UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For the fiscal year ended:

OR

For the transition period from: to

Commission File Number

(Exact name of registrant as specified in its charter)

| | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

|

|

| | |

| (Address of principal executive offices) | (Zip Code) |

| Registrant’s telephone number, including area code: ( |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

| Trading symbol |

| Name of each exchange on which registered |

| None |

| |

|

|

Securities registered pursuant to Section 12(g) of the Act:

(Title of class)

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | |||||

|

| Yes | ☐ | | ☒ |

|

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. | |||||

|

| Yes | ☐ | | ☒ |

|

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | |||||

|

| | ☒ | No | ☐ |

|

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit such files). | |||||

|

| | ☒ | No | ☐ |

|

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| | Smaller reporting company | |

|

| Emerging growth company |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐ | |||||

|

| |||||

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. | |||||

|

| |||||

| If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. | |||||

|

| |||||

| Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐ | |||||

|

| |||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | |||||

|

| Yes | ☐ | No | |

|

| The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $ |

|

|

| As of April 12, 2024, the issuer had |

|

|

| Documents incorporated by reference: None |

Table of Contents

|

|

|

Page |

|

PART I |

||

|

|

|

|

|

Item 1. |

6 |

|

|

Item 1A. |

12 |

|

| Item 1B. | Unresolved Staff Comments | 20 |

|

Item 1C. |

21 |

|

|

Item 2. |

22 |

|

|

Item 3. |

22 |

|

|

Item 4. |

22 |

|

|

|

|

|

|

PART II |

||

|

|

|

|

|

Item 5. |

23 |

|

|

Item 6. |

24 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operation |

24 |

|

Item 7A. |

34 |

|

|

Item 8. |

35 |

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

49 |

|

Item 9A. |

49 |

|

|

Item 9B. |

50 |

|

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

50 |

|

|

|

|

|

PART III |

||

|

|

|

|

|

Item 10. |

51 |

|

|

Item 11. |

54 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

57 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

59 |

|

Item 14. |

59 |

|

|

PART IV |

||

|

|

|

|

|

Item 15. |

60 |

|

|

Item 16. |

61 |

|

|

|

62 |

|

PACIFIC HEALTH CARE ORGANIZATION, INC.

Throughout this annual report on Form 10-K (this “annual report”), unless the context indicates otherwise, the terms, “we,” “us,” “our” or the “Company” refer to Pacific Health Care Organization, Inc., (“PHCO”) and our wholly owned subsidiaries Medex Healthcare, Inc. (“Medex”), Medex Managed Care, Inc. (“MMC”) and Medex Medical Management, Inc. (“MMM”), and, where applicable, our former subsidiaries Industrial Resolutions Coalition, Inc. (“IRC”), Medex Legal Support, Inc. (“MLS”) and Pacific Medical Holding Company, Inc. (“PMHC”). References to “fiscal 2023” and “fiscal 2022” mean the periods ended December 31, 2023, and 2022, respectively.

CAUTIONARY STATEMENT REGARDING

FORWARD-LOOKING STATEMENTS

All statements other than statements of historical fact included in this annual report and in the documents incorporated by reference herein, if any, including without limitation, statements regarding our future financial position or results of operations, business strategy, potential acquisitions, budgets, projected costs, and plans and objectives of management for future operations, are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. In some cases, forward-looking statements can be identified by terminology such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “foresee,” “future,” “intend,” “likely,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “should,” “strategy,” “will,” “would,” and other similar expressions and their negatives.

Forward-looking statements are not guarantees of future performance and involve known and unknown risks and uncertainties, many of which may be beyond our control. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof, and actual results could differ materially as a result of various factors. The following include some but not all of the factors that could cause actual results or events to differ materially from anticipated results or events:

|

|

● |

cost reduction efforts by our existing and prospective customers; |

|

|

● |

our ability to retain existing customers and to attract new customers; |

|

|

● |

competition within our industry, including competition from much larger competitors; |

|

|

● |

reductions in worker’s compensation claims or the demand for our services, from whatever source; |

|

|

● |

delays, reductions, or cancellations of contracts we have previously entered; |

|

|

● |

the loss, ineffective management, malfunction (including those resulting from cybersecurity incidences and breaches), or increased costs of third-party-provided technologies and services on which our operations rely; |

| ● | failure to retain or recruit, or changes in, officers and key employees, and uncertainties in our ability to maintain key consultants and advisors; | |

|

|

● |

the loss of or inability to obtain adequate insurance coverage; |

|

|

● |

cybersecurity incidences and breaches, and other software system failures, and the imposition of laws imposing costly cybersecurity and data protection compliance; |

|

|

● |

business combinations involving our customers or competitors; |

|

|

● |

legislative and regulatory requirements or changes which could render our services less competitive or obsolete; |

|

|

● |

economic and labor market conditions generally and in the industries in which we and our customers participate, including the effects resulting from economic recessions, financial sector turmoil, international conflicts, and rising domestic inflation and related economic policy responses; |

|

|

● |

our failure to successfully develop new services and/or products either organically or through acquisition, or to anticipate current or prospective customers’ needs; and |

|

|

● |

the impacts on our business of COVID-19, including the reduction of our customers’ workforces as a result of a variety of COVID-19-related causes, as well as government mandates and impacts on the workers’ compensation industry, the businesses of our customers and on the economy generally. |

For more detailed information about particular risk factors related to the Company, see Item 1A Risk Factors below.

New risk factors emerge from time to time, and it is not possible for management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

Undue reliance should not be placed on forward-looking statements. Forward-looking statements are based on the beliefs of management as well as assumptions made by and information currently available to management and apply only as of the date of this annual report or the respective dates of the documents from which it incorporates by reference. Neither we nor any other person assumes any responsibility for the accuracy or completeness of forward-looking statements. Further, except to the extent required by law, we undertake no obligations to update or revise any forward-looking statements, whether as a result of new information, future events, or a change in events, conditions, circumstances or assumptions underlying such statements, or otherwise. We may also make additional forward-looking statements from time to time. Any subsequent forward-looking statements, whether written or oral, made by us or on our behalf, are also expressly qualified by these cautionary statements.

The following discussion should be read in conjunction with our audited consolidated financial statements and the related notes contained elsewhere in this annual report and in our other filings with the Securities and Exchange Commission (the “Commission”).

PART I

| ITEM 1. | BUSINESS |

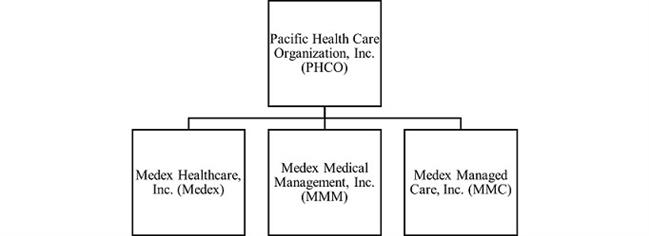

We are workers’ compensation cost containment specialists providing a range of services principally to California employers and claims administrators. The Company was incorporated under the laws of the state of Utah in April 1970, under the name Clear Air, Inc. The Company changed its name to Pacific Health Care Organization, Inc., in January 2001. In February 2001, the Company acquired Medex in a share for share exchange. Medex is a wholly owned subsidiary of the Company. Medex is in the business of managing and administering both Health Care Organizations (“HCOs”) and Medical Provider Networks (“MPNs”) in the state of California. Medex also offers Workers’ Compensation carve-out services, Medicare set-asides and expert witness testimony. In February 2012, we incorporated MMM in the state of Nevada, as a wholly owned subsidiary of the Company. MMM is responsible for overseeing and managing medical case management services. In March 2011, we incorporated MMC in the state of Nevada, as a wholly owned subsidiary of the Company. MMC oversees and manages the Company’s utilization review, medical bill review, and lien representation services. We discontinued lien representation services in the third quarter of 2023 due to the lack of demand. Following is our corporate structure as of December 31, 2023.

Business of the Company

We offer an integrated and layered array of complementary business solutions that enable our customers to better manage their employees’ worker compensation-related healthcare administration costs. We are constantly looking for ways to expand the suite of services we can provide our customers, either through strategic acquisitions or organic development.

Our business objective is to deliver value to our customers by reducing their workers’ compensation-related medical claims expense in a manner that will assure that injured employees receive high quality healthcare that allows them to recover from injury and return to gainful employment without undue delay. According to studies conducted by auditing bodies on behalf of the California Division of Workers’ Compensation, (“DWC”) the two most significant cost drivers for workers’ compensation are claims frequency and longer than average treatment duration. Our services focus on ensuring timely medical treatment to reduce the claim duration and medical treatment costs.

Our services include providing customers access to our HCOs and MPNs. We also provide medical bill review, medical case management, employee advocate services, utilization review, workers’ compensation carve-outs and Medicare set-aside services. Complementary to these services, we also provide expert witness testimony. We offer our services as a bundled solution, as standalone services, or as add-on services.

Our core services focus on reducing medical treatment costs by enabling our customers to have control and oversight of the medical treatment of their injured employees to ensure treatment is timely and appropriate. This control is primarily obtained by participation in our HCOs or one of our MPNs. Through Medex, we hold two of the total of four licenses issued by the state of California to establish and manage HCOs within the state of California. We hold several government-issued licenses to operate medical provider networks. We also hold approvals issued by the state of California to function as an MPN and currently administer 21 MPNs. Our HCO and MPN programs provide our customers with provider networks within which the customer has some ability to direct the administration of the claim. This is designed to decrease the incidence of fraudulent claims and disability awards, and ensure injured employees receive necessary vocational rehabilitation and training. Our medical bill and utilization review services provide oversight of medical billing and treatment requests, and our medical case management and employee advocate services keep workers’ compensation claims progressing to a resolution and assure treatment plans are aligned from a medical perspective.

Our customers include self-administered employers, insurers, third party administrators, municipalities, and others. Our principal customers are companies with operations located in the state of California where the cost of workers’ compensation insurance is a critical problem for employers, though we process medical bill reviews, utilization reviews and provide medical case management in several other states. Our provider networks, which are located only in California, are comprised of providers experienced in treating occupational injuries.

Our business has a long sales cycle, typically eight months or more. Once we have established a customer relationship and enrolled the employees of our employer customers, we anticipate our revenue to adjust with the growth or retraction of our customers’ employee headcount. Throughout the year, we also expect to add new customers while others terminate for a variety of reasons. The reasons for termination vary but include when a customer switches to an insurance carrier or third-party administrator that uses a different workers’ compensation administration vendor; and when our contract ends with state and local governments and they are required to engage in a public bidding process for their workers’ compensation administration vendor.

Health Care Organizations

An HCO is a network of health care providers specializing in the treatment of workplace injuries and in back-to-work rehabilitation for our customers’ injured employees. HCOs provide injured employees with a network of health care providers in the event of a workers’ compensation injury, while providing their employer (our customer) control over medical treatment and costs. In most cases, our HCOs give the employer up to 180 days of medical control in an HCO within which the employer can direct the administration of the claim. The injured employee may change providers once during this period but may not go to an out-of-network provider. The increased length of time during which the employer has control over administration of the claim is designed to decrease the incidence of fraudulent claims and disability awards. The right for the employer to control treatment within a network is based upon the notion that if the employer can direct care, it will facilitate timely and appropriate medical care and reduce the total cost of the claim.

Our two HCO licenses (respectively referred to as “Medex HCO” and “Medex 2 HCO”) allow us to provide comprehensive medical provider networks throughout California. Our HCO networks are composed of medical providers experienced in treating worker injuries. We have contracted with approximately 5,500 and 6,700 individual medical providers and clinics for Medex HCO and Medex 2 HCO, respectively, as well as hospitals, and rehabilitation centers. Our customers select one of the Medex HCO networks in which to enroll their employees based on the medical groups in the network. During initial enrollment and during the period of re-enrollment, our customers’ employees have the option to opt out of the HCO by predesignating their primary care physician to manage a workplace injury. If the employee opted out and is later injured on the job, their primary care physician would be authorized to oversee their medical care. Otherwise, the employer would be able to select the provider to oversee their medical care.

We continually review and update our networks with provider additions and removals based on feedback from internal operations, our customers, and their claims administrators. All our network providers’ credentials are reviewed and vetted by Medex.

Our HCO networks are required to be recertified every three years. The Medex HCO has been recertified through March 15, 2025, and the Medex 2 HCO through October 9, 2024. HCO guidelines impose certain medical oversight, reporting, information delivery and usage fees on HCOs. These requirements increase the administrative costs and obligations on HCOs compared to MPNs.

Medical Provider Networks

Like an HCO, an MPN is a network of health care providers, but health care providers participating in MPNs are not required to have the same level of medical expertise in treating workplace injuries. Under an MPN program the employer dictates which provider the injured employee will see for the initial visit. After the initial visit, the employee has the discretion to choose which provider in the network will continue treatment of the claim. However, the employee’s choice of provider is limited to those within the MPN for the life of the claim and the employee cannot opt-out of the MPN, which is a benefit to our customers. While the injured employee is limited to treatment by providers within the MPN, the California MPN laws and regulations allow the injured employee to dispute treatment decisions, provide for second and third medical opinions, and permit case review by an independent medical reviewer whose decision can result in the employer losing control over medical treatment of the employee.

Unlike our HCOs, our MPNs do not require our customers to pay annual enrollment fees, nor do they require our customers to comply with annual enrollment notice delivery requirements. As a result, there are fewer administrative costs to customers associated with an MPN program. This allows our MPNs to market their services at a lower cost to employers than our HCOs. For this reason, many customers may opt to use the MPN even though it provides customers with fewer rights to control medical treatment of employee injury claims.

We have received approval for and currently administer 27 MPNs. Customers can choose between two of our off-the-shelf MPNs, which serve as stand-alone networks or the foundation for the customer to customize their own MPN, in which they can add or remove specific providers or clinics. Each MPN must be reapproved every four years for each customer based on the date the MPN was approved by the California Division of Workers’ Compensation.

HCO and MPN Hybrid Offering

As a licensed HCO and approved MPN, in addition to offering HCO and MPN programs, we are also able to offer our customers a combination of the HCO and MPN programs. Under this program, a customer can enroll its employees in our HCO program, and then prior to the expiration of the 180-day treatment period under the HCO program, the customer (the employer) can then enroll their injured employees into our MPN program to keep the medical care within their network of providers. This allows our customers to take advantage of both programs, which is what our HCO customers typically do. To our knowledge, Medex is currently the only entity in California offering this hybrid program.

Medical Case Management

Medical case management oversees injured employees’ medical treatment to ensure that it progresses to a resolution and assures treatment plans are aligned from a medical perspective. Medical case management is a collaborative process that assesses, evaluates, coordinates, implements and monitors medical treatment plans and the options and services required for occupational injuries. At the direction of the employer, medical case managers function as liaisons between the injured employee, claims adjuster, medical providers, and workers’ compensation attorneys to achieve optimal results for the injured employee and their employer.

Our medical case management services are performed by nurses who are credentialed by the state and have expertise in various clinical areas and backgrounds in workers’ compensation matters. This combination allows our nurses the opportunity to facilitate medical treatment that understand the nuances of workers’ compensation, which may include litigation. By utilizing these services our customers can ensure that the injured employee receives quality medical treatment in a timely and appropriate manner to help the employee return to work and close the workers’ compensation claim. We also offer employee advocate services, which is similar to medical case management in that it utilizes our medical case managers to oversee an injured employee’s medical treatment; however, the employee advocate assists the injured worker in resolving any disputes between the employer and the claims adjusters that may arise. The employee advocate is given authorization by the employee to contact others on the employee’s behalf, such as claims adjusters, medical employees, lien claimants, human resources, return to work programs, unions, and employers, in order to facilitate resolution of the dispute. We generate revenue from these services when we receive a workers’ compensation claim and assign a medical case manager to oversee the injured workers’ medical treatment, with billing based on the number of hours a medical case manager works on the claim.

Medical Bill Review

Medical bills are one of the biggest expenses that an employer’s workers’ compensation insurance company must pay for. To curtail these expenses, our customers utilize our medical bill review services to review medical bills for services rendered to an injured employee. We provide professional analysis of medical provider services and equipment billing to ascertain proper reimbursement. Our review of medical bills includes coding review and re-bundling, confirming that the services are customary and reasonable, fee schedule compliance, out-of-network bill review, pharmacy review, and preferred provider organization repricing arrangements. While some states have adopted fee schedules, which regulate the maximum allowable fees payable under workers’ compensation for procedures performed by a variety of health treatment providers, many procedures are not covered by fee schedules and are still subject to review and negotiation.

Medical bill review services can result in significant claims savings. Our medical bill services are primarily within the state of California, but we process medical bill reviews in several other states. Out of state medical bill reviews typically are the result of an injured California employee moving to a different state, but who still requires medical care under an open workers’ compensation claim.

Utilization Review

Utilization review, also known as utilization management, is required by law in all states for workers’ compensation claims. Utilization review evaluates the medical necessity of proposed treatment by comparing medical treatment requests against accepted medical guidelines. Its purpose is to serve as a safeguard against payor liability for medical costs that are not medically appropriate or approved by the relevant medical and legal authorities. Reviews of medical treatment requests are conducted at the appropriate qualification level for the request by a nurse, peer-to-peer provider, a specialist or a medical director and within the timelines set by the relevant laws and regulations.

Our utilization review services provide an electronic intake of medical treatment requests, collection and review of the submitted documentation required for processing, and submission to the appropriately qualified reviewer for approval, modification, denial, or request for more information for the requested treatment. Once a determination is made, we process the request and notify all the stakeholders in the injured employee’s claim within the regulated timeframe.

Medicare Set-aside

Medicare set-aside services for workers’ compensation claims is a financial agreement that allocates a portion of a workers’ compensation settlement to pay for future medical services related to the work-place injury, illness, or disease. The purpose of the set-aside arrangement is to provide funds to the injured party to pay for future medical expenses that would not be covered by Medicare. This program affords our customers an effective way to overcome complications after settlement and avoids unnecessary costs attached to the claim.

Workers’ Compensation Carve-outs

Certain employers can opt out of the standard workers’ compensation regulatory dispute resolution scheme through carve-out agreements that comply with state statutory and regulatory requirements. More specifically, carve-out agreements permit employers and employees to establish alternative dispute resolution arrangements to resolve disputes in the context of workers’ compensation. These carve-out agreements are made between employers and the collective bargaining units representing the employer’s covered employees.

Utilizing our knowledge of the friction in the California workers’ compensation system, and the objectives of employers and the unions, we assist in guiding the negotiation of legal agreements for the implementation of workers’ compensation carve-outs for California customers and provide services that reflect the parties’ agreement regarding alternative dispute resolution arrangements. Under such carve-out agreements certain customers can access our HCOs, MPNs and medical case management program.

Expert Witness Testimony

As an ancillary service to our HCO and MPN services, we provide expert witness testimony before the California Workers Compensation Appeals Board. The fees we charge for this service include reimbursement of expert witness fees and travel and lodging expenses for all HCO customers except for one, whose fees are included in their monthly global fee.

Lien Representation

As of the third quarter of 2023, we discontinued providing lien representation services due to lack of customer demand.

Marketing, Customers and Pricing

We provide services to virtually any size employer in the state of California as well as insurers, third party administrators, self-administered employers, municipalities, and other industries. We also provide some customers utilization review, medical case management, and medical bill review services outside the state of California, typically to employees who suffered a workplace injury in California and then relocated to another state.

Our marketing and sales efforts focus primarily on customer referrals, conference presentations and responding to requests for proposals. We service both local and national accounts, however, with an emphasis on California focused markets. Our sales and marketing activities are conducted by account managers with the assistance of our executive team members. We do not market our services outside the state of California.

During fiscal 2023, three major customers combined accounted for 43% of sales, approximately 23%, 10%, and 10%, respectively. By comparison, during fiscal 2022 our three largest customers accounted for 44% of sales, approximately 24%, 10%, and 10%, respectively.

Our services can be integrated to allow for partial or full bundling of services and the sharing of information that creates efficiencies to further reduce the costs of claims. For example, our bundled services have allowed some customers to achieve up to a 70% reduction in the cost of injury claim resolution while maintaining superior treatment for their injured employees. The cost to our customers for our bundled services is generally the same as if the services were purchased individually.

Competition

We were one of the first commercial enterprises capable of offering HCO services and MPN services in California. While there are few HCO competitors, there are many MPN companies who compete in this market. Many of these competitors are larger than us and may have greater financial, research and marketing experience and resources than we do, and they may therefore represent substantial long-term competition. As of December 31, 2023, in California there were four certified health care organization licenses issued to three companies. We own two of the four licenses; the other two licenses are divided between two other companies. While we are aware of only one of the HCOs being active, we consider our current, direct HCO competition limited to these two licensee businesses. On the other hand, there are minimal requirements for establishing MPNs and therefore, as of December 31, 2023, there were approximately 2,486 active MPNs in the state of California according to the DWC MPN website. Of these, we have received approval for and administer 21 MPNs.

We compete on both quality and price of services. We maintain quality of service by virtue of the training, skill, and experience of our professional staff and outside consultants. We compete on price through our integration of robust information technology systems we license from various vendors. We focus our business primarily on those employers and payors who use our HCO and/or MPN services. We anticipate that this focus will keep most of this business stable and renewable. However, periodically we expect that large customers may establish the in-house capability, or their third-party administrators may offer a discounted bundle for the services we offer, as this has occurred in the past. Further, if we are unable to compete effectively either because of a degradation in quality-of-service delivery resulting from, for example, a reduction in the skill and experience of our personnel or our inability to effectively manage our information technology systems, it may be difficult for us to retain current customers or add new customers. A loss of customers, from whatever source, could materially and adversely affect our business, financial condition, and results of operations.

We rely on our well-trained and knowledgeable in-house professionals to develop service offerings that target the needs of our customers, all of whom seek efficient and effective resolution of workplace injuries and workers’ compensation claims. For example, we contract directly with medical providers based on quality determinations rather than the provision of discounted medical services. We believe this provides us with a competitive advantage because we can market a direct relationship with providers who have demonstrated expertise in treating occupational injuries and writing credible medical reports. These qualities contribute to quicker resolution of workplace injuries and workers’ compensation claims. We believe these qualities also provide more competitive value than relying on third party relationships or discounts alone.

We offer both HCO and MPN programs to potential customers, as well as an HCO/MPN combination model, which we believe also gives us a competitive advantage, because of the way the network was created. While some of our competitors offer either HCO or MPN services, to our knowledge, none of our competitors offer this type of HCO/MPN combination model, nor, in our opinion, do they have the expertise to administer one.

Governmental Regulation

Managed care programs for workers’ compensation are subject to various laws and regulations. The nature and degree of applicable regulation varies by state and by the specific services provided. Notably, services such as our HCOs, MPNs, and utilization review services that provide or arrange for the provision of healthcare services are subject to numerous, complex regulatory requirements that govern many aspects of our conduct and operations. These laws and regulations impose evolving administrative and legal burdens, expense, and risks to our business, but also provide a regulated environment in which our expertise and experience help us provide valuable services for our customers based on proven strategies that work within the existing system.

The provision of workers’ compensation managed care in the state of California is governed by legislation and secondary regulations. We are required to be licensed or receive regulatory approval to operate our HCO and MPN networks. Medex has recertified the “Medex HCO” through March 15, 2025, and the “Medex 2 HCO” through October 9, 2024. Our MPN networks are required to be reapproved every four years based upon when the MPN went into effect for each customer.

MMC is required to be accredited by the independent, nonprofit accreditation entity Utilization Review Accreditation Commission (“URAC”) in California to perform utilization review and is subject to a routine investigation by the state of California every five years. MMC has received full Utilization Management Accreditation for Workers’ Compensation as a Utilization Review Organization (“URO”) from URAC. The full accreditation requires us to have and follow specific policies and procedures for our utilization review services and demonstrate our commitment to quality and adherence to nationally recognized guidelines. MMC must apply for URAC reaccreditation every three years and was most recently reaccredited on January 1, 2024. The costs to be accredited by URAC for Workers’ Compensation Utilization Management for three years is $36,000. URAC accreditation also allows us to provide utilization review services nationally as it is widely accepted as an alternative credential to state specific licenses and certificates.

The services we provide have developed largely in response to legislation or other governmental action. In many jurisdictions, such as California, licensing laws and regulations generally grant broad discretion to supervisory authorities to adopt and amend regulations and to supervise regulated activities. Changes in the legislation, or rules and regulations regulating workers’ compensation may create greater or lesser demand for the services we offer or require us to develop new or modified services to meet the needs of the marketplace and compete effectively. Such changes could also have an impact on our costs for providing services, potentially to levels that make our services unattractive or unaffordable to existing or potential customers. We could also be materially and adversely affected if the state of California were to elect to reduce the extent of medical cost containment strategies available to insurance companies and other payors or adopt other strategies for cost containment that would not support demand for our services. To proactively address such possibilities, we have engaged a California-based lobbyist with expertise in workers’ compensation.

Healthcare reform remains a topic of considerable discussion at both the federal and state level. Due to uncertainties regarding the ultimate features of future reform initiatives and the timing of their enactment, we cannot predict which, if any, reforms will be adopted, when they may be adopted, or what impact they may have on our business or within the industry in which we participate. However, because workers’ compensation is primarily a disability program, not the focus of recent healthcare reform discussions, we do not anticipate that healthcare reform would significantly impact workers’ compensation.

Employees

Including the employees of our subsidiaries, as of April 12, 2024, we have a total of 30 full-time employees and one part-time employee. We also use the services of several consultants. Over the next twelve months, we anticipate hiring additional employees only if business revenues increase and our operating requirements warrant such hiring.

Reports to Security Holders

We file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy and information statements and other filings pursuant to Sections 13, 14 and 15(d) of the Exchange Act, and amendments to such filings with the Commission. The public may read and copy any materials we file with the Commission at its Public Reference Room at 100 F Street N.E., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The Commission maintains its internet site www.sec.gov, which contains reports, proxy and information statements and our other Commission filings. We also post electronic copies of our quarterly and annual reports on our website www.pacifichealthcareorganization.com, which can be viewed or downloaded free of charge. Materials and information on our website are not part of or otherwise incorporated into this annual report.

| ITEM 1A. | RISK FACTORS |

The risks and uncertainties described in the risk factors below are those that we currently consider material. You should carefully consider these risk factors, together with the statements contained elsewhere in this annual report, including our financial statements and the other reports we file with the Commission, in evaluating us or before making an investment in our common stock. The occurrence of any of, or a combination of, the following risks or uncertainties, or additional risks and uncertainties not presently known to us or that we currently believe to be immaterial, could materially and adversely affect our business, financial position, results of operations, liquidity, cash flows, or reputation.

You should not draw any inference as to the magnitude or likelihood of any particular risk from its position or categorization in the following discussion. Further, the headings and subheadings of the risk factors are organized based on certain shared characteristics with other risk factors, but each risk factor should be read without limiting its application or content to the heading under which it is organized.

Customer, Vendor and Competition Related Risks

A significant percentage of our revenue is generated from a few customers, the loss of one or more of which could have a material impact on our results of operations, cash flows and financial condition.

A significant portion of operating revenue is received from a relatively small group of customers. Combined sales for three customers accounted for approximately 43% and 44% of our total revenue in fiscal 2023 and fiscal 2022, respectively.

We cannot guarantee that significant customers will not, at some point, terminate or reduce our services. This has happened in the past. The loss of one or more significant customers has historically had an adverse impact on our business, results of operations, cash flows and financial condition, sometimes materially, until such time as we were able to retain new customers to replace them. While we continue to work to lessen our dependence on a few customers, we believe this will continue to be a risk in the foreseeable future.

Most of our customer contracts permit either party to terminate without cause. In the past, for example, we have lost customers due to competitive pricing pressures and customer cost reduction efforts; failure to maintain the quality of the services we provide; and our inability to retain sufficient staffing as a result of a health crisis, such as COVID-19, or other reasons. Competitive pricing is a particular challenge for us, as our larger competitors can often exploit economies of scale to price lower than us. If significant or multiple customers terminate their contracts, or do not renew or extend their contracts with us, it could have a material adverse effect on our business and results of operations.

A significant percentage of our accounts receivables is generated from a few customers, and if one or more of these customers default on their payment obligations to us, it could have a material impact on our results of operations, cash flows and financial condition.

A significant portion of our accounts receivable are received from a relatively small group of customers. Combined receivables for three customers accounted for approximately 49% of our total receivables in both fiscal 2023 and fiscal 2022, respectively. For example, a customer that accounted for 8% of our accounts receivable in fiscal 2023 has, as of the date of this annual report, a past due balance of over 90 days, which accounts for 81% of all outstanding past due invoices over 90 days. If this customer does not pay the outstanding amounts it will materially, negatively affect our results of operations and we may be forced to terminate our contract with this customer. If we are unable to diversify our customer base, we will continue to be susceptible to risks associated with customer concentration. Further, accounts receivables are typically unsecured and are thus subject to the increased risk of us being unable to collect overdue amounts. The inability or unwillingness to pay by our account debtors, for whatever reason or cause, could in turn have a material adverse effect on our financial condition.

We are reliant on the timely, accurate and consistent provision of outsourced services for various services and business functions, the disruption, malfunction, termination or replacement of which could impede our ability to provide our services and adversely affect our business.

We contract with various third-party vendors for the provision and support of our services and business functions, including the critical information systems functionality upon which our services rely. Our business is dependent on our ability to provide, in an efficient and uninterrupted manner, necessary business functions which we outsource, such as the processing and support of enrollment in our HCO and MPN programs, and the partial outsourcing of our utilization review, medical bill review, administrative services for medical case management and Medicare set-aside services. Our operations may be adversely affected if there is a failure, disruption or malfunction, (including cybersecurity breaches and other risks discussed further at “Cybersecurity, Information Technology and Outsourced Services Related Risks” below) in the provision of such outsourced services, or if the relationship with or services provided by our vendors are terminated in whole or in part. Further, we may not be able to find an alternative vendor in a timely manner, on acceptable terms, or that can provide adequate services or functionality.

Outsourcing also may require us to change our existing operations or adopt new processes for providing or managing our services. If there are delays or difficulties in changing business processes or our third-party vendors do not perform as expected, it may delay our ability to provide our services and we may not realize, or not realize on a timely basis, the anticipated functionality or benefits of these relationships. Terminating or transitioning, in whole or in part, arrangements with vendors could result in additional costs or penalties, risks of operational delays and interruptions, or potential errors and control issues during the termination or transition phase. For example, during the fourth quarter of 2022, we experienced difficulties when transitioning to a new software vendor for our utilization review and medical case management services. The vendor was unable to provide fully functional software, which resulted in the Company terminating the agreement and contracting with another software vendor. Throughout the software transitions, our automated processes had to be performed manually, which caused delays in providing services and invoicing our customers, reduced productivity, and increased outsourcing costs. Our revenues were adversely impacted in the fourth quarter of 2022 as a result of the interruptions and costs associated with these software transition difficulties. We may also be subject to future regulatory fines related to the software transition.

If we experience continued or another interruption in our ability to provide our services or loss of access to data resulting from a malfunction, termination, transition or other disruption in outsourced services, we may not be able to meet the demands of our customers and, in turn, our business and results of operations could be materially and adversely impacted.

Our revenues may decline if we cannot compete successfully in an intensely competitive market.

We target our products to employers seeking to control the cost of employee workers’ compensation claims. We face competition from a variety of companies and the markets for our services are fragmented and competitive. Our competitors include national managed care providers, preferred provider networks, smaller independent providers, third-party administrators, and insurance companies. Many of our current and potential competitors have significantly greater financial, technical, marketing, and other resources than we do. As a result, our competitors may be able to respond more quickly to new ways to manage treatment costs, including enhanced technology, changes in regulations and standards, and shifts in customer requirements. We believe that as managed care techniques continue to gain acceptance in the marketplace our competitors will increasingly consist of insurance companies, third-party administrators, large workers’ compensation managed care service companies and other significant providers of managed care products. These competitors may also be able to devote greater resources to the development, promotion and sale of their services and may be able to deliver competitive services or solutions at a lower price. Any of these competitive pressures could have a material adverse effect on our business, results of operations and financial condition.

Our business is driven substantially by the relation between the value we provide and the amount we charge for that value. If the scope and quality of our services lag behind the market or lower costs can be obtained elsewhere, we may lose customers which could have an adverse impact on our results of operations and financial condition.

We are in the business of assisting our customers in controlling the cost of their employee workers’ compensation claims. While we believe that several factors, including the quality of care provided to the employee, the rapidity at which the employee returns to work, and the service provided to the customer, play a part in attracting and retaining our customers, we believe that price is a primary determining factor in whether customers select or retain our services. While our competitors may offer direct fees less than those we charge, they have traditionally added fees to their other associated services and thus raised the total cost of their services. If our competitors reduce the cost at which they provide services, or our customers seek to reduce costs by performing similar services in-house, we anticipate we would have to likewise attempt to reduce the cost at which we provide our services or risk losing customers. Either outcome could have a material adverse impact on our business, results of operations and financial condition.

If we are unable to continue to attract and retain key employees and consultants with the skills our business requires, our business operations could be impacted negatively.

We compete with other workers’ compensation managed care companies and healthcare providers in recruiting qualified personnel and consultants. Hiring and retaining personnel with industry expertise is critical to our competitive strategy. There is intense competition for the services of such people. Furthermore, replacing executive officers and other key employees may be difficult and may take an extended period of time because of the limited number of individuals in our industry with the breadth of skills and experience required to perform these roles. Competition to hire from this limited pool is intense, and we may be unable to hire, train, retain or motivate these key personnel on acceptable terms given the competition among the numerous competitors in our industry for similar personnel, many of whom have greater financial resources than us and can offer higher salaries, better benefit packages and broader opportunities. In addition, we operate primarily in California and some of our roles require our employees to live in or near very high cost of living areas in Southern California, which corresponds to higher wage requirements and alternative employment options. We do not maintain “key person” insurance for any of our executives or employees.

Similarly, competition and pricing for our consultants and advisors, such as workers’ compensation consultants, legal, accounting, and other professional service providers, is increasing. As a relatively small business, these costs can disproportionately impact our business and results of operations compared to larger competitors. Further, our consultants and advisors may have commitments under consulting or advisory contracts with other entities that may limit their availability to us. If we are unable to continue to attract and retain such consultants, our ability to pursue our growth strategy may be limited.

We cannot guarantee that we will be able to attract and retain personnel in the future, particularly in a challenging labor market that disproportionately impacts us as a small service-oriented business. For example, during 2024, our Chief Financial Officer resigned and while have engaged the services of an outsourced CFO, we have not yet identified a full-time replacement for this role. Given the level of knowledge, experience, and skills the role of a full-time Chief Financial Officer requires, we cannot assure when we will be able to replace this role or the degree of impact on our salary and wages expenses when we do replace this role. If we are unable to effectively compete for, or otherwise attract or retain, key employees and consultants, our business and financial condition could be materially adversely affected.

Cybersecurity, Information Technology and Outsourced Services Related Risks

A cybersecurity attack or other disruption to our or our vendors’ information technology systems could result in the loss, theft, misuse, unauthorized disclosure, or unauthorized access of customer, customer-employee or company information, or could otherwise disrupt our operations, which could damage our relationships with customers, vendors or employees, expose us to litigation or regulatory proceedings, and harm our reputation, any of which could materially adversely affect our business, financial condition or results of operations.

We rely heavily on third-party provided information technology to support our business activities. Our business involves the transmission and storage of confidential and personal information, including those of our customers, their employees, and our employees. We, and the vendors we use to support our business, including vendor support of critical business functions such as IT, data management and cybersecurity, are at risk of cybersecurity breaches of the systems on which we rely, including circumvention or breach of security systems, denial-of-service attacks or other cyber-attacks, hacking, “phishing” attacks, computer viruses, ransomware, malware, employee error, social engineering, physical breaches, or other malfeasance. We anticipate that the threats of such incidents will continue to increase as dependence on information technology increases. Further, as these threats evolve, cybersecurity incidents could be more difficult to detect, defend against, and remediate.

For instance, and as previously disclosed and as discussed further in Item 1C. Cybersecurity herein, Fortra, LLC, the third-party vendor that provides the GoAnywhere managed file transfer as a service system (MFTaaS), experienced a data security incident that affected many of Fortra’s customers, including the Company. Through this incident the threat actor accessed certain of our customers’ employees’ and other third parties’ data, and such data included protected health information, as defined by the Health Insurance Portability and Accountability Act, and personal information. We have engaged outside experts to assist in investigating and responding to this incident and have provided the required notifications to the data owners, and where appropriate, to the individuals affected by the incident and to various State Attorneys General. As of the date of this annual report, this incident has not had a materially adverse impact on our results of operations. However, we have incurred expenses, and may incur in the future expenses and losses, related to this incident. Further, it is possible that we could become subject to investigations, fines, or penalties if it is determined that we have not met all of its obligations under relevant law related to this incident. It is also possible that this incident could materially impact the availability, cost, and/or coverage limits of cyber liability insurance in the future, which could materially affect our ability to contract with current or future customers depending on the cyber liability insurance requirements they require us to have. Further, any negative assessments of our IT systems and security measures, or cyber liability insurance requirements imposed on us by customers could also result in related material losses or expenses, such as those related to increased insurance expenses, losses of referrals and customers, harm to our reputation, acquiring and maintaining additional IT security enhancements, and changes to our third-party IT vendors. Furthermore, negative press, social media posts, blog posts, or other criticism of us from this incident and our responses could require us to incur additional expenses for crisis management, public relations, legal advice, or other services in our efforts to repair public perception or seek redress from third parties who may have caused or be at fault in this incident.

We continue to operate primarily remotely using employee laptops and accessories and secure, cloud-based data storage and access. As part of accommodating remote working, we rely on technology, software, hardware, and internet access and home resources of individual employees. We also have less control over the hardware, physical security of equipment, and maintenance of equipment used by our off-premises employees. Although we have implemented employee IT security training, instant remote access termination, remote hard drive wipe capabilities, and other systemic enhancements to increase security, we are still exposed to additional security and system failure risks through our accommodation of remote work.

In response to our adoption of remote working and the evolving nature of cybersecurity threats we have implemented additional security and access control measures and continue to utilize a third-party information technology vendor to manage the technological security and efficacy of our systems. We are also working to meet the standards for an organization of our size and type in conjunction with the National Institute of Standards and Technology. However, despite our efforts to mitigate cybersecurity risks, due to the ubiquitous and evolving nature of computer security attacks, cybersecurity breaches remain a risk to our business.

Any compromise or perceived compromise of our security (or the security of our third-party service providers) could damage our reputation and our relationship with our customers, third-party administrators, insurers, and enrollees; reduce demand for our services; and subject us to significant liability as well as regulatory action. Cybersecurity breaches or failure to meet customer or other required cybersecurity maturity standards could cause us to experience reputational harm, loss of customers, loss and/or delay of revenue, loss of proprietary data, loss of licenses, regulatory actions and scrutiny, sanctions or other statutory penalties, litigation, liability for failure to safeguard customers’ information, financial losses or a drop in our stock price.

We could lose cyber liability insurance coverage and be subject to uninsured liabilities.

While we seek to maintain cyber liability insurance coverage and currently have such a policy in place, we cannot be assured that we will be able to obtain cyber liability insurance coverage in the future, or that available cyber liability insurance will be adequate or will not be cost prohibitive.

As discussed elsewhere in this annual report, we responded to a cybersecurity incident in fiscal 2023. We made a claim related to that incident under the cyber liability insurance policy in effect at that time. While that claim has been covered thus far, we received a notice of non-renewal of that policy. We were able to obtain new cyber liability insurance, but we cannot assure that we will be able to in the future. Further, we could be denied further coverage of the claim we made related to the above incident. In any case, such coverage and coverage of potential future claims under our current or future cyber liability insurance policies may not adequately cover our liabilities and we cannot predict the likelihood or outcome of future legal, regulatory or governmental actions against us or the effect such matters may have on us or our future insurance availability or costs.

Additionally, cyber liability insurance is subject to policy limitations and exclusions. If the limits of our cyber liability policies are exhausted, in whole or in part, it could deplete or reduce the limits available to pay other material claims applicable to that policy period. Further, our cyber liability insurance carrier could become insolvent and unable to fulfill its obligations to defend, pay or reimburse us when those obligations become due. Loss of or material reduction in cyber liability insurance could also materially affect our ability to contract with current or future customers depending on the cyber liability insurance requirements they require us to have. In any of these cases, or if payments of claims exceed our limits or are not otherwise covered by insurance, it could have an adverse effect on our business, financial condition, or results of operations.

Our financial performance is tied to the quality of the information technology platforms we can acquire or license from third parties to provide our services, and the rapid advancements and changes in information technologies and their availability could disrupt our ability to remain competitive.

Effective and competitive delivery of our services is increasingly dependent upon the information technology resources and processes provided by third-party vendors. In addition to better serving our customers, the effective use of technology increases efficiency and enables us to reduce costs. Our future success will depend, in part, on our ability to address the needs of our customers by using technology to provide services to enhance customer convenience, as well as to create additional efficiencies in our operations. We are largely dependent on licensing and integrating various information technology systems and software from third parties for delivery of our services, the loss, ineffective management or malfunction of which could jeopardize all or parts of our ability to deliver our services. For example, in 2022 we had difficulties implementing new utilization review and medical case management software and had to transition to another vendor after the first vendor was unable to provide fully functioning software. During those transitions, our automated processes had to be performed manually, which caused delays in providing services and invoicing our customers, reduced productivity, and increased outsourcing costs. While the replacement software has restored our ability to provide services, certain important functionalities are still being developed. We cannot be assured that the new software system will remain functional, nor whether adequate software will be available from any source in the future. We anticipate that we will continue to rely on third-party software for our services in the future and many of the risks associated with the use of third-party software cannot be eliminated.

As technology in our industry changes and evolves, keeping pace may become increasingly complex and expensive, or entirely unavailable. Disruptive technologies could result in substantial increases in costs or a reduction in the need for services for which we currently charge our customers. For example, artificial intelligence and/or automation could render some of our services uncompetitive, unprofitable, or even obsolete, and require us to alter our business plans. Further, there can be no assurance that we will be able to effectively implement new technology-driven products and services, which could reduce our ability to compete effectively, particularly because many of our competitors have greater resources to invest in technological improvements than we do. The ability to provide our services may also suffer from the impacts of industry consolidation, as larger companies privatize, acquire, develop, retire or limit the licensing of the software we currently rely on for providing our services. For example, the software we used for our utilization review and medical case management services was purchased by a larger competitor and the software was discontinued because the competitor already had its own software. This resulted in us having to acquire new utilization review and medical case management software, which, as discussed in the preceding paragraph, resulted in having to make multiple transitions to access functional software, delays in providing services and invoicing our customers, reduced productivity, and incurred additional costs. We cannot be assured that this replacement software or any other software on which we are reliant will be available or adequate in the future. The cost of technologies we rely on may also change drastically, changing the profitability profiles of certain services and, in extreme cases, the viability of that line of business for us. Because we rely heavily on various technologies and their ability to integrate with other critical systems to provide our services, the occurrence of any of these events could have a material adverse impact on our business, results of operations and financial condition.

An interruption in our ability to access, review or deliver critical data may cause customers to terminate our services and/or may reduce our ability to effectively compete.

Certain aspects of our business are dependent upon our ability to store, retrieve, process and manage data, and to maintain and upgrade our data processing capabilities. Interruption of data processing capabilities for any extended length of time, loss of stored data, programming errors or other system failures could cause our customers to terminate our services and could have a material adverse effect on our business and results of operations. For example, during our fourth quarter 2022, we transitioned to new software for our utilization review and medical case management services, but the new software failed to perform as needed and we had to transition to different software for those functions. Although the current software has restored our ability to provide services, we continue to experience delays in invoicing several of our customers. We cannot assure that these customers or other customers that may be affected in the future will not dispute the amounts invoiced or otherwise terminate our services due to these or potential future functionality problems.

In addition, we expect that a considerable amount of our future growth will depend on our ability to process and manage claims data more efficiently and to provide more meaningful healthcare information to customers and payors of healthcare. There can be no assurance that our current data processing capabilities will be adequate, that we will be able to efficiently upgrade our systems to meet future needs, or that we will be able to develop, license or otherwise acquire software to competitively address market demands.

If we are unable to safeguard the security and privacy of confidential data, including personal information of our customers and their employees, our reputation and business could be harmed.

We are subject to data privacy related risks. Our services involve the collection and storage of confidential and personal information (including protected health information as defined by the Health Insurance Portability and Accountability Act) and the transmission of this information, most often electronically. For example, we collect personal information of our employees and our customers’ employees. We cannot guarantee such information is invulnerable to security breaches and other unauthorized access by third parties. In certain cases, such information is also provided to third parties, the transmission of which is also subject to security risks. Once such information is in the control of the third parties, we are most often no longer able to control the use of such information, or the security protections employed by such third parties.

For example, and as discussed in more detail in Item 1C. Cybersecurity, the third-party vendor that provides our managed file transfer as a service system experienced a data security incident that affected many of its customers, including the Company. The threat actor in this incident accessed certain of our customers’ employees’ and other third parties’ data and such data included protected health information, as defined by the Health Insurance Portability and Accountability Act, and personally identifiable information. We have provided the required notifications to the data owners, and where appropriate, to the individuals affected by the incident and to various State Attorneys General. As of the date of this annual report, this incident has not had a materially adverse impact on our results of operations. However, because of the ongoing nature of the effects of this incident and current unknown, an estimate of the future impacts, if any, on our business, results of operations and other potential liabilities, cannot be made.

In addition, as new data privacy and security laws are implemented, we may be unable to timely comply with such requirements, or such requirements may not be compatible with our current processes. Changing our processes to address new data security laws or customer requirements could be time-consuming and expensive and the failure to timely implement the required changes could result in our inability to sell our services or retain customers. For example, the California Consumer Privacy Act (“CCPA”) and amendments made to it through the California Privacy Rights Act (“CPRA”), can require certain businesses to give California consumers more control over their data and share certain notices regarding their privacy practices. We believe we are currently exempt from compliance with the CCPA and CPRA, but if we have misinterpreted the existing exemptions, or if amendments to or official guidance related to these laws changes the availability of these exemptions to us, we may incur significant costs, administrative burdens, and legal liabilities as a result.

The collection and transmission of confidential and personal information subjects us to numerous related security breach risks and regulatory compliance risks. Our failure to comply with evolving regulatory requirements related to the collection and transmission of such information or the loss, unauthorized disclosure or access of such information could lead to significant reputational or competitive harm, result in litigation, governmental or regulatory proceedings, or cause us to incur substantial liabilities, fines, penalties, or expenses.

Licensure and Regulatory Risks

Failure to maintain our licenses and/or accreditation would have a material, adverse impact on our business and results of operations.

Our HCOs require operating licenses from and our MPNs require approval by the state of California. If the California governing body were to determine that we have failed to comply with the licensure or approval requirements, it has the authority to deny, suspend or revoke our licenses or approvals. Further, our HCO licenses and MPN approvals must be recertified every three years and reapproved every four years, respectively. If our licenses or approvals were suspended, revoked, or not recertified or reapproved we would no longer be able to operate our HCO and/or MPN networks. In addition to the reduction in revenue we would experience from the loss of our HCO and/or MPN operations, the other services we offer would likely also be impacted negatively as many of the customers for our utilization review, medical bill review and medical case management services are derived from our HCO and MPN customers.

Similarly, the state of California requires workers’ compensation organizations performing utilization review in California to be accredited by URAC and undergo a routine investigation by the California Division of Workers’ Compensation every five years. We must be reaccredited by URAC every three years. If we were to lose our URAC accreditation or not earn reaccreditation, we would experience a loss of utilization review revenue in California and possibly other states. Other states in which we currently perform utilization review/utilization management each have different standards for authorizing utilization review organizations. If we were to fail to pass our routine investigations or meet those varied standards or experience administrative difficulty managing the maintenance of these various certifications and approvals, we could experience a loss or reduction in utilization review revenue and/or fines or penalties.

Our costs of operation and/or demand for our services may be negatively impacted by changes in government regulations.

Our primary business operations are subject to licensing and other regulatory requirements in California, including minimum qualification standards for personnel, confidentiality, internal quality control and dispute resolution procedures. The cost of compliance with these regulatory programs can increase our costs of operation, which may make it difficult for us to compete with other available alternatives for workers’ compensation healthcare cost control. The healthcare and workers’ compensation regulatory environment is constantly evolving. While we try to be involved in the legislative process and to stay informed on industry developments, we cannot predict what additional government initiatives affecting our business, if any, may be promulgated in the future. We cannot assure that we will always be able to adapt to new or modified regulatory requirements or to keep in force necessary licenses and government approvals. Proposals for healthcare legislative reforms are regularly considered at the federal and state levels. To the extent that such proposals affect workers’ compensation, such proposals may render us unable to deliver services profitably, reduce demand for our services, or require us to develop new or modified services. Any of these factors could materially impact our results of operations.

Industry Trend Related Risks

Challenges to the use of certain healthcare cost containment techniques may cause our revenue to decrease.

Within our industry there has been a movement among certain medical and healthcare providers and injured worker applicants’ attorneys to challenge the use of cost containment techniques. Some have even resorted to litigation to challenge the application of cost containment and medical control measures. This includes challenges to insurers’ claims adjudication, reimbursement decisions, and choice of medical provider and treatments. While these lawsuits have not yet involved us or any services we currently offer, we may be subject to them in the future, and the impacts of other legal challenges may negatively impact our ability to provide certain cost containment services in the future, which could result in material adverse impacts on our revenues.

Increased use of early intervention services could negatively impact our revenue.

Our revenue could be negatively impacted by the increased use of early intervention services such as injury occupational healthcare, first notice of loss, and telephonic case management services. The implementation at an early stage in the workers’ compensation claim by healthcare payors of these early intervention services can lead to decreases in the average length of, and the total costs associated with, a healthcare claim, which may reduce or even eliminate the need for the later stage network and healthcare management services we provide.

Declines in workers’ compensation claims could materially impact our financial condition and results of operations.

Some of our customers’ industries are labor intensive, but with the rise in costs for manual labor they may use technology to replace some of their workforce. This may cause a decline in the frequency and severity of the workers’ compensation claims and reduce the need for our services. However, even as the labor market changes, we still anticipate workers’ compensation claims will persist, as, for example, in California, employers are responsible for occupational injuries even if they occur while performing work-related activities at home. Changes in the strength of the economy also affect the size and activity of the workforce and consequently the level of workers’ compensation claims. These factors can cause cyclical and permanent material adverse impacts on our results of operations.

Additionally, we have seen recent declines in workers’ compensation claims, for example, from the decrease in the severity and frequency of COVID-19 in our customers’ workforce. During the first quarter of 2022, we saw an increase in reporting COVID-19 related claims, which resulted in increases in our claim network fees. However, that trend appears to have been short, as there was a decrease in the number of reported COVID-19 related claims in the second quarter of 2022 and through the end of fiscal 2022. Fiscal 2023 saw relatively stable COVID-19 claims frequency and severity trends, and state and local laws and regulations relating to the treatment of COVID-19 cases in the workplace had expired or relaxed, which has further reduced the overlap of COVID-19 cases on workers’ compensation claims.

Risks Related to Owning our Securities

The price and trading volume of our common stock may be volatile, which may negatively affect its value and liquidity.