UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to _______

Commission File Number

(Exact name of Registrant as specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer |

|

|

(Address of principal executive offices, including Zip Code)

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|

||

|

|

|

||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

☒ |

|

Smaller reporting company |

||

Emerging growth company |

||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

As of June 30, 2023, the last day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was $

As of March 8, 2024, the registrant had

DOCUMENTS INCORPORATED BY REFERENCE

None

Auditor Firm Id: |

Auditor Name: |

Auditor Location: |

One Stop Systems, Inc.

FORM 10-K

For the Fiscal Year Ended December 31, 2023

Table of Contents

|

|

Page |

|

|

|

Item 1. |

4 |

|

Item 1A. |

26 |

|

Item 1B. |

46 |

|

Item 1C. |

Cybersecurity |

|

Item 2. |

48 |

|

Item 3. |

48 |

|

Item 4. |

48 |

|

|

|

|

|

|

|

Item 5. |

49 |

|

Item 6. |

49 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

50 |

Item 7A. |

69 |

|

Item 8. |

69 |

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

69 |

Item 9A. |

69 |

|

Item 9B. |

70 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

70 |

|

|

|

|

|

|

Item 10. |

71 |

|

Item 11. |

79 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

89 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

92 |

Item 14. |

92 |

|

|

|

|

|

|

|

Item 15. |

94 |

|

Item 16. |

94 |

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (“Annual Report”) contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact contained in this Annual Report, including statements regarding our future operating results, financial position and cash flows, our business strategy and plans and our objectives for future operations, are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. This Annual Report also contains estimates and other statistical data made by independent parties and by us relating to market size and growth and other data about our industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions and estimates of our future performance and the future performance of the markets in which we operate are necessarily subject to a high degree of uncertainty and risk. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “would,” “could,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Annual Report are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, operating results, business strategy, short-term and long-term business operations and objectives. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of risks, uncertainties and assumptions, including those described in Part I, Item 1A, “Risk Factors.” The events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

One Stop Systems, the One Stop Systems logo, and other trademarks or service marks of One Stop Systems appearing in this Annual Report are the property of One Stop Systems, Inc. This Annual Report also includes trademarks, trade names and service marks that are the property of other organizations. Solely for convenience, trademarks and trade names referred to in this Annual Report appear without the ® and ™ symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights, or that the applicable owner will not assert its rights, to these trademarks and trade names.

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly, and current reports, proxy statements and other information required by the Securities and Exchange Act of 1934, as amended (the “Exchange Act”), with the Securities and Exchange Commission (the “SEC”). Our SEC filings are available to the public on the SEC’s internet site at http://www.sec.gov.

On our internet website, http://www.onestopsystems.com, we post the following recent filings as soon as reasonably practicable after they are electronically filed with or furnished to the SEC: our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. The information in or accessible through the SEC and our website are not incorporated into, and are not considered part of, this Annual Report. Further, our references to the URLs for these websites are intended to be inactive textual references only.

3

PART I

ITEM 1. BUSINESS.

Company History

One Stop Systems, Inc. (“we,” “our,” “OSS,” or the “Company”) was originally incorporated as a California corporation in 1999, after initially being formed as a California limited liability company in 1998. On December 14, 2017, the Company was reincorporated as a Delaware corporation in connection with its initial public offering. The Company designs, manufactures, and markets specialized rugged high-performance compute ("HPC"), high speed switch fabrics and storage systems, which are designed to target edge applications for artificial intelligence ("AI") / machine learning ("ML"), sensor processing, sensor fusion and autonomy. The Company markets its products to manufacturers of equipment used for autonomous vehicles, medical, industrial, and military applications, with special focus on platforms that move, such as planes, trucks, ships, submarines, and mobile datacenters or command posts where sensor processing, sensor fusion, AI and ML are integrated to support such applications. If an application needs AI and/or autonomous capabilities, and it moves, OSS delivers the highest performance solutions that are designed to survive and enable these challenging applications.

During the year ended December 31, 2015, the Company formed a wholly owned subsidiary in Germany, One Stop Systems, GmbH (“OSS GmbH”). Then, in July 2016, the Company acquired Mission Technologies Group, Inc. (“Magma”) and its operations.

On August 31, 2018, the Company acquired Concept Development Inc. (“CDI”) located in Irvine, California. CDI specialized in the design and manufacture of custom high-performance computing systems for airborne in-flight entertainment, flight safety equipment, and networking systems. CDI’s business was fully integrated into the core operations of the Company as of June 1, 2020.

On October 31, 2018, OSS GmbH acquired 100% of the outstanding stock of Bressner Technology GmbH, a limited liability company registered under the laws of Germany and located near Munich, Germany (“Bressner”). Bressner designs and manufactures standard and customized servers, panel PCs, and PCIe accelerator systems. It also operates as a systems integrator with standard and custom all in one hardware systems and components. In addition, Bressner serves as a channel to market for OSS ruggedized datacenter level compute and storage products to the European and Middle Eastern markets.

Our principal executive offices are located at 2235 Enterprise Street, Suite 110, Escondido, California 92029, and our telephone number is (760) 745-9883. Our website address is www.onestopsystems.com. Information contained in, or accessible through, our website is for reference purposes only.

Business Overview

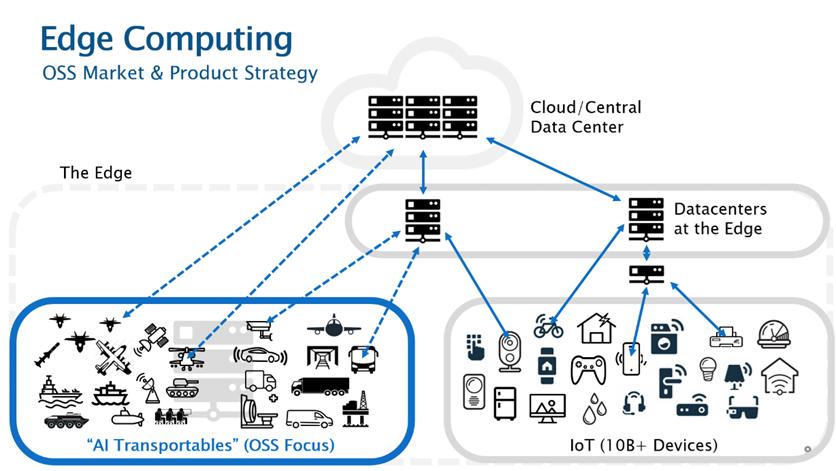

OSS designs, manufactures, and markets specialized high-performance compute, high speed switch fabrics and storage hardware and software, which are designed to target edge applications for AI/ML, sensor processing, sensor fusion and autonomy. Edge computing is a form of computing that is done on site, near a particular data source or the user, rather than in the cloud, minimizing the need for data to be processed in a remote datacenter. This growing trend increases computing performance and security, as the data does not have to travel to distant datacenter location. Edge computing is most recognizable in applications such as sensor processing, sensor fusion, autonomy and AI/ML. To meet the demands at the edge we offer specialized modules and systems that consist of computers, switch fabrics and storage products that incorporate the latest state-of-the art components with embedded proprietary software. Such modules and systems allow us to offer high-end solutions to target markets to be integrated into platforms, vehicles and applications.

The fast-growing edge computing space consists of three major segments. The first segment is comprised of smaller datacenters located near the user - on the edge. These typically include compute and storage racks in environmentally controlled buildings, similar to large cloud datacenters. Suppliers in this space tend to be the same large server and storage manufacturers whose products are used at cloud datacenters. The second segment includes billions of Internet-of-Things (“IOT”) devices that may reside in everything from home appliances to the factory production floor. These IOT devices and applications tend not to be challenged on performance and easily communicate up to the cloud or the datacenters on the edge. OSS does not focus on either of the foregoing segments. The third segment is called AI Transportables. These are primarily on land, in the air or at sea vehicles that need

4

datacenter level performance for sensor processing, sensor fusion, autonomy and AI/ML applications. This is where OSS’ vision and strategy is aligned, and where we believe that we offer the greatest unique value.

Examples of applications that utilize AI Transportables range from industrial autonomous trucks, mining equipment and smart agricultural equipment to military land, sea, and airborne weapon system platforms. Less mobile applications that utilize High Performance Compute ("HPC") or AI Transportables include items such as medical equipment, mobile command centers and certain datacenters.

Sensor fusion, autonomy and AI capabilities require these demanding applications to connect to a wide array of data sources and sensors, and to have the ability to quickly access and store large and ever-growing data sets. They must be able to maintain ultra-fast processing power to act on data or process sensor inputs in real time at the edge location, which is independent of whether a high-speed network, like 5G or a tactical data link, connects the edge application back to the distant central data or command centers. Standard servers and storage systems available in the market do not address, and typically will not survive, the AI Transportable requirements. Although the network or data link, if it exists, may transfer data, or be used for updates, the latency is not acceptable for many of these applications where time is of the essence. This increases the need for datacenter level performance using the latest generation of products from companies like NVIDIA, AMD, and Intel. In most of these applications, available space is limited and the number of inputs from sensors and other data sources are significant, thus, requiring high speed switch fabrics like the latest in PCI Express, for which OSS is a recognized expert in the market. In all cases at the edge there is a demanding operational environment that requires ruggedized solutions to ensure assured and continued operation, which must be balanced with size weight and power (“SWAP”) requirements. Solutions in this space must not only be light and fit into small volumes, but must also survive drops, g-forces and vibration. Additionally, they must continue to operate at extreme temperatures and in dusty or moist conditions.

While other edge computing suppliers may serve the needs of the environmentally controlled edge datacenters with the latest technology, the deployment of the same performance level in the AI Transportable space requires unique capabilities and know how, which is where we believe that we excel. Many companies that enter this space tend to offer solutions based on older and lower performance technology, whereas we advance our proprietary state-of-the-art technologies and utilize the latest generation of products to ensure superior performance. We leverage our proven track-record of delivering first-to-market advanced technologies and technical strength, working with the latest high-speed networks like PCI Express 5.0 and NVIDIA’s NVLink®. This is in addition to our expertise with rugged servers, compute acceleration and high-performance flash array storage systems. When combined with our execution and knowledge for deploying these systems in challenging environments, we bring the latest commercially available datacenter level technology and products to this market.

5

Business Strategy

We continue to execute our strategic commitment to the AI Transportable and rugged edge HPC market, and we believe that our engagement over the past two years in the markets and with customers and our current portfolio of business are validating this approach. In this portfolio we are witnessing some of our highest margins and repeat business and expanding levels of interest. Additionally, we have seen our five-year pipeline increase by over 25% in the past year as we pursue this strategy further.

Although we are seeing progress, it will continue to take time to pursue, secure, and turn these target opportunities into increased revenue and profits, especially as we secure positions in the military market. As part of this strategy, we are consistently focusing on expanding the number of customers and platforms while also securing multi-year contract opportunities in this space. We believe this focus provides us with a unique opportunity to drive growth and shareholder value. We will continue to execute current profitable business where we offer product and solution differentiation, but our primary focus will be on the AI Transportable market and our rugged edge HPC strategy.

We continue to see and pursue opportunities in both the commercial/industrial and military/government segments. Currently, our OSS military business accounts for approximately 25% of our overall sales, but we anticipate this will grow to 50% over the next few years and will leverage commerciality to increase margins. Commerciality is the ability to use commercial market pricing in defense procurements. We believe a balanced portfolio of commercial and military customers can serve as a strategic benefit in execution of the business, strategy, and growth. Both commercial and military markets are currently seeing an influx of autonomy and AI/ML applications that are driving market growth and strengthening opportunities. Commercial adoption of AI/ML is dramatically moving to the edge across almost all business segments. While military budgets may not expand dramatically on whole, the spend on autonomy and AI/ML represent the fastest areas of growth as the US and allied nations look to augment existing and field new sensors, platforms and weapon systems to maintain advantage over adversaries.

A key element of our business strategy is a product strategy based on technology leadership. We believe a first-to-market strategy is key to our ability to continue to win significant opportunities. As a result, we continue to develop new state-of-the-art products across a range of HPC demand, providing a unique value proposition for our customers in the targeted spaces. Current engagements for our products in the military space cover various autonomy, sensor fusion and AI/ML applications, including for multiple aircraft, drones, ships, helicopters, and land vehicles, as the Pentagon prioritizes incorporating advanced technologies into their equipment. We have pursued these engagements throughout 2023 by incorporating an AI compute and storage product strategy that applies the OSS expertise in three product levels that cover the needs of land, sea and air deployments.

At the high end, we introduced Rigel, which is a super compute edge platform. We believe that this product is currently the highest performance, most compact supercomputer in the market that can survive the most demanding edge environments, especially those in military programs available today and in the future. It brings to market the latest in Graphics Processing Units (“GPU”), Central Processing Unit (“CPU”), high speed PCI express switch fabric and memory products in a rugged compact form factor, to meet sensor processing, sensor fusion and AI/ML applications in this space. Rigel has been vetted by multiple large military prime contractors as well as the U.S. Department of Defense (“DOD”) directly for key, high visibility programs that we are pursuing.

At the mid-level, we have fielded our Short-depth Servers (“SDS”) in many commercial and government program wins due to its flexibility. The SDS provides integrated AI compute, data recording and storage at a performance level approaching Rigel, suitable for wider market adoption. In the fourth quarter of 2023, the 3U SDS was upgraded to the latest PCIe 5.0 performance levels and launched as a standard product and two original equipment manufacturer ("OEM") customer configurations that accounted for two new program wins. These upgrades consisted of advanced cold plate liquid cooling and liquid immersion options that widen the environments in which the SDS can be deployed. Top commercial applications for the SDS include autonomous trucks and ships and edge data analytics. The top applications for government use include AI sensor fusion, simulation, capturing AI datasets through data recording and serving high-speed data to crews with our Ion Accelerator™ data storage software.

At the low end of performance, but with a higher level of ruggedization, we have introduced Cernis™ and Donati™. These products create the most compact solution for autonomy, AI/ML and visualization. The Donati CPU/GPU compute and visualization systems are interconnected using the Cernis PCIe switch, creating an optimized data path that takes advantage of OSS low latency breakthroughs in PCIe interconnect, typically found in Rigel and SDS servers, while being highly rugged for use in wheeled and tracked land vehicles that require conduction cooling.

6

Our ability to drive the leading edge of technology is enabled by our strong relationships with strategic component manufactures, including NVIDIA (for GPUs, ARM processors and networking), NetList, and Micron (for flash memory), Broadcom (for PCIe switch components), and Intel and AMD (for CPUs). In many cases, we have access to product roadmaps and other technical information relating to future technology. Access to this information allows us to begin our design process well before the future components we are designing even exist. We have also expanded our market relationships to embrace companies in the AI/ML software space. These efforts allow us to establish relationships that enable our ability to offer end-to-end solutions for customers while also creating opportunity for these software companies to standardize on our hardware platforms.

We anticipate that the steps we have taken in implementing our strategy and the fast-growing markets that we are pursuing will provide accelerated revenue and margin growth for the Company over the coming years.

Industry Background and Market Opportunity

The notion of network-based computing dates to the 1960s, but many believe the first use of “cloud computing” in its modern context occurred in 2006 when Google’s then-CEO, Eric Schmidt, introduced the term during an industry conference. Years later, the explosive growth of internet of things (“IoT”) connected devices, along with new applications that require real-time computing power, started to create the drive for edge-computing systems. As the demand for AI on the edge and autonomous vehicles grew, so did the need for high-performance solutions to operate in harsh environments and reduce risk of loss of connectivity to the cloud.

Edge computing is one of the fastest growing markets in the computing space, driven by the need to do more at the edge. The concept of edge computing is simply deploying compute systems closer to the actual user of the system, rather than communicating with a distant cloud computing facility. According to Gartner, Inc., a leader in technology research, only 10% of data was gathered and processed at the edge in 2018; however, it is expected that this number will grow to 75% by 2025. This dramatic change is driving an expected growth of over 38% per year between today and 2028, according to Grand View Research, resulting in an estimated market of $61 billion later this decade.

The AI Transportable markets tend to implement sensor processing, sensor fusion, AI/ML, autonomous, and/or semi-autonomous solutions. We believe markets for these products are large and growing. Applications deploying these technologies today, or that we expect to do so in the future, include, without limitation:

We expect these applications to deploy increasingly faster computing systems to meet industry and competitive goals. Whereas the goal used to be for an edge compute platform to perform a single application, such as autonomous navigation, now this has been expanded to include in excess of ten or more AI applications running simultaneously. This expansion requires significantly more compute power and data storage than traditional embedded computers can manage while operating in harsh, challenging, and space constrained environments.

We currently estimate that the market for the AI Transportable portion of the edge computing industry will grow to approximately $5 billion in the coming years. OSS’ objective is to be a technology and market leader in this segment of the market.

Product Offerings

Our systems are built using the latest CPU, GPU, high speed switch fabrics and flash storage technologies that draw upon years of expertise in designing and manufacturing custom, semi-custom as well as standard systems for military and commercial customers. We have a history of being first-to-market with many solutions for emerging technologies. Our technological leadership includes linking different OSS product systems together.

We use leading edge, state-of-the art components from major technology providers to design purpose-built systems that solve customer problems in an efficient, cost-effective manner. We apply the component technology provided by Intel, AMD, NVIDIA, Micron, Broadcom, and others to deliver solutions to provide true value to our customers.

7

Four technologies are fundamental to the AI Transportable computing space: edge servers, GPU compute accelerators, flash memory-based storage, and high-speed switch fabric for data acquisition I/O. These technologies enable systems to ingest, process and store data at significantly higher rates than traditional systems. By harnessing these components, customers can process data much more quickly and in a more secure manner, and as a result, turn raw data into advantage in action.

Rugged Edge Servers

While simple AI applications, such as facial recognition to open a door to a secure area, may run on traditional low power embedded processor, the needs of the AI Transportable applications require datacenter-class server performance brought to a mobile platform. The sheer amount and speed of sensor processing, sensor fusion and AI/ML processing for operating an autonomous vehicle or a mobile weapon system requires multiple high-speed digitizers, high-performance networking, the fastest flash storage devices, and server-class processors. We enable the power of the datacenter to be deployed at the edge without compromising performance by employing groundbreaking ruggedization and cooling technologies for edge servers operating from various vehicle AC and DC power sources in small spaces.

GPU Compute Acceleration

When GPU technology and solid-state flash were first introduced, we began designing systems that maximized the effectiveness of these technologies. We now produce compute-systems with large numbers of GPUs and flash memory that communicate over PCIe and allow faster processing, data storage, and data retrieval. The more GPUs and flash devices available to a server, the faster that system can process and store data.

The capabilities and speed of GPU accelerated computers are driving significant advances in AI and machine learning. Massive amounts of data are collected, stored, and analyzed by today’s sophisticated algorithms. We are enabling the growth of such AI capability by adding scale with rugged systems that complement the highest performance rugged servers.

High Density Solid-State Flash Storage

The proliferation of larger and larger data sets used in edge computing, including AI, is feeding the need for higher capacity and higher performance storage devices. Traditionally, companies have used hard disk drives for their primary storage. Hard disk drive-based systems are being replaced by flash memory-based systems, which offer higher capacity, performance, reliability, and ruggedness. Flash-based storage systems also consume significantly less power. Our solutions offer the highest capacity and performance with the addition of removable media which enables the quick transportation and delivery of massive amounts of data.

Switch Fabrics For High Speed Data

At the front-end of AI Transportable systems is high speed data acquisition technology through switch fabrics. Depending on the application, data can be generated from a wide array of sensors and inputs. In many cases, such as autonomous driving or mobile weapon system platforms data is generated through arrays of video, Light Detection and Ranging (“LIDAR”), radar, Forward Looking Infrared (“FLIR”), Radio Frequency (“RF”), and other computationally intensive sensors. Our PCI express based switch fabrics provide the highest speed and lowest latency data acquisition and movement.

When PCIe was introduced in 2005, we were the first company to produce PCIe over cable adapters allowing system-to-system communication at the same speed as internal Input/Output (“I/O”) expansion significantly reducing latency. Today, we are one of the largest providers of PCIe adapters and expansion components used worldwide.

8

What Sets OSS Apart

Several factors differentiate OSS from other suppliers of high-performance edge computing solutions, including, without limitation the following:

Business Strategy

We have consistently followed a strategy of being first-to-market in leading edge deployment technologies by designing and developing products that are delivered before our competitors. We currently have products spanning the spectrum of high-performance computing, including servers, flash storage, GPU acceleration, networking, and PCIe data acquisition I/O expansion. Within these product areas, the approach implies that we:

Earnings Growth Strategy

We intend to implement different strategies to increase our revenue growth, while improving earnings. We believe that earnings growth can be accomplished by taking the following actions:

Revenue growth driven by existing OEM and new design wins:

9

Higher margins:

Optimize expenses:

Our Opportunity

The worldwide edge computing market is expected to grow at a compounded annual growth rate (“CAGR”) of 38% to $61 billion by 2028 (Grandview research, “Edge Computing Market Size,” May 2021). Within this market, we are positioned and focused on the AI/autonomous portion at the very edge, which we call AI Transportables, and we believe that this market could be as large as $5 billion within several years. The products we develop to address this market include high performance compute, storage servers, and PCIe acceleration systems that can perform in the most challenging environments. If an application needs AI and/or autonomous capabilities, and it moves, OSS strives to deliver the highest performance solutions that will survive and enable these challenging applications.

Our Technology

We design and manufacture ruggedized high performance edge computing systems, which are designed to increase compute performance while surviving in harsh environments. Our rugged servers bring the power of leading-edge datacenter-class technologies to the edge for applications in AI/ML, sensor fusion, autonomous navigation, data logging and video rendering. Our high-density compute accelerators connect directly to a server’s PCIe bus, delivering substantial compute performance. Our flash storage arrays support hundreds of terabytes of high-speed storage that can also be accessed by multiple servers.

Technology Drivers for OSS High-Performance Computing Business

We have developed expertise and core competencies in the three fundamental technology drivers within today’s high-performance edge computing market – high-speed serial interconnect technology, compute acceleration utilizing GPUs, and low latency flash storage. In combination, these three fundamental technologies, underpinned by PCI Express, are changing the economics of computing, bringing high-performance computing within the grasp of a wide

10

range of new industries and commercial applications on the edge. Simultaneously, the emergence of massive amounts of data being generated by advanced sensors in each of these industries is pushing the requirement for innovative state-of-the-art technology. We are enabling this technology to be deployed at the edge by merging these fundamental technologies with our expertise in providing system level optimization for meeting requirements for ruggedization and SWAP constraints. Our strategy is to be the disruptive leader in the platforms for rugged edge applications, based on our unique ability to design high-quality, high-performance AI workflow compute/storage engines that can be deployed in harsh dynamic environments, which require unique system level features for vibration, cooling, and power. Our target market, including various types of vehicles that move on land, in the air or at sea, creates extremely demanding requirements for compute systems, which must be compact, survive the elements and disruptions in power, as well as leverage the higher performance capabilities in the market. This is what we believe we do well.

We strive to not only provide competitive advantage for our customers, but also to address some of the most fundamental challenges in military and industrial applications. We believe that we are well situated to leverage these major industry forces. By exploiting our unique set of expertise in the underpinning technologies of high-performance computing, we strive to continue to deliver industry leading solutions, disruptive at times, and to take advantage of the opportunity to capture a growing market share in this rapidly expanding marketplace.

Switched Serial Interconnect

Switched serial interconnects are the data highways connecting many elements of today’s high-performance computing platforms. At ever increasing speeds, these pathways move data between a system’s processing units, storage, networking, and peripheral elements. For high-performance computing, the primary processing, storage, and peripheral interconnect is PCIe. PCIe Gen 5.0 has an ability to run up to 16 lanes in parallel, which allows up to 128 gigabytes (full duplex) per second bandwidth between system elements. We expanded the breadth of our products based on PCIe Gen 5.0 during 2023 to address ever increasing applications in the AI Transportable market.

Compute Acceleration with GPUs

GPUs have evolved from graphics display acceleration to becoming general-purpose processing workhorses for high-performance computing systems. Today, most of the fastest supercomputers in the world utilize GPUs as their primary compute engines. GPUs are ideal for high-performance computing workloads including AI training and inference because of their ability to complete massively parallel processing. While today traditional CPUs may have dozens of processing cores, GPUs have thousands of cores that are able to execute calculations simultaneously.

NVIDIA, a key supplier of GPUs to the market, lists more than 500 such applications across a broad set of market spaces, along with focused teams on specific industries of high growth potential such as their NVIDIA Drive team for autonomous navigation. Main markets serviced by NVIDIA GPUs include, without limitation:

11

While NVIDIA is focused on the deployment of their GPUs in hyperscale datacenters and for consumer gaming purposes, we are focused on taking the datacenter class capability to the AI Transportable market, expanding the overall market significantly. Many of these applications also scale performance, based on the number of GPU components utilized. We have designed multi-GPU systems, including up to 16 GPUs in a single system. Current state-of-the art GPUs (NVIDIA H100) provide over 48 teraflops (FP64) of performance, with future products expected to dramatically increase overall processing capabilities in the years to come.

GPUs also pose significant system design challenges due to their high-power requirements. High-end GPUs can require 500 – 700 watts of power or more, which generates a tremendous amount of heat. Sophisticated power distribution and cooling designs are required, especially for large-scale systems with multiple GPUs per chassis. OSS has significant expertise in addressing these challenges.

PCI Express Flash Storage – NVMe protocol

The use of flash memory technology for system storage has gained traction over the past decade, which we believe to be a result of the continuous decline in the cost per gigabyte. Flash memory has become the ubiquitous storage technology in high-performance systems.

Combined with the move away from traditional rotating hard drive technology, there has been the trend toward eliminating traditional storage protocols in favor of low latency flash memory protocols. Newer flash memory modules utilize a protocol known as NVMe, which connects the flash memory directly to the system’s PCIe interconnect. This direct connection allows for very high bandwidth between the storage and the other system elements, which eliminates the need for protocol translation as data moves from storage subsystems to and from the compute complex.

Today, flash memory modules with capacities up to 60 terabytes and PCIe Gen 5.0 interfaces are now available. PCIe Gen 6.0 devices are expected to be available for purchase in 2025. Our flash storage arrays with up to a thousand terabytes of capacity are available enabling the scaling of high-speed storage to meet the full range of high-performance edge application requirements.

OSS leverages the latest technology to build complete storage and data logging systems, including all the software to provide the highest density and performance in a compact form factor ideal for vehicles of all types. This, combined with our hot swappable canisters, has enabled many autonomous truck and military aircraft applications.

Our Core Technical Capabilities

We have developed unique expertise and core competency across the fundamental technologies of today’s rapidly expanding specialized high-performance edge computing marketplace. These valuable assets are embedded in the leading-edge engineering capabilities of our engineers, the proprietary intellectual property residing in our vast library of designs, and our brand equity based on our reputation as a high-quality producer of state-of-the-art, custom and standard solutions across a broad array of markets.

High Speed System Interconnect Design

Our electrical engineers are experts in high-speed digital signaling design. They have continually designed at the leading edge of the state-of-the-art signaling speeds, even as semiconductor technology has driven up the clock rate of digital transmission. We have consistently been among a small handful of companies able to come to market first with the latest technology. In fact, we delivered the industry’s first PCIe over cable solutions for PCIe Gen 1.0, Gen 2.0, Gen 3.0, Gen 4.0, and Gen 5.0. The expertise required includes circuit design, PCB (printed circuit board) layout and routing optimizations, all of which focus on achieving the highest levels of signal integrity. In our current systems,

12

PCIe Gen 5.0 signals are propagated across multiple PCBs, connectors, as well as both copper and fiber optic cabling, while maintaining the ability to recognize digital signal transitions at 32 billion times per second.

In high-performance computing systems, especially those systems that operate at the edge, the trajectory and need for ever-increasing signaling speeds is continuing; provided, however, the number of companies that have the capability to design robust, highly reliable systems at speeds that can tolerate the harsh conditions at the edge are continuing to decline. We believe our core competency in large-scale, high-speed design, and layout will allow us to remain on the forefront of this growing industry.

Complex System Design

In addition to low-level signal integrity design expertise, we have amassed expertise and intellectual property in high-performance system architecture design and software. This expertise allows us to develop extremely sophisticated systems with massive scaling, while also meeting customer demands for reliability, cost, and flexibility. To do so, we have developed deep knowledge for high-capacity input/output systems, operating system adjustments, and required configuration tuning. Due to this development, our engineers are often called upon to co-design with OEM designers to create the perfect solution to fit the needs of their customers.

For highly scalable systems, a deep understanding and experience with switching topologies, interconnect fabric design and low latency acceleration software is required. We have worked with serial switching technology, starting with the first generation of PCIe, and have been an innovator in creating unique and flexible topologies to meet the specific needs of customers. Creating custom solutions for unique customer solutions is a core competency at OSS, and we rely on this deep knowledge of switch capabilities and limitations.

For maximum system performance, unique software and design for optimizing data transfer, speeds are also important considerations. Our software expertise includes developing unique hardware drivers and configuration software that accelerate bandwidth and lower latency in PCIe GPU and NVMe system designs. We have developed expertise in system design to leverage peer-to-peer data flows between GPUs and pioneering techniques for optimized data flows between flash storage and GPU compute-engines. Our systems optimize switch and GPU configuration topologies to optimize GPU-to-GPU communication without requiring latency-inducing data transfer between host dual processors. Our platforms feature RDMA (remote direct memory access) across compute-nodes, which support data transfer without burdening the host CPU, as well as NVMe over Fabrics for efficient data transfer from remote storage to compute.

We have pioneered the ability to extend the PCIe bus beyond the confines of a single enclosure, opening the possibility of flexible system expansion options. We believe we are one of the leading designers and suppliers of PCIe host bus adapters that extend PCIe signals from the host motherboard across copper or optical cables to expansion enclosures, which provide application acceleration through scale. Our adapters provide both ends of the external cable connection. Our expertise in high-speed signal design in printed circuit boards, connectors, and cables is essential to successful expansion designs. We also hold expertise in incorporating clustering and rack scale expansion into our system designs, including 200/400 gigabit Ethernet, 200/400 gigabit InfiniBand, and emerging PCIe top-of-rack switch technology.

Expertise in power, cooling, and mechanical design are required to address the requirements of the high-performance computing customers, especially while meeting the constrained time requirements of rugged edge deployments. We have developed leadership design capability in high-power design and distribution within large rack enclosures as well as edge optimized configurations. High-end GPUs today require 500 watts or above, and in our high-end systems, up to 16 of GPUs can reside in a single chassis. Thousands of kilowatts of redundant power are required. Power stability and huge thermal loads are some of the critical design issues that must be addressed. Additionally, at the edge for AI applications, a wide range of input power sources need to be supported from standard 110-220 VAC and 48-270 VDC for terrestrial vehicles as well as three phase 400-800Hz AC for airborne applications.

We have expertise in power distribution, redundant power, and complex chassis cooling design, including materials selection, airflow simulation, fan technology, and various liquid cooling options including direct to chip conductive cooling and single and dual phase immersion cooling. We have also developed extensive expertise to help ensure regulatory compliance of our complex high-performance computing system designs that span across emission, shock, vibration, thermal, humidity, and other environmental requirements that are required for highly reliable and highly available solutions. Our engineers are experts in design for regulatory testing for FCC (Federal Communications Commission), CE (European Conformity), UL (Underwriters Laboratories), and Mil-STD (Military Standard)

13

standards. Additionally, we have expertise in rapid prototyping, design for manufacturability, and design for serviceability.

We also have expertise in system management software that enhances our competitive advantages and provides robust monitoring and management of the functions of complex computer systems. While the baseboard management controllers ("BMCs") of standard servers and workstations provide passable system management for an office or datacenter with a benign environment, the unique missions of our rugged edge systems require a more diverse level of monitoring, management. and control.

First, products like our 4UPro and EB line of PCIe expansion systems are not servers or workstations, but instead, they provide scale-out expansion of high-performance GPUs, FPGAs, NVMe drives and edge I/O devices to a server. To provide the widest compatibility and largest serviceable market for our expansion systems, our U-BMC, or “Unified Baseboard Management Controller,” allows our expansion systems to seamlessly integrate with existing customer servers or our own SDS and EOS server products, allowing a server and one or more of our expansion products to be managed, monitored and controlled, as if it were a single integrated system with a massive amount of PCIe resources interconnected by our highest bandwidth, lowest latency PCIe switched fabric.

Second, unlike the standard datacenter server, our servers are designed to operate in both government and commercial harsh edge environments where “dirty” power from generators, engines and batteries with large spikes are common. Mix in the environmental conditions in which our servers may operate autonomously, such as temperature variances in places from Death Valley to 50,000 feet altitude, with moisture ranging from salt fog to rain and extreme vibration and shock from washboard dirt roadways to a hard-landing propeller aircraft, and one can see that a higher level of management, monitoring and control than a server snug in a power and cooling conditioned datacenter is required. The U-BMC adds unique value to server-level systems in these environments, especially in autonomous operations where there are no service technicians for miles, by allowing the system to adapt to changing conditions automatically or by remote control without failing. The U-BMC has features to handle these environments, such as controlling sensors connected to the server, turning on heaters in extreme cold, changing the PCIe fabric to reroute data around failed components and connecting to the Controller Area Network ("CAN") bus in cars and autonomous trucks to monitor the vehicle conditions to be able to take action on information provided by the vehicle, such as ignition on/off. Many more U-BMC edge features unique to OSS and valuable to our customers were in development in 2023 and will continue to be added in 2024, such as throttling NVIDIA GPUs in real time based on power or temperature fluctuations to keep systems running in a reduced state rather than shutting down.

Third, due to operating in diverse industry standard and regulatory markets required by military standards, commercial aerospace FAA or EASA, and highway NHTSA or ETSC agencies, the U-BMC is designed to adapt to the unique requirements imposed by servers residing on, or controlling, vehicles. A standard datacenter server BMC needs to conform to the basic agency requirements of electrical interference and personal safety regulated by agencies such as the FCC or CE and administered by testing companies such as UL and TüV. The U-BMC is designed to cover all edge requirements of the datacenter as well as adding standards organization compliance, such as those required by military customers including SOSA compliant functions for sensor management, system management, and task management not found in datacenter server BMCs.

In 2022, we introduced the U-BMC, which is included in our Rigel edge supercomputer and PCIe Gen 5 4UPro products. In 2023, we expanded the platforms that include the U-BMC to the PCIe Gen5 SDS rugged server for commercial and military edge applications with more platforms to come. With U-BMC, we provide “single pane of glass” management of complex systems, even if the server is in a separate enclosure, and an open-source Redfish API for easy integration with industry-standard management tools. We expect to continue to expand and enhance our licensable software to create additional value, barriers of entry and stickiness with our program wins.

Storage Management Software

Given our hardware design and integration expertise, we believe that our robust software capability allows us to offer more optimized and customized systems. Our Ion Accelerator™ software design team provides the expertise to deliver full server and storage solutions that produce the highest performance from today’s leading-edge flash storage devices. The Ion Accelerator software allows flash-based modules to be put into a variety of storage and network configurations which can then be accessed by multiple edge servers. The Ion Accelerator software can do this cost-effectively, while preserving the low latency and security that is vital for many mission-critical applications, from secure network boot, database, and transaction processing to massive data collection programs.

14

Benefits of Technology and Core Capabilities to our Customers

Due to our core capabilities, we can provide our high-performance computing customers with platforms that are highly reliable and cost effective. Such performance allows our customers to solve larger problems faster, and save the cost and time of highly paid engineers, data scientists, and other human resources. Our technology enhances innovation by allowing more “what-if” analysis in a finite amount of time. Our price/performance leadership enhances our customers’ competitiveness and lowers capital expense and total cost of ownership. We work with our OEM customers to develop custom “perfect fit solutions” for their unique requirements when the anticipated return justifies the investment.

Our Products

Compute Servers

Within the server sector, we have secured a niche position of building purpose-built specialty servers, which the major server suppliers do not supply, as they require custom tuning and special features that major OEMs cannot easily provide. Our compute servers are designed to provide the highest level of performance that can be deployed in harsh edge environments. Our expansion optimized (“EOS”) line of servers is optimized for supporting a high number of add-in cards such as GPUs, FPGAs, NVMe drives and sensor inputs. Servers in this product family have a number of slots that are compatible with the PCIe host bus interface cards that we have developed. These cards enable PCIe connection over cable between the host processor and downstream I/O devices. These servers have custom basic input/output systems (“BIOS”) to ensure they work seamlessly with expansion chassis and support a high number of downstream I/O devices. Our short-depth server (“SDS”) line supports rugged deployment in space constrained environments providing a maximum depth of 20 inches. We believe that our “Rigel Edge Super Computer” (“Rigel”) is the highest performing, most dense, AI-compute platform that is deployable in extreme environments, including on military aircraft.

GPU computing uses hardware components that are optimized to perform mathematical calculations in a rapid fashion. NVIDIA is the market leader in the design and manufacturing of these components. We work closely with NVIDIA to design and build systems which use multiple GPUs to accelerate applications.

Emerging markets and applications such as AI, image rendering and processing, autonomous vehicles, deep learning, molecular modeling, genomics, advanced visualization, machine learning, and image processing, all benefit from the ability to use GPUs to accelerate the application. We build specialized compute-servers and accelerators used in these emerging growth markets. We estimate these markets to be very large and growing.

Storage Servers

We also build standard and custom flash storage arrays utilizing our unique know-how in PCIe device fan-out, packaging, cooling, and PCIe-over-cable. We deliver dense, high-performance systems that provide customers with high value and utility in the most demanding, data-intensive operations. These OSS storage servers complement our compute servers to provide an end-to-end edge solution for AI workflows.

Through a strategic agreement with Western Digital, we acquired an exclusive software license for Ion Accelerator™ Storage Area Networking (“SAN”) source code and software development rights, as well as hired their core engineering team in July 2017. Since acquiring this software asset, we have extended its capability to align with our AI Transportable strategy by adding Network Attached Storage (“NAS”), support for NVMe flash drives, NVMe over Fabric expansion capability, and several encryption methods required for government security applications. We have also implemented a proprietary Follow Me™ capability for removing a bulk pack of NVMe drives that can be easily transported to another system without rebuilding the data, operating much like a massive capacity USB stick. This provides our flash arrays with a high level of differentiation relating to storage management, latency, portability, and throughput. We provide standard flash array products and have the in-house hardware and software expertise to provide customized systems for demanding applications that are not suitable for standard offerings. For example, we provide products to a large military contractor for integration into military aircraft that requires us to design and manufacture a highly ruggedized mil-spec flash array. The resulting product provides high data density with low weight, a high degree of portability, and security for data protection. We believe our experience and capability in high speed, low-latency, digital signaling via PCIe gives us an edge in providing custom designs to OEMs, military programs, and other special purpose applications.

15

We believe that because our products are positively differentiated by speed, density, and management features for challenging edge applications, our offerings compete favorably in this market and provide a substantial growth opportunity.

PCIe Expansion and Adaptors

PCIe is the high-speed standard for communications within a computer. This standard defines the signals and connectors (i.e., slots) that are used for computer add-in cards (such as Ethernet or graphics). Traditionally, communication between computers in the network is completed via Ethernet. Although Ethernet is great for large networks, this introduces delays and latency challenges. To keep performance at the highest level, PCIe signaling can also be routed over a cable, allowing expansion input/output slots to be physically located in a separate chassis. This provides for high-performance and low latency, which are essential in this market.

Being able to separate the server from the I/O expansion, by using PCIe over a cable, facilitates disaggregation of server functionality. That is, with PCIe, server I/O functions no longer need to be contained in the physical server chassis, but instead, can be separated into a separate chassis and continue to operate at full speed. This offers many advantages over higher latency and power consuming traditional networking communications like Ethernet. From a practical perspective, servers can be connected directly to larger storage arrays or other peripheral devices, with the resulting group of chassis operating as if they were all in the same physical chassis.

We began developing our first PCIe-over-cable adaptor in 2006 and were one of the early providers of PCIe adaptors. We recognized this space as a prime opportunity to utilize our core strengths, such as:

This technology has now become a standard within the computer industry, our customers have used our adaptors to connect their custom input/output chassis and achieve performance equivalence as if the I/O was integrated into the server box. This gives designers and integrators a degree of flexibility and utility in architecting computer systems that is unprecedented. We have expanded our PCIe adaptor market in breadth and depth, including making adaptors for many OEM customers.

With our expertise developed in designing adaptor cards, the logical extension of our capability led us to develop a method for expanding the PCIe bus into an external chassis containing one or many expansion slots and using this expansion to provide storage and AI application acceleration. This allows a customer to install multiple standard PCIe boards into a chassis and accelerate their system without having to add additional servers. These are typically GPUs, FPGAs or NVMe drives to create large-scale Compute and Storage appliances. For example, we have developed a product for deployment in a mobile command center, which aggregates large amounts of high frequency data from sensors and allows in the field AI algorithms to operate in real time. This is achieved through a cluster of our compute and storage products. A user can now connect a multiplicity of PCIe devices to a single server using a single memory domain, and achieve performance throughput and low latency, which was not possible prior to the introduction of PCIe.

We have been a leader in PCIe acceleration through generations 1.0, 2.0, 3.0, 4.0 and 5.0. We delivered our initial PCIe Gen 5.0 products in 2022, well ahead of any of our direct competitors, and started shipping a full line of Gen 5.0 products throughout 2023. As PCIe evolves through generations 6.0 and beyond, we believe that we are uniquely positioned to continue our leadership role in this market. We currently offer what we believe to be the largest

16

PCIe acceleration product line, with chassis and backplanes that offer expansion from one to 64 slots. Due to its greater data throughput, lower latency and flexibility of design, we believe this is a growing market, and we intend to maintain our leadership role.

Additional Compute Products

Through Bressner, we provide small form factor IoT and high-performance industrial and panel PCs compute-platforms customizable to meet needs in commercial applications on the edge where space constraint is a fundamental consideration. We also provide ruggedized, mobile tablets and handhelds that meet the specialized requirement for devices deployed at the edge in a diverse set of environmental conditions for commercial and government applications.

Customers

We deliver the highest performance scalable products and solutions at the source of the data that enable AI/ML, sensor fusion, and sensor processing for global defense and commercial markets. We serve a global clientele consisting of multinational companies, governmental agencies, military contractors, military services, and leading technology providers. Some of our key customers are set forth below, illustrating the class of customers we pursue with our sales, product marketing and marketing communications efforts.

Raytheon – We work closely with many of the U.S. Government agencies and prime contractors to bring the latest technologies to mobile edge applications. Raytheon provides an excellent example of how we adapted high-performance computing elements used in air-conditioned datacenters to the rigorous environment encountered in a U.S. Navy aircraft. We worked closely with Raytheon to build a customized NVMe storage array, with drives installed in removable canisters for high-speed sensor data acquisition, encryption, and recording. This massive amount of mission data can then be easily off-loaded upon landing the aircraft and sent to the traditional government datacenter, which is a significant development given that satellite network links are too slow to handle transmitting that amount of data. To further enhance the data collected, we embarked on a second project with Raytheon to build a GPU accelerated “datacenter in the sky” system to enable mission data collected in the flash array to be analyzed and run through AI algorithms in real time while the mission was in process. This allowed the aircraft and crew to make real time decisions using the same level of processing power available in a ground-based system. Finally, we enhanced that “datacenter in the sky” with a 3-system cluster to provide large scale resources during missions and to carry out multiple AI tasks in real time. These applications are great examples of rugged edge products. We have continued to enhance and refresh the technology for this program while working on opportunities with other prime contractors, including other mobile applications such as video surveillance, video analytics and autonomous vehicles on land, in the sea and in the air. OSS is currently expanding its footprint within in the military market with multiple new engagements with other prime contractors and the DOD directly. Much of this activity addresses the needs of AI, sensor fusion, and autonomy required in the battlefield. Current applications include land vehicles, aircraft, drones, ships, and submersibles.

LIQID– LIQID is a market leader in composable infrastructure hardware and software solutions. Leveraging industry standard datacenter components to deliver a flexible, scalable architecture built from disaggregated resources. We provide optimized high performance computer solutions, expansion chassis and PCI Express interface cards that are used to address next-generation application in AI, IOT deployment, DevOps, cloud and edge computing, NVMe and GPU over fabric support.

Teledyne LeCroy - Teledyne LeCroy is a leading provider of test, validation and benchmarking test platforms to the storage and CXL memory device industry. We provide several PCI Express-based interface cards, PCI Express switches, NVME controllers, and host buss adaptors that are used in Teledyne’s test bed applications and end devices. We act as an extension to Teledyne’s engineering group, allowing Teledyne to complete their product roadmap in a timely and cost-effective manner.

Alcon – Alcon is a market leader in the production of computer assisted medical equipment. Bressner provides several rugged, purpose-built, high-performance workstations used in performing these AI assisted surgeries. Bressner works directly with Alcon engineers to co-design and assist in securing medical certifications for the products that doctors and patient trust for pinpoint accuracy and speed.

Torc Robotics –Torc Robotics, is a market leader in US truck manufacturing and is a subsidiary of Daimler, which manufactures globally. Daimler Technologies North America embraced a clear roadmap to level 4 autonomous trucking with planned deployments by the end of the decade. We provide the current Torc Robotics truck fleet with several OSS products, including multiple 3U SDS models for the autonomous driving functionality and our Centauri

17

data logging system that provides high-speed sensor recording and fast data transport using our removable NVMe drive canister technology.

Sales and Marketing

Our sales and marketing efforts are focused on the identification, engagement, and closure of significant targeted opportunities within the AI Transportables market.

Sales (OSS)

Our OSS sales efforts consist of five main channels:

18

Sales (Bressner)

Our Bressner sales efforts consist of four main sales channels:

OEM Industrial PC products:

Our OEM industry-focused sales team plays a vital role in driving growth and market penetration. Comprised of passionate technical experts, they actively cultivate and develop strategic partnerships with major commercial players across diverse sectors, including industrial automation, automotive, medical, artificial intelligence, security and defense, and aerospace.

This dynamic team fosters close relationships with OEM-customers, engaging directly at their facilities, industry events, and tradeshows. By deeply understanding their unique needs and challenges, our team tailors existing solutions or custom offerings, ensuring a compelling return on investment (“ROI”) and empowering their success within their respective environments.

This customer-centric approach, combined with our focus on technical expertise and strategic partnerships, has been instrumental in propelling our market expansion and securing significant customer wins.

Looking ahead, we remain dedicated to strengthening existing partnerships and forging new ones across diverse industries. We believe that our continuous investment in recruiting and developing highly skilled technical experts, coupled with our focus on delivering tangible ROI, positions us for further success in establishing ourselves as a leading provider of customized solutions for the industrial IT landscape.

Modular IPC system integration:

Our expertise in modular system integration, driven by strategic partnerships and a diverse portfolio, unlocks sales growth in emerging markets like AI, automation, medical, automotive, smart cities, imaging and more. We achieve this by:

Driving ROI, Shaping the Future:

We invest in continuous portfolio expansion, strategic partnerships, and top talent recruitment to uphold technical expertise and anticipate market demands. We believe that this unwavering focus on ROI positions us for continued leadership in modular system integration, empowering diverse industries to realize operational excellence and drive sustainable sales growth in emerging markets.

VAD Distribution Sales – Empowering Innovation, Bridging Continents:

We surpass distribution as a leading value-added distributor (“VAD”) across Europe, propelling cutting-edge technology in networking, industrial IoT, and industrial flash memory. Strategic partnerships with top-tier suppliers fuel our pipeline, while our in-house expertise delivers solutions tailored to individual needs.

EMEA Sales – Local, Agile, Customer-Centric: The Heartbeat of Our EMEA Success

Our relentless pursuit of operational excellence for EMEA customers fuels our regional ascent. This translates into three unwavering commitments:

19

Investing in the Future of EMEA Success:

We remain committed to:

Marketing Communications

Our marketing communications department is responsible for positioning OSS as an expert, thought leader, and visionary in the AI Transportables market. We generate expert content to support our market leading products, while also building cost effective brand/product awareness in several ways. We use traditional and non-traditional marketing communications, as well as partnerships and word of mouth, to convey the uniqueness and compelling value of our products and services. The AI Transportable market applications we target include AI inference applications in autonomous vehicles, medical equipment, commercial aerospace, defense/government, agriculture, and mining. Bressner also targets embedded industrial and IoT customers in the EMEA region. Among the many channels utilized are:

20

As we grow, it is anticipated our marketing efforts will likewise continue to increase in size and focus on the AI Transportable market.

Competition

Our core business is to provide specialized high-performance edge AI computing platforms to OEMs who incorporate these products into their complete solutions, which they then sell to end users in the datacenter class, rugged AI compute and storage markets. By contrast, competitors in the AI hardware market space typically provide solutions designed to meet either high performance non-rugged or low performance highly rugged applications. Although a fragmented market, there are a number of categories of potential competitors of our products.

Customer in-house design resources

Many of our larger target OEM customers have in-house engineering design resources, which could be used as an alternative to engaging with us. Examples of current OSS customers who have significant in-house resources include National Instruments, Raytheon, and Lockheed Martin. This potential competition is mitigated by the technical specialization that we have, especially in high-end and large-scale PCI Express switch fabrics and PCI Express acceleration capabilities where the option to “buy” provides a better return to “make” in an internal make/buy decision. OEMs can invest their in-house resources on value-add capabilities within their specific vertical market and outsource these horizontal technology capabilities to us. We have also developed a trusted partner relationship with many of these OEMs and have established a market reputation for technical expertise and a responsive and cost-effective engagement model. We win when our customers realize that together we can produce better products faster, and more cost-effectively than they can by themselves. This has proven to be particularly evident when customers require state-of-the-art products that are constructed of commercially available parts but need to be deployed in harsh mobile environments. This has resulted in several program wins that demonstrate our flexibility and how we can work closely with large OEM and government customers. Interestingly, it appears that when these large companies cut back on their workforce or have limited funding, such events tend to bolster our position, as we may become these companies’ only option to get their desired product or service deployed within a reasonable period.

Major Tier 1 & 2 Mainstream Computer, GPU and Storage Vendors

These vendors offer mainstream high-performance computing platforms, including servers and storage systems that can address some applications at the edge in our target markets. Typically, they do not, however, offer the enhanced value platforms or customization capabilities that we specialize in to meet unique form factor, power, ruggedization or scale out requirements sought by OEM customers. Generally, these vendors focus on the large, air-conditioned datacenters and compete with such vendors based on price/volume, as differentiation is challenging. Our strategy is specifically designed to avoid head-to-head competition in this part of the market with this class of vendors. In some scenarios, we can provide a complementary specialized component or building block, which interfaces with one of these vendors’ mainstream products. Examples of companies in this space include NVIDIA, HP, Dell/EMC, IBM, SuperMicro, Pure Storage, and NetApp.

Vertical High Performance Compute Vendors – Military/Aerospace

In certain vertical markets, there are competitors who focus primarily on the HPC military and aerospace markets. These vendors often provide complete solutions, including both hardware and software, and some specialization in terms of form factor and ruggedization. In these markets, we provide unique capability in terms of scaling of PCI Express components over cable (copper and fiber) that can address unique requirements of specific military or government programs. Many of these competitors use older technologies or low power processors and components in these more challenging environments. We are able to differentiate ourselves from such competitors due to the fact that we deploy the latest high-performance technology, which enables us to provide superior products to potential customers in this space. We have also established good relationships with prime contractors and governmental agencies (Raytheon, Sierra Nevada, Lockheed, Boeing, NASA, ONR, L3 and others), which can be important influencers or decision makers on technology selection. Competitors in this space include companies such as Mercury, Crystal, Curtiss Wright, Kontron, Trenton, Core Systems and Systel. In the past, we have been able to offer the latest

21

and differentiated technology to the rugged edge, which is normally only deployed in commercial applications, well before our competitors.

Manufacturing and Operations

Currently, OSS is certified under AS9100, and Bressner is certified under ISO 9001-2015 for “design, manufacture, and supply of industrial computers.” This means we have demonstrated our ability to consistently provide products that meet both customer requirements and applicable government regulations or statutory requirements. AS9100 is the pinnacle of quality management systems recognized by government and aerospace companies world-wide. It also indicates that we have programs and processes in place to ensure a high level of customer satisfaction, as well as continuous improvement and risk mitigation programs that ensure we get better over time.

While OSS primarily utilizes lean principles to drive our manufacturing and assembly process, we recognize the importance of smooth builds and strategic inventory in this current climate of sustained supply chain shortages. One of the key aspects of utilizing lean principles is our application of just-in-time principles to ensure effective ordering and utilization of inventory. This also helps optimize cash flow throughout the manufacturing cycle. Within the manufacturing process, our operations encompass three categories of “builds”:

We are dedicated to quality and customer satisfaction. Our continuous improvement efforts require us to review products, services, and processes with the idea that minor changes can lead to greater outcomes for our customers. Although we serve the high-end of the rugged edge computing space, we are constantly leveraging lean principles to become more efficient and drive down costs while driving up margins and quality.

Research and Development

Our ability to compete successfully in our industry is heavily dependent upon our ability to ensure a continuous and timely flow of competitive products, services, and technologies to the marketplace. We continue to develop new products and technologies and to enhance existing products that will further drive commercialization. We may also expand the range of our product offerings and intellectual property through licensing and/or acquisitions of third-party businesses and technologies.

Our intellectual property research and development is focused on the exploitation of key technologies as they evolve in the marketplace. Our product roadmap reflects new technologies for CPUs, GPUs, flash storage, and advanced PCIe switches. We design first-to-market, unique implementations targeted at the AI Transportable market utilizing market leading component technologies. Accordingly, our focus lies not in the capital-intensive development of silicon implementations of technologies (i.e., chips, processors, GPUs, or storage devices), but rather leverages leading-edge technologies and building first-to-market products that fully exploit those technologies to solve customer problems in challenging environments.

Our research and development strategy can be summarized as follows: We drive customer program wins by utilizing new key technologies to develop products that are leading edge and first-to-market and that are designed to solve challenging problems in harsh environments, while working closely with our customers to understand and address their needs.

Intellectual Property

Our primary intellectual property value emanates from the more than 600 individual design projects that we have undertaken over the decades since our founding, experience, and know how, in addition to trade secrets and copyrights.

22