REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Title of Class |

Trading Symbol |

Name of Each Exchange on Which Registered | ||

* |

||||

Representing One Ordinary Share, 25p per Ordinary Share |

| * |

Ordinary Shares, 25p par value |

☐ US GAAP |

☒ as Issued by the International Accounting Standards Board |

☐ Other |

| Former Auditor Firm ID | Former Auditor Name | Former Auditor Location | ||||||||||||||

| Auditor Firm Id: | 0 |

Auditor Name: | Auditor Location: |

Strategic progress. Sustainable profitable growth. Annual report and accounts 2023

We are the world’s leading learning company

| Strategic report |

||||

| At a glance | 2 | |||

| Chair’s note | 3 | |||

| Chief Executive’s review | 6 | |||

| Divisional overviews | 8 | |||

| 2023 highlights | 11 | |||

| Strategic priorities | 12 | |||

| Divisional spotlights | 14 | |||

| Stakeholder engagement | 16 | |||

| Business model | 22 | |||

| Key performance indicators | 24 | |||

| Financial review | 26 | |||

| Sustainability | 34 | |||

| ESG data | 49 | |||

| Risk | 56 | |||

| Governance report | ||||

| Corporate governance | 66 | |||

| Directors’ remuneration report | 107 | |||

| Additional disclosures | 131 | |||

| Financial statements | ||||

| Consolidated financial statements | 146 | |||

| Other information | ||||

| Five-year summary | 219 | |||

| Financial key performance indicators | 221 | |||

| Additional information for US listing purposes | 227 | |||

| Shareholder information | 247 | |||

The strategic report, up to and including page 65, was approved for issue by the Board on 13 March 2024 and signed on its behalf by:

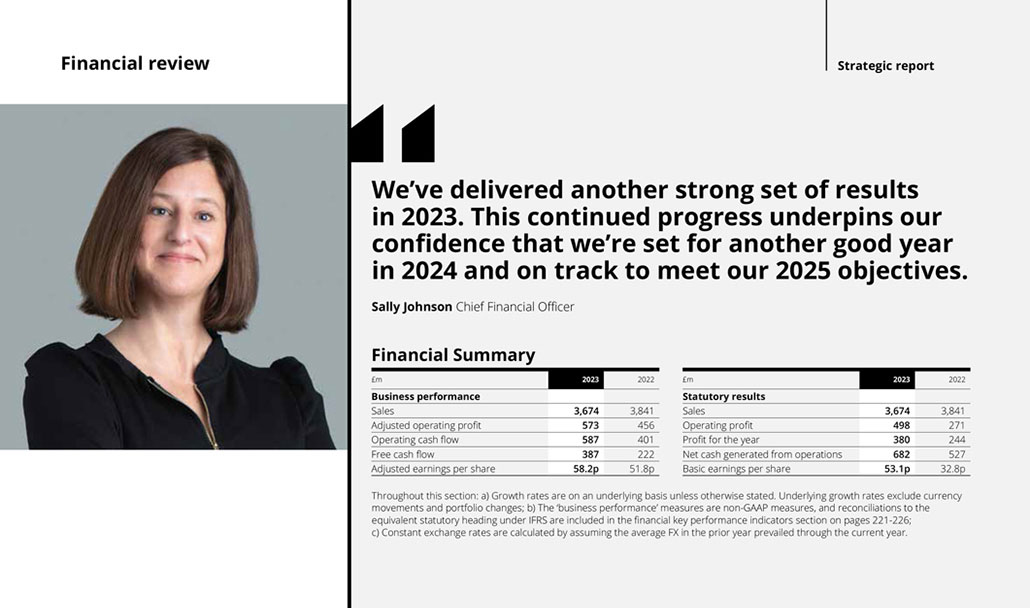

Sally Johnson Chief Financial Officer

Use this QR code to visit our Pearson plc website where you can find the online version of this report.

|

https://plc.pearson.com/en- GB/investors/2023-annual- report-accounts

|

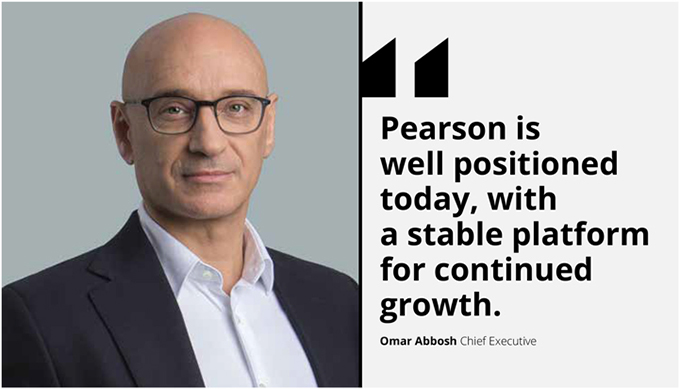

Strategic progress. Sustainable profitable growth. Pearson is a strong company with excellent market potential, people committed to our mission, and a purpose that can genuinely help communities. Omar Abbosh Chief Executive

| At a glance | Strategic report | |

|

Corporate overview

At Pearson, we know few things matter to the world more than education. That’s why we’re all working together to support people on their learning journey, wherever that path takes them. We’re on a journey too, building a company that puts learners at the heart of everything we do.

The future of learning is vibrant, high quality learning experiences that help everyone realise the life they imagine. 2023 has been a critical year in Pearson’s progress toward achieving our vision. A changing global economy, a need for new and different skills within communities, and new technology like generative AI challenged

|

the education space. Our resilience and ability to capitalise on changing market dynamics reinforced confidence in our strategy, our people, and the strength of our underlying business. As we look ahead to 2024, we remain committed to our goal of delivering long-term profitable growth, while we evolve our strategy to seize emerging opportunities and accelerate our digital expansion.

This Annual Report showcases strong 2023 growth, driven by our five divisions and our continued efforts to create interconnectivity between them. By delivering excellent financial results, driving a culture of performance, and leaning into new technology, like generative AI, we’re making progress every day toward a future of sustainable, profitable growth for 2024 and beyond. | |

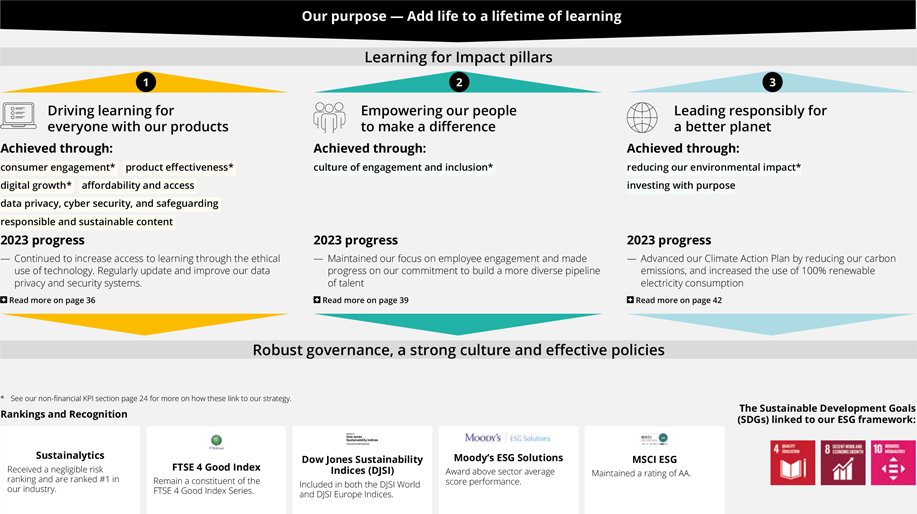

Our sustainable business pillars

|

|

| ||

| Driving learning for everyone | Empowering our people | Leading responsibly for | ||

| with our products | to make a difference | a better planet | ||

Read more on Sustainability on page 34

Read more on Sustainability on page 34

Our purpose

To add life to a lifetime

of learning.

Our vision

We want everyone to realise the life they imagine through learning.

Our mission

Create vibrant and enriching learning experiences designed for real-life impact.

| Annual report and accounts 2023 Pearson plc 2 |

| Chair’s note | Strategic report | |

| 2023 full year dividend growth

6%

Return on capital in 2023

10.3% |

Overview

I am delighted to report that Pearson colleagues around the world have delivered another strong performance in 2023. It has been a transformational year for the business, further testament to the strategy we launched three years ago that has fundamentally repositioned Pearson so that we can serve ever more people through their lifelong learning journey. Our reshaped portfolio is more focused, we are firmly established as a digital-first learning company and technology is opening up exciting opportunities that will drive growth for many years to come.

Our culture has evolved significantly so that there is now a far greater sense of accountability across the global business and an increased focus on execution and delivery. There is also more interconnectivity across our divisions with growing collaboration underpinned by a shared belief in the important role Pearson plays in improving society through learning.

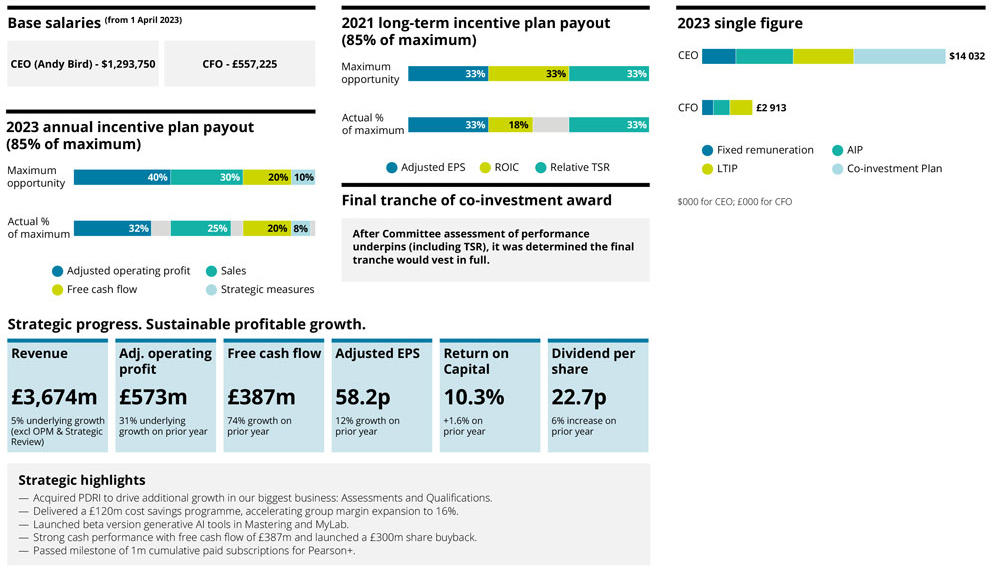

Financial and operational highlights

For a third consecutive year, Pearson has delivered a strong financial performance with sales of £3,674m (£3,841m in 2022), representing 5% growth on an underlying basis, excluding the OPM and Strategic Review businesses. Statutory operating profit was £498m (£271m in 2022), or £573m on an adjusted basis, up 31% versus 2022. This was supported by our ongoing work to streamline the business and make it more efficient. During the year we successfully delivered £120m of cost savings, improving adjusted operating profit margin to 16%.

Pearson has continued to generate strong free cash flow enabling us to maintain a robust financial position whilst also supporting ongoing investment in the business. This is fuelling Pearson’s evolution, particularly in digital and generative AI which are changing the way that people learn for good.

Our strong cash generation enables us to deliver returns for shareholders, with a £300m share buyback programme commenced in 2023 supplementing our progressive ordinary dividend. We have also announced that we will be extending this programme by £200m in 2024. Reflecting the strong performance in 2023 and its confidence in the outlook for the business, the Board is recommending a 6% increase in the final dividend for a full year dividend of 22.7 pence per share.

This will be paid on 3 May 2024 to shareholders on the register on 22 March 2024.

| Annual report and accounts 2023 Pearson plc 3 |

| Chair’s note continued | Strategic report | |

CEO succession

In September, we announced that Andy Bird would be retiring from his role as our Chief Executive. On behalf of the Board and all the Group’s stakeholders, I would like to thank Andy for his outstanding leadership, and his implementation of the ambitious vision and strategy that have successfully transitioned Pearson into the business we are today. During his tenure, adjusted operating profit has increased from £313m to £573m, and shareholders have benefited from a total 3-year return of 53%. Andy has accelerated our digital proposition and capability so that 82% of our portfolio today is digital or digitally-enabled. The launch of Pearson+ in July 2021 has been an important contributor, bringing us meaningfully closer to consumers and the platform had grown to around 5m registered users by the end of the full calendar year.

AI has been part of Pearson’s DNA for many years, and under Andy’s stewardship, we have leveraged advances in generative AI to enhance the value of our content with plans to make it available to millions more students across key titles in the year ahead. Having also put in place a strong management team, Andy leaves Pearson well-placed for the future.

Following a thorough selection process, which you can read more about on pages 83 and 91 respectively, the Board was delighted to appoint Omar Abbosh to succeed Andy. Omar is an inspirational, dynamic and growth-orientated leader with deep commercial, technology and operational expertise focused on delivering high-quality services and products across diverse markets and customer sets. He has extensive experience in creating and executing strategies to enable companies to harness technology and succeed in a world of disruptive change. He shares our values and our ambition and has a strong track record of execution. Omar joined us in January 2024 and the Board and I are enjoying working with him as we accelerate our strategy and continue to deliver value for all our stakeholders.

Learning for impact

With our purpose of adding life to a lifetime of learning, we are focused on delivering Learning for Impact. We take a considered approach to the adoption of technologies such as generative AI that have enormous potential but also entail new risks, and we are committed to the highest standards of data privacy and security. We empower our people to make a difference, making further progress on employee engagement in the year as we continue to invest in talent and drive a culture of belonging that aims for increasingly diverse representation throughout the company. We recognise our responsibility to reduce our environmental impact, and are on track to meet our target of halving our carbon emissions by 2030, having made excellent progress to date, with a reduction of 16% vs 2022. This is the product of many different initiatives across our operations and supply chain, with significant benefits coming from our strategy to become increasingly digital, reducing the footprint and impacts of our print operations.

The Board

We have a strong, diverse and highly experienced Board which continues to offer valuable perspective, insight and leadership. There were some changes to the Board during the year due to retirement, giving us the opportunity to welcome new talent and fresh thinking.

In June, we were delighted to welcome two new Non-Executive Directors, Alison Dolan and Alex Hardiman. Alison has been Chief Financial Officer at Rightmove plc since 2020 and brings extensive commercial and operational finance experience, specifically in digital businesses. Alex currently serves as The New York Times’ Chief Product Officer and was previously at Facebook where she served as Head of News Products.

Tim Score, Deputy Chair and Senior Independent Director, will step down from the Board at the AGM in April 2024 following a nine year tenure. His vast experience has been enormously valuable to Pearson and I would like to thank him hugely for the significant contribution that he has made to the business. I am pleased that Graeme Pitkethly will be taking over the role as Deputy Chair and Senior Independent Director once Tim has stepped down.

| Annual report and accounts 2023 Pearson plc 4 |

| Strategic report | ||

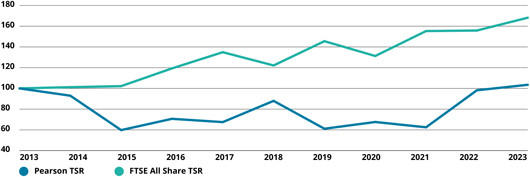

Total 1-year

shareholder return

5%

Governance

Through my face-to-face meetings with investors during the past year, I have heard first-hand views on a range of topics including strategy, succession, corporate governance, remuneration, environmental and social issues, as well as operational and financial performance. We have taken all their feedback and again sought to enhance our disclosures in this Annual Report. I look forward to hearing how we can continue to improve.

We have engaged extensively over the past year on remuneration with shareholders and their advisors, and executive remuneration remains a key area of focus for both the Board and the Remuneration Committee. The directors’ remuneration policy that was approved at last year’s AGM seeks to ensure that we can attract and retain the talent required to drive Pearson’s success; that our executives are appropriately incentivised to achieve stretching targets; and that the structure of such incentives best aligns with the interests of shareholders and supports the delivery of long-term, sustainable returns. It’s important to underline that incentives will only be realised in full if stretching annual and longer-term performance targets are met. Sherry Coutu CBE, Chair of the Remuneration Committee, sets out our approach on pages 107-109.

Outlook

Our strong performance in 2023 underpins our confidence that we have the right strategy in place to drive continued sustainable growth. Our robust financial position and strong cash generation enable investment to strengthen our platform for the future while also funding attractive distributions to shareholders. We are excited about the experience and expertise that Omar brings to Pearson. Pearson is well-placed to make good progress in the year ahead and beyond.

Omid Kordestani Chair

| Annual report and accounts 2023 Pearson plc 5 |

| Chief Executive’s review | Strategic report | |

| Sales £3,674m (2022: £3,841m) headline decrease of 4%

Underlying sales growth increase 5%* |

Statutory operating profit £498m increase year on year of 84%

Adjusted operating profit in 2023 £573m increase year on year of 31% on an underlying basis |

| * | Taking portfolio adjustments and FX into account and excluding the OPM and Strategic Review businesses. |

Dear Shareholders,

I want to start by sharing how delighted I am to join this very special company alongside this talented and passionate group of Pearson employees.

I’m pleased to report another year of strong financial performance with underlying sales growth of 5% and adjusted operating profit of £573m, up 31% compared to 2022. We have also improved the adjusted operating profit margin by 4% to 16%. This has been driven by our strong execution and the combination of our unique capabilities in assessment, content, and services, all of which stand us in good stead going forward.

Delivering for Growth

These results reflect exciting progress across the business and especially strong financial performance in Assessment & Qualifications and English Language Learning. Further, our commitment to cost efficiencies delivered £120m in savings for the Group. Our careful stewardship of shareholder funds means we launched a share buyback of £300m in 2023 and announced an extension of this by a further £200m in 2024. Our strong balance sheet and excellent cash flows help us invest in opportunities to drive growth and create further value for our stakeholders.

Several strategic achievements in 2023 also laid the foundation for our future:

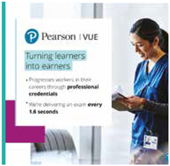

| — | In Assessment & Qualifications, we saw strong performance in Pearson VUE, particularly in the IT and healthcare sectors. We completed the acquisition of PDRI, a trusted provider of workforce assessment services. In this business, we are already seeing promising revenue generation and new contracts with the US federal government. |

| — | In English Language Learning, we won recognition for the Pearson Test of English in Canada for student and economic migration visas. With English as the gateway to employment and study in Canada, this opens a significant new business opportunity for us. In partnership with Pearson VUE, we opened our largest test centre, to help serve the growing PTE market in India. We also launched workplace specific content as well as other enhanced features in Mondly. |

| Annual report and accounts 2023 Pearson plc 6 |

| Strategic report | ||

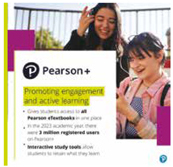

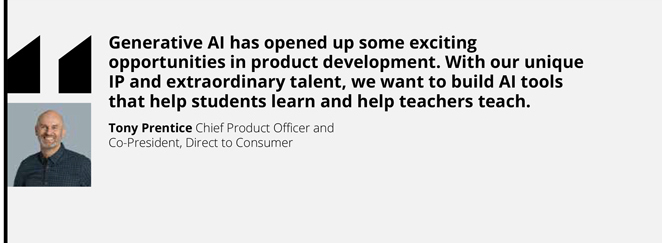

| — | Generative AI was a major focal point in Higher Education as we began the beta of our AI tools in Mastering and Pearson+. With over 60,000 AI conversations in Mastering Chemistry alone, we are helping students learn the most complex concepts. The positive student reaction to the tools led us to expand the beta for 2024. What’s more, Pearson+ passed the milestone of one million paid subscriptions this calendar year. All of this taken together with improved platform stability and improvements in our sales teams, meant Pearson’s Higher Education division increased platform sales while making significant strides in its overall digital consumer experiences. |

| — | Within our Workforce Skills business, we evolved from a unified product approach to building a powerful technology stack that has enabled us to expose the core capabilities as modular offerings that can be tailored to our customers. This is just one element underpinning the solid sales figures we saw in 2023. |

| — | Virtual Learning launched a new Connections Academy Career Pathways programme in five schools to offer students high school, university, and career credentials through an innovative tri-credit approach. We plan to roll out the initiative to more schools in 2024. |

| — | Finally, in a major step toward the simplification of our portfolio, we completed the sale of our Pearson Online Learning Services business in June. |

This progress could not have happened without the leadership of Andy Bird. He paved the way for us, and I’d like to thank him for laying the groundwork for our bright days ahead.

Looking Forward with Confidence

Since I joined Pearson, I’ve become even more confident about the reasons I came here.

First, it’s clear to me that Pearson is a strong, stable company with many growth options. Second, we have a purpose that is unmatched and a genuine ability to help people on their learning journey which, quite literally, changes lives. Finally, our world is also at an inflection point with AI. The next decade will centre on the application of AI in business, in communities, and in our individual lives.

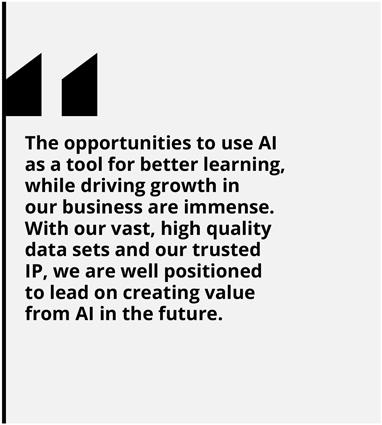

The opportunities to use AI as a tool for better learning, while driving growth in our business are immense.

With our vast, high quality data sets and our trusted IP, we are well positioned to lead on creating value from AI in the future.

It’s against this backdrop that I’m setting three strategic priorities for 2024. Firstly, we will deliver on our 2024 guidance with an intense focus on organic growth, execution, and the needs of our customers. Secondly, we are sharpening our focus on the enterprise market. This is a large and still forming market, with no dominant player and presents good opportunity for us. Thirdly, we’re optimistic about the possibilities that AI brings.

We are increasing the energy by which we infuse our products and services with AI solutions that delight and support customers and consumers.

A Future Built on Our Strengths

At Pearson we do three things. We create and curate world class learning and assessment content. We distribute this content digitally and through physical materials to millions of users globally. And we help individuals, employers and institutions build and verify skills.

These activities are made possible by our unique strengths, such as our long term and diverse customer relationships; the global size and scale of our Pearson VUE business; the depth and quality of our content in textbooks, assessments, videos, and exams; our network of trusted authors; the differentiated Global Scale of English; our deep expertise in learning science; and above all, our trusted and well-respected brand.

These strengths are a testament to the wonderful people of Pearson, and I want to thank them for their contribution to our success in 2023. I am excited for their partnership as we evolve our company to meet the diverse needs of learners around the world.

I believe Pearson is that rare type of company with an ability to deliver sustainable growth alongside a purpose that is meaningful to millions of people.

There is much more to come from Pearson.

Omar Abbosh Chief Executive

Free cash flow in 2023

£387m

| Annual report and accounts 2023 Pearson plc 7 |

| Divisional overviews | Strategic report | |

Assessment & Qualifications

The Assessment & Qualifications division comprises four business units: Pearson VUE, Clinical Assessment, US Student Assessment, and UK & International School Qualifications. Pearson VUE excels as a global leader in scaled testing services, serving numerous industry sectors with its extensive test centre network and flexible delivery options. This line of business meets the critical need for workforce reskilling and professional certification, underpinning professional development at various stages. In Clinical Assessment, Pearson provides high-quality, research-backed assessment products for mental health and learning evaluations, serving professionals in healthcare and education.

Pearson’s US Student Assessment specialises in customised large-scale testing programmes for US K-12 education, focusing on state-specific criteria and enhancing education standards. Internationally, Pearson offers globally recognised UK curriculum based qualifications such as GCSEs and A-levels, as well as courseware for English speaking regions throughout the world, supporting foundational student progression worldwide. These qualifications, coupled with Pearson’s content expertise and scale of delivery, make it a key player in shaping global education standards and student futures.

In 2023, the division demonstrated strong financial performance, growth, and overall customer retention. 2024 will focus on maintaining strong competitive positions through contract renewals and new wins, while scaling value chain and adjacent market opportunities.

Select plans include VUE moving further up the technology certification value chain, UK & International Qualifications capitalising on the growing demand for international education and Clinical Assessment building out its international portfolio and creating new digitally-enabled business subscription models.

Virtual Learning

Following the sale of the Pearson Online Learning Services business in the first half of 2023 and the loss of the ASU contract, the Virtual Learning business now works with customers in three ways: Partner Schools (c.95% sales), District Partnerships (c.3% sales), and Pearson Online Academy (c.2% sales).

The Partner Schools business provides tailored Virtual School solutions to public K-12 districts in the US, combining Pearson’s courseware, instructional services, and support for high-quality, flexible online learning. Although providing much smaller revenue contribution, the District Partnerships channel offers customisable virtual education solutions for K-12 districts, focusing on smaller student cohorts with a more disaggregated approach than Partner Schools, ensuring access to quality, adaptable remote learning for various needs. We also offer Pearson Online Academy, which while small, extends similar services to Partner Schools but as a private, globally accessible option.

Virtual Learning launched a new Connections Academy Career Pathways programme in five schools for middle and high school students, where we are offering a tri-credit approach to career-readiness courses in partnership with Coursera and Acadeum, amongst others. We saw encouraging enrolment trends in these schools and are planning to roll the initiative out to additional schools in 2024 to drive future growth.

| Annual report and accounts 2023 Pearson plc 8 |

| Strategic report | ||

Higher Education

Pearson is the market leader in providing world-class learning experiences in the post-secondary market. Renowned as a market leader in both eText and courseware products, including MyLabs, Mastering, Pearson+ and Revel, Pearson caters to millions of students worldwide.

Pearson’s goal is to scale teaching excellence, enhance learner outcomes, and to support faculty in their workflows. Pearson’s strength lies in its relationship with authors, its proprietary educational technology platforms, and deep understanding of learning science, all of which are evolving with the AI landscape. Pearson’s close relationships with instructors and faculty, who play a key role in adopting course materials, contribute significantly to its competitive edge.

In 2023, Pearson was the first major higher education publisher to integrate generative AI study tools into its propriety academic content. It also grew Pearson+ subscriptions, adding over 1 million eTextbook subscriptions during the calendar year. In the upcoming year, the focus is on scaling AI-enhanced offerings and continuing to deliver outstanding value for learners and faculty with significant product upgrades.

English Language Learning

Our vision is to become the world’s leading destination for committed learners to build and prove their proficiency in English, offering comprehensive English learning and assessment solutions, including the Pearson Test of English (PTE). Catering to a wide range of learners, including those in workplaces, schools (via institutional courseware and the Wizard platform), and individuals (through Mondly), Pearson provides diverse avenues for English proficiency. Central to Pearson’s approach is the blend of leading pedagogical expertise in English language education with advanced technology. This strategy is geared towards delivering personalised, scalable English language learning for anyone seeking to use English for their personal or professional goals.

English Language Learning expanded partnerships and grew the PTE business in 2023, administering over 1 million tests. The 2024 strategy includes scaling the PTE business in Canada and growing corporate assessment and study offerings, leveraging technological advancements.

| Annual report and accounts 2023 Pearson plc 9 |

| Divisional overviews continued | Strategic report | |

Workforce Skills

The Workforce Skills division at Pearson includes both Vocational Qualifications (VQ) and Workforce Solutions. Pearson VQ is a global leader in career-focused qualifications, offering programmes that are rooted in real-world work scenarios. These qualifications enable hundreds of thousands of students, apprentices, and workers in the UK and globally to develop and apply knowledge, skills, and behaviours essential for employability. One in five working-age individuals in the UK holds a BTEC from Pearson, and its vocational qualifications are increasingly adopted by global ministries of education to advance skills reform.

Pearson Workforce Solutions addresses the evolving needs of businesses for skilled talent in a rapidly changing economy. Workforce Solutions assists companies in understanding and bridging their skills gaps, fostering genuine skills development aligned with commercial objectives. Pearson’s corporate and employee solutions are modular and interconnected by a common skills framework, supporting organisations at various stages of their skills transformation journey and optimising their existing tools for maximum impact.

2023 saw us deliver a solid performance, with our qualifications performing well in institutional and corporate markets, and Workforce Solutions continuing to acquire new customers and expand existing relationships. The 2024 agenda includes driving market share gains, expanding addressable markets, and developing upskilling and reskilling solutions through key partnerships.

| Annual report and accounts 2023 Pearson plc 10 |

| 2023 highlights | Strategic report | |

A year of strategic and operational progress

|

|

Sales £3,674m (2022: £3,841m) headline

decrease of 4%

| |

|

|

Underlying sales growth increase of 5%*

| |

|

|

Statutory operating profit £498m increase year on year of 84%

| |

|

|

Adjusted operating profit £573m increase year on year of 31% on an underlying basis

|

| * | Taking portfolio adjustments and FX into account and excluding the OPM and Strategic Review businesses |

|

Acquired PDRI

| |

|

Delivered £120m cost savings, accelerating Group adjusted operating profit margin expansion to 16%

| |

|

|

Launched beta versions of generative AI tools in Mastering and MyLab and Pearson+

| |

|

|

Strong cash performance, with free cash flow of £387m, and launched a £300m share buyback

|

Read more on page 32

Read more on page 32

|

|

Passed milestone of 1m cumulative paid subscriptions for Pearson+

|

| Annual report and accounts 2023 Pearson plc 11 |

| Strategic priorities | Strategic report | |

|

An integrated strategy |

|

Our corporate strategy is grounded in three primary objectives – 1) to deliver sustainable, profitable sales growth, 2) to focus on execution, quality, and trust across the business, and 3) to delight our customers and be obsessed with meeting their expectations. We will achieve these objectives through our continued dedicated commitment to building trusted relationships with consumers throughout their lifelong learning journey via an ecosystem of interconnected solutions.

Realising this vision will require us to remain focused on increasing our scale and reach by investing in and deepening our institutional, enterprise, government, and direct to consumer relationships. We will continue to capitalise on synergies across our businesses and lean into our competitive strengths, most notably as a global leader in trusted learning content and assessments.

We believe that by enabling consumers with best-in-class, integrated tools for learning, along with the assessments and credentials to demonstrate their knowledge and skills, we will create lasting value for our customers, learners, and other stakeholders, whilst delivering outsized growth for our investors.

Strategic Priority #1: Pearson’s commitment to sustainable and profitable revenue growth yielded important achievements across its divisions, underlining the company’s market-leading capabilities and strategic execution. Looking to 2024, Pearson’s strategic focus remains steadfast on continuing to deliver profitable revenue growth, with each division poised to expand its market impact through targeted initiatives.

| Strategic priority | Progress in FY23 | Objectives for FY24 | ||||||

| Deliver sustainable and profitable revenue growth |

|

Acquired PDRI in March 2023, leading to major federal contract wins with the TSA and US Air Force |

|

Scale value chain and adjacent market opportunities across sub-divisions, with a continued drive to grow within the federal market by providing secure and scalable testing services tailored to the government workforce

| ||||

|

Invested in product improvements and implemented new sales teams and processes, in addition to achieving a profitability increase of 3% driven by cost savings |

|

Pilot innovative courseware pricing models to drive competitiveness in the growing Open Educational Resources (OER) and Do-It-Yourself (DIY) market segments, whilst continuing to drive international market growth with targeted investments in the Higher Education sector

| |||||

|

Grew PTE volumes c.50% to over 1m tests administered and earned recognition for the Student Direct Stream and Migration in Canada |

|

Further scale the PTE business and continue to gain market share in Canada, as well as expand the corporate offerings for assessment and study by leveraging the flexibility of the Mondly and Versant (mid-stakes assessment) platforms

| |||||

|

|

Launched and enrolled over 1k students in an innovative career readiness offering |

|

Transform the enrolment funnel to bring down the lead-to-enrolment time to 1-2 weeks, a c.75% reduction, aiming to improve student acquisition and retention

| |||||

|

Expanded workforce reach to 66 of the Fortune 500 companies, achieving a growth rate of 11% |

|

Invest in skills intelligence, credentialing, and assessment solutions, and evolve corporate solutions from single to multi-product sales

| |||||

|

Grew the Pearson+ platform to around 5m registered users by end of calendar year 2023 and passed the milestone of 1m cumulative paid subscriptions for the same calendar year |

|

Drive Pearson+ growth by expanding distribution and further scaling Channels subscriptions |

| Annual report and accounts 2023 Pearson plc 12 |

| Strategic report | ||

Strategic Priority #2: Pearson’s focus on execution, quality, and trust across its business divisions led to significant achievements, reinforcing its position as a leader in educational services and products. Looking forward, Pearson is set to further strengthen this commitment across all business divisions, with a clear focus on innovation and strategic development.

| Strategic priority | Progress in FY23 | Objectives for FY24 | ||||||

| Focus on execution, quality, and trust across the business |

|

Launched the Pearson Assessment for Learning Suite - a complementary set of services for US school districts

|

|

Invest in product and platform development to improve and expand go-to-market efforts in 2024

| ||||

|

|

Retained the market-leading position within the Higher Education space driven by reaffirming commitment to sales leadership and enhancing execution capability

|

|

Continue to develop innovative AI features and product enhancements

| |||||

|

|

Launched an enhanced e-commerce journey and fortified relationships with key PTE regional partners

|

|

Invest in digital platforms and experiences, and utilise the Mondly platform as a versatile tool for trialling technology capabilities and propositions

| |||||

|

|

Reduced marketing cost per enrolment by approximately 25% over the last year, significantly improving operational efficiency

|

|

Target development of an additional 15 career programmes, up from five last year, and scale to new schools and states

| |||||

|

|

Improved performance in qualification result delivery within Vocational Qualifications ensuring learners had their results when needed

|

|

Prioritise technology based strategic projects, such as leveraging AI in quality assurance within the enterprise qualifications businesses

| |||||

|

|

Enhanced Pearson+ from primarily an e-reading platform to a more robust educational resource by introducing Channels, delivering tutorial video content and practice problems |

|

Expand course offerings available on the Channels platform, building on the 23 college courses supported in 2023 |

Strategic Priority #3: Pearson’s dedication to delighting customers and providing exceptional educational experiences was evident across all divisions. Looking ahead, the divisions will continue to drive this strategic initiative, ensuring that customer satisfaction remains at the forefront of the company’s operations.

| Delight our customers and be obsessed with meeting their expectations |

|

Improved standards of customer care across the A&Q businesses, with examples including shifting from a regional to global approach model, in addition to VUE opening its largest company-owned test centre in Chandigarh, India, with capacity to deliver 14k high-stakes tests per month

|

|

Expand VUE value chain capabilities into learning and test prep for the technology certification segment, and release major flagship revisions for the Clinical Assessment sub-division that maintain brand promise but meet current market needs

| ||||

|

|

Piloted and launched AI-enhanced eText and Mastering titles, incorporating cutting-edge technology

|

|

Increase the selection of AI-enhanced titles and invest in the channels component of Pearson+ with diverse formats, including integrated videos

| |||||

|

|

Improved the e-commerce journey for PTE, making it easier for customers to access and purchase products, enhancing the overall user experience and improving the NPS score from 52 to 55

|

|

Implement more advanced Mondly content and expand reach to institutional and enterprise customers by harnessing synergies with the wider ELL portfolio

| |||||

|

|

Created c.370k custom assessments since the start of the 2023/24 school year, exceeding the initial target by more than 20x, enabling teachers to further improve the student learning experience and maintain a strong NPS score of +67

|

|

Improve overall customer satisfaction by integrating content directly onto the Virtual Learning platform, in addition to driving operational improvements and expanding programme offerings

| |||||

|

|

Streamlined operations and implemented an improved go-to-market strategy for strategic accounts, utilising an integrated, team-selling approach to capitalise on strong traction with government entities and large organisations for Workforce Solutions

|

|

Develop customised solutions and professional services that align with enterprise requirements, and launch the Official GED App by Summer 2024 | |||||

|

|

Invested in AI and introduced AI-generated content summarisation, explanations, and practice quizzes to enhance the user experience within Pearson+ |

|

Leverage the interconnectedness of Pearson+ with Higher Education’s courseware to enhance personalisation and trial career-focused propositions |

| Annual report and accounts 2023 Pearson plc 13 |

| Divisional spotlights | Strategic report | |

Assessment & Qualifications

Spotlight on Clinical Assessment: Business model innovation enabled by digital capability driving growth and customer satisfaction in K-12 Special Education

Opportunity

Our Clinical Assessment business represents one of the four sub-divisions within Assessment & Qualifications. We have been a longstanding leader in special education assessment, catering to the requirements of psychologists, educators, speech pathologists, and other professionals that support the special learning needs of students. Throughout our interactions, we always aim to match the evolving needs of the important customers we serve with our gold-standard products and state-of-the-art capabilities. Our portfolio of intellectual property drives much of our competitive advantage as we offer hundreds of products to the market to support a broad array of needs.

Meeting the growing mental health and learning support needs of student populations has become increasingly complex, making resource planning for physical assessment products difficult at best. With our Digital Assessment Library for Schools (DALS) offering, we leverage our expertise and digital innovation to remove the guesswork from resource planning.

Progress so far

In 2017 we launched DALS, a subscription offering that provides unlimited access to an industry-leading set of testing instruments. Our Special Education customers are no longer forced to commit to specific evaluation products and diagnostic needs of an unknown student population and are freed from having to anticipate inventory and its cost implications during the budget season. Our customers are excited by the cost-predictability. But more importantly, the access to a broader set of instruments allows our professionals to tailor evaluations to the unique needs of individual students, improving responsible and efficacious use of Individualised Education Plan (IEP) funding.

Since its inception, DALS has quickly become the preferred model for Special Education, which is outlined by its exceptional growth. In fact, other clinical assessment publishers have recognised the importance of DALS and we have begun offering optional DALS upgrades that can include competitor products.

DALS has achieved year-over-year growth of 23% and a five-year CAGR at nearly 80%, supported by exceptional renewal rates. It is now being used by districts servicing 25% of IEPs currently in place across the country. In 2023, we signed deals with some of the largest and most influential school districts in the US, including Chicago Public Schools, Miami-Dade, and Los Angeles Unified School District. These deals represent a strong endorsement of the value and quality of this offering, and we are honoured to be a trusted partner.

As we look ahead to 2024 and beyond, we are excited to expand the subscription model to new regions and markets, and are currently in the process of exploring expansion into the healthcare and private practice segments. In addition to this, we plan to introduce new features and functionalities that will further differentiate our offering from the competition. Some of the highlights include:

| — | Expanding DALS in Canada, Australia, and the UK, where we have already introduced the model in 2023 and received positive feedback from customers. We will continue to market and promote DALS in these regions, as well as explore opportunities in other international markets. |

| — | Launching the Digital Assessment Library for University & College Counselling Centres, a new segment that has a high demand for mental health assessments and interventions, especially in the wake of the COVID-19 pandemic. We have partnered with Titanium Schedule, a leading software provider for counselling centres, to integrate our offering into their platform and reach their existing customer base. |

| — | Adding new and revised assessments to the DALS portfolio, as well as complementary assessments from other test publishers, such as the MHS Education Library. This will ensure that our DALS customers have access to the most up-to-date and comprehensive selection of digital assessments available. |

The Digital Assessment Library has been an important evolutionary step for Pearson, reinforcing our leadership by facilitating a virtuous cycle of innovation, customer feedback, and continuous improvement, as we leverage our digital platforms and data to enhance our products and services. We are confident that our offering will continue to drive growth and customer satisfaction for our business in 2024 and beyond.

| Annual report and accounts 2023 Pearson plc 14 |

| Strategic report | ||

English Language Learning

Spotlight on PTE, part of our high-stakes assessments business

Opportunity

Our business is centred on three key components which represent a c.£6bn addressable market:

| — | High Stakes Assessments: an addressable market upwards of £900m. Our flagship product PTE is a verified, secure certification of English proficiency for international migrants and students. |

| — | Institutional English Language Learning: an addressable market of c.£3bn. We offer digital and blended courseware solutions to academic institutions, private language schools and enterprises across the globe. |

| — | Online Direct to Consumer: an addressable market of c.£2bn, which we have entered through our acquisition of Mondly. |

Progress so far

Our high-stakes assessments business saw strong volume growth of c.50% in 2023, driven by market share gains in key countries like India. The past year has also seen our PTE product earn key approval for the Student Direct Stream and Migration in Canada; these notable recognitions underscore the impact and extensive reach that our initiatives have had within the broader language learning sphere.

Our achievements in the broader high-stakes assessments space have been underpinned by a holistic comprehension of the challenges faced by test takers coupled with a commitment to solving their pain points. A key driver of our success lies in creating a better end-to-end experience for the test taker, from booking their test, preparing for it, and taking it in one sitting in our highly secure and convenient VUE test centres, to receiving their score in industry-leading return times, with bias and stress removed from the scoring process. Strategic collaborations with local partners in key markets have proven instrumental in scaling our operations and driving sales. Concurrently, our impactful hyper-local marketing campaigns have effectively heightened awareness of our distinctive offerings, further solidifying our market position.

We enter 2024 in a strong position, continuing the momentum from the prior year. We are poised to continue investing in our high-stakes assessment ecosystem, encompassing advancements in assessment technology, strategic partnerships, and test security and integrity. These initiatives are strategically aligned to elevate the overall customer experience, fostering increased market share gains. In addition, our commitment extends to the expansion and scaling of assessments within our portfolio, including our Versant suite of tests. These endeavours reflect our dedication to sustained growth and excellence in the dynamic landscape of mid- and high-stakes assessments. With our combination of technological capability and deep learning expertise, we will continue to bring real value to the language learning market.

Pearson+

Spotlight on the development of our Channels feature alongside user growth and monetisation

Opportunity

We are a frontrunner in the Higher Education courseware market, with our influence underscored by the millions of students currently enrolled in courses utilising Pearson eTextbooks.

Capitalising on this robust market position, our initiatives are outlined in two phases over the forthcoming year:

| 1. | Shift eTextbook consumption directly to Pearson+ and improve monetisation |

| 2. | Engage and retain students with relevant and valuable services beyond eTextbooks, to improve average revenue per user, and ultimately consumer lifetime value |

Pearson+ is currently monetised through paid access to eTextbooks by students after the faculty adopts content in their courses. Our existing Higher Education business provides a large, efficient customer acquisition funnel for Pearson+. Study features, such as Pearson+ Channels, will encourage further use of the application beyond the eTextbook. Over time, Pearson+ users can be further monetised through cross-selling other relevant Pearson products and services, such as Mondly.

Progress so far

Over 2023 we made significant progress advancing our Pearson+ strategy. Most notably, we added and enhanced what students want, including beta AI study features in three titles, improved search, simpler e-commerce, and an overall better user experience.

By further developing Channels with video content and practice questions this year, Pearson+ is an increasingly valuable study tool for students in 23 college courses, including courses that do not require Pearson eTextbooks. To provide increased access, we have also bundled together Pearson+ eTextbooks and Channels in an affordable “Study and Exam Prep Pack”.

For the first time, we saw Pearson+ reach 1m paid subscriptions in a calendar year, with the total number of Pearson+ registered users reaching around 5m by the end of the 2023 calendar year, validating the platforms appeal and effectiveness in meeting the diverse needs of our audience.

Looking ahead to 2024, we aim to drive continued growth by expanding our distribution. Additionally, we plan to capitalise on the synergies between Pearson+ and Higher Education’s courseware, in particular the combined platform capabilities, and use this as a springboard to optimise personalisation and diversify our course offerings. As we continue to expand our reach and enhance the value proposition of Pearson+, these initiatives serve as a testament to our commitment to innovation and our ability to deliver products and services that resonate with our user base.

| Annual report and accounts 2023 Pearson plc 15 |

| Stakeholder engagement | Strategic report | |

Learning from our stakeholders

As learning evolves into something more fluid and more necessary across our lifetime, the needs of learners are changing too. Our ability to meet them at this pivotal moment, depends in part on our ability to engage with and mobilise a diverse group of stakeholders. We are building a company that is digital-first and puts the consumer at the heart of all we do.

Building strong relationships inside and outside Pearson means we can make an impact on the people and communities we serve. In return, all of these stakeholders - consumers, employees, shareholders, educators, employers, business partners, and government - can make a positive impact on our business. This year, more than ever, we’ve seen a renewed effort to partner with stakeholders to respond to the needs of people as they move through different life stages.

We all benefit when a cross-section of stakeholders collaborates and comes together to meet the needs of learners and to help to drive growth for the company.

|

Consumers

|

Why and how we engage

With our efforts to engage more deeply with consumers, Pearson is bringing to life its commitment to put the consumer at the heart of everything we do. This helps us more fully understand how consumers use our products, perceive the company, and feel about the trends driving learning in a digital era.

We research and engage with consumers holistically, by studying how they use our products, how they think, and the culture that shapes their behaviour. This includes conducting consumer focus groups and ethnographic research, trend and sentiment analysis, and competitive analysis.

In some specific cases, this also includes surveying consumers directly via our products. This kind of engagement recently has been used in Pearson+ and in Mastering to gauge user opinions on the effectiveness of our new generative AI study tools. In those cases, students were asked if they believe that the tools were helpful in their studies and how likely they were to use them again. Product teams for both products have also been engaging indirectly with consumers by analysing layers of student usage data and testing enhancements based on that.

Finally, we are making a concerted effort to push consumer insights further into the company, through newsletters, employee learning sessions, and other resources. This helps us cultivate an ‘outside-in’ approach to understand the people who buy and use our products and services and generates greater awareness of the culture and trends impacting our business.

Outcome of engagement

Understanding our consumers allows us to be more effective in the design and creation of products, along with go-to-market strategies and ongoing implementation.

Consumer feedback has been particularly critical as Pearson rolled out its beta of generative AI features in Pearson+ and Mastering. Student feedback early in the design process was clear in telling us that students wanted AI features that helped them obtain better grades. Designers were able to focus on the features that would be most effective in doing that. By the end of the Autumn 2023 semester, 75% of those using the AI study tools ranked them as helpful or very helpful. In Pearson+ and Mastering, product managers have been acting on other user feedback to improve AI experiences in real time, including adjusting tonality to meet student prompts and incorporating positive language to encourage students to succeed. Together, the feedback before and during the beta will lead to the expansion of AI study in at least 40 more Mastering and MyLab titles.

| Annual report and accounts 2023 Pearson plc 16 |

| Strategic report | ||

|

| ||

|

Educational institutions and educators | |

|

|

Why and how we engage

Educators are a cornerstone of our business and they maintain a close relationship with learners. Our engagement with educators helps to improve the teaching and learning experience, and often provides them with valuable professional development and gives Pearson insights on the needs of learners at all levels.

In our Virtual Schools business, part of our Virtual Learning division, our annual teacher and school leader conferences bring together teachers, school staff, and Pearson teams to attend sessions facilitated by experts from across the learning and education industry.

In our US Student Assessment business, we hold working sessions with educator committees in customer states as assessments are being developed.

In our Higher Education business, we employ a full-time team of active faculty advisors dedicated to supporting instructors in the setup and use of our products. Our Higher Education business has also conducted two surveys with faculty this year, measuring and tracking educator sentiment on the use of generative AI in learning. The division runs an ongoing, weekly AI webinar series to serve as professional development opportunities for faculty, awarding them a Credly badge for their participation.

In the UK, we brought together the perspectives of over 6,000 educators and 1,000 students to create and release the second Pearson School Report. The report takes an in-depth look at life in schools and how educators are pioneering change. It shares their invaluable insights on challenges, opportunities, diversity, equity and inclusion, plus sustainability and digital innovation. The report has reached a vast audience through accompanying media articles, free support and events.

Outcome of engagement

All of our educator engagement leads to a better understanding of how products are used in market and also raises the profile of Pearson in this important customer segment. Through our engagement, we build trust with educators and we help them see us as a true partner in their work.

Many of our more than 2,000 Pearson authors are also educators, along with being experts in their fields. They give us valuable insights about how their own students use our products.

And, they help us test new ways of using digital tools in the courseware they author. Across the board, our work with educators contributes directly to the quality of our products.

Specifically, our engagement with educator committees at the US state level ensures that our US school assessments are aligned to state standards and free of bias.

Our Virtual Schools’ conferences ensure that educators learn from one another in peer-to-peer engagement, tailoring solutions and exploring learnings that support the needs of students.

In our Higher Education business, our faculty engagement provides ongoing feedback on new AI product features such as generative AI and helps us understand how to best tailor those features to the needs of faculty and students, helping both become more effective users of AI.

The Pearson Schools report is another example of how listening to and engaging with educators builds trust and visibility with this important customer group.

| Annual report and accounts 2023 Pearson plc 17 |

| Stakeholder engagement continued | Strategic report | |

|

| ||

|

Employers | |

|

|

Why and how we engage

Employers have always been a key stakeholder for Pearson and they are becoming even more important as the need for reskilling grows in our changing economy and jobs are being increasingly augmented by AI and other technology. Throughout our businesses, ongoing consultation and conversation with employers helps shape our offerings, with an eye toward the growth of our enterprise business. In addition, Pearson can provide useful insights and information that help employers understand the wider labour market and build important customer relationships.

Our Workforce Skills division works with employers to design solutions that fit their unique place in the labour market and help learners progress in their career goals. In our Vocational Qualification business, Pearson’s BTEC qualifications are designed with relevant sector experts and employers, to ensure they cover the most relevant content. When expanding our Esports BTECs into Higher Nationals, we worked closely with the British Esports Federation to ensure that the qualifications offer students progression to entry-level jobs in the sector. We also created a bespoke BTEC qualification for opticians, specifically at the request of, and in consultation with, one of the UK’s largest eyeglasses and contact lens retailers.

We also provide employers with data and thought leadership which helps them shape their decisions and helps to raise the profile of Pearson as a leader in workforce and career learning. In 2023, Pearson VUE completed its third Value of IT Certification report, which surveyed IT hiring managers and people managers in the US and India to understand their views on certification trends in the workplace. Not only does the research help inform the work of Pearson VUE, but it is also shared with employers so they can see the larger picture of the IT industry. The Pearson Skills Outlook, a thought leadership series that uses Faethm data to forecast skills trends, became an important outreach and engagement tool across the company with employers.

The Skills Outlook reports help with lead generation and also provides data and information to employers and HR managers looking to better understand today’s most in demand skills. English Language Learning also fielded a large piece of research in 2023, to be released in the coming year, that looks at the habits of English learners in five countries and how employers can better support them in the workplace.

Outcome of engagement

Engagement with employers helps us create offerings that meet the needs of more technology driven labour markets and appeal to large enterprise customers. By doing that, we further expand our presence in the growing workforce learning market. Specifically, feedback from enterprise customers is helping us refine our offering and go-to-market approach-including cross divisional sales to support the needs of these large accounts. For example, we identified a need for talent development assessments to support employees at a large telecommunications company. The team successfully matched a package of Pearson TalentLens, a Workforce Skills product, with our Versant language learning, an English Language Learning product, to meet the customer’s needs.

|

| ||

|

Business partners | |

|

|

Why and how we engage

Working with partners who share our commitment to doing business responsibly strengthens our supply chain relationships and reduces risk. This helps Pearson improve our product offerings and make progress on our climate and diversity commitments.

We continue to analyse the carbon performance of our major suppliers. We have also introduced new language in all of our supplier contracts, ensuring they have provisions for increasing carbon maturity and increased visibility of emissions reporting.

We also engaged directly with a targeted pool of higher carbon impact suppliers, whose contracts don’t yet include sustainability requirements. This is an effort to make them aware that alignment with our carbon targets is now a differentiating factor in our sourcing strategy.

In 2023 we spent £47.2m with diverse-owned suppliers (owners of businesses from historically underrepresented groups) and we are on track to meet our goal of spending £500m with diverse-owned suppliers by 2030.

Outcome of engagement

These actions are having a direct impact on how we execute our procurement strategies and help grow our reputation as a responsible business.

By collaborating with partners across our supply chain, we can prioritise decarbonisation efforts where they can make the biggest difference and demonstrate community level benefits of supply chain decarbonisation efforts.

Pearson’s sustainable procurement maturity score, assessed by EcoVadis, improved from good to advanced, outperforming the EcoVadis customer average across all industries.

| Annual report and accounts 2023 Pearson plc 18 |

| Strategic report | ||

|

| ||

|

Government and regulators | |

|

|

Why and how we engage

Government policymakers across the world are charged with implementing policies to grow and sustain productive economies, ensuring that individuals have the educational and skill-development opportunities to achieve their life goals. Pearson acts as an important partner with governments, schools, colleges, universities, and the business sector to help achieve those economic and educational goals within the countries in which we operate. Governments everywhere are focused on how to position themselves for the future of work, to take advantage of advancements in technology to provide residents with the requisite high-quality education and training to meet the needs of a rapidly evolving workforce. Increasingly, the rise of AI in society and in the labour market challenges governments to devise sound policies to take advantage of opportunities and mitigate against risks to the labour force. Pearson is well positioned to share its expertise and knowledge with governments as they look to enact policies to regulate AI in their countries.

Given governments’ need of support as economies face labour shortages, particularly in high-demand sectors, and students and workers seek accelerated learning opportunities and skill development, we engage, through meetings and presentations with elected and appointed government officials, discussing key concepts including skills-based hiring, certifications, and apprenticeships vital to their region.

Outcome of engagement

Our engagement helps inform policy decisions and share best practices on areas of focus for education, training, and recruitment. Many countries and students are looking to undertake English Language courses and proficiency assessments. Accordingly, we share our expertise and work with government leaders in key markets as they develop policies and programmes to meet this demand. In addition, AI, digital transformation, and energy transition are topics which countries from all regions are prioritising when developing policy and allocating investments on education and skills.

|

| ||

|

Communities | |

|

|

Why and how we engage

Pearson increases access to education around the world, ensuring our products and services enable more people to learn and develop new skills through a lifetime of learning. Learning is a key factor in empowering individuals and communities, improving social and economic outcomes, and creating a more equitable and sustainable world.

In addition to maintaining relationships with key organisations, we participate in multi-stakeholder initiatives to promote lifelong learning opportunities for all and ensure the lasting protection of our planet.

This year, we launched a skills-based social impact initiative for our employees, that focuses on learning, mobilising and building community. As part of the initiative, we evolved our volunteering policy to five days for causes aligned to our purpose and values, and award a Credly volunteering badge to recognise the skills learned while serving our communities.

Outcome of engagement

We strive to make a positive and meaningful impact in the communities in which we operate.

To support that, we gave over £477k in humanitarian aid support.

Additionally, our employees have given over 20,000 volunteer hours and supported 55 causes. You can find more detail on Learning for Impact on pages 34-43.

| Annual report and accounts 2023 Pearson plc 19 |

| Stakeholder engagement continued | Strategic report | |

|

| ||

|

Employees | |

|

|

Why and how we engage

Pearson’s greatest asset is its people. Our business success and ability to positively impact society heavily rely on our colleagues. We also know that managers account for as much as 70% of the variance in employee team engagement. That’s why we continue empowering our managers with ongoing tools and training to support them and their teams, which is pivotal in driving engagement throughout Pearson.

At the enterprise level, we regularly communicated with our people through interactive forums, town halls, newsletters, and regular storytelling.

Outcome of engagement

Throughout 2023, we encouraged managers to hold regular one-to-one meetings with their direct reports. Additionally, 82% of employees actively participated in our engagement survey with a GrandMean score of 4.09 on a 5-point Likert scale. This is up from 72%.and 3.96 respectively in 2022 and is considered ‘meaningful’ improvement by Gallup.

|

| ||

|

Investors / shareholders | |

|

|

Why and how we engage

Our shareholders play an important role in both the monitoring and safeguarding of the governance of our company and in providing access to capital. Some are also employees who have a critical role to play in the continued success of our business.

We have strong and constructive relationships with our key institutional investors and shareholders and regularly communicate with them on key issues, including at our financial results, our AGM and at investor meetings and conferences. We held 505 meetings with 272 institutions over the course of 2023, both virtually and in person. We discussed financial, operational and strategic matters.

Outcome of engagement

Our investors appreciate the time we spend with them to give them updates on our strategy and progress, and we continue to develop how we communicate effectively across a range of formats.

Our 2023 AGM was held as a hybrid (combined physical and electronic) meeting, enabling shareholders, should they so wish, to participate in the AGM, ask questions and vote on resolutions via a live webcast without being physically present at the AGM. The physical element of the meeting was held, for the first time, at our 80 Strand office in London.

| Annual report and accounts 2023 Pearson plc 20 |

| Strategic report | ||

|

| ||

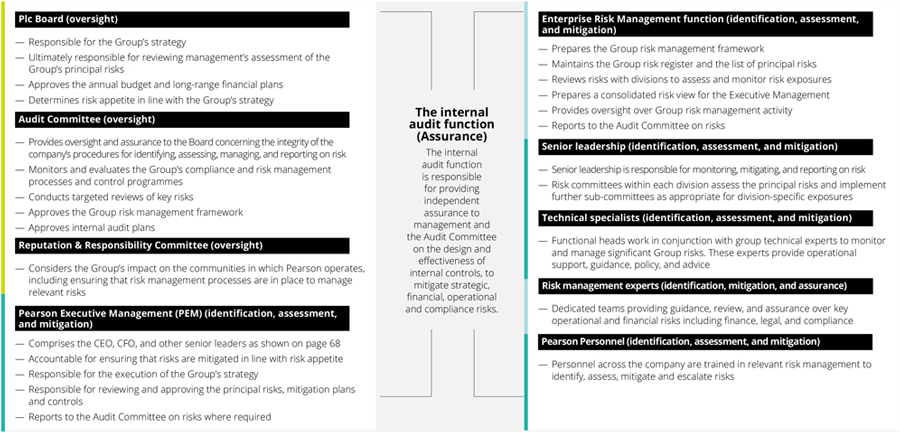

| Directors’ duties statement

In accordance with Section 172 of the Companies Act 2006 (see box to the right), the Directors fulfil their duties to promote the success of the company through a well-established governance framework. Typically, in large and complex businesses such as Pearson, this framework includes delegation of day-to-day decision-making to employees of the Group.

This governance framework, summarised throughout this document, is far more than a simple delegation of financial authority, and includes the values and behaviours expected of our employees and business partners, including the standards to which they must adhere; how we engage with stakeholders, including understanding and taking into account their views and concerns; and how the Board ensures that we have a robust system of control and assurance processes in place.

In this annual report, we provide examples of how the Directors promote the success of Pearson while taking into account the consequences of decisions in the long-term, building relationships with stakeholders (including our eight key stakeholder groups, as mentioned previously), and ensuring that business is conducted ethically and responsibly.

While there are many parts of this annual report which illustrate how the Directors do this, with the support of the wider business, the following sections in particular are relevant:

— Learning from our stakeholders (pages 16-20), which outlines:

— how we serve and engage with each of our eight key stakeholder groups, listen to their key concerns and provide our responses

— how we have adapted our business to meet their needs |

— how we have had regard to the need to foster the company’s business relationships with each of the stakeholder groups

— Understanding our stakeholders (pages 81-83), which summarises:

— how Directors have engaged with employees and shareholders, and had regard to their interests

— Sustainability (pages 34-55), which describes:

— Initiatives through which we strive to enable more engaging learning experiences, that are accessible to more people, and with a smaller carbon footprint

— Our commitment to creating a culture that prioritises human rights, our employees, DEI, and socially responsible sourcing

— How we align with widely accepted ESG reporting frameworks including GRI, SASB and TCFD. For further details on TCFD reporting, please see page 44

A continued understanding of the key issues affecting stakeholders is an integral part of the Board’s decision-making process. The insights that the Board gains through its engagement mechanisms form an important part of the context for all the Board’s discussions and decision-making processes. For an insight into how the Board has considered the interests of various stakeholders in its decision-making, and what matters the Directors considered when balancing various stakeholder perspectives, please see our case study on the Chief Executive appointment process on page 83. | |

|

Section 172 of the Companies Act |

| In summary, as required by Section 172 of the Companies Act 2006, a Director of a company must act in the way they consider, in good faith, would most likely promote the success of the company for the benefit of its shareholders as a whole. In doing this, the Director must have regard, among other matters, to: |

| — the likely consequences of any decisions in the long term, |

| — the interests of the company’s employees, |

| — the need to foster the company’s business relationships with suppliers, customers and others, |

| — the impact of the company’s operations on the community and environment, |

| — the company’s reputation for high standards of business conduct, and |

| — the need to act fairly as between members of the company. |

| Annual report and accounts 2023 Pearson plc 21 |

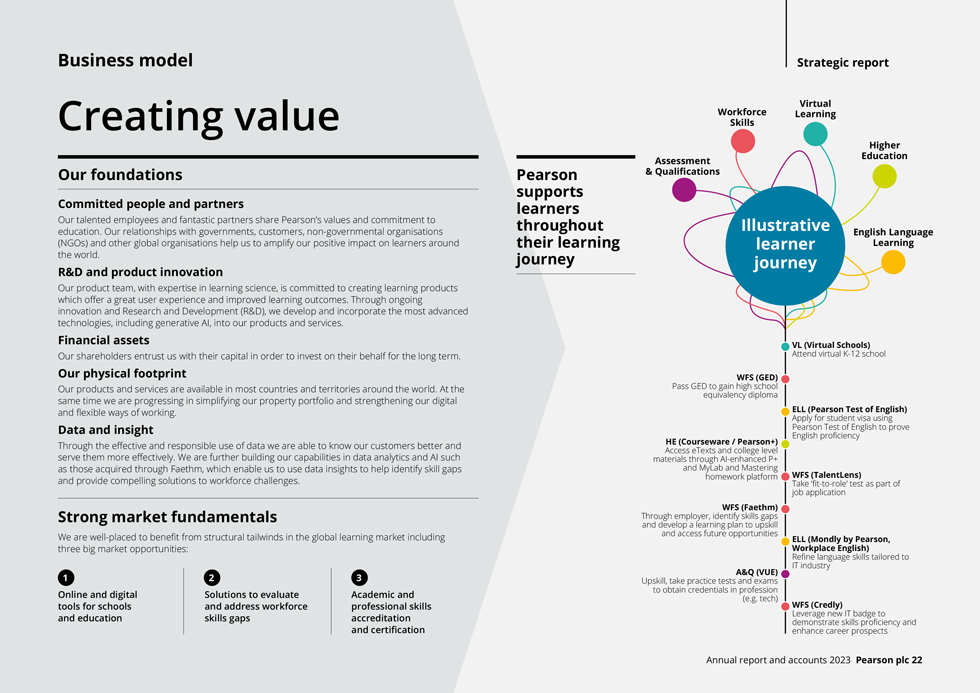

Strategic report Business model Creating value Our foundations Committed people and partners Our talented employees and fantastic partners share Pearson’s values and commitment to education. Our relationships with governments, customers, non-governmental organisations (NGOs) and other global organisations help us to amplify our positive impact on learners around the world. R&D and product innovation Our product team, with expertise in learning science, is committed to creating learning products which offer a great user experience and improved learning outcomes. Through ongoing innovation and Research and Development (R&D), we develop and incorporate the most advanced technologies, including generative AI, into our products and services. Financial assets Our shareholders entrust us with their capital in order to invest on their behalf for the long term. Our physical footprint Our products and services are available in most countries and territories around the world. At the same time we are progressing in simplifying our property portfolio and strengthening our digital and flexible ways of working. Data and insight Through the effective and responsible use of data we are able to know our customers better and serve them more effectively. We are further building our capabilities in data analytics and AI such as those acquired through Faethm, which enable us to use data insights to help identify skill gaps and provide compelling solutions to workforce challenges. Strong market fundamentals We are well-placed to benefit from structural tailwinds in the global learning market including three big market opportunities: Online and digital tools for schools and education Solutions to evaluate and address workforce skills gaps Academic and professional skills accreditation and certification Pearson supports learners throughout their learning journey

| Annual report and accounts 2023 Pearson plc 22 |

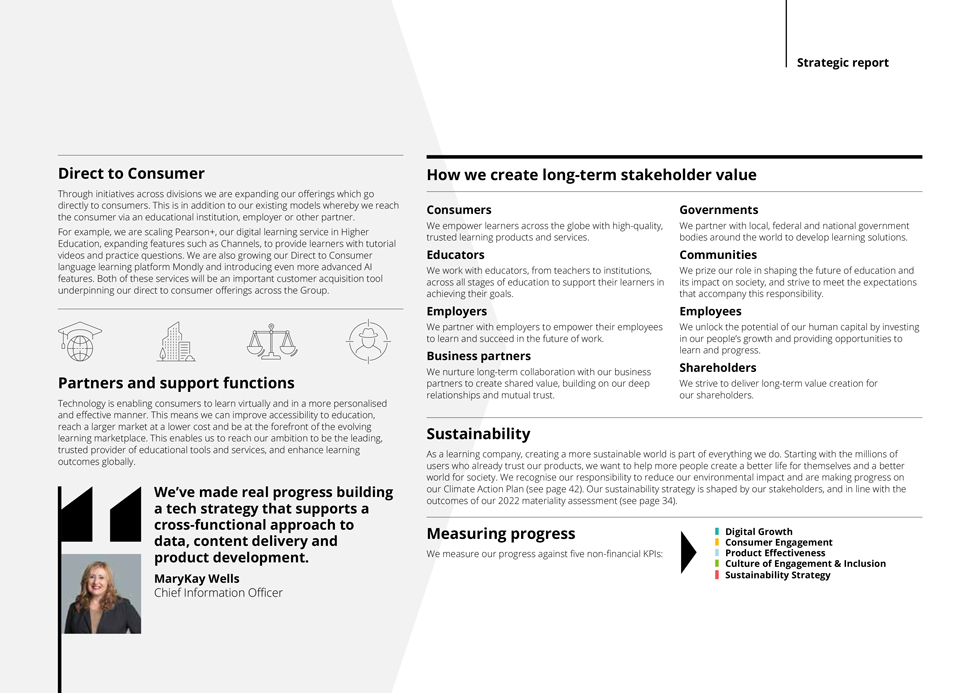

Strategic report Direct to Consumer Through initiatives across divisions we are expanding our offerings which go directly to consumers. This is in addition to our existing models whereby we reach the consumer via an educational institution, employer or other partner. For example, we are scaling Pearson+, our digital learning service in Higher Education, expanding features such as Channels, to provide learners with tutorial videos and practice questions. We are also growing our Direct to Consumer language learning platform Mondly and introducing even more advanced AI features. Both of these services will be an important customer acquisition tool underpinning our direct to consumer offerings across the Group. Partners and support functions Technology is enabling consumers to learn virtually and in a more personalised and effective manner. This means we can improve accessibility to education, reach a larger market at a lower cost and be at the forefront of the evolving learning marketplace. This enables us to reach our ambition to be the leading, trusted provider of educational tools and services, and enhance learning outcomes globally. We’ve made real progress building a tech strategy that supports a cross-functional approach to data, content delivery and product development. MaryKay Wells Chief Information Officer How we create long-term stakeholder value Consumers Governments We empower learners across the globe with high-quality, We partner with local, federal and national government trusted learning products and services. bodies around the world to develop learning solutions. Educators Communities We work with educators, from teachers to institutions, We prize our role in shaping the future of education and across all stages of education to support their learners in its impact on society, and strive to meet the expectations achieving their goals. that accompany this responsibility. Employers Employees We partner with employers to empower their employees We unlock the potential of our human capital by investing to learn and succeed in the future of work. in our people’s growth and providing opportunities to Business partners learn and progress. We nurture long-term collaboration with our business Shareholders partners to create shared value, building on our deep We strive to deliver long-term value creation for relationships and mutual trust. our shareholders. Sustainability As a learning company, creating a more sustainable world is part of everything we do. Starting with the millions of users who already trust our products, we want to help more people create a better life for themselves and a better world for society. We recognise our responsibility to reduce our environmental impact and are making progress on our Climate Action Plan (see page 42). Our sustainability strategy is shaped by our stakeholders, and in line with the outcomes of our 2022 materiality assessment (see page 34). Measuring progress We measure our progress against five non-financial KPIs: Digital Growth Consumer Engagement Product Effectiveness Culture of Engagement & Inclusion Sustainability Strategy

| Annual report and accounts 2023 Pearson plc 23 |

| Key performance indicators | Strategic report | |

Monitoring progress

Non-financial measures

| a. | Measure definition has changed to number of government-funded student enrolments at partner schools within the US as of 30th September. Excludes private-pay students at Pearson Online Academy and district partnerships. |

| This is more closely aligned to business processes. |

| b. | VUE test volumes include PTE and GED tests but sales for each of these tests are reflected in the English Language Learning and Workforce Skills divisions respectively. PDRI test volumes are not currently included in this metric. |

| c. | Previously reported ’Increasing diverse talent’ metrics retired and new strategic remuneration measures incorporated. |

| d. | The net emissions reduction figures have been assured by an independent third-party, SLR Consulting Ltd. % reduction in total tCO2e above is calculated using a location-based methodology. Within the 2023 number, 4% is due to portfolio changes. These will be removed following the normal rebasing exercise in 2024. |

| * | Historical figures restated to exclude US K-12 Courseware (sold in 2019). |

Please find further details on our Strategic KPIs here https://plc.pearson.com/en-GB/company/our-targets-kpis

|

See how this aligns strategy to management reward: page 112 |

| Annual report and accounts 2023 Pearson plc 24 |

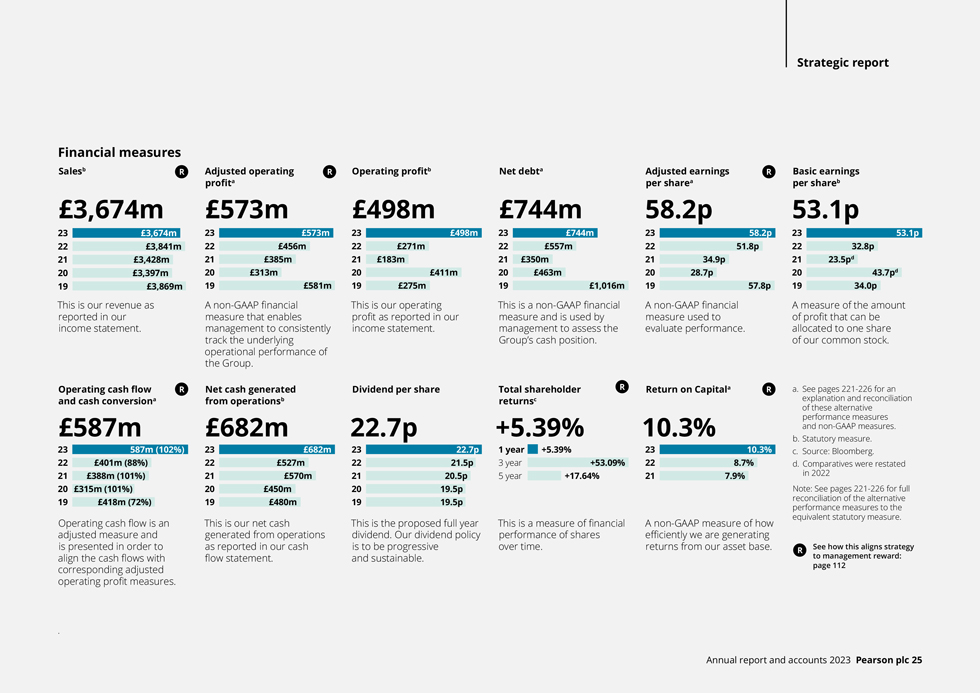

Strategic report Financial measures Salesb This is our revenue as reported in our income statement. Adjusted operating profita A non-GAAP financial measure that enables management to consistently track the underlying operational performance of the Group. Operating profitb This is our operating profit as reported in our income statement. Net debta This is a non-GAAP financial measure and is used by management to assess the Group’s cash position. Adjusted earnings per sharea A non-GAAP financial measure used to evaluate performance. Basic earnings per shareb A measure of the amount of profit that can be allocated to one share of our common stock. Operating cash flow and cash conversiona Operating cash flow is an adjusted measure and is presented in order to align the cash flows with corresponding adjusted operating profit measures. Net cash generated from operationsb This is our net cash generated from operations as reported in our cash flow statement. Dividend per share This is the proposed full year dividend. Our dividend policy is to be progressive and sustainable. Total shareholder returnsc This is a measure of financial performance of shares over time. Return on Capitala A non-GAAP measure of how efficiently we are generating returns from our asset base. a. See pages 221-226 for an explanation and reconciliation of these alternative performance measures and non-GAAP measures. b. Statutory measure. c. Source: Bloomberg. d. Comparatives were restated in 2022 Note: See pages 221-226 for full reconciliation of the alternative performance measures to the equivalent statutory measure. See how this aligns strategy to management reward: page 112