UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________

FORM 10-K

__________________________________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________ | |||||

Commission file number 001-41591

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices) | (Zip Code) | ||||

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes o No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | ||||||||

☒ | Smaller reporting company | ||||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ☒

Number of shares of the registrant’s common stock outstanding at March 27, 2024: 39,995,027

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement relating to the 2024 annual meeting of stockholders (the “2024 Proxy Statement”), which will be filed within 120 days of December 31, 2023, are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

| Form 10-K | Item and Description | Page | ||||||

Item 6. [Reserved] | ||||||||

Forward-Looking Statements

All statements, other than statements of historical facts, included in this Annual Report on Form 10-K of Skyward Specialty Insurance Group, Inc. (“Skyward Specialty” or “SKWD”) for the fiscal year ended December 31, 2023 (this “Form 10-K”), or incorporated herein by reference, including, without limitation, statements regarding Skyward Specialty’s future financial position, business strategy, budgets, projected costs, goals and plans and objectives of management for future operations, are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “believe” or “continue” or the negative thereof or variations thereon or similar terminology. Forward-looking statements speak only as the date the statements were made. Although Skyward Specialty believes that the expectations reflected in forward-looking statements have a reasonable basis, it can give no assurance that these expectations will prove to be correct. Forward-looking statements are subject to risks and uncertainties that could cause actual events or results to differ materially from those expressed in or implied by the statements. For a discussion of the most significant risks and uncertainties that could cause Skyward Specialty’s actual results to differ materially from those projected, see “Risk Factors” in Item 1A of this Form 10-K. Except to the limited extent required by applicable law, Skyward Specialty undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Select Insurance and Financial Terms

Gross written premiums

Gross written premiums are the amounts received, or to be received, for insurance policies written or assumed by us during a specific period of time without reduction for policy acquisition costs, reinsurance costs or other deductions. The volume of our gross written premiums in any given period is generally influenced by new business submissions, binding of new business submissions into policies, renewals of existing policies, and average size and premium rate of bound policies.

Ceded written premiums

Ceded written premiums are the amount of gross written premiums ceded to reinsurers. We enter into reinsurance contracts to limit our exposure to potential large losses. Ceded written premiums are earned over the reinsurance contract period in proportion to the period of risk covered. The volume of our ceded written premiums is impacted by the level of our gross written premiums and any decision we make to increase or decrease retention levels, policy limits and co-participation.

Net written premiums

Net written premiums are gross written premiums less ceded written premiums.

Net earned premiums

Net earned premiums represent the earned portion of our net written premiums. Our insurance policies generally have a term of one year and premiums are earned pro rata over the term of the policy.

Commission and fee income

Commission and fee income consists of commissions and fees earned on policies placed with third party insurance companies. In certain instances, the fee income relates to placement of business which is part of our packaged solutions. We recognize commission and fee income on the effective date of the policies.

Net investment gains (losses)

Net investments gains (losses) represent the increase or decrease in the fair value of equity securities and loans still held as investments during the period.

Net realized investment gains (losses)

Net realized investment gains (losses) are a function of the difference between the amount received by us on the sale of a security and the security’s cost basis, mark-to-market adjustments, as well as any credit impairments recognized in earnings.

Losses and LAE

Losses and loss adjustment expenses (“LAE”) represent the costs incurred for insured losses, such as losses under a policy, whether paid or unpaid, as well as expenses of settling claims, including settlements, attorneys’ fees, investigation, appraisal, adjustment, defense costs, and the portion of general expenses allocated to claim resolution. Losses and LAE include a provision for claims that have occurred but have not yet been reported to the insurer. These expenses are a function of the amount and type of insurance contracts we write, and the loss experience associated with the underlying coverage. In general, our losses and LAE are affected by:

•the occurrence, frequency and severity of claims associated with the particular types of insurance contracts that we write;

•the reinsurance agreements we have in place at the time of a loss;

•the mix of business written by us;

•changes in the legal or regulatory environment related to the business we write;

•trends in legal defense costs; and

•inflation in the cost of claims including inflation related to wages, medical costs, building materials and automobile repairs.

Losses and LAE are based on actual paid losses and expenses, as well as an actuarial analysis of the estimated losses, including losses incurred during the period and changes in estimates from prior periods. Losses and LAE may be paid out over a period of years.

Catastrophe losses

We generally define catastrophe losses as any single loss, or group of losses, related to a single Property Claim Services (“PCS” a Verisk company) designated catastrophe event. PCS has defined catastrophes in the United States, Puerto Rico, and the U.S. Virgin Islands as events that cause $25.0 million or more in direct insured losses to property and affect a significant number of policyholders and insurers.

Underwriting, acquisition and insurance expenses

Underwriting, acquisition and insurance expenses include policy acquisition costs and other underwriting and insurance expenses. Policy acquisition costs consist of commissions we pay retail agents and brokers, program administrators, captive managers and third-party administrators, net of ceding commissions we receive from reinsurers on business ceded under certain of our reinsurance contracts. In addition, acquisition expenses include premium-related taxes and other fees. Our policy acquisition costs vary with, and are directly related to, the successful production of new or renewal business. Acquisition expenses related to each policy we write are deferred and amortized to expense in proportion to the premium earned over the term of the policy. Other underwriting and insurance expenses represent the general and administrative expenses of our insurance operations including employee compensation and benefits, and corporate functions such as technology costs, office rent, depreciation and professional service fees including legal, accounting, and actuarial.

Impairment charges

Impairment charges represent reductions in the carrying value of goodwill and intangible assets.

Key Operating and Financial Metrics

We discuss certain key metrics, described below, which provide useful information about our business and the operational factors underlying our financial performance. These metrics are generally standard among insurance companies and help to provide comparability with our peers.

Net retention, expressed as a percentage, is the ratio of net written premiums to gross written premiums.

Underwriting income (loss) is a non-GAAP financial measure defined as income (loss) before income taxes excluding net investment income, net realized and unrealized gains and losses on investments, impairment charges, interest expense, amortization expense and other income and expenses.

Loss and LAE ratio, expressed as a percentage, is the ratio of losses and LAE to net earned premiums.

Expense ratio, expressed as a percentage, is the ratio of underwriting, acquisition and insurance expenses less commission and fee income to net earned premiums.

Combined ratio is the sum of loss ratio and expense ratio. A combined ratio under 100% indicates an underwriting profit. A combined ratio over 100% indicates an underwriting loss.

Adjusted loss and LAE ratio, expressed as a percentage, is a non-GAAP financial measure defined as the ratio of losses and LAE, excluding losses and LAE related to the loss portfolio transfer (“LPT”) and all development on reserves fully or partially covered by the LPT, to net earned premiums.

Adjusted combined ratio is a non-GAAP financial measure defined as the sum of the adjusted loss ratio and the expense ratio.

Adjusted operating income (loss) is a non-GAAP financial measure defined as net income excluding the net impact of the LPT, net realized and unrealized gains or losses on investments, goodwill impairment charges and other income and expenses.

Return on equity is net income as a percentage of average beginning and ending stockholders’ equity.

Adjusted return on equity is a non-GAAP financial measure defined as adjusted operating income as a percentage of average beginning and ending stockholders’ equity.

Tangible stockholders’ equity is a non-GAAP financial measure defined as stockholders’ equity less goodwill and intangible assets.

Return on tangible equity is a non-GAAP financial measure defined as net income as a percentage of average beginning and ending tangible stockholders’ equity during the applicable period.

Adjusted return on tangible equity is a non-GAAP financial measure defined as adjusted operating income as a percentage of average beginning and ending tangible stockholders’ equity during the applicable period.

PART I

Item 1. Business

Who We Are

Skyward Specialty was formed as a Delaware corporation on January 3, 2006 as an insurance holding company. We operated under the name Houston International Insurance Group, Ltd. until we re-branded as Skyward Specialty in November 2020. References to “the Company,” “we,” “our,” “us” or like terms refer to the business of Skyward Specialty Insurance Group, Inc. and its subsidiaries.

We are a growing specialty insurance company delivering commercial property and casualty (P&C) products and solutions on a non-admitted (or E&S) and admitted basis, predominantly in the United States. We focus our business on markets that are underserved, dislocated and/or for which standard insurance coverages are insufficient or inadequate to meet the needs of businesses, including our customers and prospective customers operating in these markets. Our customers typically require highly specialized, customized underwriting solutions and claims capabilities. As such, we develop and deliver tailored insurance products and services to address each of the niche markets we serve.

Our portfolio of insured risks is highly diversified—we insure customers operating in a wide variety of industries; we distribute through multiple channels; we write multiple lines of business, including general liability, excess liability, professional liability (including cyber insurance), commercial auto, group accident and health, property, agriculture, surety and workers’ compensation; we insure both short and medium duration liabilities; and our business mix is balanced between E&S and admitted markets. All of these factors enable us to respond to market opportunities and dislocations by deploying capital where we believe we can consistently earn attractive risk-adjusted returns. We believe this diversification, combined with our underwriting and claims expertise, will produce strong growth and consistent profitability across P&C insurance pricing cycles.

We are led by an entrepreneurial executive management team with decades of insurance leadership experience spanning multiple aspects of the global P&C industry. Our leadership is supported by an experienced team with a broad skill set and aligned around our strategy. We believe our high-quality leadership and underwriting and claims teams, technology DNA, advanced analytics capabilities, diversified book of business, and strong competitive position in each of our chosen market niches position us to continue to profitably grow our business. We aim to deliver long-term value for our shareholders by generating best-in-class underwriting profitability and book value per share growth across P&C market cycles.

All of our insurance company subsidiaries are group rated and have financial strength ratings of “A-” (Excellent) from the A.M. Best Company (“A.M. Best”) with positive outlook.

Our Business and Our Strategy

We have one reportable segment through which we offer a broad array of insurance coverages to a number of market niches. Each of our eight distinct underwriting divisions, or “continuing business,” has dedicated underwriting leadership supported by high-quality technical staff with deep experience in their respective niches. We believe this structure and expertise allow us to serve the needs of our customers effectively and be a value-add partner to our distributors, while earning attractive risk-adjusted returns. For the year ended December 31, 2023, 43% of our gross written premiums were written on an admitted basis and 57% were non-admitted. The year ended 2023 marked a significant underwriting achievement for us as each of our eight underwriting divisions wrote over $100.0 million in gross written premiums.

Our Underwriting Divisions

Accident & Health: Our Accident & Health (“A&H”) underwriting division provides a medical stop loss solution targeting organizations with less than 2,500 employees, as well as group and single-employer captive solutions. Our approach for managing medical costs, combined with our claims oversight, enables us to partner with select distribution partners. We target and serve a segment of the small and medium sized enterprise market that is actively seeking to take control of their healthcare costs by self-insuring a portion of their healthcare insurance. We write these products on an admitted basis and distribute primarily through retail brokers and wholesale broker partners.

Captives: Our Captives underwriting division provides group captive solutions by drawing on our underwriting and claims expertise from other underwriting divisions to create group captives for companies seeking to self-insure. By leveraging our underwriting, claims, technology, and analytical expertise across our Company, we are able to broaden our market reach and write additional profitable business with limited additional expense. Our Captive underwriting division writes group A&H, property, general liability, commercial auto, excess liability, and workers’ compensation lines of business on an E&S and an admitted basis. We often administer this business through partnerships with third-party captive managers.

1

Global Property and Agriculture: Our Global Property underwriting unit provides property-only solutions to large multi-jurisdictional entities with complex property exposures. The business is written entirely on an E&S basis. We distribute this product through retail brokers and select wholesale brokers. Our book and position with our customers and distribution partners has been curated over more than ten years, and we have become an important partner to the brokers that place this business and an equally important part of our insureds’ risk transfer program. Our Global Agriculture underwriting unit provides secondary and reinsurance solutions for crop, livestock and other renewable resources.

Industry Solutions: Our Industry Solutions underwriting division includes three underwriting units that each provide multiple coverages to the businesses they serve: Construction, Energy and Specialty Trucking. Our Construction and Energy underwriting units provide general liability, excess liability, commercial auto, workers’ compensation, and inland marine solutions, written principally on an admitted basis, to a broad range of middle market construction and energy production and servicing customers. Our Specialty Trucking unit writes on an E&S basis commercial auto and general liability solutions to mid-sized intermodal trucking companies. The industry segments we seek to underwrite often have high severity exposures that our teams of skilled and experienced underwriters and claims professionals are able to address quickly and creatively, frequently with multi-line solutions. We distribute these products through retail agents and brokers and a select network of wholesalers.

Professional Lines: Our Professional Lines underwriting division includes three underwriting units: Management Liability, Professional Liability (which includes cyber insurance), and Allied Health. Professional Liability and Allied Health provide E&S primary and excess claims-made liability products distributed exclusively through wholesale brokers, while our Management Liability unit provides both E&S and admitted products distributed through both wholesale and retail brokers.

Programs: Our Programs underwriting division partners with program administrators focused on certain markets that align with our expertise and strategy. We believe partnering with a program administrator in certain circumstances is the optimal way for us to participate profitably or extend our reach in certain markets. Typically, the program administrators possess a competitive advantage (owing to their scale in a particular market niche and/or proprietary technology) that we believe would be difficult for us to replicate on our own. For example, certain of our program administrator partners have developed proprietary technology to optimize risk selection and pricing in specific markets. We believe the combination of our underwriting and claims expertise with their scale and/or technology creates a more powerful partnership than either party could present to the market on its own. Our Programs underwriting division writes property, general liability, commercial auto liability, excess liability, and workers’ compensation lines of business on an E&S and an admitted basis.

Surety: Our Surety underwriting division provides contract, commercial and transactional surety solutions to a range of trade and services organizations requiring bonding. We principally focus on small to medium sized enterprises with aggregate bond programs up to approximately $50.0 million for contract and $75.0 million for commercial and transactional. Our underwriting and claims professionals differentiate themselves through their technical capabilities and decision making speed. We write this business on an admitted basis and distribute through retail agents and brokers.

Transactional E&S: Our Transactional E&S underwriting division provides primary and excess non-catastrophe prone property and general liability solutions, with particular emphasis on risks that are considered hard to place because of the complexity of the underlying exposure, loss history, and/or limited operating history (i.e., start up and newer businesses). Success in our target market is determined by technical underwriting, thoughtful coverage provisions and pricing, and high-quality broker service. We access the market in this division exclusively through wholesale brokers.

In addition to our continuing business, there are business units and lines of business that we previously exited and placed into run-off. We refer to these lines and businesses as our “exited business.”

Our Strategy

We seek to lead in our chosen market niches and establish sustainable competitive positions in these markets. The following key elements underpin our strategy and approach to our business:

1.Providing differentiated products, services and solutions that meet the unique needs of our target markets;

2.Attracting and retaining exceptional underwriting and claims talent and incentivizing our professionals in a manner that aligns with our organization and corporate goals;

3.Amplifying the expertise of our people with advanced technology and analytics that enable superior risk selection, pricing and claims management;

4.Empowering our underwriting and claims teams with considerable authority to make decisions and apply their expertise; and

5.Fostering a culture that promotes nimbleness and responsiveness to market opportunities and dislocation.

2

We refer to this strategy as “Rule Our Niche” and it forms the basis of our approach to building a strong defensible market position, creating a competitive moat, and winning in our chosen markets. We believe that the principles underlying our strategy are key to achieving and sustaining best-in-class underwriting results through P&C insurance pricing cycles. We consistently strive for excellence in risk selection, pricing, and claims outcomes, and to amplify these critical functions with the use of advanced technology and analytics.

Our Competitive Strengths

We believe that our competitive strengths include:

Focus on profitable niches of the market that require technical underwriting and claims management as barriers to entry.

We believe that the niche areas of the commercial lines P&C markets we have selected are a highly attractive subset of the P&C insurance market and present an opportunity to generate attractive risk-adjusted returns. We actively target markets that are underserved, dislocated or for which standard, commoditized products are insufficient or inadequate to meet the needs of our customers. The unique characteristics of the risks within our core markets require each account to be efficiently and individually underwritten, in order for us to generate an acceptable, sustainable underwriting profit. Many carriers have chosen to reject businesses that they deem to be too complex, or that requires thoughtful individual underwriting; or, alternatively, have focused on simple account risks for which more automated underwriting can be effective. Instead, we have chosen to build our underwriting divisions around deeply experienced underwriters who we empower with appropriate authority to make underwriting decisions. This structure enables us to offer innovative and unique products and solutions to our distribution partners and customers, regardless of how challenging or complex a risk may be. Further, we augment our underwriters’ experience with data and predictive analytics that are intended to differentiate risk selection and pricing decision-making while enhancing efficiency.

Highly skilled underwriters.

We focus on hiring underwriting and technical staff who help differentiate our company through their expertise and experience. Our underwriting teams are knowledgeable, experienced, and empowered — characteristics which are critical to operate successfully in the markets we serve, especially since many of the risks we underwrite are particularly difficult to automate. We do not impose strict underwriting rules (i.e., we are not “box” underwriters), but rather allow our professionals the freedom to use their expertise and judgment when evaluating and pricing risks. Simply put, we give our people the tools and appropriate authority to make decisions and do what they do best — profitably underwrite complex risks.

Superior Claims Staff and Operations.

We have cultivated a best-in-class and highly specialized team of claims professionals who are highly knowledgeable about the niches we serve and the lines of business we write. Our claims professionals systematically address first party claims with fair and equitable solutions and third-party claims with holistic and comprehensive responses, in each case seeking to ensure consistent and early loss recognition of indemnity and loss adjustment expenses (“LAE”).

We respond quickly when a claim is submitted with specialized adjusters, who are armed with expertise, advanced technology and analytics, to assist them in the claims resolution process. We embed technology deeply into our claims process and leverage our technology-enabled platform and tools from first notice of loss to investigation to settlement. Our analytics capabilities used by our senior leadership and claims teams include real-time, detailed information on open claims and benchmarks against closed claims. We believe that our industry expertise, nimble culture, and technology-embedded claims processes enables us to reach fair and appropriate claims outcomes for our customers.

Superior business intelligence platform.

SkyBI, our business intelligence platform, focuses on providing our senior leadership, as well as our technical teams, with real-time intelligence to drive superior decision making. SkyBI reflects the best practices our management team has learned from its extensive experience across the P&C insurance and technology sectors. We developed SkyBI, our single, comprehensive enterprise-wide data repository, as our foundation for reporting, business intelligence, analytics, and other advanced data capabilities. It provides our organization information and performance metrics across the Company in an easy-to-consume visualized format. The data can be filtered by many categories, including distributor, customer segment, line of business, specific industry, individual underwriter, and specific risk feature among others. SkyBI aids in establishing clear line of sight to objectives as well as facilitating our decision-making processes.

Advanced technology and new risk data for underwriting and claims.

We fundamentally believe that every underwriting and claims decision can be augmented with the use of new types of risk data and advanced technology. While our underwriting decisions are backed by reliable historical data and in-depth

3

evaluation of risks resulting from intentional investment in data collection and processing capabilities, we amplify our underwriting and claims prowess by combining this data with new forms of risk data and predictive analytics.

Diversified business that allows us to respond to, and capitalize on, changes in market conditions across P&C cycles.

We have been successful in building a diversified group of underwriting divisions spanning multiple product lines, industries, geographies and distribution channels. We aim to evolve with, and adapt to, the market growing certain lines of business when market conditions are favorable and limiting our exposure to certain markets when conditions are less favorable. We believe the diversity of our book allows us to respond to, and capitalize on, market opportunities and dislocations across P&C insurance market and pricing cycles resulting in a durable insurance franchise.

Attractive and winning culture.

As evidenced by our internal surveys, public information such as that available on Glassdoor and LinkedIn, and our selection as a “Best Places to Work in Insurance,” we have built a distinctive winning culture. Key to our culture and operating approach is a flat structure of communication and decision-making. We trust our staff to make decisions that produce or exceed our desired financial results, and we support our staff with a clear system of measurement to gauge performance. We have chosen to adopt a hybrid work schedule which provides our employees with the flexibility for remote working. We pride ourselves on maintaining an entrepreneurial environment that encourages and rewards a proactive approach to capitalize on market disruption. This environment is not only consistent with our identity as a specialty insurer but also a foundation for our success in attracting great talent and our objective of delivering best-in-class results.

High-quality, experienced leadership team that is aligned with our shareholders.

Led by our CEO, Andrew Robinson, we have an experienced, innovative and entrepreneurial executive leadership team with a track record of success in senior management roles at industry leading property and casualty companies as well as in starting and building new businesses in our industry.

Our entire senior leadership’s compensation is directly aligned with our shareholders. Each of our leaders have a material portion of their compensation in the form of long-term and short-term incentives tied to delivering sustainable, best-in-class underwriting returns. Our executive leadership team have additional long-term incentive targets tied directly to growth in book value per share.

Our Strategy in Action

With everything we do, from recruiting to marketing to underwriting to loss adjusting and claims resolution, we seek to follow the core tenets of our “Rule Our Niche” strategy, as described above. We believe our “Rule Our Niche” strategy will help us achieve our goal of generating best-in-class underwriting profitability for our niches while creating superior long-term shareholder value through growth in book value per share. The core tenets of our “Rule Our Niche” strategy include:

Attract and retain blue-chip underwriting and claims talent to expand and enhance our market position.

We seek to hire the most talented technical underwriting professionals who have long-standing industry relationships with distribution partners and claims professionals with expertise in the niches we write. These relationships are key to getting steady access to our preferred business. We believe that we have become a company of choice for the best talent in our industry and, as such, we will continue to grow our market position by bringing on world-class talent in our chosen markets.

Leverage our technology DNA to further distance ourselves from the competition.

We have demonstrated a differentiated ability to utilize new forms of risk data and advanced technology within the more complex, higher severity risk categories of the specialty P&C insurance market. SkyBI gives us the ability to promptly sense and quickly respond to market changes, while our core operating platforms allow us to move into new markets efficiently and without the complexity of burdensome systems. We believe our technological advantage positions us for profitable growth and expansion into additional specialty market niches where we can establish a strong and defensible market position.

Profitably grow existing lines of business and expand with new underwriting divisions.

We believe we are well-positioned to take advantage of several trends impacting our customers in the United States and globally. One such trend is the continued rise in demand for specialized insurance solutions because of increasing risks, as well as the complexity of risks, due to climate change/increased frequency of severe weather events, supply chain uncertainty, financial inflation risk, cyber risk, emergence of novel health risks, increased level of litigation, attorney involvement and jury awards, and healthcare delivery and cost. Another such noticeable market trend is the emergence of

4

“micro cycles and micro dislocations” where different pockets of the P&C insurance market experience hardening and softening at different times. We have demonstrated our ability to react quickly in response to these trends by launching new underwriting units, entering underserved markets, partnering with others with advanced technology, and launching new captive solutions. We believe our gross written premium growth and profitability is indicative of our momentum and provides a powerful reference for the positioning of our Company to continue to expand and grow in the markets we seek to serve.

Differentiate on daily excellence to drive best-in-class underwriting performance.

We believe that our ability to meet our long-term goals, including achieving best-in-class underwriting returns and growth in book value per share, relies on how well we execute our day-to-day operations across all of our functional departments, including but not limited to underwriting, product management, and claims management. SkyBI provides the foundation by which our senior management can monitor our performance, whether it is renewal rates, new business pricing and portfolio performance for an individual underwriter, or claims aging and reserving practices and outcomes by claims adjusters. Our focus on the fundamentals that drive underwriting excellence is at the center of our strategy. Furthermore, our cross functional collaboration ensures that our underwriting, claims, actuarial and product management teams regularly review performance and trends so that portfolio, pricing and coverage changes can be implemented quickly.

Use our balance sheet to capture a larger part of the market we serve.

We are committed to establishing and maintaining a strong balance sheet, starting with conservative loss reserves and strong capitalization ratios. We believe this is imperative to maintain the confidence of customers, distribution partners, reinsurers, regulators, rating agencies and shareholders. We have strengthened our claims case reserves practices with the aim to reserve to the expected ultimate loss within 90 days of the first notice of loss. In addition, we increase the level of IBNR reserves held above our claims case reserves. We believe our conservative reserve philosophy positions us well for consistently strong underwriting profitability in the future.

Marketing and Distribution

Our approach to marketing and distribution mirrors our approach to underwriting and is a key facet of our “Rule Our Niche” strategy. Our underwriting teams, as well as the Company as a whole, have strong and well-established relationships with our distribution partners and equally strong reputations that provide a foundation to establish affiliations with new distribution partners. We believe we win with distribution partners because of our deep expertise in niche markets, high caliber underwriters, culture of innovation, thoughtful product line-up and product design, and speed and quality of responsiveness, among other factors. All of our underwriting divisions invest meaningful time and effort into sustaining and expanding distribution partner loyalty and long-term relationships.

Just as we tailor underwriting to the individual needs of the insureds, we tailor our choice of distribution partners to access the particular business we seek to write. Accordingly, we distribute our products, through retail agents, wholesale brokers, select program administrators, and captive managers. This approach allows us to access the business we target effectively and efficiently based on the needs and dynamics of a particular market niche.

Underwriting

Our approach to underwriting is deeply embedded in our “Rule Our Niche” strategy and is core to how we win in the market. Within the eight divisions, we further specialize underwriting teams with a focus on specific niches within the markets the eight divisions serve. Kirby Hill, our President of Industry Solutions, Captives and Programs underwriting divisions, has more than 30 years of experience spanning multiple facets of the insurance business, John Burkhart, our President of Specialty Lines overseeing the Professional Lines, Surety, Transactional E&S and A&H underwriting divisions, has approximately 30 years of underwriting experience, and Doug Davies, our Senior Vice President of the Global Property and Agriculture Underwriting Division, has approximately 20 years of underwriting experience.

Our underwriting approach is underpinned by hiring highly experienced, best-in-class and diverse teams of technical underwriters with established track records in specific specialty niche markets. We then amplify our underwriters’ skill sets with advanced technology and data analytics and empower them with appropriate authority to make decisions. We believe this approach is key to superior risk selection and pricing, and producing sustainable best-in-class underwriting results across market cycles.

We strive to augment the capabilities and experience of our underwriting professionals using new forms of data and analytics for risk selection and pricing. Our underwriting data is captured in our business intelligence platform, SkyBI. This comprehensive data repository forms the foundation of our reporting, analytics, and other data capabilities and is a key tool for our senior management team and business leaders. See the section entitled “Technology” below for more information on SkyBI.

5

We are highly selective in the policies we choose to bind. If our underwriters cannot reasonably expect to bind coverage at the combination of premium and coverage terms that meets our standard, we encourage them to move on quickly to other prospective opportunities.

When accepting risks, we are careful to establish terms and price that are suited to the underlying exposure. When writing in the admitted market, we endeavor to ensure that our approved forms and filed rates are appropriate and adequate for the risks we are accepting while also allowing us the flexibility to address specific and/or unique exposures. When writing in the E&S market, we use our freedom of rate and form to ensure risk and coverage are appropriate to the unique needs and exposure that are presented in this market. We endeavor to craft policies that offer affordable and appropriate protection to address our insureds’ exposures while also constructing coverage such that potential losses are more predictable and claims cost can be best managed.

Underwriting teams are supported by active engagement and collaboration with our Claims, Actuarial, Product Management, Legal and Compliance and Finance departments so that trends in the business, legal and tort developments, and competitor and regulatory actions are analyzed, shared, and acted upon in a timely manner. We view our underwriters as the center of our company and all support functions are incented and measured to support the achievement of our underwriting profitability targets. This structure serves to surface both opportunities and issues early and forms a key part of our nimbleness and ability to take advantage of market disruptions. Finally, our underwriting controls and procedures are regularly reviewed to ensure our underwriters are acting with clear line of sight to profitably underwrite each of the markets we serve.

Claims Management

Skyward’s claims department is guided by the following principles: (1) prompt and comprehensive claim investigations, considering all aspects of each loss, and using advanced analytics and technology to improve efficiency, accuracy and speed of response; (2) providing our customers with quality claims handling service while engaging customers through the entire claims resolution process; (3) promptly establishing reserves reflective of our best estimate of ultimate loss; (4) effectively pursuing contribution and subrogation where appropriate and warranted; (5) detecting and preventing fraud activity throughout the claims handling process using a variety of tools; and (6) disciplined litigation management to provide our customers with a superior legal defense while closely monitoring legal costs. To this end, we provide continuous training to our claim staff on claim evaluation, strategy, litigation management, good-faith claims handling and best practices. Our ultimate goal is to achieve timely and optimal claim outcomes.

We handle the majority of our claims in-house. In certain instances, we utilize Third Party Administrators (TPAs), to handle claims on Skyward’s behalf, when needed. Specifically, we may utilize TPAs for programs, captives, occupational accident, workers compensation and Loss Portfolio Transfer (LPT) runoff claims. We actively manage and oversee our TPAs and monitor their individual claims-handling activities, to be in accordance with our claims handling and reserving guidelines and general best practices. We regularly audit our TPAs to ensure compliance with these guidelines and practices.

When the retention of counsel is warranted for a liability claim made against an insured, we retain independent legal counsel to defend and represent an insured. We select defense counsel based on their geographical location and expertise to ensure that they have the requisite experience and legal knowledge to defend our insureds effectively and efficiently. We have developed carefully crafted litigation guidelines for both our claims professionals and our outside counsel to follow. Adherence to these guidelines ensures that counsel is providing the appropriate defense to our insureds. Finally, to ensure that legal costs are reasonable, and customary within the respective defense counsel’s geography and practice area, we employ a legal spend management solution to analyze legal invoices for adherence to case handling and billing practice standards.

We are leveraging technology to gain efficiencies in the claims-handling process. For example, we launched a technology solution to speed up the process of creating claims correspondence and to automate routine tasks behind the scenes, such as vendor payments. Similarly, we are piloting the use of artificial intelligence to route claims to the best-suited claims handler based on likely severity. We are also developing a Large Language Model to identify claims with early indicators for potential severity, unusual types of exposures or the propensity for legal representation by third party claimants.

Additionally, we are always looking for opportunities to resolve our claims as efficiently and effectively as possible. For example, for commercial auto, we have implemented a “quick strike” program to respond to claim reports. This program involves deploying experienced investigators and other appropriate vendors to the scene of a reported auto accident, ideally within two hours of the accident, regardless of the location. This quick response assists us in evaluating the facts and circumstances of the accident to begin our investigation as quickly as possible. If appropriate, our program aids us in resolving any third-party claims as quickly as possible.

6

Finally, our claims handlers and managers are organized by line of business to ensure that the right expertise is brought to bear in handling claims. The managers and adjusters work very closely with their underwriting partners to keep them apprised of legal trends and emerging claims issues of note. The goal is to educate our underwriters on emerging areas of loss experience to assist them in their risk selection processes.

Technology

Our technology is at the heart of everything we do and every decision we make, helping us to win over the long-term. We deploy technology across our organization to drive competitive advantages in three primary functional ways:

1.Superior Business Intelligence Platform. SkyBI, our business intelligence platform, focuses on providing our senior leadership, as well as our technical teams, with real-time intelligence to drive superior decision making. SkyBI reflects the best practices our management team has learned from its extensive experience across the P&C insurance and technology sectors. We developed SkyBI, our single, comprehensive enterprise-wide data repository, as our foundation for reporting, business intelligence, analytics, and other advanced data capabilities. It provides our organization information and performance metrics across the Company in an easy-to-consume visualized format. The data can be filtered by many categories, including distributor, customer segment, line of business, specific industry, individual underwriter, and specific risk feature among others. SkyBI aids in establishing clear line of sight to objectives as well as facilitating our decision-making process.

2.Predictive Analytics Technology. We strive to augment the capabilities of our employees daily using new forms of risk data and the use of predictive analytics including artificial intelligence for risk selection, pricing and claims handling. Within every underwriting division, our actions are intentional to “Rule Our Niche.” We aim to innovate constantly, and our actions are specific to each of the divisions/markets we serve.

3.Core Transactional Platforms. Our core operating platforms, including our policy administration, billing and claims systems, are intentionally designed to enable nimble scaling and expansion of our business. We generally use, third-party vendor developed core operating applications that we have customized for our company. Our core platform organization is used for all business except for Accident & Health, Global Property and Surety as the unique features of these underwriting divisions require select dedicated core processing components. Data gathered from our core operating platforms from all divisions flows to our SkyBI platform with comparable data quality and granularity regardless of underwriting division.

Our use of advanced technology for underwriting and claims, SkyBI and core operating platforms provide our business with a flywheel effect allowing our underwriters to better select risk, our claims professionals to better adjudicate claims, our unit leaders to better communicate with reinsurance and third-party partners, and our senior leadership team to better evaluate trends in our business. These tools also have the added advantage of allowing us to communicate with our distribution partners, reinsurers, and other third-party partners more accurately, effectively, and efficiently.

Like other companies, we face external threats to our information technology systems, including the possibility of system failure, attempts to steal our customer data, and ransomware attacks. We designed our technology infrastructure to function through almost any major disruption. We replicate our data in real time to a third-party cloud disaster recovery site for use in the event of a major system failure. We also back-up our data daily for system restoration if needed. Additional actions we take to prevent disruptions to our systems and data include: actively monitoring Cybersecurity and Infrastructure Security Agency’s (CISA) cybersecurity directives, taking immediate action on any vulnerability identified in a directive; conducting monthly vulnerability scans on all network attached devices, at all locations, with patching applied whenever needed; requiring two-factor authentication for access to any of our systems; conducting monthly security training for all employees; implementing endpoint detection agents for threat detection and response; performing desktop scenarios to practice responses to breaches involving our cybersecurity insurance partners and retained security consultants; and performing annual penetration testing. We constantly review our security breach posture and regularly implement updated processes, best practices and tools.

Reinsurance

We strategically purchase reinsurance from third parties which enhances our business by protecting capital from severity events (either large single event losses or catastrophes) and reducing volatility in our earnings. Our reinsurance contracts are predominantly one year in length and renew annually throughout the year, primarily in January and June. At each annual renewal, we consider several factors that influence any changes to our reinsurance purchases, including any plans to change the underlying insurance coverage we offer, updated loss activity, the level of our capital and surplus, changes in our risk appetite and the cost and availability of reinsurance treaties.

7

We purchase quota share reinsurance, excess of loss reinsurance, and facultative reinsurance coverage to limit our exposure from losses on any one occurrence. The mix of reinsurance purchased considers efficiency, cost, our risk appetite and specific factors of the underlying risks we underwrite.

•Quota share reinsurance refers to a reinsurance contract whereby the reinsurer agrees to assume a specified percentage of the ceding company’s losses arising out of a defined class of business in exchange for a corresponding percentage of premiums, net of a ceding commission.

•Excess of loss reinsurance refers to a reinsurance contract whereby the reinsurer agrees to assume all or a portion of the ceding company’s losses for an individual claim or an event in excess of a specified amount in exchange for a premium payable amount negotiated between the parties, which includes our catastrophe reinsurance program.

•Facultative coverage refers to a reinsurance contract on individual risks as opposed to a group or class of business. It is used for a variety of reasons, including supplementing the limits provided by the treaty coverage or covering risks or perils excluded from treaty reinsurance.

The following is a summary of our reinsurance programs as of December 31, 2023:

| Line of Business | Maximum Company Retention | |||||||

| Accident & Health | $0.88 million per occurrence | |||||||

Commercial Auto(1) | $1.0 million per occurrence | |||||||

| Cyber | $2.69 million per occurrence | |||||||

Excess Casualty(1)(2) | $1.24 million per occurrence | |||||||

General Liability(1) | $1.25 million per occurrence | |||||||

Professional Lines(2) | $2.7 million per occurrence | |||||||

Property(3) | $2.8 million per occurrence | |||||||

| Representation and Warranty | $2.5 million per occurrence | |||||||

Surety(2) | $3.0 million per occurrence | |||||||

Workers’ Compensation(2) | $2.33 million per occurrence | |||||||

(1) Legal defense expenses can force exposure above the maximum company retention for Excess Casualty, Commercial Auto and General Liability. | ||||||||

(2) Reinsurance is subject to a loss ratio cap or aggregate level of loss cover that exceeds a modeled 1:250-year PML event. | ||||||||

(3) Catastrophe loss protection is purchased up to $28.0 million in excess of $12.0 million retention, which provides cover for a 1:250-year PML event. | ||||||||

For the year ended December 31, 2023, property insurance represented 27% of our gross written premiums. We actively manage and continuously monitor our aggregation of property writings by geographic area to limit our potential for aggregation of loss resulting from severe events such as hurricanes, convective storms, and earthquakes. We buy catastrophe reinsurance to further mitigate an aggregation of property losses due to a single event or series of events. To inform our purchase of catastrophe reinsurance, we use third-party stochastic and our own deterministic models to analyze the risk of aggregation of losses from such events. These models provide a quantitative view of PML events, which is an estimate of the level of loss we would expect to experience once in a given number of years (referred to as the return period). Based upon our modeling, it would take an event beyond our 1 in 250-year PML to exhaust our $28.0 million property catastrophe coverage. Additionally, we seek to expose no more than 3.0% of our stockholders’ equity to a catastrophic loss that is less than a 1 in 250-year event. We believe our current reinsurance program provides coverage well in excess of our theoretical losses from any recorded historical event.

In addition to our reinsurance programs for our continuing business, during 2020, we entered into a LPT retroactive reinsurance agreement with a third-party reinsurer domiciled in Bermuda for liabilities (including claim payments, allocated losses and LAE reserves and certain extra-contractual obligations) related to certain policies issued or assumed for policy years 2017 and prior so as to limit the volatility associated with the business written during those years. For additional information about the LPT, see Item 7 of this Form 10-K, “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Results of Operations - Losses and LAE.”

We seek to purchase reinsurance from reinsurers that are rated at least “A-” (“Excellent”) or better by A.M. Best. As of December 31, 2023, 99% of our reinsurance recoverables were either derived from reinsurers rated “A-” (Excellent) by A.M. Best, or better, or were collateralized for our reinsurance recoverable by the reinsurer. While we only select reinsurers whom we believe to have acceptable credit and A.M. Best ratings, if our reinsurers are unable to pay the claims for which they are responsible, we ultimately retain primary liability to our policyholders. Hence, failure of the reinsurer to honor its obligations could result in losses to us, and therefore, we establish allowances for amounts considered uncollectible. At December 31, 2023 and 2022, our allowance for uncollectible reinsurance was $2.3 million and $0.0 million, respectively.

8

The following table sets forth our most significant reinsurers by amount of reinsurance recoverables, as well as the reinsurers A.M. Best rating, if applicable, as of December 31, 2023:

| ($ in thousands) | ||||||||||||||

| Reinsurer | Reinsurance Recoverables | AM Best Rating | ||||||||||||

| Everest Reinsurance Co. | $ | 121,832 | A+ | |||||||||||

eCaptive PC1-IC (and PC2-IC), Inc(1) | 121,805 | Unrated | ||||||||||||

| RGA Reinsurance Company | 37,070 | A+ | ||||||||||||

| Partner Reinsurance Co. of the US | 23,381 | A+ | ||||||||||||

| Swiss Reinsurance America Corp | 22,334 | A+ | ||||||||||||

| General Reinsurance Corp | 21,548 | A++ | ||||||||||||

Randall & Quilter (R&Q Bermuda (SAC) Ltd)(2) | 20,859 | Unrated | ||||||||||||

| ACE (Chubb Property & Casualty Insurance Company) | 16,003 | A+ | ||||||||||||

| Aspen Insurance UK Limited | 14,822 | A | ||||||||||||

| Munich Reinsurance America Inc. | 14,817 | A+ | ||||||||||||

| Top 10 Total | 414,471 | |||||||||||||

| All Others | 181,863 | |||||||||||||

| Total | $ | 596,334 | ||||||||||||

(1) This reinsurer facilitates our eMaxx captive; we hold collateral in a statutory trust of $150.8 million on our reinsurance recoverables | ||||||||||||||

(2) This reinsurer facilitates our LPT reinsurance agreement; we maintain the right of offset of our recoverables for premiums we owe to the reinsurer, we held collateral in a statutory trust of $23.0 million on our net reinsurance recoverables. | ||||||||||||||

Enterprise Risk Management

Our enterprise risk management (“ERM”) is embedded in nearly every aspect of our company and guides our day-to-day activities. At the highest level, our approach to ERM is to ensure we achieve an acceptable risk adjusted return for our shareholders; as such we are intentional in our underwriting and asset portfolio construction. As an example, we aim to balance liability duration of our underwriting portfolio, and we use reinsurance to manage volatility from a single loss and for cumulative losses tied to a single event or series of events. Our investment strategy is similarly set out to have a diversified target portfolio that balances portfolio yield, liquidity, volatility, and potential for principal loss.

Our Chief Risk Officer oversees several critical ERM processes as well as chairing our cross-functional corporate ERM Committee. We formalize our own view of risk and solvency in terms of potential economic loss using our Economic Capital Model (“ECM”). We use the output of our ECM to measure potential earnings and capital loss for a range of scenarios. These outputs are measured against risk tolerances that are set out and updated annually by the ERM Committee and discussed with the Risk Committee of our Board. More specifically, our ECM provides a probabilistic modeled view of earnings and capital loss that brings together the potential loss from catastrophes, reserving, underwriting, market, credit risk, strategic and operational risks.

Aside from maintaining our ECM and overseeing our risk tolerance framework, our Chief Risk Officer works with our ERM Committee to review and maintain a comprehensive risk register with accountabilities to ensure appropriate mitigations are in place and are monitored for any change. The top 10 risks are further identified and quantified by the Chief Risk Officer and the ERM Committee and reviewed every quarter. The Chief Risk Officer and the ERM Committee submit these reports to the Risk Committee on a regular basis.

We construct our operational processes and controls with a view to identify, assess and manage key risks on an ongoing basis. For example, our Underwriting Committee is responsible for overseeing changes in risk appetite, and product line and division expansion. Within Claims, we diligently monitor our claims handling practices against guidelines through regular internal audits, conduct monthly large loss reviews, and maintain and monitor a watchlist of potential high severity claims. Within Actuarial, we perform quarterly reserve studies, and our Reserve Committee meets each quarter to review and respond to trends in loss emergence. Any key observations are subsequently discussed with the CEO. Monthly and quarterly our underwriting divisions assess rate change and retention on existing business, new business quality and pricing adequacy, and loss emergence as compared to expected. Our SkyBI platform provides real-time portfolio, underwriting, claims and actuarial analytics which is critical to ensuring that the above processes achieve the desired outcome.

Altogether, our ERM is at the center of our decision making and our day-to-day activities. It is a central component to our strategy to achieve market leading risk adjusted returns for our shareholders.

9

Reserves

We maintain reserves for specific claims incurred and reported, IBNR reserves and reserves for uncollectible reinsurance when appropriate. Our ultimate liability may be greater or less than the current reserves. In the insurance industry, there is always the risk that reserves may prove inadequate. We continually monitor reserves using new information on reported claims and a variety of statistical analyses. Anticipated inflation is reflected implicitly in the reserving process through analysis of cost trends and the review of historical development. We do not discount our reserves for losses and LAE to reflect estimated present value.

When a claim is reported, we establish a case reserve for the estimated amount of the ultimate payment after an appropriate assessment of coverage, damages and other investigation as applicable. The estimate is based on our reserving practices and on the claims adjuster’s experience and knowledge of the nature and value of the specific type of claim. Case reserves are revised periodically based on subsequent developments associated with each claim. See the section entitled “Claims Management” included in this Item 1 for more information.

We establish IBNR reserves in accordance with industry practice to provide for (i) the estimated amount of future loss payments on incurred claims not yet reported, and (ii) potential development on reported claims. IBNR reserves are estimated based on generally accepted actuarial reserving techniques that take into account quantitative loss experience data and, where appropriate, qualitative factors.

We regularly review our loss reserves using a variety of actuarial techniques. We also update the reserve estimates as historical loss experience develops, additional claims are reported and/or settled and new information becomes available. A reserve can be increased or decreased over time as claims move towards settlement, which can impact earnings in the form of either adverse development or reserve releases. For additional information regarding our loss reserves, see Item 7 of this Form 10-K, “Management’s Discussion and Analysis of Financial Condition and Results of Operations - “Results of Operations - Losses and LAE” and “Critical Accounting Policies.”

Investments

We seek to maintain a balanced investment portfolio predominantly composed of investments that generate predictable and stable returns, augmented by select strategic investments that generate attractive risk-adjusted returns. Our investment allocation strategy utilizes an Enterprise Based Asset Allocation model. This model, which is embedded in our Economic Capital Model (see ERM discussion included in this Item 1), allows us to understand the impact of our investment allocation decisions on our capital, liquidity and risk profile across a range of market scenarios.

We actively manage and monitor our investment risk to balance the goals of stable growth and liquidity with our need to comply with the insurance regulatory and rating agency frameworks within which we operate. Our portfolio is mainly comprised of cash and cash equivalents and investment-grade fixed-maturity securities, supplemented by additional investments that fit our risk appetite.

The Investment Committee of our Board of Directors reviews and approves our investment policy and strategy. This committee meets on a regular basis to review and consider investment activities, tactics, and new investment opportunities as they arise. The portfolio is directed internally and includes both self-managed investments and portfolios managed by select third-party investment management firms.

Our opportunistic fixed income portfolio is managed by Arena Investors, LP (“Arena”), which is affiliated with The Westaim Corporation (“Westaim”), the Company’s largest shareholder.

For additional discussion regarding our investments, including the market risks related to our investment portfolio, see Item 7 of this Form 10-K, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Investments.”

Competition

The specialty lines property & casualty insurance market consists of many markets and sub-markets. Each market is characterized by distinct customer needs and product and services to meet those needs, and specific economic and structural features. We face competition in our underwriting divisions from other specialty and standard insurers as well as program administrators. Competition is based on many factors including pricing of coverage, the general reputation and perceived financial strength of the company, relationships with brokers, terms and conditions of products offered, ratings assigned by independent rating agencies, speed of claims payment and reputation, and the experience and reputation of the members of the underwriting and claims teams. Given the diversity of our underwriting divisions, our competition is broad and certain competitors may be specific to only a subset of our divisions. Some of our notable competitors include: Markel Corporation; W.R. Berkley Corporation; American Financial Group Inc.; Tokio Marine Holdings, Inc.; CNA Financial

10

Corporation; Hiscox, Ltd.; RLI Corp.; Intact Finance Corporation; Kinsale Capital Group, Inc.; and James River Group Holdings, Ltd.

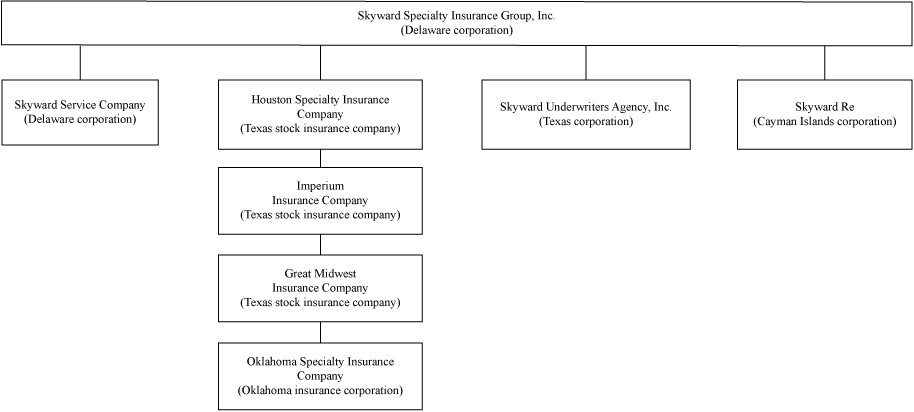

Our Structure

We conduct our operations principally through four insurance companies: Houston Specialty Insurance Company (“HSIC”), our largest insurance subsidiary, underwrites multiple lines of insurance on a surplus lines basis in 50 states, the District of Columbia and select foreign countries. Imperium Insurance Company (“IIC”), a subsidiary of HSIC, underwrites on an admitted basis in all 50 states and the District of Columbia. Great Midwest Insurance Company (“GMIC”), a subsidiary of IIC underwrites multiple lines of insurance on an admitted basis in all 50 states, the District of Columbia and is a certified surety bond company listed with the Department of the Treasury. Oklahoma Specialty Insurance Company (“OSIC”), a subsidiary of GMIC, is an approved surplus lines company in 49 states and the District of Columbia.

The following table sets forth the geographic distribution of our gross written premiums for the year ended December 31, 2023:

| 2023 | ||||||||

| Texas | 11.4 | % | ||||||

| California | 9.0 | |||||||

| New York | 8.7 | |||||||

| Louisiana | 8.0 | |||||||

| Florida | 7.3 | |||||||

| Pennsylvania | 3.4 | |||||||

| New Jersey | 3.4 | |||||||

| Georgia | 3.3 | |||||||

| Illinois | 3.2 | |||||||

| Massachusetts | 2.4 | |||||||

| All other states | 39.9 | |||||||

| Total | 100.0 | % | ||||||

In addition to our primary insurance companies, we also own Skyward Re, a wholly-owned captive reinsurance company domiciled in the Cayman Islands that was incorporated on January 7, 2020. Skyward Re was established to facilitate the LPT. For additional information about the LPT, see Item 7 of this Form 10-K, “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Results of Operations - Loss and LAE.” We also operate two non-insurance companies: Skyward Underwriters Agency, Inc., a licensed agent, managing general agent and reinsurance broker, and Skyward Service Company, which provides various administrative services to our subsidiaries.

11

Our organizational structure is set forth below. Each entity is wholly-owned by its immediate parent:

Ratings

Our insurance group, Skyward Specialty Insurance Group, Inc. currently has a rating of “A-” (Excellent) with positive outlook from A.M. Best, which rates insurance companies based on factors of concern to policyholders. A.M. Best currently assigns 16 ratings to insurance companies, which currently range from “A++” (Superior) to “F” (In Liquidation). The “A-” (Excellent) rating is the fourth highest rating. In evaluating a company’s financial and operating performance, A.M. Best reviews a company’s profitability, leverage, and liquidity, as well as its book of business, the adequacy and soundness of its reinsurance, the quality and estimated market value of its assets, the adequacy of its losses and loss expense reserves, the adequacy of its surplus, its capital structure, the experience and competence of its management and its market presence. A.M. Best’s ratings reflect its opinion of an insurance company’s financial strength, operating performance, and ability to meet its obligations to policyholders. These ratings are based on factors relevant to policyholders, agents, insurance brokers and intermediaries and are not specifically related to securities issued by the company.

Regulation

Insurance Regulation

We are regulated by insurance regulatory authorities in the states in which we conduct business. State insurance laws and regulations generally are designed to protect the interests of policyholders, consumers and claimants rather than stockholders or other investors. The nature and extent of state regulation varies by jurisdiction, and state insurance regulators generally have broad administrative power relating to, among other matters, setting capital and surplus requirements, licensing of insurers and insurance producers, review and approval of product forms and rates, establishing standards for reserve adequacy, prescribing statutory accounting methods and the form and content of statutory financial reports, regulating certain transactions with affiliates and prescribing types and amounts of investments.

Regulation of insurance companies constantly changes as governmental agencies and legislatures react to real or perceived issues. In recent years, the state insurance regulatory framework has come under increased federal scrutiny, and some state legislatures have considered or enacted laws that alter and, in many cases, increase, state authority to regulate insurance companies and insurance holding company systems. Further, the National Association of Insurance Commissioners (“NAIC”) and some state insurance regulators are re-examining existing laws and regulations specifically focusing on issues relating to the solvency of insurance companies, interpretations of existing laws and the development of new laws. Although the federal government does not directly regulate the business of insurance, federal initiatives often affect the insurance industry in a variety of ways. In addition, the Federal Insurance Office (the “FIO”) was established within the U.S. Department of the Treasury by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) in July 2010. The FIO monitors all aspects of the insurance industry, including identifying issues or gaps in the regulation of insurers that could contribute to a systemic crisis in the insurance industry or the U.S. financial system, although the FIO has no express regulatory authority over insurance companies or other insurance industry participants.

12

Insurance Holding Company Regulation

We operate as an insurance holding company system and are subject to the insurance holding company laws of the State of Texas, the state in which our primary insurance companies are domiciled, as well as those of Oklahoma. These statutes require that each insurance company in the system register with the insurance department of its state of domicile and furnish information concerning the operations of companies within the holding company system that may materially affect the operations, management or financial condition of the insurers within the system and domiciled in that state. These statutes also provide that all transactions among members of a holding company system must be fair and reasonable. Transactions between insurance subsidiaries and their parents and affiliates generally must be disclosed to the state regulators, and notice to or prior approval of the applicable state insurance regulator generally is required for any material or extraordinary transaction.

Intellectual Property

We have applied for various trademark registrations in the United States at both federal and state levels. We will pursue additional trademark registrations and other intellectual property protection to the extent we believe it would be beneficial and cost effective.

In addition, we monitor our trademarks and service marks and protect them from unauthorized use as necessary.

Employees and Human Capital

As of December 31, 2023, we had approximately 515 employees. Our employees are not subject to any collective bargaining agreement, and we are not aware of any current efforts to implement such an agreement. We believe we have good working relations with our employees. We aim to be an employer of choice, and not just for insurance. As such, we strive to create a culture committed to fostering a rich diversity of thought, background and perspective.

Diversity, Equity and Inclusion

We embrace diversity, equity and inclusion initiatives as a way to improve workplace culture and demonstrate the importance of valuing our employees as people, not just as workers. We strive to cultivate an exceptional workforce to perpetuate our ownership culture and continue to achieve superior business results. Our goal is to attract, develop and retain the best talent from diverse backgrounds, while promoting a culture where different viewpoints are valued and individuals feel respected, are treated fairly and have an opportunity to excel in their chosen careers.

Compensation and Benefits

We offer and maintain a competitive benefits package designed to support the well-being of our employees, including, but not limited to, medical, dental and vision insurance, a 401(k) plan, paid time off, family leave, employee assistance programs as well as an employee stock purchase plan available to all employees. We also emphasize the training and development of our employees and provide opportunities to further their education and professional development. We know that we cannot win at our business unless we first win with our people.

Item 1A. Risk Factors

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this report, including our consolidated financial statements and related notes, as well as in our other filings with the SEC, in evaluating our business and before investing in our common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that are not expressly stated, that we are unaware of, or that we currently believe are not material, may also become important factors that affect us. If any of the following risks occur, our business, operating results, financial condition and prospects could be materially harmed. In that event, the price of our common stock could decline, and you could lose part or all of your investment.

Summary of Material Risk Factors

Our business is subject to numerous risks and uncertainties of which you should be aware. Among others, these risks relate to:

•our financial condition and results of operations could be materially adversely affected if we do not accurately assess our underwriting risk;

•competition for business in our industry is intense;

•because our business depends on insurance retail agents and brokers, wholesalers and program administrators, we are exposed to certain risks arising out of our reliance on these distribution channels that could adversely affect our results;

13

•we may be unable to purchase third-party reinsurance in amounts we desire on commercially acceptable terms or on terms that adequately protect us, and this inability may materially adversely affect our business, financial condition and results of operations;

•our losses and loss expense reserves may be inadequate to cover our actual losses, which could have a material adverse effect on our financial condition, results of operations and cash flows;

•a decline in our financial strength rating may adversely affect the amount of business we write;

•unexpected changes in the interpretation of our coverage or provisions, including loss limitations and exclusions, in our policies could have a material adverse effect on our financial condition and results of operations;

•our reinsurers may not reimburse us for claims on a timely basis, or at all, which may materially adversely affect our business, financial condition and results of operations;

•our failure to accurately and timely pay claims could materially and adversely affect our business, financial condition, results of operations, and prospects;