UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

PURSUANT TO SECTION 13

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended:

Commission file number

(Exact name of Registrant as specified in its charter)

SUPERVIELLE GROUP S.A.

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

Republic of

(Address of principal executive offices)

Republic of

Tel: 54-

Email:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

| Trading |

| Name of each exchange |

|

| |||

|

|

*Not for trading, but only in connection with the registration of American Depositary Shares pursuant to the requirements of the New York Stock Exchange.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2023 (excluding shares held by the Company’s treasury as of December 31, 2023) was:

Title of class |

| Number of shares outstanding |

Class B ordinary shares, nominal value Ps.1.00 per share |

| |

Class A ordinary shares, nominal value Ps.1.00 per share |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated Filer |

| ☐ |

|

| ☒ | |

Non-accelerated Filer |

| ☐ |

| Emerging Growth Company |

|

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by checkmark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ☐ |

|

|

| Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

TABLE OF CONTENTS

| Page | |

iii | ||

iv | ||

vi | ||

1 | ||

Item 1. Identity of Directors, Senior Management and Advisors | 1 | |

1 | ||

1 | ||

1 | ||

1 | ||

1 | ||

1 | ||

23 | ||

23 | ||

28 | ||

109 | ||

113 | ||

113 | ||

135 | ||

135 | ||

157 | ||

Item 5.C Research and Development, patents and licenses, etc. | 164 | |

164 | ||

166 | ||

167 | ||

195 | ||

195 | ||

196 | ||

199 | ||

199 | ||

Item 8.A Consolidated Statements and Other Financial Information. | 199 | |

203 | ||

203 | ||

203 | ||

203 |

i

| Page | |

|---|---|---|

203 | ||

203 | ||

203 | ||

203 | ||

203 | ||

203 | ||

204 | ||

204 | ||

204 | ||

214 | ||

225 | ||

225 | ||

226 | ||

226 | ||

Item 11. Quantitative and Qualitative Disclosures about Market Risk | 226 | |

Item 12. Description of Securities Other Than Equity Securities | 231 | |

231 | ||

231 | ||

231 | ||

232 | ||

233 | ||

233 | ||

Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds | 233 | |

233 | ||

234 | ||

234 | ||

234 | ||

235 | ||

Item 16.D Exemptions from the Listing Standards for Audit Committees | 236 | |

Item 16.E Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 236 | |

238 | ||

238 | ||

243 | ||

Item 16.I Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 243 | |

243 | ||

245 | ||

245 | ||

246 |

ii

INTRODUCTION

CERTAIN DEFINED TERMS AND CONVENTIONS

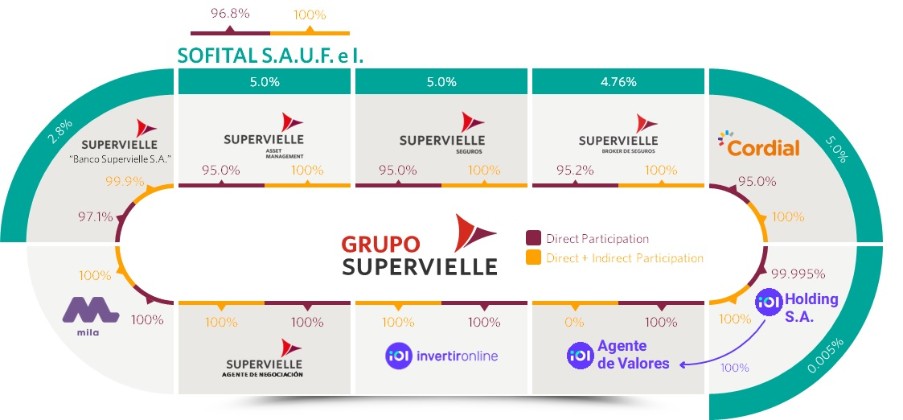

In this annual report, we use the terms “we,” “us,” “our,” “the Company” and the “Group” to refer to Grupo Supervielle S.A. and its consolidated subsidiaries, including Banco Supervielle S.A., unless otherwise indicated. References to “Grupo Supervielle” mean Grupo Supervielle S.A. References to the “Bank” mean Banco Supervielle S.A. and its consolidated subsidiaries. References to “Supervielle Seguros” mean Supervielle Seguros S.A. References to “Supervielle Productores Asesores de Seguros” mean Supervielle Productores Asesores de Seguros S.A. References to “SAM” mean Supervielle Asset Management S.A. References to “Supervielle Agente de Negociacion” mean Supervielle Agente de Negociación S.A.U. References to “IOL invertironline” mean InvertirOnline S.A.U. and Portal Integral de Inversiones S.A.U. References to “Espacio Cordial” or “Cordial Servicios” mean Espacio Cordial de Servicios S.A. References to “MILA” mean Micro Lending S.A.U. References to “IUDÚ” mean IUDÚ Compañía Financiera S.A. References to “Tarjeta” mean Tarjeta Automática S.A. References to “Bolsillo Digital” mean Bolsillo Digital S.A.U. References to “Sofital” mean Sofital S.A.U.F.e I. References to “IOL Holding” mean IOL Holding S.A. References to “Dólar IOL” mean Dólar IOL S.A.

References to “Class A shares” are to shares of our Class A common stock, with a par value of Ps.1.00 per share, references to “Class B shares” are to shares of our Class B common stock, with a par value of Ps.1.00 per share, and references to “ADSs” are to American depositary shares, each representing five Class B shares.

The term “Argentina” refers to the Republic of Argentina. The terms “Argentine government,” the “government” or the “Government” refers to the Federal Government of Argentina, the terms “Central Bank” or the “Argentine Central Bank” refer to the Banco Central de la República Argentina, and the term “CNV” refers to the Argentine Comisión Nacional de Valores, which is the Argentine securities and capital markets regulator. The term “ByMA” refers to Bolsas y Mercados Argentinos S.A., which is the Argentine securities exchange. The term “MAE” refers to Mercado Abierto Electrónico S.A., which is the Argentine electronic securities and foreign-currency trading exchange. The term “Argentine Capital Markets Law” refers to Law No. 26,831, as amended and supplemented. The term “Argentine Negotiable Obligations Law” refers to Law No. 23,576, as amended and supplemented. The term “Argentine General Corporations Law” refers to Law No. 19,550, as amended and supplemented. The term “Argentine Productive Financing Law” refers to Law No. 27,440, as amended and supplemented.

“Argentine GAAP” refers to generally accepted accounting principles in Argentina and “Argentine Banking GAAP” refers to the accounting rules of the Central Bank. “IASB” refers to International Accounting Standards Board and “IFRS” refers to the International Financial Reporting Standards, as issued by the IASB.

The term “GDP” refers to gross domestic product and all references in this annual report to GDP growth are to real GDP growth. The term “CPI” refers to the consumer price index and the term “WPI” refers to the wholesale price index.

The term “customers” refers to individuals that have at least one active product with us and made at least one transaction in the previous 90 days, and entities that have at least one active checking account with us.

The term “digital customers” refers to individuals that use our online banking services, our mobile app or our senior citizens app during the previous 90 days.

The term “Argentine banks” refers to banks that operate in Argentina. Unless the context otherwise requires, the term “financial institutions” refers to institutions regulated by the Central Bank. The term “Argentine private banks” refers to banks that are not controlled or owned by the Government or any Argentine provincial, municipality or city government.

For information from January 1, 2021 to December 31, 2021, the term “small businesses” refers to individuals and businesses with annual sales up to Ps.300 million, the term “SMEs” refers to individuals and businesses with annual sales over Ps.300 million and below Ps.1.5 billion, the term “middle-market companies” refers to companies with annual sales over Ps.1.5 billion and below Ps.3 billion and the term “large corporates” refers to companies with annual sales over Ps.3 billion. For information from January 1, 2022 to December 31, 2022, the term “small businesses” refers to individuals and businesses with annual sales up to Ps.300 million, the term “SMEs” refers to individuals and businesses with annual sales over Ps.300 million and below Ps.3 billion, the term “middle-market and large companies” refers to companies with annual sales over Ps.3 billion. For information from January 1, 2023 to December 31, 2023, the term “small businesses” refers to individuals and businesses with annual sales up to Ps.500 million, the term “SMEs” refers to individuals and businesses with annual sales over Ps.500 million and below Ps.5 billion, the term “middle-market and large companies”

iii

refers to companies with annual sales over Ps.5 billion. Since January 1, 2024, the term “small businesses” refers to individuals and businesses with annual sales up to Ps.1.5 billion, the term “SMEs” refers to individuals and businesses with annual sales over Ps.1.5 billion and below Ps.10 billion, and the term “middle-market and large companies” refers to companies with annual sales over Ps.10 billion. Although the main criteria is annual sales, in some cases the definitions also consider whether these individuals, businesses and companies provide adequate customer service models pursuant to the requirements which apply to them.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Statements

This annual report contains our audited consolidated financial statements as of December, 2023 and 2022, and for the years ended December 31, 2023, 2022 and 2021 (our “audited consolidated financial statements”), which have been audited by Price Waterhouse & Co. S.R.L.,

“Financial Reporting in Hyperinflationary Economies” (IAS 29) requires that the financial statements of an entity whose functional currency is one of a hyperinflationary economy be measured in terms of the current unit of measurement at the closing date of the reporting period, regardless of whether they are based on the historical cost method or the current cost method. This requirement also includes the comparative information in financial statements. Our audited consolidated financial statements are stated in the measurement unit current as of December 31, 2023.

We are subject to the provisions of Article 2 – Section I – Chapter I of Title IV (“Periodical Reporting Requirements”) of the rules issued by the CNV according to General Resolution No. 622/2013, as amended and supplemented (the “CNV Rules”), and we are required to present our financial statements in accordance with the Argentine Banking GAAP. The Argentine Central Bank, through Communications “A” 5541, as amended, set forth a convergence plan towards the application of IFRS as issued by the IASB and the interpretations issued by the International Financial Reporting Standards Committee (“IFRIC”), for entities under its supervision, effective for fiscal years beginning on or after January 1, 2018, subject to the following exceptions:

•the temporary exception from IFRS 9 “Financial Instruments” with respect to expected credit loss of financial instruments of the public sector;

•option to classify holdings in dual bonds at amortized cost or fair value through other comprehensive income; and

•the application of IFRS 17 "Insurance Contracts" will be optional until the BCRA makes it mandatory.

Our consolidated financial statements contained in this annual report differ in certain material respects from our financial statements as of December 31, 2023 and 2022 and for the years ended December 31, 2023, 2022 and 2021 prepared in accordance with Argentine Banking GAAP and filed with the CNV.

Unless otherwise indicated, all financial information of our company included in this annual report is stated on a consolidated basis under IFRS and presented in terms of the measuring unit current at the end of the latest reporting period.

Overview of IAS 29

IAS 29 establishes the conditions under which an entity shall restate its financial statements if it is located in an economic environment considered hyperinflationary. This standard requires that the financial statements of an entity that reports in the currency of a highly inflationary economy shall be stated in terms of the measuring unit current at the closing date of the latest reporting period, regardless of whether they are based on a historical cost approach or a current cost approach. To this end, in general terms, the inflation rate must be computed in the non-monetary items as of the acquisition date or the revaluation date, as applicable. These requirements also comprise the comparative information of the financial statements.

In order to conclude whether an economy is categorized as highly inflationary, IAS 29 outlines a series of factors to be considered, including the existence of an accumulated inflation rate in three years that is approximate to or exceeds 100%. Argentina has reported a cumulative three-year inflation rate significantly higher than 100% and therefore financial information must be adjusted for inflation in accordance with IAS 29. Consequently, we have applied IAS 29 to our audited consolidated financial statements.

iv

Adjustment for inflation in the initial balances has been calculated considering the indexes based on the price indexes published by Argentina’s National Statistics Institute (Instituto Nacional de Estadística y Censos or “INDEC,” per its initials in Spanish). The Group determined to use the Internal Wholesale Price Index (IWPI) to restate balances and transactions until the year 2016. For November and December 2015, Grupo Supervielle used the average variation of the CPI of the City of Buenos Aires since during these two months there were no IWPI measurements available at a national level. From January 2017 onwards, Grupo Supervielle used the national CPI.

The principal inflation adjustment procedures are the following:

| ● | Monetary assets and liabilities that are recorded in the current currency as of the financial position’s closing date are not restated because they are already stated in terms of the currency unit current as of the date of the financial statements. |

| ● | Non-monetary assets and liabilities are recorded at cost as of the financial position date, and equity components are restated applying the relevant adjustment ratios. |

| ● | All items in the consolidated income statement are restated applying the relevant conversion factors, as described in Note 1.1.2 to our consolidated financial statements contained in this annual report. |

| ● | The effect of inflation in Grupo Supervielle’s net monetary position is included in the consolidated income statement, in the item “Results from exposure to changes in the purchasing power of money.” |

| ● | Comparative figures have been adjusted for inflation following the procedure explained in the previous bullets. |

| ● | Upon initially applying inflation adjustment, the equity accounts were restated as follows: |

| o | Capital stock was restated as from the date of subscription or the date of the most recent inflation adjustment for accounting purposes, whichever is later. |

| o | The resulting amount was included in the “Results from exposure to changes in the purchasing power of money” account. |

| o | Consolidated Statement of Comprehensive Income were restated as from each accounting allocation. |

| o | The legal reserve and other reserves in the statement of Changes in Shareholders’ Equity were not restated as of the initial application date. |

Certain Financial Data

The term “ROAE” refers to return on average shareholders’ equity, calculated based on daily averages. The term “ROAA” refers to return on average assets, calculated based on daily averages. ROAE and ROAA are frequently used by financial institutions as benchmarks to measure profitability compared to peers but not as benchmarks to determine returns for investors, which is affected by multiple factors that ROAE and ROAA do not consider.

Currencies and Rounding

The terms “U.S. dollar” and “U.S. dollars” and the symbol “U.S.$” refer to the legal currency of the United States. The terms “Peso” and “Pesos” and the symbol “Ps.” and “$” refer to the legal currency of Argentina.

v

We have translated certain of the Peso amounts contained in this annual report into U.S. dollars for convenience purposes only. Unless otherwise indicated, the rate used to translate such amounts as of December 31, 2023 was Ps.808.48 to U.S.$1.00, which was the reference exchange rate reported by the Central Bank for U.S. dollars as of December 31, 2023. The Federal Reserve Bank of New York does not report a noon buying rate for Pesos. The U.S. dollar equivalent information presented in this annual report is provided solely for the convenience of investors and should not be construed as implying that the Peso amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate. The reference exchange rate reported by the Central Bank was Ps.873.75 per U.S.$1.00 as of April 25, 2024. See “Item 3.D. Risk Factors—Risks Relating to Argentina—Fluctuations in the value of the Peso could adversely affect the Argentine economy” and “Item 3.D. Risk Factors—Risks Relating to Argentina—The maintenance or implementation of additional exchange controls regulations, restrictions on transfers abroad and capital inflow restrictions could limit the availability of international credit and could threaten the financial system, which may adversely affect the Argentine economy.”

Certain figures included in this annual report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that precede them.

Market Share and Other Information

We make statements in this annual report about our competitive position and market share in, and the market size of, the Argentine banking industry. We have made these statements on the basis of statistics and other information derived from the Central Bank’s publications and other third-party sources that we believe are reliable. Although we have no reason to believe any of this information or these reports are inaccurate in any material respect, we have not independently verified the competitive position, market share and market size or market growth data provided by third parties or by industry or general publications.

FORWARD-LOOKING STATEMENTS

This annual report contains estimates and forward-looking statements, principally in “Item 3.D. Risk Factors,” “Item 5.A. Operating Results,” and “Item 4.B. Business Overview.” We have based these forward-looking statements largely on our current beliefs, expectations and projections about future courses of action, events and financial trends affecting our business. Many important factors, in addition to those discussed elsewhere in this annual report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including, among others:

| (i) | changes in general economic, financial, business, political, legal, social or other conditions in Argentina, including whether the new administration will be able to effectively implement its announced policies; |

| (ii) | fluctuations in the foreign exchange reserves, the exchange rate of the Peso and inflation; |

| (iii) | changes in foreign exchange regulations and exchange control measures implemented by the Central Bank and the Argentine government; |

| (iv) | changes in interest rates and the cost of deposits, which may, among other things, affect margins; |

| (v) | the compliance of the commitments and conditions included in the agreement with the International Monetary Fund (“IMF”); |

| (vi) | unanticipated increases in financing or other costs or the inability to obtain additional debt or equity financing on attractive terms, which may limit our ability to fund existing operations and to finance new activities; |

| (vii) | changes in capital markets in general that may affect policies or attitudes toward lending to or investing in Argentina or Argentine companies, including expected or unexpected volatility in domestic and international financial markets; |

| (viii) | changes in government regulation, including tax and banking regulations; |

| (ix) | the impact of pandemics, epidemics and other health events, including the coronavirus 2019 (“COVID-19”) and government measures taken in response to them, on economic activity, our results of operation and our operations; |

| (x) | adverse legal or regulatory disputes or proceedings; |

| (xi) | credit and other risks of lending, such as increases in defaults by borrowers; |

vi

| (xii) | exposure to Argentine government liabilities and fluctuations and declines in the value of Argentine public debt; |

| (xiii) | increased competition in the banking, financial services, credit card services, asset management and related industries; |

| (xiv) | a loss of market share by any of our main businesses; |

| (xv) | increase in the allowances for loan losses; |

| (xvi) | technological changes or an inability to implement new technologies, changes in consumer spending and saving habits; |

| (xvii) | threats of cybersecurity breaches; |

| (xviii) | ability to implement our business strategy; and |

| (xix) | other factors discussed under “Item 3.D. Risk Factors” in this annual report. |

The words “believe,” “may,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “forecast” and similar words are intended to identify forward-looking statements. Forward-looking statements include information concerning our possible or assumed future results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements speak only as of the date they were made, and we do not undertake any obligation to update publicly or to revise any forward-looking statements after we distribute this annual report because of new information, future events or other factors, except as required by applicable law. In light of the risks and uncertainties described above, the forward-looking events and circumstances discussed in this annual report might not occur and do not constitute guarantees of future performance. Because of these uncertainties, you should not make any investment decisions based on these estimates and forward-looking statements.

vii

PART I

Item 1.Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2.Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Item 3.A[Reserved]

Item 3.BCapitalization and indebtedness

Not applicable.

Item 3.CReasons for the offer and use of proceeds

Not applicable.

Item 3.DRisk Factors

Summary of Risk Factors

The following summarizes some, but not all, of the principal risks provided below. Please carefully consider all of the information discussed in this Item 3.D “Risk Factors” in this annual report for a detailed description of these and other risks.

| ● | Our business is largely dependent upon macroeconomic, political, regulatory and social conditions in Argentina. |

| ● | If the current levels of inflation continue or increase, the Argentine economy and our business and financial condition could be adversely affected. |

| ● | A decrease in international prices for the main commodities exported by Argentina or a significant decline in their production could negatively affect Argentina’s economic condition. |

| ● | Persistent fiscal deficit could result in long lasting adverse consequences for the Argentine economy, which in turn could adversely affect our business, financial condition and results of operations. |

| ● | Fluctuations in the value of the Peso could adversely affect the Argentine economy. |

| ● | The maintenance or implementation of additional exchange controls regulations, restrictions on transfers abroad and capital inflow restrictions could limit the availability of international credit and could threaten the financial system, which may adversely affect the Argentine economy. |

| ● | The Argentine government’s ability to obtain financing from the international loan and capital markets may be limited or costly, which may impair its ability to implement reforms and foster economic growth. |

| ● | Government intervention in the Argentine economy could undermine business and investor confidence. |

| ● | Developments in other countries may adversely affect the Argentine economy and our financial performance. |

1

| ● | We operate in a highly regulated environment, and our operations are subject to regulations adopted, and measures taken, by several regulatory agencies. |

| ● | The stability of the Argentine financial system depends upon the ability of financial institutions, including the Bank, the main subsidiary of the Group, to retain the confidence of depositors. |

| ● | The asset quality of financial institutions, including ourselves, may deteriorate if the Argentine private sector continues to be affected by adverse macroecononic conditions in Argentina. |

| ● | Argentine financial institutions, including us, continue to have significant exposure to public sector debt, including securities issued by the Argentine Central Bank, and its repayment or refinancing capacity, which in periods of uncertainty may negatively affect their results of operations. |

| ● | Enforcement of creditors’ rights in Argentina may be limited, costly and lengthy. |

| ● | Changes in market conditions and any associated risks, including interest rate and currency exchange volatility, could materially and adversely affect our consolidated financial condition and results of operations. |

| ● | Reduced spreads between interest rates on loans and those on deposits could adversely affect the Bank’s profitability. |

| ● | Due to our exposure to middle and lower-middle-income individuals and SMEs, the quality of our consolidated loan portfolio is more susceptible to economic downturns and recessions. |

| ● | Our estimates and established reserves for credit risk and potential credit losses may prove to be insufficient, which may materially and adversely affect our asset quality and our financial condition and results of operations. |

| ● | The Bank’s revenues from its business with senior citizens could decrease or cease to grow if the agreement with ANSES is terminated or not renewed. |

| ● | Cybersecurity events could negatively affect our reputation, our financial condition and our results of operations. |

| ● | Our controlling shareholder has the ability to direct our business, and potential conflicts of interest could arise. |

You should carefully consider the risks described below, as well as the other information in this annual report. Our business, results of operations, financial condition or prospects could be materially and adversely affected if any of these risks occurs. In general, investors take more risk when they invest in the securities of issuers in emerging countries such as Argentina than when they invest in the securities of issuers in the United States and other more developed markets. The risks described below are those known to us and that as of the date of this annual report believe may materially affect us.

Risks Relating to Argentina

Our business is largely dependent upon macroeconomic, political, regulatory and social conditions in Argentina.

Substantially all of our operations, property and customers are located in Argentina. As a result, the quality of our assets, our financial condition and the results of our operations are dependent upon the macroeconomic, regulatory, social and political conditions prevailing in Argentina from time to time. These conditions include growth rates, inflation rates, exchange rates, taxes, foreign exchange controls, changes to interest rates, changes to government policies, social instability, and other political, economic or international developments either taking place in, or otherwise affecting, Argentina.

Developments in economic, political, regulatory and social conditions in Argentina, and measures taken by the Argentine government, have had and are expected to continue to have a significant impact on our business, results of operations and financial condition. Argentina is an emerging country and investing in such markets generally carries additional risks.

2

The Argentine economy has experienced significant volatility in the past decades, including multiple periods of low or negative growth and high levels of inflation and currency depreciation, and may experience further volatility in the future. According to data published by the INDEC, Argentina’s GDP in 2022 increased by 5.0% compared to 2021. In 2023, Argentina’s GDP decreased by 1.6% compared to 2022, according to data published by the INDEC, primarily due to the drought which mainly affected the agricultural production in Argentina, which decreased 20.4% compared to 2022.

Argentine economic conditions are dependent on a variety of factors, including the following: (i) domestic production, international demand and prices for Argentina’s principal commodity exports; (ii) the competitiveness and efficiency of domestic industries and services; (iii) the stability and competitiveness of the Peso against foreign currencies; (iv) the rate of inflation; (v) the government’s fiscal deficits; (vi) the government’s public debt levels; (vii) foreign and domestic investment and financing; and (viii) governmental policies and the legal and regulatory environment. Government policies and regulation –which at times have been implemented through informal or de facto measures and have been subject to radical shifts– that have had a significant impact on the Argentine economy in the past, have included, among others: (i) monetary policy, including exchange controls, capital controls, high interest rates and a variety of measures to curb inflation; (ii) restrictions on exports and imports; (iii) price controls; (iv) mandatory wage increases or prohibition of dismissals; (v) taxation; and (vi) government intervention in the private sector.

The IMF and the Argentine authorities reached an understanding on key policies as part of their ongoing discussions of an IMF-supported program in order to renegotiate the principal maturities of the U.S.$44.1 billion under a stand-by arrangement. On March 25, 2022, the IMF approved the execution of the financing agreement (the “IMF Agreement”) with Argentina for a total amount of U.S.$44 billion, which included a disbursement of U.S.$9.6 billion. In October 2022, December 2022, April 2023 and August 2023, the IMF authorized disbursements of U.S.$3.8 billion, U.S.$6 billion, U.S.$5.4 billion and U.S.$7.5 billion, respectively, following Argentina’s completion of the targets set forth in the IMF Agreement. In addition, the IMF and the Argentine government agreed to revise the targets set forth in the IMF Agreement considering the negative impact that the drought had on the Argentine economy in 2023. On January 31, 2024, the new Argentine government and the IMF agreed to revise the targets set forth in the IMF Agreement. The target for reserve accumulation increased to U.S.$10 billion, originally set at U.S.$8.2 billion. As a result of these revisions, in January 31, 2024, the IMF authorized an additional disbursement of approximately U.S.$4.7 billion. As of the date of this annual report, the aggregate amount of disbursements authorized by the IMF is approximately U.S.$40.6 billion. According to the IMF, Argentina is implementing an ambitious stabilization plan focused on the establishment of a strong fiscal anchor along with policies to bring down inflation. The IMF monitors Argentina’s compliance with the agreement at the end of each quarter. We cannot assure that the conditions of the IMF Agreement will not affect Argentina’s ability to implement reforms and public policies and boost economic growth, nor the impact that the IMF Agreement may have in Argentina’s ability to access international capital markets (and indirectly in our ability to access those markets).

On November 19, 2023, a presidential runoff election took place between Javier Milei, candidate of “La Libertad Avanza” and Sergio Massa, candidate of “Union por la Patria”, with Javier Milei being elected President of the Nation, with 55.69% of the votes, and taking office on December 10, 2023. Also as a result of the 2023 elections, La Libertad Avanza has 7 of the 72 representatives in the Senate and 41 of the 257 representatives in the Chamber of Deputies. The new administration has indicated that it intends to implement business friendly policies, but we cannot assure you that it will be able to implement these policies, considering that it does not hold a majority of the representatives in each chamber of Congress.

The newly elected government faces significant macroeconomic challenges, such as reducing the inflation rate, achieving commercial and fiscal surpluses, accumulating reserves, supporting the peso, refinancing debt owed to private creditors, and improving the competitiveness of the Argentine economy based on different factors that affect it, including the conflict between Ukraine and Russia, and the conflict between Israel and Hamas in the Gaza Strip. Since the new administration took office, a large number of measures aimed at deregulating the Argentine economy and limiting government intervention in the private sector have been implemented, and it is expected that further measures will be adopted in the future. As of the date of this annual report, we cannot predict the impact that these measures, and any future measures that may be adopted by the government, will have on the Argentine economy in general and on the financial sector in particular.

Political uncertainty in Argentina regarding the policies adopted and that may be adopted in the future by the government could lead to further volatility in the market prices of the securities of Argentine issuers and could have a material adverse effect on the economy or on Argentina’s ability to meet its obligations, which in turn could adversely affect our financial condition and results of operations.

3

We cannot assure you that developments in Argentina will not affect macroeconomic, political, regulatory or social conditions in the country and, consequently, affect our business, result of operations and financial condition.

If the current levels of inflation continue or increase, the Argentine economy and our business and financial condition could be adversely affected.

In the past, inflation has materially undermined the Argentine economy and Argentina’s ability to create conditions that would permit growth. High inflation may also undermine Argentina’s competitiveness abroad and lead to a decline in private consumption which, in turn, could also affect employment levels, salaries and interest rates. Moreover, a high inflation rate could undermine confidence in the Argentine financial system, reducing the Peso deposit base and negatively affecting long-term credit markets.

In recent years, Argentina has confronted high inflationary pressures, and continues to do so. In 2021, the INDEC registered an increase in CPI of 50.9% and an increase in WPI of 51.3%. In 2022, the INDEC registered an increase in CPI of 94.8% and an increase in WPI of 94.8%. In 2023, the INDEC registered an increase in CPI of 211.4% and an increase in WPI of 276.4%, which represents the highest annual inflation since 1991. The CPI published by the INDEC for the months of January and February 2024 was 20.6% and 13.2%, respectively. In March 2024, the INDEC registered a CPI of 11.0%, reaching a level of 287.9% year over year.

In June 2018, the International Practices Task Force categorized Argentina as a country with a projected three-year cumulative inflation rate greater than 100%. Pursuant to IAS 29 (Financial Reporting in Hyperinflationary Economies), the financial statements of entities whose functional currency is that of a hyperinflationary economy must be restated in a suitable general price index to control the effects of changes. Argentine companies applying IFRS are required to apply IAS 29 to their financial statements for periods ending on and after July 1, 2018. In addition, certain regulatory authorities, such as the CNV, have required that financial statements submitted to the CNV for the periods ended on and after December 31, 2018 be restated for inflation in accordance with IAS 29.

On April 8, 2024, the Argentine Central Bank announced that the new inflation estimate for 2024 is 189.4% pursuant to its survey of market expectations (Relevamiento de Expectativas de Mercado) which was made between March 25 and March 27, 2024.

There can be no assurances that inflation rates will decrease, remain flat or not escalate in the future or that the measures adopted or that may be adopted by the administration to control inflation will be effective or successful. If inflation levels remain high or rise in the future, the development of the Argentine economy could be negatively impacted and, in particular, our costs of operation could increase, which may negatively affect our business, financial condition and results of operations.

A decrease in international prices for the main commodities exported by Argentina or a significant decline in their production could negatively affect Argentina’s economic condition.

Argentina’s reliance on the export of certain commodities, particularly soybeans and its by products, corn and wheat, has made the country more vulnerable to fluctuations in their prices. A decrease in commodity prices may adversely affect the Argentine government’s fiscal revenues and the Argentine economy as a whole and, as a result, negatively impact the Bank’s business, financial condition and results of operations. Given its reliance on these agricultural commodities, Argentina is also vulnerable to weather events, such as the droughts which occurred in Argentina in 2018 and 2023, which may negatively affect the production of such commodities, reducing fiscal revenues and the inflow of U.S. dollars. A continued fall in the international prices of the main commodities exported by Argentina or any future weather conditions that may have an adverse effect on agriculture could have a negative effect on the level of government revenues and its ability to service its public debt and could generate recessionary or inflationary pressures, depending on the government's reaction.

The negative impact that the droughts which occurred in Argentina in 2018 and 2023 have had in Argentina has been reinforced by the historic drop in the Paraná river (Argentina’s main river) and a large number of fire outbreaks in multiple Argentine provinces during 2022. These environmental events have negatively affected the agriculture sector in Argentina. If any severe weather events, including droughts, occur in the future, productive activities in Argentina, the level of foreign exchange reserves in the Central Bank and the Argentine economy as a whole could be adversely affected. Adverse weather conditions may affect the production of commodities by the agricultural sector, which represents a significant portion of Argentina's export revenues. In 2023, rainfall in the core region of Argentina, the most productive area of the country, was 20% below the historical average, although the projections for soybean and corn harvest for the 2023/24 season are positive.

4

If the international prices for agricultural commodities decrease or if the production of such commodities is diminished, Argentina’s economy could be adversely affected. In addition, such circumstances could have a negative impact on the government’s tax revenues, including its ability to repay its debt, and on the availability of foreign currency. Any such developments may adversely affect Argentina’s economy and, as a result, our business, results of operations and financial condition.

The conflict between Russia and Ukraine and the conflict between Israel and Hamas in the Gaza Strip have affected and could continue to affect other countries worldwide, generating increases in the international prices of oil, gas, and commodities, including those produced by Argentina. However, a long-term decrease in the international price of oil would negatively impact the oil and gas prospects of Argentina and result in a decrease in foreign investment in these sectors.

Persistent fiscal deficit could result in long lasting adverse consequences for the Argentine economy, which in turn could adversely affect our business, financial condition and results of operations.

During the last years, the Argentine government has sustained high levels of fiscal deficit, and has resorted regularly to the Central Bank to source part of its funding requirements. In 2021 and 2022 public sector expenditure increased approximately 49.6% and 54.8%, respectively, and the government achieved a primary fiscal deficit of 2.2% and 2.4% Argentina’s GDP, respectively, according to the Argentine Ministry of Treasury. In 2023, public sector revenues decreased approximately 4.7%, mainly as a result of the significant drop in income from withholdings as a result of the drought which occurred in Argentina in 2023, and public expenditures decreased 4.9%, mainly due to a reduction in real terms in social benefits and subsidies. The government achieved a primary fiscal deficit of 2.7% Argentina’s GDP in 2023.

Following the agreement with the IMF, in January 2024 Argentina committed to achieve a primary fiscal surplus of 2.0% of Argentina’s GDP in 2024.

Despite the announced commitment from Javier Milei’s new administration aimed at eliminating fiscal deficit, we cannot assure you that in the future the Argentine government will not seek to finance its deficit by gaining access to the liquidity available in the local financial institutions. In that case, government initiatives that increase the exposure of local financial institutions to the public sector could affect our liquidity and assets quality and have a negative effect on clients’ confidence in the financial system.

Fluctuations in the value of the Peso could adversely affect the Argentine economy.

Fluctuations in the value of the Peso continue to affect the Argentine economy. Since January 2002, the Peso has fluctuated significantly in value. Persistent high inflation, together with formal and de facto exchange controls, and restrictions on foreign trade, highly distorted relative prices have resulted in the loss of competitiveness of Argentine production, impeded investment and caused economic stagnation. In 2021 and 2022 the Peso depreciated against to the US dollar a 22% and a 72.4%, respectively. In 2023, the Peso depreciated 356% with respect to the U.S. dollar and, after the election of President Javier Milei, the exchange rate devalued by 118%. As of April 25, 2024, the exchange rate was Ps.873.75 per U.S.$1.00.

The depreciation of the Peso may have a negative impact on the ability of certain Argentine businesses to service their foreign currency denominated debt, lead to inflation, significantly reduce real wages and jeopardize the stability of businesses whose success depends on domestic market demand, and also adversely affect the Argentine government’s ability to honor its foreign debt obligations. In turn, a significant appreciation of the Peso against the U.S. dollar also presents risks for the Argentine economy, including the possibility of a reduction in exports as a consequence of the loss of external competitiveness. Any such appreciation could also have a negative effect on economic growth and employment and reduce tax revenues in real terms.

The maintenance or implementation of additional exchange controls regulations, restrictions on transfers abroad and capital inflow restrictions could limit the availability of international credit and could threaten the financial system, which may adversely affect the Argentine economy.

In the past, the Argentine government has increased controls on the sale of foreign currency, limiting transfers of funds abroad. Measures taken by the Argentine government significantly curtailed access to the official foreign exchange market and, as a result, an unofficial U.S. dollar trading market developed in which the Peso-U.S. dollar exchange rate differed substantially from the official Peso-U.S. dollar exchange rate. The current exchange controls apply with respect to access to the foreign exchange market by residents for savings and investment purposes abroad, the payment of external financial debts abroad, the payment of dividends in foreign currency

5

abroad, payments of imports and exports of goods and services, and the obligation to repatriate and settle the proceeds from exports of goods and services for Pesos, among others. For further information, see “Item 10.D. Exchange Controls”.

In September 2020, the Central Bank issued Communication “A” 7106 which restricted the access to the foreign exchange market for the repayment of principal payments under certain external financial indebtedness maturing between October 15, 2020 and March 31, 2021, which led many borrowers to refinance their debts. These restrictions were further amended and applied to external financial indebtedness maturing between October 15, 2020 and December 31, 2023. We cannot assure you whether the Central Bank will adopt similar restrictions in the future.

We cannot anticipate for how long these measures will be in force or if additional restrictions will be imposed. The Argentine government could maintain or impose new exchange controls, restrictions and take other measures in response to capital flight or a significant depreciation of the Peso, which could in turn limit access to the international capital markets and affect the Argentine economy. In addition, such evolving exchange control restrictions and measures may result in Argentine Central Banks’s information requests, enforcement actions and penalties due to diverging interpretations of foreign exchange regulatoins.

As a related matter, the international reserves deposited with the Argentine Central Bank have fluctuated significantly. The amount of international reserves of the Argentine government reached U.S.$28.4 billion as of March 2024, which represents an increase of approximately U.S.$7.0 billion since November 2023.

In addition, since the imposition of exchange controls, the difference between the official exchange rate, which is currently used for both commercial and financial operations, and other informal exchange rates that arise implicitly as a result of certain operations commonly carried out in the capital market (dollar “MEP” or “contado con liquidación”), have broadened deeply during 2023. However, in an effort to address the fiscal deficit, the newly elected government implemented a currency adjustment, leading to a devaluation of the Peso of approximately 50% in December 2023. From December 2023, the Peso has devaluated 2% every month which has reduced the gap between the official exchange rate and the other informal exchange rates to approximately 21% as of April 23, 2024.

The Argentine government could maintain a single official exchange rate or create multiple exchange rates for different types of transactions, substantially modifying the applicable exchange rate at which we acquire currency for different purposes. Furthermore, existing or future measures could undermine the Argentine government’s public finances, which could adversely affect Argentina’s economy, which, in turn, could adversely affect our business, results of operations and financial condition.

The Argentine government’s ability to obtain financing from the international loan and capital markets may be limited or costly, which may impair its ability to implement reforms and foster economic growth.

During recent years the Argentine government has faced difficulties in the payment of its sovereign debt. As a result, the Argentine government may not have access to international financing, or its access may be costly, which would limit its ability to make investments and foster economic growth. Additionally, Argentine companies may also have difficulty accessing international financing, at reasonable costs or at all.

During March 2020, the Argentine government initiated discussions with various groups of creditors to discuss a path for Argentina’s debt sustainability. With respect to Argentina’s international bonds, the Argentine executive branch approved the restructuring of certain eligible global bonds issued under foreign laws for up to U.S.$65 billion. In August 2020, the Argentine government announced that it had obtained the consents required to exchange 99% of the aggregate principal amount outstanding of all series of eligible bonds.

In March 2020, the then former Minister of Economy Martin Guzman addressed a letter to the Paris Club members expressing Argentina’s decision to postpone until May 2021 the U.S.$2.1 billion payment originally due in May 2020, in accordance with the terms of the settlement agreement Argentina had reached with the Paris Club members in May 2014 (the “Paris Club 2014 Settlement Agreement”). In addition, in April 2020, the Minister of Economy sent the Paris Club members a proposal to modify the existing terms of the Paris Club 2014 Settlement Agreement, seeking mainly an extension of the maturity dates and a significant reduction in the interest rate. In June 2021, the parties agreed that Argentina would pay U.S.$430 million to the Paris Club members before the end of July and the rest during the following year to avert default in July 2021. On March 22, 2022, the Argentine government reached an agreement with the Paris Club for a new extension of the agreement reached in June 2021.

6

On October 28, 2022, the former Minister of Economy, Sergio Massa, announced a new agreement with the Paris Club pursuant to which the maturity date of the outstanding amount of debt under the agreement entered into by the Argentina government and the Paris Club in 2014 was extended to September 2028 and the interest rate decreased from 9% to 3.9% in the first three installments, with a gradual increase to 4.5%. The payment profile implies an average semi-annual payment of U.S.$170 million (principal and interest included). Over the next two years Argentina is expected to repay 40% of outstanding debt, which amounts to U.S.$1,971 million. On June 26, 2023, Sergio Massa signed bilateral agreements with three members of the Paris Club to refinance the existing debt with the institution. Thus, after signing the new agreement reached in 2022, the former Minister of Economy was able to seal bilateral agreements with 15 of the 16 creditors of the institution.

In June 2018, the Argentine government and the IMF signed a three-year, U.S.$50 billion loan agreement, as further amended to U.S.$57.1 billion through 2021 (the “IMF 2018 Agreement”). Following an IMF report in February 2020 stating that Argentina’s debt may not be sustainable, the Argentine government requested to begin discussions with the IMF in order to renegotiate the principal maturities of the U.S.$44.1 billion disbursed between 2018 and 2019 under a stand-by arrangement. The IMF and the Argentine authorities reached an understanding on key policies as part of their ongoing discussions on an IMF-supported program. See “—Our business is largely dependent upon macroeconomic, political, regulatory and social conditions in Argentina.”

In June 2021, Morgan Stanley Capital Index (“MSCI”), in its market classification report, reclassified the Argentine market from the “Emerging Markets” category to the “Standalone” or “Independent Markets” category, classification that is reserved for those countries that have accessibility barriers to foreign investors, political tensions, small capital markets and poor economies or that lack adequate regulations. In the case of Argentina, the classification as a “Standalone” market was due to the prolonged severity of capital controls in the Argentine stock market which is not in line with the accessibility criteria of the MSCI Emerging Markets index. As a result of the reclassification, several Argentine companies suffered a negative impact on the price of their shares, and may face difficulties in obtaining financing in the future.

Due to past or future defaults on its indebtedness, we cannot assure you that Argentina will have access to international financing in the future, on favorable terms or at all. If Argentina is not able to access financing, it may not be able to foster economic growth and invest in the country. As a result, we cannot assure you that private companies in Argentina will have access to financing on favorable terms or at all, which could adversely affect our business, financial condition and results of operations.

Government intervention in the Argentine economy could undermine business and investor confidence.

The Argentine government exercises substantial control over the economy and may increase its level of intervention in certain areas of the economy, including through the regulation of market conditions and prices.

In the past, the Argentine government has increased state intervention in the economy, including through expropriation and nationalization measures, price controls, exchange controls, establishment of minimum salary levels and mandatory employee benefits and restrictions on capital flows. For example, in 2008, the administration absorbed and replaced the former private pension system for a public “pay-as-you-go” pension system. As a result, all resources administered by the private pension funds, including significant equity interests in a wide range of listed companies, have since been administered by the Argentine Social Security Administration (Administración Nacional de la Seguridad Social or “ANSES”). In 2014, the Argentine government enacted law No. 26,991, which enables the Argentine government to intervene in certain markets when it considers that any party to the market is trying to impose prices or supply restrictions in the market. This law applies to all economic processes linked to goods, facilities and services which, either directly or indirectly, satisfy basic needs of the population (so-called “basic needs goods”), and grants broad powers to the relevant enforcing agency (Secretariat of Commerce) to become involved in such processes. In June 2020, the Argentine government ordered the 60-day temporary intervention of the cereal producer group Vicentín S.A.I.C. to ensure the continuance of the company’s operations and to preserve jobs and assets. In addition, as a result of the public health emergency declared by the Argentine government due to the COVID-19 pandemic, several measures have been adopted to limit the impact on the Argentine economy, including freezing rent prices and public services tariffs, and the prohibition of work dismissals, among others.

Despite the announced measures from Javier Milei’s new administration aimed at reducing state intervention in the private sector since his taking of office, in the future, the level of intervention in the economy by the Argentine government may continue or increase, which may adversely affect Argentina’s economy and, in turn, our business, results of operations and financial condition.

7

Developments in other countries may adversely affect the Argentine economy and our financial performance.

Argentina’s economy remains vulnerable to external shocks that could be caused by adverse regional or global developments. A significant decline in the economic growth of any of Argentina’s major trading partners (including Brazil, the European Union, China and the United States) could have a material adverse impact on Argentina’s balance of trade and adversely affect Argentina’s economy. In addition, Argentina may be affected by economic and market conditions in markets worldwide, as was the case in 2008, when the global economic crisis led to a sudden economic decline in Argentina in 2009.

In the past, emerging market economies have been affected by changes in U.S. monetary policy, at times resulting in the unwinding of investments and increased volatility in the value of their currencies. During 2018, the interest rate curve in the United States shifted upward, generating a generalized devaluation in emerging markets, with the Turkish Lira and the Peso being the most affected currencies against the U.S. dollar. However, in July 2019, the U.S. Federal Reserve cut rates for the first time since 2008, indicating an expectation of lower growth in the future, with long-term rates remaining low during 2020 and 2021. In March 2022, the U.S. Federal Reserve increased the federal funds rate by 0.25% for the first time since December 2018. During 2022, the U.S. Federal Reserve further increased the federal funds rate to a range between 4.25% and 4.50%. On February 2, 2023, the U.S. Federal Reserve further increased the federal funds rate by 0.25 and on March 22, 2023 it further increased the federal funds rate by 0.25 to a range of 4.75% to 5%. If interest rates rise significantly in developed economies, including the United States, emerging market economies, including Argentina, could find it more difficult and expensive to borrow capital and refinance existing debt, which would negatively affect their economic growth.

In February 2022, Russian troops undertook a full-scale military invasion of Ukraine. This conflict had, and may continue to have, significant global economic effects, including heightened inflation, supply chain problems, increases in interest rates, market volatility and an impact on commodity prices, especially with regard to international crude oil and gas prices. The conflict and its effects could exacerbate the current slowdown in the global economy and could negatively affect the payment capacity of some of our customers. Additionally, Russia’s prior annexation of Crimea, recognition of two separatist republics in the Donetsk and Luhansk regions of Ukraine and subsequent military interventions in Ukraine have led to sanctions and other penalties being levied by the United States, the European Union and other countries against Russia, Belarus, the Crimea Region of Ukraine, the so-called Donetsk People’s Republic, and the so-called Luhansk People’s Republic. The severity of these sanctions may increase and could contribute to a shortage of raw materials and commodities, which could, in turn, generate greater levels of inflation and create interruptions in the global supply chain. Interruptions in the global supply chain could particularly affect the energy sector and could create supply chain difficulties in local markets. In addition, there is a risk that Russia and other countries supporting Russia in this conflict may launch cyberattacks against the United States and its allies and other countries, their governments and businesses, including the infrastructure in such countries.

Following a terrorist attack by Hamas in the Gaza strip on October 7, 2023, Israel declared war on Hamas and other terrorist organizations in Gaza. On October 7, 2023, Hamas terrorists infiltrated Israel’s southern border from the Gaza strip and conducted a series of attacks on civilian and military targets. Hamas also launched extensive rocket attacks on the Israeli population and industrial centers located along Israel’s border with the Gaza strip and in other areas within Israel. Following the attack, Israel’s security cabinet declared war against Hamas and the Israeli military began to call up reservists for active duty. Subsequently, on April 13, 2024, Iran launched an aerial offensive against Israel. Even though there was no significant damage, Israel’s definitive course of action is pending. Concurrently, the Milei administration has publicly stated its belief that Israel has the right to defend itself. The future of this conflict as well as its impact on international trade and on emerging market economies such as Argentina remain uncertain. At the same time, the conflict between Israel and Hezbollah in Lebanon escalated and the Houthi movement initiated attacks on marine vessels in the Red Sea. There is a possibility that these attacks will turn into a greater regional conflict in the future.

Russian military actions and the Israel-Hamas conflict, the potential expansion of such conflicts in surrounding areas, and the potential sanctions from these conflicts could adversely affect the global economy and financial markets and lead to instability and lack of liquidity in capital markets. Although our businesses, results of operations and financial position could be adversely affected by any of these factors directly or indirectly arising from these geopolitical conflicts, due to the uncertainties inherent to the scale and duration of such conflicts and their direct and indirect effects, it is not reasonably possible to estimate the impact these conflicts will have on the global economy and financial markets, on the Argentine economy and, consequently, on our business, financial condition and results of operations.

We cannot assure your that events in other market countries , in the US or elsewhere will not adversely affect our financial performance.

8

The outbreak and spread of a pandemic and other large-scale public health events could have a material adverse effect on the Group’s business, financial condition and results of operations.

Economic conditions in Argentina may be adversely affected by an outbreak of a contagious disease, such as COVID-19 (coronavirus), which develops into a regional or global pandemic and other large scale public health events. The measures taken by governments, regulators and businesses to respond to any such pandemic or event may lead to slower or negative economic growth, supply disruptions, inflationary pressures and significant increases in public debt, and may also adversely affect the Group’s counterparties (including borrowers), which may lead to increased loan losses. Such measures could also impact the business and operations of third parties that provide critical services to the Group.

During the outbreak of COVID-19, the Group experienced a decline in activity, including as a result of branch closures and remote working requirements, and was affected by a number of regulatory measures, such as: the introduction of caps and floors on interest rates and the introduction of payment deferral of loans allowed to individuals and companies and mandatory loans to be granted at interest rates below market rates.

If there were an outbreak of a new pandemic or another large-scale public health event occurs in the future, the Group may experience an adverse impact, which may be material, on its business, financial condition and results of operations, including as a result of the exacerbation of any of the other risks described in this section.

Government or labor pressure to grant salary increases and/or additional benefits may affect business conditions in Argentina.

In the past, the Argentine government has passed laws and regulations forcing privately owned companies to maintain certain wage levels and provide added benefits to their employees. Additionally, both public and private sector employers have been subject to significant pressure from the workforce and trade unions to grant salary increases and other benefits. The Argentine government has increased the minimum monthly salaries on numerous opportunities. In addition, in the past the Argentine government has arranged other measures to mitigate the impact of inflation and exchange rate fluctuation in wages, or the consequences of the COVID-19 pandemic.

Labor relations in Argentina are governed by specific legislation, such as Labor Law No. 20,744 and Collective Bargaining Law No. 14,250, which, among other things, dictate how salary and other labor negotiations are to be conducted. Most industrial or commercial activities are regulated by a specific collective bargaining agreement that groups together companies by industry and trade unions. While the process of negotiation is standardized, each chamber of industrial or commercial activity negotiates the increases of salaries and labor benefits with the relevant trade union of such commercial or industrial activity. Parties are bound by the final decision once it is approved by the labor authority and must observe the established salary increases for all employees that are represented by the respective union and to whom the collective bargaining agreement applies. On March 1, 2024, the new President Milei called upon the governors to enter into a consensus called “Pacto de Mayo” with respect to certain key political principles, including the inviolability of private property, the adoption of a tax reform to reduce the tax burden and promote trade, the review of the federal tax co-participation model, and the adoption of a labor reform.

We cannot assure you that the new Argentine administration will implement a labor reform or that it will not adopt future measures requiring that employers increase salaries and/or employee benefits, prohibition of dismissals, duplication of severance payments or that our employees and/or labor unions will not pressure for such measures themselves. Any such increase could result in an increase in our operating expenses and, therefore, adversely affect our results of operations.

Failure to adequately address actual and perceived risks of institutional deterioration and corruption may adversely affect Argentina’s economy, which in turn could adversely affect our business, financial condition and results of operations.

A lack of a solid institutional framework and corruption have been identified as, and continue to be a significant problem for Argentina. In Transparency International’s 2023 Corruption Perceptions Index survey of 180 countries, Argentina was ranked 98, down from 94 in the index for 2022, and from 96 in 2021.

Recognizing that the failure to address these issues could increase the risk of political instability, distort decision-making processes and adversely affect Argentina’s international reputation and ability to attract foreign investment, the former Macri administration announced several measures aimed at strengthening Argentina’s institutions and reducing corruption. These measures included the reduction of criminal sentences in exchange for cooperation with the government in corruption investigations, increased access to public information, the seizing of assets from corrupt officials, increasing the powers of the Anticorruption Office (Oficina

9

Anticorrupción) and the passing of a new public ethics law, among others. The current Argentine administration’s ability and determination to implement these initiatives taken by the Macri administration is still uncertain, as it would require, among other things, the involvement of the judicial branch, which is independent, as well as legislative support from opposing parties. We cannot assure whether the implementation of these measures will be successful.

The Argentine government’s inability to accurately address actual and perceived risks of institutional deterioration and corruption might adversely affect the Argentine economy which, in turn, could adversely affect our business, financial condition, and results of operations.

Risks Relating to the Argentine Financial System

We operate in a highly regulated environment, and our operations are subject to regulations adopted, and measures taken, by several regulatory agencies.

Financial institutions are subject to significant regulation relating to functions that historically have been determined by the Central Bank, the Financial Information Unit (Unidad de Información Financiera or “UIF”) and the CNV. The number of these regulations have increased in recent years and include: (i) floor on interest rates on time deposits and subsidized rates on mandatory credit lines to SMEs, (ii) minimum capital requirements; (iii) mandatory reserve requirements; (iv) requirements for investments in fixed rate assets; (v) lending limits and other credit restrictions, including mandatory allocations; (vi) limits and other restrictions on fees; (vii) reduction of the period for the financial institutions to deposit the amount of sales made with credit cards in the corresponding accounts of the sellers; (viii) limits on the amount of interest banks can charge or pay, or on the period for capitalizing interest; (ix) accounting and statistical requirements; (x) limits on dividends; (xi) reporting or controlling regimes as agents or legally bound reporting parties; (xii) changes in the deposit insurance regime and (xiii) prior approval of the Central Bank for any decision regarding closing of branches. See “Item 4—Information of the Company—Argentine Banking Regulation Overview”.

We have no control over governmental regulations or the rules governing all aspects of our operations. The Central Bank may penalize our main subsidiary, the Bank, in case of any breach of applicable regulations. Similarly, the CNV, which authorizes our securities offerings and regulates the public markets in Argentina, has the authority to impose sanctions on us and our Board of Directors for breaches of corporate governance.

The absence of a stable regulatory framework in Argentina for financial institutions and the imposition of measures that affect the profitability of financial institutions and limit the possibility of covering their positions against currency fluctuations result may limit the decisions that financial institutions, including the Bank, can make on asset allocation, which may adversely affect future financial activities and our result of operations. There can be no assurances that new and tighter regulations will not be implemented in the future, which could cause uncertainty and could negatively affect our future financial activities and results of operations. In addition, existing or future legislation and regulation may require us to make material expenditures to avoid any material adverse effect on our consolidated operations.

The stability of the Argentine financial system depends upon the ability of financial institutions, including the Bank, the main subsidiary of the Group, to retain the confidence of depositors.

The measures implemented by the Argentine government in late 2001 and early 2002, in particular the restrictions imposed on depositors to withdraw money freely from banks and the pesification and restructuring of their deposits, resulted in losses for many depositors and undermined their confidence in the Argentine financial system.

Although liquidity levels are currently reasonable, no assurances can be given that these levels will not be reduced in the future due to adverse economic conditions that could negatively affect the Bank’s business.

If, in the future, depositor confidence further weakens and the deposit base contracts, such loss of confidence and contraction of deposits will have a substantial negative impact on the ability of financial institutions, including the Bank, to operate as financial intermediaries. If the Bank is not able to act as a financial intermediary and otherwise conduct its business as usual, the results of its operations could be adversely affected or limited, which in turn could affect our results of operations and financial condition.

10

The growth and profitability of Argentina’s financial system partially depend on the development of medium and long-term funding sources.

Since most term deposits are short-term deposits with a maturity of less than three months, a substantial portion of the loans have very short maturity, and there is a small portion of medium- and/or long-term credit lines. The uncertainty about the ability to reduce inflation in the future has had, and may continue to have, a significant impact on both the supply of, and demand for, long-term loans as borrowers try to hedge against inflation risk by borrowing at fixed rates while lenders hedge against inflation risk by offering loans at floating rates.

If longer-term financial intermediation activity does not grow, the ability of financial institutions, including us, to generate profits will be negatively affected.

The asset quality of financial institutions, including ourselves, may deteriorate if the Argentine private sector continues to be affected by adverse macroecononic conditions in Argentina.

As a result of Argentina’s macroeconomic environment, the capacity of many Argentine private sector debtors to repay their loans has deteriorated significantly in 2018, 2019 and 2020 affecting the asset quality of financial institutions, including the Bank. According to data published by the INDEC, Argentina’s GDP increased by 10.4% in 2021 and 5.2% in 2022, mainly due to the recovery of the Argentine economy from the negative impact that the COVID-19 pandemic had on the Argentine economy, and decreased by 1.6% in 2023, primarily due to the drought which mainly affected the agricultural production in Argentina, which decreased 20.4% compared to 2022. In 2021, 2022 and 2023, the asset quality of Argentine financial institutions improved. However, the Argentine economy remains fragile and volatile, with inflation increasing from 94.8% in 2022 to 211.4% in 2023. As a result, in 2023 the financial system in Argentina recorded low credit demand with loans to GDP at a historical low rate of 6.7% which reflects a significantly low level of indebtedness of individuals and entities.

If customers are not able to repay their loans the quality of the Bank’s assets may deteriorate and loan loss provisions may increase, which could, in turn, adversely affect our results of operations and financial condition.

Argentine financial institutions, including us, continue to have significant exposure to public sector debt, including securities issued by the Argentine Central Bank, and its repayment or refinancing capacity, which in periods of uncertainty may negatively affect their results of operations.

To some extent, the value of the assets held by Argentine financial institutions, as well as their income generation capacity, is dependent on the public sector’s creditworthiness, which is in turn dependent on the Argentine and the provincial government’s ability to promote sustainable long-term economic growth, generate tax revenues and control public spending.