UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

or

For the Transition Period from _____ to _____

Commission

File Number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) | |

| Registrant’s telephone number, including area code: |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol | Name of exchange on which registered | ||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐

Yes ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Act.

☐

Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant

to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐

Yes

As

of June 30, 2023, the aggregate market value of the registrant’s Class A common stock held by non-affiliates of the registrant

was approximately $

As of March 26, 2024, there were outstanding shares of Class A common stock, $2.00 par value per share, and shares of Class C common stock, $2.00 par value per share.

Documents Incorporated by Reference

Security National Financial Corporation

Form 10-K

For the Fiscal Year Ended December 31, 2023

TABLE OF CONTENTS

| 2 |

PART I

Item 1. Business

Security National Financial Corporation (the “Company”) operates in three reportable business segments: life insurance, cemetery and mortuary, and mortgages. The life insurance segment is engaged in the business of selling and servicing selected lines of life insurance, annuity products, and accident and health insurance. These products are marketed in 40 states through a commissioned sales force of independent licensed insurance agents who may also sell insurance products of other companies. The cemetery and mortuary segment consists of eight mortuaries and five cemeteries in the state of Utah, one cemetery in the state of California, and one cemetery and four mortuaries in the state of New Mexico. The Company also engages in pre-need selling of funeral, cemetery, mortuary, and cremation services through its cemetery and mortuary locations. The mortgage segment originates and underwrites or otherwise purchases residential and commercial loans for new construction, existing homes, and other real estate projects. The mortgage segment operates through 100 retail offices in 23 states and is an approved mortgage lender in several other states.

The Company’s design and structure are that each business segment is related to the other business segments and contributes to the profitability of the other segments. The Company’s cemetery and mortuary segment provides a level of public awareness that assists in the sales and marketing of insurance and pre-need cemetery and funeral products. The Company’s insurance segment invests its assets (including, in part, pre-need funeral products and services) in investments authorized by the respective insurance departments of their states of domicile. The Company also pursues growth through acquisitions. The Company’s mortgage segment provides mortgage loans and other real estate investment opportunities.

The Company was organized as a holding company in 1979 when Security National Life Insurance Company (“Security National Life”) became a wholly owned subsidiary of the Company, and the former stockholders of Security National Life became stockholders of the Company. Security National Life was formed in 1965 and has acquired or purchased significant blocks of business which include Capital Investors Life Insurance Company (1994), Civil Service Employees Life Insurance Company (1995), Southern Security Life Insurance Company (1998), Menlo Life Insurance Company (1999), Acadian Life Insurance Company (2002), Paramount Security Life Insurance Company (2004), Memorial Insurance Company of America (2005 and subsequently sold in 2021 to FOXO Life Insurance Company), Capital Reserve Life Insurance Company (2007), Southern Security Life Insurance Company, Inc. (2008), North America Life Insurance Company (2011, 2015), Trans-Western Life Insurance Company (2012), Mothe Life Insurance Company (2012), DLE Life Insurance Company (2012), American Republic Insurance Company (2015), First Guaranty Insurance Company (2016), Kilpatrick Life Insurance Company (2019), and merger with FOXO Life Insurance Company (2023).

The cemetery and mortuary operations have also grown through the acquisition of other cemetery and mortuary companies. The cemetery and mortuary companies that the Company has acquired are Holladay Memorial Park, Inc. (1991), Cottonwood Mortuary, Inc. (1991), Deseret Memorial, Inc. (1991), Probst Family Funerals and Cremations L.L.C. (2019), Heber Valley Funeral Home, Inc. (2019), Rivera Funerals, Cremations and Memorial Gardens (2021), and Holbrook Mortuary (2021).

In 1993, the Company formed SecurityNational Mortgage Company (“SecurityNational Mortgage”) to originate and refinance residential mortgage loans.

See Note 15 of the Notes to Consolidated Financial Statements for additional information regarding the business segments of the Company.

Life Insurance

Products

The Company, through Security National Life, First Guaranty Insurance Company (“First Guaranty”), and Kilpatrick Life Insurance Company (“Kilpatrick”), issues and distributes selected lines of life insurance and annuities. The Company’s life insurance business includes funeral plans and interest-sensitive life insurance, as well as other traditional life, accident, and health insurance products. The Company places specific marketing emphasis on funeral plans through pre-need planning. The Company’s insurance subsidiaries, Southern Security Life Insurance Company, Inc. (“Southern Security”) and Trans-Western Life Insurance Company (“Trans-Western”), do not actively write policies, but service and maintain policies that were purchased prior to their acquisition by Security National Life.

| 3 |

A funeral plan is a small face value life insurance policy that generally has face coverage of up to $30,000. The Company believes that funeral plans represent a marketing niche that has less competition because most insurance companies do not offer similar coverage. The purpose of the funeral plan policy is to pay the costs and expenses incurred at the time of a person’s death. On a per thousand-dollar cost of insurance basis, these policies can be more expensive to the policyholder than many types of non-burial insurance due to their low face amount, requiring the fixed cost of the policy administration to be distributed over a smaller policy size, and the simplified underwriting practices that result in higher mortality costs.

Markets and Distribution

The Company is licensed to sell insurance in 40 states. The Company, in marketing its life insurance products, seeks to locate, develop and service specific niche markets. The Company’s funeral plan policies are sold primarily to people who range in age from 45 to 85 and have low to moderate income. Most of the Company’s funeral plan premiums come from the states of Arkansas, California, Florida, Georgia, Louisiana, Mississippi, Texas, and Utah.

The Company sells its life insurance products through direct agents, brokers, and independent licensed agents who may also sell insurance products of other companies. The commissions on life insurance products range from approximately 50% to 120% of first year premiums. In those cases where the Company utilizes its direct agents in selling such policies, those agents customarily receive advances against future commissions.

In some instances, funeral plan insurance is marketed in conjunction with the Company’s cemetery and mortuary sales force. When it is marketed by that group, the beneficiary is usually the Company’s cemeteries and mortuaries. Thus, death benefits that become payable under the policy are paid to the Company’s cemetery and mortuary subsidiaries to the extent of services performed and products purchased.

In marketing funeral plan insurance, the Company also seeks and obtains third-party endorsements from other cemeteries and mortuaries within its marketing areas. Typically, these cemeteries and mortuaries will provide letters of endorsement and may share in mailing and other lead-generating costs since these businesses are usually made the beneficiary of the policy. The following table summarizes the life insurance business for the five years ended December 31, 2023:

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Life Insurance | ||||||||||||||||||||

| Policy/Cert Count as of December 31 | 714,953 | 646,296 | 653,450 | 659,237 | 669,064 | |||||||||||||||

| Insurance in force as of December 31 (in thousands) | $ | 3,552,554 | $ | 3,446,836 | (1) | $ | 3,415,368 | (1) | $ | 3,379,921 | (1) | $ | 3,303,061 | (1) | ||||||

| Premiums Collected (in thousands) | $ | 113,584 | $ | 103,304 | $ | 99,006 | $ | 92,058 | $ | 78,253 | ||||||||||

(1) Prior years have been adjusted to include accidental death benefit insurance in force that was inadvertently excluded.

| 4 |

Underwriting

The factors considered in evaluating an application for ordinary life insurance coverage can include the applicant’s age, occupation, general health condition, and medical history. Upon receipt of a satisfactory (non-funeral plan insurance) application, which contains pertinent medical questions, the Company issues insurance based upon its medical limits and requirements subject to the following general non-medical limits:

| Age Nearest Birthday |

Non-Medical Limits |

|

| 0-50 | $100,000 | |

| 51-up | Medical information | |

| required (APS or exam) |

When underwriting life insurance, the Company will sometimes issue policies with higher premium rates for substandard risks.

The Company’s funeral plan insurance is written on a simplified medical application with underwriting requirements being a completed application, a phone interview of the applicant, and an intelliscript prescription history inquiry. There are several underwriting classes in which an applicant can be placed.

Annuities

Products

The Company’s annuity business includes single premium deferred annuities, flexible premium deferred annuities, and immediate annuities. A single premium deferred annuity is a contract where the individual remits a sum of money to the Company, which is retained on deposit until such time as the individual may wish to annuitize or surrender the contract for cash. A flexible premium deferred annuity gives the contract holder the right to make premium payments of varying amounts or to make no further premium payments after his initial payment. These single and flexible premium deferred annuities can have initial surrender charges. The surrender charges act as a deterrent to individuals who may wish to prematurely surrender their annuity contracts. An immediate annuity is a contract in which the individual remits a sum of money to the Company in return for the Company’s obligation to pay a series of payments on a periodic basis over a designated period, such as an individual’s life, or for such other period as may be designated.

Annuities have guaranteed interest rates that range from 1% to 6.5% per annum. Rates above the guaranteed interest rate credited are periodically modified by the Board of Directors at its discretion. For the Company to make a profit on an annuity product, the Company must maintain an interest rate spread between its investment income and the interest rate credited to the annuities. Commissions, issuance expenses, and general and administrative expenses are deducted from this interest rate spread.

Markets and Distribution

The general market for the Company’s annuities is middle to older age individuals. A major source of annuity sales come from direct agents and are sold in conjunction with other insurance sales. If an individual does not qualify for a funeral plan, the agent will often sell that individual an annuity to fund final expenses.

The following table summarizes the annuity business for the five years ended December 31, 2023:

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Annuities Policy/Cert Count as of December 31 | 24,924 | 24,225 | 24,901 | 25,476 | 26,565 | |||||||||||||||

| Deposits Collected (in thousands) | $ | 10,946 | $ | 9,972 | $ | 9,719 | $ | 9,637 | $ | 10,400 | ||||||||||

| 5 |

Accident and Health

Products

Through its various acquisitions, the Company occasionally acquires small blocks of accident and health insurance policies, which it continues to service. The Company offers a low-cost comprehensive diver’s accident insurance policy that provides worldwide coverage for medical expense reimbursement in the event of a diving accident.

Markets and Distribution

The Company currently markets its diver’s accident insurance policies through the internet.

The following table summarizes the accident and health insurance business for the five years ended December 31, 2023:

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Accident and Health Policy/Cert Count as of December 31 | 9,379 | 11,132 | 12,494 | 13,735 | 15,133 | |||||||||||||||

| Premiums Collected (in thousands) | $ | 216 | $ | 543 | $ | 353 | $ | 296 | $ | 110 | ||||||||||

Reinsurance

The primary purpose of reinsurance is to enable an insurance company to issue an insurance policy in an amount larger than the risk the insurance company is willing to assume for itself. The insurance company remains obligated for the amounts reinsured (ceded) in the event the reinsurers do not meet their obligations.

The Company currently cedes and assumes certain risks with various authorized unaffiliated reinsurers pursuant to reinsurance treaties, which are generally renewed annually. The premiums paid by the Company are based on a number of factors, primarily including the age of the insured and the risk ceded to the reinsurer.

It is the Company’s policy to retain no more than $100,000 of ordinary insurance per insured life, with the excess risk being reinsured. The total policy amount of life insurance reinsured by other companies as of December 31, 2023, was $333,211,000, which represented approximately 9.3% of the Company’s total life insurance policy amount in force on that date.

See “Management’s Discussion and Analysis of Results of Operations and Financial Condition” and “Notes to Consolidated Financial Statements” for additional disclosure and discussion regarding reinsurance.

Investments

The investments that support the Company’s life insurance and annuity obligations are determined by the investment committees of the Company’s subsidiaries and ratified by the full boards of directors of the respective subsidiaries. A significant portion of the Company’s investments must meet statutory requirements governing the nature and quality of permitted investments by its insurance subsidiaries. The Company maintains a diversified investment portfolio consisting of common stocks, preferred stocks, municipal bonds, corporate bonds, mortgage loans, real estate, and other securities and investments.

See “Management’s Discussion and Analysis of Results of Operations and Financial Condition” and “Notes to Consolidated Financial Statements” for additional disclosure and discussion regarding investments.

| 6 |

Cemetery and Mortuary

Products

Through its cemetery and mortuary segment, the Company markets a variety of products and services both on a pre-need basis (prior to death) and an at-need basis (at the time of death). The products include plots, interment vaults, mausoleum crypts, markers, caskets, urns, and other death care related products. These services include professional services of funeral directors, opening and closing of graves, use of chapels and viewing rooms, and use of automobiles and clothing. The Company has a mortuary at each of its cemeteries, other than Holladay Memorial Park and Singing Hills Memorial Park, and has six separate stand-alone mortuary facilities.

Markets and Distribution

The Company’s pre-need cemetery and mortuary sales are marketed to persons of all ages but are generally purchased by persons 45 years of age and older. The Company is limited in its geographic distribution of these products to areas lying within an approximate 20-mile radius of its mortuaries and cemeteries. The Company’s at-need sales are similarly limited in geographic area.

The Company actively seeks to sell its cemetery and funeral products to customers on a pre-need basis. The Company employs cemetery sales representatives on a commission basis to sell these products. Many of these pre-need cemetery and mortuary sales representatives are also licensed insurance salesmen and sell funeral plan insurance. In some instances, the Company’s cemetery and mortuary facilities are the named beneficiaries of the funeral plan policies.

Potential customers are located via telephone sales prospecting, responses to letters mailed by the pre-planning consultants, billboards and other outside advertising, referrals, and door-to-door canvassing. The Company trains its sales representatives and helps generate leads for them.

Mortgage Loans

Products

The Company, through SecurityNational Mortgage, is active in the residential real estate market. SecurityNational Mortgage is approved by the U.S. Department of Housing and Urban Development (HUD), the Federal National Mortgage Association (Fannie Mae), and other secondary market investors, to originate a variety of residential mortgage loan products, which are subsequently sold to investors. The Company uses internal and external funding sources to fund mortgage loans.

Security National Life originates and funds commercial real estate loans, residential construction loans, and land development loans for internal investment.

Markets and Distribution

The Company’s residential mortgage lending services are marketed primarily to real estate brokers, builders and directly to consumers. The Company has a strong retail origination presence in the Utah, Florida, Texas, Nevada and Arizona markets and many other states across the country. See “Management’s Discussion and Analysis of Results of Operations and Financial Condition” and “Notes to Consolidated Financial Statements” for additional disclosure and discussion regarding mortgage loans.

Recent Acquisitions and Other Business Activities

Real Estate Development

The Company is capitalizing on the opportunity to develop commercial and residential assets on its existing and recently acquired properties. The cost to acquire existing for-sale assets currently exceeds the replacement costs, thus creating the opportunity for development and redevelopment of the land that the Company currently owns. The Company has developed, or is in the process of developing, assets that have an initial development cost exceeding $100,000,000, primarily relating to the Center53 Development and multiple single family residential development projects. The Company plans to continue its development endeavors as based upon its assessment of the market demand.

| 7 |

Center53 Development

Center53 Development is an office development project comprising nearly 20 acres of land that is currently owned by the Company in the central valley of Salt Lake City. At final completion, the multi-year, phased development is expected to create a campus atmosphere and include nearly one million square-feet of office space in five buildings, ranging from four to eleven stories, and will be serviced by three parking structures with approximately 4,000 stalls. In 2015, the Company broke ground and commenced development on the first phase which included a six-story building of nearly 200,000 square feet and a parking garage with 748 parking stalls. The first phase of the project was completed in July 2017 and is currently 93% leased. The second phase of the project began in March 2020 and includes a second six-story building of nearly 221,000 square feet and a parking garage with approximately 870 stalls. The Company began its occupancy of a portion of the building in October 2021 and the remainder of the building is currently 100% leased. The Company plans to initiate future phases of the Center53 Development for additional Class A office space in the central valley of Salt Lake City.

Regulation

The Company’s insurance subsidiaries are subject to comprehensive regulation in the jurisdictions in which they do business under statutes and regulations administered by state insurance commissioners. Such regulation relates to, among other things, prior approval of the acquisition of a controlling interest in an insurance company; standards of solvency which must be met and maintained; licensing of insurers and their agents; nature of and limitations on investments; deposits of securities for the benefit of policyholders; approval of policy forms and premium rates; periodic examinations of the affairs of insurance companies; annual and other reports required to be filed on the financial condition of insurers or for other purposes; and requirements regarding aggregate reserves for life policies and annuity contracts, policy claims, unearned premiums, and other matters. The Company’s insurance subsidiaries are subject to this type of regulation in any state in which they conduct relevant business. Such regulation may cause unforeseen costs and operational restrictions, and delay implementation of the Company’s business plans.

The Company’s life insurance subsidiaries are currently subject to regulation in Utah, Louisiana, Mississippi and Texas under insurance holding company legislation, and other states where applicable. Generally, intercompany transfers of assets and dividend payments from insurance subsidiaries are subject to prior notice of approval from the relevant state insurance department where they are deemed “extraordinary” under relevant state law. The insurance subsidiaries are required, under state insurance laws, to file detailed annual reports with the supervisory agencies in each of the states in which they do business. Their business and accounts are also subject to examination by these agencies. The Company was last examined in 2021 (First Guaranty Insurance), 2022 (Security National Life, Southern Security and Trans-Western) and 2021 (Kilpatrick Life). Its most recent final examination reports have been approved by the insurance departments and are public records.

The Texas Department of Banking also audits pre-need insurance policies that are issued in the state of Texas. Pre-need policies include the life and annuity products sold as the funding mechanism for funeral plans through funeral homes by Security National agents. The Company is required to send the Texas Department of Banking an annual report that summarizes the number of policies in force and the face amount or death benefit for each policy. This annual report is also required to indicate the number of new policies issued for that year, all death claims paid that year, and all premiums received.

The Company’s cemetery and mortuary subsidiaries are subject to the Federal Trade Commission’s comprehensive funeral industry rules and to state regulations in the various states where such operations are domiciled. The morticians must be licensed by the respective state in which they provide their services. Similarly, the mortuaries and cemeteries are governed and licensed by state statutes and city ordinances in Utah, California, and New Mexico. The subsidiaries are required to keep annual reports on file including financial information concerning the number of spaces sold and, where applicable, funds provided to the Endowment Care Trust Fund. Licenses are issued annually based on such reports. The cemeteries maintain city or county licenses where they conduct business.

The Company’s mortgage subsidiaries are subject to the rules and regulations of the U.S. Department of Housing and Urban Development (HUD), and to various state licensing acts and regulations and the Consumer Financial Protection Bureau (CFPB). These regulations, among other things, specify minimum capital requirements; procedures for loan origination and underwriting, licensing of brokers and loan officers and quality review audits and specify the fees that can be charged to borrowers. Each year, the Company is required to have an audit completed for each mortgage subsidiary by an independent registered public accounting firm to verify compliance with the relevant regulations. In addition to the government regulations, the Company must meet loan requirements, and underwriting guidelines of various investors who purchase the loans.

| 8 |

Income Taxes

The Company’s insurance subsidiaries, Security National Life, First Guaranty and Kilpatrick are taxed under the Life Insurance Company Tax Act of 1984. Under the act, life insurance companies are taxed at standard corporate rates on life insurance company taxable income. Life insurance company taxable income is gross income less general business deductions and reserves for future policyholder benefits (with modifications). Under The Tax Cuts and Jobs Act (the “Tax Act”), December 31, 2017 policyholder surplus account balances result in taxable income over a period of eight years.

Security National Life, First Guaranty and Kilpatrick calculate their life insurance taxable income after establishing a provision representing a portion of the costs of acquisition of such life insurance business. The effect of the provision is that a certain percentage of the Company’s premium income is characterized as deferred expenses and recognized over a five or ten-year period. The Tax Act changed this recognition period for amounts deferred after December 31, 2017 to a five or fifteen-year period.

The Company’s non-life insurance company subsidiaries are taxed in general under the regular corporate tax provisions. The Company’s subsidiaries Southern Security and Trans-Western are regulated as life insurance companies but do not meet the Internal Revenue Code definition of a life insurance company, so they are taxed as insurance companies other than life insurance companies.

Competition

The life insurance industry is highly competitive. There are approximately 800 legal reserve life insurance companies in business in the United States. These insurance companies differentiate themselves through marketing techniques, product features, pricing, and customer service. The Company’s insurance subsidiaries compete with a large number of insurance companies, many of which have greater financial resources, longer business histories, and more diversified lines of insurance products than the Company. In addition, such companies generally have larger sales forces. Further, the Company competes with mutual insurance companies which may have a competitive advantage because all profits accrue to policyholders. Because the Company is smaller by industry standards and lacks broad diversification of risk, it may be more vulnerable to losses than larger, better-established companies. The Company believes that its policies and rates for the markets it serves are generally competitive.

The cemetery and mortuary industry is highly competitive. In the Utah, California, and New Mexico markets where the Company competes, there are several cemeteries and mortuaries which have longer business histories, more established positions in the community, and stronger financial positions than the Company. In addition, some of the cemeteries with which the Company must compete for sales are owned by municipalities and, as a result, can offer lower prices than can the Company. The Company bears the cost of a pre-need sales program that is not incurred by those competitors which do not have a pre-need sales force. The Company believes that its products and prices are generally competitive with those in the industry.

The mortgage industry is highly competitive with many mortgage companies and banks in the same geographic area in which the Company is operating. The mortgage industry in general is sensitive to changes in interest rates and the refinancing market is particularly vulnerable to changes in interest rates.

Seasonality

The Company’s business is generally not subject to seasonal fluctuations.

| 9 |

Human Capital Management

As of December 31, 2023, the Company employed 1,227 full-time and 246 part-time employees. Of the full-time employees, 729 were employed by the mortgage segment, 373 by the life insurance segment, and 125 by the cemetery and mortuary segment. The Company requires monthly acknowledgement of its anti-discrimination and anti-harassment policies and communicates to its employees how to report concerns that relate to their employment experience.

Employee Benefits

All eligible employees may elect coverage under the Company’s group health (including health savings and flexible spending), retirement, supplemental life and voluntary benefit programs. As of December 31, 2023, 756 employees had elected to participate in the Company’s group health insurance plans.

The Company has an employee safe harbor retirement plan for each business segment. The retirement plans qualify under section 401(k) of the Internal Revenue Code and, if approved by the board of directors, the Company makes a matching contribution in Company stock based on the employee’s contribution amount.

The Company provides other time off benefits such as paid sick and paid vacation time. The Company provides discounts on certain services provided by the Company to its employees. Additionally, the Company offers an employee assistance program that provides 24/7 counseling services for employees who may be facing challenges outside of the workplace.

Available Information

The Company’s internet address is www.securitynational.com. The Company’s investor relations website is www.investor.securitynational.com and the Company promptly makes available on this website, free of charge, the reports that it files or furnishes with the Securities and Exchange Commission.

Item 1A. Risk Factors

As a smaller reporting company, the Company is not required to provide information typically disclosed under this item.

Item 1B. Unresolved Staff Comments

None. As a smaller reporting company, the Company is not required to provide information typically disclosed under this item.

Item 1C. Cybersecurity

The Company maintains a strong information security program and systems (“Cybersecurity System”) to guard against unauthorized access, malicious software, corruption of data, disruption of its networks and systems and unauthorized release of confidential information. The Company’s Cybersecurity System is comprised of multiple layers of controls to reduce the risk of cybersecurity incidents.

Risk Management and Strategy

The Company’s Cybersecurity System includes administrative, technical, and physical safeguards and is designed to provide an appropriate level of protection to maintain the confidentiality, integrity and availability of the Company’s and its customers’ information. This includes protecting against known and evolving threats to the security of the Company’s systems and information, and against unauthorized access, compromise, or loss of data. The Cybersecurity System is managed centrally, so the same security controls, policies and procedures are implemented across the organization. The Company maintains cybersecurity policies including an Acceptable Use Policy that all system users sign to acknowledge that they understand their security responsibilities. All system users receive security awareness training which includes phishing attack simulation testing.

| 10 |

A key element of the Company’s Cybersecurity System is to mature the program to align with the Center for Internet Security (CIS) Critical Security Controls security framework. The CIS controls are designed based on real-world data about cyber-attacks, to ensure that the measures are effective against current threats. The framework provides a prioritized set of actions, which enables the Company to focus its efforts on the most effective defensive measures first. This prioritization helps in optimizing the use of resources for maximum impact on security. This strategy provides a structured and effective approach to cybersecurity, helping the Company to protect its assets, comply with regulations, manage risks, and improve its overall security posture.

The Company maintains cyber insurance coverage that may, subject to policy terms, conditions, and limitations, cover certain aspects of cybersecurity risks; however, such insurance coverage may be unavailable or insufficient to cover all losses or all types of claims that may arise in the continually evolving area of cyber risk.

Governance

The Company has established controls and procedures to escalate enterprise-level issues, including cybersecurity matters, to the appropriate management levels within its organization and to its Board of Directors, or members or committees thereof, as appropriate. The Company’s Board of Directors has oversight for enterprise risk management, including its approach to managing cybersecurity risk, and has delegated oversight responsibility of information security risks to its Audit Committee. Matters determined to present potential material impacts to the Company’s financial results, operations, and/or reputation are reported by management to the Company’s Board of Directors or its Audit Committee, as appropriate, in accordance with its escalation framework.

In addition, the Company has established procedures to ensure that management personnel are informed in a timely manner of known cybersecurity risks and incidents that may materially impact the Company’s operations and that timely public disclosure is made as appropriate. The Company’s Cybersecurity System is led by the Chief Information Officer (“CIO”) in collaboration with a third-party virtual Chief Information Security Officer (“vCISO”) and other third-party cybersecurity service providers which in turn assist in monitoring the Company’s exposure from significant information technology suppliers, significant software as service providers and major vendors with access to the Company’s information technology systems. The Company’s CIO has 10 years of cybersecurity industry experience. Further, team members who support the Company’s cybersecurity program have relevant educational and industry experience through various roles involving information technology, security, auditing, compliance, systems, and programming, as well as cybersecurity certifications such as a Certified Information Systems Security Professional (CISSP) and Certified Information Security Manager (CISM). During the last three years, the Company has not experienced a material security breach and, as a result, the Company has not incurred any material expenses from such a breach. Furthermore, during such time, the Company has not been penalized or paid any amount under any information security breach settlement.

| 11 |

Item 2. Properties

The tables below set forth the location of the Company’s office facilities and certain other information relating to these properties.

| Street | City | State | Function | Owned / Leased | Approximate Square Footage | Lease Amount |

Expiration | ||||||||||||

| 433 Ascension Way, Floors 4, 5 and 6 | Salt Lake City | UT | Corporate Headquarters, Insurance Operations, Cemetery and Mortuary Operations, Mortgage Operations and Sales | Owned | 221,000 | N/A | N/A | ||||||||||||

| 1044 River Oaks Dr. (1) | Flowood | MS | Insurance Operations | Owned | 5,522 | N/A | N/A | ||||||||||||

| 1818 Marshall St. | Shreveport | LA | Insurance Operations | Owned | 12,274 | N/A | N/A | ||||||||||||

| 812 Sheppard St. | Minden | LA | Insurance Sales | Owned | 1,560 | N/A | N/A | ||||||||||||

| 909 Foisy Ave. (2) | Alexandria | LA | Insurance Sales | Owned | 8,059 | N/A | N/A | ||||||||||||

| 1550 N. Third St. (1) | Jena | LA | Insurance Sales | Owned | 1,737 | N/A | N/A | ||||||||||||

| 1 Sanctuary Blvd. Suite 302A | Mandeville | LA | Insurance Sales | Leased | 1,335 | $ | 2,400 | / | mo | 6/30/2024 | |||||||||

| 79 E. Main Street | Midway | UT | Funeral Service Sales | Leased | 4,476 | $ | 6,233 | / | mo | 10/31/2025 | |||||||||

| 4387 S. 500 W. | Salt Lake City | UT | Funeral Service Sales | Leased | 2,168 | $ | 1,895 | / | mo | 7/31/2025 | |||||||||

| 1627A Central Ave. | Los Alamos | NM | Funeral Service Sales | Leased | 1,400 | $ | 1,600 | / | mo | 12/30/2024 | |||||||||

| 200 Market Way | Rainbow City | AL | Fast Funding Operations | Leased | 12,850 | $ | 10,490 | / | mo | 1/31/2025 | |||||||||

| 5100 N. 99th Ave., Suite 101/103 | Phoenix | AZ | Mortgage Sales | Sub-Leased | 3,940 | $ | 3,369 | / | mo | month to month | |||||||||

| 10609 N. Hayden Rd., Suite 100 | Scottsdale | AZ | Mortgage Sales | Leased | 3,585 | $ | 8,650 | / | mo | month to month | |||||||||

| 1490 S. Price Road, Suite 318 | Chandler | AZ | Mortgage Sales | Leased | 1,600 | $ | 3,050 | / | mo | 6/30/2024 | |||||||||

| 5100 N. 99th Ave., Suite 111 | Phoenix | AZ | Mortgage Sales | Sub-Leased | 720 | $ | 2,382 | / | mo | month to month | |||||||||

| 1951 West Camelback Rd, Ste 200 | Phoenix | AZ | Mortgage Sales | Leased | 2,446 | $ | 3,771 | / | mo | month to month | |||||||||

| 2636 Hwy 95 Suite 2 | Bullhead City | AZ | Mortgage Sales | Leased | 1,000 | $ | 1,225 | / | mo | month to month | |||||||||

| 2220 S. Country Club Drive Suite 101 | Mesa | AZ | Mortgage Sales | Leased | 3,274 | $ | 5,339 | / | mo | 2/14/2028 | |||||||||

| 350 West 16th Street #209 | Yum | AZ | Mortgage Sales | Leased | 1,731 | $ | 4,284 | / | mo | 6/30/2024 | |||||||||

| 102 North Cortez St. | Prescott | AZ | Mortgage Sales | Leased | 100 | $ | 600 | / | mo | month to month | |||||||||

| 15169 North Scottsdale Road, #205 - office 3012 & 3013 | Scottsdale | AZ | Mortgage Sales | Leased | Unknown | $ | 3,400 | / | mo | month to month | |||||||||

| 10265 W. Camelback Road, #100 | Phoenix | AZ | Mortgage Sales | Leased | 1,647 | $ | 3,817 | / | mo | 2/27/2024 | |||||||||

| 40977 Oak Dr. | Forest Falls | CA | Mortgage Sales | Leased | 250 | $ | - | / | mo | month to month | |||||||||

| 2934 E. Garvey Ave. South, Suite 250 | West Covina | CA | Mortgage Sales | Leased | 500 | $ | 1,100 | / | mo | month to month | |||||||||

| 7398 Fox Trail Unit B | Yucca Valley | CA | Mortgage Sales | Leased | 900 | $ | 550 | / | mo | month to month | |||||||||

| 155 S. Highway 101 Suite 7 | Solana Beach | CA | Mortgage Sales | Leased | 2,000 | $ | 7,426 | / | mo | 7/31/2026 | |||||||||

| 44441 West 16th Street #101 | Lancaster | CA | Mortgage Sales | Leased | 2,115 | $ | 2,057 | / | mo | 1/31/2024 | |||||||||

| 1420 Magnolia Ave | Oxnard | CA | Mortgage Sales | Leased | 100 | $ | 6,392 | / | mo | 3/30/2024 | |||||||||

| 625 The City Drive, Suite 450 | Orange | CA | Mortgage Sales | Leased | 2,485 | $ | 6,655 | / | mo | 12/31/2024 | |||||||||

| 27 Main St., Suite C-104B | Edwards | CO | Mortgage Sales | Leased | 680 | $ | 1,950 | / | mo | month to month | |||||||||

| 4501 Mohawk Dr. | Larkspur | CO | Mortgage Sales | Leased | 250 | $ | 50 | / | mo | month to month | |||||||||

| 7800 E. Union Ave., Suite 550 | Denver | CO | Mortgage Sales | Sub-Leased | 4,656 | $ | 11,640 | / | mo | 2/28/2026 | |||||||||

| 5982 s Zeno Ct | Aurora | CO | Mortgage Sales | Leased | 50 | $ | - | / | mo | month to month | |||||||||

| 5475 Tech Center Drive #201-A | Colorado Springs | CO | Mortgage Sales | Leased | 790 | $ | 1,218 | / | mo | 9/30/2024 | |||||||||

| 1145 Town Park Ave., Suite 2215 | Lake Mary | FL | Mortgage Sales | Leased | 5,901 | $ | 12,294 | / | mo | 2/29/2024 | |||||||||

| 8191 College Parkway, Suite 201 | Ft Myers | FL | Mortgage Sales | Leased | 4,676 | $ | 4,505 | / | mo | 8/21/2024 | |||||||||

| 2350 Fruitville Rd Ste, Ste 101 | Sarasota | FL | Mortgage Sales | Leased | 2,455 | $ | 5,266 | / | mo | 3/14/2026 | |||||||||

| 921 Club House Blvd, New Smyrna Beach, | FL | Mortgage Sales | Leased | 50 | $ | - | / | mo | month to month | ||||||||||

| 9123 N. Military Trail, #104B | Palm Beach Gardens | FL | Mortgage Sales | Leased | 150 | $ | 800 | / | mo | month to month | |||||||||

| 970 Island Grove Drive | Deland | FL | Mortgage Sales | Leased | 100 | $ | - | / | mo | month to month | |||||||||

| 10293 61st Ct N | Pinellas Park | FL | Mortgage Sales | Leased | 100 | $ | - | / | mo | month to month | |||||||||

| 5666 Seminole Blvd, Suite 106 & 111 | Seminole | FL | Mortgage Sales | Leased | 210 | $ | 1,170 | / | mo | 7/31/2024 | |||||||||

| 2033 Main Street, Suite 407 | Sarasota | FL | Mortgage Sales | Leased | 2,410 | $ | 2,812 | / | mo | 10/31/2024 | |||||||||

| 265 E Marion Ave | Punta Gorda | FL | Mortgage Sales | Leased | - | $ | 99 | / | mo | month to month | |||||||||

| 900 Cricle 75 Parkway, Ste 175 | Atlanta | GA | Mortgage Sales | Leased | 3,020 | $ | 6,341 | / | mo | 6/30/2026 | |||||||||

| 6600 Peachtree Dunwoody Rd, Ste 135 | Atlanta | GA | Mortgage Sales | Leased | 2,129 | $ | 4,988 | / | mo | 3/31/2026 | |||||||||

| 4370 Kukui Grove St., Suite 201 | Lihue | HI | Mortgage Sales | Leased | 864 | $ | 1,542 | / | mo | 2/28/2025 | |||||||||

| 1001 Kamokila Blvd. | Kapolei | HI | Mortgage Sales | Leased | 737 | $ | 1,813 | / | mo | 12/31/2025 | |||||||||

| 32 Kinoole St. Suite 101, Hilo HI | Hilo | HI | Mortgage Sales | Leased | 730 | $ | 2,373 | / | mo | 5/31/2024 | |||||||||

| 1885 Main Street #108 | Wailuku | HI | Mortgage Sales | Leased | 1,092 | $ | 1,602 | / | mo | 5/14/2024 | |||||||||

| 677 Ala Moana Blvd. Suite 609 | Honolulu | HI | Mortgage Sales | Leased | 716 | $ | 2,141 | / | mo | 1/31/2024 | |||||||||

| 970 No Kalaheo Ave, Kailua, Suite A307, HI 96734 | Kailua | HI | Mortgage Sales | Leased | 510 | $ | 1,245 | / | mo | 5/31/2024 | |||||||||

| 70 Kanoa Street Suite #140 | Wailuku | HI | Mortgage Sales | Sub-Leased | Unknown | $ | 300 | / | mo | month to month | |||||||||

| 315 Cece Way | Mccall | ID | Mortgage Sales | Leased | 100 | $ | - | / | mo | month to month | |||||||||

| 802 West Bartlett Road | Bartlett | IL | Mortgage Sales | Leased | 2,300 | $ | 6,000 | / | mo | 12/31/2024 | |||||||||

| 568 Greenluster Dr. | Covington | LA | Mortgage Sales | Leased | 150 | $ | 750 | / | mo | month to month | |||||||||

| 81 Boulder Drive, | Elizabethtown | KY | Mortgage Sales | Leased | 100 | $ | - | / | mo | month to month | |||||||||

| 8684 Veterans Hwy, Ste 101 | Millersville | MD | Mortgage Sales | Leased | 4,018 | $ | 6,927 | / | mo | 7/31/2026 | |||||||||

| 860 Blue Gentian Road Suite 205 | Eagan | NM | Mortgage Sales | Leased | 100 | $ | 383 | / | mo | month to month | |||||||||

| 12 |

Item 2. Properties (Continued)

| Street | City | State | Function | Owned / Leased | Approximate Square Footage | Lease Amount |

Expiration | |||||||||||

| 4987 Fall Creek Rd. Suite 1 | Branson | MO | Mortgage Sales | Leased | 700 | $ | 1,000 | / | mo | month to month | ||||||||

| 4700 Homewood Ct #260 | Raleigh | NC | Mortgage Sales | Leased | 2,339 | $ | 5,353 | / | mo | 2/28/2025 | ||||||||

| 110 North Center Street, Suite 203 | Hickory | NC | Mortgage Sales | Leased | 100 | $ | 680 | / | mo | 5/14/2024 | ||||||||

| 2015 Ayrsley Town Blvd, Suite 247 | Charlotte | NC | Mortgage Sales | Leased | 100 | $ | 1,644 | / | mo | month to month | ||||||||

| 1980 Festival Plaza Dr., Suite 850 | Las Vegas | NV | Mortgage Sales | Leased | 12,866 | $ | 46,446 | / | mo | 3/31/2027 | ||||||||

| 840 Pinnacle Ct., Suite 3 | Mesquite | NV | Mortgage Sales | Leased | 900 | $ | 720 | / | mo | 3/12/2022 | ||||||||

| 2635 St. Rose Pkwy, Suites D 100, 110, 120 | Hendeson | NV | Mortgage Sales | Leased | 5,788 | $ | 12,649 | / | mo | 9/30/2025 | ||||||||

| 2250 East Postal Drive, Suite 1 | Pahrump | NV | Mortgage Sales | Sub-Leased | 1,500 | $ | 1,743 | / | mo | month to month | ||||||||

| 2546 Findlater | Henderson | NV | Mortgage Sales | Leased | 120 | $ | - | / | mo | month to month | ||||||||

| 670 Meridian Way, Suite 146 | Westerville | OH | Mortgage Sales | Leased | 100 | $ | 599 | / | mo | month to month | ||||||||

| 10365 SE Sunnyside Rd., Suite 310 | Clackamus | OR | Mortgage Sales | Leased | 1,288 | $ | 2,899 | / | mo | 11/30/2024 | ||||||||

| 11592 SW Roundup Place | Terrebonne | OR | Mortgage Sales | Leased | 100 | $ | - | / | mo | month to month | ||||||||

| 709 Pacific Ave | Tillamook | OR | Mortgage Sales | Leased | 120 | $ | - | / | mo | month to month | ||||||||

| 144 Alf Taylor Rd. | Johnson City | TN | Mortgage Sales | Sub-Leased | 1,521 | $ | 800 | / | mo | month to month | ||||||||

| 4646 Poplar Avenue, #317 | Memphis | TN | Mortgage Sales | Leased | 477 | $ | 845 | / | mo | 3/31/2024 | ||||||||

| 115 W. New Street | Kingsport | TN | Mortgage Sales | Leased | 100 | $ | 650 | / | mo | month to month | ||||||||

| 11550 Fuqua, Suite 200 | Houston | TX | Mortgage Sales | Leased | 1,865 | $ | 3,341 | / | mo | 4/30/2024 | ||||||||

| 17347 Village Green Dr., Suite 102 | Houston | TX | Mortgage Sales | Sub-Leased | 3,300 | $ | 5,995 | / | mo | 12/1/2024 | ||||||||

| 9737 Great Hills Trail, Suites 150, 200, 220 | Austin | TX | Mortgage Sales | Leased | 19,891 | $ | 40,196 | / | mo | month to month | ||||||||

| 1213 East Alton Gloor Blvd., Suite H | Brownsville | TX | Mortgage Sales | Leased | 2,000 | $ | 2,310 | / | mo | 2/28/2024 | ||||||||

| 5020 Collinwood Ave., Suite 100 | Fort Worth | TX | Mortgage Sales | Leased | 2,687 | $ | 5,500 | / | mo | 1/31/2025 | ||||||||

| 722 Kiowa Dr. West | Lake Kiowa | TX | Mortgage Sales | Leased | 150 | $ | 495 | / | mo | month to month | ||||||||

| 23227 Red River Drive | Katy | TX | Mortgage Sales | Leased | 144 | $ | 750 | / | mo | month to month | ||||||||

| 5707 Cold Springs Drive | San Antonio | TX | Mortgage Sales | Leased | 100 | $ | - | / | mo | month to month | ||||||||

| 4500 1-40 West, Suite B | Amarillo | TX | Mortgage Sales | Leased | 1,238 | $ | 1,700 | / | mo | 12/31/2024 | ||||||||

| 30417 Fifth Street Suite B | Fulshear | TX | Mortgage Sales | Leased | 1,000 | $ | 1,273 | / | mo | month to month | ||||||||

| 4908 North Midkiff Road | Midland | TX | Mortgage Sales | Leased | 1,550 | $ | 2,500 | / | mo | month to month | ||||||||

| 462 Mid Cities Boulevard | Hurst | TX | Mortgage Sales | Leased | 1,640 | $ | 2,500 | / | mo | month to month | ||||||||

| 18525 West Lake Houston Parkway, Suite 222 | Humble | TX | Mortgage Sales | Leased | 1,390 | $ | 2,612 | / | mo | 9/30/2025 | ||||||||

| 2600 South Shore Boulevard, Suite 300 | League City | TX | Mortgage Sales | Leased | 94 | $ | 785 | / | mo | 4/24/2024 | ||||||||

| 106 Decker Court Suite 310 | Irving | TX | Mortgage Sales | Leased | 1,664 | $ | 4,160 | / | mo | 4/24/2024 | ||||||||

| 1600 Lee Travino, Suite A-1 | El Paso | TX | Mortgage Sales | Leased | 1,535 | $ | 2,110 | / | mo | month to month | ||||||||

| 23702 IH-10 West, Suite 105-D | San Antonio | TX | Mortgage Sales | Leased | 100 | $ | 470 | / | mo | month to month | ||||||||

| 1777 NE Loop 410, Suite 600 | San Antonio | TX | Mortgage Sales | Leased | 100 | $ | 1,070 | / | mo | month to month | ||||||||

| 299 South Columbia, | Stephenville | TX | Mortgage Sales | Leased | 3,417 | $ | 5,700 | / | mo | month to month | ||||||||

| 18756 Stone Oak Parkway Ste 200 | San Antonio | TX | Mortgage Sales | Leased | 100 | $ | 1,908 | / | mo | month to month | ||||||||

| 10000 Central Expressway Ste 428 | Dallas | TX | Mortgage Sales | Leased | 200 | $ | 1,400 | / | mo | 12/31/2024 | ||||||||

| 602 S Main St | Weatherford | TX | Mortgage Sales | Leased | 1,250 | $ | 1,282 | / | mo | 12/31/2024 | ||||||||

| 5757 Flewellen Oaks Ln #104 | Fulshear | TX | Mortgage Sales | Leased | 100 | $ | 800 | / | mo | month to month | ||||||||

| 126 W. Sego Lily Dr., Suite 126 | Sandy | UT | Mortgage Sales | Leased | 2,794 | $ | 6,933 | / | mo | 1/31/2027 | ||||||||

| 497 S. Main | Ephraim | UT | Mortgage Sales | Leased | 1,884 | $ | 1,600 | / | mo | 4/30/2025 | ||||||||

| 11240 S. River Heights Dr. | South Jordan | UT | Mortgage Sales | Leased | 3,403 | $ | 8,458 | / | mo | 11/30/2024 | ||||||||

| 500 East Village Blvd. | Stansbury Park | UT | Mortgage Sales | Leased | 1,950 | $ | 3,475 | / | mo | 10/31/2024 | ||||||||

| 1350 E. 300 S. 3rd Floor | Lehi | UT | Mortgage Sales | Leased | 15,446 | $ | 38,396 | / | mo | 12/22/2026 | ||||||||

| 2455 E. Parleys Way, Suites 120 & 150 | Salt Lake City | UT | Mortgage Sales | Leased | 5,256 | $ | 8,962 | / | mo | 7/31/2030 | ||||||||

| 859 W South Jordan Pkwy, Suite 101, | South Jordan | UT | Mortgage Sales | Leased | 3,376 | $ | 6,175 | / | mo | 5/30/2025 | ||||||||

| 768 S. 1600 W., Suite B | Mapleton | UT | Mortgage Sales | Leased | 1,500 | $ | 4,120 | / | mo | month to month | ||||||||

| UT ( ) 998 N 1200 W, Suite 104 Orem | Orem | UT | Mortgage Sales | Leased | 2,162 | $ | 5,648 | / | mo | month to month | ||||||||

| 21430 Cedar Dr., Suite 200-202 | Sterling | VA | Mortgage Sales | Leased | 6,850 | $ | 16,360 | / | mo | 3/9/2024 | ||||||||

| 15650 NE Fourth Blvd Ste 101 | Vancouver | WA | Mortgage Sales | Leased | 200 | $ | 485 | / | mo | 11/30/2024 | ||||||||

| 1508 24th Ave., Suite 23 | Kenosha | WI | Mortgage Sales | Leased | 250 | $ | 150 | / | mo | month to month | ||||||||

| 27903 99th St. | Trevor | WI | Mortgage Sales | Leased | 300 | $ | 150 | / | mo | month to month | ||||||||

(1) These two properties were sold during the first quarter of 2024.

(2) This property is currently listed for sale and under contract.

The Company believes the office facilities it occupies are in good operating condition and adequate for current operations. The Company plans to enter into additional leases or modify existing leases based on its assessments of market demand. Those leases are expected to be month to month where possible. As leases expire, the Company plans to either renew or find comparable leases or acquire additional office space.

| 13 |

Item 2. Properties (Continued)

The following table summarizes the location and acreage of the seven Company owned cemeteries, each of which includes one or more mausoleums. The acreage represents estimates of acres that are based upon survey reports, title reports, appraisal reports, or the Company’s inspection of the cemeteries. The Company estimates that there are approximately 1,200 spaces per developed acre.

| Net Saleable Acreage | ||||||||||||||||||||||

| Name of Cemetery | Location | Date Acquired | Developed Acreage | Total Acreage | Acres Sold as Cemetery Spaces (1) | Total Available Acreage | ||||||||||||||||

| Memorial

Estates, Inc. Lakeview Cemetery | 1640

East Lakeview Drive Bountiful, Utah | 1973 | 9 | 39 | 8 | 31 | ||||||||||||||||

| Memorial

Estates, Inc. Mountain View Cemetery | 3115

East 7800 South Salt Lake City, Utah | 1973 | 26 | 54 | 20 | 34 | ||||||||||||||||

| Memorial

Estates, Inc. Redwood Cemetery | 6500

South Redwood Road West Jordan, Utah | 1973 | 40 | 71 | 35 | 36 | ||||||||||||||||

| Deseret

Memorial Inc. Lake Hills Cemetery | 10055

South State Street Sandy, Utah | 1991 | 9 | 28 | 6 | 22 | ||||||||||||||||

| Holladay

Memorial Park, Inc. Holladay Memorial Park | 4900

South Memory Lane Holladay, Utah | 1991 | 12 | 14 | 8 | 6 | ||||||||||||||||

| California

Memorial Estates, Inc. Singing Hills Memorial Park | 2800

Dehesa Road El Cajon, California | 1995 | 8 | 97 | 6 | 91 (2) | ||||||||||||||||

| SNR-SF Cemetery LLC Santa Fe Memorial Gardens | 417

Rodeo Rd Santa Fe, New Mexico | 2021 | 5 (3) | 5 | 4 | 1 | ||||||||||||||||

| (1) | Includes both reserved and occupied spaces. | |

| (2) | Includes an open easement with a total acreage of approximately 62 acres. | |

| (3) | Includes five main columbariums that can hold approximately 6,000 inurnments. |

| 14 |

Item 2. Properties (Continued)

The following table summarizes the location, square footage and the number of viewing rooms and chapels of the twelve Company owned mortuaries:

| Date | Viewing | Square | ||||||||||||||||

| Name of Mortuary | Location | Acquired | Room(s) | Chapel(s) | Footage | |||||||||||||

| Memorial Mortuary, Inc. Memorial Mortuary | 5850 South 900 East, Murray, Utah | 1973 | 3 | 1 | 20,000 | |||||||||||||

| Affordable Funerals and Cremations, St. George | 157 East Riverside Dr., No. 3A, St. George, Utah | 2016 | 1 | 1 | 2,360 | |||||||||||||

| Memorial Estates, Inc. Redwood Mortuary (1) | 6500 South Redwood Rd., West Jordan, Utah | 1973 | 2 | 1 | 10,000 | |||||||||||||

| Memorial Estates, Inc. Mountain View Mortuary (1) | 3115 East 7800 South, Salt Lake City, Utah | 1973 | 2 | 1 | 16,000 | |||||||||||||

| Memorial Estates, Inc. Lakeview Mortuary (1) | 1640 East Lakeview Dr., Bountiful, Utah | 1973 | 0 | 1 | 5,500 | |||||||||||||

| Deseret Memorial Inc. Lakehills Mortuary (1) | 10055 South State St., Sandy, Utah | 1991 | 2 | 1 | 18,000 | |||||||||||||

| Cottonwood Mortuary, Inc. Cottonwood Mortuary | 4670 South Highland Dr., Holladay, Utah | 1991 | 2 | 1 | 14,500 | |||||||||||||

| SN Probst LLC Heber Valley Funeral Home | 288 North Main St., Heber City, Utah | 2019 | 1 | 1 | 5,900 | |||||||||||||

| SN Holbrook LLC Milcreek Funeral Home | 3251 S 2300 E, Millcreek, Utah | 2021 | 2 | 1 | 6,300 | |||||||||||||

| SNR-SF Mortuary LLC Rivera Family Funeral Home Santa Fe (1) | 417 Rodeo RD, Santa Fe, New Mexico | 2021 | 2 | 1 | 7,700 | |||||||||||||

| SNR-Espanola LLC Rivera Family Funeral Home Española | 305 Calle Salazar, Española, New Mexico | 2021 | 1 | 2 | 10,400 | |||||||||||||

| SNR-Taos LLC Rivera Family Funeral Home Taos | 818 Paseo Del Pueblo Sur, Taos, New Mexico | 2021 | 0 | 1 | 9,600 | |||||||||||||

| (1) | These funeral homes also provide burial niches at their respective locations. |

| 15 |

Item 3. Legal Proceedings

The Company is not a party to any material legal proceedings outside the ordinary course of business or to any other legal proceedings, which if adversely determined, would be expected to have a material adverse effect on its financial condition or results of operation.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for the Registrant’s Common Stock, Related Stockholder Matters, and Issuer Purchases of Equity Securities

The Company’s Class A common stock trades on The Nasdaq Global Select Market under the symbol “SNFCA.” As of March 26, 2024, the closing stock price of the Class A common stock was $7.62 per share. As of March 26, 2024, there were 1,747 registered stockholders of record of the Company’s Class A common stock and 42 registered stockholders of record of the Company’s Class C common stock. Because many of the Company’s shares of Class A common stock are held by brokers and other institutions on behalf of the stockholders, the Company is unable to estimate the total number of stockholders represented by these record holders.

The following were the high and low market closing stock prices for the Class A common stock by quarter as reported by NASDAQ since January 1, 2022:

| Price Range (1) | ||||||||

| High | Low | |||||||

| Period (Calendar Year) | ||||||||

| 2022 | ||||||||

| First Quarter | $ | 9.39 | $ | 8.13 | ||||

| Second Quarter | $ | 9.40 | $ | 7.46 | ||||

| Third Quarter | $ | 8.20 | $ | 5.93 | ||||

| Fourth Quarter | $ | 7.21 | $ | 5.81 | ||||

| 2023 | ||||||||

| First Quarter | $ | 7.19 | $ | 5.71 | ||||

| Second Quarter | $ | 8.45 | $ | 6.03 | ||||

| Third Quarter | $ | 8.83 | $ | 7.58 | ||||

| Fourth Quarter | $ | 9.60 | $ | 6.89 | ||||

| 2024 | ||||||||

| First Quarter (through March 26, 2024) | $ | 9.04 | $ | 7.62 | ||||

(1) Stock prices have been adjusted retroactively for the effect of annual stock dividends.

The Class C common stock is not registered or traded on a national exchange. See Note 12 of the Notes to Consolidated Financial Statements.

The Company has never paid a cash dividend on its Class A or Class C common stock. The Company currently anticipates that all its earnings will be retained for use in the operation and expansion of its business and does not intend to pay any cash dividends on its Class A or Class C common stock in the foreseeable future. Any future determination as to cash dividends will depend upon the earnings and financial position of the Company and such other factors as the Board of Directors may deem appropriate. The Company paid a 5% stock dividend on Class A and Class C common stock each year from 1990 through 2019, a 7.5% stock dividend for the year 2020, and a 5.0% stock dividend for the years 2021 through 2023.

| 16 |

On December 27, 2022, the Company executed a 10b5-1 agreement with a broker to repurchase shares of the Company’s Class A Common Stock. Under the terms of the agreement, the broker is permitted to repurchase up to 1,000,000 shares of the Company’s Class A Common Stock. The agreement is subject to the daily time, price, and volume conditions of Rule 10b-18. The agreement expired December 31, 2023.

The following table shows the Company’s repurchase activity of its common stock during the three-month period ended December 31, 2023 under the 10b5-1 agreement.

| Period | (a) Total Number of Class A Shares Purchased | (b) Average Price Paid per Class A Share (1) | (c) Total Number of Class A Shares Purchased as Part of Publicly Announced Plan or Program | (d) Maximum Number of Class A Shares that May Yet Be Purchased Under the Plan or Program (2) | ||||||||||||

| 10/1/2023-10/31/2023 | - | $ | - | - | 318,043 | |||||||||||

| 11/1/2023-11/30/2023 | - | $ | - | - | 318,043 | |||||||||||

| 12/1/2023-12/31/2023 | - | $ | - | - | 318,043 | |||||||||||

| Total | - | $ | - | - | 318,043 | |||||||||||

| (1) | Includes fees and commissions paid on stock repurchases. | |

| (2) | In September 2018, the Board of Directors of the Company approved a Stock Repurchase Plan that authorized the repurchase of 300,000 shares of the Company’s Class A Common Stock in the open market. The Company amended the Stock Repurchase Plan on December 4, 2020. The amendment authorized the repurchase of a total of 1,000,000 shares of the Company’s Class A Common Stock in the open market. Any repurchased shares of Class A common stock are to be held as treasury shares to be used as the Company’s employer matching contribution to the Employee 401(k) Retirement Savings Plan and for shares held in the Deferred Compensation Plan. |

| 17 |

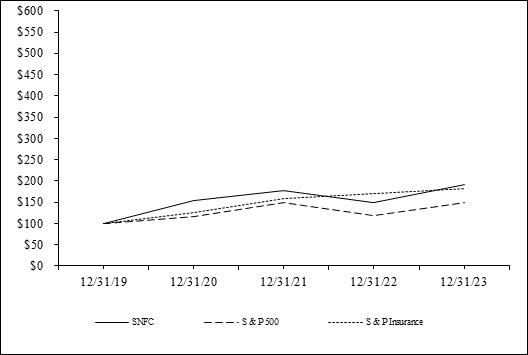

The graph below compares the cumulative total stockholder return of the Company’s Class A common stock with the cumulative total return on the Standard & Poor’s 500 Stock Index and the Standard & Poor’s Insurance Index for the period from December 31, 2019 through December 31, 2023. The graph assumes that the value of the investment in the Company’s Class A common stock and in each of the indexes was $100 as of December 31, 2019 and that all dividends were reinvested.

The comparisons in the graph below are based on historical data and are not intended to forecast the possible future performance of the Company’s Class A common stock.

| 12/31/19 | 12/31/20 | 12/31/21 | 12/31/22 | 12/31/23 | ||||||||||||||||

| SNFC | 100 | 153 | 177 | 148 | 191 | |||||||||||||||

| S & P 500 | 100 | 116 | 148 | 119 | 148 | |||||||||||||||

| S & P Insurance | 100 | 126 | 158 | 171 | 183 | |||||||||||||||

The stock performance graph set forth above is required by the Securities and Exchange Commission and shall not be deemed to be incorporated by reference by any general statement incorporating by reference this Form 10-K into any filing under the Securities Act of 1933, as amended, or under the Securities Exchange Act of 1934, as amended, except to the extent that the Company specifically incorporates this information by reference, and shall not otherwise be deemed soliciting material or filed under such acts.

Item 6. [Reserved]

As a smaller reporting company, the Company is not required to provide information typically disclosed under this item.

| 18 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

The Company’s operations over the last several years generally reflect three strategies which the Company expects to continue: (i) increased attention to “niche” insurance products, such as the Company’s funeral plan policies and traditional whole life products; (ii) increased emphasis on cemetery and mortuary business; and (iii) capitalizing on an improving housing market by originating mortgage loans.

Insurance Operations

The following table shows the condensed financial results for the Company’s insurance operations for 2023 and 2022. See Note 15 of the Notes to Consolidated Financial Statements.

| Years

ended December 31 (in thousands of dollars) | ||||||||||||

| 2023 | 2022 | 2023 vs 2022 % Increase (Decrease) | ||||||||||

| Revenues from external customers: | ||||||||||||

| Insurance premiums | $ | 114,658 | $ | 105,002 | 9 | % | ||||||

| Net investment income | 67,812 | 62,565 | 8 | % | ||||||||

| Mortgage fee income | 77 | 143 | (46 | %) | ||||||||

| Gains (losses) on investments and other assets | 963 | (459 | ) | 310 | % | |||||||

| Other | 1,666 | 1,932 | (14 | %) | ||||||||

| Total | $ | 185,176 | $ | 169,183 | 9 | % | ||||||

| Intersegment revenue | $ | 8,203 | $ | 6,601 | 24 | % | ||||||

| Earnings before income taxes | $ | 25,272 | $ | 14,196 | 78 | % | ||||||

Profitability for 2023 increased due to (a) a $9,656,000 increase in insurance premiums and other considerations, (b) a $5,247,000 increase in net investment income, (c) a $1,602,000 increase in intersegment revenue, (d) a $1,422,000 increase in gains on investments and other assets primarily due to an increase in the fair value of equity securities, and (e) a $987,000 decrease in selling, general and administrative expenses, which were partially offset by (i) a $5,150,000 increase in future policy benefits, (ii) a $1,936,000 increase in death, surrenders and other policy benefits, (iii) a $266,000 decrease in other revenues, (iv) a $176,000 increase in intersegment interest expense and other expenses, (v) a $133,000 increase in amortization of deferred policy acquisition costs primarily due to an increase in the average outstanding balance of deferred policy and pre-need acquisition costs, (vi) a $111,000 increase in interest expense, and (vii) a $66,000 decrease in mortgage fee income.

| 19 |

Cemetery and Mortuary Operations

The following table shows the condensed financial results for the Company’s cemetery and mortuary operations for 2023 and 2022. See Note 15 of the Notes to Consolidated Financial Statements.

| Years

ended December 31 (in thousands of dollars) | ||||||||||||

| 2023 | 2022 | 2023 vs 2022 % Increase (Decrease) | ||||||||||

| Revenues from external customers: | ||||||||||||

| Cemetery revenues | $ | 15,189 | $ | 13,871 | 10 | % | ||||||

| Mortuary revenues | 12,676 | 13,123 | (3 | %) | ||||||||

| Net investment income | 2,952 | 2,445 | 21 | % | ||||||||

| Gains (losses) on investments and other assets | 717 | (796 | ) | 190 | % | |||||||

| Other | 404 | 305 | 32 | % | ||||||||

| Total | $ | 31,938 | $ | 28,948 | 10 | % | ||||||

| Earnings before income taxes | $ | 8,445 | $ | 6,094 | 39 | % | ||||||

Profitability in 2023 increased due to (a) a $2,196,000 increase in cemetery pre-need sales, (b) a $1,513,000 increase in gains on investments and other assets (primarily attributable to an increase in the fair value of equity securities classified as restricted assets and cemetery perpetual care trust investments), (c) a $507,000 increase in net investment income, (d) a $99,000 increase in other revenues, (e) a $59,000 decrease in amortization of deferred policy acquisition costs, and (f) a $44,000 decrease in intersegment interest expense and other expenses, which were partially offset by (i) a $878,000 decrease in cemetery at-need sales, (ii) a $546,000 increase in selling, general and administrative expenses, (iii) a $447,000 decrease in mortuary at-need sales, (iv) a $111,000 decrease in intersegment revenues, and (v) a $85,000 increase in costs of goods sold.

Mortgage Operations

The Company’s wholly owned subsidiary, SecurityNational Mortgage, is a mortgage lender incorporated under the laws of the State of Utah and approved and regulated by the Federal Housing Administration (FHA), a department of the U.S. Department of Housing and Urban Development (HUD), which originates mortgage loans that qualify for government insurance in the event of default by the borrower, in addition to various conventional mortgage loan products. SecurityNational Mortgage originates and refinances mortgage loans on a retail basis. Mortgage loans originated or refinanced by SecurityNational Mortgage are funded through loan purchase agreements with Security National Life, Kilpatrick Life and unaffiliated financial institutions.

SecurityNational Mortgage receives fees from borrowers that are involved in mortgage loan originations and refinancings, and secondary fees earned from third party investors that purchase the mortgage loans. Mortgage loans are generally sold with mortgage servicing rights (“MSRs”) released to third-party investors or retained by SecurityNational Mortgage. SecurityNational Mortgage currently retains the MSRs on approximately 4% of its loan origination volume. These mortgage loans are serviced by either SecurityNational Mortgage or an approved third-party sub-servicer. On October 31, 2022, the Company sold certain of its MSRs. The MSRs related to mortgage loans previously originated by the Company in aggregate unpaid principal amount of approximately $7.02 billion. As a result of the sale, the book value of the Company’s MSRs decreased $51,185,906.

Mortgage rates have followed the US Treasury yields up in response to the higher-than-expected inflation and the expectation that the Federal Reserve will continue to raise rates in the near term. As expected, the rapid increase in mortgage rates has resulted in a decrease in loan originations classified as ‘refinance’. Higher mortgage rates have also had a negative effect on loan originations classified as ‘purchases’, although not as significant as those in the refinance classification.

For 2023 and 2022, SecurityNational Mortgage originated 7,185 loans ($2,173,081,000 total volume) and 10,663 loans ($3,373,554,000 total volume), respectively.

| 20 |

The following table shows the condensed financial results for the Company’s mortgage operations for 2023 and 2022. See Note 15 of the Notes to Consolidated Financial Statements.

| Years

ended December 31 (in thousands of dollars) | ||||||||||||

| 2023 | 2022 | 2023 vs 2022 % Increase (Decrease) | ||||||||||

| Revenues from external customers: | ||||||||||||

| Secondary gains from investors | $ | 68,428 | $ | 153,728 | (55 | %) | ||||||

| Income from loan originations | 31,245 | 32,772 | (5 | %) | ||||||||

| Change in fair value of loans held for sale | (478 | ) | (8,835 | ) | (95 | %) | ||||||

| Change in fair value of loan commitments | (1,124 | ) | (4,309 | ) | (74 | %) | ||||||

| Net investment income | 1,580 | 1,188 | 33 | % | ||||||||

| Gains on investments and other assets | 157 | 398 | (61 | %) | ||||||||

| Other | 1,576 | 16,580 | (90 | %) | ||||||||

| Total | $ | 101,384 | $ | 191,522 | (47 | %) | ||||||

| Earnings (loss) before income taxes | $ | (17,416 | ) | $ | 14,088 | (224 | %) | |||||

Included in other revenues is service fee income. Profitability in 2023 decreased due to (a) an $85,300,000 decrease in secondary gains from investors, (b) a $15,004,000 decrease in other revenues due to the sale of certain MSRs in October 2022, (c) a $1,535,000 increase in intersegment interest expense and other expenses, (d) a $1,527,000 decrease in income from loan originations, and (e) a $241,000 decrease in gains on investments and other assets, which were partially offset by (i) a $23,662,000 decrease in commissions, (ii) a $17,871,000 decrease in personnel expenses, (iii) a $13,180,000 decrease in other expenses, (iv) an $8,356,000 increase in the fair value of loans held for sale, (v) a $3,185,000 increase in the fair value of loan commitments, (vi) a $3,077,000 decrease in interest expense, (vii) a $1,100,000 decrease in costs related to funding mortgage loans, (viii) a $1,011,000 decrease in advertising expenses, (ix) a $392,000 increase in net investment income, (x) a $175,000 increase in intersegment revenues, (xi) a $42,000 decrease in depreciation on property and equipment, and (xii) a $52,000 decrease in rent and rent related expenses.

Critical Accounting Policies and Estimates

The following is a summary of the Company’s significant accounting policies and a review of the Company’s most critical accounting estimates. See Note 1 of the Notes to Consolidated Financial Statements.

Insurance Operations

In accordance with generally accepted accounting principles in the United States of America (“GAAP”), premiums and other considerations received for interest sensitive products are reflected as increases in liabilities for policyholder account balances and not as revenues. Revenues reported for these products consist of policy charges for the cost of insurance, administration charges, amortization of policy initiation fees and surrender charges assessed against policyholder account balances. Surrender benefits paid relating to these products are reflected as decreases in liabilities for policyholder account balances and not as expenses.

The Company receives investment income earned from the funds deposited into account balances, a portion of which is passed through to the policyholders in the form of interest credited. Interest credited to policyholder account balances and benefit claims more than policyholder account balances are reported as expenses in the consolidated financial statements.

Premiums and other considerations received for traditional life insurance products are recognized as revenues when due. Future policy benefits are recognized as expenses over the life of the policy by means of the provision for future policy benefits.

The costs related to acquiring new business, including certain costs of issuing policies and other variable selling expenses (principally commissions), defined as deferred policy acquisition costs, are capitalized, and amortized into expenses. For nonparticipating traditional life products, these costs are amortized over the premium paying period of the related policies, in proportion to the ratio of annual premium revenues to total anticipated premium revenues. Such anticipated premium revenues are estimated using the same assumptions used for computing liabilities for future policy benefits and are generally “locked in” at the date the policies are issued. For interest sensitive products, these costs are amortized generally in proportion to expected gross profits from surrender charges and investment, mortality, and expense margins. This amortization is adjusted when the Company revises the estimate of current or future gross profits or margins. For example, deferred policy acquisition costs are amortized earlier than originally estimated when policy terminations are higher than originally estimated or when investments backing the related policyholder liabilities are sold at a gain prior to their anticipated maturity.

| 21 |

Death and other policyholder benefits reflect exposure to mortality risk and fluctuate from year to year on the level of claims incurred under insurance retention limits. The profitability of the Company is primarily affected by fluctuations in mortality, other policyholder benefits, expense levels, interest spreads (i.e., the difference between interest earned on investments and interest credited to policyholders) and persistency. The Company can mitigate adverse experiences through sound underwriting, asset and liability duration matching, sound actuarial practices, adjustments to credited interest rates, policyholder dividends and cost of insurance charges.

Cemetery and Mortuary Operations

Pre-need sales of funeral services and caskets, including revenue and costs associated with the sales of pre-need funeral services and caskets, are deferred until the services are performed or the caskets are delivered.

Pre-need sales of cemetery interment rights (cemetery burial property), including revenue and costs associated with the sales of pre-need cemetery interment rights, are recognized in accordance with the retail land sales provisions of GAAP. Under GAAP, recognition of revenue and associated costs from constructed cemetery property must be deferred until a minimum percentage of the sales price has been collected. Revenues related to the pre-need sale of unconstructed cemetery property will be deferred until such property is constructed and meets the criteria of GAAP, described above.

Pre-need sales of cemetery merchandise (primarily markers and vaults), including revenue and costs associated with the sales of pre-need cemetery merchandise, are deferred until the merchandise is delivered, fulfilling the performance obligation.

Pre-need sales of cemetery services (primarily merchandise delivery and installation fees and burial opening and closing fees), including revenue and costs associated with the sales of pre-need cemetery services, are deferred until the services are performed.

Prearranged funeral and pre-need cemetery customer obtaining costs, including costs incurred related to obtaining new pre-need cemetery and prearranged funeral business are accounted for under the guidance of the provisions of GAAP. Obtaining costs, which include only costs that vary with and are primarily related to the acquisition of new pre-need cemetery and prearranged funeral business, are deferred until the merchandise is delivered or services are performed.

Revenues and costs for at-need sales are recorded when a valid contract exists, the services are performed, collection is reasonably assured, and there are no significant company obligations remaining.

Mortgage Operations

Mortgage fee income consists of origination fees, processing fees, interest income and certain other income related to the origination and sale of mortgage loans. The Company has elected to use fair value accounting for all mortgage loans that are held for sale. Accordingly, all revenues and costs are now recognized when the mortgage loan is funded and any changes in fair value are shown as a component of mortgage fee income.

The Company, through its mortgage subsidiaries, sells mortgage loans to third-party investors without recourse, unless defects are identified in the representations and warranties made at loan sale. It may be required, however, to repurchase a loan or pay a fee instead of repurchasing under certain events, which include the following: