seaborne trading and distribution patterns are primarily influenced by the relative advantage of the various sources of production, locations of consumption, pricing differentials and

seasonality. Changes to the trade patterns of crude oil or refined oil products may have a significant negative or positive impact on the ton-mile and therefore the demand for our tankers. This could have a material adverse effect on our future

performance, results of operations, cash flows and financial position.

The value of our vessels may be depressed at the time we decide to sell a vessel.

Tanker values have generally experienced high volatility. Investors can expect the fair market value of our tankers to fluctuate, depending on general economic and market conditions affecting the

tanker industry and competition from other shipping companies, types and sizes of vessels and other modes of transportation. In addition, as vessels age, they generally decline in value. These factors will affect the value of our vessels for

purposes of covenant compliance under our borrowing facilities and at the time of any vessel sale. If for any reason we sell a tanker at a time when tanker prices have fallen, the sale may be at less than the tanker’s carrying amount in our

financial statements, with the result that we would also incur a loss on the sale and a reduction in earnings from impairment charges, which could reduce our ability to pay dividends and negatively affect our business, financial condition and

operating results. The carrying values of our vessels may not represent their charter-free market value at any point in time.

An over-supply of Suezmax tanker capacity may lead to reductions in charter rates, vessel values, and profitability.

The market supply of Suezmax tankers is affected by a number of factors such as demand for energy resources, oil, and petroleum products, as well as overall economic growth in parts of the world

economy, including Asia,.

There has been a global trend towards energy efficient technologies, lower environmental emissions and alternative sources of energy. In the long-term, demand for oil may be reduced by increased

availability of such energy sources and machines that run on them. Furthermore, if the capacity of new ships delivered exceeds the capacity of tankers being scrapped and lost, tanker capacity will increase. If the supply of tanker capacity

increases and if the demand for tanker capacity does not increase correspondingly, charter rates and vessel values could materially decline. These changes could have an adverse effect on our business, results of operations and financial position.

If the capacity of new ships delivered exceeds the capacity of tankers being scrapped and lost, tanker capacity will increase. If the supply of tanker capacity increases and if the demand for

tanker capacity does not increase correspondingly, charter rates could materially decline. A reduction in charter rates and the value of our vessels may have a material adverse effect on our results of operations and our ability to pay dividends.

Delays or defaults by the shipyards in the construction of newbuildings could increase our expenses and diminish our net income and cash flows.

Vessel construction projects are generally subject to risks of delay that are inherent in any large construction project, which may be caused by numerous factors, including shortages of

equipment, materials or skilled labor, unscheduled delays in the delivery of ordered materials and equipment or shipyard construction, failure of equipment to meet quality and/or performance standards, financial or operating difficulties

experienced by equipment vendors or the shipyard, unanticipated actual or purported change orders, inability to obtain required permits or approvals, design or engineering changes and work stoppages and other labor disputes, adverse weather

conditions, pandemics or any other events of force majeure. Significant delays could adversely affect our financial position, results of operations and cash flows. Additionally, failure to complete a project on time may result in the delay of

revenue from that vessel, and we will continue to incur costs and expenses related to delayed vessels, such as supervision expense and interest expense for the issued and outstanding debt. As of December 31, 2023, we have not placed any orders

for Suezmax vessels and as such, we are not exposed to any risk related to construction of newbuildings.

Terrorist attacks and international hostilities and instability can affect the tanker industry, which could adversely affect our business.

We conduct most of our operations outside of the United States, and our business, results of operations, cash flows, financial condition and ability to pay dividends, if any, in the future may be

adversely affected by changing economic, political and government conditions in the countries and regions where our vessels are employed or registered. Moreover, we operate in a sector of the economy that is likely to be adversely impacted by the

effects of political conflicts.

Currently, the world economy continues to face a number of actual and potential challenges, including the war between Ukraine and Russia and between Israel and Hamas, current trade tension

between the United States and China, political instability in the Middle East and the South China Sea region and other geographic countries and areas, terrorist or other attacks, war (or threatened war) or international hostilities, such as those

between the United States and China, North Korea or Iran, and epidemics or pandemics, banking crises or failures, and real estate crises, such as the decreasing real estate property values in China.

In the past, political instability has also resulted in attacks on vessels, mining of waterways and other efforts to disrupt international shipping, particularly in the Arabian Gulf region and

most recently in the Black Sea in connection with the conflict between Russia and the Ukraine and in connection with the recent attacks by the Houthi movement in the Red Sea following the recent conflicts between Israel and Hamas. Acts of

terrorism and piracy have also affected vessels trading in regions such as the South China Sea and the Gulf of Aden off the coast of Somalia. Any of these occurrences could have a material adverse impact on our future performance, results of

operation, cash flows and financial position.

These factors could also increase the costs to the Company of conducting its business, particularly crew, insurance and security costs, and prevent or restrict

the Company from obtaining insurance coverage, all of which have a material adverse effect on our business, financial condition, results of operations and cash flows.

We rely on our information systems to conduct our business, and failure to protect these systems against security breaches could adversely affect our business and results of operations.

Additionally, if these systems fail or become unavailable for any significant period of time, our business could be harmed.

We rely on our computer systems and network infrastructure across our operations, including IT systems on our vessels operated by our technical managers. The safety and security of our vessels

and efficient operation of our business, including processing, transmitting and storing electronic and financial information, are dependent on computer hardware and software systems, which are increasingly vulnerable to security breaches and

other disruptions. Any significant interruption or failure of our information systems or any significant breach of security could adversely affect our business and results of operations.

Our vessels rely on information systems for a significant part of their operations, including navigation, provision of services, propulsion, machinery management, power control, communications

and cargo management. We have in place safety and security measures on our vessels and onshore operations to secure our vessels against cyber-security attacks and any disruption to their information systems. However, these measures and technology

may not adequately prevent security breaches despite our continuous efforts to upgrade and address the latest known threats. A disruption to the information system of any of our vessels could lead to, among other things, wrong routing, collision,

grounding and propulsion failure.

Beyond our vessels, we rely on industry accepted security measures and technology to securely maintain confidential and proprietary information maintained on our information systems. However,

these measures and technology may not adequately prevent security breaches. The technology and other controls and processes designed to secure our confidential and proprietary information, detect and remedy any unauthorized access to that

information were designed to obtain reasonable, but not absolute, assurance that such information is secure and that any unauthorized access is identified and addressed appropriately. Such controls may in the future fail to prevent or detect,

unauthorized access to our confidential and proprietary information. In addition, the foregoing events could result in violations of applicable privacy and other laws. If confidential information is inappropriately accessed and used by a third

party or an employee for illegal purposes, we may be responsible to the affected individuals for any losses they may have incurred as a result of misappropriation. In such an instance, we may also be subject to regulatory action, investigation or

liable to a governmental authority for fines or penalties associated with a lapse in the integrity and security of our information systems.

Our operations, including our vessels, and business administration could be targeted by individuals or groups seeking to sabotage or disrupt such systems and networks, or to steal data, and these

systems may be damaged, shutdown or cease to function properly (whether by planned upgrades, force majeure, telecommunications failures, hardware or software break-ins or viruses, other cyber-security incidents or otherwise). For example, the

information systems of our vessels may be subject to threats from hostile cyber or physical attacks, phishing attacks, human errors of omission or commission, structural failures of resources we control, including hardware and software, and

accidents and other failures beyond our control. The threats to our information systems are constantly evolving and have become increasingly complex and sophisticated. Furthermore, such threats change frequently and are often not recognized or

detected until after they have been launched, and therefore, we may be unable to anticipate these threats and may not become aware in a timely manner of such a security breach, which could exacerbate any damage we experience. We do not maintain

cyber-liability insurance at this time to cover such losses. As a result, a cyber-attack or other breach of any such information technology systems could have a material adverse effect on our business, results of operations and financial

condition. As of the date of this annual report, we have not experienced any material cybersecurity incident which would be disclosable under SEC guidelines.

We may be required to expend significant capital and other resources to protect against and remedy any potential or existing security breaches and their consequences. A cyber-attack could

materially disrupt our operations, which could also adversely affect the safety of our operations or result in the unauthorized release or alteration of information in our systems. Such an attack on us could result in significant expenses to

investigate and repair security breaches or system damages and could lead to litigation, fines, other remedial action, heightened regulatory scrutiny and diminished customer confidence. In addition, our remediation efforts may not be successful

and we may not have adequate insurance to cover these losses.

The unavailability of the information systems or the failure of these systems to perform as anticipated for any reason could disrupt our business and could have a material adverse effect on our

business, results of operations, cash flows and financial condition.

Moreover, cyber-attacks against the Ukrainian government and other countries in the region have been reported in connection with the ongoing conflict between Russia and

Ukraine. To the extent such attacks have collateral effects on global critical infrastructure or financial institutions or us, such developments could adversely affect our business, operating results and financial condition. It is difficult to

assess the likelihood of such threat and any potential impact at this time.

The EU has adopted a comprehensive overhaul of its data protection regime from the current national legislative approach to a single European Economic Area Privacy

Regulation, the General Data Protection Regulation (“GDPR”). The GDPR came into force on May 25, 2018, and applies to organizations located within the EU, as well as to organizations located outside of the EU if they offer goods or services to,

or monitor the behavior of, EU data subjects. It imposes a strict data protection compliance regime with significant penalties and includes new rights such as the “portability” of personal data. It applies to all companies processing and holding

the personal data of data subjects residing in the EU, regardless of the company’s location. Implementation of the GDPR could require changes to certain of our business practices, thereby increasing our costs. Our failure to adhere to or

successfully implement processes in response to changing regulatory requirements in this area could result in legal liability or impairment to our reputation in the marketplace, which could have a material adverse effect on our business,

financial condition and results of operations.

Further, the SEC, which, on July 26, 2023, adopted amendments requiring the prompt public disclosure of certain cybersecurity breaches. If we fail to comply with the relevant laws and

regulations, we could suffer financial losses, a disruption of our businesses, liability to investors, regulatory intervention or reputational damage. For more information on our cybersecurity risk management and strategy, please see “Item 16K.

Cybersecurity”.

If we do not manage relationships with customers or successfully integrate any acquired Suezmax tankers, we may not be able to grow or effectively manage our growth.

Our future growth will depend upon a number of factors, some of which may not be within our control. These factors include our ability to:

| • |

identify suitable tankers and/or shipping companies for acquisitions at attractive prices, which may not be possible if asset prices rise too quickly,

|

| • |

manage relationships with customers and suppliers,

|

| • |

identify businesses engaged in managing, operating or owning tankers for acquisitions or joint ventures,

|

| • |

integrate any acquired tankers or businesses successfully with our then-existing operations,

|

| • |

hire, train and retain qualified personnel and crew to manage and operate our growing business and fleet,

|

| • |

identify additional new markets,

|

| • |

improve our operating, financial and accounting systems and controls, and

|

| • |

obtain required financing for our existing and new operations.

|

Our failure to effectively identify, purchase, manage customer relationships and integrate any tankers or businesses could adversely affect our business, financial condition and results of

operations. We may incur unanticipated expenses as an operating company. It is possible that the number of employees employed by the company, or current operating and financial systems may not be adequate as we implement our plan to expand the

size of our fleet. Finally, acquisitions may require additional equity issuances or debt issuances (with amortization payments), both of which could lower dividends per share. If we are unable to expand or execute the certain aspects of our

business or events noted above, our financial condition and dividend rates may be adversely affected.

Because some of our expenses are incurred in foreign currencies, we are exposed to exchange rate fluctuations, which could negatively affect our results of operations.

The charterers of our vessels pay us primarily in U.S. dollars. While we mostly incur our expenses in U.S. dollars, we may incur expenses in other currencies, most notably the Norwegian Kroner.

Declines in the value of the U.S. dollar relative to the Norwegian Kroner, or the other currencies in which we may incur expenses in the future, would increase the U.S. dollar cost of paying these expenses and thus would affect our results of

operations.

Risks Related to the Operations of Our Vessels and Regulations

The operation of Suezmax tankers involves certain unique operational risks.

The operation of Suezmax tankers has unique operational risks associated with the transportation of oil. An oil spill may cause significant environmental damage, and a catastrophic spill could

exceed the insurance coverage available. Compared to other types of vessels, tankers are exposed to a higher risk of damage and loss by fire, whether ignited by a terrorist attack, collision, or other cause, due to the high flammability and high

volume of the oil transported in tankers.

Further, our vessels and their cargoes will be at risk of being damaged or lost because of events such as marine disasters, bad weather and other acts of God, business interruptions caused by

mechanical failures, grounding, fire, explosions and collisions, human error, war, terrorism, piracy, diseases, quarantine and other circumstances or events. Changing economic, regulatory and political conditions in some countries, including

political and military conflicts, have from time to time resulted in attacks on vessels, mining of waterways, piracy, terrorism, labor strikes and boycotts. These hazards may result in death or injury to persons, loss of revenues or property, the

payment of ransoms, environmental damage, higher insurance rates, damage to our customer relationships and market disruptions, delay or rerouting.

If our vessels suffer damage, they may need to be repaired at a drydocking facility. The costs of drydock repairs are unpredictable and may be substantial. We may have to pay drydocking costs

that our insurance does not cover at all or in full. The loss of revenues while these vessels are being repaired and repositioned, as well as the actual cost of these repairs, may be material. In addition, space at drydocking facilities is

sometimes limited and not all drydocking facilities are conveniently located. We may be unable to find space at a suitable drydocking facility or our vessels may be forced to travel to a drydocking facility that is not conveniently located

relative to our vessels’ positions. The loss of earnings while these vessels are forced to wait for space or to travel to more distant drydocking facilities may also be material. Further, the total loss of any of our vessels could harm our

reputation as a safe and reliable vessel owner and operator. If we are unable to adequately maintain or safeguard our vessels, we may be unable to prevent any such damage, costs or loss which could negatively impact our business, financial

condition, results of operations, cash flows and ability to pay dividends.

We operate our Suezmax tankers worldwide and as a result, our vessels are exposed to international risks which may reduce revenue or increase expenses.

The international shipping industry is an inherently risky business involving global operations. The operations of ocean-going vessels in international trade is affected by a number of risks. Our

vessels are at a risk of damage or loss because of events such as mechanical failure, collision, human error, war, terrorism, piracy, cargo loss and bad weather. In addition, changing economic, regulatory and political conditions in some

countries, including political and military conflicts, have from time to time resulted in attacks on vessels, mining of waterways, piracy, terrorism, labor strikes and boycotts. These sorts of events could interfere with shipping routes and

result in market disruptions which may reduce our revenue or increase our expenses.

International shipping is subject to various security and customs inspections and related procedures in countries of origin and destination and trans-shipment points. Inspection procedures can

result in the seizure of the cargo and/or our vessels, delays in loading, offloading or delivery, and the levying of customs duties, fines or other penalties against us. It is possible that changes to inspection procedures could impose additional

financial and legal obligations on us. Furthermore, changes to inspection procedures could also impose additional costs and obligations on our customers and may, in certain cases, render the shipment of certain types of cargo uneconomical or

impractical. Any such changes or developments may have a material adverse effect on our business, results of operations, cash flows, financial condition and available cash.

The smuggling of drugs or other contraband onto our vessels may lead to governmental claims against us.

We expect that our vessels will call in ports where smugglers attempt to hide drugs and other contraband on vessels, with or without the knowledge of crew members. To the extent our vessels are

found with contraband, whether inside or attached to the hull of our vessel and whether with or without the knowledge of any of our crew, we may face governmental or other regulatory claims which could have an adverse effect on our business,

results of operations, cash flows, financial condition and ability to pay dividends.

Failure to comply with the U.S. Foreign Corrupt Practices Act could result in fines, criminal penalties and an adverse effect on our business.

We may operate in a number of countries throughout the world, including countries suspected to have a risk of corruption. We are committed to doing business in accordance with applicable

anti-corruption laws. We are subject to the risk that we, our service providers or their respective officers, directors, employees and agents may take actions determined to be in violation of such anti-corruption laws, including the U.S. Foreign

Corrupt Practices Act of 1977, as amended (the “FCPA”). Any such violation could result in substantial fines, sanctions, civil and/or criminal penalties, curtailment of operations in certain jurisdictions, and might adversely affect our business,

earnings or financial condition. In addition, actual or alleged violations could damage our reputation and ability to do business. Furthermore, detecting, investigating, and resolving actual or alleged violations is expensive and can consume

significant time and attention of our senior management.

Acts of piracy on ocean-going vessels could adversely affect our business.

Acts of piracy have historically affected ocean-going vessels trading in regions of the world such as the South China Sea, the Red Sea, the Gulf of Aden off the Coast of Somalia and, in

particular, the Gulf of Guinea region off of Nigeria, which experienced increased incidents of piracy in recent years. Acts of piracy and war like conditions could result in harm or danger to the crews onboard our vessels. In addition, if piracy

attacks occur in regions in which our vessels are deployed that insurers’ characterized as “war risk” zones or by the Joint War Committee as “war and strikes” listed areas, premiums payable for such coverage could increase significantly and such

insurance coverage may be more difficult to obtain. Furthermore, the recent Houthi seizures and attacks on commercial vessels in the Red Sea and the Gulf of Aden have impacted the global economy as some companies, including Nordic American

Tankers Limited, have decided to reroute vessels to avoid the Suez Canal and Red Sea. In addition, crew costs, including costs which may be incurred to the extent we employ onboard security guards, could increase in such circumstances. We may not

be adequately insured to cover losses from these incidents, which could have a material adverse effect on us. In addition, detention hijacking as a result of an act of piracy against our vessels, or an increase in cost, or unavailability of

insurance for our vessels, could have a material adverse impact on our business, financial condition and results of operations.

Maritime claimants could arrest one or more of our vessels, which could interrupt our cash flow.

Crew members, suppliers of goods and services to a vessel, shippers of cargo and other parties may be entitled to a maritime lien against a vessel for unsatisfied debts, claims or damages. In

many jurisdictions, a maritime lien-holder may enforce its lien by “arresting” or “attaching” a vessel through foreclosure proceedings. The arrest or attachment of one or more of our vessels could result in a significant loss of earnings for the

related off-hire period. In addition, in jurisdictions where the “sister ship” theory of liability applies, a claimant may arrest the vessel which is subject to the claimant’s maritime lien and any “associated” vessel, which is any vessel owned

or controlled by the same owner. In countries with “sister ship” liability laws, claims might be asserted against us or any of our vessels for liabilities of other vessels that we own.

Governments could requisition our vessels during a period of war or emergency resulting in a loss of earnings.

A government of a vessel’s registry could requisition for title or seize one or more of our vessels. Requisition for title occurs when a government takes control of a vessel and becomes the

owner. A government could also requisition one or more of our vessels for hire. Requisition for hire occurs when a government takes control of a vessel and effectively becomes the charterer at dictated charter rates. Generally, requisitions occur

during a period of war or emergency. Government requisition of one or more of our vessels could have a material adverse effect on our business, results of operations, cash flows, financial condition and ability to pay dividends.

If we purchase secondhand vessels, we may not receive warranties from the builder and operating cost may increase as a result of aging of the fleet.

Following a physical inspection of secondhand vessels prior to purchase, we do not have the same knowledge about their condition and cost of any required (or anticipated) repairs that we would

have had if these vessels had been built for and operated exclusively by us. Accordingly, we may not discover defects or other problems with such vessels prior to purchase. Any such hidden defects or problems, when detected may be expensive to

repair, and if not detected, may result in accidents or other incidents for which we may become liable to third parties. Also, when purchasing previously owned vessels, we do not receive the benefit of any builder warranties if the vessels we buy

are older than one year.

In general, the costs to maintain a vessel in good operating condition increase with the age of the vessel. Older vessels are typically less fuel efficient than more recently constructed vessels

due to improvements in engine technology. Governmental regulations, safety and other equipment standards related to the age of vessels may require expenditures for alterations or the addition of new equipment to some of our vessels and may

restrict the type of activities in which these vessels may engage. We cannot assure you that, as our vessels age, market conditions will justify those expenditures or enable us to operate our vessels profitably during the remainder of their

useful lives. As a result, regulations and standards could have a material adverse effect on our business, financial condition, results of operations, cash flows and ability to pay dividends.

Our insurance may not be adequate to cover our losses that may result from our operations due to the inherent operational risks of the tanker industry.

We carry insurance to protect us against most of the accident related risks involved in the conduct of our business, including marine hull and machinery insurance, protection and indemnity

insurance, which includes pollution risks, crew insurance and war risk insurance. However, we may not be adequately insured to cover losses from our operational risks, which could have a material adverse effect on us. Additionally, our insurers

may refuse to pay particular claims and our insurance may be voidable by the insurers if we take, or fail to take, certain action, such as failing to maintain certification of our vessels with applicable maritime regulatory organizations. Any

significant uninsured or under-insured loss or liability could have a material adverse effect on our business, results of operations, cash flows and financial condition and our ability to pay dividends. In addition, we may not be able to obtain

adequate insurance coverage at reasonable rates in the future during adverse insurance market. Any loss of a vessel or extended vessel off-hire, due to an accident or otherwise, could have a material adverse effect on our business, results of

operations and financial condition and our ability to pay dividends.

An increase in operating costs would decrease earnings and dividends per share.

Under the charters of all of our operating vessels, we are responsible for vessel operating expenses. Our vessel operating expenses include the costs of crew, lube oil, provisions, deck and

engine stores, insurance and maintenance and repairs, which depend on a variety of factors, many of which are beyond our control. If our vessels suffer damage, they may need to be repaired at a drydocking facility. The costs of drydock repairs

are unpredictable and can be substantial. Increases in any of these expenses would decrease earnings and dividends per share.

We may be unsuccessful in competing in the highly competitive international Suezmax tanker market.

The operation of Suezmax tankers and transportation of crude and petroleum products is extremely competitive. Competition arises primarily from other tanker owners, including major oil companies

as well as independent tanker companies. Competition for the transportation of oil and oil products can be intense and depends on price, location, size, age, condition and the acceptability of the tanker and its operators to the charterers.

Competitors with greater resources could enter and operate larger tanker fleets through consolidations or acquisitions, and may be able to offer more competitive prices and fleets. We will have to compete with other tanker owners, including major

oil companies as well as independent tanker companies and our market share may decrease in the future and we may not find profitable employment for our vessels, which could adversely affect our financial condition and our ability to expand our

business.

We are subject to laws and regulations which can adversely affect our business, results of operations, cash flows and financial condition, and our ability to pay dividends.

Our operations are subject to numerous laws and regulations in the form of international conventions and treaties, national, state and local laws and national and international regulations in

force in the jurisdictions in which our vessels operate or are registered, which can significantly affect the ownership and operation of our vessels. These requirements include, but are not limited to, the United States (U.S.) Oil Pollution Act

of 1990 (OPA), the Comprehensive Environmental Response, Compensation, and Liability Act (generally referred to as CERCLA), the U.S. Clean Water Act (CWA), the U.S. Clean Air Act (CAA), the U.S. Outer Continental Shelf Lands Act, European Union

(EU) Regulations, the IMO, International Convention on Civil Liability for Oil Pollution Damage of 1969 (as from time to time amended and generally referred to as CLC), the IMO International Convention for the Prevention of Pollution from Ships

of 1973 (as from time to time amended and generally referred to as MARPOL, including the designation of emission control areas (ECAs) thereunder), the IMO International Convention for the Safety of Life at Sea of 1974 (as from time to time

amended and generally referred to as SOLAS), the IMO International Convention on Load Lines of 1966 (as from time to time amended), the International Convention on Civil Liability for Bunker Oil Pollution Damage (generally referred to as the

Bunker Convention), the IMO’s International Management Code for the Safe Operation of Ships and for Pollution Prevention (generally referred to as the ISM Code), the International Convention for the Control and Management of Ships’ Ballast Water

and Sediments Discharge (generally referred to as the BWM Convention), International Ship and Port Facility Security Code (ISPS), and the U.S. Maritime Transportation Security Act of 2002 (generally referred to as the MTSA). Compliance with such

laws, regulations and standards, where applicable, may require installation of costly equipment or operational changes and may affect the resale value or useful lives of our vessels. We may also incur additional costs in order to comply with

other existing and future regulatory obligations, including, but not limited to, costs relating to air emissions, including greenhouse gases, the management of ballast waters, maintenance and inspection, development and implementation of

emergency procedures and insurance coverage or other financial assurance of our ability to address pollution incidents. These costs could have a material adverse effect on our business, results of operations, cash flows and financial condition