UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR 12(G) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended |

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number

(Exact name of Registrant as specified in its charter) |

|

(Jurisdiction of incorporation or organization) |

|

People’s Republic of |

(Address of principal executive offices) |

|

Telephone: |

People’s Republic of |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

| |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

| Accelerated filer ☐ |

| |

|

|

|

| Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☒ |

| International Financial Reporting Standards as issued |

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

Table of Contents

Page | ||

5 | ||

7 | ||

7 | ||

7 | ||

35 | ||

63 | ||

64 | ||

79 | ||

86 | ||

89 | ||

89 | ||

90 | ||

97 | ||

98 | ||

98 | ||

98 | ||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 98 | |

98 | ||

101 | ||

101 | ||

101 | ||

101 | ||

101 | ||

102 | ||

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 102 | |

102 | ||

103 | ||

103 | ||

103 | ||

103 | ||

103 | ||

104 |

3

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements in this annual report with respect to the Company’s current plans, estimates, strategies and beliefs and other statements that are not historical facts are forward-looking statements about the future performance of the Company. Forward-looking statements include, but are not limited to, those statements using words such as “believe,” “expect,” “plans,” “strategy,” “prospects,” “forecast,” “estimate,” “project,” “anticipate,” “aim,” “intend,” “seek,” “may,” “might,” “could” or “should,” and words of similar meaning in connection with a discussion of future operations, financial performance, events or conditions. From time to time, oral or written forward-looking statements may also be included in other materials released to the public. These statements are based on management’s assumptions, judgments and beliefs in light of the information currently available to it. The Company cautions investors that a number of important risks and uncertainties could cause actual results to differ materially from those discussed in the forward-looking statements, including but not limited to, product and service demand and acceptance, changes in technology, economic conditions, the impact of competition and pricing, government regulation, and other risks contained in reports filed by the company with the Securities and Exchange Commission. Therefore, investors should not place undue reliance on such forward-looking statements. Actual results may differ significantly from those set forth in the forward-looking statements.

All such forward-looking statements, whether written or oral, and whether made by or on behalf of the company, are expressly qualified by the cautionary statements and any other cautionary statements which may accompany the forward-looking statements. In addition, the company disclaims any obligation to update any forward-looking statements to reflect events or circumstances after the date hereof.

4

PART I

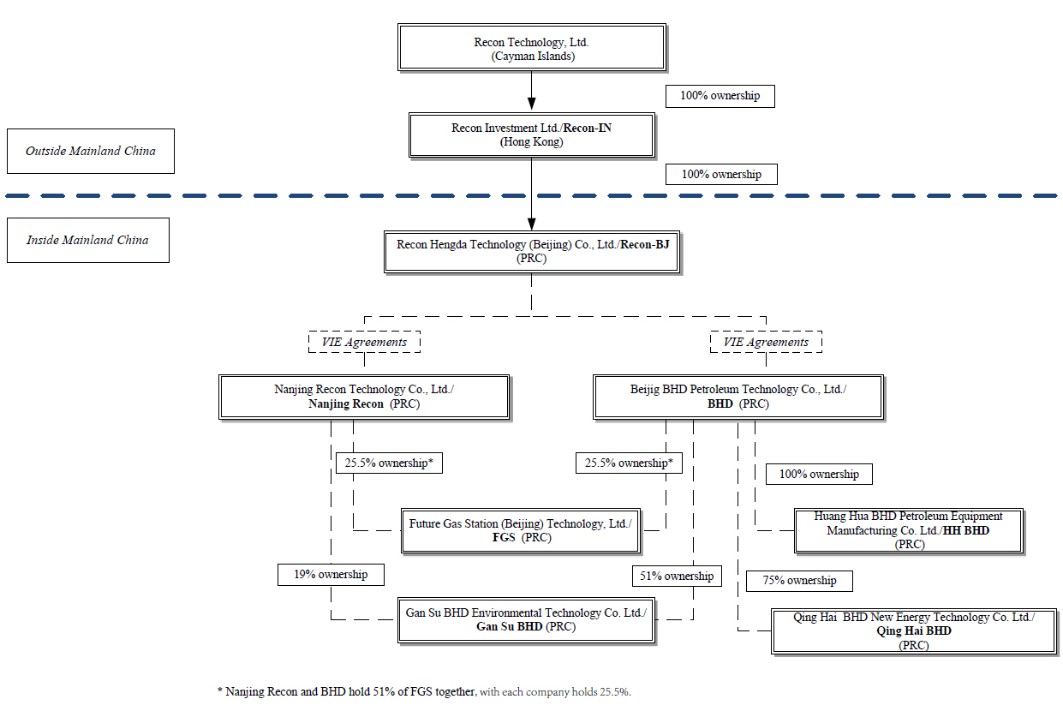

We are a Cayman Islands holding company. We are not a Chinese operating company, and do not conduct business operations directly in China. All China operations are conducted by our subsidiaries established in the People’s Republic of China (“PRC” or “China”) and in the Hong Kong Special Administrative Region of the People’s Republic of China (“HKSAR” or “Hong Kong”), and by our contractual arrangements with variable interest entities, or “VIEs,” and the VIEs’ subsidiaries located in China. This structure involves unique risks to investors. The VIE structure provides contractual exposure to foreign investment in Chinese-based companies, pursuant to which U.S. GAAP accounting rules require us to consolidate such VIEs’ financial results in our financial statements. VIE structures are generally used where Chinese law prohibits direct foreign investment in the operating companies. Investors may never directly hold equity interests in the Chinese operating companies. Unless otherwise stated, as used in this prospectus and in the context of describing our operations and consolidated financial information, “we,” “us,” “Company,” or “our,” refers to Recon Technology, Ltd, a Cayman Islands exempted limited company, together with our subsidiaries. “Our subsidiaries” refer to Recon Investment Ltd. and Recon Hengda Technology (Beijing) Co. Ltd., or Recon-IN and Recon-BJ, respectively. “VIEs” refers to the PRC variable interest entities and their subsidiaries (Nanjing Recon Technology Co., Beijing BHD Petroleum Technology Co., Gan Su BHD Environmental Technology Co. Ltd, Huang Hua BHD Petroleum Equipment Manufacturing Co. Ltd., and Qing Hai BHD New Energy Technology Co. Ltd., Future Gas Station (Beijing) Technology, Ltd., or “Nanjing Recon,” “BHD,” “Gan Su BHD,” “HH BHD,” “Qing Hai BHD,” and “FGS” respectively). You are not investing in Nanjing Recon, BHD, Gan Su BHD, HH BHD, Qing Hai BHD, or FGS. Instead, we entered into certain contracts (the “VIE Agreements”) dated April 1, 2019, which are used to provide investors exposure to foreign investment in China-based companies where Chinese law prohibits or restricts direct foreign investment in the operating companies. A wholly foreign-owned entity (“WFOE”) is a limited liability company based in the People’s Republic of China but wholly owned by foreign investors. In our instance, Recon-BJ is a WFOE wholly owned by us through our subsidiary, Recon-IN, a Hong Kong limited company. As a result of our direct ownership in the WFOE and the VIE Agreements, we are regarded as the primary beneficiary of the VIE for accounting purposes.

We mainly conduct our business through the VIEs, Nanjing Recon, BHD and their respective subsidiaries by means of Contractual Arrangements. Because we do not hold equity interests in the VIEs and their subsidiaries, we are subject to risks due to the uncertainty of the interpretation and application of the PRC laws and regulations regarding VIEs and the VIE structure, including but not limited to regulatory review of overseas listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the contractual arrangements with the VIEs. We are also subject to the risk that the PRC government could disallow the VIE structure, which would likely result in a material change in our operations and as a result the value of Securities may depreciate significantly or become worthless. At the time of this filing, the Contractual Agreements have not been tested in a court of law.

For U.S. GAAP purposes, each VIE has its own operating cash flow. Cash flow between our Company and the VIEs primarily consists of transfers from us to the VIEs for supplemental working capital, which is mainly used in purchase of materials and payment of operating expenses and investments. In addition, the VIEs occasionally make payments on our behalf when we experience a cash shortage. For the fiscal years ended June 30, 2023, 2022 and 2021, net cash transferred from the Company to the VIEs was RMB 69,562,912, RMB55,569,342 and RMB15,720,667, respectively. There was no cash transferred from the VIEs to the Company or fees paid on behalf of the Company by the VIEs during the years ended June 30, 2023, 2022 and 2021. Neither we nor the VIEs have present plans to distribute earnings or settle amounts owed under the Contractual Agreements. Cash in the VIEs are expected to be retained for business growth and operation. No dividends or distributions have been declared to pay to us from our subsidiaries or the VIEs. No dividends or distributions were made to any U.S. investors.

We are also subject to legal and operational risks associated with being based in and having the majority of the Company’s and VIEs’ operations in China. These risks may result in a material change in our operations, or a complete hindrance of our ability to offer or continue to offer our securities to investors and could cause the value of our securities to significantly decline or become worthless. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structures, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

5

On July 6, 2021, the General Office of the Communist Party of China Central Committee and the General Office of the State Council jointly issued an announcement to crack down on illegal activities in the securities market and promote the high-quality development of the capital market, which, among other things, requires the relevant governmental authorities to strengthen cross-border oversight of law-enforcement and judicial cooperation, to enhance supervision over China-based companies listed overseas, and to establish and improve the system of extraterritorial application of the PRC securities laws. On July 10, 2021, the PRC State Internet Information Office issued the Measures of Cybersecurity Review (Revised Draft for Comments, not yet effective), which requires cyberspace operators with personal information of more than 1 million users who want to list abroad to file a cybersecurity review with the Office of Cybersecurity Review. Furthermore, the Chinese education sector is going through a series of reforms and new laws and guidelines have been recently promulgated and released to regulate our industry. As of the date of this prospectus, these new laws and guidelines have not impacted the Company’s ability to conduct its business, accept foreign investments, or list on a U.S. or other foreign exchange because the Company and the VIEs are not involved in the education industry and do not maintain data of more than 1 million users; however, there are uncertainties in the interpretation and enforcement of these new laws and guidelines, which could materially and adversely impact our business and financial outlook. On February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the relevant system and rules for the management of overseas listing records, which will be implemented from March 31, 2023. A total of six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”) and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement, misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the listing and trading of our Class A Ordinary Shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required. Further, we believe, as of the date of this annual report, none of the circumstances prohibiting the overseas offering and listing by domestic companies established in mainland China as listed above applies to us, and we can offer and continue to offer our Class A Ordinary Shares on Nasdaq.

In accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we have been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or the Domestic Companies (defined below) in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or the Domestic Companies, and impose a fine of between RMB1,000,000 yuan and RMB10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

6

Further, on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which will come into effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators, any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws and regulations. Once effective, any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected of committing a crime. As of the date of this annual report, we believe that we and our subsidiaries have not provided or publicly disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. We intend to strictly comply with the Confidentiality Provisions and other relevant PRC laws and regulations in our offering and listing on Nasdaq in future.

However, any failure of us or the Domestic Companies to fully comply with the Listing Records Rules and/or the Confidentiality Provisions, once effective, may significantly limit or completely hinder our ability to offer or continue to offer our Class A Ordinary Shares on Nasdaq, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our Class A Ordinary Shares to significantly decline in value or become worthless. See “Risk Factor — Risks Related to Doing Business in China — The Chinese government exerts oversight and control over overseas offerings and listing conducted by China-based issuers under the Listing Records Rules and the Confidentiality Provisions, which could significantly limit or completely hinder our ability to offer or continue to offer our Class A Ordinary Shares to investors and could cause the value of our Class A Ordinary Shares to significantly decline or become worthless.”

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable for annual reports on Form 20-F.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable for annual reports on Form 20-F.

ITEM 3. KEY INFORMATION

A. Selected Financial Data

The following table presents the selected consolidated financial information for our company. The selected consolidated statements of operations data for the three years ended June 30, 2021, 2022 and 2023 and the consolidated balance sheet data as of June 30, 2021, 2022, and 2023 have been derived from our audited consolidated financial statements set forth in “Item 18 – Financial Statements”. The selected consolidated balance sheet data for the year ended June 30, 2021 have been derived from our audited consolidated balance sheet as of June 30, 2021, which is not included in this annual report. Our historical results do not necessarily indicate results expected for any future periods. The selected consolidated financial data should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” below. Our audited consolidated financial statements are prepared and presented in accordance with Generally Accepted Accounting Principles in the United States of America, or U.S. GAAP.

7

Following the one-for-five reverse stock split of our Class A Ordinary Shares effective on December 27, 2019, and following the dual class structure divided into Class A Ordinary Shares and Class B Ordinary Shares effective on April 5, 2021, all share and per share amounts disclosed throughout this annual report, in the table below and in our consolidated financial statements have been retroactively updated to reflect this change in capital structure, unless otherwise indicated. Please see “Item 4. Information on the Company—History and Development of the Company”.

(All amounts in thousands of Renminbi, except Dividend per share in U.S. dollars and Shares outstanding)

Statement of operations data:

| For the years ended June 30, | |||||

2023 |

| 2022 |

| 2021 | ||

| RMB¥ |

| RMB¥ |

| RMB¥ | |

Revenue |

| 67,114,378 |

| 83,777,571 |

| 47,938,575 |

Loss from operations |

| (69,332,735) |

| (82,313,417) |

| (61,578,948) |

Net income (loss) attributable to Recon Technology, Ltd |

| (59,167,301) |

| 95,586,795 |

| (22,832,734) |

Loss per share* |

|

|

|

|

|

|

-Basic |

| (1.74) |

| 3.19 |

| (1.80) |

-Diluted |

| (1.74) |

| 3.19 |

| (1.80) |

Weighted average number of Class A and Class B Ordinary Shares used in computation* |

|

|

|

|

|

|

-Basic |

| 33,923,112 |

| 30,002,452 |

| 12,697,024 |

-Diluted |

| 33,923,112 |

| 30,002,452 |

| 12,697,024 |

8

Balance sheet data:

| 2023 |

| 2022 |

| 2021 | |

RMB¥ | RMB¥ | RMB¥ | ||||

Current assets |

| 504,413,173 |

| 445,617,041 |

| 488,505,185 |

Total assets |

| 531,824,577 |

| 490,242,084 |

| 566,516,660 |

Current liabilities |

| 61,032,862 |

| 52,878,284 |

| 76,462,604 |

Total liabilities |

| 92,673,674 |

| 77,357,323 |

| 279,001,194 |

Total shareholder’s equity |

| 449,206,962 |

| 420,631,729 |

| 295,095,034 |

Shares outstanding (A Shares) | 40,528,218 |

| 29,700,718 |

| 26,868,391 | |

Shares outstanding (B Shares)* |

| 7,100,000 | 4,100,000 | — |

* The dual class structure divided into Class A Ordinary Shares and Class B Ordinary Shares effective on April 5, 2021

B. Capitalization and Indebtedness

Not applicable by 20-F as an annual report.

C. Reasons for the Offer and Use of Proceeds

Not applicable by 20-F as an annual report.

D. Risk Factors

Investing in our Class A Ordinary Shares involves a high degree of risk. Before deciding whether to invest in our Class A Ordinary Shares, you should consider carefully the risks and uncertainties described below. There may be other unknown or unpredictable economic, business, competitive, regulatory or other factors that could have material adverse effects on our future results. If any of these risks actually occurs, our business, business prospects, financial condition or results of operations could be seriously harmed. This could cause the trading price of our Class A Ordinary Shares to decline, resulting in a loss of all or part of your investment. Please also read carefully the section above entitled “Special Note Regarding Forward-Looking Statements.”

Risks Related to Our Business

Public health epidemics or outbreaks such as COVID-19 could adversely impact our business.

Our business, financial condition and results of operations may be negatively impacted by risks related to natural disasters, extreme weather conditions, health epidemics and other catastrophic incidents, such as the COVID-19 outbreak and spread, which could significantly disrupt our operations. In December 2019, COVID-19 emerged in Wuhan, Hubei Province, China. The COVID-19 outbreak and spread has caused lockdowns, quarantines, travel restrictions, and closures of businesses and schools.

In addition, COVID-19 has caused severe disruptions in transportation, limited access to our facilities, client work fields and limited support from workforce employed in our operations, and as a result, we experienced and may continue to experience the delays in provision of services to our customers and completion of contractual performance obligations, affecting our revenue recognition and collection schedule of account receivables.

During the six months ended December 31, 2022, either the Company’s or its customers’ operations were occasionally affected by regional outbreaks, resulting in some of its business still not returning to previous levels. In early December of 2022, the Chinese State Council issued a nationwide policy loosening the government’s control of the epidemic, which led to the emergence of widespread infections. At that time, most of the industries experienced work stoppages and production stoppages. Since the beginning of the calendar year 2023, although the extent of the future impact of COVID-19 cannot be predicted, we believe that the Company’s business has not been significantly affected and the impact of COVID-19 on the Company's business and financial results will not be sustainable in the long run.

9

We operate in a very competitive industry and may not be able to maintain our revenue and profitability.

Since the 1990s, several international companies engaged in supplying integrated automation services for the petroleum extraction industry have been qualified in China. These competitors have significantly greater financial and marketing resources and name recognition than we have. In addition, at least five domestic private competitors also compete with us, and more competitors may enter the market as Chinese petroleum companies seek to reduce oil production costs and improve efficiencies. There can be no assurance that we will be able to compete effectively in our industry.

In addition, our competitors may introduce new systems. If these new systems are more attractive to customers than the systems we currently use or may develop, our customers may switch to our competitors’ services, and we may lose market share. We believe that competition may become more intense as more integrated automation service providers, including Chinese/foreign joint ventures, are qualified to conduct business. We cannot assure you that we will be able to compete successfully against any new or existing competitors, or against any new systems our competitors may implement. Any of these competitive factors could have a material adverse effect on our revenue and profitability.

We must continually research and develop new technologies and products to remain competitive.

Because our industry is so competitive, we will need to continually research, develop and refine new technologies and offer new products to compete effectively. Many factors may limit our ability to develop and refine new products, including the availability of funds to dedicate to this portion of our business and access to new products and technologies that we can incorporate into our products, as well as marketplace resistance to new products and technologies. We believe that the Domestic Companies (defined in the following paragraph) and our products are able to compete in the marketplace based upon, among other things, our intellectual property. We cannot assure investors that applications of our and the Domestic Companies’ technologies or those of third parties, if developed, will not be rendered superfluous or obsolete by research efforts and technological advances by others in these fields.

Our company and our subsidiaries, Recon Investment Ltd. (“Recon-IN”) and Recon Hengda Technology (Beijing) Co., Ltd. (“Recon BJ”) are contractually engaged with the following PRC VIE companies and their subsidiaries: Beijing BHD Petroleum Technology Co., Ltd. (“BHD”), Future Gas Station (Beijing) Technology, Ltd. (“FGS”), Nanjing Recon Technology Co., Ltd. (“Nanjing Recon”), Gan Su BHD Environmental Technology Co. Ltd. (“Gan Su BHD”), Huang Hua BHD Petroleum Equipment Manufacturing Co. Ltd. (“HH BHD”), and Qing Hai BHD New Energy Technology Co. Ltd. (“Qing Hai BHD”) (collectively, the “Domestic Companies”). As new technologies are developed, the Domestic Companies and we may need to adapt and change our products and services, our method of marketing or delivery or alter our current business in ways that may adversely affect revenue and our ability to achieve our proposed business goals. Accordingly, there is a risk that the Domestic Companies’ and our technology will not support a viable commercial enterprise.

Our financial performance is dependent upon the sale and implementation of petroleum mining and extraction software and hardware and related services, a single, concentrated group of products.

We derive substantially all of our revenue from the license and implementation of software applications and hardware innovations for the Chinese petroleum industry. The life cycle of our products and services is difficult to estimate due in large measure to the potential effect of new software and hardware applications and enhancements, including those we introduce, and the maturation in both the Chinese petroleum and software/hardware industries. If we are unable to continually improve our software and hardware to address the changing needs of the Chinese petroleum industry, we may experience a significant decline in the demand for the Domestic Companies’ and our products and services. In such a scenario, our revenue may significantly decline.

A failure by our third-party vendors to fulfill their obligations would negatively affect our ability to operate profitably.

In the ordinary course of business, our third-party vendors have historically required advance payments before they deliver goods and services to us that enable our operations. These advance payments are often substantial, and we dedicate a material amount of our liquidity to advance these to such third-party vendors. There is no guarantee that the services we require will be delivered, whether due to supply chain disruptions or any other reason after we provide our advance payments, and many of our vendors lack sufficient insurance to protect us against such failures to deliver. Moreover, if a third-party vendor declares bankruptcy or we engage in litigation, we be unable to recover the advance fees in their entirety, if at all.

10

As a technology-oriented business, our ability to operate profitably is directly related to our ability to develop and protect our proprietary technology.

We rely on a combination of trademark, trade secret, nondisclosure, copyright and patent law to protect the Domestic Companies’ and our software and hardware, which may afford only limited protection.

Although the Chinese government has issued Nanjing Recon over ten copyrights on software and Nanjing Recon and BHD over forty patents on products, we cannot guarantee that competitors will be unable to develop technologies that are similar or superior to the Domestic Companies’ and our technology. Despite our efforts to protect the Domestic Companies’ and our proprietary rights, unauthorized parties, including customers, may attempt to reverse engineer or copy aspects of the Domestic Companies’ and our products or to obtain and use information that the Domestic Companies and we regard as proprietary. Furthermore, our competitors may independently develop substantially equivalent or superior proprietary information and techniques, reverse engineer information and techniques, or otherwise gain access to our proprietary technology. In the future, we cannot guarantee that others will not use the Domestic Companies’ and our technology without proper authorization. In addition, under the Chinese intellectual property law, the 50-year protection period for software copyright and 10-year patent protection period are not subject to renewal upon expiration.

The Domestic Companies and we develop our software products on third-party middleware software programs that are licensed by our customers from third parties, generally on a non-exclusive basis. The termination of any such licenses, or the failure of the third-party licensors to adequately maintain or update their products, could result in delay in our ability to develop, market or ship certain of our products while we seek to implement technology offered by alternative sources. While it may be necessary or desirable in the future to obtain other licenses, there can be no assurance that they will be able to do so on commercially reasonable terms or at all.

In addition, the Domestic Companies and we may initiate claims or litigation against third parties for infringement of our proprietary rights or to establish the validity, scope or enforceability of our proprietary rights. Any such claims could be time consuming, result in costly litigation, cause product development or shipment delays or force the Domestic Companies or us to enter into royalty or license agreements rather than dispute the merits of such claims, thereby impairing our financial performance by requiring the Domestic Companies or us to pay additional royalties and/or license fees to third parties. There is always a risk that patents, if issued, may be subsequently invalidated, either in whole or in part and this could diminish or extinguish protection for any technology we may license. In addition, the laws of China may not protect proprietary rights to the same extent as U.S. law. Therefore, we may be unable to meaningfully protect our rights in trade secrets, technical know-how and other non-patented technology. Any failure to enforce or protect the Domestic Companies’ and our rights could cause us to lose the ability to exclude others from issuing technology to develop or sell competing products.

We may not be able to adequately protect our intellectual property, which could cause us to be less competitive and negatively impact our business.

We rely on trademark, patent and trade secret law, as well as confidentiality agreements with certain of our employees to protect our proprietary rights. The product patents owned by the Company are employee service patents invented by the Company’s key employees. We generally require the Domestic Companies’ and our employees, consultants, advisors and collaborators to execute appropriate confidentiality agreements with, as applicable, the respective Domestic Companies and us. These agreements typically provide that all material and confidential information developed or made known to the individual during the course of the individual’s relationship with us is owned by the us and will be kept confidential and not disclosed to third parties except in specific circumstances. These agreements may be breached, and in some instances, we may not have an appropriate remedy available for breach of the agreements.

11

We may be accused of infringing the intellectual property rights of others.

In the future, the Domestic Companies and we may receive notices claiming that we are infringing the proprietary rights of third parties. We cannot guarantee that the Domestic Companies and we will not become the subject of infringement claims or legal proceedings by third parties with respect to the Domestic Companies’ and our current programs or future software developments. Our standard software license agreements contain an infringement indemnity clause under which we agree to indemnify and hold harmless our customers and business partners against liability and damages arising from claims of various copyright or other intellectual property infringement by our products. Neither the Domestic Companies nor we have been the subject of an intellectual property claim since our formation.

Our software products may contain integration challenges, design defects or software errors that could be difficult to detect and correct.

Despite extensive testing, we may, from time to time, discover defects or errors in the Domestic Companies’ and our software only after use by a customer. We may also experience delays in shipment of our software during the period required to correct such errors. In addition, we may, from time to time, experience difficulties relating to the integration of the Domestic Companies’ and our software products with other hardware or software in the customer’s environment that are unrelated to defects in such software products. Such defects, errors or difficulties may cause future delays in product introductions and shipments, result in increased costs and diversion of development resources, require design modifications or impair customer satisfaction with the Domestic Companies’ and our software. Since these software products are used by our customers to perform mission-critical functions related to petroleum mining and extraction, design defects, software errors, misuse of these products, incorrect data from external sources or other potential problems within or out of our control that may arise from the use of the Domestic Companies’ and our products could result in financial or other damages to our customers. We do not maintain product liability insurance. Although our license agreements with customers contain provisions designed to limit our exposure to potential claims as well as any liabilities arising from such claims, such provisions may not effectively protect us against such claims and the liability and costs associated therewith. To the extent we are found liable in a product liability case, we could be required to pay substantial amount of damages to an injured customer, thereby impairing our financial condition.

We are dependent on the state of the PRC’s economy as the majority of our business is conducted in the PRC.

Currently, the majority of our business operations are conducted in the PRC, and most of our customers are also located in the PRC. Accordingly, any significant slowdown in the PRC economy may cause our customers to reduce expenditures or delay the building of new facilities or projects. This may in turn lead to a decline in the demand for our products and services. That would have a material adverse effect on our business, financial condition and results of operations.

Our future success depends on our ability to help our customers find, develop and acquire petroleum reserves.

To remain competitive in our industry, our products must help our customers locate and develop or acquire new crude oil reserves to replace those depleted by production. Without successful exploration or acquisition activities, our customers’ reserves, production and revenue will decline rapidly. If the Domestic Companies’ and our technology is less well accepted for helping our customers locate additional reserves than our competitors’ technology, our customers may terminate their relationships with us, which could have a material adverse effect on our financial condition and future growth prospects.

Our customers are companies engaged in the petroleum industry and the greater energy industry, and, consequently, our financial performance is dependent upon the economic conditions of those industries.

We have derived most of our revenue to date from providing integrated automation services to Chinese petroleum companies at oilfields within China and other energy industry companies in China. Our customers’ success is intrinsically linked to economic conditions in China and in the petroleum and energy industries in general and the volatility of prices of crude oil, refined oil products and coal chemical products in particular. Each of the petroleum industry and energy industry is subject to intense competitive pressures and is affected by overall economic conditions. Demand for our services could be harmed by volatility in those industries. There can be no assurance that we will be able to continue our historical revenue growth or sustain our profitability on a quarterly or annual basis or that our results of operations will not be adversely affected by continuing or future volatility in those industries.

12

Our revenue are highly dependent on a very limited number of customers, which subjects our business to high seasonality. Our contracts with such customers may be terminated at any time, materially and adversely affecting our business.

Historically, we derived the majority of our revenue from two customers, (i) China National Petroleum Corporation (“CNPC”) and (ii) China Petroleum and Chemical Corporation (“Sinopec”).

Since the fiscal year ended June 30, 2017, Sinopec accounted for less than 10% of our revenue. From fiscal year 2022, as we developed new product lines, revenue from Sinopec increased and account for 28% of our revenue.

We provide products and services to CNPC under a series of agreements, each of which is terminable without notice. We first began to provide services to CNPC in 2000. CNPC accounted for approximately 50%, 39% and 39% of our revenue in the fiscal years ended June 30, 2022, 2021 and 2020, respectively, and any termination of our business relationships with CNPC would materially harm our operations.

In the fiscal year ended June 30, 2019, we had established a solid relationship with Shenhua Group Corporation Limited (“Shenhua Group”) and revenue from it in the fiscal year 2022 accounted for approximately 10% of our revenue. For fiscal year 2023, revenue from Shenhua accounted for 8% of our revenue as competition became fierce. We expect it to continue to rise in the future. Any termination of our business relationships with CNPC, Sinopec, Shenhua Group or any other major client would materially harm our operations.

Because we derive such a high percentage of our revenue from CNPC and a few new clients, our revenue has been subject to high seasonality. We recognize revenue when it is realized and earned. Revenue is recognized based on the following five steps: (i) identify the contract(s) with the customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations; (v) recognize revenue when (or as) each performance obligation is satisfied. Because these matters depend on reaching agreements with these clients, revenue recognition occurs, to a large extent, on their schedule. Accordingly, revenue recognized in the first quarter is usually the smallest in proportion to that for the whole year, due to our clients’ budgeting and planning schedules. If these clients were to change their budgeting or planning schedule our high and low quarters could also shift. This seasonality limits our ability to make accurate long-term predictions about our performance and makes it difficult to compare our revenue across quarters.

Changes in environmental and regulatory factors may harm our business.

The oil drilling industry in China to date has not been subject to the type and scope of regulation seen in Europe and the United States. However, the Chinese government may implement new legislation or regulations or may enforce existing laws more stringently. Either of these scenarios may have a significant impact on our customers’ mining and extraction operations and may require us or our customers to significantly change operations or to incur substantial costs. We believe that the Domestic Companies’ and our operations in China are in compliance with China’s applicable legal and regulatory requirements. However, there can be no assurance that China’s central or local governments will not impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures.

Petroleum reserve degradation and depletion may reduce our customers’ and our profitability.

Our profitability depends substantially on our ability to help our customers exploit their oil reserves at competitive costs. Replacement reserves may not be available to our customers when required or, if available, may not be drilled at costs comparable to those characteristics of the depleting oilfield. The Domestic Companies’ and our technology may not enable our customers to accurately assess the geological characteristics of any new reserves, which may adversely affect their decision to use the Domestic Companies’ and our products in the future.

13

We are heavily dependent upon the services of experienced personnel who possess skills that are valuable in our industry, and we may have to actively compete for their services.

Our company is much smaller than our main foreign competitors, including Schlumberger Limited, Honeywell International, Emerson Process Management and Rockwell Automation, and we compete in large part on the basis of the quality of services we are able to provide our clients. As a result, we are heavily dependent upon our ability to attract, retain and motivate skilled personnel to serve our clients. Many of our personnel possess skills that would be valuable to all companies engaged in the integrated automation services industry. Consequently, we expect that we will have to actively compete for these employees. Some of our competitors may be able to pay our employees more than we are able to pay to retain them. Our ability to profitably operate is substantially dependent upon our ability to locate, hire, train and retain our personnel. There can be no assurance that we will be able to retain our current personnel, or that we will be able to attract or assimilate other personnel in the future. If we are unable to effectively obtain and maintain skilled personnel, the development and quality of our technological products and the effectiveness of installation and training could be materially impaired.

We are substantially dependent upon our key personnel, particularly Mr. Yin Shenping, our Chief Executive Officer, Mr. Chen Guangqiang, our Chief Technology Officer and Ms. Liu Jia, our Chief Financial Officer.

Our performance is substantially dependent on the performance of our executive officers and key employees. In particular, we rely on the services of:

| ● | Mr. Yin Shenping, Chief Executive Officer; |

| ● | Mr. Chen Guangqiang, Chief Technology Officer; and |

| ● | Ms. Liu Jia, Chief Financial Officer. |

Each of these individuals would be difficult to replace. We do not have in place “key person” life insurance policies on any of our employees. The loss of the services of any of our executive officers or other key employees could substantially impair our ability to successfully development new systems and develop new programs and enhancements. In addition, we would need to spend considerable time and other resources to seek suitable replacements, which might detract from our efforts to develop our business.

Our business is capital intensive and our growth strategy may require additional capital, which may not be available on favorable terms or at all.

We may require additional cash resources due to changed business conditions, implementation of our growth strategy or potential investments or acquisitions we may pursue. To meet our capital needs, we may sell additional equity or debt securities or obtain additional credit facilities. The sale of additional equity securities or other securities convertible into such equity securities could result in dilution of your holdings. The incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. Financing may not be available in amounts or on terms acceptable to us, if at all. Any failure by us to raise additional funds on terms favorable to us, or at all, could limit our ability to expand our business operations and could harm our overall business prospects.

We do not intend to pay dividends in the foreseeable future and there are certain restrictions on the payment of dividend under PRC laws.

We have not previously paid any cash dividends, and we do not anticipate paying any dividends on our Class A Ordinary Shares. As we intend to remain in a growth mode, we intend to reinvest any profits in the foreseeable future to grow the business. We cannot assure you that our operations will continue to result in sufficient revenue to enable us to operate at profitable levels or to generate positive cash flows. Furthermore, there is no assurance our board of directors will declare dividends even if we are profitable. Dividend policy is subject to the discretion of our board of directors and will depend on, among other things, our earnings, financial condition, capital requirements and other factors. If we determine to pay dividends on any of our Class A Ordinary Shares in the future, we will be dependent, in large part, on receipt of funds from the Domestic Companies.

14

We are a holding company with no operations of our own and substantially all of our operations are conducted through Nanjing Recon and BHD, hereafter referred to as the Domestic Companies, which are established as variable interest entities (“VIEs”) under the laws of the PRC. Our ability to pay dividends is dependent upon dividends and other distributions from the Domestic Companies. Chinese legal restrictions permit payment of dividends to us by the Domestic Companies only out of their respective accumulated net profits, if any, determined in accordance with Chinese accounting standards and regulations. Under Chinese law, the Domestic Companies are required to set aside a portion (at least 10%) of their after-tax net income (after discharging all cumulated loss), if any, each year for compulsory statutory reserve until the amount of the reserve reaches 50% of the Domestic Companies’ registered capital. These funds may be distributed to shareholders at the time of each Domestic Company’s wind-up. Payments of dividends by Domestic Companies to us are also subject to restrictions including primarily the restriction that foreign invested enterprises may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents. There are no such similar foreign exchange restrictions in the Cayman Islands.

Our certificates, permits, and license are subject to governmental control and renewal, and the failure to obtain renewal would cause all or part of our operations to be suspended and may have a material adverse effect on our financial condition.

We are subject to various PRC laws and regulations pertaining to automation services for the petroleum extraction industry. We have obtained certain certificates, permits, and licenses required for the operation of an automation services provider for the petroleum extraction industry and the manufacturing and distribution of software and hardware products in the PRC.

During the application or renewal process for our licenses and permits, we will be evaluated and re-evaluated by the appropriate governmental authorities and must comply with the prevailing standards and regulations, which may change from time to time. In the event that we are not able to obtain or renew the certificates, permits and licenses, all or part of our operations may be suspended by the government, which would have a material adverse effect on our business and financial condition. Furthermore, if escalating compliance costs associated with governmental standards and regulations restrict or prohibit any part of our operations, it may adversely affect our results of operations and profitability.

Risks Related to Our Corporate Structure

Our contractual arrangements with the Domestic Companies and their respective shareholders may not be as effective in providing control over these entities as direct ownership.

We are a holding company incorporated in the Cayman Islands. As a holding company with no material operations of our own, we conduct a substantial majority of our operations through our Wholly Foreign Owned Enterprise (“WFOE”) and the VIEs and their subsidiaries in China providing certain technical and consultation services. A WFOE is a limited liability company based in the People’s Republic of China but wholly owned by foreign investors. In our instance, Recon Hengda Technology (Beijing) Co., Ltd (“Recon-BJ”) is a WFOE wholly owned by Recon Investment Ltd. (“Recon-IN”), a Hong Kong limited company, which in turn is wholly owned by us. We consolidated the financial results of BHD and Nanjing Recon into our financial statements based on the VIE agreements entered into on April 1, 2019. Most, if not all, of our revenue derives from operations of the VIEs and their subsidiaries. Our Ordinary Shares offered in this offering are shares of our offshore holding company instead of shares of the VIEs or our PRC subsidiary. These Contractual Arrangements may not be as effective in providing us with control over the VIEs as direct ownership. For example, BHD could fail to take actions required for our business or fail to pay dividends to Recon-BJ despite its contractual obligation to do so. If the Domestic Companies fail to perform under their agreements with us, we may have to rely on legal remedies under PRC law, which may not be effective. In addition, these agreements have not been tested in a court of law.

If we had direct ownership of the VIEs, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of the VIEs, which in turn could effect changes, subject to any applicable fiduciary obligations, at the management and operational level. However, under the current Contractual Arrangements, we rely on the performance by the VIEs and their shareholders of their obligations under the contracts to exercise control over the VIEs. We cannot assure you that any of the Domestic Companies’ shareholders would always act in our best interests. Such risks exist throughout the period in which we intend to operate our business through the Contractual Arrangements with the VIEs. If any dispute relating to these contracts remains unresolved, we will have to enforce our rights under these contracts through the operations of PRC law and arbitration, litigation and other legal proceedings and therefore will be subject to uncertainties in the PRC legal system. Therefore, our Contractual Arrangements with the VIEs may not be as effective in ensuring our control over the relevant portion of our business operations as direct ownership would be.

15

We have no equity ownership interest in the Domestic Companies and rely on contractual arrangements to control and operate such businesses. These contractual arrangements may not be as effective in providing control over the Domestic Companies as direct ownership.

We conduct our business through BHD, Nanjing Recon, FGS and their respective subsidiaries by means of Contractual Arrangements. If the PRC courts or administrative authorities determine that these contractual arrangements do not comply with applicable regulations, we could be subject to severe penalties and our business could be adversely affected. In addition, changes in such PRC laws and regulations may materially and adversely affect our business.

There are uncertainties regarding the interpretation and application of PRC laws, rules and regulations, including the laws, rules and regulations governing the validity and enforcement of the Contractual Arrangements between the Wholly Foreign Owned Enterprise (“WFOE”). A WFOE is a limited liability company based in the People’s Republic of China but wholly owned by foreign investors. In our instance, Recon Hengda Technology (Beijing) Co., Ltd (“Recon-BJ”) is a WFOE wholly owned by Recon Investment Ltd. (“Recon-IN”), a Hong Kong limited company, which in turn is wholly owned by us. Recon-BJ and Nanjing Recon, BHD and their respective subsidiaries. We have been advised by our PRC counsel, JingTian & GongCheng LLP, based on their understanding of the current PRC laws, rules and regulations, that (i) the structure for operating our business in China (including our corporate structure and Contractual Arrangements with the Recon-BJ, Nanjing Recon, BHD and their respective subsidiaries) will not result in any violation of PRC laws or regulations currently in effect; and (ii) the Contractual Arrangements among the Recon-BJ and Nanjing Recon, BHD and their respective subsidiaries governed by PRC law are valid, binding and enforceable, and will not result in any violation of PRC laws or regulations currently in effect. However, there are substantial uncertainties regarding the interpretation and application of current or future PRC laws and regulations concerning foreign investment in the PRC, and their application to and effect on the legality, binding effect and enforceability of the contractual arrangements. In particular, we cannot rule out the possibility that PRC regulatory authorities, courts or arbitral tribunals may in the future adopt a different or contrary interpretation or take a view that is inconsistent with the opinion of our PRC legal counsel. Therefore, the Contractual Arrangements may be determined by PRC authorities to be inconsistent with the laws and regulations of the PRC, including those related to foreign investment in certain industries. Therefore, the relevant Chinese regulatory authorities could disallow this structure and hinder our ability to exert contractual control over the Domestic Companies, which would likely result in a material change in operations and/or value of the Company’s ordinary shares, including that it could cause the value of such securities to significantly decline or become worthless.

If any of the Domestic Companies or their ownership structure or the Contractual Arrangements are determined to be in violation of any existing or future PRC laws, rules or regulations, or any of our PRC entities fail to obtain or maintain any of the required governmental permits or approvals, the relevant PRC regulatory authorities would have broad discretion in dealing with such violations, including:

| ● | revoking the business and operating licenses; |

| ● | discontinuing or restricting the operations; |

| ● | imposing conditions or requirements with which the PRC entities may not be able to comply; |

| ● | requiring us and our PRC entities to restructure the relevant ownership structure or operations, including termination of the contractual agreements with the VIE and deregistering the equity pledge of the VIE, which in turn would affect our ability to consolidate, derive economic interests from, or exert effective control the VIE; |

| ● | restricting or prohibiting our use of the proceeds from this offering to finance our business and operations in China, and taking other regulatory or enforcement actions that could be harmful to our business; or |

| ● | imposing fines or confiscating the income from our PRC subsidiaries or the VIE. |

The imposition of any of these penalties would severely disrupt our ability to conduct business and have a material adverse effect on our financial condition, results of operations and prospects.

16

Our majority stake in Future Gas Station (Beijing), which now consists of a large operating segment of our business, exposes us to risks related to consumer energy consumption and online payment technologies.

As the energy consumption market opened to private and foreign companies, and as the online payment technology continually developed, we began investing in the downstream oil industry. Over the years, we developed a close relationship with Future Gas Station (Beijing) (also referred to as “FGS”) and we now own 51% of the equity of FGS. As such, our majority stake in FGS presents both a substantial investment in the downstream of the oil industry and comprises a large part of our operations. As such, our controlling interest in FGS represents both a significant investment in the downstream of the oil industry and a large part of our business. The development of FGS depends on its cooperation with gas stations. At present, most of the gas stations in China are owned by the sales companies of PetroChina and Sinopec, so FGS's business expansion is largely dependent on the development of electronic payment systems and online settlement systems of these major oil companies and their cooperation decisions. As these major oil companies gradually increase their efforts in research and development and deployment of self-built systems, their willingness to cooperate with third-party service and operations support companies such as FGS will decrease or the depth of their cooperation will decrease, resulting in FGS's growth potential being limited and unable to meet our expectations at the time we acquired FGS. We may suffer a significant loss on our substantial investment in FGS.

Regulations relating to offshore investment activities by PRC residents may limit our ability to acquire PRC companies and could adversely affect our business.

In July 2014, SAFE promulgated the Circular on Issues Concerning Foreign Exchange Administration Over the Overseas Investment and Financing and Roundtrip Investment by Domestic Residents Via Special Purpose Vehicles, or Circular 37, which replaced Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Corporate Financing and Roundtrip Investment through Offshore Special Purpose Vehicles, or Circular 75. Circular 37 requires PRC residents to register with local branches of SAFE in connection with their direct establishment or indirect control of an offshore entity, referred to in Circular 37 as a “special purpose vehicle” for the purpose of holding domestic or offshore assets or interests. Circular 37 further requires amendment to a PRC resident’s registration in the event of any significant changes with respect to the special purpose vehicle, such as an increase or decrease in the capital contributed by PRC individuals, share transfer or exchange, merger, division or other material event. Under these regulations, PRC residents’ failure to comply with specified registration procedures may result in restrictions being imposed on the foreign exchange activities of the relevant PRC entity, including the payment of dividends and other distributions to its offshore parent, as well as restrictions on capital inflows from the offshore entity to the PRC entity, including restrictions on its ability to contribute additional capital to its PRC subsidiaries. Further, failure to comply with the SAFE registration requirements could result in penalties under PRC law for evasion of foreign exchange regulations.

As Circular 37 is relatively new, it is unclear how these regulations will be interpreted and implemented. In addition, different local SAFE branches may have different views and procedures as to the interpretation and implementation of the SAFE regulations, and it may be difficult for our ultimate shareholders or beneficial owners who are PRC residents to provide sufficient supporting documents required by the SAFE or to complete the required registration with the SAFE in a timely manner, or at all. Any failure by any of our shareholders who is a PRC resident, or is controlled by a PRC resident, to comply with relevant requirements under these regulations could subject us to fines or sanctions imposed by the PRC government, including restrictions on Recon-BJ’s ability to pay dividends or make distributions to us and on our ability to increase our investment in the Recon-BJ.

Under Circular 37, if a non-listed special purpose vehicle uses its own equity or share option to grant equity incentive awards to directors, supervisors, members of senior management or employees directly employed by a domestic enterprise that is directly or indirectly controlled by such special purpose vehicle, or with which such employee has established an employment relationship, any of such directors, supervisors, members of senior management or employees who is a PRC resident should, prior to exercising their rights, file an application with the SAFE for foreign exchange registration with respect to such special purpose vehicle. However, in practice, different local SAFE branches may have different views and procedures as to the interpretation and implementation of the SAFE regulations and, since Circular 37 was the first regulation to regulate the foreign exchange registration of a non-listed special purpose vehicle’s equity incentive granted to PRC residents, there remains uncertainty with respect to its implementation.

17

Our contractual arrangements with the Domestic Companies may result in adverse tax consequences to us.

As a result of our corporate structure and contractual arrangements between Recon-BJ and the Domestic Companies, we are effectively subject to several PRC taxes on both revenue generated by Recon-BJ’s operations in China and revenue derived from Recon-BJ’s contractual arrangements with the Domestic Companies. Moreover, we would be subject to adverse tax consequences if the PRC tax authorities were to determine that the contracts between Recon-BJ and the Domestic Companies were not on an arm’s length basis and therefore constitute a favorable transfer pricing. As a result, the PRC tax authorities could request that we adjust our taxable income upward for PRC tax purposes. If the PRC tax authorities took such action, such authorities would be able to establish in its sole discretion the amount of tax payable by Recon-BJ, so we cannot predict the effect of such action on our company other than the likely effect that our profits would decrease. Such a pricing adjustment could adversely affect us by:

| ● | increasing our tax expenses, which could subject Recon-BJ to late payment fees and other penalties for under-payment of taxes; and/or |

| ● | resulting in Recon-BJ’s loss of preferential tax treatment. |

The shareholders of the VIEs may have actual or potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.

The shareholders of the VIEs may have actual or potential conflicts of interest with us. The shareholders may refuse to sign or breach, or cause the VIEs to breach, or refuse to renew, the existing contractual arrangements we have with them and the VIEs, which would have a material and adverse effect on our ability to effectively control the VIEs and receive economic benefits from them. For example, the shareholders may be able to cause our agreements with the VIEs to be performed in a manner adverse to us by, among other things, failing to remit payments due under the contractual arrangements to us on a timely basis. We cannot assure you that when conflicts of interest arise the shareholder will act in the best interests of our company or such conflicts will be resolved in our favor. Currently, we do not have any arrangements to address potential conflicts of interest between the shareholders and our company. If we cannot resolve any conflict of interest or dispute between us and the shareholders, we would have to rely on legal proceedings, which could result in disruption of our business and subject us to substantial uncertainty as to the outcome of any such legal proceedings.

The principal shareholders of the Domestic Companies have potential conflicts of interest with us, which may adversely affect our business.

Yin Shenping, our Chief Executive Officer, and Chen Guangqiang, our Chief Technology Officer, are significant shareholders in our company. They are also the principal shareholders of each of the Domestic Companies and collectively control the Domestic Companies. Conflicts of interests between their duties to our company and the respective Domestic Companies may arise. For example, Mr. Yin and Mr. Chen could cause a Domestic Company to fail to take actions that are in the best interests of our Company or to fail to pay dividends to Recon-BJ despite its contractual obligation to do so if making such payment would harm the Domestic Company.

As Mr. Yin and Mr. Chen are also directors and executive officers of our company, they have duties of loyalty and care to us under Cayman Islands law when there are any potential conflicts of interests between our company and the Domestic Companies. Each of Mr. Yin and Mr. Chen has executed an irrevocable power of attorney to appoint the individual designated by us to be his attorney-in-fact to vote on his behalf on all matters related to the Domestic Companies requiring shareholder approval. We cannot assure you, however, that if conflicts of interest arise, they will act completely in our interests or that conflicts of interests will be resolved in our favor. In addition, Mr. Yin and Mr. Chen could violate their respective employment agreements with us or their legal duties by diverting business opportunities from us to others. If we cannot resolve any conflicts of interest between us and Mr. Yin and Mr. Chen, as applicable, we would have to rely on legal proceedings, which could result in the disruption of our business.

18

Any deterioration of the relationship between Recon-BJ and the Domestic Companies could materially and adversely affect the overall business operation of our company.

Our relationship with the Domestic Companies is governed by their agreements with Recon-BJ, which are intended to provide us, through our indirect ownership of Recon-BJ, with effective control over the business operations of the Domestic Companies. However, these agreements may not be effective in providing control over the applications for and maintenance of the licenses required for our business operations. The Domestic Companies could violate these agreements, go bankrupt, suffer from difficulties in its business or otherwise become unable to perform its obligations under these agreements and, as a result, our operations, reputation, business and stock price could be severely harmed.

If Recon-BJ exercises its purchase option of the Domestic Companies’ equity pursuant to the Exclusive Equity Interest Purchase Agreement, payment of the purchase price could materially and adversely affect our financial position.

Under the Exclusive Equity Interest Purchase Agreement, Recon-BJ holds an option to purchase all or a portion of the equity of the Domestic Companies at a price, based on the capital paid in by the Domestic Company shareholders. If applicable PRC laws and regulations require an appraisal of the equity interest or provide other restriction on the purchase price, the purchase price shall be the lowest price permitted under the applicable PRC laws and regulations. As the Domestic Companies are already contractually controlled affiliates to our company, Recon-BJ’s purchase of the Domestic Companies’ equity would not bring immediate benefits to our company and the exercise of the option and payment of the purchase prices could adversely affect our financial position and available working capital.

Our dual class structure may be dilutive to the voting power of Class A Ordinary Shareholders.

On April 5, 2021, at the 2021 annual meeting, to implement a dual class structure, our shareholders approved (i) a special resolution that the authorized share capital of the Company be amended from US$1,850,000, divided into 20,000,000 Class B Ordinary Shares of a nominal or par value of US$0.0925 each, to US$15,725,000, divided into 150,000,000 Class A Ordinary Shares of a nominal or par value of US$0.0925 each and 20,000,000 Class B Ordinary Shares of a nominal or par value of US$0.0925 each, and (ii) a special resolution that the Third Amended and Restated Memorandum and Articles of Association of the Company to substitute the Second Amended and Restated Memorandum and Articles of Association. The dual class structure of our ordinary shares has the effect of concentrating voting control with holders of Class B Ordinary Shares. Our Class B Ordinary Shares have stronger voting power than our Class A Ordinary Shares and certain existing shareholders have substantial influence over our Company and their interests may not be aligned with the interests of our other shareholders.

Our classified board structure may prevent a change in our control.

Our board of directors is divided into three classes of directors. The current terms of the directors expire in 2024, 2025 and 2026. Directors of each class are chosen for three-year terms upon the expiration of their current terms, and each year one class of directors is elected by the shareholders. The staggered terms of our directors may reduce the possibility of a tender offer or an attempt at a change in control, even though a tender offer or change in control might be in the best interest of our shareholders.

19

Shareholder rights under Cayman Islands law may differ materially from shareholder rights in the United States, which could adversely affect the ability of us and our shareholders to protect our and their interests.

Our corporate affairs are governed by our Memorandum and Articles of Association, by the Companies Law (2013 Revision) and the common law of the Cayman Islands. The rights of shareholders to take action against the directors, actions by minority shareholders, and the fiduciary responsibilities of our directors to us under Cayman Islands law are to a large extent governed by the common law of the Cayman Islands. The common law in the Cayman Islands is derived in part from comparatively limited judicial precedent in the Cayman Islands as well as from English common law, the decisions of whose courts are of persuasive authority but are not binding on a court in the Cayman Islands. In particular, the Cayman Islands has a less developed body of securities laws as compared to the United States, and some states, such as Delaware, have more fully developed and judicially interpreted bodies of corporate laws. Moreover, our company could be involved in a corporate combination in which dissenting shareholders would have no rights comparable to appraisal rights which would otherwise ordinarily be available to dissenting shareholders of United States corporations. However, Cayman Islands statutory law does provide a mechanism for a dissenting shareholder in a merger or consolidation to apply to the Grand Court for a determination of the fair value of the dissenter’s shares if it is not possible for the dissenter and the Company to agree a fair price within the time limits prescribed. Also, our Cayman Islands counsel is not aware of a significant number of reported derivative actions having been brought in Cayman Islands courts. Class actions are not recognized in the Cayman Islands, but groups of shareholders with identical interests may bring representative proceedings which are similar. Such actions are ordinarily available in respect of United States corporations in U.S. courts. Finally, Cayman Islands companies may not have standing to initiate shareholder derivative action before the federal courts of the United States. As a result, our public shareholders may face different considerations in protecting their interests in actions against the management, directors or our controlling shareholders than would shareholders of a corporation incorporated in a jurisdiction in the United States, and our ability to protect our interests may be limited if we are harmed in a manner that would otherwise enable us to sue in a United States federal court.

As we are a Cayman Islands company and most of our assets are outside the United States, it will be extremely difficult to acquire jurisdiction and enforce liabilities against us and our officers, directors and assets based in China.