UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from to

Commission file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction | (I.R.S. Employer Identification No.) |

(Address of principal executive offices) | (Zip Code) |

( | |

(Registrant’s telephone number, including area code) | |

Securities registered pursuant to Section 12(b) of the Exchange Act: | |

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

The | ||

The |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ |

Smaller reporting company | |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The aggregate market value of the registrant’s voting and non-voting common stock held by non-affiliates of the registrant (without admitting that any person whose shares are not included in such calculation is an affiliate) computed by reference to the price at which the common shares were last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was $

As of March 22, 2024, the registrant had

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement in connection with the registrant’s annual meeting of shareholders, scheduled to be held on May 30, 2024, are incorporated by reference in Part III of this report. Except as expressly incorporated by reference, such proxy statement shall not be deemed to be part of this report.

TABLE OF CONTENTS

1

In this Annual Report on form 10-K (“Annual Report”), the terms “we,” “us,” “our,” “Company” and “TMC” mean TMC the metals company Inc. (formerly Sustainable Opportunities Acquisition Corp.) and our subsidiaries. On September 9, 2021 (the “Closing Date”), Sustainable Opportunities Acquisition Corp. (“SOAC” and after the Business Combination described herein, the “Company”) consummated a business combination (the “Business Combination”) pursuant to the terms of the business combination agreement dated as of March 4, 2021 (the “Business Combination Agreement”) by and among SOAC, 1291924 B.C. Unlimited Liability Company, an unlimited liability company existing under the laws of British Columbia, Canada (“NewCo Sub”), and DeepGreen Metals Inc., a company existing under the laws of British Columbia, Canada (“DeepGreen”) under which SOAC acquired DeepGreen and its business. In connection with the Business Combination, SOAC changed its name to “TMC the metals company Inc.” (“TMC”). The combined company’s common shares and warrants to purchase common shares commenced trading on the Nasdaq Global Select Market (“Nasdaq”) on September 10, 2021, under the symbols “TMC” and “TMCWW,” respectively.

As used in this Annual Report, “Mtpa” refers to millions of tonnes per year, “ktpa” refers to thousands of tonnes per year, “dmtu” refers to dry metric tonne unit, TWh” refers to trillion-watt hours, “CO2e” refers to metric tonnes of carbon dioxide emissions and “w/w” refers to weight for weight.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that relate to future events, our future operations or financial performance, or our plans, strategies and prospects. These statements are based on the beliefs and assumptions of our management team. Although we believe that our plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, we cannot assure that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions. Generally, statements that are not historical facts, including statements concerning possible or assumed future actions, business strategies, events or performance, are forward-looking statements. These statements may be preceded by, followed by or include the words “believes,” “estimates,” “expects,” “projects,” “forecasts,” “may,” “will,” “should,” “seeks,” “plans,” “scheduled,” “anticipates” or “intends” or the negative of these terms, or other comparable terminology intended to identify statements about the future, although not all forward-looking statements contain these identifying words. The forward-looking statements are based on projections prepared by, and are the responsibility of, the Company’s management. Forward-looking statements contained in this Annual Report include, but are not limited to, statements about:

| ● | the commercial and technical feasibility of seafloor polymetallic nodule collection and processing; |

| ● | our and our partners’ development and operational plans, including with respect to the planned uses of polymetallic nodules, where and how nodules will be obtained and processed, the expected environmental, social and governance impacts thereof and our plans to assess these impacts and the timing and scope of these plans, including the timing and expectations with respect to our receipt of exploitation contracts and our commercialization plans; |

| ● | the supply and demand for battery metals and battery cathode feedstocks, copper cathode and manganese ores; |

| ● | the future prices of battery metals and battery cathode feedstocks, copper cathode and manganese ores; |

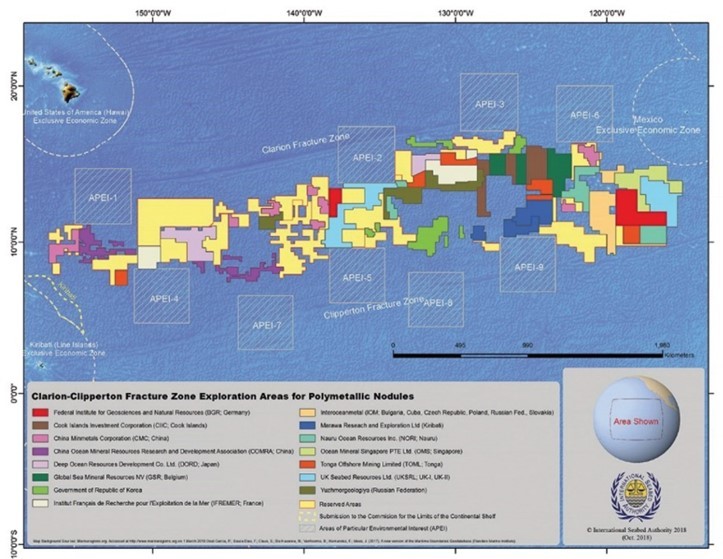

| ● | the timing and content of International Seabed Authority’s (“ISA”) final exploitation regulations that will create the legal and technical framework for exploitation of polymetallic nodules in the Clarion Clipperton Zone of the Pacific Ocean (“CCZ”); |

| ● | government regulation of mineral extraction from the deep seafloor and changes in mining laws and regulations; |

| ● | technical, operational, environmental, social and governance risks of developing and deploying equipment to collect and ship polymetallic nodules at sea, and to process such nodules on land; |

| ● | the sources and timing of potential revenue as well as the timing and amount of estimated future production, costs of production, other expenses, capital expenditures and requirements for additional capital; |

2

| ● | cash flow provided by operating activities; |

| ● | the expected activities of our partners under our key strategic relationships; |

| ● | the sufficiency of our cash on hand to meet our working capital and capital expenditure requirements, the need for additional financing and our ability to continue as a going concern; |

| ● | our ability to raise financing in the future, the nature of any such financing and our plans with respect thereto; |

| ● | any litigation to which we are a party; |

| ● | claims and limitations on insurance coverage; |

| ● | our plans to mitigate our material weaknesses in our internal control over financial reporting; |

| ● | geological, metallurgical and geotechnical studies and opinions; |

| ● | mineral resource estimates, and our ability to define and declare reserve estimates; |

| ● | our status as an emerging growth company, non-reporting Canadian issuer and passive foreign investment company (“PFIC”); |

| ● | the impact of pandemics on our business; and |

| ● | our financial performance. |

These forward-looking statements are based on information available as of the date of this Annual Report, and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Important factors could cause actual results, performance or achievements to differ materially from those indicated or implied by forward-looking statements such as those described under the caption “Risk Factors” in Item 1A of Part I of this Annual Report and in other filings that we make with the Securities and Exchange Commission (“SEC”). The risks described under the heading “Risk Factors” are not exhaustive. New risk factors emerge from time to time, and it is not possible to predict all such risk factors, nor can we assess the impact of all such risk factors on our business or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements are not guarantees of performance. You should not put undue reliance on these statements, which speak only as of the date hereof. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the foregoing cautionary statements. We undertake no obligations to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

3

PART I

Item 1.BUSINESS

Overview

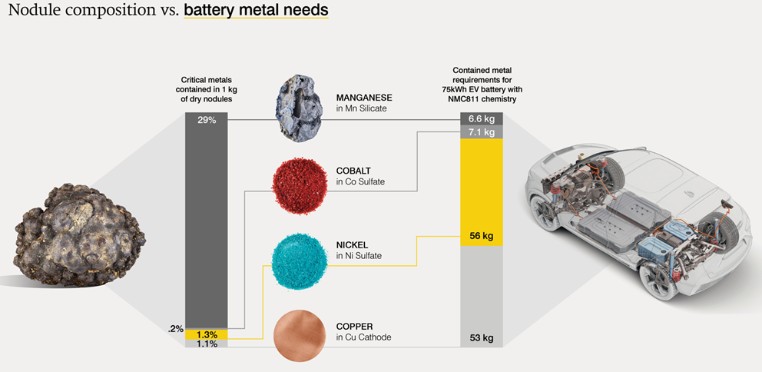

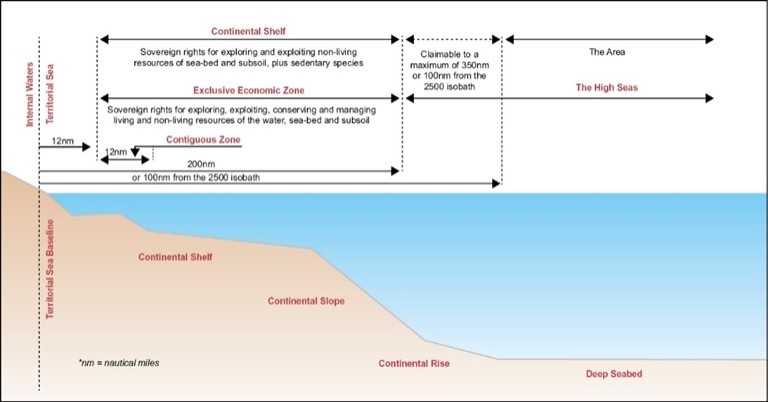

We are a deep-sea minerals exploration company focused on the collection, processing and refining of polymetallic nodules found on the seafloor in international waters of the Clarion Clipperton Zone (“CCZ”), about 1,300 nautical miles (1,500 miles or 2,400 kilometers) south-west of San Diego, California. The CCZ is a geological submarine fracture zone of abyssal plains and other formations in the Eastern Pacific Ocean, with a length of around 7,240 kilometers (4,500 miles) that spans approximately 4,500,000 square kilometers (1,700,000 square miles). Polymetallic nodules are discrete rocks that sit unattached to the seafloor, occur in significant quantities in the CCZ and have high concentrations of nickel, manganese, cobalt and copper in a single rock.

These four metals contained in the polymetallic nodules are critical for the transition to low carbon energy. Our resource definition work to date shows that nodules in our contract areas represent the world’s largest estimated undeveloped source of critical battery metals. If we are able to collect polymetallic nodules from the seafloor on a commercial scale, we plan to use such nodules to produce three types of metal products: (i) feedstock for battery cathode precursors (nickel and cobalt sulfates, or intermediary nickel-copper-cobalt matte, or nickel-copper-cobalt alloy) for electric vehicles (“EV”) and renewable energy storage markets, (ii) copper cathode for EV wiring, energy transmission and other applications, and (iii) manganese silicate for manganese alloy production required for steel production. Our mission is to build a carefully managed, shared stock of metal (a “metal commons”) that can be used, recovered and reused for generations to come. Significant quantities of newly mined metal are required because existing metal stocks are insufficient to meet rapidly rising demand.

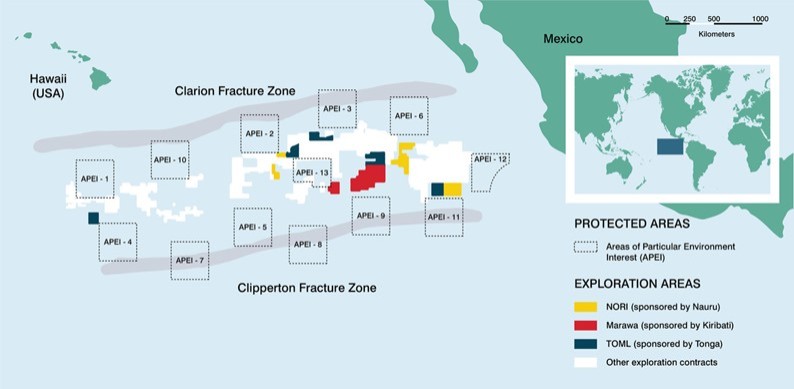

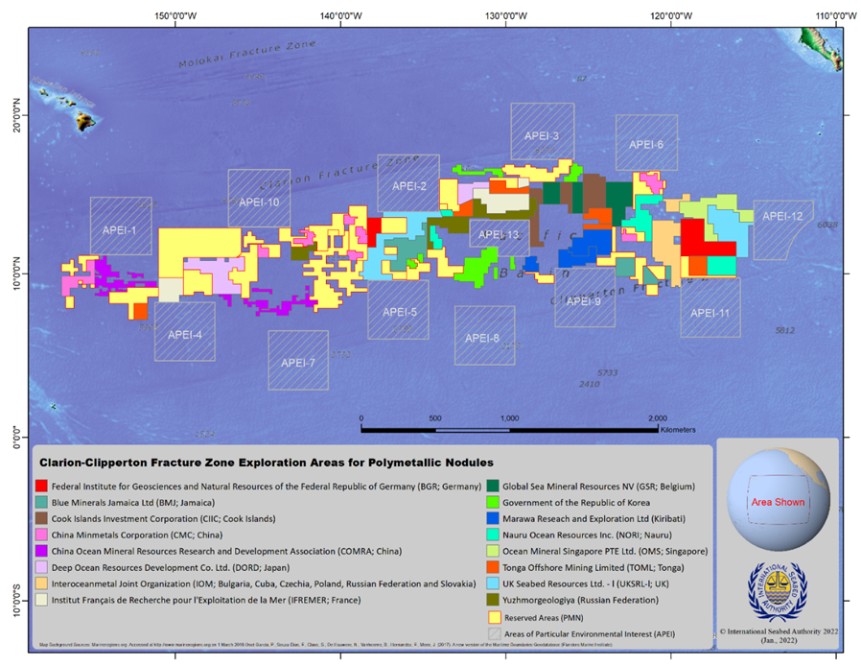

Exploration and exploitation of seabed minerals in international waters is regulated by the International Seabed Authority (“ISA”), an intergovernmental organization established pursuant to the 1994 Agreement Relating to the Implementation of the United Nations Convention on the Law of the Sea (“UNCLOS”). The ISA grants contracts to sovereign states or to private contractors who are sponsored by a sovereign state. The ISA requires that a contractor obtain and maintain sponsorship by a host nation that is a member of the ISA and signatory to UNCLOS, and that such nation maintains effective supervision and regulatory control over such sponsored contractor. The ISA has issued a total of 19 polymetallic nodule exploration contracts covering approximately 1.28 million square kilometers, or 0.4% of the global seafloor, 17 of which are in the CCZ. We hold exclusive exploration and commercial rights to three of the 17 polymetallic nodule contract areas in the CCZ through our subsidiaries Nauru Ocean Resources Inc. (“NORI”) and Tonga Offshore Mining Limited (“TOML”), sponsored by the Republic of Nauru (“Nauru”) and the Kingdom of Tonga (“Tonga”), respectively, and exclusive commercial rights through our wholly-owned subsidiary, DeepGreen Engineering Pte. Ltd.’s (“DGE”), arrangement with Marawa Research and Exploration Limited (“Marawa”), a company owned and sponsored by the Republic of Kiribati (“Kiribati”).

We are still in the exploration phase and have not yet obtained any exploitation contracts from the ISA to commence commercial scale polymetallic nodule collection in the CCZ. Additionally, we do not have the applicable environmental and/or other permits required to build and operate commercial-scale polymetallic nodule processing and refining plants on land.

4

Polymetallic Nodules

Deep-sea polymetallic nodules form on and just below the sediment-covered seafloor of the abyssal plains. These nodules contain significant amounts of metals, and their unique characteristic compared to terrestrial deposits is the presence of the four critical metals, nickel, copper, cobalt and manganese, in one deposit.

Source: TMC inaugural Impact Report 2021, filed May 2022

5

Additionally, polymetallic nodules in the CCZ possess the following characteristics:

Characteristic | What it means | |

Far removed from human communities | No need for social displacement | |

No vegetation or other obstructions covering access to nodules | No need to remove overburden, no rock cutting or blasting | |

Unbound to the seafloor, 90% of nodule mass in the top 5 cm of seafloor | No need for destructive rock cutting and excavation | |

High grades of four critical metals in a single ore | Less mass to process compared to land ores | |

Low head-grade variability | Potentially easy to process | |

2-10 cm diameter | Potentially easy to handle | |

Microporous | Potentially easy to smelt | |

Very low concentrations of certain hazardous elements like arsenic, antimony and mercury | Potential to productize almost 100% of nodule mass and design a metallurgical flowsheet that generates no tailings and leaves almost no solid waste streams behind |

The above characteristics of polymetallic nodules may provide an opportunity to compress lifecycle environmental and social impacts of producing critical metals as compared to land ores. In order to extract nickel, copper, cobalt and manganese from land ores, at least three different types of ores would need to be excavated. Mine development often involves social displacement and impacts on Indigenous people as well as deforestation, destruction of carbon sinks and biodiversity loss. In addition, several times more mass would need to be processed, often requiring significant amounts of local water resources; mining and processing tailings which can be toxic and need to be managed indefinitely in tailings dams, using dry-stacking or a practice known as deep-sea tailings placement (DSTP). Furthermore, metal production from land ores can release several toxic streams into the surrounding environment which can negatively impact the health of local communities and ecosystems. We believe using nodules to produce critical metals can help reduce several of these impacts associated with mining land ores. If our nodules are to be processed and refined in the United States (“U.S.”), we can also compress the current supply chain that some materials need to travel before reaching the U.S. of 50,000 miles down to 1,500 miles, while reducing dependency on China which dominates refining for battery metals such as nickel, cobalt and manganese.

Market Opportunity

A 2021 study by the International Energy Agency shows that the production of energy transition minerals could increase by 600% by 2040 to meet the growing demand for low-carbon energy technologies required to keep global warming at 1.5°C. Given the wide range of environmental and social impacts associated with conventional land-based mining, we believe it is important to ensure that these large amounts of critical metals are sourced with the lowest environmental, social, and economic impacts possible. As the global supply of high-grade ore remains limited and metal demand increases, we can expect a larger environmental and social footprint, potential supply shortages and volatility in metal prices should land-based ores remain the only viable source of critical metals.

6

Industries which represent an end-use segment that may require all four critical metals contained in nodules (e.g. EVs) are of particular interest to us and represent potential market opportunities. Nodules contain metals that can be employed as: (i) feedstock for battery cathode precursors (nickel, cobalt and manganese sulfates) for EV and renewable energy storage markets, (ii) copper cathode for EV wiring, energy transmission and other applications, and (iii) manganese silicate for manganese alloy production required for steel production. See Section – Competitive Strengths. While end-uses driven by the energy transition represent a small fraction of the total use of the four metals contained in polymetallic nodules today, we believe that the relative use of these four metals by EV’s and other energy transition is set to increase significantly over the next decades.

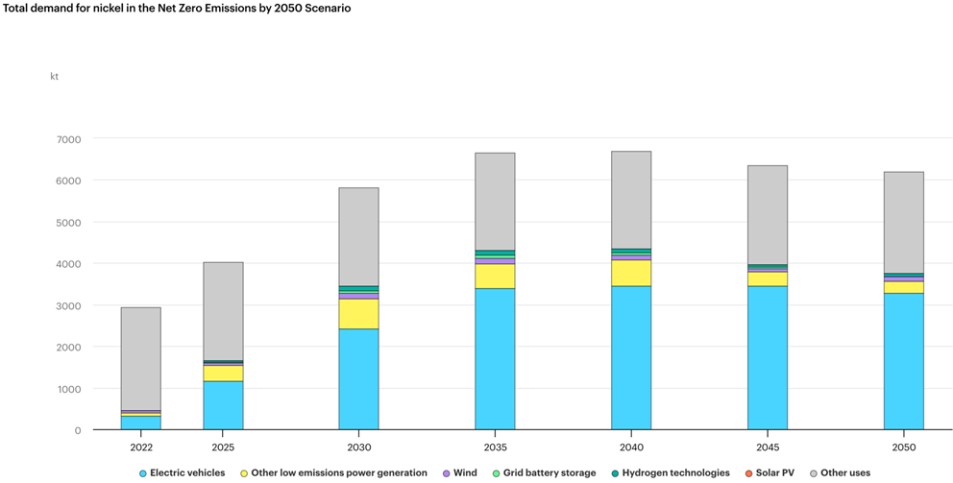

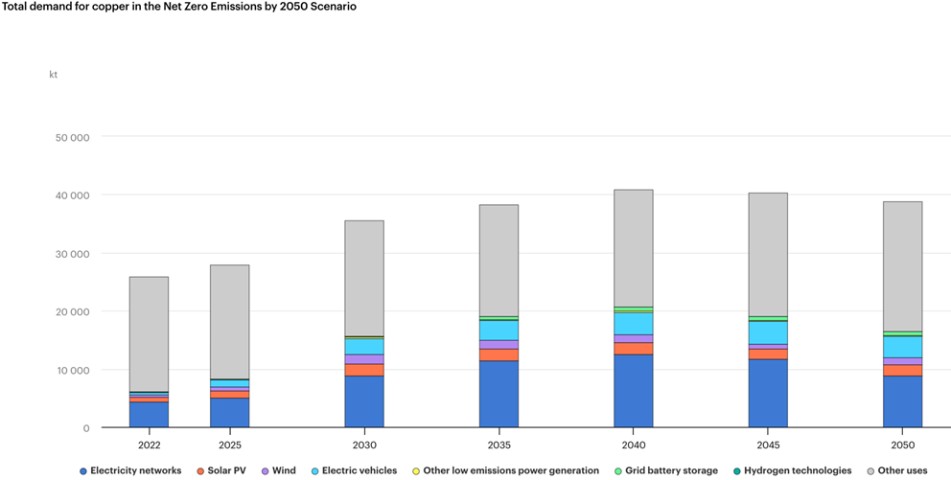

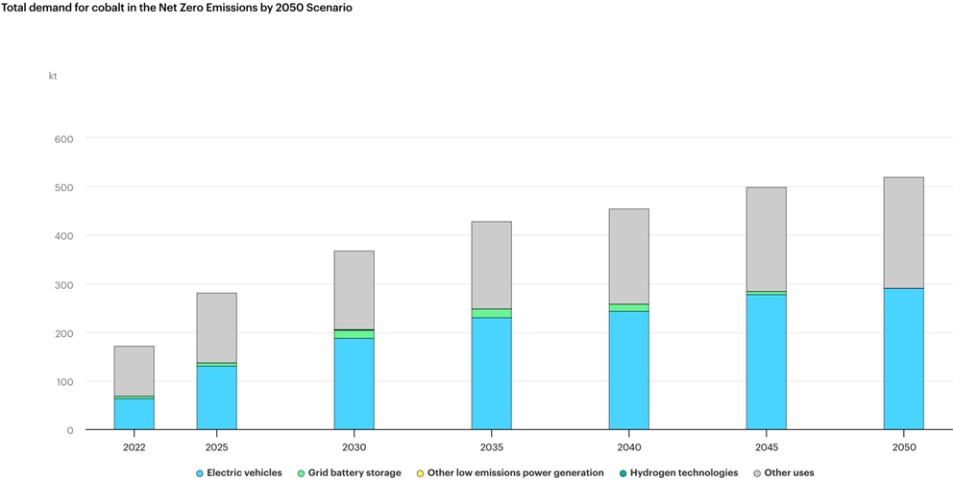

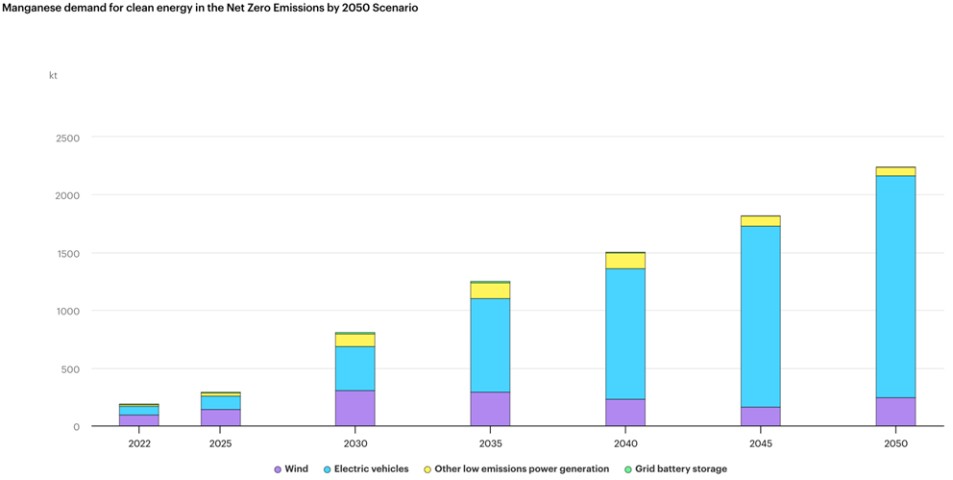

The below charts published by the International Energy Agency show increasing global demand by end-use application for nickel, cobalt, copper and manganese, under the scenario that net zero emissions is achieved by 2050. The International Energy Agency provides global demand projections for 37 critical minerals needed for clean energy transitions across various target and technology scenarios.

7

Battery Metals and EV Market Opportunity Global

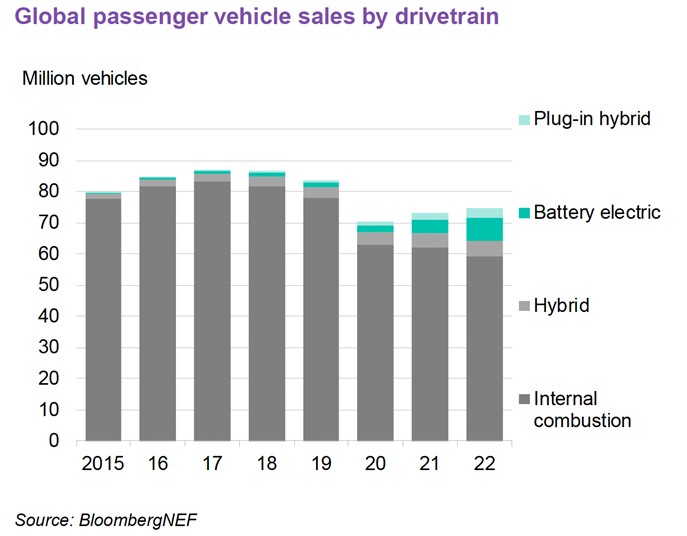

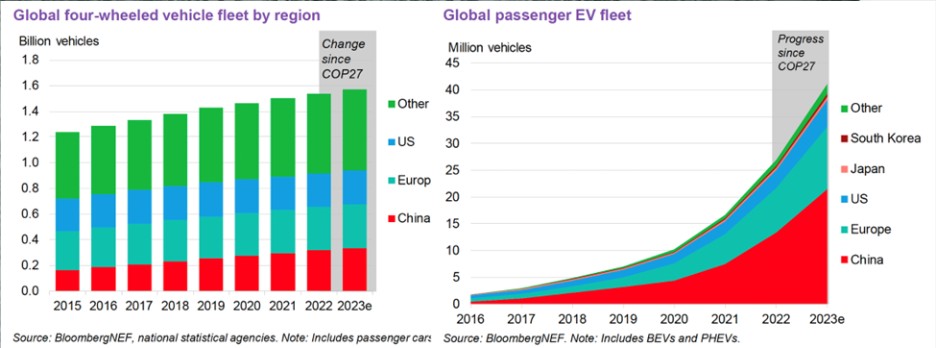

We believe the world is at the very beginning of a multi-decade electrification of road transportation. According to Bloomberg New Energy Finance (BNEF), at the end of 2023, the global fleet of four-wheeled vehicles including cars, vans, trucks, and buses numbered 1.57 billion (up 2.1% from 2022) and only 41 million passenger cars, or less than 3%, were electric. However, the new sales of internal combustion cars have decreased since 2017 as sales of battery electric and plug-in hybrids vehicles have increased and accounted for over 15% of global passenger vehicle sales in 2023. By 2030, automakers have collectively committed to sell 47 million EVs a year, a commitment that represents more than tripling of current sales levels.

The electrification of global road transportation is underpinned by the rapid expansion of the battery manufacturing capacity, which started accelerating since 2020 and is expected to reach 8TWh by 2040.

Battery chemistries that require metals contained in CCZ polymetallic nodules, nickel, cobalt and manganese, deliver high energy densities and are typically deployed in vehicles requiring long range (e.g., luxury and upmarket passenger cars) and power (trucks). In 2023, these battery chemistries accounted for 58% of overall battery manufacturing, which represented only a small portion of the overall use of nickel (~12% of nickel demand) and manganese (<1% of manganese demand). In addition, the use of batteries with different chemistries has changed over time, and we expect demand for the four metals found in polymetallic nodules to increase as the demand for batteries with certain chemistries increases.

10

We believe there will be continued growth in EV demand, with many countries committing to phasing out cars that burn fossil fuels and many original equipment manufacturers (“OEMs”) devoting significant resources to the electrification of their vehicle offerings. In 2023, the number of signatories to the Zero Emission Vehicle declaration announced at the UN Climate Change Conference (COP28) increased to 228; the declaration is aimed at accelerating the transition to zero emission vehicles with a goal to reach 100% new EV car and van sales by 2040, and by 2035 in leading markets. In the U.S., 23 states, plus the District of Columbia and Puerto Rico, have set 100% decarbonized energy goals by 2050 or sooner, with the Biden administration seeking to make half of all new vehicles sold in the U.S. zero-emissions vehicles by 2030. We believe the transition to low carbon energy and EVs will test the limits of the current supply of certain metals, as EVs require several times more of these metals (such as nickel, cobalt and copper) than cars with internal combustion engines. Following price surges in 2022 in anticipation of a period of increased demand, an oversupply of nickel largely produced in

11

Indonesia has driven down prices of the metals. These surpluses, however, could be temporary and we believe potential shortages in nickel and cobalt supply could return in the 2027/2028 timeframe, subject to developments in Indonesia and responses by the U.S. and the European Union where regulators could impose measures to differentiate between sources of metal based on the environmental and social impacts of these sources. Since prices of these metals have declined, investments by Western countries have declined and some of these interests have stopped mining/production of these metals altogether. It should be noted that current metal prices as of the date of this report are similar to projections used in the initial assessment from March 2021 for the NORI Area D project.

Battery Metals and EV Market Opportunity in the U.S.

Although the total fleet of four-wheeled vehicles in the U.S. (267 million or 17% of global) is roughly comparable in size to that of China (361 million or 23% of global), the U.S. EV fleet is three times smaller in relative terms than that of China (5.1 million EVs or 2% of national fleet vs. 22 million EVs in China or 6% of national fleet).

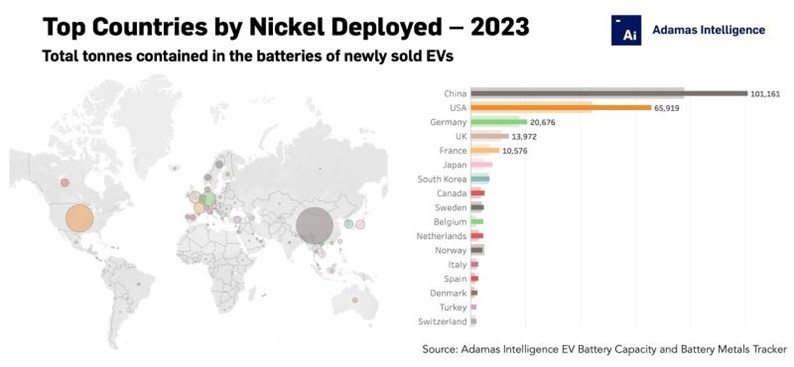

Based on 2023 data, the U.S. is the second largest consumer of battery nickel based on EV end-use. We expect this use to grow significantly in the coming years.

In August 2021, the U.S. government announced a target of 50% EV sales by 2030 and in August of 2022, the U.S. Congress enacted the Inflation Reduction Act of 2022 (“IRA”) which included incentivizing EV adoption and domestic production of clean vehicle

12

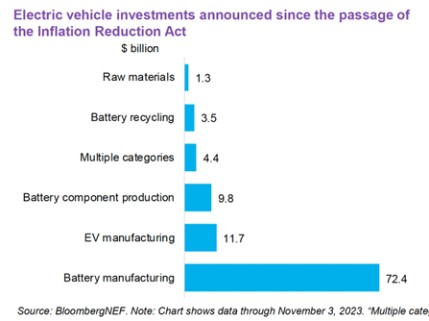

critical mineral and battery components. These announcements resulted in industry commitments to build battery cell manufacturing gigafactories, which would represent approximately 1.3TWh of aggregate capacity across North America, according to Benchmark Minerals Intelligence (“Benchmark”). While the IRA has helped attract over US$100 billion in EV value chain investments, less than 1.3% of the total is being invested in the sourcing of raw materials.

In June 2021, the Biden administration’s 100-Day Review of Critical Minerals Supply Chains estimated that fully electrifying U.S. car sales would require 1,273ktpa of Class 1 nickel, 160ktpa of cobalt and 148ktpa of manganese, compared with existing U.S. primary production of 18ktpa of nickel, 0.6ktpa of cobalt, and zero primary production of manganese. Across our NORI and TOML contract areas, we have estimated resources of 15.9Mt of nickel, 2.2Mt of cobalt and 355Mt of manganese plus 13.3Mt of copper, with the potential to take the U.S. from zero or de minimis production of those metals, which comprise the metals used in the most prominent battery cathode (NMC) in 2023 to near self-sufficiency or potentially a net export position in each. In September 2023, nine U.S. House of Representatives members wrote to the Secretary of Defense, Lloyd Austin, noting that the United States has “an opportunity to evaluate domestic processing and refining of seafloor resources from contracts held by allied parties in international waters,” and urging the Department of Defense to “assess polymetallic nodules as a viable resource to secure critical minerals and close national security vulnerabilities.” In December 2023, 31 U.S. House of Representatives members wrote to the Secretary of Defense, Lloyd Austin, emphasizing “the importance of evaluating and planning for seabed mining as a new vector of competition with China for resource superiority and security.” Additional letters from five members of the Texas House delegation as well as Senator Cornyn were written to the Department of Defense in support of our U.S. subsidiary DeepGreen Resources’ application to the Defense Production Act Title III program for support with a site-specific feasibility study for its planned full-scale processing plant.

Also in December of 2023, the U.S. National Defense Authorization Act (NDAA) was signed into law for fiscal year 2024 including a provision on ‘Critical and Strategic Minerals and Materials Sourcing from Seafloor Resources.’ In this provision, the House Armed Services Committee (HASC) directed the Assistant Secretary of Defense for Industrial Base Policy to, by March 2024, submit a report to the HASC assessing the processing of seabed resources of polymetallic nodules domestically. Although not yet submitted, the report shall include, at a minimum, the following: (1) a review of current resources and controlling parties in securing seabed resources of polymetallic nodules; (2) an assessment of current domestic deep-sea mining and material processing capabilities; and (3) a roadmap recommending how the U.S. can have the ability to source and/or process critical minerals in innovative arenas, such as deep-sea mining, to decrease reliance on sources from foreign adversaries and bolster domestic competencies. We believe the continued focus by the U.S. government may increase our opportunities to develop operations in the U.S.

Environmental Market Opportunity

All nickel, cobalt, copper and manganese going into EVs today are produced from land-based ores or recycled metal stock. Existing metal stocks available for recycling are insufficient to meet current demand. Even with high end-of-life product recycling rates, most of the new demand over the coming decades will have to be met by new mining. We believe the land mining sector is fundamentally challenged: ore grades are falling, production is moving to some of the more biodiverse and conflict-laden regions in the world (such as the Democratic Republic of the Congo, Indonesia, Philippines and South Africa), accessing ore bodies often requires a complete removal of ecosystems situated on and above such orebodies, and removing, breaking or tunneling through significant tonnage of waste rock. Toxic levels of heavy elements often found in land orebodies typically need to be removed, stored, and maintained indefinitely; a real challenge on seismically active and wet tropical islands in countries like Indonesia that accounts for most of the growth in nickel supply.

13

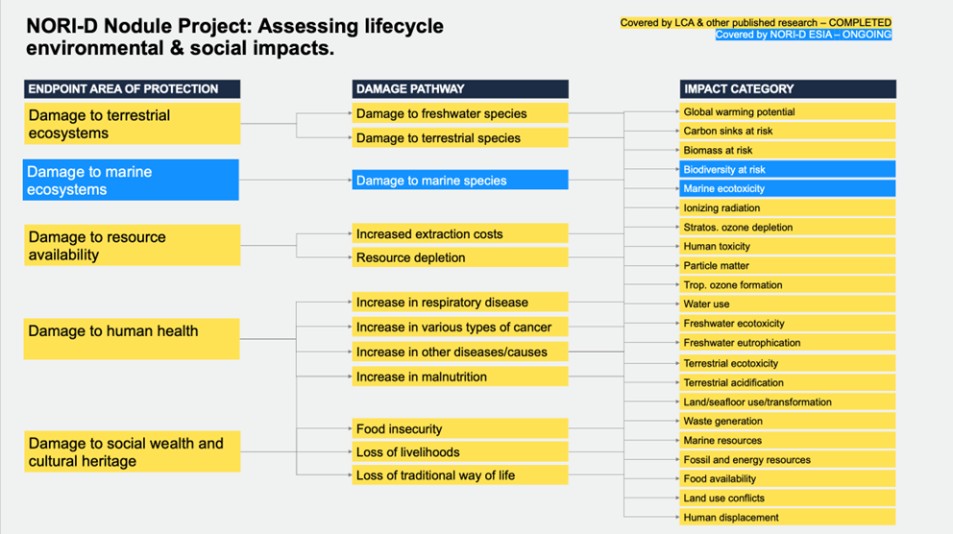

As a result of a vigorous campaign by several non-governmental organizations, some participants in the EV supply chain have called for a general moratorium on all forms of deep seabed mining until there is more knowledge about marine impacts of nodule collection operations. While our Environmental & Social Impact Assessment (ESIA) for offshore nodule collection segment of the NORI Area D Nodule Project is still ongoing, based on already completed research into lifecycle impacts of battery metal production specifically from deep-sea polymetallic nodules, we identified how nodules can potentially provide an opportunity to significantly compress most lifecycle environmental, social and governance (ESG) impacts associated with conventional metal production from land-based ores.

14

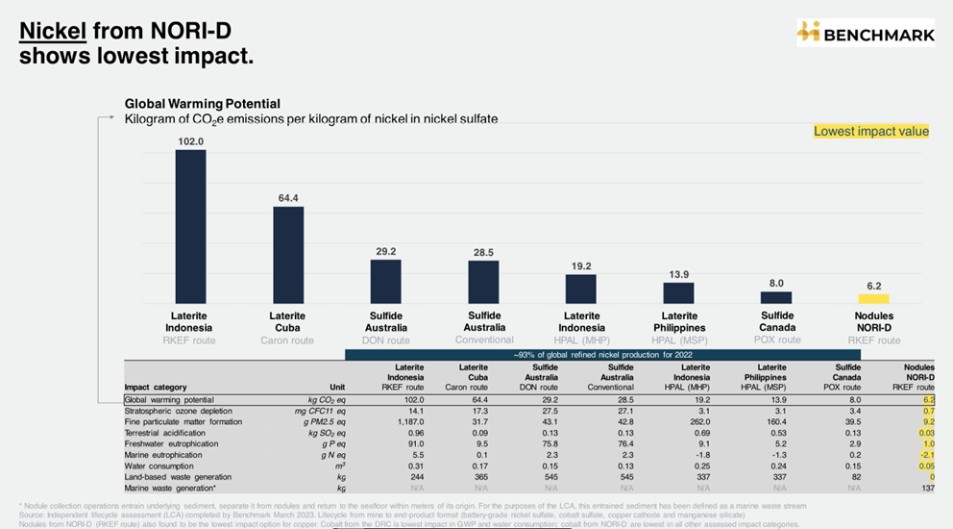

To quantify environmental footprints of metal production from nodules as compared to conventional land ores, we commissioned several lifecycle assessments (“LCAs”) looking at the cradle-to-gate impacts of producing nickel, copper, cobalt and manganese products from polymetallic nodules and how it compares to land-based routes. An LCA white paper examining a comprehensive set of impacts was commissioned by us and co-authored by certain of our executive officers in 2018 and reviewed by subject matter specialists and published on our website in April 2020; an LCA research paper focusing on climate change impacts was peer-reviewed and published in the Elsevier Journal of Cleaner Production in December 2020, an LCA research paper focusing on solid waste streams was peer-reviewed and published in the Yale Journal of Industrial Ecology in January 2022 and an independent LCA compliant with the International Organization for Standardization Standard 14040 on our NORI Area D project was conducted by Benchmark and released in March 2023. Based on these LCA assessments that we commissioned, we believe that we are positioned to become one of the lowest ESG footprint metal companies in the industry. The March 2023 LCA by Benchmark shows that the NORI Area D project model performed better in each impact category analyzed than all the land-based processing routes chosen for comparison, except for the global warming potential (“GWP”) and water consumption of producing cobalt sulfate, in which one land-based route performed better. While most of these reductions are attributable to the unique characteristics of the polymetallic nodule resource as described above, the elimination of solid processing waste streams onshore is due to our investment in a near-zero-waste flowsheet design and part of the low carbon emissions are due to our commitment to locate onshore processing facilities in places with access to low carbon power.

Benchmark modeled the land-based processing routes with background ecoinvent data and foreground data from two expert chemical engineers in the nickel and cobalt industry. The NORI Area D Project data is based on the NORI Technical Report Summary, dated March 2021, which included an initial assessment and an economic analysis of NORI Area D prepared in accordance with the SEC’s Modernization of Property Disclosures for Mining Registrants set forth in subpart 1300 of Regulation S-K (the “SEC Mining Rules”). The NORI Technical Report Summary is filed as Exhibit 96.1 to this Annual Report.

As part of the ESIA conducted by NORI in partnership with world leading deep-sea research institutions and contractors, we are currently assessing the impacts of the NORI Area D Project on marine biodiversity and ecosystem function. The CCZ abyssal plains are one of the most common and least populated habitats on the planet, akin to deserts on land. The CCZ abyssal seafloor is plant-free, food-poor and dominated by bacterial life forms. It has been studied extensively since the 1960s with over 150,000 papers published on polymetallic nodules in general and over 40,000 on CCZ nodules in particular.

15

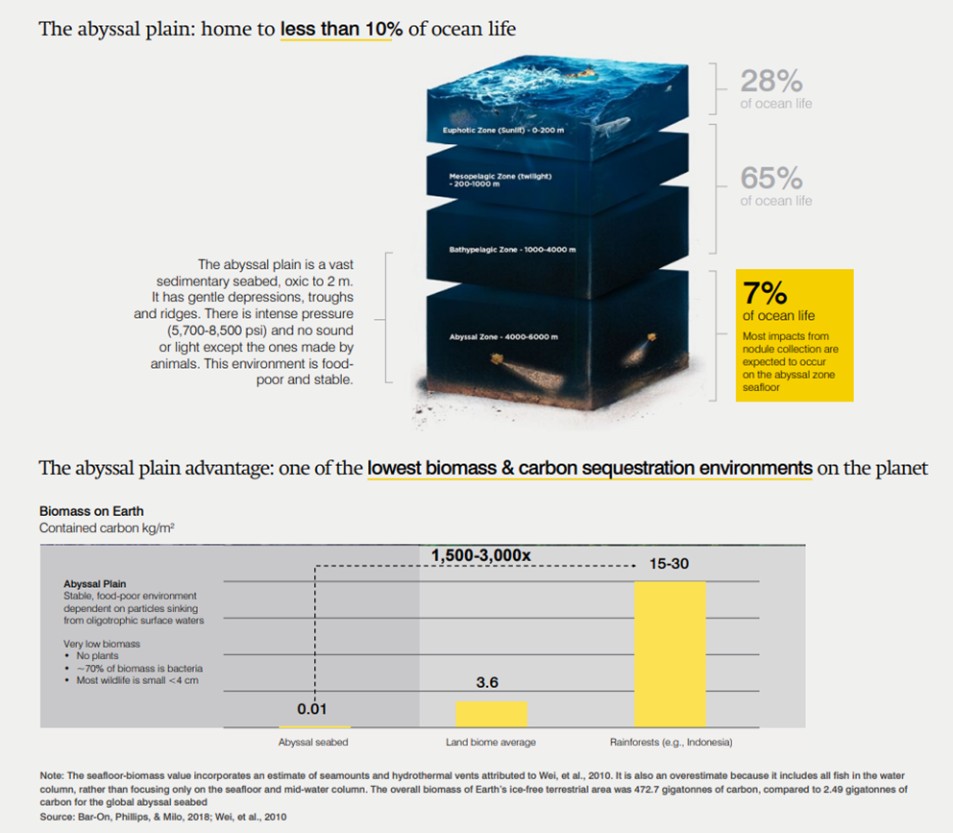

The largest driver of uncertainty in assessing the potential future impact of nodule collection operations on marine biodiversity is our ability to measure biodiversity itself. Unlike biodiversity, biomass, measured as carbon contained in live organisms per m2 of habitat, is easier to measure and compare. Based on available data we have reviewed, we believe that the CCZ is one of lowest biomass places on the planet. Metal production from nodules will reduce biomass at risk by over 90% compared to producing the same amount of metals from conventional land ores.

In contrast, land-based mining for nickel and cobalt occurs in diverse countries as identified by Benchmark in a study commissioned by us and published in November 2023. In both Indonesia and the Democratic Republic of the Congo (the “DRC”), which are the world’s largest producers of nickel and cobalt respectively, the extraction of metal ores through open pit mines requires the complete removal of overlying ecosystems and contained carbon sinks, in turn eliminating the carbon sequestration. The study found that 1 kilogram of nickel mined from saprolite and limonite ore in Sulawesi, Indonesia removes forests containing carbon stock equivalent to 7.0 and 9.4 kilograms of CO2e, and 3.6 kilograms of CO2e in the case of cobalt mined in Katanga, DRC. Due to the resulting vegetation change, mining activities cause carbon sequestration services loss of 4.8 grams and 6.5 grams of CO2e respectively for nickel, and 9.3 grams of CO2e for cobalt per year.

16

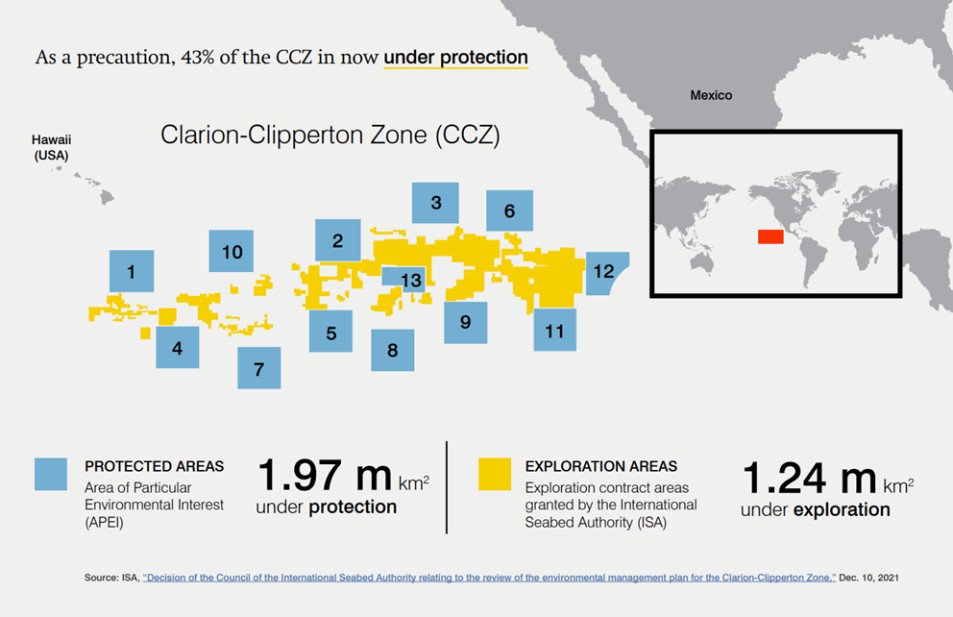

As a precautionary environmental management and protection measure, the ISA has already set aside 43% of the CCZ as protected areas or 1.97 million square kilometers, or Areas of Particular Environmental Interest (APEIs) aiming to ensure that all types of habitats that could be impacted by exploitation are represented within APEIs. For comparison, only approximately 8.2% of global oceans are protected today and the global target agreed in the High Seas Treaty in March 2023 is to protect 30% of the oceans by 2030. Additional marine impact mitigation measures such as setting aside more no-take areas inside our contract areas and leaving partial nodule cover inside collection areas to aid natural recovery of bacterial and other communities are also being evaluated. We are collaborating with some of the world’s leading researchers to conduct environmental baseline and collection impact studies to design plans that could mitigate marine impacts of nodule collection through collection system design and adaptive management systems.

If the entire CCZ area currently under exploration (1.28 million square kilometers) were to be exploited over a 30-year period, these nodule collection operations would impact 42,500 square kilometers of the abyssal seafloor per year in one of the least productive areas of the ocean (with respect to the abundance of marine life). This is less than 1% of the estimated 4,900,000 square kilometers of the seafloor currently impacted every year by trawling operations that take place primarily in highly productive coastal waters.

Potential future commercial-scale nodule collection operations in the CCZ are likely to disturb marine wildlife in the operating area. The nature and severity of these impacts on CCZ wildlife are expected to vary by species and are currently subject to uncertainty. We have completed studies baselining wildlife and ecosystem function, piloting the nodule collection system and assessing impacts arising from the use of this system immediately following the collector test and 12 months after the collector test, processing and assessment of collected data are currently in progress. Given the significant volume of deep water and the difficulty of sampling or retrieving biological specimens in the CCZ, a complete biological inventory might never be established. Accordingly, impacts on CCZ biodiversity may never be completely and definitively known. Given that similar challenges remain on land, with an estimated 70-80% of species still undescribed, it may also not be possible to definitively establish whether the impact of nodule collection on global biodiversity will be less significant than those estimated for land-based mining for a similar amount of produced metal.

17

It is also currently not definitively known how effectively the risk of biodiversity loss in the CCZ could be eliminated or reduced through mitigation strategies or how long it will take for disturbed seabed areas to recover naturally. Prior research indicates that the density, diversity and function of fauna representing most of the resident biomass (including mobile, pelagic and microbial life) are expected to recover naturally over years to decades. However, a high level of uncertainty exists around recovery of fauna that requires the hard substrate of nodules for critical life function. The extent to which planned measures such as leaving behind partial nodule cover and setting aside no-take areas would aid recruitment and recovery of nodule-dependent species in impacted areas will depend on factors like habitat connectivity, which is an area that is still under study.

We are still in the exploration phase of the project and do not have the exploitation contracts necessary to commence commercial-scale nodule collection operations in the CCZ nor have we obtained the applicable environmental and other permits required to build and operate commercial scale polymetallic nodule processing and refining plants on land.

All extractive industries result in impacts to the receiving environment. Nodule collection is no exception and will impact the deep-sea marine environment through nodule removal, disturbance of seafloor sediment (“seafloor plumes”) and return of seawater used for nodule transport that is expected to contain residual sediment and nodule fines back in the water column (“midwater plumes”). Baselining the impacted marine environment by characterizing the ecosystem and then developing measures to avoid and mitigate these impacts is the central focus of our offshore ESIA program currently being undertaken in partnership with some of the world’s leading deep-sea research institutions. Nodule removal will impact species that depend on the hard nodule substrate for attachment. The severity of the impact will depend on (1) the extent to which these species are represented in the APEIs set aside by the ISA and additional no-take areas set aside by us and (2) the extent to which residual nodule cover will aid recruitment and recovery of these species in impacted areas. Disturbance of the seafloor by nodule collector vehicles is expected to disturb (mostly microbial) organisms living in and on the sediments. Impact severity will depend on the depth of sediment disturbance (expected to be approximately 5 centimeters based on modelling, laboratory tests, and recent collector tests completed in the CCZ by our subsidiary NORI and two other nodule contract-holders, Belgium’s Global Sea Mineral Resources NV (GSR) and the German’s BGR) and the impact this disturbance has on benthic ecosystem function. Over 90% of the entrained sediment is expected to be separated from nodules inside the collector vehicle and discharged behind the collector vehicle, most settling back to the seafloor within a few hundred meters. The impact of the residual plume will depend on how quickly the smaller mobile sediment particles re-settle, how far they travel and how the resulting sedimentation impacts the benthic organisms. Less than 10% of entrained sediment that will likely evade separation inside the collector vehicle will be transported with nodules and seawater through the riser pipe to the surface production vessel where nodules get dewatered and residual water, sediment and nodules fines will be returned at some depth in the water column below the highly populated and productive photic zone. Potential impacts from the mid-water sediment plume could include clogging of the delicate respiratory and filter feeding structures of pelagic zooplankton species, such as jellyfish and krill. However, the mid-water discharge is expected to have very low solid particle concentration and dilute to low levels within minutes. The depth of discharge will be selected based on ESIA results to minimize impact on life in the midwater column. According to a research paper on midwater sediment plumes published by researchers from the Massachusetts Institute of Technology (“MIT”) in Communications Earth & Environment in July 2021, entrained sediment from the return of seawater used for nodule transport dilutes to natural background levels within a few hundred meters of the outlet. Another research paper on seafloor sediment plumes published by MIT and the Scripps Institution of Oceanography in September 2022 found that 92-98% of benthic plume generated from the pilot nodule collector vehicle rose only two meters above the seafloor.

Our Strategic Positioning

We believe we are well positioned to meet the growing demand for critical battery metals:

| ● | Supply for increasing demand: The response to climate change is driving robust demand for EVs, renewable energy storage and infrastructure. To manufacture battery cells, gigafactories will need critical battery metals like nickel, cobalt, manganese, and copper to meet rising battery demand. Globally, the number of signatories to the Zero Emission Vehicle declaration announced at COP28 in November 2023 increased to 228, which is aimed at accelerating the transition to 100% new car sales being zero emission globally by 2040, and by 2035 in leading markets. The U.S. government enacted the IRA, spurring a ramp-up of investments in battery and battery component production. Additionally, the U.S. government entered into new critical mineral trade agreement with Japan, which we believe improves our business prospects related to our plans to commercially process nodules at the Pacific Metals Co. Ltd. (“PAMCO”) facility in Hachinohe, Japan. |

18

| ● | Path to energy security: Throughout 2023, China limited exports of gallium and germanium, which are needed to produce semiconductor chips and graphite, a key ingredient in battery anodes. China also banned the export of rare earth metal extraction and separation technologies used in production of hybrid and battery electric vehicle motors. These events underscore a national security rationale for the U.S. and Western countries for reducing dependence on China as the world’s largest refiner of Class 1 nickel, cobalt and manganese. With our NORI and TOML contract areas ranked as the world’s first and second largest undeveloped nickel projects, respectively, by Mining.com in both 2022 and 2023, we believe the polymetallic nodules found in our NORI and TOML contract areas offer an internationally governed source of key battery metals that can effectively be decoupled from Chinese supply chains. |

| ● | Advancing developing countries: All three of our Sponsoring States are small developing Pacific Island nations impacted by climate change, each of which expect to receive income streams from their sponsored areas if exploration contracts are granted to extract polymetallic nodules in their sponsored areas. Royalties from commercial production of polymetallic nodules payable to the ISA are required to be distributed by the ISA with focus on developing countries. |

Our Competitive Advantages

With the potential that our resources hold and the project advancements we have made to date, we believe we are better positioned than other suppliers to provide a solution to the growing need for critical battery metals:

| ● | Availability of abundant and high-grade resource off the U.S. western seaboard: There are four critical battery metals (nickel, copper, cobalt and manganese) in relatively high concentrations in polymetallic nodules and we believe our contract areas have estimated in situ quantities of these metals equivalent to the requirement for 280 million EVs, roughly the size of the entire U.S. passenger vehicle fleet on the road today. |

| ● | Opportunity for battery metal production in the U.S.: The current supply chain of battery materials to the U.S. is approximately 50,000 miles long and is predominantly controlled by nations and companies outside of the U.S., which is leading to increasing concerns about supply chain security in the U.S. and interest in breaking the U.S. mineral dependence by re-shoring battery material supply chain in the U.S. |

| ● | Opportunity to reuse existing offshore assets and skills: We believe there is an opportunity for us to partner with offshore service providers with deep operational experience in subsea environments gained in the oil and gas industry and with existing assets that can be repurposed for our offshore nodule collection operations. We have taken advantage of this opportunity by forging a strategic alliance with Allseas Group S.A. (“Allseas”), a leading offshore contractor in 2019. In 2020, Allseas acquired a drillship that was repurposed and classified as the world’s first deep-sea mining vessel. |

| ● | Demonstrated offshore nodule collection technology: In November 2022, NORI and Allseas completed the Pilot Mining Test where approximately 4,500 tonnes of wet nodules were collected and more than 3,000 tonnes of wet nodules were lifted 4.3 kilometers to the surface after traversing over 80 kilometers of the seafloor in the NORI Area D, achieving a sustained production rate of 86.4 tonnes per hour with a scaled-down prototype seafloor nodule collector vehicle. |

| ● | Demonstrated onshore nodule processing technology: In 2021, we successfully completed the calcining and smelting of nodules into a manganese silicate product and nickel-copper-cobalt alloy intermediate product, followed by conversion and sulfidation of the alloy into matte. Testwork on the matte to define conditions for the hydrometallurgical refinery has been successfully conducted on all process stages and we anticipate completion of the program in the first quarter of 2024 with generation of what we believe will be battery-grade nickel and cobalt sulfates in test quantities. |

19

| ● | Opportunity to reuse existing onshore assets and skills: We believe there is an opportunity for us to partner with onshore processors with deep operational experience in processing nickel-bearing ores and with existing Rotary Kiln Electric Arc Furnace (“RKEF”) plants that can be repurposed for processing our nodules into intermediate products. We have taken advantage of this opportunity by signing a non-binding memorandum of understanding (“MoU”) with PAMCO, an experienced operator of a nickel laterite smelting complex in Hachinohe, Japan (IRA-compliant jurisdiction) in 2023. Following the completion of a prefeasibility exercise by PAMCO to assess nodule processing at their facility, we have signed a binding MoU in November 2023 to complete a feasibility study to process the first 1.3 Mtpa (wet) of nodules at PAMCO’s facility. A demonstration trial at PAMCO’s Hachinohe facilities with 2,000 tonnes of nodules collected during the mining pilot is expected to take place in 2024, which would further de-risk the project. |

| ● | Lower expected production cost: Based on the Initial Economic Assessment completed for NORI Area D project in March 2021, which was based on potential steady state production of approximately 12.5Mtpa of wet nodules from 2030 to 2045, we expected to be the second lowest cost nickel producer in the world, when reflecting the value of our byproducts). This Initial Economic Assessment was based on a high-capital asset expenditure (“CAPEX”) approach to our development and commercialization of operations where the majority of offshore and onshore production assets would be newly built by us. However, we are currently pursuing a low-CAPEX approach for our NORI Area D project where we reuse existing production assets. |

| ● | Lower expected environmental, social and governance footprint: The LCA completed by Benchmark in March 2023 shows that the NORI Area D project model performed better in most impact categories analyzed than all the land-based routes chosen for comparison. This favorable comparison is explained by the fact that we are developing a new type of high-grade multi-metal source found on the abyssal plain, a low biomass, low carbon sequestration deep-sea environment removed from human settlement. |

Exploration Contracts

We currently hold exclusive exploration rights through our subsidiaries NORI and TOML and exclusive commercial rights through an agreement with Marawa, to certain polymetallic nodule areas in the CCZ.

NORI. NORI our wholly-owned subsidiary, holds exploration rights to four blocks (NORI Area A, B, C, and D, the “NORI Contract Area”) covering 74,830 square kilometers in the CCZ that were granted by the ISA in July 2011. NORI is sponsored by Nauru pursuant to a certificate of sponsorship signed by the Government of Nauru on April 11, 2011. The NORI Area D is the seafloor parcel where we have performed the most resource definition and environmental work to date. NORI commissioned AMC Consulting Ltd, a leading mining consulting firm (AMC), to undertake a preliminary economic assessment (“PEA”) of the mineral resource contained in NORI Area D and to compile a technical report compliant with Canadian National Instrument (NI 43-101), which was completed in March 2021. AMC subsequently compiled the NORI Technical Report Summary, dated March 2021, which included an initial assessment and an economic analysis of NORI Area D prepared in accordance with the SEC Mining Rules. The NORI Technical Report Summary is filed as Exhibit 96.1 to this Annual Report.

TOML. TOML our wholly-owned subsidiary which we acquired in March 2020, holds exploration rights to an area covering 74,713 square kilometers in the CCZ that were granted by the ISA in January 2012 (the “TOML Contract Area”). On March 8, 2008, Tonga and TOML entered into a sponsorship agreement formalizing certain obligations of the parties in relation to TOML’s exploration application to the ISA (subsequently granted) for the TOML Contract Area. The sponsorship agreement was updated on September 23, 2021. TOML commissioned a Technical Report Summary by AMC, dated March 2021, which is filed as Exhibit 96.2 to this Annual Report.

20

Marawa. DGE, our wholly-owned subsidiary, entered into agreements with Marawa and Kiribati which provide DGE with exclusive exploration rights to an area covering 74,990 square kilometers in the CCZ (the “Marawa Contract Area”). The exploration contract between Marawa and the ISA (the “Marawa Exploration Contract”) was signed on January 19, 2015. To date, limited offshore marine resource definition activities in the Marawa Contract Area have occurred. We are collaborating with Marawa to assess the viability of any potential project in the Marawa Contract Area, although the timing of such assessment is uncertain. Marawa has delayed certain of its efforts in the Marawa Contract Area while it determines how it will move forward with additional assessment work.

Business Strategy

Our contemplated business spans the entire lifecycle from the resource acquisition and definition stage through the collection and transportation phases offshore into the processing and refining of nodules onshore and finally in product marketing and offtake (and eventually recycling of end-of-life products containing nodule-derived metals). NORI and TOML, two of our subsidiaries, intend to operate in the CCZ under the effective supervision, regulation and sponsorship of the Republic of Nauru and the Kingdom of Tonga, respectively. We intend to utilize processing operations in locations that are yet to be finalized. We have chosen a capital-light approach to our operations and have focused on forming deep strategic partnerships with leading offshore and onshore companies.

Our key strategic alliances include:

Allseas: Allseas, a leading global offshore contractor, has developed and successfully tested the pilot nodule collection system in the NORI Area D, completed in the fourth quarter of 2022. The experience from the development and testing program of the pilot system are now informing the design of upgrades and modifications into the initial smaller scale commercial production system which is expected to serve as the basis for the design of a full-scale commercial production system.

Glencore: Glencore International AG (Glencore) holds offtake rights to 50% of the NORI nickel and copper production. Glencore has the right to purchase from DGE 50% of the annual quantity of copper material and 50% of the annual quantity of nickel material produced by DGE from ore derived from the NORI Contract Area at a processing plant directly owned or controlled by DGE.

Hatch and KPM: We have worked with engineering firm Hatch Ltd. (“Hatch”) and consultants Kingston Process Metallurgy Inc. (KPM) to develop a near-zero solid waste flowsheet. The primary processing stages of the flowsheet from nodule to NiCuCo matte intermediate were demonstrated as part of our pilot plant program at FLSmidth and Xpert Process Solutions, a Glencore company (“XPS”), facilities. The matte refining stages are being tested at SGS Lakefield. The near-zero solid waste flowsheet is expected to serve as the basis for our onshore processing facilities.

21

PAMCO: In November 2022, TMC entered into a non-binding MoU with PAMCO of Japan. In November 2023, we entered into a binding MoU with PAMCO whereby they must complete a feasibility study (anticipated to be completed during the third quarter of 2024) to toll treat 1.3 million tonnes of wet polymetallic nodules per year at its Hachinohe, Japan smelting facility, which is expected to start in the second quarter of 2026, if we obtain an exploration contract from the ISA in a timely manner. PAMCO’s Hachinohe facility is located on the coast in northern Japan and is equipped with port and processing infrastructure required to receive and process polymetallic nodules and to ship products to customers.

The toll treatment is expected to take place on a dedicated RKEF processing line and produce two products: nickel-copper-cobalt alloy, an intermediate product used as feedstock to produce Li-ion battery cathodes, and a manganese silicate product used to make silico-manganese alloy, a critical input into steel manufacturing.

PAMCO successfully completed a pre-feasibility exercise pursuant to the non-binding MoU signed by the parties in November 2022. Under the binding MoU signed in November 2023:

| ● | PAMCO, with our support, expects to complete the feasibility study by the third quarter of 2024. |

| ● | We will provide PAMCO with the exclusive right to the first 1.3Mtpa of the expected 3Mtpa of wet nodule collection capacity our first nodule collection system until completion of the feasibility study. |

| ● | The parties will enter into good faith negotiations to finalize definitive processing agreements on completion of the feasibility study. |

The feasibility study is expected to confirm operating parameters and product specifications for PAMCO’s dedicated production line and define the scope and execution plan for any additional equipment requirements, which are expected to be minor. An extended pilot demonstration program utilizing existing kilns and furnaces at PAMCO’s Hachinohe, Japan facility is expected to treat a 2,000 tonne sample of polymetallic nodules collected during the successful pilot nodule collector test completed by Allseas in November 2022 on NORI Area D, with the goal of optimizing the furnace refractory selection and confirm commercial scale operating parameters such as tapping temperatures and dusting rates when treating nodules through the Hachinohe facility. The cost of processing polymetallic nodules will also be estimated to help finalize the definitive processing agreements.

In parallel, PAMCO is continuing to study the addition of a converting facility to process the intermediate alloy to nickel-copper-cobalt matte, which is an upgraded intermediate battery supply chain feedstock. It is expected that the additional facility would be constructed once commercial processing of polymetallic nodules to alloy has been demonstrated.

There can be no assurance that we will enter into a definitive strategic alliance with PAMCO in a particular time period, or at all, or on terms similar to those set forth in the binding MoU, or that if a definitive strategic alliance are entered into by us or that the existing facility will be able to successfully process nodules in a particular time period, or at all.

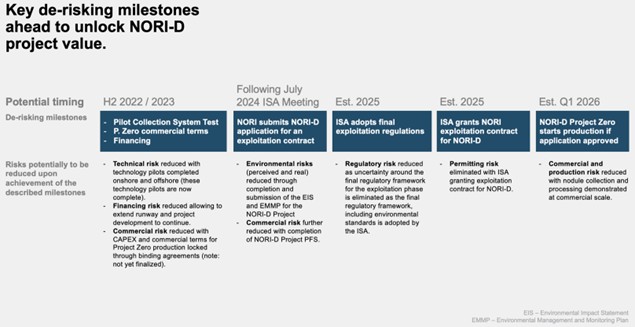

Phased Project Development

Currently, we are an exploration stage company with a completed Initial Economic Assessment, working towards a pre-feasibility study that will form an integral part of our ISA application for an exploitation contract for the NORI Contract Areas. We expect to enter into the feasibility study phase in 2024, having completed the pilot collection system test with Allseas in the CCZ in the fourth quarter of 2022. Having significantly advanced resource definition and environmental baseline studies on NORI Area D, we intend to apply for an exploitation contract on that area first. If we obtain an exploitation contract, we then plan to commence production offshore (“Project Zero”) at the end of the first quarter of 2026 using the Hidden Gem vessel which, subject to further modifications, is expected to be upgraded to a maximum capacity of 3.0 Mtpa of wet nodules. Subject to the success of Project Zero and any regulatory requirements, we then expect to move into the next phase of production (“Project One”) in which we intend to scale up production and expect to collect and process up to approximately 12.5Mtpa of wet nodules at steady state (expected 2030-2045), as outlined in the NORI – D Technical Report Summary.

22

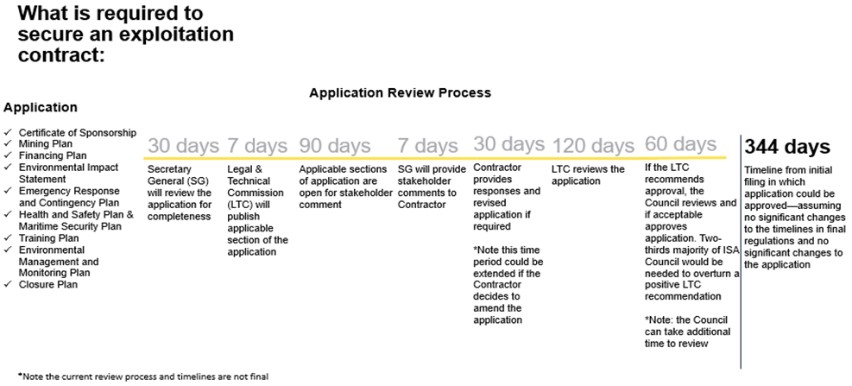

Current Work Program

We are currently focused on preparing to submit our application to the ISA for our first exploitation contract, which will include the entire NORI Contract Area, with the initial collection activities occurring within NORI Area D only following the July 2024 meetings of the ISA’s twenty-ninth session. Assuming a review process of approximately one-year, we expect to be in production offshore at the end of the first quarter of 2026, if the application is approved.

To reach our objective and initiate commercial production, we are: (i) defining our resource and project economics, (ii) developing a commercial offshore nodule collection system, (iii) assessing the environmental and social impacts of offshore nodule collection, and (iv) developing onshore technology to process collected polymetallic nodules into a manganese silicate product, and an intermediate nickel-copper-cobalt matte or nickel-copper-cobalt alloy product and/or end-products like nickel and cobalt sulfates, and copper cathode.

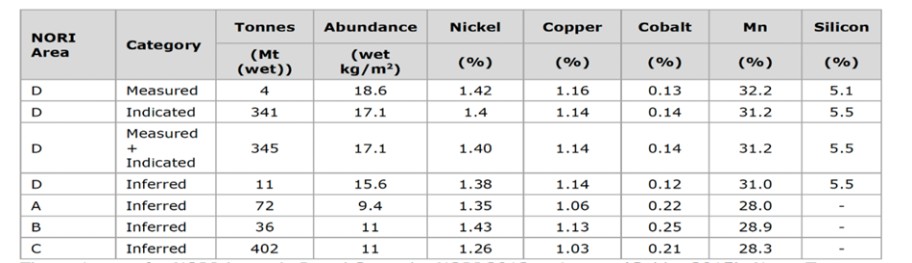

| (i) | Resource definition and project economics: Having completed a total of nine offshore resource definition campaigns, collected samples and completed subsea surveys for resource evaluation, we have defined the size and quality of our resource in the NORI and TOML Areas, as described below, in our SEC Regulation S-K (subpart 1300) compliant Technical Report Summary - Initial Assessment of the NORI Property, Clarion Clipperton Zone, Pacific Ocean dated March 17, 2021 (“NORI Initial Assessment”) and Technical Report Summary - TOML Mineral Resource, Clarion Clipperton Zone, Pacific Ocean dated March 26, 2021 (“TOML Mineral Resource Statement”), respectively, prepared by AMC. From this work, both NORI and TOML have reported measured, indicated and inferred resources as tabulated below. |

NORI Area 2020 Mineral Resource Estimate, in situ, for the NORI Areas within the CCZ at 4kg/m2 nodule abundance cut-off.

Note: Tonnes are quoted on a wet basis and grades are quoted on a dry basis, which is common practice for bulk commodities. Moisture content was estimated to 24% w/w. These estimates are presented on an undiluted basis without adjustment for resource recovery.

23

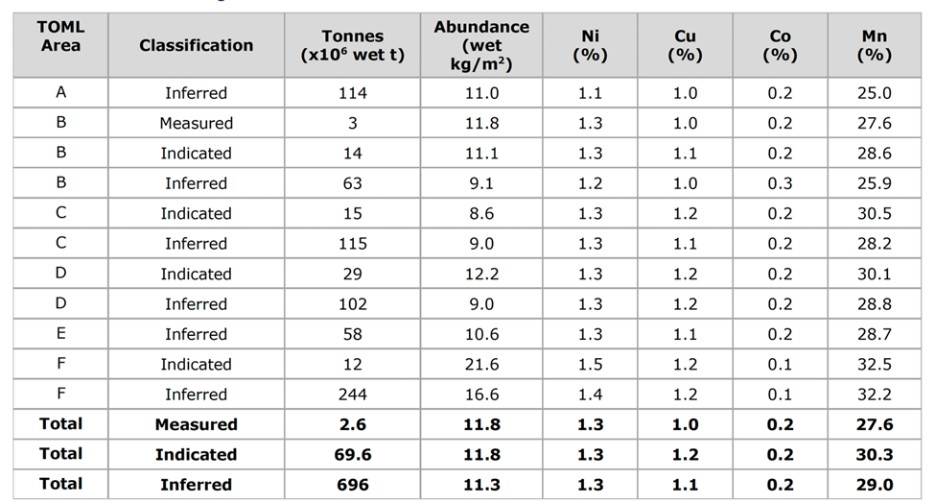

TOML Area 2020 Mineral Resource Estimate, in situ, for the TOML Areas within the CCZ at 4kg/m2 nodule abundance cut-off.

Note: Tonnes are quoted on a wet basis and grades are quoted on a dry basis, which is common practice for bulk commodities. Moisture content was estimated to 28% w/w. These estimates are presented on an undiluted basis without adjustment for resource recovery.

We plan to continue to define our resource in the NORI and TOML areas, develop project economics to pre-feasibility and feasibility level and convert resources into reserves.

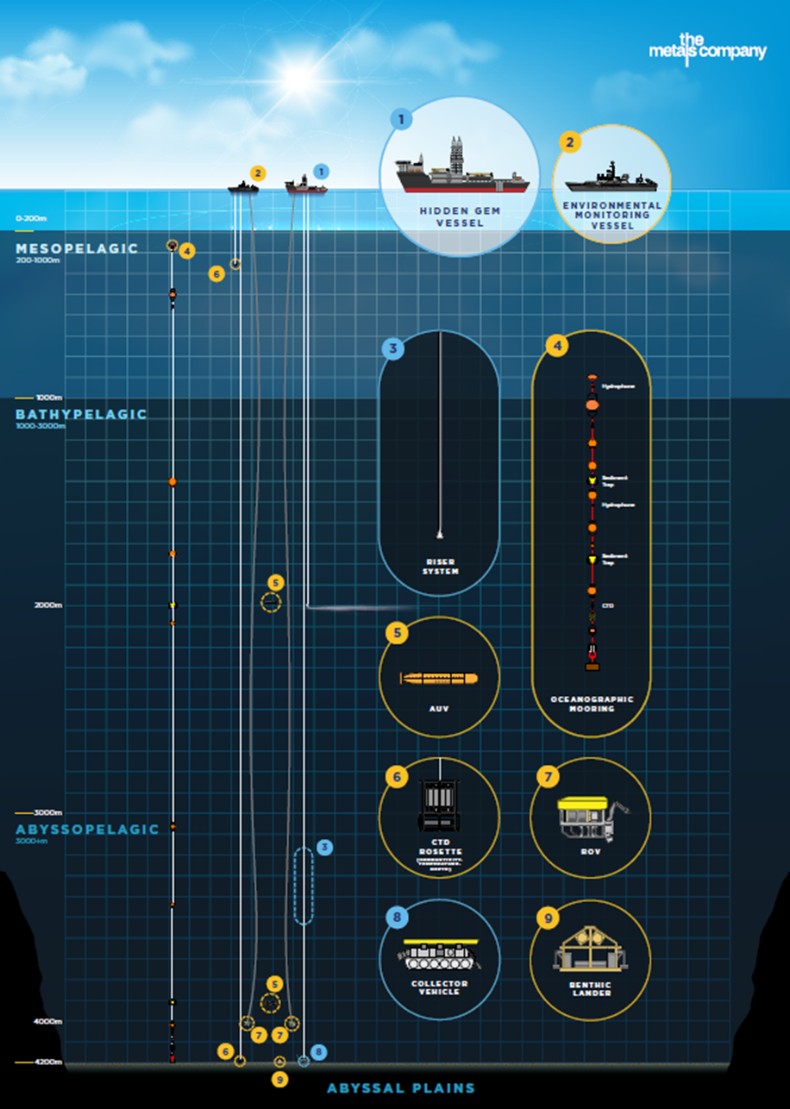

| (ii) | Commercial offshore nodule collection system development: We are working with our strategic partner and investor, Allseas, to develop a system to collect, lift and transport nodules from the seafloor to shore. The offshore collection system consists of nodule collector vehicles on the seafloor, a riser and lift system, and a surface production support vessel. The nodules are collected from the seafloor by self-propelled, tracked nodule collector vehicles using seawater jets aimed at nodules in parallel with the seafloor. No rock cutting, digging, drill-and-blast or other breakage are required at the point of collection. The collectors are remotely controlled and supplied with electric power via umbilical cables from the production support vessel, the Hidden Gem. To test the system and assess its environmental impacts, we entered into a contract with Allseas to undertake a pilot trial of the collection system in the NORI Area D, which was completed in November 2022. The successful completion of the pilot trial will support our application for an exploitation contract with the ISA. An Environmental Impact Statement (“EIS”) for this pilot trial was submitted to the ISA in July 2021 and approved on September 7, 2022, with infield testing commencing on September 19, 2022. The surface production support vessel, the Hidden Gem, was acquired by Allseas in March 2020 and has strategic importance to us, since it supported the pilot trial and is expected to be upgraded to a low-capital early production system. The vessel and collector system successfully completed trials in shallow and deepwater in the first half of 2022 prior to completing the collector test in NORI Area D in the fall of 2022, where approximately 4,500 tonnes of wet nodules were collected and more than 3000 tonnes of wet nodules were lifted 4.3 kilometers to the surface after traversing over 80 kilometers of the seafloor, achieving a production rate of 86.4 tonnes per hour. |

As a result of the successful collector test in the fourth quarter of 2022, where more than 3000 tonnes of wet nodules were lifted to the Hidden Gem, Allseas and NORI believe that they can upgrade the pilot nodule collection system, including the Hidden Gem, into the first production system, which we refer to as the Project Zero Offshore Nodule Collection System.

24

In August 2023, we announced that Allseas and NORI are executing on a plan designed based on Allseas’ estimates to increase the maximum production capacity of the Project Zero Offshore Nodule Collection System from the previous estimate of 1.3 million wet tonnes per annum to up to an estimated 3.0 million wet tonnes per annum in stepped increments, a potential increase of 130%. The upgrades are expected to include the addition of a second collector vehicle, the use of a wider diameter riser pipe from the seafloor to the surface, implementation of a larger compressor spread and improvements to the system designed to further mitigate its environmental impacts.

System capacity is expected to be increased over time as production and experience milestones are met, which we believe will help manage operational risk, minimize up-front capital expenditure requirements and allow for staged increases in capacity as environmental review thresholds are met.

The work program with Allseas during 2023 focused on the review of the pilot nodule collection system performance, review of operational issues and identification of potential improvements to overall system performance. Key aspects include scaling the technology to meeting the anticipated commercial production rates of the Project Zero Offshore Nodule Collection System and integration of the scaled-up technology into the Hidden Gem. Engineering scope has been split into six major work packages: (1) collector, (2) vertical transport system (riser and riser handling equipment), (3) storage & offloading, (4) control & automation, (5) electrical & instrumentation, and (6) flow assurance. Engineering studies have progressed on the offshore nodule offloading and transportation system, including hydrodynamic simulations and dynamic positioning analysis of the vessel-to-vessel interface during the nodule offloading activity. In line with engineering milestones, design reviews have been conducted at the Allseas office in Delft, Netherlands. The design reviews are attended by us, Allseas and third-party consultants. Regular meetings are held between us and Allseas project teams covering engineering, procurement, scheduling and estimating, operational planning (including health and safety aspects) and environmental impact.

Further to our non-binding term sheet entered into in March 2022 with Allseas, we continue discussions with Allseas regarding the specifics of these upgrades and the continued development of the Project Zero Offshore Nodule Collection System and anticipate reaching definitive agreements on commercial terms and key terms around continued development and commercial operations with Allseas before the submission of the NORI exploitation application in 2024. There can be no assurances, however, that we will enter into definitive agreements with Allseas in a particular time period, or at all, or on terms similar to those currently expected, or that if such definitive agreements are entered into that the Project Zero Offshore Nodule Collection System will be successfully developed or operated.

In addition, on August 1, 2023, we entered into an Exclusive Vessel Use Agreement with Allseas pursuant to which Allseas will give exclusive use of the Hidden Gem to us in support of the development of the Project Zero Offshore Nodule Collection System until the system is completed or December 31, 2026, whichever is earlier. In consideration of the exclusivity term, we have issued 4.15 million of our common shares to Allseas (“Common Shares”) on August 14, 2023. We expect that the definitive agreement with Allseas discussed above will extend the exclusive use of the Hidden Gem.

| (iii) | Environmental and social impact assessment (“ESIA”) for offshore nodule collection: The ESIA is an integral part of preparing our application for the ISA exploitation contract on the NORI Contract Area. Our ESIA program consists of over 100 studies and relies on the work of several independent deep-sea research institutions. In 2022, we undertook the collector test monitoring campaigns which involved completion of pre-collector test baseline data collection, monitoring of the collector test to and completion of post collection surveys to determine the immediate collector impact to the environment. The monitoring was undertaken using the Island Pride, a vessel contracted from Ocean Infinity Group Limited, deploying 2 remotely operated vehicles (“ROVs”), 3 autonomous underwater vehicles (“AUVs”) and an array of more than 50 seafloor sensors, supervised by multiple teams of scientists and sediment plume expert consultants, DHI Water and Environment Inc. and HR Wallingford. These campaigns commenced on July 15, 2022 and were completed on December 23, 2022, representing 146 operational days at sea. The preliminary plume results from the collector test have been shared with a wide range of stakeholders and presentations were conducted at the ISA during the fourth quarter of 2023. |

In October 2023 we entered into a services agreement with a third party in order for NORI to conduct an assessment of the benthic impact of the 2022 collector test in NORI Area D approximately 12 months post the collector test activities (“Campaign 8a”), which we believe will strengthen the quality of NORI’s EIS and Environmental Management and Monitoring Plan (“EMMP”) by providing additional information on the environmental regeneration of the collection test area. The key activities completed during campaign 8a were box cores, multicores, benthic and covariance lander works, and megafauna and sedimentation survey around the test field area.

25

Notwithstanding that Campaign 8a was subject to coordinated disruptive activities by Greenpeace International (“Greenpeace”) designed to prevent and obstruct the campaign, it was successfully completed on December 28, 2023. The team selected 19 sampling stations in the locality of the 2022 nodule collection system test in NORI Area D and conducted 39 multicore deployments, recovering 395 individual core samples. These yielded more than 600 subsamples that will be shared with independent researchers from leading marine research institutions for further biological analysis. Additionally using a remotely operated vehicle, the research team deployed innovative seafloor lander systems that are capable of measuring seafloor oxygen fluxes using eddy covariance methods. This resulted in over 600 hours of data acquisition at a maximum deployment depth of 4,285 meters, which we believe is the first time these bespoke sensor suites have been deployed at abyssal depths. This data is further supplemented by over one thousand core sub-samples for geochemical analysis. Researchers also conducted the fourth annual recovery and redeployment of three oceanographic moorings within NORI Area D. The sensor payload on the moorings provides insights into the soundscape, regional oceanographic currents, and particulate organic carbon flux in the Eastern CCZ regions. This data contributes to the long-term oceanographic time series and importantly will cover the El Niño-Southern Oscillation fluctuations. Greenpeace spent 11 days, actively obstructing the planned work of Campaign 8a, resulting in a significant impact to the work scopes planned for the campaign which we were able to successfully mitigate. In the case of TOML and our planned work as part of Campaign 8a, its work scope included the deployment of long-term monitoring moorings which was completely obstructed and was not able to be completed. The NORI and TOML work scopes were part of ISA approved plans of work and in NORI’s case, the post disturbance sampling was a specific suggestion of the ISA. NORI pursued legal action through the Dutch courts to halt Greenpeace’s activities and requested further assistance from the ISA. The District Court of Amsterdam ruled that Greenpeace’s occupation of NORI’s contracted vessel, the MV Coco, was unlawful, which led to the disembarkation of Greenpeace personnel. Greenpeace continued to actively obstruct NORI’s and TOML’s activities notwithstanding the court ruling.

| (iv) | Onshore technology development: To process and refine collected nodules into critical metals, we have developed a flowsheet together with a metallurgical process design firm, Hatch. This flowsheet uses conventional equipment, modified for the unique nature of the polymetallic nodule resource to deliver a process that is expected to generate near zero solid waste. The key products generated by this process are nickel sulfate, cobalt sulfate, copper cathode, manganese silicate and fertilizer-grade ammonium sulfate. The processing flowsheet also provides the potential to generate an intermediate product, a nickel-copper-cobalt matte and a nickel-copper-cobalt-iron alloy. Nickel is expected to account for almost half of future production revenues. We have completed lab-scale test work and offshore campaigns to collect a bulk sample for pilot-scale metallurgical testing. We are continuing with a metallurgical test program. In 2021, we successfully completed calcining and smelting of the nodule bulk samples into a manganese silicate product and nickel-copper-cobalt alloy intermediate, followed by converting and sulfidation of the alloy into matte. We continue testing the hydrometallurgical refining phase where matte is processed to produce nickel sulfate, cobalt sulfate, copper cathode and fertilizer grade ammonium sulfate. |

In addition, as described above and below, in 2022 and 2023, we entered into a non-binding MoU and a binding MoU with PAMCO to study the possibility of using PAMCO’s facility in Hachinohe, Japan to produce up to 1.3 million tonnes of net polymetallic nodules per year.

PAMCO is continuing to study the addition of a converting facility to process the intermediate alloy to nickel-copper-cobalt matte, which is an upgraded intermediate battery supply chain feedstock. It is expected that the additional facility would be constructed once commercial processing of polymetallic nodules to alloy has been demonstrated. There can be no assurance that we will enter into a definitive processing agreement in a particular time period, or at all, or on terms similar to those set forth in the binding MoU, or that the existing facility will be able to successfully process nodules in a particular time period, or at all.

Summary of Mineral Resources

Below is a summary table of estimated mineral resources in NORI and TOML contract areas as of December 31, 2023. The estimated mineral resources in these areas were determined in 2021 as of December 31, 2020, and also reflect the estimated mineral resources as of December 31, 2023, as none of the mineral resources in these areas were depleted by mining or any other activities. See Item 2 entitled “Properties” below for additional information about our estimated mineral resources. Both of these contract areas are in the exploration stage.

26

Summary Mineral Resources, In-Situ, at end of the fiscal year ended December 31, 2023 at 4kg/m2 abundance cut-off and based on nickel metal $16,472/t; copper metal $6,872/t; cobalt metal $46,333/t; manganese in manganese silicate $4.50/dmtu Mn.

| Measured + | |||||||||||||||

Measured mineral | Indicated mineral | indicated mineral | Inferred mineral | |||||||||||||

| resources | resources | resources | resources | ||||||||||||

| Million |

|

| Million |

|

| Million |

|

| Million |

| |||||

tonnes | Grades | tonnes | Grades | tonnes | Grades | tonnes | Grades | |||||||||

(wet) | (%) | (wet) | (%) | (wet) | (%) | (wet) | (%) | |||||||||

Ni |

|

|

|

|

|

|

|

| ||||||||

NORI |

|

|

|

|

|

|

|

| ||||||||

NORI Area A | — | — |

| — |

| — |

| — |

| — |

| 72 |

| 1.35 | ||

NORI Area B | — | — |

| — |

| — |

| — |

| — |

| 36 |

| 1.43 | ||

NORI Area C | — | — |

| — |

| — |

| — |

| — |

| 402 |

| 1.26 | ||

NORI Area D |

| 4 |

| 1.42 |

| 341 |

| 1.40 |

| 345 |

| 1.40 |

| 11 |

| 1.38 |

TOML (Areas A to F) |

| 2.6 |

| 1.33 |

| 69.6 |

| 1.35 |

| 72.2 |

| 1.35 |

| 696 |

| 1.29 |

Total |

| 6.6 |

| 1.38 |

| 410.6 |

| 1.39 |

| 417.2 |

| 1.39 |

| 1,217 |

| 1.29 |

Cu |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NORI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NORI Area A | — | — |

| — |

| — |

| — |

| — |

| 72 |

| 1.06 | ||

NORI Area B | — | — |

| — |

| — |

| — |

| — |

| 36 |

| 1.13 | ||

NORI Area C | — | — |

| — |

| — |

| — |

| — |

| 402 |

| 1.03 | ||

NORI Area D |

| 4 |

| 1.16 |

| 341 |

| 1.14 |

| 345 |

| 1.14 |

| 11 |

| 1.14 |

TOML (Areas A to F) |

| 2.6 |

| 1.05 |

| 69.6 |

| 1.18 |

| 72.2 |

| 1.18 |

| 696 |

| 1.14 |

Total |

| 6.6 |

| 1.12 |

| 410.6 |

| 1.15 |

| 417.2 |

| 1.15 |

| 1,217 |

| 1.10 |

Co |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NORI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NORI Area A | — | — |

| — |

| — |

| — |

| — |

| 72 |

| 0.22 | ||

NORI Area B | — | — |

| — |

| — |

| — |

| — |

| 36 |

| 0.25 | ||

NORI Area C | — | — |

| — |

| — |

| — |

| — |

| 402 |

| 0.21 | ||

NORI Area D |

| 4 |

| 0.13 |

| 341 |

| 0.14 |

| 345 |

| 0.14 |

| 11 |

| 0.12 |

TOML (Areas A to F) |

| 2.6 |

| 0.23 |

| 69.6 |

| 0.21 |

| 72.2 |

| 0.21 |

| 696 |

| 0.20 |

Total |

| 6.6 |

| 0.17 |

| 410.6 |

| 0.15 |

| 417.2 |

| 0.15 |

| 1,217 |

| 0.21 |

Mn |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NORI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NORI Area A | — | — |

| — |

| — |

| — |