UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

INFORMATION FOR SHAREHOLDERS (Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number

(Exact name of Registrant as specified in its charter)

(Jurisdiction of incorporation or organization) |

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol |

| Name on each exchange on which registered |

| New York Stock Exchange* |

* Not for , but only in connection with the first registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer’s class of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Yes ◻

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days:

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer, “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated Filer ◻ | Non-accelerated filer ◻ | |

Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ◻

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

◻ U.S. GAAP |

| ⌧ |

| ◻ Other |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ◻ Item 18 ◻

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

| Life Unlimited Annual Report 2023 |

| Contents Our performance Strategic Report Our performance IFC Who we are 2 Chair’s statement 4 Chief Executive Officer’s review 8 Our marketplace 14 Our business model 16 Key Performance Indicators 18 Financial review 20 Creating value through innovation 26 Taking our innovation to market 34 Building a culture of belonging 46 Shaping a healthy and sustainable future 52 Risk report 67 Our stakeholders 82 Engaging with stakeholders 84 Governance Governance at a glance 88 Board leadership and Company purpose 90 Nomination & Governance Committee Report 102 Compliance & Culture Committee Report 111 Audit Committee Report 114 Directors’ Remuneration Report 121 Accounts Statement of Directors’ responsibilities 156 Report of Independent Registered Public Accounting Firm 157 Group income statement 172 Group statement of comprehensive income 172 Group balance sheet 173 Group cash flow statement 174 Group statement of changes in equity 175 Notes to the Group accounts 176 Company financial statements 227 Notes to the Company accounts 229 Other information Group information 235 Other information 236 Shareholder information 248 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. The images used throughout the report represent the ways that Smith+Nephew is taking the limits off living and helping patients live Life Unlimited. Images used are not photographs of our patients unless expressly indicated. $5,549m Group revenue 37.5¢ Unchanged +6.4% Dividend per share Reported +7.2% Underlying1 $425m -5.4% Operating profit 7.7% -90bps Operating profit margin $970m +7.6% Trading profit1 17.5% +20bps Trading profit margin1 30.2¢ +1.3% Earnings per share (EPS) 82.8¢ +18.2% Adjusted earnings per share1 (EPSA) $829m +42.7% Cash generated from operations $635m +43.0% Trading cash flow1 $339m -1.8% R&D investment 5.9% -70bps Return on invested capital1 (ROIC) |

| Physical health is never just about our body. It’s our mind, feelings and ambitions. When something holds us back, it’s our whole life on hold. We’re here to change that, to use technology to take the limits off living, and help other medical professionals do the same. So that patients can stare down fear, see that anything is possible, then go on stronger. Inspired by a simple promise. Two words that bring together all we do… Life Unlimited To learn more about our purpose visit www.smith-nephew.com Smith+Nephew Annual Report 2023 1 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Who we are Creating value through innovation Research & Development Developing new technology through our Research & Development (R&D) programme, and acquiring exciting technologies where we can add value. Medical education The Smith+Nephew Academy network supports the safe and effective use of our products and provides opportunities to learn innovative clinical techniques. Manufacturing Building resilient manufacturing and supply chains to ensure quality and competitiveness and support new product development. Shaping a healthy and sustainable future Our ESG strategy supports our Strategy for Growth and strengthens the foundation to help us serve customers over the long term. Our ESG strategy focuses on three areas: People, Planet and Products. » People: Creating a lasting positive impact on our communities. » Planet: Aiming to reduce our impact on the environment. » Products: Innovating sustainably. Building a culture of belonging We strive to create a culture of belonging where employees can bring their full selves and best ideas, which fosters innovation, delivers business success and strengthens engagement and personal fulfilment. Our culture is based on our values of Care, Courage and Collaboration. » Care: A culture of empathy and understanding for each other, our customers and their patients. » Courage: A culture of continuous learning, innovation and accountability. » Collaboration: A culture of teamwork based on mutual trust and respect. » See pages 26–29 » See pages 30–31 » See pages 32–33 » See pages 52–66 for information on our sustainability targets and progress » See pages 46–49 for more on how we are building our culture 168 year history 14+ million patients treated with our products 100+ countries served $339 million R&D investment 18,452 employees 20 new product launches We are a leading Key facts 2023 portfolio medical technology company. We exist to restore people’s bodies and their self-belief. 2 Smith+Nephew Annual Report 2023 |

| Taking our innovation to market We take our innovation to market through three global business units of Orthopaedics, Sports Medicine & ENT, and Advanced Wound Management. These business units are responsible for strategy and global marketing, and contain specialist sales and support teams dedicated to serving the specific requirements of our healthcare professional customers. Serving our customers through our sales force We pride ourselves on giving customers a high standard of service through our specialist sales and clinical support teams. Representatives in our surgical businesses have a detailed knowledge of the products and instruments that they sell and the surgical techniques they may be used for, and provide technical and logistical support to surgeons and hospitals. In Advanced Wound Management, sales representatives develop their knowledge of how clinicians seek to prevent and treat wounds, as well as support customers through their understanding of the economic benefits of using our products within treatment protocols. Sports Medicine & ENT Our Sports Medicine & Ear, Nose and Throat (ENT) businesses offer advanced products and instruments used to repair or remove soft tissue. They operate in growing markets where unmet clinical needs provide opportunities for procedural and technological innovation. Advanced Wound Management Our Advanced Wound Management portfolio provides a comprehensive set of products and services to meet broad and complex clinical needs across hard to heal wounds, delivering on our mission to shape what is possible in wound care. Orthopaedics Orthopaedics includes an innovative range of hip and knee implants used to replace diseased, damaged or worn joints, robotics-assisted and digital enabling technologies and services that empower surgeons, and Trauma & Extremities products used to stabilise severe fractures and correct hard tissue deformities, as well as a shoulder replacement system. 40% of Group revenue 31% of Group revenue 29% of Group revenue » See pages 34–37 » See pages 38–41 » See page 42–45 Smith+Nephew Annual Report 2023 3 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Chair’s statement Encouraged by the progress made, excited by our prospects for the future “Deepak has set out a confident outlook as he leads the business in the Strategy for Growth and the second year of delivery of the 12-Point Plan.” Rupert Soames Chair Dear Fellow Shareholder, It is a great honour to write to you for the first time as Chair of Smith+Nephew, and to share my reflections on the year just gone and the journey ahead. But before I do, I want to pay tribute to my predecessor Roberto Quarta who chaired the Company with great care and diligence for nine, sometimes difficult, years. Most recently, he as Chair and Marc Owen as Senior Independent Director, have supported my induction and transition to Chair with sensitivity and skill, for which I am grateful. Since joining the Board on 26 April 2023, I have been learning about the business: its products and services; its people, customers and competitors; its strengths and weaknesses, as well as the opportunities and threats it faces. In all these things I have been supported by Deepak Nath, our Chief Executive Officer, who has deep knowledge of, and experience in, the MedTech sector. Many of our larger investors have also been generous with their time, candid in their analysis, and speak from many years’ experience of both the sector and Smith+Nephew. In addition, I had the opportunity to meet some of our smaller investors at the Annual General Meeting in April, which was a pleasure to attend and a reminder that ultimately, in all we do, there are savers and pensioners who rely on us to grow the value of their investments. Setting clear priorities In a world in which stakeholders have different, and sometimes conflicting, views on how, and to what end, companies should be run, Boards have to be resolute in discharging their responsibilities in the best interests of the Company as a whole. This means they have to have priorities, and to be clear on what their job is. 4 Smith+Nephew Annual Report 2023 |

| The first priority of the Board is to hire and retain management who can lead Smith+Nephew to be the best business it can be; and then, watching closely, encourage, support, guide and challenge them in their work. As a Board, we are very well aware that Smith+Nephew has not performed to its full potential in recent years. The reasons for this, and more importantly, what management are doing about it, are set out in the Strategy and Operating Reviews, and I am pleased to say that in 2023 there were encouraging signs of progress. In Deepak Nath, we have an exceptionally talented CEO, and the Board is following closely the implementation of the 12-Point Plan he and his executive team developed to enable Smith+Nephew to create sustainable long-term value. Deepak has a rare combination of strategic vision and grasp of detail, and under his leadership the business has begun to gather forward momentum, including accelerating revenue growth. Joining Deepak from December 2023 is John Rogers, who will succeed Anne-Françoise Nesmes as Chief Financial Officer in the first quarter of 2024. John brings long experience as a former CFO of two FTSE 100 companies, and has also managed impressive transformations of companies’ operations. I would like to thank Anne-Françoise for her dedication and support to the business over the last three years, during which she has had to support a change of CEO and the significant impact of Covid on the business. The other priority of the Board is to serve our shareholders and wider stakeholders by governing the business effectively and in accordance with regulation and good practice, but with an emphasis on substance over form, simplicity over complexity, and transparency over opaqueness. Governance at Smith+Nephew embraces many different areas. In terms of risk management, Smith+Nephew shares a similar palette of risks to other manufacturers, but the application of medical devices, products and services in the treatment of people, the global scale of our operations, and the highly regulated environment in which we operate make monitoring of operating risk a key part of the Board’s responsibilities. In matters of corporate regulation and corporate governance, being dual-listed brings a degree of complexity. Smith+Nephew hews to the rules and regulations of both the London Stock Exchange, which is our primary listing, and the New York Stock Exchange. Our NYSE listing as a foreign private issuer brings us under the ambit of the Securities and Exchange Commission, and means that we have made the significant investment required to comply with US regulations including the applicable requirements of the Sarbanes-Oxley Act. Like many listed companies, Smith+Nephew works hard to adapt to a changing landscape of regulation and reporting requirements, all of which seem to have one result in common: significantly more lengthy Annual Reports. But whilst companies can adapt to evolving and greater reporting requirements, be it on audit or environmental or social issues, what they cannot manage is operating within a framework which does not allow them to recruit and retain the management they need to grow. Visiting our Advanced Wound Management R&D and manufacturing facility in Hull, UK 37.5¢ Dividend unchanged Smith+Nephew Annual Report 2023 5 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Smith+Nephew has a proud British heritage – our Company was founded in Hull in 1856 and we have grown over the last 168 years to become a truly global organisation with over 18,000 employees operating in around 100 countries. As a result of that success and global growth, the UK accounts for around 3% of our revenues and 7% of our employees, whilst over 50% of our revenues arise in the US, and nearly all of our senior operational managers, including our CEO, are US citizens, and based in the US. Pay practices differ widely around the world, and it is axiomatic and uncontroversial that companies pay their management teams in line with the norms of the country where they live and work. This approach is accepted without qualm by stakeholders for the millions of people which businesses such as Smith+Nephew employ around the world, with one exception: Executive Directors who are expected to be paid by reference to the norms of the country in which their employer has its primary listing, irrespective of where they actually live, work, and pay tax. This is unique to a listed company environment, and of course does not apply to privately-owned businesses. Currently our remuneration policies for Executive Directors are aligned to the norms of people living and working in the UK; given the small proportion of our revenues that arise in the UK, and the fact that the centre of gravity of the MedTech industry is in the US, this is not sustainable if we are to attract and retain people who live and work in the US. It is for this reason that our Chair of Remuneration, Angie Risley, and I have had extensive consultations with our largest investors in recent months and they have confirmed their broad support for our proposals to give Smith+Nephew the ability to attract and retain senior executives in the United States, if we need to do so. Our 2024 Remuneration Policy proposes a package of long-term incentive plan adjustments for US-based executives to be more closely aligned with norms in the US in terms of structure and quantum, and a comprehensive discussion of our proposals is set out on pages 121–135 of our Remuneration Report. The Board strongly believes that these proposals are in the best interests of the Company and that they will help the Board to execute on its priority to ensure the Company is led by a first-class management team. In other issues pertaining to governance and people, we are committed to fostering diversity in its broadest sense and we continue to ensure that our Board membership draws from a wide range of backgrounds and cultures. Our Board is truly multi-cultural and includes members who are from, live, or work in the US, UK, China, India, Germany and Poland. We continue to review the composition of the Board on an ongoing basis; we actively review diversity in addition to skillsets and capabilities as part of our Board succession planning process and ensure that our candidate selection process for new Board members comprises a balanced slate of candidates for consideration. We consider diversity of candidates on every appointment and selection is based on ensuring we have the best person for the role. When Anne-Françoise steps down from the Board in 2024 our Board will continue to have three experienced female Directors (Angie Risley, Katarzyna Mazur-Hofsaess and Jo Hallas), acknowledging that our percentage of female Board members will, in the short term, reduce from 33.3% to 27.3%. Our Board succession plan will seek to address this as other NEDs step down from the Board. We have announced a number of other changes to our Board this year. I would like to thank Rick Medlock and Erik Engstrom for their highly-effective service. Erik stepped down after nine years on 31 December 2023 and Rick has confirmed to the Board that he will not submit himself for re-election at our AGM in May 2024. In their place, Jez Maiden and Simon Lowth, both of whom have extensive executive and non-executive experience within large and complex global companies, have joined the Board. Until recently, Jez was CFO of Croda International and has held a number of non-executive roles including as Senior Independent Director at Travis Perkins plc. As announced, Jez will assume the role of Chair of our Audit Committee with effect from 1 March 2024. Simon is CFO of BT Group and has previously served as a non-executive director of Standard Chartered. I am delighted that our Board has been able to attract such strong candidates to continue to encourage diversity of perspective and experience on its Board. Taken in the round, I believe that your Board has the skills, diversity, strength and experience to operate effectively in the interests of all stakeholders. You can find more information on our Board and Committees and their work in our Governance Report starting on page 88 of this Annual Report. The Board also places strong emphasis on being a good corporate citizen, supporting our communities and reducing our impact on the planet and its resources. During the year we reviewed progress across our ESG strategy, and welcomed the establishment of a new governance structure and strengthened leadership in this area. More information on our progress against our sustainability targets, including our roadmap to net zero, can be found on pages 52–66. Chair’s statement continued 6 Smith+Nephew Annual Report 2023 |

| 2023 performance 2023 saw Smith+Nephew make progress both in terms of operational performance and financial results. Revenue grew at 6.4% on a reported basis which equates to 7.2% on an underlying basis.1 Trading profit margin1 was slightly ahead of the prior year, but the strong top-line growth meant that trading profit1 grew 7.6% on a reported basis. Operating profit was $425 million, with an operating profit margin of 7.7%. Cash generation from operations improved over the prior year, but was below where it should be going forward. Having considered the performance in the round, and the ongoing investments, the Board is recommending a final dividend of 23.1¢ per share. Together with the interim dividend of 14.4¢ per share, this will give a total distribution of 37.5¢ per share, unchanged from 2022. Our colleagues Before looking ahead in the Outlook, I want to pay tribute on behalf of the Board to our Smith+Nephew colleagues. Having worked in several large and global businesses during some 40 years of executive life, I think I know what good looks like when it comes to corporate culture, and I have been deeply impressed by the resilience, commitment and skill of my colleagues. They have had many dragons to wrestle with in recent years, not the least of which has been a number of leadership changes with their attendant uncertainties and distractions. Throughout they have remained focused on their purpose of helping people to take the limits off living and restore and promote health and wellbeing. I know the Board respects and is deeply grateful for their hard work, and is proud to be part of the same team. Outlook: building momentum Deepak has set out a confident outlook as he leads the business in the Strategy for Growth and the second year of delivery of the 12-Point Plan, and the Board is encouraged by the accountability shown and the progress the business has made in 2023, and excited by the prospects for the future. We look forward to welcoming shareholders to our Annual General Meeting in person in May and to updating you further on the transformation underway at Smith+Nephew. Yours sincerely, Rupert Soames, OBE Chair »See page 88 for our Governance Report »See page 121 for our Remuneration Policy 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. Smith+Nephew Annual Report 2023 7 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

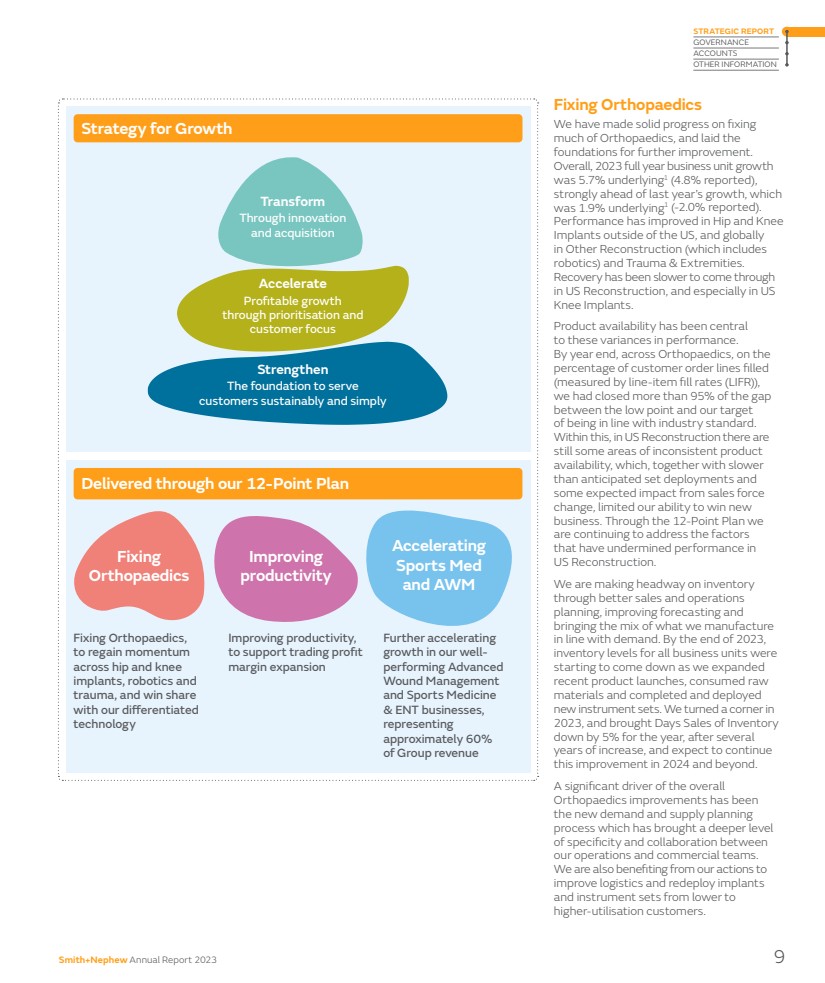

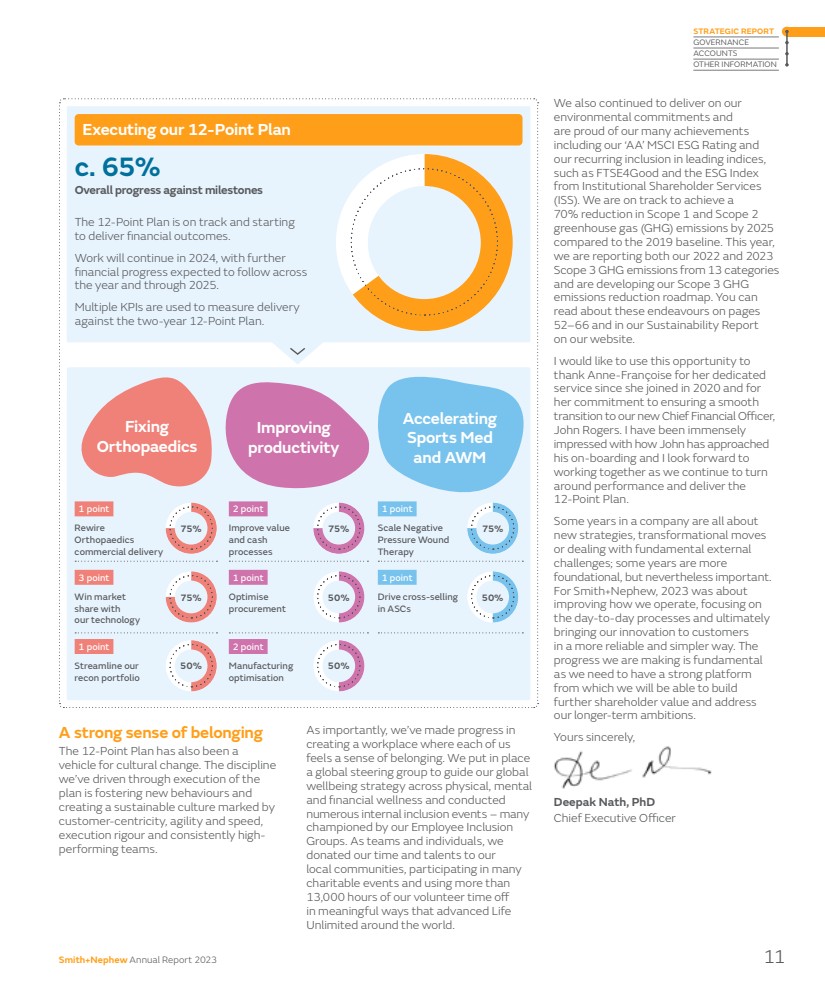

| Chief Executive Officer’s review Strong revenue growth and improved trading profit margin “The progress we are making is fundamental as we need to have a strong platform from which we will be able to build further shareholder value.” Deepak Nath, PhD Chief Executive Officer Dear Fellow Shareholder, In 2023 we delivered strong revenue growth and an improved trading profit margin1 as the results of our actions to transform Smith+Nephew started to come through. Our 12-Point Plan is on track, with progress beginning to translate into financial outcomes, and our innovation strategy is delivering a strong pipeline of new products that we expect to drive performance in the next few years and beyond. 2023 performance Group revenue in 2023 was $5,549 million, an increase of 7.2% on an underlying basis1 (6.4% reported). This growth was ahead of our full-year guidance published in February 2023 for underlying1 revenue growth between 5.0% and 6.0%, and reflects the strength of the portfolio, with all three business units delivering underlying1 growth above 5% for the full year. Operating profit was $425 million, with an operating profit margin of 7.7%. Trading profit1 for 2023 was up 7.6% on a reported basis to $970 million. The trading profit margin1 was 17.5%, a 20bps improvement on the prior year and in line with our full-year guidance. 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. Transforming Smith+Nephew In July 2022, we announced our 12-Point Plan to fundamentally change the way Smith+Nephew operates, accelerating delivery of our Strategy for Growth and transforming to a consistently higher-growth company. The 12-Point Plan is focused on: 1. Fixing Orthopaedics, to regain momentum across hip and knee implants, robotics and trauma, and win share with our differentiated technology; 2. Improving productivity, to support trading profit margin expansion; and 3. Further accelerating growth in our already well-performing Advanced Wound Management and Sports Medicine & ENT business units. Since inception we have measured our progress across the 12-Point Plan through a set of internal KPIs to drive accountability. The 12-Point Plan is on track and starting to deliver financial outcomes. Work will continue in 2024, with further financial progress expected to follow across the year and in 2025. 8 Smith+Nephew Annual Report 2023 |

| Fixing Orthopaedics We have made solid progress on fixing much of Orthopaedics, and laid the foundations for further improvement. Overall, 2023 full year business unit growth was 5.7% underlying1 (4.8% reported), strongly ahead of last year’s growth, which was 1.9% underlying1 (-2.0% reported). Performance has improved in Hip and Knee Implants outside of the US, and globally in Other Reconstruction (which includes robotics) and Trauma & Extremities. Recovery has been slower to come through in US Reconstruction, and especially in US Knee Implants. Product availability has been central to these variances in performance. By year end, across Orthopaedics, on the percentage of customer order lines filled (measured by line-item fill rates (LIFR)), we had closed more than 95% of the gap between the low point and our target of being in line with industry standard. Within this, in US Reconstruction there are still some areas of inconsistent product availability, which, together with slower than anticipated set deployments and some expected impact from sales force change, limited our ability to win new business. Through the 12-Point Plan we are continuing to address the factors that have undermined performance in US Reconstruction. We are making headway on inventory through better sales and operations planning, improving forecasting and bringing the mix of what we manufacture in line with demand. By the end of 2023, inventory levels for all business units were starting to come down as we expanded recent product launches, consumed raw materials and completed and deployed new instrument sets. We turned a corner in 2023, and brought Days Sales of Inventory down by 5% for the year, after several years of increase, and expect to continue this improvement in 2024 and beyond. A significant driver of the overall Orthopaedics improvements has been the new demand and supply planning process which has brought a deeper level of specificity and collaboration between our operations and commercial teams. We are also benefiting from our actions to improve logistics and redeploy implants and instrument sets from lower to higher-utilisation customers. Transform Through innovation and acquisition Accelerate Profitable growth through prioritisation and customer focus Strengthen The foundation to serve customers sustainably and simply Strategy for Growth Fixing Orthopaedics, to regain momentum across hip and knee implants, robotics and trauma, and win share with our differentiated technology Improving productivity, to support trading profit margin expansion Further accelerating growth in our well-performing Advanced Wound Management and Sports Medicine & ENT businesses, representing approximately 60% of Group revenue Delivered through our 12-Point Plan Fixing Orthopaedics Improving productivity Accelerating Sports Med and AWM Smith+Nephew Annual Report 2023 9 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Chief Executive Officer’s review continued We have invested in improving our commercial execution. In 2023 we repositioned our offering and undertook deeper sales training for the Orthopaedics team, and enhanced our incentive plans to better align reward with performance, sales mix, robotic placement and implant pull-through. These steps are expected to help us address the performance in Hip and Knee Implants in the US, which remains a priority. At the same time, they will also ensure we sustain the progress we have delivered elsewhere. In Trauma & Extremities, where we have successfully addressed availability of product and instrument sets for our EVOS◊ Plating system, we are focused on maintaining the improved growth dynamic delivered in the second half of 2023. Improving productivity We have made good progress on our actions to improve productivity, contributing around 160bps to our 2023 trading profit margin1. Actions have included updating and standardising pricing strategies across our portfolio and reducing days sales outstanding. We are also making procurement savings to help mitigate cost inflation and drive productivity. During 2023, we deployed an enhanced supplier selection process to identify and award business to suppliers that better align to the global business unit strategies and long-term performance metrics, and better aligned global category strategies to unlock the Smith+Nephew buying power and leverage, helping to drive volume to the most preferred suppliers and reduce cost. In line with our plan, work on manufacturing optimisation is at an earlier stage, with the benefits from network simplification and cost and asset efficiencies expected to support our mid-term margin improvement targets. The underlying work is progressing, with KPIs tracking accordingly. For instance, conversion cost, which is total direct and indirect cost to convert raw materials into finished goods as a percentage of sales, started to come down in the second half. Better aligned supply and demand process has enabled us to critically assess our manufacturing capacity. From a network perspective we are reducing excess capacity, having exited one small site in France and announced the closures of two more in China and Germany. Over the last two years we have also reduced hiring and our reliance on contingent workers. Accelerating AWM and Sports Medicine The important third pillar of the 12-Point Plan is focused on building on our consistent above-market performance from our Advanced Wound Management and Sports Medicine & ENT business units. Progress is also coming through across this workstream. Our negative pressure wound therapy business is benefiting from focused additional resource behind our sales force, delivering strong growth in 2023 across both our traditional RENASYS◊ Negative Pressure Wound Therapy System and our single-use PICO◊ Negative Pressure Wound Therapy System. We are pleased with our progress across Ambulatory Surgical Centers (ASCs), as we more than tripled the pace of cross-business unit deals between our Orthopaedics and Sports Medicine businesses in 2023. Under the 12-Point Plan we have developed a coordinated approach across these business units overseen by a dedicated strategic sales team. We are building on the strong position established by our Sports Medicine business, which is already the preferred choice for a large proportion of the ASC market, and successfully introducing our Orthopaedics portfolio. Creating value through innovation Innovation through our R&D programme is central to our higher-growth ambitions. In 2023, approaching half of our full year underlying revenue growth came from products launched in the last five years. Encouragingly, some of our key growth platforms like our robotics-enabled CORI◊ Surgical System, our EVOS◊ trauma plating platform and our REGENETEN◊ Bioinductive Implant for biological healing are not only contributing to growth today, but also have multi-year runways still ahead of them as we expand applications and launch in new markets. In 2023 we delivered a good cadence of new product launches, completing 20 with development finished on a further two ahead of launch in 2024. These included expanding CORI◊ , adding functionality and AI powered planning tools. We introduced our AETOS◊ Shoulder System, an important part of our growth plans for Trauma & Extremities which will enable Smith+Nephew to compete effectively in the $1.7 billion shoulder market, which, at around 9% CAGR, is one of the fastest growing segments in Orthopaedics. In Advanced Wound Management, we are at the early stages of rolling out the new RENASYS◊ EDGE NPWT System. RENASYS◊ EDGE brings an important new option to customers looking for enhanced intuitiveness, simplicity and durability, especially important for home-care settings. We also continued to invest behind our Sports Medicine portfolio, for instance launching REGENETEN◊ in China, India and Japan. Acquisition of CartiHeal In recent years we have successfully augmented our R&D programmes with acquisitions of exciting technologies. During the year we announced another such acquisition, CartiHeal, the developer of the CARTIHEAL◊ AGILI-C◊ Cartilage Repair Implant, a novel sports medicine technology for cartilage regeneration in the knee. CARTIHEAL◊ AGILI-C◊ is an off-the-shelf one-step treatment for osteochondral (bone and cartilage) lesions with a broader indication than existing treatments. It is indicated to treat a wide patient population, including those with lesions in knees with mild to moderate osteoarthritis, a previously unaddressed condition. Our expertise in regenerative therapy and leadership in knee repair gives me great confidence that this will be a significant value creator for Smith+Nephew over the mid-term. You can read more about our R&D programme and CARTIHEAL◊ AGILI-C◊ on pages 26–29. 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. 10 Smith+Nephew Annual Report 2023 |

| We also continued to deliver on our environmental commitments and are proud of our many achievements including our ‘AA’ MSCI ESG Rating and our recurring inclusion in leading indices, such as FTSE4Good and the ESG Index from Institutional Shareholder Services (ISS). We are on track to achieve a 70% reduction in Scope 1 and Scope 2 greenhouse gas (GHG) emissions by 2025 compared to the 2019 baseline. This year, we are reporting both our 2022 and 2023 Scope 3 GHG emissions from 13 categories and are developing our Scope 3 GHG emissions reduction roadmap. You can read about these endeavours on pages 52–66 and in our Sustainability Report on our website. I would like to use this opportunity to thank Anne-Françoise for her dedicated service since she joined in 2020 and for her commitment to ensuring a smooth transition to our new Chief Financial Officer, John Rogers. I have been immensely impressed with how John has approached his on-boarding and I look forward to working together as we continue to turn around performance and deliver the 12-Point Plan. Some years in a company are all about new strategies, transformational moves or dealing with fundamental external challenges; some years are more foundational, but nevertheless important. For Smith+Nephew, 2023 was about improving how we operate, focusing on the day-to-day processes and ultimately bringing our innovation to customers in a more reliable and simpler way. The progress we are making is fundamental as we need to have a strong platform from which we will be able to build further shareholder value and address our longer-term ambitions. Yours sincerely, Deepak Nath, PhD Chief Executive Officer A strong sense of belonging The 12-Point Plan has also been a vehicle for cultural change. The discipline we’ve driven through execution of the plan is fostering new behaviours and creating a sustainable culture marked by customer-centricity, agility and speed, execution rigour and consistently high-performing teams. As importantly, we’ve made progress in creating a workplace where each of us feels a sense of belonging. We put in place a global steering group to guide our global wellbeing strategy across physical, mental and financial wellness and conducted numerous internal inclusion events – many championed by our Employee Inclusion Groups. As teams and individuals, we donated our time and talents to our local communities, participating in many charitable events and using more than 13,000 hours of our volunteer time off in meaningful ways that advanced Life Unlimited around the world. Improve value and cash processes Scale Negative Pressure Wound Therapy Optimise procurement Drive cross-selling in ASCs Manufacturing optimisation Executing our 12-Point Plan The 12-Point Plan is on track and starting to deliver financial outcomes. Work will continue in 2024, with further financial progress expected to follow across the year and through 2025. Multiple KPIs are used to measure delivery against the two-year 12-Point Plan. c. 65% Overall progress against milestones 75% 75% 75% 50% 50% 50% Rewire Orthopaedics commercial delivery 1 point 3 point Win market share with our technology Streamline our recon portfolio 2 point 1 point 1 point 2 point 1 point 1 point Fixing Orthopaedics Improving productivity Accelerating Sports Med and AWM 75% 50% Smith+Nephew Annual Report 2023 11 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| 12 Smith+Nephew Annual Report 2023 |

| Letting brothers enjoy their vacation together Life Unlimited 13 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION Smith+Nephew Annual Report 2023 |

| Our marketplace Leading positions in attractive markets Smith+Nephew competes in global markets worth around $45 billion per annum. Long-term growth drivers Influencing the development of innovative treatments and the evolution of healthcare delivery. The medical technology industry is underpinned by compelling long-term growth drivers that make it an attractive market. Demographic trends, such as an ageing population and greater levels of physical activity later in life, continue to fuel demand for healthcare services. As the global population grows older, there is a natural increase in the prevalence of chronic diseases and age-related conditions, necessitating ongoing medical care. Other lifestyle-related health conditions, such as increasing prevalence of diabetes and obesity, create further demand. Advancements in medical technology are catalysts for long-term growth in healthcare. Breakthroughs in fields like artificial intelligence and biotechnology are leading to more effective and personalised healthcare solutions. This innovation enhances patient outcomes and creates new business opportunities supporting further growth. Emerging markets Increasing healthcare demand creates opportunities and challenges for healthcare providers. In emerging markets, the long-term growth drivers have been compounded by economic development including the emergence of an increasingly prosperous middle class driving demand for better healthcare services and products. As living standards improve, people seek access to higher-quality healthcare, including advanced medical treatments and medical devices. Additionally, emerging markets may have less mature healthcare infrastructure with a pressing need for investment in healthcare technology, which benefits companies offering innovative medical solutions. Emerging markets can be more receptive to novel healthcare solutions which fosters an environment where innovative and cost-effective approaches can gain rapid acceptance. Decentralised care Promoting accessible care outside traditional hospital settings. While the medical technology market has matured in recent years, changing customer and market dynamics have created new high-growth opportunities. In many countries care is becoming more decentralised, with more procedures moving to outpatient settings such as Ambulatory Surgery Centers (ASCs) in the US. This has long been a feature of the sports medicine market, but a growing percentage of orthopaedic joint replacement cases are now completed in such settings, bringing cost and time savings for healthcare providers. The trend towards outpatient care was accelerated by Covid as providers sought to keep patients out of hospitals and also tackle procedure backlogs. POLAR3◊ Total Hip Solution 14 Smith+Nephew Annual Report 2023 |

| Seasonality Seasonality necessitates agile strategies to navigate fluctuations in demand throughout the year. There tends to be a higher volume of orthopaedic and sports medicine procedures during the winter months in our markets, when accidents and sports-related injuries are more frequent. Elective procedures tend to slow down in the summer months due to holidays. Advanced Wound Management is less impacted by seasonality due to the nature of procedures and products. At Smith+Nephew, the majority of our business is in the northern hemisphere, including approximately 50% in the US and 20% in Europe. In the US, out-of-pocket costs for health insurance plans are tied to medical expenses in a calendar year. As a result, households that have reached their annual deductible amount and/or annual out-of-pocket cap before the year’s end will find it to be cost-effective to schedule necessary procedures later in that year rather than delaying into the next year. Cost of healthcare A pressing concern globally, necessitating comprehensive strategies for sustainable healthcare delivery. Governments are focused on reducing the cost of healthcare and are sensitive to price. Medical technology companies respond through new innovation and also provide evidence supporting both the clinical and economic benefits of products. Globally, countries are focused on increasing domestic production across critical sectors, including advanced technologies and life sciences. These actions include localisation policies and export restrictions that disrupt global supply chains. Simultaneously, many countries in key emerging markets are targeting measures to lower healthcare costs and broaden accessibility, implementing price-control policies with respect to government procurement of healthcare products. In China, we saw this reflected in the introduction of volume-based procurement in some of our segments. » See pages 67–79 for more details on risks in the Risk report High regulation Stringent regulations in the medical devices industry play a crucial role in ensuring product safety, efficacy, and quality. The medical device sector is one of the world’s most heavily regulated industries providing a high cost of entry for market participants. National regulatory authorities govern the design, development, approval, manufacture, labelling, marketing and sale of healthcare products. They also review data supporting the products to ensure they are safe and perform as intended. The majority of countries require products to be authorised or registered prior to entering the market, and such authorisation or registration needs to be subsequently maintained. Regulations and industry codes govern the way the industry interacts with healthcare professionals and government officials globally, including the AdvaMed Code of Ethics and the MedTech Europe Code of Ethical Business Practice. Companies establish global compliance programmes to help employees and third-party partners comply with laws, regulations and industry codes, and often have their own codes of conduct to guide behaviour. » See page 49 for more information on our approach to compliance Smith+Nephew Annual Report 2023 15 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Our business model How we create value Through our business model we strive to transform outcomes for the patients we serve, for the clinicians and the healthcare systems we support, for the Company and our shareholders. Our Strategy for Growth focuses our efforts, and our purpose of Life Unlimited inspires us every single day. 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. People A purpose-driven culture based on authentic values committed to doing business in the right way. R&D Innovation is at the heart of our business and we prioritise investment in new products, technologies and services. Financial strength A robust balance sheet and Capital Allocation Framework balancing investments in the future and returns today. Sustainability Addressing the long-term needs of our customers, employees, communities and stakeholders, reducing our impact on the environment. Global operations Resilient manufacturing and supply chains to ensure quality and competitiveness. What we need to create value Delivering value for stakeholders 17.5% +20bps Trading profit margin¹ 7.7% -90bps Operating profit margin $327m Dividend distribution unchanged $970m +7.6% Trading profit¹ $425m -5.4% Operating profit $5,549m +6.4% reported +7.2% underlying¹ Group revenue Investors Community $5.1m Product donations 4.20 +0.08 Gallup engagement score 97,405 Training sessions Employees Customers 20 New product launches 16 Smith+Nephew Annual Report 2023 |

| How we create value Innovative technology We offer a broad portfolio of differentiated products and services that meet often-complex clinical needs, including digital and robotic technologies, driving procedural innovation. Product development and acquisition R&D model that provides for customer and business unit focused innovation and acquiring technologies needing further development and commercialisation. Expertise and support Our sales force supports customers and works with healthcare systems to address complex business and reimbursement requirements. Medical education Through the Smith+Nephew Academy, a network of centres and online resources, we provide medical education programmes to support the safe and effective use of our products, skills development and procedural innovation. Go to market Three global business units set product strategy and deliver global marketing to drive demand in our markets, supported by clinical evidence to demonstrate efficacy. Customer feedback Building close relationships with customers to ensure a deep understanding of unmet clinical needs and changing financial and sustainability priorities within healthcare systems. 6 2 5 3 4 1 Customer centricity Smith+Nephew Annual Report 2023 17 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

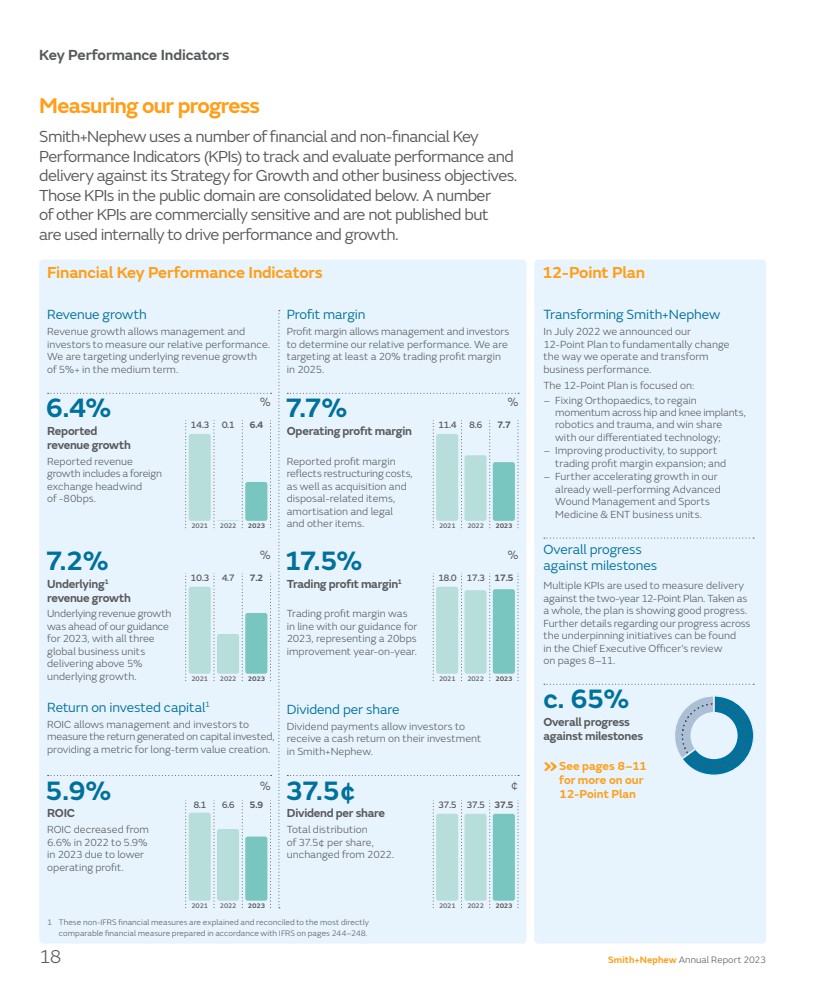

| 5.9% ROIC Key Performance Indicators Measuring our progress Smith+Nephew uses a number of financial and non-financial Key Performance Indicators (KPIs) to track and evaluate performance and delivery against its Strategy for Growth and other business objectives. Those KPIs in the public domain are consolidated below. A number of other KPIs are commercially sensitive and are not published but are used internally to drive performance and growth. Revenue growth Reported revenue growth includes a foreign exchange headwind of -80bps. Revenue growth allows management and investors to measure our relative performance. We are targeting underlying revenue growth of 5%+ in the medium term. Underlying revenue growth was ahead of our guidance for 2023, with all three global business units delivering above 5% underlying growth. Profit margin Reported profit margin reflects restructuring costs, as well as acquisition and disposal-related items, amortisation and legal and other items. Profit margin allows management and investors to determine our relative performance. We are targeting at least a 20% trading profit margin in 2025. Trading profit margin was in line with our guidance for 2023, representing a 20bps improvement year-on-year. Financial Key Performance Indicators Return on invested capital1 ROIC decreased from 6.6% in 2022 to 5.9% in 2023 due to lower operating profit. ROIC allows management and investors to measure the return generated on capital invested, providing a metric for long-term value creation. Dividend per share Total distribution of 37.5¢ per share, unchanged from 2022. Dividend payments allow investors to receive a cash return on their investment in Smith+Nephew. 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. 6.4% Reported revenue growth 7.7% Operating profit margin 7.2% Underlying1 revenue growth 17.5% Trading profit margin1 37.5¢ Dividend per share % % ¢ % % % 12-Point Plan Transforming Smith+Nephew In July 2022 we announced our 12-Point Plan to fundamentally change the way we operate and transform business performance. The 12-Point Plan is focused on: – Fixing Orthopaedics, to regain momentum across hip and knee implants, robotics and trauma, and win share with our differentiated technology; – Improving productivity, to support trading profit margin expansion; and – Further accelerating growth in our already well-performing Advanced Wound Management and Sports Medicine & ENT business units. »See pages 8–11 for more on our 12-Point Plan 2021 10.3 2023 7.2 2022 4.7 2021 18.0 2023 17.5 2022 17.3 2021 8.1 2023 5.9 2022 6.6 2021 14.3 2023 6.4 2022 0.1 2021 11.4 2023 7.7 2022 8.6 2021 37.5 2023 37.5 2022 37.5 c. 65% Overall progress against milestones Overall progress against milestones Multiple KPIs are used to measure delivery against the two-year 12-Point Plan. Taken as a whole, the plan is showing good progress. Further details regarding our progress across the underpinning initiatives can be found in the Chief Executive Officer’s review on pages 8–11. 18 Smith+Nephew Annual Report 2023 |

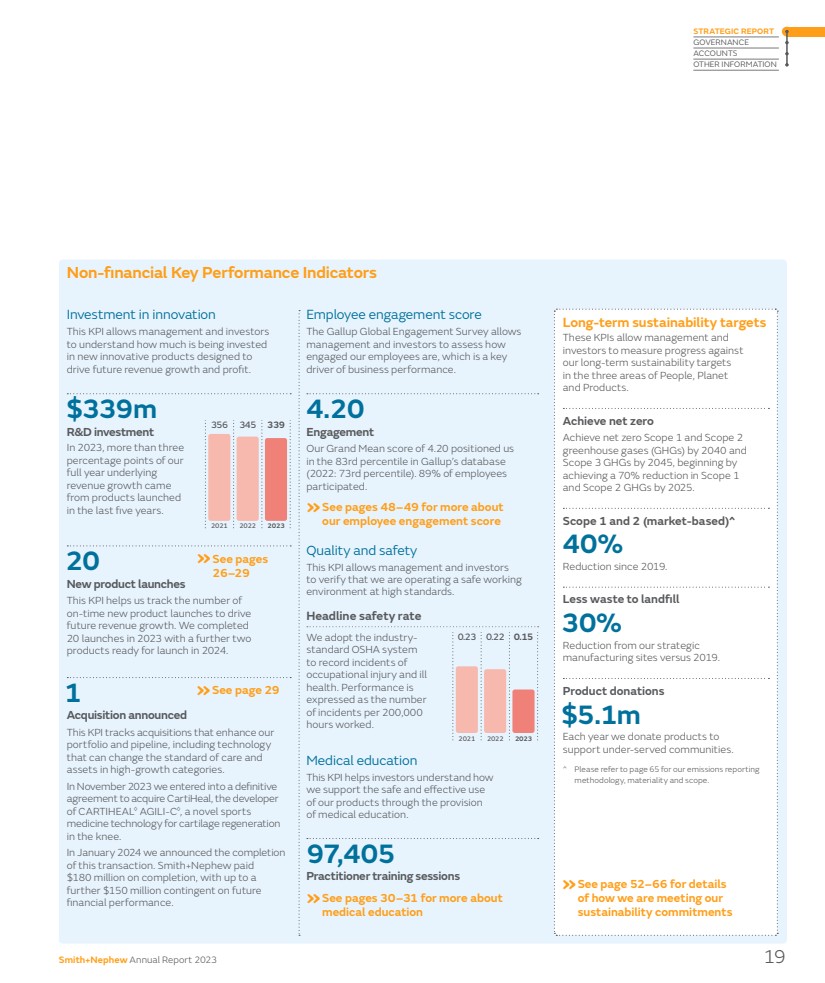

| Non-financial Key Performance Indicators Long-term sustainability targets These KPIs allow management and investors to measure progress against our long-term sustainability targets in the three areas of People, Planet and Products. Achieve net zero Achieve net zero Scope 1 and Scope 2 greenhouse gases (GHGs) by 2040 and Scope 3 GHGs by 2045, beginning by achieving a 70% reduction in Scope 1 and Scope 2 GHGs by 2025. Scope 1 and 2 (market-based) 40% Reduction since 2019. Less waste to landfill 30% Reduction from our strategic manufacturing sites versus 2019. Product donations $5.1m Each year we donate products to support under-served communities. Please refer to page 65 for our emissions reporting methodology, materiality and scope. Employee engagement score The Gallup Global Engagement Survey allows management and investors to assess how engaged our employees are, which is a key driver of business performance. 4.20 Engagement Our Grand Mean score of 4.20 positioned us in the 83rd percentile in Gallup’s database (2022: 73rd percentile). 89% of employees participated. We adopt the industry-standard OSHA system to record incidents of occupational injury and ill health. Performance is expressed as the number of incidents per 200,000 hours worked. This KPI helps investors understand how we support the safe and effective use of our products through the provision of medical education. Quality and safety This KPI allows management and investors to verify that we are operating a safe working environment at high standards. Headline safety rate Medical education 20 New product launches This KPI helps us track the number of on-time new product launches to drive future revenue growth. We completed 20 launches in 2023 with a further two products ready for launch in 2024. Investment in innovation In 2023, more than three percentage points of our full year underlying revenue growth came from products launched in the last five years. This KPI allows management and investors to understand how much is being invested in new innovative products designed to drive future revenue growth and profit. »See pages 26–29 »See pages 30–31 for more about medical education »See page 52–66 for details of how we are meeting our sustainability commitments »See pages 48–49 for more about our employee engagement score $339m R&D investment 1 Acquisition announced This KPI tracks acquisitions that enhance our portfolio and pipeline, including technology that can change the standard of care and assets in high-growth categories. In November 2023 we entered into a definitive agreement to acquire CartiHeal, the developer of CARTIHEAL◊ AGILI-C◊ , a novel sports medicine technology for cartilage regeneration in the knee. In January 2024 we announced the completion of this transaction. Smith+Nephew paid $180 million on completion, with up to a further $150 million contingent on future financial performance. 97,405 Practitioner training sessions »See page 29 2021 0.23 2023 0.15 2022 0.22 2021 356 2023 339 2022 345 Smith+Nephew Annual Report 2023 19 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Financial review 2023 performance Group revenue in 2023 was $5,549 million, an increase of 6.4% on a reported basis and 7.2% on an underlying basis1 excluding a 80bps headwind from foreign exchange, slightly above the revenue guidance range of 5.0% to 6.0% for 2023 we announced previously. The operating profit was $425 million (2022: $450 million) with an operating profit margin of 7.7% (2022: 8.6%) after acquisition and disposal related items, restructuring and rationalisation costs, amortisation and impairment of acquisition intangibles and legal and other items. Trading profit1 for 2023 was $970 million (2022: $901 million) with a trading profit margin1 of 17.5% (2022: 17.3%) reflecting improvement in revenue and productivity savings across the Group. The reported profit before tax was $290 million (2022: $235 million) after adjusting for an impairment related to Engage Surgical. We acquired this business in 2022 for a maximum consideration of $135 million payable in cash. The provisional fair value consideration was $131 million and included $32 million of contingent consideration. During 2023, management evaluated the commercial viability of Engage products and concluded that they should be discontinued. A total of $109 million of Engage’s assets and liabilities were written off as a result of this action. Efficiency and 12-Point Plan progress We have made significant progress in our 12-Point Plan to fundamentally change the way we operate and transform business performance, especially our activities to fix Orthopaedics and improve productivity. This was reflected in our improved financial performance for 2023. In 2023, restructuring costs totalled $220 million, including costs related to the efficiency and productivity under the 12-Point Plan. Overall, incremental benefits of around $68 million was recognised during the year. Strengthening our foundations Dear Fellow Shareholder, The 12-Point Plan was announced in July 2022 to improve execution and drive our Strategy for Growth. The plan focuses on fixing Orthopaedics, improving productivity and accelerating growth in Advanced Wound Management and Sports Medicine through 12 initiatives, which have underpinned our improved performance in 2023. “The 12-Point Plan is beginning to translate into improved financial outcomes in 2023.” Anne-Françoise Nesmes Chief Financial Officer 20 Smith+Nephew Annual Report 2023 |

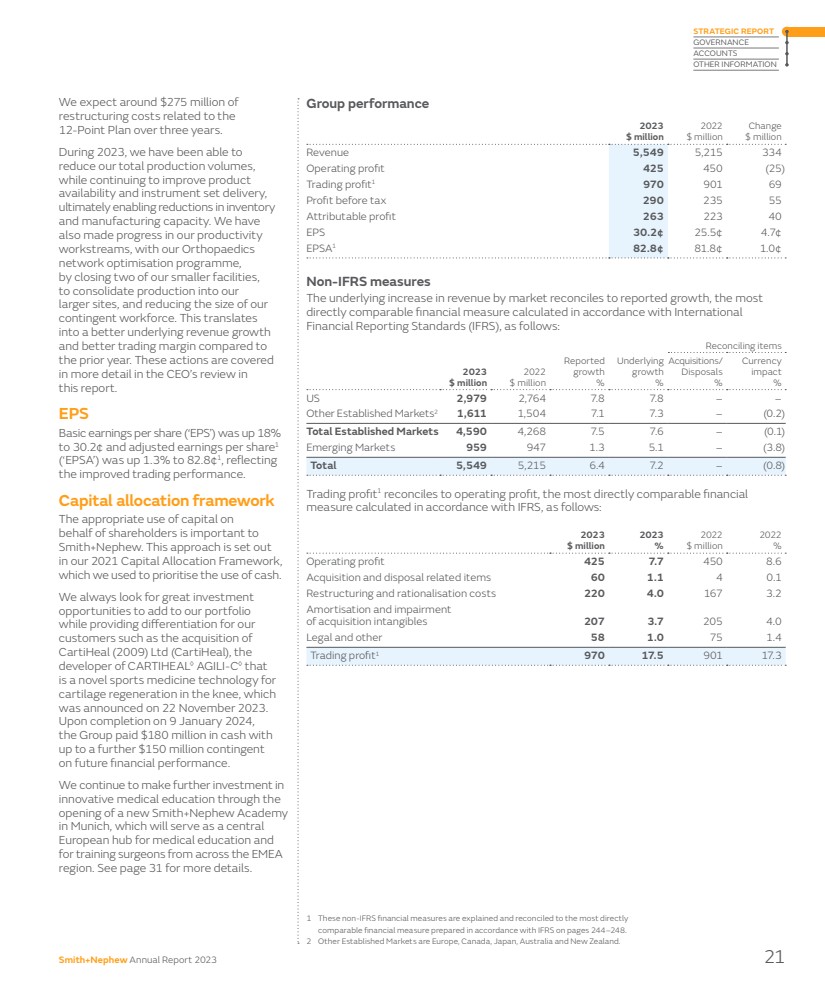

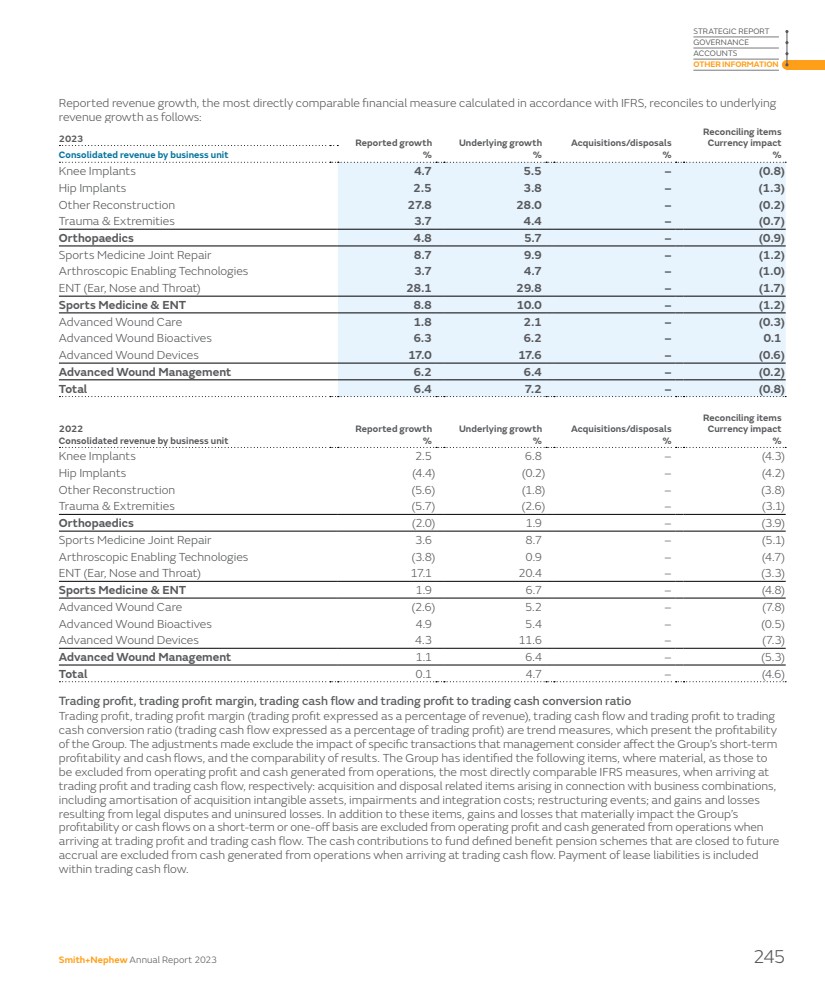

| Group performance 2023 $ million 2022 $ million Change $ million Revenue 5,549 5,215 334 Operating profit 425 450 (25) Trading profit1 970 901 69 Profit before tax 290 235 55 Attributable profit 263 223 40 EPS 30.2¢ 25.5¢ 4.7¢ EPSA1 82.8¢ 81.8¢ 1.0¢ Non-IFRS measures The underlying increase in revenue by market reconciles to reported growth, the most directly comparable financial measure calculated in accordance with International Financial Reporting Standards (IFRS), as follows: 2023 $ million 2022 $ million Reported growth % Underlying growth % Reconciling items Acquisitions/ Disposals % Currency impact % US 2,979 2,764 7.8 7.8 – – Other Established Markets2 1,611 1,504 7.1 7.3 – (0.2) Total Established Markets 4,590 4,268 7.5 7.6 – (0.1) Emerging Markets 959 947 1.3 5.1 – (3.8) Total 5,549 5,215 6.4 7.2 – (0.8) Trading profit1 reconciles to operating profit, the most directly comparable financial measure calculated in accordance with IFRS, as follows: 2023 $ million 2023 % 2022 $ million 2022 % Operating profit 425 7.7 450 8.6 Acquisition and disposal related items 60 1.1 4 0.1 Restructuring and rationalisation costs 220 4.0 167 3.2 Amortisation and impairment of acquisition intangibles 207 3.7 205 4.0 Legal and other 58 1.0 75 1.4 Trading profit1 970 17.5 901 17.3 We expect around $275 million of restructuring costs related to the 12-Point Plan over three years. During 2023, we have been able to reduce our total production volumes, while continuing to improve product availability and instrument set delivery, ultimately enabling reductions in inventory and manufacturing capacity. We have also made progress in our productivity workstreams, with our Orthopaedics network optimisation programme, by closing two of our smaller facilities, to consolidate production into our larger sites, and reducing the size of our contingent workforce. This translates into a better underlying revenue growth and better trading margin compared to the prior year. These actions are covered in more detail in the CEO’s review in this report. EPS Basic earnings per share (‘EPS’) was up 18% to 30.2¢ and adjusted earnings per share1 (‘EPSA’) was up 1.3% to 82.8¢1, reflecting the improved trading performance. Capital allocation framework The appropriate use of capital on behalf of shareholders is important to Smith+Nephew. This approach is set out in our 2021 Capital Allocation Framework, which we used to prioritise the use of cash. We always look for great investment opportunities to add to our portfolio while providing differentiation for our customers such as the acquisition of CartiHeal (2009) Ltd (CartiHeal), the developer of CARTIHEAL◊ AGILI-C◊ that is a novel sports medicine technology for cartilage regeneration in the knee, which was announced on 22 November 2023. Upon completion on 9 January 2024, the Group paid $180 million in cash with up to a further $150 million contingent on future financial performance. We continue to make further investment in innovative medical education through the opening of a new Smith+Nephew Academy in Munich, which will serve as a central European hub for medical education and for training surgeons from across the EMEA region. See page 31 for more details. 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. 2 Other Established Markets are Europe, Canada, Japan, Australia and New Zealand. Smith+Nephew Annual Report 2023 21 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

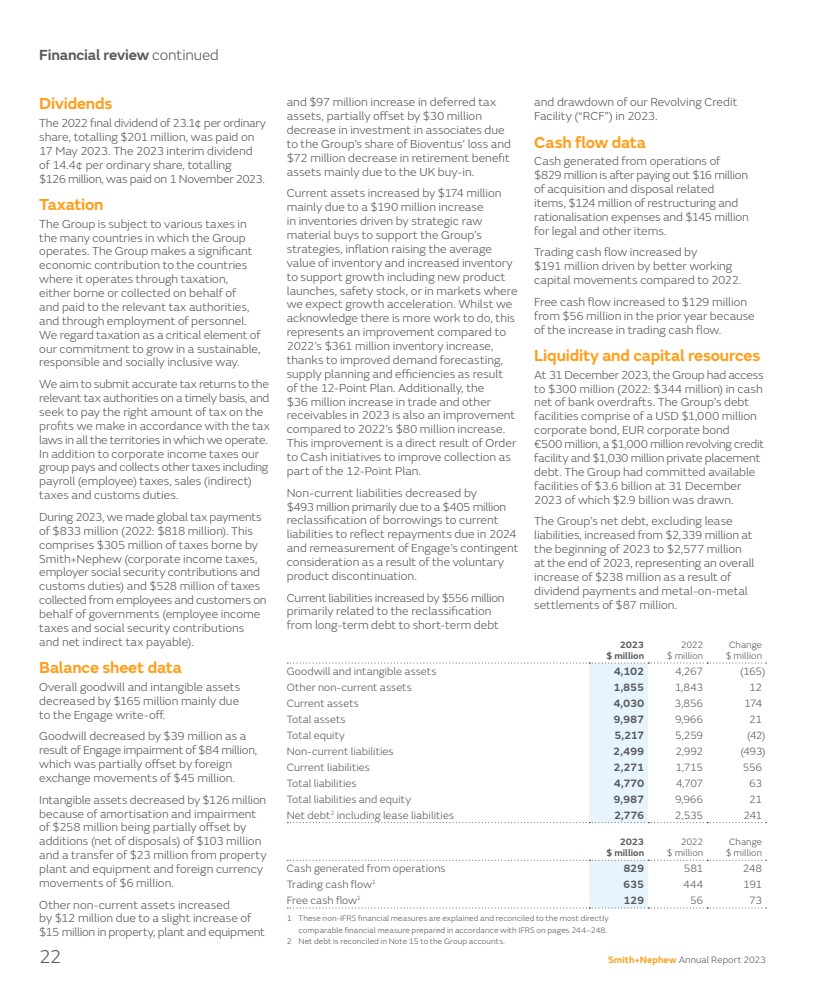

| Financial review continued 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. 2 Net debt is reconciled in Note 15 to the Group accounts. and $97 million increase in deferred tax assets, partially offset by $30 million decrease in investment in associates due to the Group’s share of Bioventus’ loss and $72 million decrease in retirement benefit assets mainly due to the UK buy-in. Current assets increased by $174 million mainly due to a $190 million increase in inventories driven by strategic raw material buys to support the Group’s strategies, inflation raising the average value of inventory and increased inventory to support growth including new product launches, safety stock, or in markets where we expect growth acceleration. Whilst we acknowledge there is more work to do, this represents an improvement compared to 2022’s $361 million inventory increase, thanks to improved demand forecasting, supply planning and efficiencies as result of the 12-Point Plan. Additionally, the $36 million increase in trade and other receivables in 2023 is also an improvement compared to 2022’s $80 million increase. This improvement is a direct result of Order to Cash initiatives to improve collection as part of the 12-Point Plan. Non-current liabilities decreased by $493 million primarily due to a $405 million reclassification of borrowings to current liabilities to reflect repayments due in 2024 and remeasurement of Engage’s contingent consideration as a result of the voluntary product discontinuation. Current liabilities increased by $556 million primarily related to the reclassification from long-term debt to short-term debt and drawdown of our Revolving Credit Facility (“RCF”) in 2023. Cash flow data Cash generated from operations of $829 million is after paying out $16 million of acquisition and disposal related items, $124 million of restructuring and rationalisation expenses and $145 million for legal and other items. Trading cash flow increased by $191 million driven by better working capital movements compared to 2022. Free cash flow increased to $129 million from $56 million in the prior year because of the increase in trading cash flow. Liquidity and capital resources At 31 December 2023, the Group had access to $300 million (2022: $344 million) in cash net of bank overdrafts. The Group’s debt facilities comprise of a USD $1,000 million corporate bond, EUR corporate bond €500 million, a $1,000 million revolving credit facility and $1,030 million private placement debt. The Group had committed available facilities of $3.6 billion at 31 December 2023 of which $2.9 billion was drawn. The Group’s net debt, excluding lease liabilities, increased from $2,339 million at the beginning of 2023 to $2,577 million at the end of 2023, representing an overall increase of $238 million as a result of dividend payments and metal-on-metal settlements of $87 million. Dividends The 2022 final dividend of 23.1¢ per ordinary share, totalling $201 million, was paid on 17 May 2023. The 2023 interim dividend of 14.4¢ per ordinary share, totalling $126 million, was paid on 1 November 2023. Taxation The Group is subject to various taxes in the many countries in which the Group operates. The Group makes a significant economic contribution to the countries where it operates through taxation, either borne or collected on behalf of and paid to the relevant tax authorities, and through employment of personnel. We regard taxation as a critical element of our commitment to grow in a sustainable, responsible and socially inclusive way. We aim to submit accurate tax returns to the relevant tax authorities on a timely basis, and seek to pay the right amount of tax on the profits we make in accordance with the tax laws in all the territories in which we operate. In addition to corporate income taxes our group pays and collects other taxes including payroll (employee) taxes, sales (indirect) taxes and customs duties. During 2023, we made global tax payments of $833 million (2022: $818 million). This comprises $305 million of taxes borne by Smith+Nephew (corporate income taxes, employer social security contributions and customs duties) and $528 million of taxes collected from employees and customers on behalf of governments (employee income taxes and social security contributions and net indirect tax payable). Balance sheet data Overall goodwill and intangible assets decreased by $165 million mainly due to the Engage write-off. Goodwill decreased by $39 million as a result of Engage impairment of $84 million, which was partially offset by foreign exchange movements of $45 million. Intangible assets decreased by $126 million because of amortisation and impairment of $258 million being partially offset by additions (net of disposals) of $103 million and a transfer of $23 million from property plant and equipment and foreign currency movements of $6 million. Other non-current assets increased by $12 million due to a slight increase of $15 million in property, plant and equipment 2023 $ million 2022 $ million Change $ million Cash generated from operations 829 581 248 Trading cash flow1 635 444 191 Free cash flow1 129 56 73 2023 $ million 2022 $ million Change $ million Goodwill and intangible assets 4,102 4,267 (165) Other non-current assets 1,855 1,843 12 Current assets 4,030 3,856 174 Total assets 9,987 9,966 21 Total equity 5,217 5,259 (42) Non-current liabilities 2,499 2,992 (493) Current liabilities 2,271 1,715 556 Total liabilities 4,770 4,707 63 Total liabilities and equity 9,987 9,966 21 Net debt2 including lease liabilities 2,776 2,535 241 22 Smith+Nephew Annual Report 2023 |

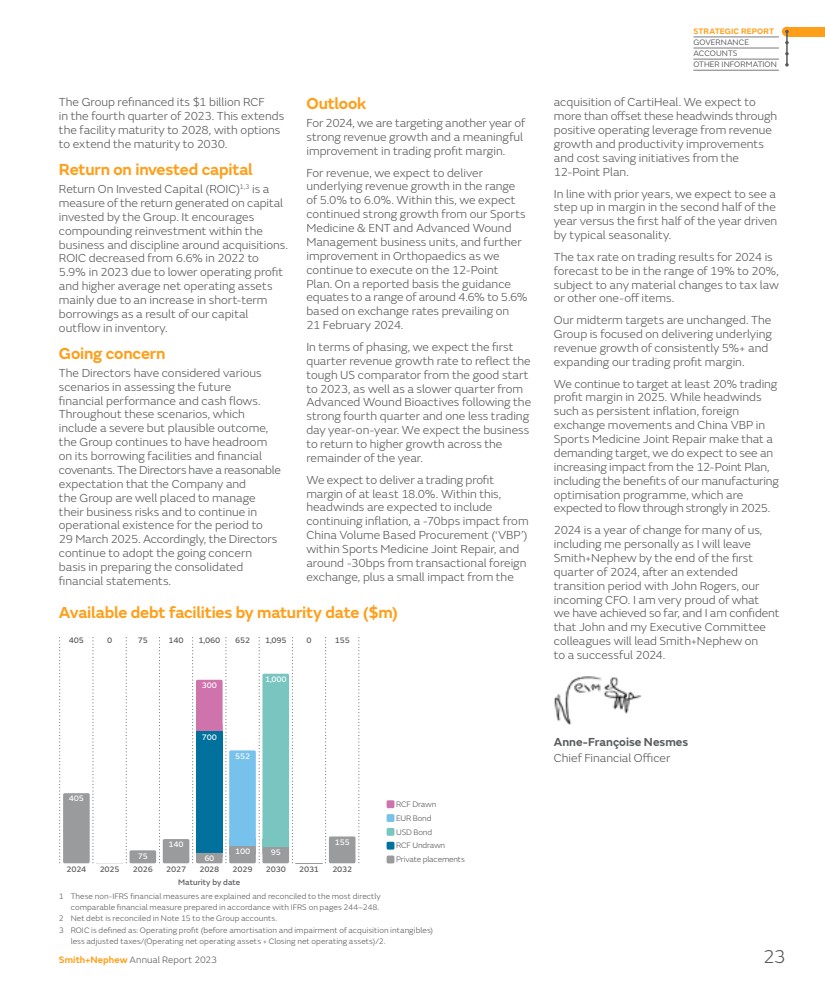

| 1 These non-IFRS financial measures are explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS on pages 244–248. 2 Net debt is reconciled in Note 15 to the Group accounts. 3 ROIC is defined as: Operating profit (before amortisation and impairment of acquisition intangibles) less adjusted taxes/(Operating net operating assets + Closing net operating assets)/2. The Group refinanced its $1 billion RCF in the fourth quarter of 2023. This extends the facility maturity to 2028, with options to extend the maturity to 2030. Return on invested capital Return On Invested Capital (ROIC)1,3 is a measure of the return generated on capital invested by the Group. It encourages compounding reinvestment within the business and discipline around acquisitions. ROIC decreased from 6.6% in 2022 to 5.9% in 2023 due to lower operating profit and higher average net operating assets mainly due to an increase in short-term borrowings as a result of our capital outflow in inventory. Going concern The Directors have considered various scenarios in assessing the future financial performance and cash flows. Throughout these scenarios, which include a severe but plausible outcome, the Group continues to have headroom on its borrowing facilities and financial covenants. The Directors have a reasonable expectation that the Company and the Group are well placed to manage their business risks and to continue in operational existence for the period to 29 March 2025. Accordingly, the Directors continue to adopt the going concern basis in preparing the consolidated financial statements. Outlook For 2024, we are targeting another year of strong revenue growth and a meaningful improvement in trading profit margin. For revenue, we expect to deliver underlying revenue growth in the range of 5.0% to 6.0%. Within this, we expect continued strong growth from our Sports Medicine & ENT and Advanced Wound Management business units, and further improvement in Orthopaedics as we continue to execute on the 12-Point Plan. On a reported basis the guidance equates to a range of around 4.6% to 5.6% based on exchange rates prevailing on 21 February 2024. In terms of phasing, we expect the first quarter revenue growth rate to reflect the tough US comparator from the good start to 2023, as well as a slower quarter from Advanced Wound Bioactives following the strong fourth quarter and one less trading day year-on-year. We expect the business to return to higher growth across the remainder of the year. We expect to deliver a trading profit margin of at least 18.0%. Within this, headwinds are expected to include continuing inflation, a -70bps impact from China Volume Based Procurement (‘VBP’) within Sports Medicine Joint Repair, and around -30bps from transactional foreign exchange, plus a small impact from the acquisition of CartiHeal. We expect to more than offset these headwinds through positive operating leverage from revenue growth and productivity improvements and cost saving initiatives from the 12-Point Plan. In line with prior years, we expect to see a step up in margin in the second half of the year versus the first half of the year driven by typical seasonality. The tax rate on trading results for 2024 is forecast to be in the range of 19% to 20%, subject to any material changes to tax law or other one-off items. Our midterm targets are unchanged. The Group is focused on delivering underlying revenue growth of consistently 5%+ and expanding our trading profit margin. We continue to target at least 20% trading profit margin in 2025. While headwinds such as persistent inflation, foreign exchange movements and China VBP in Sports Medicine Joint Repair make that a demanding target, we do expect to see an increasing impact from the 12-Point Plan, including the benefits of our manufacturing optimisation programme, which are expected to flow through strongly in 2025. 2024 is a year of change for many of us, including me personally as I will leave Smith+Nephew by the end of the first quarter of 2024, after an extended transition period with John Rogers, our incoming CFO. I am very proud of what we have achieved so far, and I am confident that John and my Executive Committee colleagues will lead Smith+Nephew on to a successful 2024. Anne-Françoise Nesmes Chief Financial Officer Available debt facilities by maturity date ($m) 2025 0 0 405 2024 405 300 2026 75 75 2027 140 140 2028 1,060 700 300 60 2029 652 100 552 2030 1,095 95 1,000 2031 0 155 2032 155 EUR Bond RCF Drawn USD Bond RCF Undrawn Private placements Maturity by date Smith+Nephew Annual Report 2023 23 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Getting grandparents back to playing with their grandchildren Life Unlimited 24 Smith+Nephew Annual Report 2023 |

| Smith+Nephew Annual Report 2023 25 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Research & Development A long history of transformative innovation Creating value through innovation JOURNEY◊ II: JOURNEY II TKA has been demonstrated to restore anatomical shape, position and motion.*1,2 This anatomical restoration can provide superior clinical outcomes and higher patient satisfaction.** 3–7 Smith+Nephew has a long and proud history of transformative innovation, dating back to our founding in 1856. In the recent past we shaped clinical practice and helped to deliver our purpose of Life Unlimited to millions of patients. In Orthopaedics, products such as our kinematic knee, JOURNEY◊ II, have brought more natural motion to joint replacement. In Sports Medicine our products have been instrumental in enabling arthroscopic repair where previously open surgery was the standard of care. And in wound care, Smith+Nephew’s PICO◊ single-use Negative Pressure Wound Management System has revolutionised the availability of this important treatment option. Over decades, we have repeatedly brought technologies to market that have disrupted established approaches and changed the standard of care.” Vasant Padmanabhan President of Research & Development and ENT $339m Invested in R&D in 2023 20 New products launched in 2023 Smith+Nephew’s innovation pipeline is a material contributor to our revenue growth, with approaching 50% of our 2023 underlying revenue growth coming from recent product launches. We expect this trend to continue as we drive innovation across our business. » For a full list of references see pages 262–264 26 Smith+Nephew Annual Report 2023 |

| CORI◊ Digital Tensioner The CORI◊ Digital Tensioner was designed to address different demographics, making this product ergonomically suitable for female and male surgeons. This approach to innovation is helping remove barriers and limitations traditionally associated with orthopaedic surgical equipment. Addressing unmet clinical needs Today, there are still significant unmet clinical needs. These needs can be for the patient, in terms of satisfaction, clinical outcomes and reduction in complications, or for the healthcare system with costs of existing treatments or of unaddressed problems. For instance, in knee replacement, 80% of recipients state that their new knee feels ‘artificial’,8 while in Sports Medicine, the re-tear rates associated with repair of large full thickness rotator cuff tears exceeds 50%.9 In ENT, almost one in 16 children undergoing total tonsillectomies have post-procedure haemorrhages,10 and in wound care the treatment for surgical site infections costs the US healthcare system more than $3 billion per year.11 These challenges, and many others like them, inspire us to invest in developing the next generation of products and services that will continue to advance clinical practice and improve outcomes for patients and payers. We are helping to shape an innovation environment that is driven by four key trends. – Robotics and digital systems enable a degree of accuracy and personalisation of procedures that has not been possible in the past. – Biologics technology is developing rapidly and enables different types of treatments – including fully restoring tissue and function. – Procedural innovation is focused on less invasive and tissue sparing methods that can improve recovery times. – Healthcare costs require greater focus on delivering compelling value and health economic benefits. Smith+Nephew’s R&D team is focused on growth segments where we can deploy our expertise in such fast developing areas of innovation, and deliver novel solutions that address unmet clinical needs. Inspiration for new products comes from observing our customers, working with healthcare professionals on design and development, acquiring technologies needing further development and commercialisation, and our co-development partners. New products are developed using a rigorous phase-gate process starting with business case review and ending with launch readiness. We also strive to embed sustainability principles into our design and packaging. Designing a world-class user experience Users perform better when they believe they are working with best-in-class equipment. In the context of product design, devices are typically considered best-in-class when they are recognised as being developed by an industry-leading brand and exhibit a compelling and purposeful user experience. Within R&D our Human Factors team strives to bring a unique user experience to product development, encompassing a common high-quality look, feel and sound across the entire portfolio of instruments and digital systems. Their philosophy is that each product should be considered a Smith+Nephew brand ambassador, expressing excellence and encouraging ease-of-use and familiarity. Smith+Nephew Annual Report 2023 27 STRATEGIC REPORT GOVERNANCE ACCOUNTS OTHER INFORMATION |

| Creating value through innovation continued Research & Development continued New products in 2023 Innovation is central to our higher-growth ambitions In 2023 we launched 20 new products, with development complete on a further two ahead of their launch in 2024. Investing in robotics and AI Our CORI◊ Surgical System is the only robotics-assisted system indicated for partial, total and revision knees. During 2023 we continued to add features and functionality. The CORI◊ Digital Tensioner is a proprietary device for soft tissue balancing in knee replacement, and the only tensioner for robotics-assisted surgery. This helps make planning more objective and eliminates inconsistencies in surgery from current manual or mechanical tools. Personalized Planning powered by AI and the RI.INSIGHTS◊ Data Visualization Platform on CORI◊ transform data into contextual intelligence by enabling surgeons to better understand how pre-operative surgical plans and intra-operative decision making link to post-operative outcomes. A new saw solution added versatility, appealing to a broader range of surgeons. CORI◊ is the only solution to offer robotics-assisted burring and saw bone-cutting options. This development was accelerated as part of our 12-Point Plan. New shoulder system In 2023 we launched our AETOS◊ Shoulder System. We acquired this technology in early 2021 and it is an important part of our growth plans for Trauma & Extremities. AETOS◊ is designed with both patient and surgeon benefits in mind. For example, the MetaStem aligns with the market trend towards minimally invasive short stem devices. Short stems are easier to implant, have improved bone preservation, and are a better fit to anatomy. AETOS◊ will enable Smith+Nephew to compete effectively in the $1.7 billion12 shoulder repair market, which, at around 9% compound annual growth rate, is one of the fastest growing segments in Orthopaedics. AETOS◊ Shoulder System CORI Surgical System 28 Smith+Nephew Annual Report 2023 |