UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One) |

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number:

(Exact name of Registrant as specified in its charter)

|

Not applicable |

|

|

|

(Translation of Registrant’s name into English) |

(Jurisdiction of incorporation or organization) |

|

PropertyGuru Group Limited

#12-01/04

(Address of principal executive offices)

#12-01/04

+

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered, pursuant to Section 12(b) of the Act

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of January 31, 2024, the registrant had

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

Non-accelerated filer ☐ |

Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

Other ☐ |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐Yes ☐ No

TABLE OF CONTENTS

|

Page |

|

|

|

|

1 |

||

|

|

|

1 |

||

|

|

|

1 |

||

|

|

|

5 |

||

|

|

|

6 |

||

|

|

|

7 |

||

|

|

|

9 |

||

|

|

|

|

Item 1. Identity of Directors, Senior Management and Advisers |

9 |

|

9 |

|

|

9 |

|

|

37 |

|

|

55 |

|

|

56 |

|

|

67 |

|

|

83 |

|

|

87 |

|

|

88 |

|

|

88 |

|

|

Item 11. Quantitative and Qualitative Disclosures About Market Risk |

95 |

|

Item 12. Description of Securities Other Than Equity Securities |

96 |

|

|

|

97 |

||

|

|

|

|

97 |

|

|

Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds |

97 |

|

97 |

|

|

98 |

|

|

98 |

|

|

98 |

|

|

99 |

|

|

Item 16D. EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES |

99 |

|

Item 16E. PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

99 |

|

99 |

|

|

99 |

|

|

100 |

|

|

Item 16I. Disclosure Regarding Foreign JURISDICTIONS that Prevent Inspections |

100 |

|

100 |

|

|

100 |

|

|

|

|

102 |

||

|

|

|

|

102 |

|

|

102 |

|

|

103 |

|

About This Annual Report

Except where the context otherwise requires or where otherwise indicated in this Annual Report, all references in this subsection to the “Company,” “we,” “us” or “our” refer to the business of PropertyGuru Group Limited and its subsidiaries, which prior to the Business Combination was the business of PropertyGuru Pte. Ltd. and its subsidiaries.

Presentation of Financial Information

Our financial statements included in this Annual Report are prepared in accordance with the International Financial Reporting Standards and its interpretations (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). Our financial statements are presented in Singapore dollars. Our fiscal year ends on December 31 of each year.

PropertyGuru refers in various places in this Annual Report to non-IFRS financial measures, Adjusted EBITDA and Adjusted EBITDA Margin which are more fully explained in “Item 5. Operating and Financial Review and Prospects—Non-IFRS Financial Measures and Key Performance Metrics.” The presentation of non-IFRS information is not meant to be considered in isolation or as a substitute for PropertyGuru’s audited consolidated financial results prepared in accordance with IFRS.

Frequently Used Terms

Key Business Terms

Unless otherwise stated or unless the context otherwise requires in this document:

“ACRA” means the Singapore Accounting and Corporate Regulatory Authority;

“agents” are real estate agents or individuals that sell, assist with the purchase of, and rent out properties for property seekers, consumers or clients (as applicable) in order to generate sales commissions from sales and property management fees from letting and management activities;

“AI” means artificial intelligence;

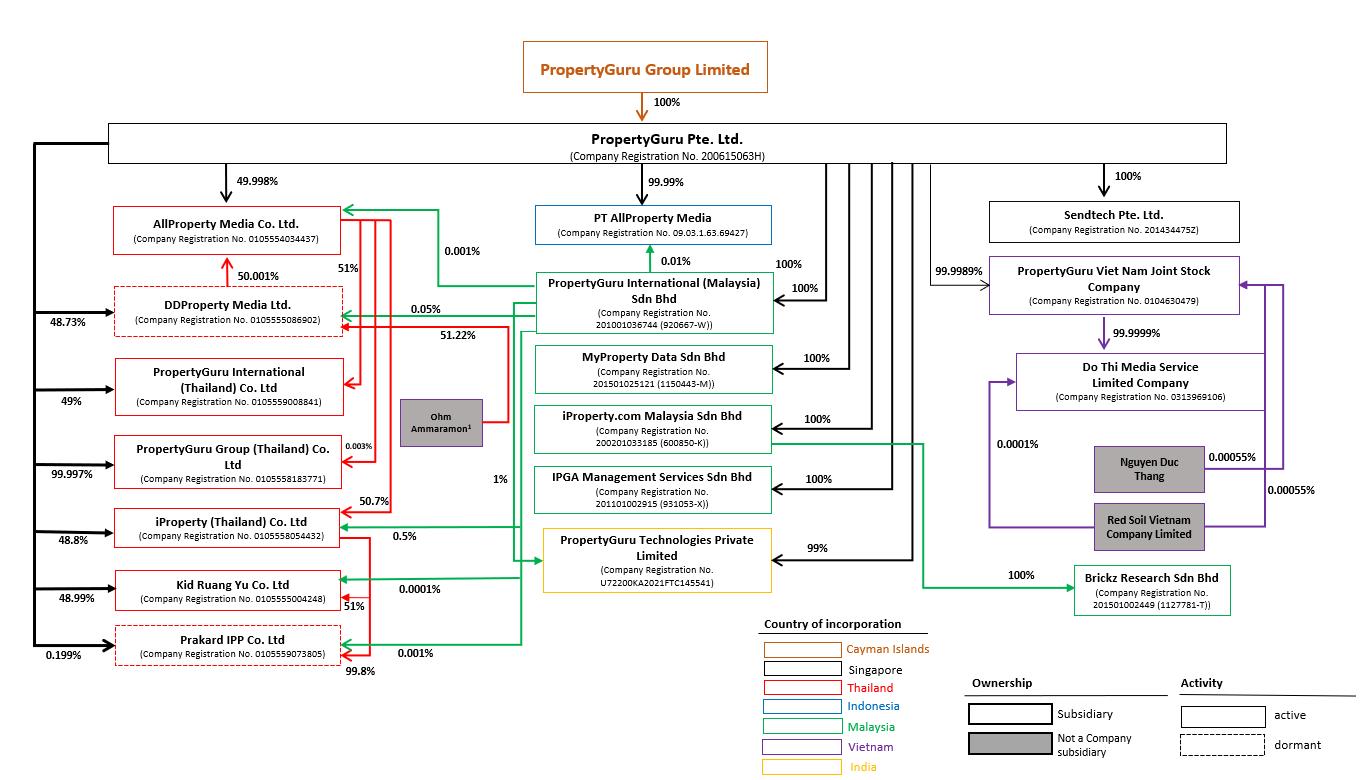

“AllProperty Media” means AllProperty Media Co., Ltd., a subsidiary of PropertyGuru;

“Amalgamation” means the amalgamation in accordance with Section 215A of the Companies Act (Chapter 50) of Singapore between Amalgamation Sub and PropertyGuru, with PropertyGuru being the surviving company and a wholly‑owned subsidiary of the Company;

“Amalgamation Effective Time” means the effective date of the Amalgamation as may be agreed by Amalgamation Sub, the Company, Bridgetown 2 and PropertyGuru in writing and specified in writing in the Amalgamation Proposal (as defined in the Business Combination Agreement) and as set out in the notice of amalgamation issued by ACRA in respect of the Amalgamation;

“Amalgamation Sub” means B2 PubCo Amalgamation Sub Pte. Ltd., a Singapore private company limited by shares and a direct wholly‑owned subsidiary of the Company;

“Amended and Restated Assignment, Assumption and Amendment Agreement” means the amendment and restatement, dated December 1, 2021, by and among Bridgetown 2, the Sponsor, the Company and Continental, to that Assignment, Assumption and Amendment Agreement, which removed Continental as a party to the Assignment, Assumption and Amendment Agreement;

“Amended Articles” means the amended and restated memorandum and articles of association of the Company adopted by special resolution dated July 23, 2021 and effective on March 16, 2022;

“API” means application programming interface;

“Assignment, Assumption and Amendment Agreement” means the amendment, dated July 23, 2021, to that certain warrant agreement, dated January 25, 2021, by and among Bridgetown 2, the Company, the Sponsor and Continental pursuant to which, among other things, Bridgetown 2 assigned all of its right, title and interest in the Existing Warrant Agreement to the Company effective upon the Merger Closing. The Assignment, Assumption and Amendment Agreement was amended and restated on December 1, 2021;

“Bridgetown 2” means Bridgetown 2 Holdings Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands;

1

“Bridgetown 2 Class A Ordinary Shares” means the Class A ordinary shares of Bridgetown 2, having a par value of $0.0001 each;

“Bridgetown 2 Class B Ordinary Shares” means the Class B ordinary shares of Bridgetown 2, having a par value of $0.0001 each;

“Bridgetown 2 Shares” means, collectively, the Bridgetown 2 Class A Ordinary Shares and Bridgetown 2 Class B Ordinary Shares;

“Business Combination” means the Merger, the Amalgamation and the other transactions contemplated by the Business Combination Agreement;

“Business Combination Agreement” means the business combination agreement, dated July 23, 2021 (as may be amended, supplemented, or otherwise modified from time to time), by and among the Company, Bridgetown 2, Amalgamation Sub and PropertyGuru;

“Business Combination Transactions” means, collectively, the Merger, the Amalgamation and each of the other transactions contemplated by the Business Combination Agreement, the Confidentiality Agreement, the PIPE Subscription Agreements, the Sponsor Support Agreement, the PropertyGuru Shareholder Support Agreement, the Registration Rights Agreement, the Amended and Restated Assignment, Assumption and Amendment Agreement, the Novation, Assumption and Amendment Agreement, the Plan of Merger, the Amalgamation Proposal, the Amended Articles and any other related agreements, documents or certificates entered into or delivered pursuant thereto;

“Cayman Companies Act” means the Companies Act (as amended) of the Cayman Islands;

“Closing” means the closing of the Amalgamation;

“Company” means PropertyGuru Group Limited, an exempted company limited by shares incorporated under the laws of the Cayman Islands, or as the context requires, PropertyGuru Group Limited and its subsidiaries and consolidated affiliated entities;

“Continental” means Continental Stock Transfer & Trust Company;

“customers” means the agents, developers, valuers, banks and other enterprise clients from which PropertyGuru generates revenue through sales of digital classifieds, property development advertising products and services and data services, as well as homeowners and tenants who engage home services providers through our Sendhelper business, which we acquired in October 2022;

“DDProperty Media” means DDProperty Media Ltd., a subsidiary of PropertyGuru;

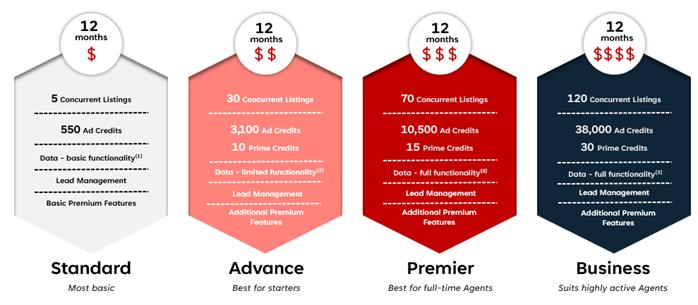

“depth products” means optional premium features and add‑ons offered to agents and integrated into PropertyGuru’s platforms such as display rankings or enhanced listings;

“developers” are property developers or individuals that develop houses, buildings, and land with the intention of selling them for a profit;

“Do Thi” means Do Thi Media Service Company Limited, a subsidiary of PropertyGuru;

“ESG” means environmental, social and governance;

“Exchange Ratio” means the quotient obtained by dividing $361.01890 by $10.00;

“Existing Warrant Agreement” means the warrant agreement, dated January 25, 2021, by and between Bridgetown 2 and Continental;

“Fintech” means financial technology;

“IASB” means the International Accounting Standards Board;

“IFRS” means the International Financial Reporting Standards, as issued by the IASB;

“iProperty” means iProperty Group Asia Pte. Ltd.;

2

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012;

“KKR” means Kohlberg Kravis Roberts & Co. L.P. and its affiliates;

“KKR Investor” means Epsilon Asia Holdings II Pte. Ltd., an affiliate of KKR;

“Malaysian Ringgit” and “MYR” means Malaysian Ringgit, the legal currency of Malaysia.

“Merger” means the merger between Bridgetown 2 and the Company, with the Company being the surviving company;

“Merger Closing” means the closing of the Merger;

“MyProperty Data” means MyProperty Data Sdn Bhd., a subsidiary of PropertyGuru;

“Novation, Assumption and Amendment Agreement” means the novation, assumption and amendment agreement, dated July 23, 2021, to that certain instrument by way of deed poll executed by PropertyGuru on October 12, 2018 (the “PropertyGuru Warrant Instrument”), to be effective upon the closing of the Business Combination, pursuant to which, among other things, the Company assumed all of PropertyGuru’s obligations and responsibilities pursuant to or in connection with the PropertyGuru Warrant Instrument;

“NYSE” means the New York Stock Exchange;

“ordinary shares” means the ordinary shares of the Company, having a par value of $0.0001 each;

“Project Panama Entities” means iProperty’s (a subsidiary of REA Group) operating entities in Malaysia and Thailand, consisting of iProperty.com Malaysia Sdn. Bhd., Brickz Research Sdn. Bhd., IPGA Management Services Sdn. Bhd., iProperty (Thailand) Co., Ltd., Prakard IPP Co., Ltd. and Kid Ruang Yu Co., Ltd, whose shares were wholly acquired by PropertyGuru on August 3, 2021;

“PDPA” means the Personal Data Protection Act 2012 of Singapore;

“PG Vietnam” means PropertyGuru Viet Nam Joint Stock Company, a subsidiary of PropertyGuru;

“PGI Thailand” means PropertyGuru International (Thailand) Co., Ltd., a subsidiary of PropertyGuru;

“PIPE Investment” or “PIPE Financing” means the commitment by the PIPE Investors to subscribe for and purchase, in the aggregate, 13,193,068 ordinary shares for $10 per share, or an aggregate purchase price equal to $131,930,680, which includes REA’s $20.0 million subscription in the PIPE Investment and an additional $31.9 million equity investment in the Company by REA relating to REA’s existing call option to acquire additional shares in PropertyGuru, pursuant to the PIPE Subscription Agreements;

“PIPE Investors” means the third‑party investors who entered into PIPE Subscription Agreements, and Red Square Singapore Limited, pursuant to the joinder agreement dated March 10, 2022, by and among the Company, Bridgetown 2, an individual and Red Square Singapore Limited;

“PIPE Subscription Agreements” means the share subscription agreements, dated July 23, 2021, by and among the Company, Bridgetown 2 and the PIPE Investors pursuant to which the PIPE Investors have committed to subscribe for and purchase, in the aggregate, 13,193,068 ordinary shares for $10 per share, or an aggregate purchase price equal to $131,930,680, which includes REA’s $20.0 million subscription in the PIPE Investment and an additional $31.9 million equity investment in the Company by REA relating to REA’s existing call option to acquire additional shares in PropertyGuru. For the avoidance of doubt, the PIPE Subscription Agreements include the REA Subscription Agreement;

“Priority Markets” means Singapore, Vietnam, Malaysia and Thailand;

“PropertyGuru” means PropertyGuru Group Limited, its Singapore-incorporated subsidiary PropertyGuru Pte. Ltd., or either such company together with its respective subsidiaries and consolidated entities, as the context requires;

“PropertyGuru Shares” means the outstanding ordinary shares of PropertyGuru;

“PropertyGuru Shareholder Support Agreement” means the voting support and lock‑up agreement, dated July 23, 2021, by and among Bridgetown 2, the Company, PropertyGuru and certain of the shareholders of PropertyGuru, pursuant to which (i) certain PropertyGuru shareholders who hold an aggregate of at least 75% of the outstanding PropertyGuru voting shares have agreed, among other things: (a) to appear for purposes of constituting a quorum at any meeting of the shareholders of

3

PropertyGuru called to seek approval of the transactions contemplated by the Business Combination Agreement and the other transaction proposals; (b) to vote in favor of the Business Combination Transactions; (c) to vote against any proposals that would materially impede the Business Combination Transactions; and (d) not to sell or transfer any of their shares prior to the closing of the Business Combination; (ii) certain shareholders of PropertyGuru have agreed to a lock‑up of the ordinary shares in the Company they have received pursuant to the Amalgamation (subject to certain exceptions) for a period of 180 days following the closing of the Business Combination; and (iii) certain shareholders of PropertyGuru and the Company have agreed to enter into a shareholders agreement governing the rights and obligations of such shareholders with respect to the Company and ordinary shares in the Company which, among other things, include certain non‑compete obligations, “drag‑along” rights applicable to and as among such shareholders, “rights of first offer” rights and board appointment rights (the “Shareholders’ Agreement”);

“PropertyGuru Warrant Instrument” has the meaning assigned to such term in the definition of “Novation, Assumption and Amendment Agreement”;

“PropertyGuru Warrants” means the 112,000 warrants to purchase PropertyGuru Shares issued to KKR Investor in accordance with the PropertyGuru Warrant Instrument;

“PropTech” means property technology;

“realestate.com.au” means realestate.com.au Pty Ltd;

“REA” means REA Asia Holding Co. Pty Ltd;

“REA Group” means REA Group Ltd;

“REA Subscription Agreement” means the subscription agreement, dated July 23, 2021, by and among the Company, Bridgetown 2 and REA Asia Holding Co. Pty Ltd;

“REA Transitional Services Agreement” means the transitional services agreement, dated August 3, 2021, by and among realestate.com.au Pty Ltd and PropertyGuru;

“Registration Rights Agreement” means the registration rights agreement, dated July 23, 2021, by and among Bridgetown 2, the Company, the Sponsor, the directors of Bridgetown 2 who hold Bridgetown 2 Shares, certain advisors of Bridgetown 2 to whom the Sponsor has transferred Bridgetown 2 Shares, certain shareholders of Bridgetown 2 affiliated with the Sponsor, and certain of the shareholders of PropertyGuru to be effective upon Closing pursuant to which, among other things, the Company agreed to undertake certain resale shelf registration obligations in accordance with the Securities Act and the Sponsor, certain Sponsor affiliated parties and certain shareholders of PropertyGuru party thereto have been granted certain demand and piggyback registration rights;

“RSU” means restricted stock units;

“SEC” means the U.S. Securities and Exchange Commission;

“Sendhelper” means Sendtech Pte. Ltd.;

“Shareholders’ Agreement” means the shareholders agreement, dated March 17, 2022, by and among the Company, each of the TPG Investor Entities, the KKR Investor, REA and REA Group Limited;

“Singapore Dollars” and “S$” means Singapore dollars, the legal currency of Singapore;

“Sponsor” means Bridgetown 2 LLC, a limited liability company incorporated under the laws of the Cayman Islands;

“Sponsor Support Agreement” means the voting support agreement, dated July 23, 2021, by and among Bridgetown 2, the Sponsor, the Company and PropertyGuru pursuant to which the Sponsor has agreed, among other things and subject to the terms and conditions set forth therein: (i) to vote in favor of the transactions contemplated in the Business Combination Agreement and the other transaction proposals, (ii) to appear at the Extraordinary General Meeting for purposes of constituting a quorum, (iii) to vote against any proposals that would materially impede the transactions contemplated in the Business Combination Agreement and the other transaction proposals, (iv) not to redeem any Bridgetown 2 Shares held by the Sponsor, (v) not to amend that certain letter agreement between Bridgetown 2, the Sponsor and certain other parties thereto, dated as of January 25, 2021, (vi) not to transfer any Bridgetown 2 Shares held by the Sponsor, subject to certain exceptions, (vii) to release Bridgetown 2, the Company, PropertyGuru and its subsidiaries from all claims in respect of or relating to the period prior to the Closing, subject to the exceptions set forth therein (with PropertyGuru agreeing to release the Sponsor and Bridgetown 2 on a reciprocal basis) and (viii) to a lock‑up of its ordinary shares in the Company during the period of one year from the Closing, subject to certain exceptions;

4

“TPG” means TPG Inc. and its affiliates;

“TPG Investor Entities” means TPG Asia VI SF Pte. Ltd. and TPG Asia VI Digs 1 L.P., each an affiliate of TPG; and

“U.S. Dollars” and “$” means United States dollars, the legal currency of the United States; and “U.S. GAAP” means United States generally accepted accounting principles.

Key Performance Metrics and Non‑IFRS Financial Measures

Unless otherwise stated or unless the context otherwise requires in this document:

“Adjusted EBITDA” is a non-IFRS financial measure defined as net profit/loss for year/period adjusted for changes in fair value of preferred shares, warrant liability and embedded derivatives, finance costs, depreciation and amortization, tax expenses or credits, impairments when the impairment is the result of an isolated, non-recurring event, share grant and option expenses, loss on disposal of plant and equipment and intangible assets, currency translation profit or loss, fair value profit or loss on lease modifications and contingent consideration, business acquisition transaction and integration cost (including contingent consideration), and the cost of listing and initial public offering (“IPO”) activities;

“Adjusted EBITDA Margin” is a non‑IFRS financial measure defined as Adjusted EBITDA as a percentage of revenue;

“ARPA” is defined as agent revenue for a period divided by the average number of agents in that period, which is calculated as the sum of the number of total agents at the end of each month in a period divided by the number of months in such period;

“Average revenue per listing” is defined as revenue for a period divided by the number of listings in such period;

“Engagement Market Share” is the average monthly engagement for websites owned by PropertyGuru as compared to average monthly engagement for a basket of peers calculated over the relevant period. Engagement is calculated as the number of visits to a website during a period multiplied by the amount of time spent per visit on that website for the same period, in each case based on data from SimilarWeb. Engagement Market Share is based on the prevailing SimilarWeb algorithm on the date the Company first filed or furnished such information to the SEC;

“Number of agents” in all Priority Markets except Vietnam is calculated for a period as the sum of the number of agents with a valid 12-month subscription package at the end of each month in a period divided by the number of months in such period. In Vietnam, number of agents is calculated as the number of agents who credit money into their account within the relevant period. When counting in aggregate across the PropertyGuru group, in markets where PropertyGuru operates more than one digital property marketplace, an agent with subscriptions to more than one portal is only counted once;

“Number of listings” in Vietnam is calculated as the sum of all listings created in each month over the relevant period (other than listings from promotional accounts). Number of listings is used to calculate average revenue per listing;

“Number of real estate listings” is calculated as the average number of listings created monthly during the period for Vietnam and the average number of monthly listings available in the period for other Priority Markets;

“property seekers” is the number of total visits to PropertyGuru’s websites over a period, based on Google Analytics data; and

“Renewal rate” is defined as the number of agents that successfully renew their annual package during a year/period divided by the number of agents whose packages are up for renewal (at the end of their 12 month subscription) during that year/period.

Industry and Market Data

This Annual Report includes industry, market and competitive position data that have been derived from publicly available information, industry publications and other third-party sources, including estimated insights from SimilarWeb and Google Analytics, as well as from PropertyGuru’s own internal data and estimates.

Industry publications and other published sources generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. While we have compiled, extracted, and reproduced industry data from these sources, we have not independently verified the data. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this Annual Report. These forecasts and forward-looking information are subject to uncertainty and risk due to a variety of factors, including those described under “Item 1. Key Information—D. Risk Factors.” These and other factors could cause results to differ materially from those expressed in any forecasts or estimates.

5

Trademarks

We have proprietary rights to trademarks used in this Annual Report that are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, trademarks and trade names referred to in this Annual Report may appear without the “®” or “™” symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies’ trademarks, trade names or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Each trademark, trade name or service mark of any other company appearing in this Annual Report is the property of its respective holder.

6

Cautionary Note Regarding Forward-Looking Statements

This Annual Report includes statements that express our opinions, expectations, beliefs, plans, objectives, assumptions or projections regarding future events or future results of operations or financial condition and therefore are, or may be deemed to be, “forward‑looking statements.” These forward‑looking statements can generally be identified by the use of forward‑looking terminology, including the terms “believes,” “estimates,” “anticipates,” “expects,” “seeks,” “projects,” “intends,” “plans,” “may,” “will” or “should” or, in each case, their negative or other variations or comparable terminology. These forward‑looking statements include all matters that are not historical facts. They appear in a number of places throughout this Annual Report and include statements regarding our intentions, beliefs or current expectations concerning, among other things, our results of operations, financial condition, liquidity, prospects, growth, strategies, future market conditions or economic performance and developments in the capital and credit markets and expected future financial performance, the markets in which we operate as well as any information concerning possible or assumed future results of our operations. Such forward‑looking statements are based on available current market material and our management’s expectations, beliefs and forecasts concerning future events impacting us. Factors that may impact such forward‑looking statements include:

7

The foregoing list of factors is not exhaustive. The forward‑looking statements contained in this Annual Report are based on our current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward‑looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward‑looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Item 3. Key Information—D. Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of the assumptions prove incorrect, actual results may vary in material respects from those projected in these forward‑looking statements. Some of these risks and uncertainties may in the future be amplified by the COVID-19 pandemic and there may be additional risks that we consider immaterial or which are unknown. It is not possible to predict or identify all such risks. We will not and do not undertake any obligation to update or revise any forward‑looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

You should read this Annual Report and the information incorporated by reference herein with the understanding that our actual future results, levels of activity, performance and events and circumstances may be materially different from what we expect.

8

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Not applicable.

Not applicable.

Our business faces significant risks and uncertainties. You should carefully consider all of the information set forth in this Annual Report and in the other documents we file with or furnish to the SEC, including the following risk factors, before deciding to invest in or to maintain an investment in our securities. Our business, financial condition or results of operations could be materially and adversely affected by any of these risks, any of which could have an adverse effect on the trading price of our securities. Additional risks not presently known to us or that we currently deem immaterial may also impair our business, financial condition and results of operations.

Summary of Risk Factors

Our business is subject to a number of risks and uncertainties, including those described in Item 3.D. of this Annual Report. If any of those risks are realized, our business, financial condition and results of operations could be materially and adversely affected. Set forth below is a summary list of the key risks to our business:

Risks Related to Our Business and Industry

9

Risks Related to Our Intellectual Property and Technology

Risks Related to Regulatory Compliance and Legal Matters

Risks Related to Ownership of Securities in the Company

Risks Relating to Taxation

10

Risks Related to Our Business and Industry

Global economic conditions have been and continue to be challenging and have had, and may continue to have, an adverse effect on financial markets, the health of the real estate industry in our Priority Markets and the economy in general.

The possibility of downturns or turbulence in global financial markets and economies as well as fiscal policies in our Priority Markets has had, continues to have, and may increasingly have a negative impact on property seekers, our customers, demand for our existing and new products and services, profitability, access to credit and our ability to operate our business.

Our financial performance is influenced by the overall condition of the real estate markets in the Priority Markets in which we operate. Each of these real estate markets are affected by various macroeconomic factors outside our control (which by their nature are cyclical and subject to change). These factors include inflation, interest rates, the general market outlook for economic growth, unemployment and consumer confidence. These factors are also affected by government policy and regulations that may change.

In many countries globally, including our Priority Markets, high inflation and concerns over potential economic recessions continue to persist, including due to global economic, political and social conditions that can give rise to global supply chain disruptions, government stimulus packages, rising costs of commodities, and geopolitical conflicts. Inflation has risen significantly in recent years, which in turn led to an increase in interest rates in 2022 and 2023, which impacted mortgage affordability. To the extent inflation and interest rates remain elevated, these pressures may negatively impact property demand and demand for our products and services. In addition, lingering effects of global and industry-wide supply chain disruptions caused by factors such as the COVID-19 pandemic and geopolitical turmoil resulted in shortages in labor, materials and services. Such shortages contributed to rising costs of labor, materials and services and scarcity of certain products and raw materials could continue to significantly impact our customers and weaken global economies. Inflationary pressures increased our operating costs in 2022 and 2023 and may have an adverse impact on our costs, margins and profitability in the future. We cannot predict any future trends in the rate of inflation, and to the extent we are unable to recover higher costs through higher prices for our products and offerings, a significant increase in inflation could negatively impact our business, financial condition and results of operation.

Our marketplaces business generates revenue from property developers from advertising activities to promote sales of residences in new property developments (which we refer to as “primary listings” to distinguish them from “secondary” sales of already existing residential properties). Given the longer lead times required and increased costs to develop and market new property developments, these primary listings may prove more volatile than secondary listings, as economic uncertainty (over a longer period) may have a greater adverse impact on the rate and extent of new property development activity and could result in fewer primary listings. In addition, most agents in our Priority Markets are effectively self-employed individuals who are largely commission remunerated and may leave the industry when market conditions deteriorate sufficiently. Accordingly, a property downturn could cause a decline in the number of agents and developers, reduce demand for our products and services or reduce our ability to increase prices in light of subdued market conditions. For example, in Vietnam, our agent customers significantly reduced their discretionary spending in the fourth quarter of 2022 and through 2023 following actions by the State Bank of Vietnam to control credit growth, including controlling loans for real estate, which suppressed consumer sentiment and the real estate market in Vietnam. This negatively impacted the number of real estate listings on our platform and in turn impacted our revenue in Vietnam, where we operate a pay-as-you-go model and effective monetization depends on our ability to sustain the number of listings that agents post to our platform. The cyclical nature of the real estate market also has an effect, where the real estate market in each country or major city tends to rise and fall in line with economic prosperity and sentiment in that country or major city (noting Priority Markets generally operate independently of one another). These macroeconomic factors, along with regulatory and political changes, also contribute to the availability of credit to purchasers, which is a main driver of housing price accretion and capability to transact.

Government and regulatory policies in our Priority Markets, including policies towards housing and infrastructure development and sustaining continued economic growth, could also have a significant impact on real estate or credit markets and, in turn, our revenues. For example, governmental actions in Vietnam in 2022 significantly limited both consumers’ and developers’ access to credit, which has suppressed the real estate market in Vietnam and weakened consumer confidence, which in turn has reduced demand for our platform, products and services in Vietnam in 2023. For further information, see “— Our business is subject to legal and regulatory risks and changes in regulatory requirements and governmental policy that could have an adverse impact on our business and prospects.”

In addition, our ability to fund our liquidity requirements and operate our business depends on our cash flows from operations and, in future, potentially our ability to access capital markets and borrow on credit facilities. Our access to and the availability of financing on acceptable terms may be adversely impacted by global economic conditions, including inflation, interest rate changes and systemic banking risks. For more information, please see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources.”

Changing economic conditions have also had and may continue to have an effect on foreign exchange rates, which in turn may affect our business. For further information, see “— Fluctuations in foreign currency exchange rates will affect our financial results, which we report in Singapore Dollars.”

11

We cannot predict the timing or duration of an economic slowdown or the timing or strength of a subsequent economic recovery generally or in the real estate industry. If macroeconomic conditions worsen or the current global economic conditions continue for a prolonged period of time, we are not able to predict the impact that such conditions will have on credit markets, the real estate industries in our Priority Markets and our results of operations.

Changes in the structure of the real estate markets in which we operate could also adversely impact our business. For example, a reduction in the customary rate of commissions earned by real estate agents from property sales could reduce agents’ capacity to pay for our products and services and could prevent us from increasing prices or even require us to reduce our subscription fees or the prices of our discretionary credits, which could have an adverse effect on our business and financial performance. This risk would be more pronounced in Vietnam where our business derives most of its revenue from agent discretionary revenue given our pay-as-you-go model in the country. Similarly, if larger agencies, rather than individual agents, become comparatively more important as a source of revenue, this could increase customer pricing power, could prevent us from increasing prices or put pressure on our existing pricing and could develop into us competing with such agencies’ own websites or platforms. The occurrence of any of these factors could adversely affect our business, financial condition and results of operations.

We have a history of losses, and we may not maintain profitability in the future.

We have a history of losses, including net losses of S$15.3 million, S$129.2 million and S$187.4 million for the years ended December 31, 2023, 2022 and 2021, respectively. We expect to continue to make investments in developing and expanding our business, including but not limited to in technology, recruitment and training, marketing, and for the purpose of pursuing strategic opportunities. We may incur substantial costs and expenses from our growth efforts before we receive any incremental revenues in respect of any acquisitions or investments in growth. We may find that these efforts are more expensive than we originally anticipate, or that these investments do not result in a sufficient increase in revenue to offset these expenses, which would further increase our losses. Additionally, we may continue to incur significant losses in the future for a number of reasons, including but not limited to:

Inflationary pressures increased our operating costs in 2022 and 2023 and the effects of inflation may have an adverse impact on our costs, margins and profitability in the future. Our initiatives to alleviate inflationary pressures, such as alternative supply arrangements and changes to our hiring policies, including hiring employees in locations with lower ongoing wage costs, may not be successful or sufficient. In addition, in light of rising operating costs, we implemented cost control actions in 2022 and 2023, including by managing discretionary costs, implementing selective hiring and reducing our sales and marketing expenses.

12

Furthermore, there can be no assurance that we will be willing or able to cover any increased costs by increasing the prices of our products and services.

If we fail to maintain our profitability or grow our revenue sufficiently to keep pace with our investments and other expenses, our business will be harmed. If our existing businesses or any future acquisitions underperform, this may result in impairments to the carrying values of assets on the balance sheet including but not limited to goodwill and intangible assets. These impairments may adversely impact our financial condition and results of operations and the confidence of shareholders, lenders, customers and our employees. Impairments may also be generated due to changes in the assessment methodology of the carrying values of assets or changes to the inputs that form part of these assessments. These changes are not predictable and many of them may be outside of our control. In addition, as a public company, we will also incur significant legal, accounting, insurance, compliance and other expenses that we did not incur as a private company.

Our business is dependent on our ability to attract new, and retain existing, customers and consumers to our platform in a cost-effective manner.

Currently, we generate revenue primarily through sales of digital classifieds and property development advertising products and services to real estate agents and developers, which we refer to as customers. Our ability to attract and retain customers, and ultimately to generate advertising revenue, depends on a number of factors, including but not limited to:

We may not succeed in capturing a greater share of our customers’ advertising expenditure if we are unable to convince them of the effectiveness or superiority of our products compared to alternatives, including but not limited to traditional offline advertising media. Property developers, in particular, continue to allocate significant advertising expenditure for the sales of residences in their new property developments to print media, including but not limited to large display advertisements in newspapers, and other media such as billboards. This is significant because property advertising in our Priority Markets predominantly involves these primary transactions (i.e., new developments advertised by property developers or their marketing agents). We also compete for a share of advertisers’ overall marketing budgets with other PropTech companies in our Priority Markets.

If we are unable to attract new customers in a cost-effective manner or if existing customers reduce or discontinue their subscription or advertising spending with us, our business, financial condition and results of operations could be adversely affected.

We do not have long-term contracts with most of our customers, and most of our customers have the ability to terminate their relationship with us on short notice by choosing not to renew their contracts with us.

Our agent subscription agreements generally have a duration of 12 months and we do not have long-term contracts with most of our other customers. Our customers could choose to modify or discontinue their relationships with us when their subscription agreements expire, which could leave us with little or no advance notice of their departure. In addition, as existing subscription agreements or other contracts expire, we may not be successful in renewing these subscription agreements or other contracts, securing new customers or increasing or maintaining the amount of revenue we derive from a given subscription agreement or other contract over time for a number of reasons, including, among others, the following:

13

Our decision to launch new product or service offerings and increase the prices of our products and services may not achieve the desired results.

The industry for residential real estate transaction services, technology, information marketplaces and advertising is dynamic, and the expectations and behaviors of customers and consumers shift constantly and rapidly. As part of our operating strategy, we have increased, and plan in the future to continue to change, the nature and number of our products (including depth products) and services and, with that, the prices we charge our customers for the products and services we offer. Changes or additions to our products and services may not attract or engage our customers, and may reduce confidence in our products and services, negatively impact the quality of our brands, negatively impact our relationships with partners or other industry participants, expose us to increased market or legal risks, subject us to new laws and regulations or otherwise harm our business. Our customers may not accept new products and services (which would adversely affect our average revenue per agent (“ARPA”)), or such price increases may not be absorbed by the market, or our price increases may result in the loss of customers or the loss of some of our customers’ business. We may not successfully anticipate or keep pace with industry changes, and we may invest considerable financial, personnel and other resources to pursue strategies that do not ultimately prove effective such that our results of operations and financial condition may be harmed. If we are not able to raise our prices or encourage our customers to upgrade their subscription packages or invest in depth products to further differentiate their listings, or if we lose some of our customers or some of our customers’ business as a result of price increases, or if the bargaining power of our customer base increases and the subscription prices and other fees we are able to charge real estate developer or agent customers decline, our business, financial condition and results of operations could be adversely affected.

If our customers do not make valuable contributions to our platform or fail to meet consumers’ expectations, we may experience a decline in the number of consumers accessing our platform and consumer engagement, which could adversely affect our business, financial condition and results of operations.

Our success depends on our ability to attract consumers to our platform, to maintain high levels of consumer engagement and to offer products and services that meet customer demand. We depend on our customers to list properties on our platform that are desirable to consumers and responsive to consumers’ expectations. The inventory of properties available for our customers to list on our platform may be affected by various factors outside of their and our control, such as the general market outlook for economic growth, the overall health of the real estate market and changes to the regulation of the real estate industry. In addition, if our customers stop using our products, services and/or platform, we may not be able to provide consumers with a sufficient range and variety of listings, which could reduce the attractiveness of our platform for consumers and lead to a reduction in consumer traffic. If our customers do not continue to make valuable contributions to our platform, our brand, reputation, traffic on our platform and sales of our products and services could be adversely affected.

Currently, we rely on the sale of listing and advertising services for the majority of our revenue. If we experience a decline in the number of consumers or a decline in consumer engagement, our customers may not view our products and services as attractive for their marketing expenditures and may reduce their spending with us, which may adversely affect our business, financial condition and results of operations.

We may not be able to attract a sufficient level of traffic to our websites and applications.

The attractiveness of our online real estate advertising platform to our real estate developer or agent customers is influenced by our ability to draw consumers (who conduct property searches and access property related information research) to our websites and applications. A decline in the level of consumer traffic to our websites and applications could have a material adverse effect on our ability to generate revenue from the sale of subscriptions and advertising on our websites and mobile applications as well as on our relationships with real estate developer or agent customers.

A number of factors may negatively affect the volume of traffic to our websites and applications, including but not limited to:

14

Any inability to attract a sufficient level of traffic to our websites and applications for the foregoing or other reasons could adversely affect our business, financial condition and results of operations.

We operate in a highly competitive and rapidly changing industry, which could impair our ability to attract users of our products, which could adversely affect our business, results of operations and financial condition.

We face competition to attract consumers to our websites, mobile and software applications and to attract real estate agents, property developers and other enterprise customers to purchase our products and services. The markets for online real estate advertising and property technology services in our Priority Markets are highly competitive and rapidly changing. In addition to competing with traditional media sources for a share of advertisers’ overall marketing budgets, our business is subject to the risk of digital and other disruption. Our success depends on our ability to continue to attract additional consumers to our websites, mobile and software applications. Existing or new competitors could expand their product offerings or develop new products or technology that compete with ours. For example, our competitors may incorporate artificial intelligence (“AI”) solutions into their products, services and features, and may leverage AI, including generative AI, in their product development, operations, and their software programming more quickly or more successfully than us and there can be no assurance that the usage of AI will enhance our products or services or be beneficial to our business, which could impair our ability to compete effectively and adversely affect our results of operations.

Southeast Asia is at an early stage of the introduction of a digital property agency business model which involves end-to-end ownership of the property seeker lifecycle. Under this business model, property seekers discover listings on the digital platform and are then introduced to agents employed by the same company which maintains the digital listing. These agents help the seekers buy their homes. This business model is still achieving maturity in markets such as the United Kingdom and the United States. Our Priority Markets are seeing the very first early-stage digital agencies testing the viability of this business model. Although at present many of these digital agencies still rely on our online marketplaces to drive traffic and awareness to their leads, there is a risk that other emerging business models may become more popular and supplant our digital marketplaces.

Furthermore, large companies with strong brand awareness in international markets or global search engines and social media sites may decide to enter the real estate market and start advertising property on their existing or new platforms, which could increase competition in our Priority Markets and may have a materially adverse effect on our business. These companies could devote greater technical and other resources than we have available, have a more accelerated time frame for deployment and leverage their existing user bases and proprietary technologies to provide products and services that consumers might view as superior to our offerings. Any of our future or existing competitors may introduce different solutions that attract consumers or provide solutions similar to our own but with better branding or marketing resources or cross-subsidize and lower their advertising rates. If we are unable to continue to grow the number of consumers who use our websites and mobile applications, our business, financial condition and results of operations could be adversely affected.

We compete to attract customers with media sites, including but not limited to other companies that operate digital property classifieds marketplaces in our Priority Markets and agent and property developer websites. We also compete for a share of advertisers’ overall marketing budgets with traditional media such as television, magazines, newspapers and home/apartment guide publications. To compete successfully for customers against future and existing competitors, we must continue to invest resources in developing our advertising platform and proving the effectiveness and relevance of our advertising products and services. New business models frequently emerge in our industry and may require us to modify our own business model or offerings in order to continue to compete effectively. For example, we may in the future face new competition from digital companies that use data to buy properties instantly from sellers, renovate/repair and then re-sell the property online at a profit. Additionally, competitors may drive traffic away from our platform and increase their market share through aggressive or high-spend marketing campaigns, or prolonged price discounting. We rely on our strong market position and healthy traffic to our platform to capture valuable market data that we use to monetize our business and develop our offerings and data software. Any failure by us to compete effectively could adversely impact our business, research and development and prospects.

We may fail to anticipate these movements and lose market share as a consequence, which may be difficult to regain quickly or at all. Pressure from competitors seeking to acquire a greater share of customers’ overall marketing budget could adversely affect our pricing and margins and lower our revenue and increase our marketing expenses. The actions of our competitors and new market entrants could also force us to undertake substantial investment in updating or improving our current technology platforms and product offering. There is no guarantee that we will be successful in developing new products and we

15

may not receive revenues from these investments for several years or at all, which may have an adverse effect on our business, financial condition and results of operations.

If we are unable to compete successfully against our existing or future competitors, our business, financial condition and results of operations could be adversely affected.

Our business is subject to legal and regulatory risks and changes in regulatory requirements and governmental policies that could have an adverse impact on our business and prospects.

Increased regulation, changes in existing regulation or increased government intervention in our industry may adversely affect our business, results of operations and financial condition. Focus areas of regulatory risks we are exposed to include, among others: (i) evolution of laws and regulations applicable to digital property marketplaces or online advertising in general, (ii) various forms of data regulation such as data privacy, data localization, data portability, cybersecurity and advertising or marketing, (iii) anti-trust and competition regulations, (iv) economic regulations such as price and supply regulation, (v) foreign ownership restrictions, (vi) artificial intelligence regulation and (vii) regulations regarding the provision of online services, including but not limited to with respect to the internet, mobile devices and e-commerce. For example, we and our agent and developer customers may be subject to stringent compliance requirements, including but not limited to privacy and security standards for handling data, which could impact the manner in which we provide our services. Further, regulators have imposed guidelines for use of cloud computing services that mandate specific controls to be located in a particular jurisdiction or require financial services enterprises to obtain regulatory approvals prior to outsourcing certain functions.

In addition, we may not be able to obtain all the licenses, permits and approvals that may be necessary to provide the products and services that we may seek to offer in the future. Relevant laws and regulations, as well as their interpretations, may be unclear or may evolve in certain jurisdictions. This can make it difficult for us to assess which licenses and approvals are necessary for our business, or the processes for obtaining such licenses in certain jurisdictions. For these reasons, we also cannot be certain that we will be able to maintain the licenses and approvals that we have previously obtained, or that once they expire, we will be able to renew them. We cannot be sure that our interpretations of the rules and their exemptions have been or will be consistent with those of the local regulators. As we expand our businesses, and in particular our mortgage brokerage business and our future Fintech and data services growth initiatives, we may be required to obtain new licenses and comply with additional laws and regulations in the markets in which we plan to operate.

Government and regulatory policies could also have a significant impact on real estate or credit markets and, in turn, our revenues. For example, the Singapore government has implemented various cooling measures since 2021 in an effort to moderate demand, regulate price increases and promote prudent borrowing in the face of rising interest rates, including raising Additional Buyer’s Stamp Duty and tightening loan-to-value limits on residential property purchases and the total debt servicing ratio threshold for property loans. In February 2022, the Singapore government announced changes to Singapore’s tax regime that included increases in property tax rates for certain residential properties in 2023 and 2024. In 2022, the State Bank of Vietnam required banks in Vietnam to take certain measures to control credit growth, including controlling loans for real estate, and. the Vietnamese government imposed more stringent conditions and requirements on the private placement of bonds, including enhanced disclosure requirements. Such measures significantly limited both consumers’ and developers’ access to credit, which has suppressed the real estate market in Vietnam. While the Vietnamese government has made efforts in 2023 to enhance credit accessibility, consumer confidence has remained low, which negatively impacted property demand and demand for our platform, products and services in 2023. In addition, the Ministry of Finance in Vietnam has approved the tax reform strategy for 2030, under which the government is expected to raise taxes on land and housing in Vietnam.

These policies, or any significant change in one or more of these policies in any of our Priority Markets could adversely impact real estate markets, which may reduce the demand for our platform and/or products and services and could adversely affect our business, financial condition and results of operations.

Our business, financial condition and results of operations could be adversely affected by global or regional health events, such as the COVID-19 pandemic, and related government, private sector and individual consumer responsive actions.

The COVID-19 pandemic, its broad impact and measures taken to contain or mitigate the pandemic have had significant negative effects on the global economy, employment levels, employee productivity, supply chains, and certain aspects of the residential real estate and financial markets. This, in turn, has had a negative impact on property seekers, our customers, demand for our existing and new products and services, profitability, access to credit and our ability to operate our business.

The occurrence or resurgence of global or regional health events, such as the COVID-19 pandemic, may cause governments to impose some or all prior or new restrictive measures with their consequential impact on economies and supply chains, which may adversely affect home buying, selling, renting, financing and shopping trends. As such, any continuing effects of, or prolonged reemergence from such global or regional health events could have a material adverse effect on our business, financial condition and results of operations.

In addition, our ability to fund our liquidity requirements and operate our business depends on our cash flows from operations and, in future, potentially our ability to access capital markets and borrow on credit facilities. Our access to and the availability of financing on acceptable terms may be adversely impacted by global or regional health events such as the COVID-19 pandemic. See also “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources.”

16

Regulations regarding environmental, social and governance (“ESG”) matters, including climate change may affect us by substantially increasing our costs and exposing us to potential liability.

We are, and may become, subject to ESG laws and regulations, which may affect aspects of our operations such as how we develop or operate our platforms and our presence in our Priority Markets, as well as require us to increase, or impact on,our reporting and compliance obligations with respect to ESG matters. Standards for tracking and reporting ESG matters continue to evolve. New laws, regulations, policies and international accords relating to ESG matters, including sustainability, climate change, human capital, human rights, value chains and diversity, are being developed and formalized in Europe, the United States, Asia and elsewhere, which may entail specific actions and/or disclosure requirements. Our processes and controls for reporting ESG matters across our operations and value chain are evolving along with multiple disparate standards for identifying, measuring and reporting ESG metrics, including ESG-related disclosures that may be required by the SEC and other regulators. Such standards may change over time, which could result in significant revisions being required to be made to our current goals, reported progress in achieving such goals and/or ability to achieve such goals in the future, as well as increased costs, internal controls, and oversight obligations. Any failure, or perceived failure, by us to comply fully with developing interpretations of ESG laws and regulations could harm our business, reputation, financial condition and operating results and require significant time and resources to make the necessary adjustments. If our ESG practices do not meet evolving investor or other stakeholder expectations and standards, then our reputation or our attractiveness as an investment, business partner, service provider or employer could be negatively impacted.

Developers and commercial and residential property builders who list their properties on our platforms may also become subject to more stringent requirements under such laws. It is unclear how these future developments and related matters will ultimately affect the regulated areas in which we may operate. While we cannot predict with certainty the extent to which developments in areas with stringent building requirements or legal restrictions or other ESG requirements that may become effective may affect us either directly or indirectly, they could require time-consuming and costly compliance programs or result in significant expenditures, which could lead to delays and increased operating costs. Our failure to comply with ESG laws could result in fines, penalties, restoration obligations, revocation of permits, and other sanctions.

In addition, there is a variety of legislation being enacted, or considered for enactment, specifically relating to energy and climate change matters. This legislation relates to items such as carbon dioxide emissions control and building codes that impose energy efficiency standards. New building code requirements that impose stricter energy efficiency standards could significantly increase the cost to construct commercial and residential properties, which could adversely affect the property market. As climate change concerns continue to grow, legislation and regulations of this nature are expected to continue and become more costly to comply with. In addition, it is possible that some form of expanded energy efficiency legislation may be passed, which may, despite being phased in over time, significantly increase the costs of building commercial and residential properties and the sale price to buyers and adversely affect our listing volumes.

We are subject to a series of risks related to climate change.

There are inherent climate-related risks wherever business is conducted. Certain of our facilities, as well as our and third-party infrastructure on which we rely, are located in areas that have experienced, and are projected to continue to experience, various meteorological phenomena (such as drought, heatwaves, wildfire, storms, and flooding, among others) or other catastrophic events that may disrupt our or our suppliers’ operations, require us to incur additional operating or capital expenditures, or otherwise adversely impact our business, financial condition, or results of operations. Climate change may increase the frequency and/or intensity of such events. Climate change may also contribute to various chronic changes in the physical environment, such as sea-level rise or changes in ambient temperature or precipitation patterns, which may also adversely impact our or our suppliers’ operations. While we may take various actions to mitigate our business risks associated with climate change, this may require us to incur substantial costs and may not be successful, due to, among other things, the uncertainty associated with the longer-term projections associated with managing climate risk. For example, to the extent catastrophic events become more frequent, it may adversely impact the availability or cost of insurance.

Additionally, we expect to be subject to risks associated with societal efforts to mitigate or otherwise respond to climate change, including but not limited to increased regulations, evolving stakeholder expectations, and changes in market demand. For more information, see “—Increased attention to, and evolving expectations for, ESG initiatives could increase our costs, harm our reputation, or otherwise adversely impact our business.” Changing market dynamics, global and domestic policy developments, and the increasing frequency and impact of meteorological phenomena have the potential to disrupt our business, the business of our suppliers and/or customers, or otherwise adversely impact our business, financial condition, or results of operations.

Increased attention to, and evolving expectations for, ESG initiatives could increase our costs, harm our reputation, or otherwise adversely impact our business.

Companies across industries are facing increasing scrutiny from a variety of stakeholders related to their ESG and sustainability practices. Expectations regarding mandatory and voluntary ESG initiatives and disclosures and consumer demand for alternative forms of energy may result in increased costs (including but not limited to increased costs related to compliance, stakeholder engagement, contracting and insurance), changes in demand for certain products, enhanced compliance or disclosure obligations, or other adverse impacts to our business, financial condition, or results of operations.

17

While we may at times engage in voluntary initiatives (such as voluntary disclosures, certifications, or goals, among others) to develop the ESG profile of our company or to respond to specific or general stakeholder expectations, such initiatives may be costly and may not have the desired effect. Expectations around our company’s management of ESG matters continues to evolve rapidly, in many instances due to factors that are out of our control. Such initiatives may also not be cost effective in achieving their goals and may not be considered to achieve return on the investment. For example, we may ultimately be unable to complete certain initiatives or targets, either on the timelines initially announced or at all, due to technological, cost, or other constraints, which may be within or outside of our control. Moreover, actions or statements that we may take based on expectations, assumptions, or third-party information that we currently believe to be reasonable may subsequently be determined to be erroneous or be subject to misinterpretation. If we fail to, or are perceived to fail to, comply with or advance certain ESG initiatives or goals (including the timeline and manner in which we complete such initiatives or achieve such goals), we may be subject to various adverse impacts, including reputational damage and potential stakeholder engagement and/or litigation, even if such initiatives or goals are voluntary. For example, there have been increasing allegations of greenwashing against companies making significant ESG claims due to a variety of perceived deficiencies in performance or methodology, including as stakeholder perceptions of sustainability continue to evolve. Simultaneously, there are efforts by some stakeholders to reduce companies’ efforts on certain ESG-related matters. Both advocates and opponents to certain ESG matters are increasingly resorting to a range of activism forms, including media campaigns and litigation, to advance their perspectives. To the extent we are subject to such activism, it may require us to incur costs or otherwise adversely impact our business.

Certain market participants, including major institutional investors and capital providers, use third-party benchmarks and scores to assess companies’ ESG profiles in making investment or voting decisions. Unfavorable ESG ratings could lead to increased negative investor sentiment towards us, which could negatively impact our share price as well as our access to and cost of capital. To the extent ESG matters negatively impact our reputation, it may also impede our ability to compete as effectively to attract and retain employees or customers, which may adversely impact our operations. In addition, we expect there will likely be increasing levels of regulation, disclosure-related and otherwise, with respect to ESG matters. For example, on March 6, 2024, the SEC adopted final rules to enhance and standardize climate-related disclosures by requiring registrants to disclose certain climate-related information in registration statements and annual reports. The final rules will become effective 60 days following publication of the adopting release in the Federal Register. The final rules are subject to litigation in the U.S., and the outcome of this litigation is currently unknown. As an accelerated filer, if the rules become effective and are not overturned, we will be required to provide the enhanced climate-related disclosures in our annual report for the year ending December 31, 2026. Compliance with these new rules may require us to incur significant additional costs to comply, including the implementation of significant additional internal controls, processes and procedures regarding matters that have not been subject to such controls in the past, and impose increased oversight obligations on our management and board of directors. For more information please also see “—Regulations regarding environmental matters and climate change may affect us by substantially increasing our costs and exposing us to potential liability.” This increase in the quantity and detail of ESG information that is subject to mandatory disclosure requirements, combined with developing stakeholder expectations will likely lead to increased costs as well as scrutiny that could heighten all of the risks identified in this risk factor. Additionally, many of our suppliers, business partners and others in our value chain may be subject to similar expectations, which may augment or create additional risks, including risks that may not be known to us.

Our ability to attract, train and retain executives and other qualified employees is critical to our business, results of operations and future growth.

Our business depends on successfully hiring and retaining key employees in senior management, sales and marketing and information technology. We require highly qualified and skilled employees, including but not limited to country managers, to generate revenue and maintain customer relationships with real estate agents and developers, along with computer programmers, software engineers and data technicians (who are in high demand by technology companies operating in Southeast Asia) to develop new products and maintain and enhance existing ones.

Competition for qualified employees in our industry has become more intense in recent years, particularly due to inflationary pressures. We have placed heightened focus to the retention of and career planning for key technology personnel due to the highly competitive employment market across our Priority Markets, especially in Singapore. If we are unable to retain or attract high quality employees required for our business activities, address the loss of any key personnel, or are required to materially increase the amount we offer in remuneration to secure the employment of key personnel, our operating and financial performance could be adversely affected.

We depend on our agents business for a significant portion of our revenue.

In the past we have derived and we believe that we will continue to derive a significant portion of our revenue from our agents business across Southeast Asia and, in particular, in Singapore. In 2023, agent revenue accounted for 81.2% of our revenue, and 65.9% of our agent revenue was generated from Singapore. In 2022, agent revenue accounted for 79.7% of our revenue, and 57.0% of our agent revenue was generated from Singapore. In 2021, agent revenue accounted for 76.4% of our revenue, and 60.3% of our agent revenue was generated from Singapore. Adverse developments affecting business activity in Singapore or our agents business may have a material adverse effect on our business, financial condition and results of operations. There can be no assurance that we will be able to sustain the number of agents and digital property listings necessary to maintain

18

and grow our agents business in Singapore or in general. Furthermore, there can be no assurance that we will succeed in expanding our agents business outside of Singapore or in growing our developers, Fintech and data services.

Our operations and investments are located in Southeast Asia and we are therefore exposed to various risks inherent in operating and investing in the region.