UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

OR

For the Fiscal Year Ended

OR

For the transition period from __________ to ___________

OR

Date of event requiring this shell company report ______________

Commission file number

| (Exact name of Registrant as specified in its charter) |

| Not Applicable |

| (Translation of Registrant’s name into English) |

| Grand Duchy of |

| (Jurisdiction of incorporation or organization) |

Grand Duchy of R.C.S. Luxembourg: B253360 Tel : + Email: |

| (Name, Telephone, E-mail and/or Facsimile number and Address Company Contact Person) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange in which registered | ||

| The | ||||

| The |

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

23,375,000 Warrants to purchase Ordinary Shares, as of December 31, 2022

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Non-accelerated filer ☐ | |

| Emerging growth company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange

Act.

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ | as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check

mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes

TABLE OF CONTENTS

i

FREQUENTLY USED TERMS

In this Annual Report:

“1915 Law” means the Luxembourg law of August 10, 1915 on commercial companies, as amended.

“Adjusted EBITDA” means EBITDA further adjusted to exclude certain isolated costs incurred as a result of the COVID-19 pandemic, certain transaction costs incurred in connection with the Business Combination, certain listing expenses incurred in connection with the Business Combination, certain costs related to business transformation initiatives, certain foreign currency translation adjustments, and certain other finance costs and other nonrecurring, nonoperational or unordinary items as the Company may deem appropriate from time to time.

“Annual Report” means this annual report on Form 20-F for the fiscal year ended December 31, 2022.

“Board of Directors” means the board of directors of the Company.

“Business Combination” means the transactions consummated pursuant to the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of March 31, 2021, as amended on September 29, 2021, by and among Union, Crynssen, the Company and Merger Sub.

“Closing” means the consummation of the Business Combination.

“Closing Date” means September 29, 2021.

“Code” means the Internal Revenue Code of 1986, as amended.

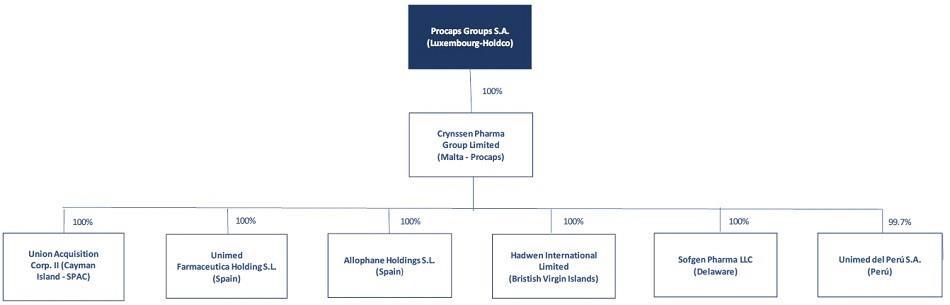

“Company” means Procaps Group, S.A., a public limited liability company (société anonyme) governed by the laws of the Grand Duchy of Luxembourg, having its registered office at 9, rue de Bitbourg, L-1273 Luxembourg, Grand Duchy of Luxembourg, and registered with the Luxembourg Trade and Companies’ Register (Registre de Commerce et des Sociétés, Luxembourg) under number B 253360.

“COVID-19” means the novel coronavirus known as SARS-CoV-2 or COVID-19, and any evolutions, mutations thereof or related or associated epidemics, pandemic or disease outbreaks.

“Crynssen” means Crynssen Pharma Group Limited, a private limited liability company registered and incorporated under the laws of Malta and, particularly, the Companies Act Cap. 386 with company registration number C 59671.

“Crynssen Ordinary Shares” means ordinary shares of Crynssen, with a nominal value of $1.00 per share.

“Crynssen Shareholders” means the shareholders of Crynssen prior to the consummation of the Business Combination.

“Deseja” means the Deseja Trust, a trust organized under the laws of the State of Delaware and a Crynssen Shareholder.

“EBITDA” means profit (loss) for the year before interest expense, net, income tax expense and depreciation and amortization.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“FDA” means the United States Food and Drug Administration.

“GAAP” means generally accepted accounting principles in the United States of America.

ii

“IASB” means the International Accounting Standards Board.

“IFC” means the International Finance Corporation, an international organization established by Articles of Agreement among its member countries, and a Crynssen Shareholder.

“IFC Redemption Agreement” means that certain Share Redemption Agreement entered into by and between the Company and IFC on March 31, 2021, and subsequently amended on September 29, 2021, pursuant to which the Company agreed to redeem 4,500,000 Redeemable B Shares from IFC for a total purchase price of $45,000,000 in accordance with the terms thereunder.

“IFRS” means the International Financial Reporting Standards, as issued by the IASB.

“IPO” means Union’s initial public offering of units, consummated on October 22, 2019.

“INVIMA” means the Colombian Instituto Nacional de Vigilancia de Medicamentos y Alimentos (National Food and Drug Surveillance Institute).

“JOBS Act” means the U.S. Jumpstart Our Business Startups Act of 2012, as amended.

“Merger” means the merging of Merger Sub with and into Union pursuant to the laws of the Cayman Islands, with Union surviving the Merger as a wholly owned subsidiary of the Company.

“Merger Effective Time” means the time at which the merger certificate was filed on September 29, 2021.

“Merger Sub” means OZLEM Limited, an exempted company incorporated under the laws of the Cayman Islands with registration number 373625.

“Nasdaq” means The Nasdaq Stock Market LLC.

“Nomination Agreement” means that certain nomination agreement by and among the Company, certain Crynssen Shareholders and the Sponsors dated September 29, 2021.

“Ordinary Shares” means the ordinary shares of the Company, nominal value $0.01 per share.

“PIPE” means the private placement pursuant to which the PIPE Investors purchased 10,000,000 SPAC Ordinary Shares, for a purchase price of $10.00 per share, which were converted into Ordinary Shares in connection with the Closing.

“PIPE Investors” means persons that entered into Subscription Agreements with the SPAC to purchase SPAC Ordinary Shares which were subsequently converted into Ordinary Shares in connection with the consummation of the Business Combination on the Closing Date.

“Redeemable A Shares” means the redeemable A shares of the Company, nominal value $0.01 per share.

“Redeemable B Shares” means the redeemable B shares of the Company, nominal value $0.01 per share.

“Registration Rights and Lock-Up Agreement” means that certain registration rights and lock-up agreement entered into on September 29, 2021 by and among the Company, the Sponsors, certain other shareholders of Union and the Crynssen Shareholders.

“SEC” means the U.S. Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Simphony” means the Simphony Trust, a trust organized under the laws of the State of Delaware and a Crynssen Shareholder.

iii

“Sognatore” means the Sognatore Trust, a trust organized under the laws of New Zealand and a Crynssen Shareholder.

“SPAC” or “Union” means Union Acquisition Corp. II, a Cayman Islands exempted company limited by shares with registration number 345887.

“SPAC Ordinary Shares” means the ordinary shares of Union, par value $0.0001 per share.

“SPAC Warrants” means warrants to purchase SPAC Ordinary Shares as contemplated under the Warrant Agreement, with each warrant exercisable for the number of SPAC Ordinary Shares stated in the applicable SPAC Warrant at an exercise price per SPAC Ordinary Share of $11.50.

“Sponsors” means Union Group International Holdings Limited and Union Acquisition Associates II, LLC.

“Subscription Agreements” means the subscription agreements entered into by Union and a number of qualified institutional buyers and institutional and individual accredited investors, in connection with the execution of the Business Combination Agreement, pursuant to which such investors agreed to purchase, and Union agreed to sell to such investors, an aggregate of 10,000,000 SPAC Ordinary Shares for a purchase price of $10.00 per share and an aggregate purchase price of $100,000,000, which SPAC Ordinary Shares were automatically converted into Ordinary Shares upon Closing.

“Transaction Support Agreement” means the Transaction Support Agreement, dated as of March 31, 2021, by and among Union, Crynssen, the Company, certain Crynssen Shareholders, the Sponsors, certain other shareholders of Union prior to the Closing of the Business Combination and certain officers and directors of Union, as amended, modified or supplemented from time to time.

“Warrant Amendment” means that certain Assignment, Assumption and Amendment Agreement entered into on September 29, 2021 by the Company, Union and Continental Stock Transfer & Trust Company as warrant agent.

“Warrant Agreement” means the warrant agreement, dated October 17, 2019, by and between Union and Continental Stock Transfer & Trust Company, as warrant agent, governing Union’s warrants.

“Warrants” mean the former warrants of Union converted at the Merger Effective Time into a right to acquire one Ordinary Share on substantially the same terms as were in effect immediately prior to the Merger Effective Time under the terms of the Warrant Agreement, which was assigned to and assumed by the Company pursuant to the Warrant Amendment.

iv

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements about our expectations, beliefs and intentions regarding, among other things, our products and services, development efforts, business, financial condition, results of operations, strategies, plans and prospects. Forward-looking statements can be identified by the use of forward-looking words such as “believe,” “expect,” “intend,” “plan,” “may,” “should,” “could,” “might,” “seek,” “target,” “will,” “project,” “forecast,” “continue” or “anticipate” or their negatives or variations of these words or other comparable words or by the fact that these statements do not relate strictly to historical matters. Forward-looking statements relate to anticipated or expected events, activities, trends or results as of the date they are made. Because forward-looking statements relate to matters that have not yet occurred, these statements are inherently subject to risks and uncertainties that could cause our actual results to differ materially from any future results expressed or implied by the forward-looking statements. Many factors could cause our actual activities or results to differ materially from the activities and results anticipated in forward-looking statements, including, but not limited to, the factors listed below:

| ● | the financial performance of Procaps following the Business Combination; |

| ● | changes to our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects and plans; |

| ● | our ability to develop and launch new products and services; |

| ● | our ability to successfully and efficiently integrate future acquisitions or execute on dispositions; |

| ● | the availability of raw materials used in our products and our ability to source such raw materials, or find adequate substitutes, in a cost-effective manner; |

| ● | our product development timeline and estimated research and development (“R&D”) costs; |

| ● | developments and projections relating to our competitors and industry; |

| ● | our expectations regarding our ability to obtain and maintain intellectual property protection and not infringe on the rights of others; |

| ● | the impact of the COVID-19 pandemic on our business; |

| ● | changes in applicable laws or regulations; and |

| ● | the outcome of any known and unknown litigation and regulatory proceedings. |

We believe these forward-looking statements are reasonable; however, these statements speak only as of the date of this Annual Report and are subject to known and unknown risks, uncertainties and other factors that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from those anticipated by the forward-looking statements. We discuss these risks in this Annual Report in greater detail under Item 3.D. “Risk Factors.” Given these uncertainties, you should not rely upon forward-looking statements as predictions of future events.

Unless required by law, we undertake no obligation to update or revise any forward-looking statement, whether as a result of new information, future events or developments or otherwise.

v

As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include:

| ● | changes in applicable laws or regulations; | |

| ● | any identified material weaknesses in our internal control over financial reporting which, if not corrected, could adversely affect the reliability of our financial reporting; |

| ● | the effects of the COVID-19 pandemic on our business; | |

| ● | the ability to implement business plans, forecasts, and other expectations after the completion of any future acquisition, and identify and realize additional opportunities; |

| ● | the risk of failure or delay in the development of new pharmaceutical products and the costs involved; | |

| ● | the risk that delays in regulatory reviews and approvals of new products could delay our ability to market such products, and that post-approval requirements, including additional clinical trials, could result in increased costs; | |

| ● | the risk associated with the markets and countries in which we operate, including, Colombia, El Salvador and Brazil; | |

| ● | our ability to identify and materialize acquisition opportunities; | |

| ● | the risk associated with fluctuations in the costs, availability, and suitability of the components of the products we manufacture, including active pharmaceutical ingredients, excipients, purchased components, and raw materials; | |

| ● | failure to comply with existing or future regulatory requirements, standards and ethical expectations, including environmental, tax, labor, anticorruption, health and safety regulations; | |

| ● | the risk associated with global supply chain crisis could interfere with the operations of certain of our direct or indirect suppliers; | |

| ● | our ability to adequately enhance our products and services or introduce new technology; | |

| ● | the risk of a change in demand for our products and services, consumer preferences and the possibility of rapid technological change in the highly competitive industry in which we operate; | |

| ● | the risk associated with the loss of, or failure to attract and retain, our key employees and specialized sales representatives; |

vi

| ● | the risk that changes to price control regulations could negatively affect our margins and its ability to pass on cost increases to our customers; | |

| ● | the dependency of our integral contract development and manufacturing organization services on customer’s research and success of their products; |

| ● | the risks associated with the effect of our products on our customers and potential exposure to product and other liability risks; | |

| ● | the risk of disruption at any of our manufacturing facilities or disruption of the relationship with our key customers; | |

| ● | the risks associated with exchange rate volatility of the currencies in which we do business; | |

| ● | the risk of any breach, disruption or misuse of our, or our external business partners’, information systems or cyber security efforts; | |

| ● | the risk of changes in market access or healthcare reimbursement for, or public sentiment towards our, or our customers’, products, or other changes in applicable policies regarding the healthcare industry; | |

| ● | the risk that we or our customers are unable to secure or protect our respective intellectual property or that we or our customers may infringe on the intellectual property rights of others; | |

| ● | the loss of customers’ confidence in the integrity of pharmaceutical products due to illegal trade; | |

| ● | the possibility that we may be adversely affected by other economic, business, and/or competitive factors; and | |

| ● | other risks and uncertainties described in this Annual Report, including those under the heading “Risk Factors” in Item 3.D of this Annual Report. |

vii

SUMMARY OF MATERIAL RISKS ASSOCIATED WITH OUR BUSINESS

Our business is subject to numerous risks and uncertainties, including those described in “Item 3.D—Key Information—Risk Factors” in this Annual Report. You should carefully consider these risks and uncertainties when investing in our Ordinary Shares. The principal risks and uncertainties affecting our business include the following:

| ● | The development of new pharmaceutical products is a complex, risky and lengthy process involving significant financial, research and development and other resources, which may be delayed due to various factors. Such delays can result in increased costs or the emergence of competing products, which may have a material adverse effect on Procaps’ business, financial condition and results of operations. |

| ● | Procaps is subject to strict controls on the commercialization processes for its pharmaceutical products, including their development, manufacture, distribution and marketing, which vary by country and by region. Any delays in regulatory reviews or approvals could delay Procaps’ ability to market our products, which could have a material adverse effect on its business, financial condition and results of operations. |

| ● | Procaps’ future results of operations are subject to fluctuations in the costs, availability, and suitability of the components of the products it manufactures, including active pharmaceutical ingredients, excipients, purchased components, and raw materials. In addition, the COVID-19 pandemic may interfere with the operations of certain of Procaps’ direct or indirect suppliers or with international trade for these supplies, which could raise Procaps’ costs or reduce the productivity or slow the timing of its operations, which could have a material adverse effect on its business, financial condition and results of operations, |

| ● | A disruption at any of Procaps’ main manufacturing facilities could materially and adversely affect its business, financial condition and results of operations. |

| ● | Procaps’ independent registered public accounting firm has included an explanatory paragraph relating to Procaps’ ability to continue as a going concern in its report on Procaps’ Annual Audited Consolidated Financial Statements included elsewhere in this Annual Report. |

| ● | Procaps has identified a material weakness in its internal control over financial reporting. If Procaps is unable to develop and maintain an effective system of internal control over financial reporting, it may not be able to accurately report its financial results in a timely manner, which may adversely affect investor confidence in Procaps and materially and adversely affect its business and results of operations. |

| ● | Procaps is an international company with operations primarily in Latin America and is subject to the market risks of the countries in which it manufactures and/or sells its products, and to risks associated with foreign exchange rates. |

| ● | If Procaps does not enhance its existing products and services, or introduce new technology or service offerings in a timely manner, its products and services may become uncompetitive over time, or customers may not buy its products or buy less of them, which could have a material adverse effect on Procaps’ business, financial condition and results of operations. |

| ● | The demand for OTC products may be impacted by changes in consumer preferences. If Procaps is unable to adapt to these changes, it may lose market share and its net sales may be negatively impacted, which could have a material adverse effect on Procaps’ business, financial condition and results of operations. |

| ● | Procaps’ business depends upon certain customers for a significant portion of its sales, therefore, a disruption of Procaps’ relationship with these customers or any material adverse change in these customers’ businesses could have a material adverse effect on Procaps’ business, financial condition and results of operations. |

| ● | Procaps depends on key personnel to operate and grow its business and to develop new and enhanced offerings and technologies and the loss of, or the failure to attract and retain, such key personnel could adversely affect its operations. |

| ● | Procaps may be unable to identify acquisition opportunities and successfully execute and close acquisitions, which could limit its potential for growth. |

| ● | Procaps may not be able to realize the benefits of business acquisitions and divestitures it enters into, including being unable to successfully and efficiently integrate acquisitions or execute on dispositions, which could have a material adverse effect on its business, financial condition and results of operations. |

| ● | The demand for Procaps’ iCDMO services depends in part on its customers’ research and development and the clinical and market success of their products. In the event Procaps’ customers spend less on, or are less successful in, these activities for any reason, including as a result of decrease in spending due to the COVID-19 pandemic or recessionary economic conditions caused in whole or in part by the pandemic, Procaps’ business, financial condition, and results of operations may be materially adversely affected. |

viii

| ● | Procaps participates in a highly competitive market, and increased competition may adversely affect its business, financial condition and results of operations. |

| ● | Changes in market access or healthcare reimbursement for, or public sentiment towards Procaps, or its customers’, products in Latin America, the United States and other countries in which Procaps operates, or other changes in applicable policies regarding the healthcare industry, could adversely affect Procaps’ financial condition and results of operations by affecting demand for Procaps’ products and services. |

| ● | The illegal trade in pharmaceutical products, including counterfeiting, theft and illegal diversion, is widely recognized. Public loss of confidence in the integrity of pharmaceutical products as a result of illegal trade could materially adversely affect Procaps’ reputation, financial condition and results of operation. |

| ● | Procaps and its customers depend on patents, copyrights, trademarks, know-how, trade secrets, and other forms of intellectual property protections, but these protections may not be adequate. |

| ● | Procaps’ products and services, or its customers’ products, may infringe on the intellectual property rights of third parties and any such infringement could have a material adverse effect on Procaps’ business. |

| ● | A significant portion of medication on the market, including Procaps’, is subject to price control regulations. This control may limit Procaps’ margins and its ability to pass on cost increases to its customers, which could have a material adverse effect on Procaps’ business, financial condition and results of operations. |

| ● | Procaps may be held liable if a consumer has an adverse health reaction to a product it sells or manufactures. |

| ● | Procaps is subject to product and other liability risks that could exceed its anticipated costs or adversely affect its results of operations, financial condition, liquidity, and cash flows. |

| ● | Failure to comply with existing and future regulatory requirements could adversely affect Procaps’ business, financial condition and results of operations, or result in claims from customers. |

| ● | Procaps’ global operations are subject to economic, political, and regulatory risks, including the risks of changing regulatory standards or changing interpretations of existing standards that could affect its financial condition and results of operation or require costly changes to its business. |

| ● | Procaps is subject to governmental export and import controls that could impair its ability to compete in international markets and subject it to liability if Procaps is not in compliance with applicable laws. |

ix

CERTAIN CONVENTIONS

The Company was incorporated under the laws of the Grand Duchy of Luxembourg on March 29, 2021. The Company owns no material assets other than its direct ownership of the issued share capital in Crynssen, a private limited liability company registered and incorporated under the laws of Malta. Except where the context otherwise requires or where otherwise indicated, all references to “Procaps,” “we,” “us” and “our” refer to the Company and its consolidated subsidiaries, as well as those businesses we account for using the equity method.

Trademarks and Trade Names

This Annual Report contains references to our trademarks and to trademarks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this Annual Report, including logos, artwork and other visual displays may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend our use or display of other companies’ trade name or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

CURRENCY PRESENTATION

In this Annual Report, unless otherwise specified or the context otherwise requires:

| ● | “U.S.$”, “$” and “U.S. dollar” each refers to the United States dollar; |

| ● | “COP” and “Colombian Peso” refers to the Colombian peso, the lawful currency of Colombia; and |

| ● | “Reais”, “R$” and “Brazilian Real” refers to the Brazilian real, the lawful currency of Brazil. |

We have translated some of the local currency amounts contained in this Annual Report into U.S. dollars for convenience purposes only. The U.S. dollar-equivalent information presented in this Annual Report is provided solely for convenience and should not be construed as implying that the amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate.

Certain numbers and percentages included in this Annual Report have been subject to rounding adjustments. Accordingly, figures shown for the same category presented in various tables or other sections of this Annual Report may vary slightly, and figures shown as totals in certain tables may not be the arithmetic aggregation of the figures that precede them.

PRESENTATION OF FINANCIAL INFORMATION

This Annual Report contains the annual audited consolidated financial statements of Procaps Group, S.A. as of December 31, 2022 and 2021, and for the years ended December 31, 2022, 2021 and 2020 (the “Annual Audited Consolidated Financial Statements”).

The Annual Audited Consolidated Financial Statements have been prepared in accordance with the IFRS as issued by the IASB and in its presentation currency of the U.S. dollar.

Our Annual Audited Consolidated Financial Statements are presented in U.S. dollars. Our fiscal year ends on December 31 of each year. Accordingly, all references to a particular year are to the year ended December 31 of that year.

Non-IFRS Information

Our management uses certain non-IFRS financial information to assess our operating performance across periods and for business planning purposes. We believe the presentation of these non-IFRS financial measures is useful to investors as it provides additional information to facilitate comparisons of historical operating results, identify trends in our underlying operating results and provide additional insight and transparency on how we evaluate our business.

We use non-IFRS financial measures to budget, make operating and strategic decisions, and evaluate our performance. Below is a description of the non-IFRS financial measures we have used in this Annual Report, including any adjustments to the IFRS financial measures derived therefrom. We believe the non-IFRS measures should always be considered along with the related IFRS financial measures. We have provided the reconciliations between the IFRS and non-IFRS financial measures in Item 5.A. of this Annual Report under the heading “Operating and Financial Review and Prospects—Operating Results––Non-IFRS Financial Measures.”

x

The primary non-IFRS financial measures utilized by our management is described below and reflects how we evaluate our current and prior-year operating results. As new events or circumstances arise, our management may alter the definitions of such measures to better reflect our financial performance or adopt new measures in the future. In the event any of these definitions change, or if new non-IFRS financial measures are adopted by our management, we will provide the updated definitions and present the related non-IFRS historical results on a comparable basis.

Use of Constant Currency

As exchange rates are an important factor in understanding period-to-period comparisons, we believe the presentation of certain financial metrics and results on a constant currency basis in addition to the IFRS reported results helps improve investors’ ability to understand our operating results and evaluate our performance in comparison to prior periods. Constant currency information is non-IFRS financial information that compares results between periods as if exchange rates had remained constant period-over-period. We use results on a constant currency basis as one measure to evaluate our performance. We currently present revenue, cost of sales, gross profit, sales and marketing expenses, administrative expenses, Contribution Margin and Adjusted EBITDA on a constant currency basis. We calculate constant currency by calculating year-end period results using prior-period foreign currency exchange rates. We generally refer to such amounts calculated on a constant currency basis as excluding the impact of foreign exchange. These results should be considered in addition to, not as a substitute for, results reported in accordance with IFRS. Results on a constant currency basis, as we present them, may not be comparable to similarly titled measures used by other companies and are not measures of performance presented in accordance with IFRS.

For more information, see the discussion on constant currency in Item 5.A of this Annual Report under the heading “Operating and Financial Review and Prospects—Operating Results––Non-IFRS Financial Measures––Use of Constant Currency.”

EBITDA, Adjusted EBITDA, and Adjusted EBITDA Margin

We define EBITDA as profit (loss) for the year before interest expense, net, income tax expense and depreciation and amortization. We define Adjusted EBITDA as EBITDA further adjusted to exclude certain isolated costs incurred as a result of the COVID-19 pandemic, certain transaction costs incurred in connection with the Business Combination, certain listing expenses incurred in connection with the Business Combination, certain costs related to business transformation initiatives, certain foreign currency translation adjustments, and certain other finance costs and other nonrecurring, nonoperational or unordinary items as the Company may deem appropriate from time to time. Adjusted EBITDA is one of the key performance indicators we use in evaluating our operating performance and in making financial, operating, and planning decisions. We believe EBITDA and Adjusted EBITDA are useful to investors in evaluating our operating performance compared to other companies in the pharmaceutical industry, as similar measures are commonly used by companies in this industry. We also report Adjusted EBITDA as a percentage of revenue as an additional measure so investors may evaluate our Adjusted EBITDA margins on revenue.

For more information and a reconciliation of profit (loss) for the year to EBITDA, Adjusted EBITDA and Adjusted EBITDA margin, see Item 5.A of this Annual Report under the heading “Operating and Financial Review and Prospects—Operating Results––Non-IFRS Financial Measures––EBITDA, Adjusted EBITDA, and Adjusted EBITDA Margin.”

Contribution Margin

We define Contribution Margin as gross profit less selling expenses. Contribution Margin is one of the key performance indicators we use in evaluating our profitability. We believe Contribution Margin is useful to investors in evaluating our operating performance compared to other companies in the pharmaceutical industry, as similar measures are commonly used by companies in this industry.

For more information and a reconciliation of gross profit to Contribution Margin, see Item 5.A of this Annual Report under the heading “Operating and Financial Review and Prospects—Operating Results––Non-IFRS Financial Measures–– Contribution Margin.”

PRESENTATION OF INDUSTRY AND MARKET DATA

In this Annual Report, we rely on, and refer to, information regarding our business and the markets in which we operate and compete. The market data and certain economic and industry data and forecasts used in this Annual Report were obtained from internal surveys, market research, governmental and other publicly available information and independent industry publications. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. We believe that these industry publications, surveys and forecasts are reliable, but we have not independently verified them and cannot guarantee their accuracy or completeness.

Certain market share information and other statements presented herein regarding our position relative to our competitors are not based on published statistical data or information obtained from independent third parties, but reflects our best estimates. We have based these estimates upon information obtained from publicly available information from our competitors in the industry in which we operate.

xi

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. Reserved

B. CAPITALIZATION AND INDEBTEDNESS

Not applicable.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

D. RISK FACTORS

You should carefully consider the risks and uncertainties described below, together with the other information contained in this Annual Report, before making any investment decision. Any of the following risks and uncertainties could have a material adverse effect on our business, prospects, results of operations and financial condition. The market price of our Ordinary Shares and Warrants could decline due to any of these risks and uncertainties, and you could lose all or part of your investment. The risks described below are those that we currently believe may materially affect us.

Risks Related to Product Development and Manufacturing

The development of new pharmaceutical products is a complex, risky and lengthy process involving significant financial, research and development and other resources, which may be delayed due to various factors. Such delays can result in increased costs or the emergence of competing products, which may have a material adverse effect on our business, financial condition and results of operations.

We develop advanced pharmaceutical oral delivery systems technologies primarily in the form of soft gelatin capsules (“Softgel”) that are used in the manufacturing of prescription pharmaceutical drugs (“Rx”) and over the counter (“OTC”) pharmaceutical products, as well as high-complexity drugs for hospital use, personal protective equipment, immunosuppressant, oncology and analgesics products and syringes, among other products. The development of new pharmaceutical products, including our advanced oral delivery systems, is a complex, inherently risky and lengthy process involving significant financial, R&D and other resources, and may not result in a commercially viable product. We must successfully develop, test, manufacture and launch our products as well as successfully register our products in each relevant jurisdiction, in advance of our competitors. A project may be delayed at any stage of the process due to various factors, including failure to obtain the required regulatory approvals for the product being developed or for its manufacturing facilities in a timely manner. Our products currently under development, if and when fully developed and tested, may not perform as we expect, or competitors may already occupy the market opportunity.

Decisions on the launch of a new oral delivery system and the timing of such launches are primarily driven by our R&D development team. Once the development of the product is completed and the results and appropriate documentation is submitted to the applicable health authority, investments made in the manufacture of pre-launch product, marketing materials and sales force training, may result in additional expenses if the product is not approved in a timely manner. Additionally, other factors such as price negotiation, large-scale natural disasters or global pandemics, and competitor activity may significantly delay the launch of a new product.

1

All of our products must meet and continue to comply with regulatory and safety standards and receive regulatory approvals in each of the markets in which they are to be commercialized. If health or safety concerns arise with respect to a product, we may be forced to withdraw it from the market and could face legal action if any harm came from the use of our products.

Significant delays in the development and anticipated launch dates of new products could hinder our achievement of development targets, adversely affect the reputation of our R&D capabilities, allow our competitors to bring competing products to the market before we do, significantly reduce the return on costs incurred in preparing for the launch of seasonal products that are launched off-season, and result in increased costs if marketing and sales efforts need to be rescheduled, which could materially adversely affect our business, financial condition and results of operations.

In addition, product development requires the accurate assessment of market trends and market acceptance among consumers and the medical community, particularly physicians and hospitals, in each of our target markets. Although hospitals often use generic products to reduce their costs, procurement departments of hospitals may not purchase our products. Physicians may not prescribe or recommend our products to patients, and pharmacists may not respect the prescription. Despite our track record of success in certain markets, the acceptance of any of our products among the medical community depends upon several factors, including the reputation of the brand, the safety and efficacy of the product, the effectiveness of our sales force, the product’s price, the product’s perceived advantages and disadvantages relative to competing products or treatments, and the prevalence and severity of side effects. Our overall profitability depends on, among other things, our ability to introduce new products in a timely manner, to differentiate our products with innovative formulations, to continue to manufacture products cost-efficiently and to manage the life cycle, including market acceptance, of our product portfolio.

We are subject to strict controls on the commercialization processes for our pharmaceutical products, including their development, manufacture, distribution and marketing, which vary by country and by region. Any delays in, or rejections of, regulatory reviews, approvals or permits could delay our ability to market our products, which could have a material adverse effect on our business, financial condition and results of operations.

We are subject to strict controls and approvals on the commercialization processes for our pharmaceutical products, including their development, manufacturing, distribution and marketing. The criteria for establishing safety, efficacy and quality, which are essential for securing marketing approvals, vary by country and by region. Obtaining approval for our products and manufacturing processes requires us to submit a dossier in respect of each international non-proprietary name (“INN”) and each formulation and dosage variation for such INN in each country in which we wish to market such product. Regulators may delay approvals and require additional data before approval is granted, or reject approvals requested, even though the pharmaceutical products may already be approved or launched in other countries.

Certain factors, including advances in science and technology, evolving regulatory science and new laws and policies, can result in delays in the approval of new pharmaceutical products, including new advanced oral delivery systems. While we seek to manage most of these risks, unanticipated and unpredictable policymaking by governments and regulators, limited regulatory authority resources or conflicting priorities can often lead to delays in regulatory approvals. Any such delays in regulatory reviews and approvals could delay the marketing of our products, resulting in increased costs as described above, which may have a material adverse effect on our business, financial condition and results of operations.

Our future results of operations are subject to fluctuations in the costs, availability, and suitability of the components of the products we manufacture, including active pharmaceutical ingredients, excipients, purchased components, and raw materials. In addition, global supply chain crisis may interfere with the operations of certain of our direct or indirect suppliers or with international trade for these supplies, which could raise our costs or reduce the productivity or slow the timing of our operations, which could have a material adverse effect on our business, financial condition and results of operations.

We depend on various active pharmaceutical ingredients, components, compounds, raw materials, and energy supplied primarily by others for our offerings. This includes, but is not limited to, pharmaceutical and biologic ingredients, gelatin, starch, and iota carrageenan for our Softgel products, packaging films for our Rx and OTC products, and glass vials and syringes for injectable fill-finish for certain of our Rx and Diabetrics (as defined below) products. Also, certain of our customers provide to us their active pharmaceutical or biologic ingredient for formulation or incorporation in the finished product and may supply other raw materials as well. It is possible that any of our or our customers’ supplier relationships could be interrupted due to changing regulatory requirements, import or export restrictions, natural disasters, international supply disruptions, whether caused by pandemics or otherwise, geopolitical issues, operational or quality issues at the suppliers’ facilities, and other events, or could be terminated in the future.

2

For example, gelatin is a critical component in most of our Softgel products produced by our NextGel segment. Gelatin is available from only a limited number of sources. In addition, much of the gelatin we use is bovine-derived. Past concerns of contamination from bovine spongiform encephalopathy (“BSE”), have narrowed the number of possible sources of particular types of gelatin. If there were a future disruption in the supply of gelatin from any one or more key suppliers, we may not be able to obtain an adequate alternative supply from our other suppliers. If future restrictions were to emerge on the use of bovine-derived gelatin due to concerns of contamination from BSE or otherwise, any such restriction could hinder our ability to timely supply our customers with products and the use of alternative non-bovine-derived gelatin could be subject to lengthy formulation, testing, and regulatory approval.

A disruption at any of our main manufacturing facilities could materially and adversely affect our business, financial condition and results of operations.

Our manufacturing operations are concentrated in seven locations throughout Colombia, Brazil, El Salvador and the United States, including the first FDA-approved pharmaceutical plant in South America and Central America and our first U.S.-based Softgel production facility and R&D center which began operations in May 2022. A significant disruption at one or more of these facilities, whether it be due to fire, natural disaster, power loss, intentional acts of vandalism, climate change, war, terrorism, insufficient quality, cyber-attacks, or pandemic could materially and adversely affect our business.

Additionally, regulatory authorities routinely inspect all of our manufacturing facilities for compliance with applicable laws, rules, regulations and practices. If a regulatory authority were to identify serious adverse findings not corrected upon follow up inspections, we may be required to issue product recalls, shut down manufacturing facilities, pay fines, and take other remedial actions. Also, if the lessor under any leased facility identifies any breach thereto, it may have the right to terminate the lease in advance. If any manufacturing facility were forced to cease or limit production, our business, financial condition and results of operations could be materially adversely affected.

Risks Related to Our Business and Financial Condition

Our independent registered public accounting firm has included an explanatory paragraph relating to our ability to continue as a going concern in its report on our Annual Audited Consolidated Financial Statements included elsewhere in this Annual Report.

Our Annual Audited Consolidated Financial Statements were prepared assuming that we will continue as a going concern. However, the report of our independent registered public accounting firm included elsewhere in this Annual Reports contains an explanatory paragraph on our consolidated financial statements stating there is substantial doubt about our ability to continue as a going concern, meaning that we may not be able to continue in operation for the foreseeable future or be able to realize assets and discharge liabilities in the ordinary course of operations. Such an opinion could materially limit our ability to raise additional funds through the issuance of new debt or equity securities or otherwise. There is no assurance that sufficient financing will be available when needed to allow us to continue as a going concern. The perception that we may not be able to continue as a going concern may also make it more difficult to raise additional funds or operate our business due to concerns about our ability to meet our contractual obligations. Any inability to raise additional funds, when needed, could materially adversely affect our business, financial condition and results of operations. For more information regarding management’s assessment regarding its ability to continue as going concern. See “Item 5. Operating and Financial Review and Prospects—Operating Results—Going Concern Update” and Note 2.1 Note 2.1 to our Annual Audited Consolidated Financial Statements, included elsewhere in this Annual Report.

3

We have identified material weaknesses in our internal control over financial reporting. If we are unable to develop and maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results in a timely manner, which may adversely affect investor confidence in us and materially and adversely affect our business and results of operations.

In connection with the audit of our Annual Audited Consolidated Financial Statements, we identified material weaknesses in our internal controls related to (i) our manual consolidation process which lacks the appropriate internal controls to prevent or detect material misstatements in a timely manner and to ensure that financial data recorded was complete and accurate, (ii) our information technology controls not being sufficiently designed and implemented to address certain information technology risks, (iii) the sufficiency of technical accounting resources with an appropriate level of technical experience required for timely and accurate financial reporting in accordance with IFRS, (iv) lack of system controls and effective processes to ensure that all manual journal entries are properly reviewed and approved prior to posting to the general ledger, and (v) our controls and monitoring activities not being effective to ascertain whether the components of our internal control are present and functioning. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of annual or interim financial statements will not be prevented or detected on a timely basis.

Our remediation activities are ongoing, and we will continue to implement our initiatives to effectively implement our internal controls over financial reporting and further document our policies, procedures and internal controls, including, among others, (i) implementation and deployment of a plan for the business planning and consolidation module, which includes improving existing controls and adjusting policies and procedures and implementing automated consolidation, (ii) design, implementation, and operation of the segregation of duties model, for which the project is being executed with the support of an external advisor, and on ensuring the proper implementation and operation of controls, (iii) recruiting additional personnel in our finance and accounting departments to ensure that we have a sufficient complement of personnel with the appropriate level of knowledge and experience required for the timely and accurate financial reporting in accordance with IFRS, (iv) designing and implementing procedures over the preparation and review of journal entries to establish that manual journal entries are properly prepared, supported by adequate documentation, and independently reviewed and approved, and (v) implementing actions to strengthen the monitoring activities of internal controls. However, if our remedial measures are insufficient to address the material weaknesses, or if additional material weakness or significant deficiencies in our internal control are discovered or occur in the future, our financial statements may contain material misstatements. If our financial statements are not accurate, investors may not have a complete understanding of our operations. Likewise, if our financial statements are not filed on a timely basis in the future, we could be subject to sanctions or investigations by Nasdaq, or any other stock exchange on which the Ordinary Shares are listed, the SEC or other regulatory authorities. Either case could adversely affect investor confidence in us and materially and adversely affect our business and results of operations. For a discussion on our remedial measures, see Item 15.B under the heading “Management’s Annual Assessment of Internal Control Over Financial Reporting –– Remediation Efforts” in this Annual Report.

We have indebtedness, which may increase risk to our business and your investment in us.

As of December 31, 2022, we had $285.9 million of outstanding indebtedness, including under our Senior Notes, Syndicated Loan, and other indebtedness, including under the Additional Loan Agreement. Our ability to make scheduled payments of the principal of, to pay cash interest on, our indebtedness, including the Senior Notes, Syndicated Loan and Additional Loan Agreement, or to refinance such indebtedness, or any other indebtedness we may incur, depends on our future performance, which is subject to economic, financial, competitive and other factors beyond our control. Our business may not generate cash flow from operations in the future sufficient to service our debt and make necessary capital expenditures. The NPA, Syndicated Loan and Additional Loan Agreement contain customary restrictive covenants that limit our ability to engage in activities that may be in our long-term best interest. Those covenants include restrictions on our ability to, among other things, incur additional debt and issue disqualified stock; create liens; pay dividends, acquire shares of capital stock, or make certain investments; issue guarantees; sell certain assets and enter into transactions with affiliates. The NPA, Syndicated Loan and Additional Loan Agreement also each contain certain financial ratio covenants that we must comply with at certain measurement dates. Our failure to comply with any of those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of our debt issued under the applicable agreement. For example, we were not in compliance with certain of these financial ratios under the NPA, Syndicated Loan and Additional Loan Agreement as of December 31, 2022, and we entered into the Waivers where the applicable parties under the Waivers (i) waived our noncompliance as of December 31, 2022 and (ii) agreed to prospectively waive any noncompliance with these certain financial ratio covenants for the quarters ended March 31, 2023, June 30, 2023 and September 30, 2023, if applicable, provided that we meet certain agreed upon adjusted ratio thresholds as specified in each Waiver under the applicable financial ratio covenants. Any such event of default or acceleration could have an adverse effect on the trading price of our Ordinary Shares. Furthermore, the terms of any future debt we may incur could have further additional restrictive covenants. We may not be able to maintain compliance with these covenants in the future, and in the event that we are not able to maintain compliance, we cannot assure you that we will be able to obtain waivers from the lenders or amend the covenants. For additional details on our indebtedness and the Waivers see “Item 5.B—Operating and Financial Review and Prospects—Liquidity and Capital Resources—Debt Financing and Borrowings.”

4

If we are unable to generate such cash flow, we may be required to adopt one or more alternatives, such as selling assets, restructuring debt or obtaining additional debt financing or equity capital on terms that may be onerous or highly dilutive. Our ability to refinance any future indebtedness will depend on the capital markets, contractual restrictions and our financial condition at such time. We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our debt obligations. In addition, any of our future debt agreements may contain restrictive covenants that may prohibit us from adopting any of these alternatives. Our failure to comply with these covenants could result in an event of default which, if not cured or waived, could result in the acceleration of our debt.

If we do not enhance our existing products and services, or introduce new technology or service offerings in a timely manner, our products and services may become uncompetitive over time, or customers may not buy our products or buy less of them, which could have a material adverse effect on our business, financial condition and results of operations.

The healthcare industry is characterized by rapid technological change. Demand for our Rx and OTC pharmaceutical products, Diabetrics products and services, and our integral contract development and manufacturing organization (“iCDMO”) services may change in ways we may not anticipate because of evolving industry standards as well as a result of evolving customer needs that are increasingly sophisticated and varied and the introduction by others of new offerings and technologies that provide alternatives to our products and services. To the extent that such technologies are protected by patents, their related offerings may become subject to competition as the patents expire. Without the timely introduction of enhanced or new products and services, and technologies, our offerings may become uncompetitive over time, in which case our revenue and operating results would suffer. For example, if we are unable to respond to changes in the nature or extent of the technological or other needs of our pharmaceutical customers through enhancing our pharmaceutical products and services offerings, our competition may develop offerings that are more competitive than ours and we could find it more difficult to renew or expand existing agreements or obtain new agreements. Potential innovations intended to facilitate enhanced or new offerings generally will require a substantial investment before we can determine their commercial viability, and we may not have financial resources sufficient to fund all desired innovations.

The success of enhanced or new pharmaceutical products and services will depend on several factors, including our ability to:

| ● | properly anticipate and satisfy customer needs, including increasing demand for lower cost products; |

| ● | enhance, innovate, develop, and manufacture new offerings in an economical and timely manner; |

| ● | differentiate our products and services from competitors’ offerings; |

| ● | achieve positive clinical outcomes for our and our customers’ new products; |

| ● | meet safety requirements and other regulatory requirements of governmental agencies; |

| ● | obtain valid and enforceable intellectual property rights; and |

| ● | avoid infringing the proprietary rights of third parties. |

5

Even if we succeed in creating enhanced or new pharmaceutical products and services from these innovations, they may still fail to result in commercially successful offerings or may not produce revenue in excess of the costs of development, and they may become uncompetitive due to changing customer preferences or the introduction by our competitors of offerings embodying new technologies or features. Finally, innovations may not be accepted quickly in the marketplace because of, among other things, entrenched patterns of clinical practice, the need for regulatory clearance, and uncertainty over market access or government or third-party reimbursement.

The demand for OTC products may be impacted by changes in consumer preferences. If we are unable to adapt to these changes, we may lose market share and our net sales may be negatively impacted, which could have a material adverse effect on our business, financial condition and results of operations.

Consumer preferences related to health concerns may change, which could negatively impact demand for our OTC products or cause us to incur additional costs to change our OTC products or product packaging. The success of certain our OTC products such as gastrointestinal, skin care and vitamins, minerals and supplements, is dependent on the continued growth in demand for overall health related products. If demand for products in this category decreases, our financial condition and results of operations would be negatively impacted.

Furthermore, our OTC consumer products customers may request changes in packaging to meet consumer demands, which could cause us to incur inventory obsolescence charges and redesign costs, which in turn could negatively impact our results of operations.

We may be unable to identify acquisition opportunities and successfully execute and close acquisitions, which could limit our potential for growth.

We have made several acquisitions in recent years, such as the U.S.-based Softgel production facility and R&D center located in West Palm Beach, Florida we acquired in January 2022, and expect to actively seek new acquisitions that management believes will provide meaningful opportunities for growth by increasing our existing capabilities and expanding into new areas and markets of operations. However, we may not be able to identify suitable acquisition candidates or complete acquisitions on acceptable terms and conditions. For example, on May 16, 2022, the Company entered into a definitive agreement to acquire Grupo Somar (including Grupo Farmacéutico Somar, S.A.P.I de C.V., Química y Farmacia S.A. de C.V., Gelcaps Exportadora de Mexico S.A. de C.V. and related entities) which acquisition (the “Acquisition”) was terminated following its failure to close by December 31, 2022.

Other companies in our industry have similar investment and acquisition strategies to ours, and competition for acquisitions may intensify. If we are unable to identify acquisition candidates that meet our criteria, or complete acquisitions on acceptable terms and condition, our potential for growth may be restricted. Additionally, because we may pursue acquisitions around the world and may actively pursue a number of opportunities simultaneously, we may encounter unforeseen expenses, complications and delays in connection with identifying or acquiring suitable acquisition targets.

We may not be able to realize the benefits of business acquisitions and divestitures we enter into, including being unable to successfully and efficiently integrate acquisitions or execute on dispositions, which could have a material adverse effect on our business, financial condition and results of operations.

We engage from time to time in acquisitions and other transactions that may complement or expand our business or in divestments of non-strategic businesses or assets. These transactions, including our acquired U.S.-based Softgel production facility and R&D center, which began operations in May 2022, are accompanied by risks, many of which are beyond our control, and any one of them could result in increased cost, decreased net sales and diversion of management’s time and energy, any or all of which could materially impact our business, financial condition, and results of operations. Such risks include, among others, risks relating to our ability to successfully and efficiently integrate acquisitions or execute on dispositions and realize anticipated benefits therefrom.

6

In order to implement our growth strategy, we evaluate opportunities to buy or otherwise acquire rights to other businesses or technologies, enter into joint ventures or otherwise enter into strategic arrangements with business partners that could complement, enhance, or expand our current business or offerings and services or that might otherwise offer us growth opportunities, or divest assets or an ongoing business. We may face competition from other companies in pursuing acquisitions and similar transactions in the pharmaceutical industry. Our ability to complete transactions may also be limited by applicable antitrust and trade laws and regulations in the jurisdictions in which we or the operations or assets we seek to acquire carry on business. To the extent that we are successful in making acquisitions, we expend substantial amounts of cash, incur debt, or assume loss-making divisions as consideration. We or the purchaser of a divested asset or business may not be able to complete a desired transaction for any number of reasons, including a failure to secure financing.

Any acquisition that we are able to identify and complete may involve a number of risks, including, but not limited to (i) the diversion of management’s attention to integrate the acquired businesses or joint ventures, (ii) the possible adverse effects on our operating results during the integration process, (iii) the potential loss of customers or employees in connection with the acquisition, (iv) delays or reduction in realizing expected synergies, (v) unexpected liabilities, (vi) exposure to compliance, intellectual property, environmental, legal or other issues, not uncovered by a limited due diligence review of the target or otherwise, and (vii) our potential inability to achieve our intended objectives for the transaction.

To the extent that we are not successful in completing desired divestitures, as such may be determined by future strategic plans and business performance, we may have to expend substantial amounts of cash, incur debt, or continue to absorb the costs of loss-making or under-performing assets. Any divestiture, whether we are able to complete it or not, may involve a number of risks, including diversion of management’s attention, a negative impact on our customer relationships, costs associated with maintaining the business of the targeted divestiture during the disposition process, and the costs of closing and disposing of the affected business or transferring remaining portions of the operations of the business to other facilities.

Our business depends upon certain customers for a significant portion of our sales, therefore, a disruption of our relationship with these customers or any material adverse change in these customers’ businesses could have a material adverse effect on our business, financial condition and results of operations.

Sales to the five largest economic groups that form part of our customer base comprised approximately 25% and 26% of our net sales for the years ended December 31, 2022 and 2021, respectively. No other customer individually comprised more than 5.7% and 6.5% of net sales for the years ended December 31, 2022 and 2021, respectively. If our relationship with one of the five largest economic groups that form part of our customer base, including the terms of doing business with such customers, changes significantly, it could have a material adverse impact on our business, financial condition and results of operations.

Many of our customers, which include major global, national, and regional retail drug, supermarket, and mass merchandise chains, major wholesalers, sourcing groups, hospitals and grocery stores located primarily in Latin America and the United States, continue to merge or consolidate. Such consolidation has provided, and may continue to provide, customers with additional purchasing leverage, and consequently may increase the pricing pressures we face. The emergence of large buying groups representing independent retail pharmacies enable those groups to extract price discounts on our products.

Additionally, if we are unable to maintain adequately high levels of customer service over time, customers may choose to obtain alternate sources for products and/or end their relationships with us.

7

We depend on our executive officers and other key personnel to operate and grow our business and to develop new and enhanced offerings and technologies and the loss of, or the failure to attract and retain, such key personnel could adversely affect our operations.

We depend on our executive officers and other key personnel, including our technical personnel, to operate and grow our business and to develop new and enhanced products, services and technologies. The loss of any of these officers or other key personnel or a failure to attract and retain suitably skilled technical personnel could adversely affect our operations.

In addition to our executive officers, we rely on seven senior vice presidents and senior management personnel to lead and direct our business. The members of the senior leadership team hold positions in areas such as corporate finance, audit and internal controls, human resources, corporate and legal affairs, international marketing and R&D, investor relations and mergers and acquisitions. Furthermore, each of our business segments (NextGel, Procaps Colombia, CAN (as defined below), CASAND (as defined below) and Diabetrics) is managed by an executive that reports directly to the Chief Operating Officer.

With respect to our technical talent, we employ more than 300 scientists, technicians and skilled personnel in R&D and innovation as of December 31, 2022. Many of our facilities are located in competitive labor markets like those in which our Colombia, Brazil, El Salvador and United States facilities are located. Global and regional competitors and, in some cases, customers and suppliers compete for the same skills and talent as we do.

We depend on our specialized sales representatives to generate the net sales and the levels of product and brand name awareness we desire.

We rely on our network of specialized sales representatives to create greater awareness of our products and brand names. As a result, our operations involve certain risks, including that our sales representatives may fail to comply with local requirements, to devote the resources necessary to achieve physician confidence or loyalty, to otherwise effectively market our products, and/or to provide us with accurate or timely information about product sales. In addition, we invest in the formation and specialization of each sales representative and have no assurance of their continued employment with us. Our future growth and profitability will depend in part on the effectiveness and efficiency of our sales force.

Inflation could adversely affect our business and results of operations.

While inflation in the United States and global markets has been relatively low in recent years, during 2021 and 2022, the economy in the United States and global markets encountered a material increase in the level of inflation. The impact of COVID-19, geopolitical developments such as the Russia-Ukraine conflict and global supply chain disruptions continue to increase uncertainty in the outlook of near-term and long-term economic activity, including whether inflation will continue and how long, and at what rate. Increases in inflation raise our costs for commodities, labor, materials and services and other costs required to grow and operate our business, and failure to secure these on reasonable terms may adversely impact our financial condition. A sustained increase in inflation may continue to increase these costs. Our efforts to recover inflation-based cost increases from our customers may be delayed or capped as a result of our contracts as well as the competitive industry and economic conditions in which we operate. The rate and scope of these various inflationary factors may continue to increase our operating costs and capital expenditures materially and may have a material adverse impact on our on our costs, profitability and financial results. Additionally, increases in inflation, along with the uncertainties surrounding COVID-19, geopolitical developments and global supply chain disruptions, have caused, and may in the future cause, global economic uncertainty and uncertainty about the interest rate environment, which may make it more difficult, costly or dilutive for us to secure additional financing. A failure to adequately respond to these risks could have a material adverse impact on our financial condition, results of operations or cash flows.

8

General inflation and increases in the minimum wage and general labor costs have affected and may continue to adversely affect our business, financial condition and results of operations.

Labor is a significant portion of our cost structure and is subject to many external factors, including minimum wage laws, prevailing wage rates, unemployment levels, health insurance costs and other insurance costs and changes in employment and labor legislation or other workplace regulation. Most companies experienced an increase in labor costs in 2022 and expect additional increases in 2023, primarily in response to raising rates of inflation. As the cost of labor and statutory minimum wage rates increase or related laws and regulations change, we will need to continue to increase not only the wage rates of our minimum wage employees, but also the wages paid to our other hourly or salaried employees. Increases in the cost of our labor could have an adverse effect on our business, financial condition and results of operations, or if we fail to pay such higher wages we could suffer increased employee turnover. Increases in labor costs generally could force us to increase prices for other customers, which could adversely impact our sales.

For some customers with multi-year fixed pricing contracts, increases in the minimum wage could decrease our profit margins or result in losses and could have a material adverse effect on our business, financial condition and results of operations.

The impact of worldwide economic conditions may adversely affect our business, operating results, and financial condition.

Our financial performance is subject to worldwide economic conditions, including adverse economic conditions caused by the continuing effects of the COVID-19 pandemic, rising inflation and interest rates, the continued conflict between Russia and Ukraine, and supply chain disruptions.

We are currently operating during a period of economic uncertainty and cannot predict the timing, strength, or duration of economic downturns. To the extent general macroeconomic conditions remain uncertain or worsen, our business may be harmed. Inflation has the potential to adversely affect our liquidity, business, operating results, and financial condition by increasing our overall cost structure, particularly if we are unable to achieve commensurate increases in the prices we charge our customers. The existence of inflation in the economy has resulted in, and may continue to result in, higher interest rates and capital costs, increased costs of labor, fluctuations in foreign currency exchange rates, and other similar effects. As a result of inflation, we have experienced, and may continue to experience, cost increases, which could materially and adversely affect our business, operating results, and financial condition.

Adverse developments affecting the financial services industry, such as actual events or concerns involving liquidity, defaults or nonperformance by financial institutions or transactional counterparties, could adversely affect our current and projected business operations and our financial condition and results of operations.