Ferrari N.V.

2023 ANNUAL REPORT AND FORM 20-F

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

OR

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Fiscal Year Ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number 001-37596

(Exact Name of Registrant as Specified in Its Charter)

| The Netherlands | ||

| (Jurisdiction of Incorporation or Organization) | ||

Tel. No.: +39 0536 949111

(Address of Principal Executive Offices)

Tel. No.: +39 0536 949111

Facsimile No.: +39 0536 241494

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 180,418,090 common shares, par value €0.01 per share, and 63,332,872 special voting shares, par value €0.01 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Act of 1934. Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | |||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP o International Financial Reporting Standards as issued by the International Accounting Standards Board þ Other o

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow: Item 17 o or Item 18 o.

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No þ

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes o No o

TABLE OF CONTENTS

| Page | |||||

| Board Report | |||||

4

Board of Directors

Executive Chairman

John Elkann

Chief Executive Officer

Benedetto Vigna

Vice Chairman

Piero Ferrari

Directors

Delphine Arnault

Francesca Bellettini

Eddy Cue

Sergio Duca

John Galantic

Maria Patrizia Grieco

Adam Keswick

Mike Volpi

Independent Registered Public Accounting Firm

Deloitte Accountants B.V. (AFM Annual Report filing)(1)

Deloitte & Touche S.p.A. (Form 20-F filing)(1)

_________________________________________________________________________

(1) Refer to “Introduction—About this Report” for additional information relating to the AFM Annual Report filing and the Form 20-F filing.

5

Introduction

About this report

This document, referred to hereafter as the “Annual Report and Form 20-F” or “Annual Report”, constitutes both the statutory annual report in accordance with Dutch legal requirements (“AFM Annual Report”) and the annual report on Form 20-F (“Form 20-F”), applicable to Foreign Private Issuers, pursuant to Section 13 or 15(d) of the United States (“U.S.”) Securities Exchange Act of 1934, for Ferrari N.V. for the year ended December 31, 2023, except as noted below.

For the cross-references of the content of this document to the Form 20-F requirements please refer to the “Form 20-F Cross Reference” section included elsewhere in this document.

This Annual Report is filed with the Netherlands Authority for Financial Markets (Autoriteit Financiële Markten, the “AFM”). The following sections have been removed for our Annual Report filing with the AFM:

•Form 20-F cover page;

•Corporate Governance — Differences between Dutch Corporate Governance Practices and NYSE Listing Standards;

•Report of Independent Registered Public Accounting Firm in respect of Internal Control over Financial Reporting for the SEC filing;

•Report of Independent Registered Public Accounting Firm in respect of the PCAOB audits of the 2023 financial statements for the SEC filing;

•Exhibits; and

•Signatures.

This Annual Report and the exhibits hereto are filed with the U.S. Securities and Exchange Commission (“SEC”) and unless otherwise stated, all references in this document to “Form 20-F” refer to the SEC filing. The following sections have been removed for our Form 20-F filing with the SEC:

•Letter from the Chairman and the Chief Executive Officer;

•Overview of Our Business — Procurement — Responsible Supply Chain;

•Overview of Our Business — Client Relations — Client Satisfaction;

•2024 Outlook;

•Corporate Governance — Disclosures pursuant to Decree Article 10 EU-Directive on Takeovers;

•Corporate Governance — Responsibilities in respect to the Annual Report;

•Non Financial Statement;

•Controls and procedures — Statement by the Board of Directors;

•Company Financial Statements;

•Other Information — Additional Information for Netherlands Corporate Governance; and

•Independent auditor’s report — Report on the audit of the financial statements 2023 included in the Annual Report in respect of the AFM filing.

6

Documents on Display

The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including the Company, at http://www.sec.gov. The address of the SEC’s website is provided solely for information purposes and is not intended to be an active link. Reports and other information concerning the business of Ferrari may also be inspected at the offices of the New York Stock Exchange, 11 Wall Street, New York, NY 10005, United States.

We also make our periodic reports as well as other information filed with or furnished to the SEC available, free of charge, through our website at https://www.ferrari.com/en-EN/corporate as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. The information on our website or the websites of any other entity is not incorporated by reference in this document.

This document is a PDF copy of the Annual Report of Ferrari N.V. at and for the year ended December 31, 2023 and is not presented in the ESEF-format as specified in the Regulatory Technical Standards on ESEF (Delegated Regulation (EU) 2019/815). The official Annual Report of Ferrari N.V. in ESEF single reporting package, as filed with the AFM, is available on Ferrari’s website.

7

Certain Defined Terms and Note on Presentation

Certain Defined Terms

In this report, unless otherwise specified, the terms “we”, “our”, “us”, the “Group”, the “Company” and “Ferrari” refer to Ferrari N.V., individually or together with its subsidiaries as the context may require. References to “Ferrari N.V.” refer to the registrant.

Note on Presentation

This Annual Report includes the consolidated financial statements of Ferrari N.V. at December 31, 2023 and 2022, and for the years ended December 31, 2023, 2022 and 2021 prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), as well as IFRS as adopted by the European Union. There is no effect on these consolidated financial statements resulting from differences between IFRS as issued by the IASB and IFRS as adopted by the European Union. The consolidated financial statements and the notes to the consolidated financial statements are referred to collectively as the “Consolidated Financial Statements”.

Basis of Preparation of the Consolidated Financial Statements

The Group’s financial information is presented in Euro. In some instances, information is presented in U.S. Dollars. All references in this document to “Euro” and “€” refer to the currency introduced at the start of the third stage of European Economic and Monetary Union pursuant to the Treaty on the Functioning of the European Union, as amended, and all references to “U.S. Dollars” and “$” refer to the currency of the United States of America (the “United States” or the “U.S.”).

The language of this Annual Report is English. Certain legislative references and technical terms have been cited in their original language in order that the correct technical meaning may be ascribed to them under applicable law.

The financial data in the section “Financial Overview” is presented in millions of Euro, while the percentages presented are calculated using the underlying figures in thousands of Euro.

Certain totals in the tables included in this document may not add due to rounding.

Except otherwise disclosed within this Annual Report, no significant change has occurred since the date of the Consolidated Financial Statements.

8

Forward-Looking Statements

Statements contained in this Annual Report, particularly those regarding our possible or assumed future performance, competitive strengths, costs, dividends, reserves and growth as well as industry growth and other trends and projections, are “forward-looking statements” that contain risks and uncertainties. In some cases, words such as “may”, “will”, “expect”, “could”, “should”, “intend”, “estimate”, “anticipate”, “believe”, “remain”, “continue”, “on track”, “successful”, “grow”, “design”, “target”, “objective”, “goal”, “forecast”, “projection”, “outlook”, “prospects”, “plan”, “guidance” and similar expressions are used to identify forward-looking statements. These forward-looking statements reflect the respective current views of Ferrari with respect to future events and involve significant risks and uncertainties that could cause actual results to differ materially from those indicated in the forward-looking statements. Such risks and uncertainties include, without limitation:

•our ability to preserve and enhance the value of the Ferrari brand;

•our ability to attract and retain qualified personnel;

•the success of our racing activities;

•our ability to keep up with advances in high performance car technology, to meet the challenges and costs of integrating advanced technologies, including hybrid and electric, more broadly into our car portfolio over time and to make appealing designs for our new models;

•the impact of increasingly stringent fuel economy, emissions and safety standards, including the cost of compliance, and any required changes to our products, as well as possible future bans of combustion engine cars in cities and the potential advent of self-driving technology;

•increases in costs, disruptions of supply or shortages of components and raw materials;

•our low volume strategy;

•our ability to successfully carry out our controlled growth strategy and, particularly, our ability to increase our presence in growth market countries;

•global economic conditions, macro events, pandemics and conflicts, including the ongoing conflict between Russia and Ukraine and the more recent hostilities between Israel and Hamas;

•changes in the general economic environment (including changes in some of the markets in which we operate) and changes in demand for luxury goods, including high performance luxury cars, demand for which is highly volatile;

•competition in the luxury performance automobile industry;

•changes in client preferences and automotive trends;

•our ability to preserve our relationship with the automobile collector and enthusiast community;

•disruptions at our manufacturing facilities in Maranello and Modena;

•climate change and other environmental impacts, as well as an increased focus of regulators and stakeholders on environmental matters;

•our ability to maintain the functional and efficient operation of our information technology systems and to defend from the risk of cyberattacks, including on our in-vehicle technology;

•the ability of our current management team to operate and manage effectively and the reliance upon a number of key members of executive management and employees;

•the performance of our dealer network on which we depend for sales and services;

•product warranties, product recalls and liability claims;

•the sponsorship and commercial revenues and expenses of our racing activities, as well as the popularity of motor sports more broadly;

•the performance of our lifestyle activities;

9

•our ability to protect our intellectual property rights and to avoid infringing on the intellectual property rights of others;

•our continued compliance with customs regulations of various jurisdictions;

•labor relations and collective bargaining agreements;

•our ability to ensure that our employees, agents and representatives comply with applicable law and regulations;

•changes in tax, tariff or fiscal policies and regulatory, political and labor conditions in the jurisdictions in which we operate;

•our ability to service and refinance our debt;

•exchange rate fluctuations, interest rate changes, credit risk and other market risks;

•our ability to provide or arrange for adequate access to financing for our dealers and clients, and associated risks;

•the adequacy of our insurance coverage to protect us against potential losses;

•potential conflicts of interest due to director and officer overlaps with our largest shareholders; and

•other factors discussed elsewhere in this document.

We expressly disclaim and do not assume any liability in connection with any inaccuracies in any of the forward-looking statements in this document or in connection with any use by any third party of such forward-looking statements. Actual results could differ materially from those anticipated in such forward-looking statements. We do not undertake an obligation to update or revise publicly any forward-looking statements.

Additional factors which could cause actual results and developments to differ from those expressed or implied by the forward-looking statements are included in the section “Risk Factors” of this Annual Report. These factors may not be exhaustive and should be read in conjunction with the other cautionary statements included in this Annual Report. You should evaluate all forward-looking statements made in this report in the context of these risks and uncertainties.

10

Creating Value for Our Shareholders

Ferrari is among the world’s leading luxury brands with unique, world-class capabilities, and a vision built on our historic foundations and strengths.

We are fiercely protective of our brand, which is among the most iconic and recognizable in the world and is critical to our value proposition to all of our stakeholders. We strive to maintain and enhance the power of our brand and the passion we inspire in clients and the broader community of automotive enthusiasts by continuing our rigorous production and distribution model, which promotes excellence in innovation, design and uniqueness.

We also support our brand value by promoting a strong connection to our company and our brand among the community of Ferrari enthusiasts. We focus relentlessly on strengthening this connection by rewarding our most loyal clients through a range of initiatives, such as driving events and client activities in Maranello and, most importantly, by providing our most loyal and active clients with preferential access to our newest, most exclusive and highest value cars. As a result, in 2023, we sold approximately 74% of our new cars to existing Ferrari clients and 40% to clients being current owners of more than one Ferrari, which reinforces the demand for our cars and the image of luxury and exclusivity inherent in our brand.

Our commitment to excellence and our pursuit of innovation, state-of-the-art performance and distinction in design and engineering in our luxury cars is inseparable from our commitment to integrity, transparency and responsibility in conducting our business. By fully integrating environmental and social considerations with economic objectives we are able to identify potential risks and capitalize on additional opportunities, resulting in a process of continuous improvement. Sustainability is a core element of our governance model and executive management plays a direct and active role in developing and achieving our sustainability objectives under the direction of our Board of Directors. As a clear demonstration of this commitment, we have strengthened the integration of environmental topics in our strategic plan by presenting, in June 2022, a decarbonization strategy that will help us reach carbon neutrality by 2030.

The foundation of a responsible company rests on being fully attentive to the nature and extent of this interconnection and our understanding of both the potential effects of our activities and how those effects can be mitigated through responsible management.

All of the above is strictly linked to our values:

•INDIVIDUAL AND TEAM: Our talented individuals are our greatest resource. However they can only pursue the extraordinary by working together as a team. By fostering integrity, excellence and generosity, we give each of our people the possibility to express their own full potential - and to be part of something greater.

•TRADITION AND INNOVATION: Tradition and innovation drive each other. The ongoing quest for lasting firsts is what fuels the Ferrari legend. Our ability to combine revolutionary technological solutions with exceptional artisanal craftsmanship is what enables us to create icons that stay timeless in a fast-changing world.

•PASSION AND ACHIEVEMENT: Ferrari’s racing spirit lives on in emotions that transcend the road and the track, ultimately becoming an authentic attitude towards life. Nothing excites us more than setting ambitious targets and expectations - and then exceeding them, to push every boundary. It is how the power of passion becomes the beauty of achievement.

Ferrari audaciously redefines the limits of possible.

To ensure tangible long-term value creation and a continuing integration of our sustainability strategy, we place particular emphasis on:

•a governance model based on transparency and integrity, fostering best practices;

•a safe and eco-friendly working environment including excellent working conditions and the utmost respect for human rights;

•continuing professional development of our employees;

11

•mutually beneficial relationships with business partners and the communities in which we operate;

•mitigation of environmental impacts from our production processes and the luxury cars we produce, addressing direct and indirect GHG emissions, focusing on energy and materials, in addition to our electrification journey.

12

Risk Factors

We face a variety of risks and uncertainties in our business. Those described below are not the only risks and uncertainties that we face. Additional risks and uncertainties that we are unaware of, or that we currently believe to be immaterial, may also become important factors that affect us.

Risks Related to Our Business, Strategy and Operations

We may not succeed in preserving and enhancing the value of the Ferrari brand, which we depend upon to drive demand and revenues.

Our financial performance is influenced by the perception and recognition of the Ferrari brand, which, in turn, depends on many factors such as the design, performance, quality and image of our cars, the appeal of our dealerships and stores, the success of our promotional activities including public relations and marketing, as well as our general profile, including our brand’s image of exclusivity. The value of our brand and our ability to achieve premium pricing for Ferrari-branded products may decline if we are unable to maintain the value and image of the Ferrari brand, including, in particular, its aura of exclusivity. Maintaining the value of our brand will depend significantly on our ability to continue to produce luxury performance cars of the highest quality. The market for luxury goods generally and for luxury automobiles in particular is intensely competitive, and we may not be successful in maintaining and strengthening the appeal of our brand. Client preferences, particularly among luxury goods, can vary over time, sometimes rapidly. We are therefore exposed to changing perceptions of our brand image, particularly as we seek to attract new generations of clients and, to that end, we continuously renovate and expand the range of our models. For example, the expansion of hybrid engine technology and electric engine technology is introducing a significant change in the overall driver experience compared to the combustion engine cars of our historical models and the customer long term response to the change, particularly with respect to fully electric models, remains unknown. Any failure to preserve and enhance the value of our brand may materially and adversely affect our ability to sell our cars, to maintain premium pricing, and to extend the value of our brand into other activities profitably or at all.

More broadly, our lifestyle strategy will significantly increase the deployment of our brand in non-car products and experiences, including a large variety of Ferrari-branded accessories and apparel. If this strategy is not successful, our brand image may be diluted or tainted. We selectively license the Ferrari brand to third parties that produce and sell Ferrari-branded luxury goods and therefore we rely on our licensing partners to preserve and enhance the value of our brand. If our licensees or the manufacturers of these products do not maintain the standards of quality and exclusivity that we believe are consistent with the Ferrari brand, or if such licensees or manufacturers otherwise misuse the Ferrari brand, our reputation and the integrity and value of our brand may be damaged and our business, operating results and financial condition may be materially and adversely affected.

In addition, given the popularity, competitiveness and demographic penetration of social media, Ferrari must maintain a presence on the principal established and emerging social media platforms. If we cannot cost effectively use these marketing tools, if we fail to promote our products and services efficiently and effectively or to properly comply with the applicable laws and regulations, or if our social media campaigns attract negative media attention or customer feedback, the value of our brand may be negatively impacted, as well as our results of operations. The popularity and reach of social media and other online platforms has also made it increasingly easier for individuals and groups to communicate and share opinions and views. Any negative or adverse publicity about us, whether or not truthful, could rapidly disseminate and harm customer and community perceptions as well as confidence in our brand and ultimately impact our business, results of operation and financial condition.

If we are not able to attract and retain qualified personnel, we may not be able to maintain our competitive position or to implement our business strategy.

Our success depends, in part, on our continuing ability to attract, recruit, develop and retain qualified talent. Failure to do so effectively would adversely affect our business. Competition to attract talented employees is intense, and there can be a limited availability of individuals with the requisite knowledge and relevant experience. In addition, we may not succeed in instilling our corporate culture and values in our personnel and we may not be able to attract, assimilate, develop or retain qualified personnel in the future. Failure to do so could adversely affect our business, including our ability to execute our global business strategy.

13

Our brand image depends in part on the success of our racing activities, particularly our Formula 1 team.

The prestige, identity, and appeal of the Ferrari brand depends in part on the success of our racing activities, which are a key component of our marketing strategy and may be perceived by our clients as a demonstration of the technological capabilities of our cars, which also support the appeal of other Ferrari-branded luxury goods. In particular, we are focused on improving the results of our Scuderia Ferrari racing team in the Formula 1 World Championship and restoring our historical position as the premier racing team in Formula 1, as our most recent Drivers’ Championship and Constructors’ Championship were in 2007 and 2008, respectively. If we are unable to attract and retain the necessary talent to succeed in international competitions or devote the capital necessary to fund successful racing activities, the value of the Ferrari brand and the appeal of our cars and other luxury goods may suffer. Even if we are able to attract such talent and adequately fund our racing activities, there is no assurance that this will lead to competitive success for our racing teams.

The success of our racing teams depends in particular on our ability to attract and retain top drivers, racing team management and engineering talent. Our primary Formula 1 drivers, team managers and other key employees of Scuderia Ferrari are critical to the success of our Scuderia Ferrari racing team and if we were to lose their services, this could have a material adverse effect on our success and correspondingly the Ferrari brand. If we are unable to find adequate replacements or to attract, retain and incentivize drivers and team managers, other key employees or new qualified personnel, the success of our racing teams may suffer. In addition, the caps on spending imposed by the Formula 1 governing body may hinder our ability to restore our racing preeminence (See “Our revenues from Formula 1 activities may decline and our related expenses may grow”). Because the success of our racing teams forms a large part of our brand identity, a sustained period without racing success could detract from the Ferrari brand and, as a result, from potential clients’ enthusiasm for the Ferrari brand and their perception of our cars, which could have an adverse effect on our business, results of operations and financial condition.

If we are unable to keep up with advances in high performance car technology, our brand and competitive position may suffer.

Performance cars are characterized by leading-edge technology that is constantly evolving. In particular, advances in racing technology often lead to improved technology in road cars. Although we invest heavily in research and development, we may be unable to maintain our leading position in high performance car technology and, as a result, our competitive position may suffer. As technologies change, we plan to upgrade or adapt our cars and introduce new models in order to continue to provide cars with the latest technology. However, our cars may not compete effectively with our competitors’ cars if we are not able to develop, source and integrate the latest technology into our cars. For example, in the next few years luxury performance cars will increasingly transition to hybrid and electric technology, albeit at a slower pace compared to mass market vehicles. See “The introduction of electric technology in our cars is costly and its long-term success is uncertain”. We are also investing in connectivity, which requires significant investments in research and development; we expect that the future generation of cars will feature a higher degree of connectivity for purposes of infotainment, safety and regulatory compliance. These in-car features may also in the near-to-medium term be driven by advances in artificial intelligence (or AI) which may need to be sourced externally and integrated into the car technology.

Developing or acquiring and applying new automotive technologies is costly, and may become even more costly in the future as available technology advances and competition in the industry increases. If our research and development efforts do not lead to improvements in car performance relative to the competition, or if we are required to spend more to achieve comparable results, the sales of our cars or our profitability may suffer.

If our cars do not perform as expected our ability to develop, market and sell our cars could be harmed.

Our cars may contain defects in design and manufacture that may cause them not to perform as expected or that may require repair. There can be no assurance that we will be able to detect and fix any defects in the cars prior to their sale to consumers. Our cars may not perform in line with our clients’ evolving expectations or in a manner that equals or exceeds the performance characteristics of other cars currently available. For example, our newer cars may not have the durability or longevity of current cars, and may not be as easy to repair as other cars currently on the market. Any product defects or any other failure of our performance cars to perform as expected could harm our reputation and result in adverse publicity, lost revenue, delivery delays, product recalls, product liability claims, harm to our brand and reputation, and significant warranty and other expenses, and could have a material adverse impact on our business, operating results and financial condition.

14

If our car designs do not appeal to clients, our brand and competitive position may suffer.

Design and styling are an integral component of our models and our brand. Our cars have historically been characterized by distinctive designs combining the aerodynamics of a sports car with powerful, elegant lines. We believe our clients purchase our cars for their appearance as well as their performance. However, we will need to renew over time the style of our cars to differentiate the new models we produce from older models, and to reflect the broader evolution of aesthetics in our markets. We devote great efforts to the design of our cars and most of our current models are designed by the Ferrari Design Centre, our in-house design team. The design of our electric cars and, more generally, of our future models with increased connectivity features will depart from past designs in appearance and functionality, thereby requiring new skills and presenting new challenges. If the design of our future models fails to meet the evolving tastes and preferences of our clients and prospective clients, or the appreciation of the wider public, our brand may suffer and our sales may be adversely affected.

The introduction of electric technology in our cars is costly and its long-term success is uncertain.

We are gradually introducing electric technology in our cars and we currently plan to introduce the first full electric Ferrari in 2025. In accordance with our strategy, we believe electric technology, together with hybrid and other advanced technologies, will be key to providing continuing performance upgrades to our sports car customers, and will also help us capture the preferences of the urban, affluent car purchasers whom we are increasingly targeting, while helping us meet increasingly stricter emissions requirements.

The integration of electric technology more broadly into our car portfolio over time may present challenges and costs. We expect to continue to increase research and development spending in the medium term, particularly on electric technology-related projects. Although we expect to price our cars appropriately to recoup the investments and expenditures we are making, we cannot be certain that these expenditures will be fully recovered or that they will be recovered with our desired margins. In addition, this transformation of our car technology creates risks and uncertainties such as the impact on driver experience and the impact on the cars’ residual value over time. Other manufacturers of luxury sports cars may be more successful in implementing electric technology. In the long-term, although we believe that combustion engines will continue to be fundamental to the Ferrari driver experience for the foreseeable future, hybrid and pure electric cars may become the prevalent technology for performance sports cars thereby displacing combustion engine models. See also “If we are unable to keep up with advances in high performance car technology, our brand and competitive position may suffer.”.

Because electric technology is a core component of our strategy, and in the medium term we plan to increase the portion of our shipments that feature vehicles with electric technology, if the introduction of electric cars proves too costly or is unsuccessful in the market, our business and results of operations could be materially adversely affected.

New or changing laws, regulations or policies of governmental organizations regarding, among other things, increased fuel economy requirements, reduced greenhouse gas or pollutant emissions, or vehicle safety, may have a significant effect on our costs of operation and/or how we do business.

We are subject throughout the world to comprehensive and constantly evolving laws, regulations and policies. We expect the extent of the legal and regulatory requirements affecting our business and our costs of compliance to continue to increase significantly in the future. Failure to comply with applicable laws and regulatory requirements, in addition to the fines it may attract, may negatively impact our business, results of operation and financial condition as well as our reputation.

In Europe and the United States, for example, significant governmental regulation is driven by environmental, fuel economy, vehicle safety and noise emission concerns. Evolving regulatory requirements could significantly affect our product development plans and may limit the number and types of cars we sell and where we sell them, which may affect our revenue and profitability. Governmental regulations may increase the costs we incur to design, develop and produce our cars and may affect our product portfolio. Regulation may also result in a change in the character or performance characteristics of our cars, which may render them less appealing to our clients. We anticipate that the number and extent of these regulations, and their effect on our cost structure and product line-up, will increase significantly in the future.

In the United States, there is increasing focus on emissions and pollution regulations in light of changing policies under the current administration. New regulations are in the process of being developed, and many existing and potential regulatory initiatives are subject to review by federal or state agencies or the courts. However, the coming federal elections throw considerable uncertainty on future changes. In May 2023, the US Environmental Protection Agency (EPA) released its

15

2027 and later Multi-Pollutant Rulemaking proposal, introducing among other requirements, stricter emission standards (e.g. particulate matter) and a potential ban of fuel enrichment for component protection. Moreover, special provisions for SVMs have almost been completely eliminated; i.e. GHG alternative standards are removed from model year 2025 and no flexibility on exhaust emission standards are provided. Depending on the requirements included in the final rule, the costs of compliance associated with Multi-Pollutant Rulemaking may be substantial.

In addition, we are subject to legislation relating to the emission of other air pollutants such as, among others, the EU “Euro 6” standards and Real Driving Emissions (RDE) standards, the “Tier 3” Motor Vehicle Emission and Fuel Standards issued by the U.S. Environmental Protection Agency (“EPA”), and the Zero Emission Vehicle regulation in California, which are subject to similar derogations for Small Volume Manufacturers (“SVMs”). We lost our status as an SVM for the United States National Highway Traffic Safety Administration (“NHTSA”) in 2019, because our global production exceeded 10,000 vehicles, but we have not lost our SVM status for EU CO2 regulations or for EPA GHG regulations in the United States. In 2021, 2022 and 2023, our global production exceeded 10,000 vehicles again and therefore we were no longer considered a SVM by the NHTSA for the model years 2021, 2022 and 2023. We purchased the fuel economy (“CAFE”) credits needed to fulfill both our 2021 and 2022 deficits and we are currently evaluating the purchase of credits for 2023. We expect to continue to purchase credits in the coming years if required. We could lose our status as an SVM in the EU, the United States and other countries if we do not continue to meet all of the necessary eligibility criteria under applicable regulations as they evolve, not only in relation to volumes but also in relation to the conditions of operational independence. In order to meet these criteria we may need to modify our growth plans or other operations. Furthermore, even if we continue to benefit from derogations as an SVM, we may have a substantial impact on our financial results.

As the state of California has been granted special authority under the Clean Air Act to set its own vehicle emission standards, the California Air Resources Board (“CARB”) enacted regulations under which manufacturers of vehicles for certain model years that are in compliance with the EPA greenhouse gas emissions regulations are also deemed to be in compliance with California’s greenhouse gas emission regulations (the so-called “deemed to comply” provision). These regulations have evolved over time. In 2018, the CARB amended its existing regulations to clarify that the “deemed to comply” provision would not be available for certain model years if the EPA standards for those years were altered via an amendment of federal regulations and, in 2019, EPA announced a decision to withdraw California’s waiver of preemption under the Clean Air Act. In this decision, the EPA also affirmed the NHTSA’s authority to set nationally applicable regulatory standards under the preemption provisions of the Energy Policy and Conservation Act (EPCA). On March 9, 2022, the EPA rescinded its withdrawal of the waiver for California’s light-duty vehicle GHG and zero emission vehicle (ZEV) standards. California and Section 177 states may again enforce those standards. Subsequently, CARB clarified that the compliance with CARB’s GHG regulations is expected from model year 2021 for all manufacturers. Ferrari meets the requirements to be classified as an SVM based on the relevant regulations in the state of California. Therefore, in 2023, in agreement with CARB, Ferrari petitioned for SVM 2021-2025 alternative standards. No official approval has been received from CARB to date. It may be necessary also to increase the number of tests to be performed in order to follow the CARB specific procedures.

In relation to the safety legislation framework, in December 2023, NHTSA published an advanced notice of proposed rulemaking as a first regulatory step to introduce a new FMVSS regulation providing requirements for new technologies to prevent driver distraction, drowsiness, and drunk impaired driving. The costs of compliance associated with these and similar rulemaking may be substantial.

Other governments around the world, such as those in Canada, South Korea, China and certain Middle Eastern countries, are also creating new policies to address these issues which could be even more stringent than the U.S. or European requirements. As in the United States and Europe, these government policies if applied to us could significantly affect our product development plans. Under these existing regulations, as well as new or stricter rules or policies, we could be subject to sizable civil penalties or have to restrict or modify product offerings drastically to remain in compliance. We may have to incur substantial capital expenditures and research and development expenditures to upgrade products and manufacturing facilities, which would have an impact on our cost of production and results of operation.

In the future, the advent of self-driving technology may result in regulatory changes that we cannot predict but may include limitations or bans on human driving in specific areas. In 2020 the European Commission issued its new digital strategy policies and in 2022 its new digital strategy, which represent a priority in the European Commission’s regulatory agenda. Although no regulations have been issued in this regard, the European Commission has showed a determination to

16

strengthen Europe’s digital sovereignty and role as a standard setter, with a clear focus on data, technology, and infrastructure.

Similarly, driving bans on combustion engine vehicles could be imposed, particularly in metropolitan areas, as a result of progress in electric and hybrid technology. Several others regulations are also emerging to take into account the non-exhaust emissions such as brakes and tires particulate emissions and the environmental impact of the electric and hybrid vehicles components, with a particular focus on batteries and waste batteries.

To comply with current and future environmental rules in all markets in which we sell our cars, we may have to incur substantial capital expenditure and research and development expenditure to upgrade products and manufacturing facilities, which would have an impact on our cost of production and results of operations.

For a description of the regulations referred to in the paragraphs above please see “Overview of Our Business—Regulatory Matters”.

We depend on our suppliers, many of which are single source suppliers; and if these suppliers fail to deliver necessary raw materials, components, parts, systems, services or infrastructure of appropriate quality in a timely manner, our operations may be disrupted.

Our business depends on a significant number of suppliers, which provide the raw materials, components, parts, systems, services and infrastructure we require to manufacture cars and parts and to operate our business. We use a variety of raw materials in our business, including aluminum, and precious metals such as palladium and rhodium. We source materials from a limited number of suppliers. We cannot guarantee that we will be able to maintain access to these raw materials, and in some cases this access may be affected by factors outside of our control and the control of our suppliers. In addition, prices for these raw materials fluctuate and while we seek to manage this exposure, we may not be successful in mitigating these risks.

As with raw materials, we are also at risk of supply disruption and shortages in parts and components we purchase for use in our cars. We source a variety of key components from third parties, including transmissions, brakes, driving-safety systems, navigation systems, mechanical, electrical and electronic parts, plastic components as well as castings and tires, which makes us dependent upon the suppliers of such components. In coming years, we will also require a greater number of components for hybrid and electric engines as we continue to deploy hybrid and electric technology in our cars, and we expect producers of these components will be called upon to increase the levels of supply as the shift to hybrid or electric technology gathers pace in the industry. While we obtain components from multiple sources whenever possible, similar to other small volume car manufacturers, most of the key components we use in our cars are purchased by us from single source suppliers. We generally do not qualify alternative sources for most of the single-sourced components we use in our cars and we do not maintain long-term agreements with a number of our suppliers. Furthermore, we have limited ability to monitor the financial stability of our suppliers.

While we believe that we may be able to establish alternate supply relationships and can obtain or engineer replacement components for our single-sourced components, we may be unable to do so in the short term, or at all, at prices or costs that we believe are reasonable. Qualifying alternate suppliers or developing our own replacements for certain highly customized components of our cars may be time consuming, costly and may force us to make costly modifications to the designs of our cars.

Moreover, as the lifecycle of several components becomes shorter in light of the technological shift affecting the industry, a number of the components we use in our production processes may become in the near term obsolete, which will require us to implement new procurement strategies. Those strategies may not be successful and we may not be able to source new components in a timely manner or at competitive prices, and our results of operations may be adversely affected.

In the past, we have replaced certain suppliers because they failed to provide components that met our quality control standards. The loss of any single or limited source supplier or the disruption in the supply of components from these suppliers could lead to delays in car deliveries to our clients, which could adversely affect our relationships with our clients and also materially and adversely affect our operating results and financial condition. The supply of raw materials, parts and components may also be disrupted or interrupted by natural disasters, or by unexpected fluctuations in market demand and supply, such as the global shortage of semiconductors that impacted the automotive industry in particular, primarily in 2021. If any major disasters occur, such as earthquakes, fires, floods, hurricanes, wars, terrorist attacks, pandemics or other events,

17

our supply chain may be disrupted, which may stop or delay production and shipment of our cars. The ongoing conflict between Russia and Ukraine, the recognition by Russia of the independence of the self-proclaimed republics of Donetsk and Luhansk, in the Donbas region of Ukraine and the resulting geopolitical tensions continue to have a significant impact on the global economy resulting in a sharp increase in energy prices and higher prices for certain raw materials and goods and services, which in turn is contributing to higher inflation globally. The Russian/Ukrainian conflict has continued to escalate without a resolution expected in the near future, with the short and long-term impact on financial and business conditions in Europe remaining highly uncertain. Many governments around the world, including those of the United States, the European Union and Japan, have announced the imposition of sanctions on certain industry sectors and parties in Russia and the regions of Donetsk and Luhansk, as well as enhanced export controls on certain industries and products, including luxury goods, and the exclusion of certain Russian financial institutions from the SWIFT system. On March 11, 2022, the President of the United States issued an executive order prohibiting exports to Russia of luxury goods (including luxury transportation items such as automobiles and racing cars). Shortly thereafter, on March 15, 2022, the Council of the European Union imposed new sanctions on Russia prohibiting the export of luxury goods having a value in excess of €300 per item. These and any additional sanctions and export controls, as well as any counterresponses by the governments of Russia or other jurisdictions, could adversely affect, directly or indirectly, our supply chain, with negative implications on the availability and prices of raw materials, and our customers, as well as the global financial markets and financial services industry. See also “We are subject to risks related to pandemics or public health crises that may materially and adversely affect our business” for a discussion of widespread public health crises which may affect our supply chain directly or indirectly.

Changes in our supply chain have in the past resulted and may in the future result in increased costs and delays in car production. We have also experienced cost increases from certain suppliers in order to meet our quality targets and development timelines and because of design changes that we have made, and we may experience similar cost increases in the future. We are negotiating with existing suppliers for cost reductions, seeking new and less expensive suppliers for certain parts, and attempting to redesign certain parts to make them less expensive to produce. If we are unsuccessful in our efforts to control and reduce supplier costs while maintaining a stable source of high quality supplies, our operating results will suffer. Additionally, cost reduction efforts may disrupt our normal production processes, thereby harming the quality or volume of our production.

Furthermore, if our suppliers fail to provide components in a timely manner or at the level of quality necessary to manufacture our cars, our clients may face longer waiting periods which could result in negative publicity, harm our reputation and relationship with clients and have a material adverse effect on our business, operating results and financial condition.

Our low volume strategy may limit potential profits, and if volumes increase our brand exclusivity may be eroded.

A key to the appeal of the Ferrari brand and our marketing strategy is the aura of exclusivity and the sense of luxury which our brand conveys. A central facet to this exclusivity is the limited number of models and cars we produce and our strategy of maintaining our car waiting lists to reach the optimal combination of exclusivity and client service. Our low volume strategy is also an important factor in the prices that our clients are willing to pay for our cars. This focus on maintaining exclusivity limits our potential sales growth and profits compared to manufacturers less reliant on the exclusivity of their products.

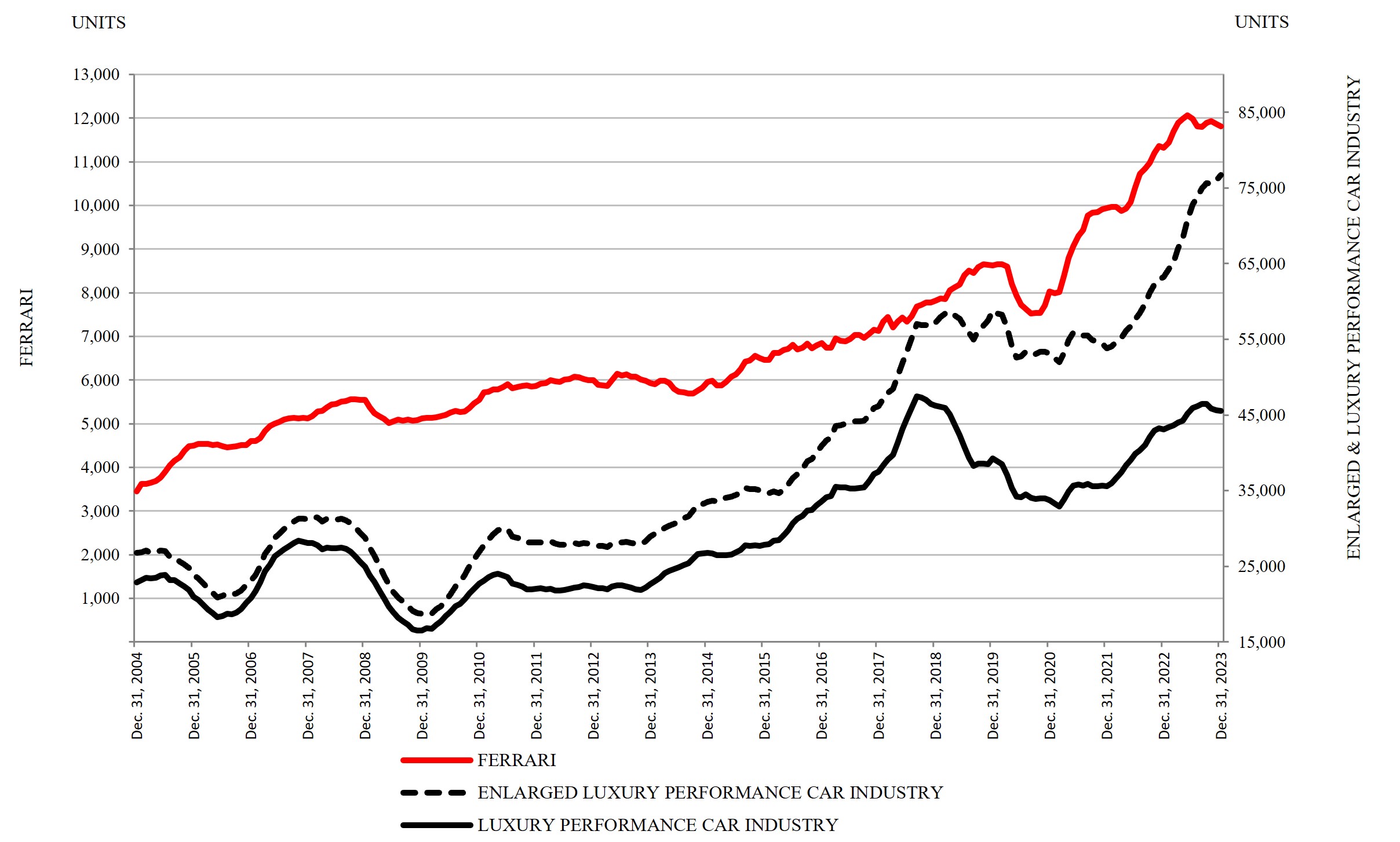

On the other hand, our current growth strategy contemplates a measured but significant increase in car sales above current levels as we target a larger customer base and modes of use, we increase our focus on reaching a younger customer base and creating new Ferrari collectors, and our product portfolio evolves with a broader product range. We sold 13,663 cars in 2023 compared to 11,155 cars in 2021 and 7,255 cars in 2014, the year before our initial public offering, and sales are expected to continue to increase gradually.

In pursuit of our strategy, we may be unable to maintain the exclusivity of the Ferrari brand. If we are unable to balance brand exclusivity with increased production, we may erode the desirability and ultimately the consumer demand or relative pricing for our cars. As a result, if we are unable to increase car production meaningfully or introduce new car models without eroding the image of exclusivity in our brand we may be unable to significantly increase our revenues.

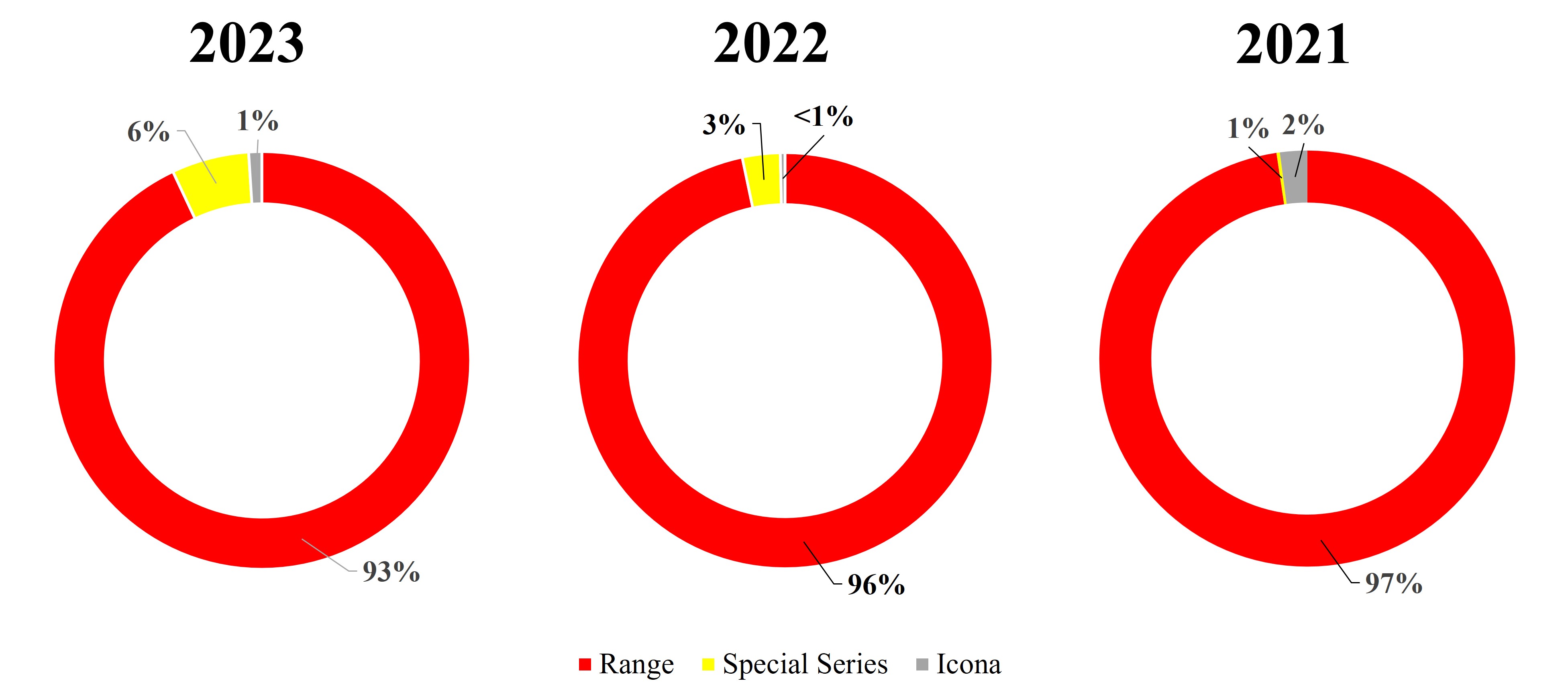

The small number of car models we produce and sell may result in greater volatility in our financial results.

We depend on the sales of a small number of car models to generate our revenues. Our current product portfolio consists of eight Range models, four Special Series models and one strictly limited edition Icona model. In 2022, with the

18

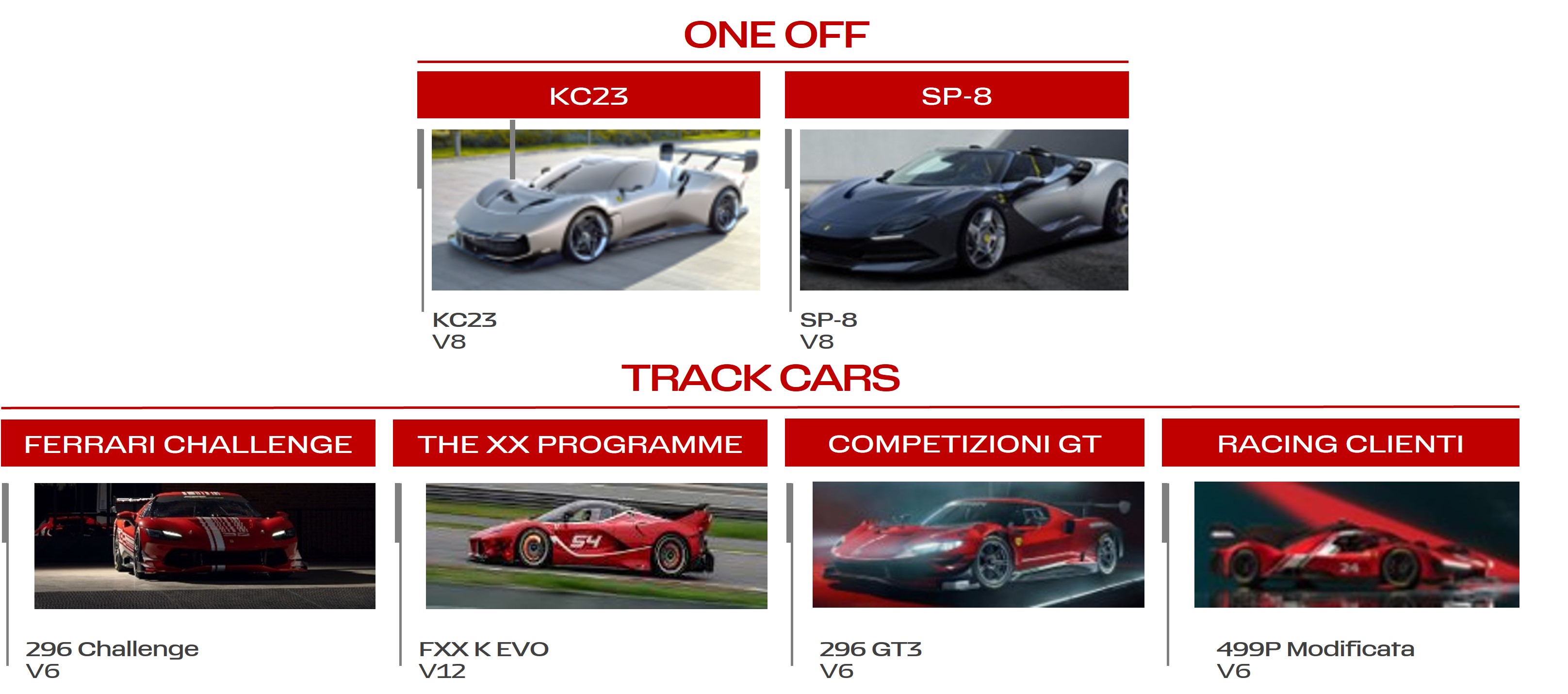

launch of the Purosangue and the 296 GTS, we met our previously announced objective of introducing 15 new models by 2022 (as announced at our Capital Markets Day in September 2018), which is unprecedented for Ferrari over a similar time frame. At our Capital Markets Day in June 2022, we announced our plan to introduce 15 new models over the period from 2023 to 2026. In 2023, we launched five new models: the Roma Spider, the SF90 XX Stradale and SF90 XX Spider (the first ever street legal XX models), the 296 Challenge and the 499P Modificata. Despite our expanded offering, a limited number of models will continue to account for a large portion of our revenues at any given time in the foreseeable future, compared to other automakers. Therefore, a single unsuccessful new model would harm us more than it would other automakers. There can be no assurance that our cars will continue to be successful in the market, or that we will be able to launch new models on a timely basis compared to our competitors. It generally takes several years from the beginning of the development phase to the start of production for a new model and the car development process is capital intensive. As a result, we would likely be unable to replace quickly the revenue lost from one of our main car models if it does not achieve market acceptance. Furthermore, our revenues and profits may also be affected by our Special Series and limited edition models (including the Icona limited editions) that we launch from time to time and which are typically priced higher than our range models. There can be no assurance that we will be successful in developing, producing and marketing additional new cars (including our Special Series and limited edition models) to sustain sales growth in the future.

Our controlled growth strategy exposes us to risks.

Our growth strategy includes a controlled expansion of our sales and operations, including the launching of new car models and expanding sales, as well as dealer operations and workshops, in targeted growth regions internationally. In particular, our growth strategy includes the opportunity for us to expand operations in regions and markets that we have identified as having relatively high growth potential. We may encounter difficulties in entering and establishing ourselves in these markets, including in establishing new successful dealership networks and facing more significant competition from competitors that are already present in those regions.

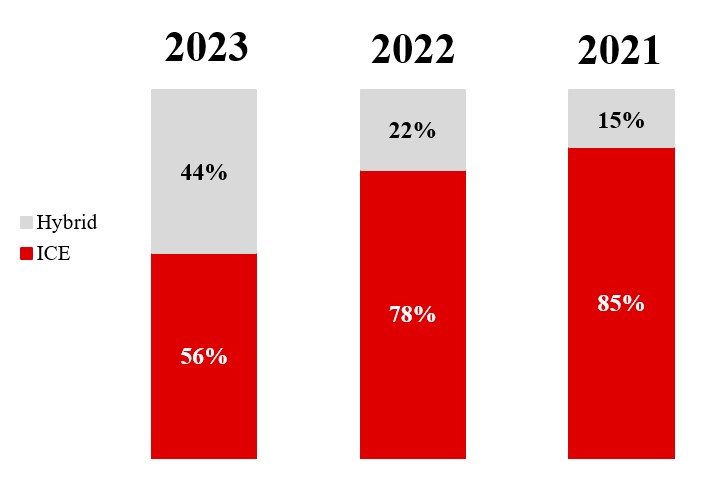

Our growth depends on the continued success of our existing cars, as well as the successful introduction of new cars. Our ability to create new cars and to sustain existing car models is affected by whether we can successfully anticipate and respond to consumer preferences and car trends. The failure to develop successful new cars or delays in their launch that could result in others bringing new products and leading-edge technologies to the market first, could compromise our competitive position and hinder the growth of our business. As part of our growth strategy, we broadened the range of our models to capture additional customer demand for different types of vehicles and modes of utilization. In 2022, with the launch of the Purosangue and the 296 GTS, we met our previously announced objective of introducing 15 new models by 2022 (as announced at our Capital Markets Day in September 2018), which is unprecedented for Ferrari over a similar time frame. At our Capital Markets Day in June 2022, we announced our plan to introduce 15 new models over the period from 2023 to 2026. In 2023, we launched five new models: the Roma Spider, the SF90 XX Stradale and SF90 XX Spider (the first ever street legal XX models), the 296 Challenge and the 499P Modificata. In addition, we are gradually but rapidly expanding the use of hybrid and electric technology in our road cars as we broaden and expand our product portfolio. In 2023, hybrid cars represented 44% of our shipments. While we will seek to ensure that these changes remain fully consistent with the Ferrari car identity, we cannot be certain that they will prove profitable and commercially successful.

Our controlled growth strategy may expose us to new business risks that we may not have the expertise, capability or the systems to manage. This strategy will also place significant demands on us by requiring us to continuously evolve and improve our operational, financial and internal controls. Continued expansion also increases the challenges involved in maintaining high levels of quality, management and client satisfaction, recruiting, training and retaining sufficiently skilled management, technical and marketing personnel. If we are unable to manage these risks or meet these demands, our growth prospects and our business, results of operations and financial condition could be adversely affected.

We continuously improve our international network footprint and skill set. We also plan to open additional retail stores in international markets. We do not yet have significant experience directly operating in many of these markets, and in many of them we face established competitors. Many of these countries have different operational characteristics, including but not limited to employment and labor, transportation, logistics, real estate, environmental regulations and local reporting or legal requirements.

Consumer demand and behavior, as well as tastes and purchasing trends may differ in these markets, and as a result, sales of our products may not be successful, or the margins on those sales may not be in line with those we currently anticipate. Furthermore, such markets will have upfront short-term investment costs that may not be accompanied by sufficient revenues to achieve typical or expected operational and financial performance and therefore may be dilutive to us

19

in the short-term. In many of these countries, there is significant competition to attract and retain experienced and talented employees.

Consequently, if our international expansion plans are unsuccessful, our business, results of operations and financial condition could be materially adversely affected.

Global economic conditions and macro events may adversely affect us.

Our sales volumes and revenues may be affected by overall general economic conditions within the various countries in which we operate. Deteriorating general economic conditions may affect disposable incomes and reduce consumer wealth impacting client demand, particularly for luxury goods, which may negatively impact our profitability and put downward pressure on our prices and volumes. Furthermore, during recessionary periods, social acceptability of luxury purchases may decrease and higher taxes may be more likely to be imposed on certain luxury goods including our cars, which may affect our sales. Adverse economic conditions may also affect the financial health and performance of our dealers in a manner that will affect sales of our cars or their ability to meet their commitments to us.

The luxury performance car market is generally affected by global macroeconomic conditions and many factors affect the level of consumer spending in the luxury performance car industry, including the state of the economy as a whole, stock market performance, interest and exchange rates, inflation, political uncertainty, the availability of consumer credit, tax rates, unemployment levels and other matters that influence consumer confidence. In general, although our sales have historically been comparatively resilient in periods of economic turmoil, sales of luxury goods tend to decline during recessionary periods when the level of disposable income tends to be lower or when consumer confidence is low. Global economic growth slowed sharply in the recent years and a recovery in 2024 is uncertain. In addition, significant inflationary pressures appeared in 2021 in many of the markets in which we operate and this trend was exacerbated in 2022. While inflation recorded in 2023 was more moderate than in 2022, if inflation remains elevated or increases in the future we could face further increases in the costs we incur for raw materials, utilities or services, which could adversely affect our business and results of operations if we are not able to pass on the increased costs to our customers or successfully implement other mitigating actions. Following the rise in inflation, several main central banks raised interest rates rapidly over the course of 2022 and part of 2023. While certain central banks now appear to follow a softer monetary stance, a higher cost of borrowing compared to recent historical periods may persist in the market. Such increases could impact our ability to obtain affordable financing or could make our cars less affordable to clients, which could cause consumers to delay the purchase of our cars or to purchase less expensive cars.

We distribute our products internationally and we may be affected by downturns in general economic conditions or uncertainties regarding future economic prospects that may impact the countries in which we sell a significant portion of our products. In particular, the majority of our current sales are in the EU and in the United States; if we are unable to expand in other growth markets, a downturn in mature economies such as the EU and the United States may negatively affect our financial performance. In addition, uncertainties regarding future trade arrangements and industrial policies in various countries or regions create additional macroeconomic risk. In the United States, any policy to discourage import into the United States of vehicles produced elsewhere could adversely affect our operations. Any new policies may have an adverse effect on our business, financial condition and results of operations. In general, the banking, economic and monetary crisis, as well as the escalating energy prices triggered by the ongoing conflict between Russia and Ukraine, as well as conflicts elsewhere in the world (including the conflict between Israel and Hamas which has the potential for escalation in the region), may reduce customers’ interest for, and financial ability to buy, luxury products. Although Mainland China, Hong Kong and Taiwan only represented 10 percent of our net revenues in 2023 and is expected to represent a limited proportion of our growth in the short term, slowing economic conditions in Mainland China, Hong Kong and Taiwan may adversely affect our revenues in that region. A significant decline in the EU, the global economy or in the specific economies of our markets, or in consumers’ confidence, could have a material adverse effect on our business. See also “Developments in China and other growth markets may adversely affect our business”.

Additionally, sanctions and export controls which could be introduced as a result of geopolitical tensions and conflicts could adversely affect, directly or indirectly, our supply chain and customers, as well as the global financial markets and financial services industry. See also “We depend on our suppliers, many of which are single source suppliers; and if these suppliers fail to deliver necessary raw materials, systems, components and parts of appropriate quality in a timely manner, our operations may be disrupted”.

20

We are subject to risks related to epidemics, pandemics or other public health crises that may materially and adversely affect our business.

Public health crises such as epidemics, pandemics or similar outbreaks could adversely impact our business. From 2020 to 2022, the global spread of COVID-19, including variants thereof, led to governments around the world mandating increasingly restrictive measures to contain the pandemic, including social distancing, quarantine, “shelter in place” or similar orders, travel restrictions and suspension of non-essential business activities. The COVID-19 pandemic caused significant disruption to the global economy, including changes in consumer spending and behavior, disruption to supply chains and financial markets, as well as restrictions on business and individual activities, leading to a global economic slowdown and a severe recession in several of the markets in which we operate, which may reverberate after all restrictions are lifted. Our operations were also profoundly disrupted, with our production suspended at our two plants for several months in 2020, and our suppliers and dealers were similarly affected. Governmental restrictions were lifted and partly reintroduced reflecting developments in the pandemic. Future pandemics may have similar, or worse, impacts on our operations.

Furthermore, pandemics or other widespread public health crises may lead to financial distress for our suppliers or dealers, as a result of which they may have to permanently discontinue or substantially reduce their operations.

Any of the foregoing could limit customer demand or our capacity to meet customer demand and have a material adverse effect on our business, results of operations and financial condition.

Pandemics or other widespread public health crises may also exacerbate other risks disclosed in this section, including, but not limited to, our competitiveness, demand for our products, shifting consumer preferences, exchange rate fluctuations, customers’ and dealers’ access to affordable financing, and credit market conditions affecting the availability of capital and financial resources.

We face competition in the luxury performance car industry.

We face competition in all product categories and markets in which we operate. We compete with other international luxury performance car manufacturers which own and operate well-known brands of high-quality cars, some of which form part of larger automotive groups and may have greater financial resources and bargaining power with suppliers than we do, particularly in light of our policy to maintain low volumes in order to preserve and enhance the exclusivity of our cars. In addition, several other manufacturers have recently entered or are attempting to enter the upper end of the luxury performance car market, including with advanced electric technology, thereby increasing competition. We believe that we compete primarily on the basis of our brand image, the performance and design of our cars, our reputation for quality and the driving experience for our customers. If we are unable to compete successfully, our business, results of operations and financial condition could be adversely affected.

Our business is subject to changes in client preferences and trends in the automotive and luxury industries.

Our continued success depends in part on our ability to originate and define products and trends in the automotive and luxury industries, as well as to anticipate and respond promptly to changing consumer demands and automotive trends in the design, styling, technology, production, merchandising and pricing of our products. Our products must appeal to a client base whose preferences cannot be predicted with certainty and are subject to rapid change. Evaluating and responding to client preferences has become even more complex in recent years, due to our expansion in new geographical markets. The introduction of hybrid and electric technology and the associated changes in customer preferences that may follow are also a challenge we will face in future periods. See also “If we are unable to keep up with advances in high performance car technology, our brand and competitive position may suffer” and “The introduction of electric technology in our cars is costly and its long-term success is uncertain”. In addition, there can be no assurance that we will be able to produce, distribute and market new products efficiently or that any product category that we may expand or introduce will achieve sales levels sufficient to generate profits. Furthermore this risk is particularly pronounced as we expand in accordance with our strategy into adjacent segments of the luxury industry, where we do not have a level of experience and market presence comparable to the one we have in the automotive industry. Any of these risks could have a material adverse effect on our business, results of operations and financial condition.

21

Demand for luxury goods, including luxury performance cars, is volatile, which may adversely affect our operating results.

Volatility of demand for luxury goods, in particular luxury performance cars, may adversely affect our business, operating results and financial condition. The market in which we sell our cars is subject to volatility in demand. Demand for luxury automobiles depends to a large extent on general, economic, political and social conditions in a given market as well as the introduction of new vehicles and technologies. Global economic growth slowed sharply in 2022, stabilized in 2023 and the outlook for 2024 is uncertain. As a luxury performance car manufacturer and low volume producer, we compete with larger automobile manufacturers many of which have greater financial resources in order to withstand changes in the market and disruptions in demand. Demand for our cars may also be affected by factors directly impacting the cost of purchasing and operating automobiles, such as the availability and cost of financing, prices of raw materials and parts and components, fuel costs and governmental regulations, including tariffs, import regulation and other taxes, including taxes on luxury goods, resulting in limitations to the use of high performance sports cars or luxury goods more generally. Volatility in demand may lead to lower car unit sales, which may result in downward price pressure and adversely affect our business, operating results and financial condition. The impact of a luxury market downturn may be particularly pronounced for the most expensive among our car models, which generate a more than proportionate amount of our profits, therefore exacerbating the impact on our results. In addition, these effects may have a more pronounced impact on us given our low volume strategy and relatively smaller scale as compared to large global mass-market automobile manufacturers.

The value of our brand depends in part on the automobile collector and enthusiast community.

An important factor in the connection of clients to the Ferrari brand is our strong relationship with the global community of automotive collectors and enthusiasts, particularly collectors and enthusiasts of Ferrari automobiles. This is influenced by our close ties to the automotive collectors’ community and our support of related events (such as car shows and driving events) at our headquarters in Maranello and through our dealers, the Ferrari museums and affiliations with regional Ferrari clubs. The support of this community also depends upon the perception of our cars as collectibles, which we also support through our Ferrari Classiche services, and the active resale market for our automobiles which encourages interest over the long-term. The increase in the number of cars we produce relative to the number of automotive collectors and purchasers in the secondary market may adversely affect our cars’ value as collectible items and in the secondary market more broadly.

If there is a change in collector appetite or damage to the Ferrari brand, our ties to, and the support we receive from, this community may be diminished. Such a loss of enthusiasm for our cars from the automotive collectors’ community could harm the perception of the Ferrari brand and adversely impact our sales and profitability.

We depend on our manufacturing facilities in Maranello and Modena.

We assemble all of the cars that we sell and manufacture, and all of the engines we use in our cars, at our production facility in Maranello, Italy, where we also have our corporate headquarters. We manufacture all of our car chassis in a nearby facility in Modena, Italy. Our Maranello or Modena plants could become unavailable either permanently or temporarily for a number of reasons, including contamination, power shortage or labor unrest. Alternatively, changes in law and regulation, including export, tax and employment laws and regulations, or economic conditions, including wage inflation, could make it uneconomic for us to continue manufacturing our cars in Italy. In the event that we were unable to continue production at either of these facilities or it became uneconomic for us to continue to do so, we would need to seek alternative manufacturing arrangements which would take time and reduce our ability to produce sufficient cars to meet demand. Moving manufacturing to other locations may also affect the perception of our brand and car quality among our clients. Such a transfer would materially reduce our revenues and could require significant investment, which as a result could have a material adverse effect on our business, results of operations and financial condition.

Maranello and Modena are located in the Emilia-Romagna region of Italy which has the potential for seismic activity. For instance, in 2012 a major earthquake struck the region, causing production at our facilities to be temporarily suspended for one day. If major disasters such as earthquakes, fires, floods, hurricanes, wars, terrorist attacks, pandemics or other events occur, our headquarters and production facilities may be seriously damaged, or we may stop or delay production and shipment of our cars. Such damage from disasters or unpredictable events could have a material adverse impact on our business, results from operations and financial condition.

22

We are subject to risks associated with climate change and other environmental impacts, as well as an increased focus of regulators and stakeholders on environmental matters.

Global climate change is resulting, and is expected to continue to result, in natural disasters and extreme weather, such as drought, wildfires, storms, sea-level rise, flooding, heat waves and cold waves, occurring more frequently or with greater intensity. Such extreme events are driving changes in market dynamics, stakeholder expectations, local, national and international climate change policies and regulations.

We are subject to climate-related risks where we conduct our business. Physical impacts of climate change, including natural disasters and adverse weather, could result in disruptions to us, our suppliers, vendors, customers and logistics hubs. These risks may also exacerbate other risks disclosed in this “Risk Factors” section, including but not limited to, our competitiveness, demand for our products, shifting consumer preferences, availability and price of raw materials, and concentration of our production activities in Maranello and Modena.

The global automotive industry in particular is currently experiencing significant developments due to an increased focus on climate change and evolving regulatory requirements relating to fuel efficiency, electrification and greenhouse gas emissions, among others. These evolving requirements and technological changes have caused us, and are expected to continue to cause us, to adapt and change certain aspects of our operations, our future plans and strategies and the allocation of our resources. Failure to effectively manage these aspects may result in increased costs, reputational risks, limits in our ability to manufacture or market certain of our products, or otherwise negatively impact our business, results of operations, profitability and competitive position.