UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

| For the fiscal year ended |

|

|

OR | |

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

| For the transition period from ____________________ to ____________________ |

Commission file number:

|

(Exact name of Registrant as specified in its charter) |

British Columbia,

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone:

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Copy of communications to:

James Guttman Dorsey & Whitney LLP

Brookfield Place 161 Bay Street, Suite 4310

Toronto, Ontario, Canada M5J 2S1

Telephone: (416) 367-7376 Facsimile: (416) 367-7371

Securities registered or to be registered pursuant to Section 12 (b) of the Act: None

Securities registered or to be registered pursuant to Section 12 (g) of the Act.

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | ☒ | |

Accelerated filer | ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐

If “Other” has been checked in response to previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

TABLE OF CONTENTS

|

|

| Page |

| |

|

|

|

|

|

|

|

|

| |||

|

|

|

|

|

|

| 9 |

| |||

|

|

|

|

|

|

| 9 |

| |||

|

|

|

|

|

|

| 9 |

| |||

|

|

|

|

|

|

|

| 9 |

| ||

|

| 9 |

| ||

|

| 9 |

| ||

|

| 9 |

| ||

|

|

|

|

|

|

| 21 |

| |||

|

|

|

|

|

|

|

| 21 |

| ||

|

| 28 |

| ||

|

| 30 |

| ||

|

| 32 |

| ||

|

|

|

|

|

|

| 89 |

| |||

|

|

|

|

|

|

| 89 |

| |||

|

|

|

|

|

|

|

| 89 |

| ||

|

| 92 |

| ||

|

| 95 |

| ||

|

| 95 |

| ||

|

|

|

|

|

|

| 96 |

| |||

|

|

|

|

|

|

|

| 96 |

| ||

|

| 99 |

| ||

|

| 102 |

| ||

|

| 103 |

| ||

|

| 104 |

| ||

|

|

|

|

|

|

| 105 |

| |||

|

|

|

|

|

|

|

| 105 |

| ||

|

| 105 |

| ||

|

| 106 |

| ||

|

|

|

|

|

|

| 106 |

| |||

|

|

|

|

|

|

|

| 106 |

| ||

|

| 106 |

| ||

|

|

|

|

|

|

| 106 |

| |||

|

|

|

|

|

|

|

| 106 |

| ||

|

| 106 |

| ||

|

| 106 |

| ||

|

| 107 |

| ||

|

| 107 |

| ||

|

| 107 |

| ||

|

|

|

|

|

|

| 107 |

| |||

|

|

|

|

|

|

|

| 107 |

| ||

|

| 107 |

| ||

|

| 109 |

| ||

|

| 109 |

| ||

|

| 109 |

| ||

|

| 115 |

| ||

|

| 115 |

| ||

|

| 115 |

| ||

|

| 116 |

| ||

| 2 |

| Table of Contents |

| 116 |

| |||

|

|

|

|

|

|

| 116 |

| |||

|

|

|

|

|

|

|

| 116 |

| ||

|

| 116 |

| ||

|

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| 117 |

| |||

|

|

|

|

|

|

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

| 117 |

| ||

|

|

|

|

|

|

| 117 |

| |||

|

|

|

|

|

|

|

| 117 |

| ||

| Management’s Annual Report on Internal Control Over Financial Reporting |

| 117 |

| |

|

| 117 |

| ||

|

| 117 |

| ||

|

|

|

|

|

|

| 117 |

| |||

|

|

|

|

|

|

| 118 |

| |||

|

|

|

|

|

|

| 118 |

| |||

|

|

|

|

|

|

| 118 |

| |||

|

|

|

|

|

|

| 118 |

| |||

|

|

|

|

|

|

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

| 118 |

| ||

|

|

|

|

|

|

| 118 |

| |||

|

|

|

|

|

|

| 118 |

| |||

|

|

|

|

|

|

| 119 |

| |||

|

|

|

|

|

|

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

| 119 |

| ||

|

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| 120 |

| |||

|

|

|

|

|

|

| 120 |

| |||

|

|

|

|

|

|

| 120 |

| |||

| 3 |

| Table of Contents |

INTRODUCTORY NOTES

GENERAL INFORMATION

In this annual report on Form 20-F (the “Annual Report”), the terms “we”, “our”, “us”, the “Company” refer, unless the context requires otherwise, to Silver Elephant Mining Corp. and its subsidiaries.

References herein to “Common Shares” are references to the Common Shares without par value of the Company.

PRESENTATION OF FINANCIAL AND OTHER DATA

We prepare our audited consolidated financial statements in accordance with International Financial Reporting Standards, or “IFRS”, as issued by the International Accounting Standards Board, or the “IASB”. The financial information and related discussion and analysis contained in this annual report on Form 20-F are presented in Canadian dollars, unless stated otherwise. The financial information analysis in this annual report on Form 20-F is based on our consolidated financial statements as of December 31, 2021, 2020 and 2019, included elsewhere in this document. Percentages and some amounts in this annual report on Form 20-F have been rounded for ease of presentation. Any discrepancies between totals and the sums of the amounts listed are due to rounding.

CURRENCY

Unless otherwise indicated, all references to “dollars” or “$” are to Canadian dollars and all references to “US dollars,” “USD”, “US$” or “USD$” are to United States of America dollars.

SHARE CONSOLIDATIONS AND FORWARD SPLIT

2016 Share Consolidation

On June 7, 2016, we completed a consolidation of our issued and outstanding Common Shares on the basis of one post consolidation Common Share, option and warrant, for 100 pre- consolidation Common Shares, options and warrants, as applicable (we refer to this as the “2016 Consolidation”).

Forward Split

On August 8, 2018, we completed a split of our issued and outstanding Common Shares on the basis of ten post-split Common Shares, options and warrants for 1 pre-split Common Share, option and warrant, as applicable (the “Forward Split”).

2021 Share Consolidation

On December 22, 2021, the shareholders approved a consolidation of our issued and outstanding Common Shares on the basis of one (1) new Common Share for every ten (10) issued and outstanding Common Shares (we refer to this as the “2021 Consolidation”). The 2021 Consolidation was effected on January 14, 2022.

All Common Share and “per share” information in this Annual Report have been retroactively adjusted to reflect the 2021 Consolidation, as applicable, for all periods presented, unless otherwise indicated.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Annual Report constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of Canadian securities laws and are intended to be covered by the safe harbors provided by such regulations (collectively referred to herein as “forward-looking statements”). Forward-looking statements in this Annual Report are frequently, but not always, identified by words such as “expects”, “anticipates”, “intends”, “believes”, “estimates”, “potentially” or similar expressions, or statements that events, conditions or results “will”, “may”, “would”, “could”, “should” occur or are “to be” achieved, and statements related to matters which are not historical facts. Information concerning management’s expectations regarding our future growth, results of operations, performance, business prospects and opportunities may also be deemed to be forward-looking statements, as such information constitutes predictions based on certain factors, estimates and assumptions subject to significant business, economic, competitive and other uncertainties and contingencies, and involve known and unknown risks which may cause the actual results, performance, or achievements to be different from future results, performance, or achievements contained in our forward- looking statements.

Such forward-looking statements include, but are not limited to, statements regarding the following:

| · | the Company’s planned and future exploration and/or development of the Pulacayo Paca silver-lead-zinc property located in the Potosí Department, Antonnio Quijarro province, Bolivia and the Gibellini vanadium project located in the State of Nevada, USA; |

| · | the volatility of the novel coronavirus (“COVID-19”) outbreak as a global pandemic; |

| · | political instability and social unrest in Bolivia and other jurisdictions where the Company operates; |

| · | the use of proceeds from the February 2021 Private Placement and November 2021 Private Placement; |

| 4 |

| Table of Contents |

| · | the Company’s goals regarding exploration, and development of, and production from its projects, and regarding raising capital and conducting further exploration and developments of its properties; |

| · | the Company’s future business plans; |

| · | the Company’s future financial and operating performance; |

| · | the future price of silver, lead, zinc, vanadium and other metals; |

| · | expectations regarding any environmental issues that may affect planned or future exploration and development programs and the potential impact of complying with existing and proposed environmental laws and regulations; |

| · | the ability to obtain or maintain any required permits, licenses or other necessary approvals for the exploration or development of the Company’s projects; |

| · | government regulation of mineral exploration and development operations in Bolivia and other relevant jurisdictions; |

| · | the Company’s reliance on key management personnel, advisors and consultants; |

| · | the volatility of global financial markets; |

| · | the timing and amount of estimated future operating and exploration expenditures; |

| · | the costs and timing of the development of new deposits; |

| · | the continuation of the Company as a going concern; |

| · | the likelihood of securing project financing; |

| · | the impacts of changes in the legal and regulatory environment in which the Company operates; |

| · | the timing and possible outcome of any pending litigation and regulatory matters; and |

| · | other information concerning possible or assumed future results of the Company’s operations. |

The forward-looking statements in this Annual Report are based upon our current business and operating plans, and are subject to certain risks, uncertainties and assumptions. Many factors could cause our actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by our forward-looking statements, including, among others:

| · | the Company is an exploration stage company; |

| · | the cost, timing and amount of estimated future capital, operating exploration, acquisition, development and reclamation activities; |

| · | the volatility of the market price of the Common Shares; |

| · | judgment of management when exercising discretion in the use of proceeds from offerings of securities; |

| · | sales of a significant number of Common Shares in the public markets, or the perception of such sales, could depress the market price of the Common Shares; |

| · | potential dilution with the issuance of additional Common Shares; |

| · | none of the properties in which the Company has a material interest have mineral reserves; |

| · | estimates of mineral resources are based on interpretation and assumptions and are inherently imprecise; |

| · | the Company has not received any material revenue or net profit to date; |

| · | exploration, development and production risks; |

| · | no history of profitable mineral production; |

| · | actual capital costs, operating costs, production and economic returns may differ significantly from those the Company has anticipated; |

| · | foreign operations and political condition risks and uncertainties; |

| · | legal and political risk, including as a result of the new Biden administration in the United States; |

| · | amendments to local laws; |

| · | the ability to obtain, maintain or renew underlying licenses and permits; |

| · | title to mineral properties; environmental risks; |

| · | competitive conditions in the mineral exploration and mining business; |

| · | availability of adequate infrastructure; |

| · | the ability of the Company to retain its key management and employees and the impact of shortages of skilled personnel and contractors; |

| · | limits of insurance coverage and uninsurable risk; |

| · | reliance on third party contractors; |

| · | the availability of additional financing on reasonable terms or at all; |

| · | foreign exchange risk; |

| · | impact of anti-corruption legislation; |

| · | recent global financial conditions; |

| · | changes to the Company’s dividend policy; |

| · | conflicts of interest; |

| · | cyber security risks; |

| · | litigation and regulatory proceedings; |

| · | the obligations which the Company must satisfy in order to maintain its interests in its properties; |

| · | the influence of third-party stakeholders; |

| · | the Company’s relationships with the communities in which it operates; |

| 5 |

| Table of Contents |

| · | human error; |

| · | the speculative nature of mineral exploration and development in general, including the risk of diminishing quantities or grades of mineralization; |

| · | proposed legislation in Nevada that could increase the costs or taxation of our operations; |

| · | the Company is likely a “passive foreign investment company”, which may have adverse U.S. federal income tax consequences for U.S. investors; and |

| · | other risks and the factors discussed under the heading “Risk Factors” in this Annual Report. |

This foregoing list is not exhaustive of the factors that may affect any of our forward-looking statements. Some of the important risks and uncertainties that could affect forward- looking statements are described further under the heading “Risk Factors” in this Annual Report. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein. For the reasons set forth above and elsewhere in this Annual Report, we caution you not to place undue reliance on forward-looking statements in this Annual Report.

The forward-looking statements in this Annual Report speak only as to the date of this Annual Report and are based on our beliefs, opinions and expectations at the time they are made. Except as required by law, we undertake no obligation to update or review any forward-looking statements whether as a result of new information, future developments or otherwise.

METRIC CONVERSION TABLE

To Convert Imperial Measurement Units |

| To Metric Measurement Units |

| Multiply by |

Acres |

| Hectares |

| 0.4047 |

Feet |

| Meters |

| 0.3048 |

Miles |

| Kilometers |

| 1.6093 |

Tons (short) |

| Tonnes |

| 0.9072 |

Gallons |

| Liters |

| 3.785 |

Ounces (troy) |

| Grams |

| 31.103 |

Ounces (troy) per ton (short) |

| Grams per tonne |

| 34.286 |

TECHNICAL INFORMATION

This Annual Report contains information of a technical or scientific nature respecting the Company’s mineral properties (the “Technical Information”). Technical Information is primarily derived from the documents referenced herein. All Technical Information which appears in this Annual Report has been reviewed and approved by Danniel Oosterman, Vice President Exploration of the Company who is a “Qualified Person” as defined by the guidelines in NI 43-101 and S-K 1300. The Company operates quality assurance and quality control of sampling and analytical procedures.

On October 31, 2018, the United States Securities and Exchange Commission (“SEC”) adopted Subpart 1300 of Regulation S-K (“S-K 1300”) along with the amendments to related rules and guidance in order to modernize the property disclosure requirements for mining registrants under the Securities Act and the Securities Exchange Act. Registrants engaged in mining operations must comply with Regulation S-K 1300 for the first fiscal year beginning on or after January 1, 2021. Accordingly, the Company is providing disclosure in compliance with Regulation S-K 1300 for its fiscal year ending December 31, 2021, and all of its mineral resources have been determined in accordance with Regulation S-K 1300 as well as in accordance with NI 43-101.

GLOSSARY OF TERMS

Ag | silver |

|

|

Au | gold |

|

|

deposit | means a mineral deposit which is a mineralized mass that may be economically valuable, but whose characteristics may require more detailed information. Mineral resources are calculated from geological data collected from deposits, however, deposits do not necessarily reflect the presence of mineral resources. |

|

|

Fe | iron |

|

|

ft | feet |

|

|

g/t | Grams per tonne |

|

|

lb. | pound (2,000 lbs. to 1 ton, 2,204.6 lbs. to 1 tonne) |

| 6 |

| Table of Contents |

Indicated Coal Resource

| That part of a Coal Resource for which quantity or quality, densities, shape, and physical characteristics can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and quality continuity to be reasonably assumed. |

|

|

Indicated Mineral Resources

| That part of a Mineral Resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a reasonable level of confidence. It is based on exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. The locations are too widely or inappropriately spaced to confirm geological and/or grade continuity but are spaced closely enough for continuity to be assumed. |

|

|

Inferred Coal Resource | That part of a Coal Resource for which quantity and quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and quality continuity. The estimate is based on limited information and sampling, gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings, and drill holes. |

|

|

Inferred Mineral Resource | Inferred Mineral Resource is the part of a mineral resource for which tonnage, grade and mineral content can be estimated with a low level of confidence. It is inferred from geological evidence and assumed but not verified geological or grade continuity. |

|

|

m | meters |

|

|

Measured Mineral Resource | That part of a Mineral Resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a high level of confidence. It is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. The locations are spaced closely enough to confirm geological and grade continuity. |

|

|

mineral resource

| means a concentration or occurrence of natural, solid, inorganic, or fossilized organic material in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics, and continuity of a mineral resource are known, estimated, or interpreted from specific geological evidence and knowledge. Mineral resources are sub-divided, in order of increasing geological confidence, into Inferred, Indicated, and Measured categories. Note that the confidence level in Inferred Mineral Resources is insufficient to allow the application of technical and economic parameters or to enable an evaluation of economic viability worthy of public disclosure. Regardless of category, a mineral resource is estimated through application of the guidelines of the Canadian Institute of Mining, Metallurgy and Petroleum Standards for Mineral Resources and Reserves: Definitions and Guidelines, as amended in 2014. A “historic” mineral resource estimate refers to a mineral resource estimate of the quantity, grade, or metal or mineral content of a deposit that the Company has not verified as current, and which was prepared before the Company acquired or entered into an agreement to acquire, an interest in the property that contains the deposit. |

|

|

NI 43-101 | Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects. |

|

|

oz. | troy ounce (12 oz. to 1 pound) |

|

|

Preliminary Economic Assessment (PEA) | A preliminary assessment study which includes an economic analysis of the potential viability of a material resource prior to the completion of a prefeasibility study. Based on the Society for Mining, Metallurgy and Exploration (SME) study types a PEA (also known as a conceptual or scoping study used to support a NI 43-101 Technical Report is within +/-35% degree of accuracy. |

| 7 |

| Table of Contents |

Preliminary Feasibility Study (PFS)

| A comprehensive study of the viability of a project that has advanced to a stage where the mining method and pit configuration has been established and an effective method of coal processing has been determined, and includes a financial analysis based on reasonable assumptions of technical, engineering, legal, operating, economic, social, and environmental factors, and the evaluation of other relevant factors which are sufficient for a Qualified Person (QP), acting reasonably, to determine if all or part of a Resource can be classified as a Reserve (CIM Standards, 2014). Based on the SME study types a PFS used to support a NI 43-101 Technical Report is within +/-25% degree of accuracy. |

|

|

Qualified Person Or QP

| An individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation, or mineral project assessment, or any combination of these; has experience relevant to the subject matter of the mineral project and the technical report; and is a member or licensee in good standing of a professional association recognized under NI 43-101 and S-K 1300 (CIM Standards, 2014). |

|

|

S-K 1300 | Subpart 1300 of Regulation S-K which sets forth the required mining disclosures required by the SEC. |

|

|

S-K 1300 – Indicated Mineral Resource | Indicated mineral resource is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of adequate geological evidence and sampling. The level of geological certainty associated with an indicated mineral resource is sufficient to allow a qualified person to apply modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Because an indicated mineral resource has a lower level of confidence than the level of confidence of a measured mineral resource, an indicated mineral resource may only be converted to a probable mineral reserve. |

|

|

Ti | Titanium |

|

|

V | Vanadium |

| 8 |

| Table of Contents |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

This section describes some of the risks and uncertainties faced by us. An investment in the Company involves a high degree of risk. You should carefully consider the risks described below and the risks described elsewhere in this Annual Report when making an investment decision related to the Company. We believe the risk factors summarized below are most relevant to our business. These are factors that, individually or in the aggregate, could cause our actual results to differ significantly from anticipated or historical results. The occurrence of any of the risks could harm our business and cause you to lose all or part of your investment. However, you should understand that it is not possible to predict or identify all such factors. The risks and uncertainties described and discussed below and elsewhere in this Annual Report are not the only risks and uncertainties that we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations. If any of these risks actually occurs, our business, financial condition and results of operations would suffer. The risks discussed below also include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements. See the discussion under the heading “Cautionary Note Regarding Forward-Looking Statements” at the beginning of this Annual Report for more detail.

Except as required by law, we undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events, or otherwise.

| 9 |

| Table of Contents |

We have a history of net losses and do not anticipate having positive cash flow in the foreseeable future.

We have not received any material revenue or net profit to date. Exploration and development of mineral properties requires large amounts of capital and usually results in accounting losses for many years before profitability is achieved, if ever. We have incurred losses and negative operating cash flow during our most recently completed financial year and for the current financial year to date. We believe that commercial mining activity is warranted on our Gibellini Project (as defined herein) and Pulacayo Project (as defined herein). Even if we undertake future development activity on any of our properties, there is no certainty that we will produce revenue, operate profitably or provide a return on investment in the future. The exploration of our properties depends on our ability to obtain additional required financing. There is no assurance that we will be successful in obtaining the required financing, which could cause us to postpone our exploration plans or result in the loss or substantial dilution of our interest in our properties.

We will need a significant amount of capital to carry out our proposed business plan. Unless we are able to raise sufficient funds, we may be forced to discontinue our operations.

We are in the exploration stage and will likely operate at a loss until our business becomes established. We will require additional financing in order to fund future operations. Our ability to secure any required financing in order to commence and sustain our operations will depend in part upon prevailing capital market conditions as well as our business success. There can be no assurance that we will be successful in our efforts to secure any additional financing on terms satisfactory to our management. If additional financing is raised by issuing Common Shares, control may change, and shareholders may suffer additional dilution. If adequate funds are not available or they are unavailable on acceptable terms, we may be required to scale back our business plan or cease operating.

Our mineral exploration efforts are highly speculative in nature and may be unsuccessful.

The exploration for and development of minerals involve significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. Few properties which are explored are ultimately developed into producing mines. There can be no guarantee that the estimates of quantities and qualities of minerals disclosed will be economically recoverable. With all mining operations there is uncertainty and, therefore, risk associated with operating parameters and costs resulting from the scaling up of extraction methods tested in pilot conditions. Mineral exploration is speculative in nature and there can be no assurance that any minerals discovered will result in an increase in our resource base.

Our operations are subject to all of the hazards and risks normally encountered in the exploration, development and production of minerals. These include unusual and unexpected geological formations, rock falls, seismic activity, flooding and other conditions involved in the extraction of material, any of which could result in damage to, or destruction of, mines and other producing facilities, damage to life or property, environmental damage and possible legal liability. Although precautions to minimize risk will be taken, operations are subject to hazards that may result in environmental pollution and consequent liability that could have a material adverse impact on our business, operations and financial performance.

Substantial expenditures are required to establish ore reserves through drilling, to develop metallurgical processes to extract the metal from the ore and, in the case of new properties, to develop the mining and processing facilities and infrastructure at any site chosen for mining. Although substantial benefits may be derived from the discovery of a major mineralized deposit, no assurance can be given that minerals will be discovered in sufficient quantities to justify commercial operations or that funds required for development can be obtained on a timely basis. The economics of developing vanadium, silver, coal and other mineral properties is affected by many factors including the cost of operations, variations in the grade of ore mined, fluctuations in metal markets, costs of processing equipment and such other factors such as government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals and environmental protection. The remoteness and restrictions on access of properties in which we have an interest will have an adverse effect on profitability as a result of higher infrastructure costs. There are also physical risks to the exploration personnel working in the terrain in which our properties are located, often in poor climate conditions.

Our long-term commercial success depends on our ability to find, acquire, develop and commercially produce vanadium, silver, coal and other minerals. No assurance can be given that we will be able to locate satisfactory properties for acquisition or participation. Moreover, if such acquisitions or participations are identified, we may determine that current markets, terms of acquisition and participation or pricing conditions make such acquisitions or participations uneconomic.

We have no history of profitably commercially producing vanadium, silver, coal or other metals from our mineral exploration properties and there can be no assurance that we will successfully establish mining operations or profitably produce vanadium, silver, coal or other base or precious metals.

None of our properties are currently under development. The future development of any property found to be economically feasible will require the construction and operation of mines, processing plants and related infrastructure. As a result, we are subject to all of the risks associated with establishing new mining operations and business enterprises, including:

| · | the timing and cost of the construction of mining and processing facilities; |

| · | the availability and costs of skilled labor and mining equipment; |

| · | the availability and cost of appropriate smelting and/or refining arrangements; |

| · | the need to obtain necessary environmental and other governmental approvals and permits and the timing of those approvals and permits; and |

| · | the availability of funds to finance construction and development activities. |

| 10 |

| Table of Contents |

The costs, timing and complexities of mine construction and development are increased by the remote location of our mining properties. It is common in new mining operations to experience unexpected problems and delays during development, construction and mine start-up. In addition, delays in the commencement of mineral production often occur. Accordingly, there are no assurances that our activities will successfully establish mining operations, result in profitable operations or that vanadium, silver, coal or other metals will be produced at any of our properties.

All of the properties in which we hold an interest are considered to be in the exploration stage only and do not contain a known body of commercial minerals. The figures for our resources are estimates based on interpretation and assumptions and may yield less mineral production under actual operating conditions than is currently estimated.

All of the properties in which we hold an interest are considered to be in the exploration stage only and do not contain a known body of commercial minerals. The figures for our resources are estimates based on interpretation and assumptions and may yield less mineral production under actual operating conditions than is currently estimated. Unless otherwise indicated, mineralization figures presented in this Annual Report and in our other filings with securities regulatory authorities, news releases and other public statements that may be made from time to time are based upon estimates made by our personnel and independent geologists. These estimates may be imprecise because they are based upon geological and engineering interpretation and statistical inferences drawn from drilling and sample analysis, stated operating conditions, and mineral processing tests, which may prove to be unreliable. There can be no assurance that:

| · | these estimates will be accurate; |

| · | resource or other mineralization figures will be accurate; or |

| · | the resource or mineralization could be mined or processed profitably. |

Because we have not commenced production at any of our properties, other than Ulaan Ovoo, and have not defined or delineated any proven or probable reserves on any of our properties, the mineralization estimates for our properties may require adjustments including possible downward revisions based upon further exploration or development work, actual production experience, or current costs and sales prices. In addition, the quality of coal or grade of ore ultimately mined, if any, may differ from that indicated by drilling and beneficiation testing results. There can be no assurance that the type and amount of minerals recovered in laboratory analyses and small-scale beneficiation tests will be duplicated in large-scale tests under on-site conditions or in production scale.

The resource estimates contained in this Annual Report have been estimated based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for vanadium, silver, coal or other metals may render portions of our mineralization uneconomic and result in reduced reported mineralization. Any material reductions in estimates of mineralization, or of our ability to extract this mineralization, could have a material adverse effect on our results of operations or financial condition.

Actual capital costs, operating costs, production and economic returns may differ significantly from those we have anticipated and there are no assurances that any future development activities will result in profitable mining operations.

Actual capital costs, operating costs, production and economic returns may differ significantly from those we have anticipated, and we cannot assure you that any future development activities will result in profitable mining operations. The capital costs required to take our projects into production may be significantly higher than anticipated. None of our mineral properties has a sufficient operating history upon which we can base estimates of future operating costs. Any potential decisions about the possible development of these and other mineral properties would ultimately be based upon feasibility studies which may or may not be undertaken. Feasibility studies derive estimates of cash operating costs based upon, among other things:

| · | anticipated tonnage, grades and metallurgical characteristics of the ore or quality of the vanadium, silver, coal or other minerals to be mined and/or processed; |

| · | anticipated recovery rates of metals from the ore; |

| · | cash operating costs of comparable facilities and equipment; and |

| · | anticipated climatic conditions. |

Cash operating costs, production and economic returns, and other estimates contained in studies or estimates prepared by or for us may differ significantly from those anticipated by our current studies and estimates, and there can be no assurance that our actual operating costs will not be higher than currently anticipated.

COVID-19 - The outbreak of contagious diseases, including the spread of the coronavirus, could impact our business operations, results of operations and/or financial condition.

An emerging risk is a risk not well understood at the current time and for which the impacts on strategy and financial results are difficult to assess or are in the process of being assessed. Since December 31, 2019, the outbreak of the novel strain of coronavirus, specifically identified as “COVID-19”, has resulted in governments worldwide enacting emergency measures to combat the spread of the virus. These measures, which include the implementation of travel bans, self-imposed quarantine periods and social distancing, have caused material disruption to businesses globally, resulting in an economic slowdown. Global equity markets have experienced significant volatility and weakness. Governments and central banks have reacted with significant monetary and fiscal interventions designed to stabilize economic conditions. The duration and impact of the COVID-19 outbreak is unknown at this time, as is the efficacy of the government and central bank interventions. It is not possible to reliably estimate the length and severity of these developments and the impact on the financial results and condition of the Company and its operating subsidiaries in future periods.

| 11 |

| Table of Contents |

Our business operations could be significantly adversely affected by the effects of a widespread global outbreak of contagious disease, including the recent outbreak of respiratory illness caused by COVID-19. We cannot accurately predict the impact COVID-19 will have on third parties, including our employees or contractors, ability to fulfil their obligations to the Company, including due to uncertainties relating to the ultimate geographic spread of the virus, its severity, the duration of the outbreak, and the restrictions imposed by governments of affected countries to combat COVID-19. In addition, a significant outbreak of contagious diseases in the human population could result in a widespread health crisis that could adversely affect the economies and financial markets of many countries (including those countries in which our properties are located and other countries we rely on to conduct our business operations), resulting in an economic downturn that could negatively impact our operating results and financial condition. There can be no assurance that any policies or procedures that have been or that may be put in place by the Company will mitigate the risks associated with, or that they will not cause us to experience, less favourable health, safety and economic outcomes, including the ability to obtain financing for business operations as needed or on terms acceptable to the Company.

We are subject to substantial government regulation in the United States and Canada. Changes to regulation or more stringent implementation could have a material adverse effect on our results of operations and financial condition.

Mining and exploration activities at our properties in North America are subject to various laws and regulations relating to the protection of the environment, such as the U.S. federal Clean Water Act and the Nevada Water Pollution Control Law. Although we intend to comply with all existing environmental and mining laws and regulations, no assurance can be given that we will be in compliance with all applicable regulations or that new rules and regulations will not be enacted, including by the new Biden administration in the United States, or that existing rules and regulations will not be applied in a manner that could limit or curtail development of our properties.

All claims held by us in the United States are unpatented lode mining claims and all claims held by us in Ontario are patented claims. Our Manitoba claims are Crown Land mineral claims and mineral leases administered by the Manitoba Provincial government. At present, there is no royalty payable to the United States on production from unpatented mining claims, but exploration and development on these claims is subject to regulation and requires permits from the U.S. Department of Interior and various state agencies. There is a tax imposed on profits from the extraction of mineral substances raised and sold by operators of Ontario mines. There have been legislative attempts to impose a royalty on production from unpatented mining claims in the United States in recent years. Amendments to current laws and regulations governing exploration, development and mining or more stringent implementation thereof could have a material adverse effect on our business and cause increases in exploration expenses or capital expenditures or require delays or abandonment in the development of our properties.

Our operations are also subject to laws and regulations governing the protection of endangered and other specified species. In May 2015, the U.S. Department of the Interior released a plan to protect the greater sage grouse, a species whose natural habitat is found across much of the western United States, including Nevada. The U.S. Department of the Interior’s plan is intended to guide conservation efforts on approximately 70 million acres of national public lands. No assurances can be made that restrictions relating to conservation will not have an adverse impact on our operations in impacted areas.

We are also required to expend significant resources to comply with numerous corporate governance and disclosure regulations and requirements adopted by Canadian federal and provincial governments, as well as the Toronto Stock Exchange (the “TSX”). These additional compliance costs and related diversion of the attention of management and key personnel could have a material adverse effect on our business.

Reform of the General Mining Law could adversely impact our results of operations.

All of our unpatented mining claims are on U.S. federal lands. Legislation has been introduced regularly in the U.S. Congress over the last decade to change the General Mining Law of 1872, as amended (the “General Mining Law”), under which we hold these unpatented mining claims. It is possible that the General Mining Law may be amended or replaced by less favorable legislation in the future. Previously proposed legislation contained a production royalty obligation, new environmental standards and conditions, additional reclamation requirements and extensive new procedural steps which would likely result in delays in permitting. The ultimate content of future proposed legislation, if enacted, is uncertain. If a royalty on unpatented mining claims were imposed, the profitability of our U.S. operations could be materially adversely affected.

Any such reform of the General Mining Law could increase the costs of our U.S. mining activities or could materially impair our ability to develop or continue our U.S. operations, and as a result, could have an adverse effect on us and our results of operations.

We are required to obtain government approvals and permits in order to conduct operations.

Government approvals and permits are currently required in connection with all of our operations, and further approvals and permits may be required in the future. We must obtain and maintain a variety of licenses and permits, which include or cover, without limitation, air quality, water quality, water rights, dam safety, fire safety, emergency preparedness, hazardous materials, mercury control, waste rock management, solid waste disposal, storm water runoff, water pollution control, water treatment, rights of way and tailings operations. Such licenses and permits are subject to change in regulations and in various operating circumstances. The duration and success of our efforts to obtain permits are contingent upon many variables outside of our control. Obtaining governmental approvals and permits may increase costs and cause delays depending on the nature of the activity to be permitted and the applicable requirements implemented by the permitting authority.

| 12 |

| Table of Contents |

There can be no assurance that all necessary approvals and permits will be obtained or timely obtained. In addition, there can be no assurance that, if obtained, the costs of the approvals and permits will not exceed our estimates or that we will be able to maintain such approvals and permits. To the extent such approvals or permits are required and not obtained or maintained, our operations may be curtailed, or we may be prohibited from proceeding with planned exploration, development or operation of our mineral properties.

Certain of our current exploration properties are located in Bolivia and Mongolia, and their operations may be exposed to various levels of political, economic, and other risks and uncertainties.

Certain of our current exploration properties are located in Bolivia and Mongolia. In these countries, their operations may be exposed to various levels of political, economic, and other risks and uncertainties. These risks and uncertainties include, but are not limited to, political and bureaucratic corruption and uncertainty, terrorism, hostage taking, military repression, fluctuations in currency exchange rates, high rates of inflation, labor unrest, civil unrest, expropriation and nationalization, renegotiation or nullification of existing concessions, licenses, permits and contracts, illegal mining, changes in taxation policies, restrictions on foreign exchange and repatriation, changing political conditions, currency controls, and governmental regulations that favor or require the awarding of contracts to local contractors or require foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction.

Future political and economic conditions may result in a government adopting different policies with respect to foreign development and ownership of mineral resources. Any changes in policy may result in changes in laws affecting ownership of assets, foreign investment, taxation, rates of exchange, resource sales, environmental protection, labour relations or practices, price controls, repatriation of income, and return of capital which may affect both our ability to undertake exploration and development activities in respect of future properties in the manner currently contemplated, as well as our ability to continue to explore, develop, and operate those properties to which we have rights relating to exploration, development, and operations.

Changes in regulations or shifts in political attitudes in Bolivia and Mongolia, as well as in neighboring countries, are beyond our control and may adversely affect our business and financial condition.

Any changes in regulations or shifts in political attitudes in Bolivia and Mongolia are beyond our control and may adversely affect our business, financial condition and prospects.

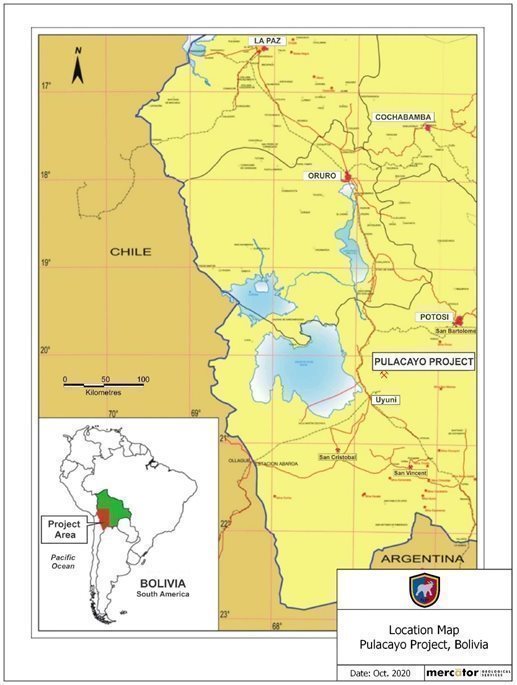

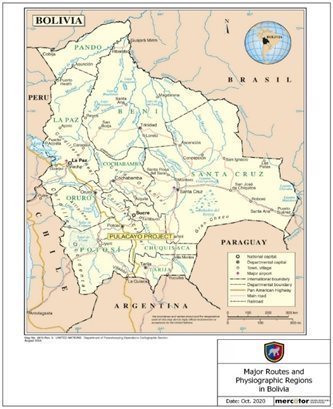

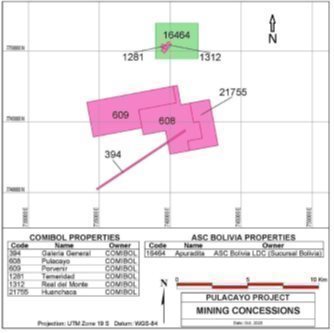

The Bolivian government adopted a new constitution (which we refer to as the “NCPE”) in early 2009 which increased state control over key economic sectors, including mining. The NCPE provides that all minerals, among all natural resources, belong to the Bolivian people who are represented by the government. Such entity is the only one capable of managing all minerals throughout the production chain. Consequently, only the Bolivian central government possesses the authority to grant mining rights. Bolivian President Evo Morales signed a new law, the Law of Mining Rights, increasing the State’s expropriation powers over the mining sector. It was specifically drafted to target mines deemed by the state as unproductive, inactive or idle. The Bolivian government has assigned responsibility for determining whether a concession is idle to the Vice Ministry of Regulation, Auditing and Mining Policy. Mining areas occupied by cooperatives or local groups will not be regarded as idle. There have been recent actions by the government of Bolivia to ease concerns of foreign exploration and mining investors. As reported in the Mining Journal, at a UK-Bolivia trade and investment forum in London in June of 2016, Félix César Navarro, Minister of Mining and Metallurgy (“Minister Navarro”), talked of new safeguards for foreign investors looking to put cash into the country, stating, that new contracts governing exploration, mining and processing were currently going through Bolivia’s congress that would give foreign investors the legal security they need to invest in the country (report by Mining Journal June 10, 2016). Certain Company officials also met with Minister Navarro in March, October and November of 2016. During the meeting in March at the 2016 PDAC convention, Minister Navarro expressed his full support for the start-up and development of the Pulacayo mine. During the October meeting, Minister Navarro stated that the aim of the recent mining regulation is to support the investors and ensure the inclusion of cooperative labor in their projects. At the November meeting, Minister Navarro stated that both public and private mining sectors will try to attract foreign investment disclosing and sharing their experience with investors from several parts of the world. We consider our investment in the Pulacayo Project to be safe. However, we cannot provide any assurance that our operations at the Pulacayo Project will not be affected by changes in the political environment of Bolivia or the political attitudes of the Bolivian government. Further, there can be no assurance that neighboring countries’ political and economic policies in relation to Bolivia will also not have adverse economic effects on our business, including our ability to transport and sell our product and access construction labor, supplies and materials.

The Mongolian legal system shares several of the qualitative characteristics typically found in a developing country and many of its laws, particularly with respect to matters of environment and taxation, are still evolving. A transaction or business structure that would likely be regarded under a more established legal system as appropriate and relatively straightforward might be regarded in Mongolia as outside the scope of existing Mongolian law, regulation, or legal precedent. As the legal framework in Mongolia is in many instances based on recent political reforms or newly enacted legislation which may not be consistent with long-standing conventions and customs, certain business arrangements or structures and certain tax planning mechanisms may carry significant risks. In particular, when business objectives and practicalities dictate the use of arrangements and structures that, while not necessarily contrary to settled Mongolian law, are sufficiently novel within a Mongolian legal context, it is possible that such arrangements may be invalidated.

| 13 |

| Table of Contents |

The legal system in Mongolia has inherent uncertainties that could limit the legal protections available to us. These uncertainties include, without limitation: (i) inconsistencies between laws; (ii) limited judicial and administrative guidance on interpreting Mongolian legislation; (iii) substantial gaps in the regulatory structure due to delay or absence of implementing regulations; (iv) the lack of established interpretations of new principles of Mongolian legislation, particularly those relating to business, corporate and securities laws; (v) a lack of judicial independence from political, social and commercial forces; and (vi) bankruptcy procedures that are not well developed and are subject to abuse. The Mongolian judicial system has relative little experience in enforcing the laws and regulations that currently exist, leading to a degree of uncertainty as to the outcome of any litigation, it may be difficult to obtain swift and equitable enforcement, or to obtain enforcement of a judgment by a court of another jurisdiction.

In addition, while legislation has been enacted to protect private property against expropriation and nationalization, due to the lack of experience in enforcing these provisions and political factors, these protections may not be enforced in the event of an attempted expropriation or nationalization. Whether legitimate or not, expropriation or nationalization of any of our assets, or portions thereof, potentially without adequate or any compensation, could materially and adversely affect our business and results of operations. Further, there can be no assurance that neighboring countries’ political and economic policies in relation to Mongolia will not have adverse economic effects on our business, including our ability to transport and sell our product and access construction labor, supplies and materials.

In Bolivia, recent and anticipated changes to mining laws and policies and mining taxes and expected changes in governmental regulation or governmental actions may adversely affect us.

In Bolivia, recent and anticipated changes to mining laws and policies and mining taxes and expected changes in governmental regulation or governmental actions may adversely affect us. On May 28, 2014, Law 535 of Mining and Metallurgy (which we refer to as the “May Mining Law”) was adopted and placed into effect. Pursuant to the May Mining Law, we must develop our mining activities to comply with the economic and social function, which means observing the sustainability of the mining activities, work creation, respecting the rights of our mining workers, and ensuring the payment of mining patents and the continuity of existing activities.

The Framework Law on Mother Earth and Integral Development for Living Well (together with the May Mining Law, the “New Mining Laws”), in effect since October 15, 2012, prioritizes the importance of nature to the Bolivian people and could have significant consequences to the country’s mining industry. This law established 11 new rights for “mother earth” including, the right to life and to exist; the right to continue vital cycle and processes free from human alteration; the right to pure water and clean air; the right to balance; the right not to be polluted; and the right to not have cellular structure modified or genetically altered. At present, it is unclear how the New Mining Laws will affect exploration companies with projects in the area or how the law will be enforced.

In the past, the Government of Bolivia has nationalized the assets of certain companies in various industries. Nationalization or other expropriation of our assets, without adequate compensation, could have a material adverse effect on our business and/or result in the total loss of our investment in Bolivia.

Our mineral rights may be terminated or not renewed by governmental authorities and we may be negatively impacted by changes to mining laws and regulations.

Our activities are subject to government approvals, various laws governing prospecting, development, land resumptions, production taxes, labor standards and occupational health, mine safety, toxic substances and other matters, including issues affecting local native populations. Although we believe that our activities are currently carried out in accordance with all applicable rules and regulations, no assurance can be given that new rules and regulations will not be enacted or that existing rules and regulations will not be applied in a manner which could limit or curtail production or development. Amendments to current laws and regulations governing operations, including by the new Biden administration in the United States and proposed changes to tax laws in Nevada, and activities of exploration and mining, or more stringent implementation thereof, could have a material adverse impact on our business, operations and financial performance. Further, the mining licenses and permits issued in respect of our projects may be subject to conditions which, if not satisfied, may lead to the revocation of such licenses. In the event of revocation, the value of our investments in such projects may decline.

In the United States, the tenures are in the form of claims where exploration and development rights are retained so long as annual maintenance fees are paid and certain forms filed. The maintenance fees may be substantial with a large number of claims and the fees are adjusted periodically. Diligent periodic assessment of the resource and development value of claims by the claimant is required.

Title to our mineral properties may be disputed by third parties.

Title to mineral properties, as well as the location of boundaries on the grounds may be disputed. Moreover, additional amounts may be required to be paid to surface right owners in connection with any mining development. At all of such properties where there are current or planned exploration activities, we believe that we have either contractual, statutory, or common law rights to make such use of the surface as is reasonably necessary in connection with those activities. Although we believe we have taken reasonable measures to ensure proper title to our properties, there is no guarantee that title to our properties will not be challenged or impaired. Successful challenges to the title of our properties could impair the development of operations on those properties.

| 14 |

| Table of Contents |

Environmental regulations worldwide have become increasingly stringent over the last decade which will require us to dedicate more time and money to compliance and remediation activities.

All phases of the mining business present environmental risks and hazards and are subject to environmental regulation pursuant to a variety of international conventions, and federal, state and municipal laws and regulations. Environmental legislation provides for, among other things, restrictions and prohibitions on spills and releases or emissions of various substances produced in association with mining operations. The legislation also requires that wells and facility sites be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. Compliance with such legislation can require significant expenditures and a breach may result in the imposition of fines and penalties, some of which may be material. Environmental legislation is evolving in a manner expected to result in stricter standards and enforcement, larger fines and liability and potentially increased capital expenditures and operating costs. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies and their directors, officers and employees. The cost of compliance with changes in governmental regulations has a potential to reduce the profitability of operations.

Failure to comply with applicable laws, regulations, and permitting requirements may result in enforcement actions under, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Entities engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations and, in particular, environmental laws.

Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on our business and cause increases in capital expenditures, production costs or reduction in levels of production at producing properties, or require abandonment or delays in the development of new mining properties.

Certain of our properties are located on land that is or may become subject to traditional territory, title claims and/or claims of cultural significance by certain Native American tribes or Aboriginal communities and stakeholders, and such claims and the attendant obligations of the provincial and federal governments to those tribal or Aboriginal communities and stakeholders may affect our current and future operations.

Native American and Aboriginal interests and rights as well as related consultation issues may impact our ability to pursue exploration and development at our U.S. and Canadian properties. There is no assurance that claims or other assertion of rights by tribal or Aboriginal communities and stakeholders or consultation issues will not arise on or with respect to our properties or activities. These could result in significant costs and delays or materially restrict our activities. Opposition by Native American tribes or Aboriginal communities and stakeholders to our presence, operations or development on land subject to their traditional territory or title claims or in areas of cultural significance could negatively impact us in terms of public perception, costly legal proceedings, potential blockades or other interference by third parties in our operations, or court-ordered relief impacting our operations. In addition, we may be required to, or may voluntarily, enter into certain agreements with such Native American tribes or Aboriginal communities and stakeholders in order to facilitate development of our properties, which could reduce the expected earnings or income from any future production.

Litigation and Regulatory Proceedings

The Company may be subject to civil claims (including class action claims) based on allegations of negligence, breach of statutory duty, public nuisance or private nuisance or otherwise in connection with the Company’s operations, or investigations relating thereto. While the Company is presently unable to quantify any potential liability under any of the above heads of damage, such liability may be material and may materially adversely affect the Company’s ability to continue operations. In addition, the Company may be subject to actions or related investigations by governmental or regulatory authorities in connection with its business activities, including, but not limited to, current and historic activities at the Company’s properties. Such actions may include prosecution for breach of relevant legislation or failure to comply with the terms of the Company’s licenses and permits and may result in liability for pollution, other fines or penalties, revocations of consents, permits, approvals or licenses or similar actions, which could be material and may impact the results of the Company’s operations. The Company’s current insurance coverage may not be adequate to cover any or all the potential losses, liabilities and damages that could result from the civil and/or regulatory actions referred to above.

The mining industry in general is intensely competitive. Furthermore, there is no assurance that, even if commercial quantities are discovered, a ready market will exist for sale of the same mineral ore.

The mining industry in general is intensely competitive and there is no assurance that, even if commercial quantities of ore are discovered, a ready market will exist for the sale of same. Marketability of natural resources which we may discover will be affected by numerous factors beyond our control, such as market fluctuations, the proximity and capacity of natural resource markets and processing equipment, government regulations including regulations relating to prices, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of such factors cannot be predicted but they may result in us not receiving an adequate return on our investment.

The mining business is subject to inherent risks, some of which are not insurable.

Our business is subject to a number of risks and hazards, including adverse environmental conditions, industrial accidents, labor disputes, unusual or unexpected geological conditions, ground or slope failures, cave-ins, changes in the regulatory environment and natural phenomena such as inclement weather conditions, floods and earthquakes. Such occurrences could result in damage to mineral properties or production facilities, personal injury or death, environmental damage to our properties or the properties of others, delays in development or mining, monetary losses and possible legal liability.

| 15 |

| Table of Contents |

Although we maintain insurance to protect against certain risks in amounts that we consider reasonable, our insurance will not cover all the potential risks associated with our operations. We may also be unable to maintain insurance to cover these risks at economically feasible premiums. Insurance coverage may not continue to be available or may not be adequate to cover any resulting liability. Moreover, insurance against risks such as environmental pollution or other hazards as a result of exploration and production is not generally available to us or to other companies in the mining industry on acceptable terms. We may also become subject to liability for pollution or other hazards which may not be insured against or which we may elect not to insure against because of premium costs or other reasons. Losses from these events may cause us to incur significant costs that could have a material adverse effect upon our financial performance, results of operations and business outlook.

We depend on a number of key personnel, including our directors and executive officers, the loss of any one of whom could have an adverse effect on our operations.

We depend on a number of key personnel, including our directors and executive officers, the loss of any one of whom could have an adverse effect on our operations. We have employment and consulting contracts with several key personnel, and we do not have key man life insurance.

Our ability to manage growth effectively will require us to continue to implement and improve management systems and to recruit and train new employees. We cannot assure you that we will be successful in attracting and retaining skilled and experienced personnel.

Our business is highly dependent on the international market prices of the metals we plan to produce, which are both cyclical and volatile.

Our revenues, if any, are expected to be in large part derived from the mining and sale of vanadium, silver, nickel, coal and other minerals. The prices of those commodities have fluctuated widely, particularly in recent years, and are affected by numerous factors beyond our control including international economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumption patterns, speculative activities and increased production due to new mine developments and improved mining and production methods.

The price of vanadium, silver and coal may have a significant influence on the market price of our securities and the value of our mineral properties. Mineral prices fluctuate widely and are affected by numerous factors beyond our control. The level of interest rates, the rate of inflation, the world supply of mineral commodities and the stability of exchange rates can all cause significant fluctuations in prices. Such external economic factors are in turn influenced by changes in international investment patterns, monetary systems and political developments. The price of mineral commodities has fluctuated widely in recent years, and future price declines could cause commercial production to be impracticable, thereby having a material adverse effect on our business, financial condition and result of operations.

We may be subject to misconduct by third-party contractors.

We will be heavily reliant upon our contractors during the development of large scale projects. Companies are often measured and evaluated by the behavior and performance of their representatives, including in large part their contractors. We work hard to build in controls and mechanisms to choose and retain employees and contractors with similar values to our own; however, these controls may not always be effective. Sound judgment, safe work practices, and ethical behavior is expected from our contractors both on and off-site. Any work disruptions, labor disputes, regulatory breach or irresponsible behavior of our contractors could reflect on us poorly and could lead to loss of social license, delays in production and schedule, unsafe work practices and accidents and reputational harm.

Our business requires substantial capital expenditures and is subject to financing risks.

We estimate that our current financial resources are insufficient to undertake presently planned exploration and development programs. Further exploration and development of our mineral properties may require additional capital. One source of future funds presently available to us is through the sale of equity capital. There is no assurance that this source will continue to be available as required or at all. If it is available, future equity financings may result in substantial dilution to shareholders. Another alternative for the financing of further exploration and/or development would be the offering of an interest in our mineral properties to be earned by another party or parties carrying out further exploration or development thereof. There can be no assurance that we will be able to conclude any such agreements on favorable terms or at all.

Any failure to obtain the required financing on acceptable terms could have a material adverse effect on our financial condition, results of operations and liquidity and may require us to cancel or postpone planned capital investments.

Foreign Operations, Including Emerging and Developing Market Risk

Changes in mining, investment or other applicable policies or shifts in political attitude in Bolivia may adversely affect the Company’s operations or profitability and may affect the Company’s ability to fund its ongoing expenditures. Regardless of the economic viability of the Company’s properties, such political changes, which are beyond the Company’s control, could have a substantive impact and prevent or restrict (or adversely impact the financial results of) mining of some or all of any deposits on the Pulacayo Project.

| 16 |

| Table of Contents |

Bolivia is a mining-friendly jurisdiction with a long history of mining and an experienced labour force. The majority of the Company’s operating costs in relation to Pulacayo Project are denominated in Bolivian boliviano. The Company has not hedged its exposure to any exchange rate fluctuations applicable to its business, and is therefore exposed to currency fluctuation risks. The Company’s operations are also subject to Bolivian regulations pertaining to environmental protection, the use and development of mineral properties and the acquisition or use of rural properties by foreign investors or Bolivian companies under foreign control and various other Bolivian regulatory frameworks, as described below.