UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number:

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Tel: (

Fax: (86-10)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each Class |

| Trading Symbol |

| Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period (September 30, 2023) covered by the annual report: there were issued and outstanding 6,334,998 ordinary shares as of September 30, 2023, and

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company.

☐ Large accelerated filer | ☐ Accelerated filer | ☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by a check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standard as Issued by the | Other ☐ | |

| International Accounting Standards Board ☐ |

|

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐Item 17 ☐Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐Yes

ORIGIN AGRITECH LIMITED

TABLE OF CONTENTS

1 | |||

13 | |||

13 | |||

13 | |||

37 | |||

49 | |||

50 | |||

59 | |||

67 | |||

67 | |||

68 | |||

68 | |||

77 | |||

77 | |||

78 | |||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 78 | ||

78 | |||

79 | |||

79 | |||

79 | |||

80 | |||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 80 | ||

80 | |||

80 | |||

81 | |||

81 | |||

82 |

i

INTRODUCTION

Except where the context otherwise requires and for purposes of this Annual Report only:

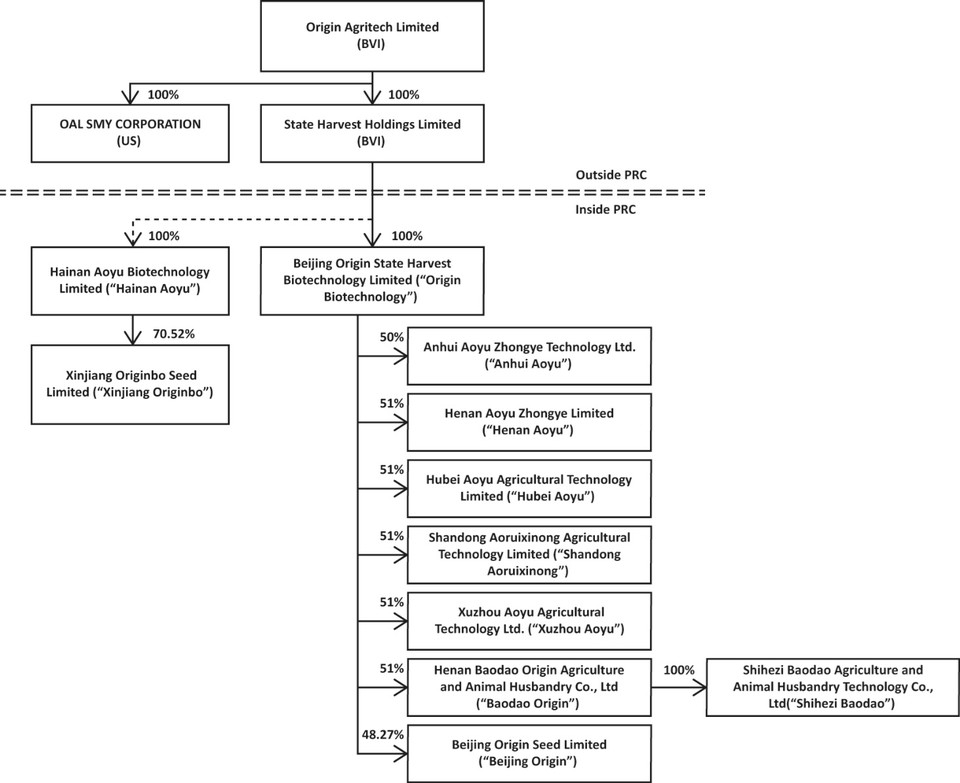

| ● | “we,” “us,” “our company,” “our,” the “Company” and “Origin” refer to Origin Agritech Limited and an intermediate holding company, State Harvest Holdings Limited, both companies formed in the British Virgin Islands and the following, which are collectively described in this Annual Report as “our PRC Operating Companies.” |

The PRC Operating Companies are:

1.State Harvest Holdings Limited (“State Harvest”), a company formed in British Virgin Islands, which is a 100% equity owned company of Origin, as a holding company for our other direct and indirect subsidiaries in China, including:

2.Beijing Origin State Harvest Biotechnology Limited (“Origin Biotechnology”), a company formed in China, collectively for itself and its China formed subsidiaries listed below, all of which are, directly or indirectly, wholly or partly equity owned by State Harvest.

| (i) | Hubei Aoyu Agricultural Technology Limited, (“Hubei Aoyu”) in Hubei province, |

| (ii) | Anhui Aoyu Zhongye Technology Ltd. (“Anhui Aoyu”) in Anhui province, |

| (iii) | Xuzhou Aoyu Agricultural Technology Ltd. (“Xuzhou Aoyu”) in Jiangsu province, |

| (iv) | Henan Aoyu Zhongye Limited (“Henan Aoyu”) in Henan province, |

| (v) | Shandong Aoruixinong Agricultural Technology Limited (Shandong Aoruixinong), |

| (vi) | Hainan Aoyu Biotechnology Limited (“Hainan Aoyu”) in Hainan province and its subsidiary Xinjiang Originbo Seed Limited ("Xinjiang Originbo"), |

| (vii) | Henan Baodao Origin Agriculture and Animal Husbandry Co., Ltd (“Baodao Origin”) in Henan province, and its subsidiaries Shihezi Baodao Agriculture and Animal Husbandry Technology Co., Ltd (“Shihezi Baodao”) in Xinjiang, and |

3.OAL SMY Limited, a company formed in New Jersey, United States, is a 100% equity owned company of Origin.

| ● | “last year,” “fiscal year 2023,” “the year ended September 30, 2023” and “the fiscal year ended September 30, 2023” refer to the twelve months ended September 30, 2023, which is the period covered by this Annual Report; |

| ● | all references to “Renminbi,” “RMB” or “yuan” are to the legal currency of China; all references to “U.S. dollars,” “dollars,” “$” or “US$” are to the legal currency of the United States. Any discrepancies in any table between totals and sums of the amounts listed are due to rounding. The translation of Renminbi amounts into United States dollar amounts has been made for the convenience of the reader. Such translation amounts should not be construed as representations that the Renminbi amounts could be readily converted into United States dollar amounts at that rate or any other rate; |

| ● | “China” or “PRC” refers to the mainland of People’s Republic of China; |

| ● | “Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China; and |

| ● | “shares” and “ordinary shares” refer to our ordinary shares, “preferred shares” refers to our preferred shares. |

1

Corporate Structure

The public company, Origin, in which investors hold shares, is a holding company incorporated in the British Virgin Islands. All of our business activities currently take place in China. Part of our operations are conducted in China through a variable interest enterprise, or VIE. The portion of the business that is a VIE is Hainan Aoyu and its subsidiary Xinjiang Origin. This portion of the business is the seed development operations of Origin. The balance of our operations are conducted through wholly and partly equity owned operations, in or under Origin Biotechnology, which in turn is 100% equity owned by State Harvest.

Due to PRC legal restrictions on foreign ownership in certain food development and production related businesses, such as our general seed development operations, we do not have full equity ownership of those parts of our business. Instead, we rely on contractual arrangements among our PRC subsidiaries and their nominee shareholders to control the portion of the business operations not owned by means of the VIE arrangements. These VIE contractual agreements enable us, we believe, to (i) exercise contractual control over the VIE, (ii) receive the economic benefits of the VIE, and (iii) have an exclusive call option to purchase all or part of the equity interests in the VIE when and to the extent permitted by PRC law. As a result of these contractual arrangements, we consolidate the financial results of the VIE in our financial statements under U.S. GAAP. Investors in our ordinary shares are purchasing an equity interest in a British Virgin Islands holding company, which in turn has equity interests in some of its subsidiaries in China and a contractual arrangement with owners of the VIEs in another entity.

2

We and the VIE face various legal and operational risks and uncertainties related to doing business in China. Origin and the VIE are subject to complex and evolving PRC laws and regulations as a result. For example, we and the VIE face risks associated with regulatory approvals of offshore offerings, the use of variable interest entities, anti-monopoly regulatory actions, cybersecurity and data privacy, which may impact our ability to conduct certain businesses, accept foreign investments, or list on a United States or other foreign exchange. These risks could result in a material adverse change in our operations and the value of the ordinary shares of the parent holding company, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. Additionally, these concerns may limit the ability to maintain the listing of our ordinary shares on a securities exchange in the United States and in other capital markets.

Our corporate structure is subject to risks associated with the contractual arrangements with the VIE and the parties to those contractual arrangements. Investors in the BVI holding company may never have a direct ownership interest in the part of the business that is conducted by the VIE. If the PRC government finds that the agreements that establish the structure for operating our business in China do not comply with PRC laws and regulations, or if these regulations or the interpretation of existing regulations change or are interpreted differently in the future, we and the VIE could be subject to severe penalties or be forced to relinquish our interests in those parts of the operations. This would result in the VIE being deconsolidated for financial statement purposes. The seed development assets, including certain licenses to conduct that part of the business in China, are held by the VIE. A part of our revenues are generated by the VIE. An event that results in the deconsolidation of the VIE would have a material effect on our operations and result in the value of the ordinary shares being diminished or even becoming worthless. Our holding company, our PRC subsidiaries and the VIE, and investors of our ordinary shares face uncertainty about potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIE and, consequently, significantly affect the financial performance of the VIE and our company as a whole.

Because of our operations in the development of genetically modified seeds and involvement in the production of seeds as well as for other reasons, the PRC government may intervene or act to influence our operations, or may exert more control over offerings conducted overseas and/or foreign investment in us. Such intervention or influence over the manner in which we operate could result in a material change in our operations or the value of our ordinary shares. Any actions by the PRC government to exert more oversight and control over offerings that are conducted overseas or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities and our other outstanding securities to significantly decline or be worthless.

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the Opinions on Severe and Lawful Crackdown on Illegal Securities Activities. These opinions emphasized the need to strengthen the administration over illegal securities activities and the supervision on overseas listings by China-based companies. These opinions proposed to take effective measures, such as promoting the construction of relevant regulatory systems, to deal with the risks and incidents facing China-based overseas-listed companies and the demand for cybersecurity and data privacy protection. These opinions and any related implementation rules may subject us to additional compliance requirement in the future.

With the trend of strengthening anti-monopoly supervision around the world, the PRC government has issued a series of anti-monopoly laws and regulations since 2021, paying more attention to corporate compliance. On February 7, 2021, the Anti-monopoly Commission of the State Council of the PRC promulgated the Guidelines for Anti-monopoly in the field of Platform Economy. On November 15, 2021, the State Administration for Market Regulation of the PRC promulgated the Guidelines for the Overseas Anti-monopoly Compliance of Enterprises. We believe that these regulations currently have little impact on us, but we cannot guarantee that regulators will agree with us or that these regulations will not affect our business operations in the future.

Cybersecurity and data privacy and security issues are subject to increasing legislative and regulatory focus in China. The State Council of the PRC promulgated the Security Protection Regulations for Critical Information Infrastructure (the “CII Regulation”) on July 30, 2021, which took effect on September 1, 2021. This regulation requires, among others, certain competent authorities to identify critical information infrastructures. The Cybersecurity Administration of China (the “CAC”) and a number of other departments under the State Council promulgated the Measures for Cybersecurity Review on December 28, 2021, which became effective on February 15, 2022. According to this regulation, critical information infrastructure operators purchasing network products and services and network platform operators carrying out data processing activities, which affect or may affect national security, are required to conduct cybersecurity review. We believe that these regulations have little impact on us, because we are neither a critical information infrastructure operator nor a network platform operator within the meanings of these regulation. However, we cannot guarantee that the regulators will agree with us.

3

On September 1, 2021, the PRC Data Security Law became effective, which imposes data security and privacy obligations on entities and individuals conducting data-related activities, and introduces a data classification and hierarchical protection system. In addition, the Standing Committee of the PRC National People’s Congress promulgated the Personal Information Protection Law (the “PIPL”) on August 20, 2021, which took effect on November 1, 2021. The PIPL further emphasizes processors’ obligations and responsibilities for personal information protection and sets out the basic rules for processing personal information and the rules for cross-border transfer of personal information. On July 7, 2022, the CAC promulgated the Security Assessment Measures for Outbound Data Transfers (the “Assessment Measures”) which became effective on September 1, 2022, subject to a six month implementation grace period, along with the guidelines. According to the Assessment measures, a data processor shall declare security assessment for its outbound data transfer to the CAC through the local cyberspace administration at the provincial level under any of the following circumstances: (a) where a data processor provides critical data abroad; (b) where a critical information infrastructure operator or a data processor processing the personal information of more than one million individuals provides personal information abroad; (c) where a data processor has provided personal information of 100,000 individuals or sensitive personal information of 10,000 individuals in total abroad since January 1 of the previous year; and (d) other circumstances prescribed by the CAC for which declaration for security assessment for outbound data transfers is required. We have the opportunity to contact, obtain or be exposed to personal information of our subscribers and their close relatives. We may be required to declare security assessment once we fall under any of the aforementioned circumstances and our business operations may be restricted according to the regulations above mentioned.

On December 24, 2021, the China Securities Regulatory Commission (“CSRC”) published the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments), and Administrative Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments), or, collectively, the Draft Overseas Listing Regulations, which set out the new regulatory requirements and filing procedures for Chinese companies seeking direct or indirect listing in overseas markets. The Draft Overseas Listing Regulations, among others, stipulate that Chinese companies that seek to offer and list securities in overseas markets must fulfill the filing procedures with and report relevant information to the CSRC, and that an initial filing must be submitted within three working days after the application for an initial public offering in an overseas market is submitted, and a second filing must be submitted within three working days after the listing is completed. Moreover, an overseas offering and listing is prohibited under circumstances if (i) it is prohibited by PRC laws, (ii) it may constitute a threat to or endanger national security as reviewed and determined by competent PRC authorities, (iii) it has material ownership disputes over equity, major assets, and core technology, (iv) in the past three years, the Chinese operating entities and their controlling shareholders and actual controllers have committed relevant prescribed criminal offenses or are currently under investigations for suspicion of criminal offenses or major violations, (v) the directors, supervisors, or senior executives have been subject to administrative punishment for severe violations, or are currently under investigations for suspicion of criminal offenses or major violations, or (vi) it has other circumstances as prescribed by the State Council. The Draft Overseas Listing Regulations, among others, stipulate that when determining whether an offering and listing shall be deemed as “an indirect overseas offering and listing by a Chinese company”, the principle of “substance over form” will be followed, and if the issuer meets the following conditions, its offering and listing will be determined as an “indirect overseas offering and listing by a Chinese company” and is therefore subject to the filing requirement: (i) the revenues, profits, total assets or net assets of the Chinese operating entities in the most recent financial year accounts for more than 50% of the corresponding data in the issuer’s audited consolidated financial statements for the same period; and (ii) the majority of senior management in charge of business operation are Chinese citizens or have domicile in PRC, and its principal place of business is located in PRC or main business activities are conducted in PRC. We cannot predict the impact of the Draft Overseas Listing Regulations on us at this stage.

Since these regulatory actions are relatively new, it is uncertain how soon legislative or administrative regulation-making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, or the potential impact such modified or new laws and regulations will have on our daily business operation, or our ability to accept foreign investments and listing on a U.S. or other foreign exchange. PRC laws and their interpretations and enforcement continue to develop and are subject to change, and the PRC government may adopt other rules and restrictions in the future.

4

Our financial statements contained in this annual report have been audited by B F Borgers CPA PC, an independent registered public accounting firm that is headquartered in Lakewood, Colorado. It is a firm registered with the U.S. Public Company Accounting Oversight Board (the “PCAOB”), and is required by the laws of the U.S. to undergo regular inspections by the PCAOB to assess its compliance with the laws of the U.S. and professional standards. Therefore, we believe, Article 177 of the PRC Securities Law, which became effective in March 2020, should not apply to us. That law provides that no overseas securities regulator is allowed to directly conduct investigation or evidence collection activities within the territory of the PRC. Accordingly, without the consent of competent PRC securities regulators and relevant authorities, no organization or individual may provide the documents and materials relating to securities business activities to overseas parties. The United States Holding Foreign Companies Accountable Act, or the HFCA Act, was enacted on December 18, 2020. The HFCA Act states that if the SEC determines that a company has filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit such ordinary shares from being traded on a national securities exchange or in the over-the-counter trading market in the U.S. The SEC has adopted rules to implement the HFCA Act and, pursuant to the HFCA Act, the PCAOB has issued a report notifying the Securities and Exchange Commission of its determination that it is currently unable to inspect accounting firms headquartered in mainland China or Hong Kong. Further, the United States Senate has passed the Accelerating Holding Foreign Companies Accountable Act, or the AHFCA Act, which, if enacted, would decrease the number of “non-inspection years” from three years to two years, and thus, would reduce the time before securities may be prohibited from trading or be delisted. Currently, we do not believe that we are subject to the various laws mentioned above, and we do not believe our ordinary shares will be delisted from NASDAQ because of these laws.

On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed the Chinese mainland and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. For this reason, we do not expect to be identified as a Commission-Identified Issuer under the HFCAA.

On December 29, 2022, the President signed the Consolidated Appropriations Act, 2023, which, among other things, amended the HFCAA to reduce the number of consecutive years an issuer can be identified as a Commission - Identified Issuer before the Commission must impose an initial trading prohibition on the issuer's securities from three years to two years. Therefore, once an issuer is identified as a Commission - Identified Issuer for two consecutive years, the Commission is required under the HCFAA to prohibit the trading of the issuer's securities on a national securities exchange and in the over - the - counter market.

Internal Cash Transfers and Dividends

Cash is transferred through our organization in the following manner:

5

Please refer to the selected condensed consolidated financial information below in this Section and the consolidated financial statements commencing at page F-1, included in this Annual Report on Form 20-F, as amended.

VIE Structure Evaluation

The consignment agreement, or VIE, structure that we have, provides contractual opportunity for foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the operating companies. For example, foreign ownership in food production is subject to significant regulations in China. For accounting purposes, we receive the economic benefits of Hainan Aoyu and its subsidiary, in part, through certain contractual arrangements. Such contractual arrangements enable us to consolidate the financial results of the VIE and its subsidiary in our consolidated financial statements under US Generally Accepted Accounting Principles, or GAAP, which VIE structure involves unique risks to investors. Our ordinary shares are shares of Origin, the holding company in the British Virgin Islands, instead of shares of our PRC subsidiaries, or the VIEs or its subsidiary in China. As of the date of this report, the contractual arrangements have not been tested in court in either the PRC or the United States. Neither the investors in the holding company nor the Company have an full equity ownership in, direct foreign investment in, or control as effective as equity ownership of, the VIE.

Because we do not directly hold all equity interests in the VIE or its subsidiary, we and the VIE are subject to risks and uncertainties of the interpretations and applications of PRC laws and regulations, including but not limited to, the validity and enforcement of the contractual arrangements and uncertainties about any future actions of the PRC government resulting in disallowing the VIE structure. The loss of our operations conducted under the contractual arrangements would likely result in a material change in our operations, and the value of our ordinary shares may depreciate significantly or become worthless.

Origin evaluates all transactions and relationships with variable interest entities (“VIE”) to determine whether the Company is the primary beneficiary of the entities in accordance with FASB ASC 810, Consolidation. Origin’s overall methodology for evaluating transactions and relationships under the VIE requirements includes the following two steps:

In performing the first step, the significant factors and judgments that the Company considers in making the determination as to whether an entity is a VIE include:

6

If the Company identifies a VIE based on the above considerations, it then performs the second step and evaluates whether it is the primary beneficiary of the VIE by considering the following significant factors and judgments:

Based on its evaluation of the above factors and judgments, as of September 30, 2021, 2022 and 2023, the Company consolidated any VIEs in which it was the primary beneficiary.

Risks Associated with VIE Structure

We discuss the risks of being a BVI holding company with operations only in the PRC in greater detail In Item 3, subpart D, to the Annual Report on Form 20-F, for the fiscal year ended September 30, 2023.

Selected Condensed Consolidated Financial Information

The following table presents our condensed consolidating schedule of financial position for our top-tier holding company, Origin Agritech Limited, our wholly-owned subsidiaries that are the primary beneficiaries of the VIEs under U.S. GAAP (the “Primary Beneficiaries of VIEs”), our other subsidiaries that are not VIEs (the “Other Subsidiaries”), and VIEs and their subsidiaries that we consolidate as of the dates presented were as follows:

(1) Parent: Origin Agritech Limited (BVI);

(2) Other subsidiaries that are equity owned: OAL SMY Limited (United States), Beijing Origin State Harvest Biotechnology (PRC) and its partly owned subsidiaries Anhui Aoyu, Henan Aoyu, Hubei Aoyu, Shandong Aoruixinong, Xuzhou Aoyu, Beijing Origin and Baodao Origin and the subsidiary of BaoDao Origin, Shihezi Baodao (all PRC);

(3) Primary Beneficiary of VIE: State Harvest Holdings Limited (PRC); and

(4) VIE and VIE subsidiary : Hainan Aoyu Biotechnology Limited (PRC) and Xinjiang Originbo Seed Limited (PRC)

7

Selected Condensed Consolidated Balance Sheets Data

In RMB’000

As of September 30, 2023 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Intercompany receivables (1) |

| 237,923 |

| 119,300 |

| — |

| — |

| (357,223) |

| — |

Total current assets |

| 246,788 |

| 181,944 |

| — |

| 70,273 |

| (357,223) |

| 141,782 |

Investments in subsidiaries (2) |

| — |

| 11,386 |

| — |

| 130,541 |

| (141,927) |

| — |

Benefits through VIEs and VIE’s subsidiaries (2) |

| — |

| — |

| 233,520 |

| — |

| (233,520) |

| — |

Working capital | 239,913 | (38,630) | (215,363) | (157,599) | — | (171,679) | ||||||

Total Assets |

| 246,788 |

| 241,062 |

| 233,520 |

| 220,777 |

| (703,641) |

| 238,506 |

Intercompany payables (1) | — | — | 215,347 | 141,876 | (357,223) | — | ||||||

Fiscal year ended September 30, 2022 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Intercompany receivables |

| 216,571 |

| — |

| — |

| 59,417 |

| (275,988) |

| — |

Total current assets |

| 223,896 |

| 56,807 |

| — |

| 76,825 |

| (275,988) |

| 81,540 |

Intercompany payables |

| — |

| 63,040 |

| 212,948 |

| — |

| (275,988) |

| — |

Working capital |

| 223,172 |

| (52,156) |

| (212,964) |

| (169,376) |

| — |

| (211,325) |

Investments in subsidiaries |

| — |

| 90,907 |

| — |

| — |

| (90,907) |

| — |

Benefits through VIEs and VIE’s subsidiaries |

| — |

| — |

| 233,520 |

| — |

| (233,520) |

| — |

Total Assets |

| 223,896 |

| 165,831 |

| 233,520 |

| 112,123 |

| (600,415) |

| 135,955 |

8

Selected Condensed Consolidated Statements of Operations Data

For the Year Ended September 30, 2023 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Third-party revenues |

| — |

| 39,696 |

| — |

| 53,611 |

| — |

| 93,307 |

Intra- group revenues |

| — |

| 18,574 |

| — |

| — |

| (18,574) |

| — |

Total revenue |

| — |

| 58,270 |

| — |

| 53,611 |

| (18,574) |

| 93,307 |

Third-party costs of Revenue |

| — |

| (30,208) |

| — |

| (45,876) |

| 24 |

| (76,060) |

Intra- group costs of Revenue |

| — |

| (18,574) |

| — |

| — |

| 18,574 |

| — |

Total costs of Revenue |

| — |

| (48,782) |

| — |

| (45,876) |

| 18,598 |

| (76,060) |

Total Operating expenses |

| (5,022) |

| (20,448) |

| — |

| (7,568) |

| 800 |

| (32,238) |

Income from subsidiaries and VIE |

| 39,458 |

| — |

| 39,458 |

| — |

| (78,916) |

| — |

Income (loss) from non-operations |

| — |

| (39,394) |

| — |

| 89,807 |

| 27,409 |

| 77,822 |

Income before income tax expenses |

| 34,436 |

| (50,354) |

| 39,458 |

| 89,974 |

| (50,683) |

| 62,831 |

Less: income tax (benefit) expenses |

| — |

| (162) |

| — |

| — |

| — |

| (162) |

Net income |

| 34,436 |

| (50,516) |

| 39,458 |

| 89,974 |

| (50,683) |

| 62,669 |

Less: net income (loss) attributable to non-controlling interests |

| — |

| — |

| — |

| 7,337 |

| — |

| 7,337 |

Net income attributable to Origin Agritech Limited’s shareholders |

| 34,436 |

| (50,516) |

| 39,458 |

| 82,637 |

| (50,683) |

| 55,332 |

For the Year Ended September 30, 2022 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Third-party revenues |

| — |

| 45,000 |

| — |

| 7,580 |

| — |

| 52,580 |

Intra- group revenues |

| — |

| 2,584 |

| — |

| 3,224 |

| (5,808) |

| — |

Total revenue |

| — |

| 47,584 |

| — |

| 10,804 |

| (5,808) |

| 52,580 |

Third-party costs of Revenue |

| — |

| (31,591) |

| — |

| (4,795) |

| — |

| (36,386) |

Intra- group costs of Revenue |

| — |

| (2,584) |

| — |

| (3,224) |

| 5,808 |

| — |

Total costs of Revenue |

| — |

| (34,175) |

| — |

| (8,019) |

| 5,808 |

| (36,386) |

Total Operating expenses |

| (5,261) |

| (17,000) |

| — |

| (10,345) |

| 3,516 |

| (29,090) |

Income from subsidiaries and VIE |

| 6,316 |

| — |

| — |

| 6,316 |

| — |

| (12,632) |

Income (loss) from non-operations |

| — |

| (57,603) |

| — |

| 75,056 |

| (2,246) |

| 15,207 |

Income before income tax expenses |

| 1,055 |

| — |

| (61,194) |

| 6,316 |

| — |

| 67,496 |

Less: income tax (benefit) expenses |

| — |

| 14 |

| — |

| — |

| — |

| — |

Net income (loss) |

| 1,055 |

| — |

| (61,180) |

| 6,316 |

| — |

| 67,496 |

Less: net income (loss) attributable to non-controlling interests |

| — |

| — |

| — |

| 8,590 |

| — |

| 8,590 |

Net income (loss) attributable to Origin Agritech Limited’s shareholders |

| 1,055 |

| (61,180) |

| 6,316 |

| 58,906 |

| (11,362) |

| (6,265) |

9

For the Year Ended September 30, 2021 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Third-party revenues | — | 40,660 | — | 5,765 | — | 46,425 | ||||||

Intra- group revenues | — | 9,965 | 3,416 | (13,381) | — | — | ||||||

Total revenue | — | 50,625 | — | 9,181 | (13,381) | 46,425 | ||||||

Third-party costs of Revenue | — | (28,135) | — | (5,476) | — | (33,611) | ||||||

Intra- group costs of Revenue | — | (9,965) | — | (3,416) | 13,381 | — | ||||||

Total costs of Revenue |

| — |

| (38,100) |

| — |

| (8,892) |

| 13,381 |

| (33,611) |

Total Operating expenses |

| (19,316) |

| (57,790) |

| — |

| (78,357) |

| 4,735 |

| (150,728) |

Income from subsidiaries and VIE |

| (110,363) |

| (110,363) |

| 220,726 |

| — |

| — |

| — |

Income (loss) from non-operations |

| — |

| (3,792) |

| — |

| 16,940 |

| (2,137) |

| 11,011 |

Income before income tax expenses |

| (129,679) |

| (49,057) |

| (110,363) |

| (61,128) |

| 223,324 |

| (126,903) |

Less: income tax (benefit) expenses |

| — |

| (178) |

| — |

| — |

| — |

| (178) |

Net income (loss) |

| (129,679) |

| (49,235) |

| (110,363) |

| (61,128) |

| 223,324 |

| (127,081) |

Less: net income (loss) attributable to non-controlling interests |

| 1,492 |

| (37,044) |

| (35,552) |

| — |

| — |

| — |

Net income (loss) attributable to Origin Agritech Limited’s shareholders |

| (129,679) |

| (49,235) |

| (111,855) |

| (24,084) |

| 223,324 |

| (91,529) |

Selected Condensed Consolidated Cash Flows Information

For the Year Ended September 30, 2023 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Total cash provided by operating activities |

| (19,864) |

| 2,717 |

| — |

| 11,691 |

| — |

| (5,456) |

Total cash used in investing activities |

| — |

| (2,312) |

| — |

| (8,912) |

| — |

| (11,224) |

Total cash used in financing activities |

| 17,636 |

| 6,884 |

| — |

| (1,587) |

| — |

| 22,933 |

Effect of exchange rate changes |

| (214) |

| — |

| — |

| — |

| — |

| (214) |

Restricted cash |

| — |

| — |

| — |

| — |

| — |

| — |

Net decrease in cash, cash equivalents and restricted cash |

| (2,442) |

| 7,289 |

| — |

| 1,192 |

| — |

| 6,039 |

For the Year Ended September 30, 2022 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Total cash provided by operating activities |

| (4,567) |

| (2,661) |

| — |

| 10,519 |

| — |

| 3,291 |

Total cash used in investing activities |

| — |

| (480) |

| — |

| (622) |

| — |

| (1,102) |

Total cash used in financing activities |

| 1,614 |

| 7,306 |

| — |

| (9,252) |

| — |

| (332) |

Effect of exchange rate changes |

| 447 |

| — |

| — |

| — |

| — |

| 447 |

Restricted cash |

| — |

| — |

| — |

| 14 |

| — |

| 14 |

Net decrease in cash, cash equivalents and restricted cash |

| (2,506) |

| 4,165 |

| — |

| 659 |

| — |

| 2,318 |

For the Year Ended September 30, 2021 | ||||||||||||

Other | Primary | VIE and | Eliminations | Consolidated | ||||||||

| Parent |

| Subsidiaries |

| Beneficiary of VIE |

| VIE subsidiary (PRC) |

| adjustments |

| Total | |

Total cash provided by operating activities |

| — |

| (24,693) |

| — |

| (384) |

| — |

| (25,077) |

Total cash used in investing activities |

| — |

| 639 |

| — |

| (1,715) |

| (133) |

| (1,209) |

Total cash used in financing activities |

| (8,637) |

| 26,142 |

| — |

| 2,200 |

| 133 |

| 19,838 |

Effect of exchange rate changes |

| (816) |

| — |

| — |

| — |

| — |

| (816) |

Restricted cash | — | — | — | 133 | — | 133 | ||||||

Net decrease in cash, cash equivalents and restricted cash |

| (9,453) |

| 2,088 |

| — |

| 234 |

| — |

| (7,131) |

10

FORWARD-LOOKING INFORMATION

This Annual Report on Form 20-F contains forward-looking statements that are based on our current expectations, assumptions, estimates, and projections about our company and industry. All statements other than statements of historical fact in this Annual Report are forward-looking statements. These forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “estimate,” “plan,” “believe,” “is/are likely to” or other similar expressions. The forward-looking statements included in this Annual Report relate to, among others:

| ● | our expectations for our future business and product development, business prospects, results of business operations and current financial condition; |

| ● | future development of China based agricultural biotechnology as a whole, including our genetically modified seed research and development and its distribution and acceptance in the China market; |

| ● | our ability to develop and commercialize any alternative businesses; |

| ● | address the scope and impact of the governing and regulatory policies and laws on our business, including that of the research and development of genetically modified seed products and any other ancillary businesses in which we engage, and importantly the regulation of VIE business structures in the United States and China; |

| ● | our plans to license or co-develop seed products or technologies; |

| ● | likelihood of recurrence of accounting charges or impairments; |

| ● | expected changes in our sources of revenues and income base and our ability to generate income from our diversified business lines, and how funds might be up-streamed to our holding company, and any limitations thereon imposed by China regulation; |

| ● | competition in our business lines, including the crop seed industry, development of GM seeds; |

| ● | our plans for current staffing requirements and research and development and business expansion; |

| ● | our ability to successfully raise capital to accommodate company needs which are under acceptable terms and at an acceptable share price; and |

| ● | adequacy of our facilities for our operations. |

We believe it is important to communicate our expectations to our shareholders. However, there may be certain events in the future that we are not able to predict with accuracy or over which we have no control. The risk factors and cautionary language discussed in this Annual Report provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations in these forward-looking statements, including among other things:

| ● | changing interpretations of Generally Accepted Accounting Principles (“GAAP”); |

| ● | outcomes of PRC and international government reviews, inquiries, investigations and related litigations, including PCAOB compliance issues and VIE issues; |

| ● | continued compliance with government regulations of PRC and other governments, including that about our business operations and corporate structure; |

| ● | legislative and regulatory environments, requirements or changes adversely affecting the businesses in which we and our PRC operating companies are engaged; and |

| ● | management of the growth of our business and introduction of genetically modified products. |

11

The forward-looking statements in this Annual Report involve various risks, assumptions, and uncertainties. Although we believe that our expectations expressed in these forward-looking statements are reasonable, we cannot be certain that our expectations will materialize. Our actual results could be materially different from our expectations. Important risks and factors that could cause our actual results to be materially different from our expectations are generally set forth in the risk factors included in this Annual Report.

The forward-looking statements made in this Annual Report relate only to events or information as of the date of the statements. Readers should read these statements in conjunction with the risk factors disclosed in this Annual Report.

All forward-looking statements included herein attributable to us or other parties or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, we undertake no obligations to update these forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

12

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

A. Selected financial data.

The following selected consolidated financial information was derived from our fiscal year end consolidated financial statements. The following information should be read in conjunction with those statements and Item 5, “Operating and Financial Review and Prospects.”

Our summary consolidated statements of operations and comprehensive income data for the fiscal years ended September 30, 2021, 2022 and 2023, and our summary consolidated balance sheet data as of September 30, 2022 and 2023, as set forth below, are derived from, and are qualified in their entirety by reference to, our audited consolidated financial statements, including the notes thereto, which are included in this Annual Report.

13

Our consolidated financial statements are prepared and presented in accordance with accounting principles generally accepted in the United States, or U.S. GAAP.

2021 | 2022 | 2023 | 2023 | |||||

| RMB’000 |

| RMB’000 |

| RMB’000 |

| US$’000 | |

Revenues |

| 46,425 |

| 52,580 |

| 93,307 |

| 12,996 |

Cost of revenues |

| (33,611) |

| (36,386) |

| (76,060) |

| (10,594) |

Gross profit |

| 12,814 |

| 16,194 |

| 17,247 |

| 2,402 |

Operating expenses |

|

|

|

|

|

| ||

Selling and marketing |

| (5,564) |

| (7,335) |

| (8,359) |

| (1,164) |

General and administrative |

| (73,315) |

| (14,321) |

| (14,228) |

| (1,982) |

Research and development |

| (1,979) |

| (7,434) |

| (7,447) |

| (1,037) |

Impairment of assets |

| (69,870) |

| — |

| (2,204) |

| (307) |

Total operating expenses, net |

| (150,728) |

| (29,090) |

| (32,238) |

| (4,490) |

Loss from operations |

| (137,914) |

| (12,896) |

| (14,991) |

| (2,088) |

Interest income, net |

| (8,558) |

| (8,228) |

| (982) |

| (137) |

Impairment of long-term investment |

| (5,958) |

| (2,906) |

| (1,490) |

| (208) |

Rental income |

| 10,603 |

| 10,603 |

| 10,603 |

| 1,477 |

Other non-operating income (expense), net |

| 14,924 |

| 15,738 |

| 69,691 |

| 9,707 |

Loss before income taxes |

| (126,903) |

| 2,311 |

| 62,831 |

| 8,751 |

Income tax (expense) benefits, Current |

| (178) |

| 14 |

| (162) |

| (23) |

Net loss |

| (127,081) |

| 2,325 |

| 62,669 |

| 8,728 |

Less: Net (loss) income attributable to non-controlling interests |

| (35,552) |

| 8,590 |

| 7,337 |

| 1,022 |

Net loss attributable to Origin Agritech Limited |

| (91,529) |

| (6,265) |

| 55,332 |

| 7,706 |

Other comprehensive loss |

|

|

|

|

|

| ||

Net loss |

| (127,081) |

| 2,325 |

| 62,669 |

| 8,728 |

Foreign currency translation difference |

| (816) |

| 447 |

| (214) |

| (30) |

Comprehensive loss |

| (127,897) |

| 2,772 |

| 62,455 |

| 8,698 |

Less: Comprehensive (loss) income attributable to non-controlling interests |

| (35,552) |

| 8,590 |

| 7,337 |

| 1,022 |

Comprehensive loss attributable to Origin Agritech Limited |

| (92,345) |

| (5,818) |

| 55,118 |

| 7,676 |

Basic and diluted net income (loss) per share (note 21) |

|

|

|

|

|

|

| |

Continuing operations | (16.29) |

| (1.09) |

| 8.45 |

| 1.18 | |

Basic and diluted net loss per share attributable to Origin Agritech Limited (note 21) | (16.29) |

| (1.09) |

| 8.43 |

| 1.17 | |

Shares used in computing earnings per share: |

|

|

|

|

|

|

| |

Shares used in calculating basic and diluted net income (loss) per share* | 5,617,424 |

| 5,773,094 |

| 6,546,153 |

| 6,546,153 | |

Diluted* | 5,617,424 |

| 5,773,094 |

| 6,562,278 |

| 6,562,278 |

14

| Sept 30 |

| Sept 30 |

| Sept 30 | |

| 2022 |

| 2023 |

| 2023 | |

RMB’000 | RMB’000 | US$’000 | ||||

Consolidated balance sheet data: |

|

|

|

|

|

|

Cash and cash equivalents |

| 17,669 |

| 23,708 |

| 3,302 |

Restricted cash |

| — |

| 561 |

| 78 |

Current working capital (2) |

| (211,325) |

| (171,679) |

| (23,912) |

Total assets |

| 135,955 |

| 238,506 |

| 33,220 |

Total current liabilities |

| 292,865 |

| 313,461 |

| 43,660 |

Total liabilities |

| 308,597 |

| 319,766 |

| 44,538 |

Non-controlling interests |

| (38,770) |

| (23,862) |

| (3,323) |

Total Origin Agritech Limited shareholders’ equity |

| (172,642) |

| (81,260) |

| (11,318) |

| (1) | Translation of Renminbi amounts into United States dollar amounts has been made for the convenience of the reader for the fiscal year ended September 30, 2023, and has been made at the exchange rate quoted by the State Administration of Foreign Exchange in China on September 30, 2023, of RMB 7.1798 to US$1.00. Such translation amounts should not be construed as a representation that the Renminbi amounts could be readily converted into United States dollar amounts at that rate or any other rate. |

| (2) | Current working capital is the difference between total current assets and total current liabilities. |

Exchange Rate Information

The conversion of Renminbi into U.S. dollars in this Annual Report is based on the statistics of the State Administration of Foreign Exchange. The consolidated financial statements are presented in Renminbi, which is our reporting currency. The translation of Renminbi amounts into United States dollar amounts has been made for the convenience of the reader and has been made at the exchange rate quoted by the State Administration of Foreign Exchange in China on September 30, 2023, of RMB 7.1798 to US$1.00. Unless otherwise noted, for the years ended September 30, 2022 and 2023, all translations from Renminbi to U.S. dollars in this Annual Report were made at RMB 7.0998 and RMB 7.1798 per US $1.00, respectively, which were the prevailing year or period end closing rates for those periods. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, the rates stated below, or at all. The PRC government imposes controls over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade.

The following table sets forth information concerning exchange rates between the Renminbi and the U.S. dollar for the periods indicated. These rates are not necessarily the exchange rates that we used in this Annual Report or will use in the preparation of our periodic reports or any other information to be provided to you. The source of the rates is the State Administration of Foreign Exchange in China.

| Average (1) |

| High |

| Low |

| Period-end | |

2019 |

| 6.8694 |

| 7.0884 |

| 6.685 |

| 7.0729 |

2020 |

| 6.9969 |

| 7.1316 |

| 6.7591 |

| 6.8101 |

2021 |

| 6.5059 |

| 6.7796 |

| 6.3572 |

| 6.4854 |

2022 |

| 6.7324 |

| 6.7620 |

| 6.6863 |

| 6.7437 |

2023 |

| 7.0467 |

| 7.2157 |

| 7.1265 |

| 7.1305 |

July 2023 |

| 6.7949 |

| 6.8906 |

| 6.7324 |

| 6.8906 |

August 2023 |

| 6.9621 |

| 7.1107 |

| 6.8821 |

| 7.0998 |

September 2023 |

| 7.1287 |

| 7.1768 |

| 7.0992 |

| 7.1768 |

October 2023 |

| 7.1628 |

| 7.2555 |

| 7.0363 |

| 7.1769 |

November 2023 |

| 6.9833 |

| 7.1225 |

| 6.9565 |

| 6.9646 |

December 2023 |

| 7.1039 |

| 7.1176 |

| 7.0827 |

| 7.0827 |

| (1) | Annual averages are calculated from month-end rates. Monthly averages are calculated using the average of the daily rates during the month. |

15

B. Capitalization and indebtedness.

Not Applicable

C. Reasons for the offer and use of proceeds.

Not Applicable.

D. Risk factors.

Summary of Risk Factors

Below is a summary of what the Company believes to be the primary risk factors that an investor should consider when judging an investment in the Company. Those risk factors identified below should not be to the exclusion of all the other risk factors discussed in this report.

| ● | We operate a portion of our seed business, the seed development business, through a VIE structure, which means investors ultimately may be found not to own a part of our business. There are many risks associated with a VIE structure, which are explained at length herein. |

| ● | Aspects of our business are conducted under technical service agreements and other contractual arrangements, which may not provide the business results and assurances we expect from our contract partners. |

| ● | Our auditor has issued their opinion with a going concern qualification. We expect to need working capital from time to time in the future; we have no assured means of raising capital. |

| ● | We need to continue to develop new seed traits to maintain our biotech pipeline of products. If we do not develop new products and keep up with industry trends, our business will experience setbacks. |

| ● | Although we believe there is a significant, encouraging change in the regulatory approach to GMO products in the PRC, these changes are recent, and there still is uncertainty about full government acceptance and consumer acceptance of GMO products. |

| ● | Development of aspects of our business is through joint ventures. Therefore we rely on others to help us develop our business; we may not be able to maintain these relationships or control our business partners cooperation. |

| ● | We face competition from many sources, including traditional seed products and international competition in the GM seed market. |

| ● | To maintain our product integrity, we must protect our intellectual property rights and the quality of our products in the market place. |

| ● | We operating in a regulated industry, therefore if we do not comply with the different applicable laws and regulations, our business may be impaired and we may suffer economic disruption and penalties. |

| ● | As a foreign private issuer, you may not be able to enforce rights common to investors in companies based in or founded in the United States. Also, under SEC and Nasdaq rules, we do not have to provide in our reports and corporate governance certain information and investor protections. |

| ● | The trading of our ordinary shares on Nasdaq is volatile and inconsistent. You may not be able to effect transactions in your shares at a posted price or in the quantity you desire. |

16

Risks relating to our business

We currently use regional joint venture companies for our seed distribution business; These companies may not be able to perform as we expected.

We have regional joint venture companies for our seed distribution business. The Company has stock positions of 51% or 50% in these joint ventures. Most of the joint venture partners were the Company’s regional distributors in the past. As this is a new business model for the Company and our joint venture partners are engaging with the Company differently than before, no assurance can be given that the joint ventures will perform as well as we expect, which could impact the overall performance of the Company. Because these are separate companies, we may not be able to control their distribution methods for our seed products, with the consequence that our sales may not be as expected.

If we do not manage our ongoing operations successfully, our growth and chances for profitability will be hindered or impeded.

Our Company engages in corn seed research and development, deploying our biotechnology assets. These activities are conducted through the VIE. We plan to continue our seed research and development activities, with a view to licensing our seed traits and seed germplasm characteristics and performing contract research and development services. Our business continues to require substantial investment, human resources and on our cash assets. Our current resources are not likely to be fully support our longer term planned operations and expansion.

Our independent auditors have issued their reports with a going concern statement.

The reports on our financial statements for the fiscal years ended September 30, 2021, 2022 and 2023, included in this Annual Report on Form 20-F, contain a going concern statement. During fiscal years 2021, 2022 and 2023, we raised capital through the sale of our ordinary shares under an at-the-market arrangement and a self-sell registered transaction. Notwithstanding this additional capital, based on our financial resources and our planned operations, we will need to obtain a capital to continue our business as planned, for which we do not have any long term arrangements, and/or generate increased revenue from operations to cover our expenses, of which we cannot be certain. If we are unable to fund our operations, we may have to curtail substantial parts of our business operations or cease our business operations. Investors should evaluate their investment in the Company based on these financial uncertainties.

The successful development and commercialization of our biotech pipeline of products will be important for our growth.

We focus our seed business on biotechnology development in the seed industry. We conduct our own research and development efforts for genetically modified seeds, referred to as GM. We also collaborate with the Chinese Academy of Agricultural Sciences, the National Maize Improvement Center, China Agricultural University, and Zhejiang University in the PRC under various agreements for seed genetic modifications and other seed biotechnologies that give us the right to market the seeds and technologies they develop. We also seek other development and marketing arrangements with other entities in China and elsewhere. The length of time and the risk associated with seed breeding and biotech pipelines are similar and interlinked because both are required as a package for commercial success in markets where biotech traits are approved for growers. Regulatory requirements affect the development of our biotech products, including the GM crop testing of seeds containing the biotech traits. If we do not meet the regulatory requirements, our business and results of operations will be adversely affected. The testing procedures can be lengthy and costly, with no guarantee of success. It could have an adverse effect on our operations if our genetically modified products are unable to pass the safety evaluation for genetically modified agricultural organisms.

17

The potential uncertainty in the government regulation in China of genetic technology and genetically modified, or GM, agricultural products and the acceptance of these products by the public could have an adverse effect on our business.

Genetically modified seed products are controversial; thus genetic modification has not yet been accepted in many countries throughout the world. The Chinese government has only recently begun to issue GM crop safety certificates for eventual commercial cultivation of GM seeds. The Chinese government is encouraging food independence as a country, and we believe that it will increasingly favor GM food products as these products provide better yield and can accommodate changing climatic changes. Consumer reaction to GM products is also becoming a factor in the overall approval process and the ability of companies, such as ours, to sell or license our GM products. Food related GM products have had limited approvals in China, and Chinese consumers continue to be reluctant to embrace GM food products and food using GM products in production. The relative novelty and the potential uncertainty in the government regulation of genetic technology and ultimate consumer acceptance will have an effect on our business development strategy and research activities and may cause us to re-evaluate our development programs for developing new seeds.

The government may not approve or may limit commercialization of genetically modified corn products, which could have an adverse impact on the future of the company.

Even though we believe biotechnology is important in agricultural applications in China, and the Chinese government has supported and approved some uses of genetically modified seeds, we cannot predict whether or when the government will approve the full commercialization of GM seeds, including genetically modified corn such as we develop. We have received research grants in the past that are related to our GM research, which we believe demonstrates support for at least some GM seed use in the future. Notwithstanding expressions of government support, it is still possible that the government may not approve the full commercialization of GM seeds, including GM corn, and it may even ultimately conclude to limit or ban commercialization and/or research relating to genetically modified corn and other seed products. Local governments in China may also seek to evaluate GM seed products and issue their own interpretations and regulations. Any of these actions could have an adverse impact on our future development, and we would not be able to recover our research and development costs spent in developing biotechnology products.

Any sales or operations outside China will be subject to foreign regulatory and legislative requirements, and it will be costly to comply with those regulatory requirements. If we are unable to meet these requirements, we will not be able to distribute our products.

Foreign regulatory and legislative requirements will impact the development and distribution of our seed products in the global market. Certain markets require rigorous testing and pre-approval prior to a market release of the GM seeds. For example, prior to the entry into the United States market, importers of non-United States seeds will need to obtain regulatory approval from various federal and state governmental agencies. The United States Department of Agriculture has to determine if there are any “plant pest” issues with the specific crop and traits. Further, some products may have to be submitted to the US Environmental Protection Agency (the “EPA”) to determine if there are any pesticide-related traits that are subject to regulation. There may also have to be submitted a Microbial Commercial Activity Notice (MCAN) to the EPA, which includes detailed information describing the seed’s characteristics and genetic construction, health and environmental effects, and other data, before GM seeds can be used in the United States for commercial purposes. Finally, even if a seed product has the required certificates and permits, there will be continuous Food and Drug Administration (“FDA”) regulation compliance about food safety, which place responsibility on the seed producer to assure the safety of the GM seed in the food chain and proof that GM crop seeds are “substantially equivalent” to non-modified versions of the seed. In the United States, there is also substantive state regulations applying to seeds: for example, some states have required specific labeling, banned planting and cultivation, and imposed additional certification requirements for use of GM seeds. These types of central and local government regulation and restrictions exist in many other countries around the world.

Obtaining and maintaining permits and certificates for production and sales, and obtaining and maintaining testing, planting and import approvals for our GM seeds, can be time-consuming and costly, with no guarantee of success. In addition, regulatory and legislative requirements may change over time which may affect sales and profitability in those markets. The failure to receive necessary permits or approvals could have long-term effects on our ability to enter into foreign markets.

18

Joint ventures, partnerships, and companies with which we will engage for various aspects of our business present a number of challenges that could have a material adverse effect on our business and results of operations and cash flows.

We use joint ventures in China for our seed business and, as part of our business strategy, we may enter into other joint ventures or similar transactions. These transactions typically involve a number of risks and present financial, managerial and operational challenges, including the existence of unknown potential disputes, liabilities or contingencies that arise after entering into the joint venture related to the counterparties to such joint ventures We could experience financial or other setbacks if transactions encounter unanticipated problems due to challenges, including problems related to execution or integration. Any of these risks could reduce our revenues or increase our expenses, which could adversely affect our results of operations and cash flows.

If we fail to keep up with industry trends or technological developments, our business, results of operations and financial condition may be materially and adversely affected.

The seed business and distribution channels are evolving and subject to continuous technological and market preference changes. Our success in this business area will depend on our ability to keep up with the changes in technology and user behavior, developing new products and creating innovations. Research, development and technological changes and innovations will require substantial capital expenditures in product development as well as in modification of products, services or infrastructure. We cannot assure that we can obtain financing to cover such expenditure. If we fail to adapt our products and services to such changes in an effective and timely manner, we may suffer from decreased user traffic and user base, which, in turn, could materially and adversely affect our business, financial condition and results of operations.

We operate in an evolving market.

Some aspects of our business and prospects depend on the continuing development and growth of e-commerce in China as well as the expansion of the communication network of rural China, and the continuing modernization of rural logistics system, which are affected by numerous factors and not within our control. Furthermore, product quality, user experience, technological innovations, development of internet and internet-based services, and the regulatory environment and macroeconomic environment are also important factors that have the potential to affect our business and prospects. The markets for our products, in particular our genetically modified seeds, are relatively new and rapidly developing and are subject to significant challenges. In addition, our continued growth depends, in part, on our ability to respond to constant changes in the e-commerce industry, particularly in the use e-commerce platforms in rural China, rapid technological evolution, continued shifts in customer demands, frequent introductions of new products and services and constant emergence of new industry standards and practices. Developing and integrating products, services or infrastructure could be expensive and time-consuming, and these efforts may not yield the benefits we expect to achieve. If we cannot successfully access e-commerce platforms to address markets in rural China or maintain and grow our customer base once platforms are available, our business, financial condition and results of operation may be materially and adversely affected.

The degree of public acceptance or perceived public acceptance of our biotechnology products can affect our operations.

Although all genetically modified products must go through rigorous testing, some opponents of the technology consistently attempt to raise public concern about the potential for adverse effects of genetically modified seed products on human or animal health, other plants and the environment. The potential for the adventitious presence of commercial biotechnology traits in conventional seed, or in the grain or products produced from conventional or organic crops, is another factor that could affect the public’s acceptance of these traits. Public concern can affect the timing of, and whether we are able to obtain, government approvals. Even after approvals are granted, public concern may lead to increased regulation or legislation, which could affect our business and operations, and may adversely affect sales of our products to farmers, due to their concerns about available markets for the sale of crops or other products derived from biotechnology.

The seed production business is competitive both in China and throughout the rest of the world.

All levels of the seed development, marketing and distribution business is competitive throughout the world, dominated by a limited number of companies. Increasingly, foreign seed producers are entering the China market with their seed products, which also include GM seeds. In addition to international competitors, we also face China based competition from many seed producers who deploy both traditional seed development methods and more advanced technologically oriented seed producers. Pricing of seed products, which favor the less expensive traditional seeds, is also an issue for those producers of technologically advanced seeds and GM seeds, such as us. To the extent we are uncompetitive, our business will be adversely affected and our financial results negatively impacted.

19

The global competition in biotechnology will affect our business.

We believe we are a leader in biotechnology in China since we have been conducting our proprietary biotechnology research program for many years and have an internal biotech research center. However, as multinational corporations engaged in the crop seed business expand into the agricultural market in China, we anticipate that they will have a greater portfolio of seed products and more advanced technologies than us. Major multinational competitors have a long history in the research and commercialization of their products, sophisticated marketing capabilities, and strong intellectual property estates, all of which may give them competitive advantage over us. Any of these competitive advantages could cause our existing or future products to become less competitive or outdated, and adversely affect our product acceptance in the market place and our results of operations.

We face significant international competition in the GM seed market and the competition may affect our overall sales.

The GM seed market outside China is highly competitive, dominated by a limited number of major, multi-national companies. Compared to us, these companies have greater experience of the GM market and substantially greater resources in the research and development of plant biotechnology. These companies also have substantial production facilities for crop seeds. In addition, they have established market presence, have obtained patent protection in some instances for different seeds, and have built up their brand reputation and distribution networks globally. For example, in the United States, Monsanto (Bayer) and Corteva Agriscience, dominate the GM corn seed market with an estimated 70% of that market. These companies’ extensive GM portfolio of seeds and their success in developing new traits in the seeds could render our existing products less competitive within the China markets, resulting in reduced sales and licensing opportunities compared to our expectations.

A reversion in the Chinese government’s policy of favoring state owned enterprises, including seed companies, at the expanse of privately owned companies may disadvantage our competitive position in the industry.

In China, state owned enterprises including state owned seed companies typically enjoy preferential policy treatments such as more favorable access to capital, tax breaks and subsidies at various levels of government. These treatments have created barriers of entry protecting state companies at the expense of private ones, both domestic and international. Despite the reform of the Chinese seed industry in implemented in the 2008 time frame and the anticipated market-driven industry consolidation going forward, any reversion in the Chinese government’s policy to protect state owned seed companies may again pose competitive challenges to non-state owned companies such as Origin.

We may not be able to maintain our market advantage by improving our GM seeds to fit the needs of the market.

GM seeds varieties need to be improved and altered over a relatively short time frame because the weeds and insects develop resistance to herbicides and pesticides, which often renders the benefits of a particular GM traits less effective. GM seeds need to be altered to tolerate higher doses and/or new varieties of herbicides and pesticides and other farming practices. Changing climatic conditions, such as changes in average rainfall and temperatures will require other modifications to GM seed so that they can be drought resistant. If our GM seed portfolio does not keep pace with these changes or goes in a direction that is not effective in the market, our position in the market would be adversely impacted. Alternatively, we believe that this characteristic of GM seeds gives us an opportunity to introduce our products into various seed markets needing new varieties. We will be required to continue to invest in new research to develop our portfolio of GM seeds so that our GM seeds can adapt to new herbicides and pesticides and differing soil, weather (drought) and growing conditions.

We have a comparatively short operating history in the field of biotechnology research when compared with international seed companies, and our business is subject to the risks of any evolving and developing enterprise, any one of which could limit our growth and our product and market development.

It continues to be difficult to predict how our continuing seed business will develop over the long term. Accordingly, we are still facing all of the risks and uncertainties encountered by companies in the earlier stages of development, such as:

| ● | uncertain and continued market acceptance for our product extensions and our services; |

| ● | evolving nature of the crop seed industry in the PRC, which is marked by seed company consolidation, changing aspects of government subsidies to farmers and becoming more limited, over production of crop seeds, and less adherence to the qualities of branded seeds, among other things; |

20

| ● | highly competitive conditions from both other branded seeds and unbranded seeds and changing customer preferences or needs that will harm sales of our products; |

| ● | the competitive landscape of e-commerce in the PRC and the evolving use of e-commerce by the Chinese population and their needs and preferences; |

| ● | maintaining our competitive position in the PRC and competing with Chinese and international companies, many of which have longer operating histories and greater resources than us; |

| ● | the aging technology of our seed products that do not reflect current agricultural and farmer needs and the continual need to develop new seed products; |

| ● | the cost of our products compared to other sources of seeds for the same crop types; |

| ● | maintaining our current licensing arrangements and entering into new ones to expand our product offerings in both our domestic market and sought after international markets; |

| ● | using a joint venture model for our continuing business where we maintain only a simple majority stake; |