UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

OR

For the fiscal year ended

OR

For the transition period from___to____.

OR

Date of event requiring this shell company report

Commission file number:

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone: +

Email:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

| NYSE: |

| ||

NYSE: |

* Effective on August 16, 2017, the ratio of ADSs to Class A common shares was changed from one ADS representing two Class A common shares to three ADSs representing one Class A common share.

** Not for trading, but only in connection with the listing on The New York Stock Exchange of American depositary shares.

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of February 28, 2023,

and

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically, if any, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☒ | ☐ International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

TABLE OF CONTENTS

Page | ||

1 | ||

2 | ||

3 | ||

3 | ||

3 | ||

3 | ||

65 | ||

95 | ||

95 | ||

113 | ||

121 | ||

122 | ||

124 | ||

124 | ||

135 | ||

135 | ||

137 | ||

137 | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 137 | |

137 | ||

139 | ||

139 | ||

139 | ||

139 | ||

139 | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 140 | |

140 | ||

140 | ||

140 | ||

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 140 | |

142 | ||

142 | ||

142 | ||

142 | ||

INTRODUCTION

In this annual report, except where the context otherwise requires, unless otherwise indicated and for purposes of this annual report only:

| ● | “ADSs” refers to our American depositary shares, each three of which represent one Class A common share; |

| ● | “China” or “PRC” refers to the People’s Republic of China, and only in the context of describing PRC laws, regulations and other legal or tax matters in this annual report, excludes Taiwan, Hong Kong and Macau; |

| ● | “K-12” refers to the year before the first grade through the last year of high school; |

| ● | “K-9 Academic AST Services” refers to after-school tutoring services on academic subjects offered to students from kindergarten through grade nine; |

| ● | “RMB” or “Renminbi” refers to the lawful currency of China; |

| ● | “shares” or “common shares” refers to our Class A and Class B common shares, par value $0.001 per share; |

| ● | “student enrollments of normal priced long-term course” for a certain period refers to the total number of normal priced long-term courses enrolled in and paid for by our learners during that period, including multiple courses enrolled in and paid for by the same learner, excluding courses offered at significant discounts for promotional purposes or short-term courses offered on an ad hoc basis; |

| ● | “$,” “US$” or “U.S. dollars” refers to the lawful currency of the United States; |

| ● | “U.S. GAAP” refers to generally accepted accounting principles in the United States; |

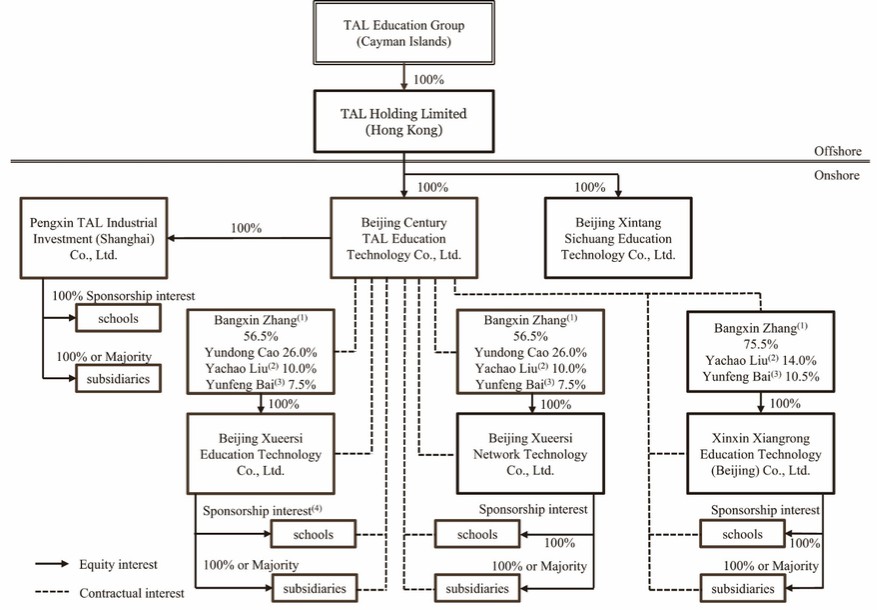

| ● | “VIEs” refers to variable interest entities including, among others, Beijing Xueersi Network Technology Co., Ltd., or Xueersi Network, Beijing Xueersi Education Technology Co., Ltd., or Xueersi Education, and Xinxin Xiangrong Education Technology (Beijing) Co., Ltd. (previously known as Beijing Dididaojia Education Technology Co., Ltd.), or Xinxin Xiangrong, all of which are domestic companies incorporated in the PRC in which we do not have equity interests but whose financial results have been consolidated into our consolidated financial statements in accordance with U.S. GAAP. See “Item 4. Information on the Company—C. Organizational Structure” for an illustrative diagram of our corporate structure; |

| ● | “VIE Subsidiaries” refers to the VIEs’ direct and indirect subsidiaries and schools; |

| ● | “VIE Contractual Arrangements” refer to the series of contractual agreements, including exclusive business service agreements, call option agreements, equity pledge agreements, letters of undertaking, and power of attorney agreements entered into by and among our subsidiaries incorporated in the PRC, or PRC subsidiaries, the VIEs and their respective shareholders, and VIE Subsidiaries; and |

| ● | “we,” “us,” “our company” and “our” refer to TAL Education Group, which is not a PRC operating company but a Cayman Islands holding company, and its subsidiaries, and, in the context of describing our operations and consolidated financial information, the VIEs and VIE Subsidiaries. We primarily conduct our operations in China through (i) our PRC subsidiaries and (ii) the VIEs with which we have maintained contractual arrangements, and VIE Subsidiaries. This structure entails unique risks to investors. See “Item 3. Key Information—D. Risk Factors—Risks Related to our Corporate Structure” for more details. |

Our financial statements are expressed in U.S. dollars, which is our reporting currency. Certain of our financial data in this annual report on Form 20-F are translated into U.S. dollars solely for the reader’s convenience. Unless otherwise noted, all convenient translations from Renminbi to U.S. dollars in this annual report on Form 20-F were made at a rate of RMB6.9325 to $1.00, the exchange rate set forth in the H.10 statistical release of the Federal Reserve Board on February 28, 2023. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, at the rate stated above, or at all.

1

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements that reflect our current expectations and views of future events. These forward looking statements are made under the “safe-harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by these forward-looking statements.

You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to” or other similar expressions. These forward-looking statements include statements relating to:

| ● | PRC laws, regulations and policies relating to the learning solutions industry; |

| ● | our anticipated growth strategies; |

| ● | competition in the markets where we offer learning products and services; |

| ● | our future business development, results of operations and financial condition; |

| ● | expected changes in our revenues and certain cost and expense items; |

| ● | our ability to increase learner enrollments and expand solution and product offerings; and |

| ● | risks associated with the expansion of our geographic reach and our offering of new learning products and services. |

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Although we believe that our expectations expressed in these forward-looking statements are reasonable, our expectations may later be found to be incorrect. You should read this annual report and the documents that we refer to in this annual report completely and with the understanding that our actual future results may be materially different from and/or worse than what we expect. We qualify all of our forward-looking statements with these cautionary statements. Other sections of this annual report include additional factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

2

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Our Holding Company Structure and VIE Contractual Arrangements

TAL Education Group is not a PRC operating company but a Cayman Islands holding company. We primarily conduct our operations in China through (i) our PRC subsidiaries, and (ii) the VIEs with which we have maintained contractual arrangements, and VIE Subsidiaries. The PRC laws and regulations impose foreign investment restrictions and license requirements on certain learning business and value-added telecommunication services. Therefore, we operate substantially all of such business in China through the VIEs and VIE Subsidiaries and rely on contractual arrangements among our PRC subsidiaries, the VIEs and their nominee shareholders, and VIE Subsidiaries, or VIE Contractual Arrangements, to control the business operations of the VIEs and VIE Subsidiaries. Accordingly, we are considered the primary beneficiary of these entities, whose financial results are consolidated in TAL Education Group’s consolidated financial statements under the U.S. GAAP for accounting purposes. Net revenues contributed by the VIEs and VIE Subsidiaries accounted for 94.4%, 95.5% and 84.9% of our net revenues in the fiscal years ended February 28, 2021, 2022 and 2023, respectively. As used in this annual report, “we,” “us,” “our company,” and “our” refers to TAL Education Group, a Cayman Islands company, its subsidiaries, and, in the context of describing our operations and consolidated financial information, the VIEs and VIE Subsidiaries. As of the date of this annual report, all of the VIEs and VIE Subsidiaries are domestic companies incorporated in the PRC in which we do not have any equity ownership but whose financial results have been consolidated into our consolidated financial statements based solely on the VIE Contractual Arrangements in accordance with U.S. GAAP. Investors of our ADSs are not purchasing the equity interest in the VIEs or VIE Subsidiaries in China, but instead are purchasing equity interest in a holding company incorporated in the Cayman Islands, and may never hold equity interests in the VIEs or VIE Subsidiaries.

The VIE Contractual Arrangements include:

(i) exclusive business service agreements, pursuant to which Beijing Century TAL Education Technology Co., Ltd., or TAL Beijing, or its designated affiliates have the exclusive right to provide the VIEs comprehensive intellectual property licensing and various technical and business support services and relevant VIEs agreed to pay service fees annually or regularly to TAL Beijing or its designated affiliates and adjust the service fee rates from time to time at TAL Beijing’s discretion, and TAL Beijing or its designated affiliates is entitled to charge the VIEs and VIE Subsidiaries service fees regularly that amount to substantially all of the net income of the VIEs and VIE Subsidiaries before the service fees;

(ii) call option agreements, pursuant to which the respective shareholders of the VIEs unconditionally and irrevocably granted TAL Beijing or its designated party an exclusive option to purchase from the shareholders part or all of the equity interests in the respective VIEs for the minimum amount of consideration permitted by the applicable PRC laws and regulations under the circumstances where TAL Beijing or its designated party is permitted under PRC laws and regulations to own all or part of the equity interests of the respective VIEs or where we otherwise deem it necessary or appropriate to exercise the option, and TAL Beijing has sole discretion to decide when to exercise the option, and whether to exercise the option in part or in full;

(iii) equity pledge agreements, as supplemented, pursuant to which the respective shareholders of the VIEs unconditionally and irrevocably pledged all of their equity interests in the respective VIEs to TAL Beijing to guarantee performance of the obligations of the respective VIEs and VIE Subsidiaries under the technology support and service agreements with TAL Beijing;

3

(iv) letters of undertaking, pursuant to which all shareholders of the VIEs covenanted with and undertook to TAL Beijing that, if, as the respective shareholders of the VIEs, such shareholders receive any dividends, interests, other distributions or remnant assets upon liquidation from the respective VIEs, such shareholders shall, to the extent permitted by applicable laws, regulations and legal procedures, remit all such income after payment of any applicable tax and other expenses required by laws and regulations to TAL Beijing without any compensation therefore; and

(v) power of attorney agreements, pursuant to which each of the shareholders of the VIEs has executed an irrevocable power of attorney appointed TAL Beijing, or any person designated by TAL Beijing as their attorney-in-fact to vote on their behalf on matters of the respective VIEs requiring shareholder approval, and TAL Beijing has the ability to exercise effective control over each of the VIEs respectively through shareholder votes and, through such votes, to also control the composition of the board of directors.

In addition, the spouse of each shareholder, who is a natural person, of the VIEs has entered into a spousal consent letter to acknowledge that she is aware of, and consents to, the execution by her spouse of the call option agreement described above. Each such spouse further agrees that she will not take any actions or raise any claims to interfere with performance by her spouse of the obligations under the above mentioned agreements.

Terms contained in each set of the VIE Contractual Arrangements are substantially similar. As a result of the VIE Contractual Arrangements, we have effective control over and are considered the primary beneficiary of the VIEs for accounting purposes, and we have consolidated the financial results of the VIEs and VIE Subsidiaries in our consolidated financial statements.

4

The following diagram sets out details of our significant subsidiaries, VIEs and VIE Subsidiaries as of February 28, 2023.

| (1) | Mr. Bangxin Zhang is our chairman and chief executive officer who owned 26.7% of the common shares and 72.1% of the voting power of TAL Education Group as of April 30, 2023. |

| (2) | Mr. Yachao Liu is our chief operating officer who owned 4.2% of the common shares and 5.4% of the voting power of TAL Education Group as of April 30, 2023. |

| (3) | Mr. Yunfeng Bai is our director who owned less than 1.0% of the common shares and less than 1.0% of the voting power of TAL Education Group as of April 30, 2023. |

| (4) | Among these schools, certain schools’ majority ownership are directly or indirectly held by Xueersi Education, and the remaining minority ownership are directly or indirectly held by Xueersi Network. For the other schools, Xueersi Education held either 100% or majority ownership for which the remaining minority ownership were held by third parties. |

5

However, the VIE Contractual Arrangements may not be as effective as direct ownership in providing us with control over the VIEs. If we had direct ownership of the VIEs, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of these entities, which in turn could effect changes, subject to any applicable fiduciary obligations, at the management level. However, under the VIE Contractual Arrangements, we rely on the performance by the VIEs and their respective shareholders of their obligations under the contracts to exercise control over and receive economic benefits from the VIEs. In addition, we cannot assure you that when conflicts of interest arise, any or all of these individuals will act in the best interests of our company or such conflicts will be resolved in our favor. In addition, these individuals may breach, or cause the VIEs to breach, or refuse to renew, the existing VIE Contractual Arrangements. If we cannot resolve any conflict of interest or dispute between us and these individuals, we would have to rely on legal proceedings, which could result in disruption of our business and subject us to substantial uncertainty as to the outcome of any such legal proceedings. As such, we may incur substantial costs to enforce the terms of the VIE Contractual Arrangements. In addition, the VIE Contractual Arrangements have not been tested in a court of law as of the date of this annual report. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We rely on the VIE Contractual Arrangements for our operations in China, which may not be as effective in providing operational control as direct ownership” and “—The legal owners of the VIEs may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition” for further details.

Our corporate structure is subject to unique risks associated with the VIE Contractual Arrangements. If the PRC government deems that the VIE Contractual Arrangements do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change or are interpreted differently in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. The PRC regulatory authorities could disallow the VIE structure, which would likely result in a material adverse change in our operations, and our ADSs may decline significantly in value or become worthless. Our holding company, our PRC subsidiaries, the VIEs and VIE Subsidiaries, and investors of our company face uncertainty about potential future actions by the PRC government that could affect the enforceability of the VIE Contractual Arrangements and, consequently, significantly affect the financial performance of the VIEs, VIE Subsidiaries and our company as a whole. For a detailed description of the risks associated with our corporate structure, please refer to risks disclosed under “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.”

There are also substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations and rules regarding the status of the rights of our Cayman Islands holding company with respect to the VIE Contractual Arrangements. It is uncertain whether any new PRC laws or regulations related to variable interest entity structures will be adopted or, if adopted, what they would provide. If we or any of the VIEs is found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required licenses, permits or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government determines that the agreements that establish the structure for operating our business in China are not in compliance with applicable PRC laws and regulations, we could be subject to severe penalties.”

6

We primarily conduct our operations in China through (i) our PRC subsidiaries and (ii) the VIEs with which we have maintained contractual arrangements, and VIE Subsidiaries. Our revenues are primarily generated from China. Though the PRC’s Foreign Investment Law does not explicitly classify contractual arrangements as a form of foreign investment, the definition of “foreign investment” thereunder is relatively wide and contains a catch-all provision which includes investments made by foreign investors through means stipulated in laws or administrative regulations or other methods prescribed by the State Council of the PRC government. Therefore, there is no assurance that foreign investments via contractual arrangements would not be interpreted as a type of indirect foreign investment activities in the future. If any of the VIEs were deemed as a foreign-invested enterprise under any such future laws, administrative regulations or provisions and any of our business would be included in any negative list or other form of restrictions on foreign investment, we may need to take further actions to comply with such future laws, administrative regulations or provisions. Such actions may have a material and adverse impact on our business, financial condition, result of operations and prospects. In addition, if the PRC regulatory authorities were to find our legal structure and the VIE Contractual Arrangements to be in violation of any PRC laws, administrative regulations or provisions, we are uncertain what impact of actions by above PRC regulatory authorities would have on us and our ability to consolidate the VIEs and VIE Subsidiaries in the consolidated financial statements. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Uncertainties exist with respect to the interpretation and implementation of the Foreign Investment Law and how it may impact our business, financial condition and results of operations.”

We face various risks and uncertainties related to doing business in China. Our business operations are primarily conducted in China, and we are subject to complex and evolving PRC laws and regulations. For example, we face risks associated with regulatory approvals on offshore offerings, anti-monopoly regulatory actions, regulations on the use of variable interest entities, and oversight on cybersecurity and data privacy. These risks could result in a material adverse change in our operations and the value of our ADSs, significantly limit or completely hinder our ability to continue to offer securities to investors, or cause the value of such securities to significantly decline. For a detailed description of risks related to doing business in China, “Item 3. Key Information— D. Risk Factors—Risks Related to Doing Business in China.”

The PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations in this nature may cause the value of such securities to significantly decline. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PRC government’s oversight and discretion over our business operations could result in a material adverse change in our operations and the value of our ADSs.”

Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our ADSs. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Uncertainties with respect to the PRC legal system could have a material adverse effect on us.”

The Holding Foreign Companies Accountable Act

Pursuant to the Holding Foreign Companies Accountable Act, or the HFCAA, if the Securities and Exchange Commission, or the SEC, determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspections by the Public Company Accounting Oversight Board, or the PCAOB, for two consecutive years, the Securities and Exchange Commission, or SEC, will prohibit our shares or our ADSs from being traded on a national securities exchange or in the over-the-counter trading market in the United States. On December 16, 2021, the PCAOB issued a report to notify the SEC of its determination that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in the mainland of China and Hong Kong, including our auditor, which is headquartered in the mainland of China. In July 2022, the SEC conclusively listed us as a “covered issuer”, or SEC-Identified Issuer, under the HFCAA following the filing of our annual report on Form 20-F for the fiscal year ended February 28, 2022. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed the mainland of China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. For this reason, we do not expect to be identified as an SEC-Identified Issuer under the HFCAA after we file this annual report on Form 20-F.

7

Each year, the PCAOB will determine whether it can inspect and investigate completely audit firms in the mainland of China and Hong Kong, among other jurisdictions. If the PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in the mainland of China and Hong Kong and we use an accounting firm headquartered in one of these jurisdictions to issue an audit report on our financial statements filed with the SEC, we would be identified as an SEC-Identified Issuer following the filing of the annual report on Form 20-F for the relevant fiscal year. There can be no assurance that we would not be identified as an SEC-Identified Issuer for any future fiscal year, and if we were so identified for two consecutive years, we would become subject to the prohibition on trading under the HFCAA. See “Item 3. Key Information—Risk Factors—Risks Related to Doing Business in China—The audit report included in this annual report is prepared by an auditor which the PCAOB was unable to inspect and investigate completely before 2022 and, as such, our investors have been deprived of the benefits of such inspections in the past, and may be deprived of the benefits of such inspections in the future.” and “—If the PCAOB determines that it is unable to inspect or investigate completely our auditor at any point in the future, our ADSs may be prohibited from trading in the United States under the HFCAA and any such trading prohibition on our ADSs or threat thereof may materially and adversely affect the price of our ADSs and value of your investment.”

Permissions Required from the PRC Government Authorities for Our Operations

We primarily conduct our business through our subsidiaries and the VIEs and VIE Subsidiaries in China. Our operations in China are governed by the PRC laws and regulations. As of the date of this annual report, other than disclosed in “Item 3. Key Information—D. Risk Factors—Risks Related to Our Business and Industry—We are required to obtain various operating licenses and permits and to make registrations and filings for our current business in China; failure to comply with these requirements may materially and adversely affect our business and results of operations” and “—Risks Related to Doing Business in China—If we fail to obtain and maintain licenses, permits or approvals or to complete registrations and filings required under the evolving regulatory regime for online learning in China, our business, financial condition and results of operations may be materially and adversely affected,” based on the advice of our PRC counsel, we believe our PRC subsidiaries and the VIEs and VIE Subsidiaries have obtained the requisite licenses and permits from the PRC government authorities that are necessary for their material business operations in China, including, among others, the private school operating permit, license for internet information services, or ICP license, the License for the Production and Operation of Radio and Television Program, and the Permit for Operating Publications Business.

Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we may be required to obtain additional licenses, permits, filings, or approvals for our business operations.

Furthermore, in connection with our issuance of securities to foreign investors in the past, under current PRC laws, regulations, and rules, as of the date of this annual report, we, our PRC subsidiaries, and the VIEs and VIE Subsidiaries (i) have not been required to obtain permissions from or complete filings with the China Securities Regulatory Commission, or the CSRC, (ii) have not been required to go through cybersecurity review by the Cyberspace Administration of China, or the CAC, and (iii) have not received or have not been denied such requisite permissions by the CSRC or the CAC. Our PRC counsel has consulted the relevant government authorities, which acknowledged that, under the currently effective PRC laws and regulations, a company already listed in a foreign stock exchange before promulgation of the latest Cybersecurity Review Measures is not required to go through a cybersecurity review by the CAC to conduct a securities offering or maintain its listing status on the foreign stock exchange on which its securities have been listed. Therefore, we believe that under the currently effective PRC laws and regulations, we are not required to go through a cybersecurity review by the CAC for conducting a securities offering or maintain our listing status on the NYSE. In addition, on February 17, 2023, the CSRC released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Overseas Listing Trial Measures, and five supporting guidelines, effective on March 31, 2023. Pursuant to the Overseas Listing Trial Measures, domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedure and report relevant information to the CSRC. Pursuant to the press conference held by CSRC for the release of the Overseas Listing Trial Measures and the Notice on Administration for the Filing of Overseas Offering and Listing by Domestic Companies, domestic companies that have been listed on a foreign stock exchange prior to the effective date of the Overseas Listing Trial Measures are not required to complete filing with the CSRC to maintain their listing status on the foreign stock exchange, but are required to file with the CSRC within three working days after such domestic companies complete a securities offering on the foreign stock exchange on which their securities have been listed. Since the Overseas Listing Trial Measures were newly promulgated, there are substantial uncertainties as to its interpretation, application and enforcement. If the filing procedure with the CSRC under the Overseas Listing Trial Measures is required for any future offerings, listing or any other capital raising activities by us, it is uncertain whether we could complete the filing procedure in a timely manner, or at all. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The approval of or filing with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under PRC laws, and, if required, we cannot predict whether or for how long we will be able to obtain such approvals or complete such filings.”

8

The PRC government has recently indicated an intent to exert more oversight over offerings that are conducted overseas and/or foreign investment in China-based issuers like us and published a series of new rules and regulations in this regard. Since these laws, regulations and rules are newly issued, there are substantial uncertainties as to the interpretation, application and enforcement of such laws, regulations and rules. If we had inadvertently concluded that such approvals were not required, or if applicable laws, regulations or interpretations change in a way that requires us to obtain such approvals in the future, we may be unable to obtain such necessary approvals in a timely manner, or at all, and such approvals may be rescinded even if obtained. Any such circumstance could subject us to penalties, including fines, suspension of business and revocation of required licenses, significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PRC government’s oversight and discretion over our business operations could result in a material adverse change in our operations and the value of our ADSs.”

Cash and Asset Flows Through Our Organization

TAL Education Group is a Cayman Islands holding company with no operations of its own. We primarily conduct our operations in China through our PRC subsidiaries and the VIEs and VIE Subsidiaries. As a result, although other means are available for us to obtain financing at the holding company level, TAL Education Group’s ability to pay dividends to the shareholders and to service any debt it may incur depends upon dividends paid by our PRC subsidiaries and license and service fees paid by the VIEs and VIE Subsidiaries. If any of our subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to TAL Education Group. In addition, to the extent cash or assets in our business is in the mainland of China or Hong Kong or a mainland of China or Hong Kong entity, such cash or assets may not be available to fund operations or for other use outside of China due to interventions in, or the imposition of restrictions and limitations on, the ability of our holding company, our PRC subsidiaries, or the VIEs or VIE Subsidiaries by the PRC government to transfer cash or assets. Cash may be transferred within our organization in the following manners:

(i) Under PRC laws, TAL Education Group may directly provide funding to our PRC subsidiaries through capital contributions, loans and cross-border RMB fund pool established under applicable PRC laws and regulations, and to the VIEs and VIE Subsidiaries through loans and cross-border RMB fund pool established under applicable PRC laws and regulations, subject to satisfaction of applicable government registration and approval requirements. With respect to the cross-border RMB fund pool, TAL Education Group, Pengxin TAL Industrial Investment (Shanghai) Co., Ltd. (a wholly-owned subsidiary of TAL Education Group), five of our wholly-owned subsidiaries and one VIE as a Multinational Enterprise Group, started a Round-way Cross-border RMB Fund Pool Business and opened a special deposit account, where the Multinational Enterprise Group can optimize and balance cross-border RMB funds among its domestic and foreign members.

For the years ended February 28, 2021, 2022 and 2023, TAL Education Group, through its intermediate holding companies, provided capital contributions of $10.0 million, $110.2 million and nil to its subsidiaries in China, respectively. TAL Education Group provided $0.4 million, $70.8 million and nil, respectively, to other members in the Multinational Enterprise Group, for the years ended February 28, 2021, 2022 and 2023. For the years ended February 28, 2021, 2022 and 2023, there was no repayment from other members in the Multinational Enterprise Group to TAL Education Group.

9

(ii) Our subsidiaries, including our PRC subsidiaries, could declare dividends or other distributions to their shareholders and eventually to TAL Education Group. As of the date of this annual report, no dividends or distributions have been made to TAL Education Group by our PRC subsidiaries or other subsidiaries. Our PRC subsidiaries are permitted to pay dividends to their shareholders and eventually to TAL Education Group only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Such payment of dividends by entities registered in China is subject to limitations, which could result in limitations on the availability of cash to fund dividends or make distributions to shareholders of our securities. The amount of dividends paid by our PRC subsidiaries to us primarily depends on the service fees paid to our PRC subsidiaries from the VIEs and VIE Subsidiaries, and, to a lesser degree, our PRC subsidiaries’ retained earnings. For any amounts owed by the VIEs and VIE Subsidiaries to our PRC subsidiaries under the VIE Contractual Arrangements, unless otherwise required by the PRC tax authorities, we are able to have such amounts settled without limitations under the currently effective PRC laws and regulations, provided that the VIEs and VIE Subsidiaries have sufficient funds to do so and that the VIEs and VIE Subsidiaries, if they are in the form of non-enterprise institution, follow the principles of openness, fairness and impartiality, set prices reasonably and establish appropriate decision-making processes, and do not damage the interests of the state, the non-enterprise institution, teachers or students when conducting such transactions. In the fiscal years ended February 28, 2021, 2022 and 2023, our relevant PRC subsidiaries collectively charged $1,123.5 million, $1,174.6 million and $96.2 million in service fees, respectively, to the VIEs and VIE Subsidiaries. The VIEs and VIE Subsidiaries collectively paid $784.4 million, $839.9 million and $316.1 million in service fees to relevant PRC subsidiaries in the fiscal years ended February 28, 2021, 2022 and 2023, respectively. As of February 28, 2021, 2022 and 2023, the balance of the amount payable for the service fees was $417.5 million, $752.2 million and $532.3 million, respectively. The VIEs and VIE Subsidiaries collected net proceeds from relevant PRC subsidiaries of $1,762.4 million and $1,536.3 million in the fiscal years ended February 28, 2021 and 2022, respectively, and provided net funds to relevant PRC subsidiaries of $108.5 million in the fiscal year ended February 28, 2023.

For the details of the financial position, cash flows and results of operation of the VIEs and VIE Subsidiaries, please refer to the “Item 3. Key information—Financial Information Related to the VIEs and VIE Subsidiaries.”

Our PRC subsidiaries and the VIEs and VIE Subsidiaries are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. For more details, see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Holding Company Structure” and “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We may rely on dividends paid by our subsidiaries for our cash needs, and any limitation on the ability of our subsidiaries to make payments to us could limit our ability to pay dividends to holders of our ADSs and common shares.”

In November 2010, we paid a $30 million cash dividend to our shareholders of record as of September 29, 2010 out of our cash balance. In December 2012, we paid a $39.0 million cash dividend with $0.25 per share to our shareholders of record at the close of business on December 7, 2012 out of our cash balance. In May 2017, we paid $41.2 million special cash dividend with $0.25 per share to our shareholders of record at the close of business on May 11, 2017 out of our cash balance. No dividends or distributions have been made to the holding company by WFOEs, the VIEs or other subsidiaries. See “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Dividend Policy.” For PRC and United States federal income tax considerations of an investment in our ADSs, see “Item 10. Additional Information—E. Taxation.”

10

We currently do not have cash management policies in place that dictate how funds are transferred between TAL Education Group, our subsidiaries, the VIEs, VIE Subsidiaries and the investors. Rather, the funds can be transferred in accordance with applicable PRC laws and regulations. For purposes of illustration, the following discussion reflects the hypothetical taxes that might be required to be paid within China, assuming that: (i) we have taxable earnings, and (ii) we determine to pay a dividend in the future:

| Tax calculation (1) |

| |

Hypothetical pre-tax earnings(2) |

| 100 | % |

Tax on earnings at statutory rate of 25%(3) |

| (25) | % |

Net earnings available for distribution |

| 75 | % |

Withholding tax at standard rate of 10%(4) |

| (7.5) | % |

Net distribution to Parent/Shareholders |

| 67.5 | % |

Notes:

| (1) | For purposes of this example, the tax calculation has been simplified. The hypothetical book pre-tax earnings amount, not considering timing differences, is assumed to equal taxable income in China. |

| (2) | Under the terms of the VIE Contractual Arrangements, our PRC subsidiaries may charge the VIEs and VIE Subsidiaries for services provided to such entities. These service fees shall be recognized as costs and expenses of the VIEs and VIE Subsidiaries, with corresponding amounts as service income by our PRC subsidiaries and eliminated in consolidation. For income tax purposes, our PRC subsidiaries and the VIEs and VIE Subsidiaries file income tax returns on a separate company basis. The service fees paid are recognized as tax deductions by the VIEs and VIE Subsidiaries and as income by our PRC subsidiaries and are tax neutral. |

| (3) | Certain of our PRC subsidiaries and the VIEs and VIE Subsidiaries qualify for a preferential income tax rate which is lower than the statutory rate of 25%. However, such rate is subject to qualification, is temporary in nature, and may not be available in a future period when distributions are paid. For purposes of this hypothetical example, the table above reflects a maximum tax scenario under which the full statutory rate would be effective. |

| (4) | The PRC Enterprise Income Tax Law imposes a withholding income tax of 10% on dividends distributed by a foreign invested enterprise, or FIE, to its immediate holding company outside of China. A lower withholding income tax rate of 5% is applied if the FIE’s immediate holding company is registered in Hong Kong or other jurisdictions that have a tax treaty arrangement with China, subject to a qualification review at the time of the distribution. For purposes of this hypothetical example, the table above assumes a maximum tax scenario under which the full withholding tax would be applied. |

The table above has been prepared under the assumption that all profits of the VIEs and VIE Subsidiaries will be distributed as fees to TAL Beijing under tax-neutral contractual arrangements. If, in the future, the accumulated earnings of the VIEs and VIE Subsidiaries exceed the service fees paid to TAL Beijing (or if the current and contemplated fee structure between the intercompany entities is determined to be non-substantive and disallowed by PRC tax authorities), the VIEs and VIE Subsidiaries could make a non-deductible transfer to our PRC subsidiaries for the amounts of the stranded cash in the VIEs and VIE Subsidiaries. This would result in such transfer being non-deductible expenses for the VIEs and VIE Subsidiaries but still taxable income for our PRC subsidiaries. Such a transfer and the related tax burdens would reduce our after-tax income to approximately 50.6% of the pre-tax income. Our management believes that there is only a remote possibility that this scenario would happen.

11

Financial Information Related to the VIEs and VIE Subsidiaries

The following table presents the condensed consolidating schedule of financial position for the VIEs and VIE Subsidiaries and other entities as of the dates presented.

Selected Condensed Consolidated Statements of Operations Information

For the Year Ended February 28, 2023 | ||||||||||||

VIEs and | ||||||||||||

VIE | Consolidated | |||||||||||

The Company | WFOEs(1) | Subsidiaries | Others | Eliminations | Total | |||||||

US$ | ||||||||||||

(In thousands) | ||||||||||||

Third-party net revenues |

| — |

| 112,260 |

| 865,846 |

| 41,666 |

| — |

| 1,019,772 |

Inter-company revenues |

| — |

| 107,282 |

| 30,204 |

| 428 |

| (137,914) |

| — |

Total costs and operating expenses |

| (117,005) |

| (297,313) |

| (782,753) |

| (50,217) |

| 114,103 |

| (1,133,185) |

(Loss)/income from government subsidies and non-operations |

| (138,504) |

| 81,786 |

| 63,419 |

| (24,620) |

| 21,613 |

| 3,694 |

Income from subsidiaries and VIEs |

| 123,668 |

| 153,225 |

| — |

| 158,557 |

| (435,450) |

| — |

(Loss)/income before income tax and income/(loss) from equity method investments |

| (131,841) |

| 157,240 |

| 176,716 |

| 125,814 |

| (437,648) |

| (109,719) |

Less: income tax (expenses)/benefits |

| (1,796) |

| 1,318 |

| (19,630) |

| (246) |

| 343 |

| (20,011) |

Loss from equity method investments |

| (1,975) |

| — |

| (273) |

| — |

| — |

| (2,248) |

Net (loss)/income |

| (135,612) |

| 158,558 |

| 156,813 |

| 125,568 |

| (437,305) |

| (131,978) |

For the Year Ended February 28, 2022 | ||||||||||||

VIEs and | ||||||||||||

VIE | Consolidated | |||||||||||

The Company | WFOEs(1) | Subsidiaries | Others | Eliminations | Total | |||||||

US$ | ||||||||||||

(In thousands) | ||||||||||||

Third-party net revenues |

| — |

| 177,551 |

| 4,193,212 |

| 20,144 |

| — |

| 4,390,907 |

Inter-company revenues |

| — |

| 1,173,049 |

| 11,449 |

| 5,175 |

| (1,189,673) |

| — |

Total costs and operating expenses |

| (521,184) |

| (812,986) |

| (4,812,029) |

| (70,319) |

| 1,190,283 |

| (5,026,235) |

(Loss)/income from government subsidies and non-operations |

| (125,514) |

| 9,534 |

| (20,547) |

| 2,157 |

| (8,432) |

| (142,802) |

Loss from subsidiaries and VIEs |

| (501,143) |

| (918,903) |

| — |

| (452,185) |

| 1,872,231 |

| — |

Loss before income tax and income/(loss) from equity method investments |

| (1,147,841) |

| (371,755) |

| (627,915) |

| (495,028) |

| 1,864,409 |

| (778,130) |

Less: income tax (expenses)/benefits |

| — |

| (80,454) |

| (316,832) |

| 294 |

| — |

| (396,992) |

Income/(loss) from equity method investments |

| 11,726 |

| — |

| (939) |

| — |

| — |

| 10,787 |

Net loss |

| (1,136,115) |

| (452,209) |

| (945,686) |

| (494,734) |

| 1,864,409 |

| (1,164,335) |

For the Year Ended February 28, 2021 | ||||||||||||

VIEs and | ||||||||||||

VIE | Consolidated | |||||||||||

The Company | WFOEs(1) | Subsidiaries | Others | Eliminations | Total | |||||||

US$ | ||||||||||||

(In thousands) | ||||||||||||

Third-party net revenues |

| — |

| 236,916 |

| 4,244,907 |

| 13,932 |

| — |

| 4,495,755 |

Inter-company revenues |

| — |

| 1,141,716 |

| 12,272 |

| 14,547 |

| (1,168,535) |

| — |

Total costs and operating expenses |

| (216,782) |

| (657,460) |

| (5,182,473) |

| (65,157) |

| 1,168,402 |

| (4,953,470) |

Income/(loss) from government subsidies and non-operations |

| 10,772 |

| 76,857 |

| 145,836 |

| (806) |

| 433 |

| 233,092 |

Income/(loss) from subsidiaries and VIEs |

| 83,269 |

| (594,633) |

| — |

| 120,898 |

| 390,466 |

| — |

(Loss)/income before income tax and income/(loss) from equity method investments |

| (122,741) |

| 203,396 |

| (779,458) |

| 83,414 |

| 390,766 |

| (224,623) |

Less: income tax (expenses)/benefits |

| (63) |

| (82,518) |

| 152,361 |

| 117 |

| — |

| 69,897 |

Income from equity method investments |

| 6,814 |

| — |

| 4,862 |

| — |

| — |

| 11,676 |

Net (loss)/income |

| (115,990) |

| 120,878 |

| (622,235) |

| 83,531 |

| 390,766 |

| (143,050) |

12

Selected Condensed Consolidated Balance Sheets Information

As of February 28, 2023 | ||||||||||||

VIEs and | ||||||||||||

VIE | Consolidated | |||||||||||

The Company | WFOEs(1) | Subsidiaries | Others | Eliminations | Total | |||||||

US$ | ||||||||||||

(In thousands) | ||||||||||||

Assets |

|

|

|

|

|

|

| |||||

Cash and cash equivalents |

| 1,336,235 |

| 330,994 |

| 331,081 |

| 23,617 |

| — |

| 2,021,927 |

Amount due from Group companies |

| 361,461 |

| 2,555,380 |

| 341,862 |

| 19,435 |

| (3,278,138) |

| — |

Other current assets |

| 936,003 |

| 271,245 |

| 234,186 |

| 5,046 |

| — |

| 1,446,480 |

Total current assets |

| 2,633,699 |

| 3,157,619 |

| 907,129 |

| 48,098 |

| (3,278,138) |

| 3,468,407 |

Investment in subsidiaries and VIEs |

| 919,829 |

| — |

| — |

| 1,127,388 |

| (2,047,217) |

| — |

Property and equipment, net |

| — |

| 55,431 |

| 238,898 |

| 2,177 |

| (7,629) |

| 288,877 |

Other non-current assets |

| 324,237 |

| 18,245 |

| 619,221 |

| 5,367 |

| — |

| 967,070 |

Total assets |

| 3,877,765 |

| 3,231,295 |

| 1,765,248 |

| 1,183,030 |

| (5,332,984) |

| 4,724,354 |

Liabilities |

|

|

|

|

|

| ||||||

Deferred revenue-current |

| — |

| 7,072 |

| 213,239 |

| 14,578 |

| — |

| 234,889 |

Amount due to Group companies |

| 30,388 |

| 461,489 |

| 2,554,768 |

| 232,356 |

| (3,279,001) |

| — |

Other current liabilities |

| 2,734 |

| 90,797 |

| 449,854 |

| 5,591 |

| — |

| 548,976 |

Total current liabilities |

| 33,122 |

| 559,358 |

| 3,217,861 |

| 252,525 |

| (3,279,001) |

| 783,865 |

Deficits of investment in subsidiaries and VIEs |

| — |

| 1,539,489 |

| — |

| — |

| (1,539,489) |

| — |

Other non-current liabilities |

| — |

| 5,065 |

| 112,807 |

| 1,704 |

| — |

| 119,576 |

Total liabilities |

| 33,122 |

| 2,103,912 |

| 3,330,668 |

| 254,229 |

| (4,818,490) |

| 903,441 |

Total equity |

| 3,844,643 |

| 1,127,383 |

| (1,565,420) |

| 928,801 |

| (514,494) |

| 3,820,913 |

Total liabilities and equity |

| 3,877,765 |

| 3,231,295 |

| 1,765,248 |

| 1,183,030 |

| (5,332,984) |

| 4,724,354 |

As of February 28, 2022 | ||||||||||||

VIEs and | ||||||||||||

The | VIE | Consolidated | ||||||||||

| Company |

| WFOEs(1) |

| Subsidiaries |

| Others |

| Eliminations |

| Total | |

US$ | ||||||||||||

(In thousands) | ||||||||||||

Assets | ||||||||||||

Cash and cash equivalents |

| 812,377 |

| 456,595 |

| 359,208 |

| 10,009 |

| — |

| 1,638,189 |

Amount due from Group companies |

| 612,066 |

| 3,256,687 |

| 480,722 |

| 44,309 |

| (4,393,784) |

| — |

Other current assets |

| 1,657,282 |

| 54,842 |

| 276,804 |

| 2,259 |

| — |

| 1,991,187 |

Total current assets |

| 3,081,725 |

| 3,768,124 |

| 1,116,734 |

| 56,577 |

| (4,393,784) |

| 3,629,376 |

Investment in subsidiaries and VIEs |

| 882,221 |

| — |

| — |

| 1,145,901 |

| (2,028,122) |

| — |

Property and equipment, net |

| — |

| 79,995 |

| 206,030 |

| 3,587 |

| (8,386) |

| 281,226 |

Other non-current assets |

| 251,808 |

| 26,479 |

| 883,759 |

| 9,880 |

| — |

| 1,171,926 |

Total assets |

| 4,215,754 |

| 3,874,598 |

| 2,206,523 |

| 1,215,945 |

| (6,430,292) |

| 5,082,528 |

Liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

Deferred revenue-current |

| — |

| 19 |

| 182,337 |

| 5,362 |

| — |

| 187,718 |

Amount due to Group companies |

| 182,926 |

| 736,275 |

| 3,165,700 |

| 300,368 |

| (4,385,269) |

| — |

Other current liabilities |

| 2,677 |

| 123,887 |

| 583,051 |

| 5,251 |

| — |

| 714,866 |

Total current liabilities |

| 185,603 |

| 860,181 |

| 3,931,088 |

| 310,981 |

| (4,385,269) |

| 902,584 |

Deficits of investment in subsidiaries and VIEs |

| — |

| 1,858,676 |

| — |

| — |

| (1,858,676) |

| — |

Other non-current liabilities |

| — |

| 9,834 |

| 164,169 |

| 3,679 |

| — |

| 177,682 |

Total liabilities |

| 185,603 |

| 2,728,691 |

| 4,095,257 |

| 314,660 |

| (6,243,945) |

| 1,080,266 |

Total equity |

| 4,030,151 |

| 1,145,907 |

| (1,888,734) |

| 901,285 |

| (186,347) |

| 4,002,262 |

Total liabilities and equity |

| 4,215,754 |

| 3,874,598 |

| 2,206,523 |

| 1,215,945 |

| (6,430,292) |

| 5,082,528 |

13

Selected Condensed Consolidated Cash Flows Information

For the Year Ended February 28, 2023 | ||||||||||||

VIEs and | ||||||||||||

The | VIE | Consolidated | ||||||||||

| Company |

| WFOEs(1) |

| Subsidiaries |

| Others |

| Eliminations |

| Total | |

US$ | ||||||||||||

(In thousands) | ||||||||||||

Net cash provided by / (used in) operating activities | 14,674 | 40,908 | (56,397) | 8,173 | — | 7,358 | ||||||

Loan and fund pool to entities within the Group |

| (4,557) |

| (13,124) |

| (2,100) |

| — |

| 19,781 |

| — |

Repayment of loan to entities within the Group |

| 2,717 |

| 121,641 |

| 5 |

| — |

| (124,363) |

| — |

Investment in entities within the Group |

| (865) |

| — |

| — |

| — |

| 865 |

| — |

Other investing activities |

| (24,024) |

| (201,092) |

| (76,209) |

| (301) |

| — |

| (301,626) |

Net cash used in investing activities |

| (26,729) |

| (92,575) |

| (78,304) |

| (301) |

| (103,717) |

| (301,626) |

Net proceeds from loan and fund pool from entities within the Group |

| 2,100 |

| — |

| 13,124 |

| 4,557 |

| (19,781) |

| — |

Repayment of loan to entities within the Group |

| (3) |

| — |

| (121,635) |

| (2,725) |

| 124,363 |

| — |

Proceeds from group capital contribution |

| — |

| — |

| — |

| 865 |

| (865) |

| — |

Other financing activities |

| (66,184) |

| — |

| — |

| — |

| — |

| (66,184) |

Net cash (used in) / provided by financing activities |

| (64,087) |

| — |

| (108,511) |

| 2,697 |

| 103,717 |

| (66,184) |

For the Year Ended February 28, 2022 | ||||||||||||

VIEs and | ||||||||||||

The | VIE | Consolidated | ||||||||||

| Company |

| WFOEs(1) |

| Subsidiaries |

| Others |

| Eliminations |

| Total | |

US$ | ||||||||||||

(In thousands) | ||||||||||||

Net cash provided by / (used in) operating activities |

| 74,281 | 433,808 | (1,418,908) | (28,365) | — | (939,184) | |||||

Loan and fund pool to entities within the Group |

| (212,542) |

| (1,538,343) |

| — |

| — |

| 1,750,885 |

| — |

Repayment of loan to entities within the Group |

| 2,352 |

| 2,085 |

| — |

| — |

| (4,437) |

| — |

Investment in entities within the Group |

| — |

| — |

| — |

| (110,200) |

| 110,200 |

| — |

Other investing activities |

| 994,197 |

| 569,214 |

| (194,349) |

| (346) |

| — |

| 1,368,716 |

Net cash provided by / (used in) investing activities |

| 784,007 |

| (967,044) |

| (194,349) |

| (110,546) |

| 1,856,648 |

| 1,368,716 |

Net proceeds from loan and fund pool from entities within the Group |

| — |

| 70,757 |

| 1,538,343 |

| 141,785 |

| (1,750,885) |

| — |

Repayment of loan to entities within the Group |

| — |

| — |

| (2,085) |

| (2,352) |

| 4,437 |

| — |

Proceeds from group capital contribution |

| — |

| 110,200 |

| — |

| — |

| (110,200) |

| — |

Other financing activities |

| (2,766,679) |

| — |

| — |

| — |

| — |

| (2,766,679) |

Net cash (used in) / provided by financing activities |

| (2,766,679) |

| 180,957 |

| 1,536,258 |

| 139,433 |

| (1,856,648) |

| (2,766,679) |

14

| For the Year Ended February 28, 2021 | |||||||||||

VIEs and | ||||||||||||

The | VIE | Consolidated | ||||||||||

| Company |

| WFOEs(1) |

| Subsidiaries |

| Others |

| Eliminations |

| Total | |

US$ | ||||||||||||

(In thousands) | ||||||||||||

Net cash (used in) / provided by operating activities |

| (11,253) |

| 2,053,596 |

| (1,034,695) |

| (52,916) |

| — |

| 954,732 |

Loan and fund pool to entities within the Group |

| (79,469) |

| (1,762,356) |

| — |

| — |

| 1,841,825 |

| — |

Repayment of loan to entities within the Group |

| 11,083 |

| — |

| — |

| — |

| (11,083) |

| — |

Investment in entities within the Group |

| — |

| — |

| — |

| (10,000) |

| 10,000 |

| — |

Other investing activities |

| (1,842,514) |

| (574,720) |

| (224,235) |

| — |

| — |

| (2,641,469) |

Net cash used in investing activities |

| (1,910,900) |

| (2,337,076) |

| (224,235) |

| (10,000) |

| 1,840,742 |

| (2,641,469) |

Net proceeds from loan and fund pool from entities within the Group |

| — |

| 367 |

| 1,762,356 |

| 79,102 |

| (1,841,825) |

| — |

Repayment of loan to entities within the Group |

| — |

| — |

| — |

| (11,083) |

| 11,083 |

| — |

Proceeds from group capital contribution |

| — |

| 10,000 |

| — |

| — |

| (10,000) |

| — |

Other financing activities |

| 4,798,331 |

| — |

| (3,518) |

| — |

| — |

| 4,794,813 |

Net cash provided by financing activities |

| 4,798,331 |

| 10,367 |

| 1,758,838 |

| 68,019 |

| (1,840,742) |

| 4,794,813 |

Notes:

| (1) | As used in this section, “WFOEs” include WFOEs that are the primary beneficiary of the VIEs, their designated affiliates, also being WFOEs, which charged service fees on the VIEs, VIE Subsidiaries and other PRC subsidiaries. |

Cessation of K-9 Academic AST Services in the Mainland of China

In compliance with regulatory policies promulgated in 2021, including the Opinions on Further Alleviating the Burden of Homework and After-School Tutoring for Students in Compulsory Education published in July 2021 by the General Office of the CPC Central Committee and the General Office of the State Council, or the Alleviating Burden Opinion Regarding Compulsory Education, we ceased offering the K-9 Academic AST Services in the mainland of China at the end of 2021. The cessation has had a substantial adverse impact on our revenues for the fiscal year ended February 28, 2022 and subsequent periods. In the fiscal years ended February 28, 2021 and 2022, the revenues from offering K-9 Academic AST Services in the mainland of China accounted for a substantial majority of our total net revenues prior to the cessation of such services. More specifically, the impact of cessation of K-9 Academic AST Services in the mainland of China includes the following items in our consolidated financial statements.

Net Revenues

Our total net revenues decreased by 2.3% from $4,495.8 million for the fiscal year ended February 28, 2021 to $4,390.9 million for the fiscal year ended February 28, 2022, and further decreased by 76.8% to $1,019.8 million for the fiscal year ended February 28, 2023. The decrease was mainly driven by the cessation of the K-9 Academic AST Services in the mainland of China by the end of December 2021.

Property and Equipment

$256.0 million and $0.7 million impairment loss was recorded for certain property and equipment and the leasehold improvements of certain learning centers and offices in the fiscal year ended February 28, 2022 and 2023, respectively. The impairment loss in the fiscal year ended February 28, 2022 was mostly due to the downsize of learning centers as result of regulatory and market changes and the cessation of K-9 Academic AST Services in the mainland of China.

15

Intangible Assets

For the fiscal year ended February 28, 2022, an impairment loss of $51.5 million was recorded on our acquired intangible assets as a result of the changes in business outlook primarily due to the regulatory development which led to the cessation of K-9 Academic AST Services in the mainland of China. We recorded nil impairment loss for the fiscal year ended February 28, 2023.

Goodwill

Due to regulatory developments over the after-school tutoring services, we noted impairment indicators during the fiscal year ended February 28, 2022. As a result, an impairment loss amounting to $453.6 million was recorded for the year. Goodwill was fully impaired as of February 28, 2022 as a result of changes in the regulatory and the operating environment which led to the changes of our business outlook. The fair value of the reporting units was determined by us with the assistance of independent valuation appraisers using the income-based valuation methodology. We recorded nil impairment loss for the fiscal year ended February 28, 2023.

Leases

Certain of our leases were terminated before the expiration of the lease term due to the downsized capacity relating to the cessation of K-9 Academic AST Services in the mainland of China, and the relevant right-of-use asset, with a carrying amount totaled at $1.1 billion and $57.7 million during the fiscal year ended February 28, 2022 and 2023, respectively, and the corresponding lease liability were derecognized upon the effectiveness of the early termination.

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Summary of Risk Factors

An investment in our ADSs involves significant risks. Below is a summary of material risks we face, organized under relevant headings. These risks are discussed in more details in “Item 3. Key Information—D. Risk Factors.”

Risks Related to Our Business and Industry

| ● | If we are not able to develop new types of learning products or services under the recent regulatory policies in China to successfully attract prospective learners and customers in a timely or cost-effective manner or to continue to attract learners and customers to purchase our existing products or services, our business, results of operations and prospects will continue to be materially and adversely affected. |

| ● | If we fail to successfully design and execute our growth strategies, our business and prospects may be materially and adversely affected. |

| ● | If we are not able to maintain and enhance the value of our brands, our business and operating results may be harmed. |

| ● | Significant uncertainties exist in relation to the interpretation and implementation of, or proposed changes to, the PRC laws, regulations and policies regarding the after-school tutoring industry. In particular, our compliance with the Alleviating Burden Opinion Regarding Compulsory Education and the implementation measures issued by the relevant PRC government authorities has had, and could have further, material adverse effect on us. |

16

| ● | We are required to obtain various operating licenses and permits and to make registrations and filings for our current business in China; failure to comply with these requirements may materially and adversely affect our business and results of operations. |

| ● | We face significant competition, and if we fail to compete effectively, we may lose our market share or fail to gain additional market share, and our profitability may be adversely affected. |

| ● | Our historical financial and operating results, growth rates and profitability may not be indicative of future performance. |

| ● | We may not be able to recruit, train and retain qualified and dedicated teachers, who are critical to the success of our business and the effective delivery of our services to learners. |

| ● | We are subject to risks related to global expansion. |

Risks Related to Our Corporate Structure

| ● | TAL Education Group is not a PRC operating company but a Cayman Islands holding company with no equity ownership in the VIEs. We primarily conduct our operations in China through (i) our PRC subsidiaries and (ii) the VIEs with which we have maintained contractual arrangements, and VIE Subsidiaries. Investors of our ADSs thus are not purchasing equity interest in the VIEs in China but instead are purchasing equity interest in a Cayman Islands holding company. If the PRC government deems that the VIE Contractual Arrangements do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. Our holding company, our PRC subsidiaries, the VIEs and VIE Subsidiaries, and the investors of our company face uncertainty about potential future actions by the PRC government that could affect the enforceability of the VIE Contractual Arrangements and, consequently, significantly affect the financial performance of the VIEs, VIE Subsidiaries and our company as a group. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government determines that the agreements that establish the structure for operating our business in China are not in compliance with applicable PRC laws and regulations, we could be subject to severe penalties” for details. |

| ● | We rely on the VIE Contractual Arrangements for our operations in China, which may not be as effective in providing operational control as direct ownership. |

| ● | Any failure by the VIEs or their respective shareholders or VIE Subsidiaries to perform their obligations under the VIE Contractual Arrangements would have a material adverse effect on our business and financial condition. |

| ● | The legal owners of the VIEs may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition. |

Risks Related to Doing Business in China

| ● | Uncertainties with respect to the PRC legal system could have a material adverse effect on us. Certain laws and regulations are relatively new and can change quickly with little advance notice. In addition, the interpretations of many laws, regulations and rules are not always consistent, and enforcement of these laws, regulations and rules involve uncertainties, which may limit the available legal protections. Furthermore, the PRC administrative and court authorities have significant discretion in interpreting and implementing or enforcing statutory rules and contractual terms, and it may be more difficult to predict the outcome of administrative and court proceedings and the level of legal protection we may enjoy in China than under some more developed legal systems. These uncertainties may affect our judgment on the relevance of legal requirements and our decisions on the measures and actions to be taken to fully comply therewith and may affect our ability to enforce our contractual or tort rights. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Uncertainties with respect to the PRC legal system could have a material adverse effect on us” for details. |

17

| ● | We conduct our business primarily in China. Our operations in China are governed by PRC laws and regulations. The PRC government has significant oversight and discretion over the operation of our business, and it may influence our operations at any time, which could result in a material adverse change in our operation and the value of our ADSs. In addition, implementation of industry-wide regulations directly targeting our operations could cause the value of our securities to significantly decline. Therefore, investors of our company and our business face potential uncertainty from actions taken by the PRC government affecting our business. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PRC government’s oversight and discretion over our business operations could result in a material adverse change in our operations and the value of our ADSs” for details. |

| ● | Failure to comply with various evolving PRC laws and regulations regarding cybersecurity and data privacy could subject us to penalties, damage our reputation and brand, and harm our business and results of operations. |

| ● | The PRC government has recently indicated an intent to exert more oversight over overseas offerings by and foreign investment in China-based issuers like us. On February 17, 2023, the CSRC released the Overseas Listing Trial Measures, and five supporting guidelines, effective on March 31, 2023. Pursuant to the Overseas Listing Trial Measures, domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedure and report relevant information to the CSRC. In addition, domestic companies that have been listed on a foreign stock exchange prior to the effective date of the Overseas Listing Trial Measures are required to file with the CSRC within three working days after such domestic companies complete a securities offering on the foreign stock exchange on which their securities have been listed. Since the Overseas Listing Trial Measures were newly promulgated, there are substantial uncertainties as to its interpretation, application and enforcement. If the filing procedure with the CSRC under the Overseas Listing Trial Measures is required for any future offerings, listings or any other capital raising activities by us, it is uncertain whether we could complete the filing procedure in a timely manner, or at all. Any such circumstance could significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The approval of or filing with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under PRC laws, and, if required, we cannot predict whether or for how long we will be able to obtain such approvals or complete such filings” for details. |

| ● | The audit report included in this annual report is prepared by an auditor which the PCAOB was unable to inspect and investigate completely before 2022 and, as such, our investors have been deprived of the benefits of such inspections in the past, and may be deprived of the benefits of such inspections in the future. |

| ● | If the PCAOB determines that it is unable to inspect or investigate completely our auditor at any point in the future, our ADSs may be prohibited from trading in the United States under the HFCAA and any such trading prohibition on our ADSs or threat thereof may materially and adversely affect the price of our ADSs and value of your investment. |