UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

[ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the quarterly period ended | ||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the transition period from ________________ to _________________ | ||

Commission File Number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

(Address of principal executive offices and zip code)

(

(Registrant’s telephone number, including area code)

_________________________________________________________

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

The |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ⌧

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ⌧

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ◻ | Accelerated filer ◻ |

Smaller reporting company | |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ◻

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

◻ Yes

APPLICABLE ONLY TO CORPORATE ISSUERS

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of January 31, 2024, there were

PROVIDENT FINANCIAL HOLDINGS, INC.

Table of Contents

PART 1 - | FINANCIAL INFORMATION | Page | |

ITEM 1 - | Financial Statements. The Unaudited Interim Condensed Consolidated Financial Statements of | ||

Condensed Consolidated Statements of Financial Condition | 1 | ||

2 | |||

3 | |||

4 | |||

Condensed Consolidated Statements of Cash Flows | 6 | ||

Notes to Unaudited Interim Condensed Consolidated Financial Statements | 7 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations: | |||

37 | |||

38 | |||

38 | |||

39 | |||

39 | |||

Comparison of Financial Condition at December 31, 2023 and June 30, 2023 | 40 | ||

Comparison of Operating Results for the Quarters and Six Months Ended December 31, 2023 and 2022 | 41 | ||

51 | |||

53 | |||

53 | |||

55 | |||

56 | |||

60 | |||

60 | |||

61 | |||

61 | |||

61 | |||

61 | |||

61 | |||

62 | |||

63 | |||

PROVIDENT FINANCIAL HOLDINGS, INC.

Condensed Consolidated Statements of Financial Condition

(Unaudited)

In Thousands, Except Share and Per Share Information

December 31, | June 30, | |||||

2023 |

| 2023 | ||||

Assets | ||||||

Cash and cash equivalents | $ | | $ | | ||

Investment securities - held to maturity, at cost with |

| |

| | ||

Investment securities - available for sale, at fair value with |

| |

| | ||

Loans held for investment, net of allowance for credit losses of $ |

| |

| | ||

Accrued interest receivable |

| |

| | ||

FHLB - San Francisco stock |

| |

| | ||

Premises and equipment, net |

| |

| | ||

Prepaid expenses and other assets |

| |

| | ||

|

|

|

| |||

Total assets | $ | | $ | | ||

|

|

|

| |||

Liabilities and Stockholders’ Equity |

|

|

|

| ||

|

|

|

| |||

Liabilities: |

|

|

|

| ||

Noninterest-bearing deposits | $ | | $ | | ||

Interest-bearing deposits |

| |

| | ||

Total deposits |

| |

| | ||

|

|

|

| |||

Borrowings |

| |

| | ||

Accounts payable, accrued interest and other liabilities |

| |

| | ||

Total liabilities |

| |

| | ||

|

|

|

| |||

Commitments and Contingencies |

|

|

|

| ||

|

|

|

| |||

Stockholders’ equity: |

|

|

|

| ||

Preferred stock, $ |

|

| ||||

Common stock, $ |

| |

| | ||

Additional paid-in capital |

| |

| | ||

Retained earnings |

| |

| | ||

Treasury stock at cost ( |

| ( |

| ( | ||

Accumulated other comprehensive loss, net of tax |

| ( |

| ( | ||

|

| |||||

Total stockholders’ equity |

| |

| | ||

|

| |||||

Total liabilities and stockholders’ equity | $ | | $ | | ||

The accompanying notes are an integral part of these condensed consolidated financial statements.

1

PROVIDENT FINANCIAL HOLDINGS, INC.

Condensed Consolidated Statements of Operations

(Unaudited)

In Thousands, Except Per Share Information

| Quarter Ended | Six Months Ended | |||||||||||

December 31, | December 31, | ||||||||||||

| 2023 | 2022 |

| 2023 | 2022 |

| |||||||

Interest income: |

|

| |||||||||||

Loans receivable, net | $ | |

| $ | | $ | |

| $ | | |||

Investment securities |

| |

|

| |

| |

|

| | |||

FHLB - San Francisco stock |

| |

|

| |

| |

|

| | |||

Interest-earning deposits |

| |

|

| |

| |

|

| | |||

Total interest income |

| |

|

| |

| |

|

| | |||

|

|

|

| ||||||||||

Interest expense: |

|

|

|

| |||||||||

Checking and money market deposits | | | | | |||||||||

Savings deposits | | | | | |||||||||

Time deposits | | | | | |||||||||

Borrowings |

| |

|

| |

| |

|

| | |||

Total interest expense |

| |

|

| |

| |

|

| | |||

|

|

|

| ||||||||||

Net interest income |

| |

|

| |

| |

|

| | |||

(Recovery of) provision for credit losses |

| ( |

|

| |

| ( |

|

| | |||

Net interest income, after (recovery of) provision for credit losses |

| |

|

| |

| |

|

| | |||

|

|

|

| ||||||||||

Non-interest income: |

|

|

|

| |||||||||

Loan servicing and other fees |

| |

|

| |

| |

|

| | |||

Deposit account fees |

| |

|

| |

| |

|

| | |||

Card and processing fees |

| |

|

| |

| |

|

| | |||

Other |

| |

|

| |

| |

|

| | |||

Total non-interest income |

| |

|

| |

| |

|

| | |||

|

|

|

| ||||||||||

Non-interest expense: |

|

|

|

| |||||||||

Salaries and employee benefits |

| |

|

| |

| |

|

| | |||

Premises and occupancy |

| |

|

| |

| |

|

| | |||

Equipment |

| |

|

| |

| |

|

| | |||

Professional |

| |

|

| |

| |

|

| | |||

Sales and marketing |

| |

|

| |

| |

|

| | |||

Deposit insurance premium and regulatory assessments |

| |

|

| |

| |

|

| | |||

Other |

| |

|

| |

| |

|

| | |||

Total non-interest expense |

| |

|

| |

| |

|

| | |||

|

|

|

| ||||||||||

Income before income taxes |

| |

|

| |

| |

|

| | |||

Provision for income taxes |

| |

|

| |

| |

|

| | |||

Net income | $ | |

| $ | | $ | |

| $ | | |||

|

| ||||||||||||

Basic earnings per share | $ | |

| $ | | $ | |

| $ | | |||

Diluted earnings per share | $ | |

| $ | | $ | |

| $ | | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

2

PROVIDENT FINANCIAL HOLDINGS, INC.

Condensed Consolidated Statements of Comprehensive Income

(Unaudited)

In Thousands

| For the Quarter Ended | For the Six Months Ended | ||||||||||

December 31, | December 31, | |||||||||||

| 2023 |

| 2022 |

| 2023 |

| 2022 | |||||

Net income | $ | |

| $ | | $ | |

| $ | | ||

|

|

| ||||||||||

Change in unrealized holding income (losses) on securities available for sale and interest-only strips |

| |

|

| ( |

| |

|

| ( | ||

Other comprehensive income (loss), before income tax expense (benefit) |

| |

|

| ( |

| |

|

| ( | ||

Income tax expense (benefit) |

| |

|

| ( |

| |

|

| ( | ||

Other comprehensive income (loss) |

| |

|

| ( |

| |

|

| ( | ||

Total comprehensive income | $ | |

| $ | | $ | |

| $ | | ||

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

PROVIDENT FINANCIAL HOLDINGS, INC.

Condensed Consolidated Statements of Stockholders' Equity

(Unaudited)

In Thousands, Except Share and Per Share Information

For the Quarters Ended December 31, 2023 and 2022:

|

|

|

|

|

| Accumulated |

|

| ||||||||||||

Other |

| |||||||||||||||||||

Common | Additional | Comprehensive |

| |||||||||||||||||

Stock | Paid-In | Retained | Treasury | (Loss) Income, |

| |||||||||||||||

Shares | Amount | Capital | Earnings | Stock | Net of Tax | Total | ||||||||||||||

Balance at September 30, 2023 |

| | $ | | $ | | $ | | $ | ( | $ | ( | $ | | ||||||

| ||||||||||||||||||||

Net income |

|

|

|

|

| |

|

|

|

| | |||||||||

Other comprehensive income |

|

|

|

|

|

|

|

|

| | | |||||||||

Purchase of treasury stock |

| ( |

|

|

|

|

| ( |

|

| ( | |||||||||

Distribution of restricted stock |

| |

|

|

|

|

|

|

| — | ||||||||||

Awards of restricted stock |

| — |

|

| ( |

|

| |

|

| — | |||||||||

Amortization of restricted stock |

|

|

| |

|

|

|

|

|

| | |||||||||

Stock options expense |

|

|

| |

|

|

|

|

|

| | |||||||||

Tax effect from stock based compensation | ( | ( | ||||||||||||||||||

Cash dividends(1) |

|

|

|

|

| ( |

|

|

|

| ( | |||||||||

Balance at December 31, 2023 |

| | $ | | $ | | $ | | $ | ( | $ | ( | $ | | ||||||

| (1) |

|

|

|

|

|

| Accumulated |

|

| ||||||||||||

Other |

| |||||||||||||||||||

Common | Additional | Comprehensive |

| |||||||||||||||||

Stock | Paid-In | Retained | Treasury | Income (Loss), |

| |||||||||||||||

Shares | Amount | Capital | Earnings | Stock | Net of Tax | Total | ||||||||||||||

Balance at September 30, 2022 |

| | $ | | $ | | $ | | $ | ( | $ | ( | $ | | ||||||

Net income |

|

|

|

| |

|

| | ||||||||||||

Other comprehensive loss |

|

|

|

|

|

| ( | ( | ||||||||||||

Purchase of treasury stock |

| ( |

|

|

|

| ( |

| ( | |||||||||||

Amortization of restricted stock |

|

|

| |

|

|

| | ||||||||||||

Stock options expense |

|

|

| |

|

|

| | ||||||||||||

Tax effect from stock based compensation | ( | ( | ||||||||||||||||||

Cash dividends(1) |

|

|

|

| ( |

|

| ( | ||||||||||||

Balance at December 31, 2022 |

| | $ | | $ | | $ | | $ | ( | $ | ( | $ | | ||||||

| (1) |

4

For the Six Months Ended December 31, 2023 and 2022:

Accumulated |

| |||||||||||||||||||

Other |

| |||||||||||||||||||

Common | Additional | Comprehensive |

| |||||||||||||||||

Stock | Paid-In | Retained | Treasury | (Loss) Income, |

| |||||||||||||||

| Shares |

| Amount |

| Capital |

| Earnings |

| Stock |

| Net of Tax |

| Total | |||||||

Balance at June 30, 2023 | | $ | | $ | | $ | | $ | ( | $ | ( | $ | | |||||||

|

| |||||||||||||||||||

Net income |

|

|

|

|

| |

|

|

|

| | |||||||||

Other comprehensive income |

|

|

|

|

|

|

| |

| | ||||||||||

Purchase of treasury stock |

| ( |

|

|

|

|

| ( |

|

|

| ( | ||||||||

Distribution of restricted stock |

| |

|

|

|

|

|

|

|

| — | |||||||||

Awards of restricted stock |

|

|

| ( |

|

| |

|

| — | ||||||||||

Amortization of restricted stock |

|

|

|

| |

|

|

|

|

| | |||||||||

Stock options expense |

|

|

|

| |

|

|

|

|

| | |||||||||

Tax effect from stock based compensation | ( | ( | ||||||||||||||||||

Cash dividends(1) |

|

|

|

|

| ( |

|

|

|

| ( | |||||||||

Adoption of CECL standard | ( | ( | ||||||||||||||||||

| ||||||||||||||||||||

Balance at December 31, 2023 |

| | $ | | $ | | $ | | $ | ( | $ | ( |

| $ | | |||||

| (1) |

|

|

|

|

|

| Accumulated |

|

| ||||||||||||

Other |

| |||||||||||||||||||

Common | Additional | Comprehensive |

| |||||||||||||||||

Stock | Paid-In | Retained | Treasury | Income (Loss), |

| |||||||||||||||

Shares | Amount | Capital | Earnings | Stock | Net of Tax | Total | ||||||||||||||

Balance at June 30, 2022 |

| | $ | | $ | | $ | | $ | ( | $ | | $ | | ||||||

|

|

|

|

| ||||||||||||||||

Net income |

|

|

|

|

|

| |

|

|

|

|

| | |||||||

Other comprehensive loss |

|

|

|

|

|

|

|

|

|

| ( |

| ( | |||||||

Purchase of treasury stock |

| ( |

|

|

|

|

|

| ( |

|

|

| ( | |||||||

Awards of restricted stock | ( | | — | |||||||||||||||||

Amortization of restricted stock |

|

|

|

| |

|

|

|

|

|

|

| | |||||||

Stock options expense |

|

|

|

| |

|

|

|

|

|

|

| | |||||||

Tax effect from stock based compensation | ( | ( | ||||||||||||||||||

Cash dividends(1) |

|

|

|

|

|

| ( |

|

|

|

|

| ( | |||||||

|

|

|

|

| ||||||||||||||||

Balance at December 31, 2022 |

| | $ | | $ | | $ | | $ | ( | $ | ( | $ | | ||||||

| (1) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

5

PROVIDENT FINANCIAL HOLDINGS, INC.

Condensed Consolidated Statements of Cash Flows

(Unaudited - In Thousands)

| Six Months Ended | ||||||

December 31, | |||||||

| 2023 |

| 2022 |

| |||

Cash flows from operating activities: |

| ||||||

Net income | $ | |

| $ | | ||

Adjustments to reconcile net income to net cash provided by operating activities : |

| ||||||

Depreciation and amortization |

| |

|

| | ||

(Recovery of) provision for credit losses |

| ( |

|

| | ||

Stock-based compensation |

| |

|

| | ||

Provision for deferred income taxes |

| |

|

| | ||

Decrease in accounts payable, accrued interest and other liabilities |

| ( |

|

| ( | ||

Increase in prepaid expenses and other assets |

| ( |

|

| ( | ||

Net cash provided by operating activities |

| |

|

| | ||

|

| ||||||

Cash flows from investing activities: |

| ||||||

Net decrease (increase) in loans held for investment |

| |

|

| ( | ||

Maturity of investment securities - held to maturity |

| |

|

| | ||

Principal payments from investment securities - held to maturity |

| |

|

| | ||

Principal payments from investment securities - available for sale |

| |

|

| | ||

Purchase of premises and equipment |

| ( |

|

| ( | ||

Net cash provided by (used for) investing activities |

| |

|

| ( | ||

Cash flows from financing activities: | |||||||

Net decrease in deposits | ( | ( | |||||

Proceeds from long-term borrowings | | | |||||

Repayments of long-term borrowings | ( | ( | |||||

(Repayments of) proceeds from short-term borrowings, net | ( | | |||||

Treasury stock purchases | ( | ( | |||||

Cash dividends | ( | ( | |||||

Net cash (used for) provided by financing activities | ( | | |||||

Net (decrease) increase in cash and cash equivalents | ( | | |||||

Cash and cash equivalents at beginning of period | | | |||||

Cash and cash equivalents at end of period | $ | | $ | | |||

Supplemental information: | |||||||

Cash paid for interest | $ | | $ | | |||

Cash paid for income taxes | $ | | $ | | |||

The accompanying notes are an integral part of these condensed consolidated financial statements.

6

PROVIDENT FINANCIAL HOLDINGS, INC.

Notes to Unaudited Interim Condensed Consolidated Financial Statements

December 31, 2023

Note 1: Basis of Presentation

The unaudited interim condensed consolidated financial statements included herein reflect all adjustments which are, in the opinion of management, necessary to present a fair statement of the results of operations for the interim periods presented. All such adjustments are of a normal, recurring nature. The condensed consolidated statement of financial condition at June 30, 2023 is derived from the audited consolidated financial statements of Provident Financial Holdings, Inc. and its wholly-owned subsidiary, Provident Savings Bank, F.S.B. (the "Bank") (collectively, the "Corporation"). Certain information and note disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") have been omitted pursuant to the rules and regulations of the United States Securities and Exchange Commission ("SEC") with respect to interim financial reporting. It is recommended that these unaudited interim condensed consolidated financial statements be read in conjunction with the audited consolidated financial statements and notes thereto included in the Corporation’s Annual Report on Form 10-K for the fiscal year ended June 30, 2023 (“2023 Annual Form 10-K”). The results of operations for the quarter and six months ended December 31, 2023 are not necessarily indicative of results that may be expected for the entire fiscal year ending June 30, 2024.

Note 2: Accounting Standard Updates (“ASU”)

ASU 2023-09:

In December 2023, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures. This ASU requires public business entities to annually (a) disclose specific categories in the rate reconciliation and (b) provide additional information for reconciling items that meet a quantitative threshold of equal to or greater than five percent of the amount computed by multiplying pretax income or loss by the applicable statutory income tax rate. This ASU is effective for annual periods beginning after December 15, 2024. Early adoption is permitted. The Corporation is in the process of reviewing the impact of this ASU and has not yet determined the impact of the adoption of this ASU on its consolidated financial statements.

ASU 2023-07:

In November 2023, the FASB issued ASU No. 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures. This ASU improves reportable segment disclosure requirements, primarily through enhanced disclosures about significant segment expenses. The key amendments include: (a) introduce a new requirement to disclose significant segment expenses regularly provided to the chief operating decision maker (“CODM”), (b) extend certain annual disclosures to interim periods, (c) clarify single reportable segment entities must apply ASC 280 in its entirety, (d) permit more than one measure of segment profit or loss to be reported under certain conditions, and (e) require disclosure of the title and position of the CODM. This ASU is effective for public entities fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted. The Corporation is in the process of reviewing the impact of this ASU and has not yet determined the impact of the adoption of this ASU on its consolidated financial statements.

ASU 2020-04:

In March 2020, the FASB issued ASU No. 2020-04, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting. This ASU applies to contracts, hedging relationships and other transactions that reference the London Interbank Offered Rate (“LIBOR”) or other rate references expected to be discontinued because of reference rate reform. The ASU permits an entity to make necessary modifications to eligible contracts or transactions without requiring contract remeasurement or reassessment of a previous accounting determination. In January 2021, ASU 2021-01 clarified that certain optional expedients and exceptions in Topic 848 for contract modifications and hedge accounting apply to derivatives that are affected by the changes in the interest rates used for margining, discounting, or contract price alignment for derivative instruments that are being implemented as part of the market-wide transition to new reference rates (commonly referred to as the “discounting transition”). In December

7

2022, the FASB issued ASU 2022-06, Deferral of the Sunset Date of Topic 848. The FASB had originally included a sunset provision within Topic 848 based on expectations of when the LIBOR would cease being published. In March 2021, it was announced that the intended cessation date of LIBOR was extended to June 30, 2023. As a result, the FASB issued ASU 2022-06 deferring the sunset date of Topic 848 from December 31, 2022 to December 31, 2024. This ASU is effective for all entities as of March 12, 2020 through December 31, 2024. As of June 30, 2023, the Corporation had approximately $

ASU 2016-13:

In June 2016, the FASB issued ASU 2016-13, “Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments,” and subsequent amendments to the initial guidance. On July 1, 2023, the Corporation adopted this ASU that replaced the incurred loss methodology with the current expected credit loss (“CECL”) methodology. CECL requires an estimate of credit losses for the remaining estimated life of the financial asset using historical experience, current conditions, and reasonable and supportable forecasts and applies to financial assets measured at amortized cost, including loans held for investment and held-to-maturity investment securities, and some off-balance sheet credit exposures such as unfunded commitments to extend credit. Financial assets measured at amortized cost will be presented at the net amount expected to be collected by using an allowance for credit losses (“ACL”).

In addition, CECL made changes to the accounting for available for sale investment securities. One such change is to require credit losses to be presented as an allowance rather than as a write-down on available for sale debt securities if management does not intend to sell and does not believe that it is more likely than not, they will be required to sell.

The Corporation adopted ASC 326, “Financial Instruments – Credit Losses,” and all related subsequent amendments using the prospective transition approach for all financial assets measured at amortized cost and off-balance sheet credit exposures. The transition adjustment of the adoption of CECL included an $

The Corporation adopted ASC 326 using the prospective transition approach for debt securities for which other-than-temporary impairment had been recognized prior to July 1, 2023. As of June 30, 2023, the Corporation did not have any other-than-temporary impaired investment securities. Therefore, upon adoption of ASC 326, the Corporation determined that an ACL on available for sale securities was not deemed necessary.

8

The following table illustrates the impact on the ACL from the adoption of ASC 326:

Allowance for | Allowance | Impact to | |||||||

credit losses | before adoption | allowance after ASC | |||||||

under ASC 326 | of ASC 326 | 326 adoption | |||||||

(In Thousands) | (07/01/2023) | (06/30/2023) | (07/01/2023) | ||||||

Assets: |

|

|

|

|

|

| |||

Mortgage loans: |

| ||||||||

Single-family | $ | | $ | |

| $ | | ||

Multi-family | | | ( | ||||||

Commercial real estate | | | ( | ||||||

Construction | | | | ||||||

Other | | | | ||||||

Commercial business loans | | | ( | ||||||

Consumer loans | — | | ( | ||||||

ACL on loans | $ | | $ | | $ | | |||

Liabilities: | |||||||||

Unfunded loan commitment reserve | $ | | $ | | $ | — | |||

In March 2022, FASB issued ASU 2022-02, “Financial Instruments-Credit Losses (Topic 326) Troubled Debt Restructurings and Vintage Disclosures.” This ASU provides new guidance on the treatment of troubled debt restructurings (“TDR”) in relation to the adoption of the CECL model for the accounting for credit losses (see note above regarding ASU 2016-13). Previous accounting guidance related to TDRs is eliminated and new disclosure requirements are adopted in regards to loan refinancing and restructurings made to borrowers experiencing financial difficulties under the assumption that the CECL model will capture credit losses related to TDRs. These required disclosures regarding gross write-offs for financing receivables by year of origination and loan modifications are also included in this ASU. Subsequent to the adoption of ASC 326, the Corporation will no longer report TDRs or classify loans as TDRs given those previously recognized as TDRs have been incorporated into the CECL methodology in regard to loan loss reserves as of July 1, 2023 and as of December 31, 2023, there were

1

Note 3: Earnings Per Share

Basic earnings per share (“EPS”) excludes dilution and is computed by dividing income available to common shareholders by the weighted-average number of shares outstanding for the period. Diluted EPS reflects the potential dilution that could occur if securities or other contracts to issue common stock were exercised or converted into common stock or resulted in the issuance of common stock that would then share in the earnings of the Corporation.

As of December 31, 2023 and 2022, there were outstanding stock options to purchase

9

The following table provides the basic and diluted EPS computations for the quarters and six months ended December 31, 2023 and 2022, respectively.

For the Quarter Ended | For the Six Months Ended | |||||||||||

December 31, | December 31, | |||||||||||

(In Thousands, Except Earnings Per Share) | 2023 |

| 2022 |

| 2023 |

| 2022 | |||||

Numerator: | ||||||||||||

Net income – numerator for basic earnings per share and |

| |||||||||||

diluted earnings per share - available to common | ||||||||||||

stockholders | $ | $ | $ | $ | ||||||||

Denominator: | ||||||||||||

Denominator for basic earnings per share: | ||||||||||||

Weighted-average shares |

| |

| |

| |

| | ||||

Less effect of dilutive shares: | ||||||||||||

Stock options |

| — |

| — |

| — |

| — | ||||

Restricted stock |

| |

| |

| |

| | ||||

Denominator for diluted earnings per share: | ||||||||||||

Adjusted weighted-average shares and assumed |

| |||||||||||

conversions | ||||||||||||

Basic earnings per share |

| $ | |

| $ | |

| $ | |

| $ | |

Diluted earnings per share |

| $ | |

| $ | |

| $ | |

| $ | |

Note 4: Investment Securities

The amortized cost and estimated fair value of investment securities as of December 31, 2023 and June 30, 2023 were as follows:

|

|

| Gross |

| Gross |

| Estimated |

| |||||||

Amortized | Unrealized | Unrealized | Fair | Carrying | |||||||||||

December 31, 2023 | Cost | Gains | (Losses) | Value | Value | ||||||||||

(In Thousands) |

|

|

|

|

|

|

|

|

|

| |||||

Held to maturity |

|

|

|

|

|

|

|

|

|

| |||||

U.S. government sponsored enterprise MBS(1) | $ | | $ | | $ | ( | $ | | $ | | |||||

U.S. government sponsored enterprise CMO(2) | | | ( | | | ||||||||||

U.S. SBA securities(3) |

| |

| |

| ( |

| |

| | |||||

Total investment securities - held to maturity | | | ( | | | ||||||||||

|

|

|

|

|

|

|

|

|

| ||||||

Available for sale |

|

|

|

|

|

|

|

|

|

| |||||

U.S. government agency MBS | | | ( | | | ||||||||||

U.S. government sponsored enterprise MBS | | | ( | |

| | |||||||||

Private issue CMO |

| |

| |

| ( |

| |

| | |||||

Total investment securities - available for sale | | | ( | | | ||||||||||

Total investment securities | $ | | $ | | $ | ( | $ | | $ | | |||||

10

|

|

| Gross |

| Gross |

| Estimated |

| |||||||

Amortized | Unrealized | Unrealized | Fair | Carrying | |||||||||||

June 30, 2023 | Cost | Gains | (Losses) | Value | Value | ||||||||||

(In Thousands) |

|

|

|

|

|

|

|

|

|

| |||||

Held to maturity |

|

|

|

|

|

|

|

|

|

| |||||

U.S. government sponsored enterprise MBS | $ | | $ | | $ | ( | $ | | $ | | |||||

U.S. government sponsored enterprise CMO | | | ( | | | ||||||||||

U.S. SBA securities |

| |

| |

| ( |

| |

| | |||||

Total investment securities - held to maturity | | | ( | | | ||||||||||

|

|

|

|

|

|

|

|

|

| ||||||

Available for sale |

|

|

|

|

|

|

|

|

|

| |||||

U.S. government agency MBS | | | ( | | | ||||||||||

U.S. government sponsored enterprise MBS |

| |

| |

| ( |

| |

| | |||||

Private issue CMO |

| |

| |

| ( |

| |

| | |||||

Total investment securities - available for sale | | | ( | | | ||||||||||

Total investment securities | $ | | $ | | $ | ( | $ | | $ | | |||||

In the second quarters of fiscal 2024 and 2023, the Corporation received MBS principal payments of $

For the first six months of fiscal 2024 and 2023, the Corporation received MBS principal payments of $

The Corporation held investments with an unrealized loss position of $

As of December 31, 2023 | Unrealized Holding Losses | Unrealized Holding Losses | Unrealized Holding Losses | |||||||||||||||

(In Thousands) | Less Than 12 Months | 12 Months or More | Total | |||||||||||||||

Fair | Unrealized | Fair | Unrealized | Fair | Unrealized | |||||||||||||

Description of Securities |

| Value |

| Losses |

| Value |

| Losses |

| Value |

| Losses | ||||||

Held to maturity | ||||||||||||||||||

U.S. government sponsored enterprise MBS | $ | | $ | | $ | | $ | | $ | | $ | | ||||||

U.S. government sponsored enterprise CMO | — | — | | | | | ||||||||||||

U.S. SBA securities | — | — | | | | | ||||||||||||

Total investment securities - held to maturity | — | — | | | | | ||||||||||||

Available for sale | ||||||||||||||||||

U.S government agency MBS | — | — | | | | | ||||||||||||

U.S. government sponsored enterprise MBS | | | | | | | ||||||||||||

Private issue CMO | — | — | | | | | ||||||||||||

Total investment securities - available for sale | | | | | | | ||||||||||||

Total investment securities | $ | | $ | | | $ | | $ | | $ | | |||||||

11

As of June 30, 2023 | Unrealized Holding Losses | Unrealized Holding Losses | Unrealized Holding Losses | |||||||||||||||

(In Thousands) | Less Than 12 Months | 12 Months or More | Total | |||||||||||||||

Fair | Unrealized | Fair | Unrealized | Fair | Unrealized | |||||||||||||

Description of Securities |

| Value |

| Losses |

| Value |

| Losses |

| Value |

| Losses | ||||||

Held to maturity | ||||||||||||||||||

U.S. government sponsored enterprise MBS | $ | | $ | | $ | | $ | | $ | | $ | | ||||||

U.S. government sponsored enterprise CMO | — | — | | | | | ||||||||||||

U.S. SBA securities | | | — | — | | | ||||||||||||

Total investment securities - held to maturity | | | | | | | ||||||||||||

Available for sale | ||||||||||||||||||

U.S government agency MBS | | | | | | | ||||||||||||

U.S. government sponsored enterprise MBS | | | | | | | ||||||||||||

Private issue CMO | — | — | | | | | ||||||||||||

Total investment securities - available for sale | | | | | | | ||||||||||||

Total investment securities | $ | | $ | | $ | | $ | | $ | | $ | | ||||||

The Corporation adopted ASC 326 on July 1, 2023. The Corporation evaluates individual investment securities quarterly for impairment. At December 31, 2023, predominately all of the $

In order to maintain adequate liquidity, the Bank has established borrowing facilities with various counterparties. The Bank had a remaining borrowing capacity of $

At June 30, 2023, the Bank had a remaining borrowing capacity of $

At December 31, 2023 and 2022, the Corporation did not hold any investment securities with the intent to sell and determined it had the ability to hold these investment securities until maturity. It also determined that it was more likely

12

than not that the Corporation would not be required to sell the securities prior to recovery of the amortized cost basis; therefore,

Contractual maturities of investment securities as of December 31, 2023 and June 30, 2023 were as follows:

December 31, 2023 | June 30, 2023 | |||||||||||

|

| Estimated |

|

| Estimated | |||||||

Amortized | Fair | Amortized | Fair | |||||||||

(In Thousands) | Cost | Value | Cost | Value | ||||||||

Held to maturity |

|

|

|

|

|

|

|

| ||||

Due in one year or less | $ | | $ | | $ | | $ | | ||||

Due after one through five years |

| |

| |

| |

| | ||||

Due after five through ten years |

| |

| |

| |

| | ||||

Due after ten years |

| |

| |

| |

| | ||||

Total investment securities - held to maturity | | | | | ||||||||

|

|

|

|

|

|

|

| |||||

Available for sale |

|

|

|

|

|

|

|

| ||||

Due in one year or less | | | | | ||||||||

Due after one through five years |

| |

| |

| |

| | ||||

Due after five through ten years |

| |

| |

| |

| | ||||

Due after ten years |

| |

| |

| |

| | ||||

Total investment securities - available for sale | | | | | ||||||||

Total investment securities | $ | | $ | | $ | | $ | | ||||

Note 5: Loans Held for Investment

Loans held for investment, net of fair value adjustments, consisted of the following:

December 31, | June 30, | ||||||

(In Thousands) | 2023 |

| 2023 | ||||

Mortgage loans: |

|

|

|

|

| ||

Single-family | $ | | $ | | |||

Multi-family |

| |

| | |||

Commercial real estate |

| |

| | |||

Construction |

| |

| | |||

Other |

| |

| | |||

Commercial business loans |

| |

| | |||

Consumer loans |

| |

| | |||

Total loans held for investment, gross |

| |

| | |||

|

|

|

| ||||

Advance payments of escrows |

| |

| | |||

Deferred loan costs, net |

| |

| | |||

ACL on loans |

| ( |

| ( | |||

Total loans held for investment, net | $ | | $ | | |||

13

The following table sets forth information at December 31, 2023 regarding the dollar amount of loans held for investment that are contractually repricing during the periods indicated, segregated between adjustable rate loans and fixed rate loans. At December 31, 2023 and June 30, 2023, fixed-rate loans comprised

Adjustable Rate | ||||||||||||||||||

|

| After |

| After |

| After |

|

| ||||||||||

Within | One Year | 3 Years | 5 Years | |||||||||||||||

(In Thousands) | One Year | Through 3 Years | Through 5 Years | Through 10 Years | Fixed Rate | Total | ||||||||||||

Mortgage loans: | ||||||||||||||||||

Single-family | $ | | $ | | $ | | $ | | $ | | $ | | ||||||

Multi-family |

| |

| |

| |

| |

| |

| | ||||||

Commercial real estate |

| |

| |

| |

| — |

| |

| | ||||||

Construction |

| |

| — |

| — |

| — |

| — |

| | ||||||

Other |

| — |

| — |

| — |

| — |

| |

| | ||||||

Commercial business loans |

| |

| — |

| — |

| — |

| — |

| | ||||||

Consumer loans |

| |

| — |

| — |

| — |

| — |

| | ||||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | $ | | $ | | ||||||

The Corporation has developed an internal loan grading system to evaluate and quantify loans held for investment with respect to quality and risk. Management continually evaluates the credit quality of the loan portfolio and conducts a quarterly review of the adequacy of the ACL. The Corporation has adopted an internal risk rating policy in which each loan is rated for credit quality with a rating of pass, special mention, substandard, doubtful or loss.

The two primary components that are used during the loan review process to determine the proper allowance levels are individually evaluated allowances and collectively evaluated allowances. The collectively evaluated allowance is based on a pooling method for groups of homogeneous loans sharing similar loan characteristics to calculate an allowance which reflects an estimate of lifetime expected credit losses using historical experience, current conditions, and reasonable and supportable forecasts. Loans identified to be individually evaluated have an allowance that is based upon the appraised value of the collateral, less selling costs or discounted cash flow with an appropriate default factor.

The Corporation categorizes all of the loans held for investment into risk categories based on relevant information about the ability of the borrower to service their debt such as current financial information, historical payment experience, credit documentation, public information, and current economic trends, among other factors. A description of the general characteristics of the risk grades is as follows:

| ● | Pass - These loans range from minimal credit risk to average, but still acceptable, credit risk. The likelihood of loss is considered remote. |

| ● | Special Mention - A special mention loan has potential weaknesses that may be temporary or, if left uncorrected, may result in a loss. While concerns exist, the Corporation is currently protected and loss is considered unlikely and not imminent. |

| ● | Substandard - A substandard loan is inadequately protected by the current sound worth and paying capacity of the borrower or of the collateral pledged, if any. Loans so classified must have a well-defined weakness, or weaknesses, that may jeopardize the liquidation of the debt. A substandard loan is characterized by the distinct possibility that the Corporation will sustain some loss if the deficiencies are not corrected. |

| ● | Doubtful - A doubtful loan has all of the weaknesses inherent in one classified as substandard with the added characteristic that the weaknesses make collection or liquidation in full, on the basis of the currently existing facts, conditions and values, highly questionable and improbable. |

| ● | Loss - A loss loan is considered uncollectible and of such little value that continuance as an asset of the institution is not warranted. |

14

The following table presents the Corporation’s recorded investment in loans by risk categories and gross charge-offs by year of origination as of December 31, 2023:

December 31, 2023 | Term Loans by Year of Origination | Revolving | ||||||||||||||||||||||

(In Thousands) |

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| Prior |

| Loans |

| Total | ||||||||

Mortgage loans: | ||||||||||||||||||||||||

Single-family: | ||||||||||||||||||||||||

Pass | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | ||||||||

Special Mention | - | - | - | - | - | | - | | ||||||||||||||||

Substandard | - | - | - | - | - | | - | | ||||||||||||||||

Total single-family | | | | | | | | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Multi-family: | ||||||||||||||||||||||||

Pass | | | | | | | - | | ||||||||||||||||

Special Mention | - | - | | - | - | - | - | | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total multi-family | | | | | | | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Commercial real estate: | ||||||||||||||||||||||||

Pass | | | | | | | - | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total commercial real estate | | | | | | | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Construction: | ||||||||||||||||||||||||

Pass | | | | - | - | - | - | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total construction | | | | - | - | - | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Other: | ||||||||||||||||||||||||

Pass | - | - | - | | - | - | - | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total other | - | - | - | | - | - | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Commercial business loans: | ||||||||||||||||||||||||

Pass | - | | - | - | - | - | | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total commercial business loans | - | | - | - | - | - | | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Consumer loans: | ||||||||||||||||||||||||

Not graded | | - | - | - | - | - | - | | ||||||||||||||||

Pass | - | - | - | - | - | - | | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total consumer loans | | - | - | - | - | - | | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | ||||||||

Total current period charge-offs | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||

15

The following table presents the Corporation’s recorded investment in loans by risk categories by year of origination as of June 30, 2023:

June 30, 2023 | Term Loans by Year of Origination | Revolving | ||||||||||||||||||||||

(In Thousands) |

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| Prior |

| Loans |

| Total | ||||||||

Mortgage loans: | ||||||||||||||||||||||||

Single-family: | ||||||||||||||||||||||||

Pass | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | ||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | | - | | - | | ||||||||||||||||

Total single-family | | | | | | | | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Multi-family: | ||||||||||||||||||||||||

Pass | | | | | | | - | | ||||||||||||||||

Special Mention | - | - | | - | - | - | - | | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total multi-family | | | | | | | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Commercial real estate: | ||||||||||||||||||||||||

Pass | | | | | | | - | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | | - | | ||||||||||||||||

Total commercial real estate | | | | | | | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Construction: | ||||||||||||||||||||||||

Pass | | | | - | - | - | - | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total construction | | | | - | - | - | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Other: | ||||||||||||||||||||||||

Pass | - | - | - | | - | - | - | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total other | - | - | - | | - | - | - | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Commercial business loans: | ||||||||||||||||||||||||

Pass | - | | - | - | - | - | | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total commercial business loans | - | | - | - | - | - | | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Consumer loans: | ||||||||||||||||||||||||

Not graded | | - | - | - | - | - | - | | ||||||||||||||||

Pass | - | - | - | - | - | - | | | ||||||||||||||||

Special Mention | - | - | - | - | - | - | - | - | ||||||||||||||||

Substandard | - | - | - | - | - | - | - | - | ||||||||||||||||

Total consumer loans | | - | - | - | - | - | | | ||||||||||||||||

Current period gross charge-off | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | ||||||||

Total current period charge-offs | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||

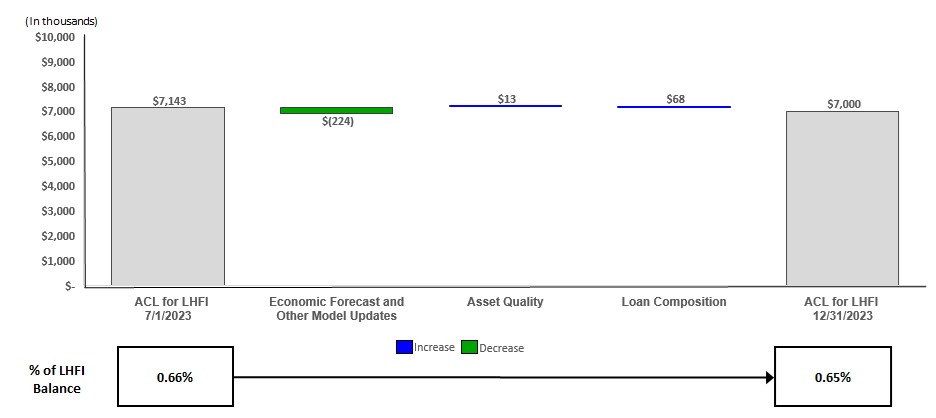

As required by ASC 326, on July 1, 2023 the Corporation implemented CECL and recognized a $

16

in order to group and determine portfolio loan segments with similar risk characteristics. The Corporation primarily utilizes historical loss rates for the CECL calculation based on its own specific historical losses and/or with peer loss history where applicable.

The expected loss rates are applied to expected monthly loan balances estimated through the consideration of contractual repayment terms and expected prepayments. The prepayment assumptions applied to expected cash flow over the contractual life of the loans are estimated based on historical and bank-specific experience and the consideration of current and expected conditions and circumstances including the level of interest rates. The prepayment assumptions may be updated by management in the event that changing conditions impact management’s estimate or additional historical data gathered has resulted in the need for a reevaluation.

For its reasonable and supportable forecasting of current expected credit losses, the Corporation utilizes a regression model using forecasted economic metrics and historical loss data. The regression model utilized upon implementation of CECL on July 1, 2023, and as of December 31, 2023, relied upon reasonable and supportable 12-month forecasts of the National Unemployment Rate and change in the Real Gross Domestic Product, aferwhich it reverts to a historical loss rate. Management selected the National Unemployment Rate and the Real Gross Domestic Product as the drivers of the forward look component of the collectively evaluated allowance, primarily as a result of high correlation coefficients identified in regression modeling, the availability of forecasts including the quarterly Federal Open Market Committee forecast, and the widespread familiarity with these economic metrics.

Management recognizes that there are additional factors impacting risk of loss in the loan portfolio beyond what is captured in the quantitative portion of allowance on collectively evaluated loans. As current and expected conditions, may vary compared with conditions over the historical lookback period, which is utilized in the calculation of quantitative allowance, management considers whether additional or reduced allowance levels on collectively evaluated loans may be warranted given the consideration of a variety of qualitative factors. The following qualitative factors (“Q-factors”) considered by management reflect the regulatory guidance on the Q-factors:

| ● | Changes in the experience, ability, and depth of lending management and other relevant staff. |

| ● | Changes in the value of underlying collateral for collateral-dependent loans. |

| ● | The existence and effect of any concentrations of credit, and changes in the level of such concentrations. |

| ● | Changes in international, national, regional, and local economic and business conditions and developments that affect the collectability of the portfolio, including the condition of various market segments. |

| ● | The effect of other external factors such as competition and legal and regulatory requirements on the level of estimated credit losses in the institution's existing portfolio. |

| ● | Changes in the volume and severity of past due loans, the volume of non-performing loans, and the volume and severity of adversely classified or graded loans. |

| ● | Changes in the quality of the Corporation’s loan review system. |

| ● | Changes in the nature and volume of the portfolio and in the terms of loans. |

| ● | Changes in lending policies and procedures, including changes in underwriting standards and collection, charge-off, and recovery practices not considered elsewhere in estimating credit losses. |

The qualitative portion of the Corporation’s allowance on collectively evaluated loans are calculated using management judgement, to determine risk categorizations in each of the Q-factors presented above. The amount of qualitative allowance is also contingent upon the relative weighting of the Q-factors according to management’s judgement.

Loans that do not share risk characteristics are evaluated on an individual basis. When management determines that foreclosure is probable and the borrower is experiencing financial difficulty, the expected credit losses are based on the fair value of collateral at the reporting date, less selling costs.

Accrued interest receivable for loans is included in the accrued interest receivable line item on the Corporation’s Condensed Consolidated Statements of Financial Condition. The Corporation elected not to measure an allowance for accrued interest receivable and instead elected to reverse accrued interest income on loans that are placed on non-performing status. A non-performing status is defined as when loans are 90 days or more delinquent and the Bank has stopped accruing interest income. Any outstanding interest receivable that has not been collected is reversed, disclosed

17

accordingly; and therefore, no allowance is established. The Corporation believes this policy results in the timely reversal of uncollectible interest.

Pursuant to ASU 2022-02, “Troubled Debt Restructurings and Vintage Disclosures,” the Corporation may agree to different types of modifications, including principal forgiveness, interest rate reductions, term extension, significant payment delay or any combination of modifications noted above. During the six months ended December 31, 2023, there were

Management believes the ACL on loans held for investment is maintained at a level sufficient to provide for expected losses on the Corporation’s loans held for investment based on historical loss experience, current conditions, and reasonable and supportable forecasts. The provision for (recovery of) credit losses is charged (credited) against operations on a quarterly basis, as necessary, to maintain the ACL at appropriate levels. Future adjustments to the ACL may be necessary and results of operations could be significantly and adversely affected as a result of economic, operating, regulatory, and other conditions beyond the Corporation’s control.

Non-performing loans are charged-off to their fair market values in the period the loans, or portion thereof, are deemed uncollectible, generally after the loan becomes

18

The following table is provided to disclose additional details for the periods indicated on the Corporation’s ACL on loans held for investment:

For the Quarter Ended |

| For the Six Months Ended |

| ||||||||||

December 31, | December 31, |

| |||||||||||

(Dollars in Thousands) |

| 2023 |

| 2022 |

| 2023 |

| 2022 |

| ||||

Allowance at beginning of period | $ | | $ | | $ | | $ | | |||||

Impact of ASC 326 CECL adoption(1) | — | — | | — | |||||||||

(Recovery of) provision for credit losses |

| ( |

| |

| ( |

| | |||||

Recoveries: |

|

|

|

|

|

|

|

| |||||

Mortgage loans: |

|

|

|

|

|

|

|

| |||||

Single-family |

| — |

| |

| — |

| | |||||

Total recoveries |

| — |

| |

| — |

| | |||||

Total charge-offs |

| — |

| — |

| — |

| — | |||||

Net recoveries (charge-offs) |

| — |

| |

| — |

| | |||||

Allowance at end of period | $ | | $ | | $ | | $ | |

| ||||

ACL as a percentage of gross loans held for investment |

| | % |

| | % |

| | % |

| | % | |

Net (recoveries) charge-offs as a percentage of average loans receivable, net, during the period (annualized) |

| % |

| ( | % |

| % |

| ( | % | |||

ACL as a percentage of gross non-performing loans at the end of the period | | % | | % | | % | | % | |||||

| (1) | Represents the impact of adopting ASC 326 on July 1, 2023. Since that date, as a result of adopting ASC 326, the methodology to compute the ACL has been based on CECL methodology, rather than the previously applied incurred loss methodology. |

The following tables denote the past due status of the Corporation's gross loans held for investment, net of fair value adjustments, at the dates indicated.

December 31, 2023 | ||||||||||||

30-89 Days Past | Total Loans Held for | |||||||||||

(In Thousands) |

| Current |

| Due |

| Non-Performing |

| Investment, Gross | ||||

Mortgage loans: | ||||||||||||

Single-family | $ | | $ | | $ | | $ | | ||||

Multi-family |

| |

| — |

| — |

| | ||||

Commercial real estate |

| |

| — |

| — |

| | ||||

Construction |

| |

| — |

| — |

| | ||||

Other |

| |

| — |

| — |

| | ||||

Commercial business loans |

| |

| — |

| — |

| | ||||

Consumer loans |

| |

| |

| — |

| | ||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | ||||

19

June 30, 2023 | ||||||||||||

|

| 30-89 Days Past |

|

| Total Loans Held for | |||||||

(In Thousands) | Current | Due | Non-Performing | Investment, Gross | ||||||||

Mortgage loans: | ||||||||||||

Single-family | $ | | $ | — | $ | | $ | | ||||

Multi-family |

| |

| — |

| — |

| | ||||

Commercial real estate |

| |

| — |

| — |

| | ||||

Construction |

| |

| — |

| — |

| | ||||

Other | |

| — |

| — |

| | |||||

Commercial business loans |

| |

| — |

| — |

| | ||||

Consumer loans |

| |

| |

| — |

| | ||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | ||||

The following tables summarize the Corporation’s ACL and recorded investment in gross loans, by portfolio type, at the dates and for the periods indicated.

| Quarter Ended December 31, 2023 |

| |||||||||||||||||||||||

Single- | Multi- | Commercial | Commercial | ||||||||||||||||||||||

(In Thousands) |

| family |

| family |

| Real Estate | Construction | Other |

| Business | Consumer | Total | |||||||||||||

ACL: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Allowance at beginning of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | — | $ | | |||||||||

(Recovery of) provision for credit losses | ( | ( | ( | ( | ( | | — | ( | |||||||||||||||||

Recoveries |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — | |||||||||

Charge-offs |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — | |||||||||

ACL, end of period | $ | $ | $ | $ | $ | $ | $ | — | $ | ||||||||||||||||

ACL: |

|

|

|

|

|

|

|

|

| ||||||||||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| — |

| | |||||||||

ACL, end of period | $ | $ | $ | $ | $ | $ | $ | — | $ | ||||||||||||||||

Loans held for investment: |

|

|

|

|

|

|

|

|

| ||||||||||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| |

| | |||||||||

Total loans held for investment, gross | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||

ACL as a percentage of gross loans held for investment |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % |

| — | % |

| | % | |

Net (recoveries) charge-offs to average loans receivable, net during the period | — | % | — | % | — | % | — | % | — | % | — | % | — | % | — | % | |||||||||

20

| Quarter Ended December 31, 2022 | ||||||||||||||||||||||||

Single- | Multi- | Commercial | Commercial | ||||||||||||||||||||||

(In Thousands) |

| family |

| family |

| Real Estate | Construction |

| Other | Business | Consumer | Total | |||||||||||||

ACL: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Allowance at beginning of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

Provision for (recovery of) credit losses |

| |

| ( |

| |

| ( |

| — |

| |

| |

| | |||||||||

Recoveries |

| |

| — |

| — |

| — |

| — |

| — |

| — |

| | |||||||||

Charge-offs |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — | |||||||||

ACL, end of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

ACL: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| |

| | |||||||||

ACL, end of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

Loans held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| |

| | |||||||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

ACL as a percentage of gross loans held for investment |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % | |

Net (recoveries) charge-offs to average loans receivable, net during the period | ( | % | — | % | — | % | — | % | — | % | — | % | — | % | — | % | |||||||||

21

Six Months Ended December 31, 2023 |

| ||||||||||||||||||||||||

Commercial | Commercial | ||||||||||||||||||||||||

(In Thousands) |

| Single-family |

| Multi-family |

| Real Estate |

| Construction |

| Other |

| Business |

| Consumer |

| Total |

| ||||||||

ACL: |

| ||||||||||||||||||||||||

Allowance at beginning of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

Adjustment to allowance for adoption of ASC 326 |

| |

| ( |

| ( |

| |

| |

| ( |

| ( |

| | |||||||||

Recovery of credit losses | ( | ( | ( | ( | ( | ( | — | ( | |||||||||||||||||

Recoveries |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — | |||||||||

Charge-offs |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — | |||||||||

ACL, end of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | — | $ | | |||||||||

ACL: | |||||||||||||||||||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| — |

| | |||||||||

ACL, end of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | — | $ | | |||||||||

Loans held for investment: | |||||||||||||||||||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| |

| | |||||||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

ACL as a percentage of gross loans held for investment |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % |

| — | % |

| | % | |

Net (recoveries) charge-offs to average loans receivable, net during the period | — | % | — | % | — | % | — | % | — | % | — | % | — | % | — | % | |||||||||

22

Six Months Ended December 31, 2022 |

| ||||||||||||||||||||||||

Commercial | Commercial | ||||||||||||||||||||||||

(In Thousands) |

| Single-family |

| Multi-family |

| Real Estate |

| Construction |

| Other |

| Business |

| Consumer |

| Total |

| ||||||||

ACL: |

| ||||||||||||||||||||||||

Allowance at beginning of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

Provision for (recovery of) credit losses |

| |

| |

| |

| ( |

| — |

| |

| — |

| | |||||||||

Recoveries |

| |

| — |

| — |

| — |

| — |

| — |

| — |

| | |||||||||

Charge-offs |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — | |||||||||

ACL, end of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

ACL: |

| ||||||||||||||||||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| |

| | |||||||||

ACL, end of period | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

Loans held for investment: |

| ||||||||||||||||||||||||

Individually evaluated for impairment | $ | | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | | |||||||||

Collectively evaluated for impairment |

| |

| |

| |

| |

| |

| |

| |

| | |||||||||

Total loans held for investment, gross | $ | | $ | | $ | | $ | | $ | | $ | | $ | | $ | | |||||||||

ACL as a percentage of gross loans held for investment |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % |

| | % | |

Net (recoveries) charge-offs to average loans receivable, net during the period | ( | % | — | % | — | % | — | % | — | % | — | % | — | % | — | % | |||||||||

23

The following tables identify the Corporation’s total recorded investment in non-performing loans by type at the dates and for the periods indicated. Generally, a loan is placed on non-performing status when it becomes 90 days past due as to principal or interest or if the loan is deemed impaired, after considering economic and business conditions and collection efforts, where the borrower’s financial condition is such that collection of the contractual principal or interest on the loan is doubtful. In addition, interest income is not recognized on any loan where management has determined that collection is not reasonably assured. A non-performing loan may be restored to accrual status when delinquent principal and interest payments are brought current, the borrower(s) has demonstrated sustained payment performance and future monthly principal and interest payments are expected to be collected on a timely basis. Loans with a related allowance have been (a) collectively evaluated using a pooling method analysis or (b) individually evaluated for impairment using either a discounted cash flow analysis or, for collateral dependent loans, current appraisals less costs to sell, to establish realizable value. This analysis may identify a specific impairment amount needed or may conclude that no allowance is needed.

At December 31, 2023 | |||||||||||||||

Unpaid | Net | ||||||||||||||

Principal | Related | Recorded | Recorded | ||||||||||||

(In Thousands) |

| Balance |

| Charge-offs |

| Investment |

| Allowance(1) |

| Investment | |||||

Mortgage loans: | |||||||||||||||

Single-family: |

|

|

|

|

|

|

|

|

|

| |||||

With a related allowance | $ | | $ | — | $ | | $ | ( | $ | | |||||

Without a related allowance(2) |

| |

| ( |

| |

| — |

| | |||||

Total single-family loans |

| |

| ( |

| |

| ( |

| | |||||

Total non-performing loans | $ | | $ | ( | $ | | $ | ( | $ | | |||||

| (1) | Consists of an ACL, specifically assigned to the individual loan. |

| (2) | There was no related ACL because the loans were charged-off to their fair value or the fair value of the collateral was higher than the loan balance. |

At June 30, 2023 | |||||||||||||||

Unpaid | Related | Net | |||||||||||||

Principal | Charge-offs | Recorded | Recorded | ||||||||||||

(In Thousands) |

| Balance |

| Related |

| Investment |

| Allowance(1) |

| Investment | |||||

Mortgage loans: |

|

|

|

|

|

|

|

|

|

| |||||

Single-family: |

|

|

|

|

|

|

|

|

|

| |||||

With a related allowance | $ | | $ | — | $ | | $ | ( | $ | | |||||

Without a related allowance(2) |

| |

| ( |

| |

| — |

| | |||||

Total single-family loans |

| |

| ( |

| |

| ( |

| | |||||

Total non-performing loans | $ | | $ | ( | $ | | $ | ( | $ | | |||||

| (1) | Consists of an ACL, specifically assigned to the individual loan. |

| (2) | There was no related ACL because the loans were charged-off to their fair value or the fair value of the collateral was higher than the loan balance. |

At December 31, 2023, there were

For the quarters ended December 31, 2023 and 2022, the Corporation’s average recorded investment in non-performing loans was $

24

For the six months ended December 31, 2023 and 2022, the Corporation’s average recorded investment in non-performing loans was $

The following tables present the average recorded investment in non-performing loans and the related interest income recognized for the quarters and six months ended December 31, 2023 and 2022:

Quarter Ended December 31, | ||||||||||||

2023 | 2022 | |||||||||||

Average | Interest | Average | Interest | |||||||||

Recorded | Income | Recorded | Income | |||||||||

(In Thousands) |

| Investment |

| Recognized |

| Investment |

| Recognized | ||||

Without related allowances: |

|

|

|

|

|

|

|

| ||||

Mortgage loans: |

|

|

|

| ||||||||

Single-family | $ | | $ | | $ | |

| $ | — | |||

|

| |

| |

| |

|

| — | |||

With related allowances: |

|

|

|

|

|

| ||||||

Mortgage loans: | ||||||||||||

Single-family |

| |

| |

| |

|

| | |||

|

| |

| |

| |

|

| | |||

Total | $ | | $ | | $ | |

| $ | | |||

Six Months Ended December 31, | ||||||||||||

2023 | 2022 | |||||||||||

Average | Interest | Average | Interest | |||||||||

Recorded | Income | Recorded | Income | |||||||||

(In Thousands) |

| Investment |

| Recognized |

| Investment |

| Recognized | ||||

Without related allowances: |

|

|

|

|

|

|

|

| ||||

Mortgage loans: |

|

|

|

| ||||||||

Single-family | $ | | $ | | $ | |

| $ | — | |||

| |

| |

| |

| — | |||||

With related allowances: |

|

|

|

| ||||||||

Mortgage loans: | ||||||||||||

Single-family | |

| |

| |

| | |||||

| |

| |

| |

| | |||||

Total | $ | | $ | | $ | |

| $ | | |||

During the quarters and six months ended December 31, 2023 and 2022,

25

As outlined in the implementation of ASC 326, the Bank includes the off-balance sheet reserve for unfunded loan commitments within the provision for credit losses.

The following table provides information regarding the unfunded loan commitment reserve for the quarters and six months ended December 31, 2023 and 2022.

For the Quarter Ended | For the Six Months Ended | |||||||||||

December 31, | December 31, | |||||||||||

(In Thousands) |

| 2023 |

| 2022 |

| 2023 |

| 2022 | ||||

Balance, beginning of the period | $ | | $ | | $ | | $ | | ||||

Impact of ASC 326 CECL adoption |

| — |

| — |

| — |

| — | ||||

Recovery of credit losses | ( | ( | ( | ( | ||||||||

Balance, end of the period | $ | | $ | | $ | | $ | | ||||

The method for calculating the unfunded commitment reserve is based on a historical funding rate applied to the undisbursed loan amount to estimate an average outstanding amount during the life of the loan commitment. The Corporation applies the same assumptions and methodologies by loan groupings to these unfunded loan commitments as it does for its funded loans held for investment to determine the reserve rate and the allowance. Assumptions are evaluated by management periodically as part of the CECL procedures. The unfunded commitment reserve is recorded in Accounts payable, accrued interest and other liabilities on the Condensed Consolidated Statements of Financial Condition.

Note 6: Derivative and Other Financial Instruments with Off-Balance Sheet Risks