Use these links to rapidly review the document

TABLE OF CONTENTS

SPROTT PHYSICAL PLATINUM AND PALLADIUM TRUST INDEX TO FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

OR |

||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2012 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

OR |

||

o |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Date of event requiring this shell company report: Not applicable

Commission file number: 001-34928

| SPROTT PHYSICAL PLATINUM AND PALLADIUM TRUST (Exact name of Registrant as specified in its charter) |

(Translation of Registrant's name into English) |

PROVINCE OF ONTARIO, CANADA (Jurisdiction of incorporation or organization) |

Suite 2700, South Tower, Royal Bank Plaza 200 Bay Street Toronto, Ontario Canada M5J 2J1 (Address of principal executive offices) |

Kirstin H. McTaggart (416) 362-7172 kmctaggart@sprott.com Suite 2700, South Tower Royal Bank Plaza 200 Bay Street Toronto, Ontario Canada M5J 2J1 (Name, telephone, e-mail and/or facsimile number and address of company contact person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

Units |

NYSE Arca |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2012, there were 28,000,000 units outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o |

Yes | ý | No |

If this report is an annual report or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

o |

Yes | ý | No |

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

ý |

Yes | o | No |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

o |

Yes | o | No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of accelerated filer and large accelerated filer in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

o | Accelerated filer | o | Non-accelerated filer | ý |

Indicate by check mark which basis of accounting the Registrant has used to prepare the financial statements included in this filing.

o |

U.S. GAAP | ý | International Financial Reporting Standards as issued by the International Accounting Standards Board | o | Other |

If "Other" has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o |

Item 17 | o | Item 18 |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o |

Yes | ý | No |

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Matters discussed in this document may constitute forward-looking statements.

The Private Securities Litigation Reform Act of 1995 provides safe harbor protections for forward-looking statements in order to encourage companies to provide prospective information about their business. Forward-looking statements include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and other statements, which are other than statements of historical facts.

Please note in this annual report, "we", "us", "our", "the Trust", and "Sprott" all refer to Sprott Physical Platinum and Palladium Trust.

Sprott Physical Platinum and Palladium Trust, or the Trust, desires to take advantage of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and is including this cautionary statement in connection with this safe harbor legislation. This document and any other written or oral statements made by us or on our behalf may include forward-looking statements, which reflect our current views with respect to future events and financial performance. The words "anticipate", "believe", "continue", "could", "estimate", "expect", "intend", "may", "might", "plan", "possible", "potential", "predict", "project", "forecast", "should", "would" and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this annual report may include, for example, statements about:

- •

- the Trust's objectives and strategies to achieve the objectives;

- •

- success in retaining or recruiting, or changes required in, the officers or key employees of the Sprott Asset

Management LP, to whom we will refer as the Manager; and

- •

- the platinum and palladium industries, sources of and demand for platinum and palladium, and the performance of the platinum and palladium markets.

The forward-looking statements in this document are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, managements examination of historical operating trends, data contained in our records and other data available from third parties. Although we believe that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies which are difficult or impossible to predict and are beyond our control, we cannot assure you that we will achieve or accomplish these expectations, beliefs or projections. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Trust's control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include those factors described under the heading "Risk Factors". Should one or more of these risks or uncertainties materialize, or should any of the Trust's or the Manager's assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Trust has included in this document material risks known to it; however, there may be other, unknown risks or risks that the Trust currently deems immaterial that may adversely affect the actual results of the Trust. Each of the Trust and the Manager undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

ii

ITEM 1 — IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2 — OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

A. Selected Financial Data

The following table summarizes our selected historical financial information at the dates and for the periods indicated prepared in conformity with the International Financial Reporting Standards as issued by the International Accounting Standards Board, to which we will refer as IFRS. The statement of operations data for the period from January 1, 2012 to December 31, 2012 and the balance sheet data as of December 31, 2012 have been derived from our audited financial statements included elsewhere in this 2012 Annual Report. The selected financial data should be read in conjunction with Item 5, Operating and Financial Review and Prospects, the financial statements, related notes, and other financial information included elsewhere in this 2012 Annual Report.

SPROTT PHYSICAL PLATINUM AND PALLADIUM TRUST

STATEMENT OF FINANCIAL POSITION

As at December 31, 2012

Statement of financial position

|

|

|

|||||

|---|---|---|---|---|---|---|---|

| |

As at December 31, 2012 |

As at December 31, 2011 |

|||||

| |

$ |

$ |

|||||

Assets |

|||||||

Cash (note 6) |

153,348,584 | 10 | |||||

Bullion |

244,536,496 | — | |||||

Total assets |

397,885,080 | 10 | |||||

Liabilities |

|||||||

Due to brokers |

135,274,906 | — | |||||

Accounts payable |

693,467 | — | |||||

Total liabilities |

135,968,373 | — | |||||

Equity |

|||||||

Unitholders' capital |

280,000,000 | 10 | |||||

Unit premium and reserves |

— | — | |||||

Returned earnings |

(3,473,293 | ) | — | ||||

Underwriting commissions and issue expenses |

(14,610,000 | ) | — | ||||

Total equity (note 8) |

261,916,707 | 10 | |||||

Total liabilities and equity |

397,885,080 | 10 | |||||

Total equity per Unit |

9.35 | 10 | |||||

The accompanying notes are an integral part of these annual financial statements.

B. Capitalization and Indebtedness

Not Applicable.

1

C. Reasons for the Offer and Use of Proceeds

Not Applicable.

D. Risk Factors

The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair the performance of the Trust. If any of the following risks occur, the performance of the Trust could be materially adversely affected and the trading price of our Units could decline. You should also refer to the other information included in this document, including the Trust's financial statements and the related notes.

The value of the Units relates directly to the value of physical platinum and palladium bullion held by the Trust, and fluctuations in the price of platinum or palladium could materially adversely affect an investment in the Units.

The principal factors affecting the value of the Units are factors that affect the price of platinum or palladium. Platinum and palladium bullion are traded internationally and their prices are generally quoted in U.S. dollars. The price of the Units will depend on, and typically fluctuate with, the prices of platinum and palladium. The Manager expects the prices of platinum and palladium may be affected at any time by many international, economic, monetary and political factors, many of which are unpredictable. These factors include, without limitation:

- •

- global supply and demand, which is influenced by such factors as: (i) forward selling of platinum or palladium by

platinum and palladium producers; (ii) purchases made by platinum or palladium producers to unwind platinum or palladium hedge positions; (iii) central bank purchases and sales;

(iv) production and cost levels in major platinum- and palladium-producing countries; (v) new production projects; and (vi) industrial demand for platinum and palladium;

- •

- investors' expectations for future inflation rates;

- •

- exchange rate volatility of the U.S. dollar, the principal currency in which the price of platinum and palladium

are generally quoted;

- •

- interest rate volatility; and

- •

- unexpected global, or regional, political or economic incidents.

Changing tax, royalty, land and mineral rights ownership and leasing regulations in countries in which platinum or palladium are produced may have an impact on market functions and expectations for future platinum and palladium supply. This can affect both share prices of platinum and palladium mining companies and the relative prices of other commodities, which are both factors that may affect investor decisions in respect of investing in platinum and palladium.

An investment in the Trust will yield long-term gains only if the value of physical platinum and palladium bullion held by the Trust increases in an amount in excess of the Trust's expenses.

The Trust will not actively trade physical platinum and palladium bullion to take advantage of short-term market fluctuations in the price of platinum or palladium or actively generate other income. Accordingly, the Trust's long-term performance is dependent on the long-term performance of the price of platinum and palladium. As a result, an investment in the Trust will yield long-term gains only if the value of physical platinum and palladium bullion held by the Trust increases in an amount in excess of the Trust's expenses. For an analysis of the gains the Trust will need to achieve to cover the Trust's anticipated expenses, please see Item 4.B — Information on the Company — Business Overview — Impact of Trust Expenses on Net Asset Value below.

A redemption of Units for cash will yield a lesser amount than selling the Units on NYSE Arca or the TSX, if such a sale is possible.

Because the cash redemption value of the Units is based on 95% of the lesser of (i) the volume-weighted average trading price of the Units traded on NYSE Arca or, if trading has been suspended on NYSE Arca, the

2

volume-weighted average trading price of the Units traded on the TSX, for the last five days on which the respective exchange is open for trading for the month in which the redemption request is processed and (ii) the aggregate value of the NAV per Unit of the redeemed Units, on the last day of the month on which NYSE Arca is open for trading for the month in which the redemption request is processed, redeeming the Units for cash will generally yield a lesser amount than selling the Units on NYSE Arca or the TSX, assuming such a sale is possible. You should consider the manner in which the cash redemption value is determined before exercising your right to redeem your Units for cash.

A decrease in investment demand for physical platinum or palladium bullion could decrease the price of such platinum or palladium and adversely affect an investment in the Units.

Since 2008, demand for physical platinum and palladium bullion for investment purposes has been at historically high levels. There can be no assurance that such high level of investment demand will continue. If the investment demand for physical platinum or palladium bullion decreases, the price of physical platinum or palladium may decrease accordingly. Such decrease in the price of platinum and palladium could adversely affect an investment in the Units.

If a Unitholder redeems Units for physical platinum and palladium bullion and requests to have the platinum and palladium delivered to a destination other than an institution authorized to accept and hold Good Delivery plates or ingots, the physical platinum and palladium bullion will no longer be deemed Good Delivery once it has been delivered.

Good Delivery plates and ingots have the advantage that a purchaser generally will accept such plates and ingots as consisting of Good Delivery Standards without assaying or otherwise testing them. This provides Good Delivery plates and ingots with added liquidity as a sale of such plates and ingots can be completed more easily than the sale of plates and ingots that are not Good Delivery. The Trust will only purchase physical platinum and palladium bullion that is certified Good Delivery, and physical platinum and palladium bullion owned by the Trust will retain its status as Good Delivery while it is stored at the Mint or the sub-custodian of the Mint. If a Unitholder redeems Units for physical platinum and palladium bullion and has such bullion delivered to an institution authorized to accept and hold Good Delivery plates and ingots through an armored transportation service carrier that is eligible to transport Good Delivery plates and ingots, it is likely that the physical platinum and palladium bullion delivered to the redeeming Unitholder in respect of the redemption will retain its Good Delivery status while in the custody of that institution. However, if the redeeming Unitholder instructs that physical platinum and palladium bullion be delivered to a destination other than such an institution, physical platinum and palladium bullion delivered to the redeeming Unitholder in respect of the redemption will no longer be deemed Good Delivery once such physical platinum and palladium bullion has been delivered pursuant to the redeeming Unitholder's delivery instructions, which may make a future sale of such physical platinum and palladium bullion more difficult.

Physical platinum and/or palladium bullion received in Canada by a redeeming Unitholder will be subject to sales tax, and physical platinum and/or palladium bullion received in a province by a redeeming Unitholder may (depending on the province) also be subject to PST.

A redeeming Unitholder that receives physical palladium bullion in Canada will be required to pay HST or GST and PST on the value of the physical palladium bullion received. The rate of HST or GST and any PST will differ based on the province or territory in which the physical palladium bullion is delivered or made available to the redeeming Unitholder. The HST or GST and any PST applicable to the physical palladium bullion represents an additional cost for the redeeming Unitholder when it redeems Units for physical platinum and palladium bullion.

In addition, depending on the province or territory in which physical platinum bullion is delivered or made available to a redeeming Unitholder, PST may also be payable by such Unitholder.

3

Because the Trust's physical palladium bullion will be held outside of North America, transportation expenses for physical palladium bullion in the event of a redemption will be higher than if the Trust's palladium would be held in North America.

A Unitholder redeeming Units for physical platinum and palladium bullion will be responsible for expenses incurred in connection with such redemption. These expenses include expenses associated with the handling of the notice of redemption, the delivery and transportation of physical platinum and palladium bullion for Units that are being redeemed, the applicable platinum and palladium storage in-and-out fees and applicable taxes. As the Trust's physical palladium bullion will be held at Via Mat in London or Zurich, depending on where the Unitholder wishes to have his, her or its physical platinum and palladium delivered, the expenses associated with the delivery of physical palladium bullion to the Unitholder from Via Mat may be greater than the expenses associated with the transportation of physical platinum bullion from the Mint and greater than if the palladium had been held at the Mint or another location in North America.

Fluctuations in the prices of physical platinum and palladium bullion may result in the Trust having a greater proportion of its assets invested in physical platinum or palladium bullion than at the time the Trust purchased bullion with the proceeds of its initial offering.

The Manager purchased approximately equal dollar amounts of each of physical platinum and palladium bullion in an aggregate amount approximately equal to the net proceeds of the offering less the amount to be held by the Trust to pay ongoing expenses. Fluctuations in the prices of physical platinum and palladium bullion after such purchase may, over time, result in the Trust having a greater proportion by value of its assets invested in physical platinum or palladium bullion than at the time the Trust purchased bullion with the proceeds of the offering. The Trust will not rebalance the Trust's invested assets in physical platinum and palladium bullion back to equal weight following the closing of its initial public offering, but may in the future allocate any additional proceeds raised in subsequent offerings of Units with a view to balancing the value of the Trust's holdings of physical platinum and palladium bullion at then current prices.

It may take longer for a redeeming Unitholder to receive physical palladium bullion than physical platinum bullion.

If a Unitholder redeems Units for physical platinum and palladium bullion, the Unitholder's physical platinum and palladium bullion will be transported by an armored transportation service carrier engaged by or on behalf of the redeeming Unitholder. As the Trust's physical palladium bullion will be stored at Via Mat in London or Zurich, depending on where the Unitholder wishes to have the physical platinum and palladium delivered, the amount of time it will take to deliver physical palladium bullion to the Unitholder may be greater than the amount of time it will take to deliver physical platinum bullion from the Mint.

Unitholders who wish to exercise redemption privileges for physical platinum and palladium bullion may not receive the entire amount of their redemption proceeds in physical platinum and palladium bullion.

Unitholders wishing to redeem Units for physical platinum and palladium bullion may not receive bullion in proportion to the value of the physical platinum and palladium bullion held by the Trust or at all. The amount of physical platinum and palladium bullion a redeeming Unitholder is entitled to receive will be determined by the Manager by allocating the Redemption Amount to physical platinum and palladium bullion in direct proportion to the value of physical platinum and palladium bullion held by the Trust at the time of the redemption and the make-up of the Trust's inventory of plates and ingots, as the case may be, of platinum and palladium. Any portion of platinum or palladium bullion not available at the time of redemption will be paid in cash at a rate equal to 100% of aggregate value of the NAV per Unit of such unavailable amount.

The Trust may conduct further offerings of Units from time to time, at which time it will offer Units at a price that will be above the NAV per Unit at the time of the offering but that may be below the trading price of Units on NYSE Arca or TSX at that time.

The Trust may conduct further offerings of Units from time to time. Under the provisions of the Trust Agreement, the net proceeds to the Trust of any offering must be above the NAV per Unit at the time of the offering. Follow-on offerings of securities of issuers that are traded on an exchange usually are priced below the

4

trading price of such securities at the time of an offering to induce investors to purchase securities in the follow-on offering rather than through the exchange on which such securities are traded. Consequently, the price to the public at which such Units are offered likely will be below the trading price of Units of the Trust on NYSE Arca or TSX at the time of the offering, which may have the effect of lowering the trading price of Units immediately after the pricing of such follow-on offering.

The trading price of Units of the Trust on NYSE Arca and the TSX is not predictable and may be affected by factors beyond the control of the Trust.

The Trust cannot predict whether the Units will trade above, at or below the NAV per Unit. The trading price of Units may not closely track the value of the Trust's physical platinum and palladium bullion, and Units of the Trust may trade on NYSE Arca or the TSX at a significant premium or discount from time to time. In addition to changes in the value of physical platinum and palladium bullion, the trading price of Units may be affected by other factors beyond the control of the Trust, which may include the following: macroeconomic developments in North America and globally; market perceptions of attractiveness of physical platinum and palladium bullion as an investment; the lessening in trading volume and general market interest in the Trust's Units which may affect a Unitholder's ability to trade significant numbers of Units; and the size of the Trust's public float which may limit the ability of some institutions to invest in the Trust's Units.

The current high trading prices of platinum and palladium may not be sustained.

The Manager anticipates that the price of physical platinum and palladium bullion going forward and, in turn, the future NAV and the NAV per Unit, will be dependent upon factors such as global platinum and palladium supply and demand, investors' inflation expectations, exchange rate volatility and interest rate volatility. An adverse development with regard to one or more of these factors may lead to a decrease in platinum and palladium trading prices. A decline in prices of platinum or palladium bullion would decrease the NAV and the NAV per Unit.

The sale of physical platinum and palladium bullion by the Trust to pay expenses and to cover certain redemptions will reduce the amount of physical platinum and palladium bullion represented by each Unit on an ongoing basis irrespective of whether the trading price of the Units rises or falls in response to changes in the price of platinum or palladium.

Each outstanding Unit will represent an equal, fractional, undivided ownership interest in the net assets of the Trust attributable to the Units. As the Trust does not expect to generate any net income and will sell physical platinum and palladium bullion over time on an as-needed basis to pay for its ongoing expenses and to cover certain redemptions, the amount of physical platinum and palladium bullion represented by each Unit will, and the NAV per Unit may, gradually decline over time. This is true even if additional Units are issued in future offerings of Units by the Trust from time to time, as the amount of physical platinum and palladium bullion acquired by the proceeds of any such future offering of Units will proportionately reflect the amount of physical platinum and palladium bullion represented by such Units. Assuming constant platinum and palladium prices, the trading price of the Units would be expected to gradually decline as the amount of physical platinum and palladium bullion represented by the Units gradually declines. The Units will only maintain their original value if the price of platinum or palladium increases enough to offset the Trust's expenses.

Investors should be aware that the gradual decline in the amount of physical platinum and palladium bullion held by the Trust will occur regardless of whether the trading price of the Units rises or falls in response to changes in the price of such bullion. The estimated ordinary operating expenses of the Trust, which accrue daily commencing after the first day of trading of the Units on NYSE Arca and the TSX, are described in Item 4.B — Information on the Company — Business Overview — Fees and Expenses.

The sale of the Trust's physical platinum and palladium bullion to pay expenses or to cover certain redemptions at a time of low platinum or palladium prices could adversely affect the Net Asset Value.

The Manager intends to sell physical platinum and palladium bullion held by the Trust in proportion to the value of its physical holdings of physical platinum and palladium bullion (to the extent practicable) to pay Trust

5

expenses or to cover certain redemptions on an as-needed basis irrespective of then-current prices of such bullion, and no attempt will be made to buy or sell physical platinum and palladium bullion to protect against or to take advantage of fluctuations in the prices of platinum and palladium bullion. Consequently, the Trust's physical platinum and palladium bullion may be sold at a time when platinum and palladium prices are low.

Sales at relatively lower prices for such physical platinum and palladium bullion will require the sale of more physical platinum and palladium bullion, which in turn will have an adverse effect on the NAV and the NAV per Unit.

The Trust will not insure its assets and there may not be adequate sources of recovery if its physical platinum and palladium bullion is lost, damaged, stolen or destroyed.

The Trust will not insure its assets, including physical platinum and palladium bullion stored at the Mint or the sub-custodian of the Mint. Consequently, if there is a loss of assets of the Trust through theft, destruction, fraud or otherwise, the Trust and Unitholders will need to rely on insurance carried by applicable third parties, if any, or on such third party's ability to satisfy any claims against it. The amount of insurance available or the financial resources of a responsible third party may not be sufficient to satisfy the Trust's claim against such party. Also, Unitholders are unlikely to have any right to assert a claim directly against such third party; such claims may only be asserted by the Manager on behalf of the Trust. In addition, if a loss is covered by insurance carried by a third party, the Trust, which is not a beneficiary on such insurance, may have to rely on the efforts of the third party to recover its loss. This may delay or hinder the Trust's ability to recover its loss in a timely manner or otherwise.

A loss with respect to the Trust's physical platinum and palladium bullion that is not covered by insurance and for which compensatory damages cannot be recovered would have a negative impact on the NAV per Unit and would adversely affect an investment in the Units. In addition, any event of loss may adversely affect the operations of the Trust and, consequently, an investment in the Units.

If there is a loss, damage or destruction of the Trust's physical platinum and palladium bullion in the custody of the Mint and the Manager, on behalf of the Trust, does not give timely notice, all claims against the Mint will be deemed waived.

In the event of loss, damage or destruction of the Trust's physical platinum or palladium bullion in the Mint's custody, care and control (including at the sub-custodian of the Mint), the Manager, for and on behalf of the Trust, must give written notice to the Mint within five Mint Business Days after its discovery of any such loss, damage or destruction, but in any event no more than 30 days after the delivery by the Mint to the Manager, on behalf of the Trust, of an inventory statement in which the discrepancy first appears. If such notice is not given in a timely manner, all claims against the Mint will be deemed to have been waived. In addition, no action, suit or other proceeding to recover any loss, damage or destruction can be brought against the Mint unless timely notice of such loss, damage or destruction has been given and such action, suit or proceeding will have commenced within 12 months from the time a claim is made. The loss of the right to make a claim or of the ability to bring an action, suit or other proceeding against the Mint may mean that any such loss will be non-recoverable, which will have an adverse effect on the NAV and the NAV per Unit.

RBC Investor Services, the Mint and other service providers engaged by the Trust may not carry adequate insurance to cover claims against them by the Trust.

Unitholders cannot be assured that RBC Investor Services, the Mint or other service providers engaged by the Trust will maintain insurance with respect to the Trust's assets held by them or the services that such parties provide to the Trust and, if they maintain insurance, that such insurance is sufficient to satisfy any losses incurred by them in respect of their relationship with the Trust. In addition, none of the Trust's service providers are required to include the Trust as a named beneficiary of any such insurance policies that are purchased. Accordingly, the Trust will have to rely on the efforts of the service provider to recover from its insurer compensation for any losses incurred by the Trust in connection with such arrangements.

6

All redemption amounts will be determined using U.S. dollars, which will expose redeeming non-U.S. Unitholders to currency risk.

All redemption amounts will be determined using U.S. dollars. All redeeming Unitholders will receive any cash amount to which the Unitholder is entitled in connection with the redemption in U.S. dollars, and will be exposed to the risk that the exchange rate between the U.S. dollar and any other currency in which the Unitholder generally operates will result in a lesser redemption amount than the Unitholder would have received if the redemption amount had been calculated and delivered in such other currency. In addition, because any cash as a result of the redemption will be delivered in U.S. dollars, the redeeming Unitholder may be required to open or maintain an account that can receive deposits of U.S. dollars.

In the event any of the Trust's physical platinum or palladium bullion is lost, damaged, stolen or destroyed, recovery may be limited to the market value of such physical platinum and palladium bullion at the time the loss is discovered.

If there is a loss due to theft, loss, damage, destruction or fraud or otherwise with respect to any physical platinum or palladium bullion held by one of the Trust's custodians or sub-custodians and such loss is found to be the fault of such custodian or sub-custodian, the Trust may not be able to recover more than the market value of physical platinum or palladium bullion at the time the loss is discovered. If the market value of such physical platinum or palladium bullion increases between the time the loss is discovered and the time the Trust receives payment for its loss and purchases physical platinum or palladium bullion to replace the losses, less physical platinum or palladium bullion will be acquired by the Trust and the Net Asset Value will be negatively affected.

A redeeming Unitholder that suffers loss of, or damage to, its physical platinum and palladium bullion during delivery from the Mint or the sub-custodian of the Mint will not be able to claim damages from the Trust, the Mint or the Mint's sub-custodian.

If a Unitholder exercises its option to redeem Units for physical platinum and palladium bullion, the Unitholder's physical platinum and palladium bullion will be transported by an armored transportation service carrier engaged by or on behalf of the redeeming Unitholder. Because ownership of the physical platinum and palladium bullion will transfer to such Unitholder at the time the Mint or its sub-custodian surrenders the physical platinum and palladium bullion to the armored transportation service carrier, the redeeming Unitholder will bear the risk of loss from the moment the armored transportation service carrier takes possession of physical platinum and palladium bullion on behalf of such Unitholder. In the event of any loss or damage in connection with the delivery of any part of the physical platinum or palladium bullion after such time, such Unitholder will not be able to claim damages from the Trust, the Mint or its sub-custodian, but will instead need to bring a claim against the armored transportation service carrier.

Because the Trust will be primarily invested in physical platinum and palladium bullion, an investment in the Trust may be more volatile than an investment in a more broadly diversified portfolio.

The Trust will be primarily invested at all times in physical platinum and palladium bullion. As a result, the Trust's holdings will not be diversified. Accordingly, the NAV per Unit may be more volatile than another investment vehicle with a more broadly diversified portfolio and may fluctuate substantially over time. An investment in the Trust may be deemed speculative and is not intended as a complete investment program. An investment in Units should be considered only by persons financially able to maintain their investment and who can bear the risk of loss associated with an investment in the Trust. Investors should review closely the objective and strategy, the Investment and Operating Restrictions and the redemption provisions of the Trust as outlined herein and familiarize themselves with the risks associated with an investment in the Trust.

Under Canadian law, the Trust and Unitholders may have limited recourse against the Mint.

The Mint is a Canadian Crown corporation. A Crown corporation may be sued for breach of contract or for wrongdoing in tort where it has acted on its own behalf or on behalf of the Crown. However, a Crown corporation may be entitled to immunity if it acts as agent of the Crown rather than in its own right and on its own behalf. The Mint has entered into the storage agreement in respect of the Trust's physical platinum bullion

7

held by the Mint or its appointed sub-custodian, as applicable, dated December 17, 2012 between the Manager, for and on behalf of the Trust, and the Mint; to which we will refer as the Platinum Storage Agreement, and the storage agreement in respect of the Trust's physical palladium bullion held by the Mint or its appointed sub-custodian, as applicable, dated December 17, 2012 between the Manager, for and on behalf of the Trust, and the Mint; to which we will refer as the Palladium Storage Agreement and together with the Platinum Storage Agreement, as the Storage Agreements, relating to the custody of the Trust's physical platinum and palladium bullion on its own behalf and not on behalf of the Crown; nevertheless, a court may determine that, when acting as custodian of the Trust's physical platinum and palladium bullion, the Mint acts as agent of the Crown and, accordingly, the Mint may be entitled to immunity of the Crown. Consequently, the Trust or a Unitholder may not be able to recover for any losses incurred as a result of the Mint's acting as custodian of the Trust's physical platinum and palladium bullion.

A notice of redemption is irrevocable.

In order to redeem Units for cash or physical platinum and palladium bullion, a Unitholder must provide a notice of redemption to the Trust's transfer agent. Except in the event that redemptions are suspended by the Manager, once a notice of redemption has been received by the transfer agent, it can no longer be revoked by the Unitholder under any circumstances, though it may be rejected by the transfer agent if it does not comply with the requirements for a notice of redemption.

The Mint may become a private enterprise, in which case its obligations will not constitute the unconditional obligations of the Government of Canada.

In the past, there has been speculation regarding whether the Government of Canada might privatize the Mint. The Mint will not remain a Crown corporation if the Government of Canada privatizes the Mint. If the Mint were to become a private entity, its obligations would no longer generally constitute unconditional obligations of the Government of Canada and, although it would continue to be responsible for and bear the risk of loss of, and damage to, the Trust's physical platinum and palladium bullion that is in its custody, there would be no assurance that the Mint would have the resources to satisfy claims of the Trust against the Mint based on a loss of, or damage to, the Trust's physical platinum and palladium bullion in the custody of the Mint.

The Trust may terminate and liquidate at a time that is disadvantageous to Unitholders.

If the Trust is required to terminate and liquidate or the Manager determines to terminate and liquidate the Trust, such termination and liquidation could occur at a time which is disadvantageous to Unitholders, such as when platinum or palladium prices are lower than the prices for such bullion at the time when Unitholders purchased their Units. In such a case, when the Trust's physical platinum and palladium bullion is sold as part of the Trust's liquidation, the resulting proceeds distributed to Unitholders will be less than if the prices for such bullion were higher at the time of sale. In certain circumstances, the Manager has the ability to terminate the Trust without the consent of Unitholders. The Manager's interests may differ from those of the Unitholders, and the Manager may terminate the Trust at a time that is not advantageous for the Unitholder.

The Units may trade at a price which is at, above or below the NAV per Unit, and any discount or premium in the trading price relative to the NAV per Unit may widen as a result of non-concurrent trading hours between NYSE Arca, LPPM and the TSX.

Units may trade in the market at a premium or discount to the NAV per Unit. This risk is separate and distinct from the risk that the NAV per Unit may decrease. The amount of the discount or premium in the trading price relative to the NAV per Unit may be influenced by non-concurrent trading hours between the LPPM, which is the main global exchange on which platinum and palladium for physical delivery is traded, and NYSE Arca and the TSX. Liquidity in the global platinum and palladium markets will be reduced after the close of regular trading hours on the LPPM at 4:00 p.m. London, UK time (11:00 a.m. Eastern time). The Units will trade on NYSE Arca and the TSX until 4:00 p.m. Eastern time. As a result of the reduced liquidity in the global platinum and palladium markets after the close of regular trading hours on the LPPM, trading spreads, and the resulting premium or discount to the NAV per Unit, may widen between the close of regular trading hours for the bullion on LPPM and 4:00 p.m. Eastern time.

8

The Trust may suspend redemptions, which may affect the trading price of the Units.

In certain circumstances, the Manager, on behalf of the Trust, may suspend the right of Unitholders to request a redemption of their Units or postpone the date of delivery or payment of the redemption proceeds of the Trust (whether in physical platinum and palladium bullion or cash, as the case may be) with the prior approval of Canadian securities regulatory authorities having jurisdiction, where required. Such circumstances include any period during which the Manager determines that conditions exist which render impractical the sale of assets of the Trust or which impair the ability of the Manager to determine the value of the assets of the Trust or the redemption amount for the Units. This may affect the trading price of the Units at a time when an investor wishes to sell its Units on NYSE Arca or the TSX. Accordingly, Units may not be an appropriate investment for investors who seek immediate liquidity or access to platinum or palladium bullion.

The market for Units and the liquidity of Units may be adversely affected by competition from other methods of investing in physical platinum and palladium bullion.

The Trust will compete with other financial vehicles, including traditional debt and equity securities issued by companies in the resource industry and other securities backed by or linked to platinum or palladium, direct investments in platinum or palladium and investment vehicles similar to the Trust. Market and financial conditions, and other conditions beyond the Manager's control, may make it more attractive to invest in other financial vehicles or to invest in platinum or palladium directly, which could limit the market for the Units and reduce the liquidity of the Units and, accordingly, the price received for sales of Units on NYSE Arca or the TSX.

A slowdown in the automobile industry may have the effect of causing a decline in the prices of platinum and palladium and a corresponding decline in the trading price of the Units on NYSE Arca and the TSX.

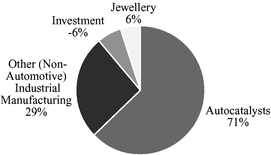

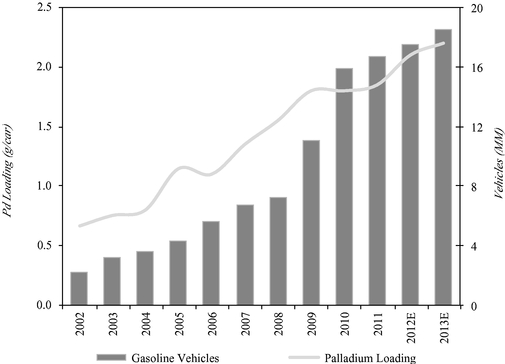

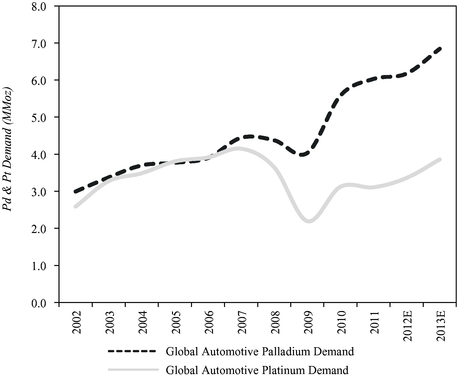

Autocatalysts, automobile components that use platinum and palladium, accounted for approximately 38% of the global demand in platinum and 71% of the global demand in palladium in 2011. Reduced automotive industry sales may result in a decline in demand for autocatalysts. This means that a decline in the global automotive industry may impact the price of platinum and palladium and affect the trading price of the Units on NYSE Arca and the TSX.

Large-scale sales of platinum or palladium could decrease the price of such platinum or palladium and adversely affect an investment in the Units.

The possibility of large-scale sales of platinum or palladium may have a short-term negative impact on the price of platinum or palladium and adversely affect an investment in the Units. Large scale sales of platinum or palladium may impair the price performance of such bullion, which would, in turn, adversely affect an investment in the Units.

The Trust will sell physical platinum and palladium bullion to provide available funds for its expenses and for any cash redemptions.

The Trust has retained cash from the net proceeds of its initial offering in an amount not exceeding 3% of the net proceeds of the offering in order to provide available funds for expenses and any cash redemptions. If the Trust's expenses are higher than estimated, the Trust may need to sell physical platinum and palladium bullion earlier than anticipated to meet its expenses and any cash redemptions. In addition, from time to time the Trust will sell physical platinum and palladium bullion as required to replenish this cash reserve to meet its expenses and any cash redemptions. Such sales may result in a reduction of the NAV per Unit and the trading price of the Units. There is no limit on the total amount of such physical platinum and palladium bullion that the Trust may sell in order to pay expenses.

Unitholders will not have the protections associated with ownership of shares in an investment company registered under the Investment Company Act or the protections afforded by the Commodity Exchange Act.

The Trust is not registered as an investment company under the Investment Company Act of 1940, as amended, and is not required to register under such act. Consequently, Unitholders will not have the regulatory

9

protections provided to investors in investment companies. The Trust will not hold or trade in commodity futures contracts regulated by the Commodity Exchange Act of 1936, which we will refer to as the Commodity Exchange Act, as administered by the U.S. Commodity Futures Trading Commission, which we will refer to as the CFTC. Furthermore, the Trust is not a commodity pool for purposes of the Commodity Exchange Act, and none of the Manager, the Trustee or the underwriters is subject to regulation by the CFTC as a commodity pool operator or a commodity trading advisor in connection with the Units. Consequently, Unitholders will not have the regulatory protections provided to investors in Commodity Exchange Act-regulated instruments or commodity pools nor may COMEX or any futures exchange enforce its rules with respect to the Trust's activities. In addition, Unitholders do not benefit from the protections afforded to investors in platinum or palladium futures contracts on regulated futures exchanges.

The Manager and its affiliates also manage other funds that may invest in physical platinum and palladium bullion and conflicts of interest by the Manager or its affiliates may occur.

Pursuant to the Management Agreement and the Trust Agreement, the Manager is responsible for the day-to-day business and operation of the Trust and, therefore, exercises significant control over the Trust. The Manager may have different interests than the Unitholders and consequently may act in a manner that is not advantageous to Unitholders at any particular time. The Manager and its general partner, the general partner's directors and officers, and their respective affiliates and associates may engage in the promotion, management or investment management of other accounts, funds or trusts that invest in physical platinum or palladium bullion, or both. The Manager currently manages other investment funds which may include platinum or palladium bullion as part of their portfolios from time to time. It is possible that at certain times the staff of the Manager may have conflicts in allocating their time and services among the Trust and the other accounts, funds or trusts managed by the Manager. The amount of time that the Manager devotes to each of the mutual funds and hedge funds it manages will vary significantly depending on market conditions.

The Trust's obligation to reimburse the Trustee, the Manager, the underwriters or certain parties related to them for certain indemnified liabilities could adversely affect an investment in the Units.

Under certain circumstances, the Trust might be subject to significant indemnification obligations in favor of the Trustee, the Manager, the underwriters or certain parties related to them. The Trust will not carry any insurance to cover such potential obligations and, to the Manager's knowledge, none of the foregoing parties will be insured for losses for which the Trust has agreed to indemnify them. Any indemnification paid by the Trust would reduce the NAV and, accordingly, the NAV per Unit.

Unitholders are not entitled to participate in management of the Trust.

Unitholders are not entitled to participate in the management or control of the Trust or its operations, except to the extent of exercising their right to vote their Units when applicable. See Item 10.B — Additional Information — Trust Agreement. Unitholders do not have any input into the Trust's daily activities.

The rights of Unitholders differ from those of shareholders of a corporation.

Because the Trust is organized as a trust rather than a corporation, the rights of Unitholders are set forth in the Trust Agreement rather than in a corporate statute. This means that Unitholders do not have the statutory rights normally associated with the ownership of shares in an Ontario corporation. For example, the Trust is not subject to minimum quorum requirements, is not required to hold annual meetings, and has no officers or directors. Unitholders have the right to vote on matters brought before Unitholders in accordance with the Trust Agreement but do not have a right to elect the Manager, though Unitholders do have the right to remove the Manager in certain circumstances. In addition, Unitholders do not have the right to bring "oppression" or "derivative" suits available under corporate statutes.

10

The investment objective and restrictions of the Trust and the attributes of a particular class or series of a class of Units of the Trust may be changed by way of an extraordinary resolution of all Unitholders and Unitholders of such class or series of a class of Units, respectively.

The investment objective and restrictions of the Trust and the attributes of a particular class or series of a class of Units may be changed by extraordinary resolution as determined in accordance with the Trust Agreement. "Extraordinary resolution" means a resolution passed in person or by proxy, by Unitholders holding Units representing in aggregate not less than 662/3% of the Net Asset Value as determined in accordance with the Trust Agreement, at a duly constituted meeting of Unitholders, or at any adjournment thereof, called and held in accordance with the Trust Agreement, or a written resolution signed by Unitholders holding Units representing in aggregate not less than 662/3% of the Net Asset Value as determined in accordance with the Trust Agreement. Such changes to the investment objective or restrictions of the Trust or the attributes of the Units may be more favorable or less favorable to you than the investment objective or restrictions of the Trust or the attributes of the Units, as the case may be, as described in this document. The value of the Units sold hereby may decrease as a result of such changes.

Substantial redemptions of Units may affect the liquidity and trading price of Units and increase the pro rata expenses per Unit.

Substantial redemptions of Units could result in a decrease in the trading liquidity of the Units and increase the amount of Trust expenses allocated to each remaining Unit. Such increased expenses may reduce the NAV, the NAV per Unit and the trading price of the Units.

Fluctuation in foreign exchange rates may have an adverse effect on the Trust and on the trading price of the Units.

The Trust maintains its accounting records, reports its financial position and will purchase physical platinum and palladium bullion in U.S. dollars. As certain of the Trust's expenses are paid in Canadian dollars, an increase in the value of the Canadian dollar would increase the reported expenses of the Trust that are payable in Canadian dollars, which could result in the Trust being required to sell more physical platinum and palladium bullion to pay its expenses. Further, such appreciation could adversely affect the Trust's reported financial results, which may have an adverse effect on the trading price of the Units.

The Trust expects to be a passive foreign investment company, which may have adverse U.S. federal income tax consequences to U.S. Holders who do not make certain elections.

Based on its proposed method of operation, the Trust expects to be treated as a passive foreign investment company, which we will refer to as a PFIC, for U.S. federal income tax purposes. Therefore, a U.S. Holder (as defined in Item 10.E — Additional Information — Taxation — Material U.S. Federal Income Tax Considerations — U.S. Federal Income Taxation of U.S. Holders) of the Units that does not make a QEF election or a mark-to-market election with respect to the Units generally will be liable to pay U.S. federal income tax at the then prevailing income tax rates on ordinary income plus interest upon excess distributions and upon any gain from the disposition of the Units as if the excess distribution or gain had been recognized ratably over the U.S. Holder's holding period for the Units. A U.S. Holder generally may mitigate these U.S. federal income tax consequences by making a QEF election, or, to a lesser extent, a mark-to-market election. See Item 10.E — Additional Information — Taxation — Material U.S. Federal Income Tax Considerations — Material U.S. Federal Income Tax Considerations — U.S. Federal Income Taxation of U.S. Holders for a more comprehensive discussion of the U.S. federal income tax consequences to U.S. Holders arising from the Trust's status as a PFIC and the procedures for making a QEF election or a mark-to-market election.

A U.S. Holder that makes a QEF election with respect to his, her or its Units may be required to include amounts in income for U.S. federal income tax purposes if any holder redeems Units for cash or physical platinum and palladium bullion.

As noted above and described in detail under Item 10.E — Taxation — Material U.S. Federal Income Tax Considerations — Material U.S. Federal Income Tax Considerations — U.S. Federal Income Taxation of U.S. Holders, below, a U.S. Holder generally may mitigate the adverse U.S. federal income tax consequences under the adverse PFIC rules of holding Units by making a QEF election. A U.S. Holder that makes a QEF election must report each year for U.S. federal income tax purposes his, her or its pro rata share of the Trust's

11

ordinary earnings and the Trust's net capital gain, if any, regardless of whether or not distributions were received from the Trust by the U.S. Holder. If any holder redeems Units for physical platinum and palladium bullion (regardless of whether the holder requesting redemption is a U.S. Holder or has made a QEF election), the Trust will be treated as if it sold the physical platinum and palladium bullion for its fair market value. As a result, all the U.S. Holders who have made a QEF election will be required to currently include in their income their pro rata share of the Trust's gain from such deemed disposition (which generally will be taxable to non-corporate U.S. Holders at a maximum rate of 28% under current law if the Trust has held the physical platinum and palladium bullion for more than one year), even though such deemed disposition is not attributable to any action on their part. If any holder redeems Units for cash and the Trust sells physical platinum and palladium bullion to fund the redemption (regardless of whether the holder requesting redemption is a U.S. Holder or has made a QEF election), all the U.S. Holders who have made a QEF election similarly will include in their income their pro rata share of the Trust's gain from the sale of the physical platinum and palladium bullion, which will be taxable as described above, even though the Trust's sale of physical platinum and palladium bullion is not attributable to any action on their part. See Item 10.E — Additional Information — Taxation — Material U.S. Federal Income Tax Considerations — Material U.S. Federal Income Tax Considerations — U.S. Federal Income Taxation of U.S. Holders — Taxation of U.S. Holders Making a Timely QEF Election."

Unitholders may be liable for obligations of the Trust to the extent the Trust's obligations are not satisfied out of the Trust's assets.

The Trust Agreement provides that no Unitholder will be subject to any liability whatsoever, in tort, contract or otherwise, to any person in connection with the investment obligations, affairs or assets of the Trust and all such persons will look solely to the Trust's assets for satisfaction of claims of any nature arising out of or in connection therewith. Also, under the Trust Beneficiaries' Liability Act, 2004 (Ontario), holders of units of a trust governed by the laws of the Province of Ontario that is a reporting issuer under the Securities Act (Ontario) are not, as beneficiaries, liable for any act, default, obligation or liability of the trust. Notwithstanding the above, there is a risk that a Unitholder could be held personally liable for obligations of the Trust to the extent that claims are not satisfied out of the assets of the Trust if a court finds (i) that Ontario law does not govern the ability of a third party to make a claim against a beneficiary of a trust and that the applicable governing law permits such a claim, or (ii) that the Unitholder was acting in a capacity other than as a beneficiary of the trust. In the event that a Unitholder should be required to satisfy any obligation of the Trust, under the Trust Agreement, such Unitholder will be entitled to reimbursement from any available assets of the Trust.

Canadian registered plans that redeem their Units for physical platinum and palladium bullion may be subject to adverse consequences.

Physical platinum and palladium bullion received by a Canadian registered plan, such as a registered retirement savings plan, on a redemption of Units for physical platinum and palladium bullion will not be a qualified investment for such plan. Accordingly, such plans (and in the case of certain plans, the annuitants or beneficiaries thereunder or holders thereof) may be subject to adverse Canadian tax consequences including, in the case of registered education savings plans, revocation of such plans.

If the Trust ceases to qualify as a mutual fund trust for Canadian income tax purposes, it or the Unitholders could become subject to material adverse consequences.

In order to qualify as a mutual fund trust under the Tax Act, the Trust must comply with various requirements contained in the Tax Act, including (in many or most circumstances) requirements to hold substantially all its property in assets (such as physical platinum and palladium bullion and cash) that are not "taxable Canadian property", and to restrict its undertaking to the investing of its funds. See Item 10.E — Additional Information — Taxation — Material Canadian Federal Income Tax Considerations — Qualification as a Mutual Fund Trust. If the Trust were to cease to qualify as a mutual fund trust (whether as a result of a change of law or administrative practice, or due to its failure to comply with the current Canadian requirements for qualification as a mutual fund trust), it may experience various potential adverse consequences, including becoming subject to a requirement to withhold tax on distributions made to non-resident Unitholders of any capital gains realized from the dispositions of physical platinum and palladium bullion, the Units not qualifying

12

for investment by Canadian registered plans and the Units ceasing to qualify as "Canadian securities" for the purposes of the election provided in subsection 39(4) of the Tax Act.

If the Trust were to carry on a business in Canada in a taxation year or acquire securities that were "non-portfolio properties", it could become subject to tax at full corporate tax rates on some or all of its income for that year.

The Manager anticipates that the Trust will make sufficient distributions in each year of any income (including taxable capital gains) realized by the Trust for Canadian tax purposes in the year so as to ensure that it will not be subject to Canadian income tax on such income. Such income generally will become subject to Canadian income tax at full corporate rates if the Trust becomes a specified investment flow-through trust, which we will refer to as a SIFT, even if distributed in full. If the Trust, contrary to its investment restrictions, were to carry on a business in Canada in a taxation year and use its property in the course of any such business, or acquire securities that were "non-portfolio properties", it could become a SIFT trust. The anticipated activities of the Trust, as described in this document, are intended to avoid having the Trust characterized as a SIFT trust. The Canada Revenue Agency, which we will refer to as the CRA, may take a different (and adverse) view of this issue and characterize the Trust as a SIFT trust. If the Trust were a SIFT trust for a taxation year of the Trust, it would effectively be taxed similarly to a corporation on income and capital gains in respect of such non-portfolio properties at a combined federal/provincial tax rate comparable to rates that apply to income earned and distributed by Canadian corporations. Distributions of such income received by Unitholders would be treated as dividends from a taxable Canadian corporation. See Item 10.E — Additional Information — Taxation — Material Canadian Federal Income Tax Considerations — SIFT Trust Rules.

If the Trust treats distributed gains as being on capital account and the CRA later determines that the gains were on income account, then Canadian withholding taxes would apply to the extent that the Trust has distributed the gains to non-resident Unitholders and Canadian resident Unitholders could be reassessed to increase their taxable income. Any taxes borne by the Trust itself would reduce the NAV per Unit and the trading prices of the Units.

The Manager anticipates that the Trust generally will treat gains (or losses) as a result of dispositions of physical platinum and palladium bullion as capital gains (or capital losses), although depending on the circumstances, it may instead include (or deduct) the full amount of such gains in computing its income. See Item 10.E — Additional Information — Taxation — Material Canadian Federal Income Tax Considerations — Canadian Taxation of the Trust. If any transactions of the Trust are reported by it on capital account but are subsequently determined by the CRA to be on income account, there may be an increase in the net income of the Trust for tax purposes and the taxable component of redemption proceeds (or any other amounts) distributed to Unitholders, with the result that Canadian resident Unitholders could be reassessed by the CRA to increase their taxable income by the amount of such increase, and non-resident Unitholders potentially could be assessed directly by the CRA for Canadian withholding tax on the amount of net gains on such transactions that were treated by the CRA as having been distributed to them. The CRA can assess the Trust for a failure of the Trust to withhold tax on distributions made by it to non-resident Unitholders that are subject to withholding tax, and typically would do so rather than assessing the non-resident Unitholders directly. Accordingly, any such re-determination by the CRA may result in the Trust being liable for unremitted withholding taxes on prior distributions made to Unitholders who were not resident in Canada for the purposes of the Tax Act at the time of the distribution. As the Trust may not be able to recover such withholding taxes from the non-resident Unitholders whose Units were redeemed, payment of any such amounts by the Trust likely would reduce the NAV per Unit and the trading prices of the Units. See Item 10.E — Additional Information — Taxation — Material Canadian Taxation of Unitholders — Unitholders Not Resident in Canada.

Exemption from GST or HST on the Trust's purchase in Canada of platinum plates is not certain.

In order for the purchase in Canada of Good Delivery plates of platinum bullion to be exempt from GST or HST, various requirements must be satisfied including a requirement that such plates qualify as "ingots", or "bars" or "wafers". The Manager anticipates that the Trust will not be charged HST on its purchases in Canada of such plates in accordance with the Manager's understanding of the assessing practices of the CRA. However, in the event that the CRA were to challenge the exemption from GST and HST of such purchases, the Trust could be required to pay GST or HST on its purchases of platinum plates, potentially including purchases made by it prior to the time of any such challenge. This likely would reduce the NAV of Units.

13

A Unitholder may be unable to bring actions or enforce judgments against the Trust, the Trustee, the Manager, the Manager's general partner or any of their officers and directors under U.S. federal securities laws in Canada or to serve process on any of them in the United States.

Each of the Trust, the Trustee, the Manager, and the Manager's general partner is organized under the laws of the Province of Ontario, Canada, and all of their executive offices and administrative activities and assets are located outside the United States. In addition, the directors and officers of the Trustee and the Manager's general partner are residents of jurisdictions other than the United States and all or a substantial portion of the assets of those persons are or may be located outside the United States. As a result, a Unitholder may be unable to serve legal process within the United States upon any of the Trust, the Trustee, the Manager or the Manager's general partner or any of their directors or officers, as applicable, or enforce against them in the appropriate Canadian courts judgments obtained in United States courts, including judgments predicated upon the civil liability provisions of the federal securities laws of the United States, or bring an original action in the appropriate Canadian courts to enforce liabilities against the Trust, the Trustee, the Manager, the Manager's general partner or any of their directors of officers, as applicable, based upon the U.S. federal securities laws.

The development of new technology or new alloys could reduce the demand for platinum and palladium and adversely affect platinum and palladium prices and the Net Asset Value.

Demand for platinum and/or palladium may be reduced if manufacturers in the automotive, electronics and dental industries find substitutes for platinum and/or palladium. The development of a substitute alloy or synthetic material which has catalytic characteristics similar to PGMs could result in a decrease in demand for platinum and/or palladium. Furthermore, if the automotive industry were to develop automobiles that do not require catalytic converters and that gain market acceptance, such as pure electric vehicles, it could significantly reduce the demand for platinum and/or palladium. High prices for platinum or palladium can create an incentive for the development of substitutes. Any such developments could have a material adverse effect on the long term prices of platinum and/or palladium and, as a result, the Net Asset Value.

Canadian registered plans that redeem their Units for physical platinum and palladium bullion may be subject to adverse consequences.

Physical platinum and palladium bullion received by a Canadian registered plan, such as a registered retirement savings plan, on a redemption of Units for physical platinum and palladium bullion will not be a qualified investment for such plan. Accordingly, such plans (and in the case of certain plans, the annuitants or beneficiaries thereunder or holders thereof) may be subject to adverse Canadian tax consequences including, in the case of registered education savings plans, revocation of such plans.

ITEM 4 — INFORMATION ON THE COMPANY

A. History and Development of the Trust

The Sprott Physical Platinum and Palladium Trust was established under the laws of the Province of Ontario, Canada pursuant to a trust agreement dated as of December 23, 2011, as amended and restated as of June 6, 2012, which we will refer to as the Trust Agreement. The Trust was created to invest and hold substantially all of its assets in physical platinum and palladium bullion. The Trust seeks to provide a convenient and exchange-traded investment alternative for investors interested in holding physical platinum and palladium bullion without the inconvenience that is typical of a direct investment in physical platinum and palladium bullion. The Trust intends to invest primarily in long-term holdings of unencumbered, fully allocated, physical platinum and palladium bullion and will not speculate with regard to short-term changes in platinum and palladium prices. The Trust does not anticipate making regular cash distributions to Unitholders.

The Trust's office is located at Suite 2700, South Tower, Royal Bank Plaza, 200 Bay Street, Toronto, Ontario, Canada M5J 2J1. The Manager's office is located at Suite 2700, South Tower, Royal Bank Plaza, 200 Bay Street, Toronto, Ontario, Canada M5J 2J1 and its telephone number is (416) 362-7172. The office of the Trust's trustee, RBC Investor Services Trust, is located at 155 Wellington Street West, Street Level, Toronto, Ontario, Canada M5V 3L3. The custodian for the Trust's physical platinum and palladium bullion, the Mint, is located at 320 Sussex Drive, Ottawa, Ontario, Canada K1A 0G8. The Mint will engage Via Mat as a sub-custodian for the Trust's physical palladium bullion. The principal office of Via Mat is located at

14

130 Sheridan Blvd., Inwood, New York, USA 11096. The custodian for the Trust's assets other than physical platinum and palladium bullion, RBC Investor Services, is located at 155 Wellington Street West, Street Level, Toronto, Ontario, Canada M5V 3L3.

Our Status As an Emerging Growth Company

We qualify as an emerging growth company under the JOBS Act, and will continue to so qualify until the earlier of: (i) the last day of our fiscal year following the fifth anniversary of the date of our initial public offering, (ii) the date on which we become a large accelerated filer, or (iii) the date on which we will have issued an aggregate of $1 billion in non-convertible debt during the preceding three years. As an emerging growth company, we are eligible for certain reduced reporting and other obligations, including the following:

- •

- the ability to present only two years of audited financial statements and two years of related Management's Discussion and

Analysis of Financial Condition and Results of Operations in the registration statement of our initial public offering;

- •

- an exemption from the auditor attestation requirement in our assessment of the internal control over financial reporting

as required by Section 404(b) of the Sarbanes-Oxley Act of 2002;

- •

- an exemption from new or revised financial accounting standards applicable to public companies until such standards are

also applicable to private companies; and

- •

- an exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board, or the PCAOB, requiring mandatory audit firm rotation or a supplement to our auditor's report in which the auditor would be required to provide additional information about the audit and our financial statements.

We have, however, voluntarily elected to "opt out", or to not to avail ourselves, of any of the reduced regulatory and reporting requirements available to emerging growth companies, including opting out of the extended transition period relating to the exemption from new or revised financial accounting standards. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable, and we will treat our election to opt out of any other reduced regulatory and reporting requirements available to emerging growth companies as irreversible as well.

B. Business Overview

The Trust is authorized to issue an unlimited number of units in one or more classes and series of units. Each unit of a class represents an undivided ownership interest in the net assets of the Trust attributable to that class or series of a class of units. Units are transferable and redeemable at the option of the Unitholder in accordance with the provisions set forth in the Trust Agreement. All units of the same class or series of a class have equal rights and privileges with respect to all matters, including voting, receipt of distributions from the Trust, liquidation and other events in connection with the Trust. Units and fractions of units will be issued only as fully paid and non-assessable. The Units have no preference, conversion, exchange or pre-emptive rights. Each whole unit of a particular class or series of a class entitles the holder thereof to one vote at meetings of Unitholders where all classes vote together and to one vote at meetings of Unitholders where that particular class or series of a class of Unitholders votes separately as a class or series of a class.

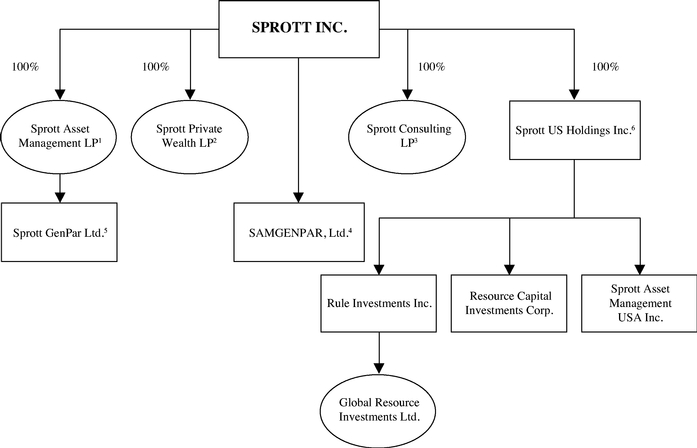

Sprott Asset Management LP is the Manager and RBC Investor Services, a trust company organized under the laws of Canada, is the trustee of the Trust. The fiscal year-end of the Trust is December 31.

The Trust is considered a mutual fund under Canadian securities legislation. The Trust is not registered as an investment company under the Investment Company Act of 1940 and is not a commodity pool for purposes of the Commodity Exchange Act of 1936, and neither the Manager nor the Trustee is subject to regulation by the CFTC as a commodity pool operator or commodity trading advisor in connection with the Units.

The Trust employs two custodians. The Royal Canadian Mint, a Canadian Crown corporation, acts as custodian for the Trust's physical platinum and palladium bullion, pursuant to a precious metals storage agreement between the Manager, for and on behalf of the Trust, and the Mint, to which we will refer as the Precious Metals Storage Agreement. RBC Investor Services acts as custodian of the Trust's assets other than physical platinum and palladium bullion pursuant to the Trust Agreement.

15

The Trust sold 28,000,000 Units in aggregate on December 18, 2012 in connection with the initial public offering. The Trust was created to invest and hold substantially all of its assets in physical platinum and palladium bullion. The Trust seeks to provide a secure, convenient and exchange-traded investment alternative for investors interested in holding physical platinum and palladium bullion without the inconvenience that is typical of a direct investment in physical platinum and palladium bullion. The Trust invests primarily in long-term holdings of unencumbered, fully allocated, physical platinum and palladium bullion and will not speculate with regard to short-term changes in platinum and palladium prices. The Trust does not anticipate making regular cash distributions to Unitholders. Sprott Asset Management LP is the sponsor and promoter of the Trust and serves as manager of the Trust pursuant to a management agreement with the Trust. Each outstanding unit represents an equal, fractional, undivided ownership interest in the net assets of the Trust attributable to the particular class of units. Expected advantages of investing in the Units include:

- •

- Convenient Way to Own Physical Platinum and Palladium

Bullion. The Trust's Units are listed on the NYSE Arca and the TSX. The Trust provides institutional and retail investors with indirect

access to the physical platinum and palladium bullion market while providing them with the liquidity of an exchange traded security. The Units may be bought and sold on the NYSE Arca and the TSX like

any other exchange-listed securities.

- •

- Investment in Physical Platinum and Palladium Bullion

Only. Except with respect to cash held by the Trust to pay expenses and anticipated redemptions, the Trust currently owns only physical

platinum and palladium bullion that is certified as conforming to the London Good Delivery Standard of the London Platinum and Palladium Market, or LPPM, to which we will refer as Good

Delivery. The Manager currently holds and intends to continue to invest and hold approximately 97% of the total net assets of the Trust in physical platinum and palladium bullion in London Good

Delivery plate or ingot form. The Trust does not invest in platinum or palladium certificates, futures or other financial instruments that represent platinum and palladium or that may be exchanged for

platinum and palladium.

- •

- Lower Transaction Costs. The Manager expects that, for