UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

(Mark One)

| | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

For the transition period from ______ to ________

Commission File No.

USIO, INC.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name on each exchange on which registered |

| | | The |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company | |

| Emerging Growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

The aggregate market value of the voting stock held by non-affiliates of the registrant on June 30, 2023, was $

As of March 22, 2024, the number of outstanding shares of the registrant's common stock was

DOCUMENTS INCORPORATED BY REFERENCE: Items 10, 11, 12, 13 and 14 of Part III will be incorporated by reference information from the registrant’s proxy statement to be filed with the Securities and Exchange Commission in connection with the solicitation of proxies for the registrant’s 2024 Annual Meeting of Stockholders to be held on June 18, 2024

| Usio, Inc. |

| FORM 10-K |

| For the Year Ended December 31, 2023 |

| Page |

||

| Item 1. | Business. | 1 |

| Item 1A. |

||

| Item 1B. | Unresolved Staff Comments. | 17 |

| Item 1C. | Cybersecurity | 17 |

| Item 2. |

||

| Item 3. |

||

| Item 4. |

||

| Item 5. |

||

| Item 6. |

||

| Item 7. |

Management's Discussion and Analysis of Financial Condition and Results of Operations. |

|

| Item 7A. |

||

| Item 8. |

||

| Item 9. |

Changes In and Disagreements with Accountants on Accounting and Financial Disclosure. |

|

| Item 9A |

||

| Item 9B. | ||

| Item 9C. | Disclosure regarding Foreign Jurisdictions that Prevent Inspections | 43 |

| Item 10. |

||

| Item 11. |

||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. |

|

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence. |

|

| Item 14. |

||

| Item 15. |

||

| Item 16. |

||

| 48 | ||

FACTORS THAT MAY AFFECT FUTURE RESULTS

This Annual Report on Form 10-K and the documents incorporated herein by reference contain certain forward-looking statements as defined under the federal securities laws. Specifically, all statements other than statements of historical facts included in this Annual Report on Form 10-K regarding our financial performance, business strategy and plans and objectives of management for future operations and any other future events are forward-looking statements and based on our beliefs and assumptions. If used in this report, the words "will," "anticipate," "believe," "estimate," "expect," "intend," and words or phrases of similar import are intended to identify forward-looking statements. Such statements reflect our current view with respect to future events and are subject to certain risks, uncertainties, and assumptions, including, but without limitation, those risks and uncertainties contained in the Risk Factors section of this Annual Report on Form 10-K and our other filings made with the SEC. Although we believe that our expectations are reasonable, we can give no assurance that such expectations will prove to be correct. Based upon changing conditions, any one or more of these events described herein as anticipated, believed, estimated, expected or intended may not occur. All prior and subsequent written and oral forward-looking statements attributable to our Company or persons acting on our behalf are expressly qualified in their entirety by this cautionary statement. We do not intend to update any of the forward-looking statements after the date of this Annual Report to conform these statements to actual results or to changes in our expectations, except as required by law.

Factors to consider when evaluating these forward-looking statements include, but are not limited to:

| • | Loss of key resellers could reduce our revenue growth. |

| • | If our security applications are breached by cyberattacks or are not adequate to address changing market conditions and customer concerns, we may incur significant losses and be unable to sell our services. |

| • | Our efforts to expand our product portfolio and market reach, including through acquisitions, may not succeed and may reduce our revenue growth and we may not achieve or maintain profitability. |

| • | We may need additional financing in the future. We may be unable to obtain additional financing or if we obtain financing it may not be on terms favorable to us. You may lose your entire investment. |

| • | Unauthorized disclosure of cardholder data, whether through breach of our computer systems or otherwise, could expose us to liability and protracted and costly litigation. |

EXPLANATORY NOTE

This Annual Report includes estimates and other statistical data made by independent parties and by us relating to market size and growth and other data about our industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions and estimates of our future performance and the future performance of the markets in which we operate are necessarily subject to a high degree of uncertainty and risk.

INTELLECTUAL PROPERTY

We own or have rights to trademarks or trade names that we use in connection with the operation of our business, including our corporate names, logos and website names. In addition, we own or have the rights to copyrights, trade secrets and other proprietary rights that protect the content of our products and the formulations for such products. Solely for convenience, some of the trademarks, trade names and copyrights referred to in this report are listed without the ©, ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights to our trademarks, trade names and copyrights. Please see “Business –Trademarks and Domain Names” for more information.

Other trademarks and trade names in this Annual Report are the property of their respective owners.

____________________________________

Unless the context indicates otherwise, all references in this Annual Report to “Usio,” the “Company,” “we,” “us,” and “our” refer to Usio, Inc. and its subsidiaries.

General

As a cloud-based, Fintech payment processor, we serve multiple industry verticals with technology that facilitates payment acceptance and funds disbursement in a single, full-stack ecosystem. We provide payment acceptance through multiple payment methods including: payment facilitation, prepaid card and electronic billing products and services to businesses, merchants and consumers. We seek to grow our business both organically through the continued development and enhancement of our products and services and through acquisitions of new products and services. We will continue to look for opportunities (both internally and externally) to enhance our offerings to meet customer demands as they arise.

Since 1998, Usio has entered a number of market verticals within the payments industry in order to satisfy the growing payment needs of consumers and merchants across the United States. Beginning with our Electronic Bill Presentment and Payment, or EBPP, product that launched the Company, we entered into the electronic funds transfer space through the ACH network, developing ancillary and complementary products such as PINless debit in 2016, and Remotely Created Checks, or RCC, account validation, and account inquiry in 2019. These supplementary product options offer customers access to faster and more convenient payment options and tools to improve operating efficiencies. Further, our credit card payment offering was expanded in 2017 with the development of Payment Facilitation, or PayFac, that utilizes our unique technology that allows for instant enrollment of merchants and combined our suite of payment options into an integrated platform for merchants and customers to utilize.

Through our innovative Prepaid Debit Card platform, we offer a variety of prepaid card products such as reloadable, incentive, promotional and corporate card programs. Combined with our printing and mailing services, through the acquisition of IMS in December of 2020, we can satisfy the diverse requirements of customer needs with physical and virtual document creation and distribution, including traditional paper checks. Our Consumer Choice product developed and debuted in 2022 that provides flexible ways to initiate a variety of payment distributions through a multitude of payment methods including physical prepaid and virtual cards, ACH, paper checks, real-time PINless debit and others. This offering allows us a superior opportunity to increase our cross-selling efforts through all of our payment methods.

With the growing need for faster payment methods, we continue to invest in technology that can help us further expand our suite of payment technology. With the rise of Real Time Payments, or RTP, we began expansion into this market vertical in 2023, which serves as an alternative to ACH payments. As well, we continue to enhance our existing product offerings, with improvements in reporting, data management, fraud and risk monitoring, ease of access, and accelerations in client onboarding and implementation times. With our transition to a cloud-based platform, our speed, security, and scalability in payment processing is further expanded, allowing us to seamlessly grow as the market demands.

Payment Acceptance. We provide integrated electronic payment processing services to merchants and businesses, including credit, and debit card-based processing services and electronic funds transfer via the ACH network. The ACH network is a nationwide electronic funds transfer system that is regulated by the Federal Reserve and the National Automatic Clearing House Association, or NACHA, the electronic payments association, and provides for the clearing of electronic payments between participating financial institutions. Our ACH processing services enable merchants or businesses to both disburse and collect funds electronically using e-checks instead of traditional paper checks. An e-check is an electronic debit to a bank checking account that is initiated at the point-of-sale, on the Internet, over the telephone, or via a bill payment sent through the mail via a physical check. E-checks are processed using the ACH network. We are one of nine companies that hold the prestigious NACHA certification for Third-Party Senders and were the second company to receive the certification and are the most tenured to hold the certification.

Our payment acceptance services are delivered in a variety of forms and situations. For example, our capabilities allow merchants to convert a paper check to an e-check or receive card authorization at the point-of-sale, allow our merchants’ respective customer service representatives to take e-check or card payments from their consumers by telephone, and enable their consumers to make e-check or card payments directly through the use of a website or by calling an interactive voice response telephone system.

Similarly, our PINless debit product allows merchants to debit and credit accounts in real-time.

Card-Based Services. Our card-based processing services enable merchants to process both traditional card-present, tap-and-pay, or "swipe" transactions, as well as card-not-present transactions. A traditional card-present transaction occurs whenever a card holder physically presents a credit or debit card to a merchant at the point-of-sale. A card-not-present transaction occurs whenever the customer does not physically present a payment card at the point-of-sale and may occur over the Internet, mail, or telephone. A tap-and-pay transaction occurs whenever a consumer taps their phone on a physical terminal utilizing third party wallet services like Apple Pay®, Samsung Pay™ and Google Pay™.

Payment Facilitation. Following the completion of the Singular Payments acquisition in 2017, we launched our payment facilitation, or PayFac, platform called "PayFac-in-a-Box" in late 2018 targeting partnership opportunities with app and software developers in bill-centric verticals, such as legal, healthcare, property management, utilities and insurance. The PayFac-in-a-Box platform 'integration layer' offers a simple integration experience for technology companies who are looking to monetize payments within an existing base of downstream clients. The added value of offering our integration partners access to real-time merchant enrollment, credit card, debit card, ACH and prepaid card issuance capabilities through a single vendor partner relationship in face-to-face, mobile and virtual payment acceptance environments provides a true single channel commerce experience through an application programming interface, or API.

Prepaid and Incentive Card Services. Through our December 2014 acquisition of the assets of Akimbo Financial, Inc., we added a highly talented technical staff of industry subject matter experts and an innovative cardholder service platform including cardholder web and mobile applications and launched what is now our UsioCard business. As a result of this acquisition, through our subsidiary, FiCentive, Inc., we offer customizable prepaid cards which companies use for expense management, incentives, refunds, claims and disbursements, as well as unique forms of compensation such as per diem payments, government disbursements, and similar payments. This comprehensive money disbursement platform allows businesses to pay their contractors, employees, or other recipients by choosing among a prepaid debit Mastercard, real-time deposit to a checking account, traditional ACH, direct deposit or paper check. These cardholder web and mobile applications have been fully integrated into FiCentive’s prepaid card core processor, and now support all program types and brands offered by FiCentive and its clients.

As part of our Prepaid card-based processing services, we develop and manage a variety of Mastercard-branded prepaid card program types, including consumer reloadable, consumer gift, incentive, promotional, general and government disbursement and corporate expense cards. We also offer prepaid cards to consumers for use as a tool to stay on budget, manage allowances and share money with family and friends. Our UsioCard platform supports Apple Pay®, Samsung Pay™ and Google Pay™.

In our over 20+year history, we have created a loyal customer base that relies on us for our convenient, secure, innovative and adaptive services and technology, and we have built long-standing and valuable relationships with premier banking institutions such as Fifth Third Bank, Sunrise Bank, TransPecos and others.

Electronic Billing. On December 15, 2020, we entered into the business of electronic bill presentment, document composition, document decomposition and printing and mailing services serving hundreds of customers representing a wide range of industry verticals, including utilities and financial institutions through the acquisition of IMS. This product offering provides an outsourced solution for document design, print, and electronic delivery to potential customers and entities looking to reduce postage costs and increase efficiencies. This acquisition increased our ability to grow new revenue streams and allowed us to reenter the electronic bill presentment and payment revenue stream. The success of this new business line depends on our ability to realize the anticipated growth opportunities; we cannot provide any assurance that we will be able to realize these opportunities.

Industry Background and Trends

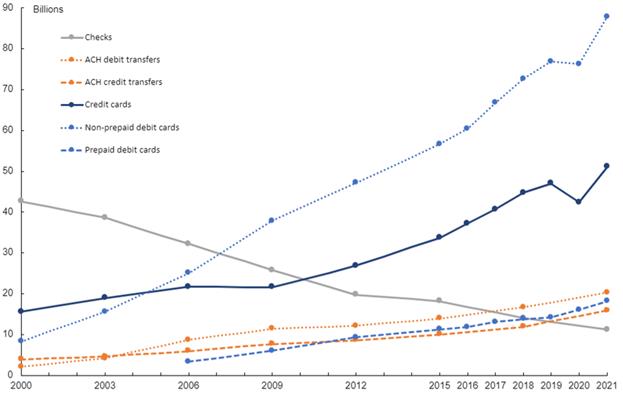

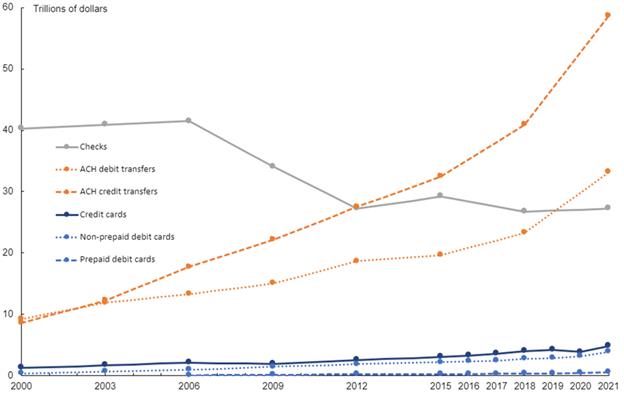

In the United States, the use of non-paper-based forms of payment, such as credit and debit cards, has risen steadily over the past several years. According to the triennial 2022 Federal Reserve Payments Study, or FRPS, as updated through July 27, 2023, the estimated number of non-cash payments continue to increase at accelerated rates. The FRPS reflects the effects of the COVID-19 pandemic which resulted in an increase of non-paper payments by 24% from 2019 through the end of 2020. The growth of electronic commerce has made the acceptance of card-based and other electronic forms of payment a necessity for businesses, both large and small, in order to remain competitive.

| • | The value of core noncash payments in the United States grew 9.5% per year since 2018, faster than in any previous FRPS measurement period since 2000. |

| • | The number of core non-cash payments, comprising debit card, credit card, ACH, and check payments, reached 204.5 billion in 2021, an increase of 30.7 billion from 2018. The value of these payments totaled $128.51 trillion in 2021, an increase of $31.47 trillion from 2018, more than twice the rate of increase in the previous three-year period (2015 to 2018). |

| • | ACH payments exhibited accelerating growth, increasing 8.3% per year by number and 12.7% per year by value from 2018 to 2021, and accounted for more than 90% of the rise in non-cash payments. |

| • | In 2021 ACH transfers grew to $91.85 trillion, representing 72% of core non-cash payments value. |

| • | Card payments continued to show robust growth from 2018 to 2021, collectively increasing 6.2% per year by number and 10% by value up from the 8.6% yearly rate of increase in the 2015 to 2018. |

| • | From 2015 to 2018, total card payments - the sum of credit card, non-prepaid debit card and prepaid debit card payments - increased 25.9 billion to reach 157 billion payments by number and increased $2.35 trillion to reach $9.43 trillion by value in 2018. |

| • | Within card payments, prepaid debit card payments had the highest growth rate in 2021 over 2018, by value, at 20.6%, compared with 13.7% per year for non-prepaid debit card payments and 7% for credit card payments. |

| • | Remote payments, by the end of 2020, represented 37.65% of the total number of card payments, having increased 7.2 billion by number and $37 billion in value over 2020. As a result, e-commerce comprised more than two-thirds of remote card payments by number, and 59.16% by value. |

| • | Chip authenticated payments accounted for 75.2% of in-person general-purpose card payments in 2020, compared with 2.0% in 2015, and grew 22.6% by number from 2018 to 2020. |

| • | From 2019 to 2020 innovative payment methods grew in popularity, such as contactless card, digital wallet, and P2P payments. |

Figure 1 (below) illustrates the overall growth in key non-cash metrics since the Federal Reserve Payments Study was first reported for the year 2000 and reflects the acceleration of growth in recent years.

Figure 2 (below) illustrates the overall growth in key cash metrics since the Federal Reserve Payments Study was first reported for the year 2000 and reflects the acceleration of growth in recent years.

Note: All estimates are on a triennial basis, except that card payments were also estimated for 2016, 2017, 2019, and 2020. Credit card payments include general-purpose and private-label versions. Prepaid debit card payments include general-purpose, private-label, and electronic benefits transfer, or EBT, versions. Estimates for prepaid debit card payments are not available for 2000 or 2003. The points mark years for which data were collected and estimates were produced. Lines connecting the points are linear interpolations.

Source: 2022 Federal Reserve Payments Study

We believe that the electronic payment processing industry will continue to benefit from the following trends:

Favorable Demographics

As consumers age, we expect that they will continue to use the payment technology to which they have grown accustomed. More consumers are beginning to use card-based and other electronic payment methods for purchases at an earlier age. These consumers have witnessed the wide adoption of card products, technology innovations such as mobile phone payment applications, widespread adoption of the internet and a significant increase in card not present transactions and on-line shopping during COVID-19. As younger consumers comprise an increasing percentage of the population and as they enter the work force, we expect purchases using electronic payment methods will become a larger percentage of total consumer spending. We believe the increasing usage of smart phones as an instrument of payment will also create further opportunities for us in the future. We also believe that contact-less payments like Apple Pay®, Samsung Pay™ and Google Pay™ will increase payment processing opportunities for us.

Increased Electronic Payment Acceptance by Small Businesses

Small businesses are a vital component of the U.S. economy and are expected to contribute to the increased use of electronic payment methods. The lower costs associated with electronic payment methods are making these services more affordable to a larger segment of the small business market. In addition, we believe these businesses are experiencing increased pressure to accept electronic payment methods in order to remain competitive and to meet consumer expectations. As a result, many of these small businesses are seeking to provide customers with the ability to pay for merchandise and services using electronic payment methods, including those in industries that have historically accepted cash and checks as the only forms of payment for their merchandise and services.

Growth in Online Transactions

Market researchers expect continued growth in card-not-present transactions due to the steady growth of the internet and electronic commerce. According to the U.S. Census Bureau, estimated retail e-commerce sales for 2023 were estimated at $1,118.7 billion, an increase of approximately 7.6% from 2022.

Products and Services

Our suite of payment solutions is driven by a sophisticated infrastructure that merges our own technology with strategic alliances, offering secure, scalable, and resilient payment processing services. Leveraging the latest in cloud computing and cybersecurity, including Microsoft Azure's robust security features, we ensure the protection of data transmissions and transactions. Our adoption of Azure's hub-spoke architecture and other cutting-edge technologies supports enhanced performance and security, facilitating seamless integrations with third-party processors and offering tailored payment services to meet the specific requirements of our clients.

The platform supports secure data exchanges using state-of-the-art encryption standards and secure communication protocols, using the latest technology in best-practices encryption to safeguard electronic transactions across the internet. With comprehensive data warehousing, we offer efficient storage, retrieval, and data analysis, ensuring all sensitive information is encrypted and securely managed.

Payment Acceptance. Our service offerings encompass a broad spectrum of ACH transaction processing, including innovative solutions like Represented Check and Check Conversion for electronic payment facilitation. Clients have the flexibility to initiate transactions via our online portal or leverage our expertise for transaction processing on their behalf via a robust API set.

We extend merchant services across major card networks (VISA, Mastercard, American Express, Discover, JCB), supported by online and physical terminal access. Our proprietary platform merges ACH and card processing capabilities, enabling businesses to handle both e-checks and card payments efficiently.

The expansion of our platform and the transition to cloud-based infrastructure underscore our commitment to speed, security, and scalability in payment processing. Our direct Fed ACH system integration, facilitated by NACHA certification, exemplifies our efforts to optimize processing efficiency, reduce costs, and enhance merchant services.

Prepaid and Incentive Card Services. Our Prepaid and Incentive Card Issuance Services are anchored by our sophisticated processing platform, which supports an array of card program types in partnership with prominent banks and offers highly customizable digital solutions. A key feature of our innovative service offerings is the integration of an external authorization engine that provides real-time transaction authorization through a unique dual-funding mechanism, enhancing transactional flexibility and user experience by allowing for the application of real-time value loads by the program managers. This engine, coupled with our comprehensive support for popular mobile wallets via Mastercard’s Digital Enablement Services, underscores our commitment to leveraging cutting-edge technology to deliver seamless and enriched payment experiences. Our platform's rapid custom solution deployment capability further cements our position as a leader in the market, demonstrating our dedication to innovation and operational agility in meeting the advanced payment solution needs of our clients.

Electronic Billing. Following the acquisition of Information Management Solutions, LLC, or IMS, we've enhanced and expanded our services to include electronic bill presentment and comprehensive document management solutions, catering to a wide array of industries. Our state-of-the-art digital printing capabilities, combined with our status as a seamless mailer with USPS, enable us to meet high-volume demands efficiently, ensuring we remain at the forefront of printing and mailing services. Output Solutions provides printing and mailing services to utilities, healthcare providers, credit unions, banks, governmental agencies, and manufacturing and other customers that have high volume billing and printing needs.

Relationships with Sponsors and Processors

We have agreements with several processors that provide us, on a non-exclusive basis,with transaction processing and transmittal, transaction authorization and data capture, and access to various reporting tools. In order to provide payment processing services for ACH transactions, we must maintain a relationship with an Originating Depository Financial Institution, or ODFI, in the ACH network because we are not a bank and therefore, we are not eligible to be an ODFI. For the ODFI portion of our ACH business, we have entered into agreements with the North American Banking Company, or NABC, Metropolitan Commercial Bank and TransPecos Banks. We are financially liable for all fees, fines, chargebacks, and losses related to our ACH processing merchant customers. We may also require cash deposits and other types of collateral from certain merchants to mitigate any such risk. Similarly, in order to provide payment-processing services for Visa, Mastercard and Discover transactions, we must be sponsored by a financial institution that is a principal member of the respective Visa, Mastercard and Discover card associations. Central Bank of St. Louis and Fifth Third Bank have, respectively, sponsored us under the designations Third Party Processor, or TPP, and Independent Sales Organization, or ISO, with the Visa card association, and under the designations Third Party Servicer, or TPS, and Merchant Service Provider, or MSP, with the Mastercard card association. We have an agreement with TriSource Solutions, LLC and an agreement with Global Payments, Inc. through which their member banks, Central Bank of St. Louis and Fifth Third Bank, sponsor us for membership in the Visa, Mastercard, American Express, and Discover card associations and settle card transactions for our merchants. These agreements may be terminated by the processor if we materially breach the agreements and we do not cure the breach within 30 days, or if we enter bankruptcy or file for bankruptcy. We also maintain a bank sponsorship agreement with Sunrise Banks, N.A. for our prepaid card programs. We are liable for any card-associated losses for cards that we issue that might incur a negative balance and we are liable for card association fines, fees and chargebacks.

Under our processing agreement with TriSource Solutions and Vantiv, we are financially liable for all fees, fines, chargebacks and losses related to our card processing merchant customers. Under our processing agreement with Global Payments, Inc., we are not financially liable for all fees, chargebacks and losses related to our card processing merchant customers, but we are liable for potential card association fines. If, due to insolvency or bankruptcy of our merchant customers, or for another reason, we are unable to collect from our merchant customers amounts that have been refunded to the cardholders because the cardholders properly initiated a charge-back transaction to reverse the credit card charges, we must bear the credit risk for the full amount of the card holder transaction. We utilize a number of systems and procedures to evaluate and manage merchant risk, such as obtaining approval of prospective merchants from our processor and sponsor bank, setting transaction limits and monitoring account activity. We may also require cash deposits and other types of collateral from certain merchants to mitigate any such risk. We maintain a reserve for losses resulting from card processing and related chargebacks. We estimate our potential loss for chargebacks by performing a historical analysis of our charge-back loss experience with similar merchants and considering other factors that could affect that experience in the future, such as the types of card transactions processed and nature of the merchant relationship with their consumers.

We are currently sponsored by Evolve Bank & Trust, TransPecos Bank and CBW Bank in order to access certain regional debit networks. Through these sponsorships, we created a new service in late 2016 to provide both the issuance of real time credits and debits to a debit card holder via a regional network without using a PIN. Regional networks are not affiliated with major credit card associations and operate independently. Through our sponsorships with Evolve Bank & Trust, TransPecos Bank and CBW Bank, we are financially liable for all fees, fines, chargebacks and losses related to our PINless debit card processing for our merchant customers. We may also require cash deposits and other types of collateral from certain merchants to mitigate any such risk. The banking sponsor and each of the regional debit networks have the ability to terminate our access or anyone of our merchant’s access to process payments without notice. If either case occurs, our revenue could be negatively affected. In January 2018, our previous sponsor, Pueblo Bank and Trust, terminated their relationship with our gateway provider and as a result we stopped processing PINless debit transactions for a short period of time. We secured a relationship with Evolve Bank & Trust and resumed processing PINless debit transactions and subsequently secured a sponsoring relationship with CBW Bank in 2021 and TransPecos bank in 2023.

We maintain an allowance for estimated losses resulting from the inability or failure of our merchant customers to make required payments for fees charged by us. Amounts due from customers may be deemed uncollectible because of merchant disputes, fraud, insolvency or bankruptcy. We determine the allowance based on an account-by-account review, taking into consideration such factors as the age of the outstanding receivable, historical pattern of collections and financial condition of the customer. We closely monitor extensions of credit and if the financial condition of our customers were to deteriorate, resulting in an impairment of their ability to make contractual payments, additional allowances may be required.

Sales and Marketing

We sell and market our ACH products and services primarily through non-exclusive resellers that act as an external sales force, with minimal direct investment in sales infrastructure and management, as well as direct contact by our sales personnel. Our direct sales efforts are coordinated by two sales executives and supported by other employees who function in sales capacities. Our primary market focus is on companies generating high volumes of electronic payment transactions. We tailor our sales efforts to reach this market by pre-qualifying prospective sales leads through direct contact or market research. Our sales personnel typically initiate contact with prospective customers that we identify as meeting our targeted customer profile.

We also market and sell our prepaid card program directly to government entities, corporations and to consumers through the Internet. A major initiative will be the packaging and cross selling of our platform of payment options across our portfolio of merchants. As a part of this major initiative, we will continue to analyze our sales and marketing efforts to optimize productivity, increase sales force effectiveness, broaden our reach through reseller initiatives and advantageous alliances and effectively optimize sales and marketing expenses while meeting our revenue and profit objectives.

We also offer additional services relating to electronic bill presentment, document composition, document decomposition and printing and mailing services serving hundreds of customers representing a wide range of industry verticals, including utilities and financial institutions. This service, which we began with the acquisition of IMS in December 2020, allows us to cross-sell existing service offerings to our customers.

Customers

Our customers are consumers, merchants, and businesses that use our Automated Clearing House and/or card-based processing services in order to provide their consumers with the ability to pay for goods and services without having to use cash or a paper check. These merchant customers operate in a variety of predominately retail industries and are under contract with us to exclusively use the services that we provide to them. Recent areas of customer focus have included system integrators, law firms, churches, charitable organizations, medical and dental clinics, doctor's offices, property management and homeowner associations, hospitality firms and municipalities. Most of our merchant customers have signed long-term contracts, generally with three-year terms, that provide for volume-based transaction fees. Our merchant accounts increased 12% to 6,281 customers at December 31, 2023 from 5,601 customers at December 31, 2022. Our customers are geographically dispersed throughout the United States.

No customer accounted for more than 10% of revenues in 2023 or 2022.

Competition

The payment processing industry is highly competitive. Many small and large companies compete with us in providing payment processing services and related services to a wide range of merchants. There are a number of large transaction processors, including Fiserv, Inc., Elavon Inc., WorldPay, Stripe and Square that serve a broad market spectrum from large to small merchants and provide banking, automatic teller machine, and other payment-related services and systems in addition to card-based payment processing. There are also a large number of smaller transaction processors that provide various services to small and medium- sized merchants. Many of our competitors have substantially greater capital resources than us and operate as subsidiaries of financial or bank holding companies, which may allow them on a consolidated basis to own and conduct depository and other banking activities that we do not have the regulatory authority to own or conduct. We believe that the principal competitive factors in our market include:

| • |

quality of service; |

| • |

reliability of service; |

| • |

ability to evaluate, undertake and manage risk; |

| • |

ability to offer customized technology solutions; |

| • |

speed in implementing payment processes; |

| • |

price and other financial terms; and |

| • |

multi-channel payment capability. |

We believe that our specific focus on providing integrated payment processing solutions to merchants, in addition to our keen understanding of the needs and risks associated with providing payment processing services electronically, gives us a competitive advantage over other competitors, which have a narrower market perspective, and over competitors of a similar or smaller size that may lack our experience and expertise in the electronic payments industry. We believe this allows us to satisfy the market demands for risk management, and service reliability. Furthermore, we believe we present a competitive distinction through our internal technology to provide a single integrated payment warehouse that consolidates, processes, tracks and reports all payments regardless of payment source or channel. This integrated payments approach helps offer superior quality in service, alongside industry leading implementation times, and platform reliability. We also believe our customized technology solutions and high level of service provide a competitive advantage, particularly for smaller businesses that do not have large internal technology capabilities or the ability to comply with payment security regulations, saving our customers time and money, while offering a broad range of diverse payment options.

Due to our proprietary systems and our ability to create and establish corporate-branded card programs in shorter time frames than our competitors, our prepaid card offerings are competitive with those of much larger companies. We also believe that our ten plus years of prepaid industry experience in processing and managing prepaid card programs is a competitive advantage over many of our competitors. We believe our connectivity and the ability to process via the contact-less networks of Apple Pay®, Samsung Pay™ and Google Pay™ are also competitive advantages. We also believe that the Akimbo mobile application technology and advanced card holder websites provide a competitive advantage in securing both consumers and business clients that have a need for a card program for their customer base. Finally, we believe we hold a significant competitive advantage over potential entrants into the prepaid industry as a result of the significant barrier in obtaining bank sponsorships for prepaid card program management and an even higher barrier for performing prepaid card processing.

Trademarks and Domain Names

We own federally registered trademarks on the marks “Usio,” “Payment Data Systems, Inc.,” “Akimbo,” “FiCentive Innovations in Prepaid Card Solutions,” “Don’t change your bank, just your card” and “ZBILL” and their respective designs.

Some of our material websites are www.usio.com, www.payfacinabox.com, www.ficentive.com, www.akimbocard.com, and www.usiooutput.com. The inclusion of these website addresses in this Annual Report do not include or incorporate by reference the information on or accessible through these websites, and the information contained on or accessible through these websites should not be considered as part of this annual report on Form 10-K.

We rely on a combination of copyright, trademark and trade secret laws, employee and third-party nondisclosure agreements, and other intellectual property protection methods to protect our services and related products.

Government Regulation

Our industry is highly regulated. Any new, or changes made to, U.S. federal, state and local laws, regulations, card network rules or other industry standards affecting our business may require significant development efforts or have an unfavorable impact to our financial results. Failure to comply with these laws and regulations may result in the suspension or revocation of licenses or registrations, the limitation, suspension or termination of services and/or the imposition of civil and criminal penalties, including fines. Certain of our services are also subject to rules set by various payment networks, such as Visa and Mastercard.

The Dodd-Frank Act

President Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, into law on July 21, 2010. The Dodd-Frank Act caused significant structural reforms to the financial services industry. The Dodd-Frank Act regulates the fees charged or received by issuers for processing debit transactions and the transaction routing options available to merchants. The Dodd-Frank Act also established the Consumer Financial Protection Bureau or CFPB to regulate consumer financial services, including many services offered to our customers. These rules clarify the prepaid regulatory landscape for consumer access to disclosures, fees and statements, error resolution, limited liability and overdrafts. Additionally, the Durbin Amendment to the Dodd-Frank Act provided that interchange fees that a card issuer or payment network receives or charges for debit transactions will now be regulated by the Federal Reserve and must be “reasonable and proportional” to the cost incurred by the card issuer in authorizing, clearing and settling the transaction. In addition, the Durbin Amendment contains prohibitions on network exclusivity and merchant routing restrictions.

The Dodd-Frank Act caused interchange fees to be lowered on large bank-issued debit cards. The lowered interchange fees had a mild negative impact on our revenues and increased our earnings due to the fact that we were able to keep our prices constant with our merchants. If our competitors start to pass the extra margin into savings to their merchants, we may be forced to follow their actions and become exposed to lower earnings on the debit card transactions for large banks.

CARD Act

As an agent of, and third-party service provider to, our issuing banks, we are subject to indirect regulation and direct audit and examination by the Office of Thrift Supervision, the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, or FRB, and the Federal Deposit Insurance Corporation.

On March 23, 2010, the FRB issued a final rule implementing Title IV of the Credit Card Accountability, Responsibility, and Disclosure Act of 2009, or CARD Act, which imposes requirements relating to disclosures, fees and expiration dates that are generally applicable to gift certificates, store gift cards and general-use prepaid cards. We believe that our general purpose re-loadable prepaid cards, and the maintenance fees charged on our general purpose re-loadable cards, are exempt from the requirements under this rule, as they fall within an express exclusion for cards which are re-loadable and not marketed or labeled as a gift card or gift certificate. However, this exclusion is not available if the issuer, the retailer selling the card to a consumer or the program manager, promotes, even if occasionally, the use of the card as a gift card or gift certificate. As a result, we provide retailers with instructions and policies regarding the display and promotion of our general purpose re-loadable cards. However, it is possible that despite our instructions and policies to the contrary, a retailer engaged in offering our general purpose re-loadable cards to consumers could take an action with respect to one or more of the cards that would cause each similar card to be viewed as being marketed or labeled as a gift card, such as by placing our general purpose re-loadable cards on a display which prominently features the availability of gift cards and does not separate or otherwise distinguish our general purpose re-loadable cards from the gift cards. In such event, it is possible that such general purpose re-loadable cards would lose their eligibility for such exclusion to the CARD Act and its requirements, and therefore we could be deemed to be in violation of the CARD Act and the rule, which could result in the imposition of fines, the suspension of our ability to offer our general purpose re-loadable cards, civil liability, criminal liability, and the inability of our issuing banks to apply certain fees to our general purpose re-loadable cards, each of which would likely have a material adverse impact on our revenues.

In 2014, we resumed issuing gift cards. Any gift cards we issue will be governed by the CARD Act and other various regulations. Any violations with our gift card issuance could result in the imposition of fines, the suspension of our ability to offer our gift cards, civil liability, criminal liability, and the inability of our issuing banks to apply certain fees to our gift cards, each of which would likely have a material adverse impact on our revenues.

Anti-Money Laundering and Counter Terrorist Regulation

Our business is subject to U.S. federal anti-money laundering laws and regulations, including the Bank Secrecy Act (BSA), as amended by the USA PATRIOT Act of 2001, or collectively, the BSA. The BSA, among other things, requires money services businesses to develop and implement risk-based anti-money laundering programs, report large cash transactions and suspicious activity and maintain transaction records. On September 29, 2017, the Financial Crimes Enforcement Network, or FinCEN, amended the Customer Due Diligence Rule, or CDD Rule, requiring the collection and verification of beneficial owners holding equal to or greater than 25% equity interest. The CDD Rule states that sole proprietorships-individual or spousal-and unincorporated associations are not legal entity customers as defined by the Rule, even though such businesses may file with the Secretary of State in order to register a trade name or establish a tax account. This is because neither a sole proprietorship nor an unincorporated association is a separate legal entity from the associated individual(s), and therefore beneficial ownership is not inherently obscured. The CDD Rule does not rely on the tax-exempt status of an entity as described in the Internal Revenue Code “IRC”. All nonprofit entities-whether or not tax-exempt-that are established as a nonprofit, or non-stock corporation, or similar entity that has been validly organized with the proper State authority are excluded from the ownership/equity prong of the requirement because nonprofit entities generally do not have ownership interests. As of May 2018, we are required to collect and verify beneficial owners holding equal to or greater than 25% equity interest based on rules promulgated by FinCEN.

We are also subject to certain economic and trade sanctions programs that are administered by the Treasury Department’s Office of Foreign Assets Control, or OFAC, that prohibit or restrict transactions to or from or dealings with specified countries, their governments and, in certain circumstances, their nationals, narcotics traffickers, and terrorists or terrorist organizations.

Similar anti-money laundering, counter terrorist financing and proceeds of crime laws apply to movements of currency and payments through electronic transactions and to dealings with persons specified on lists maintained by organizations similar to OFAC in several other countries and which may impose specific data retention obligations or prohibitions on intermediaries in the payment process.

Prepaid Services

Prepaid card programs managed by us are subject to various federal and state laws and regulations, which may include laws and regulations related to consumer and data protection, licensing, consumer disclosures, escheat, anti-money laundering, banking, trade practices and competition and wage and employment. As regulations evolve, or change, we may be required to obtain state licenses to expand our distribution network for prepaid cards, which licenses we may not be able to obtain. Furthermore, the CARD Act and the Federal Reserve’s Regulation E impose requirements on general-use prepaid cards, store gift cards and electronic gift certificates. These laws and regulations are evolving, unclear and sometimes inconsistent and subject to judicial and regulatory challenge and interpretation, and therefore the extent to which these laws and rules have application to, and their impact on, us, financial institutions, merchants or others is in flux. At this time, we are unable to determine the impact that the clarification of these laws and their future interpretations, as well as new laws, may have on us, financial institutions, merchants or others in a number of jurisdictions. Prepaid services may also be subject to the rules and regulations of Visa®, Mastercard® and other payment networks with which we and the card issuers do business. The programs in place to process these products generally may be modified by the payment networks at their discretion and such modifications could also impact us, financial institutions, merchants and others.

Environmental Laws

We are subject to a variety of federal, state, local and foreign environmental, health and safety laws and regulations governing, among other things, the generation, storage, handling, use and transportation of hazardous materials; the emission and discharge of hazardous materials into the environment; and the health and safety of our employees. We have incurred and expect to continue to incur costs to maintain or achieve compliance with environmental, health and safety laws and regulations. To date, these costs have not been material to the Company.

Human Capital Resources

As of December 31, 2023, we had 126 full-time employees. We are not a party to any collective bargaining agreements. We believe that our relations with our employees are good.

Growth and Development. Our strategy to develop and retain the best talent includes an emphasis on employee training and development. We promote our core values of ownership, innovation, camaraderie, service, authenticity and trust as an organization and offer awards to colleagues who exemplify these qualities. We require a mandatory online training curriculum for our employees that includes annual anti-harassment and anti-discrimination training.

Inclusion and Diversity. Our inclusion and diversity program focuses on our employees, workplace and community. We believe that our business is strengthened by a diverse workforce that reflects the communities in which we operate. We believe all of our employees should be treated with respect and equality, regardless of gender, ethnicity, sexual orientation, gender identity, religious beliefs or other characteristics. Inclusion and diversity remain a common thread in all of our human resource practices so that we can attract, develop and retain the best talent for our workforce.

Available Information

Usio was founded under the name Billserv.com, Inc. in July 1998 and incorporated in the State of Nevada. On June 26, 2019, we changed our corporate name from Payment Data Systems, Inc. to Usio, Inc. Our principal offices are located at 3611 Paesanos Parkway, Suite 300, San Antonio, TX 78231. Our telephone number is (210) 249-4100.

Our corporate website is located at www.usio.com. We make available on this website, free of charge, copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, as applicable and as soon as reasonably practicable after we electronically file or furnish such materials to the U.S. Securities and Exchange Commission. Interested persons can view such materials without charge under the "Investor Relations" section and then by clicking "Financials" on the Company's website, www.usio.com.

The inclusion of website addresses in this Annual Report does not include or incorporate by reference the information on or accessible through these websites, and the information contained on or accessible through these websites should not be considered as part of this annual report on Form 10-K.

You may also read and copy any materials we file with or furnish to the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at https://www.sec.gov.

An investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors and other information included in this annual report on Form 10-K. If any of the following risks actually occur, our business, financial condition or results of operations could be materially and adversely affected, and you may lose some or all of your investment.

RISKS RELATED TO OUR BUSINESS

Loss of key resellers could reduce our revenue growth.

We rely on our reseller sales channel, which purchases and resells our end-to-end services to its own portfolio of merchant customers. This channel is a strong contributor to our revenue growth. If a reseller switches to another transaction processor, shuts down, becomes insolvent, or enters the processing business themselves, we may no longer receive new merchant referrals from the reseller, and we risk losing existing merchants that were originally enrolled by the reseller, all of which could negatively affect our revenues and earnings.

If our security applications are breached by cyberattacks or are not adequate to address changing market conditions and customer concerns, we may incur significant losses and be unable to sell our services.

Unauthorized parties have attempted, and we expect that they will continue to attempt, to gain access to our systems or facilities through various means, including, but not limited to, hacking into our systems or facilities or those of our customers, partners, or vendors, and attempting to fraudulently induce users of our systems, including employees and customers, into disclosing user names, passwords, payment information, or other sensitive information used to gain access to such systems or facilities. This information may in turn be used to access our customers’ personal or proprietary information and payment data that are stored on or accessible through our information technology systems and those of third parties with whom we partner. Numerous and evolving cybersecurity threats, including advanced and persisting cyberattacks, cyberextortion, distributed denial-of-service attacks, ransomware, spear phishing and social engineering schemes, the introduction of computer viruses or other malware, and the physical destruction of all or portions of our information technology and infrastructure and those of third parties with whom we partner could compromise the confidentiality, availability, and integrity of the data in our systems. We may experience in the future, breaches of our security measures due to human error, malfeasance, insider threats, system errors or vulnerabilities, or other irregularities.

Any cyberattacks or data security breaches affecting our information technology or infrastructure or of our customers, partners, or vendors could have negative effects. For example, on December 25, 2021, we detected a ransomware attack that accessed and encrypted a small portion of our information technology systems. The unauthorized access included the download of non-payment processing related data files from our externally hosted Office 365 environment which is separate from our payment processing environment. Throughout the incident, we remained operational. Promptly upon the detection of the event, we launched an investigation, notified law enforcement and our insurance carrier, and engaged legal counsel, computer forensic firms and other incident response professionals. We also implemented a series of containment and remediation measures to address this situation and reinforce the security of our information technology systems. Our systems were not only fully restored and capable of resuming normal operations to the extent they were impaired, but enhanced following our immediate and long term response. Further preventative and proactive security measures were integrated, including incremental network and cloud defenses, implementation of third party cyber defense applications, structured incident response and disaster recovery plans, along with advanced employee cyber security training. We actively pursue any potential actions that will improve our existing systems. This cyber event had no material impact on the business, and no cardholder, or payments related data was compromised. Our direct losses associated with the cyber incident and its response were largely covered by our cybersecurity insurance, except for a deductible.

Our use of applications designed for premium data security and integrity to process electronic transactions may not be sufficient to address changing market conditions or the security and privacy concerns of existing and potential customers. If our security applications are breached and sensitive data is lost or stolen, we could incur significant costs to not only assess and repair any damage to our systems, but also to reimburse customers for losses that occur from the fraudulent use of the data. We may also be subject to fines and penalties from the credit card associations or regulatory agencies in the event of the loss of confidential account information. Our insurance policies may not be adequate to compensate us for the potential costs and other losses arising from cybersecurity-related disruptions, failures, attacks or breaches. In addition, such insurance may not be available to us in the future on economically reasonable terms, or at all. Further, adverse publicity raising concerns about the safety or privacy of electronic transactions, or widely reported breaches of our or another provider's security, have the potential to undermine consumer confidence in the technology and could have a materially adverse effect on our business.

Our efforts to expand our product portfolio and market reach, including through acquisitions, may not succeed and may reduce our revenue growth and we may not achieve or maintain profitability.

Since 2014, we have completed a total of four acquisitions which have allowed us to expand our product offerings. For example, we acquired the assets of IMS, a business of electronic bill presentment, document composition, document decomposition and printing and mailing services serving hundreds of customers representing a wide range of industry verticals, including utilities and financial institutions on December 15, 2020. We also continue to invest in our established business lines and new markets, such as our payment facilitation, and prepaid card business. While we have grown the proportion of revenue from these newer products and services and we intend to continue to broaden the scope of products and services we offer, we may not be successful in maintaining or growing our current revenue streams or deriving any significant new revenue streams from these products and services. Failure to successfully broaden the scope of products and services that are attractive may inhibit our growth and harm our business. Furthermore, we expect to continue to expand our markets in the future, and we may have limited or no experience in such newer markets. We cannot assure you that any of our products or services will be widely accepted in any market or that they will continue to grow in revenue. Our offerings may present new and difficult technological, operational, regulatory, risks, and other challenges, and if we experience service disruptions, failures, or other issues, our business may be materially and adversely affected. Our expansion into newer markets may not lead to growth and may require significant management time and attention, and we may not be able to recoup our investments in a timely manner or at all. If any of this were to occur, it could damage our reputation, limit our growth, and materially and adversely affect our business.

We may need additional financing in the future. We may be unable to obtain additional financing or if we obtain financing it may not be on terms favorable to us. You may lose your entire investment.

Based on our current plans, we believe our existing cash and cash equivalents and cash flow from operations will be sufficient to fund our operating expense and capital requirements for at least 12 months, although we may need funds in the future. At December 31, 2023 we had $7.2 million of cash and cash equivalents, and for the year ended December 31, 2023, operating activities provided $14.9 million. After adjusting for the impact of operating lease right-of-use assets, operating lease liabilities, prepaid card load obligations and merchant reserves included in the statement of cash flows, net cash provided by adjusted operating activities, was $2.8 million for the year ended December 31, 2023. Adjusted operating cash flow is viewed by the company as a superior indicator of the Company's operating performance and ability to fund acquisitions, capital expenditures and other investments and, in the absence of refinancing options, to repay debt obligations. Refer to Item 7, under the subsection "Management's Discussion and Analysis of Financial Condition and Results of Operations - Key Business Metrics - Non-GAAP Financial Measures" for our reconciliation of operating cash flows to adjusted operating cash flows. If our capital resources are insufficient to meet future capital requirements, we will have to raise additional funds by selling assets, borrowing money from a third party, or by selling debt or equity securities. If we are unable to obtain additional funds on terms favorable to us, we may be required to cease or reduce our operating activities. If we must cease or reduce our operating activities, you may lose your entire investment.

Unauthorized disclosure of cardholder data, whether through breach of our computer systems or otherwise, could expose us to liability and protracted and costly litigation.

We collect and store personal identifiable information about our cardholders, including names, addresses, social security numbers, driver’s license numbers and account numbers, and maintain a database of cardholder data relating to specific transactions, including account numbers, in order to process transactions and prevent fraud. As a result, we are required to comply with the privacy provisions of the Gramm-Leach-Bliley Act, various other federal and state privacy statutes and regulations, and the Payment Card Industry Data Security Standard, each of which is subject to change at any time. Compliance with these requirements is often difficult and costly, and our failure, or our distributors’ failure, to comply may result in significant fines or civil penalties, regulatory enforcement action, liability to our issuing banks and termination of our agreements with one or more of our issuing banks, each of which could have a material adverse effect on our financial position and/or operations. In addition, a significant breach could result in our Company being prohibited from processing transactions for any of the relevant card associations or network organizations, including Visa, Mastercard, American Express, Discover or regional debit networks, which would also have a significant material adverse impact on our financial position and/or operations.

Furthermore, if our computer systems are breached by unauthorized users, we may be subject to liability, including claims for unauthorized purchases with misappropriated bank card information, impersonation or similar fraud claims. We could also be subject to liability for claims relating to misuse of personal information, such as unauthorized marketing purposes, or failure to comply with laws governing notification of such breaches. These claims also could result in protracted and costly litigation. In addition, we could be subject to penalties or sanctions from the relevant card associations or network organizations.

If our efforts to protect the security of information about our customers, cardholders and vendors are unsuccessful, we may face additional costly government enforcement actions and private litigation, and our sales and reputation could suffer.

An important component of our business involves the receipt and storage of information about our cardholders and banking information. We have multiple programs and processes in place to detect and respond to data security incidents; however, because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and may be difficult to detect for long periods of time, we may be unable to anticipate these techniques or implement adequate preventive measures. In addition, hardware, software, or applications we develop or procure from third parties may contain defects in design or manufacture or other problems that could unexpectedly compromise information security. Unauthorized parties may also attempt to gain access to our systems or facilities, or those of third parties with whom we do business, through fraud, trickery, or other forms of deceiving our vendors, contractors, and employees. If we, our customers, or our vendors experience significant data security breaches or fail to detect and appropriately respond to significant data security breaches, we could be exposed to government enforcement actions and private litigation. In addition, our cardholders and customers could lose confidence in our ability to protect their information, which could cause them to discontinue using our services.

If we do not adapt to rapid technological change, including as a result of artificial intelligence, our business may fail.

Our success depends on our ability to develop new and enhanced services and related products that meet ever changing customer needs and industry standards. However, the market for our services is characterized by rapidly changing technology, evolving industry standards, emerging competition and frequent new and enhanced software, service and related product introductions. In addition, the software market is subject to rapid and substantial technological change. To remain successful, we must respond to new developments in hardware and semiconductor technology, operating systems, programming technology and computer capabilities. In many instances, new and enhanced services, products and technologies are in the emerging stages of development and marketing and are subject to the risks inherent in the development and marketing of new software, services and products. We may not successfully identify new service opportunities and develop and introduce new and enhanced services and related products to market in a timely manner. Even if we do bring such services, products or technologies to market, they may not become commercially successful. Additionally, services, products or technologies developed by others may render our services and related products noncompetitive or obsolete. If we are unable, for technological or other reasons, to develop and introduce new services and products in a timely manner in response to changing market conditions or customer requirements, our business may fail.

Business interruptions or systems failures may impair the availability of our websites, applications, products or services, or otherwise harm our business.

Our systems and operations and those of our service providers and partners have experienced from time to time, and may experience in the future, business interruptions or degradation because of distributed denial-of-service and other cyberattacks, insider threats, hardware and software defects or malfunctions, human error, earthquakes, hurricanes, floods, fires, and other natural disasters, public health crises (including pandemics), power losses, disruptions in telecommunications services, fraud, military or political conflicts, terrorist attacks, computer viruses or other malware, or other events. A catastrophic event that results in a disruption or failure of our systems or operations could result in significant losses and require substantial recovery time and significant expenditures to resume or maintain operations, which could have a material adverse impact on our business, financial condition, and results of operations. Additionally, some of our systems, including those of companies we have acquired, are not fully redundant, and our disaster recovery planning may not be sufficient for all possible outcomes or events. As a provider of payment solutions, we are subject to heightened scrutiny by regulators that may require specific business continuity, resiliency and disaster recovery plans, and rigorous testing of such plans, which may be costly and time-consuming to implement, and may divert our resources from other business priorities.

We have experienced, and expect to continue to experience, system failures, cyberattacks, unplanned outages, and other events or conditions from time to time that have and may interrupt the availability, or reduce or adversely affect the speed or functionality, of our products and services. These events could result in future losses of revenue. A prolonged interruption in the availability or reduction in the availability, speed, or functionality of our products and services could materially harm our business. Frequent or persistent interruptions in our services could permanently harm our relationship with our customers and partners and our reputation. Moreover, if any system failure or similar event results in damage to our customers or their business partners, they could seek significant compensation or contractual penalties from us for their losses, and those claims, even if unsuccessful, would likely be time-consuming and costly for us to address, and could have other consequences described in this “Risk Factors” section under the caption “If our security applications are breached by cyberattacks or are not adequate to address changing market conditions and customer concerns, we may incur significant losses and be unable to sell our services.”

We have undertaken and continue to undertake certain system upgrades and re-platforming efforts designed to improve the availability, reliability, resiliency, and speed of our platform. These efforts are costly and time-consuming, involve significant technical risk, and may divert our resources from new features and products, and there can be no guarantee that these efforts will be effective. Frequent or persistent site interruptions could lead to regulatory scrutiny, significant fines and penalties, and mandatory and costly changes to our business practices, and ultimately could cause us to lose existing licenses that we need to operate or prevent or delay us from obtaining additional licenses that may be required for our business.

We also rely on facilities, components, applications, and services supplied by third parties, including data center facilities and cloud data storage and processing services. From time to time, we have experienced interruptions in the provision of such facilities and services provided by these third parties. If these third parties experience operational interference or disruptions (including a cybersecurity incident), breach their agreements with us, or fail to perform their obligations and meet our expectations, our operations could be disrupted or otherwise negatively affected, which could result in customer dissatisfaction, regulatory scrutiny, and damage to our reputation and brands, and materially and adversely affect our business. While we maintain insurance policies intended to offset the financial impact we may experience from these risks, our coverage may be insufficient to compensate us for all losses caused by interruptions in our service as a result of systems failures and similar events.

In addition, any failure to successfully implement new information systems and technologies, or improvements or upgrades to existing information systems and technologies in a timely manner could have an adverse impact on our business, internal controls (including internal controls over financial reporting), results of operations, and financial condition.

Fraud by merchants or others could have an adverse effect on our operating results and financial condition.

We have potential liability for fraudulent bankcard, ACH and prepaid card transactions or credits initiated by merchants or others. Examples of merchant fraud include when a merchant knowingly uses a stolen or counterfeit bankcard, card number or bank account to record a false sales transaction, processes an invalid bankcard, or intentionally fails to deliver the merchandise or services sold in an otherwise valid transaction. Criminals are using increasingly sophisticated methods to engage in illegal activities such as counterfeit and fraud. While we have systems and procedures designed to detect and reduce the impact of fraud, we cannot assure the effectiveness of these measures. It is possible that incidents of fraud could increase in the future. Failure to effectively manage risk and prevent fraud would increase our chargebacks liability or cause us to incur other liabilities, including regulatory and association fines, penalties and harm to our reputation. Increases in chargebacks or other liabilities could have an adverse effect on our operating results and financial condition.

We rely on our relationship with the Automated Clearing House network, and if the Federal Reserve rules were to change, our business could be adversely affected.

We have contractual relationships with North American Banking Company, or NABC, Metropolitan Commercial Bank, and TransPecos Bank, which are Originating Depository Financial Institutions, or ODFI, in the ACH network. The ACH network is a nationwide batch-oriented electronic funds transfer system that provides for the interbank clearing of electronic payments for participating financial institutions. An ODFI is a participating financial institution that must abide by the provisions of the ACH Operating Rules and Guidelines. Through our relationships with Metropolitan Commercial Bank, TransPecos Bank, and NABC, we process payment transactions on behalf of our customers and their consumers by submitting payment instructions in a prescribed ACH format. We pay volume-based fees to TransPecos Bank, and NABC for debit and credit transactions processed each month, and pay fees for other transactions such as returns and notices of change to bank accounts. These fees are part of our agreed-upon cost structures with the banks. If the Federal Reserve rules were to introduce restrictions or modify access to the Automated Clearing House, our business could be materially adversely affected. Further, if one or all of Metropolitan Commercial Bank, TransPecos Bank, or NABC were to cancel our respective contract with the bank, our business could be materially affected. At this time, we believe we could find and enter into additional agreements with other bank sponsors on similar contractual terms, but no assurances can be made.

If we lose key personnel or we are unable to attract, recruit, retain and develop qualified employees, our business, financial condition and results of operations may be adversely affected.

In order for us to successfully compete and grow, we must attract, recruit, retain and develop the necessary personnel who can provide the needed expertise and skills across the spectrum of our intellectual capital needs. The market for qualified personnel is highly competitive and we may not be successful in recruiting qualified personnel for needed skill sets or replacing current personnel who leave us. Failure to retain or attract key personnel and skill sets could have a material adverse effect on our business, financial condition and results of operations.